determinants of academic cheating behavior: the future for accountancy in ireland

TRANSCRIPT

DT

Ja

b

c

ARRA

KICGIR

1

acstaatA

tIfsChe

0h

Accounting Forum 38 (2014) 55– 66

Contents lists available at ScienceDirect

Accounting Forum

jo u r n al homep age : www.elsev ier .com/ locate /acc for

eterminants of academic cheating behavior:he future for accountancy in Ireland

.A. Ballantinea,∗, P. McCourt Larresb, M. Mulgrewc

Department of Accounting, University of Ulster, Jordanstown BT37 0QB, United KingdomQueen’s University Management School, Queen’s University, Belfast BT9 5EE, United KingdomDCU Business School, Dublin City University, Dublin 9, Ireland

a r t i c l e i n f o

rticle history:eceived 29 August 2012eceived in revised form 2 August 2013ccepted 25 August 2013

eywords:rish accountancy professionheating behaviorender

dealismelativism

a b s t r a c t

This paper considers the potential for improving the reputation of the Irish accountancyprofession by exploring undergraduate accounting students’ intolerance of academic cheat-ing as a predictor of future attitudes to unethical workplace practices. The study reportsthat females are significantly more intolerant of cheating than males. Further, with regardto ethical ideology, idealism was found to have a significant positive association withintolerance of cheating while relativism reported no association. It is anticipated that thegrowing admission of women to professional accountancy membership together with edu-cational intervention to increase idealism may improve ethical attitudes and help restorethe profession’s reputation.

© 2013 Elsevier Ltd. All rights reserved.

. Introduction

The basic premise of efficient capital market investment is that the financial information on which investment decisionsre made is reliable. A crucial factor impinging upon reliability is the honesty and integrity of those involved in finan-ial statement preparation. However, in recent years public confidence in financial reporting has been undermined by aeries of high profile corporate scandals which have exposed extremely dishonest financial practices. There is little doubthat these major financial scandals have damaged the reputation of the accountancy profession. To address the problem,ccounting regulators have issued rigorous and far-reaching legislation (for example the Sarbanes Oxley Act 2002 in the US)nd established dedicated regulatory bodies such as the Public Company Accounting Oversight Board (PCAOB) in the US,he Monitoring Committee of the Financial Reporting Council in the UK and the Irish Auditing and Accounting Standardsuthority (IAASA).

One country which has seen its fair share of unethical business practices among accountants at a very high level, par-icularly in the banking sector,1 is Ireland. As a result, the reputation of accountants in this small island has been damaged.ndeed recently, in an open letter to the membership, the president of Chartered Accountants Ireland (CAI) commented that,ollowing recent financial scandals affecting the profession, restoring its reputation was the first and most crucial of the fivetrategic objectives that the CAI’s Council had set itself over a 5 year period from 2012. Set against the backdrop of what the

AI president referred to as the biggest and longest recession in living memory, it is hardly surprising that the Irish publicave taken exception to the fact that they are expected to make considerable economic and financial sacrifices while newsmerges that wealthy accountants have been engaging in dubious self-serving financial transactions. With the importance∗ Corresponding author. Tel.: +44 028 90366204; fax: +44 028 90368502.E-mail address: [email protected] (J.A. Ballantine).

1 See for example, Ryan (2011) which discusses the case of Anglo-Irish Bank.

155-9982/$ – see front matter © 2013 Elsevier Ltd. All rights reserved.ttp://dx.doi.org/10.1016/j.accfor.2013.08.002

56 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

of this issue in mind, the current study assesses the prospects for restoring public confidence in the Irish accountancy pro-fession by considering the ethical judgment of future accountancy professionals as measured by undergraduate accountingstudents’ intolerance of academic cheating. This approach is consistent with that of Allmon, Page, and Robert (2000) whosuggested that attitudes to academic cheating are an indicator of future attitudes to unethical business practices. In otherwords, what students deem acceptable behavior in the classroom impacts upon their expectations of what is acceptableprofessionally (Nonis & Swift, 2001).

By using undergraduate accounting students’ intolerance of academic cheating to predict Irish accountants’ future ethicaljudgment, the current study also addresses a deficiency in the literature highlighted by Pierce and Sweeney (2010) in theirstudy of ethical decision making among Irish trainee accountants. They concluded that greater priority should be given toethical decision making by accounting educators, researchers and practitioners. The current study’s focus on intoleranceof academic cheating addresses Pierce and Sweeney’s (2010) suggestion with respect to one particular aspect of ethicaldecision making, namely ethical judgment.

The current study adopts a multi-campus approach and considers the variables which may influence Irish accountingstudents’ intolerance of cheating behavior. It explores three possible determinants of intolerance of cheating behavior,namely gender, idealism and relativism: the latter two being constructs of ethical ideology. In so doing, it sheds light onwhy some individuals may be more intolerant of academic cheating than others and considers the implications of this forrestoring confidence in the Irish accountancy profession.

The results of the study provide contemporary evidence that both gender and idealism are significantly associated withintolerance of cheating behavior, with females and idealists displaying greater levels of intolerance. However, the otherconstruct of ideology, namely relativism, was found to have no such association. Accordingly, it could be concluded fromthese findings that influencing idealism among accounting students could make a positive contribution to improving ethicalattitudes in the classroom and, thereafter, in the workplace. Furthermore, the finding that female accounting students aremore intolerant of cheating than their male counterparts augurs well for accountancy in Ireland in that female representationin the profession has risen in recent years (Financial Reporting Council, 2013). It is anticipated that this gender trend togetherwith educational intervention to influence levels of idealism could result in an overall improvement in ethical judgmentwhich may go some way to restore integrity to the profession.

The remainder of the paper is structured as follows. First, a literature review presents a comprehensive consideration ofresearch in the area. Secondly, the research method applied to the study is set out. Thirdly, the results of the tests undertakenare analyzed and discussed. Finally, conclusions are discussed, limitations of the study considered and further work identified.

2. Literature review

2.1. Cheating in an academic context

Cheating is defined as acting dishonestly or unfairly to gain an advantage (Oxford English Dictionary). When applied toan academic environment, this definition provides students with a range of opportunities to engage in cheating behavior.A review of the literature identifies a number of examples of behavior which constitute cheating. These include, for exam-ple: the use of unauthorized materials in exams or assignments; fabricating information, references or results; intentionalplagiarism; providing false excuses for missed exams; and facilitating or assisting other students to commit a dishonestacademic act (see for example, McCabe & Trevino, 1993; Pratt & McLaughlin, 1989).

In one of the earliest US studies to consider academic cheating Bowers (1964) drew on a large sample from a numberof campuses and reported that business students engaged in various forms of academic dishonesty (including turning inwork done by another and plagiarism) and that ‘honor codes’ were associated with lower levels of cheating. A number ofsimilar multi-campus studies followed that of Bowers (1964). For example, McCabe and Trevino (1993) reported that peerbehavior had the most significant relationship with student cheating and that lower levels of cheating were associated withthe existence of an ‘honor code’. Collecting data across the same campuses as Bowers (1964), McCabe and Bowers (1994)reported an increase in cheating among male undergraduate college students between 1963 and 1991. More recently,McCabe, Ingram, and Dato-on (2006), using a large data set from the US and Canada, found that graduate business studentscheat more than their non-business peers and that cheating was most significantly associated with perceived peer behavior.

Whilst a substantial body of research into academic dishonesty has focused on North American institutions, some similarwork has been conducted elsewhere. For example, in the UK, Franklyn-Stokes and Newstead (1995) reported high levelsof cheating and Newstead, Franklin-Stokes, and Armstead (1996) found that less able, less intrinsically motivated youngermale students tended to cheat more. These findings were confirmed in later UK based work by Norton, Tilley, Newstead, andFranklyn-Stokes (2001). More recently, Kidwell and Kent (2008) considered attitudes to various cheating behavior amongAustralian students studying on campus and via distance learning. They reported that, while age and gender were significantinfluences on cheating behavior, mode of study (namely, on campus versus distance learning) was more significant.

