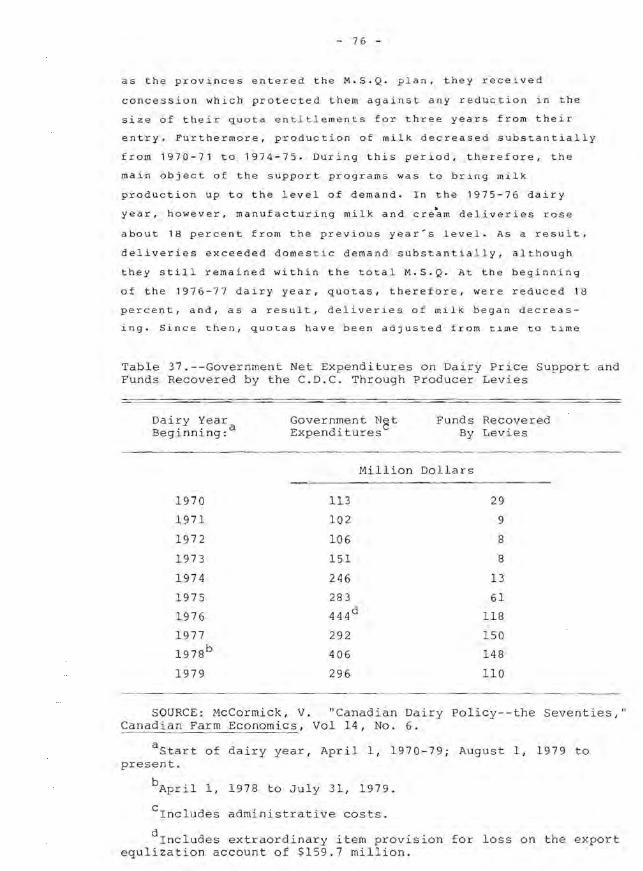

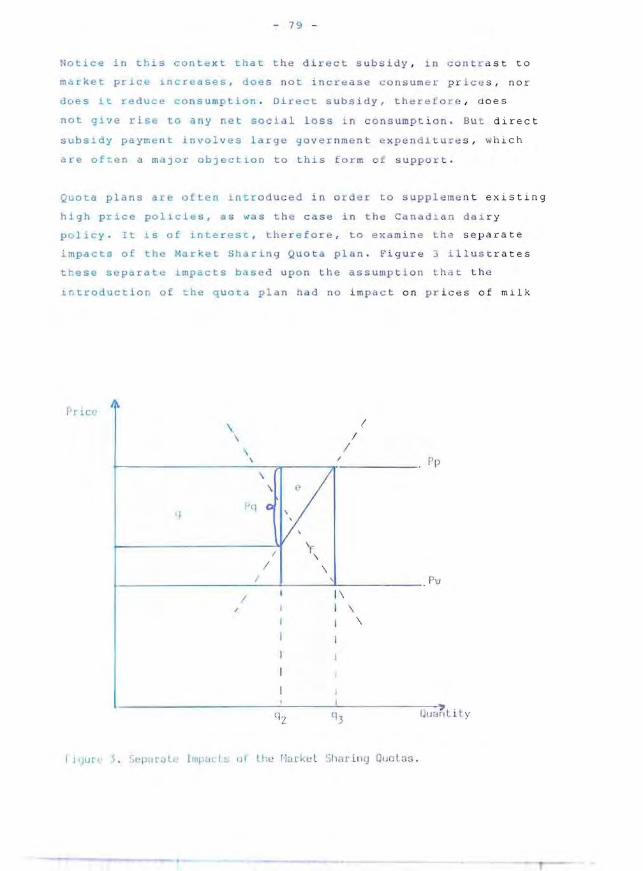

dairy price policies in north america - results and ... · dairy price policies in north america -...

TRANSCRIPT

Jordbrugs!3konomi kIn, titut

Dairy Price Policies in North America

Rapport or. 10

- Results and Experiences

J OJ'( I bru ~s(1k ( lIlOI1l isk I nsl i II I r

Ra Pilon Ill , I ()

Dairy Price Policies

in North America

- Results and Experiences

(l1lvd cLlI1!\k sammendrag)

/111/\ l1t1l1S1' 11

I korlllll is, illil !ins LI I H I IILI Sh() ldI1I1 1gS"cl~bhc lS F()]-i;lg I \~)ill'nlla\ I I I q:-{:!

JORDBRUGS¢KONOMISK INSTITUT

Valby Langgade 19

2500 Valby

TLF. (01) 304522

ISSN 0107 - 5357

FO RORD

De fo r tSat store o mkostn ~ nger i Eorbi ndels e me d overskudde t

aE rne j erip r odukter i EF er n l ed ni n ge n t il de t t e studie af

m ange'r~gE reg u leringer og ~nd g re b i me j e r i pr oduktsektoren i

USA og Canada. Kendskab til e r fa ringe rne i ra Nord a merika er

u tviv l somt ny~t i gt i _orb i ndelse me d ~n d ringe r l EF ' s politlk

for me)eriprodukter .

Publlkatio n en er u d arbej d et i fo r b in d e l s e me d f o r fatter e ns

stud~eophold l USA , hvo r f o r den publice r es pi e n g e lsk. Der

er dog aT omiactende uansk samm en d rag .

Jordbrugs~konom~s~ In~tit u t . j ul i 1~ 8 2

Ar n e Larsen

ACKNOWLEDGMENTS

I would like to thank the Department of Agricultural Econo

mics at Michigan State University for giving me the opportu

nity to study at the department from September 1980 to Dec

ember 1981. Particular thanks to Professor Vernon L. Soren

son, MSU, for his assiitance in the planning of my study and

for his suggestions in prepering this report.

I would also like to thank The Danish Agricultural and Vete

rinary Research Council as well as NATO Science Fellowship

Programme for providing the necessary financial support.

Thanks also to Dr. Arne Larsen, Director, Institute of Agri

cultural Economics, for encouragements and assistance during

the preparation of my study in the U.S.

Institute of Agricultural Economics, July 1982

Jens Hansen

CONTENT S

1. Introduclion 7

PII.RT I. DAIRY FARMING AND DAIRY PR ODUCT CONSU MPTION IN THE

3.

UN ITED STATES AND CANADA .•.•..• . ....... 0........ 11

Patt~rns and Trends in Dairy Farmin g ... .........•. 0 •• 12

2. 1. Structure or dairy f arming ........ ........... 0.. 12

LocatLon of dairy far ming

Trends Ln mLlk product i on

20

23

2.4. PaCt.erns of product io n and r",sou r ce use .......• 23

2.5 . Technology and Product i v i ty ... .................. 31

2.G. Trends in prLces of milk and in prices of

r.,sourc .. s 34

Pat terns and Trends in Da i r y Produc t Consumption 37

PART II. DAIRY PRICE POLICIES I N THE U ITED STATES AND

IL

4.

5.

B .

6 .

CANADA ....•...•. .......•........... ..........

UNITED STATES

PricE Support of Manufacturing Mi lk

4 . 1 . Obj""c iVE<s . pri c ing , and oper ti o n

43

43

44

44

4 . 2 . Impacts .•. . .......•..........•.... • ....•...•.• 0. 49

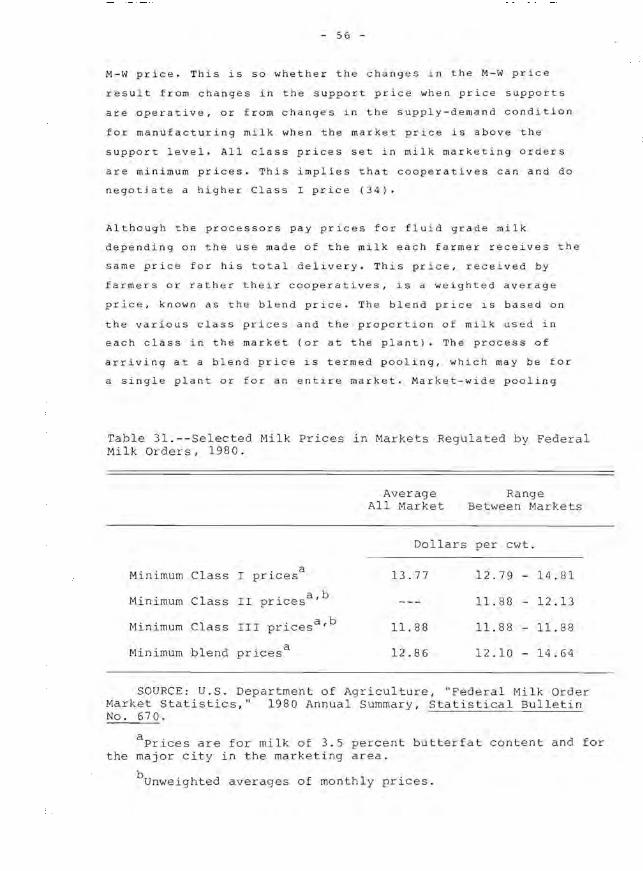

~larketing urders for F luid Mil k •..•••.•••••••••• ....

5. , .

5.2.

Object i ves , p r Lc~ng , and ope rati o n ••... ........

Lmpac ts .. . ... . ..•...... . ..•..•.••.•.• • •• • 0 •••

CANADA

Manuta.Cl.ur~n'l Mi lk Market •.•••••• . • • ••. .•• • • .. •• ..• >.

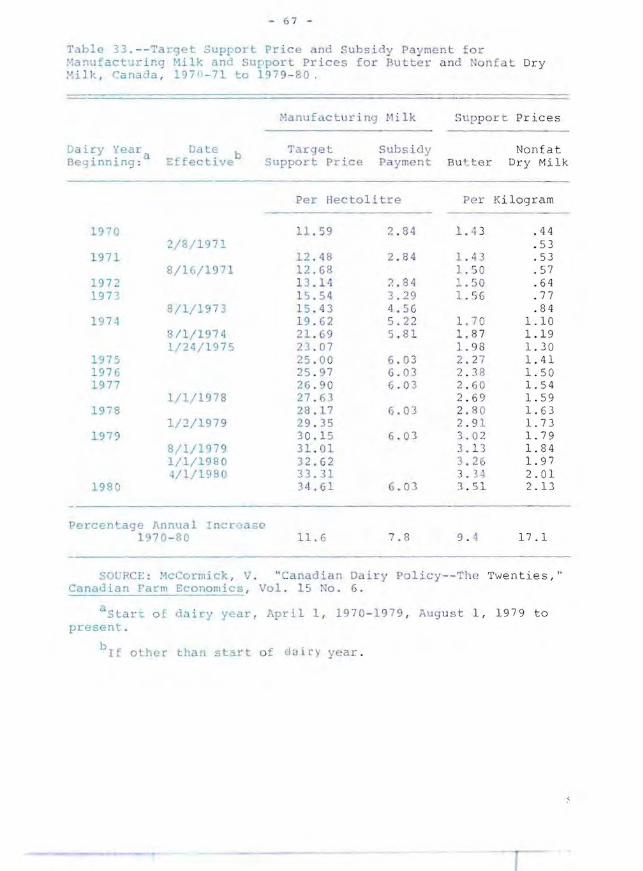

6. 1. Market vr~c~ support nd direct su b sidy payments.

6.2 . Subs~dy El~gLb~lity Quotas ... • . •• .. .....• .. •••.•

54

54

57

63

64

64

70

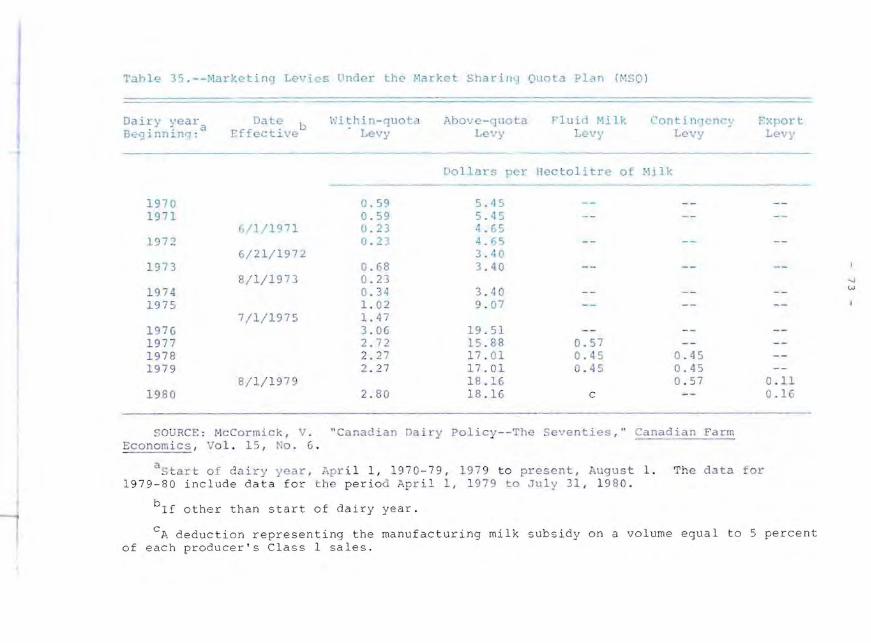

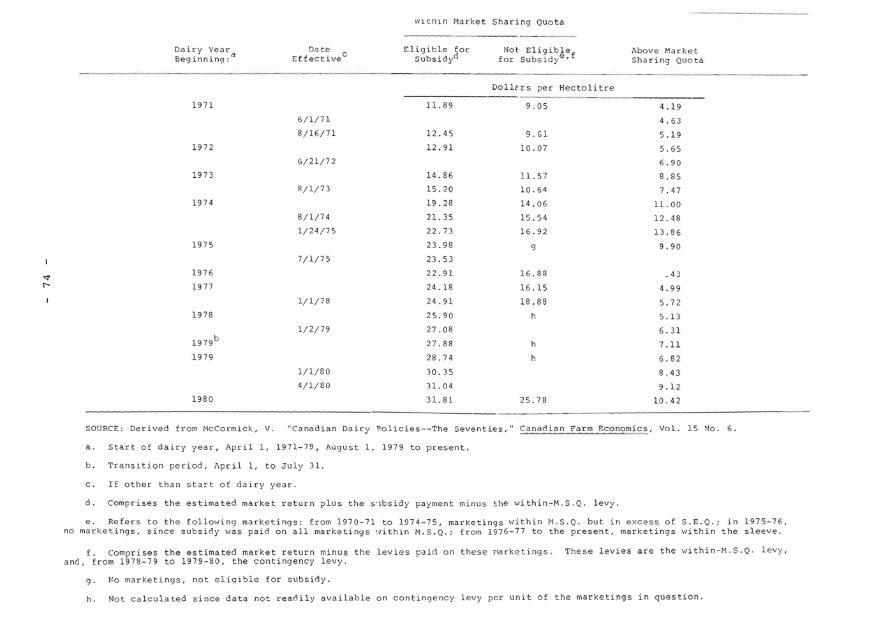

6.3. Market Sharing Quotas ..............•...........• 71

6.4. Policy impacts ... • .••..................•........ 77

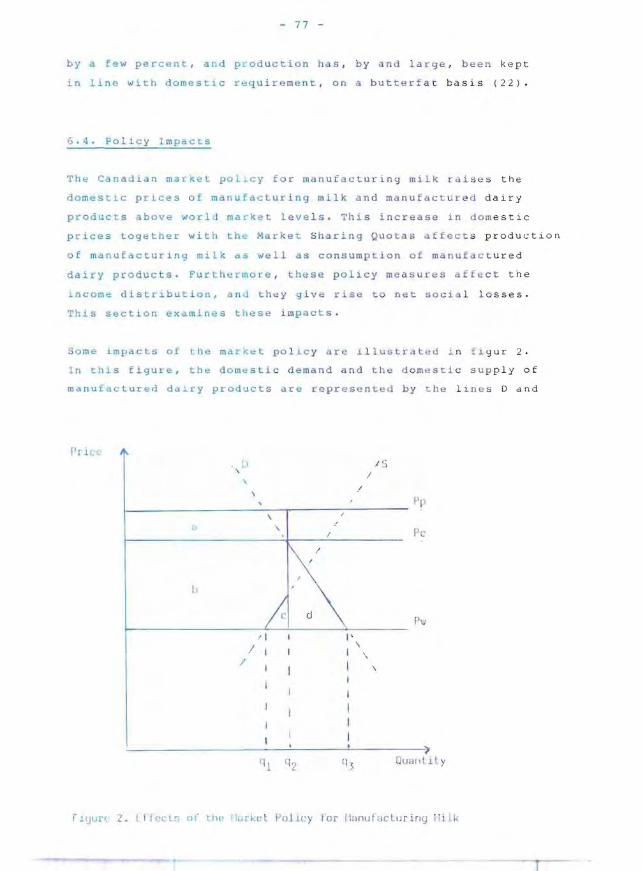

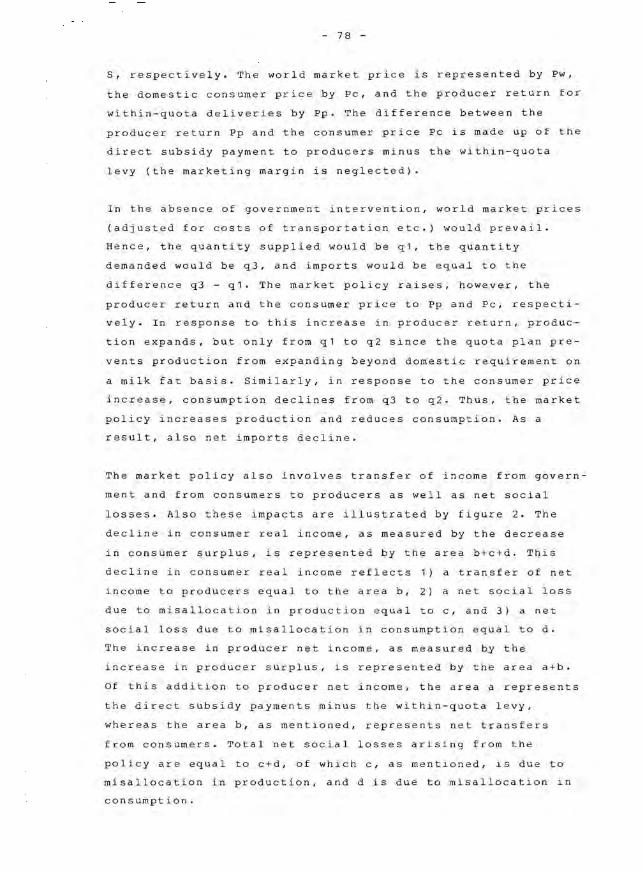

PART III. IMPLICATIONS OF DIFFERENT DAIRY POLICY INSTRUMENTS

7.

