1

Personal Finance

7.02: Understand ways to protect personal credit.

2

Activity

Show the video clip “Amateur Rock Star” by Scott Blair from this link: http://www.whatsmyscore.org/contest/videos.php.

Discussion: How can having a bad credit score negatively affect a

person? If bills are not paid, what items may be repossessed? What is the impact when seeking credit in the future? What is the overall message of this video clip?

Main Idea: Individuals should check their credit report, know their scores, and not spend beyond their financial limits.

3

Activity

Display Appendix 7.03A, “Use of Credit---Agree or Disagree.” Have students record in their notes whether they agree or disagree with each data statement about use of credit by college/university undergraduates.

4

Journal Entry

What do you think Credit is?

5

Credit Overview

6

What Is Credit? Obtaining goods and services with a promise to pay for

them from future income

A temporary money substitute since it allows a person to buy today and pay tomorrow

Can be a valuable resource when used wisely Credit involves two parties, a lender and a

borrower Lender (creditor, credit-provider, source of credit)

One who provides money for purchases based on a person’s promise to repay

Lender expects borrower to pay extra, known as interest, for the use of the money

Borrower (debtor)---One who received credit from a lender

7

Types of Consumer Credit

Sales Credit Regular charge accountInstallment accountRevolving credit account

Cash Credit---Secured and Unsecured Company or retail store credit cardsTravel and entertainment credit cardsGeneral-purpose credit cards

8

Solve Credit Problems

Actively deal with the problemStop using credit; focus on repaymentSee a credit counselorDevelop a spending plan with living expenses and a plan for repaymentAsk creditors to adjust credit terms

9

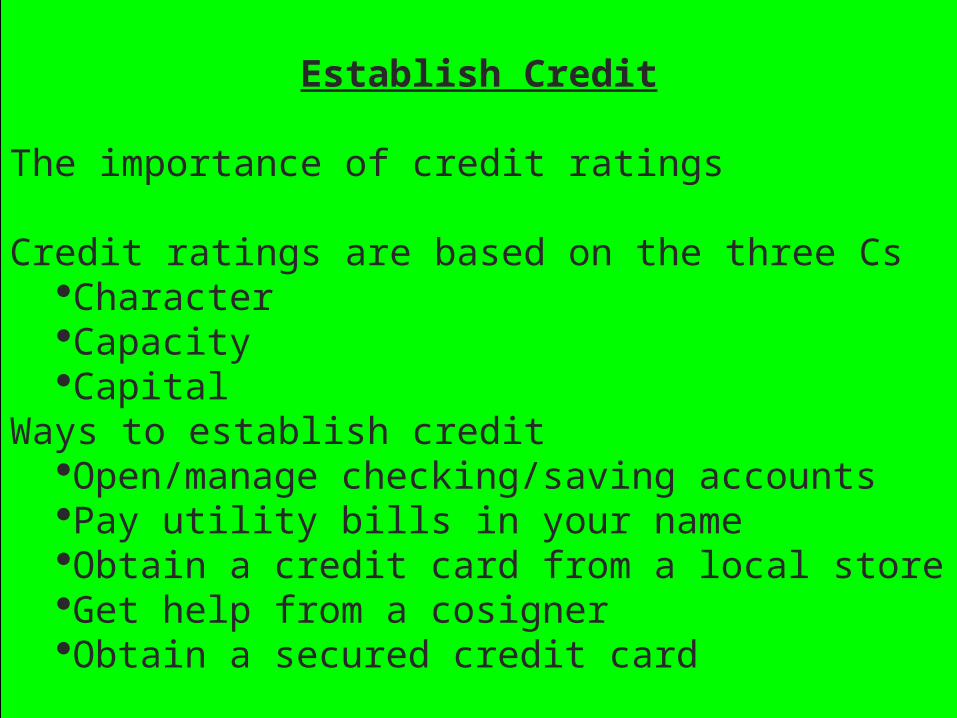

Establish Credit

The importance of credit ratings

Credit ratings are based on the three CsCharacterCapacityCapital

Ways to establish creditOpen/manage checking/saving accountsPay utility bills in your nameObtain a credit card from a local storeGet help from a cosignerObtain a secured credit card

10

Maintain Good Credit

Evaluate when you really need creditShop for the right type of credit for each purchaseShop for the best credit termsKnow how you will pay backUse only the amount of credit you can repayMeet terms of credit agreementsKeep accurate recordsConsult creditors immediately if you cannot pay on timeResolve billing errors promptly

Credit Card

Understanding Your Credit Card

Credit UnitTake Charge of Your

Finances

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

12

Credit

When goods, services or money is received in exchange for a promise to pay a definite sum

of money at a future date

The price of money- when referring to credit, interest is the charge for

borrowing money

CREDIT-

INTEREST-

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

13

Lender and Borrower

LENDER-The person or

organization who has the resources

to provide the individual with a

loan

BORROWER-

The person or organization that is

receiving the money from the

lender

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

14

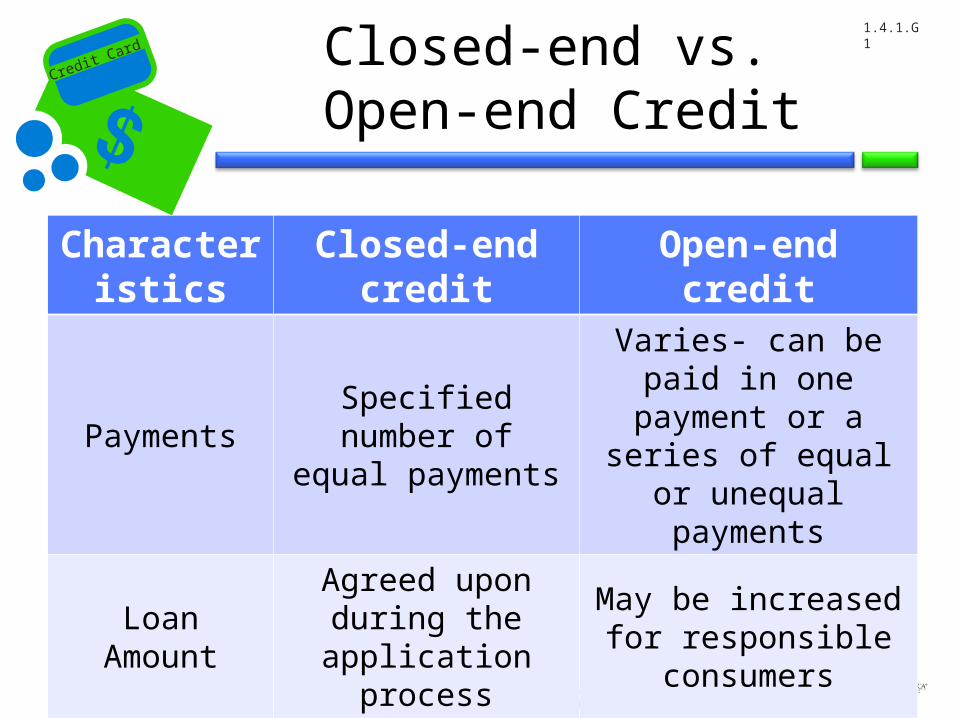

Closed-end vs. Open-end Credit

Characteristics

Closed-end credit

Open-end (revolving)