In an Irish context, some limited research has focused on one aspect of cheating behavior, namely plagiarism. Ledwith and

Risquez (2008) explored the effects of introducing the anti-plagiarism software tool Turnitin to 197 first year Irish engineeringstudents. The findings of the study suggested that students were generally positive about the use of the software, makingthem more aware of the originality of their own work. A significant reduction in internet plagiarism as a result of the use ofTurnitin was also reported. More recently, Risquez, O’Dwyer, and Ledwith (2011) reported that an online plagiarism tutorial

eo

2

mnmBtaarst

&e&(

uOwr(Tpswso

sswjojtdTs

tSersdiipsa

bao(

J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66 57

nabled entrepreneurship students to better recognize and avoid plagiarism. However, the authors argued that more thanne prevention tutorial may be required to substantially change views related to engagement in plagiarism.

.2. Gender

Of all the factors thought to influence ethical judgment both in the classroom and in the workplace, gender is the deter-inant variable most frequently reported. However the results of this empirical work have been far from consistent. A

umber of these studies has concluded that gender has a significant impact on ethical decision making and that men areore likely to become involved in unethical behavior than women (see for example Ameen, Guffey, & McMillan, 1996; Beu,

uckley, & Harvey, 2003; Pierce & Sweeney, 2010). Terpstra, Rozelle, and Robinson (1993) suggested that, because menend to be more competitive, the finding that competitive individuals exhibit a predilection for unethical behavior providesdditional support for a difference between the genders. In a recent study which focuses on Irish trainee accountants, Piercend Sweeney (2010) investigated gender differences in relation to ethical judgment, intention, intensity and culture. Withespect to ethical judgment, the subject of the current study, they reported that Irish female trainee accountants demon-trated higher ethical judgment than their male counterparts in relation to all four audit scenarios investigated. However,he findings were not conclusive in that these differences were significant in respect of only one scenario.

Conversely, a number of studies have found no relationship between gender and ethical behavior (see for example, Davis Welton, 1991; Radtke, 2000; Sikula & Costa, 1994; Stanga & Turpen, 1991). This body of research reports gender equality inthical judgment with respect to, for example, accounting students (Stanga & Turpen, 1991), college business students (Davis

Welton, 1991), management undergraduates across three years of study (Sikula & Costa, 1994) and practicing accountantsRadtke, 2000).

The lack of consensus across these gender ethics studies reflects the contrasting views of the two major theories whichnderpin the relationship between gender and moral judgment, namely gender socialization theory and structural theory.n the one hand, gender socialization theory contends that gender identity, established at an early age, results in men andomen bringing different ethical values to bear on their academic or workplace ethical behavior and, as a consequence,

esults in them making different ethical decisions (Betz, O’Connell, & Shepard, 1989). This thesis is consistent with Gilligan’s1982) ‘ethic of caring’ in which she identified a compassionate dimension present only in female ethical decision making.he result, according to Gilligan (1982), is that women are more ethical than men. On the other hand, a contrast in gendererspective is offered by the structural approach which suggests that different values which may have existed between theexes in their early years gradually disappear as men and women are subject to similar education and training programs,ork environments and reward structures (Betz et al., 1989). Applying the structural theory specifically to accounting

tudents, Ameen et al. (1996) concluded that ‘the structural approach predicts that men and women. . .training for a particularccupation will exhibit the same ethical priorities’ (p. 593).

Adopting the basic premise that ethical judgment in the classroom predicts future ethical judgment in a professionaletting, several studies have tested these alternative gender theories on the ethical judgment of business and accountingtudents. One of the earliest of these studies was carried out by Betz et al. (1989) who, after presenting business studentsith a number of open-ended questions pertaining to their career goals, reported that females demonstrated greater ethical

udgment than males, providing evidence to support the gender socialization theory. However, in a similar study carried outn accounting students around the same time, Stanga and Turpen (1991) found no evidence of gender difference in ethicaludgment and concluded, in support of the structural approach, that ‘behavioral differences that once existed betweenhe sexes now seem to be rapidly disappearing’ (Stanga & Turpen, 1991, p. 746). Continuing the investigation of genderifferences among accounting students, Ameen et al. (1996) reported results that contrasted with those of Stanga andurpen (1991) but supported the work of Betz et al. (1989) namely that ‘the gender socialization approach dominates thetructural approach’ (Ameen et al., 1996, p. 591).

The gender differences reported by Ameen et al. (1996) were based on a survey instrument containing examples of ques-ionable academic activities with which the students were familiar rather than real-world scenarios such as those adopted bytanga and Turpen (1991). Ameen et al.’s approach mirrored that of Forrest and Pritchett (1990) who recommended that thethical judgment of business students is best assessed using classroom activities with which they are familiar i.e. ‘a temporaleality’ rather than presenting them with unfamiliar real-world business scenarios which create ‘a remote, unexperiencedituation’ (Forrest & Pritchett, 1990, p. 118). Forrest and Pritchett (1990) operationalized the students’ temporal reality byeveloping the Cheating Behaviors Questionnaire (CBQ) containing a number of questionable classroom behaviors based on

ssues which business executives had highlighted as being unethical. For example, claiming credit for someone else’s work,dentified as an unethical practice by business executives (Ferrell & Weaver, 1978) was included in the CBQ as items such aslagiarizing published material and having someone else complete an assignment. Accordingly, by employing an instrumentuch as the CBQ, students’ evaluation of the acceptability of cheating in the classroom represents their evaluation of what iscceptable in a business context (Forrest & Pritchett, 1990).

The seminal gender ethics studies carried out by Stanga and Turpen (1991) and Ameen et al. (1996) were influenced

y the increasing representation of females in the accountancy profession in the US. This trend has also been a feature ofccountancy in Ireland where a traditionally male-dominated profession (Flood & Wilson, 2008) has, over time, given way tone which reflects a more equal gender balance. For example, recent statistics report an equal gender split among studentsi.e. 50% females and 50% males) registering as Irish chartered accountancy students in 2012 (Financial Reporting Council,

58 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

2013). Accordingly, the current study aims to contribute to and update the extant literature on gender ethics by providing acontemporary perspective on the issue within an Irish accountancy context. To this end, the following hypothesis is tested:

Hypothesis 1. There is no association between undergraduate accounting students’ intolerance of cheating behavior andtheir gender.

2.3. Ethical ideology

Ethical ideology is defined as one’s approach to ethical decision making and is considered to be a determinant of ethicaljudgment (Forsyth, 1980). According to Schlenker and Forsyth (1977), one’s ethical ideology comprises two scales, namelyidealism and relativism. An individual’s levels of idealism and relativism are assessed using the Ethics Position Questionnaire(EPQ) developed by Forsyth (1980). Idealism is concerned with the extent to which an individual has a genuine concern forthe welfare of others and for taking only those actions which do not harm others (Forsyth, 1992). A high level of idealismsuggests a tendency to assume that good consequences ensue from the proper action being taken. Alternatively, a low levelof idealism acknowledges that bad as well as good consequences may follow an action. Relativism is associated with theacceptance of moral rules. High levels of relativism are associated with individuals who reject universal moral rules whilethose who adopt a less relativistic position stress the importance of following universal moral principles when making anethical decision.

Schlenker and Forsyth (1977) developed their ethical construct of idealism and relativism from the classical philosophiesof deontology, teleology and ethical skepticism. Deontology applies pre-defined rules or duties to determining the choiceof action in an ethical dilemma. In deontological ethics the moral rightness of an action is judged by a characteristic ofthe action itself rather than the product of the action. The motivation of the agent in performing the action rather thanthe consequences of the action determines whether it is good or bad. This contrasts markedly with teleological ethicswhich proposes that moral judgment regarding an action should be based on the consequences that are likely to ensuefrom the action. The rigid normative position of both these philosophies is, however, rejected in the various branchesof ethical skepticism. Ethical skepticism, which includes emotivism, cultural relativism and ethical egoism, completelyrefutes the notion of following universal rules when faced with a moral dilemma, irrespective of whether the rules arefounded on deontological or teleological principles. Indeed, ethical skepticism, on account of its pragmatism, is the preferredethical philosophy of a number of researchers when faced with the inherent difficulties of applying the rigid normativepropositions of both deontology and teleology to resolve ethical dilemmas in a business context (Barnett, Bass, & Brown,1994).