8 .

IN RELATION TO THE EUROPEAN COMMUNITy........... 83

The Problem of Surplus Agricultural Products ......••..

Dairy Policy Instruments •.........••............•.•..

8.1. Direct subsidy payments ..•••...............•••..

8 .2.

8.3.

8 .4.

Price discrimination

Levies on milk production

Individual producer quotas

83

86

86

87

88

89

SAMMENDRAG..................................... . ............ 93

Malkekv~gsektoren og forbruget af mejeriprodukter i

USA og Canada ..........................••.......... 94

Markedsordninger for mejeriprodukter i USA og Canada 97

Effekten af forskellige markedspolitiske instrumenter

i relation til overskuddet af mejeriprodukter i F~lles-

markedet 10 3

BIBLIOGRAPHY .....••••..........••••• •.... ..........•. •.•.. 1 U9

7 -

1. Intr o duction

The European Communi~y is facing a prob lem of substantial

surplus of da1ry products. The price suppo rt policy f or dairy

products, whi ch is i n ~ e nd ed to support farm pr ices of milk

and farm incomes, encourages farmer s to expand milk production

in excess of LnternaL dema nd. Si nce t he ou t lets f or surplus

dairy produc t s are limited , the price po l i c y involves large

expendi t ures. The p resen t pric e policy , the r efore, seems

insufficient as a means to insur e dai r y farme r s an acceptable

lncome without crea t ing a substa ntial s u r plus of dairy

products, the disposal of whi c h req ui res l arg e expenditures.

In view of th is situatio n, i t might be app r opriate to

supplement the present dairy pol i cy by measur es to reduce milk

production or to increase interna l co nsumpti on of dairy

products so as to reduce o r e l iminate the surplu s of dairy

products.

An examina~ion of rlalry price po l i cies i n the United States

and Canada may i ndica t e possl ble sol ut ions to the problem o f

surpl us da i ry products i n ~he Eu r opean Communi ty. The dairy

price policies in boch these coun t r i es comp r is e separate

prog r ams for manufac t ur i ng mi lk and f lui d milk.

The pric e suppor t programs for manufa e Lur i ng mi lk in Ca na da

and particularly that in the Uni t ed St ates ha v e much in c ommon

w~th the pri ~ e SUPPO&t pro g ram for milk in the European Com

munity . hl! t hese progra ms , for i nstance, main tain farm pr ice s

of milk above a mi n ~mum level by offers t o pur chase manufactu-

red da~ry products at pre-de t er mi ned prices .

port program for manufacture d mi lk di ffe r s ,

The Cana di an s up

however, from EC's

program 1n two respects : First ly, by applyi ng a mar ke ting quo

ta p l an . Secondly, by comprising a d i r e ct subsidy payments to

f rmers to supplemen t Lhe mdrket re tu rns . The quota plan con

trols mi l k product1on a n d , in s o doing, llmit s the fundS

required to suppo r t the d s po s al o f su r plus p r o du c tion. The

direct subsidy makes it possible t o low e r c on sumer prices of

man uf actured ddiry produc ts a nd, thereby , t o inc rea se domestic

- 8 -

consumption. The United States program for manufacturing milk

does not apply any quota plan nor any direct subsidy.

The United States and the Canadian programs for fluid milk

attempt to enhance producer returns by establishing prices for

fluid milk substantially above the prices of milk used for

manufacturing purposes. This form of price discrimination

takes advantage of the fact that the demand for fluid milk

products is more inelastic than is the demand for manufactured

dairy products. Thus, although the dairy policies in the

United States and in Canada have much in common with that in

the European Community,

apply some instruments,

the dairy policies in these countries

not yet applied in the European

Community. It is of interest to examine whether these

instruments could be used in the EC to help solve the problem

of surplus dairy products.

The supply as well as the demand of dairy products are affected

by several factors. One of the major factors affecting the

supply is the possibilities for shifting resources, material

as well as human, from dairy farming to other lines of farm

production or to other sectors of the economy. These

possibilities for removing resources from dairy farming

depend to a large extent of the structure and the organization

of dairy farming. Larger farms, for instance, are usually

better able to adjust production and resource use in response

to new technologies and to shifts in relative factor prices

than are smaller farms.

The structure and the organization of dairy farming in North

America differ in some respects from that in the European

Community. Dairy farms in Canada and particularly in the

United States are larger and more highly specialized than they

are in the European Community. The relative large dairy farms

in the United States might, therefore, explain why the United

States has succeeded better in limiting surplus milk

production than has the European Community.

Major factors affecting the demand of dairy products are

changes in population and in per capita income as well as

- 9 -

changes in consumer t~ste s a n d p r e f e ren ce s . Especially changes

in co n sumer Las t es a n d p ref er e n c e s hav e h a d an adverse impact

on the demand of rlalty pr o d u c t s both in No r t h America and In

t h e Europea n Commu n tty . The s e ~ h a n g e s , of c o ut ee, have

i ncreased t he d i ff i culti e s o f ba l a n cing the demand and the

su pply o f dairy products .

This report omptlces t. ilr ee pa rt s. Pa r t I d l s cribes patterns

a n d trends in da i ry farm i n g a nd in da i r y p r o duct consumption

I n the U n~ t ed S t ates and i n Can ada with pa r t icular emphaSIS

on those ttends that tend to cause i mb a la n ce be t ween supply

and demand . Part lL d_scrlbes t h e d a i r y sup p o rt programs in

the Uni t ed S tates a nd Canada and examines t he impacts of those

p rogra ms . Part III Ind i cate s Imp l i ca t i ons o f differen t dairy

policy Instrum ~ n ts I n re l a t i o n t o t h e s i t u a t i on in the

Eu ropea n Co mmu n i ty .

1 1

PART I

DAIRY FARMING AND DAIRY PRUDUC T CO S UMP TIU N

IN THE UI ITED STATES AND CANADA

The capac i ty ~o produc~ agr i c ul~u rcl l pr o du ct s in the Unit ed

Scaces and in Canada has exceed~d c ommerci a l dema nd in most

years during the last three decades. This e xC e sS capac ity is

indleated by a rat e of rdt u rn for certa i n resou~c es employed

in farming that has been si~nificantl y b e low t h e r et urn for

compa r able resourc·s . r' other sectors of the eco nomy. Other

iodications of the excess capacity are governme nt interventi ons

aLmed at curtailLnq agricult u r~l prod u cti on a s we ll as stocks

of surplus produ c ts . Tile excess capacit y r~prese nt s two major

prob ems : a resour~e allac tio n problem an d an income problem.

The resource allccatLon prob l em r e f lec ts the fa c t that total

production in the ~con~my wou l d be incrEdsed if resources were

shifled from farming tv othe L Sectors . The inc o me problem is

due to the [~ct that fdrm income , in the abs ence of government

Lntervention , wou ld be lower than wha t i s polit ically accepta

ble.

Th e excess ~apaci y in (arming in th e Unite d States and Canada,

as ~n oLher developed market ec o nomies , is root ed in conditions

surroundLny p~oduction dnd consumpt~ o n of ayri cultural products.

Hathaway (l b ) cla ims tlat ~ he excess capac i t y hdS arisen and

persist ed because of d simultaneous ex isten ce of the f o llowing

conditions: 11 rd pLd rdt~ s of technolo yic al imp r ov ements in far-

ming, 2 ) ilL9" d yl ",e o f asset f i xlty , J) a compet itiv e market

struc ure , 4) a low price el asticity o f de mand for farm

products , and 5 ) a low income e l astici t y of the demand .

Brlefly sated thOSl1 "o ndltions i nte!d c t as fo llows: The rapld

rates of tech no l ogi ca l lmp r ovements ledd t o a substantial

increase i n proauLtivlty , which 1.n t urn lesul Ls in a rapid

i.ncrease 1n aggrt:gat ", sup ply (a sh l. tt to the rlyht In the

supply c.: U1.'J ~) .

12 -

The aggregate demand of agricultural products also increases

but more slowly. This more slow increase in the aggregate de

mand is due to a modest increase in population and the low

income elasticity of demand for agricultural products.

Together, the rap~d increase in supply and the modest increase

in demand result in falling product prices and farm incomes

unless governments intervene in the market.

Furthermore this decline in product prices is seriously aggra

vated by the low price elasticity of demand for agricultural

products as well as by a low price elasticity of the supply.

This low price elasticity of the supply is caused by two con

ditions: the high degree of asset fixity and the competitive

market structure. The high degree of asset fixity inhibits a

removal of resources from farming. The competitive market

structure provides no motivation for the individual farmer to

limit production by leaving resources unused when product

prices tend to decline since his action will not prevent them

from doing so. Thus the disequilibrium problem in agriculture

is caused by the simultaneous existence of several conditions.

Part I of this analysis attempts, in the light of the above

mentioned theory, to analyze patterns and trends in dairy

farming and in dairy product consumption in North America.

2. Patterns and Trends in Dairy Farming

2.1. Structure of dairy farming

Dairy farming is a significant segment of farming in the United

States and in Canada, but its relative importance has been

declining slightly during the last two decades. of total cash

receipts from marketing of u.s. farm products, sales of milk

and cream accounted for 11.3 percent in 1978-79 compared to

14.0 percent in 1960-61. Similarly in Canada, sales of milk

and cream, inclusive of government subsidies, accounted for

14.5 percent in 1978-79 compared to 17.5 percent in 1960-61.

13 -

The structure o f farm ~ n g i n th e u .s . a nd in Can ada has change d

substantially during the l as t decades . ~h ese cha nges have led

to fewer but ldrger faems , t o in~r~ased con c e ntrat i on, and t o

increased speci llzation. The maj o r ca u ses o f th e se chang es in

the structure of Earm~ng are u n doubt ed ly the eme rgence of new

farm technolog~~s and cha nges i n r elat ive p r ic e ~ of lnput s .

Both ( f chese factors have e n c ourag e d farme r s to subst itut e

capital for lab o r , and Lhi s subst i tut i o n has re q uired a ne w

farm sttucture. FUcthecmor e , t he adoption o f n ew farm

t echnolo gies has i ncr~ase d t h e mi nimum siz e of farms and o f

e n terprises n ec~ssa ry to altain full e eonomles o f sc al e . This

also has a f fe~ted thd farm str u c ture .

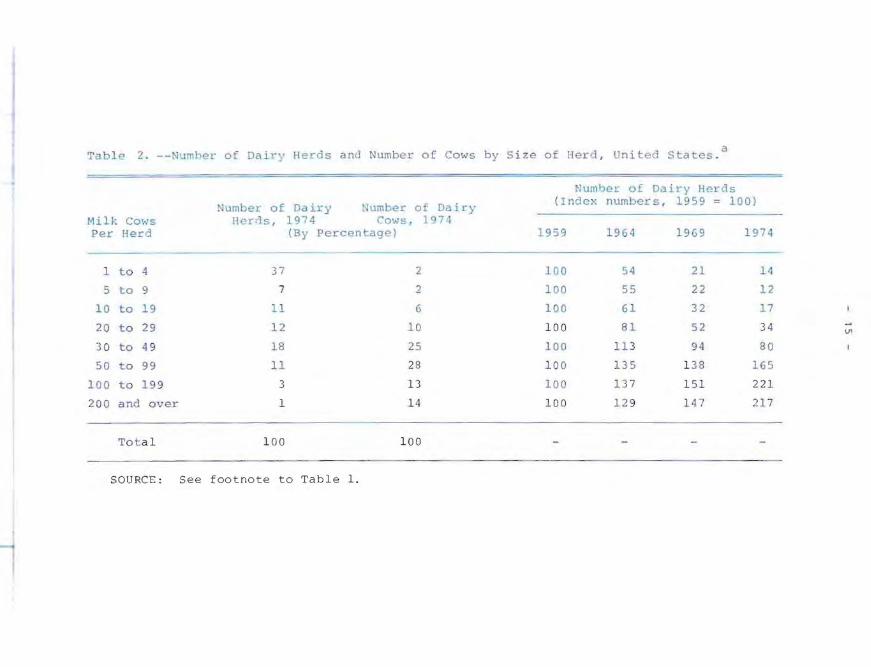

Also the S ; lu c ture of dairy farmlnq has change d s ub stan tiaily.

Th~ small da~ry farms are d i sappearin g , Mn d s o a re the

s1de li ne dairy ente r pr 4 ses, whereas th e r e ma i ning dai ry farm s

are expanai n g the~r da~ry e nt e r p r i s6s ( 3 3 ). I n total t hese

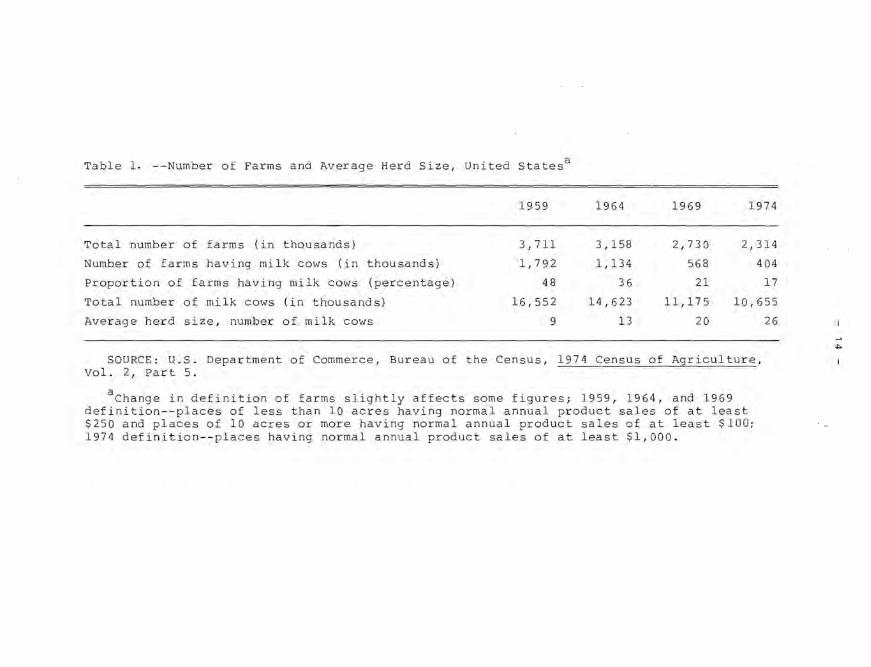

changes in U. S . dalry f~rmi ng have lead to a d e c lin e in th e

number of (arms hav ng milk cow s f ro m 1, 792 , 0 0 0 in 1959 t o

404,ODU i n 1974, a de Clin e in th e pr opo r tion of (a rms having

milk c ows from 48 t o 17 percent , and an in c r eas e in a ver age

herd s~ze from 9 to 26 mil k cows ( Tabl e 1 ) • Al so the e la tive

importd n C<l of the di f t .. re nt s ize group s has ,-,hanged subs tan-

tiaily since H59; thE numb e r of hel-ds W1 th le ss than 30 COI .... s

ha s decl i ned sharply, S1 n Cl:! 1964 , also the n um ber with 30-49

cows h as declin d , and the number of herds with more t h an 50

cows has 1nc eased sharp l y (Ta b le 2 ). De s pi t e this decline in

the ~mportan c e of small h erd s r l ativ e to l arg~ herds, 45

percent of the u . s. ' ale y h.,rd W iHi st i l l hel d on f a r ms having

less than SO cows 1n 1~74 , and only 27 p"r~l:I n~ was held on

farms having mo];/; Lhan 100 cows (Tilb le 2 ).

