dma insight: marketer email tracker 2017

TRANSCRIPT

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20161

ContentsIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

Sponsor’s perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Council’s perspective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Executive summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

1. Importance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

2. Objective . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

3. Customer contact . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

4. Usage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .14

5. ROI. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

6. Email effectiveness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19Unsubscribes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

7. Expectations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

8. Marketing automation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27

Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

About dotmailer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

About the DMA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Copyright and disclaimer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20162

The Marketer email tracker 2017 closes our series of email research for this year and there are reasons for both optimism and concern in the results.

Marketers believe that email has never been so important, and the nature of email is changing, with ‘content’ rising in importance every year, and we expect this trend to continue.

They also agree with customers that trust is the most important factor in persuading people to sign up to hear from a brand in the first place. This is very encouraging.

Unfortunately, while marketers are doing the right things in getting consumers to sign up, once they have signed up then they don’t take quite so much care.

When looking at consumer perceptions of email, customers worry about the relevance and volume of email in their inboxes, and marketers are not addressing these concerns.

Email volumes are increasing and relevance remains a ‘known unknown’ for many marketers, with fewer than one in 10 marketers (9%) saying all their emails are relevant to their customers and more worryingly, only two in five (42%) say that at best ‘some’ of their emails are relevant to consumers.

If email is to continue to grow and thrive as a channel, then marketers need to heed consumer concerns and take care to give them what they want.

Rachel Aldighieri MD at the DMA

Introduction

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20163

I have been in email marketing for over 17 years and I still have the same conversations with clients today that I had 17 years ago. Batch and blast is not best practice. The best practice is to refine your targeting down to segments of one if possible. As a consultant however, I also have to work with clients to be practical. In many cases, the cost of doing this level of targeting – from creating all of the versions of the content, processing the data and the campaign management overhead – can outweigh the incremental lift in sales. In other words, it costs more than it makes and so should not be done to that level.

That said, this report – in combination with the Consumer email tracker 2016 – paints a worrying picture. Yes, both marketers and consumers love email, as evidenced by the £30:£1 ROI. Because email works so well, it is probably not surprising that marketers reported sending an average of over 4 emails per month. Yet at the same time, consumers are saying they get over 21 brand emails per week and that most of these are untargeted and irrelevant. More worrying is that 42% of marketers agree that some or none of their email is actually relevant to the people they’re sending it to.

The warning signs are there. More than 50% of consumers have reported that they have at least considered deleting their email account to control the flow of marketing emails that they receive. As email marketers, we have a responsibility to our customers, to ourselves and to our businesses to keep our channel not just viable but thriving long into the future.

Skip Fidura Client services director at dotmailer & Chair of the DMA’s Responsible marketing committee

Sponsor’s perspective

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20164

Email remains the bedrock of digital marketing. It’s favoured by consumers and 95% of marketers agree that it continues to retain a very important place within marketing. Therefore, it’s crucial to understand how marketers use email effectively and how this correlates to consumer’s expectations. Reading this report alongside the DMA’s Consumer email tracker 2016 report provides invaluable insight into the correlations and differences of perceptions between both marketers and consumers.

With the increasing buzz surrounding the GDPR, it’s not a surprise to discover that marketers are now starting to assess whether the communications they send subscribers are relevant. This report highlights that less than one in 10 marketers are sending relevant emails all the time. I’m pleased that, firstly, marketers are admitting this because consumers have been telling us this for a couple of years and, secondly, no-one wants a guilty conscious. We’ve all been saying for years that email marketing should be relevant to the subscriber…now marketers are telling us they too want to be sending relevant emails and move away from the batch and blast mentality.

Of course, this doesn’t come without its challenges; the biggest for marketers are a ‘lack of strategy’ closely followed by a ‘lack of data’ and ‘data silos’.

However, for me the key insight from this report is that 78% of marketers believe there should be a contact rule to not over communicate with subscribers. This highlights more than ever that email marketers are beginning to think more about the subscriber and starting to be conscious of not over emailing.

Jenna Tiffany Founder & Strategy Director at Let’sTalk Strategy & member of the DMA Email council’s Research hub

Council’s perspective

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20165

Email remains ‘important’ or ‘very important’ for the majority (95%) of marketers, but fewer than one in 10 (9%) say all their emails are relevant to their customers. More than two in five (42%) say that at best ‘some’ of their emails are relevant to consumers, which demonstrates a disconnect between what marketers say they want to achieve and what they admit they produce.

Average ROI for email has increased slightly year-on-year, with average returns of £30.01, which is up from £29.64 last year. However, there is a significant difference between junior and senior marketers in whether they can calculate this ROI. Many senior marketers and managers say they can calculate the ROI from their campaigns, but the more junior members say they cannot.

The biggest concerns for marketers are ‘lack of strategy’ (28%), a 5% increase compared to last year, followed by ‘lack of data’ (27%) and ‘data siloes’ (26%). ‘Limited internal resources’, the top choice last year on 42%, and ‘lack of content’ were each problems for a quarter (25%) of respondents.

‘Lack of content’ has increased as an issue for marketers consistently since 2012, now the joint fourth biggest problem identified. Marketers need content to feed their campaigns, and a lack of content is only likely to grow as a problem while email remains so important for marketers. B2C marketers in particular say ‘content’ is the leading driver of effectiveness, although this is also in sharp contrast to what consumers say they want.

Almost one-third of marketers (31%) use an in-house solution for their email, meaning they are more likely to miss out on new technologies and techniques in their campaigns.

Marketers may not test their emails consistently. While fewer marketers say they do not conduct email testing, down from 17% last year to 8% this year, there was an increase in those who said they had ‘no competence’ in email testing, up from 5% to 14%. 40% of respondents said fewer than a quarter of emails included a test. B2C marketers are more likely to test their emails. This is probably because they have larger lists.

Marketers and consumers agree that ‘trust’ is the leading factor for persuading consumers to sign up to brand emails.B2C marketers expect their budgets to increase next year in tandem with costs, while B2B marketers believe that budgets and costs are to remain the same.

Marketers have found significant barriers to automation, with those using typical automation triggers declining significantly compared to last year. However, there is some evidence that B2B marketers are better disposed to automation than B2C marketers, most likely due to well defined funnels and budget cycles.