credit

Definition A one-time loanCredit extended in

advance

Purpose of loan

Specified in application

May be used for a variety of purposes

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

15

Closed-end vs. Open-end Credit

Characteristics

Closed-end credit

Open-end credit

PaymentsSpecified number

of equal payments

Varies- can be paid in one payment or a series of equal or unequal payments

Loan Amount

Agreed upon during the application

process

May be increased for responsible

consumers

ExamplesMortgage,

automobile, education loans

Credit cards

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

16

Credit Card

What is a credit card?Pre-approved credit which can be used for the

purchase of goods and services now and payment of them later

A credit cards credit limit varies based upon an individual’s

perceived creditworthinessCredit limit is the maximum dollar amount

loaned

Creditworthiness is an individuals ability and

willingness to pay the money back

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

17

Credit Card Interest

Interest is charged each month the balance is not

paid in full

The cost of credit expressed as

a yearly interest rate

Rate at which interest is charged is referred to as:

Annual Percentage Rate

(APR)

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

18

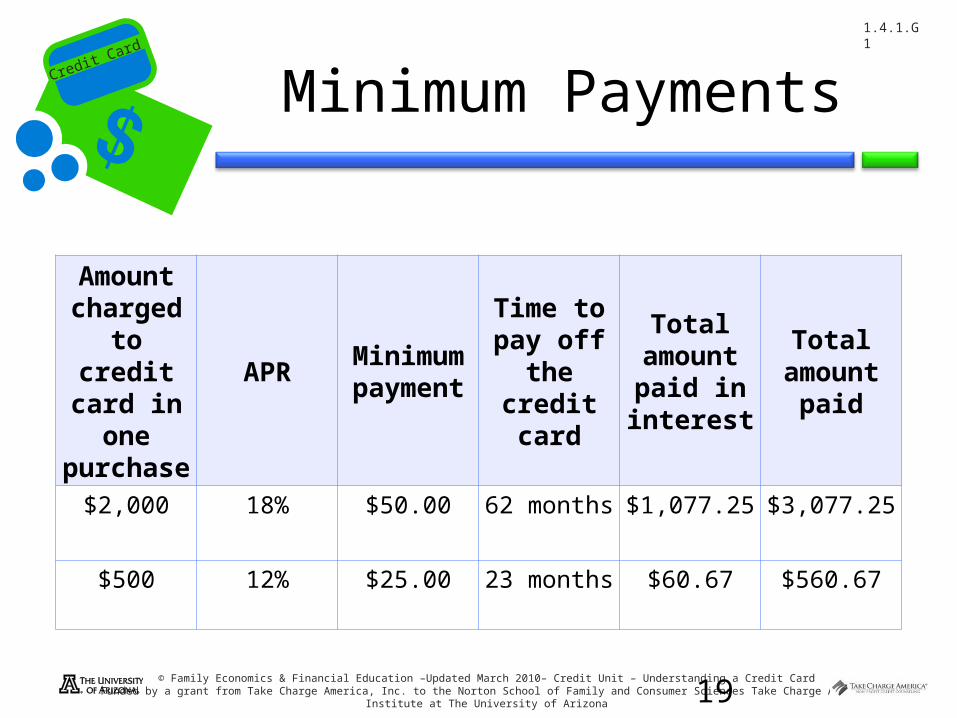

Minimum Payments

• Required to make at least a minimum payment each month– Usually only a small percentage (2.5-5%) of

the total balance due

• Cardholders who only make the minimum payment:– Make slow progress paying off card balance– Pay substantially more than what was

initially charged to the card

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

19

Minimum Payments

Amount charged to credit card in

one purchas

e

APRMinimu

m payment

Time to pay off

the credit card

Total amount paid in interest

Total amount

paid

$2,000 18% $50.00 62 months $1,077.25 $3,077.25

$500 12% $25.00 23 months $60.67 $560.67

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

20

Advantages to using Credit Cards

AdvantagesConvenient payment

toolUseful for emergencies

Often required to hold a reservation

Able to purchase “big ticket” items and spread

out payments

Protection against fraud

Opportunity to establish a positive credit history

Online shopping is safer than using a debit card

because of the Fair Credit Billing Act protectionPossibility of receiving

bonuses, such as frequent flyer miles or cash rebates

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

21

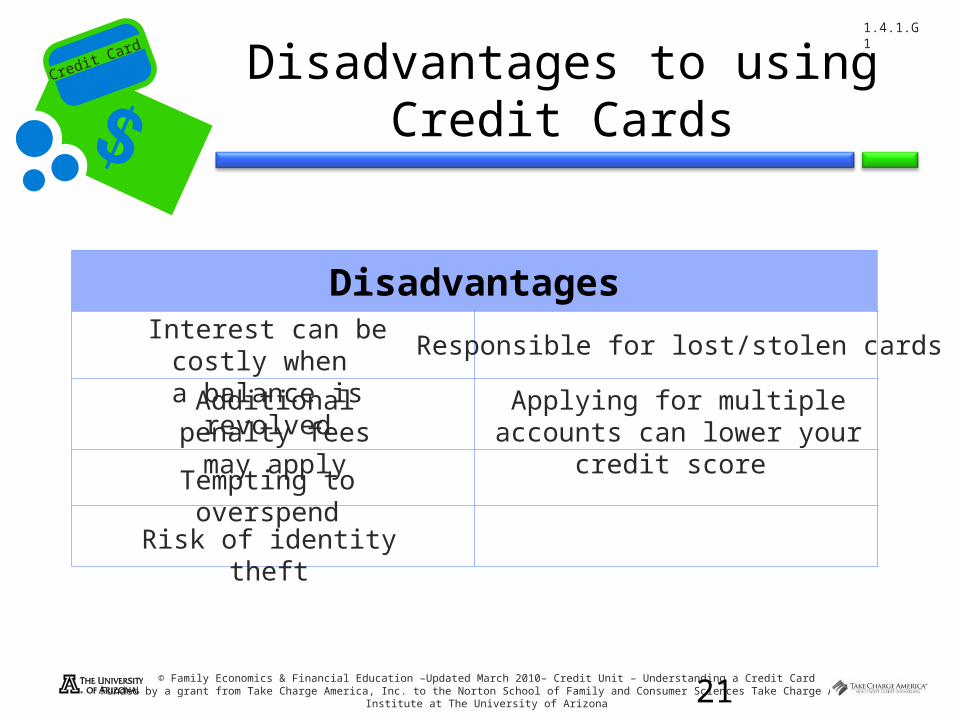

Disadvantages to using Credit Cards

DisadvantagesInterest can be costly

when a balance is revolvedAdditional

penalty fees may apply

Tempting to overspend

Risk of identity theft

Responsible for lost/stolen cards

Applying for multiple accounts can lower your

credit score

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

22

Debit Cards

• What is a debit card?– A plastic card which looks like a credit

card, but is electronically connected to the cardholder’s bank account

– Money is immediately withdrawn from the cardholders checking account

What is the difference between a credit card and a debit card?

