dewan housing kirloskar pneumatic companyreports.choiceindia.com/reports/fur291220170436241.pdf ·...

TRANSCRIPT

‘Growing business at cheap valuation’

DEWAN HOUSING Kirloskar Pneumatic Company ‘Buy, Add on Dips’

Shareholding Pattern Particulars Sep'17 Jun'17 Mar'17 Promoter 53.7% 53.0% 68.0% FPIs 1.6% 1.6% 0.1% Insti. 23.9% 21.0% 18.3% N. Insti. 20.8% 24.4% 13.6%

Relative Capital Market Strength

Kirloskar Pneumatic Company Limited is a holding company engaged in the manufacture of compressors, gears and gear boxes. The Company's segments include Compression Products/ Systems and Transmission Products. The Compression Products/ Systems segment offers products, such as air, gas and refrigeration compressors, and packages and systems to the oil and gas, cold chain and other industrial markets. It offers refrigeration and gas compression systems for refineries, petrochemical plants and compressed natural gas stations; ammonia compressor and packages for the cold store units, dairy units and pharmaceutical plants; air compressors and packages for cement, steel, power, engineering and other markets, and heating, ventilating and air conditioning systems and air compressor packages for defense sector. The Company's Transmission Products segment offers traction gears, customized gearboxes and specialized products for Indian Railways, wind power projects and other industrial markets.

Kirloskar Pneumatic Company Ltd

Q2FY17 Result Analysis: KPCL’s revenues decreased by 29.0% to Rs.871.mn in Q2FY18 as against Rs.1228.2mn in Q2FY17. EBIDTA decreased by 170.2% to Rs.(45.4)mn in Q2FY18 as against Rs.64.7mn in Q2FY17. EBITDA margins also decreased to 5.2% in Q2FY18 as against 5.3% in Q2FY17. PAT decreased by 125.0% to Rs.(15.9)mn in Q2FY18 from Rs.63.5mn in Q2FY17. Net profit margin stood at (1.8)% vs 5.2% in Q2FY17. Break up of key expenditures include cost of materials consumed at Rs.492.6mn, employee cost at Rs.221.9mn and Depreciation & Amortization exp. at Rs.40.0mn and other expenses at Rs.258.9mn. Outlook: Global air compressor market size is expected to exceed USD 37 billion by 2022. Increasing adoption of remote sensing technology to monitor performance expected to contribute to market growth over the forecast period. Strong demand from food & beverage industry, mainly due to mandates on food safety and health requirements is projected to drive growth. Low maintenance, retrofitting of existing systems, efficient operation at lower costs, and rising adoption of variable-speed systems are some of the other factors driving demand across key end-use industries. The decrease in crude oil price in the international market and adoption of Bharat VI norms is expected to encourage fresh investment in expansion of oil refining capacities, construction of new refineries.

