digital manufacturing lab - economia.unipd.it · organization at the geographical level...

TRANSCRIPT

Digital Manufacturing Lab

Second Report Industry 4.0 in Italian SMEs

Survey 2017 (Released April 2018)

Research goals

• Fully supported by DSEA funds, the first research promoted by Digital Manufacturing Lab aims at: – carrying out a first map of degree of Industry 4.0

technological investments– understanding advantages and results achieved in the

introduction of such technologies– exploring reasons preventing firms in the adoption of

those technologies– deepening analysis on impacts concerning manufacturing

organization at the geographical level (internationalization) as well as in terms of environmental sustainability

2

Methodology

• Research on a sample of 7,293 manufacturing firms selected as follows (source AIDA database):– Made in Italy industries (Home furnishing, Mechanics, Fashion)– Geographical location: Northern Italy (Piedmont, Lombardy,

Veneto, Trentino-Alto Adige, Friuli Venezia Giulia, Emilia-Romagna)– Firms with 2015 turnover > 1 Ml € (firms with 2015 turnover < 1Ml € in industries characterized by industrial districts)

• Mixed method: CAWI addressing entrepreneurs and Chief Operations Officers (survey) and case studies

• Interviewed firms: 1,020 firms (14% response rate) (May - December 2017)

3

Adopting firms

4

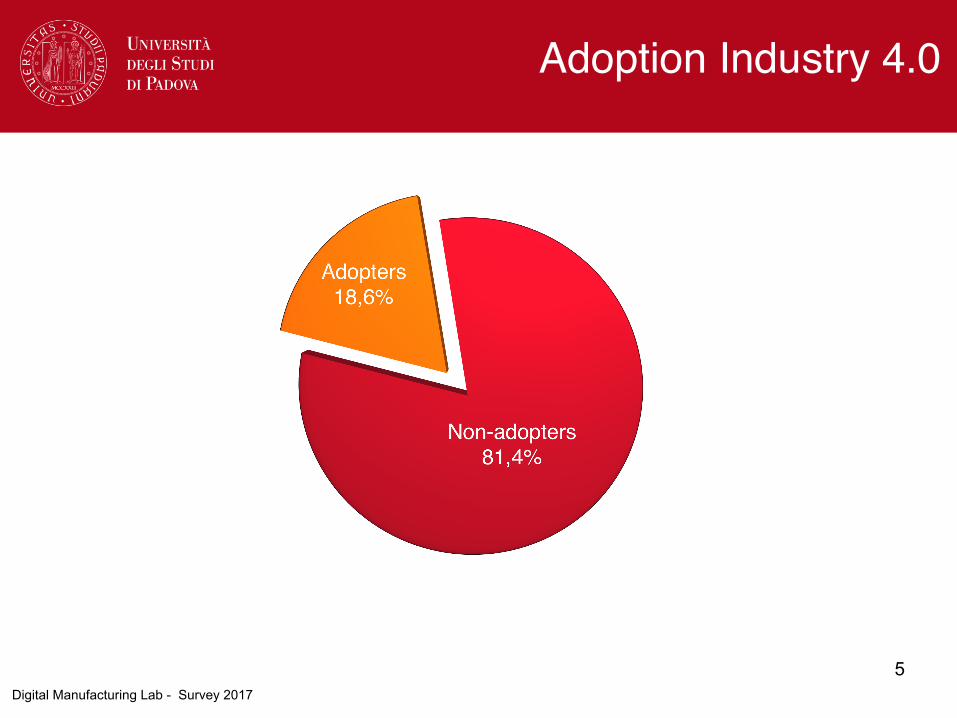

Adoption Industry 4.0

5Digital Manufacturing Lab - Survey 2017

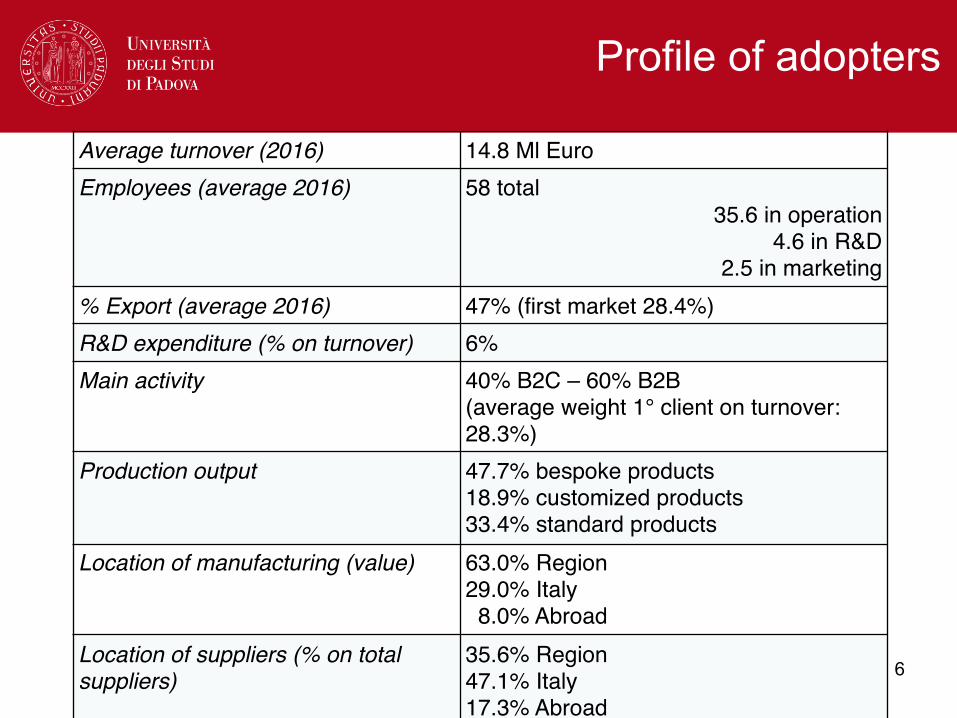

Profile of adopters

Average turnover (2016) 14.8 Ml EuroEmployees (average 2016) 58 total

35.6 in operation 4.6 in R&D

2.5 in marketing% Export (average 2016) 47% (first market 28.4%)R&D expenditure (% on turnover) 6%Main activity 40% B2C – 60% B2B

(average weight 1° client on turnover: 28.3%)

Production output 47.7% bespoke products18.9% customized products33.4% standard products

Location of manufacturing (value) 63.0% Region29.0% Italy 8.0% Abroad

Location of suppliers (% on total suppliers)