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

23

Credit History

Credit ReportA record of a consumer’s credit history that

includes information about credit card use as well as the use of other types of credit, such as auto loans, student loans and mortgage loans

A number that summarizes an individual’s credit record and history. It is a numeric “grade” of a

consumer’s financial reliability

Credit Score

Credit cards can have a positive or negative impact on an individuals credit history

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

24

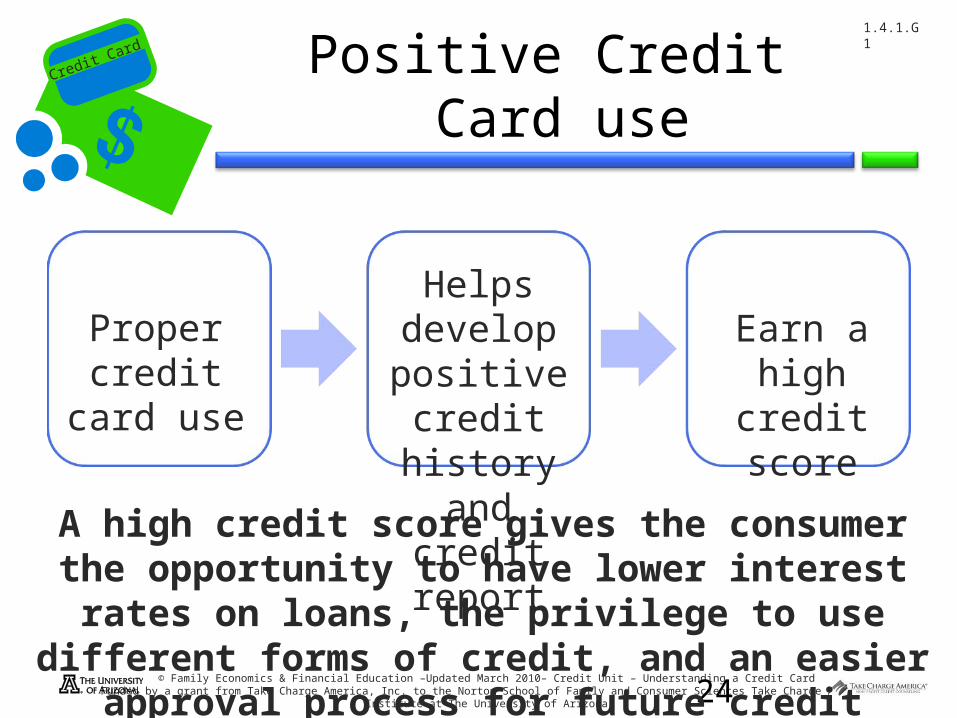

Positive Credit Card use

Proper credit card

use

Helps develop positive credit history

and credit report

Earn a high credit

score

A high credit score gives the consumer the opportunity to have lower interest rates on loans, the privilege to use different forms of credit, and an easier approval process

for future credit

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

25

Positive Credit Card Use

• Examples of positive credit card behaviors:– Paying credit card balances in full every

month– Paying credit card bills on time – Applying for only credit cards that are needed– Keeping track of all charges by keeping

receipts and using a check register– Checking the monthly credit card statement

for errors

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

26

Negative Credit Card Use

Consumers with low credit scores have difficulty getting loans, difficulty renting apartments, pay higher interest rates, pay higher insurance rates, and have

difficulty obtaining a job

Improper credit card

use

Develops negative

credit history

and credit report

Lower credit score

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

27

Negative CreditCard use

• Examples of negative credit card behaviors:– Making late credit card payments– Paying only the minimum payment– Exceeding the card’s credit limit (usually

triggers a penalty fee)– Charging items that can’t be paid off

immediately– Owning too many credit cards

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

28

NO Credit

• If an individual has not used credit, they will not have any information in their credit report

• Not having a credit report can cause an individual to be denied credit

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

29

Credit Card Offers

Credit card issuers are required to disclose the terms and fees of credit cards in an easy to read