Schlenker and Forsyth (1977), in establishing the scales of idealism and relativism, abandoned the notion of a normativeposition of rightness entrenched in both deontology and teleology and, instead, considered the differences among all threeclassical theories with regard to rules-orientation and pragmatism. For example, deontology is associated with high levelsof idealism in that both are concerned with the welfare of individuals and treating each person ethically irrespective of thepotential consequences. Teleology, on the other hand, is allied to the non-idealistic position insofar as both acknowledgethat bad as well as good consequences may ensue from an action: the utilitarian aspect of teleology being that positiveconsequences must outweigh negative. Ethical skepticism, on account of its various branches, is associated with the completeidealism scale from the non-idealistic pure pragmatic perspective through to high levels of idealism (Barnett, Bass, & Brown,1996).

The association between relativism and the classical philosophies is less diverse in that both deontology and teleology areassociated with a non-relativistic position. Analogous to the non-relativistic view, they both promote adherence to universalmoral principles, teleology’s being based on the consequences of an action and deontology’s on the intrinsic rightness of anaction based on pre-determined rules and duties. However, the various branches of ethical skepticism, on the other hand,espouse a very clear relativistic perspective in that they completely renounce the notion of universal moral rules.

A number of studies have investigated the impact of idealism and relativism on ethical decision making among students.While Chan and Leung (2006) and Forsyth and Berger (1982) found limited association between idealism and relativism onthe one hand and ethical decision making on the other, the majority of studies have reported that idealism is more positivelyand significantly associated with stricter ethical judgment than relativism. For example, Barnett et al. (1994) confirmed thestronger influence of idealism on stricter ethical judgment among US business studies students when presented with a widerange of work-based moral dilemmas. In a later study, again by Barnett et al. (1996), idealism was found to have a strongerimpact than relativism on business studies students’ intention to report cheating behavior. In more recent work, Sierra andHyman (2008) also found evidence to suggest that high levels of idealism are associated with efforts to minimize cheatingintentions.

The current study also focuses on the impact of students’ ethical ideology, as determined by their levels of relativism andidealism, on their intolerance of classroom cheating behavior, but does so specifically in an Irish accountancy context. Giventhat ‘it has been demonstrated that unethical behavior in school can lead to unethical behavior in business’ (Granitz & Loewy,2007, p. 293), it is anticipated that the findings of the current study will provide contemporary evidence of how scale-basedethical ideology may impact on the ethical judgment of future accountancy professionals at a time when financial institutionsin general and the reputation of the modern Irish accountant in particular have been called into question (O’Carroll, 2010).

Ha

Ha

3

3

twstb

BPblaoraacuwoi“c

iwtnoiseftmtsaf

3

gt

3

t

J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66 59

Given the foregoing discussion, the following hypotheses are stated for testing:

ypothesis 2. There is a negative association between accounting undergraduate students’ intolerance of cheating behaviornd their level of relativism.

ypothesis 3. There is a positive association between accounting undergraduate students’ intolerance of cheating behaviornd their level of idealism.

. Methodology

.1. Measuring cheating behavior

The hypotheses developed in the current study were tested using an ordered Logit model, the aim being to understandhe relationship between students’ intolerance of cheating behavior, gender, relativism and idealism. A multi-campus studyas employed. A questionnaire comprising three sections was developed and distributed at three Irish universities. The first

ection of the questionnaire was designed to elicit general information regarding the respondents. Given the sensitivity ofhe subject matter and in line with ethics policy at the three universities, this section was designed to collect inoffensiveackground information such as gender and country where pre-university education was obtained.

The second section contained a number of statements pertaining to unethical classroom behavior set out in the Cheatingehaviors Questionnaire (CBQ) developed by Forrest and Pritchett (1990). Following the approach adopted by Forrest andritchett (1990), accounting students’ ethical judgment in the current study is measured by their attitude to unethicalehavior in the classroom rather than presenting them with unfamiliar real-world business case scenarios as ‘most students

ack corporate work experience’ (Jones, Hamilton, & Ingram, 2007, p. 40). Indeed, it is for this reason that the CBQ has beendopted in a number of studies which have gauged ethical judgment among business and accounting students as a predictorf future workplace ethical judgment (see for example Allmon et al., 2000; Jones et al., 2007). The CBQ comprises nine itemsepresenting common types of academic cheating behavior, such as cheating in an exam and copying extracts from publishedrticles. Sample statements include, “I believe cheating in an exam is. . .” and “I believe plagiarizing published articlesnd submitting them as my own work is. . .”. The CBQ requires respondents to evaluate the ethicality of these classroomheating behaviors by selecting a position on a Likert-type scale ranging from (1) ‘always acceptable’ through to (5) ‘alwaysnacceptable’. In terms of moral philosophy, ‘always unacceptable’, represents the deontological perspective of moral truthherein cheating, lying and stealing are intrinsically wrong. On the other hand, ‘always acceptable’ approaches a position

f ethical amorality or ethical nihilism, the former contending that common good is served by adopting a position of self-nterest (Steiner & Steiner, 2011), the latter denying the existence of any objective moral truth. The tenth statement, namelyI believe that honesty is more important than getting good grades”, captures the student’s general attitude to classroomheating. It is also answered from a five-point Likert scale with (5) “agree strongly” and (1) “disagree strongly” as anchors.

To ascertain students’ intolerance of academic cheating behavior, responses to the ten statements were consolidatednto a single metric. This variable, ‘WBEHt’ is a weighted measure which gauges students’ intolerance of academic cheating

ith higher (lower) values indicating greater (less) intolerance. In order to develop this weighted measure, an analysis ofhe ten cheating behaviors which comprise the CBQ was first undertaken. Three areas of cheating behavior were identified,amely behavior related to cheating in examinations, behavior related to cheating in continuous assessment activity andther more general aspects of cheating behavior. Following this, a review of the accounting programs in all three institutionsnvolved in the study was undertaken to ascertain the contribution of examinations and continuous assessment to measuringtudents’ progress. This review identified the existence of notable consistencies in terms of the weightings attached toxamination and continuous assessment marks across the three institutions, with substantially more marks being awardedor the former. Given this, the following weightings were applied. A higher weight (65%) was attached to the questions inhe CBQ pertaining to the potential for cheating in examinations. This reflects the greater contribution which examinations

ake to the universities’ overall degree classification. With respect to continuous assessment, a weight of 25% was attachedo reflect the lower contribution that continuous assessment makes toward the academic progress of the students in theample. Finally, the remaining 10% weighting was allocated to the statements in the CBQ which related to more generalspects of cheating behavior. The resulting dependent variable, namely WBEHt, was then rounded to the nearest integer toacilitate use of the ordered Logit model.

.2. Measuring gender

A key facet of the current study is to test for the association between students’ intolerance of cheating behavior andender. Accordingly, ‘GENDERt’ is included as an independent variable and is set equal to 1 if the student is female and 0 ifhe student is male.

.3. Measuring relativism and idealism

The final section of the questionnaire was designed to measure respondents’ levels of relativism and idealism usinghe Ethical Position Questionnaire (EPQ). It contains 20 statements, 10 measuring relativism and 10 measuring idealism.

60 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

Relativism statements include, for example, “Different types of morality cannot be compared to ‘rightness”’ and “There areno ethical principles that are so important that they should be a part of any code of ethics”. Statements to measure idealisminclude: “People should make certain that their actions never intentionally harm another even to a small degree” and “Theexistence of potential harm to others is always wrong, irrespective of the benefits to be gained”. Respondents’ agreementor disagreement with the statements was registered using a five-point Likert scale ranging from (5) “agree strongly” to (1)“disagree strongly”. Consistent with Forsyth (1980), an average of students’ responses for each of the ten questions making upthe relativism subscale was calculated. The resulting variable, ‘RELt’ provides an average score of students’ relativism, namelya measure of the extent to which they accept/reject universal moral rules. Similarly, the average of students’ responses foreach of the ten questions relating to idealism was computed. The resulting variable, namely ‘IDEALt’, provides an averagescore of students’ idealism, measuring their tendency to assume that good/bad consequences ensue from the action beingtaken.

3.4. Model specification

Hypotheses 1–3 are empirically tested using the following ordered Logit model:

WBEHt = ˛0 + ˛1GENDERt + ˛2RELt + ˛3IDEALt + ˛4PRE-EDt + ˛5 AGEt + ˛6UNIt + εt

The above model includes a number of control variables. First, ‘PRE-EDt’ which is set equal to 1 if the student has receivedthe bulk of his/her pre-university education outside Ireland and 0 if otherwise. Secondly, ‘AGEt’ measures the student’sage. Finally, given the multiple sources of data used in the study, the variable ‘UNIt’ is included in the model to capturepotential diversity among universities. This variable is coded 1 for students enrolled at University 1, 2 for students enrolledat University 2 and 3 for students enrolled at University 3.