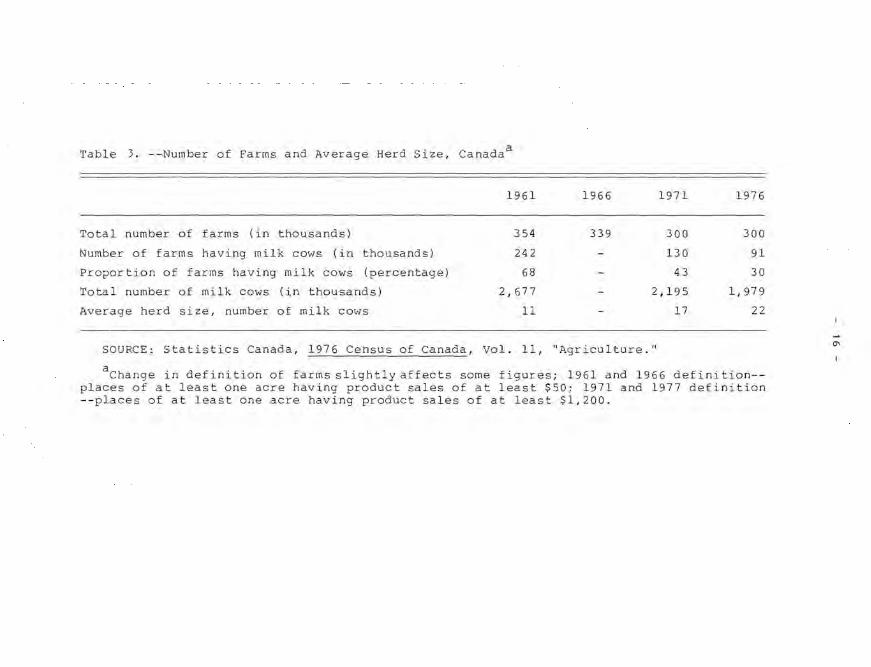

The change ~ n tne s~ructur~ of dair y f arm i ng i n Canadd has

lead to Ll",cline .~n t il " nurnbe r o f f a r ms hav i ng m~i k COl-iS

from 242 , OUO in 196 1 to Y 1 ,OO O in 1 9 76 , a dec li n e in the

proportion of farms havi ng milk cows f r o m 68 to 30 per c en t,

and an in c rease in av e rd ge herd siz e from 11 to 22 milk cows

(Tab l " 3). Th",s.~ ..:hd ll q"',. ha v e b "e n a~ c omp a n i ed by a shar p

dec110a 10 Lhe number of he rd s w~th les s th a n 1 8 milk co ws,

Table 1. --Number of Farms and Average Herd Size, United Statesa

1959 1964 1969 1974

Total number of farms (in thousands) 3 ,711 3,158 2,730 2,314

Number of farms having milk cows (in thousands) 1,792 1,134 568 404

Proportion of farms having milk cows (percentage) 48 3 6 21 17

Total number of milk cows (in thousands) 16,552 14,623 11,175 10,655

Av erage herd size, number of milk cows 9 13 20

SOURCE: U.S. Department of Commerce, Bureau of the Census, 1974 Census of Agriculture, Vol. 2, Part 5.

aChange in definition of farms slightly affects some figures; 1959, 1964, and 1969 definition--places of less than 10 acres having normal annual product sales of at least $250 and places of 10 acres or more hav ing normal annual product sales of at least $100; 197 4 definition--places having normal annual product sales of at least $1,000.

26

~

Table 2 . --Numher of Dairy Herds and Number of Cows by S i ze of Herd, United Statcs.a

Num"er of Dairy Herds

Number of Da iry Number of Dajry ( Index numbers , 1959 100)

Milk CO\olS H'?r<is, 1974 Cows, 1974 Per Herd (By Percentage) 1959 1964 1969 1 974

- - - - -I to 4 37 2 1 00 54 21 14

5 to 9 7 2 100 5') 22 12

10 to 19 11 6 1 00 61 32 17

20 to 29 12 10 1 00 8 1 52 3 4 V1

3 0 to 4 9 18 25 100 11 3 94 80

50 to 99 11 2B 1 00 135 13 8 16 5

100 to 199 3 13 100 13 7 1 51 22 1

200 and over 1 1 4 10 0 12 9 1 47 217

Tota l 1 00 10 0

SOlJRCE : Se e f ootnote t o Tab l e 1.

Table 3. --Number of Farms and Average Herd Size, Canada a

1961 1966 1971 1976

Total number of farms (in thousands) 354 339 300 300

Number of farms having milk cows (in thousands) 242 130 91

Pro;?or tion of farms having milk cows (percentage) 68 43 30

Total number of milk cows (in thousands) 2 ,677 2 ,195 1,979

Averag e herd size, number of milk cows 11 17 22

SOURCE: Statistics Canada, 1976 Ce nsus of Canada, Vo l. 11, "Agriculture."

aChange in definition of farms slightly affects some figures; 1961 and 196 6 definition-places of at least one acre having product sales of at least $50; 1971 and 1977 definition --places of at l east one acre having product sales of at least $1,200.

0'

T.Jb1c :. . --Nu mbc l- of Dairy !lerds an,1 Number of nait-y Cows by Siz.e of !lerd , Canada"

Number of f)a i ry Herds

~~ilk :':0\-;5

Per ile r d

1 to 2

3 to 7

8 t o 1 7

1 8 to 3 2

33 t o 62

6 3 t o 9 2

9 3 and over

To ta l

Number 01 Dairy Number of "~iry ll"'nls , 1976 COy]S, 197(,

2 4

13

1 ')

23

21

3

1

1 00

(By Percentage)

2

3

8

27

.<12

11

7

100

( I nr-lt":: :'; umber s , 1 () t 1 100)

1%1 1% 6 1971 1976

1 00 73 4 0 3 3

1 00 58 23 1 2

10 0 6 5 31 13

100 1 02 82 56

10 0 16 1 21 5 24 4

1 00 1 8 5 213 50 1

1 00 172 295 54 0

. , 1 9 7G Cen -SOU RCE : S l a tist i c s Ca nada , 1 9 7 1 Cen sus o f Ca nad a , Vo l. 4, Pa rt 1; sn s o f ~a nClcla, 1101. 11. - ---

OSe e foo l note (a) t o Tab le 3.

--.J

18 -

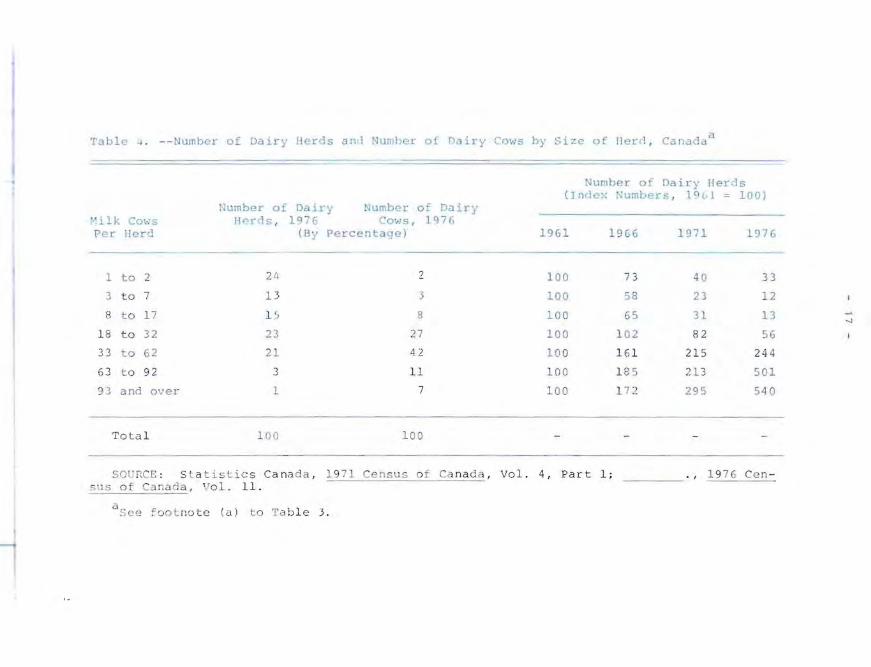

a decline, since 1966, in those with 18 to 32 cows, and a

sharp increase in the number of herds with more than 32 cows

(Table 4). In spite of these changes in the relative

importance of the different size groups, 40 percent of the

Canadian dairy herd was still held on farms having less than

33 cows in 1976, and only 7 percent was held on farms having

more than 92 cows.

Thus, the structure of dairy farming in the u.s. and Canada

has changed drastically in the last two decades. Dairy farming

has become concentrated on a relatively sma ll proportion of

'farms, particularly in the United States, and the average herd

size has increased substantially. None the less, a significant

proportion of the dairy herd in the U.S. and particularly in

Canada, is still held on farms with herds too small to attain

full economies of size.

The structure and organization of dairy farming varies among

regions. Some regions in the U.S. have come further in the

process of adopting the farm structure to modern technologies

than have other regions. The question arises, therefore,

whether dairy farming in those regions indicates the future

structure and organization of dairy farming in North America.

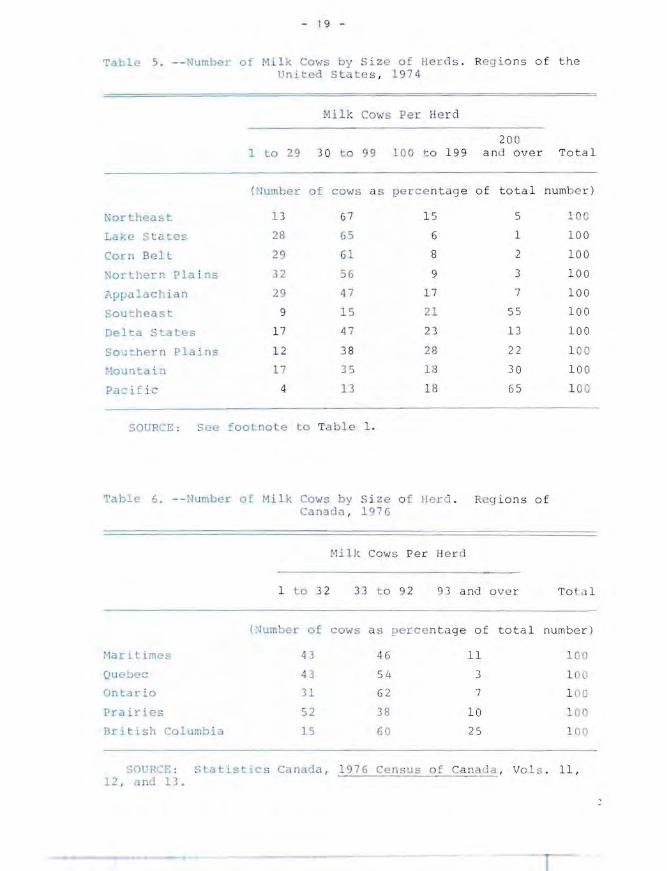

The regions having this different dairy farm structure are the

Pacific (especially California), the Southeast (especially

Florida), the Mountain (especially Arizona) and the Southern

Plains (especially southern Texas). In those regions, a

considerable proportion of the dairy production is concentra

ted on farms having more than 200 cows (Table 5). In the

Pacific, 65 percent of all dairy cows was held on farms with

more than 200 cows, and the average size of those herds was

437 cows; in the Southeast, 55 percent, and 523 cows ; in the

Mountain, 30 percent, and 447 cows; and in the Southern

Plains, 22 percent, and 346 milk cows. In the other regions in

the U.S. and in Canada (Table 6) , the proportion of cows held

on such large-scale farms is far le ss.

The large-scale dairy enterprises are based mostly on purcha

sed feed - beside concentrates, bi-products from the fruit

- 1 9 -

TIle 5 . - - Number of Milk Cows by S ize of H r ds . Reg i o ns of the Uni -ed S ta t e s , 1 974

Milk Cows Pe r He rd

20 0 1 to 29 3 0 to 99 10 0 t o 1 99 an J over Tota l

(Number of cows a s percentag e of total numb e r)

Nor Lheast 13 67 1 5 5 ~O C

Lake S t ates 2B 65 6 1 1 00

Corn Belt 29 61 8 2 100

:-.lorthern P la i 05 32 56 9 3 1 00

',.PP< lachian 29 47 17 7 10 0

Sou~heast 9 1 5 21 55 1 00

Delta StatGS 17 4 7 23 13 100

Sou~hern Pla ins 12 38 28 22 1 00

:·!ounta i n 17 35 1£3 30 10 0

Pa i fi _ 4 13 IB 65 1 0 0

SOU R-:E : See footnote to Tabl e 1.

Table 6. --Number of Mi lk Cow by Si z e o f Herd . R g ' ons of Canaail , 197 6

Milk CO vl S Per fl e r d

1 to 3 2 33 t o 'J2 93 a nd over T ol 1

(~umber o f cows a s per e n t age of tota l numbe r )

Mar Lt imes 4 3 46 11 100

Quebec 43 54 3 1 00

Ontar io 31 62 7 I no Prairies 52 3 8 10 1 00

Bl- i t i S J1 Columbia 1 5 60 25 I OO

SOl R!'E: Statistics Canad a , 1976 Census o f Cana ' a , Vo l s . 11, 11 , and 13.

20 -

sector in Florida, and mainly hay in the other regions. There

are probably several reasons that those large-scale dairy

farms have emerged in those regions and not in other regions.

One important factor seems to be the existence of conditions

allowing a separation of milk production from forage produc

tion; in Florida, the availability of bi-products from the

fruit se=tor; and in the other regions, favorable conditions

for producing hay, which is less expensive to transport than

are other forage crops. It is not likely, therefore, that

those large-scale dairy enterprises will develop in regions

outside the ones mentioned, at least not in the near future.

2.2. Location of dairy farming

Although some dairy farming is dispersed throughout all

regions in North America apart from the northern territories

of Canada, dairy farming is largely concentrated in certain

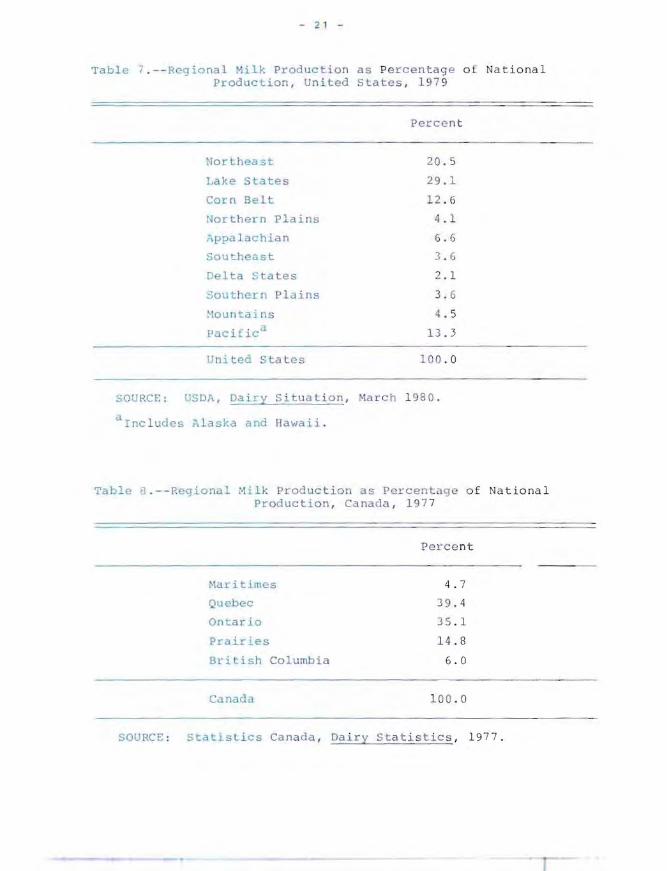

areas. u.s. dairy farming is mainly concentrated in the Lake

States and in the Northeast, which in 1979 accounted for 29.1

and 20.5 percent of total U.S. milk production (Table 7). Next

in importance comes the Pacific with 13.3 percent and the Corn

Belt with 12.6 percent, while the other regions accounted for

the remaining 24.5 percent. Canadian dairy farming is mainly

concentrated in Quebec and Ontario, which in 1977 accounted

for 39.4 and 35.1 percent of total production, while the other

provinces accounted for the remaining 25.5 percent (Table 8).

This location of dairy farming is determined mainly by

comparative cost advantages and by cost of transporting milk.