box format

This is called the Schumer box

Credit Card

30

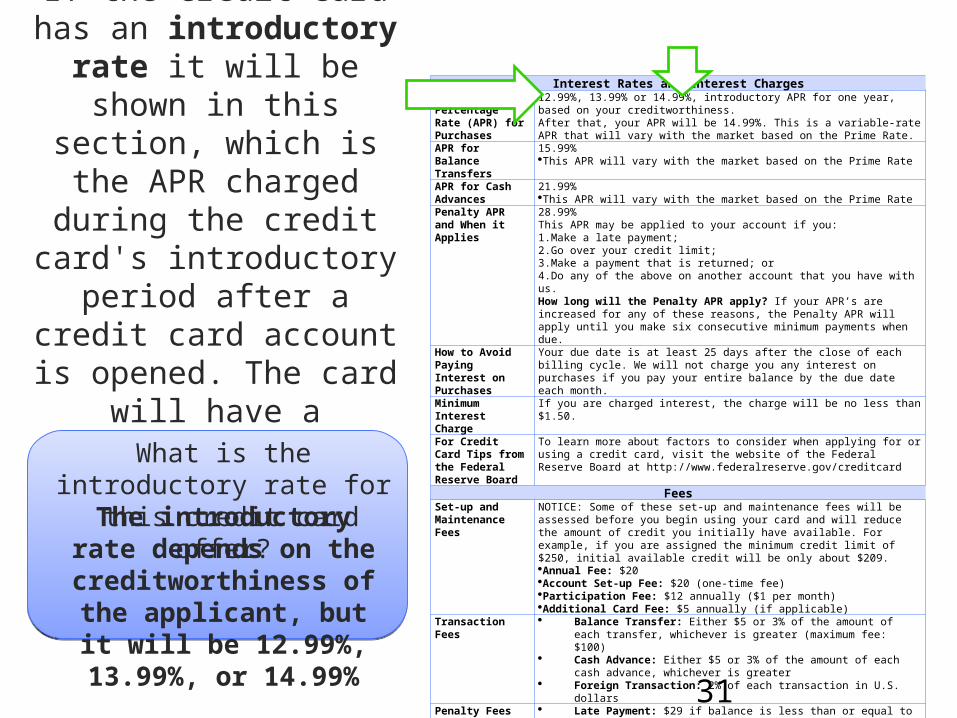

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

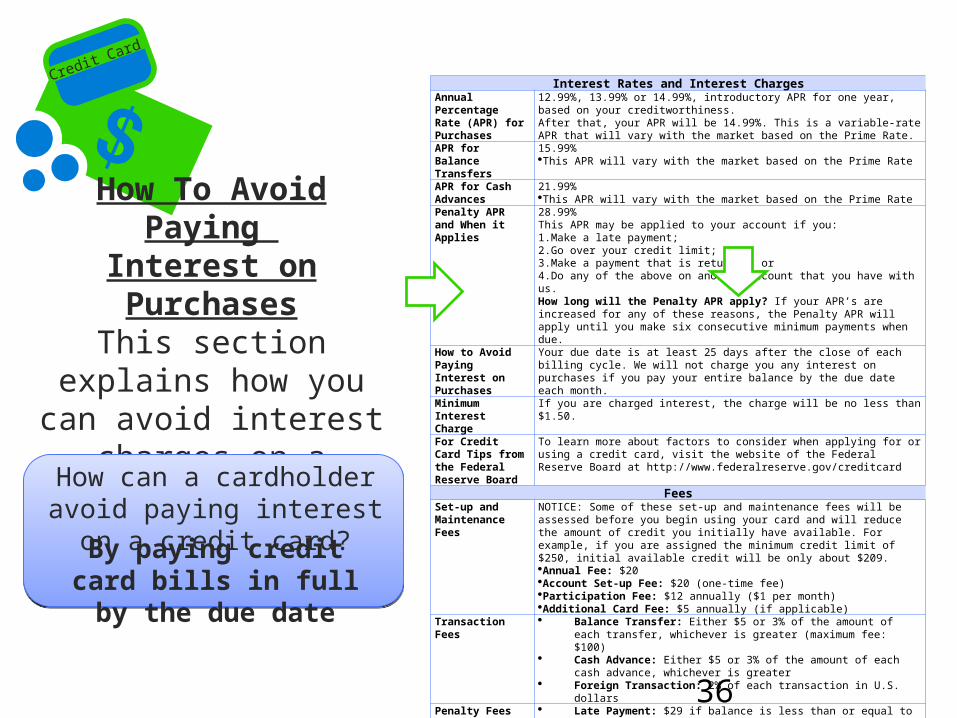

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

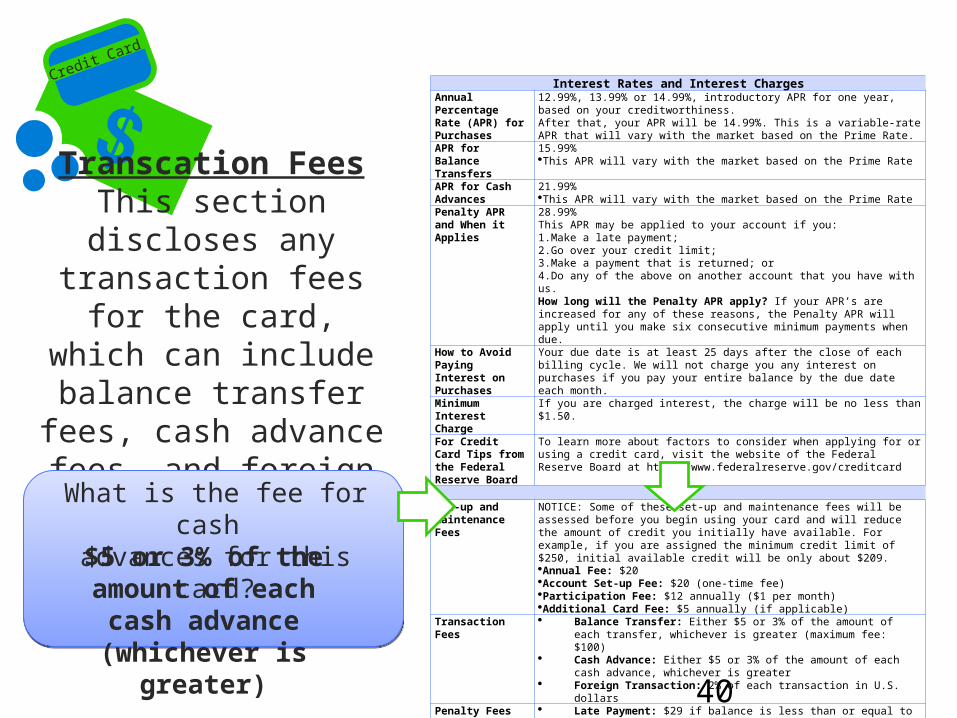

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

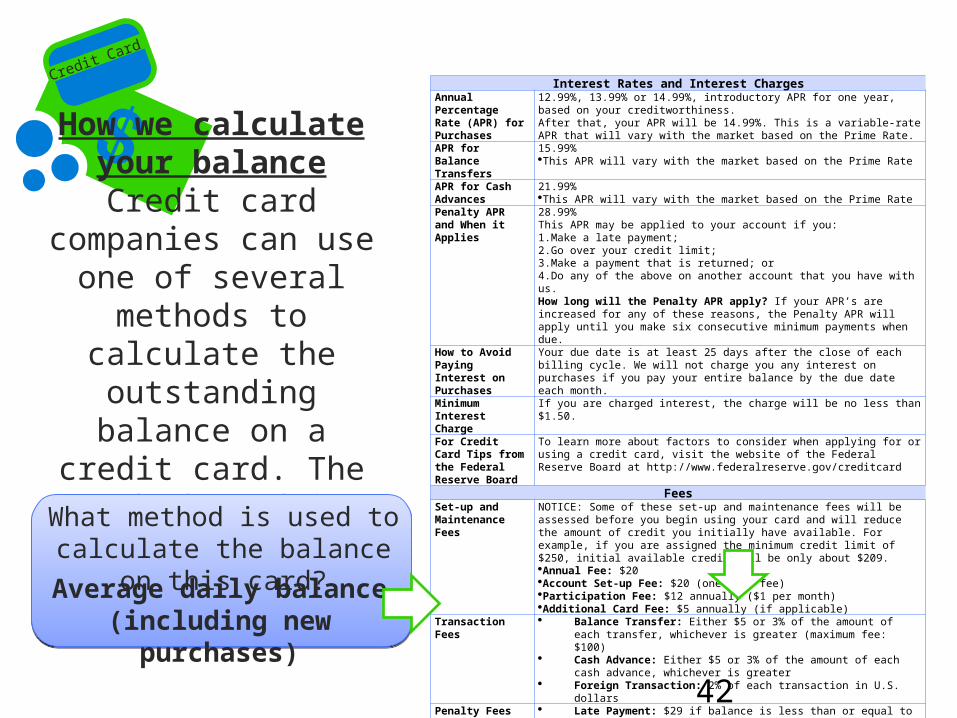

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Annual Percentage Rate (APR) for

