dhl global forwarding, freight ocean freight market update · dhl global forwarding, freight...

TRANSCRIPT

1

OCEAN FREIGHT MARKET UPDATE

DHL Global Forwarding, Freight

November 2017

2 2

Contents

DHL Global Forwarding | OFR Market Update | Nov 2017

TOPIC OF THE MONTH

Global GDP Growth vs. Container Throughput Growth: 1990-2020F

HIGH LEVEL DEVELOPMENT

MARKET OUTLOOK

Freight Rates and Volume Development

ECONOMIC OUTLOOK & DEMAND DEVELOPMENT

CAPACITY DEVELOPMENT

CARRIERS

§ REGULATIONS

? DID YOU KNOW ?

Evolution of CMA CGM Capacity, 1995-2017

3 3

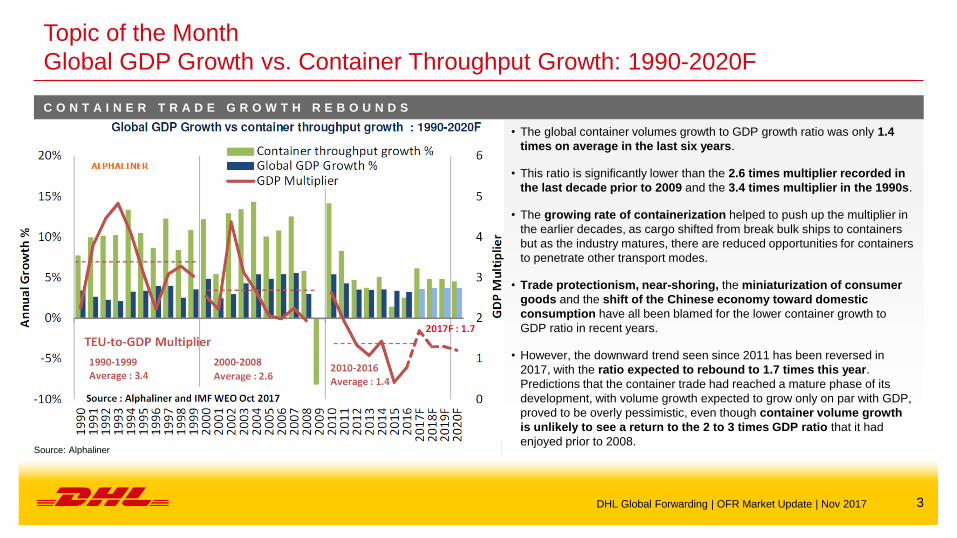

Topic of the Month

Global GDP Growth vs. Container Throughput Growth: 1990-2020F

C O N T A I N E R T R A D E G R O W T H R E B O U N D S

• The global container volumes growth to GDP growth ratio was only 1.4

times on average in the last six years.

• This ratio is significantly lower than the 2.6 times multiplier recorded in

the last decade prior to 2009 and the 3.4 times multiplier in the 1990s.

• The growing rate of containerization helped to push up the multiplier in

the earlier decades, as cargo shifted from break bulk ships to containers

but as the industry matures, there are reduced opportunities for containers

to penetrate other transport modes.

• Trade protectionism, near-shoring, the miniaturization of consumer

goods and the shift of the Chinese economy toward domestic

consumption have all been blamed for the lower container growth to

GDP ratio in recent years.

• However, the downward trend seen since 2011 has been reversed in

2017, with the ratio expected to rebound to 1.7 times this year.

