dhl global forwarding, freight ocean freight market …...market outlook december 2018 – ocean...

TRANSCRIPT

1

OCEAN FREIGHT MARKET UPDATE

DHL Global Forwarding, Freight

December 2018

PUBLIC

2 2

Contents

TOPIC OF THE MONTH

IMO 2020 regulation effective 1st January 2020

HIGH LEVEL DEVELOPMENT

MARKET OUTLOOK

Freight Rates and Volume Development

ECONOMIC OUTLOOK & DEMAND DEVELOPM ENT

CAPACITY DEVELOPMENT

CARRIERS

REGULATIONS

? DID YOU KNOW?

Top 10 Carriers Capacity Share November 2018

PUBLIC

DHL Global Forwarding | OFR Market Update | Dec 2018

3 3

International Convention for the Prevention of Pollution from Ships (MARPOL)

Topic of the Month

IMO 2020 regulation effective 1st January 2020

Source: DHL

DHL Global Forwarding | OFR Market Update | Dec 2018

IMO2020 is the f irst regulation in a series of steps by the International Maritime Organization (IMO) to reduce

emissions in response to climate change. It introduces a new marine fuel regulation, w hich limits the sulphur

emissions caused by marine fuels. Sulphur, a natural element of crude oil from w hich shipping fuel is derived, is a

key cause of air-polluting particulates (soot) emitted by ships. The new sulphur level regulation is intended to

reduce the amount of air pollution generated by the shipping industry and improve air quality.

To date, ships have been able to use high sulphur fuel oil (HSFO) w ith a sulphur content of up to 3.5%. IMO2020

requires using fuel w ith a sulphur content of 0.5 % or lower and w ill come into effect as of 1st January 2020.

Ocean carriers are currently evaluating and testing three options to be compliant w ith the new regulation:

1. converting to more expensive low-sulphur fuel oil (LSFO 0.5%)

2. using Exhaust Gas Cleaning Systems (EGCSs) also called scrubbers

3. deploying ships pow ered by liquefied natural gas (LNG)

The spread between HSFO 3.5% and LSFO 0.5% is estimated approximately at USD 250 per ton, w hile the

installation of scrubbers is estimated at about USD 6 – 10 million per vessel. In regards to LNG, shipping lines

seem reluctant to use it because of the safety risks.

It is clear that this change w ill affect the entire shipping industry and the cost of compliance w ith the new

regulation w ill be significant. The ocean carriers, as w ell as the forw arders will not be able to absorb these

additional costs.

At this stage it is not possible to define the exact cost impact. We are in constant dialogue and negotiation w ith our

partner carriers and w e w ill do our outmost to mitigate the impact for our customers.

4 4

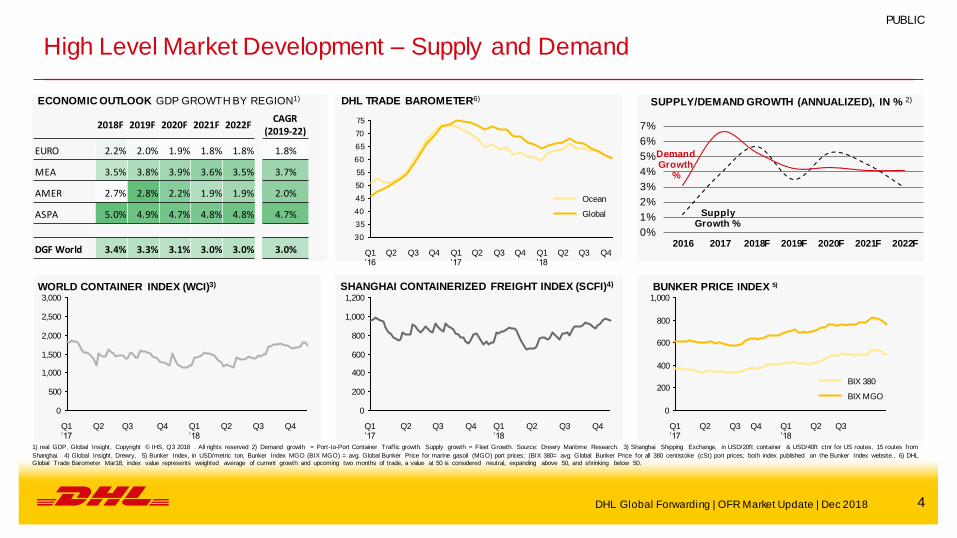

High Level Market Development – Supply and Demand

ECONOMIC OUTLOOK GDP GROWTH BY REGION1)

DHL Global Forwarding | OFR Market Update | Dec 2018

2018F 2019F 2020F 2021F 2022F CAGR

(2019-22)

EURO 2.2% 2.0% 1.9% 1.8% 1.8% 1.8%

MEA 3.5% 3.8% 3.9% 3.6% 3.5% 3.7%

AMER 2.7% 2.8% 2.2% 1.9% 1.9% 2.0%

ASPA 5.0% 4.9% 4.7% 4.8% 4.8% 4.7%

DGF World 3.4% 3.3% 3.1% 3.0% 3.0% 3.0%

PUBLIC

Supply Growth %

Demand Growth

%

0%

1%

2%

3%

4%

5%

6%

7%

2016 2017 2018F 2019F 2020F 2021F 2022F

SUPPLY/DEMAND GROWTH (ANNUALIZED), IN % 2)

1) real GDP, Global Insight, Copyright © IHS, Q3 2018 . All rights reserved 2) Demand growth = Port-to-Port Container Traffic growth. Supply growth = Fleet Growth. Source: Drewry Maritime Research. 3) Shanghai Shipping Exchange, in USD/20ft container & USD/40ft ctnr for US routes, 15 routes from

Shanghai. 4) Global Insight, Drewry, 5) Bunker Index, in USD/metric ton, Bunker Index MGO (BIX MGO) = avg. Global Bunker Price for marine gasoil (MGO) port prices; (BIX 380= avg. Global Bunker Price for all 380 centistoke (cSt) port prices; both index published on the Bunker Index website., 6) DHL Global Trade Barometer Mar18, index value represents weighted average of current growth and upcoming two months of trade, a value at 50 is considered neutral, expanding above 50, and shrinking below 50.