PurchasesThis section discloses the interest paid for

purchases on the card. Multiple interest rates

may be listed here, because the final interest rate may

depend on the creditworthiness of the

applicant

31

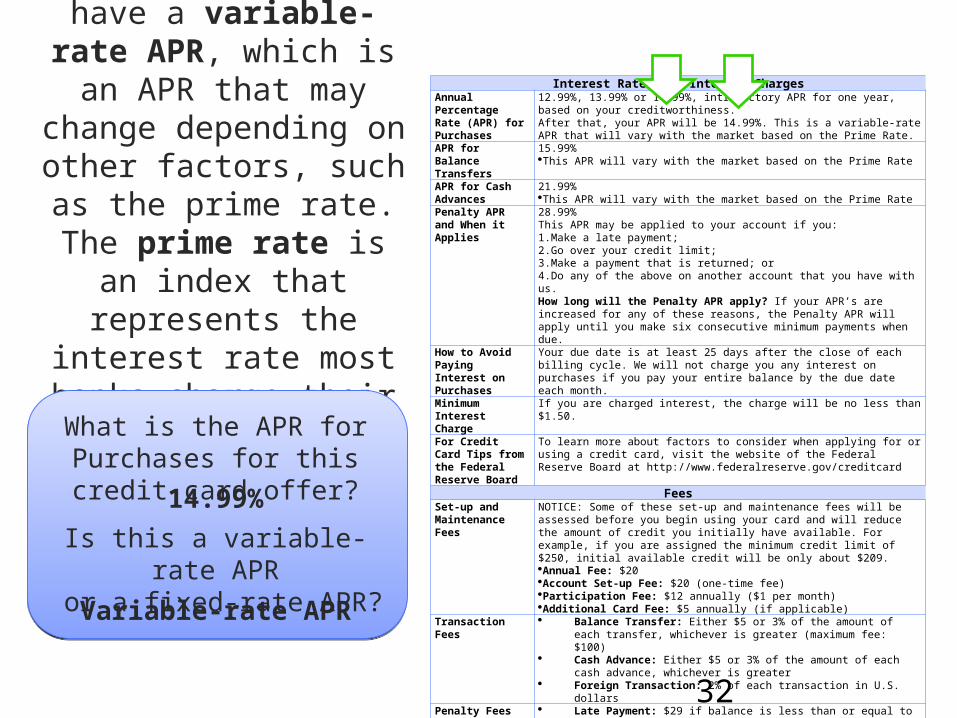

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Introductory RateIf the credit card has an introductory rate it will be shown in this section, which is the

APR charged during the credit card's

introductory period after a credit card account is opened. The card will have a different APR after the introductory

period endsWhat is the introductory rate for

this credit card offer?The introductory rate depends on the

creditworthiness of the applicant, but it

will be 12.99%, 13.99%, or 14.99%

32

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Variable-rate APRSome cards will have a variable-rate APR, which is an APR that

may change depending on other factors, such as the prime rate. The prime rate is an index

that represents the interest rate most banks charge their most credit-worthy

customers What is the APR for Purchases for this credit

card offer?14.99%

Is this a variable-rate APR or a fixed-rate APR?

Variable-rate APR

33

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

APR for Balance Transfers

This section discloses the interest paid for balance transfers, which is the act of

transferring debt from one credit card account

to another. Balance transfer fees may apply,

even if the balance transfer APR is 0% What is the APR for balance transfers for this

credit card offer?15.99%

Credit Card

34

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

APR for Cash Advances

This section discloses the interest paid for

cash advances, such as withdrawing cash from an ATM using a credit

card. Cash advance fees may also apply

What is the APR for cash advances for this credit

card offer?21.99%

35

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Penalty APR and When it Applies

This section discloses the penalty APR, as well

as the penalty terms that trigger the penalty

APR to take effect

•Penalty APR is the interest rate charged on new transactions if the penalty terms in the credit card contract are triggered

What is the Penalty APR for this credit card offer?

21.99%

Credit Card

36

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

How To Avoid Paying

Interest on Purchases

This section explains how you can avoid

interest charges on a credit cardHow can a cardholder

avoid paying interest on a credit card?By paying credit card

bills in full by the due date

Credit Card

37

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Minimum Interest Charge

Credit card companies often have a minimum interest

amount. These charges typically

range from $0.50 to $2 per month and are

disclosed in this section of the credit

card offerWhat is the minimum

interest charge for this credit card?$1.50

Credit Card

38

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

For Credit Card Tips from the

Federal Reserve Board

This section directs consumers to the Federal Reserve website to obtain more information about credit cards

39

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Set-up and Maintenance FeesThis section discloses

any set-up and maintenance fees for the card, which can include annual fees, account set-up fees, participation fees,

and additional card fees

•Annual fee is a yearly fee that may be charged for having a credit card

What is the annual fee for this credit card?

$20

Credit Card

40

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Transcation FeesThis section discloses any transaction fees for the card, which can include balance transfer fees, cash advance fees, and foreign transaction

fees What is the fee for cash advances for this card?

$5 or 3% of the amount of each cash advance (whichever is

greater)

41

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Penalty FeesThis section discloses the penalty fees for the card, which can

include late-payment, over-the-limit, and returned payment

fees

•Late payment fee is charged when a cardholder does not make the minimum monthly payment by the due date•Over-the-limit fee is charged if the account balance goes over the set credit limit

Does this card have an over-the limit fee?

Yes, the over-the-limit fee is $29.

Credit Card

42

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

How we calculate your balance

Credit card companies can use

one of several methods to calculate

the outstanding balance on a credit card. The method

used is disclosed in this section

What method is used to calculate the balance on

this card?Average daily balance (including new

purchases)

43

Interest Rates and Interest ChargesAnnual Percentage Rate (APR) for Purchases

12.99%, 13.99% or 14.99%, introductory APR for one year, based on your creditworthiness.After that, your APR will be 14.99%. This is a variable-rate APR that will vary with the market based on the Prime Rate.

APR for Balance Transfers

15.99%This APR will vary with the market based on the Prime Rate

APR for Cash Advances

21.99%This APR will vary with the market based on the Prime Rate

Penalty APR and When it Applies

28.99%This APR may be applied to your account if you:1.Make a late payment;2.Go over your credit limit;3.Make a payment that is returned; or4.Do any of the above on another account that you have with us.How long will the Penalty APR apply? If your APR’s are increased for any of these reasons, the Penalty APR will apply until you make six consecutive minimum payments when due.

How to Avoid Paying Interest on Purchases

Your due date is at least 25 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.

Minimum Interest Charge

If you are charged interest, the charge will be no less than $1.50.

For Credit Card Tips from the Federal Reserve Board

To learn more about factors to consider when applying for or using a credit card, visit the website of the Federal Reserve Board at http://www.federalreserve.gov/creditcard

FeesSet-up and Maintenance Fees

NOTICE: Some of these set-up and maintenance fees will be assessed before you begin using your card and will reduce the amount of credit you initially have available. For example, if you are assigned the minimum credit limit of $250, initial available credit will be only about $209.Annual Fee: $20Account Set-up Fee: $20 (one-time fee)Participation Fee: $12 annually ($1 per month)Additional Card Fee: $5 annually (if applicable)

Transaction Fees

Balance Transfer: Either $5 or 3% of the amount of each transfer, whichever is greater (maximum fee: $100)

Cash Advance: Either $5 or 3% of the amount of each cash advance, whichever is greater

Foreign Transaction: 2% of each transaction in U.S. dollarsPenalty Fees Late Payment: $29 if balance is less than or equal to $1000

OR $35 if balance is more than $1000 Over-the-limit: $29 Returned Payment: $35

* How We Will Calculate Your Balance: We use a method called “average daily balance (including new purchases).”* Loss of Introductory APR- We may end your introductory APR and apply the Penalty APR if you become more than 60 days late in paying your bill

Loss of Introductory APRIf the card has an

introductory rate, this area will list how the lower introductory rate can be lost

How can the introductory APR be lost on this card?

