document of the world bankdocuments.worldbank.org/curated/pt/... · nrb nepal rastra bank pad...

TRANSCRIPT

Document of The World Bank

Report No: ICR2218

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IDA-37270 TF-50593)

ON A

CREDIT

IN THE AMOUNT OF SDR 12.4 MILLION

(US$ 16.0 MILLION EQUIVALENT)

TO THE

GOVERNMENT OF NEPAL

FOR A

FINANCIAL SECTOR TECHNICAL ASSISTANCE PROJECT

August 14, 2012

Finance and Private Sector Development South Asia

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective September 30, 2009)

Currency Unit = Nepalese Rupees (NPR) 1.00 = US$0.0129

US$1.00 = Rupee 77.19

FISCAL YEAR July 15 – July 14

ABBREVIATIONS AND ACRONYMS

ADB Asian Development Bank BFIA Banking and Financial Institutions Act BOD Banking Operations Department CAS Country Assistance Strategy CIAA Commission for the Investigation of the Abuse of Authority CICL Credit Information Center Limited DCA Development Credit Agreement DFID UK’s Department for International Development DPC Development Policy Credit DRT Debt Recovery Tribunal FMS Financial Management Specialist FSRP Financial Sector Restructuring Project FSSS Financial Sector Strategy Statement FSTAP Financial Sector Technical Assistance Project GON Government of Nepal ICR Implementation Completion and Results Report IDA International Development Association IDF Institutional Development Fund IFC International Finance Corporation IMF International Monetary Fund IRR Internal Rate of Return ISR Implementation Status and Results Report MOF Ministry of Finance MTR Mid Term Review NBL Nepal Bank Limited NPC National Planning Commission NPL Non Performing Loans NPV Net Present Value NRB Nepal Rastra Bank PAD Project Appraisal Document PCD Project Closing Date PDO Project Development Objective PPF Project Preparation Facility PRO Public Relations Officer PRSC Poverty Reduction Support Credit RBB Rastriya Banijya Bank SLR Statutory Liquidity Requirement

STR Secured Transaction Registry TA Technical Assistance VRS Voluntary Retirement Scheme

Vice President: Isabel M. Guerrero

Country Director: Ellen A. Goldstein

Sector Manager: Ivan Rossignol

Project Team Leader: Sabin Raj Shrestha

ICR Team Leader: Ann Christine Rennie

ICR Primary Author: Kiran Afzal

NEPAL Financial Sector Technical Assistance Project

CONTENTS

Data Sheet A. Basic Information B. Key Dates C. Ratings Summary D. Sector and Theme Codes E. Bank Staff F. Results Framework Analysis G. Ratings of Program Performance in ISRs H. Restructuring

1. Project Context, Development Objectives and Design ............................................... 1 2. Key Factors Affecting Implementation and Outcomes ............................................ 10 3. Assessment of Outcomes .......................................................................................... 15 4. Assessment of Risk to Development Outcome ......................................................... 20 5. Assessment of Bank and Borrower Performance ..................................................... 20 6. Lessons Learned ....................................................................................................... 23 7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners .......... 24 Annex 1. Project Costs and Financing .......................................................................... 26 Annex 2. Outputs by Component……………………………………………………..31 Annex 3. Economic and Financial Analysis ................................................................. 28 Annex 4. Bank Lending and Implementation Support/Supervision Processes ............ 29 Annex 5. Beneficiary Survey Results ........................................................................... 30 Annex 6. Stakeholder Workshop Report and Results .................................................. 31 Annex 7. Summary of Borrower's ICR and/or Comments on Draft ICR ..................... 32 Annex 8. Comments of Cofinanciers – DFID .............................................................. 41 Annex 9. List of Supporting Documents ...................................................................... 43

MAP…………………………………………………………………………………..44

i

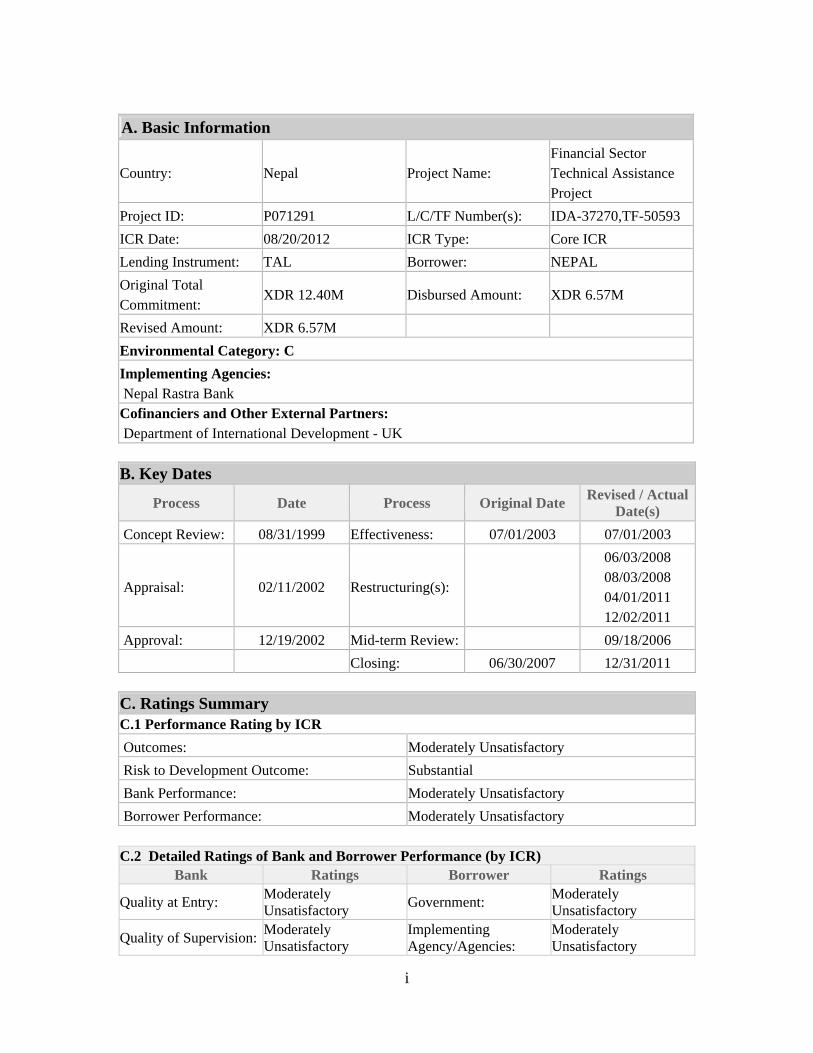

A. Basic Information

Country: Nepal Project Name: Financial Sector Technical Assistance Project

Project ID: P071291 L/C/TF Number(s): IDA-37270,TF-50593

ICR Date: 08/20/2012 ICR Type: Core ICR

Lending Instrument: TAL Borrower: NEPAL

Original Total Commitment:

XDR 12.40M Disbursed Amount: XDR 6.57M

Revised Amount: XDR 6.57M

Environmental Category: C

Implementing Agencies: Nepal Rastra Bank Cofinanciers and Other External Partners: Department of International Development - UK B. Key Dates

Process Date Process Original Date Revised / Actual

Date(s)

Concept Review: 08/31/1999 Effectiveness: 07/01/2003 07/01/2003

Appraisal: 02/11/2002 Restructuring(s):

06/03/2008 08/03/2008 04/01/2011 12/02/2011

Approval: 12/19/2002 Mid-term Review: 09/18/2006

Closing: 06/30/2007 12/31/2011 C. Ratings Summary C.1 Performance Rating by ICR

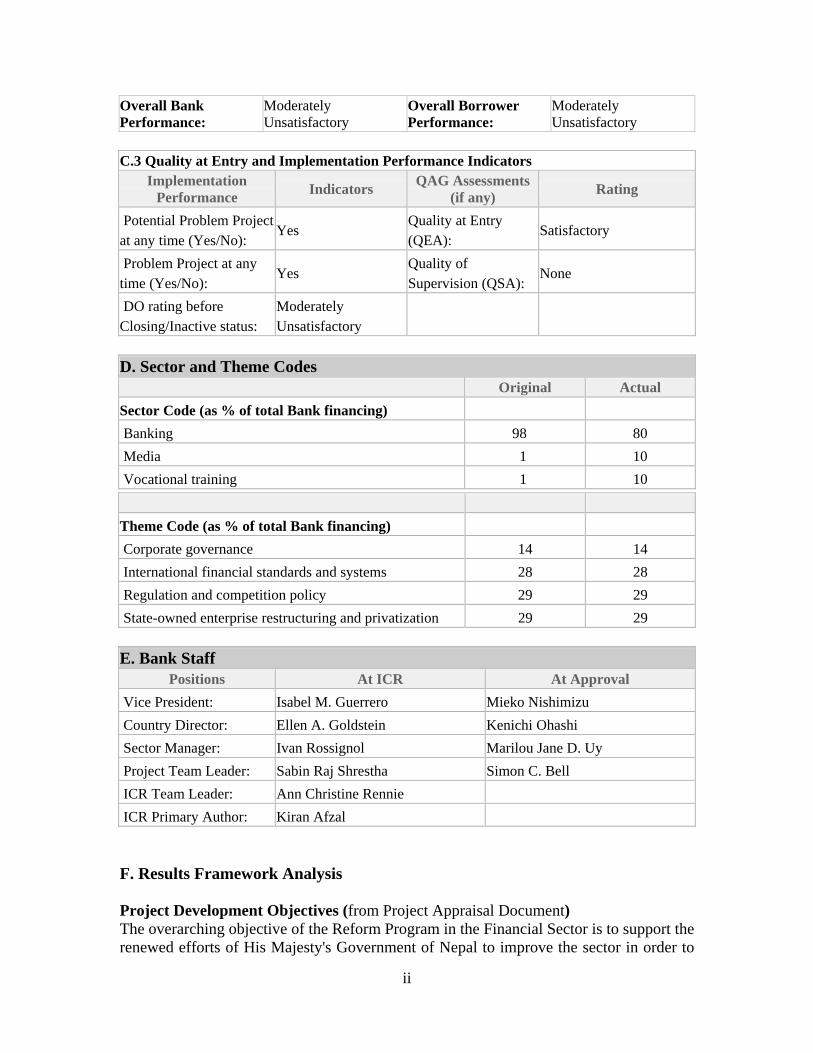

Outcomes: Moderately Unsatisfactory

Risk to Development Outcome: Substantial

Bank Performance: Moderately Unsatisfactory

Borrower Performance: Moderately Unsatisfactory

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR) Bank Ratings Borrower Ratings

Quality at Entry: Moderately Unsatisfactory

Government: Moderately Unsatisfactory

Quality of Supervision: Moderately Unsatisfactory

Implementing Agency/Agencies:

Moderately Unsatisfactory

ii

Overall Bank Performance:

Moderately Unsatisfactory

Overall Borrower Performance:

Moderately Unsatisfactory

C.3 Quality at Entry and Implementation Performance Indicators

Implementation Performance

Indicators QAG Assessments

(if any) Rating

Potential Problem Project at any time (Yes/No):

Yes Quality at Entry (QEA):

Satisfactory

Problem Project at any time (Yes/No):

Yes Quality of Supervision (QSA):

None

DO rating before Closing/Inactive status:

Moderately Unsatisfactory

D. Sector and Theme Codes

Original Actual

Sector Code (as % of total Bank financing)

Banking 98 80

Media 1 10

Vocational training 1 10

Theme Code (as % of total Bank financing)