Executive summary

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20166

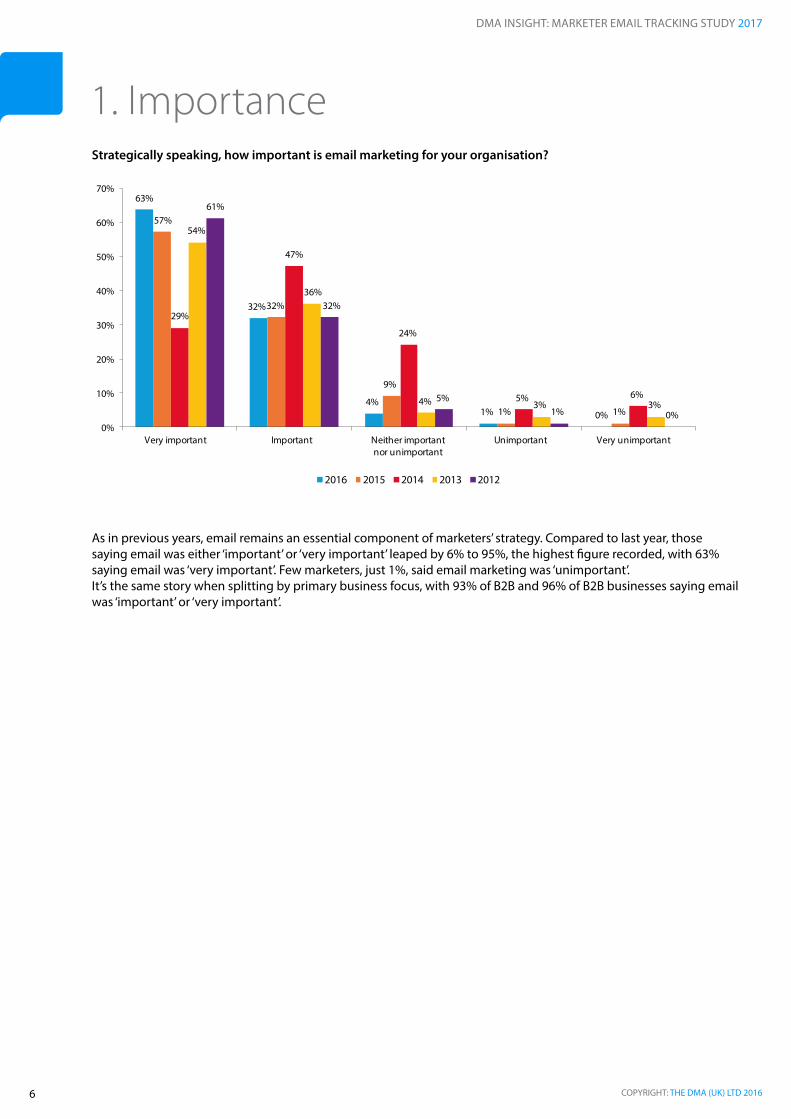

Strategically speaking, how important is email marketing for your organisation?

As in previous years, email remains an essential component of marketers’ strategy. Compared to last year, those saying email was either ‘important’ or ‘very important’ leaped by 6% to 95%, the highest figure recorded, with 63% saying email was ‘very important’. Few marketers, just 1%, said email marketing was ‘unimportant’.It’s the same story when splitting by primary business focus, with 93% of B2B and 96% of B2B businesses saying email was ‘important’ or ‘very important’.

1. Importance

63%

32%

4%1% 0%

57%

32%

9%

1% 1%

29%

47%

24%

5% 6%

54%

36%

4% 3% 3%

61%

32%

5%1% 0%

0%

10%

20%

30%

40%

50%

60%

70%

Very important Important Neither important nor unimportant

Unimportant Very unimportant

2016 2015 2014 2013 2012

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

7

What are the most significant challenges to successfully executing your email marketing programmes? You can select up to three choices

In 2016 the biggest single challenge to marketers is ‘lack of strategy’, a problem for almost three in 10 (28%) and a 5% increase compared to last year. The next most popular choices are ‘lack of data’ for 27%, and ‘data silos’ for 26%. ‘Limited internal resources’ was the top choice last year on 42% but has this year dropped to 25%, the same level as ‘lack of content’.

These last two statistics demonstrate something else. While ‘limited internal resource’ has plummeted as a concern since 2012, dropping consistently from 54% to 25%, ‘lack of content’ has risen every year from 13% to the same proportion.

23%28%

Lack of strategy

27%36%

26%26%

27%Lack of data

(speci�cally email addresses)

8%26%

Data siloes

13%15%

19%21%

25%

Lack of content

54%45%

34%42%

25%

Limited internal resource

3%8%

29%22%

19%

Data degradation

30%27%

18%21%

15%

Ine�cient internal processes

10%16%

11%14%

15%

Poor interdepartmental communication

13%10%

16%9%

15%

Outdated ESP technology

28%28%

15%11%

13%

Outdated in-house technology

38%17%

14%17%

12%

Limited budget

21%5%

11%4%

10%

Lack of senior support

2%7%

Choosing latest ratherthan e�ective channels

0%0%

9%4%4%

Other

0%0%

3%6%

2%

None

0% 10% 20% 30% 40% 50% 60%

2016 2015 2014 2013 2012

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

8

Alternatively, could the top concerns be getting worse, meaning that problems like ‘lack of resource’ remain, but have been displaced by other concerns?

We have reached the tipping point between email as a ‘nice to have’ and departments struggling to keep up, to email as an essential resource, with more manpower but without the content to make email as good as it could be.

The next phase in the development of email should be investing in copywriters, journalists or designers to feed email with the content it desperately needs.

Last year we noted that when taken together, data was the biggest single concern for those using email for marketing. The same is true this year, with ‘lack of data’, data silos’ and ‘data degradation’ problems for a total of 59%, data remains the single biggest problem, and may reflect increasing concerns about how to maintain data as we move to the GDPR in 2018.

Who do you involve in your email marketing?

With so many new categories compared to last year, it’s difficult to track trends, but it is significant that those choosing ‘CMO’ has almost halved, falling to 11% from 19% in 2015. Despite the importance of email indicated at the start of the survey, this could indicate its decreasing importance to top marketers.

Alternatively, this may be for purely pragmatic reasons, as the CMO will be unlikely to have the time to micromanage, email production, too demanding of time and resource for CMO involvement to work effectively.

57%

48% 46% 44% 42%

34%

11%

38%

48%

58%

19%

0%

10%

20%

30%

40%

50%

60%

70%

2016 2015

Marketing m

anager

CRM/database manager

Marketing Dire

ctor

Marketingexecutiv

e

Senior marketin

g manager

Online/m

ultimedia desig

nerCMO

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 20169

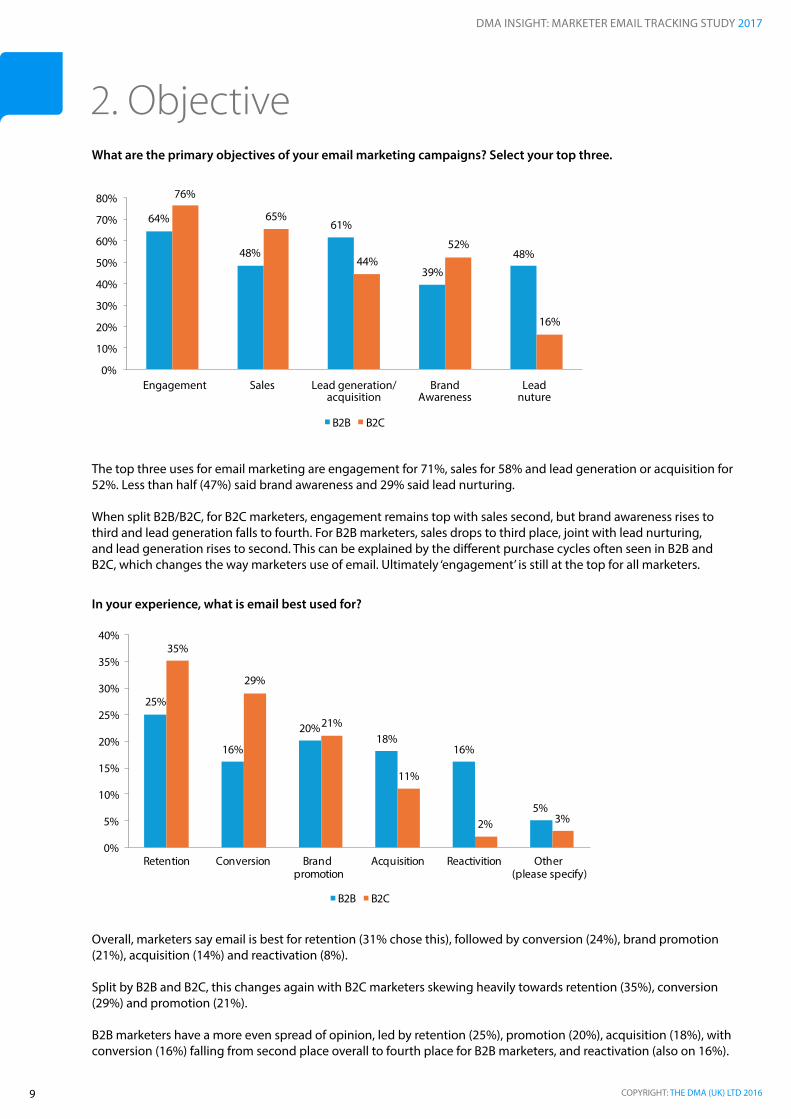

What are the primary objectives of your email marketing campaigns? Select your top three.

