!do not print! front cover goes here · !do not print! front cover goes here see separate artwork...

TRANSCRIPT

!DO NOT PRINT!

FRONT COVERGOES HERE

SEE SEPARATE ARTWORK SUPPLIEDFF GROUP_STATS 11_COVER_AW

Registered Number 614802952 Weeks Ended 28 May 2011

!DO NOT PRINT!

INSIDE FRONT COVERGOES HERE

SEE SEPARATE ARTWORK SUPPLIEDFF GROUP_STATS 11_COVER_AW

Registered Number 614802952 Weeks Ended 28 May 2011

FatFace GroupLimited(formerly Fat Face World Limited)

Directors’ Report & ConsolidatedFinancial Statements

ContentsSection One: Business ReviewGroup Chairman’s Statement 2Business Review and Directors’ Report 4Statement of Directors’ Responsibilities 10Independent Auditor’s Report 11

Section Two: Financial StatementsConsolidated Income Statement 13Statement of Comprehensive Income 14Statement of Financial Position 15Statement of Changes in Equity 16Cash Flow Statements 18

Section Three: NotesNotes to the Financial Statements 20

Life is out there...fatface.com

2 / Directors’ Report & Consolidated Financial Statements

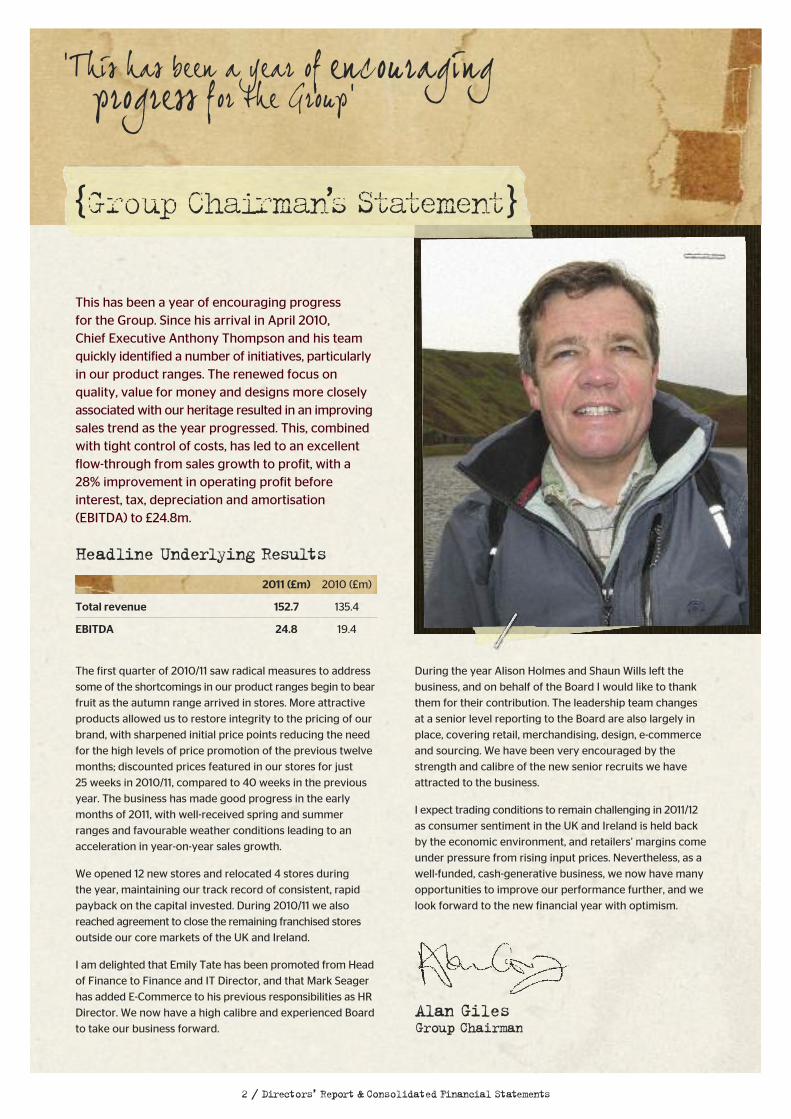

This has been a year of encouraging progress for the Group. Since his arrival in April 2010, Chief Executive Anthony Thompson and his teamquickly identified a number of initiatives, particularlyin our product ranges. The renewed focus onquality, value for money and designs more closelyassociated with our heritage resulted in an improvingsales trend as the year progressed. This, combinedwith tight control of costs, has led to an excellentflow-through from sales growth to profit, with a28% improvement in operating profit beforeinterest, tax, depreciation and amortisation(EBITDA) to £24.8m.

‘This has been a year of encouraging progress for the Group’

During the year Alison Holmes and Shaun Wills left the

business, and on behalf of the Board I would like to thank

them for their contribution. The leadership team changes

at a senior level reporting to the Board are also largely in

place, covering retail, merchandising, design, e-commerce

and sourcing. We have been very encouraged by the

strength and calibre of the new senior recruits we have

attracted to the business.

I expect trading conditions to remain challenging in 2011/12

as consumer sentiment in the UK and Ireland is held back

by the economic environment, and retailers’ margins come

under pressure from rising input prices. Nevertheless, as a

well-funded, cash-generative business, we now have many

opportunities to improve our performance further, and we

look forward to the new financial year with optimism.

Alan GilesGroup Chairman

The first quarter of 2010/11 saw radical measures to address

some of the shortcomings in our product ranges begin to bear

fruit as the autumn range arrived in stores. More attractive

products allowed us to restore integrity to the pricing of our

brand, with sharpened initial price points reducing the need

for the high levels of price promotion of the previous twelve

months; discounted prices featured in our stores for just

25 weeks in 2010/11, compared to 40 weeks in the previous

year. The business has made good progress in the early

months of 2011, with well-received spring and summer

ranges and favourable weather conditions leading to an

acceleration in year-on-year sales growth.

We opened 12 new stores and relocated 4 stores during

the year, maintaining our track record of consistent, rapid

payback on the capital invested. During 2010/11 we also

reached agreement to close the remaining franchised stores

outside our core markets of the UK and Ireland.

I am delighted that Emily Tate has been promoted from Head

of Finance to Finance and IT Director, and that Mark Seager

has added E-Commerce to his previous responsibilities as HR

Director. We now have a high calibre and experienced Board

to take our business forward.

2011 (£m) 2010 (£m)

Total revenue 152.7 135.4

EBITDA 24.8 19.4

Headline Underlying Results

{GroupChairman’sStatement}

3 / Directors’ Report & Consolidated Financial Statements

SectionOne:

BusinessReview

4 / Directors’ Report & Consolidated Financial Statements

{Business Review & Directors’Report}

BusinessReview

Principal ActivitiesFat Face is a UK based retailer, specialising in the design and sale of active lifestyle clothing and related accessories.From a few sweatshirts in 1988, the Fat Face brand hasgrown to what it has become today. The Group offers a wide range of womenswear, menswear, childrenswear,footwear and accessories. Distribution is via three mainchannels: 190 stores in the UK and Ireland, home shoppingchannel and wholesale.

TradingWhilst the retail sector continued to face tough marketconditions, the initiatives put in place, particularly focused onimproving the product ranges over the last year, have meantthat the Group saw trading improve as the year progressed.

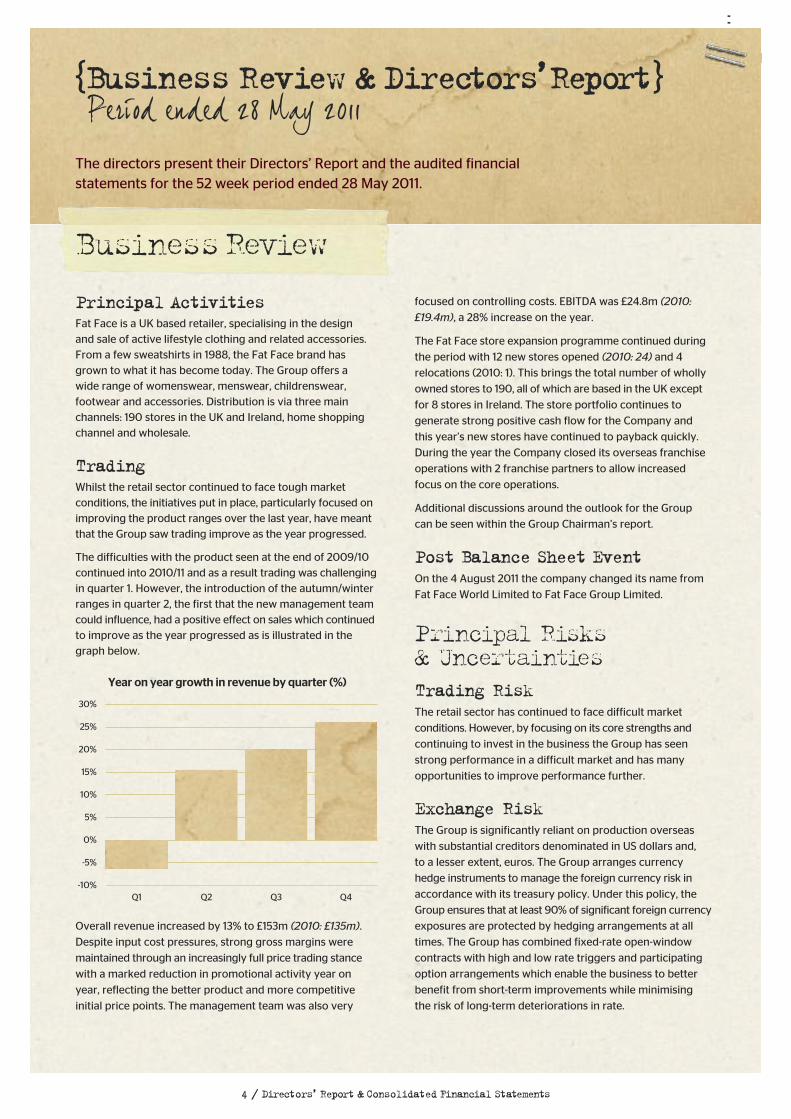

The difficulties with the product seen at the end of 2009/10continued into 2010/11 and as a result trading was challengingin quarter 1. However, the introduction of the autumn/winterranges in quarter 2, the first that the new management teamcould influence, had a positive effect on sales which continuedto improve as the year progressed as is illustrated in thegraph below.

Overall revenue increased by 13% to £153m (2010: £135m).

Despite input cost pressures, strong gross margins were

maintained through an increasingly full price trading stance

with a marked reduction in promotional activity year on

year, reflecting the better product and more competitive

initial price points. The management team was also very

The directors present their Directors’ Report and the audited financialstatements for the 52 week period ended 28 May 2011.

Year on year growth in revenue by quarter (%)

-5%

-10%

0%

5%

10%

15%

20%

25%

30%

Period ended 28 May 2011

3.93.93.93.93.93.93.9

Q1 Q2 Q3 Q4

focused on controlling costs. EBITDA was £24.8m (2010:

£19.4m), a 28% increase on the year.

The Fat Face store expansion programme continued during

the period with 12 new stores opened (2010: 24) and 4

relocations (2010: 1). This brings the total number of wholly

owned stores to 190, all of which are based in the UK except

for 8 stores in Ireland. The store portfolio continues to

generate strong positive cash flow for the Company and

this year’s new stores have continued to payback quickly.

During the year the Company closed its overseas franchise

operations with 2 franchise partners to allow increased

focus on the core operations.

Additional discussions around the outlook for the Group

can be seen within the Group Chairman’s report.

Post Balance Sheet EventOn the 4 August 2011 the company changed its name from

Fat Face World Limited to Fat Face Group Limited.

Principal Risks & UncertaintiesTrading RiskThe retail sector has continued to face difficult market

conditions. However, by focusing on its core strengths and

continuing to invest in the business the Group has seen

strong performance in a difficult market and has many

opportunities to improve performance further.