35.6% Region47.1% Italy17.3% Abroad

6

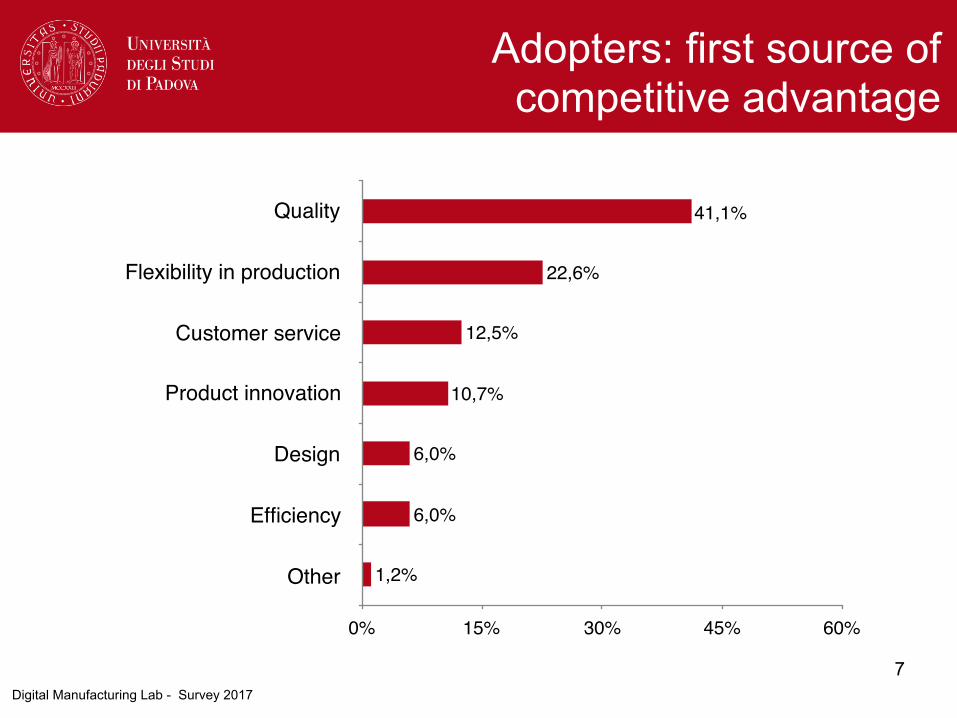

7

Quality

Flexibility in production

Customer service

Product innovation

Design

Efficiency

Other

0% 15% 30% 45% 60%

1,2%

6,0%

6,0%

10,7%

12,5%

22,6%

41,1%

Adopters: first source of competitive advantage

Digital Manufacturing Lab - Survey 2017

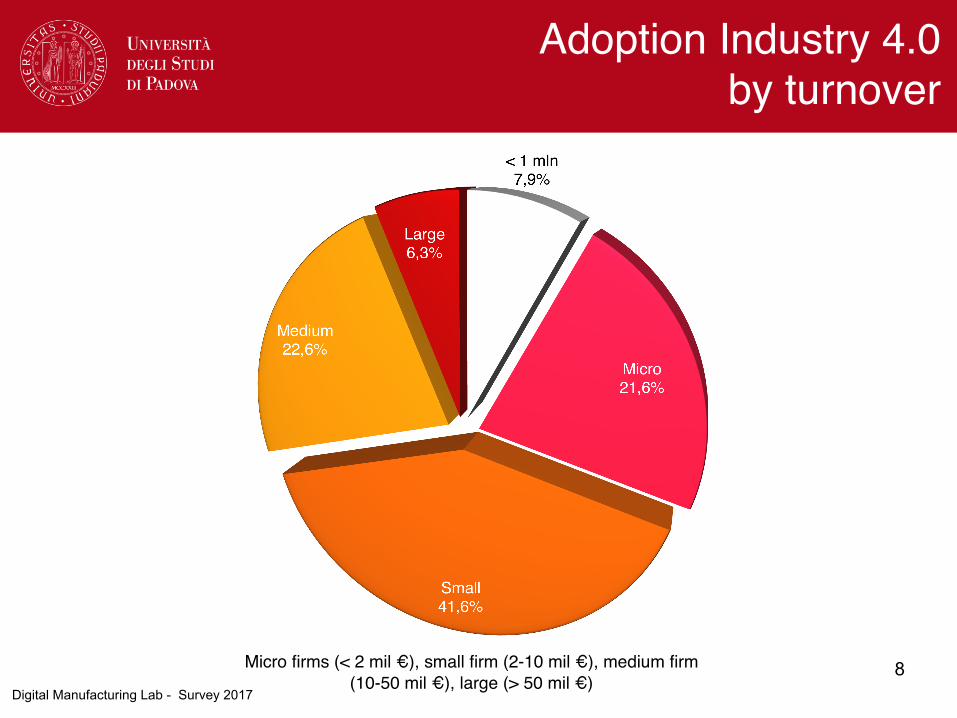

8Digital Manufacturing Lab - Survey 2017

Adoption Industry 4.0 by turnover

Micro firms (< 2 mil €), small firm (2-10 mil €), medium firm (10-50 mil €), large (> 50 mil €)