If the cardholder is more than 60 days

late in paying the billWhat APR will the

cardholder be charged if the introductory rate

is lost?The Penalty APR of 28.99%

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

44

Credit Card Chaos

• The educator will identify terms associated with a credit card offer

• Identify which term is true on your provided credit card offer and move to that poster

• In a small group, define the term on the poster

• As a class, discuss which credit card characteristic is better for a consumer and why

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

45

Credit Card Chaos

• Fixed-rate APR for Purchases vs. Variable-rate APR for Purchases

• Introductory Rate vs. No Introductory Rate• APR for Purchases Greater than or Equal to 15%

vs. APR for Purchases Less than 15%• No Minimum Interest Charge vs Minimum

Interest Charge• Annual Fee vs. No Annual Fee• Balance Transfer Fee vs. No Balance Transfer Fee• Late Payment Fees vs. No Late Payment Fees

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

46

Credit Card Benefits

• Research benefits that may be received from the card– Cash rebates– Warranties for items purchased with the card– Travel accident insurance– Frequent flyer miles

• Make sure to know all terms and conditions of card benefits

• Cards that offer benefits may charge fees or higher interest rates

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

47

Receiving a Credit Card

1. Compare credit card offers and determine which card to apply for

2. Complete a credit application– A form requesting information about a

person’s ability to repay and the applicant’s age

– Can be completed through the mail, the internet or over the phone

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

48

Receiving a Credit Card

3. Lenders conduct a credit investigation

– A comparison of information on credit application to information on a credit report

4. Applicants may or may not be approved for the card they apply for

– Approval depends on the applicant's credit history

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

49

Pre-Approved Credit Card Applications

• Credit card companies send pre-approved credit card applications in the mail– If an individual is pre-approved for that

particular card, they have passed the initial credit check

Credit Card

© Family Economics & Financial Education –Updated March 2010– Credit Unit – Understanding a Credit CardFunded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The

University of Arizona

Credit Card

1.4.1.G1

50

Credit Card Statements

• Credit card statements outline important information about the card

• The 2009 CARD Act required credit card companies to include specific information about a card account in the statement

Andrew’s Credit Card StatementPlease help Andrew interpret his credit card

statement.

51

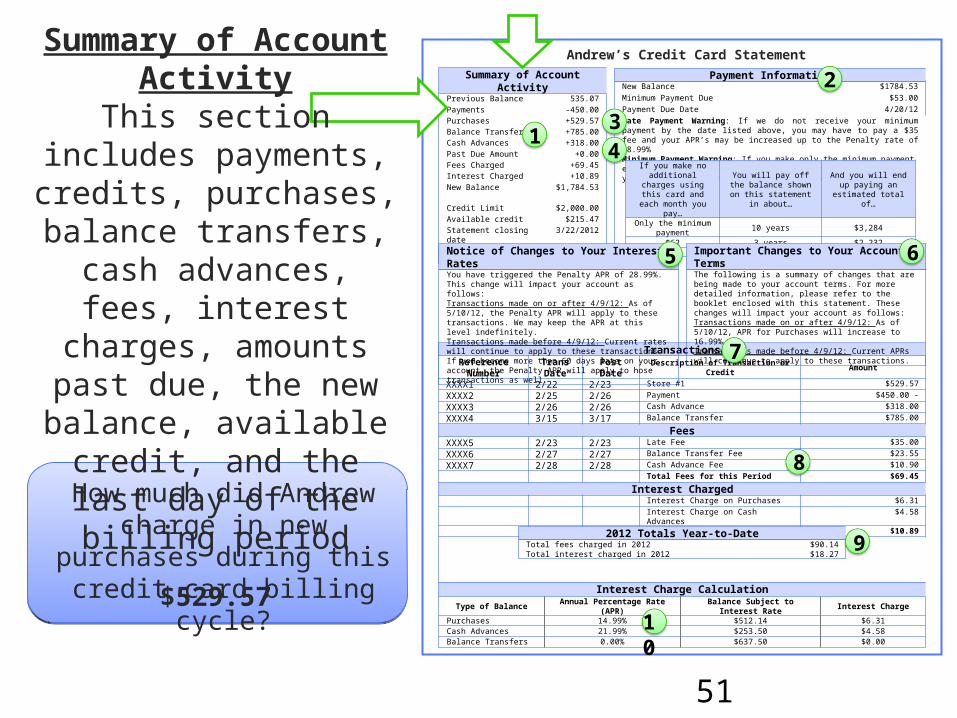

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89

Payment InformationNew Balance $1784.53Minimum Payment Due $53.00Payment Due Date 4/20/12Late Payment Warning: If we do not receive your minimum payment by the date listed above, you may have to pay a $35 fee and your APR’s may be increased up to the Penalty rate of 28.99%Minimum Payment Warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example…

Interest Charge CalculationType of Balance

Annual Percentage Rate (APR)

Balance Subject to Interest Rate

Interest Charge

Purchases 14.99% $512.14 $6.31Cash Advances 21.99% $253.50 $4.58Balance Transfers 0.00% $637.50 $0.00

Summary of Account Activity

Previous Balance 535.07Payments -450.00Purchases +529.57Balance Transfers +785.00Cash Advances +318.00Past Due Amount +0.00Fees Charged +69.45Interest Charged +10.89New Balance $1,784.53 Credit Limit $2,000.00Available credit $215.47Statement closing date

3/22/2012

Days in billing cycle 30

If you make no additional charges using this card and

each month you pay…

You will pay off the balance shown on this statement in

about…

And you will end up paying an

estimated total of…

Only the minimum payment

10 years $3,284

$62 3 years $2,232

Notice of Changes to Your Interest RatesYou have triggered the Penalty APR of 28.99%. This change will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, the Penalty APR will apply to these transactions. We may keep the APR at this level indefinitely.Transactions made before 4/9/12: Current rates will continue to apply to these transactions. If you become more than 60 days late on your account, the Penalty APR will apply to hose transactions as well.

Important Changes to Your Account TermsThe following is a summary of changes that are being made to your account terms. For more detailed information, please refer to the booklet enclosed with this statement. These changes will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, APR for Purchases will increase to 16.99%.Transactions made before 4/9/12: Current APRs will continue to apply to these transactions.