3.5. Sample and data collection

All respondents surveyed were enrolled on accounting undergraduate degree programs, each of three years’ duration.The universities in the study all enjoy a close relationship with Chartered Accountants Ireland (CAI), wherein their respectivedegree programs conform to and reflect the content of the CAI’s professional training program. In so doing, the three univer-sities provide accounting graduates with generous exemptions from the CAI’s professional examinations for qualification asIrish chartered accountants. To this end, there is substantial comparability among the accounting degree programs providedby the three universities, thereby rendering the sample relatively homogeneous in this regard.

Questionnaires were distributed to accounting undergraduate students at the three Irish universities. Prior to distribu-tion, the instructors provided guidance on completing the research instrument and the respondents were informed that theresults were to be used for research purposes only. Students were given approximately 20 minutes to complete the ques-tionnaire. Usable questionnaires were obtained for 752 students, representing 295 (39%) from University One, 270 (36%)from University Two and 187 (25%) from University Three (representing 76.6% of students enrolled in accounting programsat the three universities).

Prior to analysis, the data were tested for internal consistency reliability using Cronbach’s alpha. The reliability coefficientsmeasured 0.789 for the classroom behavior statements, and 0.71 and 0.830 for the relativism and idealism subscales respec-tively. Since a reliability coefficient of .70 or higher is considered acceptable in most social science research situations, theseresults indicate that the internal consistency and reliability of the CBQ and the EPQ, used in this research, are acceptable.Additionally, since the total sample includes respondents from different universities, all variables included in the model weretested for homogeneity. The results showed no significant differences in the variables tested among the three universitiessurveyed. Therefore, following the approach adopted by Allmon et al. (2000), responses from the three universities werecombined to constitute the total sample to be tested.

4. Analysis and findings

4.1. Descriptive statistics

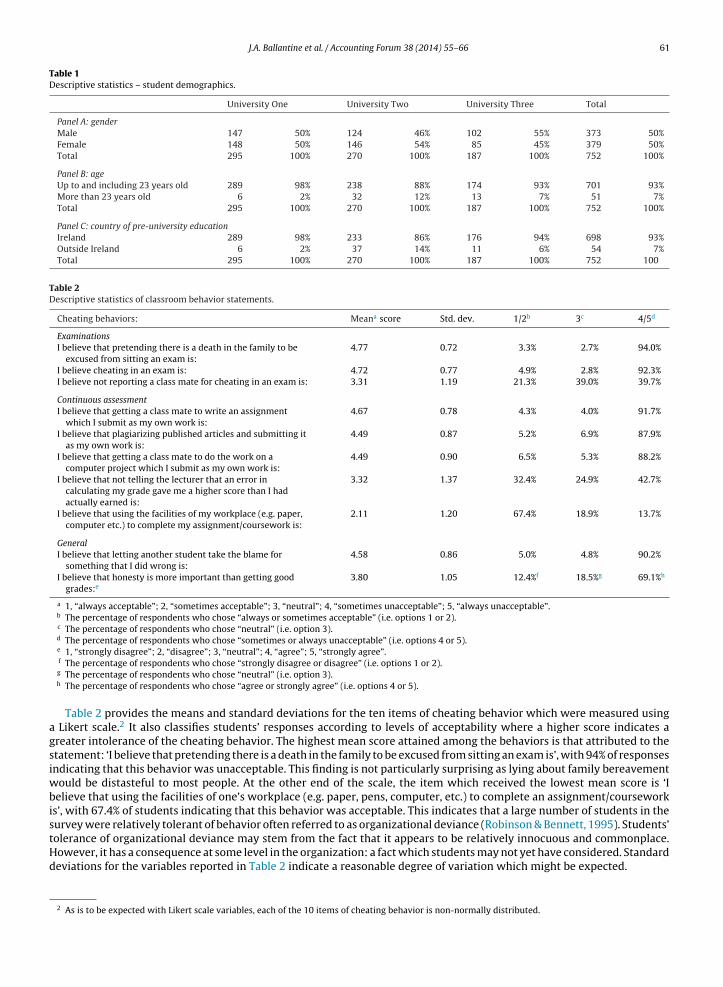

Table 1 presents statistical information pertaining to the respondents’ gender, age and the country in which they received

the bulk of their pre-university education. First, Panel A reveals that the total sample is split equally between male and femalerespondents. When this variable is further analyzed according to university, a similar gender balance exists. Secondly, PanelB provides the age profile of the sample, with the overwhelming majority of respondents, both by university and in total,falling into the age range 23 years and younger. Finally, Panel C reports the country in which the respondents received thebulk of their pre-university education with 93% being educated in Ireland and the remainder in China. In summary, theresults set out in Table 1, Panels B and C indicate a high level of homogeneity with respect to the variables contained therein.

J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66 61

Table 1Descriptive statistics – student demographics.

University One University Two University Three Total

Panel A: genderMale 147 50% 124 46% 102 55% 373 50%Female 148 50% 146 54% 85 45% 379 50%Total 295 100% 270 100% 187 100% 752 100%

Panel B: ageUp to and including 23 years old 289 98% 238 88% 174 93% 701 93%More than 23 years old 6 2% 32 12% 13 7% 51 7%Total 295 100% 270 100% 187 100% 752 100%

Panel C: country of pre-university educationIreland 289 98% 233 86% 176 94% 698 93%Outside Ireland 6 2% 37 14% 11 6% 54 7%Total 295 100% 270 100% 187 100% 752 100

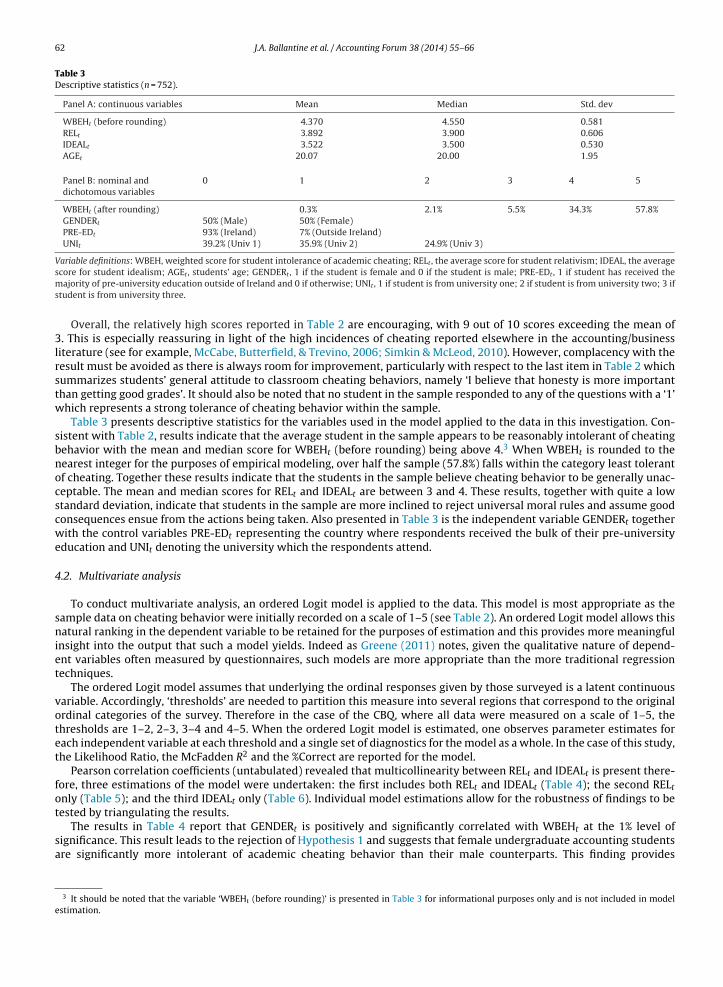

Table 2Descriptive statistics of classroom behavior statements.

