deutsche bank ag · q1 2016 q2 2016 q3 2016 q4 2016 q1 2017 q2 2017 q3 2017 q4 2017 q1 2018 q2 2018...

TRANSCRIPT

FINANCIAL INSTITUTIONS

ISSUER COMMENT1 February 2019

Contacts

Michael Rohr +49.69.70730.901VP-Sr Credit [email protected]

Peter E. Nerby, CFA +1.212.553.3782Senior Vice [email protected]

Yana Ruvinskaya +44.20.7772.1618Associate [email protected]

Laurie Mayers +44.20.7772.5582Associate Managing [email protected]

Ana Arsov +1.212.553.3763MD-Financial [email protected]

Deutsche Bank AGQ4 2018: Restructuring progress meets challenging marketconditions

Deutsche Bank AG (DB, A3/A3, negative, ba11) reported a fourth-quarter net loss of€409 million, following a net loss of €2.4 billion in the prior-year quarter2. While partlyowing to additional restructuring and higher loan loss charges booked in the final quarter of theyear, DB suffered from revenue pressure in its Corporate and Investment Bank (CIB), as well asin Asset Management (AM). This could not be compensated for by a better-than-expected costperformance with total adjusted expenses of €22.8 billion for 2018, below the bank’s €23 billiontarget (Q4 2018: €5.4 billion). Overall, and considering the more adverse market conditionsduring the fourth quarter of 2018, the results are in-line with our expectations.

On a pretax operating basis3, DB reported a €387 million pretax loss for Q4 2018, comparedto a €1.1 billion loss one year ago. Based on a normalised tax rate of 35%, DB’s net returnon risk weighted assets (RWA) stood at -29 basis points (bps) for the quarter, comparedto -86 bps one year ago. On this basis, the bank's underlying post-tax return on averageshareholder’s equity stood at -1.6% compared to -4.5% in Q4 2017.

Challenging market conditions strain revenues. Revenue generation was weakercompared to last year’s fourth quarter, especially in the Corporate and Investment Bank,driven by significantly lower client activity negatively affecting the bank’s fixed incomebusinesses. Deutsche Bank’s ability to rebuild and stabilize revenues in coming quartersacross the various businesses will be paramount to the long term success of its restructuringplan and remains work in progress.

Progress on costs becomes visible. DB reported adjusted costs of €5.4 billion in thequarter, down 15% compared to Q4 2017 and down 1% sequentially. Thereby, DB beat itscost target of €23 billion for 2018 and also slightly lowered its 2019 (adjusted) cost targetfrom €22 billion to €21.8 billion. Considering the firms progress in reducing staff (year-endfull-time staff of 91,737 versus the planned <93,000), we believe DB is well on track toachieve this revised cost target.