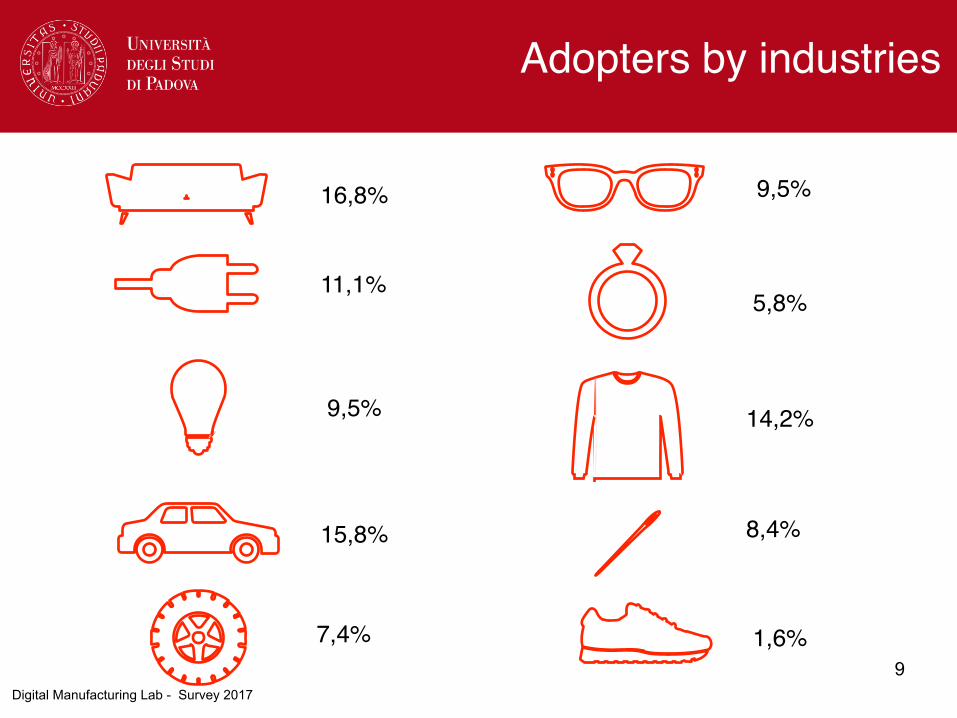

16,8%

11,1%

9,5%

15,8%

9,5%

5,8%

1,6%7,4%9

14,2%

8,4%

Digital Manufacturing Lab - Survey 2017

Adopters by industries

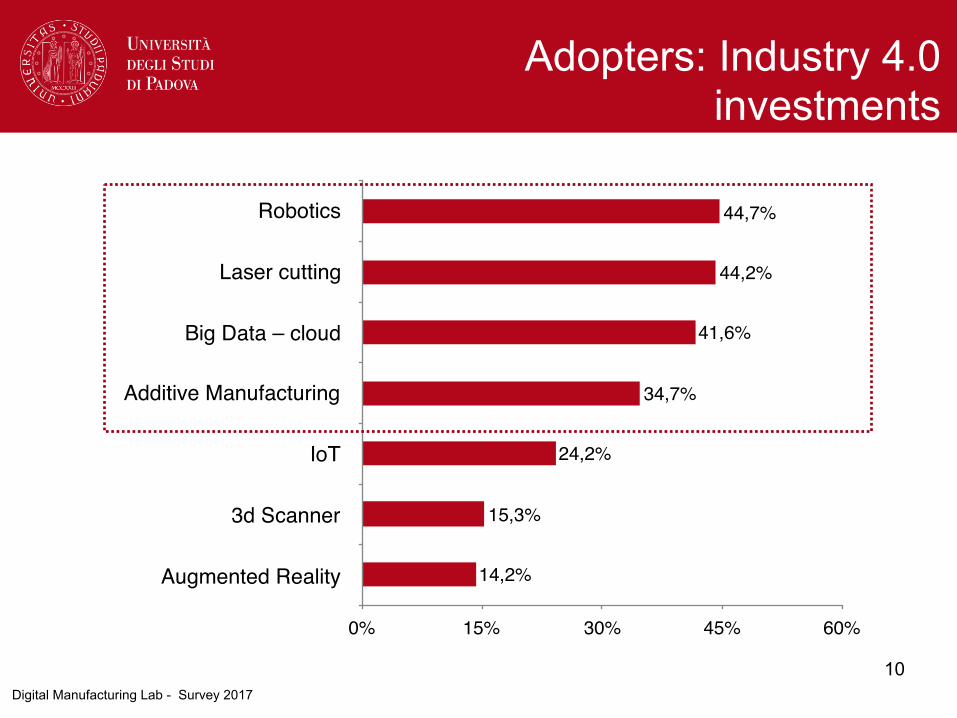

Robotics

Laser cutting

Big Data – cloud

Additive Manufacturing

IoT

3d Scanner

Augmented Reality

0% 15% 30% 45% 60%

14,2%

15,3%

24,2%

34,7%

41,6%

44,2%

44,7%

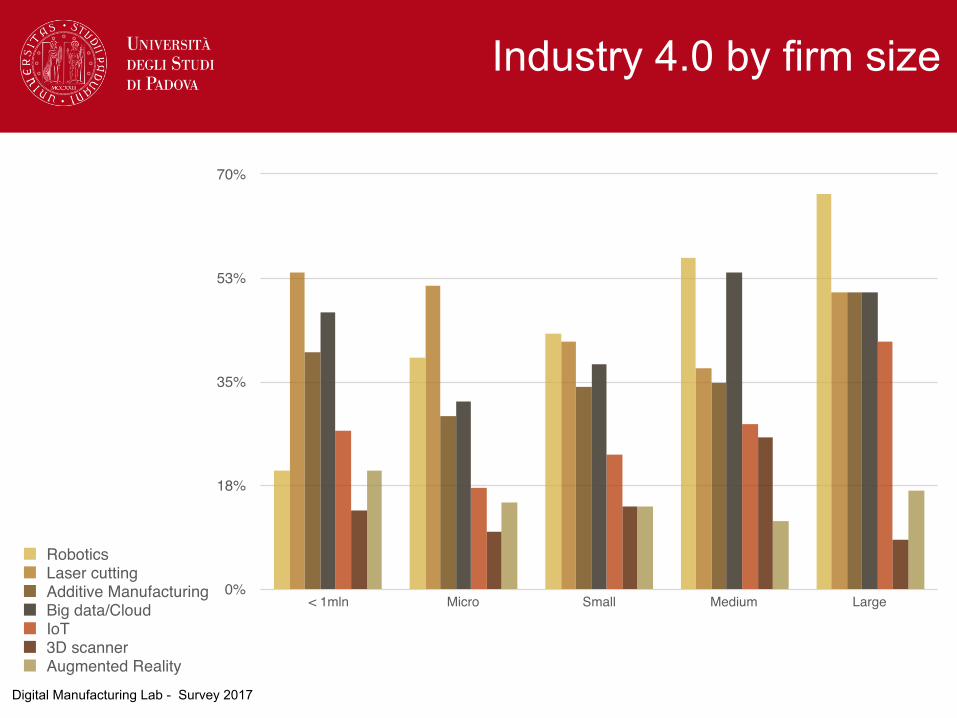

10Digital Manufacturing Lab - Survey 2017

Adopters: Industry 4.0 investments

0%

18%

35%

53%

70%

< 1mln Micro Small Medium Large

RoboticsLaser cuttingAdditive ManufacturingBig data/CloudIoT3D scannerAugmented Reality

Digital Manufacturing Lab - Survey 2017

Industry 4.0 by firm size

0%

25%

50%

75%

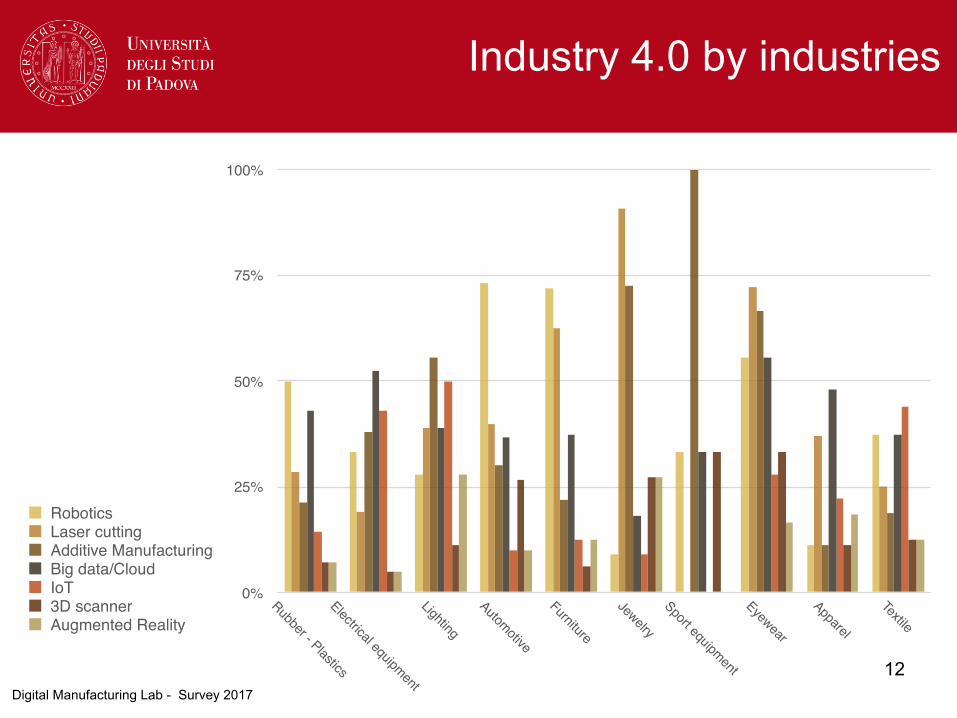

100%

Rubber - PlasticsElectrical equipmentLighting

Automotive

Furniture

JewelrySport equipmentEyewear

Apparel

Textile

RoboticsLaser cuttingAdditive ManufacturingBig data/CloudIoT3D scannerAugmented Reality