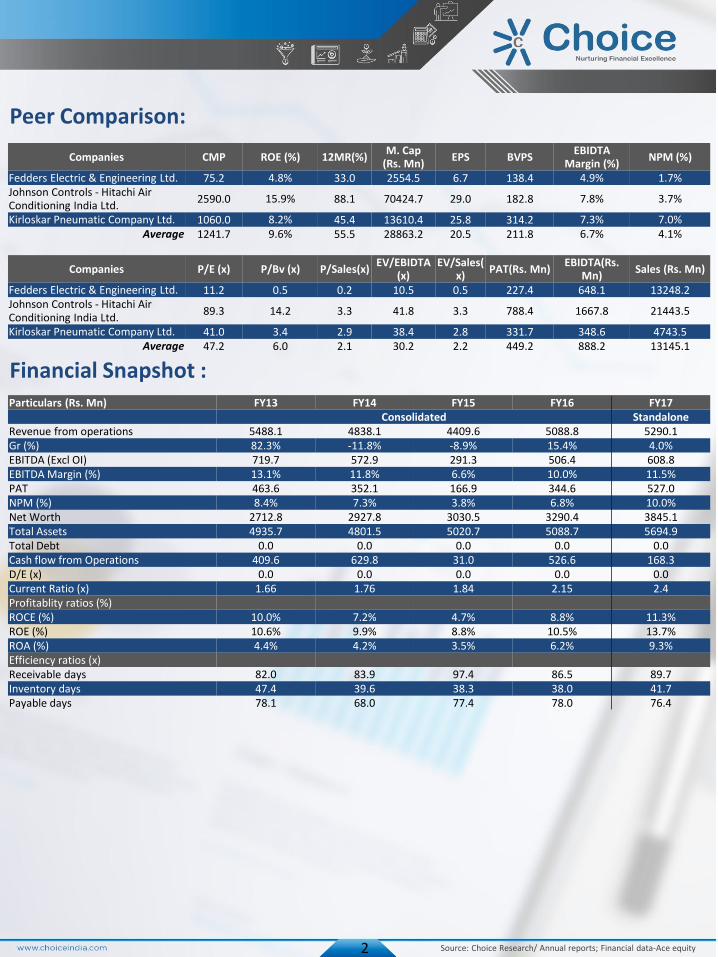

All oil companies will be investing in upgrading refining processes in the forthcoming two fiscal years. The Company is also working on export opportunities in specific countries and this is going to add to our current business in Oil & Gas business. an estimated 40% of vegetable produce and 15% of milk is wasted due to improper storage and transportation. The Government of India, therefore, is aggressively pushing for the infrastructure development for cold chain. The Government has also announced incentives for infrastructure development in cold chain. Demand for compressors for cold stores, is therefore, expected to grow in the next few years. Cold chain market is expected to grow at 10% annually. The Government of India's thrust on “Make in India” in the defense sector is an opportunity for the Company in the coming years. They also takes up Annual Maintenance Contract of the equipment at remote areas to assist our Armed Forces. Valuation: Though the revenue declined over the last two quarters due to the several factors the company position to gain from the various government initiatives, especially that of the roadrailer projects and the changing dynamics of various industries, they are expected to perform well in the coming quarters . On valuation front, at the CMP of Rs. 1060.0, the stock is available at cheap valuation at P/E of 41.0(x) compared to peers average of 47.2(x), while EV/EBITDA stood at 38.4(x) compared to the peer average of 30.2(x). Thus we recommend a “Buy, Add on Dips” rating on this stock.

1

Dec 28, 2017

Rating Matrix

CMP Rs. 1060.0

Rating Buy, Add on Dips

Holding Period 2-3 Years Current Level Long Term Investment

Upside Potential 50%

52 week H/L Rs. 1389.9/700.0

Face value Rs. 10

Sector Industrial Machines

Category Small Cap

F&O Stock N/A

Source: Choice Research/ Annual reports; Financial data-Ace equity

Q2FY18 Q2FY17 Change

(YoY) Q1FY18

Change (QoQ)

Change (QoQ)

871.9 1228.2 -29.0% 923.0 -5.5% -24.7% -45.4 64.7 -170.2% -49.9 -9.0% -23.6% -5.2% 5.3% (1050) Bps -5.4% 20 Bps 20 Bps -15.9 63.5 -125.0% -24.5 -35.1% -44.1% -1.8% 5.2% (700) Bps -2.7% 80 Bps (220) Bps

762.2

106.6

3.1

Compression System

Transmission System

Other

Revenue Segmentation

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Kirloskar Pneumatic Company Ltd.

Sensex

2 Source: Choice Research/ Annual reports; Financial data-Ace equity

Financial Snapshot :

Peer Comparison:

Particulars (Rs. Mn) FY13 FY14 FY15 FY16 FY17 Consolidated Standalone Revenue from operations 5488.1 4838.1 4409.6 5088.8 5290.1 Gr (%) 82.3% -11.8% -8.9% 15.4% 4.0% EBITDA (Excl OI) 719.7 572.9 291.3 506.4 608.8 EBITDA Margin (%) 13.1% 11.8% 6.6% 10.0% 11.5% PAT 463.6 352.1 166.9 344.6 527.0 NPM (%) 8.4% 7.3% 3.8% 6.8% 10.0% Net Worth 2712.8 2927.8 3030.5 3290.4 3845.1 Total Assets 4935.7 4801.5 5020.7 5088.7 5694.9 Total Debt 0.0 0.0 0.0 0.0 0.0 Cash flow from Operations 409.6 629.8 31.0 526.6 168.3 D/E (x) 0.0 0.0 0.0 0.0 0.0 Current Ratio (x) 1.66 1.76 1.84 2.15 2.4 Profitablity ratios (%) ROCE (%) 10.0% 7.2% 4.7% 8.8% 11.3% ROE (%) 10.6% 9.9% 8.8% 10.5% 13.7% ROA (%) 4.4% 4.2% 3.5% 6.2% 9.3% Efficiency ratios (x) Receivable days 82.0 83.9 97.4 86.5 89.7 Inventory days 47.4 39.6 38.3 38.0 41.7 Payable days 78.1 68.0 77.4 78.0 76.4

Companies CMP ROE (%) 12MR(%) M. Cap

(Rs. Mn) EPS BVPS

EBIDTA Margin (%)

NPM (%)

Fedders Electric & Engineering Ltd. 75.2 4.8% 33.0 2554.5 6.7 138.4 4.9% 1.7% Johnson Controls - Hitachi Air Conditioning India Ltd.