Corporate governance 14 14

International financial standards and systems 28 28

Regulation and competition policy 29 29

State-owned enterprise restructuring and privatization 29 29 E. Bank Staff

Positions At ICR At Approval

Vice President: Isabel M. Guerrero Mieko Nishimizu

Country Director: Ellen A. Goldstein Kenichi Ohashi

Sector Manager: Ivan Rossignol Marilou Jane D. Uy

Project Team Leader: Sabin Raj Shrestha Simon C. Bell

ICR Team Leader: Ann Christine Rennie

ICR Primary Author: Kiran Afzal F. Results Framework Analysis

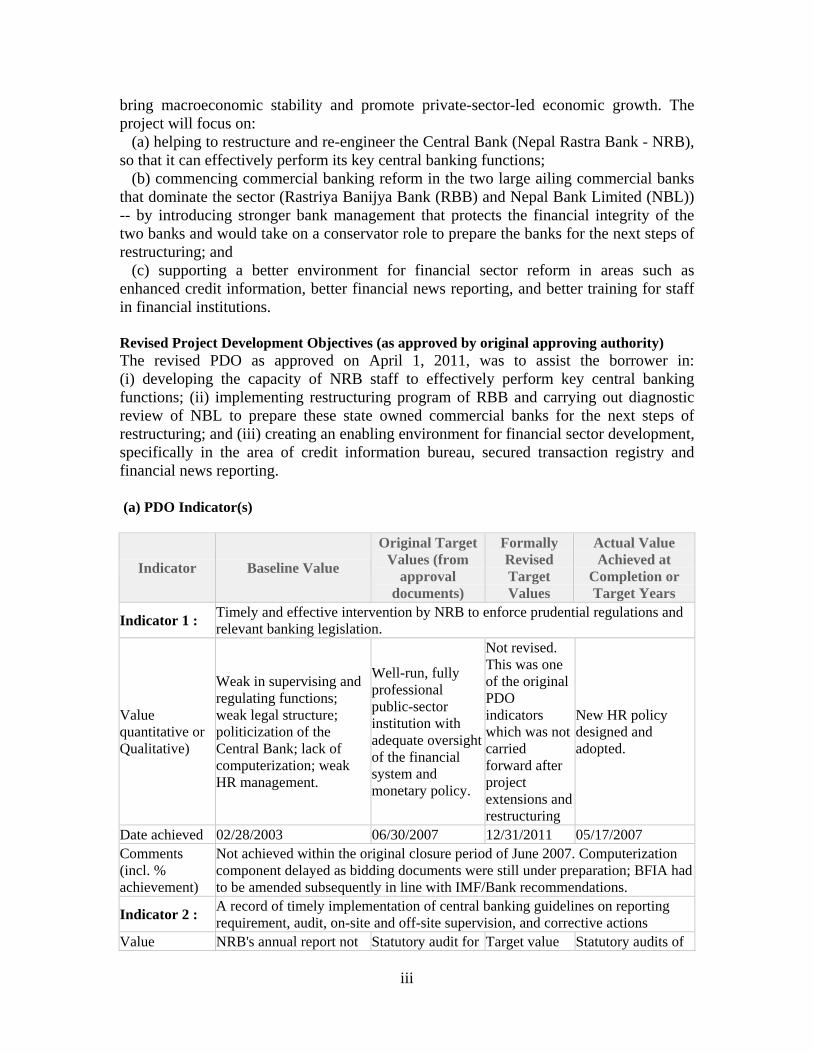

Project Development Objectives (from Project Appraisal Document) The overarching objective of the Reform Program in the Financial Sector is to support the renewed efforts of His Majesty's Government of Nepal to improve the sector in order to

iii

bring macroeconomic stability and promote private-sector-led economic growth. The project will focus on: (a) helping to restructure and re-engineer the Central Bank (Nepal Rastra Bank - NRB), so that it can effectively perform its key central banking functions; (b) commencing commercial banking reform in the two large ailing commercial banks that dominate the sector (Rastriya Banijya Bank (RBB) and Nepal Bank Limited (NBL)) -- by introducing stronger bank management that protects the financial integrity of the two banks and would take on a conservator role to prepare the banks for the next steps of restructuring; and (c) supporting a better environment for financial sector reform in areas such as enhanced credit information, better financial news reporting, and better training for staff in financial institutions. Revised Project Development Objectives (as approved by original approving authority) The revised PDO as approved on April 1, 2011, was to assist the borrower in: (i) developing the capacity of NRB staff to effectively perform key central banking functions; (ii) implementing restructuring program of RBB and carrying out diagnostic review of NBL to prepare these state owned commercial banks for the next steps of restructuring; and (iii) creating an enabling environment for financial sector development, specifically in the area of credit information bureau, secured transaction registry and financial news reporting. (a) PDO Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1 : Timely and effective intervention by NRB to enforce prudential regulations and relevant banking legislation.

Value quantitative or Qualitative)

Weak in supervising and regulating functions; weak legal structure; politicization of the Central Bank; lack of computerization; weak HR management.

Well-run, fully professional public-sector institution with adequate oversight of the financial system and monetary policy.

Not revised. This was one of the original PDO indicators which was not carried forward after project extensions and restructuring

New HR policy designed and adopted.

Date achieved 02/28/2003 06/30/2007 12/31/2011 05/17/2007 Comments (incl. % achievement)

Not achieved within the original closure period of June 2007. Computerization component delayed as bidding documents were still under preparation; BFIA had to be amended subsequently in line with IMF/Bank recommendations.

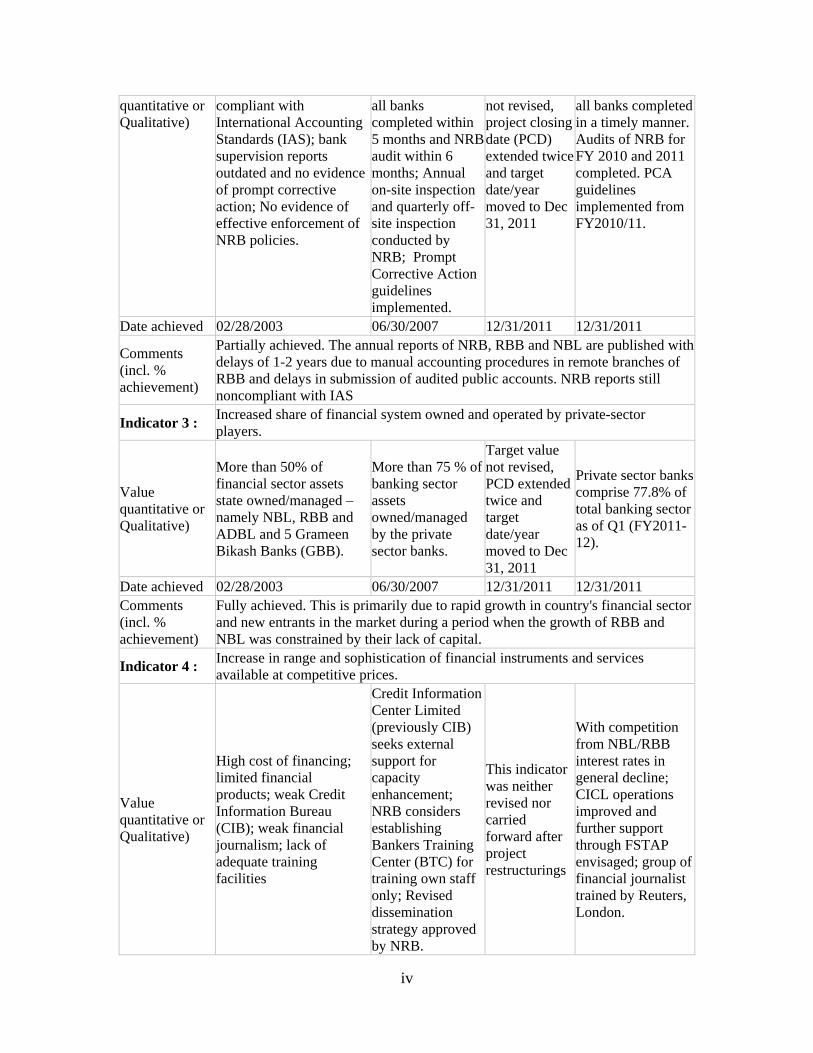

Indicator 2 : A record of timely implementation of central banking guidelines on reporting requirement, audit, on-site and off-site supervision, and corrective actions

Value NRB's annual report not Statutory audit for Target value Statutory audits of

iv

quantitative or Qualitative)

compliant with International Accounting Standards (IAS); bank supervision reports outdated and no evidence of prompt corrective action; No evidence of effective enforcement of NRB policies.

all banks completed within 5 months and NRB audit within 6 months; Annual on-site inspection and quarterly off-site inspection conducted by NRB; Prompt Corrective Action guidelines implemented.

not revised, project closing date (PCD) extended twice and target date/year moved to Dec 31, 2011

all banks completed in a timely manner. Audits of NRB for FY 2010 and 2011 completed. PCA guidelines implemented from FY2010/11.

Date achieved 02/28/2003 06/30/2007 12/31/2011 12/31/2011

Comments (incl. % achievement)

Partially achieved. The annual reports of NRB, RBB and NBL are published with delays of 1-2 years due to manual accounting procedures in remote branches of RBB and delays in submission of audited public accounts. NRB reports still noncompliant with IAS

Indicator 3 : Increased share of financial system owned and operated by private-sector players.

Value quantitative or Qualitative)

More than 50% of financial sector assets state owned/managed – namely NBL, RBB and ADBL and 5 Grameen Bikash Banks (GBB).

More than 75 % of banking sector assets owned/managed by the private sector banks.

Target value not revised, PCD extended twice and target date/year moved to Dec 31, 2011

Private sector banks comprise 77.8% of total banking sector as of Q1 (FY2011-12).

Date achieved 02/28/2003 06/30/2007 12/31/2011 12/31/2011 Comments (incl. % achievement)

Fully achieved. This is primarily due to rapid growth in country's financial sector and new entrants in the market during a period when the growth of RBB and NBL was constrained by their lack of capital.

Indicator 4 : Increase in range and sophistication of financial instruments and services available at competitive prices.

Value quantitative or Qualitative)

High cost of financing; limited financial products; weak Credit Information Bureau (CIB); weak financial journalism; lack of adequate training facilities

Credit Information Center Limited (previously CIB) seeks external support for capacity enhancement; NRB considers establishing Bankers Training Center (BTC) for training own staff only; Revised dissemination strategy approved by NRB.

This indicator was neither revised nor carried forward after project restructurings

With competition from NBL/RBB interest rates in general decline; CICL operations improved and further support through FSTAP envisaged; group of financial journalist trained by Reuters, London.

v

Date achieved 02/28/2003 06/30/2007 12/31/2011 05/17/2007

Comments (incl. % achievement)

Partially Achieved. CICL was strengthened, but that cannot be attributed directly to FSTAP. CICL sought support from Asian Development Bank (ADB) for expansion of its activities and for automation. BTC functional, financial journalists trained abroad.