12Digital Manufacturing Lab - Survey 2017

Industry 4.0 by industries

0%

10%

20%

30%

40%

One technology Two technologies Three technologies More than three

16,9%

12,1%

36,2%38,4%

13Digital Manufacturing Lab - Survey 2017

Number of adopted technologies

14

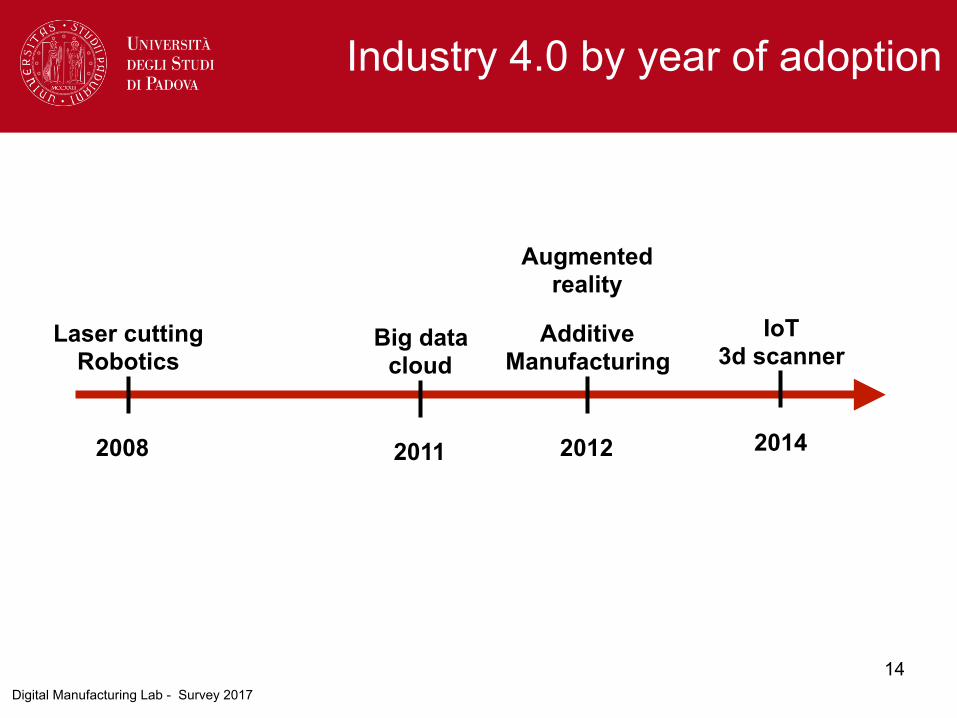

Laser cutting Robotics

2008

Augmented reality

2011

Big data cloud

2012

Additive Manufacturing

2014

IoT 3d scanner

Digital Manufacturing Lab - Survey 2017

Industry 4.0 by year of adoption

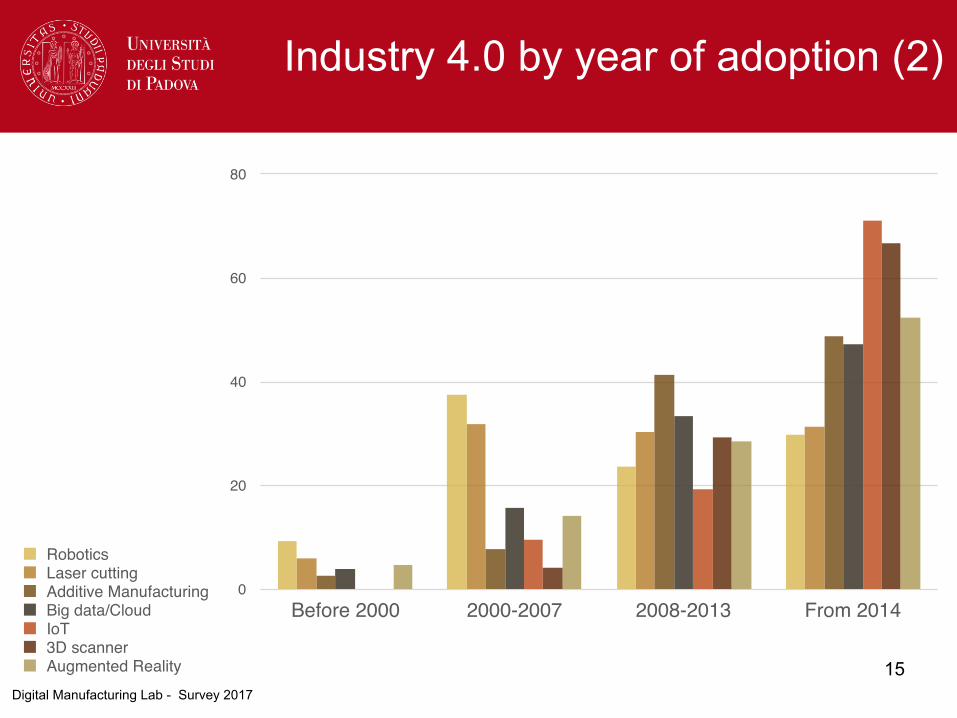

15

0

20

40

60

80

Before 2000 2000-2007 2008-2013 From 2014

RoboticsLaser cuttingAdditive ManufacturingBig data/CloudIoT3D scannerAugmented Reality

Digital Manufacturing Lab - Survey 2017

Industry 4.0 by year of adoption (2)

Non-adopting firms

16

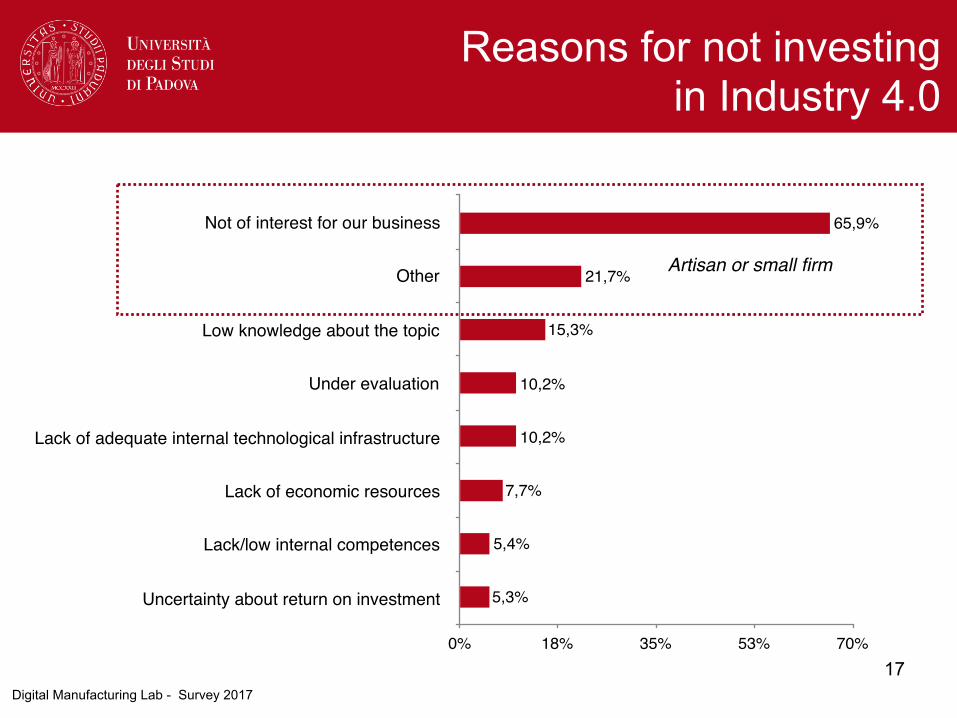

Not of interest for our business

Other

Low knowledge about the topic

Under evaluation

Lack of adequate internal technological infrastructure

Lack of economic resources

Lack/low internal competences

Uncertainty about return on investment

0% 18% 35% 53% 70%

5,3%

5,4%

7,7%

10,2%

10,2%

15,3%

21,7%

65,9%

Artisan or small firm

17Digital Manufacturing Lab - Survey 2017

Reasons for not investing in Industry 4.0

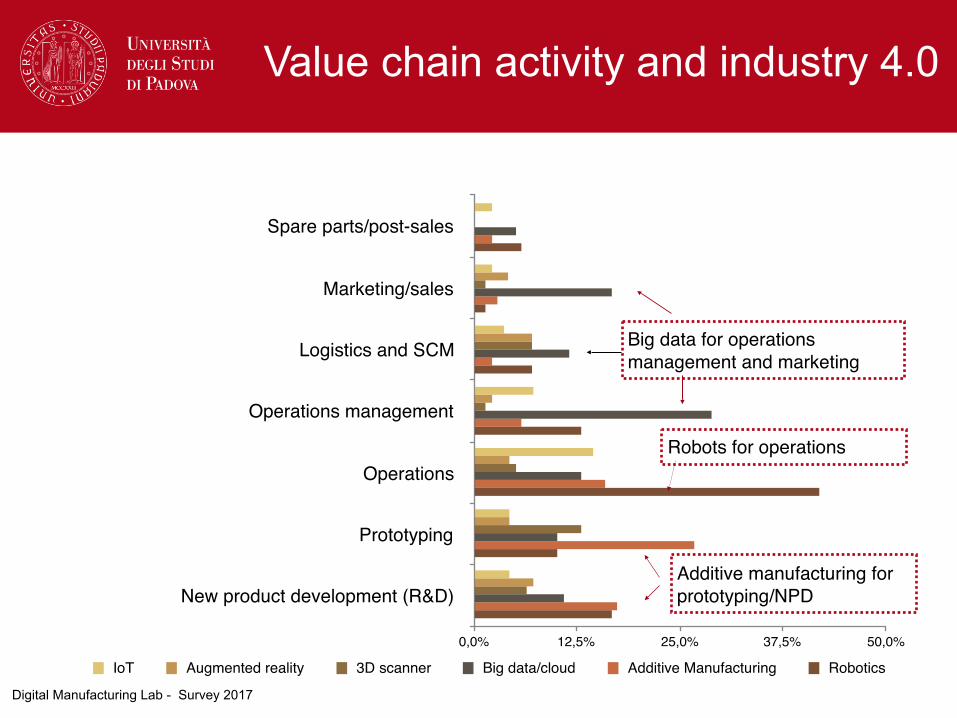

Industry 4.0 and areas of application

18

Spare parts/post-sales

Marketing/sales

Logistics and SCM

Operations management

Operations

Prototyping

New product development (R&D)