BUNKER PRICE INDEX 5) WORLD CONTAINER INDEX (WCI)3) SHANGHAI CONTAINERIZED FREIGHT INDEX (SCFI)4)

DHL TRADE BAROMETER6)

Q1 ’17

Q3 Q2

3,000

2,500

2,000

1,500

1,000

0

Q4 Q3 Q2

500

Q4 Q1 ’18

1,000

800

600

400

200

0

Q4 Q3 Q2 Q1 ’18

Q4 Q3

1,200

Q2 Q1 ’17

Q2 Q1 ’17

Q2 Q1 ’18

200

Q3

0

Q3 Q4

600

400

1,000

800

BIX MGO

BIX 380

30

35

40

45

50

55

60

65

70

75

Q4 Q3 Q2 Q1 ’18

Q4 Q3 Q2 Q1 ’17

Q4 Q3 Q2 Q1 ’16

Ocean

Global

5 5

Market Outlook – Volume Outlook in Main Trade Lanes, 2018 Estimate &

2019/22 Growth Forecast in %

N O R T H A M E R I C A

I n c l . M E X I C O

4.0 mTEU +2.4%

2.2 mTEU +3.1%

1.6 mTEU +4.3%

1.7 mTEU +2.5%

N O R T H A M E R I C A

I n c l . M E X I C O

L A T I N

A M E R I C A

E U R O P E

I n c l . M E D

12.8 mTEU +2.4%

7.3 mTEU +3.4%

8.5 mTEU +4.7%

18.7 mTEU +3.1%

1.7 mTEU +2.2%

4.2 mTEU +4.6%

2018e, in mTEU 2019e-2022e CAGR, in %

F A R E A S T

I N T R A A S I A

excl. Oceania

41.6 mTEU +4.8%

2.0 mTEU

+4.5%

1.6 mTEU

+4.3%

L A T I N

A M E R I C A

G L O B A L C O N T A I N E R T R A D E 2 0 1 8 e 1 5 2 . 6 m T E U + 4 . 1 % C A G R 2 0 1 9 e - 2 0 2 2 e

Mid-term growth is mainly driven by Asian tradelanes.

Source: Seabury Nov18 update

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

6 6

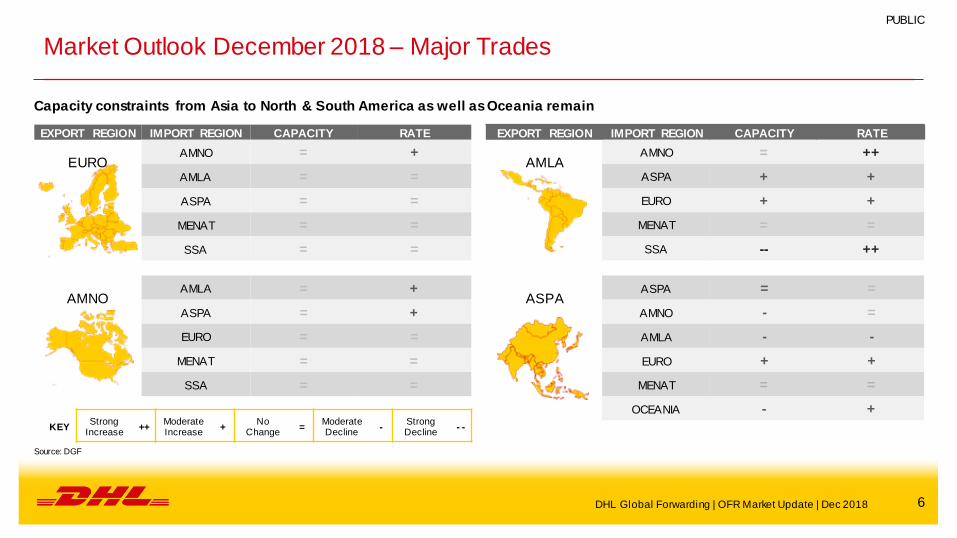

Market Outlook December 2018 – Major Trades

Capacity constraints from Asia to North & South America as well as Oceania remain

KEY Strong

Increase ++

Moderate Increase

+ No

Change =

Moderate Decline

- Strong Decline

- -

EXPORT REGION IMPORT REGION CAPACITY RATE

EURO AMNO = +

AMLA = =

ASPA = =

MENAT = =

SSA = =

AMNO AMLA = +

ASPA = +

EURO = =

MENAT = =

SSA = =

EXPORT REGION IMPORT REGION CAPACITY RATE

AMLA AMNO = ++

ASPA + +

EURO + +

MENAT = =

SSA -- ++

ASPA ASPA = =

AMNO - =

AMLA - -

EURO + +

MENAT = =

OCEANIA - +

DHL Global Forwarding | OFR Market Update | Dec 2018

Source: DGF

PUBLIC

7 7

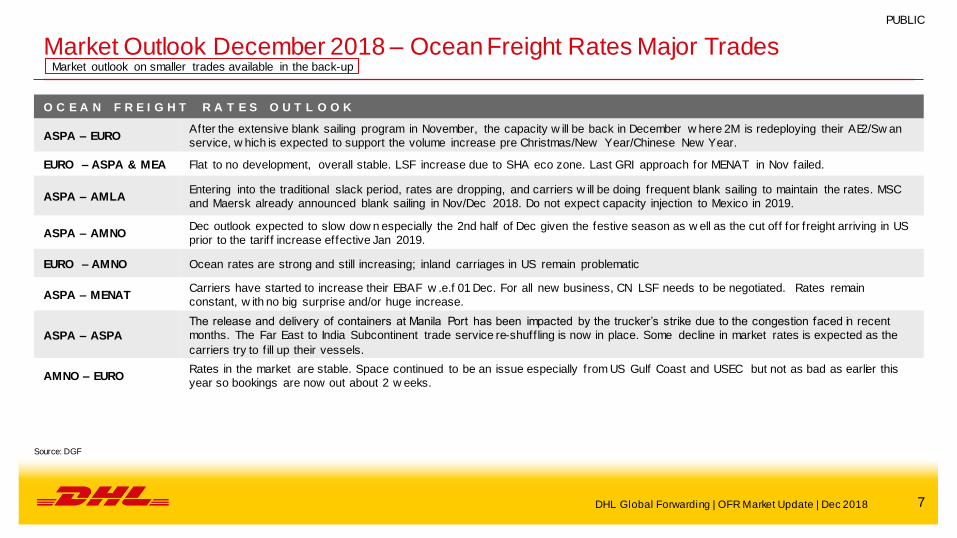

Market Outlook December 2018 – Ocean Freight Rates Major Trades Market outlook on smaller trades available in the back-up

O C E A N F R E I G H T R A T E S O U T L O O K

ASPA – EURO After the extensive blank sailing program in November, the capacity w ill be back in December w here 2M is redeploying their AE2/Sw an

service, w hich is expected to support the volume increase pre Christmas/New Year/Chinese New Year.

EURO – ASPA & MEA Flat to no development, overall stable. LSF increase due to SHA eco zone. Last GRI approach for MENAT in Nov failed.

ASPA – AMLA Entering into the traditional slack period, rates are dropping, and carriers w ill be doing frequent blank sailing to maintain the rates. MSC

and Maersk already announced blank sailing in Nov/Dec 2018. Do not expect capacity injection to Mexico in 2019.

ASPA – AMNO Dec outlook expected to slow dow n especially the 2nd half of Dec given the festive season as w ell as the cut off for freight arriving in US

prior to the tariff increase effective Jan 2019.

EURO – AMNO Ocean rates are strong and still increasing; inland carriages in US remain problematic

ASPA – MENAT Carriers have started to increase their EBAF w .e.f 01 Dec. For all new business, CN LSF needs to be negotiated. Rates remain

constant, w ith no big surprise and/or huge increase.

ASPA – ASPA

The release and delivery of containers at Manila Port has been impacted by the trucker’s strike due to the congestion faced in recent

months. The Far East to India Subcontinent trade service re-shuffling is now in place. Some decline in market rates is expected as the

carriers try to f ill up their vessels.