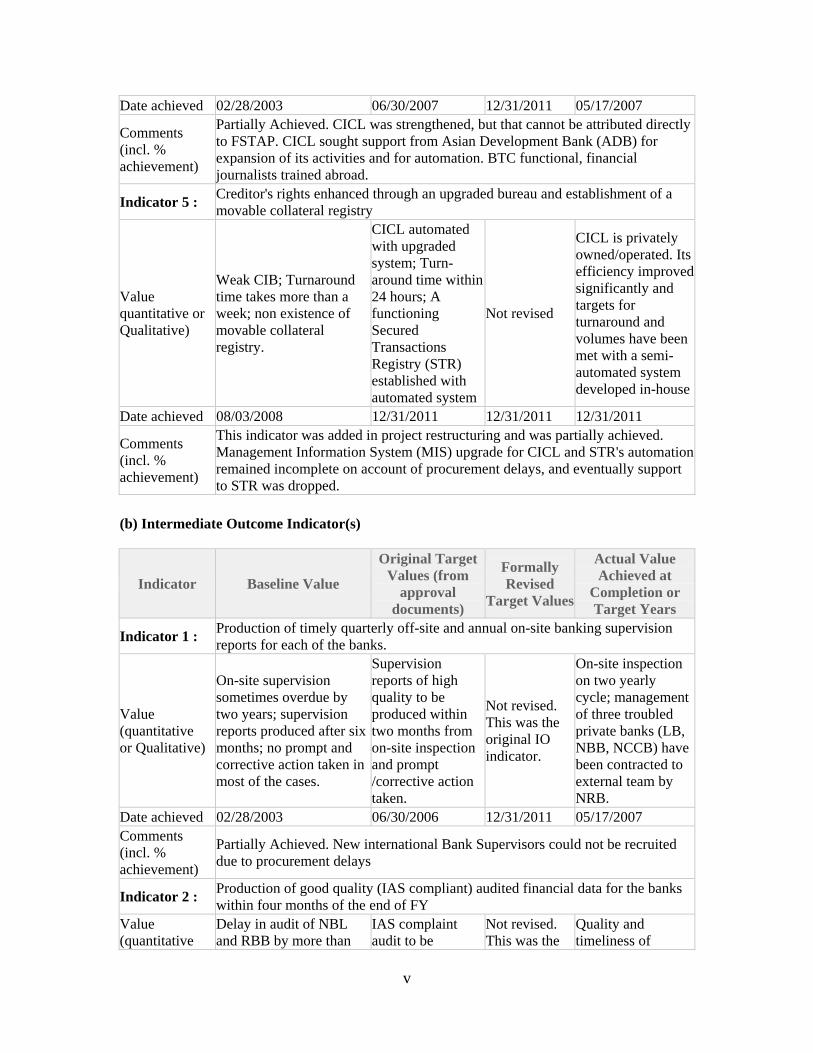

Indicator 5 : Creditor's rights enhanced through an upgraded bureau and establishment of a movable collateral registry

Value quantitative or Qualitative)

Weak CIB; Turnaround time takes more than a week; non existence of movable collateral registry.

CICL automated with upgraded system; Turn-around time within 24 hours; A functioning Secured Transactions Registry (STR) established with automated system

Not revised

CICL is privately owned/operated. Its efficiency improved significantly and targets for turnaround and volumes have been met with a semi-automated system developed in-house

Date achieved 08/03/2008 12/31/2011 12/31/2011 12/31/2011

Comments (incl. % achievement)

This indicator was added in project restructuring and was partially achieved. Management Information System (MIS) upgrade for CICL and STR's automation remained incomplete on account of procurement delays, and eventually support to STR was dropped.

(b) Intermediate Outcome Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised

Target Values

Actual Value Achieved at

Completion or Target Years

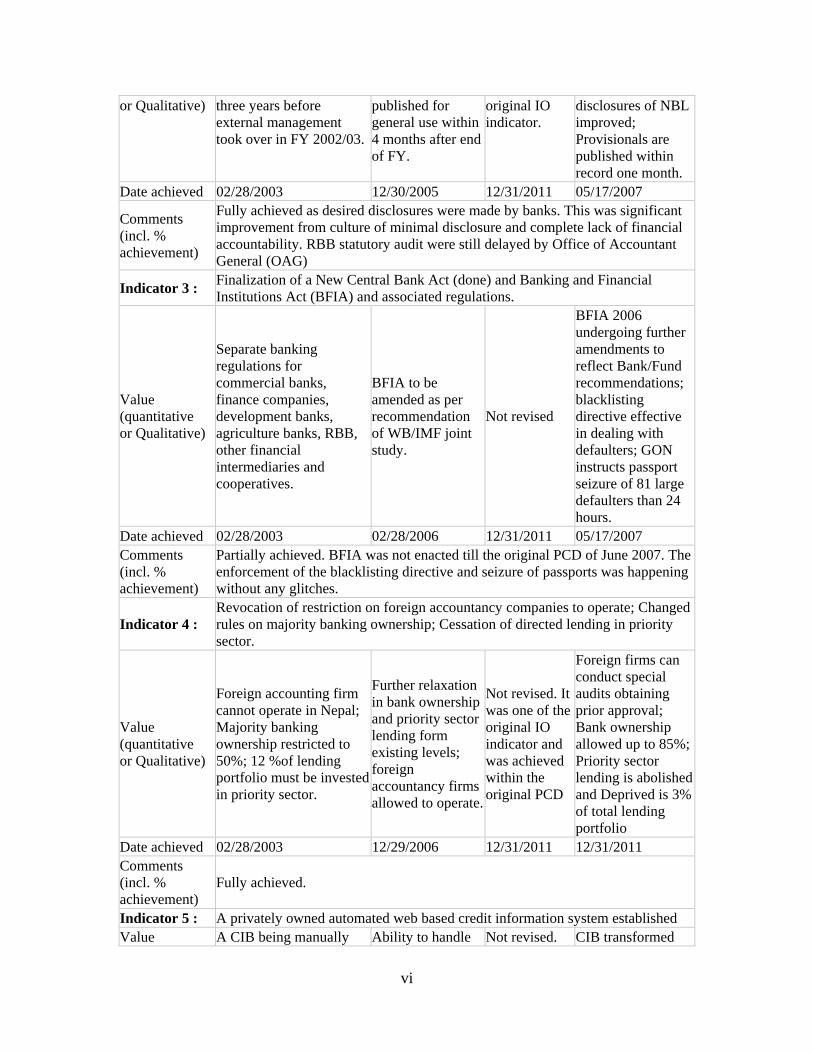

Indicator 1 : Production of timely quarterly off-site and annual on-site banking supervision reports for each of the banks.

Value (quantitative or Qualitative)

On-site supervision sometimes overdue by two years; supervision reports produced after six months; no prompt and corrective action taken in most of the cases.

Supervision reports of high quality to be produced within two months from on-site inspection and prompt /corrective action taken.

Not revised. This was the original IO indicator.

On-site inspection on two yearly cycle; management of three troubled private banks (LB, NBB, NCCB) have been contracted to external team by NRB.

Date achieved 02/28/2003 06/30/2006 12/31/2011 05/17/2007 Comments (incl. % achievement)

Partially Achieved. New international Bank Supervisors could not be recruited due to procurement delays

Indicator 2 : Production of good quality (IAS compliant) audited financial data for the banks within four months of the end of FY

Value (quantitative

Delay in audit of NBL and RBB by more than

IAS complaint audit to be

Not revised. This was the

Quality and timeliness of

vi

or Qualitative) three years before external management took over in FY 2002/03.

published for general use within 4 months after end of FY.

original IO indicator.

disclosures of NBL improved; Provisionals are published within record one month.

Date achieved 02/28/2003 12/30/2005 12/31/2011 05/17/2007

Comments (incl. % achievement)

Fully achieved as desired disclosures were made by banks. This was significant improvement from culture of minimal disclosure and complete lack of financial accountability. RBB statutory audit were still delayed by Office of Accountant General (OAG)

Indicator 3 : Finalization of a New Central Bank Act (done) and Banking and Financial Institutions Act (BFIA) and associated regulations.

Value (quantitative or Qualitative)

Separate banking regulations for commercial banks, finance companies, development banks, agriculture banks, RBB, other financial intermediaries and cooperatives.

BFIA to be amended as per recommendation of WB/IMF joint study.

Not revised

BFIA 2006 undergoing further amendments to reflect Bank/Fund recommendations; blacklisting directive effective in dealing with defaulters; GON instructs passport seizure of 81 large defaulters than 24 hours.

Date achieved 02/28/2003 02/28/2006 12/31/2011 05/17/2007 Comments (incl. % achievement)

Partially achieved. BFIA was not enacted till the original PCD of June 2007. The enforcement of the blacklisting directive and seizure of passports was happening without any glitches.

Indicator 4 : Revocation of restriction on foreign accountancy companies to operate; Changed rules on majority banking ownership; Cessation of directed lending in priority sector.

Value (quantitative or Qualitative)

Foreign accounting firm cannot operate in Nepal; Majority banking ownership restricted to 50%; 12 %of lending portfolio must be invested in priority sector.

Further relaxation in bank ownership and priority sector lending form existing levels; foreign accountancy firms allowed to operate.

Not revised. It was one of the original IO indicator and was achieved within the original PCD

Foreign firms can conduct special audits obtaining prior approval; Bank ownership allowed up to 85%; Priority sector lending is abolished and Deprived is 3% of total lending portfolio

Date achieved 02/28/2003 12/29/2006 12/31/2011 12/31/2011 Comments (incl. % achievement)

Fully achieved.

Indicator 5 : A privately owned automated web based credit information system established Value A CIB being manually Ability to handle Not revised. CIB transformed

vii

(quantitative or Qualitative)

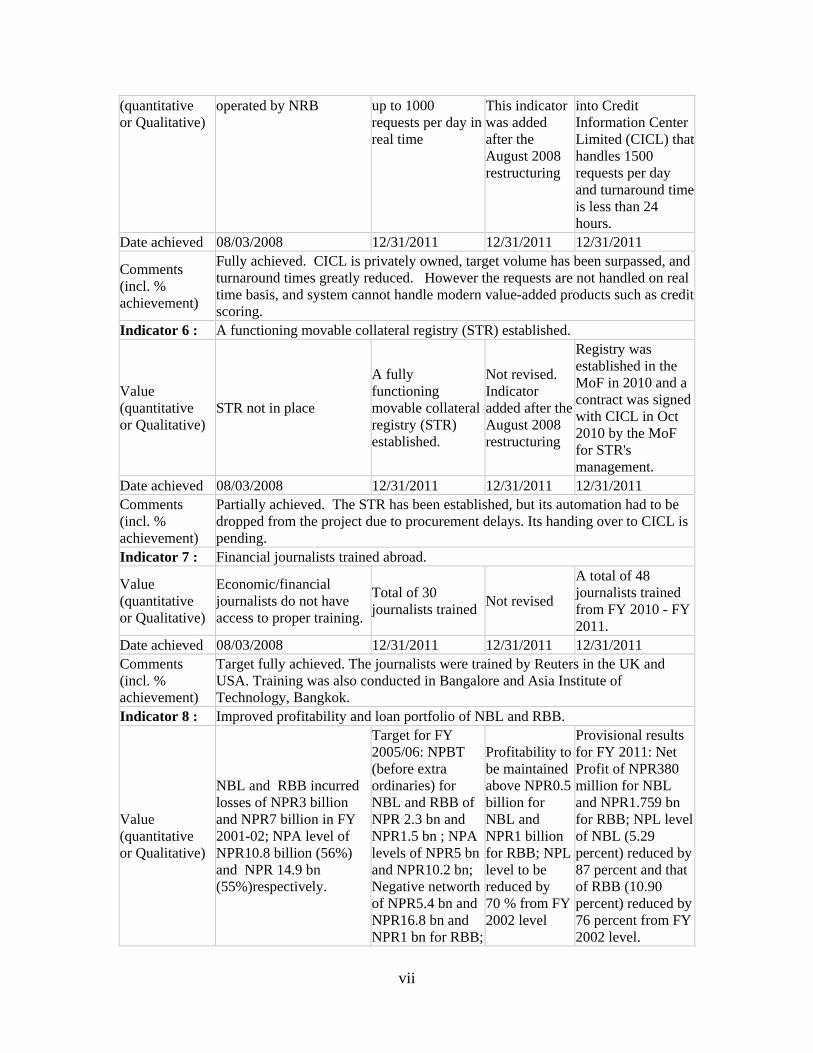

operated by NRB up to 1000 requests per day in real time

This indicator was added after the August 2008 restructuring

into Credit Information Center Limited (CICL) that handles 1500 requests per day and turnaround time is less than 24 hours.