Exchange RiskThe Group is significantly reliant on production overseas

with substantial creditors denominated in US dollars and,

to a lesser extent, euros. The Group arranges currency

hedge instruments to manage the foreign currency risk in

accordance with its treasury policy. Under this policy, the

Group ensures that at least 90% of significant foreign currency

exposures are protected by hedging arrangements at all

times. The Group has combined fixed-rate open-window

contracts with high and low rate triggers and participating

option arrangements which enable the business to better

benefit from short-term improvements while minimising

the risk of long-term deteriorations in rate.

5 / Directors’ Report & Consolidated Financial Statements

These are monitored via the risk register which has been

introduced during this financial year. The directors oversee

the development of internal control processes to ensure that

these risks are managed appropriately. Executive directors

and operational management are delegated with the task

of implementing these processes and reporting to the Board

on their outcomes.

Topics included on the register or which are reviewed

regularly by the Board include:

Health and SafetyThe directors recognise the importance of health and safety

at work. The health and safety of the Group’s employees,

customers, contractors, sites and equipment is of great

importance. There is a comprehensive structure of processes

and procedures to mitigate the health and safety risk, including

risk assessments, accident reporting, and nominated health

and safety representatives across the business. Policies and

procedures are reviewed and audited regularly to make

safety management more robust and fully up to date.

Ethical TradingWith a large global supplier base, the directors recognise

that there is a potential risk that certain suppliers may not

work within the required ethical standards of the Group.

This could result in a poor perception of the Group in the

market and could have a negative impact on the brand.

The Group has developed an ethical trading policy with

which it ensures that all suppliers are in agreement. It is also

a member of the Ethical Trading Initiative. For further details

please refer to the Corporate Social Responsibility section

of this report.

SectionOne:

BusinessReview

Euro denominated sales are more than sufficient to offset

the exchange risk arising from purchases denominated in

euros. The excess euro cash generated from sales is not

sufficient to represent a material risk to the business.

Financial RiskThe Group manages its exposure to interest rate risk by the

use of an interest rate cap covering most of its variable rate

debt. In addition, detailed reporting and cash forecasting

ensures that the Group’s liquidity is maintainable into the

medium term.

The Group’s external financing arrangements include

conventional covenant tests as is customary with agreements

of this type. The Group’s performance against those tests is

measured on a quarterly basis and management maintain

ongoing forecasts of performance to ensure that all tests

can be met. The Group met all covenants tested during

the period.

Liability RiskThe Group maintains usual commercial insurance policies for

a business of this type. The Group undertakes a critical review

of all coverage limits and the applicability of deductibles and

franchises during each annual review process.

-----In addition to the risks above, the Board has a policy of

ongoing identification and review of key business risks which

may restrict or seriously impact the ability of the Group to

carry on its operations or may damage the brand.

6 / Directors’ Report & Consolidated Financial Statements

Key PerformanceIndicatorsA key performance indicator (KPI) scorecard is currently beingdeveloped to allow the directors to review detailed informationcovering a range of financial and non-financial indicators for the Group. Some of the key indicators which are alreadybeing monitored include:

• operating profit before depreciation (EBITDA)

• payroll % to sales

• labour turnover rate

• cash

Corporate SocialResponsibilitySuppliersFat Face’s supplier base is crucial to meeting the Group’srequired quality and ethical standards and ensuring that the product is available on time. Through a combination of extending the supplier base and managing the existingsuppliers, the Group is able to reduce any over-reliance onparticular suppliers and improve on the competitiveness of the product.

The Group continues to ensure that all suppliers are awareof and agree to the Group’s ethical and operating standardswhich are fully documented and shared with suppliers. In addition to ensuring that all local laws are adhered to,these require:

• remuneration for employees must be fair andcommensurate with the work undertaken;

• children may not be employed;

• no discrimination on the basis of race, gender, religion or ethnic background;

• no forced labour;

• no inappropriate disciplinary practices;

• freedom of association for all employees; and

• health & safety policies must be established and enforced.

To underpin the Group’s commitment in this area, Fat Face is a member of the Ethical Trading Initiative. Under thisinitiative the Group agrees to audit the ethical standards of its suppliers and make the results of these audits available to other members. Equally, the Group is able to access theinvestigations carried out by other members into its current and potential suppliers.

Fat Face seeks to ensure that terms of payment specifiedand agreed with suppliers are not exceeded.

At the year end there were 54 days purchases in tradepayables (2010: 45).

SectionOne:

BusinessReview

7 / Directors’ Report & Consolidated Financial Statements

EmployeesThe Group is committed to valuing diversity, thereby seeking

to ensure the effective use of people in the best interests of

both the Group and its employees. It is the policy of Fat Face

to provide employment and development opportunities to

persons regardless of age, race, colour, religion, sex, sexual

preference, marital status, nationality, ethnic origin or

disability. It is Group policy to wherever possible retain in

employment employees who become disabled, providing

retraining opportunities where appropriate.

EnvironmentThe Group continually reviews its production processes to

ensure that it produces high quality product in ways that

reduce the impact on the environment. The Group recycled

321 (2010: 302) tonnes of cardboard out of Fat Base and

plastic out of many stores.

The Group continues to encourage better waste

management and energy efficiency around the business.

During the period Fat Face has installed around 70 smart

meters to around 60 stores across the estate which will

measure emissions within those stores, and this will provide

information to stores allowing them to control their energy

usage more efficiently.

All product suppliers are required to have an environmental

policy signed by their Chief Executive.

CommunityThe Group is committed to supporting the local

community, both in respect of employment and social

responsibility. As part of this the Group has worked with

the Education Business Partnership to encourage young

people into industry.

Proposed DividendThe directors do not recommend the payment of a dividend

(2010: nil).

Political& CharitableContributionsThe Group made no political contributions during the

current or preceding period.

In February 2009 the Fat Face Foundation was founded.

This is a registered charity with the objective of enabling

people to actively enjoy the outdoors and respect the

environments we play in. Most of the funding for the

Foundation has come from the sale of Foundation

associated products by the Group.

Donations to UK charities by the Group

during the year amounted to £87,981

(2010: £29,029), which was all donated to

the Foundation (2010: £28,573). During

the year, the Fat Face Foundation made

donations of £21,883 (2010: £24,705).

8 / Directors’ Report & Consolidated Financial Statements

Toby Bowhill(Appointed 28 June 2011)

Appointed Brand Director in May 2010, Toby joined Fat Faceafter spending eight years at Abercrombie and Fitch latterlyin the role of Hollister & Ruehl Concept Director.

Simon Pickering(Appointed 28 June 2011)

Appointed Design and Buying Director, Simon held a SeniorDirector role within the Arcadia Group, responsible for BHSand Burton. He is a former Director of Gap Europe,responsible for Menswear. Simon has previously held seniorbuying roles in Debenhams and Burton group.

Mark Seager (Appointed 28 June 2011)

Mark joined Fat Face in January 1997 as a store manager. Heprogressed through the retail channel with various field andcentrally based operational roles before taking on the wholesale,licensing and franchise programmes in 2008. In 2010 Markwas promoted to E-Commerce and HR Director.

Shaun Wills (Resigned 25 November 2010)

Left to right: Toby Bowhill, Simon Pickering, Becky Bateman, Emily Tate, Anthony Thompson, Mark Seager

{Directors}The directors who held office during the year were as follows:

Executive DirectorsAnthony Thompson

Appointed Chief Executive in April 2010, Anthony was

previously Managing Director of the George brand within the

international division of Walmart Stores, and an executive

director of ASDA Stores Ltd. He is a former Retail Director of

Marks and Spencer plc, Senior Vice President of Gap in Europe

and Chief Executive of Blackwell Limited.

Emily Tate(Appointed 26 May 2011)

Appointed Finance Director in May 2011, Emily was internally

promoted from her position as Head of the Finance

Department, having joined the Group in November 2008.

She has significant retail experience having previously

worked for Polo Ralph Lauren and B&Q. Emily qualified

as a Chartered Accountant with PricewaterhouseCoopers.

Becky Bateman(Appointed 28 June 2011)

Appointed Retail Director in July 2010, Becky’s previous role

was Head of Retail for Top Shop/Top Man overseeing the

flagships in Oxford Circus, London and New York.

SectionOne:

BusinessReview

ShareholdersBridgepoint has been Fat Face Group Limited’s majority

shareholder since 2007. For details of their shareholding

please refer to note 26. Bridgepoint hold the investment

within its Bridgepoint Europe III Fund. Guy Weldon and

Benoit Alteirac are monitoring the fund’s investment on

behalf of Bridgepoint.

Going ConcernIn adopting the going concern basis for preparing the

financial statements, the directors have considered the

principal activities as well as the business risks as set out

on pages 4 to 5. Based on the Group’s improved trading

performance in the period, cash flow forecasts and

projections and notwithstanding the net liabilities of

£22,213,000 (2010: £24,097,000), the Board continues to

be satisfied that the Group will be able to operate within

the level of its facilities for the foreseeable future (see note 17

in the financial statements for details of the Group facilities).

For this reason the Group continues to adopt the going

concern principle in preparing its financial statements.

Disclosure of Information to AuditorsThe directors who held office at the date of approval of this

Directors’ Report confirm that, so far as they are each aware,

there is no relevant audit information of which the Group’s

auditors are unaware; and each director has taken all the steps

that they ought to have taken as a director to make themselves

aware of any relevant audit information and to establish that

the Group’s auditors are aware of that information.

AuditorsPursuant to Section 487 of the Companies Act 2006, the

auditors will be deemed to be reappointed and KPMG LLP

will therefore continue in office.

By order of the board:

Anthony ThompsonChief Executive Officer

Unit 3, Ridgway, Havant, Hampshire PO9 1QJ

22 August 2011

9 / Directors’ Report & Consolidated Financial Statements

Non-Executive DirectorsAlan Giles

Alan Giles is Chairman of the Group. He was previously

Chief Executive of HMV Group from 1999 to 2006.

He formed HMV Group as a leveraged buy-out and led the

Group through its London Stock Exchange IPO in 2002.

He is a non-executive director of Rentokil Initial plc and

The Office of Fair Trading, an Associate Fellow at Said

Business School, University of Oxford and Honorary Visiting

Professor at Cass Business School.

Guy Weldon(Appointed by Bridgepoint)

Guy Weldon is a Bridgepoint partner and is responsible

for Bridgepoint’s UK investment activities as well as being

a member of the European Consumer investment team.

He joined Bridgepoint in 1990 and is based in its

London office.

Benoit Alteirac(Appointed by Bridgepoint on 28 June 2011)

Benoit joined Bridgepoint in 2002 and is also a member

of Bridgepoint’s European consumer investment team.

He is based in Bridgepoint’s London office.

Patrick Fox(Appointed by Bridgepoint, resigned 28 June 2011)

The Group provides Directors’ and Officers’ insurance protection

for all of the directors of the companies in the Group with

a £10,000,000 (2010: £10,000,000) limit of indemnity.

{Statementof Directors’Responsibilities}

10 / Directors’ Report & Consolidated Financial Statements

The directors are responsible for preparing the Directors' Report and the financial statements in accordance with applicable

law and regulations.

Company law requires the directors to prepare group and parent company financial statements for each financial year.

Under that law they have elected to prepare both the Group and the parent company financial statements in accordance

with IFRSs as adopted by the EU and applicable law.

Under company law the directors must not approve the financial statements unless they are satisfied that they give a true

and fair view of the state of affairs of the Group and parent company and of their profit or loss for that period.

In preparing each of the Group and parent company financial statements, the directors are required to:

• select suitable accounting policies and then apply them consistently;

• make judgments and estimates that are reasonable and prudent;

• state whether they have been prepared in accordance with IFRSs as adopted by the EU; and

• prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Group

and the parent c ompany will continue in business.

The directors are responsible for keeping adequate accounting records that are sufficient to show and explain the group and

parent company's transactions and disclose with reasonable accuracy at any time the financial position of the group and parent

company and enable them to ensure that the financial statements comply with the Companies Act 2006. They have general

responsibility for taking such steps as are reasonably open to them to safeguard the assets of the group and to prevent and

detect fraud and other irregularities.

in respect of the Directors’ Reportand the Financial Statements

{Independent Auditor’s Report}

• the Group financial statements have been properly prepared

in accordance with IFRSs as adopted by the EU;

• the parent company financial statements have been properly

prepared in accordance with IFRSs as adopted by the EU

and as applied in accordance with the provisions of the

Companies Act 2006; and

• the financial statements have been prepared in accordance

with the requirements of the Companies Act 2006.