Predictions that the container trade had reached a mature phase of its

development, with volume growth expected to grow only on par with GDP,

proved to be overly pessimistic, even though container volume growth

is unlikely to see a return to the 2 to 3 times GDP ratio that it had

enjoyed prior to 2008. Source: Alphaliner

DHL Global Forwarding | OFR Market Update | Nov 2017

4 4

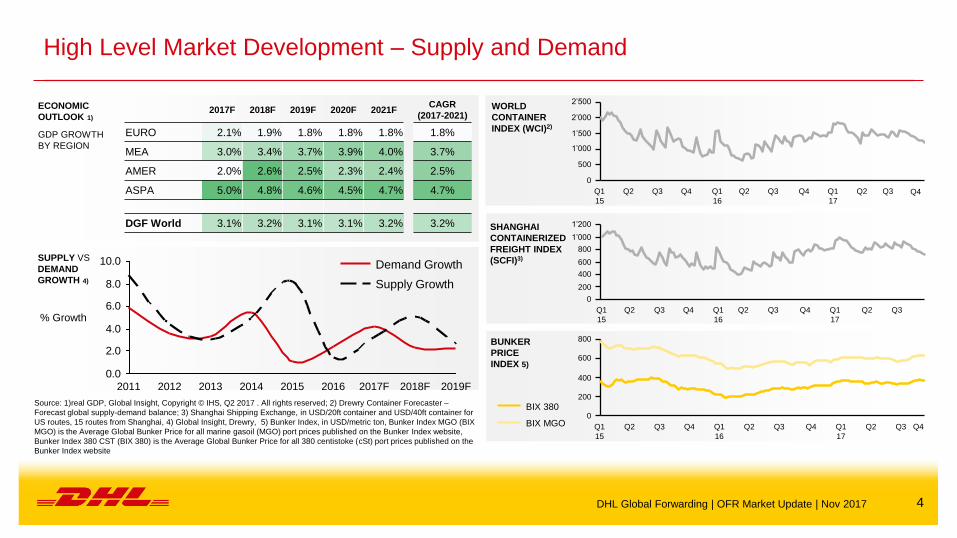

High Level Market Development – Supply and Demand

1’200

0

1’000

600

800

400

200

Q3 Q4 Q1

16

Q3 Q1

15

Q2 Q2 Q1

17

Q2 Q3 Q4

2’000

1’500

1’000

500

0

2’500

Q2 Q2 Q3 Q4 Q1

17

Q1

15

Q3 Q2 Q3 Q1

16

Q4

0

200

600

800

400

Q1

17

Q2 Q4 Q2 Q3 Q1

15

Q3 Q4 Q1

16

Q3 Q2

BIX 380

BIX MGO

SHANGHAI

CONTAINERIZED

FREIGHT INDEX

(SCFI)3)

WORLD

CONTAINER

INDEX (WCI)2)

BUNKER

PRICE

INDEX 5)

ECONOMIC

OUTLOOK 1)

GDP GROWTH

BY REGION

SUPPLY VS

DEMAND

GROWTH 4)

Source: 1)real GDP, Global Insight, Copyright © IHS, Q2 2017 . All rights reserved; 2) Drewry Container Forecaster –

Forecast global supply-demand balance; 3) Shanghai Shipping Exchange, in USD/20ft container and USD/40ft container for

US routes, 15 routes from Shanghai, 4) Global Insight, Drewry, 5) Bunker Index, in USD/metric ton, Bunker Index MGO (BIX

MGO) is the Average Global Bunker Price for all marine gasoil (MGO) port prices published on the Bunker Index website,

Bunker Index 380 CST (BIX 380) is the Average Global Bunker Price for all 380 centistoke (cSt) port prices published on the

Bunker Index website

0.0

2.0

4.0

6.0

8.0

10.0

2012 2013 2011 2014 2017F 2019F 2016 2015 2018F

% Growth

Demand Growth

Supply Growth

DHL Global Forwarding | OFR Market Update | Nov 2017

2017F 2018F 2019F 2020F 2021F CAGR

(2017-2021)

EURO 2.1% 1.9% 1.8% 1.8% 1.8% 1.8%

MEA 3.0% 3.4% 3.7% 3.9% 4.0% 3.7%

AMER 2.0% 2.6% 2.5% 2.3% 2.4% 2.5%

ASPA 5.0% 4.8% 4.6% 4.5% 4.7% 4.7%

DGF World 3.1% 3.2% 3.1% 3.1% 3.2% 3.2%

Q4

Q4

5 5

Market Outlook November 2017 – Major Trades

Market slightly picking up again after Chinese Golden Week

KEY Strong

Increase ++

Moderate

Increase +

No

Change =

Moderate

Decline -

Strong

Decline - -

EXPORT REGION IMPORT REGION CAPACITY RATE

EURO AMNO = =

AMLA - +

ASPA = =

MENAT = =

SSA = =

AMNO AMLA - +

ASPA = =

EURO = =

MENAT = =

SSA = =

EXPORT REGION IMPORT REGION CAPACITY RATE

AMLA AMNO - ++

ASPA - ++

EURO - +

MENAT - +

SSA = ++

ASPA ASPA - +

AMNO - +

AMLA = +

EURO = +

MENAT = =

OCEANIA = +

DHL Global Forwarding | OFR Market Update | Nov 2017

Source: DGF

6 6

Market Outlook August 2017 – Ocean Freight Rates Major Trades Market outlook on

smaller trades available

in the back-up

O C E A N F R E I G H T R A T E S O U T L O O K

ASPA – EURO High vessel utilization after the Golden week holiday due to the extensive blank sailing program and addition port omissions.

GRI announced for 1st November & additional blank sailings in wk46

EURO – ASPA & MEA rates are dropping for high volume spot cargo; no influence on tender pricing, which is still kept stable

ASPA – AMLA

MX & WCSA rates expected to increase on 1st Nov, to capitalize on final shipments to arrive AMLA destination in time for Christmas. For

ECSA, expecting 2 extra loaders in early Nov, proposed GRI may not be successful. Still, bookings must be placed 15 days before

vessel arrive at origin.

