does the capital structure matter for islamic microfinance ... · pdf filedoes the capital...

TRANSCRIPT

WP# 1435-12

Does the Capital Structure Matter for Islamic Microfinance Institutions?

Abdul Ghafar Ismail, Bayu Taufiq Possumah

02 Ramadan 1433H | June 29, 2012

Islamic Economics and Finance Research Division

IRTI Working Paper Series

IRTI Working Paper 1435-12

Title: Does the Capital Structure Matter for Islamic Microfinance Institutions?

Author(s): Abdul Ghafar Ismail, Bayu Taufiq Possumah

Abstract

One of the leading and contemporarily become prominent issue in the finance institutions is the capital structure. Islamic microfinance institutions as one of instrument to solve the poverty problem have risen to the forefront as invaluable institutions in the development process. Since capital constraints have precluded the expansion of microfinance programs and microfinance institutions have had various degrees of performance and sustainability, the question of how best to finance these organizations is a key issue. This paper attempt to explore how changes and variety source of fund in capital structure could improve Islamic microfinance institutions efficiency and financial performance.

Keywords: Capital Structure, leverage ratio, Islamic Microfinance, Performance

JEL Classification: D40, D53, G21, G32,

Islamic Research and Training Institute

P.O. Box 9201, Jeddah 21413, Kingdom of Saudi Arabia

IRTI Working Paper Series has been created to quickly disseminate the findings of the work in progress and

share ideas on the issues related to theoretical and practical development of Islamic economics and finance

so as to encourage exchange of thoughts. The presentations of papers in this series may not be fully polished.

The papers carry the names of the authors and should be accordingly cited. The views expressed in these

papers are those of the authors and do not necessarily reflect the views of the Islamic Research and Training

Institute or the Islamic Development Bank or those of the members of its Board of Executive Directors or

its member countries.

Does the Capital Structure Matter for Islamic

Microfinance Institutions?

Abdul Ghafar Ismaili, BayuTaufiqPossumahii

1. Introduction

Microfinance institution is considered as a provider of financial services to low-income, consumers and the self-employed, who traditionally lack access to the banking and related services. Therefore, microfinance is regarded as an effective way to resolve poverty in many developing countries. Generally microfinance and micro-credit are synonymous. It refers to an array of financial services (targeting the poor) including financing, savings, and takaful while micro-credit is the provision of credit which is usually used as capital for small business development. Microfinance institution can be operated as Non-governmental Organizations (NGOs), cooperatives or other non-bank financial intermediaries or Islamic banks. Microfinance institutions have come as a breakthrough in the philosophy and practices of poverty eradication, and also economic empowerment and inclusive growth. However in some countries, given the extent of economic forces and lack of institutional arrangements (such as no legal and regulations) and also the lack of donors, microfinance is still an unfinished agenda.

In an effort to reducing poverty, in general, microfinance institutions face some obstacles such have extended limits of formal finance and involved the deprived predominantly females into formal commercial systems thus diversifying families’ income bases, physical, humanoid and social assets through decent money managing after economic tremors hence smoothening consumption (Hulme and Mosley, 1996; Hulme, 1999; Cohen, 2003). Extraordinary operating costs and capital constraints have vetoed microfinance institution from fulfilling the mammoth demand. Dehejia, Montgomery and Morduch (2005) exhibited that the demand for credit by the deprived is elastic. Hence, higher interest rates may limit microfinance institution capacity to attend to the poorer possible clienteles and urging that microfinance institution capital structure is critical for their sustainability and performance.

In recent years, internal and external pressures for the microfinance institutions have been increasing to decrease dependence on subsidized or grant funding. It means that microfinance institution should be looking for external funding. Hence, the issue of capital structure looks worth to be discussed. By referring to Coleman (2007), financial theory has made considerable progress in efforts at explaining capital structure decisions and its determinants. In this quest, various theoretical models have been proposed to explain capital

i He is head of research division and Professor of Banking and Financial Economics. He is currently on

leave from School of Economics, Universiti Kebangsaan Malaysia. He is also principal research fellow,

Institut Islam Hadhari, Universiti Kebangsaan Malaysia and AmBank Group Resident Fellow for

Perdana Leadership Foundation. ii Postdoctoral Researcher, Institut Islam Hadhari, Universiti Kebangsaan Malaysia

* Paper has been presented at the Thematic Workshop on Business Models in Islamic Microfinance, 6

nd 7 May 2014, International Islamic University of Islamabad, Pakistan

2

structure patterns across companies and countries, and many of these models have been empirically tested in the real business world. However, most of this research has concentrated on large and listed firms, mostly in the developed world, with the consequence that other critical sectors such as microfinance institutions, especially in developing economies, have been neglected.

On the other hand, the strong financial performance paves the way for the social mission of microfinance institutions to be successful. The external funding may increase the cost that may affect the financial performance. Thus, understanding the effect of capital structure on the financial performance is crucial in reducing the poverty.

The main objective of this paper, therefore, focuses on how changes and variety sources of fund in capital structure could improve microfinance institutions especially their efficiency and financial performance.