The top three uses for email marketing are engagement for 71%, sales for 58% and lead generation or acquisition for 52%. Less than half (47%) said brand awareness and 29% said lead nurturing.

When split B2B/B2C, for B2C marketers, engagement remains top with sales second, but brand awareness rises to third and lead generation falls to fourth. For B2B marketers, sales drops to third place, joint with lead nurturing, and lead generation rises to second. This can be explained by the different purchase cycles often seen in B2B and B2C, which changes the way marketers use of email. Ultimately ‘engagement’ is still at the top for all marketers.

In your experience, what is email best used for?

Overall, marketers say email is best for retention (31% chose this), followed by conversion (24%), brand promotion (21%), acquisition (14%) and reactivation (8%).

Split by B2B and B2C, this changes again with B2C marketers skewing heavily towards retention (35%), conversion (29%) and promotion (21%).

B2B marketers have a more even spread of opinion, led by retention (25%), promotion (20%), acquisition (18%), with conversion (16%) falling from second place overall to fourth place for B2B marketers, and reactivation (also on 16%).

2. Objective

64%

48%

61%

39%

48%

76%

65%

44%52%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

B2B B2C

Engagement Sales Lead generation/acquisition

BrandAwareness

Leadnuture

25%

16%

20%18%

16%

5%

35%

29%

21%

11%

2% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Retention Conversion Brand promotion

Acquisition Reactivition Other (please specify)

B2B B2C

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

10

How would you rate your company’s overall level of competence in email marketing? Note. Definitions have changed this year.

This year we have given these the different categories more detailed, specific definitions. This has perhaps accelerated the decline in those who say they are ‘advanced’ at email, down to 9% from 17% last year. Those who say they are ‘intermediate’ or ‘good’ both declined to 43% from 47%, and to 21% from 27% respectively. The big change is in those reporting they have ‘basic’ skills, increasing from 7% to 24% compared to last year.

Clearly in the past, email marketers have overestimated their skills but recent developments in fields such as AI may make marketers feel left behind.

How would you rate your company’s overall level of competence in email testing?

For email testing there is a sharp decline in those who say they do not conduct email testing, down from 17% to 8%, but a corresponding increase for those who claim to have ‘no competence’, up from 5% to 14%. Four in 10 (40%) of respondents said fewer than a quarter of emails included a test. This is likely to be down to time or resource constraints, or even a narrow focus on production over wider marketing aims.

3%

24%

43%

21%

9%

2%

7%

47%

27%

17%

3%

12%

49%

29%

0%

22%

38%

32%

2%

20%

33%

39%

0%

10%

20%

30%

40%

50%

60%

None at all Basic Intermediate Good Advanced

2016 2015 2014 2013 2012

8%

14%

44%

27%

7%

17%

5%

47%

25%

6%

13%

7%

18%

48%

13%

19%

9%

21%

36%

19%

0%

10%

20%

30%

40%

50%

60%

We don't conduct email testing

No competence at all Basic Intermediate Advanced

2016 2015 2014 2013

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

11

How often does your organisation conduct email testing?

When split by B2B/B2C, we find that B2C marketers test significantly more emails, with 21% testing more than three quarters of emails, compared to 10% of B2B marketers.

As described last year, there is a correlation between ROI on email marketing and testing (although this correlation was weaker this year), so while this trend is moving in the right direction, more coordinated testing will bring better results for marketers.

Which of these technologies do you involve in your email marketing programmes? Select all that apply.

Email is used most with CRM systems and outsourced technologies. However, almost one-third (31%) use an in-house solution, which may limit what brands are able to achieve with new technologies and capabilities constantly becoming available.

43%

36%

12%10%

38%

25%

16%

21%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Under a quarter of emailssent include a test

Between a quarter and half include a test

Between half and three-quarters include a test

Over three-quartersinclude a test

B2B B2C

64%

55%

31%

24% 24%

17%

6%

0%

10%

20%

30%

40%

50%

60%

70%

CRM

Outsourced email

marketing so

lution

In-house email

marketing so

lution

Multi-channel in

tegrations

(SMS, App noti�

cations,

Postal d

irect m

ail, Social m

edia)

Segmentation platfo

rm

Content management s

ystem

Other (please sp

ecify)

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201612

What is the maximum number of times you contact an email address in a month?

The maximum number of times brands contact specific addresses in a month has increased slightly, with the number of businesses emailing just once a month dropping from 25% to 9% this year. The number of brands contacting customers between four and five times per month has increased by 11% since last year.

What is the maximum number of times you contact an email address in a month?

B2C marketers contact email addresses more often than those working in B2B, with one additional email sent per month on average. Close to two-thirds of organisations (62%) either don’t have a policy about the maximum number of contacts per month or don’t know.

3. Customer contact

9%

38%

28%

8%10%

6%

25%

36%

17%

8% 8%5%

19%

35%

21%

9% 8% 8%

26% 26%

38%

17%

10%

4%

13%

35%

19%

8%

16%

9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once 2 - 3 times 4 - 5 times 6 - 8 times More than 8 times Don't know

2016 2015 2014 2013 2012

18%

37%

25%

7%5%

7%

3%

37%

30%

11%14%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Once

B2B B2C

2 - 3 times 4 - 5 times 6 - 8 times More than 8 times

Don't know

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

13

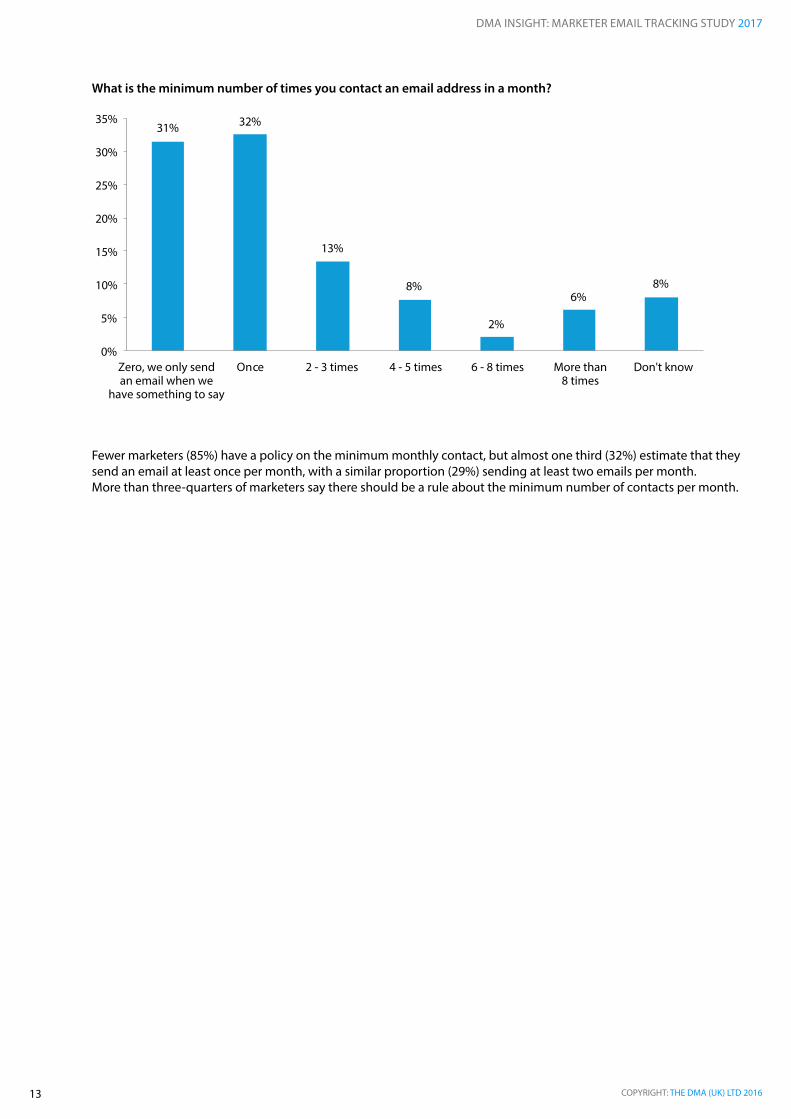

What is the minimum number of times you contact an email address in a month?