AMNO – EURO Rates in the market are stable. Space continued to be an issue especially from US Gulf Coast and USEC but not as bad as earlier this

year so bookings are now out about 2 w eeks.

DHL Global Forwarding | OFR Market Update | Dec 2018

Source: DGF

PUBLIC

8 8

Economic Outlook & Demand Development

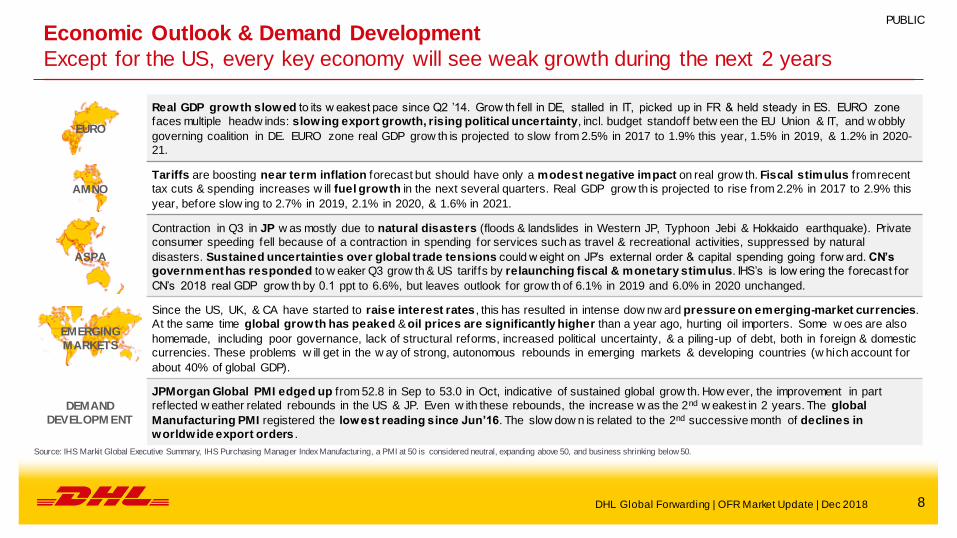

Except for the US, every key economy will see weak growth during the next 2 years

Source: IHS Markit Global Executive Summary, IHS Purchasing Manager Index Manufacturing, a PMI at 50 is considered neutral, expanding above 50, and business shrinking below 50.

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

EURO

Real GDP growth slowed to its w eakest pace since Q2 ’14. Grow th fell in DE, stalled in IT, picked up in FR & held steady in ES. EURO zone

faces multiple headw inds: slowing export growth, rising political uncertainty, incl. budget standoff betw een the EU Union & IT, and w obbly

governing coalition in DE. EURO zone real GDP grow th is projected to slow from 2.5% in 2017 to 1.9% this year, 1.5% in 2019, & 1.2% in 2020-

21.

AMNO

Tariffs are boosting near term inflation forecast but should have only a modest negative impact on real grow th. Fiscal stimulus from recent

tax cuts & spending increases w ill fuel growth in the next several quarters. Real GDP grow th is projected to rise from 2.2% in 2017 to 2.9% this

year, before slow ing to 2.7% in 2019, 2.1% in 2020, & 1.6% in 2021.

ASPA

Contraction in Q3 in JP w as mostly due to natural disasters (floods & landslides in Western JP, Typhoon Jebi & Hokkaido earthquake). Private

consumer speeding fell because of a contraction in spending for services such as travel & recreational activities, suppressed by natural

disasters. Sustained uncertainties over global trade tensions could w eight on JP’s external order & capital spending going forw ard. CN’s

government has responded to w eaker Q3 grow th & US tariffs by relaunching fiscal & monetary stimulus. IHS’s is low ering the forecast for

CN’s 2018 real GDP grow th by 0.1 ppt to 6.6%, but leaves outlook for grow th of 6.1% in 2019 and 6.0% in 2020 unchanged.

EMERGING

MARKETS

Since the US, UK, & CA have started to raise interest rates , this has resulted in intense dow nw ard pressure on emerging-market currencies.

At the same time global growth has peaked & oil prices are significantly higher than a year ago, hurting oil importers. Some w oes are also

homemade, including poor governance, lack of structural reforms, increased political uncertainty, & a piling-up of debt, both in foreign & domestic

currencies. These problems w ill get in the w ay of strong, autonomous rebounds in emerging markets & developing countries (w hich account for

about 40% of global GDP).

DEMAND

DEVELOPM ENT

JPMorgan Global PMI edged up from 52.8 in Sep to 53.0 in Oct, indicative of sustained global grow th. How ever, the improvement in part

reflected w eather related rebounds in the US & JP. Even w ith these rebounds, the increase w as the 2nd w eakest in 2 years. The global

Manufacturing PMI registered the lowest reading since Jun’16. The slow dow n is related to the 2nd successive month of declines in

worldwide export orders .

9 9

Capacity Development 1/2

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Alphaliner, carriers

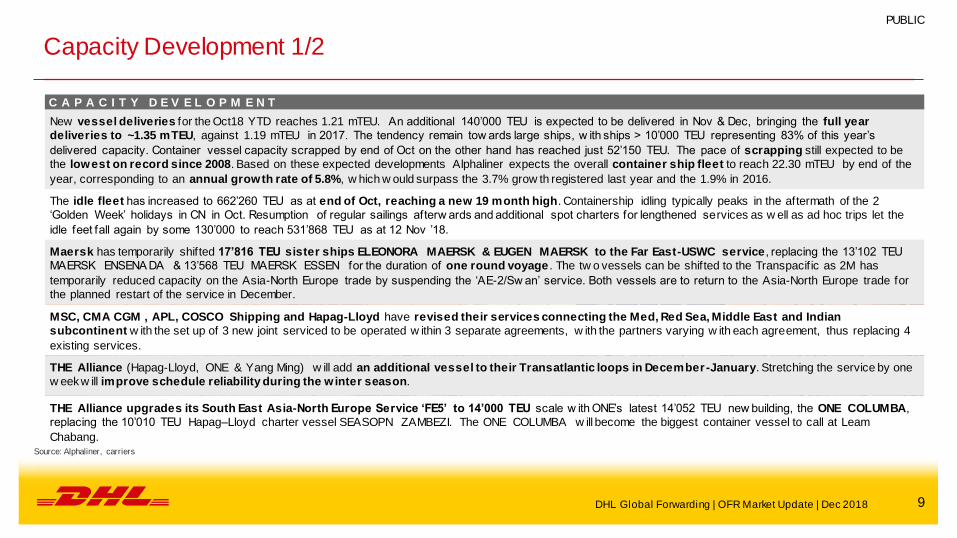

C A P A C I T Y D E V E L O P M E N T

New vessel deliveries for the Oct18 YTD reaches 1.21 mTEU. An additional 140’000 TEU is expected to be delivered in Nov & Dec, bringing the full year

deliveries to ~1.35 mTEU, against 1.19 mTEU in 2017. The tendency remain tow ards large ships, w ith ships > 10’000 TEU representing 83% of this year’s

delivered capacity. Container vessel capacity scrapped by end of Oct on the other hand has reached just 52’150 TEU. The pace of scrapping still expected to be

the lowest on record since 2008. Based on these expected developments Alphaliner expects the overall container ship fleet to reach 22.30 mTEU by end of the

year, corresponding to an annual growth rate of 5.8%, w hich w ould surpass the 3.7% grow th registered last year and the 1.9% in 2016.