The remaining discussion of this paper will be divided into six sections. We discuss about the facts about capital structure in microfinance institutions in section2. Funding sources and profitability will also be discussed. Then leverage ratio and its impact to microfinance performance, and profitability and capital structure will be analyzed sequentially in sections 3 and 4. The last section is conclusion.

2. The Stylized Facts about Capital Structure in Microfinance Institutions

Financial sustainability has been identified as one of the issues in the livelihood of microfinance institutions. The issue is necessary condition for institutional sustainability (Hollis and Sweetman, 1998 and Thapa, et al., 1992). It has been defined as the ability of microfinance institutions to cover all its costs from its own generated income from operations without depending on external support or subsidy. Dunford (2003) defines financial sustainability as the ability to keep ongoing towards microfinance objective without continued donor support. Both definitions center on one point that is the ability to depend on self-operation and the possibility of making profit out of the operations.

The sustainability, as mentioned by Otero and Rhyne (1994), involves different stages. It starts from the stage when the microfinance institutions are totally dependent on subsidies and grants for running its operations to the final stage when the programs are fully financed from resources mobilized from the clients and on funds raised from financial institutions on commercial rates of return. While according to Meyer (2002) financial sustainability can be measured in two stages, these are operational sustainability and financial self-sufficiency. Operational sustainability refers to the ability of the microfinance institutions to cover its operational costs from its operating income regardless of whether it is subsidized or not. On the other hand, microfinance institutions are financially self- sufficient when they are able to cover from their own generated income, both operating and financing costs and other form of subsidy valued at market prices. Then Hulme and Mosley (1996) assert that sustainable financial institutions should be able to reduce transaction cost, allocate resources efficiently, manage risk and also make their resources grow dynamically.

Therefore, financial sustainability depends on multiple factors. One factor that affect to financial sustainability of microfinance institutions is capital structure. Given significant capital structure, expansion of microfinance programs remains a formidable challenge facing the microfinance industry. Moreover, it is observed that microfinance institutions have had various degrees of sustainability. Capital structure describes how a microfinance institution

3

finances its assets. This structure is usually a combination of several sources of debt and equity. Wise microfinance institutions use the right combination of debt and equity to keep their true cost of capital as low as possible. Depending on how complex the structure, there may in fact be dozens of financing sources included, drawing on funds from a variety of entities in order to generate the complete financing package.

Figure 2 shows the funding structure of MFIs according to their region and charter type. In most regions debt represented at least one-third of the funding sources of MFIs. NBFIs and especially NGOs are reliant on debt as a source of funding since deposit mobilization for these institutional types tends to be more limited, with the exception of Africa.

4

Figure1. MFI Funding Structure Evolution 2007-2010

Source: MIX Market, 2007-2010. Cross Market Analysis

Figure2.MFI Funding Structure Evolution by region 2010

Source: MIX Market, 2007-2010. Cross Market Analysis. EAP = East Asia and the Pacific, ECA= Eastern Europe and Central Asia, LAC = Latin America and the Caribbean, MENA = Middle East and North Africa, S.Asia = South Asia

The facts that microfinance institutions are often financed by a combination of grants and

concessional funding, so there are four types of funding used by microfinance institutions MFI.

5

Deposits

Figure1 and Figure 2 show that deposits become the main sources of liabilities. Normally, microfinance institutions serve the low income group. They use small deposits to fund their financing operations. Therefore, they cannot take for granted that any of their deposits are stable. In long term, they should analyze typical savings patterns in their portfolio of deposit products. The analysis then informs their liquidity management and their funding strategy. Accordingly, deposit-taking microfinance institutions should use the same type of analysis on their deposit products, and refine their liquidity planning and funding operations accordingly.

They should also realize that some portion of small balance deposits in their portfolio could be considered a stable source of funds. Therefore, microfinance institutions should analyze their particular depositor base to determine what proportion of it can safely be used for long-term financing. The analysis should be done by broad product categories (e.g., current accounts, demand savings, and time deposits) and should include at least three years of monthly and one year of daily data points to capture long-run trends, seasonal effects and daily volatility patterns.

Debt

As shown in Figure 1 and Figure 2, borrowing becomes the second important sources of liabilities. The importance sources of borrowing come from public-sector institutions and donors. It allows microfinance institutions to enjoy lower cost of borrowing and maturities that would be difficult to obtain from domestic or international commercial lenders. Borrowing from these former sources allows microfinance institutions to reduce liquidity and term mismatch risks. At the same time, the cost of borrowing charged by these sources is clearly positive in real terms and is trending up toward commercial rates. This would produce the creation of serious distortions in the financial system and at the same time prepares microfinance institutions to increasingly access commercial financing.

But the importance of debt financing for microfinance institutions also raises a number of questions about how microfinance institutions fund their operations. What types of actors lend money to microfinance institutions? What instruments are used to finance them? How prevalent is cross-border funding? In which countries can microfinance institution access local market debt and why? How much do microfinance institutions pay to borrow and what are the terms of their borrowings?