Opinion on Other Matter Prescribedby the Companies Act 2006In our opinion the information given in the Directors’ Report

for the financial year for which the financial statements are

prepared is consistent with the financial statements.

Matters on Which we are Requiredto Report by ExceptionWe have nothing to report in respect of the following matters

where the Companies Act 2006 requires us to report to you if,

in our opinion:

• adequate accounting records have not been kept by the

parent company, or returns adequate for our audit have

not been received from branches not visited by us; or

• the parent company financial statements are not in

agreement with the accounting records and returns; or

• certain disclosures of directors' remuneration specified

by law are not made; or

• we have not received all the information and explanations

we require for our audit.

W SmithSenior Statutory Auditor

For and on behalf of KPMG LLP, Statutory Auditor

Chartered Accountants, Dukes Keep

Marsh Lane, Southampton SO14 3EX

22 August 2011

SectionOne:

BusinessReview

11 / Directors’ Report & Consolidated Financial Statements

to the Members of Fat Face Group Limited(formerly Fat Face World Limited)

We have audited the financial statements of Fat Face Group

Limited (formerly Fat Face World Limited) for the period ended

28 May 2011 set out on pages 13 to 43. The financial reporting

framework that has been applied in their preparation is

applicable law and International Financial Reporting Standards

(IFRSs) as adopted by the EU and, as regards the parent

company financial statements, as applied in accordance with

the provisions of the Companies Act 2006.

This report is made solely to the company's members,

as a body, in accordance with Chapter 3 of Part 16 of the

Companies Act 2006. Our audit work has been undertaken

so that we might state to the company's members those

matters we are required to state to them in an auditor’s

report and for no other purpose. To the fullest extent

permitted by law, we do not accept or assume responsibility

to anyone other than the company and the company's

members, as a body, for our audit work, for this report,

or for the opinions we have formed.

Respective Responsibilities of Directors & AuditorAs explained more fully in the Directors' Responsibilities

Statement set out on page 10, the directors are responsible

for the preparation of the financial statements and for being

satisfied that they give a true and fair view. Our responsibility

is to audit, and express an opinion on, the financial statements

in accordance with applicable law and International Standards

on Auditing (UK and Ireland). Those standards require us to

comply with the Auditing Practices Board's (APB's) Ethical

Standards for Auditors.

Scope of the Audit of theFinancial StatementsA description of the scope of an audit of financial

statements is provided on the APB’s website at:

www.frc.org.uk/apb/scope/private.cfm

Opinion on Financial StatementsIn our opinion:

• the financial statements give a true and fair view of the state

of the Group’s and of the parent company's affairs as at 28

May 2011 and of the Group’s loss for the period then ended;

12 / Directors’ Report & Consolidated Financial Statements

Note Trading Non- 2011 Trading Non- 2010Results Recurring Results Recurring

2011 Items 2010 Items£000 £000 £000 £000 £000 £000

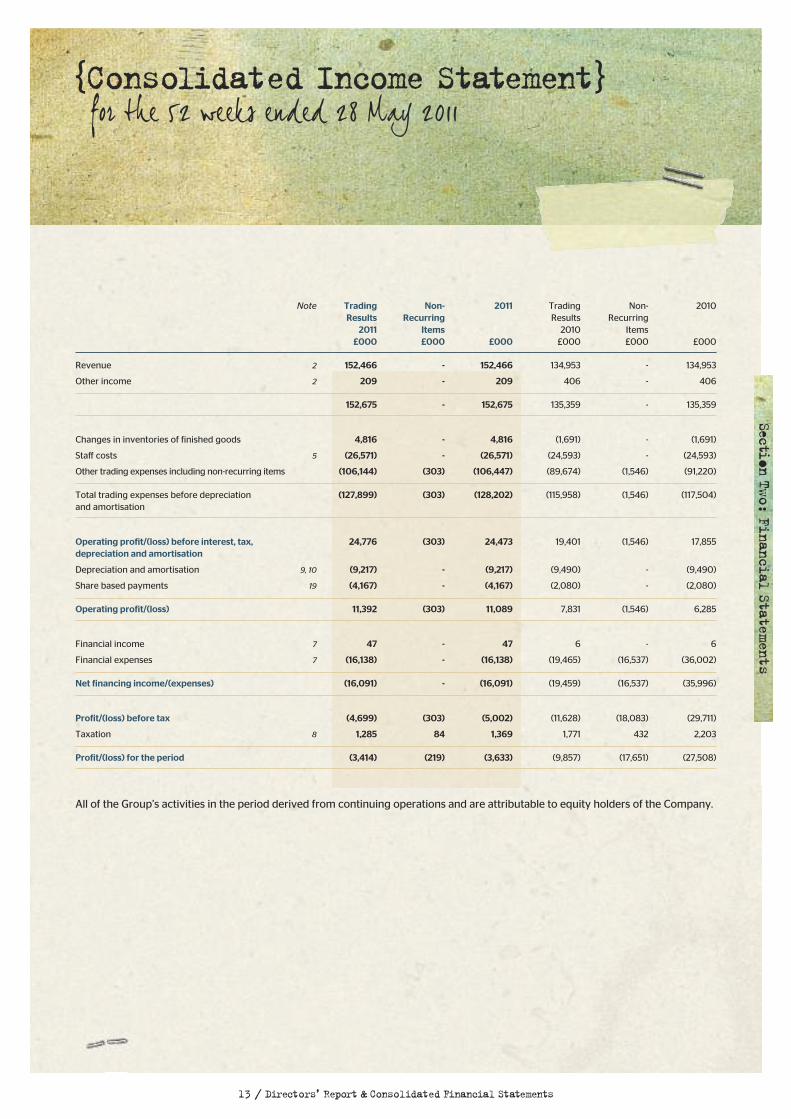

Revenue 2 152,466 - 152,466 134,953 - 134,953

Other income 2 209 - 209 406 - 406

152,675 - 152,675 135,359 - 135,359

Changes in inventories of finished goods 4,816 - 4,816 (1,691) - (1,691)

Staff costs 5 (26,571) - (26,571) (24,593) - (24,593)

Other trading expenses including non-recurring items (106,144) (303) (106,447) (89,674) (1,546) (91,220)

Total trading expenses before depreciation (127,899) (303) (128,202) (115,958) (1,546) (117,504)and amortisation

Operating profit/(loss) before interest, tax, 24,776 (303) 24,473 19,401 (1,546) 17,855depreciation and amortisation

Depreciation and amortisation 9, 10 (9,217) - (9,217) (9,490) - (9,490)

Share based payments 19 (4,167) - (4,167) (2,080) - (2,080)

Operating profit/(loss) 11,392 (303) 11,089 7,831 (1,546) 6,285

Financial income 7 47 - 47 6 - 6

Financial expenses 7 (16,138) - (16,138) (19,465) (16,537) (36,002)

Net financing income/(expenses) (16,091) - (16,091) (19,459) (16,537) (35,996)

Profit/(loss) before tax (4,699) (303) (5,002) (11,628) (18,083) (29,711)

Taxation 8 1,285 84 1,369 1,771 432 2,203

Profit/(loss) for the period (3,414) (219) (3,633) (9,857) (17,651) (27,508)

All of the Group’s activities in the period derived from continuing operations and are attributable to equity holders of the Company.

13 / Directors’ Report & Consolidated Financial Statements

SectionTwo:

FinancialStatements

{Consolidated Income Statement}for the 52 weeks ended 28 May 2011

Group Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

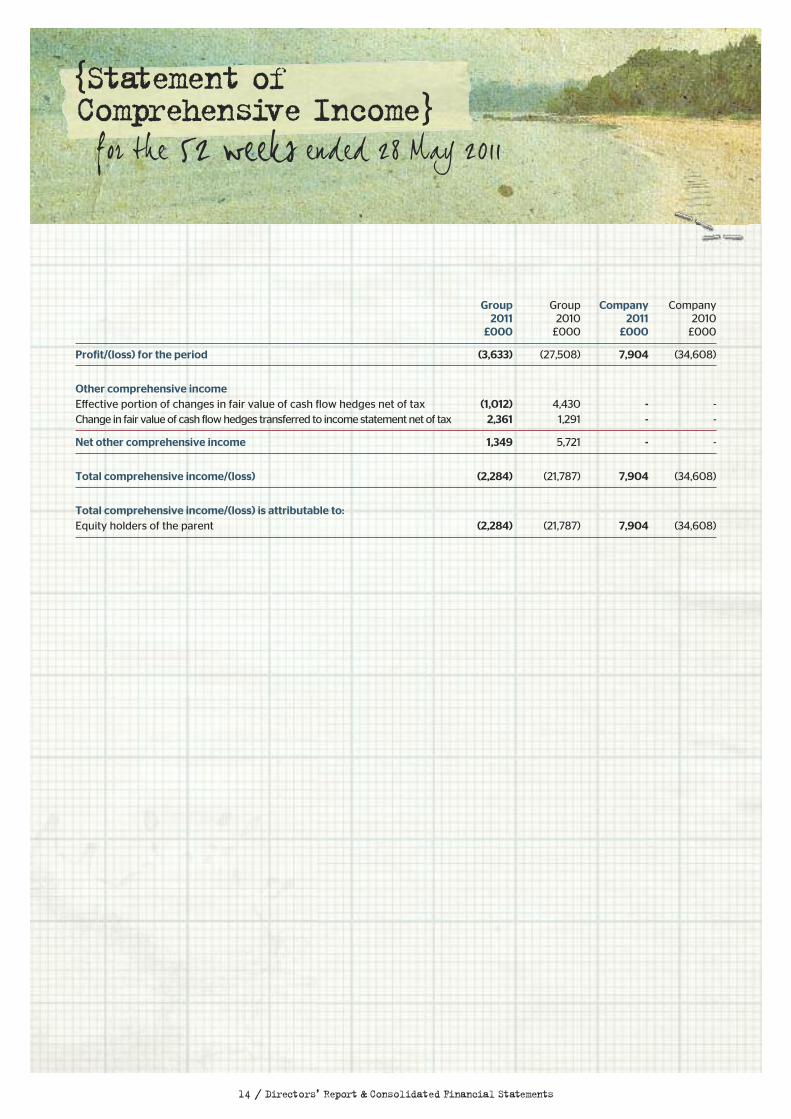

Profit/(loss) for the period (3,633) (27,508) 7,904 (34,608)

Other comprehensive incomeEffective portion of changes in fair value of cash flow hedges net of tax (1,012) 4,430 - -Change in fair value of cash flow hedges transferred to income statement net of tax 2,361 1,291 - -

Net other comprehensive income 1,349 5,721 - -

Total comprehensive income/(loss) (2,284) (21,787) 7,904 (34,608)

Total comprehensive income/(loss) is attributable to:Equity holders of the parent (2,284) (21,787) 7,904 (34,608)