Date achieved 08/03/2008 12/31/2011 12/31/2011 12/31/2011

Comments (incl. % achievement)

Fully achieved. CICL is privately owned, target volume has been surpassed, and turnaround times greatly reduced. However the requests are not handled on real time basis, and system cannot handle modern value-added products such as credit scoring.

Indicator 6 : A functioning movable collateral registry (STR) established.

Value (quantitative or Qualitative)

STR not in place

A fully functioning movable collateral registry (STR) established.

Not revised. Indicator added after the August 2008 restructuring

Registry was established in the MoF in 2010 and a contract was signed with CICL in Oct 2010 by the MoF for STR's management.

Date achieved 08/03/2008 12/31/2011 12/31/2011 12/31/2011 Comments (incl. % achievement)

Partially achieved. The STR has been established, but its automation had to be dropped from the project due to procurement delays. Its handing over to CICL is pending.

Indicator 7 : Financial journalists trained abroad.

Value (quantitative or Qualitative)

Economic/financial journalists do not have access to proper training.

Total of 30 journalists trained

Not revised

A total of 48 journalists trained from FY 2010 - FY 2011.

Date achieved 08/03/2008 12/31/2011 12/31/2011 12/31/2011 Comments (incl. % achievement)

Target fully achieved. The journalists were trained by Reuters in the UK and USA. Training was also conducted in Bangalore and Asia Institute of Technology, Bangkok.

Indicator 8 : Improved profitability and loan portfolio of NBL and RBB.

Value (quantitative or Qualitative)

NBL and RBB incurred losses of NPR3 billion and NPR7 billion in FY 2001-02; NPA level of NPR10.8 billion (56%) and NPR 14.9 bn (55%)respectively.

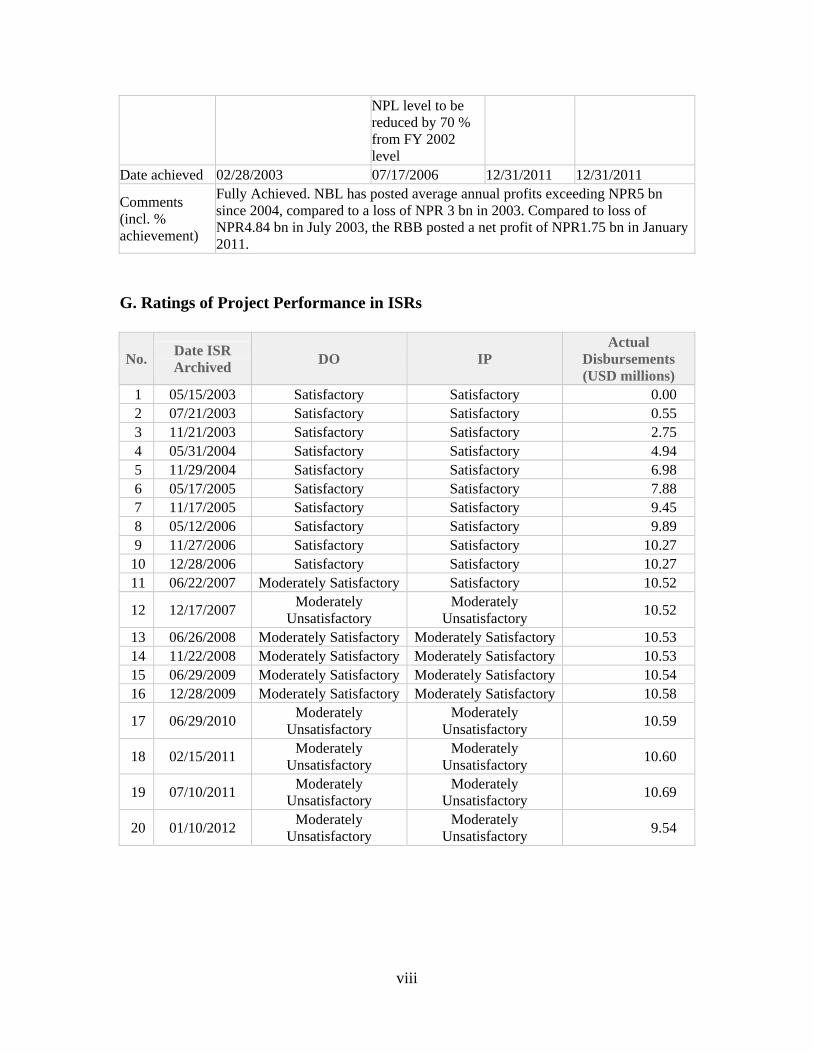

Target for FY 2005/06: NPBT (before extra ordinaries) for NBL and RBB of NPR 2.3 bn and NPR1.5 bn ; NPA levels of NPR5 bn and NPR10.2 bn; Negative networth of NPR5.4 bn and NPR16.8 bn and NPR1 bn for RBB;

Profitability to be maintained above NPR0.5 billion for NBL and NPR1 billion for RBB; NPL level to be reduced by 70 % from FY 2002 level

Provisional results for FY 2011: Net Profit of NPR380 million for NBL and NPR1.759 bn for RBB; NPL level of NBL (5.29 percent) reduced by 87 percent and that of RBB (10.90 percent) reduced by 76 percent from FY 2002 level.

viii

NPL level to be reduced by 70 % from FY 2002 level

Date achieved 02/28/2003 07/17/2006 12/31/2011 12/31/2011

Comments (incl. % achievement)

Fully Achieved. NBL has posted average annual profits exceeding NPR5 bn since 2004, compared to a loss of NPR 3 bn in 2003. Compared to loss of NPR4.84 bn in July 2003, the RBB posted a net profit of NPR1.75 bn in January 2011.

G. Ratings of Project Performance in ISRs

No. Date ISR Archived

DO IP Actual

Disbursements (USD millions)

1 05/15/2003 Satisfactory Satisfactory 0.00 2 07/21/2003 Satisfactory Satisfactory 0.55 3 11/21/2003 Satisfactory Satisfactory 2.75 4 05/31/2004 Satisfactory Satisfactory 4.94 5 11/29/2004 Satisfactory Satisfactory 6.98 6 05/17/2005 Satisfactory Satisfactory 7.88 7 11/17/2005 Satisfactory Satisfactory 9.45 8 05/12/2006 Satisfactory Satisfactory 9.89 9 11/27/2006 Satisfactory Satisfactory 10.27

10 12/28/2006 Satisfactory Satisfactory 10.27 11 06/22/2007 Moderately Satisfactory Satisfactory 10.52

12 12/17/2007 Moderately

Unsatisfactory Moderately

Unsatisfactory 10.52

13 06/26/2008 Moderately Satisfactory Moderately Satisfactory 10.53 14 11/22/2008 Moderately Satisfactory Moderately Satisfactory 10.53 15 06/29/2009 Moderately Satisfactory Moderately Satisfactory 10.54 16 12/28/2009 Moderately Satisfactory Moderately Satisfactory 10.58

17 06/29/2010 Moderately

Unsatisfactory Moderately

Unsatisfactory 10.59

18 02/15/2011 Moderately

Unsatisfactory Moderately

Unsatisfactory 10.60

19 07/10/2011 Moderately

Unsatisfactory Moderately

Unsatisfactory 10.69

20 01/10/2012 Moderately

Unsatisfactory Moderately

Unsatisfactory 9.54

ix

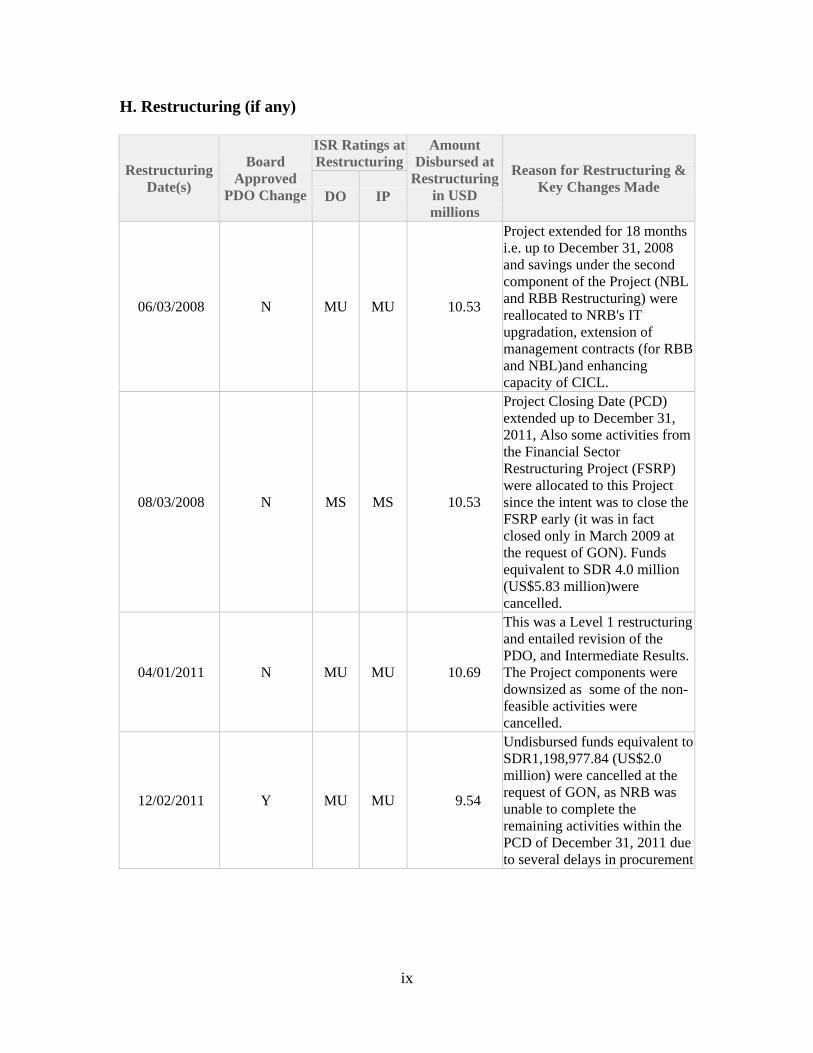

H. Restructuring (if any)

Restructuring Date(s)

Board Approved

PDO Change

ISR Ratings at Restructuring

Amount Disbursed at

Restructuring in USD millions

Reason for Restructuring & Key Changes Made

DO IP

06/03/2008 N MU MU 10.53

Project extended for 18 months i.e. up to December 31, 2008 and savings under the second component of the Project (NBL and RBB Restructuring) were reallocated to NRB's IT upgradation, extension of management contracts (for RBB and NBL)and enhancing capacity of CICL.

