do you ‘feel’ asean? - miti.gov.my weekly bulletin/miti_weekly...economic freedom index of asean...

TRANSCRIPT

As Chair of ASEAN, at the end of this week Malaysia will welcome the 10 leaders of the region and their delegations to Kuala Lumpur for the 26th ASEAN Summit. As we get caught up in the hive of activity around the preparations for the Summit, I must share a recent incident that serves as a reality check for all of us involved in ASEAN.

I was part of panel that selected university students to represent Malaysia at an Asia leadership programme. The theme of the programme is related to ASEAN connectivity, specifically public transportation. The students were bright and articulate. They could discuss with us how data analytics could be used to improve our public transport system. Yet, of the 12 students interviewed, only ONE could tell me what the acronym “ASEAN” meant, which countries were members of the grouping, and who the Chair of ASEAN was this year!

Do you ‘feel’ ASEAN?

Disappointing? Of course. Understandable? Perhaps. But it also validates, Malaysia’s choice of the theme “Our People, Our Community, Our Vision” to focus on a “people-centred ASEAN”. So what if ASEAN is emerging as one of the world’s economic drivers? Or that ASEAN home to some 600 million people? Or ASEAN’s population is twice that of the USA; and that ASEAN is collectively the 7th largest economy in the world and the third largest in Asia? Or, that according to JP Morgan, USD5.3 trillion of global trade passes through ASEAN waterways each year, and that ASEAN should become the fourth-largest market after the EU, US and China by 2030?

All these mean little if the average person in ASEAN can neither appreciate, nor “feel” ASEAN. Therein lies the challenge for governments as we declare ourselves a community at the end of this year. It is thus less about the declaration and more about the effect and impact of being a community.Yes, over the past two years the Ministry of International Trade and Industry (MITI) has had a series of outreach, and numerous information-sharing, sessions at the universities. Also, programmes to inform the business community and the members of the media about the work being done to step up ASEAN economic integration. And, why ASEAN economic integration matters.

To translate this into an initiative that students can appreciate, we collaborated with TalentCorp to launch the MY ASEAN Internship initiative. This programme was announced by Prime Minister Dato’ Sri Najib Tun Abdul Razak last year. It will involve the best and brightest of Malaysia’s young talents. It is backed by global partner companies, including Maybank, Air Asia, CIMB, BDO, Sunway, Nestle, Sime Darby, Digi, Axiata, GE, ZICOlaw, as well as the Securities Commission Malaysia.

MITI Weekly Bulletin / www.miti.gov.my

By: Rebecca Fatima Sta. Maria, Secretary-General, Ministry of International Trade and Industry, Malaysia18 April 2015

Malaysian students will have opportunities to intern in ASEAN member states. ASEAN students studying in Malaysia will get the opportunity to intern in Malaysian companies that have a regional presence. In partnership with these institutions, the MY ASEAN Internship will offer unique opportunities for youths to be exposed to ASEAN as a market, and to its leading companies. For over 10 weeks, cohorts of 70-100 ASEAN youths will also have a chance to develop new skillsets required by industry. In addition, we would like to have these MY ASEAN interns become informal ambassadors to promote Malaysia, and ASEAN.

In collaboration with the ASEAN Business Advisory Council (ABAC) we established the ASEAN Young Entrepreneurs Association, and later, the ASEAN Women Entrepreneurs Association. In May we will have the ASEAN small and medium enterprises in Kuala Lumpur for the inaugural ASEAN SME Showcase. These initiatives aside, my experience with those 12 students tells me that we must do more so folks appreciate what it means to be an ASEAN citizen.Our message is simple: Through our community building efforts we want to ensure prosperity in the region. But more importantly, prosperity that is inclusive. And an economic community with benefits that are far-reaching. So when we are done with the easy part of declaring ourselves an economic community at the end of 2015, we know that we are only at the beginning of the journey towards becoming one.