Fewer marketers (85%) have a policy on the minimum monthly contact, but almost one third (32%) estimate that they send an email at least once per month, with a similar proportion (29%) sending at least two emails per month.More than three-quarters of marketers say there should be a rule about the minimum number of contacts per month.

31% 32%

13%

8%

2%

6%8%

0%

5%

10%

15%

20%

25%

30%

35%

Zero, we only send an email when we

have something to say

Once 2 - 3 times 4 - 5 times 6 - 8 times More than 8 times

Don't know

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201614

Email works well, but like every other marketing channel, it works better in combination.

Considering your contact strategy, which channel(s) integrate with email most effectively to realise your campaign objectives? Select up to three choices.

Marketers say email works best with their own website (61% chose this, the same proportion as last year), followed by organic social media, rising to 45% from 40% last year, direct mail at 30%, and mobile more than doubled to 25% from 11% last year.

Two channels dropped significantly: face-to-face from 19% to 11%, and experiential from 20% to 15% since last year.Clearly marketers see digital channels as supreme and mobile as increasingly significant, although direct mail continues to be an effective channel.

4. Usage

2%

2%

4%

7%

9%

10%

19%

20%

17%

20%

11%

30%

40%

61%

1%

2%

3%

4%

8%

10%

11%

15%

18%

22%

25%

30%

45%

61%

None

Outdoor

Other (please specify)

Online web chat

Web banners

Display advertising

Face-to-face

Experiential/events/retail

Telemarketing

Social media (paid)

Mobile

Direct mail

Social media (organic)

Website (own)

2016 2015

0% 10% 20% 30% 40% 50% 60% 70%

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

15

However, when split by B2B and B2C, more differences emerge:

Considering your contact strategy, which channel(s) integrate with email most effectively to realise your campaign objectives? Select up to three choices.

B2C marketers find their website, social media (both paid and organic), direct mail and display to be far more effective in attaining their campaign goals with email. B2C marketers have a distinct preference for digital channels plus direct mail.

For B2B marketers, the personal touch is far more significant, with telemarketing, experiential and face-to-face significantly more effective when used with email.

1%

0%

3%

3%

10%

14%

6%

13%

10%

27%

25%

35%

48%

65%

0%

5%

2%

5%

9%

5%

18%

18%

32%

14%

25%

23%

41%

57%

B2B B2C

None

Outdoor

Other (please specify)

Online web chat

Web banners

Display advertising

Face-to-face

Experiential/events/retail

Telemarketing

Social media (paid)

Mobile

Direct mail

Social media (organic)

Website (own)

0% 10% 20% 30% 40% 50% 60% 70%

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201616

Are you able to calculate the return generated from your email marketing activities?

While 2016 seems to be the tipping point for content, last year was the tipping point for calculating ROI.

In 2016, for the first time, fewer marketers were able to calculate the ROI on their marketing campaigns than those who could. Those unable to calculate the ROI on their campaigns has dropped consistently since 2012 when 60% could calculate the ROI on their email campaigns.

Are you able to calculate the return generated from your email marketing activities?

However, when we split by B2B/B2C, this continues to be more of a problem for B2B marketers, 60% of whom are unable to calculate the return on their campaigns, compared to 60% of B2C marketers who can. As B2B sales cycles are typically both longer and more nuanced than B2C cycles, attribution to a specific channel may well prove challenging.

There is also a clear sliding scale between those who can and cannot calculate ROI, moving from senior marketers who are the most able to (54% can) down to junior marketers, where only one in 10 can calculate ROI.

5. ROI

45%

50%53%

58%60%

55%

50%47%

42%40%

0%

10%

20%

30%

40%

50%

60%

70%

2016 2015 2014 2013 2012

Yes No

40%

60%54%

35%

10%

60%

40%46%

65%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

B2B B2C Senior Manager Junior

Yes No

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

17

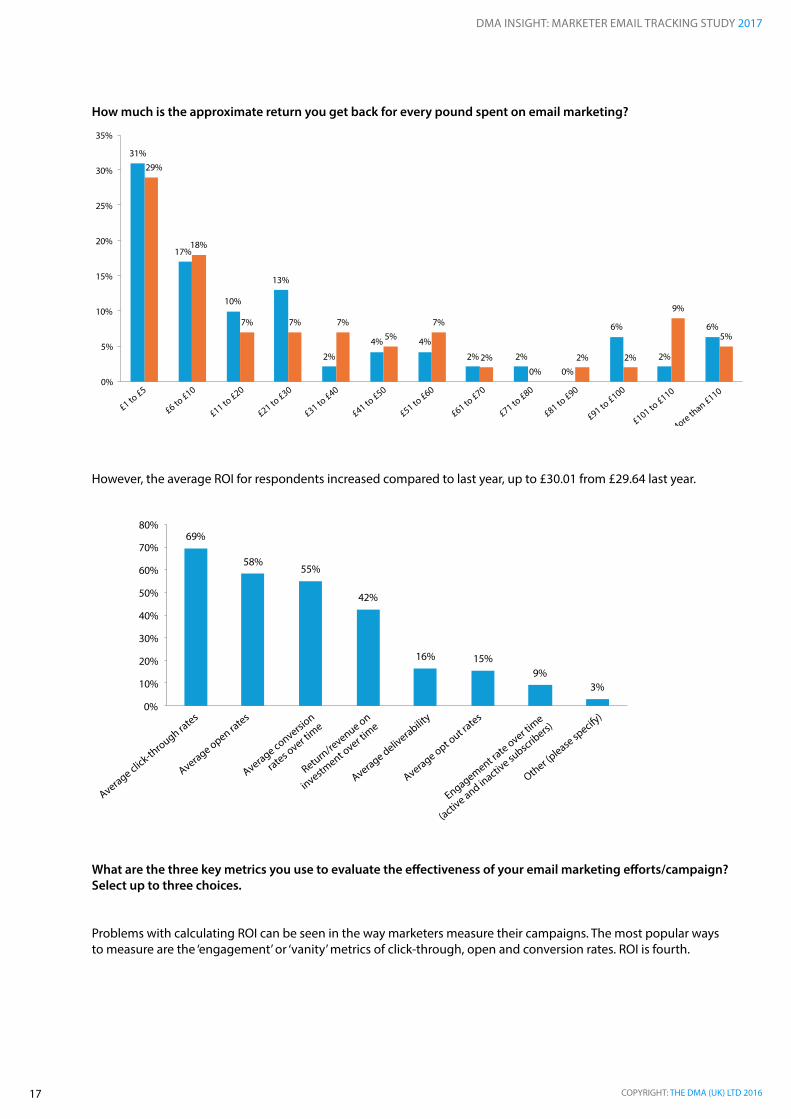

How much is the approximate return you get back for every pound spent on email marketing?

However, the average ROI for respondents increased compared to last year, up to £30.01 from £29.64 last year.

What are the three key metrics you use to evaluate the effectiveness of your email marketing efforts/campaign? Select up to three choices.

Problems with calculating ROI can be seen in the way marketers measure their campaigns. The most popular ways to measure are the ‘engagement’ or ‘vanity’ metrics of click-through, open and conversion rates. ROI is fourth.