2590.0 15.9% 88.1 70424.7 29.0 182.8 7.8% 3.7%

Kirloskar Pneumatic Company Ltd. 1060.0 8.2% 45.4 13610.4 25.8 314.2 7.3% 7.0% Average 1241.7 9.6% 55.5 28863.2 20.5 211.8 6.7% 4.1%

Companies P/E (x) P/Bv (x) P/Sales(x) EV/EBIDTA

(x) EV/Sales(

x) PAT(Rs. Mn)

EBIDTA(Rs. Mn)

Sales (Rs. Mn)

Fedders Electric & Engineering Ltd. 11.2 0.5 0.2 10.5 0.5 227.4 648.1 13248.2 Johnson Controls - Hitachi Air Conditioning India Ltd.

89.3 14.2 3.3 41.8 3.3 788.4 1667.8 21443.5

Kirloskar Pneumatic Company Ltd. 41.0 3.4 2.9 38.4 2.8 331.7 348.6 4743.5 Average 47.2 6.0 2.1 30.2 2.2 449.2 888.2 13145.1

3

Setting Up Joint Venture: The company is planning to set up a joint venture with AECOM India Pvt Ltd for carrying out the Air Quality control system business in India. The share capital of the project will be on 50:50 basis. The company is has received letter of acceptance from GSPL India Transco Limited (GITL), for natural gas compression services including supply and installation of gas compression on rental basis for a value for Rs. 600mn. Compression Products: Oil & Gas Business: The company offers refrigeration and gas compression systems for refineries, petrochemical plants, CNG stations to City Gas Distribution companies etc. The company enjoys a strong market leadership position in both these segments. The decrease in crude oil price in the international market and adoption of Bharat VI norms is expected to encourage fresh investment in expansion of oil refining capacities, construction of new refineries, petrochemical complexes, debottlenecking and MSQ projects. All oil companies will be investing in upgrading refining processes in the forthcoming two fiscal years. The Company is also working on export opportunities in specific countries and this is going to add to our current business in Oil & Gas business. Cold Chain Business: With about 140 million ton of fruits and vegetable production, India is second largest producer in the world. India is the largest producer of milk in the world with 100 million ton production. However, an estimated 40% of vegetable produce and 15% of milk is wasted due to improper storage and transportation. The Government of India, therefore, is aggressively pushing for the infrastructure development for cold chain. The Government has also announced incentives for infrastructure development in cold chain. Demand for compressors for cold stores, is therefore, expected to grow in the next few years. Cold chain market is expected to grow at 10% annually. International Business: After a subdued FY17 due to lower private investment, the much needed Government push for the road construction projects, demand for diesel portable compressors has increased. Defense: KPCL is in the business of products like HVAC systems for the Indian Navy and Ground Support Units for defense installations. The Government of India's thrust on “Make in India” in the defense sector is an opportunity for the Company in the coming years. They also takes up Annual Maintenance Contract of the equipment at remote areas to assist our Armed Forces.

Transmission Products: Railway Business: The company, over the years has developed capability of manufacturing entire range of gear pinion requirement of Indian Railways. It has been approved as part 1 supplier for the new generation high speed locomotives manufacturing units of Indian Railways. Demand for railway gears and pinions has remained stagnant with little possibility of growth in near future. Spares demand continued to be similar to previous year. Wind Turbine Gearbox Business: With a change in the Government policy on wind power projects the demand for gearbox has reduced substantially. In fact new wind power annual installations have dramatically dropped. In this diminishing market KPCL has maintained its market share and executed few orders for replacement of gearboxes in the sub megawatt class. Industrial Gearbox Business: With a fluctuating demand in wind turbine gearbox market, the company strategically decided to work in the industrial markets with customized gearboxes. These are planetary gearboxes for sugar mills, cement plants, steel plants. As part of the strategy execution, KPCL has emphasized on developing competency and knowledge base in design and marketing. With this, KPCL has successfully developed and executed some of high-end gearbox orders for applications like cranes, Steel, Cement and Sugar Mills etc. This will help the company will grow in the long term. RoadRailer Project: The Company has developed innovative RoadRailer for the logistics sector. This technology has been developed with the support of Wabash Inc, USA. It offers quicker, safer and economical transportation of cargo. RoadRailer rake manufactured by the Company has successfully completed the EBD (Emergency Brake Distance) test. The company is now awaiting few clearances from the necessary authorities for commencing the operations. There is a Chennai- Delhi project under the pipeline and talks of a Chennai-Mumbai projects are also underway.