The idle fleet has increased to 662’260 TEU as at end of Oct, reaching a new 19 month high. Containership idling typically peaks in the aftermath of the 2

‘Golden Week’ holidays in CN in Oct. Resumption of regular sailings afterw ards and additional spot charters for lengthened services as w ell as ad hoc trips let the

idle feet fall again by some 130’000 to reach 531’868 TEU as at 12 Nov ’18.

Maersk has temporarily shifted 17’816 TEU sister ships ELEONORA MAERSK & EUGEN MAERSK to the Far East-USWC service , replacing the 13’102 TEU

MAERSK ENSENA DA & 13’568 TEU MAERSK ESSEN for the duration of one round voyage . The tw o vessels can be shifted to the Transpacif ic as 2M has

temporarily reduced capacity on the Asia-North Europe trade by suspending the ‘AE-2/Sw an’ service. Both vessels are to return to the Asia-North Europe trade for

the planned restart of the service in December.

MSC, CMA CGM , APL, COSCO Shipping and Hapag-Lloyd have revised their services connecting the Med, Red Sea, Middle East and Indian

subcontinent w ith the set up of 3 new joint serviced to be operated w ithin 3 separate agreements, w ith the partners varying w ith each agreement, thus replacing 4

existing services.

THE Alliance (Hapag-Lloyd, ONE & Yang Ming) w ill add an additional vessel to their Transatlantic loops in December-January. Stretching the service by one

w eek w ill improve schedule reliability during the winter season.

THE Alliance upgrades its South East Asia-North Europe Service ‘FE5’ to 14’000 TEU scale w ith ONE’s latest 14’052 TEU new building, the ONE COLUMBA,

replacing the 10’010 TEU Hapag–Lloyd charter vessel SEASOPN ZAMBEZI. The ONE COLUMBA w ill become the biggest container vessel to call at Leam

Chabang.

10 10

Capacity Development 2/2

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Alphaliner, carriers

C A P A C I T Y D E V E L O P M E N T

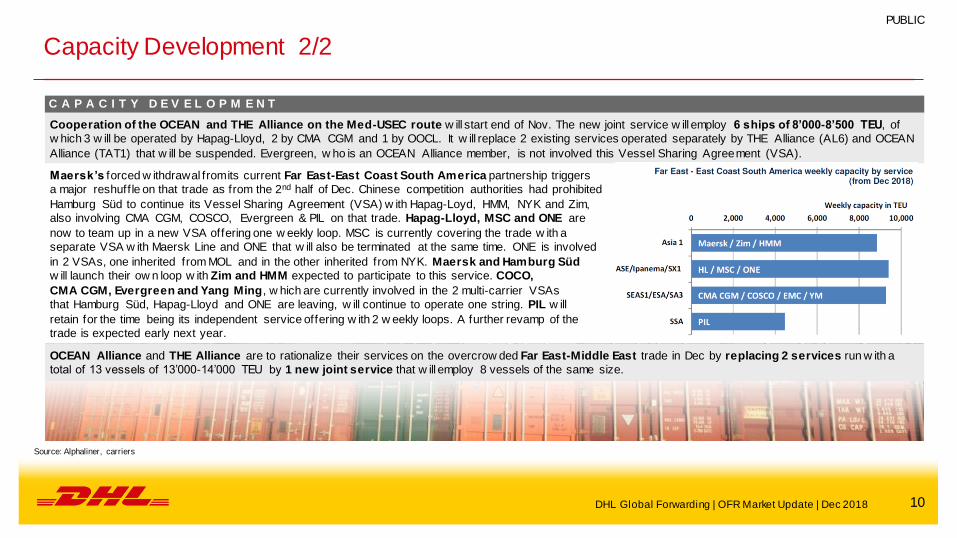

Cooperation of the OCEAN and THE Alliance on the Med-USEC route w ill start end of Nov. The new joint service w ill employ 6 ships of 8’000-8’500 TEU, of

w hich 3 w ill be operated by Hapag-Lloyd, 2 by CMA CGM and 1 by OOCL. It w ill replace 2 existing services operated separately by THE Alliance (AL6) and OCEAN

Alliance (TAT1) that w ill be suspended. Evergreen, w ho is an OCEAN Alliance member, is not involved this Vessel Sharing Agreement (VSA).

Maersk’s forced w ithdrawal from its current Far East-East Coast South America partnership triggers

a major reshuff le on that trade as from the 2nd half of Dec. Chinese competition authorities had prohibited

Hamburg Süd to continue its Vessel Sharing Agreement (VSA) w ith Hapag-Loyd, HMM, NYK and Zim,

also involving CMA CGM, COSCO, Evergreen & PIL on that trade. Hapag-Lloyd, MSC and ONE are

now to team up in a new VSA offering one w eekly loop. MSC is currently covering the trade w ith a

separate VSA w ith Maersk Line and ONE that w ill also be terminated at the same time. ONE is involved

in 2 VSAs, one inherited from MOL and in the other inherited from NYK. Maersk and Hamburg Süd

w ill launch their ow n loop w ith Zim and HMM expected to participate to this service. COCO,

CMA CGM, Evergreen and Yang Ming, w hich are currently involved in the 2 multi-carrier VSAs

that Hamburg Süd, Hapag-Lloyd and ONE are leaving, w ill continue to operate one string. PIL w ill

retain for the time being its independent service offering w ith 2 w eekly loops. A further revamp of the

trade is expected early next year.

OCEAN Alliance and THE Alliance are to rationalize their services on the overcrow ded Far East-Middle East trade in Dec by replacing 2 services run w ith a

total of 13 vessels of 13’000-14’000 TEU by 1 new joint service that w ill employ 8 vessels of the same size.

11 11

Carriers – Q3 ’18 Results (1/2)

Source: Alphaliner, carriers

C A R R I E R S

OOCL volumes grow amidst stagnating freight rates. Total liftings increased by 6.9% to reach a record of 1.71 mTEU but freight rates remained flat at

USD910/TEU. Transpacific trade show ed the best grow th w ith 7.3% volume increase w hile average rates increased by 7.6%. Asia-Europe on the other hand

saw volume growth of 10.4% but average freight rates fell by -9.5%. The intra-Asia & Australasia volumes also grew by 6.6% but rates fell by -4%. The

Transatlantic trade registered a -1.5% volume decline but rates increased by 5.5%.

Would COSCO not have received 1’125 mRMB (162 mUSD) in subsidies form the CN Government for scrapping 8 vessels in 2016 & 2017, their Q3 earnings

w ould have been negative. The carrier could now post a net profit of 822 mRMB for Q3 w hile liftings increased by 7.3% to 5.02mTEU. The additional OOCL

liftings of 1.71 mTEU w ould bring the group’s consolidated liftings to 6.7 mTEU.