0,0% 12,5% 25,0% 37,5% 50,0%

IoT Augmented reality 3D scanner Big data/cloud Additive Manufacturing Robotics

Digital Manufacturing Lab - Survey 2017

Value chain activity and industry 4.0

Big data for operations management and marketing

Robots for operations

Additive manufacturing for prototyping/NPD

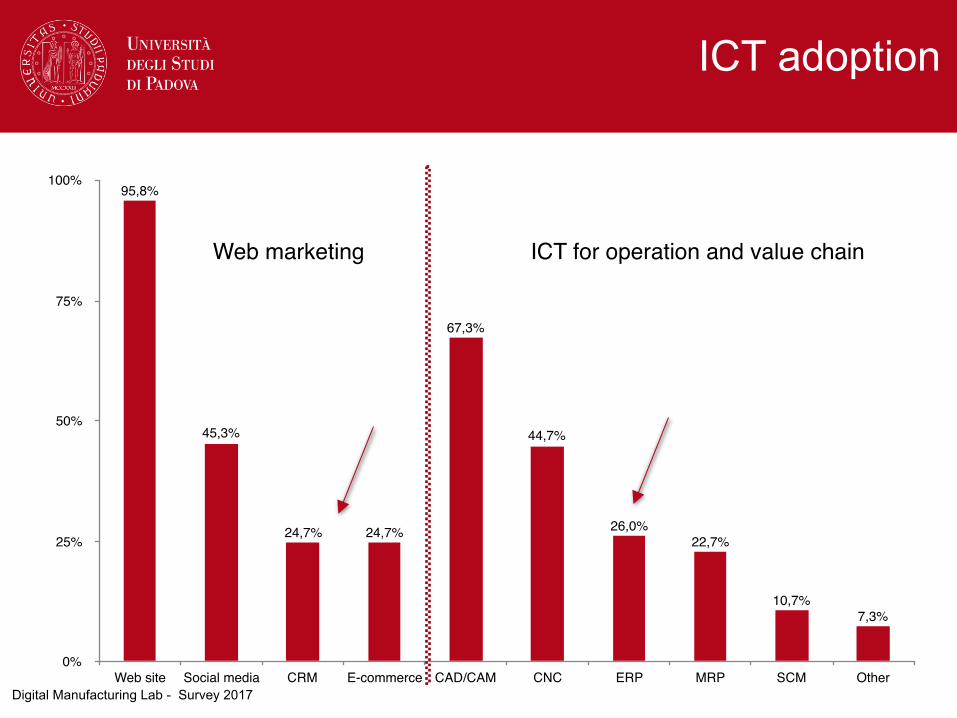

ICT adoption

0%

25%

50%

75%

100%

Web site Social media CRM E-commerce CAD/CAM CNC ERP MRP SCM Other

7,3%10,7%

22,7%26,0%

44,7%

67,3%

24,7%24,7%

45,3%

95,8%

Web marketing ICT for operation and value chain

Digital Manufacturing Lab - Survey 2017

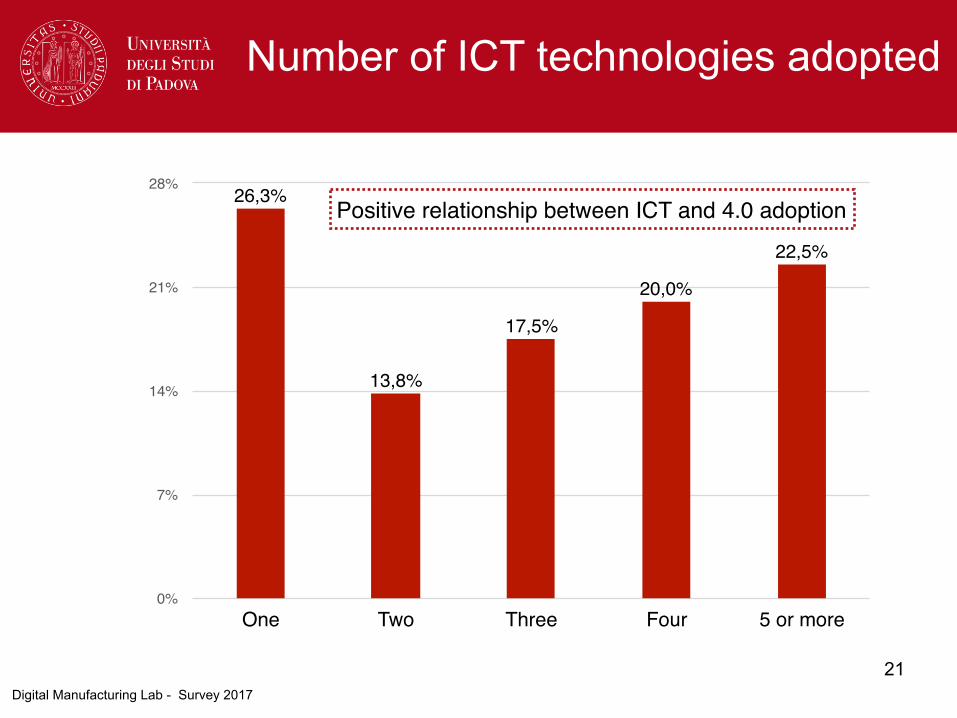

Number of ICT technologies adopted

0%

7%

14%

21%

28%

One Two Three Four 5 or more

22,5%

20,0%

17,5%

13,8%

26,3%

21

Positive relationship between ICT and 4.0 adoption

Digital Manufacturing Lab - Survey 2017

Management of Industry 4.0 projects

22

0

1,25

2,5

3,75

5

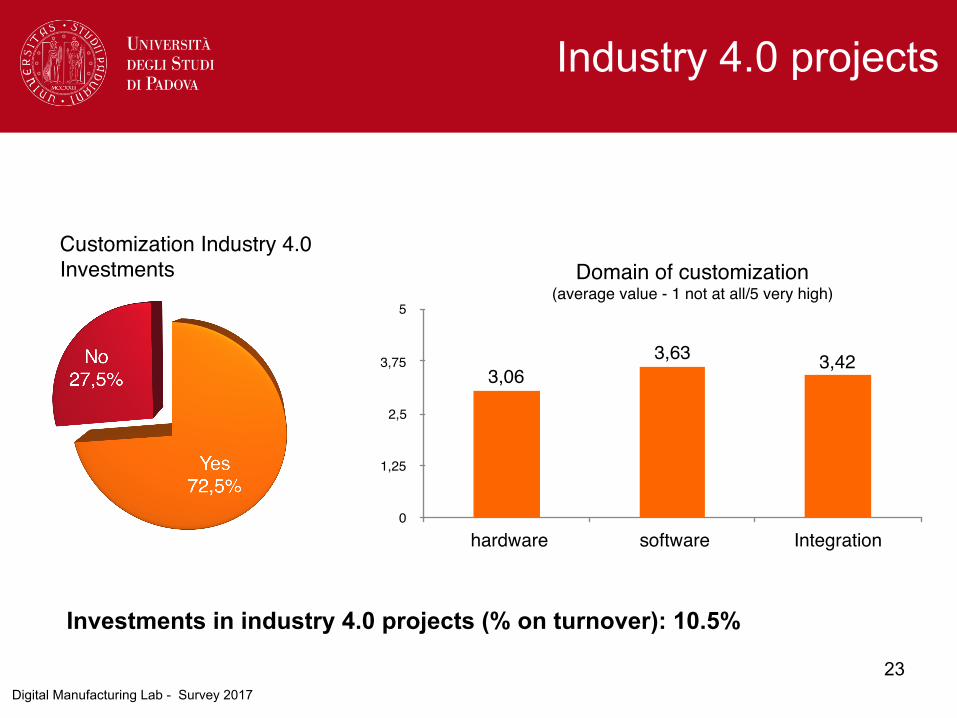

hardware software Integration

3,423,633,06

23Digital Manufacturing Lab - Survey 2017

Industry 4.0 projects

Investments in industry 4.0 projects (% on turnover): 10.5%

Customization Industry 4.0 Investments Domain of customization

(average value - 1 not at all/5 very high)