ASPA – AMNO Overall space continue to be tight due to blank sailings in October. Space situation expected to continue in Nov with THE all iance

already announcing their blank sailings in wk 46 & 47.

EURO – AMNO Rates are stable to USEC & GU, small increase to USWC. Vessels are well utilized and space can be a concern depending on Carrier,

Week and Loop. Early bookings is advised.

ASPA – MENAT

Rates have been reduced slightly and/or extended till End October except for Middle East. Tight vessel utilization after Golden Week,

(mainly due to blank sailing that Carriers have implemented). Carriers are trying to go for another round of GRI w.e.f 01 Nov.

Severe thunder storm has worsened the situation in Durban. This bad ailment has caused some damages at the terminal, vessels and

affecting ships operations. All vessels calling Durban are affected. At this moment, cargos are expected to suffer at least a week delay.

ASPA – ASPA Space is tight with the blank sailings during the China Golden Week period, especially to IPBC and expected to remain in the month of

November. Several carriers have announced a NOV GRI for IPBC.

AMNO – EURO Unchanged and stable

DHL Global Forwarding | OFR Market Update | Nov 2017

Source: DGF

7 7

Economic Outlook & Demand Development

F O R 1 S T T I M E S I N C E 2 0 1 1 , G D P G R O W I S I N L I N E W I T H P R E V I O U S Y E A R ’ S F O R E C A S T

EURO

2017 GDP growth has been upgraded by 0.3% to 2.1% as EURO economy has further strengthened, and its upside potential over the short

term has improved. Markedly improved labor markets, decent global demand, accommodative monetary policy, and elevated business and

consumer confidence support growth.

AMER 2017 AMNO GDP forecast was slightly down due to expected volatility of US economic activity over the next few quarters, induced by

Hurricane Harvey. Weaker doller, combined with stronger growth abroad, accounted for unexpected turnaround in export growth in US.

ASPA

Robust start into 2017 for most major AP economies with support from strong demand for electronics industry, recovering agricultural

production, higher commodity prices, and stronger-than-expected conumption activity led a slight forecast upgrade. Export forecasts strongly

revised down for KR & IN, leading to decline of the regional forecast.

EMERGING

MARKETS

Growth of BR economy was unbalanced in the beginning of 2017, as exports grew, but private consumption, investment, and government

spending declined. MX exports outlook was revised upwards.

DEMAND

DEVELOPMENT

Global Manufacturing PMI was at 75-month high in Aug. EURO PMI continuously pointed to strengthening industrial activity within the

disclosed period. In US the Manufacturing PMI signaled strong expansion and both Asian manufacturing PMI’s (Caixin and Nikkei) signaled

expansion in Aug. BR manufacturing PMI dipped in June but returned into expansion zone in Jul. Also MX PMI signaled improvement in Aug.

Source: Global Executive Summary, IHS Markit, Sep 2017. The Purchase Manager Index is an IHS proprietary metric that polls purchasing managers to understand if they are to order more or less in the future, hence giving a representative estimation

of the global business sentiment. Assessed monthly, a PMI at 50 is considered neutral, expanding above 50, and shows business shrinking below 50.

DHL Global Forwarding | OFR Market Update | Nov 2017

8 8

Capacity Development

Source: Alphaliner, carriers

C A P A C I T Y D E V E L O P M E N T

Zim will continue to offer its med-ECAS service through a slot arrangement on the new joint loop that Hapag-Lloyd and MSC are setting up in Oct. COSCO pursues

Europe-ECSA link through slots on new joint service of Maersk, Hamburg Süd and CMA CGM. The changes on this trade lane were triggered by the absorption of

Hamburg Süd by Maersk Line.

Weekly capacity on the Far East-West Africa route has increased by more than 35% since Jul, with the launch of 3 new services (Maersk ‘FEW7’, Maersk/CMA

CGM ‘FEW5/WAX2’, COSCO/GSL ‘WAX5/FA3’) and the upgrade of MSC’s African Express service.

Idle fleet edged upwards due to a lack of demand in the larger sizes from the effects of China’s ‘Golden Week’ holidays. Unlike in previous years when carriers

would have announced capacity withdrawals for the slack season starting in Oct, there have not been any announcements yet, regarding the main carrier’s winter

deployment plans while carriers keep battling for market share.

Chinese port volumes surged in Sep just ahead of Chinese National ‘Golden Week’ holidays, reflecting a strong peak season, although there were no reports of

space shortages as carriers deployed multiple extra loaders to cater for the additional demand.