Therefore, borrowing also raises several risks faced by microfinance institutions. First, when microfinance institutions have credit lines that have not been fully utilized, liquidity management is greatly facilitated since these funds can be mobilized quickly to deal with short-term difficulties. Second, exchange rate risk is normally increased, given that a substantial part of microfinance institutions borrowing is in foreign currency, while most microfinance institutions financing are in local currency. Third, cost of borrowing risks are also increased, given that most microfinance institutions borrowing is at variable rates (especially borrowing from government second tier facilities, donors and social investors) and most microfinance institutions financing are at fixed rates. Finally, borrowing may increase concentration risk, by leading microfinance institutions to depend on a small number of creditors.

6

Bond Issue

Borrowing can also happen through issuing bond. Bond is considered as debt instrument. Microfinance institutions can issue bond at national and international capital markets. However, direct investment in debt instruments may raise investors' concerns with respect to the related liquidity risk. Microfinance institutions are not publicly listed and bond investment occurs through privately placed assets that are not liquid in the short term. In addition, there are often no local secondary markets for the trading of debt instruments issued by microfinance institutions. Therefore, indirect investment through specialized microfinance funds enables investors to diversify the specific risk of a particular microfinance institution and to partly avoid the liquidity risk

Stock Issue

Microfinance institutions may use a medium-term strategy for funding the asset side through a capitalization plan. There are three main scenarios for incorporating new shareholders. The first scenario is the option to choose the non-governmental organizations (NGOs) that have become regulated. The second scenario occurs via the entities, such financial intermediaries and non-financial companies, in which the shares are primarily owned by private investors. The third scenario involves privatizing microfinance institutions that are owned by the government-linked companies. These scenarios may affect the ownership structure that lead towards a social-based or profit-based microfinance institutions.

7

Table 1: Equity, Deposit and Debt by Regions

Region

Number of

MFI

Equity (USD

million)

Deposit (USD

million)

Debt (USD

million)

2007

Africa 300 1,160.5 3,323.2

682.9

East Asia and The Pasific 194 1,127.1 6,024.5

1,857.9

Eastern Europe and Central Asia 324 1,739.2 5,040.4

3,980.1

Latin America and Central Caribbean 382 3,000.1 8,834.4

4,868.2

Middle East and North Africa 59 466.4 62.9

716.1

South Asia 195 913.0 1,183.3

2,154.4

2008

Africa 299 1,309.8 4,016.9

978.9

East Asia and The Pasific 179 1,323.7 6,151.5

2,821.8

Eastern Europe and Central Asia 313 2,141.8 6,141.0

4,707.1

Latin America and Central Caribbean 402 3,391.4 10,042.2

5,106.3

Middle East and North Africa 69 577.8 75.6

803.4

South Asia 220 1,265.2 1,996.9

2,991.5

2009

Africa 358 1,647.7 5,366.1

1,198.4

East Asia and The Pasific 191 1,610.3 10,216.9

3,515.5

Eastern Europe and Central Asia 270 2,500.9 5,242.6

4,707.6

Latin America and Central Caribbean 408 4,430.6 13,508.9

5,972.3

Middle East and North Africa 73 641.3 121.3

789.3

South Asia 254 1,797.9 2,591.9

4,755.2

2010

Africa 355 1,882.9 6,680.2

1,503.8

East Asia and The Pasific 195 3,339.3 32,924.0

3,267.8

Eastern Europe and Central Asia 265 2,326.9 7,423.7

3,872.5

Latin America and Central Caribbean 431 5,386.2 15,781.4

6,728.7

Middle East and North Africa 71 681.7 142.3

752.6

South Asia 263 2,223.2 3,369.8

5,392.1

2011

Africa 294 2,329.9 8,028.6

1,753.4

East Asia and The Pasific 235 4,486.4 31,084.1

2,853.2

Eastern Europe and Central Asia 243 2,728.2 7,715.5

4,486.2

Latin America and Central Caribbean 420 6,503.7 20,194.8

7,728.3

8

Middle East and North Africa 59 727.2 247.3

737.8

South Asia 248 2,185.3 3,283.7

4,062.7

2012

Africa 313 2,377.7 5,008.7

4,094.9

East Asia and The Pacific 157 5,266.1 46,654.1

937.2

Eastern Europe and Central Asia 204 2,639.7 7,298.3

4,248.4

Latin America and Central Caribbean 372 7,103.1 24,118.7

7,884.2

Middle East and North Africa 38 596.7 22.0

599.5

South Asia 165 1,304.5 3,482.0

4,268.5

Source: Cross-Market Analysis (Mixmarket.org)

3. Leverage Ratio and Its impact to Microfinance Performance

Generally leverage ratio is defined as any ratio used to calculate the financial leverage (or capital structure) of a company. It gives an idea of the company's methods of financing or to measure its ability to meet financial obligations. According to the trade-off theory, a classical view of capital structure theory, the determination of capital structure is the strategic decision of company, and it is different for every industry and for every company. The companies should choose optimal target leverage ratios to balance bankruptcy risks with the tax benefits from debt financing (Chen and Zhao, 2006). This theory also suggest that firm should choose best combination of debt and equity, firm should try to minimize its weighted average cost of capital.

Leveraging is a way to use funds whereby most of the money is raised by borrowing rather than by stock issue (for a company) or use of capital (by an individual). At its most basic, leveraging means taking out a loan so that company can invest the money and hoping the investment makes more money than company will have to pay in interest on the loan. A high debt to equity ratio may show up possible difficulty in paying interest and capital while obtaining extra funding.