11,315.3

12,303.9

12,675.8

13,119.5

13,634.6

13,931.6

7,218.1

7,955.5

8,129.5

8,338.8

8,485.4

8,577.6

4,097.2

4,348.4

4,546.3

4,780.7

5,149.2

5,354.0

0 2000 4000 6000 8000 10000 12000 14000

2009

2010

2011

2012

2013

2014

Total Female Male

MALAYSIA

Source : Department of Statistics, Malaysia

Labour Force Participation by Gender2009 - 2014

Notes:*Age between 15 to 64 ** all persons not classified as employed or unemployed such as housewives, students (including those going for further studies), retired, disabled persons and those not interested in looking for job

Labour Force Market , 2014Working Age Population*

386.5

RM386.5 bil.

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

Employed

8.4 mil 5.2 milUnemployed

0.2 mil 0.2 mil

male Female

Outside Labour Force**

2.1 mil 4.6 mil

Persons (‘000)

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.mySource : Department of Statistics, Malaysia

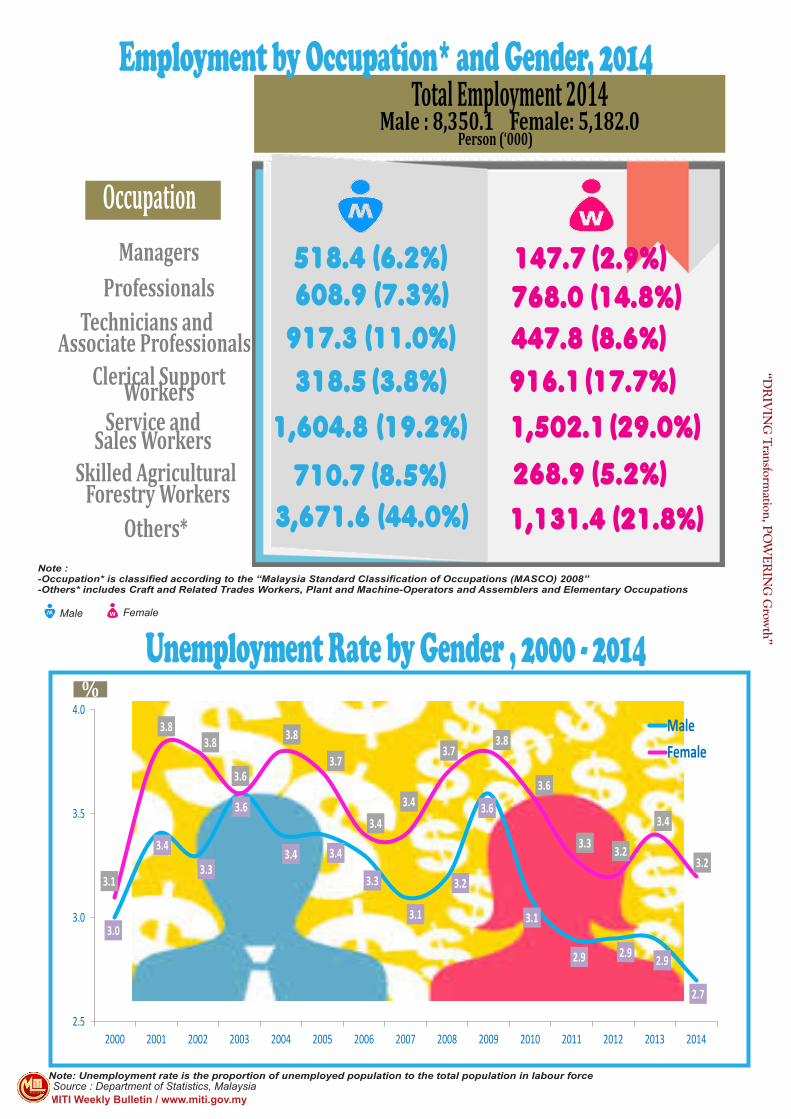

Employment by Occupation* and Gender, 2014

Unemployment Rate by Gender , 2000 - 2014

Note : -Occupation* is classified according to the “Malaysia Standard Classification of Occupations (MASCO) 2008”-Others* includes Craft and Related Trades Workers, Plant and Machine-Operators and Assemblers and Elementary Occupations

518.4 (6.2%) 147.7 (2.9%)608.9 (7.3%) 768.0 (14.8%)

917.3 (11.0%) 447.8 (8.6%)318.5 (3.8%) 916.1 (17.7%)

1,604.8 (19.2%) 1,502.1 (29.0%)