Source: Alphaliner, carriers

DHL Global Forwarding | OFR Market Update | Nov 2017

9 9

Carriers

Source: Alphaliner, carriers

C A R R I E R S

Hapag-Lloyd has completed on 17 Oct its capital increase that was agreed upon as part of the merger of Hapag-Lloyd and UASC. The proceeds from a rights issue

offered to all shareholders on 28 Sep amounted to EUR 352m. The capital increase was backstopped by the four primary shareholders CSAV Germany Container

Holding GmbH, Kuehne Martime GmbH, Qatar Holding Germany GmbH and The Public Investment Fund of the Kingdom of Saudi Arabia who acquired all the

remaining unsubscribed shares.

Yang Ming to raise USD 197m from the issue of 500m new shares. 80% of the new shares that are to be issued are reserved for existing shareholders while 10% is

reserved for employees, leaving 10% of the shares open to the public. The new capital increase follows its first round of capital increase in Feb 17 which raised USD

55. The carrier had earlier planned to complete the 2nd stage of its recapitalization program in Jun 17 but the plan was delayed due to weak market conditions. The

Taiwan government is expected to contribute the main portion of the cash to be raised. The share price fell by 28% from its recent peak.

The two state-owned shipping groups China COSCO Shipping and China Merchant Shipping intend to dispose of their equity shares in Shanghai Jin Jiang

Shippings (SJJ), a Chinese regional carrier offering short sea container services in East Asia. The current majority shareholder of SJJ is Shanghai International Port

Group (SIPG), which holds a 79.2% equity share.

APL has announced the launch of its enhanced ‘Eagle Guaranteed’ program to cater for priority shipments on the eastbound transpacific from 1 Nov ’17. The

program consists of 3 separate products:

• Eagle GO (EGO), where the EGO surcharge paid by the shipper will be refunded if shipment not loaded on specified vessel

• Eagle GET (EGT) guarantees the discharge of containers within 12 hrs of vessel cargo operation for a flat EGT surcharge

• Eagle REACH (ERC) provides a day definite rail delivery to reach 6 inland destinations in the US

HMM has announced on 13 Oct a rights issue to raise KRW 693.6bn (USD 614m) from its existing shareholders. The company will issue 120m new shares and

plans to use KRW 293.6bn from the expected proceeds for working capital and KRW 400bn to invest in new ships & terminals. Korea Development Bank (KDB),

which currently holds a 13.1% in HMM, is expected to fund most of the capital increase. The share price has tumbled by 15% since the announcement.

Source: Alphaliner, carriers

DHL Global Forwarding | OFR Market Update | Nov 2017

10 10

Regulations

Source: Alphaliner, carriers

R E G U L A T I O N S

The newly introduced Thailand customs ACT B.E.2560 will replace the Customs ACT B.E.2469 on cargoes with departure and arrival from 13 Nov ’17 onwards.

Section: 211: all cases of packages containing goods shall bear marks and numbers and such marks and numbers shall be shown on all documents and the

cargoes. If an importer or exporter refuses or neglects to comply with the aforesaid requirements, such person/company shall be liable to a fine not exceeding

50’000 baht.

The shipping marks must be shown on all documents related to the shipment. This includes:

• HBL

• Commercial Packing list

• The cargo itself.

Note: “Blank” or “no mark” is no longer acceptable by the customs.

According to a survey from ExxonMobil, shipping lines are unprepared for the 2020 deadline for ships to burn low-sulphur fuel. In 2016 the International Maritime

Organization (IMO) promised to have greenhouse gas emissions regulations in place from 2020 onwards when a 0.5% sulphur cap on marine fuel consumption will

come into effect.