In line w ith their profit w arning from 16 Oct, ONE reports -192 mUSD net loss in Q3 (f iscal Q2), bringing its total losses for the f irst 6 months of its operations to

311 mUSD. ONE blames lower liftings, higher empty repositioning costs and a shortfall in expected cost savings for the result. Although lif tings on the

Asia-North America & Asia-Europe route have recovered and utilization has reached 90% on the headhaul, the backhaul has remained w eak at only 33% from

North America & 47% from Europe. ONE has also adjusted its projected synergy cost savings target of 240 m to only 160 mUSD due to higher fuel consumption

caused by unexpected w eather delays.

Hapag-Lloyd posts 112 mEUR net profit in Q3, its best quarter since 2015. The improved results came from record liftings of 3.05 mTEU, an increase of 8.7%

over the same quarter last year. It also benefitted from increasing freight rates, even though the average rate of 1’055 USD/TEU w as 1% low er than in the same

quarter last year. Rate declines on the Middle East trade w ere offset by increases on the Transpacif ic, Transatlantic and Lat in America trades.

Yang Ming has reported a net loss of -910 mNTD (30 mUSD) in Q3, extending its cumulative net loss YTD to 6.67 bnNTD (220 mUSD). An increase in total

liftings to a record of 1.41 mTEU during the quarter w as not enough to lif t the carrier out of the red. Total revenue increased by 8.2%. Yang Ming blamed the

continued supply-demand imbalance for the weak freight rates and the higher bunker fuel costs for the negative performance. The company w ill introduce

four 14’000 TEU chartered new buildings next year, w hile returning 7 higher-cost chartered vessels.

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Alphaliner, Dynaliners, carriers

12 12

Carriers – Q3 ’18 Results (2/2)

Source: Alphaliner, carriers

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Alphaliner, Dynaliners, carriers

C A R R I E R S

Maersk Ocean has posted an increase in top line revenue & EBITDA in Q3 , mainly due to the addition of Hamburg Süd. Total revenue reached 7’321 mUSD

(+32%), EBITDA 925 mUSD (+16%). How ever, EBITDA margins dropped from 14.4% to 12.6% due to higher bunker costs and lower than expected liftings .

Liftings w ere 26.7% higher in YoY but fell -1.9% compared to Q2 due to low er volumes in Europe & LATAM. Maersk also failed to capitalize on the Transpacif ic

volume strength due to its relative under-w eight position on that trade.

With an operating loss of -110 bnKRW (-98 mUSD) in Q3 HMM is now loss–making for 16 consecutive quarters. Its operating margin of -8.6% leaves the carrier

at the bottom of the main carriers. HMM failed to capitalize on rising liftings and freight rates during the quarter and continues to suffer from high operating

costs w hile capacity utilization was reported to have dropped from 79.3% in Q2 to 79.0% in Q3.

CMA CGM posts net profits of 103 mUSD in Q3, reversing the negative results of the 1st half of the year. Operating profits (core EBIT) reached 2’241 mUSD

for a positive operating margin of 4.0%. Total liftings reached 5.26 mTEU (+5.5% YoY) w hile average freight rates increased by +0.8% YoY and +4.9% QoQ

to 1’154 USD/TEU mainly due to gains on the transpacif ic. Fuel costs increase to 922 mUSD (+49%) YoY resulting in reduced margins.

Zim ’s revenue rose 2.4 bnUSD (+8%) in Q3, w hile liftings increased by +13% to 2.2 mTEU. Revenue per TEU dropped by -4% to USD 1’089, EBITDA by -

60% and net results turned from a positive 31 mUSD to -74 mUSD.

13 13

Carriers

Source: Alphaliner, carriers

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Alphaliner, Dynaliners, carriers

C A R R I E R S

CMA CGM has received regulatory approval from the EU Commission to take over the shortsea carrier “Containerships” on 31 Oct ’18. The transaction w as

announced on 20 June. All container logistics operations are to be integrated in CMA CGM’s intra-regional market offering in North Europe and the Mediterranean.

Costamar Shipping agreed to install scrubbers and increase the charter rates for 5 vessels that are currently on 10-year charters to MSC. The ships involved

are the 2014-built 9’403 TEU container vessels MSC AZOV, MSC AJACIO & MSC AMALFI and the 2013-built 8’827 TEU MSC ATHENS & MSC ATHOS.

Capital Product Partners have agreed w ith HMM to equip w ith scrubbers five 5’023 TEU widebeam container vessels currently on long term charters to

HMM. The 5 ships involved all delivered in 2013 w ith 12-year charters from Capital. Effective 1 Jan ’20 or from the installation date of the scrubbers, HMM w ill pay

USD 4’900 per day more for the charter hire of each ship. As the charters run until 2025 HMM w ould pay an extra of 9 mUSD per ship.

Yang Ming opts for scrubbers on 8 newbuildings of 2’800 TEU ordered in Aug ’18. The price has been revised in Nov by 4 mUSD per ship due to “new

installation of marine equipment”, that is believed to be related to the installation of scrubber on the ships.

Maersk has committed 80 mUSD for the installation of scrubbers and retrofitting for a selected part of its f leet. Alphaliner estimates that 10-20 vessels will be

f itted based at a reported cost of betw een 4 mUSD and 8 mUSD each.

Hapag-Lloyd has ordered 10 scrubbers to be retrofitted on its HAMBURG EXPRESS 13’169 TEU class vessels. Earlier the carrier had already disclosed a pilot

project to convert one of its vessels to LNG propulsion.

Moller-Maersk, CMA CGM, Hapag-Lloyd, MSC and ONE are discussing the creation of common IT standards w hich shall be openly available and free of

charge for all stakeholder in the container shipping industry to pave the w ay for digitalization and standardization. The founding carriers control 58% of the global

capacity but does not include some of the largest Asian carriers.

14 14

Regulations

Source: Alphaliner, carriers

R E G U L A T I O N S

South Africa: High Cube Container Notification - UPDATE

The ministry of transport has agreed in a meeting w ith representative of the Freight Association to extend the current leniency of Regulation 224 of the Road

Traff ic Act w hich means that 40 foot high cube containers can continue to be transported on standard trailers. This extension w ill be effective from 01 January

2019 until 01 January 2020.