710.7 (8.5%) 268.9 (5.2%)3,671.6 (44.0%) 1,131.4 (21.8%)

Person (‘000)

Managers

Occupation

Total Employment 2014Male : 8,350.1 Female: 5,182.0

ProfessionalsTechnicians and Associate Professionals

Clerical Support WorkersService and

Sales WorkersSkilled Agricultural Forestry Workers

Others*

Note: Unemployment rate is the proportion of unemployed population to the total population in labour force

3.0

3.4

3.3

3.6

3.4 3.4

3.3

3.1

3.2

3.6

3.1

2.9 2.9 2.9

2.7

3.1

3.83.8

3.6

3.8

3.7

3.4

3.4

3.73.8

3.6

3.3 3.2

3.4

3.2

2.5

3.0

3.5

4.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MaleFemale

%

Male Female

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

Sabah

Potential Employment* in Manufacturing 2005-2014

Approved Manufacturing Projects , 2005-2014

MITI Weekly Bulletin / www.miti.gov.mySource: Malaysian Investment Development Authority (MIDA)Note: * Estimate of job created

0.9

4.2

1.1 0.6 0.4

0.8 0.9

4.8

2.4 2.4

0.3

0.8

2.2

0.3

5.2

0.5 0.0

0.3

1.0 0.5

0.0

2.0

4.0

6.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RM billion

Domestic Investment Foreign Investment

2,233

4,650

2,820

3,244

2,509

3,481

1,648

2,153

1,873 1,796

800

1,300

1,800

2,300

2,800

3,300

3,800

4,300

4,800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

RM m

il.

Potential Employment

Economic Freedom Index of ASEAN Members 2015Overall ScoreCountryRank

Singapore 89.41

MALAYSIA 70.82

Brunei 68.93

Thailand 62.44Philippines 62.25Indonesia 58.16Cambodia 57.57Viet Nam 51.78

Laos 51.49Burma 46.910

The Index of Economic Freedom is a series of 10 economic measurements created by the Heritage Foundation and Wall Street Journal. The index scores nations on 10 broad factors of economic freedom using statistics from organizations like the World Bank, the International Monetary Fund and the Economist Intelligence Unit:• Business freedom• Trade freedom• Monetary freedom• Government size• Fiscal freedom• Property rights• Investment freedom• Financial freedom• Freedom from corruption• Labor freedomThe 10 factors are averaged equally into a total score.

MITI Weekly Bulletin / www.miti.gov.my

MITI’s ASEAN Portal can be accessed via http://www.miti.gov.my/

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

and You’

Source: http://heritage.org/index/

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

5.4

2.2 2.42.8

3.3

4.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2011 2012 2013 2014

International Repor tMerchandise Trade Volume Growth, 2011-2016 a

Expor ts and Impor ts Volume Growth by region, 2011-2016 a,

World Merchandise Trade

2016 P

Annual % change

2015 P

Note: a Figures for 2015 and 2016 are projections b Other regions comprise the Africa, Commonwealth of Independent States and Middle East P - Projection

MITI Weekly Bulletin / www.miti.gov.mySource: WTO International Trade Statistics for trade.

Annual % Change

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

Singapore’s External Trade March 2015

Total Trade: S$81.2 bil (RM216.9 bil) , 22.9%

Expor ts: S$44.9 bil (RM120.0 bil) , 24.5%

Impor ts: S$36.3 bil (RM96.9bil) , 20.9%

Note: % refer to m-o m growth

Bilateral Trade Singapore’s second largest trading partner

Malaysia , with total trade worth S$8.8 bil (RM23.5 bil) Singapore’s third major export destination

Malaysia , with total exports of S$4.8 bil (RM12.7 bil) Singapore’s third largest source of import

Malaysia , with total imports of S$4.0 bil (RM10.8 bil)

Major Trading Partners , January - March 2015

MITI Weekly Bulletin / www.miti.gov.mySource: MITI Singapore

MITI Weekly Bulletin / www.miti.gov.my

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

The World’s ‘Most Power ful’ Passpor ts, 2015

Note: The Passport Index is an interactive tool, which collects, displays and ranks the passports of the world, based on how many countries their holders can visit without obtaining a visa before arrival or at all.