Another leveraging ratio can be used to measure the operating cost mix. This helps to indicate how any change in output may affect operating income. There are two types of operating costs: fixed and variable. The mix of these will differ depending on the company and the industry. A high operating leverage can lead to forecasting risk. For example, a tiny error made in a sales forecast could trigger far bigger errors when it comes to projecting cash flows based on those sales. There is also interest coverage, which measures a company’s margin of safety and indicates how many times the company can make its interest payments. This figure is calculated by dividing earnings prior to interest and taxes by the interest expense.

The issue of capital structure has been studied intensely since Modigliani and Miller published their landmark paper, “The Cost of Capital, Corporate Finance and the Theory of Investment”. Modigliani and Miller (1958) argue that capital structure is irrelevant to the value of the company. They set the following assumptions: existence of perfect capital market, homogeneous expectations, absence of taxes and no transaction costs. This theory then known as irrelevant theory. Modigliani and Miller (1958) further argue that both levered and unlevered companies have same value, which is determined through its profitability, regardless of its capital structure.

9

In another study, Berger and Bonaccorsi di Patti (2006) also found that a high ratio of debt might reduce agency costs, on the other side the same level of debt will increase the value of the companies for two reasons: firstly, if a company leverage over a certain point, it also increases the expected costs of financial distress, bankruptcy or liquidation; secondly it also increases the conflict between shareholders and debt holders. As a consequence these agency costs lead to higher interest expenses to compensate debt holders of the risk.

Later studies have considered other relevant elements which are related to capital structures such as tax advantages, transaction costs, asymmetric information, or corporate control, for examples Faulkender and Petersen (2006); Harris and Raviv (1991); Titman and Wessels (1988); Bradley, Jarrell, and Kim (1984), Baker and Martin (2011), and Pfaffermayr (2013). In the presence of tax advantages and transaction costs, the studies reported that capital structure is found to be having both influence on profitability and sustainability of a company. Thus, capital structure of company has become much more salient issues.

Theoretically, the capital structure of a company also reports a trade-off of high profits in fragile markets and low profits in safe markets. It shows that capital structure affects the financial performance. By looking at the studies that link both variables, the relation may be classified into two categories. First, based on information asymmetries and signaling. Internally, companies possess some private information about the characteristics of the company information asymmetries between borrowers and lenders induce some adverse selection problems: the impossibility of lenders to price a loan according to the borrower’s quality results in an imperfect pricing, leading to credit rationing (Stiglitz and Weiss, 1981). The second category, Jensen and Meckling (1976) assumed that significant agency costs can indeed arise from conflicts of interest between categories of agents (managers, shareholders, debt-holders). The authors identify in fact two types of conflicts that have different implications leading to opposite theories on the link leverage-performance.

Furthermore, Well (undate) observed two additional key elements for the understanding of the link leverage-performance. The first element is the fact that all studies test this link only in one country, which can explain the different results as the institutional framework may play a role on the relationship between leverage and financial performance. The second element concerns the used measures of performance, either accounting measures of total factor productivity indicators or efficiency scores to evaluate performance. Efficiency scores own a couple of advantages in comparison of other measures of performance. Comparing to raw measures of performance, efficiency scores allow the inclusion of several outputs and inputs and provide consequently synthetic measures of performance. In comparison to all other measures of performance (raw measures or productivity measures), efficiency scores have the advantage to offer relative scores that take directly into account the comparison with the best companies.

4. Islamic Microfinance Profitability and Capital Structure

Islamic microfinance institutions play an important role in promoting socio-economic development of the poor and small entrepreneurs without charging interest (riba). Therefore, Islamic microfinance institutions should be operated without interest. They can be operated base on sharia principles. The operations can earn profits from three areas: trading, leasing and by direct financing in risk sharing contacts. Currently, according to the CGAP2013 note on Islamic microfinance, the overall supply of Islamic products is still quite small relative to the conventional microfinance sector in spite of a twofold increase in the number of providers

01

and in the number of poor client using sharia-compliant products. CGAP surveys in 2011 also states that customers using sharia-compliant products represent less than 1 percent of total microfinance outreach.

Refer to CGAP 2013 survey, the majority of microfinance institutions offering sharia-compliant microfinance services, in terms of absolute number, are rural banks. However, commercial banks are the largest providers of Sharia-compliant financial services when measured by the number of clients served. Commercial banks serve 60 percent of the 1.28 million Islamic microfinance clients served, whereas rural banks serve only 16 percent (see Figure 3).

00

Figure 3: Institutions Offering Islamic Microfinance Products

Sources: CGAP 2013 Survey

Figure 3 shows that Islamic microfinance products are offered by private investors like micro-finance bank, commercial bank and rural bank. There is only a small portion that is owned by NGO or foundation. It shows that their main motives are profit.