2012 Totals Year-to-DateTotal fees charged in 2012 $90.14Total interest charged in 2012 $18.27

Andrew’s Credit Card Statement

Summary of Account Activity

This section includes payments, credits, purchases, balance

transfers, cash advances, fees,

interest charges, amounts past due, the new balance, available credit, and the last day

of the billing periodHow much did Andrew charge in new purchases

during this credit card billing cycle?$529.57

10

9

8

7

6

2

4

5

13

52

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89

Payment InformationNew Balance $1784.53Minimum Payment Due $53.00Payment Due Date 4/20/12Late Payment Warning: If we do not receive your minimum payment by the date listed above, you may have to pay a $35 fee and your APR’s may be increased up to the Penalty rate of 28.99%Minimum Payment Warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example…

Interest Charge CalculationType of Balance

Annual Percentage Rate (APR)

Balance Subject to Interest Rate

Interest Charge

Purchases 14.99% $512.14 $6.31Cash Advances 21.99% $253.50 $4.58Balance Transfers 0.00% $637.50 $0.00

Summary of Account Activity

Previous Balance 535.07Payments -450.00Purchases +529.57Balance Transfers +785.00Cash Advances +318.00Past Due Amount +0.00Fees Charged +69.45Interest Charged +10.89New Balance $1,784.53 Credit Limit $2,000.00Available credit $215.47Statement closing date

3/22/2012

Days in billing cycle 30

If you make no additional charges using this card and

each month you pay…

You will pay off the balance shown on this statement in

about…

And you will end up paying an

estimated total of…

Only the minimum payment

10 years $3,284

$62 3 years $2,232

Notice of Changes to Your Interest RatesYou have triggered the Penalty APR of 28.99%. This change will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, the Penalty APR will apply to these transactions. We may keep the APR at this level indefinitely.Transactions made before 4/9/12: Current rates will continue to apply to these transactions. If you become more than 60 days late on your account, the Penalty APR will apply to hose transactions as well.

Important Changes to Your Account TermsThe following is a summary of changes that are being made to your account terms. For more detailed information, please refer to the booklet enclosed with this statement. These changes will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, APR for Purchases will increase to 16.99%.Transactions made before 4/9/12: Current APRs will continue to apply to these transactions.

2012 Totals Year-to-DateTotal fees charged in 2012 $90.14Total interest charged in 2012 $18.27

Andrew’s Credit Card Statement

10

9

8

7

6

2

4

5

13Payment

InformationThis section includes

the total new balance, the minimum payment amount, and the date

payment is due

What is Andrew’s minimum payment due for

this billing cycle?$53.00

53

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89

Payment InformationNew Balance $1784.53Minimum Payment Due $53.00Payment Due Date 4/20/12Late Payment Warning: If we do not receive your minimum payment by the date listed above, you may have to pay a $35 fee and your APR’s may be increased up to the Penalty rate of 28.99%Minimum Payment Warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example…

Interest Charge CalculationType of Balance

Annual Percentage Rate (APR)

Balance Subject to Interest Rate

Interest Charge

Purchases 14.99% $512.14 $6.31Cash Advances 21.99% $253.50 $4.58Balance Transfers 0.00% $637.50 $0.00

Summary of Account Activity

Previous Balance 535.07Payments -450.00Purchases +529.57Balance Transfers +785.00Cash Advances +318.00Past Due Amount +0.00Fees Charged +69.45Interest Charged +10.89New Balance $1,784.53 Credit Limit $2,000.00Available credit $215.47Statement closing date

3/22/2012

Days in billing cycle 30

If you make no additional charges using this card and

each month you pay…

You will pay off the balance shown on this statement in

about…

And you will end up paying an

estimated total of…

Only the minimum payment

10 years $3,284

$62 3 years $2,232

Notice of Changes to Your Interest RatesYou have triggered the Penalty APR of 28.99%. This change will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, the Penalty APR will apply to these transactions. We may keep the APR at this level indefinitely.Transactions made before 4/9/12: Current rates will continue to apply to these transactions. If you become more than 60 days late on your account, the Penalty APR will apply to hose transactions as well.

Important Changes to Your Account TermsThe following is a summary of changes that are being made to your account terms. For more detailed information, please refer to the booklet enclosed with this statement. These changes will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, APR for Purchases will increase to 16.99%.Transactions made before 4/9/12: Current APRs will continue to apply to these transactions.

2012 Totals Year-to-DateTotal fees charged in 2012 $90.14Total interest charged in 2012 $18.27

Andrew’s Credit Card Statement

10

9

8

7

6

2

4

5

13Late Payment

WarningThis section states any additional fees and the

higher interest rate that may be charged if

a payment is late

How much is Andrew’s late payment fee?

$35

54

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89

Payment InformationNew Balance $1784.53Minimum Payment Due $53.00Payment Due Date 4/20/12Late Payment Warning: If we do not receive your minimum payment by the date listed above, you may have to pay a $35 fee and your APR’s may be increased up to the Penalty rate of 28.99%Minimum Payment Warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example…

Interest Charge CalculationType of Balance

Annual Percentage Rate (APR)

Balance Subject to Interest Rate

Interest Charge

Purchases 14.99% $512.14 $6.31Cash Advances 21.99% $253.50 $4.58Balance Transfers 0.00% $637.50 $0.00

Summary of Account Activity

Previous Balance 535.07Payments -450.00Purchases +529.57Balance Transfers +785.00Cash Advances +318.00Past Due Amount +0.00Fees Charged +69.45Interest Charged +10.89New Balance $1,784.53 Credit Limit $2,000.00Available credit $215.47Statement closing date

3/22/2012

Days in billing cycle 30

If you make no additional charges using this card and

each month you pay…

You will pay off the balance shown on this statement in

about…

And you will end up paying an

estimated total of…

Only the minimum payment

10 years $3,284

$62 3 years $2,232

Notice of Changes to Your Interest RatesYou have triggered the Penalty APR of 28.99%. This change will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, the Penalty APR will apply to these transactions. We may keep the APR at this level indefinitely.Transactions made before 4/9/12: Current rates will continue to apply to these transactions. If you become more than 60 days late on your account, the Penalty APR will apply to hose transactions as well.

Important Changes to Your Account TermsThe following is a summary of changes that are being made to your account terms. For more detailed information, please refer to the booklet enclosed with this statement. These changes will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, APR for Purchases will increase to 16.99%.Transactions made before 4/9/12: Current APRs will continue to apply to these transactions.

2012 Totals Year-to-DateTotal fees charged in 2012 $90.14Total interest charged in 2012 $18.27

Andrew’s Credit Card Statement

10

9

8

7

6

2

4

5

13

Minimum Payment Warning

This section includes an estimate of how

long it can take to pay off a credit card

balance if only the minimum payment is

made each month, and an estimate of the total amount paid, including

interest, if the bill is paid in three years

(assuming no additional charges are

made)How long will it take

Andrew to pay off the balance of his credit card if he only pays the minimum

payment?10 years

55

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89

Payment InformationNew Balance $1784.53Minimum Payment Due $53.00Payment Due Date 4/20/12Late Payment Warning: If we do not receive your minimum payment by the date listed above, you may have to pay a $35 fee and your APR’s may be increased up to the Penalty rate of 28.99%Minimum Payment Warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example…

Interest Charge CalculationType of Balance

Annual Percentage Rate (APR)

Balance Subject to Interest Rate

Interest Charge

Purchases 14.99% $512.14 $6.31Cash Advances 21.99% $253.50 $4.58Balance Transfers 0.00% $637.50 $0.00

Summary of Account Activity

Previous Balance 535.07Payments -450.00Purchases +529.57Balance Transfers +785.00Cash Advances +318.00Past Due Amount +0.00Fees Charged +69.45Interest Charged +10.89New Balance $1,784.53 Credit Limit $2,000.00Available credit $215.47Statement closing date

3/22/2012

Days in billing cycle 30

If you make no additional charges using this card and

each month you pay…

You will pay off the balance shown on this statement in

about…

And you will end up paying an

estimated total of…

Only the minimum payment

10 years $3,284

$62 3 years $2,232

Notice of Changes to Your Interest RatesYou have triggered the Penalty APR of 28.99%. This change will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, the Penalty APR will apply to these transactions. We may keep the APR at this level indefinitely.Transactions made before 4/9/12: Current rates will continue to apply to these transactions. If you become more than 60 days late on your account, the Penalty APR will apply to hose transactions as well.