14 / Directors’ Report & Consolidated Financial Statements

{Statement of Comprehensive Income}

for the 52 weeks ended 28 May 2011

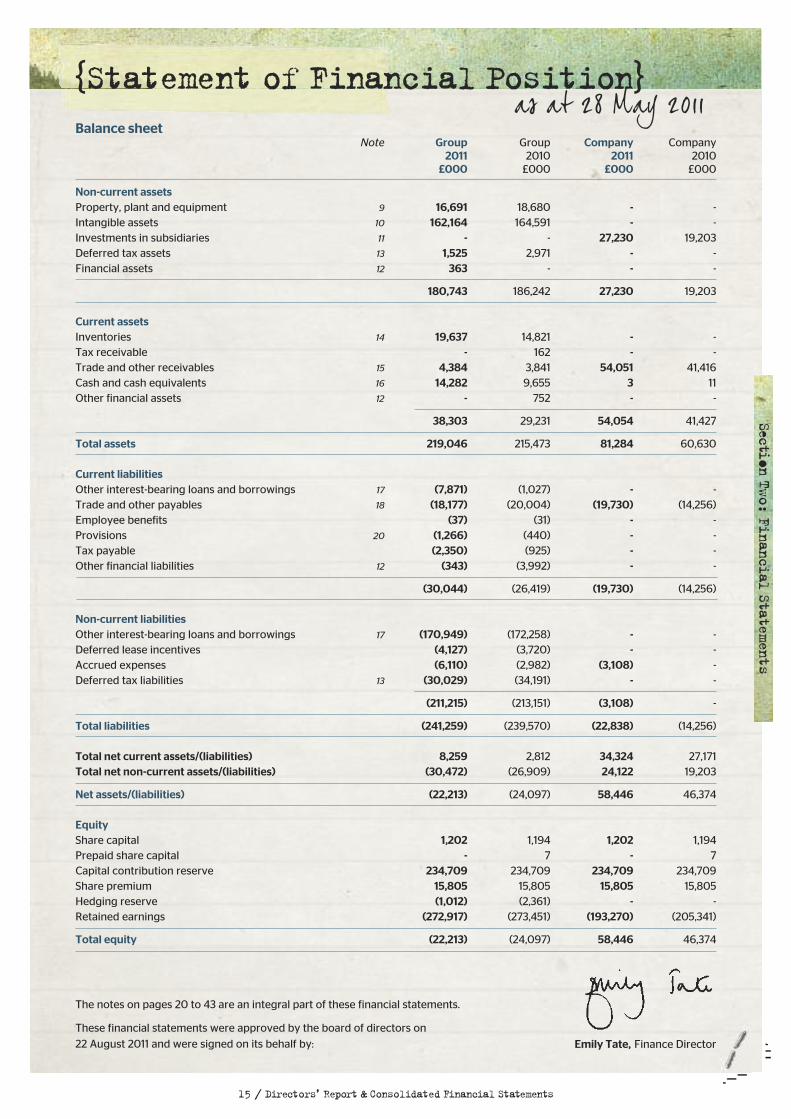

Balance sheetNote Group Group Company Company

2011 2010 2011 2010£000 £000 £000 £000

Non-current assetsProperty, plant and equipment 9 16,691 18,680 - -Intangible assets 10 162,164 164,591 - -Investments in subsidiaries 11 - - 27,230 19,203Deferred tax assets 13 1,525 2,971 - -Financial assets 12 363 - - -

180,743 186,242 27,230 19,203

Current assetsInventories 14 19,637 14,821 - -Tax receivable - 162 - -Trade and other receivables 15 4,384 3,841 54,051 41,416Cash and cash equivalents 16 14,282 9,655 3 11Other financial assets 12 - 752 - -

38,303 29,231 54,054 41,427

Total assets 219,046 215,473 81,284 60,630

Current liabilitiesOther interest-bearing loans and borrowings 17 (7,871) (1,027) - -Trade and other payables 18 (18,177) (20,004) (19,730) (14,256)Employee benefits (37) (31) - -Provisions 20 (1,266) (440) - -Tax payable (2,350) (925) - -Other financial liabilities 12 (343) (3,992) - -

(30,044) (26,419) (19,730) (14,256)

Non-current liabilitiesOther interest-bearing loans and borrowings 17 (170,949) (172,258) - -Deferred lease incentives (4,127) (3,720) - -Accrued expenses (6,110) (2,982) (3,108) -Deferred tax liabilities 13 (30,029) (34,191) - -

(211,215) (213,151) (3,108) -

Total liabilities (241,259) (239,570) (22,838) (14,256)

Total net current assets/(liabilities) 8,259 2,812 34,324 27,171Total net non-current assets/(liabilities) (30,472) (26,909) 24,122 19,203

Net assets/(liabilities) (22,213) (24,097) 58,446 46,374

EquityShare capital 1,202 1,194 1,202 1,194Prepaid share capital - 7 - 7Capital contribution reserve 234,709 234,709 234,709 234,709Share premium 15,805 15,805 15,805 15,805Hedging reserve (1,012) (2,361) - -Retained earnings (272,917) (273,451) (193,270) (205,341)

Total equity (22,213) (24,097) 58,446 46,374

The notes on pages 20 to 43 are an integral part of these financial statements.

These financial statements were approved by the board of directors on

22 August 2011 and were signed on its behalf by:

{Statement of Financial Position}as at 28 May 2011

15 / Directors’ Report & Consolidated Financial Statements

SectionTwo:

FinancialStatements

Emily Tate, Finance Director

16 / Directors’ Report & Consolidated Financial Statements

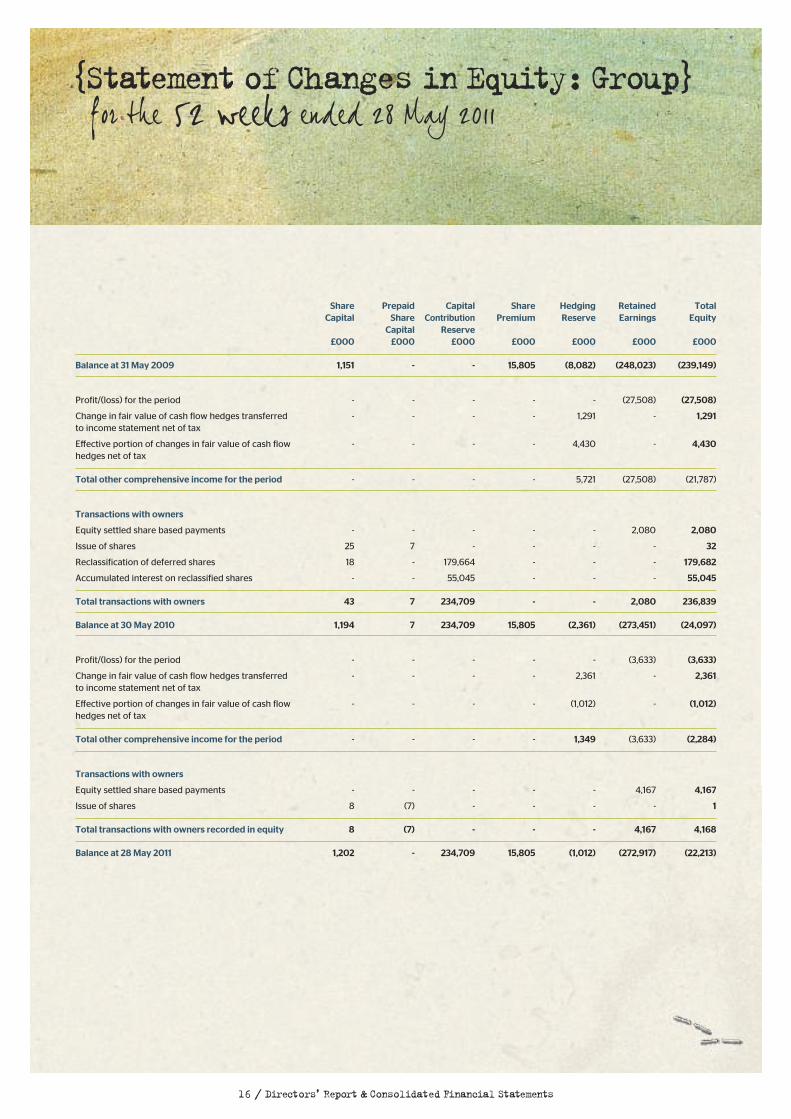

Share Prepaid Capital Share Hedging Retained TotalCapital Share Contribution Premium Reserve Earnings Equity

Capital Reserve£000 £000 £000 £000 £000 £000 £000

Balance at 31 May 2009 1,151 - - 15,805 (8,082) (248,023) (239,149)

Profit/(loss) for the period - - - - - (27,508) (27,508)

Change in fair value of cash flow hedges transferred - - - - 1,291 - 1,291to income statement net of tax

Effective portion of changes in fair value of cash flow - - - - 4,430 - 4,430hedges net of tax

Total other comprehensive income for the period - - - - 5,721 (27,508) (21,787)

Transactions with owners

Equity settled share based payments - - - - - 2,080 2,080

Issue of shares 25 7 - - - - 32

Reclassification of deferred shares 18 - 179,664 - - - 179,682

Accumulated interest on reclassified shares - - 55,045 - - - 55,045

Total transactions with owners 43 7 234,709 - - 2,080 236,839

Balance at 30 May 2010 1,194 7 234,709 15,805 (2,361) (273,451) (24,097)

Profit/(loss) for the period - - - - - (3,633) (3,633)

Change in fair value of cash flow hedges transferred - - - - 2,361 - 2,361to income statement net of tax

Effective portion of changes in fair value of cash flow - - - - (1,012) - (1,012)hedges net of tax

Total other comprehensive income for the period - - - - 1,349 (3,633) (2,284)

Transactions with owners

Equity settled share based payments - - - - - 4,167 4,167

Issue of shares 8 (7) - - - - 1

Total transactions with owners recorded in equity 8 (7) - - - 4,167 4,168

Balance at 28 May 2011 1,202 - 234,709 15,805 (1,012) (272,917) (22,213)

{StatementofChanges in Equity:Group}for the 52 weeks ended 28 May 2011

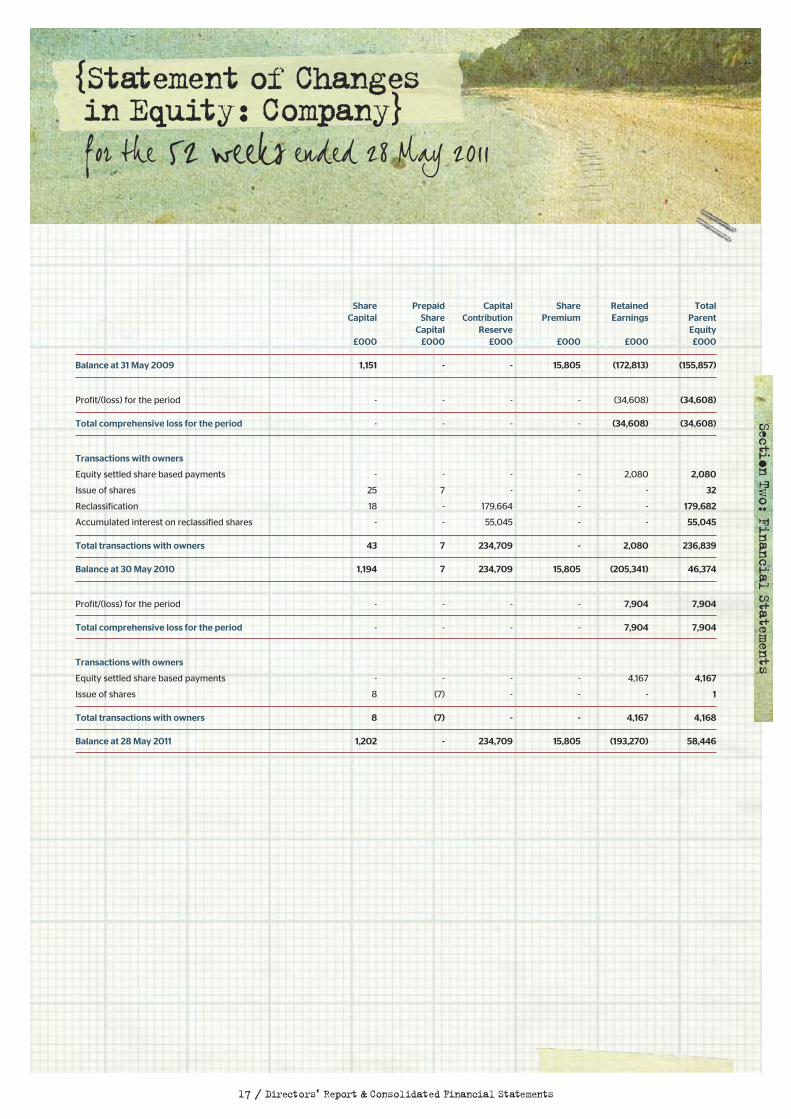

Share Prepaid Capital Share Retained TotalCapital Share Contribution Premium Earnings Parent