Thus most milk used for fluid products is produced within the

region in which it is comsumed because of the relative high

cost of transporting milk. None the less, a small proportion

of fluid milk in the U.S. is produced outside the consuming

region and transported over long distances. By contrast, milk

used for manufactured dairy products is produced primarily in

areas having comparative cost advantages in dairy farming and

with less demand for fluid products. The areas having

comparative cost advantages are the Lake States and the North

east in the U.S. and Quebec and Ontario in Canada. The

- 2 1 -

Table 7.--Regional Milk Production as Pe rcen t a g e of Nationa l Production, Un i ted States , 19 7 9

Northeast

Lake States

Corn Belt

Northern Plains

.:\ppa1achian

Southeast

Del ta S ta tes

Souther Plains

10untains

pacifica

United Sta Les

Perce n t

20 .5

29 . 1

1 2 . 6

4 .1

6. G

3 . 6

2. 1

3. 6

.; . 5

13. 3

100 .0

SOURCE: USDA, Dajry S ituaLi on , March 1980 .

alnc lud es Alaska and Hawaii.

Table O. --Pegional Milk Production as Percentage o f Na tional Production , C3nada , 1 97 7

~lal: i times

Quebec

Ontario

Prairies

British Columbia

Canada

Pe r cent

4. 7

39 . 4

35 . 1

1 4. 8

6 . 0

100 . 0

SOURCE : Statistics Canada , Dairy Sta t is t i c s , 1977.

- 22 -

Table 9.--Milk Production, United States and Canada, 1960 to 1980 (In Billions of Pounds)

United States Canada

1960 123.1 17.7

1961 12S.7 18.3

1962 126.3 18.4

1963 12S.2 18.4

1964 127.0 18.S

1965 124.2 18.4

1966 119.9 18.3

1967 118.7 18.0

1968 117.2 18.2

1969 116.1 18.S

1970 117.0 18.0

1971 118.6 17.S

1972 120.0 17.7

1973 l1S. S 16.9

1974 l1S.6 16.8

197 S l1S.3 17.7

1976 120.3 16.9

1977 122.7 17.1

1978 121.6 16.4a

1979 123.6 16.4a

1980 128.4 17.1a

SOURCE: USDA, Dairy Situation, various issues; Statistics Canada, Handbook of Agricultural Statistics, Part VII, "Dairy Statistics, 1920-73"; ., Dairy Statistics, various issues; ________ ., The Dairy Review, various issues.

aQuantities used as farm-home consumption and as feed for livestock estimated by the author.

No r c h e a st i n t h e U . S., a lt houg h having com p ar at i v e cost

ad v an t Ages 1n da Lr y fat mi ng , prod u c e s pri marily fluid milk

b~cause of it s loca tio n c l o se to l ar g e p op ul a t i on centers of

t h e Eas t Co a s t .

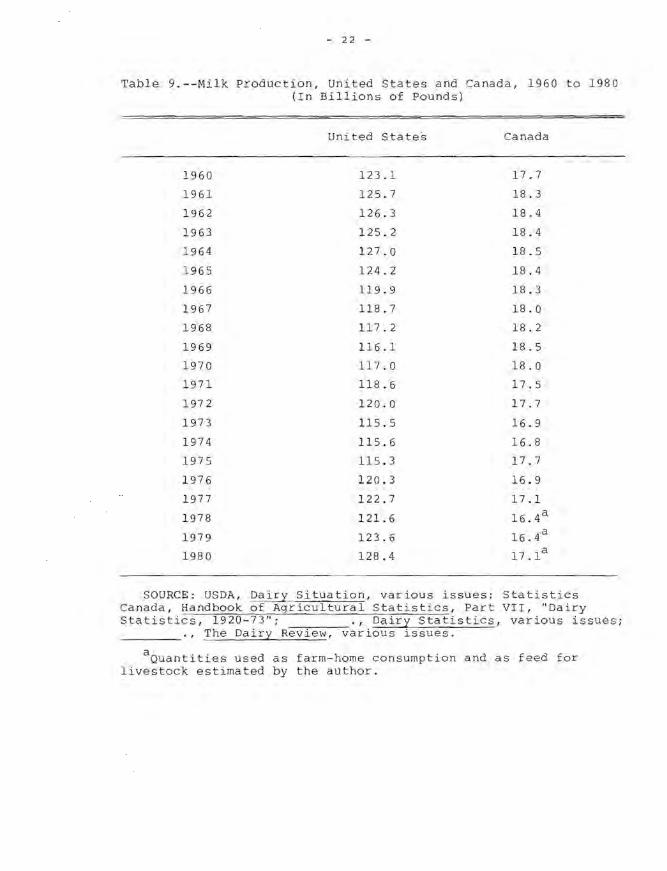

2 . 3. TL e n ds in mi l k prod u c t ion

Mi l k pr od uc ti on in the U. S. a n d Can ad a s ho wed a long-term

upward tr en d up un t il th e 1 9 6 0 '~, b ut t h i s t r e nd appears to

have c o me to a s t op si nc e then . Some s hift s h a v e occurred.

ho wever , Ln t he sho rt-t e r m tr e nd s ince 1960 . In the early

s i xties , mil k productlo n c ont i n ued an up war d t r e nd in both

count r Le s and rea c he u r e co r d h i g h s in 19 6 4 - in the U.S. of

127. 0 bil lion p o und s a nd i n Canada of 18 . 5 b l llion pounds

( Ta b l e 9 ) . Th e n ~xt t an - y e a r per i o d s h o we d a downward trend

r: e a ch ing , r:ou n 197 3 t o 19 74 , a leve l abo u t 9 percent below

the 19 6 4 r ecord s i n b o th c o untries . In the la st half of the

seve nt ie s, U. S . mi lk pr o d u c t i o n moved u pward a gain reaching an

a 1 1- 10 ime t. i 9 h i n 19 80 - per c ent a bov e th e 1 9 6 4 record level.

By c ontrast , the Ca l a d L .. n p r otl u IC t i on l: emain ed at the same

l eve l ~h r o u g h u t t h e la st h a lf of t h e s e v ent ies although

f lu c tu a ting some whd L f ro m y ea r to year .

2.4. Pat t~ rn s of p roull ct ion il n d r es o urce us e

The pat Lerns of prod uc t i on a Dd par t i c ula r l y t h e patter ns of

re s o u rce us ~ on da Le y f Lms p r o v id e an in dica t i on of the de-

gre8 (Jf ets s e fi xi t y i n th e da i r y s e c tor a n d , thereb y . of the

s~ctor 's 3 b i l i t y t o ad Jus t i t s l:eso u r c e use an d its output. l)

1) Th e d d~a o n prod u~ t ion a nd r e sou r: c e use , gL v en in this s e ct l ~ n , are n a tio nal averages for d a i r y [ a rms. as defln e d i n th e a gr i cult u ra l c ensuse s. I n bot h th e U. S. and Canada, :h e ce n s u s cla s s L f ica t l on of farms a c c o r d i n g to type of e n te l' prise c omp ris,",s on l y f arnls wi t h "a l e" o f S 2,500 or more . Al l dat.a In t h is s e c t i on , tl e re f ar e , re fe r t o farms D C th i s Slze , and t o p r o d uc tion a n d co s t s, etc. on these [ a r ms wh ether d1l Y f a r ms or o tl e r f a rm s . it not otherWlse l n d l C(ite S~I I C" t he da t a are n ation a l a v e ra ges, they l nd ic a l e the mix o t p rodu c ts - n d t h e mi x o E r e source use in t h e U. S . and Cillla.lJ.a n d a iry secto r s . 'J'he s e d ata may, ho wever , be mJ. s L~ad Lng as indicator s o f Lh e organization of n d i v1~ ual da Lr y f arms b e c ause o f wide d i f f e rences among

lair y f a r ms w l. t h~n ea ch c ounLry .

- 24

In the U.S., dairy farms, as defined in the agricultural

made up only 12.0 percent of the total number of

farms in 1974, but they held 89.3 percent of all dairy cows,

and they accounted for 93.7 percent of total cash receipts

from sales of milk and cream. In Canada dairy farms 2 ) made up

only 17.9 percent of the total number of farms in 1976, but

they held 85.9 percent of all milk cows. Thus dairy farming in

the U.S. and Canada is mainly concentrated on a small

proportion of all farms. Because of this high degree of

concentration, data given on dairy farms represent quite well

the entire dairy segment in question.

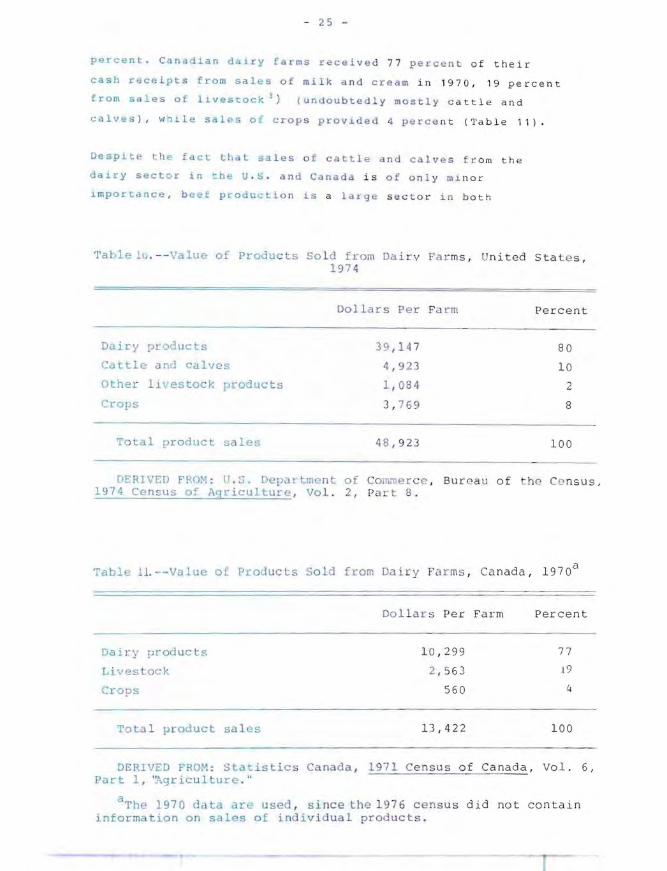

Most dairy farms in the U.S. and Canada are highly speciali z ed

in the sence that the dairy enterprise constitutes the only,

or almost only, source of farms income. Sale of milk is by far

the most important source, while sales of cattle and calves is

of only minor importance. As shown in Table 10, U.S. dairy farms

received in 1974, on an average, 80 percent of their cash

receipts from sales of dairy produ c ts, 10 percent from sales

of cattle and calves, 3) whereas sales of other livestock

products and sales of crops accounted for the remaining 10

2) Dairy farms in the U.S. are defined as farms where (a) sales of milk and cream accounted for 50 percent or more of total sales (b) sales of milk and cream accounted for 30 to 50 percent of total sales provided that one-half of the cows, at least, were milk cows and that the sales of milk and cream together with the sales of cattle and cows accounted for 50 percent or more of total sales.

In Canada, dairy farms are defined as farms wqere (a) fifty -one percent or more of the total potential value of agri c ultural products sold is obtained from the dairy production; (b) fourty percent to 50.9 percent of the total potential value of agricultural products sold is obtained from dairy production provided that the value obtained from dairy produ c tion together with the value obtained from cattle and calves amounts to 51.0 percent or more of the total value of agricultural products sold.

3) The cash receipts from sales of cattle and calves, as with sales of other items, are gross figures in that they include inter-farm trade; the net receipts from sales of cattle and calves are even lower.

- 25 -

percent . C nadian dalcy farm s received 77 percent of their

casb receipts from s al es of milk and cream in 1970, 19 percent

from sa .. es of ll.vestock 3 ) (undou btedly mos t ly c at tl e and

calves ), w~il e sales Q< crop s provl.ded 4 perc e nt (Table 11)

Despite the Eact that $ales o f ca ctle and calves fr om the

dairy sector ~n t:h~ U. S . and Canada is of only mi nor

l.rnporcance, bc~f produ~tion is a 1 rge s ec t o r in b oth

TaGlelu. - - Value of Products So l d from Dai rv Farms, United State s, 19 7 4

Dollars Per Farm Percent

Dairy ,n:o ducts 39,14 7 80

Ca ttle and calves 4,92 3 10

Other Ii" estock products 1,084 2

Crops 3 , 769 8

TOlal product sales 48 ,92 3 100

D£RIVED FI' OM : U . S. Department of Com:ne rcc , Bur e au o f !1 C nsus, 1974 Census of Aqriculture , Vol. 2, Part 8.

Table l L--Valuc of Produc t s So ld from Dai ry Fa r ms , Ca nada, 197 0u

Dai]") [Jroducts

Livestock

Crops

Tota l product sales

Dol l ars Per Farm Percent

1 0 ,2 99

2 ,5 63

560

13 ,4 22

77

[9

4

100

DERIVED FROM : Sta istics Canada , 1 971 Census of Canada, Vo l. 6, Pact l , ':;gricu1turc."

a The 1970 data ace used , since the 1976 censu s did no t contain information o n sales of individual products.

- 26 -

countries. But beef production and dairy farming constitute

two almost entirely separate sectors. Dairy farming and beef

production in the U.S. and in Canada differ in this respect

significantly from these sectors in most European countries.

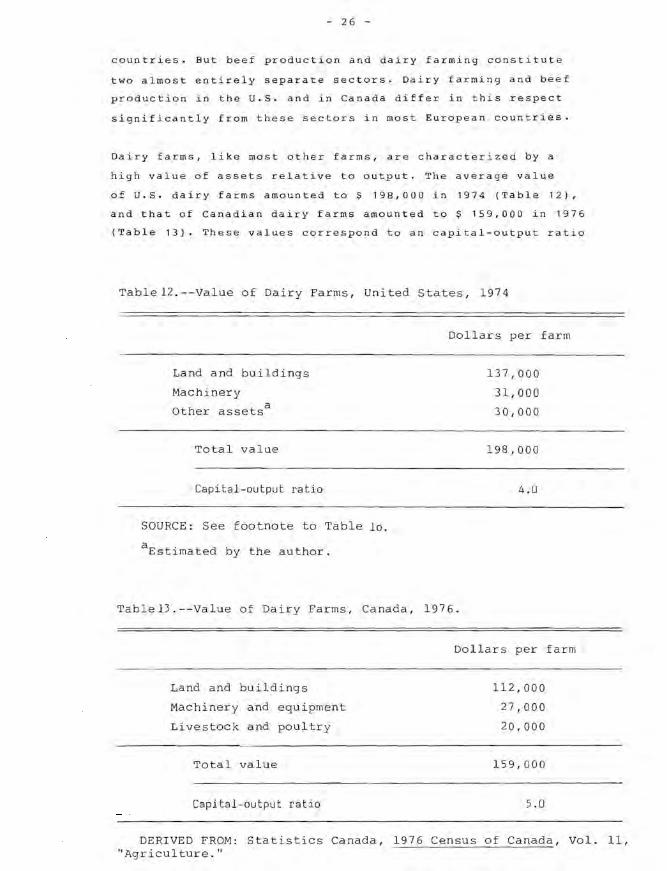

Dairy farms, like most other farms, are characterized by a

high value of assets relative to output. The average value

of U.S. dairy farms amounted to S 198,000 in 1974 (Table 12),

and that of Canadian dairy farms amounted to S 159,000 in 1976

(Table 13). These values correspond to an capital-output ratio

Table12.--Value of Dairy Farms, United States, 1974

Land and buildings

Machinery

Other assets a

Total value

Capital-output ratio

SOURCE: See footnote to Table 10.

aEstimated by the author.

Dollars per farm

137,000

31,000

30,000

198,000

4.0

Table13.--Value of Dairy Farms, Canada, 1976.

Dollars per farm

Land and buildings 112,000

Machinery and equipment 27,000

Livestock and poultry 20,000

Total value 159,000

Capital-output ratio 5 .0

DERIVED FROM: Statistics Canada, 1976 Census of Canada, Vol. 11, "Agriculture."

- 27

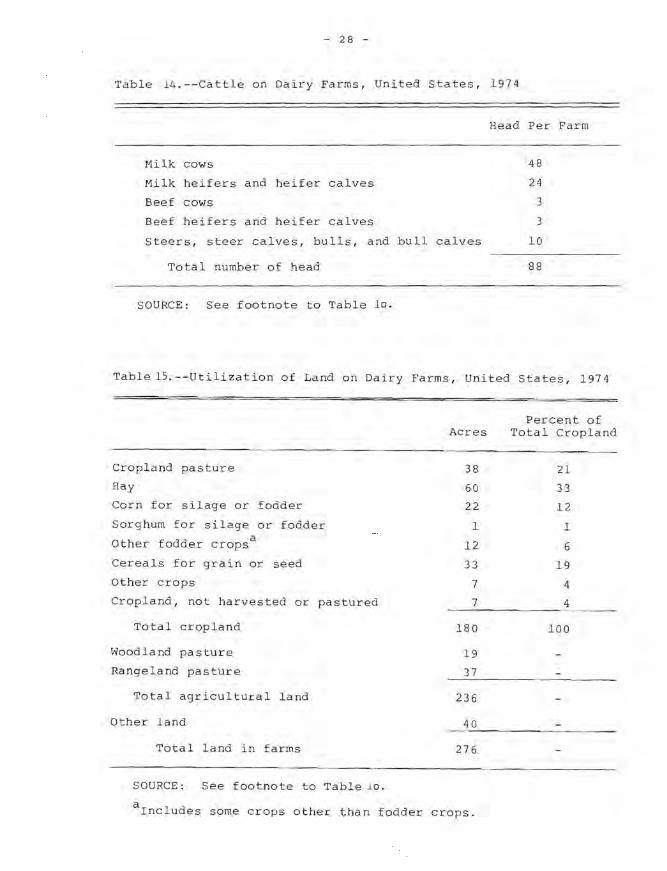

of 4 ~nd 5, respectively, which are hi g h c ompar ed with most

non - farm indus tr ies.

t hat dairy farming,

These high cap~ta l - o u tput r a t ios

lik~ most o t he r t yp e s of Iar ming,

indi cate

involves

a reldrively arge amount o f du r a bl e ass ets ; a characteristic

that contributes to a hi gh degree of ass e t fi xi ty in farming.