31%

17%

10%

13%

2%

4% 4%

2% 2%

0%

6%

2%

6%

29%

18%

7% 7% 7%5%

7%

2%0%

2% 2%

9%

5%

0%

5%

10%

15%

20%

25%

30%

35%

£1 to £5

£6 to £10

£11 to £20

£21 to £30

£31 to £40

£41 to £50

£51 to £60

£61 to £70

£71 to £80

£81 to £90

£91 to £100

£101 to £110

More than £110

2016 2015

69%

58%55%

42%

16% 15%9%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Average click-through ra

tes

Average open rates

Average conversion

rates over ti

me

Return/revenue on

investment o

ver time

Average deliverabilit

y

Average opt out ra

tes

Engagement rate over ti

me

(active and in

active su

bscribers)

Other (please sp

ecify)

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

18

What are the most important three metrics you use to evaluate the effectiveness of an individual email? Select up to three choices.

The same pattern emerges when considering individual emails.

80%

59%

50%

36%

19% 17%10%

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Click-through ra

tes

Open rates

Conversion ra

tes

Return/revenue on in

vestment

Deliverabilit

y

Opt out ra

tes

Engagement rate over ti

me

(active and in

active su

bscribers)

Other (please sp

ecify)

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201619

Marketers have a curious relationship with their consumers.

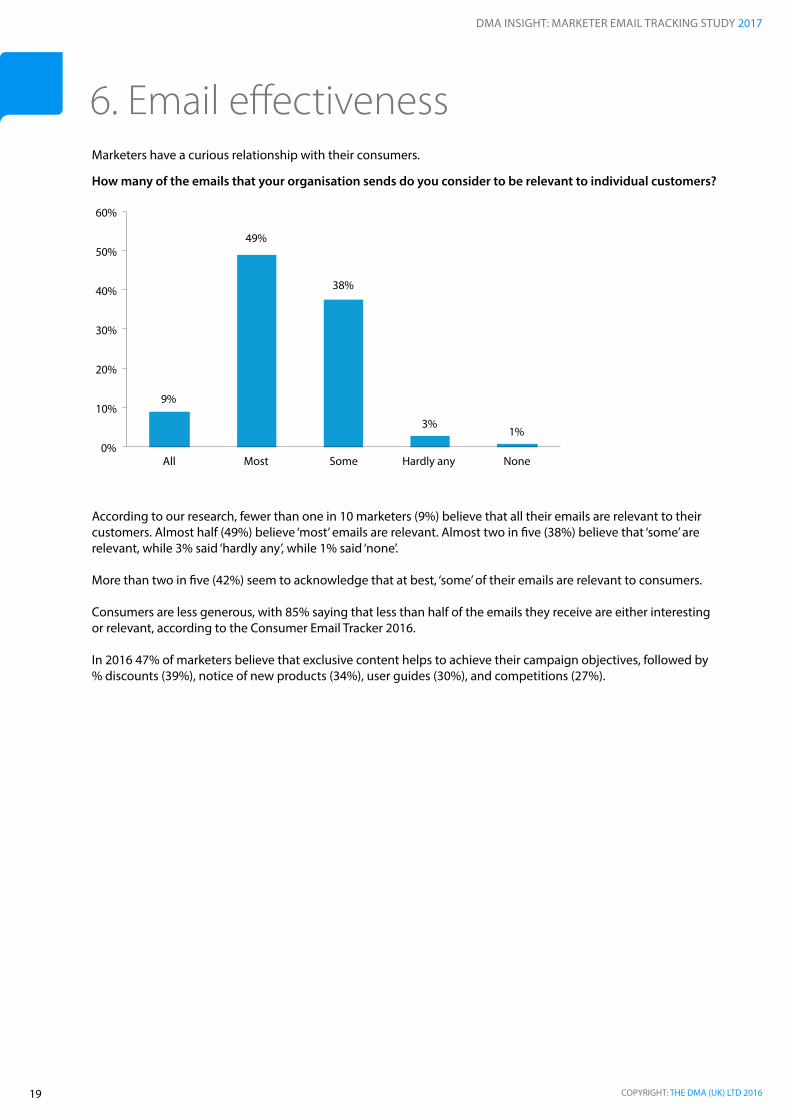

How many of the emails that your organisation sends do you consider to be relevant to individual customers?

According to our research, fewer than one in 10 marketers (9%) believe that all their emails are relevant to their customers. Almost half (49%) believe ‘most’ emails are relevant. Almost two in five (38%) believe that ‘some’ are relevant, while 3% said ‘hardly any’, while 1% said ‘none’.

More than two in five (42%) seem to acknowledge that at best, ‘some’ of their emails are relevant to consumers.

Consumers are less generous, with 85% saying that less than half of the emails they receive are either interesting or relevant, according to the Consumer Email Tracker 2016.

In 2016 47% of marketers believe that exclusive content helps to achieve their campaign objectives, followed by % discounts (39%), notice of new products (34%), user guides (30%), and competitions (27%).

6. Email effectiveness

9%

49%

38%

3%1%

0%

10%

20%

30%

40%

50%

60%

All Most Some Hardly any None

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

20

What marketers believe to be effective compared to what consumers say they like

This contrasts sharply with what consumers say they want from marketing, which skews heavily towards discounts, free gifts, free delivery and loyalty rewards.

While content is singled out by marketers as being the most effective tool for them, it is also the single least appealing feature for consumers considering opting-in to brand emails.

There may be inconsistencies in the language used – consumers may not understand ‘content’ in the same way as marketers, but such a huge disparity in the perception of ‘content’ must be significant.

Rationally, consumers want ‘free’ offers or ‘discounts’, but practically, they respond to content, according to marketers.

47%

39%

34%

30%27% 27%

22%21%

19%15% 14%

8%7%

3%

64%

30%

40%

36%

19%20%

31%

20%

11%7% 8%

7%

13%

2%4%

50%

23%

6%

23%

51%

4%

16%

38%

12%

43%

38%

9%

0%

10%

20%

30%

40%

50%

60%

70%

2016 2015 What consumers like best in emails

Exclusive content

% o� discounts

Advance notice of n

ew products

User guides

Competitions

Money-o� discounts

Peer-generated so

cial content

(e.g. tweets,

videos, photos, b

logs)

Product reviews

Loyalty program re

wards

VIP access

Free samples/g

ifts

Free delivery

Other (please sp

ecify)

None

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

21

What B2C marketers believe to be effective compared to what consumers say they like

When comparing the desires of consumers to the experience of those marketing to them, then these same inconsistencies persist.

This also suggests that what works for consumers will also broadly work for B2B messaging. There is some difference between the experiences of B2C marketers and of all marketers, particularly in the middle of the tables above, but these differences are not very large. Recipients will consistently opt for money off, for example.

41% 41%

35%33%

29%

21% 21%17% 16%

14% 13%

8% 8%5%4%

50% 51%

23% 23%

6%

38%

4%

16%12%

43%

38%

9%

0%

10%

20%

30%

40%

50%

60%

B2C What consumers like best in emails

Exclusive content

% o� discounts

Advance notice of n

ew products

User guides

Competitions

Money-o� discounts

Peer-generated so

cial content

(e.g. tweets,

videos, photos, b

logs)

Product reviews

Loyalty program re

wards

VIP access

Free samples/g

ifts

Free delivery

Other (please sp

ecify)