Next, in this section, we would like to examine one of critical issue in Islamic microfinance studies that begins with a question; is Islamic microfinance institution profitability determined also by capital structure as reflected to others non-financial companies? The question arises since there are some different sources of funding between conventional microfinance and Islamic microfinance. The question is supported also by the matter of fact that conventional microfinance profitability determined by capital structure from different sources and choice of fund as analyzed by some researchers such Muriu (2011), Abor (2005), Michaelas et al. (1999) etc. In light of that research question, this study seeks to broaden and deepen our understanding on the impacts of capital structure on Islamic microfinance profitability.

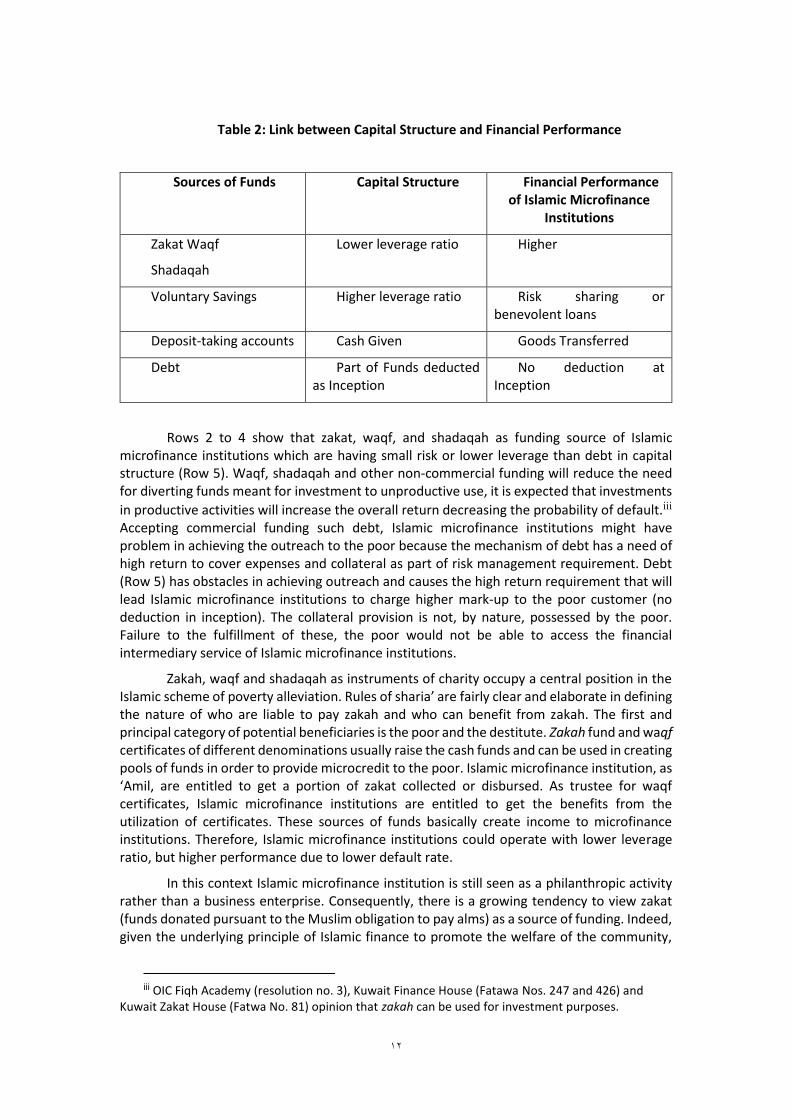

Generally Islamic microfinance funded by four sources, (i) Islamic microfinance funds under the wakalah model, zakah fund, Shadaqah, waqf and tabaru’ money – Row 2, Table 2; (ii) voluntary saving accounts – Row 3, Table 2; (iii) deposit-taking accounts - Row 4, Table 2; (iv) borrowing on commercial basis - Row 4, Table 2.

02

Table 2: Link between Capital Structure and Financial Performance

Sources of Funds Capital Structure Financial Performance of Islamic Microfinance

Institutions

Zakat Waqf

Shadaqah

Lower leverage ratio Higher

Voluntary Savings Higher leverage ratio Risk sharing or benevolent loans

Deposit-taking accounts Cash Given Goods Transferred

Debt Part of Funds deducted as Inception

No deduction at Inception

Rows 2 to 4 show that zakat, waqf, and shadaqah as funding source of Islamic microfinance institutions which are having small risk or lower leverage than debt in capital structure (Row 5). Waqf, shadaqah and other non-commercial funding will reduce the need for diverting funds meant for investment to unproductive use, it is expected that investments

in productive activities will increase the overall return decreasing the probability of default.iii Accepting commercial funding such debt, Islamic microfinance institutions might have problem in achieving the outreach to the poor because the mechanism of debt has a need of high return to cover expenses and collateral as part of risk management requirement. Debt (Row 5) has obstacles in achieving outreach and causes the high return requirement that will lead Islamic microfinance institutions to charge higher mark-up to the poor customer (no deduction in inception). The collateral provision is not, by nature, possessed by the poor. Failure to the fulfillment of these, the poor would not be able to access the financial intermediary service of Islamic microfinance institutions.