Source: Choice Research/ Annual reports; Financial data-Ace equity

16

4.5

24

4.9

20

0.3

15

6.1

16

9.9

0

50

100

150

200

250

300

FY13 FY14 FY15 FY16 FY17

Contribution of Exports

Choice’s Rating Rationale The price target for a large cap stock represents the value the analyst expects the stock to reach over next 12 months. For a stock to be classified as Outperform, the expected return must exceed the local risk free return by at least 5% over the next 12 months. For a stock to be classified as Underperform, the stock return must be below the local risk free return by at least 5% over the next 12 months. Stocks between these bands are classified as Neutral. Don’t be an Investor by Force, Be an investor by CHOICE

• Create a Wealth Building Portfolio with the help of CHOICE Fundamental Research. • CHOICE Fundamental Research will handpick stocks for you to invest in an oversold market by helping you build positions in

heavily beaten down fundamentally strong stocks. • Opportunities to invest in fundamentally strong stocks at a low arise only 2-3 times in a full year cycle. • Investors are advised to sell the stock if the recommended upside potential achieves. • If recommended upside potential remains under-achieved, investors are advised to consider the update report on

suggested stock.

Fundamental Research Team

Name Designation Email id Contact No.

Sunder Sanmukhani Head-Fundamental Research [email protected] 022 - 6707 9910

Satish Kumar Research Analyst [email protected] 022 - 6707 9913

Rajnath Yadav Research Analyst [email protected] 022 - 6707 9912

Aman Lamba Research Associate [email protected] 022 - 67079917

Devanshi Shah Research Associate [email protected] 022 - 67079916

Shrey Gandhi Research Associate [email protected] 022 - 67079914

Dhvanit Wadia Research Associate [email protected] 022 - 67079915

4

OUR TEAM

Disclaimer

This is solely for information of clients of Choice Broking and does not construe to be an investment advice. It is also not intended as an offer or solicitation for the purchase and sale of any financial instruments. Any action taken by you on the basis of the information contained herein is your responsibility alone and Choice Broking its subsidiaries or its employees or associates will not be liable in any manner for the consequences of such action taken by you. We have exercised due diligence in checking the correctness and authenticity of the information contained in this recommendation, but Choice Broking or any of its subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this recommendation or any action taken on basis of this information. This report is based on the fundamental analysis with a view to forecast future price. The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Choice Broking has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Choice Broking makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. The opinions contained within the report are based upon publicly available information at the time of publication and are subject to change without notice. The information and any disclosures provided herein are in summary form and have been prepared for informational purposes. The recommendations and suggested price levels are intended purely for stock market investment purposes. The recommendations are valid for the day of the report and will remain valid till the target period. The information and any disclosures provided herein may be considered confidential. Any use, distribution, modification, copying, forwarding or disclosure by any person is strictly prohibited. The information and any disclosures provided herein do not constitute a solicitation or offer to purchase or sell any security or other financial product or instrument. The current performance may be unaudited. Past performance does not guarantee future returns. There can be no assurance that investments will achieve any targeted rates of return, and there is no guarantee against the loss of your entire investment.

POTENTIAL CONFLICT OF INTEREST DISCLOSURE (as on date of report) Disclosure of interest statement – • Analyst interest of the stock /Instrument(s): - No. • Firm interest of the stock / Instrument (s): - No.

Choice Equity Broking Pvt. Ltd. Choice House, Shree Shakambhari Corporate Park, Plt No: -156-158,

J.B. Nagar, Andheri (East), Mumbai - 400 099.

+91-022-6707 9999 +91-022-6707 9959 www.choicebroking.in

5