None

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

22

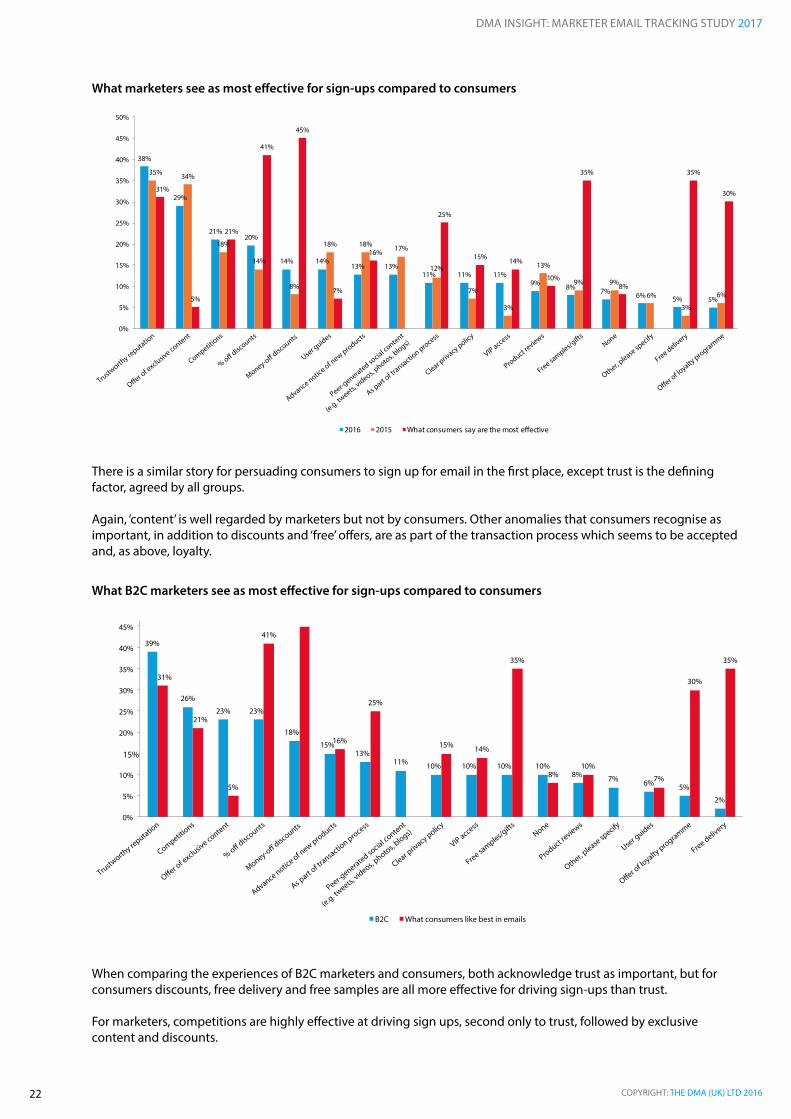

What marketers see as most effective for sign-ups compared to consumers

There is a similar story for persuading consumers to sign up for email in the first place, except trust is the defining factor, agreed by all groups.

Again, ‘content’ is well regarded by marketers but not by consumers. Other anomalies that consumers recognise as important, in addition to discounts and ‘free’ offers, are as part of the transaction process which seems to be accepted and, as above, loyalty.

What B2C marketers see as most effective for sign-ups compared to consumers

When comparing the experiences of B2C marketers and consumers, both acknowledge trust as important, but for consumers discounts, free delivery and free samples are all more effective for driving sign-ups than trust.

For marketers, competitions are highly effective at driving sign ups, second only to trust, followed by exclusive content and discounts.

38%

29%

21%20%

14% 14%13% 13%

11% 11% 11%9% 8% 7% 6% 5% 5%

35% 34%

18%

14%

8%

18% 18% 17%

12%

7%

3%

13%

9% 9%

6%

3%

6%

31%

5%

21%

41%

45%

7%

16%

25%

15% 14%

10%

35%

8%

35%

30%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2016 2015 What consumers say are the most e�ective

Trustworth

y reputatio

n

O�er of e

xclusive content

Competitions

% o� discounts

Money-o� discounts

User guides

Advance notice of n

ew products

Peer-generated so

cial content

(e.g. tweets,

videos, photos, b

logs)

As part o

f transactio

n process

Clear priv

acy policy

VIP access

Product reviews

Free samples/g

iftsNone

Other, please sp

ecify

Free delivery

O�er of lo

yalty programme

39%

26%

23% 23%

18%

15%13%

11% 10% 10% 10% 10%8% 7% 6% 5%

2%

31%

21%

5%

41%

45%

16%

25%

15% 14%

35%

8%10%

7%

30%

35%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

B2C What consumers like best in emails

Trustworth

y reputatio

n

O�er of e

xclusive content

Competitions

% o� discounts

Money-o� discounts

User guides

Advance notice of n

ew products

Peer-generated so

cial content

(e.g. tweets,

videos, photos, b

logs)

As part o

f transactio

n process

Clear priv

acy policy

VIP access

Product reviews

Free samples/g

iftsNone

Other, please sp

ecify

Free delivery

O�er of lo

yalty programme

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

23

Unsubscribes

More than half of consumers (51%) expect to never hear from a consumers again if they unsubscribe according to the Consumer email tracker 2016, with a further 30% saying unsubscribing makes no difference.

When a customer unsubscribes from your organisation’s emails, what happens next? Please tick all that apply.

The confusion is understandable. Marketers have rather different approaches to what happens when a consumer hits ‘unsubscribe’, ranging from taking them off all lists immediately (42%) to taking them to a preference centre (7%).

B2B marketers are more likely to process unsubscribes immediately (48% vs 40%), while B2C marketers are more likely to wait and either not send more emails (13% vs 7%) or continue to send transactional emails (11% vs 7%).

Under the GDPR, which comes into force in May 2018, consumers will have the right to manage their own data, making preference centres exceptionally important in allowing consumers to have more control.

48%

27%

7% 7%9%

2%0%

40%

27%

13%11%

5%2% 3%

0%

10%

20%

30%

40%

50%

60%

We never sent a

nother email

We continue se

nding transactio

nal

emails, but n

ot marketin

g emails

We send no emails

from th

e

next time w

e process the data

We continue se

nding transactio

nal

emails, but n

ot marketin

g emails fro

m

the next time w

e process the data

We take th

em to a preference centre

We take th

em to a su

rvey

Other (please sp

ecify)

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201624

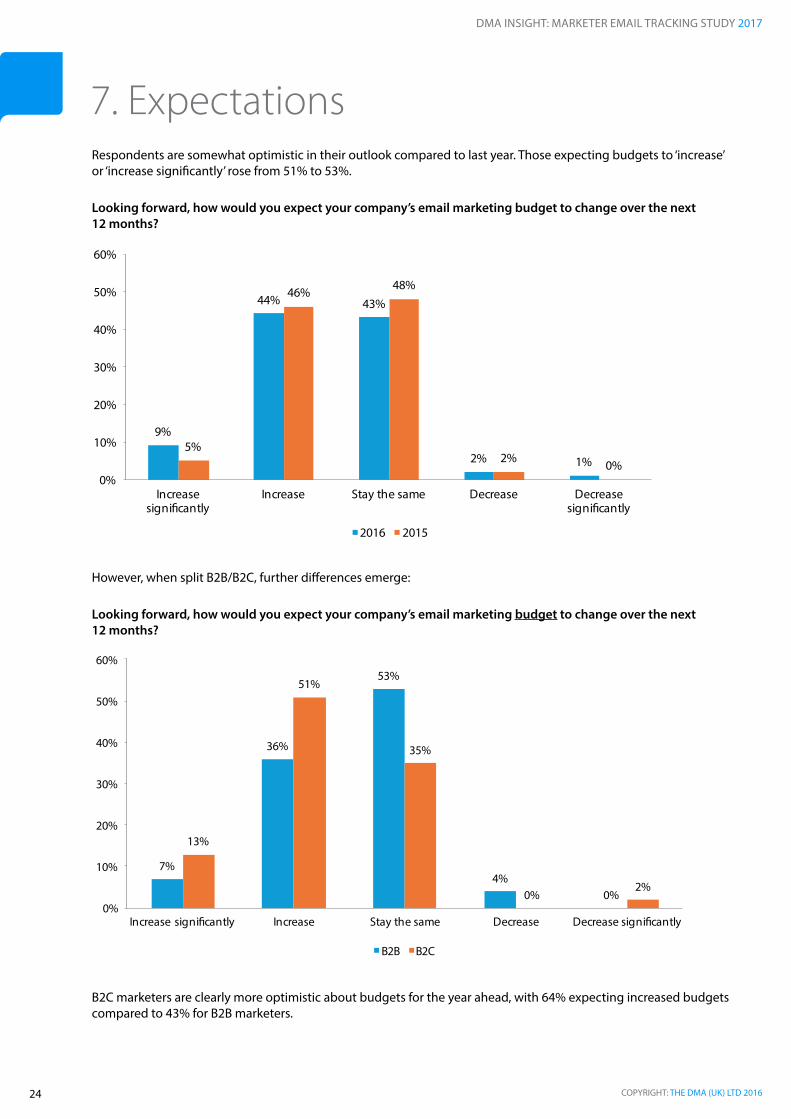

Respondents are somewhat optimistic in their outlook compared to last year. Those expecting budgets to ‘increase’ or ‘increase significantly’ rose from 51% to 53%.