Zakah, waqf and shadaqah as instruments of charity occupy a central position in the Islamic scheme of poverty alleviation. Rules of sharia’ are fairly clear and elaborate in defining the nature of who are liable to pay zakah and who can benefit from zakah. The first and principal category of potential beneficiaries is the poor and the destitute. Zakah fund and waqf certificates of different denominations usually raise the cash funds and can be used in creating pools of funds in order to provide microcredit to the poor. Islamic microfinance institution, as ‘Amil, are entitled to get a portion of zakat collected or disbursed. As trustee for waqf certificates, Islamic microfinance institutions are entitled to get the benefits from the utilization of certificates. These sources of funds basically create income to microfinance institutions. Therefore, Islamic microfinance institutions could operate with lower leverage ratio, but higher performance due to lower default rate.

In this context Islamic microfinance institution is still seen as a philanthropic activity rather than a business enterprise. Consequently, there is a growing tendency to view zakat (funds donated pursuant to the Muslim obligation to pay alms) as a source of funding. Indeed, given the underlying principle of Islamic finance to promote the welfare of the community,

iii OIC Fiqh Academy (resolution no. 3), Kuwait Finance House (Fatawa Nos. 247 and 426) and

Kuwait Zakat House (Fatwa No. 81) opinion that zakah can be used for investment purposes.

03

zakat funds appear ideally suited to support Islamic microfinance. However, a heavy reliance on charity is not necessarily the best model for the development of a large and sustainable sector, and more reliable, commercially motivated streams of funding should be explored. In significant ways, current Muslim philanthropy is becoming more focused in its aims to use available resources more effectively to tackle the underlying causes of important social problems without confining itself to assuage the effects of social issues.

A proportional deposit as a percentage of total assets (Row 3-Table 2, Row 2-Table 3 and Row 4-Table 2, Row 4-Table 3) also can improve profitability of Islamic microfinance institution, associated with assumption that the deposits program is cost efficient. Related to this assumption, voluntary deposit mobilization may help Islamic microfinance institutions achieve independence from donors and investors, which is particularly important in periods of liquidity constraints. Savings mobilization may therefore lead to greater profitability since it provides Islamic microfinance institutions with inexpensive and sustainable source of funds for lending. This perhaps explains why it is an indispensable element for well-performing Islamic microfinance institutions. Deposits may however require widespread branching and other expenses. But for Islamic microfinance institutions to collect deposits, they require license for taking public deposits which calls for transition to regulation.

The differences of funding sources and the methods of financing affect differently on institutional performance, particularly in terms of profitability and viability. Thus, in order to capture the effects of capital structure on Islamic microfinance profitability, we will summarize the findings from empirical studies. The study done by Muriu (2011) which

analyzed data taken from Mix Market group,iv tried to establish the impact of different sources of funding on microfinance institutions profitability which include: (i) accept deposits; (ii) deposits relative to assets ratio; (iii) loans relative to assets ratio; and (iv) debt to equity ratio (gearing). Given that capital structure data is specific to microfinance institutions and collected from Mix Market, we will also utilize the Mix Market definitions of key variables as reported in Table 3.

Table 3: Funding Source of Microfinance Institutions

Variable Notation Measure Affect Source of Data

Accepts

Depositv

DEP Value of 1 if microfinance institutions accept deposits and 0 otherwise

Positive The Mix Market

Portfolio to Assets

Portfolio Asset

Adjusted Gross Loan

Positive The Mix Market

ivThe MIX Market and Micro Banking Bulletin databases are produced by the Microfinance

Information Exchange (MIX),www.themix.org. Data on individual MFIs in the Micro Banking Bullet are confidential and can only be used with the permissionof the respective MFI

v “Deposits” in this study refer to general type of instrument used by MFI to mobilize deposits and not

restricted to specific instrument, such as time deposits or saving accounts

04

Portfolio/adjusted Total Assets

Deposits to Assets

Deposit Asset

Voluntary Deposit/Adjusted Gross Loan Portfolio

Positive The Mix Market

Debt to Equity (Gearing)

GR Debt/Equity ratio

Indeterminate The Mix Market

Capital CAP Equity/Assets Positive The Mix Market

Source: Mixmarket.org

We also try to analyze the findings from empirical study done by Ahmed (2002). He provides a comparative analysis of conventional microfinance institutions and Islamic microfinance institutions operating in Bangladesh. In measuring profitability and efficiency of Islamic microfinance institutions, he follows Rose and Frase (1988). As presented in column 1, Table 3, he use some ratios such as: (i) Return on Assets (ROA) = (Net Income/ Assets), (ii) Net Interest (Return) Margin (NIM) = [Total income from investment, and interest-Total borrowing Cost (interest payments)/ Total Assets]; (iii) Operating Costs as a Percentage of Loan Disbursed (OCL) = (Operating Costs/Loan Disbursed), and (iv) Beneficiaries to Employee Ratio (BER) = Total Beneficiaries/Full-time Employees. After comparing financial ratios of the Islamic microfinance institutions with well-established and largest conventional microfinance institutions, he found that Islamic microfinance institutions have performed relatively well when compared to the well-established conventional microfinance institutions in terms of profitability and efficiency. Among the Islamic microfinance institutions, Rescue has the poorest figures. Rescue, however, has some indicators that are better than conventional MFI. The comparisons given are shown in Column 2-5, Table 4.