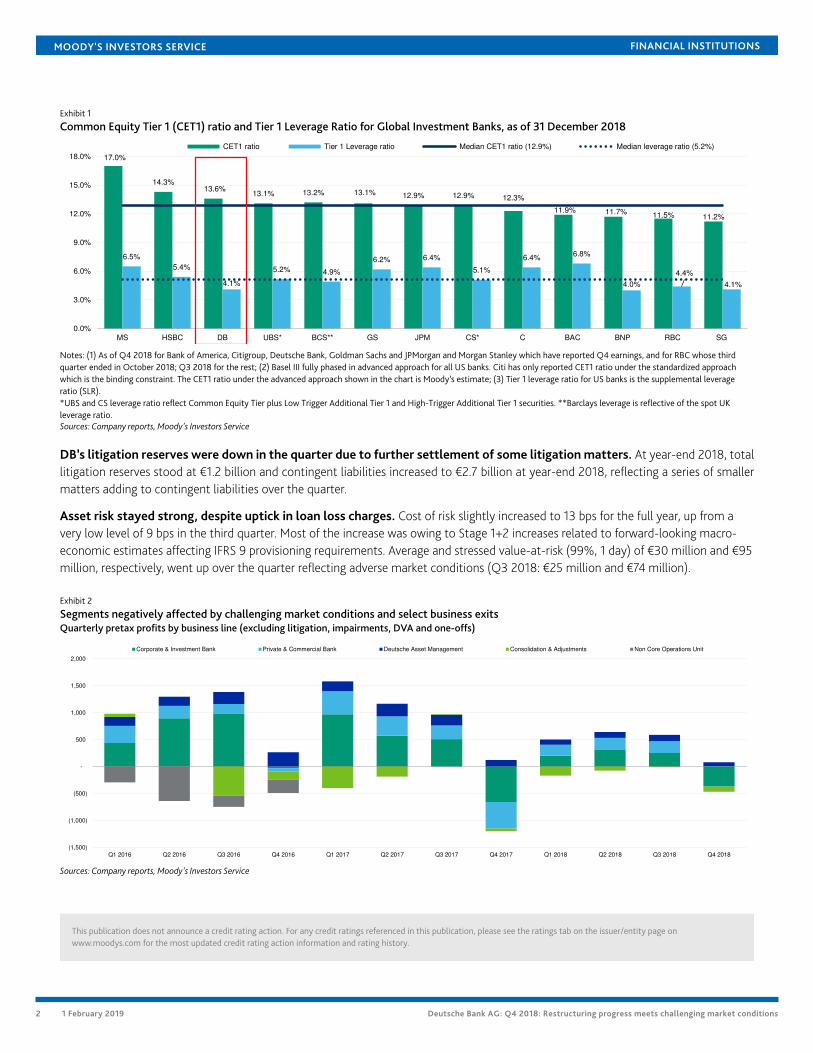

Capital and liquidity remain sound. Although DB recorded a loss for the quarter, itscapitalization and balance sheet liquidity remained sound. On the back of higher RWA asa result of heightened market risk, DB’s Common Equity Tier 1 (CET1) ratio declined to13.6%, down from 14.0% as of the end of the third quarter. Despite the decline, DB remainedpositioned above the peer group average (see Exhibit 1). The firm’s leverage ratio of 4.1%improved slightly over the quarter. In addition, DB’s balance sheet remained very liquid: DBreported a liquidity reserve of €259 billion and a LCR of 140% as of year-end 2018.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Exhibit 1

Common Equity Tier 1 (CET1) ratio and Tier 1 Leverage Ratio for Global Investment Banks, as of 31 December 2018

17.0%

14.3%13.6%

13.1% 13.2% 13.1% 12.9% 12.9% 12.3%

11.9% 11.7% 11.5% 11.2%

6.5%

5.4%

4.1%

5.2% 4.9%

6.2% 6.4%

5.1%

6.4%6.8%

4.0%

4.4%

4.1%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

MS HSBC DB UBS* BCS** GS JPM CS* C BAC BNP RBC SG

CET1 ratio Tier 1 Leverage ratio Median CET1 ratio (12.9%) Median leverage ratio (5.2%)

Notes: (1) As of Q4 2018 for Bank of America, Citigroup, Deutsche Bank, Goldman Sachs and JPMorgan and Morgan Stanley which have reported Q4 earnings, and for RBC whose thirdquarter ended in October 2018; Q3 2018 for the rest; (2) Basel III fully phased in advanced approach for all US banks. Citi has only reported CET1 ratio under the standardized approachwhich is the binding constraint. The CET1 ratio under the advanced approach shown in the chart is Moody’s estimate; (3) Tier 1 leverage ratio for US banks is the supplemental leverageratio (SLR).*UBS and CS leverage ratio reflect Common Equity Tier plus Low Trigger Additional Tier 1 and High-Trigger Additional Tier 1 securities. **Barclays leverage is reflective of the spot UKleverage ratio.Sources: Company reports, Moody's Investors Service

DB’s litigation reserves were down in the quarter due to further settlement of some litigation matters. At year-end 2018, totallitigation reserves stood at €1.2 billion and contingent liabilities increased to €2.7 billion at year-end 2018, reflecting a series of smallermatters adding to contingent liabilities over the quarter.