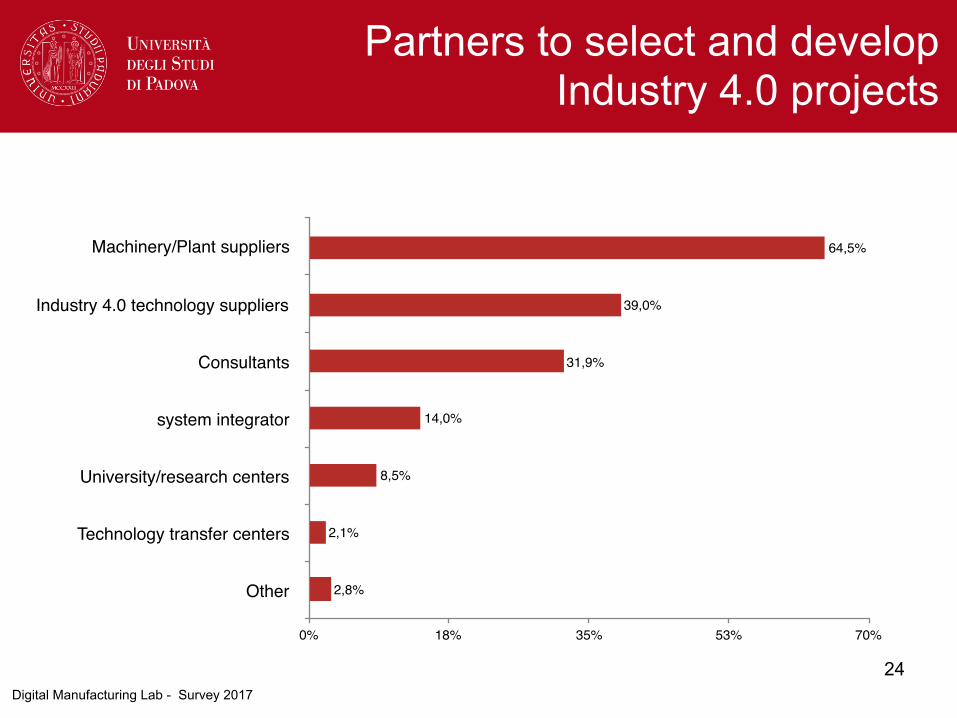

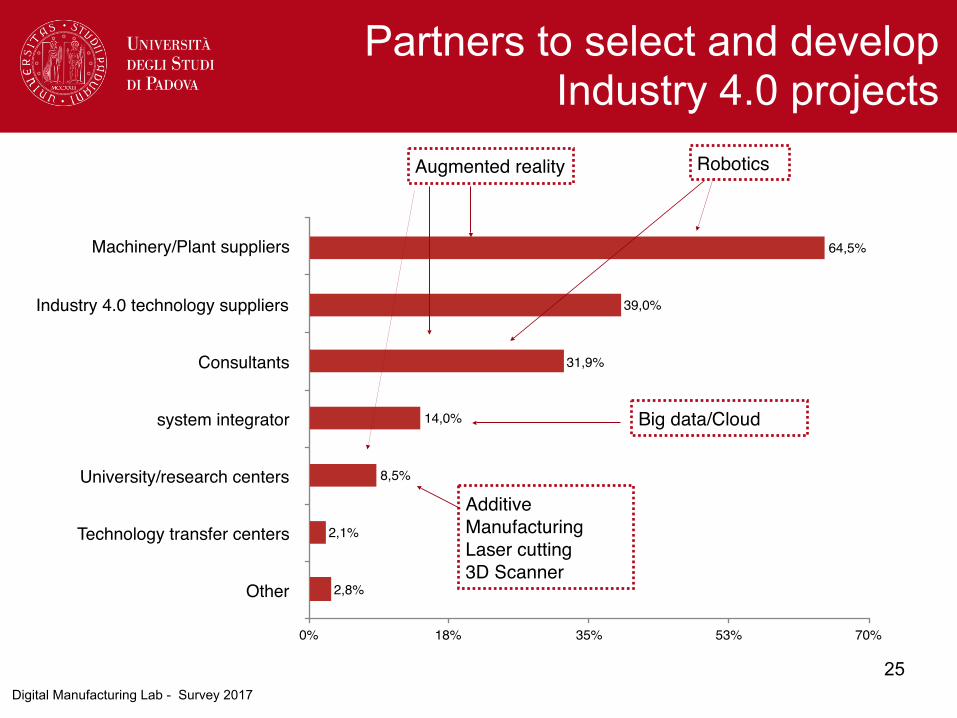

Machinery/Plant suppliers

Industry 4.0 technology suppliers

Consultants

system integrator

University/research centers

Technology transfer centers

Other

0% 18% 35% 53% 70%

2,8%

2,1%

8,5%

14,0%

31,9%

39,0%

64,5%

24Digital Manufacturing Lab - Survey 2017

Partners to select and develop Industry 4.0 projects

Machinery/Plant suppliers

Industry 4.0 technology suppliers

Consultants

system integrator

University/research centers

Technology transfer centers

Other

0% 18% 35% 53% 70%

2,8%

2,1%

8,5%

14,0%

31,9%

39,0%

64,5%

25

Robotics

Additive ManufacturingLaser cutting3D Scanner

Big data/Cloud

Augmented reality

Digital Manufacturing Lab - Survey 2017

Partners to select and develop Industry 4.0 projects

Reasons for investments and results achieved

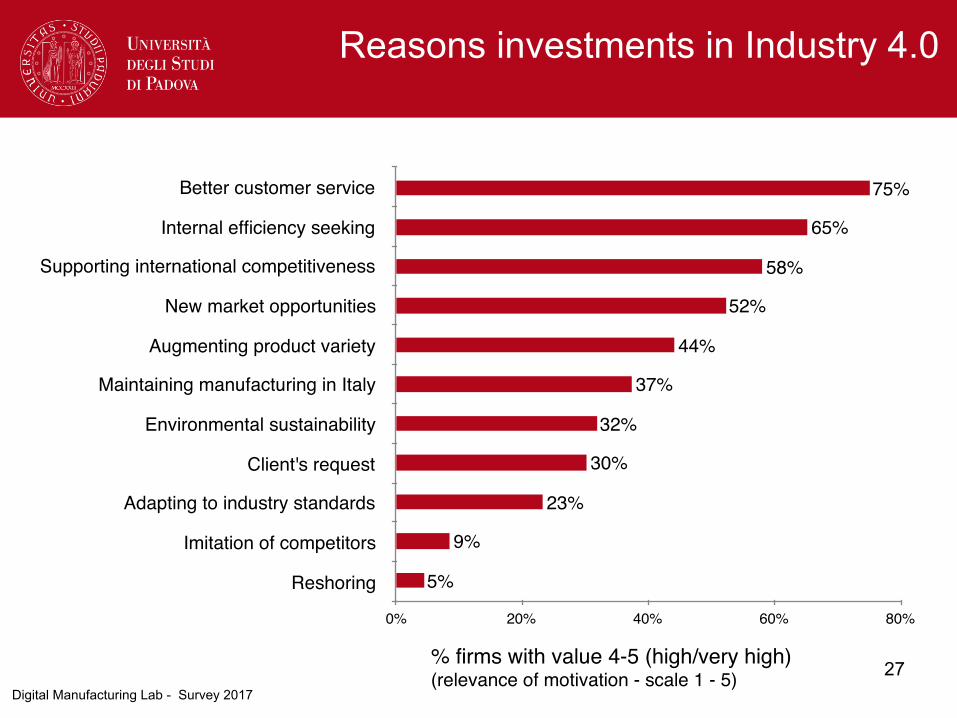

26

Better customer service

Internal efficiency seeking

Supporting international competitiveness

New market opportunities

Augmenting product variety

Maintaining manufacturing in Italy

Environmental sustainability

Client's request

Adapting to industry standards

Imitation of competitors

Reshoring

0% 20% 40% 60% 80%

5%

9%

23%

30%

32%

37%

44%

52%

58%

65%

75%

27Digital Manufacturing Lab - Survey 2017

Reasons investments in Industry 4.0

% firms with value 4-5 (high/very high)(relevance of motivation - scale 1 - 5)

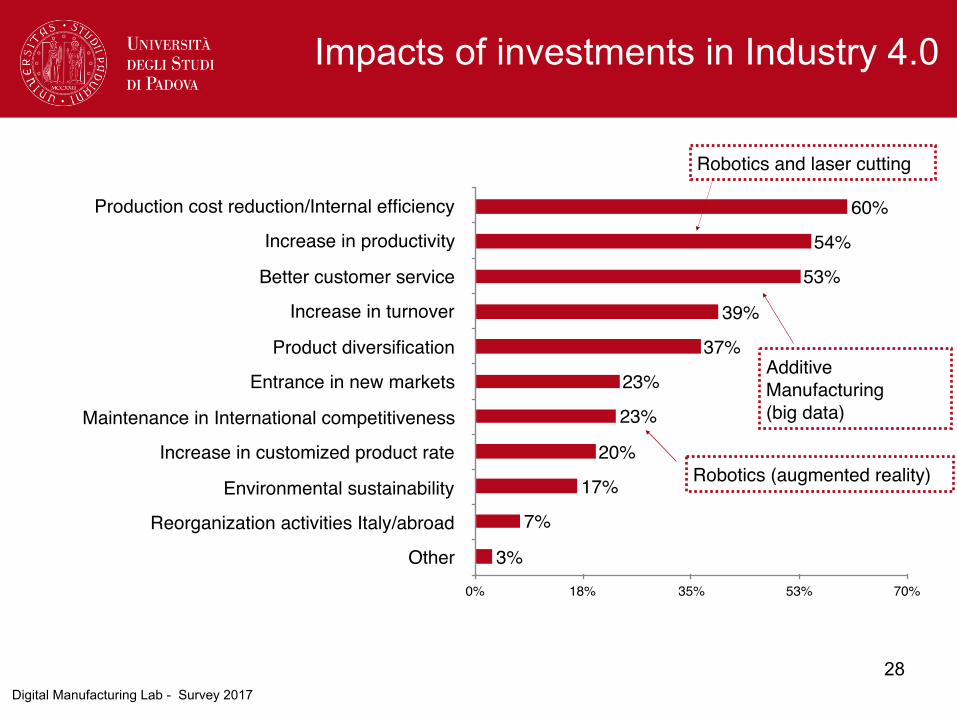

Production cost reduction/Internal efficiency

Increase in productivity

Better customer service

Increase in turnover

Product diversification

Entrance in new markets

Maintenance in International competitiveness

Increase in customized product rate

Environmental sustainability

Reorganization activities Italy/abroad

Other0% 18% 35% 53% 70%

3%

7%

17%

20%

23%

23%

37%

39%

53%

54%

60%

28Digital Manufacturing Lab - Survey 2017

Impacts of investments in Industry 4.0

Robotics and laser cutting

Additive Manufacturing(big data)