Source: DHL, Ti

DHL Global Forwarding | OFR Market Update | Nov 2017

11 11

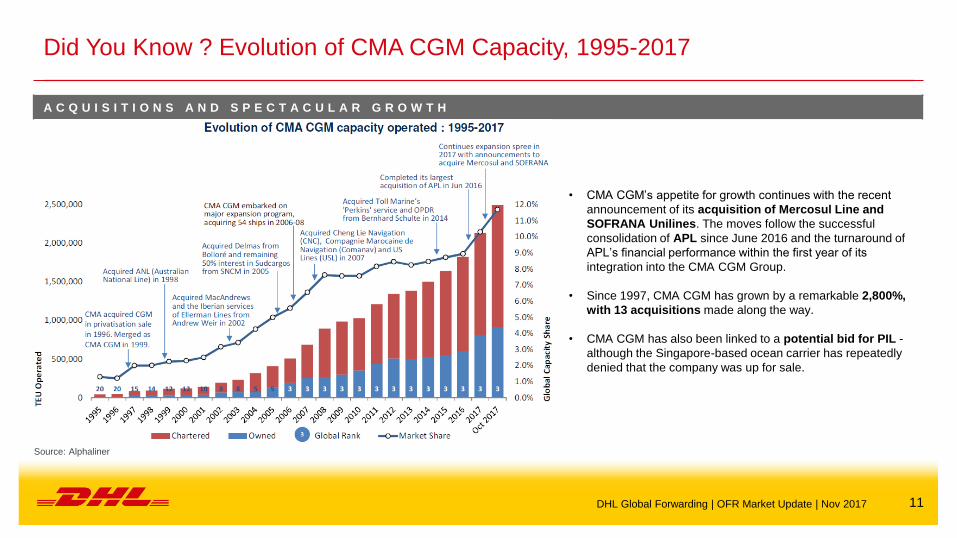

Did You Know ? Evolution of CMA CGM Capacity, 1995-2017

Source: Alphaliner

A C Q U I S I T I O N S A N D S P E C T A C U L A R G R O W T H

• CMA CGM’s appetite for growth continues with the recent

announcement of its acquisition of Mercosul Line and

SOFRANA Unilines. The moves follow the successful

consolidation of APL since June 2016 and the turnaround of

APL’s financial performance within the first year of its

integration into the CMA CGM Group.

• Since 1997, CMA CGM has grown by a remarkable 2,800%,

with 13 acquisitions made along the way.

• CMA CGM has also been linked to a potential bid for PIL -

although the Singapore-based ocean carrier has repeatedly

denied that the company was up for sale.

DHL Global Forwarding | OFR Market Update | Nov 2017

12 12 B A C K - U P

13 13

Source: DGF

Market Outlook November 2017 – Ocean Freight Rates Additional Trades (1/2)

Ocean Freight Rates Outlook

EURO – AMLA next step of rate increases to SAEC materialized for November. It´s a more slight increase as expected, as carriers are still cautious and are

still monitoring capacity and utilization carefully.

EURO – SSA unchanged stable, well utilized vessels. Space to South Africa will become tight during the next weeks due to upcoming Christmas / Summer

Holidays in South Africa.

AMNO – MENAT

No change in the current market situation. Space is still tight from USEC & USGC Ports.

1 or 2 weeks out from USEC and 2-3 weeks from USGC.. It appears that current rates will stay the same until

end of this year or might even drop few dollars from USEC to main ports in MEA such as Jebel Ali/Jeddah in November

AMNO – SSA

Space is available to all destinations in South & West Africa.

E. Africa is tighter due to routing via congested transshipment ports.

APL & CMA applied GRIs to most African destinations

AMNO – AMLA

Rate trending upward all US to WCSA and selected ECSA destinations.

Rate trending upward Gulf to all AMLA

Capacity reduced slightly w/CMA cancelling Gulf to CL on Brasex

AMLA Exports

Rates from SAEC continue to rise as fruit season begins and capacity is cut to EURO

Bookings are being made 4-6 weeks out(SAEC)

Space issues continue on WCSA

Numerous GRI’s being announced

Source: DGF team

Source: DGF team

Source: DGF team

DHL Global Forwarding | OFR Market Update | Nov 2017

14 14

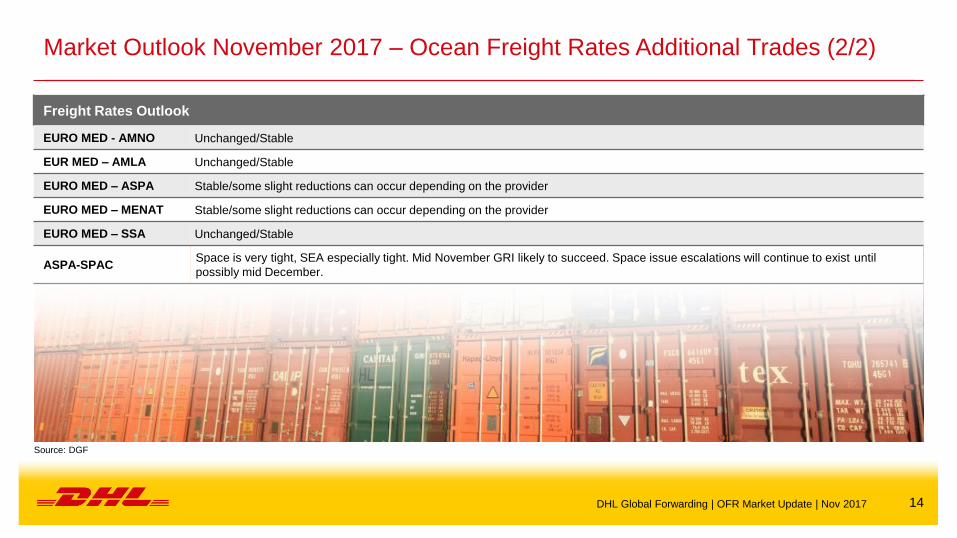

Market Outlook November 2017 – Ocean Freight Rates Additional Trades (2/2)

Freight Rates Outlook

EURO MED - AMNO Unchanged/Stable

EUR MED – AMLA Unchanged/Stable

EURO MED – ASPA Stable/some slight reductions can occur depending on the provider

EURO MED – MENAT Stable/some slight reductions can occur depending on the provider

EURO MED – SSA Unchanged/Stable

ASPA-SPAC Space is very tight, SEA especially tight. Mid November GRI likely to succeed. Space issue escalations will continue to exist until

possibly mid December.