Table 4: Comparison Profitability and Efficiency between Conventional and Islamic Microfinance Institutions

Islamic Microfinance Institutions

Conventional Microfinance Institutions

Return on Assets (ROA): (Net Income/ Assets)*100

0.49 -0.50

Net Interest (Return) Margin (NIM): (interest payments) / Total

Assets]*100

19.5 6.9

Operating Costs as a Percentage of Loan Disbursed (OCL) = (Operating

Costs/Loan Disbursed)*100

9.6 12.7

05

Beneficiaries to Employee Ratio (BER) (% of Total)

169.8 174.2

Capital Structure (Fund

accumulated)vi (% of Total)

13.2 36.0

Source: Ahmed (2002)

Table 4 explains that Islamic microfinance institutions have performed the best among the microfinance institutions in terms of economic viability. It has the highest ROA and NIM and the lowest OCL. Islamic microfinance institutions, however, is not productive in terms of reaching the beneficiaries as it has the lowest BER. It also can operate with a lower capital structure.

Supporting to the above finding, Ines and Asma (2013) gauge the relative performance of Islamic microfinance institutions compared to conventional institutions in Arab countries during the crisis 2005-2010. Ines and Asma (2013) provide an empirical evidence of the performance comparison between Islamic and conventional microfinance institutions using an array of indicators measuring financial performance and outreach. By using DEA, they found that there is a significant difference in the average efficiency for the two groups. On average, DEA estimators reveal that Islamic microfinance institutions appear to be more efficient than conventional institutions for the first sub-period 2005-2007. For this sub-period, the average efficiency of conventional microfinance institutions evolves inversely to the average efficiency of Islamic microfinance institutions. The change was recorded in the average performance begins in 2007 when the Global Financial Crisis started. These results give evidence, contrary to expectations, of the superior performance of conventional microfinance institutions during the crisis. Performance of these institutions is also more stable in the time. But the majority of the microfinance institutions from the MENA region are NGO and not commercial banks and most Islamic microfinance institutions offer both conventional and Islamic products, except the case of Sudan and Iran where only Islamic products are permitted. But not all institutions provide separate sets of financial statements which make difficult to compute quantitative indicators.

Hence, the several findings reported above show that Islamic microfinance institutions profitability correlated with some of capital structure variables which is referred to the mix of different types of securities (long-term debt, common stock, preferred stock) issued by a Islamic microfinance institutions to finance its assets. Funding source of Islamic microfinance institutions is primarily a combination from outright donor grants, government subsidies, and in the later stage of microfinance development commercial funding. Then, by utilizing the MIX Market definitions of financial and operational sustainability, these studies indicate that the size of a microfinance institution’s assets and a microfinance institution’s capital structure are very associated with sustainability.

Notably, grants as a percent of assets is significant and negatively related to sustainability. We can see that for Islamic microfinance institution size does matter and the use of grants does have a negative relationship with sustainability. This reinforces the view that the long term use of grants may be related to greater (more costly) outreach or to inefficient operations due to lack of competitive pressures associated with attracting market funding. Thus, grants could hinder the development of Islamic microfinance institution into competitive, efficient, sustainable operations. But sometime obtaining subsidies or grants

vi Debt funding percentage from total capital

06

raise dependency issue of microfinance to donor and government even though not necessarily a negative factor in itself; it is actually useful for sustainability, but it is unpredictable.

In avoiding this dependency and unpredictability Islamic microfinance institution may focus on Qard Hassan products with no fees or a small fee. However, this product may unable to cover operational costs and remained dependent on subsidies which prevented a wide outreach. Islamic microfinance institutions may Murabahah which is the closest to the conventional microcredit. To be sustainable, Islamic microfinance institutions may charge make-up rate and fees that are equal or higher than the lending rates of conventional loans. However, it may make clients wary because of the high cost of services. Thus, the efficiency of a microfinance institution should not be measured so much on a lower dependence on grants and loans, but on the capability of keeping these funding sources stable over time.

5. Conclusion

This paper attempts to explore how changes and variety sources of fund in capital structure could improve Islamic microfinance institutions efficiency and financial performance. Our analysis produces the following findings: first, Islamic microfinance institutions have to strengthen the capital structure to achieve the performance objective, then sustainability will also be achieved simultaneously. Second, the microfinance institution should have a strong source of funding and to be managed with the view of making it sustainable. However, to be able to offer low costs of financing, Islamic microfinance institutions should practice a combination of funding source, i.e., savings, debt, and grant, and also Islamic microfinance institutions should utilize alternative cheap funding, such as: philanthropy funds. Third, each type of funding has its own benefit and limitation, if Islamic microfinance institutions use grant and subsidies, they raise dependency issue of microfinance to donor and government, therefore Islamic microfinance institutions should find other funding alternative which is relatively stable and cheap source of funds; it will reduce dependency on external borrowing. Free microfinance from subsidies dependency considered as the idea to the better future of Islamic microfinance institutions.