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

Rank Country

#2

#3

#1147145

144

United States of AmericaUnited Kingdom

FranceSouth Korea

Germany

Number of visa-free countries

Italy Sweden

143Denmark

SingaporeFinland

JapanLuxembourg

Netherlands

#7 140Malaysia

#4

#18

#57#60#73#80

#551256361574428

BruneiThailand

Philippines

IndonesiaCambodia

Myanmar

Source:www.passportindex

0.46

0.48

0.50

0.52

0.54

0.56

0.58

0.60

3.703.803.904.004.104.204.304.404.504.60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

1 EUR = RM 1 CNY = RM1 CNY = RM 0.59

1 EUR = RM 3.99

Source : http://www.gold.org/investments/statistics/gold_price_chart/

Source : http://www.hardassetsalliance.com/charts/silver-price/usd/oz

Malaysian Ringgit Exchange Rate with Euro and Chinese Yuan

Gold Prices, 2 January - 17 April 2015

Silver Prices, 2 January - 17 April 2015

Source : Bank Negara, Malaysia

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

37.7

38.7

36.0

37.0

38.0

39.0

40.0

41.0

42.0

43.0

2 Ja

n

9 Ja

n

16 Ja

n

23 Ja

n

30 Ja

n

6 Fe

b

13 F

eb

20 F

eb

27 F

eb

6 M

ar

13 M

ar

20 M

ar

27 M

ar

3 Ap

r

10 A

pr

17 A

pr

US$/Gram Gold

15.8

16.3

14.5

15.0

15.5

16.0

16.5

17.0

17.5

18.0

18.5

2 Ja

n

9 Ja

n

16 Ja

n

23 Ja

n

30 Ja

n

6 Fe

b

13 F

eb

20 F

eb

27 F

eb

6 M

ar

13 M

ar

20 M

ar

27 M

ar

3 Ap

r

10 A

pr

17 A

pr

US$/Oz Silver

Source: Ministry of International Trade and Industry, Malaysia

Notes: The preference giving countries under the GSP scheme are Japan, Switzerland, the Russian Federation, Norway, Cambodia, Liechtenstein, Belarus and Kazakhstan.

AJCEP: ASEAN-Japan Comprehensive Economic Partnership (Implemented since 1 February 2009) ACFTA: ASEAN-China Free Trade Agreement (Implemented since 1 July 2003) AKFTA: ASEAN-Korea Free Trade Agreement (Implemented since 1 July 2006)

AANZFTA: ASEAN-Australia-New Zealand Free Trade Agreement(Implemented since 1 January 2010)

AIFTA: ASEAN-India Free Trade Agreement (Implemented since 1 January 2010)

ATIGA: ASEAN Trade in Goods Agreement (Implemented since 1 May 2010)

MICECA: Malaysia-India Comprehensive Economic Cooperation Agreement (Implemented since 1 July 2011)

MNZFTA: Malaysia-New Zealand Free Trade Agreement (Implemented since 1 August 2010)MCFTA: Malaysia-Chile Free Trade Agreement (Implemented since 25 February 2012)MAFTA: Malaysia-Australia Free Trade Agreement (Implemented since 1 January 2013)

MPCEPA: Malaysia-Pakistan Closer Economic Partnership Agreement (Implemented since 1 January 2008)

MJEPA: Malaysia-Japan Economic Partnership Agreement (Implemented since 13 July 2006)

22 Feb 1 Mar 8 Mar 15 Mar 22 Mar 29 Mar 5 Apr 12 AprAANZFTA 74 89 73 84 319 88 87 68AIFTA 122 126 136 92 175 110 212 83AJCEP 72 55 78 74 101 57 85 84

0

50

100

150

200

250

300

350

RM

mill

ion

22 Feb 1 Mar 8 Mar 15 Mar 22 Mar 29 Mar 5 Apr 12 AprATIGA 9,861 4,055 596 950 3,154 703 2,475 784ACFTA 165 865 780 916 539 841 663 483AKFTA 592 1,795 117 127 695 173 131 138