Cheating behaviors: Meana score Std. dev. 1/2b 3c 4/5d

ExaminationsI believe that pretending there is a death in the family to be

excused from sitting an exam is:4.77 0.72 3.3% 2.7% 94.0%

I believe cheating in an exam is: 4.72 0.77 4.9% 2.8% 92.3%I believe not reporting a class mate for cheating in an exam is: 3.31 1.19 21.3% 39.0% 39.7%

Continuous assessmentI believe that getting a class mate to write an assignment

which I submit as my own work is:4.67 0.78 4.3% 4.0% 91.7%

I believe that plagiarizing published articles and submitting itas my own work is:

4.49 0.87 5.2% 6.9% 87.9%

I believe that getting a class mate to do the work on acomputer project which I submit as my own work is:

4.49 0.90 6.5% 5.3% 88.2%

I believe that not telling the lecturer that an error incalculating my grade gave me a higher score than I hadactually earned is:

3.32 1.37 32.4% 24.9% 42.7%

I believe that using the facilities of my workplace (e.g. paper,computer etc.) to complete my assignment/coursework is:

2.11 1.20 67.4% 18.9% 13.7%

GeneralI believe that letting another student take the blame for

something that I did wrong is:4.58 0.86 5.0% 4.8% 90.2%

I believe that honesty is more important than getting goodgrades:e

3.80 1.05 12.4%f 18.5%g 69.1%h

a 1, “always acceptable”; 2, “sometimes acceptable”; 3, “neutral”; 4, “sometimes unacceptable”; 5, “always unacceptable”.b The percentage of respondents who chose “always or sometimes acceptable” (i.e. options 1 or 2).c The percentage of respondents who chose “neutral” (i.e. option 3).d The percentage of respondents who chose “sometimes or always unacceptable” (i.e. options 4 or 5).e 1, “strongly disagree”; 2, “disagree”; 3, “neutral”; 4, “agree”; 5, “strongly agree”.

agsiwbistHd

f The percentage of respondents who chose “strongly disagree or disagree” (i.e. options 1 or 2).g The percentage of respondents who chose “neutral” (i.e. option 3).h The percentage of respondents who chose “agree or strongly agree” (i.e. options 4 or 5).

Table 2 provides the means and standard deviations for the ten items of cheating behavior which were measured using Likert scale.2 It also classifies students’ responses according to levels of acceptability where a higher score indicates areater intolerance of the cheating behavior. The highest mean score attained among the behaviors is that attributed to thetatement: ‘I believe that pretending there is a death in the family to be excused from sitting an exam is’, with 94% of responsesndicating that this behavior was unacceptable. This finding is not particularly surprising as lying about family bereavement

ould be distasteful to most people. At the other end of the scale, the item which received the lowest mean score is ‘Ielieve that using the facilities of one’s workplace (e.g. paper, pens, computer, etc.) to complete an assignment/coursework

s’, with 67.4% of students indicating that this behavior was acceptable. This indicates that a large number of students in theurvey were relatively tolerant of behavior often referred to as organizational deviance (Robinson & Bennett, 1995). Students’

olerance of organizational deviance may stem from the fact that it appears to be relatively innocuous and commonplace.owever, it has a consequence at some level in the organization: a fact which students may not yet have considered. Standardeviations for the variables reported in Table 2 indicate a reasonable degree of variation which might be expected.2 As is to be expected with Likert scale variables, each of the 10 items of cheating behavior is non-normally distributed.

62 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

Table 3Descriptive statistics (n = 752).

Panel A: continuous variables Mean Median Std. dev

WBEHt (before rounding) 4.370 4.550 0.581RELt 3.892 3.900 0.606IDEALt 3.522 3.500 0.530AGEt 20.07 20.00 1.95

Panel B: nominal anddichotomous variables

0 1 2 3 4 5

WBEHt (after rounding) 0.3% 2.1% 5.5% 34.3% 57.8%GENDERt 50% (Male) 50% (Female)PRE-EDt 93% (Ireland) 7% (Outside Ireland)UNIt 39.2% (Univ 1) 35.9% (Univ 2) 24.9% (Univ 3)

Variable definitions: WBEH, weighted score for student intolerance of academic cheating; RELt , the average score for student relativism; IDEAL, the average

score for student idealism; AGEt , students’ age; GENDERt , 1 if the student is female and 0 if the student is male; PRE-EDt , 1 if student has received themajority of pre-university education outside of Ireland and 0 if otherwise; UNIt , 1 if student is from university one; 2 if student is from university two; 3 ifstudent is from university three.Overall, the relatively high scores reported in Table 2 are encouraging, with 9 out of 10 scores exceeding the mean of3. This is especially reassuring in light of the high incidences of cheating reported elsewhere in the accounting/businessliterature (see for example, McCabe, Butterfield, & Trevino, 2006; Simkin & McLeod, 2010). However, complacency with theresult must be avoided as there is always room for improvement, particularly with respect to the last item in Table 2 whichsummarizes students’ general attitude to classroom cheating behaviors, namely ‘I believe that honesty is more importantthan getting good grades’. It should also be noted that no student in the sample responded to any of the questions with a ‘1’which represents a strong tolerance of cheating behavior within the sample.

Table 3 presents descriptive statistics for the variables used in the model applied to the data in this investigation. Con-sistent with Table 2, results indicate that the average student in the sample appears to be reasonably intolerant of cheatingbehavior with the mean and median score for WBEHt (before rounding) being above 4.3 When WBEHt is rounded to thenearest integer for the purposes of empirical modeling, over half the sample (57.8%) falls within the category least tolerantof cheating. Together these results indicate that the students in the sample believe cheating behavior to be generally unac-ceptable. The mean and median scores for RELt and IDEALt are between 3 and 4. These results, together with quite a lowstandard deviation, indicate that students in the sample are more inclined to reject universal moral rules and assume goodconsequences ensue from the actions being taken. Also presented in Table 3 is the independent variable GENDERt togetherwith the control variables PRE-EDt representing the country where respondents received the bulk of their pre-universityeducation and UNIt denoting the university which the respondents attend.

4.2. Multivariate analysis

To conduct multivariate analysis, an ordered Logit model is applied to the data. This model is most appropriate as thesample data on cheating behavior were initially recorded on a scale of 1–5 (see Table 2). An ordered Logit model allows thisnatural ranking in the dependent variable to be retained for the purposes of estimation and this provides more meaningfulinsight into the output that such a model yields. Indeed as Greene (2011) notes, given the qualitative nature of depend-ent variables often measured by questionnaires, such models are more appropriate than the more traditional regressiontechniques.

The ordered Logit model assumes that underlying the ordinal responses given by those surveyed is a latent continuousvariable. Accordingly, ‘thresholds’ are needed to partition this measure into several regions that correspond to the originalordinal categories of the survey. Therefore in the case of the CBQ, where all data were measured on a scale of 1–5, thethresholds are 1–2, 2–3, 3–4 and 4–5. When the ordered Logit model is estimated, one observes parameter estimates foreach independent variable at each threshold and a single set of diagnostics for the model as a whole. In the case of this study,the Likelihood Ratio, the McFadden R2 and the %Correct are reported for the model.

Pearson correlation coefficients (untabulated) revealed that multicollinearity between RELt and IDEALt is present there-fore, three estimations of the model were undertaken: the first includes both RELt and IDEALt (Table 4); the second RELt

only (Table 5); and the third IDEALt only (Table 6). Individual model estimations allow for the robustness of findings to betested by triangulating the results.