DHL Global Forwarding | OFR Market Update | Nov 2017

Source: DGF

15 15

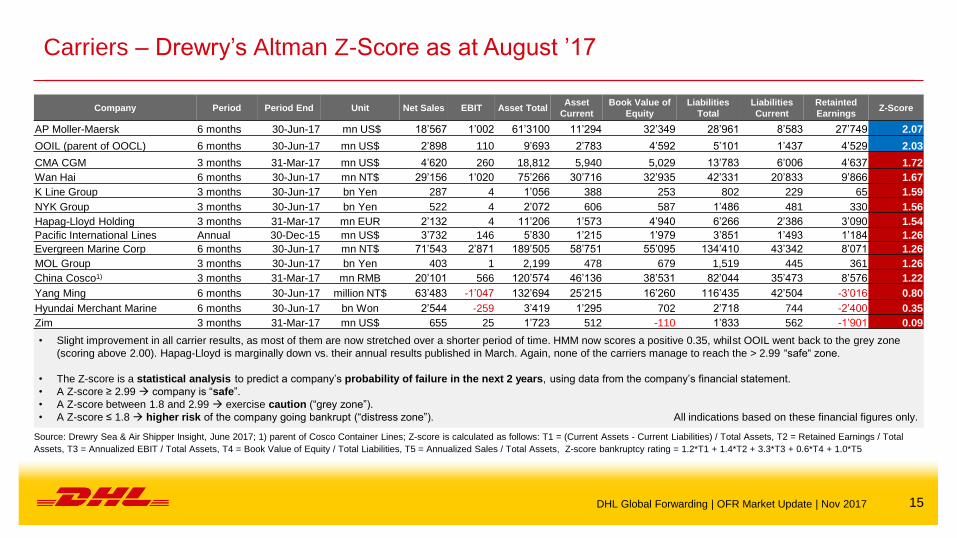

Carriers – Drewry’s Altman Z-Score as at August ’17

Company Period Period End Unit Net Sales EBIT Asset Total Asset

Current

Book Value of

Equity

Liabilities

Total

Liabilities

Current

Retainted

Earnings Z-Score

AP Moller-Maersk 6 months 30-Jun-17 mn US$ 18’567 1’002 61’3100 11’294 32’349 28’961 8’583 27’749 2.07

OOIL (parent of OOCL) 6 months 30-Jun-17 mn US$ 2’898 110 9’693 2’783 4’592 5’101 1’437 4’529 2.03

CMA CGM 3 months 31-Mar-17 mn US$ 4’620 260 18,812 5,940 5,029 13’783 6’006 4’637 1.72

Wan Hai 6 months 30-Jun-17 mn NT$ 29’156 1’020 75’266 30’716 32’935 42’331 20’833 9’866 1.67

K Line Group 3 months 30-Jun-17 bn Yen 287 4 1’056 388 253 802 229 65 1.59

NYK Group 3 months 30-Jun-17 bn Yen 522 4 2’072 606 587 1’486 481 330 1.56

Hapag-Lloyd Holding 3 months 31-Mar-17 mn EUR 2’132 4 11’206 1’573 4’940 6’266 2’386 3’090 1.54

Pacific International Lines Annual 30-Dec-15 mn US$ 3’732 146 5’830 1’215 1’979 3’851 1’493 1’184 1.26

Evergreen Marine Corp 6 months 30-Jun-17 mn NT$ 71’543 2’871 189’505 58’751 55’095 134’410 43’342 8’071 1.26

MOL Group 3 months 30-Jun-17 bn Yen 403 1 2,199 478 679 1,519 445 361 1.26

China Cosco1) 3 months 31-Mar-17 mn RMB 20’101 566 120’574 46’136 38’531 82’044 35’473 8’576 1.22

Yang Ming 6 months 30-Jun-17 million NT$ 63’483 -1’047 132’694 25’215 16’260 116’435 42’504 -3’016 0.80

Hyundai Merchant Marine 6 months 30-Jun-17 bn Won 2’544 -259 3’419 1’295 702 2’718 744 -2’400 0.35

Zim 3 months 31-Mar-17 mn US$ 655 25 1’723 512 -110 1’833 562 -1’901 0.09

• Slight improvement in all carrier results, as most of them are now stretched over a shorter period of time. HMM now scores a positive 0.35, whilst OOIL went back to the grey zone

(scoring above 2.00). Hapag-Lloyd is marginally down vs. their annual results published in March. Again, none of the carriers manage to reach the > 2.99 “safe“ zone.