0

2,000

4,000

6,000

8,000

10,000

12,000

RM

mill

ion

22 Feb 1 Mar 8 Mar 15 Mar 22 Mar 29 Mar 5 Apr 12 AprMICECA 40.80 132.78 49.74 44.86 48.01 50.53 64.51 55.21MNZFTA 0.02 0.13 0.01 0.06 0.08 0.35 0.06 0.47MCFTA 5.61 9.29 6.00 11.37 23.46 46.12 9.08 8.54MAFTA 25.27 36.27 23.40 42.25 36.51 34.36 35.39 26.70

0

20

40

60

80

100

120

140

RM m

illio

n

22 Feb 2015 1 Mar 2015 8 Mar 2015 15 Mar 2015 22 Mar 2015 29 Mar 2015 5 Apr 2015 12 Apr 2015

AANZFTA 467 835 658 805 776 910 869 770AIFTA 485 467 561 478 651 529 708 462AJCEP 116 172 154 241 250 177 209 163ATIGA 2,648 3,695 4,107 4,433 4,562 4,322 4,496 3,719ACFTA 790 1,659 1,454 1,354 1,566 1,569 1,464 1,484AKFTA 610 643 765 844 889 782 767 661MICECA 236 278 297 360 355 289 385 322MNZFTA 2 5 1 7 4 14 3 6MCFTA 27 56 42 75 57 52 52 54MAFTA 206 360 259 481 409 336 402 290MJEPA 608 775 823 812 775 838 836 819MPCEPA 139 150 173 172 118 165 160 125GSP 73 170 104 114 139 112 164 68

22 Feb 1 Mar 8 Mar 15 Mar 22 Mar 29 Mar 5 Apr 12 AprMJEPA 116 145 131 670 167 129 191 146MPCEPA 72 19 52 113 38 16 20 33GSP 14 22 75 18 26 15 21 9

0

100

200

300

400

500

600

700

800

RM

mill

ion

Value of Preferential Certificates of Origin

Number and Value of Preferential Certificates of Origin (PCOs)Number of Certificates (Provision Data)

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

CommodityCrude

Petroleum (per bbl)

Crude Palm Oil (per MT)

Raw Sugar

(per MT)

Rubber SMR 20(per MT)

Cocoa SMC 2

(per MT)

Coal(per MT)

Scrap Iron HMS

(per MT)17 Apr 2015

(US$) 55.7 651.5 275.5 1,390.0 2,067.5 55.2 270 (high)250 (low)

% change* 7.9 1.4 unchanged 1.2 1.2 2.2 unchangedunchanged

2014i 54.6 - 107.6 823.3 352.3 1,718.3 2,615.8 59.8 370.0

2013i 88.1 - 108.6 805.5 361.6 2,390.8 1,933.1 .. 485.6

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

Commodity Prices

Notes: All figures have been rounded to the nearest decimal point * Refer to % change from the previous week’s price i Average price in the year except otherwise indicated n.a Not availble

Sources: Ministry of International Trade and Industry Malaysia, Malaysian Palm Oil Board, Malaysian Rubber Board, Malaysian Cocoa Board, Malaysian Iron and Steel Industry Federation, Bloomberg and Czarnikow Group.

Highest and Lowest Prices, 2014/2015

Lowest (US$ per bbl)

Highest(US$ per bbl)

Crude Petroleum (17 April 2015)US$55.7 per bbl

201413 June 2014: 107.6

201426 Dec 2014: 54.6

201517 Apr 2015: 55.7

201513 Mar 2015: 44.8

Lowest (US$ per MT)

Highest(US$ per MT)

Crude Palm Oil (17 April 2015)

US$651.5 per MT

201414 Mar 2014: 982.5

201426 Dec 2014: 664.0

201516 Jan 2015: 701.0

20156 Feb 2015: 621.0

Steel Bars(per MT)

RM1,840 - RM1,940

Average Domestic Prices, 10 Apr 2015

Billets(per MT)

RM1,450 - RM1,500

Sources : Ministry of International Trade and Industry Malaysia, Malaysian Palm Oil Board, Malaysian Rubber Board, Malaysian Cocoa Board, Malaysian Pepper Board, Malaysian Iron and Steel Industry Federation, Bloomberg and Czarnikow Group, World Bank.