Although da iry fa lm s 10 t h e u. s . and i n Ca nada are consider

ably larger chan in most Wes t Eu r o pea n c o untries , t he major

ity are family en t e rprise s i n tbe se n ce that t h e f a mily pr o

vides a l l o r most of t he l a bor i nputs . On U.S . dairy f arms the

herd size averag~d 48 milk cows , and t he c r o p l and ave r aged 1 8 0

acres ~ n 1974 (T ble 14 and Tab l e 1 5) . The c orr e spondl.ng

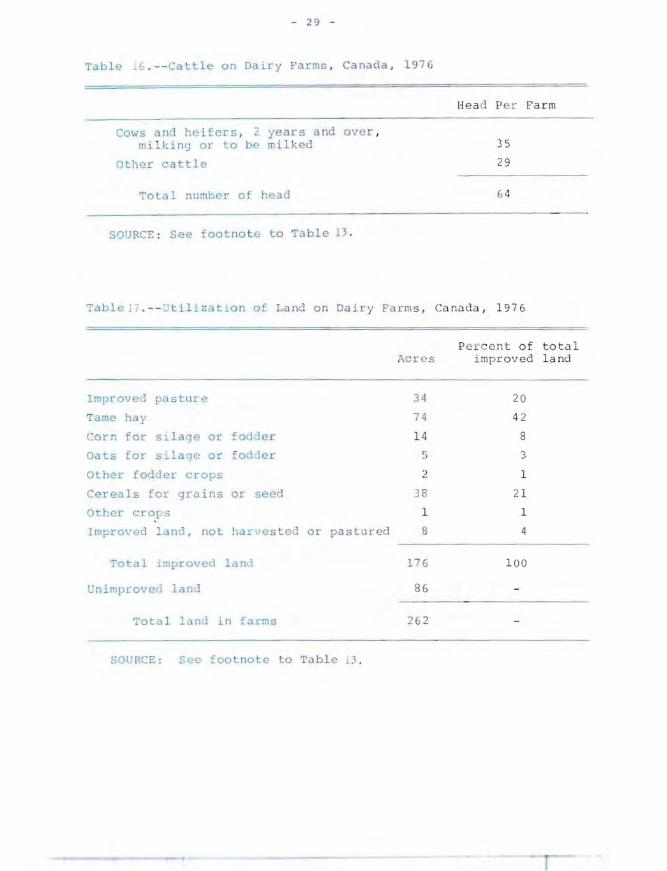

figures fo r Canadian dai ry far ms we re 35 milk cows an d 176

acres of i mprov ed land (Ta bl e 1 6 and Tabl e 17). Although the

daIry en t er p rise consLitutes t h e only o r almos t t h e only

source o f income on uairy fa~ms, th e dairy ent e rp rise is not

the on ly lmportan~ enterp r is e on th~se farms . Mos t da i ry farms

selll produce all or most of the i r fee d requi rement . The

extent to which dalry f a rm i ny relie s on hom e - g rown feed and,

thereby , on farm land is i ndic a ted by the l and use, shown l.n

Tables 1 5 and 17. 01 Lot al cropla n d on U.S . da ir y fa rms

averag1ng 180 a.;r.,s, 2 1 percent wa s used for past ure, 33

percent f r hay, 13 p~rcent for corn and sor g hum f or silage or

fodder , 19 petcant for cerea ls , an d th e remainin g 14 percent

waS used for o th er c rops or was left i d l e . DE total improve d

land on Canadian dal.~y farm~ averag i n y 176 ac res , 20 percent

'""as us ed for pasture , 42 perce n t for hay , ' 1 per cent for corn

and oats for si lage or odder, 21 per c ent for c e redls, whereas

the rema i ning 6 percent was used for othe r cro p s or was l ef t

idle . This reldtively la l-ge land base and tIll S larye

proportion of land used f or fee d crops show that dairy farming

in the U.S . and in Cana da is heav i l y dep~nde n t on home -gr own

feed and on :a nd. Nond the les s , the long-run trend in som e

reg:ons or the U.S. h s been to ward l e ss d e p e nd e nce on la nd.

Par~icularly large s~dle [arms in Fl o rida , sou ~ he rn Texas,

Arizon dnd California often pur c hdse all o r most o f the feed

requirement , c ncenLr tes as we ll as fu r age ( '18 ).

- 28 -

Table 14.--Cattle on Dairy Farms, United States, 1974

Head Per Farm

Milk cows 48

Milk heifers and heifer calves 24

Beef cows 3

Beef heifers and heifer calves 3

Steers, steer calves, bulls, and bull calves 10

Total number of head 88

SOURCE: See footnote to Table 10.

Table 15.--Utilization of Land on Dairy Farms, United States, 1974

Cropland pasture

Hay

Corn for silage or fodder

Sorghum for silage or fodder

Other fodder cropsa

Cereals for grain or seed

Other crops

Cropland, not harvested or pastured

Total cropland

Woodland pasture

Rangeland pasture

Total agricultural land

Other land

Total land in farms

SOURCE: See footnote to Table 10.

Acres

38

60

22

1

12

33

7

7

180

19

37

236

40

276

arncludes some crops other than fodder crops.

Percent of Total Cropland

21

33

12

1

6

19

4

4

100

- 2 9 -

Table~ . - -Cattle on Dairy Fa r ms , Can~da , 1 97 6

Cows and he i fers , : yea rs a nd over , mi 1kins or 0 be mi l ked

other cattle

To l al number of head

SIJURCE : See footno t e to Table n .

Head Per Farm

35

29

(; 4

Tablej 7 . -- ~ til ization of Land on Dair y Fa rm s, Canada , 197 6

Improved pasture

Tame hay

Corn for s~la:je

Oats for s':'lage

or :oc.l·ler

or [odJer

}\cr s

34

7 4

14 ,. .)

Olher fodJer crops 2

Cereals for grains or seen 38

Other cro~s 1

Impro ed Ian , not harllesteG or pa stured 8

To al improve(l lanl 176

Unimproveu land 86

Tota l _and in farms

SOURCE: ee foolno e to 'I'abl e 13 .

Pe rc e nt of tota l improved l and

20

42

8

3

1

21

1

4

1 00

- 30 -

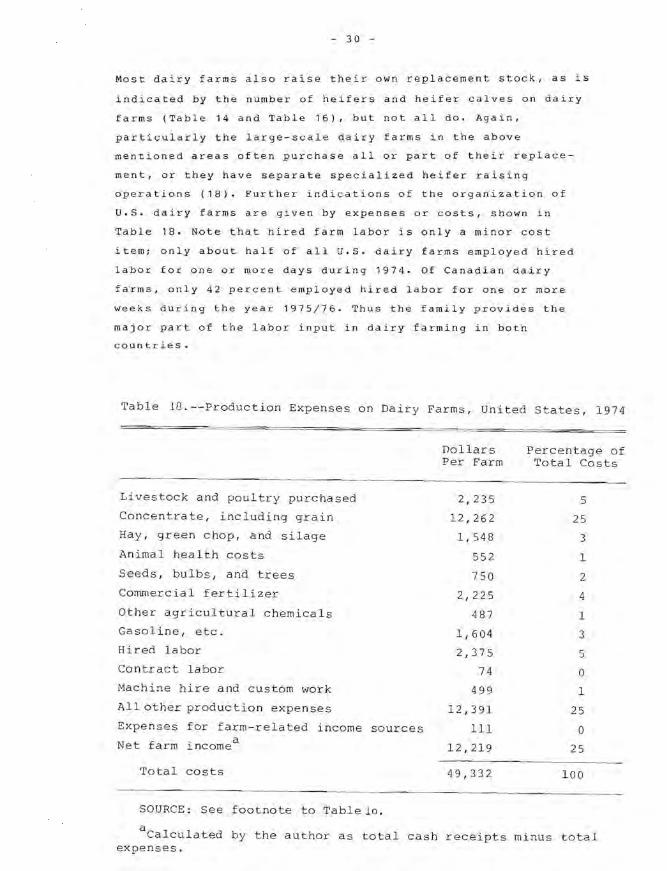

Most dairy farms also raise their own replacement stoc k, as is

indicated by the number of heifers and heifer calves on dairy

farms (Table 14 and Table 16), but not all do. Again,

particularly the large-scale dairy farms in the above

mentioned areas often purchase all or part of their replace

ment, or they have separate specialized heifer raising

operations (18). Further indications of the organization of

U.S. dairy farms are given by expenses or costs, shown in

Table 18. Note that hired farm labor is only a minor cost

item; only about half of all U.S. dairy farms employed hired

labor for one or more days during 1974. Of Canadian dairy

farms, only 42 percent employed hired labor for one or more

weeks during the year 1975/76. Thus the family provides the

major part of the labor input in dairy farming in both

countries.

Table IG.--Production Expenses on Dairy Farms, United States, 1974

Livestock and poultry purchased

Concentrate, including grain

Hay, green chop, and silage

Animal health costs

Seeds, bulbs, and trees

Commercial fertilizer

Other agricultural chemicals

Gasoline, etc.

Hired labor

Contract labor

Machine hire and custom work

All other production expenses

Expenses for farm-related income sources

Net farm . a lncome

Total costs

SOURCE: See footnote to Table 10.

Dollars Per Farm

2,235

12,262

1,548

552

750

2,225

487

1,604

2,375

74

499

12,391

III

12,219

49,332

Percentage of Total Costs

5

25

3

1

2

4

1

3

5

o 1

25

o 25

100

aCalculated by the author as total cash receipts minus total expenses.

3 1

In conclusion , most U.S. a nd Canadia n dai r y f arm s still are

characte l ized by a h~gh degr~e of a ss et f ix it y . Thi s is due t o

the fact that th~ maJority are family e n te rpr i ses and that

they are heavily dependent on land . Also , uti l i zation o f

special1zed equipment and bu i ld i ngs contributes to a high

degree of clsset fixity.

The extent to WhLCh th~ va~ ' ous resour c e s be c ome f ixed in agri

culture is affected not o n l y by fac tors wi t hin a g r iculture but

also by faclo~s o u ts1de agricult u re . Thus t he out migration of

labor from U.S . and Canadia n agricul t u re has been facilitated

up to the early 1970 -s by a prolonged period ot ra p id economi c

gtowth and l ow leve l s of unemployment. Farm la n d , in contr ast

to l abor, has had limited alternative us e ou t side agriculture,

and land , therefore, has tended to be the mo s t s La b le factor in

agr1cultur~. Only when ~conom i c condi t ion s have d e te riorated

sufficienLly to reduce the marginal v alue of land t o zero, has

land been removed from prOd uc tion . Th is ha~ happen e d in the

Northeast , one of the major dair y rdgio ns in t h e U.S. In this

region land us d for cro9s d e clined fro m a pe a k ot 21 milli on

"cres in 19~4 to a low of 12 mi l l i o n acr eS in 1969 (3 3) .

2.5. T~chnoloyy and productivity

Technological improvements in f~rming may be de f i ned as those

Changes In the produ~tion functi on for i ndividua l farms that

r~sult 1n a better Lerm of trans f ormation. Tec h no Lo gic a l

impl"OVem nts, so deflned, hav e thr",,,, important iml' a cts on

production and resource use . F i rst , t hey re sult 1 n an

increase i n total produl:tivlty, as meas u red by th e ratio

of tota l output Lo total lnput. By incre as i ng t ot a l productivity,

technological lmprovemenls lo wer unit costs of p r od uctio n.

Second, technolo<jicc intpl"OV ement.-; may change (or lea ve

unchanged) the tdtes of subst i tut ion amon y input s an d, 1n so

doln they atf~ct the op~im~l combin at i on o f i np u t s . Th ird.

=echnological 1mprovements may di rec t ( o r leave u na f fected)

the economies ot sc 1 ". BeCdU>it! of til .. t vlO last me ntioned

lmpacts , different technO l ogical improvemenc s in facm i ng often

32

have quite different implications on the organization and the

structure of farming. This seems to have been the case in

dairy farming.

Two important categories of technological improvements adopted

in dairy farming in past decades are new types of deadstock,

such as buildings and equipment, and genetic improvements of

dairy cattle. The adoption of new buildings and equipment has

without doubt tended to increase the rate at which capital

substitutes for labor and, in so doing, has stimulated a

substitution of capital for labor. Furthermore, new buildings

and equipment have tended to increase the economies of scale

by reducing unit costs more on larger farms than on smaller

ones. These technological improvements, therefore, have

stimulated individual farmers to expand production. The

improvements of dairy cattle breeds, by contrast, have left

the substitution rates unchanged, by and large, and likewise,

have not affected the economies of scale.

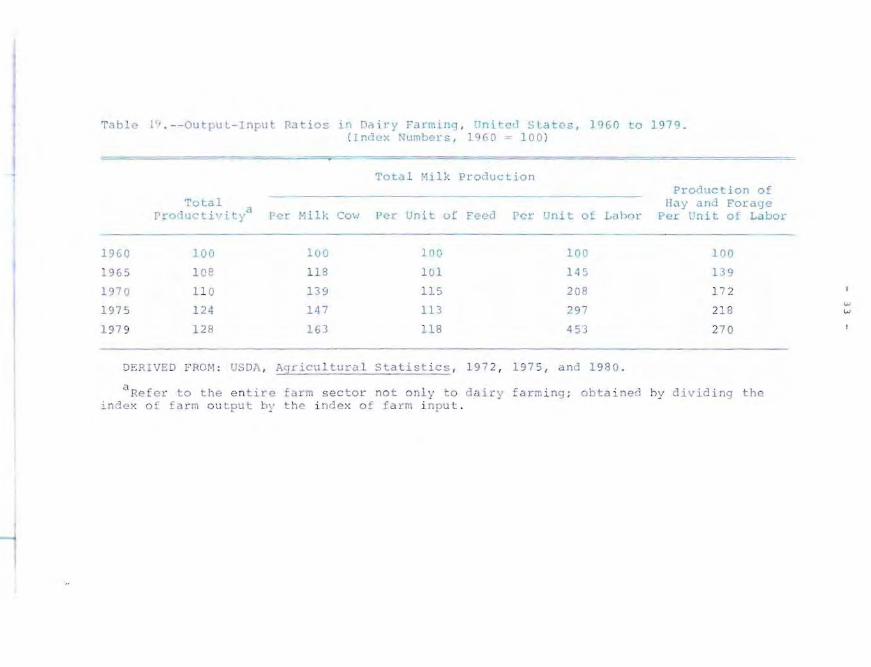

An indication of the impacts of technological improvements is

provided by the increase in the various productivities or out

put-input ratios (Table 19). The increase in such producti

vities in U.S. dairy farming from 1960 to 1979 was as follows

(Table 19): Total product~vity (not in the dairy sector alone

but in the entire farm sector), 28 percent; milk yield per

cow, 63 percent (from 7,029 to 11,471 pounds); milk production

per unit of feed, 18 percent; milk production per hour of

labor input, 353 percent; and forage production per unit of

labor input, 170 percent.

the same level in 1979 as

Since U.S. milk production was at

in 1960, these changes directly

reflect declines in the amount of resources use in dairy

farming. These declines in resource use were as follows:

number of milk cows, 38 percent (from 17.5 million in 1960 to

10.8 million in 1979); amount of feed, 15 percent, hours of

labor used in the dairy sector, 78 percent.

In Canada milk yield per cow increased from 5.986 pounds in

Table l ~ . --Outpul-Input Ratios in ~Hiry Farming, Unitc~ SLates, 1960 to 1979. (Index Numbers, l0G O = 100 )

Total Milk Production Production of

Total l1ilY and Forage Pro,luc tivi tya [er [-lill;. Co ... .' per Un i 1: uf F,aed Per UniL ot Lahor Per .1ni t of Labor

- - -1960 100 1uO lOCo 1riO 100

1965 lC8 118 l UI 145 139

1970 11 0 139 115 208 172

1975 1 24 147 113 297 218

197 9 128 163 118 453 270

D~RIVED FROM : USDA , Agricultural statistic s , 197 2 , 1975, and 1980 .