07

References

Abdul Rahman, Abdul Rahim, 2007. Islamic Microfinance: A Missing Component in Islamic Banking, Kyoto Bulletin of Islamic Area Studies, 1-2(2007): 38-53

Abor, J. (2005) “The effect of capital structure on profitability: An empirical analysis of listed firms in Ghana”, The Journal of Risk Finance, 6(5): (438-447)

Ahmed, H, 2002. Financing Micro Enterprises: An Analytical Study of Islamic Microfinance Institutions, Journal of Islamic Economic Studies 9(2)

Alaeddin, Omar and Anwar, Nurhayati, (2013), Critical Analysis of Diverse Funding Of Islamic Microfinance Institution: A Case Study in BMT Amanah Ummah Surabaya Indonesia, Proceeding 2nd ISRA Colloquium, Malaysia

Berger, A. N. and E. Bonaccorsi di Patti, (2006), ‘Capital Structure and Firm Performance: A New Approach to Testing Agency Theory and an Application to the Banking Industry’, Journal of Banking and Finance, Vol. 30, pp. 1065-1102

Chen, Long and Zhao, Xinlei, (2006), Mechanical Mean Reversion of Leverage Ratios, Department of Finance, Michigan State University

Cohen, M. (2003) The Impact of Microfinance, CGAP Donor Brief 13, www.cgap.org/gm/document-1-9.2407/DonorBrief_13.pdf

CGAP (2003), “Microfinance consensus guidelines: Guiding principles on regulation and supervision of microfinance”, Washington, DC

Dunford, C. (2003), “The Holy Grail of Microfinance: Helping the poor and sustainable: Microfinance evolution, Achievements and Challenges”, ITDG, London

Dehejia, M., H. Montgomery, and J. Morduch (2005), “Do Interest Rates Matter? Credit Demand in the Dhaka Slums”, Working Paper

Faulkender and Petersen (2006), Does the Source of Capital Affect Capital Structure? The Review of Financial Studies, V0l. 19, No. 1

Harris, M. and A. Raviv (1991), ‘The Theory of Capital Structure’, Journal of Finance, Vol. 46, pp. 297-355

Hollis, A. and Sweetman, A. (1998), “Micro-credit: What can we learn from the past?”, World Development, vol. 26, pp.1875-91

Hulme, David, and Paul Mosley (1996), Finance Against Poverty, Routledge, London

Hulme, D. (1999). Client Drop-outs From East African Microfinance Institutions. Mimeo, Micro Save

Iezza, P.(2010) “Financial sustainability of microfinance institutions (MFIs): an empirical analysis”, Master’s Thesis, Copenhagen Business School

Ines Ben Abdelkader, Asma Ben Salem, (2013), Islamic vs Conventional Microfinance Institutions: Performance analysis in MENA countries, International Journal of Business and Social Research, Vol.3 No.5

Jensen, M. & Meckling, W. (1976) “Theory of the Firm: Managerial behaviour, agency cost and Ownership Structure”, Journal of Financial Economics, 43: 271-281

Kyereboah-Coleman, A. (2007) “The Impact of Capital Structure on the Performance of microfinance institutions”, The Journal of Risk Finance, 8(1): 56-71

08

Baker, H. Kent and Martin, Gerald S., (2011), Capital Structure and Corporate Financing Decisions, John Wiley & Sons

Maisch, Felipe Portocarrero, et.al, (2006), How Should Microfinance Institutions Best Fund Themselves? Inter-American Development Bank, Washington, D.C.

Meyer, J. (2002), “Track record of financial institutions in assessing the poor in Asia”, ADB research institute paper, No. 49, [Online] Available: http://www.esocialsciences.com/articles (September 30, 2011)

Modigliani, F. & Miller, M.H. (1958), “The cost of Capital, Corporate Finance and the Theory of Investment”, American Economic Review, 48: 261-297

Michaelas, N., Chittenden, F. & Poutziouris, P., 1999, 'Financial Policy and Capital Structure Choice in UK SMEs: Empirical Evidence from Company Panel Data', Small Business Economics 12, 113-130

Peter W Muriu, (2011), Microfinance Profitability, Theses, Birmingham Business School University of Birmingham

Pfaffermayr, M., Stockl and H., Winner (2013) Capital Structure, Corporate Taxation and Firm Age. Fiscal Fiscal Studies, 34 (Issue 1): 109-135.

Otero, M and Rhyne, E, eds (1994), The New World of Microenterprise Finance, London: IT Publications

Rose, P.S. and D.R. Fraser (1988). Financial Institutions: Understanding and ManagingFinancial Services. Business Publications: Plano Tex, USA

Sharma, S. R. and Nepal, V., (1997), Strengthening of Credit Institutions /Programs for rural poverty alleviation in Nepal, United Nations, Economic and Social Council (ECOSOC) for Asia and Pacific, Bangkok, Thailand

Stiglitz, J., and Weiss, A., (1981), Credit rationing in markets with imperfect information, American Economic Review 71 (3), 393}410

Thapa, B., et.al, (1992), “Banking with the poor, report and recommendations prepared by lending Asian banks and non-governmental organizations”, Brisbane, Australia

Titman, S. and R. Wessels (1988), ‘The Determinants of Capital Structure Choice’, Journal of Finance, Vol. 43, pp. 1-19

Weill, Laurent, (undate), Leverage and Corporate Performance :A Frontier Efficiency Analysis, unpublished paper