Commodity Price Trends“D

RIV

ING

Transform

ation, PO

WER

ING

Grow

th”

MITI Weekly Bulletin / www.miti.gov.my

645.0

621.0

685.0 690.0 689.0

692.5

673.5

648.0650.5

658.5661.0

651.5

600

610

620

630

640

650

660

670

680

690

700

30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar 20 Mar 27 Mar 3 Apr 10 Apr 17 Apr

US$

/mt

Crude Palm Oil

2,065.2

1,958.9

2,003.9

2,060.0

2,113.7

2,124.6

2,110.42,107.8

1,974.8

2,042.9

2,017.1

2,042.12,067.5

1,900

1,950

2,000

2,050

2,100

2,150

23 Jan 30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar20 Mar27 Mar 3 Apr 10 Apr 17 Apr

US$

/mt

Cocoa

345.5

331.3

324.3

330.0326.8

310.8

300.5

291.0

283.8

272.5275.5 275.5

260

270

280

290

300

310

320

330

340

350

360

23 Jan 30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar 20 Mar 27 Mar 3 Apr 10 Apr

US$

/mt

Raw Sugar

1,384.5

1,418.5

1,426.5

1,419.5

1,438.0

1,412.0

1,412.5

1,405.5

1,413.5

1,403.0

1,373.0

1,390.0

1,350

1,360

1,370

1,380

1,390

1,400

1,410

1,420

1,430

1,440

1,450

30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar 20 Mar 27 Mar 3 Apr 10 Apr 17 Apr

US$

/mt

Rubber SMR 20

5,740

5,779 5,843

6,245

6,469

6,515

6,864

7,822

7,707

7,967

7,894 7,806

7,507

7,286 7,267

7,734

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

2014 2015

USD

/ to

nne

Black Pepper

* until 10 April 2015

48.2

51.7

52.8

50.8

49.849.6

44.8

46.6

48.9 49.1

51.6

55.7

40

42

44

46

48

50

52

54

56

58

30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar 20 Mar 27 Mar 3 Apr 10 Apr 17 Apr

US$

/bbl

Crude Petroleum

Sources : Ministry of International Trade and Industry Malaysia, Malaysian Palm Oil Board, Malaysian Rubber Board, Malaysian Cocoa Board, Malaysian Pepper Board, Malaysian Iron and Steel Industry Federation, Bloomberg and Czarnikow Group, World Bank.

Commodity Price Trends“D

RIV

ING

Transform

ation, PO

WER

ING

Grow

th”

MITI Weekly Bulletin / www.miti.gov.my

1,727

1,695 1,705

1,811

1,751

1,839

1,948

2,030

1,990

1,946

2,056

1,909

1,815

1,818

1,774

1,500

1,600

1,700

1,800

1,900

2,000

2,100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

US$

/ to

nne

Aluminium

14,101 14,204

15,678

17,374

19,401

18,629

19,118

18,600 18,035

15,812 15,807

15,962

14,849 14,574

13,756

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

US$

/ to

nne

Nickel

320.0 320.0 320.0 320.0

330.0

320.0

280.0 280.0

260.0

270.0 270.0 270.0

300.0 300.0 300.0 300.0

320.0

300.0

250.0 250.0

240.0

250.0 250.0 250.0

220

240

260

280

300

320

340

360

5 Dec 12 Dec 19 Dec 26 Dec 2 Jan 9 Jan 6 Feb 13 Feb 27 Feb 13 Mar 27 Mar 10 Apr

US$

/mt

Scrap Iron

Scrap Iron/MT (High)

Scrap Iron/MT(Low)

7,291

7,149

6,650 6,674

6,891

6,821

7,113

7,002

6,872

6,737

6,713

6,446

5,831

5,729

5,940

5,500

5,700

5,900

6,100

6,300

6,500

6,700

6,900

7,100

7,300

7,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

US$

/ to

nne

Copper

49.9

51.1

56.1

56.9 56.8

57.7

58.4 58.6 58.558.2

56.4

55.2

48.0

50.0

52.0

54.0

56.0

58.0

60.0

30 Jan 6 Feb 13 Feb 20 Feb 27 Feb 6 Mar 13 Mar 20 Mar 27 Mar 3 Apr 10 Apr 17 Apr

US$

/mt

Coal

128.1

121.4

111.8

114.6

100.6

92.7

96.192.6

82.4

81.0

74.0

68.0

68.0

63.0

58.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015

US$

/dm

tu

Iron Ore

SUCCESS STORYKota Kinabalu Industrial Park (KKIP)