Source: DHL

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

15 15

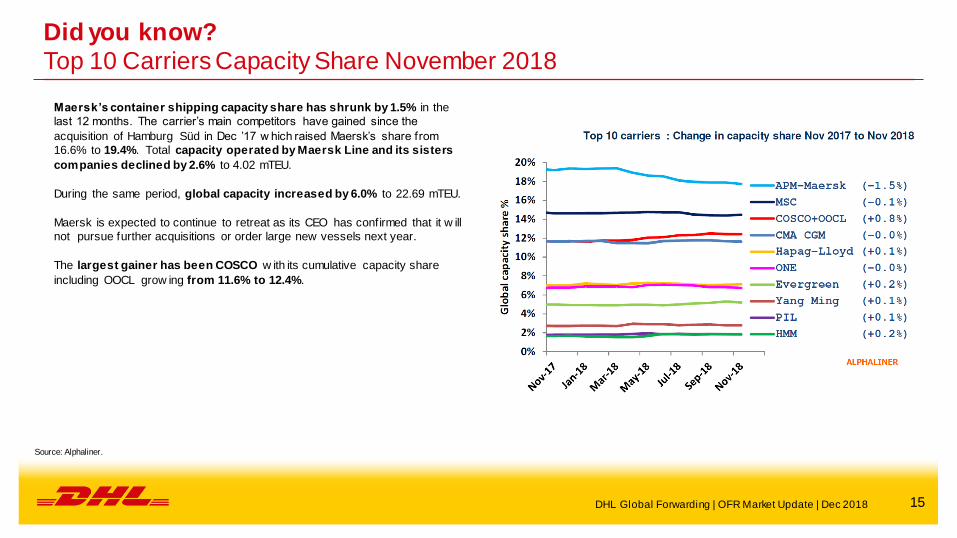

Maersk’s container shipping capacity share has shrunk by 1.5% in the

last 12 months. The carrier’s main competitors have gained since the

acquisition of Hamburg Süd in Dec ’17 w hich raised Maersk’s share from

16.6% to 19.4%. Total capacity operated by Maersk Line and its sisters

companies declined by 2.6% to 4.02 mTEU.

During the same period, global capacity increased by 6.0% to 22.69 mTEU.

Maersk is expected to continue to retreat as its CEO has confirmed that it w ill

not pursue further acquisitions or order large new vessels next year.

The largest gainer has been COSCO w ith its cumulative capacity share

including OOCL grow ing from 11.6% to 12.4%.

Did you know?

Top 10 Carriers Capacity Share November 2018

Source: Alphaliner.

DHL Global Forwarding | OFR Market Update | Dec 2018

16 16 B A C K - U P

PUBLIC

17 17

Source: DGF

Market Outlook December 2018 – Ocean Freight Rates Additional Trades (1/2)

O C E A N F R E I G H T R A T E S O U T L O O K

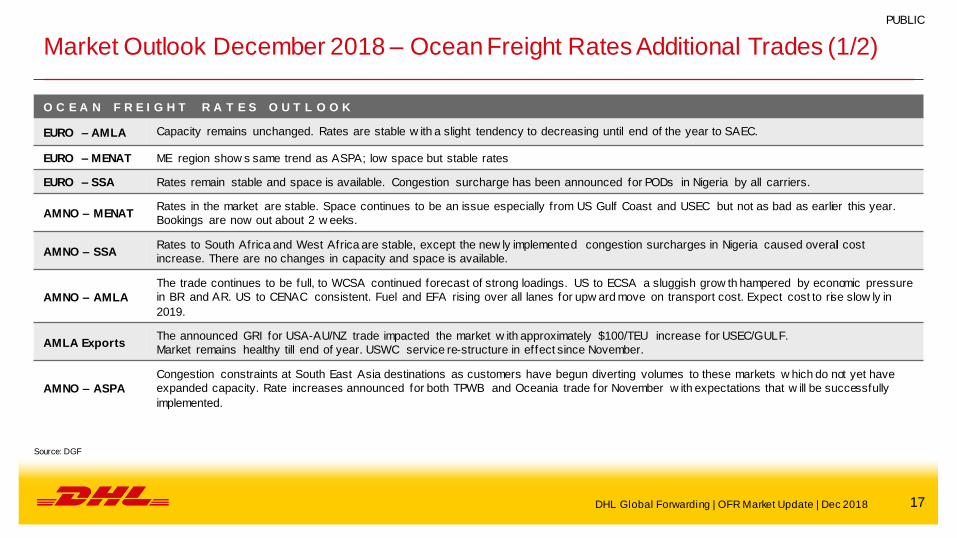

EURO – AMLA Capacity remains unchanged. Rates are stable w ith a slight tendency to decreasing until end of the year to SAEC.

EURO – MENAT ME region show s same trend as ASPA; low space but stable rates

EURO – SSA Rates remain stable and space is available. Congestion surcharge has been announced for PODs in Nigeria by all carriers.

AMNO – MENAT Rates in the market are stable. Space continues to be an issue especially from US Gulf Coast and USEC but not as bad as earlier this year.

Bookings are now out about 2 w eeks.

AMNO – SSA Rates to South Africa and West Africa are stable, except the new ly implemented congestion surcharges in Nigeria caused overall cost

increase. There are no changes in capacity and space is available.

AMNO – AMLA

The trade continues to be full, to WCSA continued forecast of strong loadings. US to ECSA a sluggish grow th hampered by economic pressure

in BR and AR. US to CENAC consistent. Fuel and EFA rising over all lanes for upw ard move on transport cost. Expect cost to rise slow ly in

2019.

AMLA Exports The announced GRI for USA-AU/NZ trade impacted the market w ith approximately $100/TEU increase for USEC/GULF.

Market remains healthy till end of year. USWC service re-structure in effect since November.

AMNO – ASPA

Congestion constraints at South East Asia destinations as customers have begun diverting volumes to these markets w hich do not yet have

expanded capacity. Rate increases announced for both TPWB and Oceania trade for November w ith expectations that w ill be successfully

implemented.

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

18 18

Market Outlook December 2018 – Ocean Freight Rates Additional Trades (2/2)

O C E A N F R E I G H T R A T E S O U T L O O K

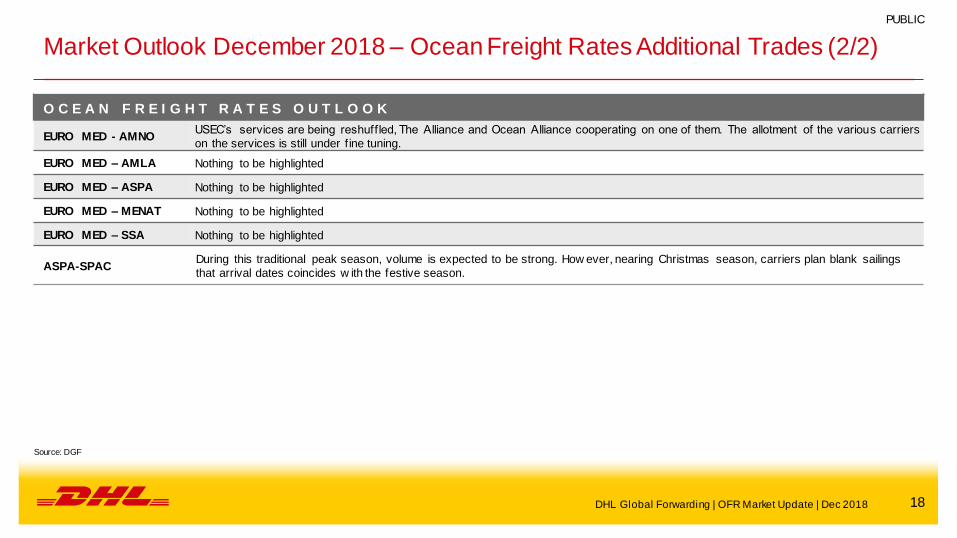

EURO MED - AMNO USEC’s services are being reshuffled, The Alliance and Ocean Alliance cooperating on one of them. The allotment of the various carriers

on the services is still under f ine tuning.