Capital Reserve Equity£000 £000 £000 £000 £000 £000

Balance at 31 May 2009 1,151 - - 15,805 (172,813) (155,857)

Profit/(loss) for the period - - - - (34,608) (34,608)

Total comprehensive loss for the period - - - - (34,608) (34,608)

Transactions with owners

Equity settled share based payments - - - - 2,080 2,080

Issue of shares 25 7 - - - 32

Reclassification 18 - 179,664 - - 179,682

Accumulated interest on reclassified shares - - 55,045 - - 55,045

Total transactions with owners 43 7 234,709 - 2,080 236,839

Balance at 30 May 2010 1,194 7 234,709 15,805 (205,341) 46,374

Profit/(loss) for the period - - - - 7,904 7,904

Total comprehensive loss for the period - - - - 7,904 7,904

Transactions with owners

Equity settled share based payments - - - - 4,167 4,167

Issue of shares 8 (7) - - - 1

Total transactions with owners 8 (7) - - 4,167 4,168

Balance at 28 May 2011 1,202 - 234,709 15,805 (193,270) 58,446

{Statementof Changesin Equity:Company}

SectionTwo:

FinancialStatements

for the 52 weeks ended 28 May 2011

17 / Directors’ Report & Consolidated Financial Statements

Note Group Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

Cash flows from operating activities

Profit/(loss) before tax for the year (5,002) (29,711) 12,160 (29,302)

Adjustments for:

Depreciation, amortisation and impairment 9,10,11 9,217 9,490 - 31,719

Equity settled share-based payment expenses 19 4,167 2,080 - -

Financial income 7 (47) (6) (16,499) (20,598)

Financial expense 7 16,138 36,001 4,108 16,536

(Gain)/loss on sale of property, plant and equipment - (5) - -

Cash generated from operations 24,473 17,849 (231) (1,645)

Change in trade and other receivables (748) (226) 102 (12)

Change in inventory (4,816) 1,691 - -

Change in trade and other payables 5,221 1,062 120 1,447

Change in provisions and employee benefits 7 (89) - -

24,137 20,286 (9) (210)

Tax paid (1,004) (750) - -

Net cash from operating activities 23,133 19,536 (9) (210)

Cash flows from investing activities

Proceeds from sale of property, plant and equipment - 43 - -

Interest received 7 47 6 - -

Acquisition of property, plant and equipment 9 (5,390) (8,843) - -

Lease incentives, net of amortisation 1,082 3,741 - -

Acquisition of other intangible assets 10 (9) (34) - -

Net cash from investing activities (4,270) (5,087) - -

Cash flows from financing activities

Proceeds from the issue of share capital 21 1 32 1 32

Proceeds from new loans 17 - 176,427 - -

Acquisition of a hedging instrument 17 (997) - - -

Interest paid (12,206) (18,510) - -

Repayment of borrowings 17 (357) (168,260) - -

Net cash from financing activities (13,559) (10,311) 1 32

Net increase/(decrease) in cash and cash equivalents 5,304 4,138 (8) (178)

Cash and cash equivalents at start of period 8,978 4,840 11 189

Cash and cash equivalents at end of period 16 14,282 8,978 3 11

{Cash Flow Statements}for 52 weeks ended 28 May 2011

18 / Directors’ Report & Consolidated Financial Statements

19 / Directors’ Report & Consolidated Financial Statements

SectionTwo:

FinancialStatements

20 / Directors’ Report & Consolidated Financial Statements

(Forming part of theFinancial Statements)

{Notes to the Financial Statements}

1.Accounting PoliciesFat Face Group Limited (formerly Fat Face World Limited)

(the ‘Company’) is a company incorporated in the UK.

The Group financial statements consolidate those of the

Company and its subsidiaries (together referred to as the

‘Group’). The parent company financial statements present

information about the Company as a separate entity and

not about its Group.

Both the parent company financial statements and the Group

financial statements have been prepared and approved by the

directors in accordance with International Financial Reporting

Standards as adopted by the EU (‘Adopted IFRSs’). On publishing

the parent company financial statements here together with the

Group financial statements, the Company is taking advantage

of the exemption in s408 of the Companies Act 2006 not to

present its individual income statement and related notes

that form a part of these approved financial statements.

The following new standards and amendments to standards

are mandatory for the first time for financial years beginning

on or after 1 January 2010.

• IFRS 3 (revised), ‘Business combinations’, and consequential

amendments to IAS 27, ‘Consolidated and separate financial

statements’, IAS28, ‘Investments in associates’, and IAS 31,

‘Interests in joint ventures’, are effective prospectively to

business combinations when the acquisition date is on

or after the beginning of the first annual reporting period

beginning on or after 1 July 2009. The revised standard

continues to apply the acquisition method to business

combinations but with some significant changes

compared with IFRS 3.

Whilst the revised standard has been applied, there have

been no acquisitions with the Group since 1 July 2009,

and therefore no impact has been reflected within the

statutory accounts.

Adopted IFRS not yet applied The following new standards, amendments and interpretations

have been issued but are not effective for the financial year

and have not been early adopted.

• Revised IAS 24 (revised). ‘Related party disclosures’,

issued in November 2009. It supersedes IAS 24, ‘Related

party disclosures’ issued in 2003. IAS 24 (revised) is

mandatory for periods beginning on or after 1 January

2011. Earlier application in whole or in part is permitted.

The revised standard clarified and simplified the definition

of a related party. The Group will apply the revised

standard for 2011/12 financial statements.

The accounting policies set out below have, unless otherwisestated, been applied consistently to all periods presented inthese consolidated financial statements.

Judgements made by the directors, in the application of theseaccounting policies that have significant effect on the financialstatements and estimates with a significant risk of materialadjustment in the next year are discussed in notes 10, 19 and20, and in the lives of intangible assets as noted below.

Measurement conventionThe financial statements are prepared on an historical costbasis with the exception of derivative financial instrumentswhich are stated at their fair value.

Basis of consolidation – subsidiariesSubsidiaries are entities controlled by the Group. Controlexists when the Group has the power, directly or indirectly,to govern the financial and operating policies of an entity so as to obtain benefits from its activities. In assessing control,potential voting rights that are currently exercisable orconvertible are taken into account. The financial statements of subsidiaries are included in the consolidated financialstatements from the date that control commences until the date that control ceases.

Foreign currencyTransactions in foreign currencies are translated at theforeign exchange rate ruling at the date of the transaction.Monetary assets and liabilities denominated in foreigncurrencies at the balance sheet date are translated at theforeign exchange rate ruling at that date. Foreign exchangedifferences arising on translation are recognised in theincome statement. Non-monetary assets and liabilities thatare measured in terms of historical cost in a foreign currencyare translated using the exchange rate at the date of thetransaction. Non-monetary assets and liabilities denominatedin foreign currencies that are stated at fair value are translatedat foreign exchange rates ruling at the date of transactionthe fair value was determined.

Exchange differences related to qualifying hedges are takendirectly to the translation reserve. They are released into the income statement upon disposal.

Where the Group holds applicable hedged positions, the accounting policy is reported below.

CurrenciesThe Group uses sterling as its presentational and functionalcurrency and all values have been rounded to the nearestthousand unless otherwise stated.

The Company uses sterling as its functional currency.

21 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

Property, plant and equipmentProperty, plant and equipment are stated at cost less

accumulated depreciation and impairment losses.

Where parts of an item of property, plant and equipment

have different useful lives, they are accounted for as

separate items of property, plant and equipment.

Depreciation is provided to write off the cost less the estimated

residual value of tangible fixed assets by equal instalments

over their estimated useful economic lives as follows:

Freehold buildings 2% per annum

Leasehold land and buildings life of lease

Equipment and fittings:

Computer and communications equipment 33%

Shopfit, fixtures & fittings, furniture, mannequins 20%

Plant and machinery 25%

Motor vehicles 25%

Assets in the course of construction are not depreciated.

Assets in the course of construction refers to expenditure on

new stores not yet trading. Ongoing refurbishment projects

in respect of existing stores are charged directly into the

appropriate asset categories.

Intangible assets and goodwillAll business combinations are accounted for by applying

the purchase method. Goodwill represents amounts arising

on acquisition of subsidiaries, associates and jointly controlled

entities being the difference between the cost of the acquisition

and the net fair value of the identifiable assets, liabilities and

contingent liabilities acquired. Identifiable intangibles are

those which can be sold separately or which arise from legal

rights regardless of whether those rights are separable.

Goodwill is stated at cost less any accumulated impairment

losses. Goodwill is not amortised but is tested annually

for impairment.

Other intangible assets that are acquired by the Group are stated

at cost less accumulated amortisation and impairment losses.

Amortisation is charged to the income statement on a

straight-line basis over the estimated useful lives of the assets

unless such lives are indefinite. Intangible assets with an

indefinite useful life and goodwill are systematically tested

for impairment at each balance sheet date. Property leases

are valued against their estimated marketability and an

impairment charge is recorded if appropriate. Other intangible

assets are amortised from the date they are available for use.

The estimated useful lives are as follows:

Trademarks acquired Over the registered life

Trademarks – 2% internally generated value

Customer lists 25%

Licences Over the estimated useful life

Going concernIn adopting the going concern basis for preparing the financialstatements, the directors have considered the principal activitiesas well as the business risks as set out on pages 4 to 5. Basedon the Group’s improved trading performance in the period,cash flow forecasts and projections and notwithstanding thenet liabilities of £22,213,000 (2010: £24,097,000), the Boardcontinues to be satisfied that the Group will be able to operatewithin the level of its facilities for the foreseeable future (seenote 17 in the financial statements for details of the Groupfacilities). For this reason the Group continues to adopt thegoing concern principle in preparing its financial statements.

Non-derivative financial instrumentsNon-derivative financial instruments comprise investmentsin equity and debt securities, cash and cash equivalents, andloans and borrowings.

Investments in debt and equity securitiesInvestments in debt and equity securities held by the Company arestated at the lower of original cost and fair value, with any resultantcumulative impairment losses recognised in profit or loss. Wherethese investments are interest-bearing, interest calculated usingthe effective interest method is recognised in profit or loss.

Cash and cash equivalentsCash and cash equivalents comprise cash balances and calldeposits. Bank overdrafts that are repayable on demand andform an integral part of the Group’s cash management areincluded as a component of cash and cash equivalents for the purpose of the statement of cash flows only.

Interest-bearing borrowingsInterest-bearing borrowings are recognised at face value plusaccumulated unpaid interest costs incurred.

Derivative financial instruments and hedgingDerivative financial instrumentsDerivative financial instruments are recognised at fair value.The gain or loss on re-measurement to fair value is recognisedimmediately in the income statement. However, wherederivatives qualify for hedge accounting, recognition of anyresultant gain or loss depends on the nature of the itembeing hedged (see below).

Cash flow hedgesWhere a derivative financial instrument is designated as a hedgeof the variability in cash flows of a recognised asset or liability, ora highly probable forecast transaction, the effective part of anygain or loss on the derivative financial instrument is recogniseddirectly in the hedging reserve. Any ineffective portion of thehedge is recognised immediately in the income statement.

For cash flow hedges, the associated cumulative gain or loss is removed from equity and recognised in the incomestatement in the same period or periods during which thehedged forecast transaction affects profit or loss.

When a hedging instrument expires or is sold, terminated orexercised, the cumulative gain or loss at that point remains inequity and is recognised in accordance with the above policywhen the transaction occurs. If the hedged transaction is nolonger expected to take place, the cumulative unrealised gainor loss recognised in equity is recognised in the incomestatement immediately.

22 / Directors’ Report & Consolidated Financial Statements

Employee benefitsDefined contribution plansThe Group operates a defined contribution pension plan

under which the Group pays fixed contributions into a

separate entity and will have no legal or constructive obligation

to pay further amounts. Obligations for contributions to

defined contribution pension plans are recognised as an

expense in the income statement as incurred.

Share-based payment transactionsSome employees of Fat Face Limited, an indirect subsidiary,

have been granted shares in the Company. In these consolidated

financial statements the fair value of shares acquired is

recognised as an employee expense with a corresponding

increase in equity. The company financial statements also

record an increase investment in subsidiaries and

corresponding increase in equity.