• The Z-score is a statistical analysis to predict a company’s probability of failure in the next 2 years, using data from the company’s financial statement.

• A Z-score ≥ 2.99 company is “safe”.

• A Z-score between 1.8 and 2.99 exercise caution (“grey zone”).

• A Z-score ≤ 1.8 higher risk of the company going bankrupt (“distress zone”). All indications based on these financial figures only.

Source: Drewry Sea & Air Shipper Insight, June 2017; 1) parent of Cosco Container Lines; Z-score is calculated as follows: T1 = (Current Assets - Current Liabilities) / Total Assets, T2 = Retained Earnings / Total

Assets, T3 = Annualized EBIT / Total Assets, T4 = Book Value of Equity / Total Liabilities, T5 = Annualized Sales / Total Assets, Z-score bankruptcy rating = 1.2*T1 + 1.4*T2 + 3.3*T3 + 0.6*T4 + 1.0*T5

DHL Global Forwarding | OFR Market Update | Nov 2017

16 16

Market Outlook – Volume Outlook in Main Trade Lanes, 2017 Estimate & Growth

Forecast 2017/20 in %

N O R T H

A M E R I C A I n c l .

M E X I C O

3.5 mTEU +1.2%

1.7 mTEU +0.9%

1.7 mTEU +1.3%

0.2 mTEU +3.0%

N O R T H

A M E R I C A I n c l .

M E X I C O

L A T I N

A M E R I C A

E U R O P E

I n c l . M E D

11.9 mTEU +1.6%

7.0 mTEU +0.9%

7.6 mTEU +0.7%

15.8 mTEU +0.9%

7.0 mTEU +0.9%

4.5 mTEU +2.8%

2017e, in mTEU 2017e-2021e CAGR, in %

F A R E A S T

I N T R A A S I A

excl. Oceania

35.1 mTEU +3.1%

3.5 mTEU

+1.3%

2.0 mTEU

+0.7%

L A T I N

A M E R I C A

G L O B A L C O N T A I N E R T R A D E 2 0 1 7 e 1 3 8 . 5 m T E U + 2 . 3 % C A G R 2 0 1 7 e - 2 0 2 0 e

Mid-term growth is mainly driven by Asian tradelanes.

Source: Drewry

DHL Global Forwarding | OFR Market Update | Nov 2017

17 17

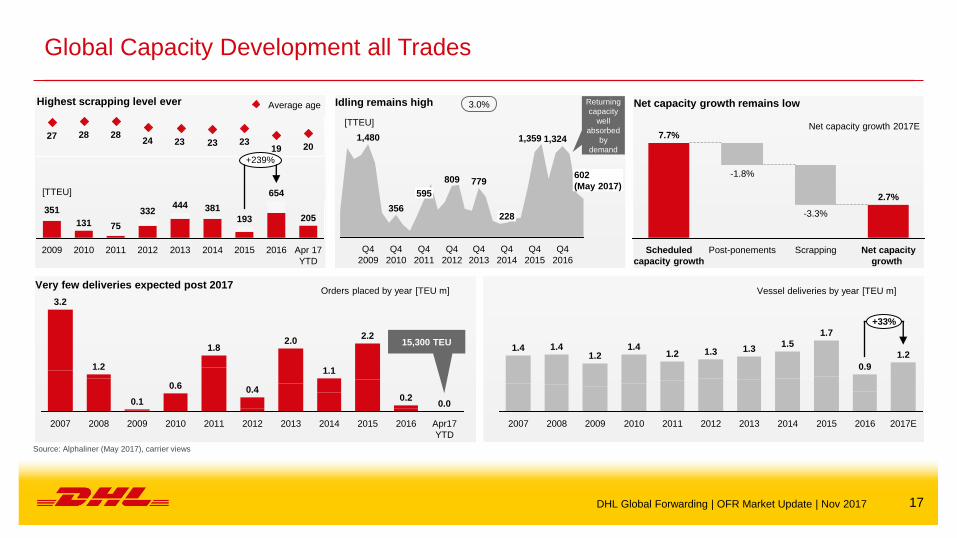

Global Capacity Development all Trades

20 19 23 23 23 24

28 28 27

Highest scrapping level ever Idling remains high

[TTEU]

602

(May 2017)

1,324

Q4

2016

Q4

2015

1,359

Q4

2014

228

Q4

2013

779

Q4

2012

809

Q4

2011

595

Q4

2010

356

Q4

2009

1,480

Returning

capacity

well

absorbed

by

demand

3.0%

[TTEU]