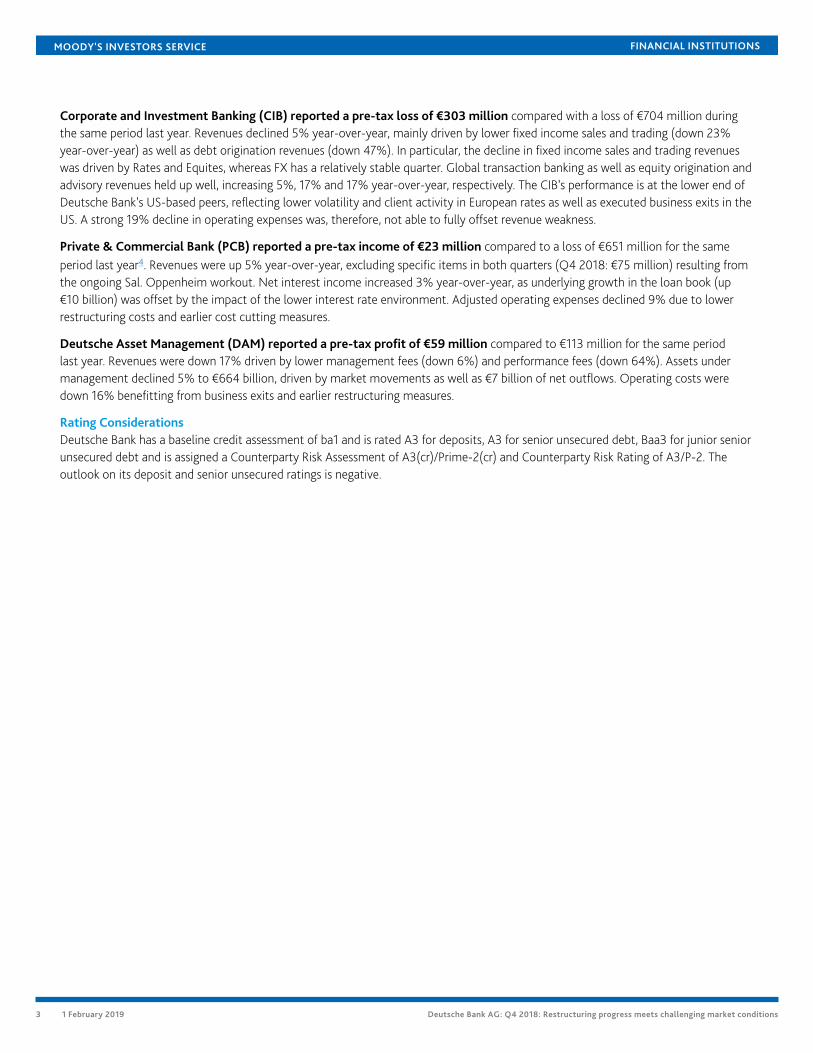

Asset risk stayed strong, despite uptick in loan loss charges. Cost of risk slightly increased to 13 bps for the full year, up from avery low level of 9 bps in the third quarter. Most of the increase was owing to Stage 1+2 increases related to forward-looking macro-economic estimates affecting IFRS 9 provisioning requirements. Average and stressed value-at-risk (99%, 1 day) of €30 million and €95million, respectively, went up over the quarter reflecting adverse market conditions (Q3 2018: €25 million and €74 million).

Exhibit 2

Segments negatively affected by challenging market conditions and select business exitsQuarterly pretax profits by business line (excluding litigation, impairments, DVA and one-offs)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018

Corporate & Investment Bank Private & Commercial Bank Deutsche Asset Management Consolidation & Adjustments Non Core Operations Unit

Sources: Company reports, Moody's Investors Service

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Corporate and Investment Banking (CIB) reported a pre-tax loss of €303 million compared with a loss of €704 million duringthe same period last year. Revenues declined 5% year-over-year, mainly driven by lower fixed income sales and trading (down 23%year-over-year) as well as debt origination revenues (down 47%). In particular, the decline in fixed income sales and trading revenueswas driven by Rates and Equites, whereas FX has a relatively stable quarter. Global transaction banking as well as equity origination andadvisory revenues held up well, increasing 5%, 17% and 17% year-over-year, respectively. The CIB’s performance is at the lower end ofDeutsche Bank’s US-based peers, reflecting lower volatility and client activity in European rates as well as executed business exits in theUS. A strong 19% decline in operating expenses was, therefore, not able to fully offset revenue weakness.

Private & Commercial Bank (PCB) reported a pre-tax income of €23 million compared to a loss of €651 million for the sameperiod last year4. Revenues were up 5% year-over-year, excluding specific items in both quarters (Q4 2018: €75 million) resulting fromthe ongoing Sal. Oppenheim workout. Net interest income increased 3% year-over-year, as underlying growth in the loan book (up€10 billion) was offset by the impact of the lower interest rate environment. Adjusted operating expenses declined 9% due to lowerrestructuring costs and earlier cost cutting measures.

Deutsche Asset Management (DAM) reported a pre-tax profit of €59 million compared to €113 million for the same periodlast year. Revenues were down 17% driven by lower management fees (down 6%) and performance fees (down 64%). Assets undermanagement declined 5% to €664 billion, driven by market movements as well as €7 billion of net outflows. Operating costs weredown 16% benefitting from business exits and earlier restructuring measures.

Rating ConsiderationsDeutsche Bank has a baseline credit assessment of ba1 and is rated A3 for deposits, A3 for senior unsecured debt, Baa3 for junior seniorunsecured debt and is assigned a Counterparty Risk Assessment of A3(cr)/Prime-2(cr) and Counterparty Risk Rating of A3/P-2. Theoutlook on its deposit and senior unsecured ratings is negative.

3 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Moody's Related ResearchCredit Opinions

» Deutsche Bank AG, August 2018

Issuer Comment

» CEO change highlights strategic challenges still confronting Deutsche Bank

» Deutsche Bank passes credit-positive milestone with IPO of DWS Asset Management

Issuer In-Depth

» Cleaner balance sheet buys time to execute deep reengineering

» Deutsche Bank AG: Capital Raise, Strategic Course Correction Are Credit Positive

Rating Action

» Moody's downgrades Deutsche Bank legacy senior debt to Baa3 following change in bank insolvency law and affirms A3counterparty and deposit ratings

Banking System Outlook

» Germany, October 2018

Rating Methodology

» Banks, August 2018

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of thisreport and that more recent reports may be available. All research may not be available to all clients.

4 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Endnotes1 The ratings shown in this report are DB’s deposit rating, senior unsecured debt rating, outlook, and baseline credit assessment (BCA).

2 All figures in this report relate to Q4 2018 and comparisons are made to Q4 2017, unless otherwise indicated.

3 This excludes asset sale gains, impairments, litigation, and DVA.

4 The prior-year result was negatively affected by a €157 million loss related to the now executed disposal of DB's Polish retail banking activities.

5 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2019 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SRATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDITRATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAYALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDITRATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONSARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONSWITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDERCONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for ratings opinions and services rendered by it feesranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1159849

6 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Contributors

Yana RuvinskayaAssociate Analyst

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

7 1 February 2019 Deutsche Bank AG: Q4 2018: Restructuring progress meets challenging market conditions