The fair value is measured at grant date and spread over the

period during which the employees become unconditionally

entitled to the fair value of the shares. The fair value of the

shares acquired is measured using an EBITDA multiple,

taking into account the terms and conditions upon which

the shares were granted. The amount recognised as an

expense is adjusted to reflect the forecast number of shares

expected to be forfeit without reaching full fair value.

During 2009/10, the directors of the company considered that

the fair value of C2 shares issued in the Company could not

be estimated reliably. In accordance with IFRS 2 the group

adopted the intrinsic value methodology for these shares,

whereby the intrinsic value of this share based payment is

remeasured at each reporting date, with changes recognised

in profit or loss until the instrument is settled.

RevenueRevenue represents the invoiced amounts of goods sold

and services provided during the period, stated net of value

added tax.

Revenue arising from the sale of gift vouchers is deferred

and recognised at the point of redemption.

Revenue arising from wholesale and franchise sales is

recognised when invoiced.

ExpensesOperating lease paymentsPayments made under operating leases are recognised in the

income statement on a straight-line basis over the term of the

lease. Lease incentives received are recognised in the income

statement as an integral part of the total lease expense.

Net financing costsNet financing costs comprise interest payable, finance

charges on finance leases, interest receivable on funds

invested, and foreign exchange gains and losses that are

recognised in the income statement.

Interest income and interest payable is recognised in profit

or loss as it accrues, using the effective interest method.

1.Accounting Policies(continued)

Trade and other receivablesTrade and other receivables are recognised at their nominal

amount, less any impairment losses and provisions for bad

and doubtful debts.

InventoriesInventories are stated at the lower of cost and net realisable

value. Cost is based on the weighted average principle and

includes expenditure incurred in acquiring the inventories

and bringing them to their existing location and condition.

As required by IFRS 3, at date of acquisition of subsidiary

entities the fair value of inventory is established by reference

to its present location and condition, which may vary from

historic cost in the acquired entity.

Lease incentivesContributions received from landlords are deemed to be

incentives and as such are recognised as deferred income

and subsequently released over the life of the lease.

Trade and other payablesTrade and other payables are recognised at face value.

Impairment The carrying amounts of the Company’s and Group’s

assets other than inventories and deferred tax assets are

reviewed at each balance sheet date to determine whether

there is any indication of impairment. If any such indication

exists, the asset’s recoverable amount is estimated.

An impairment loss is recognised whenever the carrying

amount of an asset or its cash generating exceeds its

recoverable amount. Impairment losses are recognised

in the income statement.

The results of the impairment review on groups of assets

are disclosed in the relevant notes below.

Interest-bearing borrowingsInterest-bearing borrowings are recognised initially at fair

value less attributable transaction costs. Subsequent to initial

recognition, interest-bearing borrowings are stated at amortised

cost with any difference between cost and redemption value

being recognised in the income statement over the period

of the borrowings on an effective interest basis.

The effective interest basis is the implicit interest rate which,

over the life of an investment or liability, will compound to the

expected final asset or liability value, including all of the costs

and revenues expected from that asset or liability over its life.

Debt instruments issued by Group companies that are

held by other Group companies are reported net in these

Consolidated Financial Statements.

23 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

ProvisionsA provision is recognised in the balance sheet when the

Group has a present legal or constructive obligation as a

result of a past event, that can be reliably measured and

it is probable that an outflow of economic benefits will be

required to settle the obligation.

TaxationTax on the profit or loss for period comprises current and

deferred tax. Tax is recognised in the income statement except

to the extent that it relates to items recognised directly in

equity, in which case it is recognised in equity.

Current tax is the expected tax payable on the taxable income

for the period, using tax rates enacted or substantively enacted

at the balance sheet date, and any adjustment to tax payable

in respect of previous years.

Deferred tax is provided on temporary differences between

the carrying amounts of assets and liabilities for financial

reporting purposes and the amounts used for taxation purposes.

The following temporary differences are not provided for:

• the initial recognition of goodwill;

• the initial recognition of assets or liabilities that affect

neither accounting nor taxable profit other than in a

business combination; and

• differences relating to investments in subsidiaries to

the extent that they will probably not reverse in the

foreseeable future.

The amount of deferred tax provided is based on the expected

manner of realisation or settlement of the carrying amount of

assets and liabilities, using tax rates enacted or substantively

enacted at the balance sheet date.

A deferred tax asset is recognised only to the extent that it is

probable that future taxable profits will be available against

which the asset can be utilised.

2.Revenue2011 2010

£000 £000

Sale of goods 152,466 134,953

Rent receivable 75 142

Royalties 134 264

152,675 135,359

Revenue and other income attributable to geographical markets outside

the United Kingdom amounted to 2.8% (2010: 3.8%).

3.Other OperatingIncome2011 2010

£000 £000

Net gain on disposal of property, plant and equipment - 5

Other trading expenses are shown net of other operating income.

4.Expenses&Auditor’s RemunerationIncluded in the loss for the period are the following non-recurring items:

2011 2010£000 £000

Restructuring costs expensed as incurred 303 1,546

303 1,546

Operating profit is stated afterInventories written down and recognised as an expense in the period 317 293

Operating leases: Land and buildings 18,597 16,977

Operating leases: Other 125 228

Depreciation of tangible assets (net of third party contributions) 6,781 7,205

Amortisation 2,436 2,484

Auditor’s remunerationAudit of these financial statements 7 9

Amounts receivable by auditors and their associates in respect of:

Audit of financial statements of subsidiaries pursuant to legislation 105 70

Other services relating to taxation and sundry matters 17 16

Other services relating to the refinancing - 73

24 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

25 / Directors’ Report & Consolidated Financial Statements

5.Staff Numbers & Costs The contracted number of persons employed by the Group (excluding non-executive directors) during the period, analysed by category, was as follows:

Group GroupNumber of employees 2011 2010

Fat Base (head office) 274 299Stores 1,809 1,698

Total 2,083 1,997

The Company had no employees during the period.

The aggregate payroll costs of these persons were as follows:2011 2010

£000 £000

Wages and salaries 24,701 22,641Social security costs 1,753 1,797Other pension costs 90 128Healthcare costs 27 27

Total before share based payments 26,571 24,593Share based payments (see note 19) 4,167 2,080

Total 30,738 26,673

6.Directors’EmolumentsDirectors’ emoluments on behalf of the group are as follows:

2011 2010£000 £000

Directors’ emoluments 825 824Company contributions to defined contribution pension plans - 11Share based payments 946 1,396

Total 1,771 2,231

The aggregate of emoluments of the highest paid director was £576,042(2010: £375,304), and company pension contributions of nil (2010 £11,143)were made to a defined contribution scheme on their behalf.

Number of Directors 2011 2010

Retirement benefits are accruing to the following number of directors under:Defined contribution benefit plans: - -

The amount accrued in respect of directors’ pensions at 28 May 2011 was nil (2010: nil).

7.FinanceIncome & Expense2011 2010

£000 £000

Bank interest income 19 6Net foreign exchange gain 28 -

Financial income 47 6

Bank interest expense 11,566 19,219Exit fee accrual 3,108 -Other interest payable 1,464 237Net foreign exchange loss - 9

Finance expense 16,138 19,465

Of the Bank interest expenses £5,337,700 relates to cash interest payable on bank debt (2010: £13,950,000) with the remainderrelating to payment in kind (PIK) interest which is added to the loan principal. Other interest payable consists of non-cash intereston loan notes which is added to the loan principal (see note 17).

26 / Directors’ Report & Consolidated Financial Statements

8.TaxationRecognised in income statement

2011 2010Total Total£000 £000

Current tax expenseCurrent year 2,667 -

Adjustments for prior years (405) -

Total current tax 2,262 -

Deferred tax expenseCurrent year (1,325) (2,704)

Adjustments in respect of previous periods (11) 501

Deferred tax rate change (2,295) -

Total deferred tax (3,631) (2,203)

Total tax in income statement (1,369) (2,203)

Reconciliation of effective tax rate2011 2010

£000 £000

Loss before tax (5,002) (29,711)

Tax using the UK corporation tax rate of 27.833% (2010: 28%) (1,392) (8,319)

Non-deductible expenses 2,675 5,615

Under / (over) provided in prior years (416) 501

Impact of rate change on brought forward balance (2,295) -

Rate difference on deferred tax 59 -

Total tax in income statement (1,369) (2,203)

Tax recognised directly in equity2011 2010

£000 £000

Deferred tax recognised directly in equity 911 2,225

On 23 March 2011 the Chancellor announced the reduction in the main rate of UK corporation tax to 26 per cent with effect from

1 April 2011 and a further reduction to 25 per cent with effect from 1 April 2012. These changes became substantively enacted on

29 March 2011 and 5 July 2011 respectively and therefore the effect of these rate reductions creates a reduction in the deferred

tax liability which has been included in the figures above.

27 / Directors’ Report & Consolidated Financial Statements

9.Property, Plant& Equipment - GroupFreehold land Assets in Short Equipment Motor Totaland buildings the course of leasehold land and fixtures vehicles

construction and buildings£000 £000 £000 £000 £000 £000

CostBalance at 31 May 2009 124 115 2,178 28,741 36 31,194

Additions - 362 841 7,640 - 8,843

Transfers between categories - (115) - 115 - -

Disposals - - (8) (211) - (219)

Balance at 29 May 2010 124 362 3,011 36,285 36 39,818

Balance at 30 May 2010 124 362 3,011 36,285 36 39,818

Additions - 257 337 4,796 - 5,390

Transfers between categories - (362) 107 255 - -

Disposals - - (44) (526) - (570)

Balance at 28 May 2011 124 257 3,411 40,810 36 44,638

Depreciation and impairment Balance at 31 May 2009 (6) - (696) (13,378) (23) (14,103)

Depreciation charge for the period (3) - (207) (6,998) (8) (7,216)

Disposals - - 8 173 - 181

Balance at 29 May 2010 (9) - (895) (20,203) (31) (21,138)

Balance at 30 May 2010 (9) - (895) (20,203) (31) (21,138)

Depreciation charge for the period (3) - (45) (7,184) (5) (7,237)

Disposals - - 15 413 - 428

Balance at 28 May 2011 (12) - (925) (26,974) (36) 27,947

Net book valueAt 29 May 2010 115 362 2,116 16,082 5 18,680

At 28 May 2011 112 257 2,486 13,836 - 16,691

The depreciation and impairment charge is recognised in the following line items in the income statement together with the

amortisation of lease incentives held on the balance sheet and amortised over the life of the lease:

2011 2010£000 £000

Depreciation and amortisation of tangible property, plant and equipmentTangible assets 7,237 7,216

Unwinding of deferred lease incentives (456) (249)

Depreciation and amortisation 6,781 6,967 SectionThree:

Notes

28 / Directors’ Report & Consolidated Financial Statements

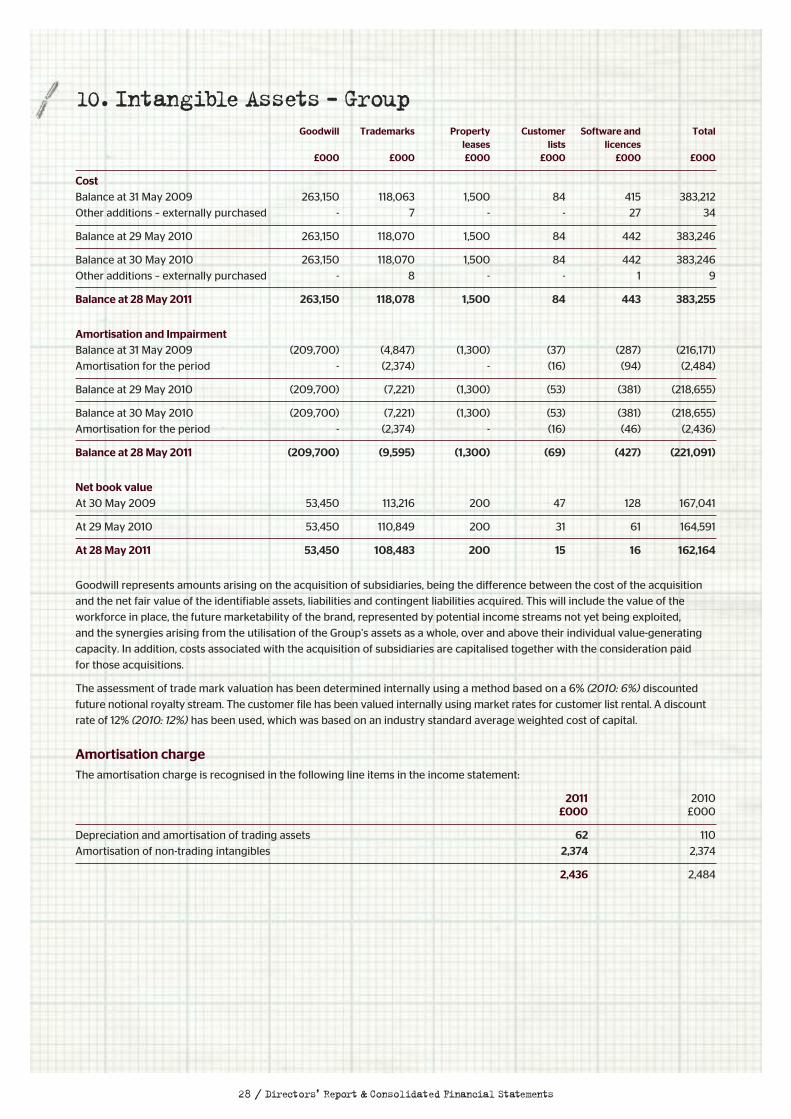

10.Intangible Assets - GroupGoodwill Trademarks Property Customer Software and Total

leases lists licences£000 £000 £000 £000 £000 £000

CostBalance at 31 May 2009 263,150 118,063 1,500 84 415 383,212

Other additions – externally purchased - 7 - - 27 34

Balance at 29 May 2010 263,150 118,070 1,500 84 442 383,246

Balance at 30 May 2010 263,150 118,070 1,500 84 442 383,246

Other additions – externally purchased - 8 - - 1 9

Balance at 28 May 2011 263,150 118,078 1,500 84 443 383,255

Amortisation and ImpairmentBalance at 31 May 2009 (209,700) (4,847) (1,300) (37) (287) (216,171)

Amortisation for the period - (2,374) - (16) (94) (2,484)

Balance at 29 May 2010 (209,700) (7,221) (1,300) (53) (381) (218,655)

Balance at 30 May 2010 (209,700) (7,221) (1,300) (53) (381) (218,655)

Amortisation for the period - (2,374) - (16) (46) (2,436)

Balance at 28 May 2011 (209,700) (9,595) (1,300) (69) (427) (221,091)

Net book valueAt 30 May 2009 53,450 113,216 200 47 128 167,041

At 29 May 2010 53,450 110,849 200 31 61 164,591

At 28 May 2011 53,450 108,483 200 15 16 162,164

Goodwill represents amounts arising on the acquisition of subsidiaries, being the difference between the cost of the acquisition

and the net fair value of the identifiable assets, liabilities and contingent liabilities acquired. This will include the value of the

workforce in place, the future marketability of the brand, represented by potential income streams not yet being exploited,

and the synergies arising from the utilisation of the Group’s assets as a whole, over and above their individual value-generating

capacity. In addition, costs associated with the acquisition of subsidiaries are capitalised together with the consideration paid

for those acquisitions.

The assessment of trade mark valuation has been determined internally using a method based on a 6% (2010: 6%) discounted

future notional royalty stream. The customer file has been valued internally using market rates for customer list rental. A discount

rate of 12% (2010: 12%) has been used, which was based on an industry standard average weighted cost of capital.

Amortisation chargeThe amortisation charge is recognised in the following line items in the income statement:

2011 2010£000 £000

Depreciation and amortisation of trading assets 62 110

Amortisation of non-trading intangibles 2,374 2,374

2,436 2,484

29 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

Impairment testingThe Group’s management has reviewed the carrying value

of goodwill for possible impairment based on the group of

cash generating units which comprise the lowest level at

which goodwill is monitored. This is equivalent to the business

as a whole. As in previous years, the Group’s management

has determined that the income approach (which is equivalent

to utilising the ‘value in use’ valuation technique) is the most

appropriate method for valuing the business at the current

stage of its development in the present market. The Group’s

management does not believe an impairment of the

goodwill in the business is required (2010: nil).

Income stream forecasts The key revenue driver for the business will continue to be

the development of the retail portfolio. The directors believe

that there is significant capacity for growth through improving

sales densities, relocating and refitting stores in successful

markets and expanding the portfolio. However, longer term

forecasts are inherently less reliable and the impairment

assessment consequently includes very prudent growth

assumptions beyond 2015. No material overseas expansion

of the brand has been included.

Cost growth forecasts Costs are assumed to grow at a reasonable rate to support

the continued expansion.

Discount RateThe Group’s weighted average cost of capital (WACC) as

adjusted for a market based interest rate and capital structure

has been used as a discount rate in the calculation. WACC –

what stakeholders could reasonably expect as an average

return for their investment – has been estimated at 14%

(2010: 14%).

This calculation has been built up by comparing the equity

returns expected from a range of similar companies, both UK

and overseas, and adjusting this for specific Group factors

such as debt structure, company size, and the effects of a

private, rather than public, equity structure.

The equivalent pre-tax discount rate is also 14% (2010: 14%).

SensitivityThe key assumptions as noted above are revenue

generation and the WACC used. A decrease in revenue in

each year of 1% would reduce the valuation of the business

by approximately £13m. An increase in the WACC from

14% to 15% would reduce the valuation of the business

by approximately £22m.

30 / Directors’ Report & Consolidated Financial Statements

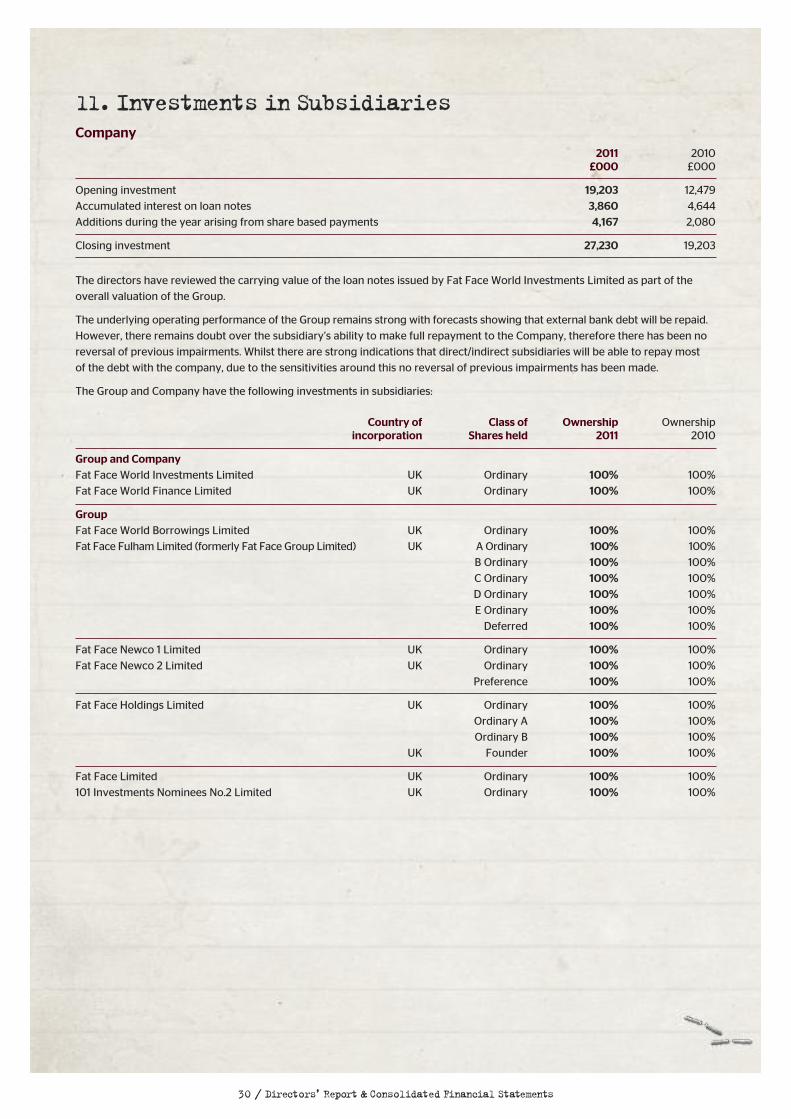

11.Investments in SubsidiariesCompany

2011 2010£000 £000

Opening investment 19,203 12,479

Accumulated interest on loan notes 3,860 4,644

Additions during the year arising from share based payments 4,167 2,080

Closing investment 27,230 19,203

The directors have reviewed the carrying value of the loan notes issued by Fat Face World Investments Limited as part of the

overall valuation of the Group.

The underlying operating performance of the Group remains strong with forecasts showing that external bank debt will be repaid.

However, there remains doubt over the subsidiary’s ability to make full repayment to the Company, therefore there has been no

reversal of previous impairments. Whilst there are strong indications that direct/indirect subsidiaries will be able to repay most

of the debt with the company, due to the sensitivities around this no reversal of previous impairments has been made.

The Group and Company have the following investments in subsidiaries:

Country of Class of Ownership Ownershipincorporation Shares held 2011 2010

Group and CompanyFat Face World Investments Limited UK Ordinary 100% 100%

Fat Face World Finance Limited UK Ordinary 100% 100%

GroupFat Face World Borrowings Limited UK Ordinary 100% 100%

Fat Face Fulham Limited (formerly Fat Face Group Limited) UK A Ordinary 100% 100%

B Ordinary 100% 100%

C Ordinary 100% 100%

D Ordinary 100% 100%

E Ordinary 100% 100%

Deferred 100% 100%

Fat Face Newco 1 Limited UK Ordinary 100% 100%

Fat Face Newco 2 Limited UK Ordinary 100% 100%

Preference 100% 100%

Fat Face Holdings Limited UK Ordinary 100% 100%

Ordinary A 100% 100%

Ordinary B 100% 100%

UK Founder 100% 100%

Fat Face Limited UK Ordinary 100% 100%

101 Investments Nominees No.2 Limited UK Ordinary 100% 100%

31 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

12.Other Financial Assets & LiabilitiesGroup Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

CurrentFair value of exchange rate hedge (343) 752 - -Fair value of interest rate hedge 363 (3,992) - -

For details on valuation methodology adopted, see note 22.