EURO MED – AMLA Nothing to be highlighted

EURO MED – ASPA Nothing to be highlighted

EURO MED – MENAT Nothing to be highlighted

EURO MED – SSA Nothing to be highlighted

ASPA-SPAC During this traditional peak season, volume is expected to be strong. How ever, nearing Christmas season, carriers plan blank sailings

that arrival dates coincides w ith the festive season.

DHL Global Forwarding | OFR Market Update | Dec 2018

Source: DGF

PUBLIC

19 19

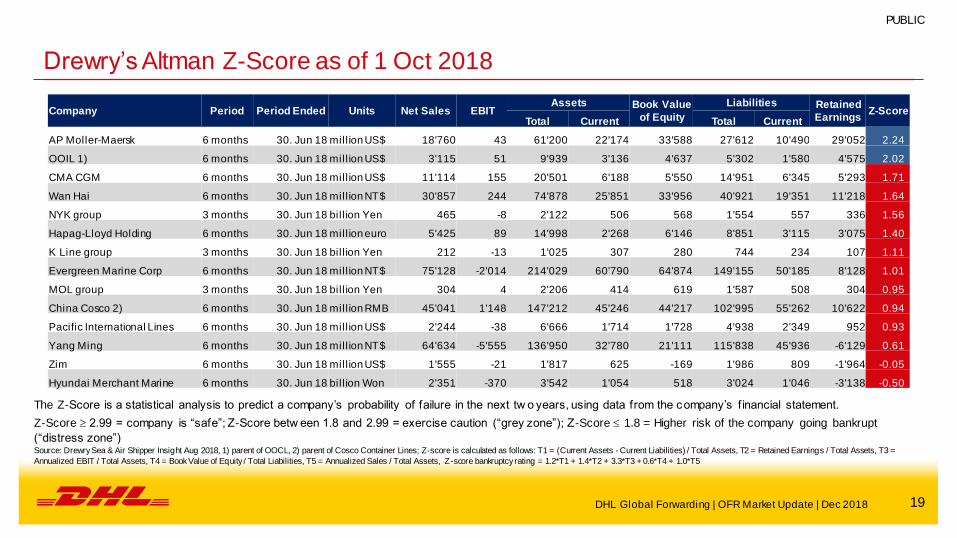

Drewry’s Altman Z-Score as of 1 Oct 2018

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC

Source: Drewry Sea & Air Shipper Insight Aug 2018, 1) parent of OOCL, 2) parent of Cosco Container Lines; Z-score is calculated as follows: T1 = (Current Assets - Current Liabilities) / Total Assets, T2 = Retained Earnings / Total Assets, T3 =

Annualized EBIT / Total Assets, T4 = Book Value of Equity / Total Liabilities, T5 = Annualized Sales / Total Assets, Z-score bankruptcy rating = 1.2*T1 + 1.4*T2 + 3.3*T3 + 0.6*T4 + 1.0*T5

The Z-Score is a statistical analysis to predict a company’s probability of failure in the next tw o years, using data from the company’s f inancial statement.

Z-Score 2.99 = company is “safe”; Z-Score betw een 1.8 and 2.99 = exercise caution (“grey zone”); Z-Score 1.8 = Higher risk of the company going bankrupt

(“distress zone”)

Company Period Period Ended Units Net Sales EBIT Assets Book Value

of Equity

Liabilities Retained

Earnings Z-Score

Total Current Total Current

AP Moller-Maersk 6 months 30. Jun 18 mill ion US$ 18'760 43 61'200 22'174 33'588 27'612 10'490 29'052 2.24

OOIL 1) 6 months 30. Jun 18 mill ion US$ 3'115 51 9'939 3'136 4'637 5'302 1'580 4'575 2.02

CMA CGM 6 months 30. Jun 18 mill ion US$ 11'114 155 20'501 6'188 5'550 14'951 6'345 5'293 1.71

Wan Hai 6 months 30. Jun 18 mill ion NT$ 30'857 244 74'878 25'851 33'956 40'921 19'351 11'218 1.64

NYK group 3 months 30. Jun 18 bill ion Yen 465 -8 2'122 506 568 1'554 557 336 1.56

Hapag-Lloyd Holding 6 months 30. Jun 18 mill ion euro 5'425 89 14'998 2'268 6'146 8'851 3'115 3'075 1.40

K Line group 3 months 30. Jun 18 bill ion Yen 212 -13 1'025 307 280 744 234 107 1.11

Evergreen Marine Corp 6 months 30. Jun 18 mill ion NT$ 75'128 -2'014 214'029 60'790 64'874 149'155 50'185 8'128 1.01

MOL group 3 months 30. Jun 18 bil l ion Yen 304 4 2'206 414 619 1'587 508 304 0.95

China Cosco 2) 6 months 30. Jun 18 mill ion RMB 45'041 1'148 147'212 45'246 44'217 102'995 55'262 10'622 0.94

Pacific International Lines 6 months 30. Jun 18 mill ion US$ 2'244 -38 6'666 1'714 1'728 4'938 2'349 952 0.93

Yang Ming 6 months 30. Jun 18 mill ion NT$ 64'634 -5'555 136'950 32'780 21'111 115'838 45'936 -6'129 0.61

Zim 6 months 30. Jun 18 mill ion US$ 1'555 -21 1'817 625 -169 1'986 809 -1'964 -0.05

Hyundai Merchant Marine 6 months 30. Jun 18 bill ion Won 2'351 -370 3'542 1'054 518 3'024 1'046 -3'138 -0.50