381

2013

444

2012

332

2011

75

2010

131

2009

351

+239%

Apr 17

YTD

205

2016

654

2015

193

2014

Average age Net capacity growth remains low

Net capacity growth 2017E

Scrapping Net capacity

growth

2.7%

-3.3%

-1.8%

Scheduled

capacity growth

Post-ponements

7.7%

Orders placed by year [TEU m] Vessel deliveries by year [TEU m]

0.2

2015

0.0

2016

2.2

2014

1.1

2013

2.0

2012

0.4

2011

1.8

2010

0.6

2009

0.1

2008

1.2

2007

3.2

Apr17

YTD

+33%

1.2

2017E 2016

0.9

2015

1.7

2014

1.5

2013

1.3

2012

1.3

2011

1.2

2010

1.4

2009

1.2

2008

1.4

2007

1.4 15,300 TEU

Very few deliveries expected post 2017

Source: Alphaliner (May 2017), carrier views

DHL Global Forwarding | OFR Market Update | Nov 2017

18 18

Carrier Mergers, Acquisitions and Alliances

M E R G E R S A N D A Q U I S I T I O N S

China

Shipping Cosco

OOCL TBC

Evergreen APL CMA

CGM Hapag

Lloyd

United

Arab

Shipping

Hyundai

Merchant

Marine

Hamburg

Süd Maersk

Line MSC K Line MOL NYK

Yang

Ming Hanjin

Shipping

CHINA COSCO SHIPPING EVER

GREEN CMA CGM HAPAG-LLOYD/UASC

HYUNDAI

MERCHANT

MARINE MAERSK LINE MSC

OCEAN NETWORK

EXPRESS (ONE) YANG

MING Bankrupt

A L L I A N C E S

F O R M E R A L L I A N C E S P R E S E N T A L L I A N C E S

2M MAERSK LINE

MSC OCEAN 3

CMA CGM

CHINA SHIPPING

UNITED ARAB

SHIPPING COMPANY

2M

MAERSK LINE

MSC

HMM (strategic

cooperation)

OCEAN

ALLIANCE

OOCL

CMA CGM

CHINA COSCO SHIPPING

EVERGREEN

G6

HAPAG-LLOYD

MOL

NYK

APL

HYUNDAI

MERCHANT

MARINE

OOCL

CKYHE

COSCO

EVERGREEN

HANJIN

SHPPING

K-LINE

YANG MING THE ALLIANCE

HAPAG-LLOYD/UASC

ONE

YANG MING

Source: Carriers

DHL Global Forwarding | OFR Market Update | Nov 2017

19

Acronyms and Explanations

2M - Carrier Alliance: Maersk / MSC OCRS - Operational Cost Recovery surcharge

AMLA - Latin America OWS - Overweight Surcharge

AMNO - North America PH - Philippines

AR - Argentina PNW - Pacific North West

ASPA - AsiaPacific Ppt. - Percentage points

BR - Brazil PSW - Pacific South West

CAGR - Compound Annual Growth Rate RR(I) - Rate Restoration

CENAC - Central Amercia and Caribbean SAEC - South America East Coast

CKYHE - Carrier Alliance: Cosco, K-Line, YangMing, Hanjin and Evergreen SAWC - South America West Coast

CNC - CNC Line (Cheng Lie Navigation Co. Ltd.) SOLAS - Safety of Life at Sea

DG - Dangerous Goods SPRC - South People’s Republic of China – South China

DWT - Dead Weight Tonnage SSA - Sub-Saharan Africa

EB - Eastbound SSL - Steam Ship Line

ECSA - East Coast South America T - Thousands

EURO - Europe TEU - Twenty foot equivalent unit (20‘ container)

FMC - US Federal Marine Commission TP - Trans Pacific

G6 - Carrier Alliance: APL, Hapag Lloyd, Hyundai, MOL, NYK and OOCL TSA - Trans Pacific Stabilization Agreement

GRI - General Rate Increase ULCS - Ultra Large Container Ship

HJS - Hanjin Shipping USGC - US Gulf Coast

HMM - Hyundai US FMC - US Federal Maritime Commission

HSUD - Hamburg Süd USEC - US East Coast

HWS - Heavy Weight Surcharge USWC - US West Coast

IA - Intra Asia VGM - Verified Gross Mass

IPBC - India Pakistan Bangladesh Colombo VLCS - Very Large Container Ship

IPI - Inland Point Intermodal VSA - Vessel Sharing Agreement

ISC - Indian Sub Continent WB - Westbound

MENAT - Middle East and North Africa WCSA - West Coast South America

mn - Millions YML - Yang Ming Line

MoM - Month-on-Month YoY - Year-on-Year

NOO - Non-operating (vessel) owners YTD - Year-to-Date

Ocean 3 - Carrier Alliance: CMA, UASC, China Shipping

DHL Global Forwarding | OFR Market Update | Nov 2017