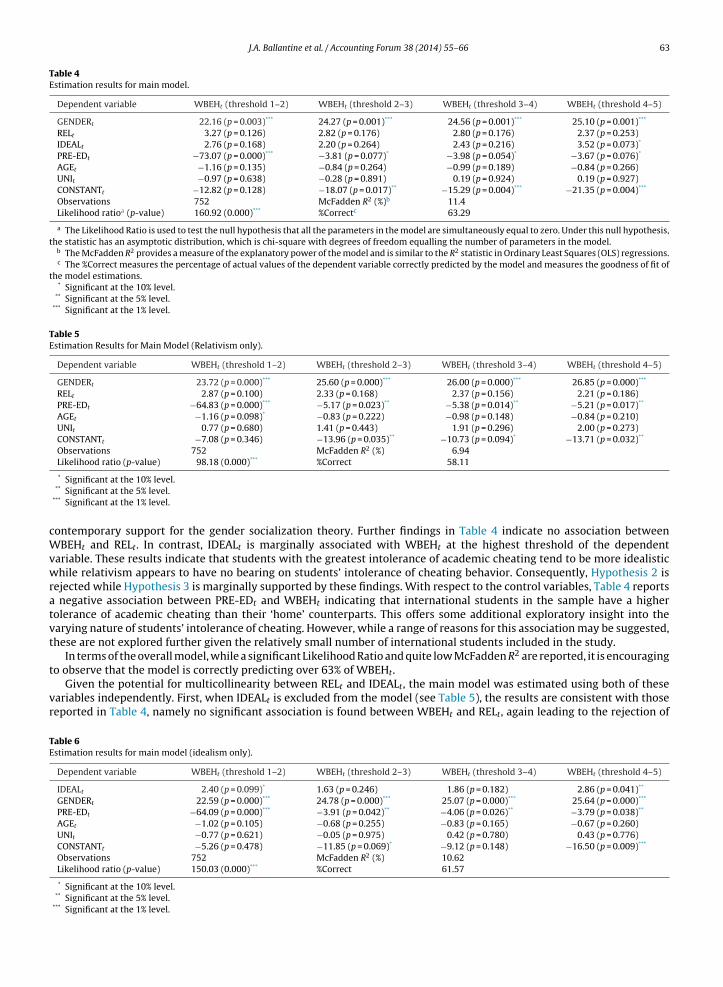

The results in Table 4 report that GENDERt is positively and significantly correlated with WBEHt at the 1% level ofsignificance. This result leads to the rejection of Hypothesis 1 and suggests that female undergraduate accounting studentsare significantly more intolerant of academic cheating behavior than their male counterparts. This finding provides

3 It should be noted that the variable ‘WBEHt (before rounding)’ is presented in Table 3 for informational purposes only and is not included in modelestimation.

J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66 63

Table 4Estimation results for main model.

Dependent variable WBEHt (threshold 1–2) WBEHt (threshold 2–3) WBEHt (threshold 3–4) WBEHt (threshold 4–5)

GENDERt 22.16 (p = 0.003)*** 24.27 (p = 0.001)*** 24.56 (p = 0.001)*** 25.10 (p = 0.001)***

RELt 3.27 (p = 0.126) 2.82 (p = 0.176) 2.80 (p = 0.176) 2.37 (p = 0.253)IDEALt 2.76 (p = 0.168) 2.20 (p = 0.264) 2.43 (p = 0.216) 3.52 (p = 0.073)*

PRE-EDt −73.07 (p = 0.000)*** −3.81 (p = 0.077)* −3.98 (p = 0.054)* −3.67 (p = 0.076)*

AGEt −1.16 (p = 0.135) −0.84 (p = 0.264) −0.99 (p = 0.189) −0.84 (p = 0.266)UNIt −0.97 (p = 0.638) −0.28 (p = 0.891) 0.19 (p = 0.924) 0.19 (p = 0.927)CONSTANTt −12.82 (p = 0.128) −18.07 (p = 0.017)** −15.29 (p = 0.004)*** −21.35 (p = 0.004)***

Observations 752 McFadden R2 (%)b 11.4Likelihood ratioa (p-value) 160.92 (0.000)*** %Correctc 63.29

a The Likelihood Ratio is used to test the null hypothesis that all the parameters in the model are simultaneously equal to zero. Under this null hypothesis,the statistic has an asymptotic distribution, which is chi-square with degrees of freedom equalling the number of parameters in the model.

b The McFadden R2 provides a measure of the explanatory power of the model and is similar to the R2 statistic in Ordinary Least Squares (OLS) regressions.c The %Correct measures the percentage of actual values of the dependent variable correctly predicted by the model and measures the goodness of fit of

the model estimations.* Significant at the 10% level.

** Significant at the 5% level.*** Significant at the 1% level.

Table 5Estimation Results for Main Model (Relativism only).

Dependent variable WBEHt (threshold 1–2) WBEHt (threshold 2–3) WBEHt (threshold 3–4) WBEHt (threshold 4–5)

GENDERt 23.72 (p = 0.000)*** 25.60 (p = 0.000)*** 26.00 (p = 0.000)*** 26.85 (p = 0.000)***

RELt 2.87 (p = 0.100) 2.33 (p = 0.168) 2.37 (p = 0.156) 2.21 (p = 0.186)PRE-EDt −64.83 (p = 0.000)*** −5.17 (p = 0.023)** −5.38 (p = 0.014)** −5.21 (p = 0.017)**

AGEt −1.16 (p = 0.098)* −0.83 (p = 0.222) −0.98 (p = 0.148) −0.84 (p = 0.210)UNIt 0.77 (p = 0.680) 1.41 (p = 0.443) 1.91 (p = 0.296) 2.00 (p = 0.273)CONSTANTt −7.08 (p = 0.346) −13.96 (p = 0.035)** −10.73 (p = 0.094)* −13.71 (p = 0.032)**

Observations 752 McFadden R2 (%) 6.94Likelihood ratio (p-value) 98.18 (0.000)*** %Correct 58.11

cWvwratvt

t

vr

TE

* Significant at the 10% level.** Significant at the 5% level.

*** Significant at the 1% level.

ontemporary support for the gender socialization theory. Further findings in Table 4 indicate no association betweenBEHt and RELt. In contrast, IDEALt is marginally associated with WBEHt at the highest threshold of the dependent

ariable. These results indicate that students with the greatest intolerance of academic cheating tend to be more idealistichile relativism appears to have no bearing on students’ intolerance of cheating behavior. Consequently, Hypothesis 2 is

ejected while Hypothesis 3 is marginally supported by these findings. With respect to the control variables, Table 4 reports negative association between PRE-EDt and WBEHt indicating that international students in the sample have a higherolerance of academic cheating than their ‘home’ counterparts. This offers some additional exploratory insight into thearying nature of students’ intolerance of cheating. However, while a range of reasons for this association may be suggested,hese are not explored further given the relatively small number of international students included in the study.

In terms of the overall model, while a significant Likelihood Ratio and quite low McFadden R2 are reported, it is encouraging

o observe that the model is correctly predicting over 63% of WBEHt.Given the potential for multicollinearity between RELt and IDEALt, the main model was estimated using both of theseariables independently. First, when IDEALt is excluded from the model (see Table 5), the results are consistent with thoseeported in Table 4, namely no significant association is found between WBEHt and RELt, again leading to the rejection of

able 6stimation results for main model (idealism only).

Dependent variable WBEHt (threshold 1–2) WBEHt (threshold 2–3) WBEHt (threshold 3–4) WBEHt (threshold 4–5)

IDEALt 2.40 (p = 0.099)* 1.63 (p = 0.246) 1.86 (p = 0.182) 2.86 (p = 0.041)**

GENDERt 22.59 (p = 0.000)*** 24.78 (p = 0.000)*** 25.07 (p = 0.000)*** 25.64 (p = 0.000)***

PRE-EDt −64.09 (p = 0.000)*** −3.91 (p = 0.042)** −4.06 (p = 0.026)** −3.79 (p = 0.038)**

AGEt −1.02 (p = 0.105) −0.68 (p = 0.255) −0.83 (p = 0.165) −0.67 (p = 0.260)UNIt −0.77 (p = 0.621) −0.05 (p = 0.975) 0.42 (p = 0.780) 0.43 (p = 0.776)CONSTANTt −5.26 (p = 0.478) −11.85 (p = 0.069)* −9.12 (p = 0.148) −16.50 (p = 0.009)***

Observations 752 McFadden R2 (%) 10.62Likelihood ratio (p-value) 150.03 (0.000)*** %Correct 61.57

* Significant at the 10% level.** Significant at the 5% level.

*** Significant at the 1% level.

64 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

Hypothesis 2. Secondly, when RELt is excluded from the model (see Table 6), IDEALt is found to be significantly associated (at5%) with WBEHt at the highest threshold. This confirms and strengthens the findings in Table 4 with respect to IDEALt andleads to the acceptance of Hypothesis 3. Finally, with respect to GENDERt, the findings reported in Tables 5 and 6 provideadditional support for those of Table 4, namely that a consistently positive and significant association is found betweenGENDERt and WBEHt. As a consequence, Hypothesis 1 is rejected.

The McFadden R2 and the %Correct reported in Tables 5 and 6 confirm that idealism is a better explanator of cheatingintolerance than relativism. Indeed, the results of these two statistics with respect to idealism compare favorably with thosereported for the main model (Table 4).