8Re f e r 1..0 t ile e n tire farm sector not onl y to dai r y f arm i ng ; obtaine':] hy l1i vid ing the index of fa rm oU Lput by the i ndex o f [ a rm i nput .

w w

34 -

1960 to 8.650 pounds in 1979 or by 45 percent~) while the

number of cows declined from 2.96 million to 1.97 million.

(Other data on productivity in the Canadian dairy sector are

not readily available).

Thus the productivity in u.s. dairy farming has increased

substantially during the last two decades. Total resource use

has declined, and the resource mix has changed. These changes

shows that U.S. dairy farming to a large extent has been able

to adjust production and resource use to new technologies as

well as to changes in relative prices.

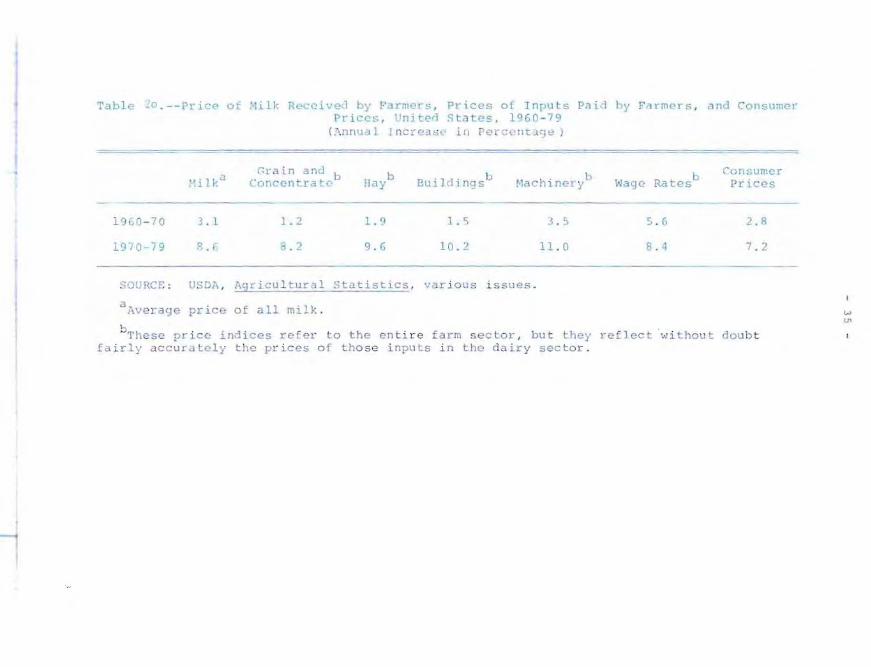

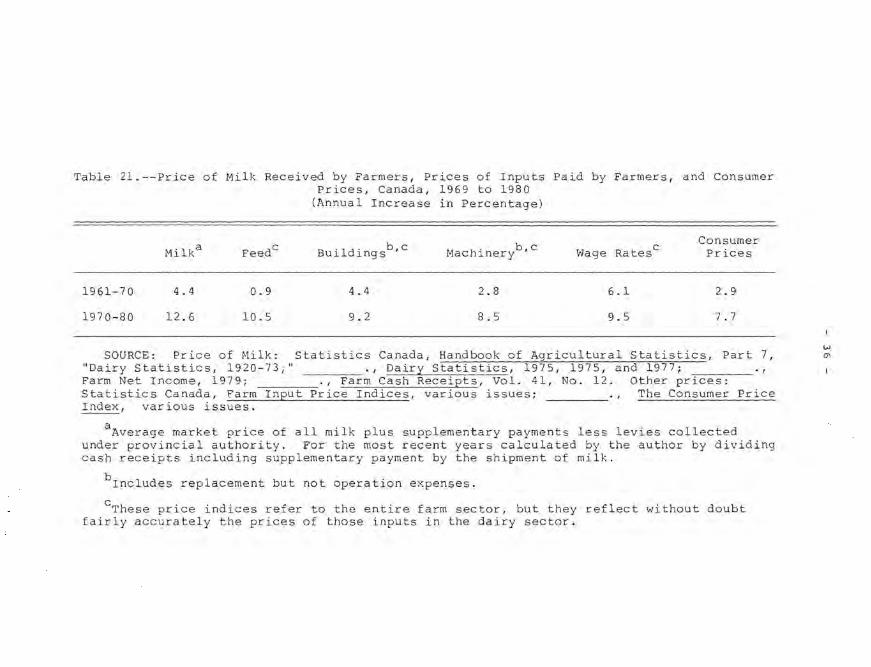

2.6. Trends in prices of milk and in prices of resources

The price received by U.S. and Canadian farmers for milk

increased more than did the general price level in the sixties

and in the seventies (Table 20 and Table 21). Thus in the

United States the increase in the price of milk averaged 3.1

percent annually in the sixties and 8.6 percent annually in

the seventies compared to an inflation rate of 2.8 and 7.2

percent, respectively, measured by the consumer price index.

In Canada, the milk price increase averaged 4.4 percent in the

sixties and 12.6 percent in the seventies compared to an infla

tion rate of 2.9 and 7.7 percent, respectively.

Also prices of input used in dairy farming have changed

considerably in the last two decades (Table 20 and Table 21).

In the sixties the wage rates increased more whereas the price

of most capital inputs increased less than did the general

price level. As a result labor became more expensive relative

to capital. In the seventies the price increase for all major

groups of inputs exceeded the rate of inflation, as measured

by the consumer price index, but the relative prices of inputs

remained remarkably stable apart from year-to-year fluctuation

and apart from an increase in relative energy prices.

4) These figures for yield per cow underestimate the true yield, as the number of milk cows includes heifers two years or older not yet fresh.

Table LO .--Prlc(> oi :-li11, Re..:clved by f'arnl'~ls , Pl' ices at Inpu t s Pilid by Farmel-s . <'I nd Consumer PricQs, Unjt0~ Sta t es . l Q60-7g

( 7I.nlllla 1 J nce(!::!;;, .. ill Perc(1llt.),)e )

rHlki:l

1 % 0-70 3 . 1

1970-79 RJ

SOt'RCE : USDA ,

(~l·ain 3 ncl b C:oncen tra t.-

1.2

B. 2

b lIiJY

1.9

Cl . G

Ag r i cu l tu r al Stat i stics ,

aAvera ge pr i c e o f a l l milk .

·1 1· b Bu~ (.:1 ngs b

~1 il c lnnery

1.'i 5 . S

1 0 . 2 1 1. 0

var i ou s i s sue s ,

b \"l ag("~ Rates

5 . 6

3 . 4

r- n ll~umc)"

Prices

2.8

7 . 2

bThese pr ic D i ndices refer to t he en ti r e f a rm s e c tor . b u t they refle ct wi thou t d o u b t fa i r l y acc u r~tely t he p r i c e s o f Lha se inp u t s i n the da i r y sector,

W IJ'

Table 21.--Price of Milk Received by Farmers, Prices of Inputs Paid by Farmers, and Consumer Prices, Canada, 1969 to 1980

Hilka Feedc

1961-70 4.4 0.9

1970-80 12.6 10.5

(Annual Increase in Percentage)

'ld' b,c BUl lngs

4.4

9.2

h ' b,c Mac lnery

2.8

8.5

Wage RatesC

6.1

9.5

Consumer Prices

2.9

7.7

w SOURCE: Price of Milk: Statistics Canada, Handbook of Agricultural Statistics, Part 7, ~

"Dairy Statistics, 1920-73;" ., Dairy Statistics, 1975, 1975, and 1977;_ Farm Net Income, 1979; ., Farm Cash Receipts, Vol. 41, No. 12. Other prices: Statistics Canada, Farm Input Price Indices, various issues; The Consumer Price Index, various issues.

aAverage market price of all milk plus supplementary payments less levies collected under provincial authority. For the most recent years calculated by the author by dividing cash receipts including supplementary payment by the shipment of milk.

bIncludes replacement but not operation expenses.

cThese price indices refer to the entire farm sector, but they reflect without doubt fairly accurately the prices of those inputs in the dairy sector.

- 37 -

The increase in the relat~ve p r ~ce of l abo e in th e sixties has

wi th o ut do ub t been an Lmpor t a n t facto r i n sti mulati n g farmers

to s u bst i tute cap Ltal for l abor . Bu t thi s mo t i v a t i o n t o chang e

t he reso u cce mix h a s b een dec l i ning dS th e rel a t i v e pri c es

have rema in ed more s ta b lcl s i nce th e e ar ly seve nt i e s .

Neverthe l e s s , su b st it u t on o f c a pita l for lcb o r in d a i r y

far mi n9 has t ake n place al so d ur i~g t h e s even t i e s . Th is sub

stit u tion may b e exp l ained p art l y by the fa c t t h a t new t e c h

nolo9i~s COn t i n Ue to be de v el op e d and p a r tl y b y t h e f a ct that

substit u ti o n occ ur s w i th a tlme- l ag b e cause of t h e exi s te n c e

of fi x ed a S S<l t s .

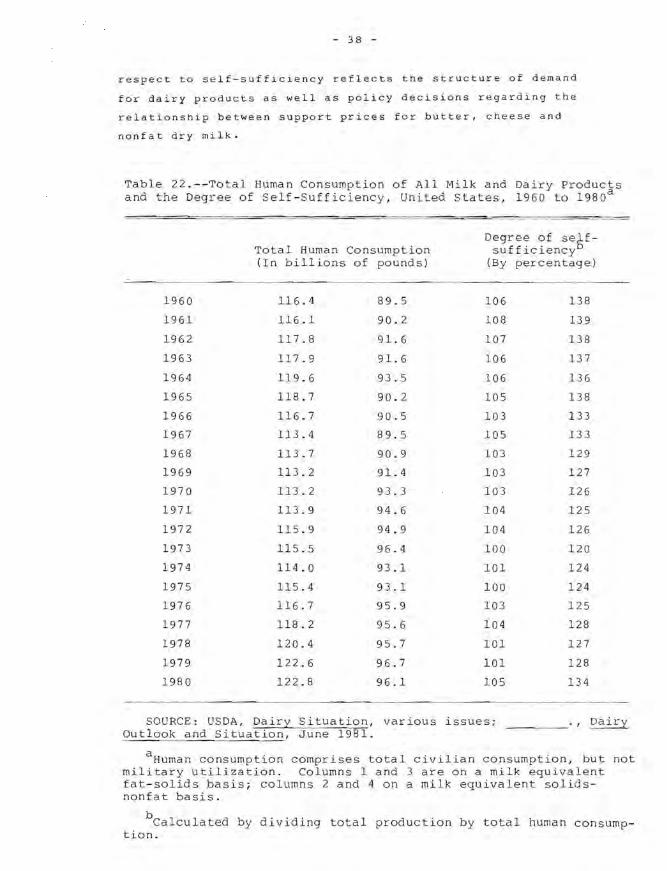

3 . Pd tte r ns and Tre nd s i n Dairy P r oduct Co n s u mp ti o n.

During the last tw o de c ade s , total co ns u mp t i o n of a ll milk

an d dair y p ro d uc t s i n the Un i t ed State s and 1 n Ca na d a h a s

1 n c r eased o nl y sl ig h t l y . On a milk eqUivale n t fat c o nt ent

basis , the Lncreas~ ~ ~ tota l U. S . c o n s umpt i on wa s 5.5 pe r ce n t

fro m 11 6 . 4 b il li o n poun ds i.n 19 6 0 t o 1 2 2 . 8 b i l li o n p o unds in

1980 . On a mi lk e qu1val~nt s ol ids-nonfat basi s , th e incr e as e

wa s 7 . 4 pel:cent - fro m 89 . 5 t o 9 6 . 1 mill i on poun d s (Tabl e 22)

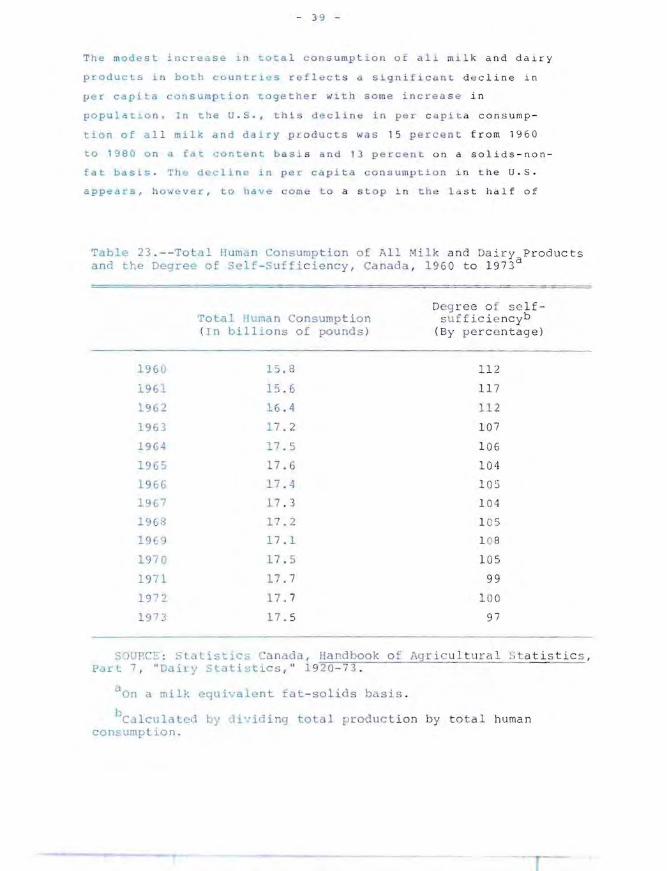

In Canada to t a l cons u mpti o n o n a mi l k eqUi v a len t fat c o ntent

bas i s . I nc re a sed f r om 15 . 8 b i l l i on pound s i n 196 0 t o 1 . 5

b il l ion pou nd s in 1 973 or b y 1 0.7 per ce n t ( Tabl e 2 3 ).

The degree of self - suft i cie ncy , def i ned as t ot d l pr o du c ti o n

div:ded by t OLa l hu man co n s u mp tion , h 5 v a rie d S i gn ifi c antl y

S.l.nce 196U in b oth COUll r i cs ( Tab l e 2 2 an d Tab l e 2 3 ) - in the

U.S., f ro m a lo w ':>( <lbo u t 10 0 p e rcent in 19 7 3 - 75 , o n a fat

conc"n t basis , lQ high of a bo u t 10 6 to l UB pe r c e n t in the

early s i x t i es i n Canada, f r o m a l ow of ~7 perce n t in 1 9 7 3 to

a h i gh of , 17 p~rc",n in 19 6 1. The low d e g r e e o f se lf-

suffiC i ency i n the mid-se v en t ie s i n b OLh coun Lr i e s was c a u s e d

by ~ .l e clin e in mt lk p ro duct ion brou g h t abo u t by h i g h d o mest1c

feed p r i ces r ",f Lec t in'1 t-e mpo r ar y short a ges o f g ra i n d n d o il

seed on t il': wor l d mdrk"t . Th e d gre." o f s el f -s uf .i c i ", n c y f o r

so 1 1os - no n id t 1S consiJera bly high e r tha n t hat f o r milk fat ~n

bot h (; oun Lr l..es (for U . S . s ee 'r d b le 2 2 ) . T h i s d i f fer e n c e wl.th

- 38 -

respect to self-sufficiency ref~ects the structure of demand

for dairy products as well as policy decisions regarding the

relationship between support prices for butter, cheese and

nonfat dry milk.

Table 22.--Total Human Consumption of All Milk and Dairy Products and the Degree of Self-Sufficiency, United States, 1960 to 1980 a

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1 975

1976

1977

1978

1979

1980

Total Human Consumption (In billions of pounds)

116.4

116.1

117.8

117.9

119.6

118.7

116.7

113.4

113.7

113.2

113.2

113.9

115.9

115.5

114.0

115.4

116.7

118.2

120.4

122.6

122.8

89.5

90.2

91.6

91.6

93.5

90.2

90 .5

89 . 5

90.9

91. 4

93.3

94.6

94 . 9

96 .4

93.1

93.1

95.9

95.6

95.7

96.7

96.1

Degree of seSfsufficiency

(By percentage)

106

108

107

106

106

105

103

105

10 3

103

103

104

104

100

101

100

103

104

101

101

105

138

139

138

137

136

138

133

133

129

127

126

125

126

120

124

124

125

128

127

128

134

SOURCE : USDA, Dairy Situation , various issues; Out look and Situation , June 1981.

_____ ., Dairy

aHuman consumption comprises total civilian consumption , but not military utilization. Columns 1 and 3 are on a milk equivalent fat-solids basis; columns 2 and 4 on a milk equivalent solidsnonfat basis.

bcalculated by dividing total production by total human consumption.