13.Deferred Tax Assets & Liabilities - GroupRecognised deferred tax assets and liabilities Deferred tax assets and liabilities are attributable to the following:

Assets Assets Liabilities Liabilities2011 2010 2011 2010

£000 £000 £000 £000

Property, plant and equipment (1,332) (1,589) - 607Intangible assets - - 28,254 31,144Financial assets - - 5 211Accruals (193) (131) - -Provisions and employee benefits - (134) - -Discounted debt - - 1,770 2,229Financial liabilities - (1,117) - -

Tax (assets) / liabilities (1,525) (2,971) 30,029 34,191Net of tax (assets) (1,525) (2,971)

Net tax liabilities 28,504 31,220

Movement in deferred tax during the period

1 June 2009 Recognised Recognised 29 May 2010in income in equity

£000 £000 £000 £000

Property, plant and equipment 248 (1,230) - (982)Intangible assets 31,810 (666) - 31,144Financial assets - - 211 211Accruals (190) 59 - (131)Provisions and employee benefits (158) 24 - (134)Discounted debt 2,619 (390) - 2,229Financial liabilities (3,131) - 2,014 (1,117)

31,198 (2,203) 2,225 31,220

30 May 2010 Recognised Recognised 28 May 2011in income in equity

£000 £000 £000 £000

Property, plant and equipment (982) (350) - (1,332)Intangible assets 31,144 (2,890) - 28,254Financial assets 211 - (211) -Accruals (131) (62) - (193)Provisions and employee benefits (134) 134 - -Discounted debt 2,229 (459) - 1,770Financial liabilities (1,117) - 1,122 5

31,220 (3,627) 911 28,504

32 / Directors’ Report & Consolidated Financial Statements

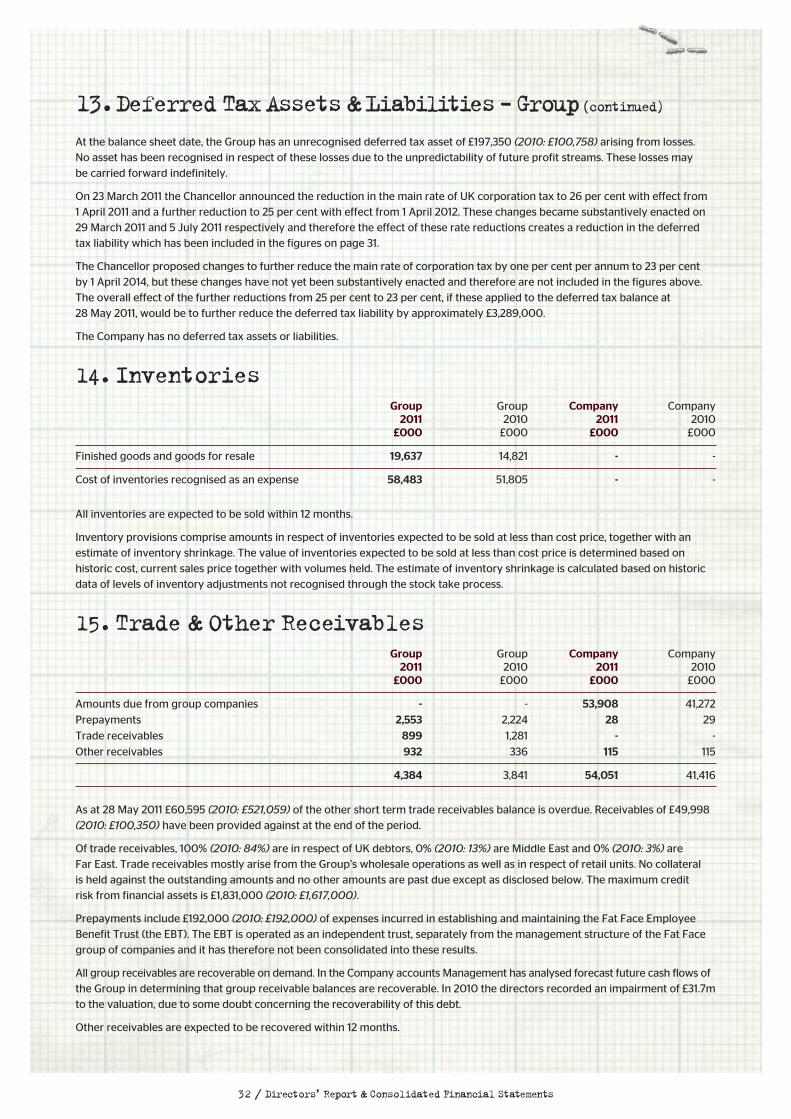

13.DeferredTaxAssets&Liabilities -Group(continued)

At the balance sheet date, the Group has an unrecognised deferred tax asset of £197,350 (2010: £100,758) arising from losses. No asset has been recognised in respect of these losses due to the unpredictability of future profit streams. These losses may be carried forward indefinitely.

On 23 March 2011 the Chancellor announced the reduction in the main rate of UK corporation tax to 26 per cent with effect from 1 April 2011 and a further reduction to 25 per cent with effect from 1 April 2012. These changes became substantively enacted on29 March 2011 and 5 July 2011 respectively and therefore the effect of these rate reductions creates a reduction in the deferredtax liability which has been included in the figures on page 31.

The Chancellor proposed changes to further reduce the main rate of corporation tax by one per cent per annum to 23 per cent by 1 April 2014, but these changes have not yet been substantively enacted and therefore are not included in the figures above.The overall effect of the further reductions from 25 per cent to 23 per cent, if these applied to the deferred tax balance at 28 May 2011, would be to further reduce the deferred tax liability by approximately £3,289,000.

The Company has no deferred tax assets or liabilities.

14.InventoriesGroup Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

Finished goods and goods for resale 19,637 14,821 - -

Cost of inventories recognised as an expense 58,483 51,805 - -

All inventories are expected to be sold within 12 months.

Inventory provisions comprise amounts in respect of inventories expected to be sold at less than cost price, together with anestimate of inventory shrinkage. The value of inventories expected to be sold at less than cost price is determined based onhistoric cost, current sales price together with volumes held. The estimate of inventory shrinkage is calculated based on historicdata of levels of inventory adjustments not recognised through the stock take process.

15.Trade & Other ReceivablesGroup Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

Amounts due from group companies - - 53,908 41,272

Prepayments 2,553 2,224 28 29

Trade receivables 899 1,281 - -

Other receivables 932 336 115 115

4,384 3,841 54,051 41,416

As at 28 May 2011 £60,595 (2010: £521,059) of the other short term trade receivables balance is overdue. Receivables of £49,998 (2010: £100,350) have been provided against at the end of the period.

Of trade receivables, 100% (2010: 84%) are in respect of UK debtors, 0% (2010: 13%) are Middle East and 0% (2010: 3%) are Far East. Trade receivables mostly arise from the Group’s wholesale operations as well as in respect of retail units. No collateral is held against the outstanding amounts and no other amounts are past due except as disclosed below. The maximum credit risk from financial assets is £1,831,000 (2010: £1,617,000).

Prepayments include £192,000 (2010: £192,000) of expenses incurred in establishing and maintaining the Fat Face EmployeeBenefit Trust (the EBT). The EBT is operated as an independent trust, separately from the management structure of the Fat Facegroup of companies and it has therefore not been consolidated into these results.

All group receivables are recoverable on demand. In the Company accounts Management has analysed forecast future cash flows ofthe Group in determining that group receivable balances are recoverable. In 2010 the directors recorded an impairment of £31.7mto the valuation, due to some doubt concerning the recoverability of this debt.

Other receivables are expected to be recovered within 12 months.

33 / Directors’ Report & Consolidated Financial Statements

SectionThree:

Notes

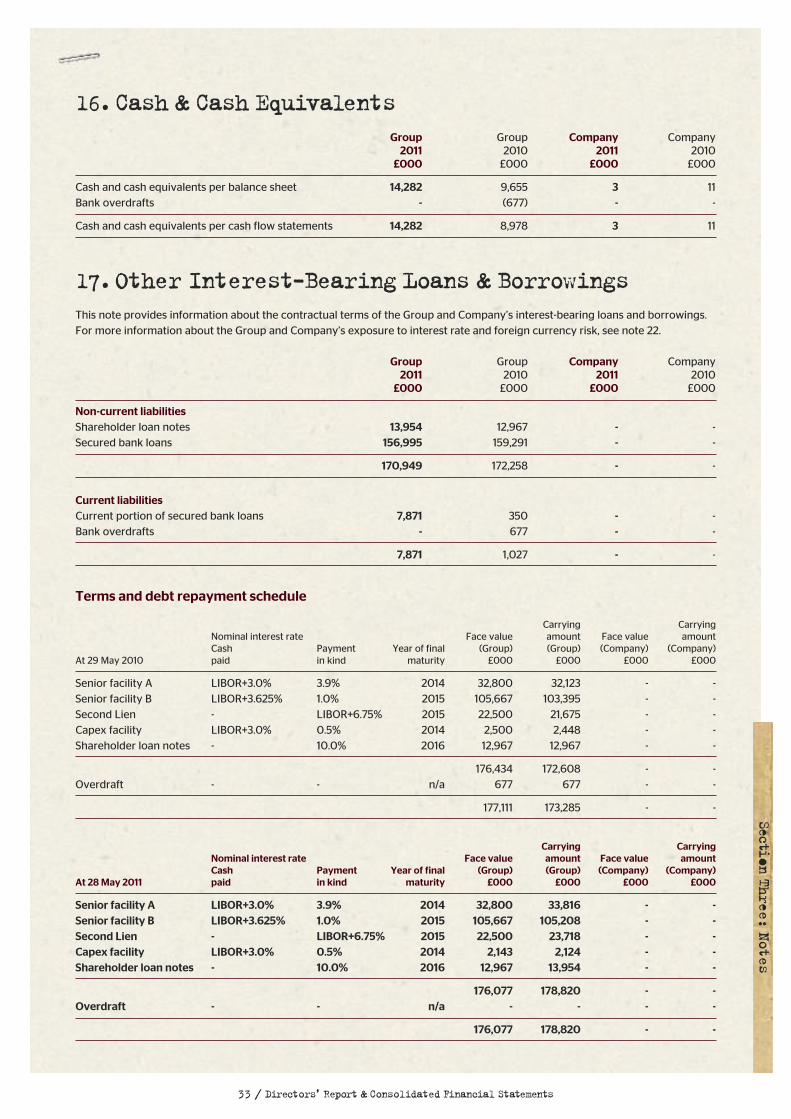

16.Cash & Cash EquivalentsGroup Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

Cash and cash equivalents per balance sheet 14,282 9,655 3 11Bank overdrafts - (677) - -

Cash and cash equivalents per cash flow statements 14,282 8,978 3 11

17.Other Interest-Bearing Loans & BorrowingsThis note provides information about the contractual terms of the Group and Company’s interest-bearing loans and borrowings.For more information about the Group and Company’s exposure to interest rate and foreign currency risk, see note 22.

Group Group Company Company2011 2010 2011 2010

£000 £000 £000 £000

Non-current liabilitiesShareholder loan notes 13,954 12,967 - -Secured bank loans 156,995 159,291 - -

170,949 172,258 - -

Current liabilitiesCurrent portion of secured bank loans 7,871 350 - -Bank overdrafts - 677 - -

7,871 1,027 - -

Terms and debt repayment schedule

Carrying CarryingNominal interest rate Face value amount Face value amountCash Payment Year of final (Group) (Group) (Company) (Company)

At 29 May 2010 paid in kind maturity £000 £000 £000 £000

Senior facility A LIBOR+3.0% 3.9% 2014 32,800 32,123 - -Senior facility B LIBOR+3.625% 1.0% 2015 105,667 103,395 - -Second Lien - LIBOR+6.75% 2015 22,500 21,675 - -Capex facility LIBOR+3.0% 0.5% 2014 2,500 2,448 - -Shareholder loan notes - 10.0% 2016 12,967 12,967 - -

176,434 172,608 - -Overdraft - - n/a 677 677 - -

177,111 173,285 - -

Carrying CarryingNominal interest rate Face value amount Face value amountCash Payment Year of final (Group) (Group) (Company) (Company)

At 28 May 2011 paid in kind maturity £000 £000 £000 £000

Senior facility A LIBOR+3.0% 3.9% 2014 32,800 33,816 - -Senior facility B LIBOR+3.625% 1.0% 2015 105,667 105,208 - -Second Lien - LIBOR+6.75% 2015 22,500 23,718 - -Capex facility LIBOR+3.0% 0.5% 2014 2,143 2,124 - -Shareholder loan notes - 10.0% 2016 12,967 13,954 - -

176,077 178,820 - -Overdraft - - n/a - - - -

176,077 178,820 - -

17.Other Interest-BearingLoans&Borrowings(continued)

The Group’s banking facilities include a £20m revolving credit facility from which the capex facility loan above is drawn. A repayment

of £357k was made in May 2011 on the capex facility. Of the remaining £17.5m, Fat Face Limited, an indirect subsidiary of the Company,

has drawn £10m under an Ancillary Facilities agreement. This provides overdraft, guarantee, and supplier credit facilities for the

day-to-day operations of the Group. The Group has paid a non-utilisation fee of 1% on the remaining £7.5m revolving credit facility

plus any unutilised portion of the Ancillary Facilities Agreement.

The Group’s banking facilities are subject to EBITDA, interest and cash cover covenants typical for borrowings of this nature.

All of the direct and indirect subsidiaries of the Company are obligors and joint guarantors of the Group’s banking facilities.