4.3. Robustness tests

To assess the robustness of findings, additional tests were conducted. Clearly the value of the dependent variable, WBEHt,is determined by the weightings applied to the ten cheating behaviors which comprise the CBQ. Consequently the authorsapplied a suite of alternative weightings, ranging from a simple mean across all CBQ questions to a weighting which reflectedthe number of questions in the CBQ pertaining to examinations, continuous assessment and other aspects of academicdishonesty. Findings from this untabulated analysis were consistent with those reported above.

A second sensitivity test which re-estimated the research model excluding each control variable was carried out tocorroborate the main results reported in Tables 4–6. While there are numerous iterations of the model when conductingsuch further tests, results from these untabulated results support all of the main findings reported in Tables 4–6, namelythat gender and idealism are positively and significantly correlated with the dependent measure of cheating behavior.

Finally, as an additional means of corroborating the findings with respect to both relativism and idealism, alternativemeasures were developed and applied in the model estimations. Since multicollinearity between relativism and idealism ispresent, purer measures of both sub-scales can be derived by regressing each measure on the other. The residuals of suchestimations may be seen as ‘pure’ measures of relativism and idealism, and are more formally stated as:

RELt = ˛0 + ˛1DEALt + εt [εt = pure relativsm (PURERELt)]

IDEALt = ˛0 + ˛1RELt + εt [εt = pure idealism (PUREDEALt)]

Both PURERELt and PUREIDEALt were replaced in model estimations. Untabulated results from this analysis yield thesame results as those reported above, thus providing further support for the findings with respect to relativism and idealismas reported in Tables 4–6.

5. Discussion and conclusions

The current study reports that Irish accounting undergraduate students, the majority of whom proceed to a career inaccountancy, are fairly intolerant of academic cheating behavior. This finding is encouraging from two perspectives. First,it augurs well for the students’ immediate academic careers. Despite the fact that a recession-hit world has created greatercareer uncertainty for students, cheating does not appear to be an acceptable way of achieving academic success. Secondly,when one considers the premise that the academic integrity and honesty demonstrated at undergraduate level is a strongpredictor of workplace ethical behavior, these findings provide a degree of reassurance regarding the future moral directionof the Irish accountancy profession. Bearing in mind that many of these accounting graduates progress to become the Irishaccountancy professionals of the future4, the basic assertion which emanates from these findings is that the continuationof these attitudes through to the workplace may make a positive contribution to restoring public confidence to an Irishbusiness world which has been seriously undermined by recent financial scandals.

In an effort to establish why some individuals are more intolerant of cheating behavior than others, the study consideredthree possible determinants, namely gender, relativism and idealism. First, gender was found to be significantly associatedwith undergraduate accounting students’ intolerance of cheating behavior with females having a more ethical attitude toclassroom cheating than their male counterparts. While Pierce and Sweeney (2010) also reported a stricter position amongIrish female accountancy trainees with respect to ethical judgment, their findings were less conclusive in that significancewas reported in only one of the four scenarios tested. Therefore the findings of the current study with respect to genderethics not only corroborate but also strengthen those reported by Pierce and Sweeney (2010). Given the relatively equalrepresentation of males and females in Irish accounting programs where women share so many educational and training

experiences with their male counterparts, one may have expected some degree of equalization in the ethical judgment ofboth sexes. However, this was not found to be the case. Instead, the current study confirms that gender differences in ethicalattitude still appear to be relevant. To this end, given the increasing female representation in the profession, the conclusionto be drawn from these findings echoes that of Ameen et al. (1996), published some time ago, that ‘the influx of female4 The vast majority of students who study accounting at university level go on to become Irish chartered accountants. For example, 84% of entrants toChartered Accountants Ireland in 2012 held a relevant accounting degree (Irish Auditing and Accounting Supervisory Authority, 2012, p. 22).

actr

bsescfmssaaptfwe2tiipaTt

lsfwhebsWtsd

R

AA

A

BB

BBBCC

C

DFFF

J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66 65

ccountants could have a positive effect on the business community’ (Ameen et al., 1996, p. 596). More specifically, in theontext of the current study, the findings with respect to gender may go some way to providing a positive influence onhe ethical judgment of future accountants and enable Chartered Accountants Ireland to achieve its strategic objective ofebuilding trust in the Irish accountancy profession.

This multi-campus study also considered the impact of idealism and relativism on intolerance of academic cheatingehavior. The findings with respect to these two variables were in marked contrast to one another. Idealism was found to beignificantly associated with greater levels of intolerance of academic cheating behavior among accounting students. How-ver, no significant association between relativism and intolerance of academic cheating was found at any level. This woulduggest that, in the context of academic cheating, being an idealist is more desirable than being a relativist. These findingsonfirm those reported by Sierra and Hyman (2008) who suggested that idealism among students is to be encouraged andostered as a bulwark to cheating behavior in the classroom. To this end, they recommended that “instructors should try to

inimize ethical relativism among students” (p. 62) and promote idealism. The expectation is that this focus on idealismhould, in turn, reduce the likelihood of unethical behavior in the workplace. Indeed, prior research has reported that it is pos-ible to influence an individual’s personal moral philosophy. For example, Coyne, Massey and Thibodeau (2005) and Masseynd Van Hise (2009) found that, following an educational intervention, business studies and accounting students exhibited

reduction in relativism and an increase in idealism scores. The expectation is that, if individuals comprehend their ethicalhilosophy more fully prior to leaving higher education, they will be better equipped to contend with the ethical decisionshey may encounter throughout their careers (Caldwell, Karri, & Matula, 2005). With appropriate direction and guidancerom educators, students could be presented with ethical dilemmas and be introduced to alternative ethical perspectiveshich stimulate discussion and promote reflection on each other’s moral position. While it is accepted that no amount of

thics education will ever change the ethical attitude of the most ‘egregious violators’ (Adams, Tashchian, & Shore, 1999, p.43), nevertheless, making students aware of alternative ethical perspectives should, at some level, encourage some of themo take the moral consequences of their actions into account in ways they previously would not have considered. By so doing,t is anticipated that undergraduate students will be provided with a more rounded moral perspective which encouragesdealism and thereby serves them well in their working lives. The business world is ill-served by recruiting graduates whoossess a set of dubious moral values. As gatekeepers of a respected profession (Saunders, 1993), accounting academics have

role to play in shaping the ethical ideology of those entering the workforce by providing some measure of moral direction.his direction, combined with the increased focus on the importance of ethical standards within professional accountancyraining should hopefully go some way to restoring faith in the tarnished reputation of the accountancy profession in Ireland.

The findings of this study should be interpreted in the light of the following limitations. First, attitudinal data were col-ected using questionnaires completed by undergraduate students in a classroom environment. However, what individualsay and what they do may not be one and the same. Whilst attitudinal data serves as a reasonable proxy for actual behavior,urther research in this area might consider the use of experimental methodologies which aim to bridge the gap betweenhat students say they do and what they actually do. For example, Roig (1997) and Rettinger, Jordan, and Peschiera (2004)ave reported on the use of scenarios and experimental vignette methods when exploring one aspect of academic dishon-sty, namely plagiarism. Additionally, more recently educational technology has been employed to directly observe cheatingehaviors in the case of plagiarized materials (see for example, Keck, 2006; Ledwith & Risquez, 2008). Secondly, the presenttudy has not considered other possible determinants of cheating behavior including, for example religiosity and culture.

ith respect to religiosity, it was not possible to consider the impact of this variable due to the restrictions imposed by thehree ethics committees who regarded this information to be sensitive. Further, due to the small number of internationaltudents in the sample, the impact of culture could not be adequately explored. Future research might investigate theseeterminants and others in the context of classroom cheating behaviors and the implications for workplace ethics.

eferences

dams, J., Tashchian, A., & Shore, T. H. (1999). Frequency, recall and usefulness of undergraduate ethics education. Teaching Business Ethics, 3(3), 241–253.llmon, D. E., Page, D., & Robert, R. (2000). Determinants of perceptions of cheating: Ethical orientation, personality and demographics. Journal of Business

Ethics, 23(4), 411–422.meen, E., Guffey, D. M., & McMillan, J. J. (1996). Gender differences in determining the ethical sensitivity of future accounting professionals. Journal of