- 3 9 -

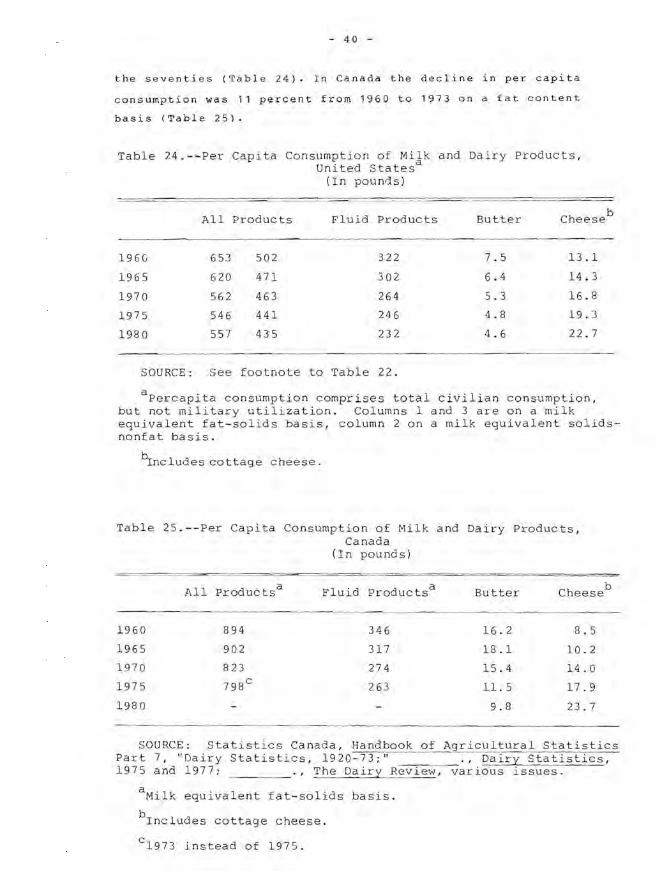

The mode s t i n crea s e 1 n tota l consu mp t i on of all mil k and dairy

prod u c t s ~n both cD u ntries r e fl e c t s a si gni f ic ant d e cline in

per ca pit a c onsu mp t i on toget he r with some i n cr e ase in

populatio n . 1n the U. S .• t h i d e cline i n per c api t a consump-

t~c n of a l l mil k a n d d a ~r y pr o ducts was 1 5 percen t from 1960

to 1 9 8 8 on a fat conte n t ba s i s a n d 13 p e rc e nt un a solids-non

fa t basi s . The dec l i n e in pe r cap i ta co nsu mpt i on in th e U.S.

apPdars . h o we v er , t o have c o me to a s top in the l a st half of

Table 23 . --To t a 1 Human Con sump tion o [ .1\11 1ilk and Dai r y Products a nd the Degree of ~e1[-Suffic i e ncy , Canada , 19 60 to 1 973 a

Deg ree o f sc1f-Total Huma n Co nsumptio n s u ff icie ncyb ( Tn b il L10 n s of pou nds ) (By p erc e ntage)

1960 lS . R 112

1961 15 . 6 117

1962 1 6 . 4 11 2

1963 1 7 .2 107

1%4 17 . 5 1 06

1965 17 .6 104

1 9 66 17 . 4 105

19 ( 7 17 . 3 1 0 4

1%8 17 . 2 1 0 5

19 ·9 1 7. 1 1 0 8

1970 1 7 . 5 105

1 <) 71 1 7. 7 99

1 ')"1 2 17. 7 l llO

1973 17 . 5 97

Sl)[JPCF: staListic .,; Ca nada , Handb ook o f Al;j r i c u l t Part 7 , " Daily SLatistlcS ,· 19 20-7 3 .

a OD a milk eqUivalen t fat-so lids ba s i s .

I-J Cu iculaLc:rl by Ji ' l di ng t o t a l produc t ion by t o t al human

consump L~o n.

- 40 -

the seventies (Table 24). In Canada the decline in per capita

consumption was 11 percent from 1960 to 1973 on a fat content

basis (Table 25).

Table 24.--Per Capita Consumption of Milk and Dairy Products, United Statesa

(In pounds)

All Products Fluid Products Butter Cheese b

1960 653 502 322 7.5 13 .1

1965 620 471 302 6.4 14.3

1970 562 463 264 5.3 16.8

1975 546 441 246 4.8 19.3

1980 557 435 232 4.6 22.7

SOURCE: See footnote to Table 22.

apercapita consumption comprises total civilian consumption, but not military utilization. Columns 1 and 3 are on a milk equivalent fat-solids basis, column 2 on a milk equivalent solidsnonfat basis.

b Includes cottage cheese.

Table 25.--Per Capita Consumption of Milk and Dairy Products, Canada

(In pounds)

All Productsa Fluid Productsa Butter Cheese

1960 894 346 16.2 8.5

1965 902 317 18.1 10.2

1970 823 274 15.4 14.0

1975 798 c 263 ll. 5 17.9

1980 9.8 23.7

b

SOURCE: Statistics Canada, Handbook of Agricultural Statistics Part 7, "Dairy Statistics, 1920-73;" ., Dairy Statistics, 1975 and 1977; ., The Dairy Review, various issues.

a Milk equivalent fat-solids basis.

b Includes cottage cheese.

c 1973 instead of 1975.

- 4 1 -

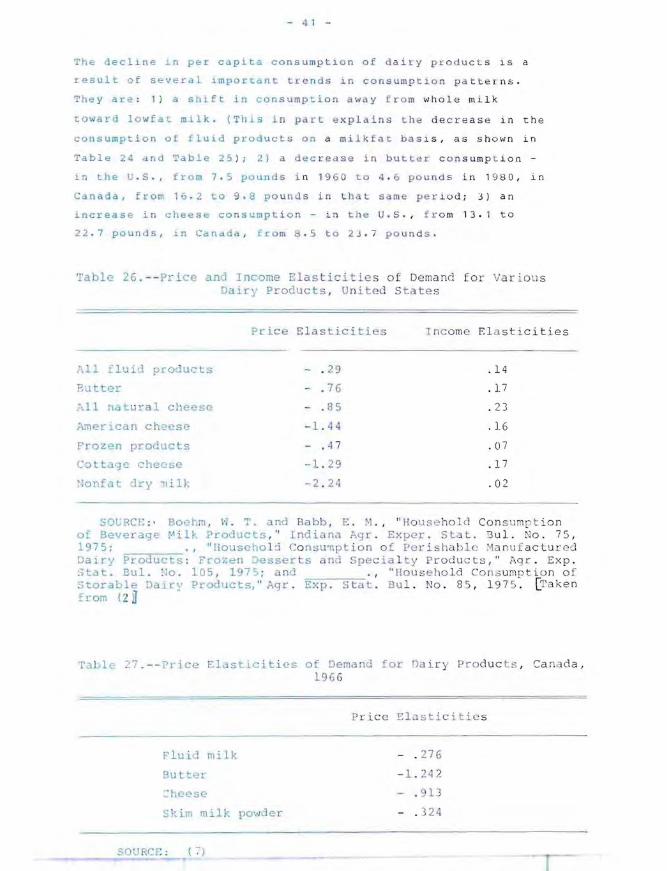

Th& dec l ~ne ~n per c apita consumpt~ o n of d a i ~y pr o du c L s is a

result of sev~ral LmpOr~ant Lr en d s ~ n con sump t i o n p a t t e r ns .

They ar,, ; 1 ) a shift in consumpt iol) a\< a y f r o m \-Ih o l e milk

t:Qward lowE 1.: milk . (This i n part e xp l a in s t h e dec r e a se ~n t he

consumption of flu i d product s on a milk far ba s ls , as s h o wn in

Table 24 nd Table 25 ) ; 2} a dec re a s e in b u t t e r c on s u mp t io n -

i n the u . S . , from 7 . 5 pOLlnds i n 19 6 0 t.o 4 . 6 p ound s in 1 98 0 , in

Canada, from 11; . 2 to 9 . 8 po u n tl s i n t hat: sa me pe r i o d; 3) an

increase in cheese co n sumpt. i o n - i n t.he U.S . , fr o m 1 3 . 1 t o

22 . 7 pounds, in C.,nd'a , from 8 . 5 t o 23 .7 po u n d s .

Tahlc 2fi .--Price an' Income Elas t i c i t ie s of Demand for '/ ar- i o ll S Dairy ProJucts , Un iteJ s t a t e s

Price El a s ticit i e s I nCome El a stic iti es

All fluiu proaucts

Butter

,:',11 n .... tural cheese

Arner 1 _an ch~ese

Frozen l.roducts

Coltage cheese

:Ionfa t '1ry lId):

- . 2 9

- . 76

- . 85

- 1. 44

- , 4 7

- 1 . 29

- 2 . 2'1

.1 4

. 17

. 23

. 16

,07

.1 7

. 02

SOl;RCr: : , Boe"m , 1-1, T, and Ba bb, E . ~ . , " Hous e ho ld Con s u mp t i o n of Beveraq_ ~ ill ?roducts ," India n Cl .l>'lr . Exper , S Lat. DuL 0 , 7 5 , 1975; ., "Househo l d COnsu'llption o f Per i sha hl' .'4anu f ac t u !:0Cl Dairy ProJuc s ; Frozen )esser t s and Specia l t y prod uc t s, " Agr . Ex p. Stilt. Bul . 110 . 105 , 1975 ; and . , "Ho use ho ld Cot1 s u mp t i o n of' S .. orable DcHJ:'y Ploollcts," Agr . Exp . Stat . BU _ . !\lo . 8 5 , 1 97 5 . [Ta k en from ! 2 il

TaJ 1e ~7 . --I'l-ic Elasticiti es of Demand for Da i r y Pr o duc t5 , Ca n d a, 196 6

P ric e E lastic it i e s

flui mi.1 k - , 2 76

- 1. 2 4 2

'!10ese - . 9 13

Skim milk powder - . 324

_____ --_30U ReF. : ( -:-)

- 42 -

These rather substantial changes in per capita consumption are

caused mainly by changes in consumer tastes and preferences.

Nevertheless, prices of dairy products and of dairy product

substitutes as well as per capita income affect consumption of

dairy products. Furthermore, the effects of dairy product

prices on consumption are of special interest in relation to

government support programs, as product prices are important

decision variables in those programs.

The response in consumption to change in price and income

varies among dairy products, as shown in Table 26 and Table

27. In the u.s. the price elasticity of demand is about -.3

for all fluid products, -.8 for butter, and -1.4 for American

cheese. In Canada the price elasticity is about -.3 for fluid

milk, -1.2 for butter and -.9 for cheese. Thus, in both

countries consumption of fluid milk or fluid products responds

less to price changes than does consumption of butter or

cheese. The response in consumption to change in income is

quite low for all dairy products (Table 26).

A . UNITED ST AT ES

- 43 -

P A R1' I I

DAI RY PRIC E P O LI ~I E S I N THE

UNITE D STATE S AND C ANA DA

The r e ate two main sector s ~n t h e U. S . dairy i ndus try - the

fl u i d ml lk sector and the m a nu f actu r ~ng milk s e c t o r alt hough

s o m ~ ~rossover o ccurs betwee n t hese t wo sector s . The market

for fluid mil k 1S supplied on l y by produc e rs of fl uid grade

milk . The market fOl mi l k u se d for ma nuf act ur e d pr od u c t s .

ma~nly b u tter . cheese an d no nf at dry mi l k , ho we ve r . is s up

p l ied partly by manufactu ring mi lk p r oducer s nd partl y by

exce s s production from fluid mi l k pr o d uc e rs .

The l wa sectors O L ra t ber gr ade s o f mi l k a r e r g Ul a t e d or

supported by separate pr og ra ms . They ar e: 1 1 Th e price support

prog ram . w'1ch p laces a f loo r u nder the pric e of manufacturlng

m1 1 k thro u gh otfer~ of p urch a sin g ma nu f ac t ure d d a i r y products

at pre-det~r mined pricQs. 2 ) The mi l k mark e t i ng order program,

which establ i shes mi nim um price s for f lui d gr ade milk

de p e n d i ng on whecher the mi l k i s us e d for f l u i d p r oduc t s o r is

dive r ted i nto manufactur Ln g use . Bot h thes e supp o r t p ro grams

origillated oU L of the c1e pr es s ed ;,co nomy in t h e 1930s , and the y

have cont i nued in mod~fie d forms up t o t he p r e s e nt .

Othe r pr o gra ms closely re l at e d to d a iry p ric e po l l c i es are

imporL restrictions , exp o rt p r og ra ms, and d o me s tic food

programs . I mpor t restrIct i o n s an d e x por t p r o gr dms are required

s i nce the prlce support p l o gr a m ma i n t a in s d o me st ic prices of

manufact u red dairy proiuct s a b o v e wo r l d mar k ~ t prlces.

Domestlc fao e! programs serve a s outlet s f or purchds e s made

under the prlce sur port program a n d , to so me ~ xte n t. also f o r

cu r re n t productJ.on. Th i s .n~ po l: t, h o we ver , f OCU5 (' S primarily o n

the price support progra m ~ nd t he mil k ma rke t iny o rct uL

progra m.

- 44 -

4. Price Support of Manufacturing Milk

4.1. Objectives, pricing, and operation

The price support program is authorized by the Agricultural

Act of 1949, as amended. This Act (in its permanent form) di

rects the Secretary of Agriculture to support the price of

milk at a level between 75 and 90 percent of the parity priceS)

as he "determines necessary in order to assure an adequate

supply of pure and wholesome milk to meet current needs,

reflect changes in the cost of production, and assure a level

of farm income adequate to maintain production capacity

sufficient to meet future needs".

The support of the milk price is provided through purchase of

manufactured dairy products. The Secretary of Agriculture

announces, before the beginning of each marketing year, the

support price of manufacturing quality milk. He also announces

the prices at which the Government is ready to purchase

manufactured products. The support level for milk, as measured

in percentage of parity, may be raised during the year, but

not lowered.

5) The parity concept, as used in U.S. agricultural policy, evolved early in this century as a standard of fairness and equity for farmers. Originally, the parity price of a product was defined as that price which would give a unit of the product the same purchasing power with respect to goods and services farmers buy as this unit had in the base period, i.e., the period 1910-14. Actually, the parity price was calculated by multiplying the base price o f the product by the parity index. In this context, the base price is the price received by farmers in 1910-14, and the parity index is a price index for goods and services farmers use in farm production and in living.

This original parity formula did not take into account differences among products with respect to changes in supply and demand over time. In an attempt to overcome this limitation, a new formula was develoved around 1950. In this new formula, the base price is replaced by an adjusted base price. This implies that the new formula takes into account differences among products with respect to changes in demand and supply since the base period to the extent that these differences are reflected in the average market prices in the most recent ten-year period. Thus, some long-term trends in relative demand and supply are accounted for, whereas short-term changes or fluctuations are not (40).

- 45 -

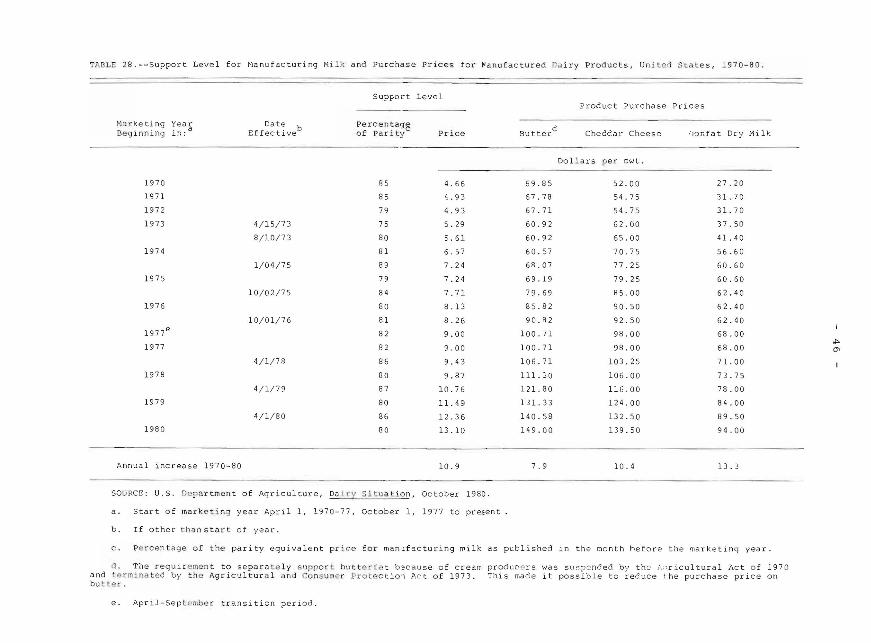

Tb~ Food and Agricultural Act of 19 7 7 p ro vL d es f ur ther t hat

th~ suppor t price of milk in d o llar s b e ad ju s te d du ri ng the

marke t 1ng year to reflect chan g e s Ln t he par i LY in~ x, i.e.

the 1ndex a! pr1ces pa1d b y farmers . This adj u s tm e nt take s

place at the midpoin of the marketi n g y e ar and if cha n ges in

the 1ndex are substanLicll also . a l t h y b e gi nni ng of th e se cond

and fourLh quarters.