Looking forward, how would you expect your company’s email marketing budget to change over the next 12 months?

However, when split B2B/B2C, further differences emerge:

Looking forward, how would you expect your company’s email marketing budget to change over the next 12 months?

B2C marketers are clearly more optimistic about budgets for the year ahead, with 64% expecting increased budgets compared to 43% for B2B marketers.

7. Expectations

9%

44% 43%

2% 1%5%

46% 48%

2% 0%0%

10%

20%

30%

40%

50%

60%

Increase signi�cantly

Increase Stay the same Decrease Decrease signi�cantly

2016 2015

7%

36%

53%

4%0%

13%

51%

35%

0%2%

0%

10%

20%

30%

40%

50%

60%

Increase signi�cantly Increase Stay the same Decrease Decrease signi�cantly

B2B B2C

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

25

Looking forward, how would you expect your company’s email marketing costs to change over the next 12 months?

Expectations match predictions on costs for both B2B and B2C marketers, with a majority of B2C marketers expecting an increase in costs while a majority of B2B marketers expect costs to stay the same.

What percentage of your marketing budget is spent on email?

Spend on email seems to have stabilised, with the clear majority (82%) spending between 0 and 20% of their marketing budget on email. Outliers spending more than 50% on email has reached a new low of 3%, down from 5% last year.

43%

53%

4%

64%

35%

2%

0%

10%

20%

30%

40%

50%

60%

70%

Increase Stay the same Decrease

B2B B2C

82%

14%

4% 3%

81%

10%6% 5%

74%

18%

2% 4%

61%

18%

10% 11%

63%

20%

7%11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0-20% 21-40% 41-50% More than 50%

2016 2015 2014 2013 2012

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

26

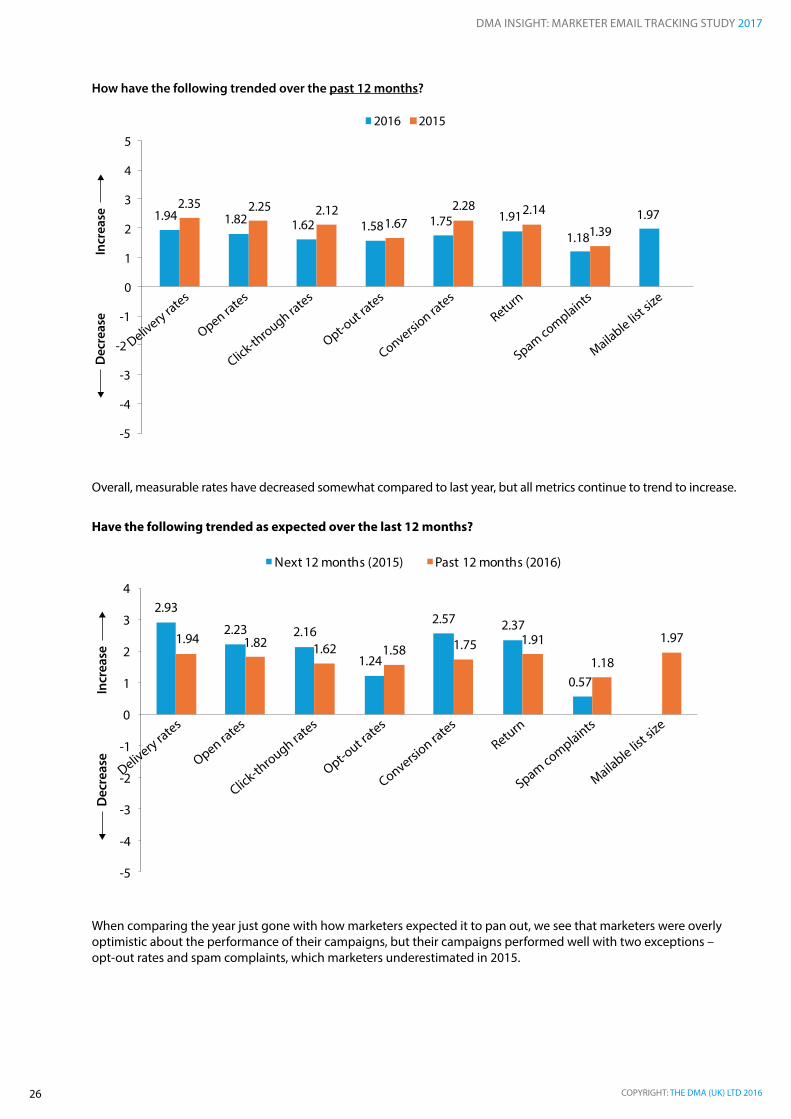

How have the following trended over the past 12 months?

Overall, measurable rates have decreased somewhat compared to last year, but all metrics continue to trend to increase.

Have the following trended as expected over the last 12 months?

When comparing the year just gone with how marketers expected it to pan out, we see that marketers were overly optimistic about the performance of their campaigns, but their campaigns performed well with two exceptions – opt-out rates and spam complaints, which marketers underestimated in 2015.

1.94 1.82 1.62 1.58 1.75 1.91

1.18

1.972.35 2.25 2.12

1.672.28 2.14

1.39

-5

-4

-3

-2

-1

0

1

2

3

4

5

2016 2015

Delivery ra

tes

Open rates

Click-through ra

tes

Opt-out ra

tes

Conversion ra

tes

Return

Spam complaints

Mailable lis

t size

Incr

ease

Dec

reas

e

2.93

2.23 2.16

1.24

2.57 2.37

0.57

1.94 1.82 1.62 1.58 1.75 1.91

1.18

1.97

-5

-4

-3

-2

-1

0

1

2

3

4

Next 12 months (2015) Past 12 months (2016)