08/03/2008 N MS MS 10.53

Project Closing Date (PCD) extended up to December 31, 2011, Also some activities from the Financial Sector Restructuring Project (FSRP) were allocated to this Project since the intent was to close the FSRP early (it was in fact closed only in March 2009 at the request of GON). Funds equivalent to SDR 4.0 million (US$5.83 million)were cancelled.

04/01/2011 N MU MU 10.69

This was a Level 1 restructuring and entailed revision of the PDO, and Intermediate Results. The Project components were downsized as some of the non-feasible activities were cancelled.

12/02/2011 Y MU MU 9.54

Undisbursed funds equivalent to SDR1,198,977.84 (US$2.0 million) were cancelled at the request of GON, as NRB was unable to complete the remaining activities within the PCD of December 31, 2011 due to several delays in procurement

x

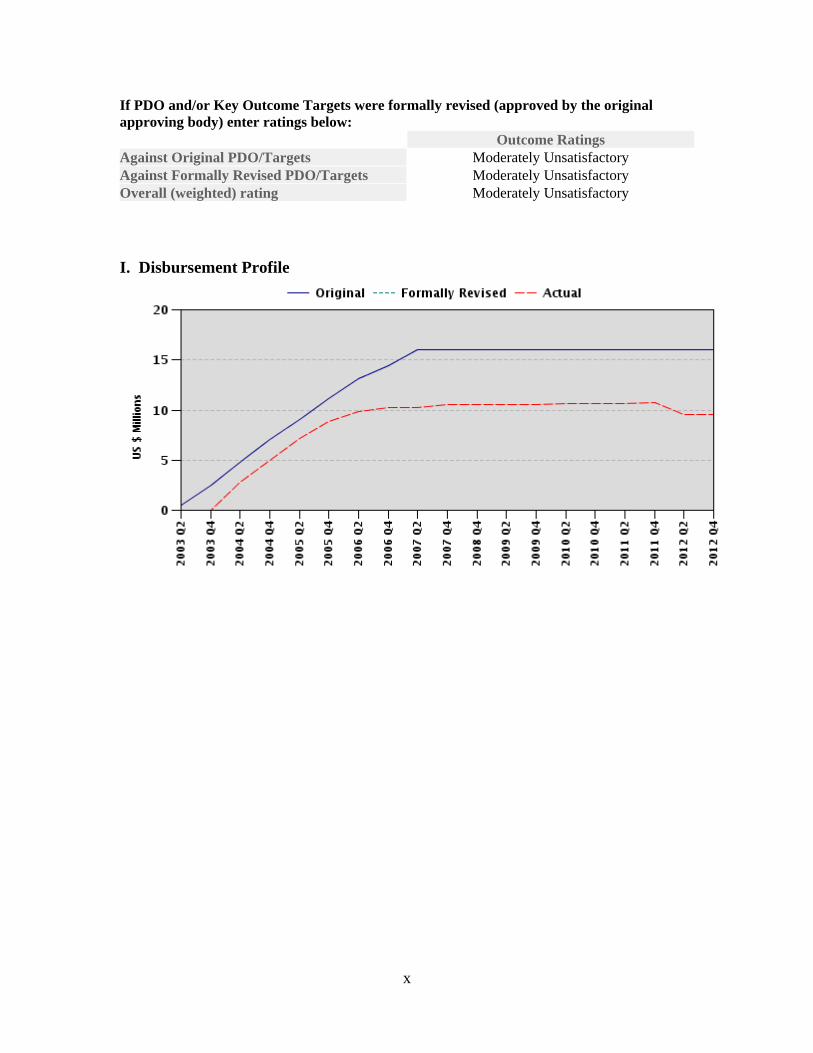

If PDO and/or Key Outcome Targets were formally revised (approved by the original approving body) enter ratings below: Outcome Ratings Against Original PDO/Targets Moderately Unsatisfactory Against Formally Revised PDO/Targets Moderately Unsatisfactory Overall (weighted) rating Moderately Unsatisfactory

I. Disbursement Profile

1

1. Project Context, Development Objectives and Design

1.1 Context at Appraisal Country and Sector Background 1.1.1 When the Financial Sector Technical Assistance Project (FSTAP) was being designed, Nepal had a population of 24 million, and, with a Gross Domestic Product (GDP) per capita of US$220, it was one of the poorest countries in the world. The transition to multi-party democracy, which began in 1991, had resulted in a high degree of political instability, with numerous changes in government between 1991 and 2001. Its social indicators also deteriorated during the decade long conflict in the country, which came to an end in 2006. 1.1.2 Until the mid-1980’s, all financial sector activity was dominated by two state-owned commercial banks; Rastriya Banijya Bank (RBB) and Nepal Bank Limited (NBL). Following financial sector liberalization in the 1980s, the sector became more diversified, and by 2002, it had grown to include five commercial banks, eight development banks, five regional rural development banks, one postal savings bank, forty eight finance companies, thirty non-government microfinance institutions, and thirty-five non-government cooperative societies involved in limited banking activities. In the absence of a strong regulatory framework and sound technical capacities of the regulators, this diversity proved problematic. By 2002, the financial sector was grappling with serious governance issues, rising non-performing loans (NPLs), political interference in banking activities, and weak institutional management. The overall legal and regulatory framework for the sector was outdated, and had serious shortcomings in the areas of collateral, credit activity and bankruptcy laws. These factors were contributing to a build-up of systemic risks and potential fiscal costs that called for immediate redressal measures. 1.1.3 The two largest state owned commercial banks, RBB and NBL accounted for 50 percent of banking sector assets and were in a precarious financial position. The RBB, which represented 27 percent of commercial banking sector assets, had 71 percent NPLs. Both banks were characterized by overstaffing, strong and politicized staff unions, poor financial information systems, and a tradition of non-repayment of loans. A KPMG/Barents report completed in 2000 estimated the cumulative losses in these two institutions were between US$368 million and US$426 million. This was equivalent to approximately 8 percent of Nepal’s GDP and 40-46 percent of the country’s budget. The magnitude of these losses clearly demanded the attention of the Government of Nepal (GON). 1.1.4 The KPMG/Barents report recommended a number of steps to reform the financial sector, which included a clear statement of GON’s commitment to financial reforms, bringing in qualified management teams to run the two large state-owned banks,

2

and ultimately recapitalizing and privatizing RBB and NBL after turning them into saleable entities. 1.1.5 In response to the prevailing distress in the banking sector, GON embarked on institutional reforms and released a Financial Sector Strategy Statement (FSSS) in 2000. FSSS made a case for a strengthened financial sector supervisory and regulatory regime to ensure financial discipline, improved legislation, and strong corporate governance. It envisioned a modern Nepal Rastra Bank (NRB) and advocated for a new NRB Act that could provide sufficient autonomy in NRB’s conduct of monetary policy, banking system regulation and supervision, and the licensing of banks and non banking financial institutions. It also aimed at restructuring NRB and RBB, and ultimately recapitalizing them and diluting GON’s ownership in the banks. 1.1.6 Until January, 2002, when the new NRB Act 2002 was passed into law, the Central Bank fell under the direct authority of the Ministry of Finance (MoF). This lack of autonomy hindered NRB’s ability to properly regulate and supervise the state-dominated banking system. In addition, NRB had been only partially successful in developing its core central banking functions, and required a complete re-engineering. The areas that required strengthening included human resource management, banking supervision and regulation, accounting and auditing, research and monetary policy analysis, information technology and internal audit. Rationale for Bank Assistance 1.1.7 FSSS and the measures adopted by GON sent a clear message to stakeholders that GON would support financial sector reforms going forward. GON approached the Bank, International Monetary Fund (IMF), and the UK’s Department for International Development (DFID), seeking financial and technical assistance (TA) for implementing its reform agenda. 1.1.8 The Bank completed an assessment of Nepal’s financial sector in 2002, which made a strong case for providing support to the sector to stem the mounting losses of the public sector banks, to strengthen the Central Bank and its supervisory function, and to strengthen the legal and regulatory framework of the financial system. Its findings endorsed the need for a financial sector TA operation to support GON’s reforms. These findings, coupled with the GON’s commitment to financial sector reforms (outlined in the 2000 FSSS and demonstrated by GON’s initial reform measures), provided the rationale for Bank assistance to the sector. 1.1.9 At the same time, the Bank recognized the risks inherent in the proposed financial sector reform program, given political uncertainty and limited implementation capacity. A history of weak coalitions and frequent changes in government increased the risk of policy reversals that could jeopardize project outcomes. As a result, a decision was made to undertake support for the reform program in three phases. FSTAP was conceived under Phase I. This TA was to focus on the re-engineering of NRB; restructuring of RBB and NBL; and improving the enabling environment for financial sector development.

3

The projects under Phase II and III were to complement the activities under the FSTAP, with the objective of recapitalizing and privatizing NBL and RBB. 1.1.10 FSTAP was in line with the Bank’s 1998 Nepal Country Assistance Strategy (CAS) that emphasized structural reforms in four key areas; (i) restructuring/privatization of RBB and NBL; (ii) the development of NRB’s regulatory and supervisory capacity; (iii) development of a uniform legal framework for Nepal’s financial system; and (iv) establishment of additional private financial institutions supported by the International Finance Corporation (IFC). 1.1.11 Poverty Reduction Support Credit (PRSC) – 2003: Soon after the effectiveness of the FSTAP, a US$70 million PRSC was approved by the Bank. The prior actions for the financial sector under PRSC, which mirrored the objectives of FSTAP, were as follows: (i) Dissolve boards of RBB and NBL, introduce new professional management teams

at RBB and NBL – (PRSC I prior action) (ii) Implement scheme to rationalize excess staff at NRB, NBL and RBB – (PRSC II

Indicative action expected by September 2004). The first prior action was implemented when GON appointed the management team at NBL and a Chief Executive Officer (CEO) at RBB in 2002. The second action was supported through FSTAP and the Phase II Reform Project, the Financial Sector Restructuring Project (FSRP)1 which became effective in 2004. Co-financing Arrangements with DFID and GON 1.1.12 DFID also endorsed GON’s financial sector reform agenda and agreed to provide financial and technical support to FSTAP. It committed a US$10 million grant to supplement the International Development Association (IDA) credit. A Memorandum of Understanding (MoU) was signed in 2003 between the Bank and DFID, and it was decided that the funds would be disbursed in the proportion of 62 percent IDA and 38 percent DFID 2 . The grant was to be administered according to IDA’s financial management (FM), disbursement and procurement guidelines. GON was to contribute the balance of US$4.1 million to this project.

1 The US$7.0 million FSRP was the second operation under the Bank’s financial sector reform program for GON. The main objective of FSRP was to improve corporate governance by providing management support to NBL and RBB in order to move them into the private sector, and to sustain the banking reforms. The project also financed Voluntary Retirement Schemes (VRS) schemes at the two banks. The undisbursed funds equivalent to SDR13.7 million, under FSRP, were cancelled at the request of GON in two steps in May 2008 and March 2009, and the project closed on September 30, 2009.

2 This was subsequently changed. Subsequent governments expressed a reluctance to borrow for TA, and consequently much of the TA work was funded under the DFID grant.