Robotics (augmented reality)

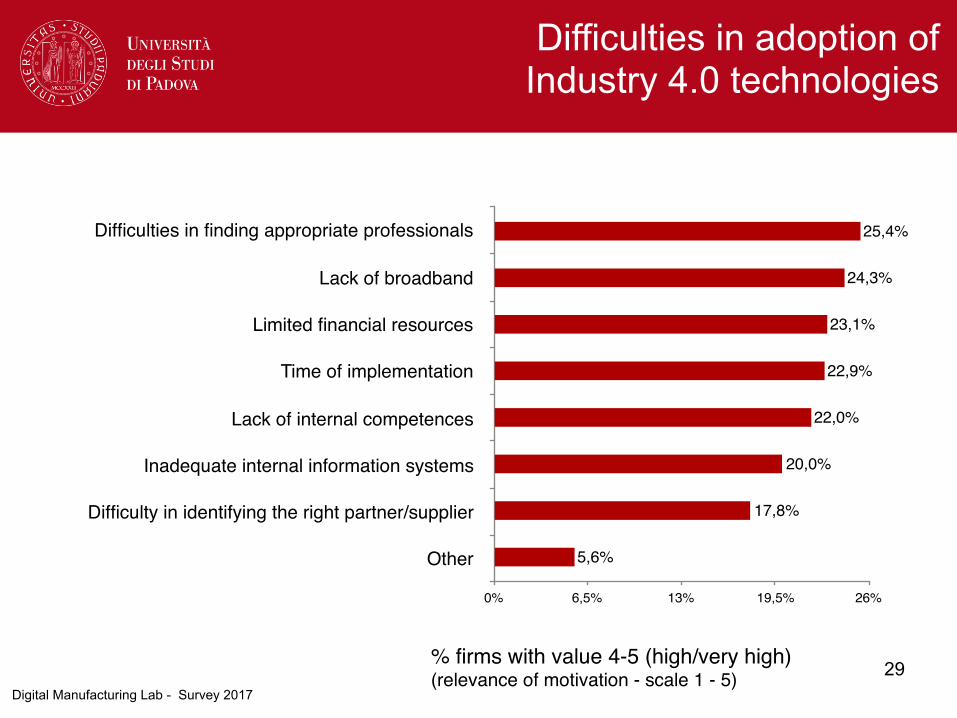

Difficulties in finding appropriate professionals

Lack of broadband

Limited financial resources

Time of implementation

Lack of internal competences

Inadequate internal information systems

Difficulty in identifying the right partner/supplier

Other

0% 6,5% 13% 19,5% 26%

5,6%

17,8%

20,0%

22,0%

22,9%

23,1%

24,3%

25,4%

29Digital Manufacturing Lab - Survey 2017

Difficulties in adoption of Industry 4.0 technologies

% firms with value 4-5 (high/very high)(relevance of motivation - scale 1 - 5)

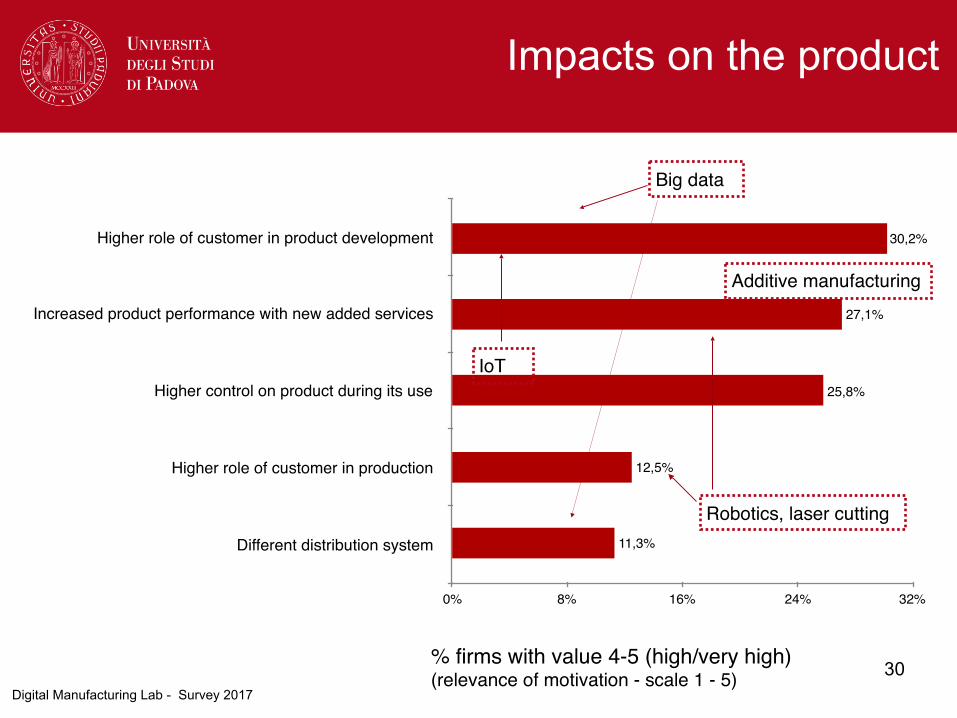

Higher role of customer in product development

Increased product performance with new added services

Higher control on product during its use

Higher role of customer in production

Different distribution system

0% 8% 16% 24% 32%

11,3%

12,5%

25,8%

27,1%

30,2%

30Digital Manufacturing Lab - Survey 2017

Impacts on the product

% firms with value 4-5 (high/very high)(relevance of motivation - scale 1 - 5)

Robotics, laser cutting

Additive manufacturing

Big data

IoT

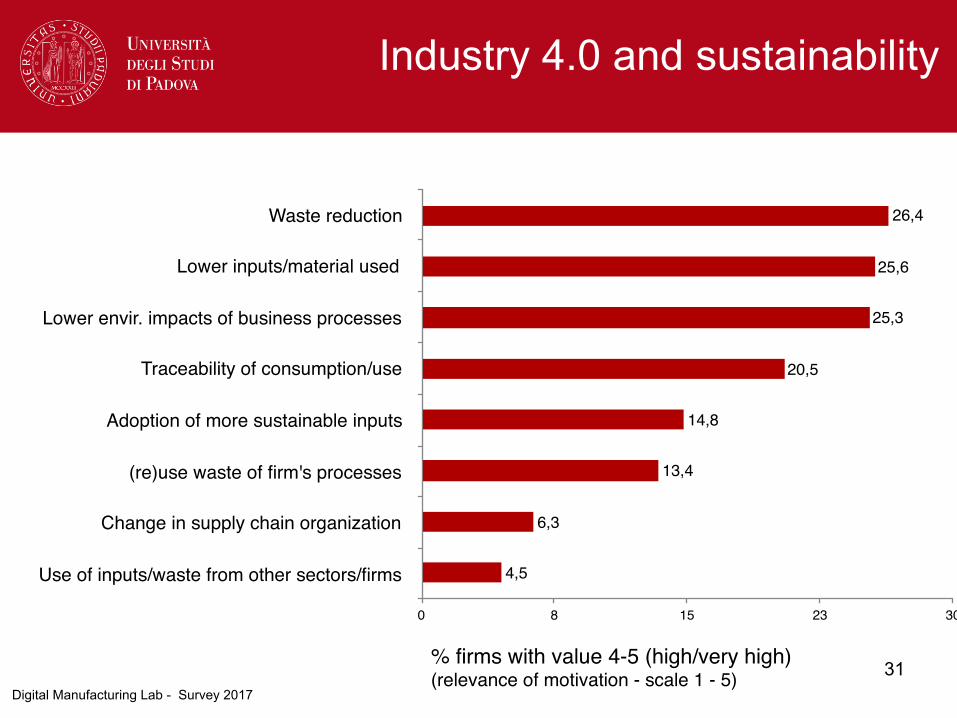

Waste reduction

Lower inputs/material used

Lower envir. impacts of business processes

Traceability of consumption/use

Adoption of more sustainable inputs

(re)use waste of firm's processes

Change in supply chain organization

Use of inputs/waste from other sectors/firms

0 8 15 23 30

4,5

6,3

13,4

14,8

20,5

25,3

25,6

26,4

31Digital Manufacturing Lab - Survey 2017

Industry 4.0 and sustainability

% firms with value 4-5 (high/very high)(relevance of motivation - scale 1 - 5)