Kota Kinabalu Industrial Park is a project of the Sabah State Government. Its role is to facilitate both economic development as well as the optimum utilization of the state’s rich natural resources and attractions.Being in the strategic location is a key ingredient in a business success. Located north of Kota Kinabalu, the capital city of Sabah, KKIP occupies an area of more than 8320 acres. The park falls within the “Knowledge Corridor” as recognized by the state government, where the avant-garde Universiti Malaysia Sabah, Universiti Teknologi Mara and a host of training and research institutions are located.

Contact Details :Lot 11B, Amenity Centre, Industrial Zone 1, No 9, Jalan 1A, KKIP SelatanKota Kinabalu Industrial Park,m 88660 Kota Kinabalu.P. O. Box 21955, 88777 Luyang.

This modern metroplex integrates residential, commercial, and industrial properties to cater a satellite township of 100,000 people. Sabah is a convenient gateway to a substantial consumer market of 52 million, being strategically located within the East Asean Growth Polygon (BIMP-EAGA). Combined with modern deep-sea ports, road network, state-of-the-art infrastructure and utilities, Kota Kinabalu Industrial Park complements its investment potentials. Providing opportunities across 4 dedicated zones, Kota Kinabalu Industrial Park actively promotes a high quality standard of living and working environment for its people. KKIP’s industrial zone is the key investment area where it caters to light-to-medium-scale industries that need high human-resource content.

KKIP promises a modern lifestyle catering to a populace with a variety of social, retail, service, educational and recreational facilities. Aiming to deliver sustainable value through thoughtfully planned developments, KKIP is committed to uplift the quality of life as well as conserve the rich, natural environment of the park. By integrating sustainability, KKIP maximizes resource efficiency and help to shape the local communities. As a global entity, KKIP aims to build a better sustainable future. It is essential for KKIP to develop involvement across the business and beyond.

Tel : 088-498001-498005, 412787 – 412788 Fax : 088-498011, 498014E-mail : [email protected] / [email protected]

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

Semperit Engineering & Technology Asia Sdn Bhd

Semperit Engineering & Technology Asia Sdn Bhd (SET) is a subsidiary of Semperit AG Holding from Austria. Its main activities include manufacturing of specialised rubber and plastic products for the medical sector and other industries. SET was incorporated in 2013 to undertake R&D activities on equipment and processes in glove manufacturing, providing end-to-end solutions. The R&D services offered by SET to its related and unrelated companies in the gloves manufacturing industries in Malaysia will ensure the competitiveness of Semperit Group in producing environmentally friendly products. Through Latexx Partners Berhad, a related company by which the R&D services will be provided, the medical examination gloves are being distributed to more than 300 customers in 80 countries.

Malaysia Investment Performance 2014

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

MITI ProgrammePerasmian SICPA APAC Regional Centre, CYBERJAYA

16 April 2015

MITI Weekly Bulletin / www.miti.gov.my 15

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

MITI Weekly Bulletin / www.miti.gov.my

Save the Date...

1 May-31 October 2015

Construction work at the site of the Malaysia Pavilion

“DR

IVIN

G T

ransformation, P

OW

ERIN

G G

rowth”

6 February 2015

http://www.miti.gov.my/cms_matrix/form.jsp?formId=c1148fbf-c0a81573-3a2f3a2f-1380042c

Comments & SuggestionsDear Readers,Kindly click the link below for any comments in this issue. MWB reserves the right to edit and to republish letters as reprints.

Name : Zamawani ShariDesignation : Librarian AssistantJob Description : Responsible for assisting

and handling of library taskssuch as document and processlibrary materials andinformation sources

Division : Resource CentreContact No : 03 - 62034593Emel : [email protected]

Name : Hartini HarisDesignation : Librarian AssistantJob Description : Responsible for assisting

and handling of library taskssuch as document and processlibrary materials andinformation sources

Division : Resource CentreContact No : 03 - 62034594Emel : [email protected]

MITI Weekly Bulletin / www.miti.gov.my