Business Ethics, 15(5), 591–597.arnett, T., Bass, K., & Brown, G. (1994). Ethical ideology and ethical judgment regarding ethical issues in business. Journal of Business Ethics, 13(6), 469–480.arnett, T., Bass, K., & Brown, G. (1996). Religiosity, ethical ideology, and intentions to report a peer’s wrongdoing. Journal of Business Ethics, 15(11),

1161–1171.etz, M., O’Connell, L., & Shepard, J. M. (1989). Gender differences in proclivity for unethical behavior. Journal of Business Ethics, 8(5), 321–324.eu, D., Buckley, S. M. R., & Harvey, M. G. (2003). Ethical decision-making: A multidimensional construct. Business Ethics: A European Review, 12(1), 88–107.owers, W. (1964). Student dishonesty and its control in college. New York: Columbia University, Bureau of Applied Social Research.aldwell, C., Karri, R., & Matula, T. (2005). Practicing what we teach – Ethical considerations for business schools. Journal of Academic Ethics, 3(1), 1–25.han, S. Y. S., & Leung, P. (2006). The effects of accounting students’ ethical reasoning and personal factors on their ethical sensitivity. Managerial Auditing

Journal, 21(4), 436–475.oyne, M., Massey, D., & Thibodeau, J. (2005). Raising students’ ethical sensitivity with a value relevance approach. In B. N. Schwartz, & J. E. Ketz (Eds.),

Advances in accounting education: Teaching and curriculum innovations (Vol. 7) (pp. 171–205). San Diego, US: Elsevier.

avis, J. R., & Welton, R. E. (1991). Professional ethics: Business students’ perceptions. Journal of Business Ethics, 10(6), 451–463.errell, O. C., & Weaver, K. M. (1978). Ethical beliefs of marketing managers. Journal of Marketing, 42(July), 69L 73.inancial Reporting Council. (2013). Key facts and trends in the accountancy profession. London: Financial Reporting Council.lood, B., & Wilson, R. M. S. (2008). An exploration of learning approaches of prospective professional accountants in Ireland. Accounting Forum, 32(3),225–239.

66 J.A. Ballantine et al. / Accounting Forum 38 (2014) 55– 66

Forrest, P., & Pritchett, T. K. (1990). Business students’ perceptions of ethics in the classroom. Journal of Midwest Marketing, 5(Spring), 117–124.Forsyth, D. R. (1980). A taxonomy of ethical ideologies. Journal of Personality and Social Psychology, 39(1), 175–184.Forsyth, D. R. (1992). Judging the morality of business practices: The influence of personal moral philosophies. Journal of Business Ethics, 11(5–6), 461–470.Forsyth, D. R., & Berger, R. E. (1982). The effects of ethical ideology on moral behavior. Journal of Social Psychology, 117(1), 53–56.Franklyn-Stokes, A., & Newstead, S. E. (1995). Undergraduate cheating: Who does what and why? Studies in Higher Education, 20(2), 159–172.Gilligan, C. (1982). In a different voice. Cambridge, MA: Harvard University Press.Granitz, N., & Loewy, D. (2007). Applying ethical theories: Interpreting and responding to student plagiarism. Journal of Business Ethics, 72(3), 293–306.Greene, W. H. (2011). Econometric analysis (7th ed.). New York: Pearson Prentice Hall.Irish Auditing and Accounting Supervisory Authority (IAASA). (2012). Údarás Maoirseachta Iniúchta agus Cuntasaíochta na hÉireann. Profile of the Profession,

Kildare, Ireland: IAASA.Jones, R. C., Hamilton, K. L., & Ingram, R. (2007). Students’ perception of ethical classroom behaviour: A closer look. Journal of Business, Industry and Economics,

8(1), 39–55.Keck, C. (2006). The use of paraphrase in summary writing: A comparison of L1 and L2 writers. Journal of Second Language Writing, 15(4), 261–278.Kidwell, L. A., & Kent, J. (2008). Integrity at a distance: A study of academic misconduct among university students on and off campus. Accounting Education:

An International Journal, 17(Supplement S3–S16), 3L 16.Ledwith, A., & Risquez, A. (2008). Using anti-plagiarism software to promote academic honesty in the context of peer reviewed assignments. Studies in

Higher Education, 33(4), 371–384.Massey, D., & Van Hise, J. (2009). Walking the walk: Integrating lessons from multiple perspectives in the development of an accounting ethics capstone.

Issues in Accounting Education, 24(4), 481–510.McCabe, D. L., & Bowers, W. J. (1994). Academic dishonesty among males in college: A thirty year perspective. Journal of College Student Development, 35(1),

5–10.McCabe, D. L., & Trevino, L. K. (1993). Academic dishonesty: Honor codes and other contextual influences. Journal of Higher Education, 64(5), 522–538.McCabe, A. C., Ingram, R., & Dato-on, M. C. (2006). The business of ethics and gender. Journal of Business Ethics, 64(2), 101–116.McCabe, D. L., Butterfield, K. D., & Trevino, L. K. (2006). Academic dishonesty in graduate business programs: Prevalence, causes, and proposed action.

Academy of Management Learning and Education, 5(3), 294–305.Newstead, S. E., Franklyn-Stokes, A., & Armstead, P. (1996). Individual differences in student cheating. Journal of Educational Psychology, 88(2), 229–241.Nonis, S., & Swift, C. O. (2001). An examination of the relationship between academic dishonesty and workplace dishonesty: A multicampus investigation.

Journal of Education for Business, 77(2), 69–77.Norton, L. S., Tilley, A. J., Newstead, S. E., & Franklyn-Stokes, A. (2001). The pressures of assessment in undergraduate courses and their effect on student

behaviours. Assessment and Evaluation in Higher Education, 26(3), 269–284.O’Carroll, L. (2010). Former Irish Nationwide boss Michael Fingleton still hasn’t paid bonus back, The Guardian. http://www.guardian.co.uk/business/

ireland-business-blog-with-lisa-ocarroll/2010/dec/23/irish-nationwide-michael-fingleton-bonusPierce, B., & Sweeney, B. (2010). The relationship between demographic variable and ethical decision making of trainee accountants. International Journal

of Auditing, 14(1), 79–99.Pratt, C., & McLaughlin, G. (1989). An analysis of predictors of students’ ethical inclinations. Research in Higher Education, 30(2), 195–219.Radtke, R. R. (2000). The effects of gender and setting on accountants’ ethically sensitive decisions. Journal of Business Ethics, 24(4), 299–312.Rettinger, D. A., Jordan, A. E., & Peschiera, F. (2004). Evaluating the motivation of other students to cheat: A vignette experiment. Research in Higher Education,

45(8), 873–890.Risquez, A., O’Dwyer, M., & Ledwith, A. (2011). Technology enhanced learning and plagiarism in entrepreneurship education. Education and Training, 53(8),

750–761.Robinson, S. L., & Bennett, R. J. (1995). A typology of deviant workplace behaviors: A multidimensional scaling study. Academy of Management Journal, 38(2),

555–572.Roig, M. (1997). Can undergraduate students determine whether text has been plagiarized? Psychological Record, 47(1), 113–123.Ryan, C. (2011). The euro crisis and crisis management: Big lessons from a small island. International Economics and Economic, Policy, 8(1), 31–43.Saunders, E. J. (1993). Confronting academic dishonesty. Journal of Social Work Education, 29(2), 224–230.Schlenker, B. R., & Forsyth, D. R. (1977). On the ethics of psychological research. Journal of Experimental Social Psychology, 13, 369–396.Sierra, J. J., & Hyman, M. R. (2008). Ethical antecedents of cheating intentions: Evidence of mediation. Journal of Academic Ethics, 6(1), 51–66.Sikula, A., Sr., & Costa, A. D. (1994). Are women more ethical than men? Journal of Business Ethics, 13(11), 859–871.

Simkin, M., & McLeod, A. (2010). Why do college students cheat? Journal of Business Ethics, 94(3), 441–453.Stanga, K. G., & Turpen, R. A. (1991). Ethical judgements on selected accounting issues: An empirical study. Journal of Business Ethics, 10(10), 739–747.Steiner, G. A., & Steiner, J. F. (2011). Business, government and society: A managerial perspective. New York, NY: McGraw-Hill.Terpstra, D. E., Rozelle, E. J., & Robinson, R. K. (1993). The influence of personality and demographic variables on ethical decisions related to insider trading.The Journal of Psychology: Interdisciplinary and Applied, 127(4), 375–389.