Important Changes to Your Account TermsThe following is a summary of changes that are being made to your account terms. For more detailed information, please refer to the booklet enclosed with this statement. These changes will impact your account as follows:Transactions made on or after 4/9/12: As of 5/10/12, APR for Purchases will increase to 16.99%.Transactions made before 4/9/12: Current APRs will continue to apply to these transactions.

2012 Totals Year-to-DateTotal fees charged in 2012 $90.14Total interest charged in 2012 $18.27

Andrew’s Credit Card Statement

10

9

8

7

6

2

4

5

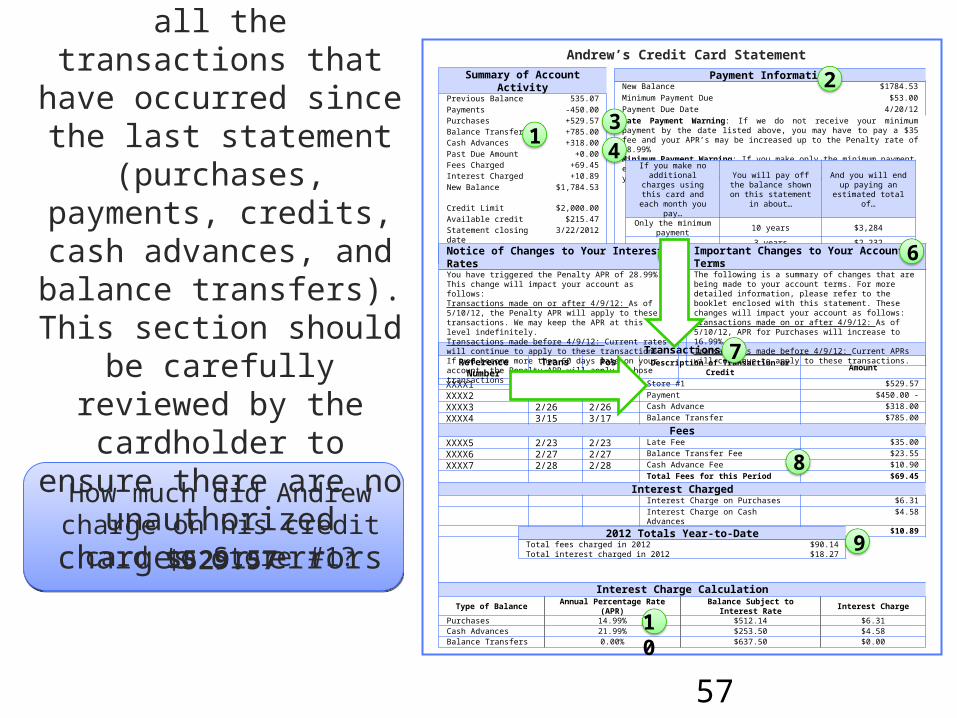

13Notice of Changes to

Your Interest RatesIf a cardholder triggers the Penalty APR, the

credit card issuer must notify them on their statement that their

rates will be increasing

Has Andrew triggered the Penalty APR?

Yes, he will pay 28.99% on all transactions made after 4/9/12.

56

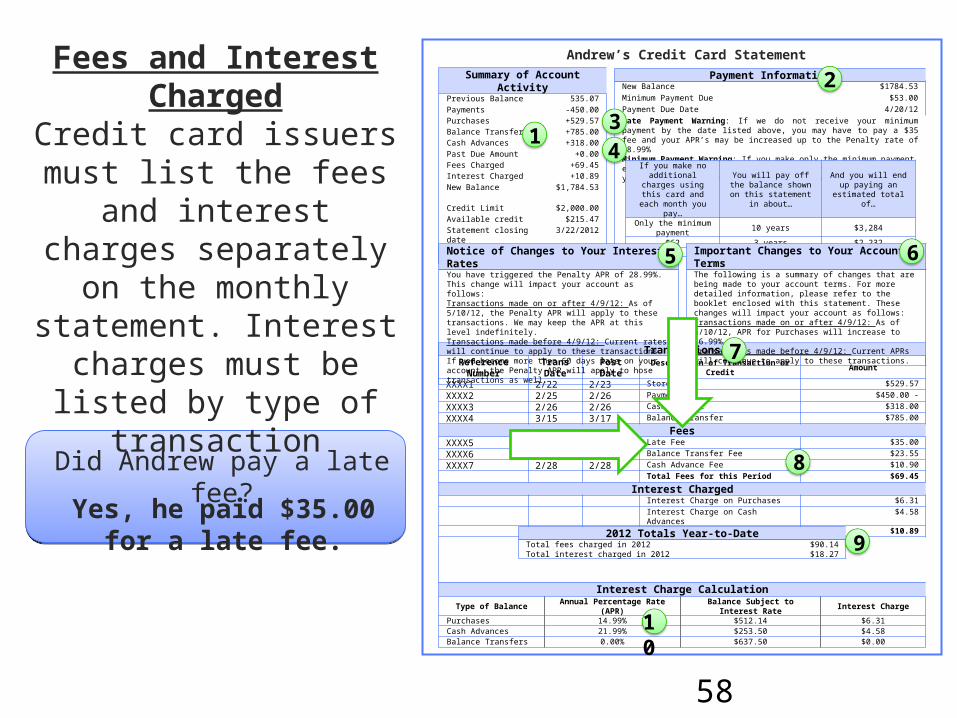

TransactionsReference Number

Trans Date

Post Date

Description of Transaction or Credit

Amount

XXXX1 2/22 2/23 Store #1 $529.57

XXXX2 2/25 2/26 Payment $450.00 -

XXXX3 2/26 2/26 Cash Advance $318.00

XXXX4 3/15 3/17 Balance Transfer $785.00

FeesXXXX5 2/23 2/23 Late Fee $35.00

XXXX6 2/27 2/27 Balance Transfer Fee $23.55

XXXX7 2/28 2/28 Cash Advance Fee $10.90

Total Fees for this Period $69.45

Interest Charged Interest Charge on Purchases $6.31

Interest Charge on Cash Advances $4.58

Total Interest for this Period $10.89