The prevd~Ling support level , i n per c e n t o f par i t y . has changed

substantially and frequent ly . wit h i n t h e ra n ge set by t he

basJ.c leg i s ation (Tabl '" 2S). These changes alee Lh e r ' s u lt of

e1ther administrdtiv e dtC1s i ons or legis lative ae l i on . Thu s

congr~ss has rais~ Lhe minim u m l~gd l s up p o r t l e ve l of 75

percenL i n The baslc legislation to 80 p erc e nt sev e ra l tim e s

last 1n September 1977 , ",no Cortgress hds extt'nded t h e 80

percent minimum from 1979 to 1 9S 1 ( g , 21 ) .

Dur ' oy the ast decade. the suppor t pr i ce of mi lk in dol Lars

has increased su b stanLLdlly. eVe n af t er allowanc t' s are made

for in f l ation . Thus tile support pr i ce i n c re asc:d , all an

average , 1 0.9 percent annua l ly f rom 19 70 to 1~ I:l O (Tab le 2l:l)

compared with dn i nfla 1 0n rate of 7 . 2 p e rcent ( me asu red by

t he Consumer Pr~ce I n de:<) . 'rh e correspo n d i ng a l n u a l i nc reas es

In the ofEer-to - pur c hds~ p r ic e s were as f 11 0 ws (Tab l e 28)

fOl' but t er , 7.9 p er ... ent; Ear cheddar chee s e , 10 . 4 perce n t ; an d

for nonfat ~ry milk. 1J.3 percent . These 1 n cre a ses in pU le c hase

pr1ces taken togeth~r cor r espo n d . b y and large . t o the

lnCL'ease in the SUppO!:T plicO;! of mi l k . The d if te Le nc es am ong

Lhese c teS o[ pricd increases r e flect a sh i ft 1n the burden

of support1ng m11k way from b utto:!t:fdt t o wa L' d s >:io l ids Ilo n f ctt.

u overnment purchases of mdnufac tu red da i ry pr o d u ct s un der

the pr l ce supporl ptOyrdm a l e Carrie d out b y r ho Co mmo di ty

Credil Corporation (CCC) . The ce e offers to purchds e m ~ inl y

buLter , ch~dddr chees~. and nonf t dry mi l k to prev e n t the

f~rm price of m11k from f l11n9 below the support p~ i ce level.

Th e prices at \,hiclt tne ec c oLters to pur-chase ma n ufac !: ured

products are aes1gnud to enable m n u fac t u r e ~ s to P d y tho:!

supporL prLce to ploJu ~o:! rs of manufacL uL i y ffi 1 1 k , Wl e t he r o~

~AnLE 2B. -- Support Level for Manufacturing Mi lk and Purchase Prices f or ~anufactured Da i ry Pr oducts , Un ited States, 19 70-BO.

Suppor t Level Procuct Purchase Prices

"'jar:~et~n g ~ea~ Date b Percentage: d Be g l nn lng 1n: Effective o f Parity Price Butter Checdar Cheese 'J"":)nfa t Dry Mi l k

Dollar s pe< cwt .

19 70 85 4.66 69.8 5 52.00 27.20

1971 85 4. 93 67.78 54 .75 31 .70

1972 79 4.93 67.7 1 54 . 75 3 1. 70

1973 4/1 5/73 75 5 . 29 60.92 62 . 00 37.50

8/10/7 3 80 5. 61 60.9 2 65.00 41. 40

1974 8 1 6.57 60.57 70.75 56 . 60

1/04/75 89 7 . 24 6R . 07 77.25 60.6 0

1975 79 7.24 69 .19 79.25 60.60

1 0/02/75 84 7.71 79 . 69 85.00 62.4 0

1976 80 8.13 85.82 90.50 62.40

10/0 1/76 81 8.26 90 .R2 92 .50 62.40

1 97 7e 82 9.00 100.71 98.00 68.00

1977 82 9.00 10 0.7 1 98. 00 68.00

4/1/78 8 6 9 . 43 106.71 103.2 5 7 1. 00

197 8 80 9 .87 111.30 106.00 73.75

4/1/ 79 87 1 0 .7 6 121. 80 116. 00 78.00

19 79 80 11. 49 131. 33 124 . 00 84 .0 0

4/1 /80 86 12.36 14 0.5 8 13 2 . 50 89.50

1980 80 13 .10 149 .00 139.50 94.00

Annua l increase 1970-80 10.9 7.9 10. 4 13.3

SOURCE: U. S. De :''':l artment of Aqr i cu l ture, Da i ry S i tua tion, October 1980 .

a . Start of mark e ting year April 1, 1970-77, October I, 1977 to present

b . If other th~ ns tar t o f year.

c. P0 rcen t age of the parity equivalent pr ice f or man~facturing milk as publ ished in the ao nth hefore the mark eting year.

Th e requ irement to separa te ly s uppo c t b!ltterfa t b~cause of cream producers was s u~ p c nded by the ~ !; ricultural Act of 19 70 and t ermina t e d by th e Agricultur a l ~nd Cons um e r Protect i o1 Ac t of 1973. This mad e it possible to reduce t he purchase price on bu l~e ", .

e. J'..pr iI- September transi ti c n per iod.

'" 0'

- 4 7 -

noc farmers actually r ecei v e t h e sup port p r ice d e p e nds on

co mpet 'tio n in thE mark~ts ( 2 1).

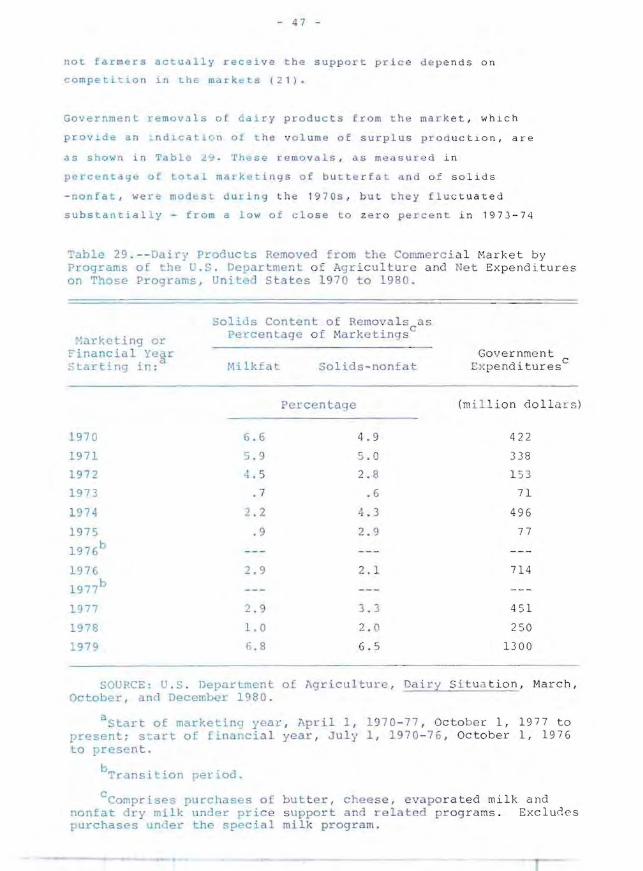

Government removdls of riairy p r o du ct s f rom t h e ma r k e t, WhlCh

provlde an _ n dlc~tlnn of t h e v ol ume o f surpl us pr o d uctlon, are

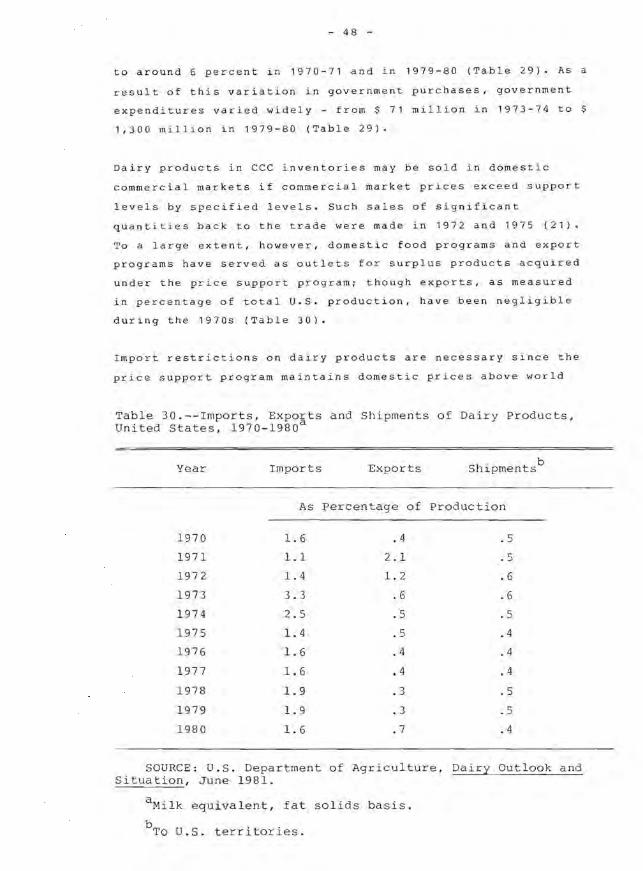

as shown i n Table 29 . These ~e mo v als , as meas u r e d in

perc~ntaq~ of to a1 mark~ti n g s of bu t t e r fat an d o f s o li d s

- nonfat , we re modbst during the 19 7 0s , b u t t h ey f l u c tuated

su b stantially - fro m a low o f c l os e to z e r o pe r c e nt in 1973-74

Table 29 . - - Dair}' Products Removed from t he Commerc i a l Harket b y Programs of he U. S . Depart ment o f Agricu l t u r e u nd Ne t Expenditures on Those Programs , United S t ate s 1 97 0 to 19 BO .

I--:arkeling or Financia l Year , . a Startl.ng l.r :

1970

1971

1972

1973

1974

1975

1976h

19 7 6

1977b

l!J77

1978

1979

Solids Content of Removal s as Pe-centage o f Mar ke ting s C

Milkfat

G. 6

5 . 9

<1 . 5

. 7

2.2

. 9

2.9

2 . 9

1. 0

r.8

o l ids - nonfat

Perc en t a e

4 .9

5 . 0

2. 8

. 6

4 . 3

2. 9

2 .1

3 . 3

2 . C'

6 .5

Governme nt Ex pendituresc

(mil l ion dolla r s )

422

3 38

15 3

71

496

77

714

4 5 1

250

1300

SOURCE: U. S . Department of Aq r i cul t ure , Dai ry S i t u a tion, March, October, and December 1980 .

astart of marketing year , Apr i l I , 197 0- 7 7 , Oc tober 1, 1977 to present ; s cart o f financia l ye a r , J uly 1 , 1 970 -7 6 , October I, 197 6 to present .

b , 1: ' , , Transl lon rerloCi.

CCornpt'lses purchases of bu t t e r, cheese , e vapo rated milk and nonfat dry milk u nder price s uppor t and re lated prog r ams. Excludes purchases under the special mi l k p rogram .

- 48 -

to around 6 percent in 1970-71 and in 1979-80 (Table 29). As a

result of this variation in government purchases, government

expenditures varied widely - from $ 71 million in 1973-74 to $

1,300 million in 1979-80 (Table 29).

Dairy products in CCC inventorie s may be sold in domestic

commercial markets if commercial market pri ces exceed support

levels by specified levels. Such sales of significant

quantities back to the trade were made in 1972 and 1975 (21).

To a large extent, however, domestic food programs and export

programs have served as outlets for surplus products acquired

under the price support program; though exports , as measured

in percentage of total U.S. production, have been negligible

during the 1970s (Table 30)

Import restrictions on dairy products are necessary since the

price support program maintains domestic prices above world

Table 30.--Imports, Exports and Shipments of Dairy Products, United States, 1970-1980a

Year Imports Exports h. b S l.pments

As Percentage of Production

1970 1.6 .4 . 5

1971 1.1 2.1 .5

1972 1.4 1.2 .6

197 3 3.3 .6 .6

1974 2 .5 .5 .5

1975 1.4 .5 .4

1976 1.6 .4 .4

1977 1.6 .4 .4

1978 1.9 .3 .5

1979 1.9 .3 .5

1980 1.6 .7 .4

SOURCE: U.S. Department of Agriculture, Dairy Outlook and Situa tion, June 1981.

a Milk equivalent, fat solids basis.

b To U.S. territories.

- 49 -

m rket l e v e ls. The €x~sti n g i mpo r t r e gulat io ns on d a i ry

products can b e devided into maj or categor ~ es - qu o tas and

coun erva~ lin g dut~t!6. Impo rt quotas are , u tho r i z t! d un de r

Sacr.ion 2 2 of the )\ytl.r...ultura l Adjustme n t Act of 1 <) 33 , as

mended. This Act .llo~s res r ic tlons On i mports of ag r icu l

tural produces when necessary to prevent impo Lt s f r om

int:eri~ring with damestLc agricultural pr Lcc s u ppo rt program s.

Co untervai l ~n g dutles dre au horized by Se c t i on 3U 3 of th e

Tarlff Act of 1930. This Act direct s the Secr et ary o f th e

Treasury to impose counlervailing d u tLes ayalns t an imp o rt

i &em Lf t he production or th e e xportatio n of th e it e m ha s been

subSidiz"d (21) .

Total ~mpo r tS oE dalry products have been mod ~ Ht , a r o un d 1.5

to 2.0 in Pblcentage of to td l U. S . pr o d u ction , on a fat so li d

baSis, i n masL y ~drs (Table 30 ) . The impolLs c ons ist mai nly o f

c heese.

4 . 2 . ImpacLs

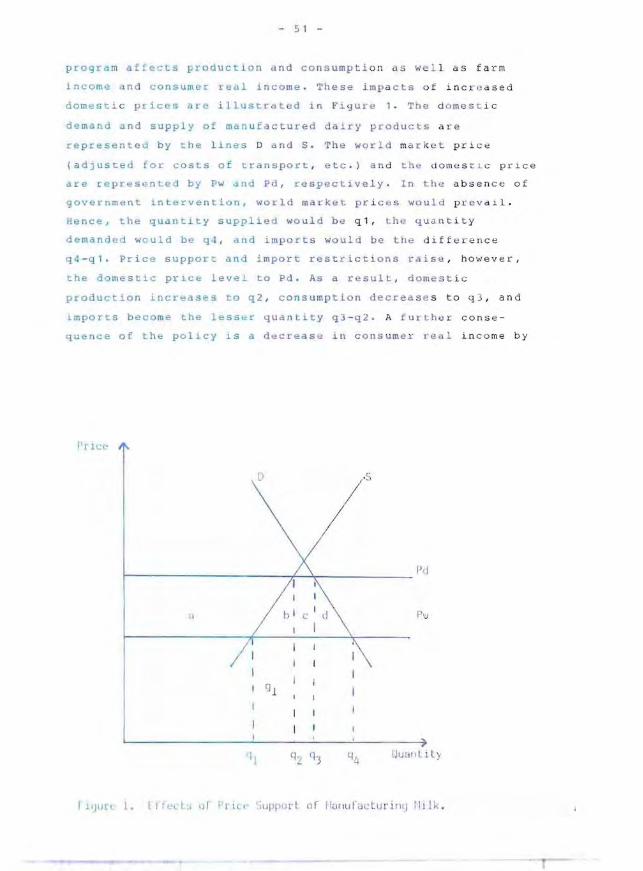

T h e prIce support p~ogram e [ f ~~ts pLi~ c ~ o f mi lk ~ n d dairy

products at al~ l~vels . I n so d OL fi g , th e program inf lu ence s

prOducLion dnd c onsumpLion dS we l l a s farm i nco me a n d consumer

real l.ncome. This secti un de a l s wi th some (')f tI ,ns ." i mp a c t s.

In man3ging the pr~C2 SUp~Olt program c o nc~r ns se e m t o focu s

nn accomplishing th- [ollowiny two objectiv~ s: 1 ) sta bi Llz ati on

of production, pr~ces and produce r return; and 2 ) enh a n c ement

of producer r~turn. A t h " rd objec t ive or r~st r i c &~ on o f

concern consLsts of cunscrdint s on government expen d ltu r e s .

The extt<nt to whl h Lh" .. e Obje c t i ves have be " n a CH ie v e d in the

past hdve been dfrecte J by preva i ling eco nom ic c n d ~ t i ons ,

<::hardcteristic of t. h e pl"ogram , and politi c a l pr ess ures .

The program undoubLedly has h~lped ke~p prl c es , p r o ductLon

dnd farm ln~om~ more stable. Prices h ave bee n p r eve n t e d f ro m

fal l1ny below the SUPPOIC level b y CCc p u rchases of surp lus

product.s d n d prlc's 11aVt< been prev t! nted fro m i nc r ea sing mo r e

50 -

than they did by sales of CCC stocks of dairy products back

in the trade (21).

The price support program did not succeed, however, to provide

stability in milk production in the early seventies. As feed