Employment

32

33Digital Manufacturing Lab - Survey 2017

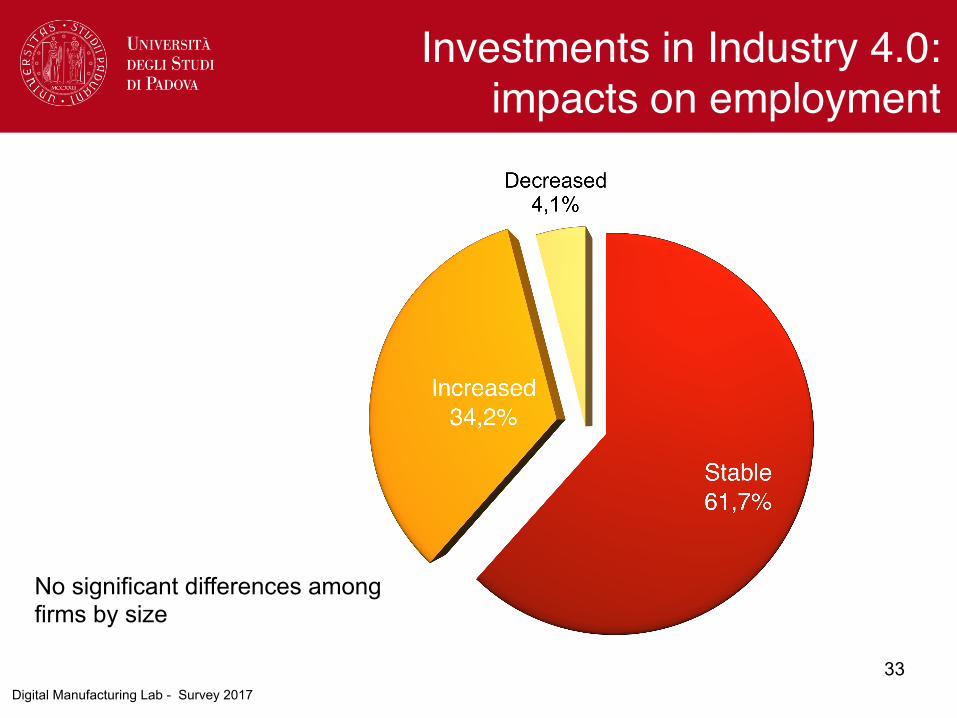

Investments in Industry 4.0: impacts on employment

No significant differences among firms by size

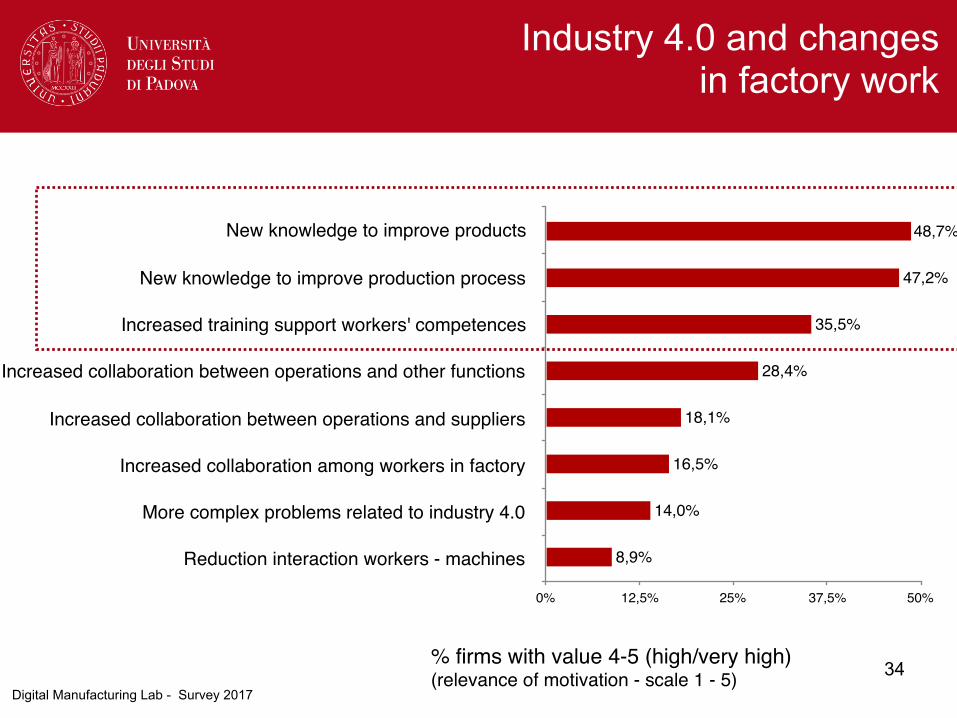

Industry 4.0 and changes in factory work

New knowledge to improve products

New knowledge to improve production process

Increased training support workers' competences

Increased collaboration between operations and other functions

Increased collaboration between operations and suppliers

Increased collaboration among workers in factory

More complex problems related to industry 4.0

Reduction interaction workers - machines

0% 12,5% 25% 37,5% 50%

8,9%

14,0%

16,5%

18,1%

28,4%

35,5%

47,2%

48,7%

34Digital Manufacturing Lab - Survey 2017

% firms with value 4-5 (high/very high)(relevance of motivation - scale 1 - 5)

Industry 4.0 and business performance

35

Investimenti industria 4.0 e performance

• Positive impacts of industry 4.0 investments on business performance (analysis on average EBIDTA/sales and Sales growth 2014-2016 between adopters and non-adopters)

• In particular positive impact refers only to the adoption of 1 or 2 technologies (not significant for higher number of technologies)

36Digital Manufacturing Lab - Survey 2017

37

Executive summary

• Results on more than 1,000 imprese (including textile and apparel) confirm a process of adoption • still limited (about 19%)• that involve also small firms (more than 40% of adopters)• implemented for a long time (average years of adoption

between 2008 and 2014) • with industry variety (industry of specialization impacts

on this process)• market-driven (first reason: better customer service)

• Adopters are innovative firms, often with already implemented ICT investments

38Digital Manufacturing Lab - Survey 2017

Executive summary 1

• Technologies are applied differently within the firm: 3D printing mainly in prototyping and new product development, robots in operations, big data for operations management and marketing.

• Industry 4.0 technologies are adopted mainly to product customized products. 66.6% of adopters produce bespoke or customized products, while only 33.4% of them standard products.

• Investments in Industry 4.0 technologies/projects have increased firm’s innovation capabilities.

39Digital Manufacturing Lab - Survey 2017

Executive summary 2

• Impact-wise, firms mention three main results achieved: efficiency (60%), increase in productivity (54%),increase in quality of customer service (53%), with a different role played by different technologies.

• Increased value related to product in terms of customization (co-design), related services and traceability/control on product, and environmental sustainability

• Positive relation with employment (more than 61% of adopters have maintained stable employment, while 34% has increased it), with an impact on work within the factory mainly on knowledge management (new knowledge to improve products or processes or development of competences through training)

• Positive impacts on performance (EBIDTA/sales and sales growth) in particular with 1 or 2 technologies, where the selection of technologies is aligned with business strategy (quality more than quantity, selection based on business goals

40Digital Manufacturing Lab - Survey 2017

Executive summary 3

• Those technologies require ad hoc 4.0 projects of implementations (72% of adopters), they are not off-the-shelf technologies ready to be used immediately. Accompanying activities are essential and the primary partners are firm’s technological suppliers (even though a variety of partners emerges and it is linked to different technologies adopted)

• A positive relation with investments on ICT technologies • Three main difficulties in the adoption process: lack of internal/

external competences, broadband and time of implementation• The main motivation for not-adopting firms is linked to business

strategy and culture (more than 65% declare that those technologies are not of interest for their business) rather than financial motivation. This result is confirmed by the second motivation: being a small firm/artisan.

41Digital Manufacturing Lab - Survey 2017

Executive summary 4

Contact:

Prof. Eleonora Di Maria [email protected]

http://www.economia.unipd.it/en/DML/Digital-Manufacturing-Lab