4

1.2 Original Project Development Objectives (PDO) and Key Indicators 1.2.1 The overarching objective of FSTAP is to support efforts of GON to improve the sector in order to bring macroeconomic stability and to promote private sector led economic growth. Specifically, the project will focus on: (a) helping to restructure and re-engineer the Central Bank (NRB), so that it can effectively perform its key central banking functions; (b) commencing the restructuring of RBB and NBL by introducing stronger bank management that protects the financial integrity of the two banks and would take on a conservator role to prepare the banks for the next steps of restructuring; and (c) supporting a better environment for financial sector reform in areas such as credit information and secured transactions, better financial news reporting, and better training for staff in financial institutions. Key Indicators 1.2.3 The PDO level key indicators were: (i) timely and effective intervention by NRB to enforce prudential regulations and relevant banking legislation; (ii) a record of timely, effective, and independent implementation of central banking policies; (iii) increased share of financial system owned and operated by private sector players; and (iv) increase in the range and sophistication of financial instruments and services available at competitive prices. This ICR assesses the performance of the project against the original PDO and revised PDO and outcome indicators. All of these have been tabulated and evaluated in the Results Framework Analysis, Section F, of this ICR’s datasheet.

1.3 Revised PDO and Key Indicators, and reasons/justification 1.3.1 The PDO was revised in April 2011 as a result of a Level-1 restructuring that also included cancellation of funds equivalent to SDR615,000 (IDA) and GBP1.964 million (DFID Grant). The detailed background of this restructuring is given in section 1.7 of this document. 1.3.2 The revised PDO was to strengthen the financial sector, notably the NRB and the state controlled banks, and to create an enabling environment for financial sector development. The project was to assist GON in (i) developing the capacity of the NRB staff to effectively perform key central banking functions; (ii) implementing the planned restructuring program of RBB and carrying out a diagnostic review of NBL to prepare NBL and RBB for the next steps of their restructuring; and (iii) creating an enabling environment for financial sector development, specifically in the areas of the Credit Information Bureau (CIB), Secured Transactions Registry (STR) and financial news reporting. The intermediate results indicators were also revised accordingly.

5

1.4 Main Beneficiaries, 1.4.1 The main beneficiaries or the primary target group of this project were NRB, RBB and NBL. The actions implemented under the project were expected to foster a sound commercial banking system, with oversight provided by a modern, effective, and technically competent central bank. The FSTAP also aimed at creating a financially sound, prudent, and effectively regulated financial sector, that could contribute to macroeconomic stability and growth. This could not be achieved without strengthening the Central Bank and the country’s two largest banks, RBB and NBL. NRB: Although NRB had been able to develop some core central banking functions, it was handicapped by a lack of autonomy, an inadequate and outdated legal framework, and a large number of poorly trained and unproductive staff. NBL and RBB: Established in 1938, NBL is the oldest bank in Nepal. GON is the largest shareholder, with 41 percent ownership. The remaining shares are held 49 percent by private businessmen and 10 percent by the public3. RBB, established as a 100% government-owned bank in 1966, is Nepal’s largest commercial bank. At project inception, both banks were overstaffed, suffered serious shortfalls in governance, management and operations, and had negative net worth. 1.4.2 A key benefit of the project was to be the emergence of a more dynamic and competitive banking system that would support private-sector led growth for the benefit of Nepali enterprises and the general public.

1.5 Original Components 1.5.1 The three main components of FSTAP are tabulated below, along with the cost breakdown by financier: Table 2: Project Components and Cost by financier (US$ million) Component IDA DFID GON Total Re-engineering NRB 2.64 1.56 0.48 4.68Restructuring RBB and NBL 12.81 8.10 3.52 24.43Capacity building in the Financial Sector

0.55 0.34 0.10 0.99

Total 16.00 10.00 4.10 30.10 1.5.2 Component 1: Re-engineering NRB (US$4.68 million): The specific activities envisaged under this component included hiring of a Human Resource (HR) professional

3 GON had owned 51 percent of the NBL, but sold 10 percent to the public in 1998 through a listing on the stock exchange. At the time of listing, NBL had a negative net-worth of US$85-140 million which is in violation of the listing rules of the exchange. New management hired under FSTAP requested the de-listing of the NBL in 2003.

6

who would revise the HR policies, identifying staff for retrenchment, designing the VRS, and computerizing the HR function. Additionally, this component aimed at strengthening NRB’s supervisory capacities by training its staff and by hiring experienced bank supervisors to assist with the implementation of NRB’s plan for regulatory development. This component also envisaged improving the quality and efficiency of NRB’s Accounting and Auditing Department, strengthening the Research Department, and providing IT support. Some funding was also allocated to strengthening the Legal and Internal Audit Departments, and providing training to NRB staff involved in these functions. Finally, the FSTAP envisaged providing support to NRB to engage legal experts to review the legislative and regulatory framework, and finalize the Central Bank Act and the Banking and Financial Institution Act (BFIA). 1.5.3 Component 2: Restructuring RBB and NBL (US$24.43 million): The restructuring of these two institutions was to be accomplished under the supervision of professional management teams who were to take complete control of the day to day operations of these banks, immediately stabilize their financial and operational positions, and strengthen their accounting, Management Information System (MIS) and HR functions. The ultimate objective of these efforts was to stem the losses being incurred by these banks and prepare NBL and RBB for recapitalization and ultimately privatization or liquidation. 1.5.4 Component 3: Capacity Building in the Financial Sector (US$0.99 million): The activities under this component were to support reforms introduced through the first two components and improve the environment for financial intermediation. Specific activities included; (a) support for the Bankers’ Training Center; (b) strengthening the processes of the CIB; (c) developing the capacities of the financial journalists to improve the quality of reports on financial sector issues; and (d) financing the cost of the Coordination Support team (CST) while strengthening its project management capabilities. 1.5.5 Implementation Arrangements: GON agreed with the Bank that the financial sector program would be overseen by three Government bodies, namely the MoF, NRB and the National Planning Commission (NPC). For implementation of activities at the project level, a dedicated unit called CST was formed within the Banking Operations Department (BOD) of NRB. The CST was supported by a team comprising the Executive Director of BOD, a Financial Management Specialist (FMS), a Procurement Specialist and requisite ancillary staff. FSTAP funded the operating costs of CST on a declining cost basis over the period of project’s implementation. It was also agreed to centralize the procurement function within the CST and equip it with the desired resources to ensure an effective implementation of the project’s procurement plan.

1.6 Revised Components 1.6.1 At the request of GON in June 2008, the FSTAP was assigned certain additional activities that had not been implemented under the Phase II project, FSRP, prior to closure. As the PDOs of FSRP remained largely unachieved, it was decided to close that project in August 2008, ahead of its closing date of September 2009. Due to some

7

pending payments of already incurred expenditures under the project, the FSRP’s closing eventually occurred in September 2009. 1.6.2 The activities that were transferred to FSTAP included; (i) strengthening NRB’s supervision capacity by hiring a Supervision Expert with focus on risk based supervision; (ii) hiring of a Bank Restructuring Advisor for the end game resolution of NBL and RBB; (iii) strengthening the capacity of the Debt Recovery Tribunal (DRT); and (iv) establishing STR. While the PDO remained unchanged, new outcome indicators were added for the new components which were; (i) final resolution of NBL and RBB through either sale or closure; (ii) number of court cases resolved in a period and average number of days taken for resolution of a case by DRT; and (iii) full functioning of STR. 1.6.3 Later, at the request of GON, the original components of the project were downsized during the April 2011 restructuring, based on what was possible to achieve within the revised Project Closing Date (PCD) of December 31, 2011. The following activities were dropped under each component: Component 1: Re-engineering of NRB:

(i) Recruitment of Supervision Expert: It was agreed that the IMF would take on the recruitment of two Resident Advisors for one year to strengthen the Bank Supervision and Financial Institutions Supervision departments.

(ii) HR Expert: After an initial consultant completed his assignment, NRB indicated that it wanted to utilize in-house expertise rather than external consultants.

(iii) Procurement Expert: NRB did not see the need for this expert as no new procurement was planned.

(iv) Public Relations Officer: This was also dropped as NRB wanted to use its own resources.

Component 2: Management Contracts for Restructuring NBL and RBB:

(i) CEO of NBL: NBL decided not to recruit a new CEO using project funds (ii) Bank Restructuring (sales) Advisor: NRB decided against hiring an Advisor,

as GON was still divided over the ultimate disposition of GON’s shares in NBL and RBB.

Component 3: Other Financial Sector Assistance:

(i) DRT: NRB did not receive any new requests from DRT for the procurement of goods and training, hence this was dropped.

At the same time, the following activity was added at the request of GON:

(i) Diagnostic Assessment of NBL: NRB wanted to conduct a fast track diagnostic assessment of NBL’s situation to help GON decide on next restructuring steps for the Bank.

8

As noted above, three out of the four activities allocated to FSTAP from the FSRP were dropped during the April 2011 restructuring, as no progress had been made between 2008 and 2011 due to procurement issues and NRB’s reluctance to pursue certain institutional reforms.

1.7 Other significant changes 1.7.1 FSTAP was restructured four times in a span of four years (2007-2011), including a level-one restructuring, three cancellations of funds, and two extensions in the PCD. 1.7.2 Significant progress had been made under the project during the period 2003-2006, especially on the restructuring of RBB and NBL. By mid-2007 however, FSTAP started to suffer from the adverse impacts of successive changes in GON and the post-conflict transition, which resulted in an extremely difficult political environment for reforms in the banking sector. Although the restructuring of NBL and RBB was broadly on track, there was increasing political resistance to privatization. June 2007 Restructuring: 1.7.3 The first extension in PCD was requested by GON in March 2007 as NRB wanted to hire three local experts for NBL in addition to extending the contract of the management team at NBL which was due to expire in July 2007. 1.7.4 In order to sustain progress made on restructuring NBL and RBB, the Bank extended the PCD to December 31, 2008 with an agreement that the NRB would make progress on the pending recruitment of sales advisors and bank supervisors. The approval for this extension was granted by the Country Management of the Bank in June 2007. Consequently, the budget was also reallocated, as DFID agreed to fund the second extension of the management contracts for another eighteen months. August 2008 Restructuring: 1.7.5 Following the 2007 restructuring, a major setback occurred when a case for fraudulent procurement was filed against the Governor and Executive Director (ED) of NRB by the Commission for Investigation of Abuse of Authority (CIAA). The case, which involved procurement under the Bank funded FSRP, took two years to be resolved in favor of the Governor and ED, brought reform and procurement activities within NRB to a virtual standstill. 1.7.6 At about the same time, there was a major change in the political landscape as Maoists had agreed to a cease fire and to participate in the Constituent Assembly elections planned for April 2008. Due to these political developments, the final resolution of the two banks had to be postponed in order to seek political consensus. However, it was felt that it was important to continue with restructuring efforts until a decision on the final resolution was reached. Stepping away from these institutions could

9

have resulted in a reversal of the significant gains that had been achieved over the previous five years. 1.7.7 GON requested closing FSRP and reallocating some of its activities to FSTAP. At that time, the disbursements of FSTAP lagged Project Appraisal Document (PAD) projections by approximately 35 percent largely due to significant savings on the management contracts of NBL and RBB. The Bank therefore restructured the project again in August 2008 to reallocate US$10.11 million (IDA: US$3.77 million and DFID Grant: US$6.34 million) from FSTAP towards three activities of the FSRP. The Bank also cancelled funds equivalent to SDR4 million from FSTAP. The Development Credit Agreement (DCA) was amended accordingly, and the PCD was extended a second time, to December 31, 2011. April 2011 Level-1 Restructuring: 1.7.8 Even with this restructuring in August 2008, the project could not make satisfactory progress on implementation and disbursements. Procurement and procedural delays intensified, especially as NRB was reluctant to initiate sensitive reforms in the two banks. During its supervision missions, the Bank recorded these developments in the project Implementation Status and Results Reports (ISRs) and flagged the issues while downgrading the project ratings during the period Jun 2010 – Jan 2012. 1.7.9 DFID’s Cancellation of Funds: When the Bank downgraded the project ‘Implementation Progress’ and ‘achievement of development objectives’ from Moderately Satisfactory (MS) to a Moderately Unsatisfactory (MU) in July 2010, DFID made a decision to close its grant in March 2011 before the revised PCD. With that, US$3.16 million (GBP2.17 million) was cancelled by DFID from the total committed funds of US$10 (GBP6.86 million). At the time of cancellation, a total of US$7.49 million (GBP4.51 million) had been disbursed by the project from the DFID Grant. 1.7.10 The Bank team, however, believed it would still be possible to complete some of the uncontroversial reforms, notably the automation of the Credit Information Center Limited (CICL) and STR. In light of this, a Restructuring Paper was submitted to the Bank Board in January 2011 at the request of GON. It was approved in April 2011, just 8 months before the revised PCD. This restructuring resulted in the cancellation of a number of politically sensitive activities (listed in section 1.6.3 of this ICR), a revision in the PDO, and amendments to the results and monitoring framework, project costs, financing plan and procurement plan. December 2011 Restructuring: 1.7.11 As the PCD approached, it became clear the NBL diagnostic and automation of CICL and STR could not be completed by December 31, 2011. Project funds equivalent to SDR1.198 million were therefore cancelled in December 2011 and returned to IDA for allocation to other Bank projects in Nepal.