Delivery ra

tes

Open rates

Click-through ra

tes

Opt-out ra

tes

Conversion ra

tes

Return

Spam complaints

Mailable lis

t size

Incr

ease

Dec

reas

e

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201627

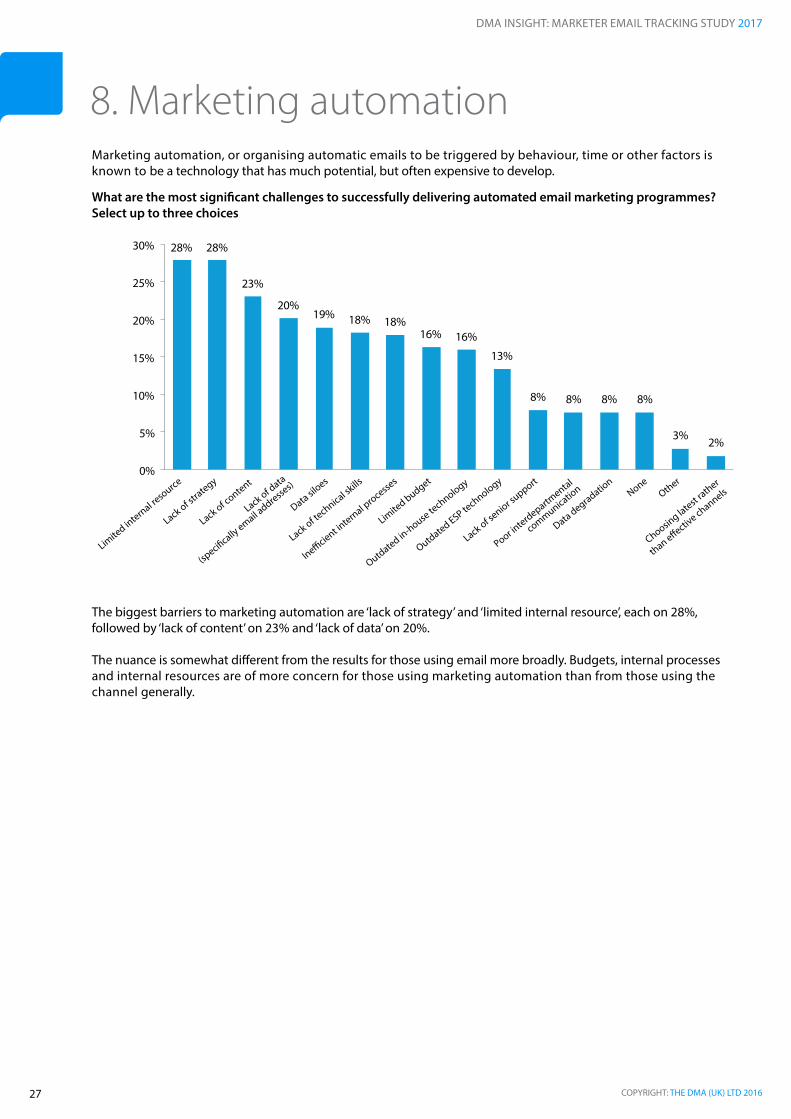

Marketing automation, or organising automatic emails to be triggered by behaviour, time or other factors is known to be a technology that has much potential, but often expensive to develop.

What are the most significant challenges to successfully delivering automated email marketing programmes? Select up to three choices

The biggest barriers to marketing automation are ‘lack of strategy’ and ‘limited internal resource’, each on 28%, followed by ‘lack of content’ on 23% and ‘lack of data’ on 20%.

The nuance is somewhat different from the results for those using email more broadly. Budgets, internal processes and internal resources are of more concern for those using marketing automation than from those using the channel generally.

8. Marketing automation

28% 28%

23%

20%19% 18% 18%

16% 16%

13%

8% 8% 8% 8%

3% 2%

0%

5%

10%

15%

20%

25%

30%

Limite

d internal re

source

Lack of strategy

Lack of content

Lack of data

(speci�cally

email addresse

s)

Data siloes

Lack of technical sk

ills

Ine�cient internal p

rocesses

Limite

d budget

Outdated in-house te

chnology

Outdated ESP technology

Lack of senior s

upport

Poor interdepartm

ental

communication

Data degradation

NoneOther

Choosing latest

rather

than e�ective channels

COPYRIGHT: THE DMA (UK) LTD 2016

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

28

What are the key contact segments you use in your email marketing programmes? Select up to three choices.

Marketing automation may be declining as a technology amongst marketers. According to the above graph, typical automation triggers are falling. ‘Reader behaviour’ has almost halved, down from 36% in 2014 down to 19% in 2016, while ‘reader life stages’, another automation trigger, has also almost halved, down from 42% to 23% (although slightly up compared to last year).

What are the key contact segments you use in your email marketing programmes? Select up to three choices.

However, ‘reader life stages’ are considerably higher for B2B marketers (32% vs 18%), suggesting that some B2B marketers with specific timeframes in mind or well-defined sales funnels are better-suited to this type of automation. B2B marketers also favour specific defined audiences (48% vs 40%).

43%

39%

29%27% 26%

23% 22%19% 18%

4%

65%

25%

38%

9%

18%

13%

29%

14%

10%

51%

25%

37%

20%

42%

14%

36%

6%

2%

0%

10%

20%

30%

40%

50%

60%

70%

Audience de�nition/type

Most/least engaged

Recency of purchase

Subscriber preferences

Frequency of purchase

Reader life stages

Lifetime value of reader

Reader behaviour

Value of purchase

Other, please specify

2016 2015 2014

48%

36%

27% 27%23%

32%

16%18%

9%7%

40% 40%

31%

26% 27%

18%

26%

19%

24%

2%

0%

10%

20%

30%

40%

50%

60%

B2B B2C

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201629

The Marketer email tracking report is an initiative undertaken by the DMA’s Email council in conjunction/collaboration with the Email benchmarking hub.

The research was conducted from October to December 2016 via a survey that was hosted online. It was promoted on the DMA home page and via various members of the Email council. A link to the survey was added to a select number of DMA members’ weekly newsletters, social networks and websites.

A wide range of both DMA members and non-members were surveyed. This sample included a cross section of company types and sizes. A wide range of UK geographical locations were also reached. The respondents also operated in a wide range of sectors. The data was collated and analysed by the DMA’s Marketing and Insight department, who also wrote the report. The final report was produced in collaboration with the sponsor, dotmailer, and the DMA Email mail benchmarking hub. The report was designed by the DMA’s in house design team.

The survey consisted of 46 questions in total, which were a mixture of both qualitative and quantitative questions. These questions were reviewed by the DMA, dotmailer, and the DMA Email benchmarking hub to ensure they reflected the current market scenario. The survey had 209 respondents (42% B2B and 58% B2C). Respondents were incentivised to complete the survey by offer of the chance to win a £100 Amazon voucher in a prize draw.

The findings were launched at an event on 9 February 2016. The report is hosted on the DMA website.

Methodology

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201630

Our missionPut simply, our mission is to make it as easy as possible for marketers to get results that make a dramatic improvement to their business.

We continue to experience exciting growth in our business since we began in 1999. We’re proud to have retained our culture and individualism over the years, and in particular our focus on making dotmailer a great place to work; we know that happy people equal happy clients and successful businesses.

Our heritagedotmailer was founded in 1999. The aim was to enable organisations to grow their business through online channels. Made up of dotmailer, dotsearch, dotcommerce, dotagency and dotsurvey, the group’s expertise covered the entire spectrum of online marketing and ecommerce.

Our futureToday, the group is solely focused on email marketing. It has grown to become a leader in the provision of intuitive Software as a service (SaaS) email marketing and cross channel tools. Even better, we’ve retained the people and knowledge of ecommerce and agency within our business.

About dotmailer

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201631

A DMA membership will grow your business. Our network of more than 1,000 UK companies is privy to research, free legal advice, political lobbying and industry guidance. Our members connect at regular events that inspire creativity, innovation, responsible marketing and more. Most of them are free.

A DMA membership is a badge of accreditation. We give the industry best-practice guidelines, legal updates and a code that puts the customer at the heart. We represent a data-driven industry that’s leading the business sector in creativity and innovation.

One-to-one-to-millions marketing attracts the brightest minds; individuals that will shape the future. By sharing our knowledge, together, we’ll make it vibrant.

Published by The Direct Marketing Association (UK) Ltd Copyright © Direct Marketing Association. All rights reserved.

www.dma.org.uk

About the DMA

DMA INSIGHT: MARKETER EMAIL TRACKING STUDY 2017

COPYRIGHT: THE DMA (UK) LTD 201632

The Marketer email tracking study 2017 is published by The Direct Marketing Association (UK) Ltd Copyright © Direct Marketing Association. All rights reserved. No part of this publication may be reproduced, copied or transmitted in any form or by any means, or stored in a retrieval system of any nature, without the prior permission of the DMA (UK) Ltd except as permitted by the provisions of the Copyright, Designs and Patents Act 1988 and related legislation. Application for permission to reproduce all or part of the Copyright material shall be made to the DMA (UK) Ltd, DMA House, 70 Margaret Street, London, W1W 8SS.

Although the greatest care has been taken in the preparation and compilation of the Marketer email tracking study 2017, no liability or responsibility of any kind (to extent permitted by law), including responsibility for negligence is accepted by the DMA, its servants or agents. All information gathered is believed correct at February 2017. All corrections should be sent to the DMA for future editions.

Copyright and disclaimer