20 20

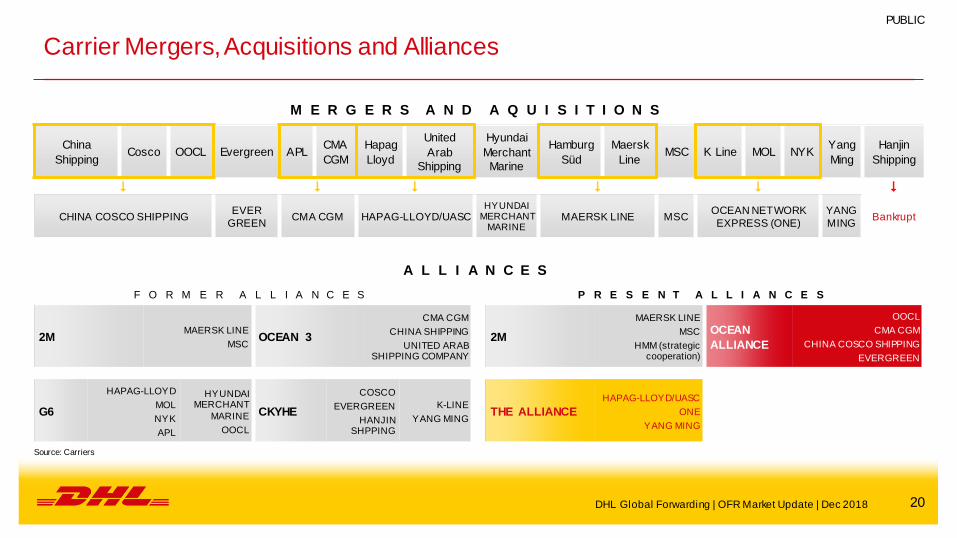

Carrier Mergers, Acquisitions and Alliances

M E R G E R S A N D A Q U I S I T I O N S

China

Shipping Cosco OOCL Evergreen APL

CMA

CGM

Hapag

Lloyd

United

Arab

Shipping

Hyundai

Merchant

Marine

Hamburg

Süd

Maersk

Line MSC K Line MOL NYK

Yang

Ming

Hanjin

Shipping

CHINA COSCO SHIPPING EVER

GREEN CMA CGM HAPAG-LLOYD/UASC

HYUNDAI MERCHANT

MARINE MAERSK LINE MSC

OCEAN NETWORK

EXPRESS (ONE) YANG

MING Bankrupt

A L L I A N C E S

F O R M E R A L L I A N C E S P R E S E N T A L L I A N C E S

2M MAERSK LINE

MSC OCEAN 3

CMA CGM

CHINA SHIPPING

UNITED ARAB SHIPPING COMPANY

2M

MAERSK LINE

MSC

HMM (strategic cooperation)

OCEAN

ALLIANCE

OOCL

CMA CGM

CHINA COSCO SHIPPING

EVERGREEN

G6

HAPAG-LLOYD

MOL

NYK

APL

HYUNDAI MERCHANT

MARINE

OOCL

CKYHE

COSCO

EVERGREEN

HANJIN SHPPING

K-LINE

YANG MING THE ALLIANCE

HAPAG-LLOYD/UASC

ONE

YANG MING

Source: Carriers

PUBLIC

DHL Global Forwarding | OFR Market Update | Dec 2018

21 21

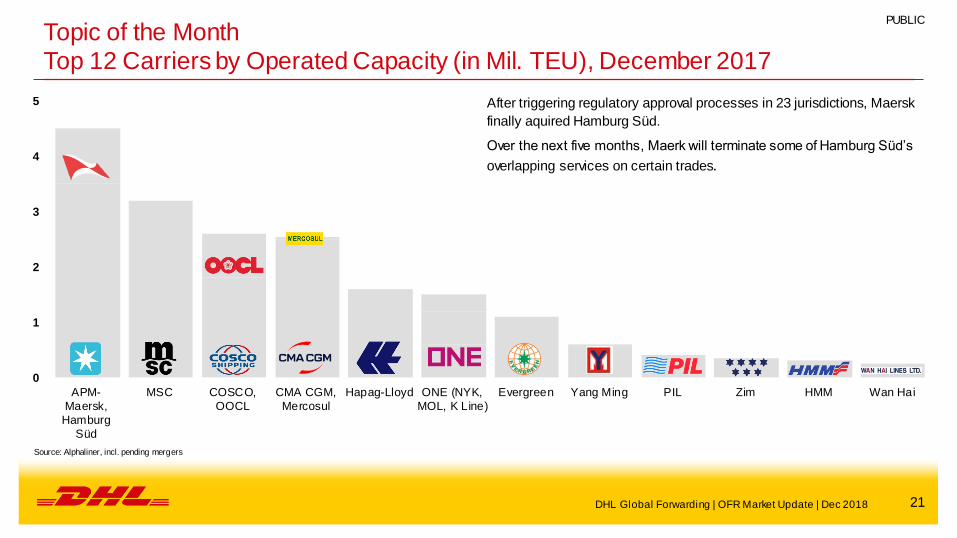

Topic of the Month

Top 12 Carriers by Operated Capacity (in Mil. TEU), December 2017

0

1

2

3

4

5

APM-

Maersk,

Hamburg

Süd

MSC COSCO,

OOCL

CMA CGM,

Mercosul

Hapag-Lloyd ONE (NYK,

MOL, K Line)

Evergreen Yang Ming PIL Zim HMM Wan Hai

Source: Alphaliner, incl. pending mergers

After triggering regulatory approval processes in 23 jurisdictions, Maersk

finally aquired Hamburg Süd.

Over the next five months, Maerk will terminate some of Hamburg Süd’s

overlapping services on certain trades.

PUBLIC

DHL Global Forwarding | OFR Market Update | Dec 2018

22 22

Acronyms and Explanations

2M - Carrier Alliance: Maersk / MSC Ocean 3 - Carrier Alliance: CMA, UASC, China Shipping

AMLA - Latin America OCRS - Operational Cost Recovery surcharge

AMNO - North America OOCL - Orient Ov erseas Container Line AR - Argentina OWS - Ov erweight Surcharge

ASPA - AsiaPacific PH - Philippines

BR - Brazil PNW - Pacif ic North West

CAGR - Compound Annual Growth Rate Ppt. - Percentage points

CENAC - Central Amercia and Caribbean PSW - Pacif ic South West

CKYHE - Carrier Alliance: Cosco, K-Line, YangMing, Hanjin and Evergreen RR(I) - Rate Restoration

CNC - CNC Line (Cheng Lie Navigation Co. Ltd.) SAEC - South America East Coast

DG - Dangerous Goods SAWC - South America West Coast

DWT - Dead Weight Tonnage SOLAS - Saf ety of Life at Sea

EB - Eastbound SPRC - South People’s Republic of China – South China

ECSA - East Coast South America SSA - Sub-Saharan Af rica

EGLV - Ev ergreen Marine Corp SSL - Steam Ship Line EURO - Europe T - Thousands

FMC - US Federal Marine Commission TEU - Twenty f oot equivalent unit (20‘ container)

G6 - Carrier Alliance: APL, Hapag Lloyd, Hyundai, MOL, NYK and OOCL TP - Trans Pacif ic

GRI - General Rate Increase TSA - Trans Pacif ic Stabilization Agreement

HJS - Hanjin Shipping ULCS - Ultra Large Container Ship

HMM - Hy undai USGC - US Gulf Coast

HL - Hapag -Lloy d US FMC - US Federal Maritime Commission

HSUD - Hamburg Süd USEC - US East Coast

HWS - Heav y Weight Surcharge USWC - US West Coast

IA - Intra Asia VGM - Verif ied Gross Mass

IPBC - India Pakistan Bangladesh Colombo VLCS - Very Large Container Ship

IPI - Inland Point Intermodal VSA - Vessel Sharing Agreement

ISC - Indian Sub Continent WB - Westbound

MENAT - Middle East and North Africa WCSA - West Coast South America

ML - Maersk Line WHL - Wan Hai

mn - Millions YML - Yang Ming Line

MoM - Month-on-Month YoY - Year-on-Year

NOO - Non-operating (vessel) owners YTD - Year-to-Date

DHL Global Forwarding | OFR Market Update | Dec 2018

PUBLIC