10

2. Key Factors Affecting Implementation and Outcomes

2.1 Project Preparation, Design and Quality at Entry 2.1.1 The Bank team designed this project after undertaking one identification and three appraisal missions between the 2000 and 2002, during which discussions were held with the stakeholder group comprising NRB, RBB, NBL, MoF, DFID, Asian Development Bank (ADB), and IMF. The project design benefitted from the 1998 CAS for Nepal and the Bank’s 2002 Financial Sector Assessment Report on Nepal. Between the Project Concept Note approval in 1999 and project effectiveness in 2003, a Project Preparation Facility (PPF)4 of US$1.15 million was made available to NRB in two stages. The first PPF of US$550,000 supported the consultancy services in the area of banking supervision and training activities. The second PPF advance of US$ 600,000 financed the NBL Management Team and consultancies at RBB. The PPF was refinanced as part of the total credit amount of FSTAP. Therefore, implementation of key activities under FSTAP had begun prior to project approval. 2.1.2 The PAD correctly identified the risk of policy reversal under the project (rated as High Risk). However, it did not specifically factor in the conflict between the objectives of FSTAP and those of the staff unions in NBL and RBB, which predictably opposed many of the reforms envisaged. It also failed to identify risks associated with the lack of capacity of the judicial system to deal with enforcement of financial contracts and insolvency, though it did note that taking defaulted borrowers to court would be controversial. 2.1.3 The PAD indicated that there had been (unspecified) problems with procurement in the past, and noted that NRB had no experience with conducting procurement in accordance with World Bank rules. The team proposed the recruitment and training of an experienced procurement expert for the CST, which was done. The severe procurement issues which arose as a result of the CIAA case were not foreseeable. 2.1.4 Project alternatives considered included both a broader and narrower project focus. The project team, DFID and IMF all concurred that focusing on the two large commercial banks and the Central Bank represented the minimum required to address critical problems in the sector, while a broader program was ill-advised given capacity constraints. 2.1.5 The team appropriately drew on lessons learned from an earlier Structural Adjustment Credit that had focused on the financial sector by requiring that commitment and action be taken up-front by GON—starting with the placing of external management teams in the two banks. This was done while FSTAP was being prepared. Other lessons learned and which were reflected in project design included, inter-alia, (i) the need to

4 A PPF is an advance of project funds extended to the project counterparts for undertaking activities necessary to achieve readiness for project effectiveness and implementation.

11

enhance the autonomy and skills of the regulator to sustain banking sector reforms; (ii) the necessity for requisite legal reforms; (iii) the importance of sequencing reforms and focusing on a limited number of activities; (iv) that commercial banks should not be recapitalized without fundamental changes in ownership and governance; and, (v) strong borrower commitment to the reforms is needed, as reforms forced from the outside are not always sustainable.

2.2 Implementation 2.2.1 Implementation of FSTAP began quite smoothly and enjoyed strong support from MoF and NRB during the first four years of its implementation, particularly for Component 2. When the new management teams were appointed at NBL and RBB in 2003, both banks had accumulated huge losses and were insolvent, and neither had proper MIS, financial reporting, internal controls or credit procedures. By 2006, both banks were profitable, NPLs had declined quite significantly, MIS systems, internal controls and credit procedures were in place, and the banks were producing regular and timely financial statements. 2.2.2 Mid-term review (MTR): The Bank undertook two supervision missions (September 18-29, 2006 and November 6-8, 2006) to conduct the MTR, close to the original closing date of June 30, 2007. This delay in the MTR was due to discussions between GON and Bank to decide the fate of FSRP. Both projects were running in parallel, and the Bank was considering transferring some FSRP components to FSTAP, which was eventually done. Eventually the MTR was completed in November 2006. It observed that the restructuring of NBL and RBB had progressed well, and an increasing share of the financial system was owned and operated by the private sector, in line with project objectives. The share of banking sector assets owned by NBL and RBB had declined from 51 percent in 2002 to 32 percent in FY 2006. The management teams in the two banks were performing well and their contracts were due to expire in 2007. At that time, GON was committed to maintaining external management teams at NBL and RBB until the point of sale to strategic investors. 2.2.3 The MTR also observed that there was considerable work required to strengthen the capacity of the Banking Supervision Department within NRB, and additional support to accomplish this was being provided through FSRP. It recommended that in order for DRT to function smoothly, additional resources should be extended under the project for office equipment and staff training. 2.2.4 Despite progress made on all components under FSTAP, at the time of the MTR, disbursements lagged projections by 35 percent. This was mainly due to the savings in restructuring of NBL/RBB (US$7.2 million) and under-spending of the training component for NRB (US$1.7 million). Otherwise, procurement and disbursement of equipment and consultancy services were largely on track. The MTR recommended that the Project should be extended with the savings reallocated, and that the management contracts for NBL and RBB should be extended to ensure continuity of reforms.

12

2.2.5 Finally, it was recommended that the GON expedite its application for an Institutional Development Fund (IDF) grant which came through towards the end of 2006. The Bank approved the IDF Grant of US$405,000 in April 2007 for Nepal’s Supreme Court. The Grant was to complement the objectives of the ongoing FSTAP and FSRP. Specifically, it aimed to build the capacity of the judiciary in or to enable it to provide dispute resolution services in banking and commercial matters, to strengthen the commercial bench, and to facilitate data collection and analysis.5 2.2.6 The success of the reforms undertaken in NBL and RBB encouraged NRB to consider replacing international consultants with local management teams after 2007. The higher than anticipated profitability of the banks perhaps also initiated a change in the attitude of NRB and GON towards recapitalization of the two banks, as they began to believe that recapitalization could be achieved over time through retained earnings. However, after the departure of the international management team from NBL in July 2007, progress on the second component of FSTAP slowed. NRB was unable to identify and recruit an appropriate local management team for NBL after the contract of the international management team expired in July 2007. After a delay of 7-8 months, NBL’s management was handed over to a team from within NRB. 2.2.7 In addition to the disruption caused by the departure of the management teams, progress on all components stalled following the CIAA corruption case and forced resignations of the Governor and ED of NRB in July 2007. Despite subsequent attempts by the Bank to expedite implementation, NRB officials were understandably reluctant to take decisions on procurement, fearing a reaction from CIAA. The individuals were subsequently cleared of all charges and re-instated, but virtually all procurement under the project ground to a halt after mid 2007. Critical procurement, including the appointment of a replacement management team at NBL, hiring of an IT consultant for NRB, and procurement of IT systems for the automation of STR and CICL were not completed despite two extensions to the PCD. The Bank’s 2008 implementation support mission observed that 58 percent of the IDA Credit under FSTAP remained undisbursed, mainly due to the lack of progress in procurement. Moreover, after mid-2007, the Bank team noted a considerable deterioration in GON’s commitment towards the privatization of RBB and NBL. Earlier GON had fully endorsed the need for resolving governance issues within NBL and RBB through privatization in its Letter of Development Policy.

5 The Grant closed in August 2010 and could not fully achieve its development objective due to narrow focus on commercial courts and absence of performance benchmarks for commercial benches. Despite that there were some accomplishments during the implementation of this IDF. For instance the Supreme Court profited from the partially automated case management system, the legal library, the training, and the exchange of experience with other courts in the region. The commercial benches received technology, reading material on law, and benefitted from training and consultations on procedural designs and management of judiciary.

13

2.2.8 The re-engineering of NRB was also falling short of expectations. project activities and disbursements were severely affected by NRB’s inability to procure and hire consultants. The recruitment of Bank Supervisors for NRB and Sales/Restructuring Advisors for NBL and RBB was postponed several times. Between 2007 and 2010, the Bank pursued the matter with GoN and NRB on numerous occasions but to no avail. Ultimately, these components were dropped in the 2011 restructuring. 2.2.9 This project went through four restructurings between 2007 and 2011 including two extensions in PCD and two restructurings in 2011. The last restructuring, in December, 2011 led to a cancellation of SDR1.198 million which was reallocated to other IDA operations in Nepal.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization 2.3.1 M&E under this project was regularly conducted through the Bank’s implementation support missions, some of which were conducted jointly for FSTAP and FSRP. The MTR was conducted in September 2006. The Bank team used the project results indicators and results framework to measure performance of NRB during these missions. Aide Memoires were shared with the GON, MoF and NRB management towards the end of the each mission. Correspondence between Bank management and MoF after 2007 sought to expedite implementation and obtain GON’s renewed commitment towards privatization as the overall objective for NBL and RBB. 2.3.2 CST administered FSTAP and thus was in-charge of M&E implementation. The absence of a strong MIS within CST prevented the smooth flow of information and effective monitoring of project results. Consequently CST was unable to provide coherent and organized data to the Bank team during implementation. Similarly, no periodic supervision was conducted at the project level by NRB, MoF and NPC to monitor progress towards the achievement of PDOs.

2.4 Safeguard and Fiduciary Compliance Procurement: 2.4.1 The overall Procurement Rating is Unsatisfactory. 2.4.2 An assessment of NRB at appraisal identified that its staff had almost no experience of public procurement, and no knowledge or experience in Bank procurement procedures. In addition, the internal decision-making chain at NRB, which often required Governor level approval, took time. Thus, many planned procurement activities were delayed, including the initial procurement of management teams for NBL and RBB. The team thus recommended that CST include an experienced individual Procurement Expert who, in addition to assisting NRB with carrying out project related procurement, would also provide on-the-job training to some key staff. Though the expert was placed in CST,

14

this did not result in any major improvement in the timeliness of procurement, and his services were discontinued in 2006. 2.4.3 The slow pace of procurement came to a standstill from 2007 when the CIAA filed cases against the Governor and ED related to procurement of consultants under FSRP. Even though both officials were ultimately exonerated, the fear of further CIAA investigations persisted. This gravely affected several critical procurement activities such as the appointment of a replacement management team at NBL, hiring of an IT consultant for NRB, and procurement of IT systems for the automation of STR and CICL. Financial Management (FM): 2.4.4 The FM rating for this Project is Moderately Satisfactory. 2.4.5 Project Financial Management: The dedicated project implementation unit (CST) was responsible for the FM of the project and overall FM was rated MS. Although there were some start-up delays, the project took the initiative to maintain a reliable FM information system which resulted in timely generation of financial reports and audit reports. Trimester Implementation Progress Reports which included Financial Monitoring Reports were submitted relatively on time. Over the period of implementation, the quality of financial reports improved. Audit reports were submitted on time. There were no major issues with staffing as the staff deputed to the project was of high caliber. 2.4.6 Entity Financial Management: Over the life of the project, there was little improvement in NRB’s FM capability and inadequate attention by NRB Board and management to address the weaknesses in FM which were repeatedly highlighted in the qualified entity annual audit reports of the NRB and through Bank supervision. Major issues and weaknesses in the entity's FM included: Non-compliance with NRB Act 2002 - NRB's audit reports were never completed

within four months of the end of the fiscal year; Non-compliance with International Accounting Standards; Establishing computerized FM systems within a reasonable time period; Establishing systems for assets management; Control weaknesses in banking transactions and accounting systems; and Weaknesses in internal control and internal audit. 2.4.7 Frequent changes of staffing in the Finance Division restricted any action being taken and the limited measures to improve FM by some individuals did not have major impact. There were provisions under FSRP to provide funding for FM improvements but NRB declined to make use of this provision.

Safeguards:

2.4.8 This was an Environmental Category ‘C’, project hence none of the environment and safeguards policies were triggered.

15

2.5 Post-completion Operation/Next Phase 2.5.1 The proposed third phase of Bank assistance to GON for financial sector reforms was intended to support the financial re-engineering of banks (re-capitalization) at the point of sale after satisfactory changes in governance arrangements and cost restructuring had taken place. Given the lack of political will to privatize, the Bank did not pursue this, and did not launch Phase III. However, the Bank is pursuing discussions with GON on a Development Policy Credit (DPC) for FY13 to address the macroeconomic and financial sector vulnerability in Nepal. The Bank and GON have reached an in-principle agreement to a set of indicative prior actions for DPC1 and DPC2, which include a series of measures intended to support a more robust and inclusive financial sector. These include full recapitalization of RBB and NBL, a decision to transfer shares of NBL to a reputable strategic investor, and diagnostic audits of a selection of financial institutions. At end June 2012, the Cabinet announced a decision to inject equity into the two state controlled banks. RBB received NPR4.32 billion and NBL received NPR1.37 billion. However, even after these announced capital injections, both banks will still fall short of minimum capital requirement as per Central Bank guidelines. 2.5.2 While the positions of NBL and RBB improved significantly over the life of this project, the financial condition of other banks in Nepal has deteriorated due, inter-alia, to large exposure to a collapsing real estate market. Strengthening of the legal and regulatory framework for effective bank resolution is therefore a key prior action under discussion with GON for the DPC. 2.5.3 According to DFID’s assessment of FSTAP completed in March 2011, any future intervention in the financial sector of the country should factor in the highly fragile governance environment in the country and GON’s involvement in the economy. DFID is providing TA in conjunction with preparation of the proposed DPC. As DFID has the flexibility to carry out own procurement under TA grants, a program which combines TA support from DFID and budget support from the Bank, it is unlikely to encounter the procurement problems that plagued FSTAP.

3. Assessment of Outcomes

3.1 Relevance of Objectives, Design and Implementation 3.1.1 Both the original and revised PDOs of this project are still relevant to the financial sector development of Nepal. Restructuring of NBL and RBB remain incomplete, and both banks remain insolvent. NRB still requires strengthening to perform its core Central Bank functions, and the financial sector as a whole is quite fragile. A few years after the project commenced, the priorities of GON changed, and privatization lost its importance in front of other reforms. For the same reason, the original PDO i.e. improving the macroeconomic stability and achieving private sector led economic growth was revised to a more realistic PDO in 2011. One can hope that the planned financial sector DPC enables GON to effectively deal with the distressed financial sector institutions.

16

3.1.2 On a positive note, FSTAP managed a commendable turnaround in the two banks, and some important progress was made in each component. The project resulted, inter-alia, in greater financial discipline in the banking sector, a strengthened legal and regulatory framework, and greatly improved financial disclosure and credit information.

3.2 Achievement of Project Development Objectives 3.2.1 This section primarily details the performance on the revised PDOs and downsized components of FSTAP. The achievements against the original PDO indicators and intermediate outcome indicators have been tabulated in section F (Results Framework Analysis) of the ICR datasheet. Restructuring the two big state controlled banks (NBL and RBB):

3.2.2 The targeted outcomes for the restructuring of NBL and RBB were achieved to a great extent. The banks have been profitable and have been reporting positive cash flows for seven years in a row. When the project initiated its activities, these banks were incurring substantial losses. The number of staff within NBL and RBB was reduced from 5,652 and 5,522 to 2,342 and 2,555 respectively.

3.2.3 The banks have also made considerable progress in automation and financial reporting. The computerization of RBB branches met targets with 95 percent of deposits and 98 percent of loans automated and on-line. A total of 46 Automated Teller Machines (ATMs) were installed at various locations including markets and other public places. The quarterly financial statements and annual audited financial statements are published in a timely manner. NBL’s 58 branches were automated and 77 percent of deposit base and 88 percent of loans were covered by the IT platform.

3.2.4 Asset quality at the two banks has improved significantly. Since July 2003 NPLs have decreased from 58 percent for NBL and 60 percent for RBB to 5.29 percent and 10.9 percent respectively as of mid-October 2011. Reengineering NRB: 3.2.5 The objectives of this component were not achieved to a satisfactory level. The supervisory capacity of NRB has improved somewhat as a result of TA provided; however the agreed outcomes remained incomplete at PCD. The Central Bank did not recruit the international supervision experts needed to strengthen NRBs supervisory capacity. The project did achieve results on improving the regulatory framework as the NRB Act was enacted for the first time and BFIA was amended. However, the amendments to BFIA are still pending with the Parliament. 3.2.6 The PRO hired by NRB also proved very effective while he was in place as he implemented NRB’s communication strategy with the objective of informing the public on the restructuring efforts and their significance for the economy. Some progress was also made in HR policy reform.

17

Capacity Building in the Financial Sector: 3.2.7 The objectives under this component were partially achieved, with mixed results on the various activities. 3.2.8 CICL and STR: The project funded a consultant to draft a business plan for CICL’s establishment and operations. At the start of the project in 2003, Nepal’s CIB was a very basic structure within NRB that had limited resources and manual data entry systems. During the lifetime of FSTAP, it turned around completely as the private sector took over CICL’s management with an independent board. CICL now generates the requested credit reports within 24 hours, which has facilitated lending decisions by commercial banks. STR was established in 2010, but is not yet operational due to the failure to procure the requisite systems. Its management was outsourced to CICL by MoF; however there has been no action on this decision. 3.2.9 DRT: The project enhanced the capacity of DRT through training programs and exposure visits of DRT staff to similar institutions in other South Asian countries. The Bank has received positive feedback on the performance of DRT from commercial banks, who indicate that DRT has helped in debt recovery efforts. 3.2.10 In addition, FSTAP also contributed to the Banker’s Training Center by supporting its automation, enhancing its capacities to train professionals, and developing a strategic plan for the Center. 3.2.11 Training of Journalists: The project organized international training for 44 financial journalists, and financial reporting in the press appears to have improved as a result. More factual and accurate financial reporting has ensured greater public awareness of what is happening in the financial sector, and has contributed to greater credit discipline. As a result of press reports, for example, a former Prime Minister was made to repay a loan taken by friends (with his guarantee). 3.3 Efficiency Due to the nature of project activities and the mix of results accomplished under FSTAP (and FSRP), it has not been possible to calculate an accurate Net Present Value (NPV) or Economic Rate of Return (ERR) for this intervention. While many of the ultimate results expected, including the recapitalization of NBL and RBB, have not yet been achieved, there has been a number of significant cost savings realized. The two restructured public banks have generated NPR30 billion (US$400 million) in operating profits since 2003, when they were losing US$80 million per annum before restructuring efforts began under FSTAP. While some of the savings and turnaround can also be attributed to the 2nd phase FSRP (or indeed other factors), assuming the losses had continued at the same rate, the fiscal savings to GON exceed US$1 billion (losses of US$640 million over 8 years versus profits of US$400 million). Total expenditures for both projects were approximately only US$78 million. While the net worth of the two banks remain negative, the deficit has

18

declined significantly, thereby substantially reducing the ultimate fiscal cost of recapitalizing the banks.

3.4 Justification of Overall Outcome Rating Rating: Moderately Unsatisfactory 3.4.1 The original and revised PDOs of FSTAP are still relevant to Nepal’s financial sector development. NRB should be strengthened to assume its core Central Bank and regulatory functions. Similarly in order to sustain the progress made in reforming RBB and NBL, there needs to be a resolution to the ownership and negative capital position of the public banks, as originally envisaged in FSSS. The change in the political economy for financial sector reform, coupled with the unfortunate prosecution of senior NRB officials for mis-procurement, brought progress under the project to a virtual stand-still from 2007 onwards. The following review of outcomes under the project components substantiates the rating: 3.4.2 Restructuring of RBB and NBL: This is the centerpiece of the project, and efforts to restructure and improve the performance of RBB and NBL showed very significant results. The project achieved virtually all of the targets and outcomes during the first five years of its implementation. Both banks were incurring losses until 2003 and were subsequently turned around by the management teams, proper procedures and financial reporting were put in place, and NPLs were brought down from 61 percent and 60 percent to 5.3 percent and 10.9 percent for NBL and RBB respectively by PCD. More than 80 percent of the deposit base was computerized. The overall staff levels were reduced by 48 percent and 44 percent in NBL and RBB respectively by July 2007, largely due to the VRS funded through FSRP. The ultimate outcome of strengthening corporate governance of the banks cannot be achieved until there is a final resolution of the ownership and negative net worth of the two banks, but these were not objectives of FSTAP. Recognizing the risk of a policy reversal, the program was designed in three phases, and the first phase FSTAP had limited objectives of restructuring the banks and preparing them for eventual recapitalization and privatization or liquidation. This was largely achieved, though its sustainability cannot be assured until there is a more lasting resolution of the ownership, governance and management of the banks. 3.4.3 Developing the capacity of NRB staff to effectively perform key central banking functions: This outcome has not been achieved to a significant degree. Needed financial legislation was prepared under the project but has not been enacted due to the current political situation in Nepal (BFIA approval pending). The objective of strengthening the supervision capacity of NRB was not achieved. A consulting firm was recruited in 2006 for this assignment but left Nepal abruptly due to the security situation. While NRB was trying to replace the team in 2007 the Governor was charged by CIAA. Subsequent efforts to recruit banking supervision experts failed, though, as noted above, the Bank and IMF both sought to provide support through alternative arrangements which did not require NRB procurement i.e. through First Initiative and IMF TA. The current

19

fragile state of Nepal’s banking system demonstrates that NRB’s regulatory and supervisory capacity remains weak, however. 3.4.4 Creating an enabling environment for the financial sector development: The key elements of this component were either not achieved or only partially achieved, due, inter-alia, to NRB’s inability to procure the requisite goods and services. While some progress was made on credit discipline through the establishment of DRT, and financial reporting and credit information improved, outcomes have fallen short of expectations in key respects. Nepal still does not have a modern and fully automated STR or CIB, both of which are critical pieces of the country’s financial infrastructure. Similarly, the diagnostic of NBL, which was to provide a road map for the resolution of the bank, had to be dropped due to procurement issues. 3.4.5 Considering the above, the outcomes of FSTAP have been rated as Moderately Unsatisfactory.