credit card debt & credit scores how to use them, but not abuse them

TRANSCRIPT

Credit Card Debt & Credit Scores

How to Use Them, But Not How to Use Them, But Not Abuse ThemAbuse Them

Students & Credit Cards

Some recent statistics (2008)Some recent statistics (2008) 84% of undergraduates had at least one credit 84% of undergraduates had at least one credit

card, up from 76% in 2004.card, up from 76% in 2004. 50% of college students have four credit cards 50% of college students have four credit cards

or moreor more The average undergraduate owes $3,173The average undergraduate owes $3,173 21% of undergraduates had balances of 21% of undergraduates had balances of

between $3,000 and $7,000 between $3,000 and $7,000 In 2008 more than 150,000 people under the In 2008 more than 150,000 people under the

age of 25 filed for bankruptcyage of 25 filed for bankruptcy

More Statistics

40% said they’ve charged items knowing they 40% said they’ve charged items knowing they didn’t have the money to pay the bill. didn’t have the money to pay the bill.

Only 17 % said they regularly paid off all cards Only 17 % said they regularly paid off all cards each montheach month

1% had parents, a spouse, or other family members 1% had parents, a spouse, or other family members paying the bill. The remaining 82 % carried paying the bill. The remaining 82 % carried balances and thus incurred finance charges each balances and thus incurred finance charges each month.month.

Introduction to Credit WS

What is an interest rate (APR?)

APR stands for annual APR stands for annual percentage rate. This percentage rate. This represents the represents the percentage on your percentage on your balance that you have balance that you have to pay ON TOP of to pay ON TOP of what you borrowed. what you borrowed.

The lending company The lending company is charging you for the is charging you for the loan. loan.

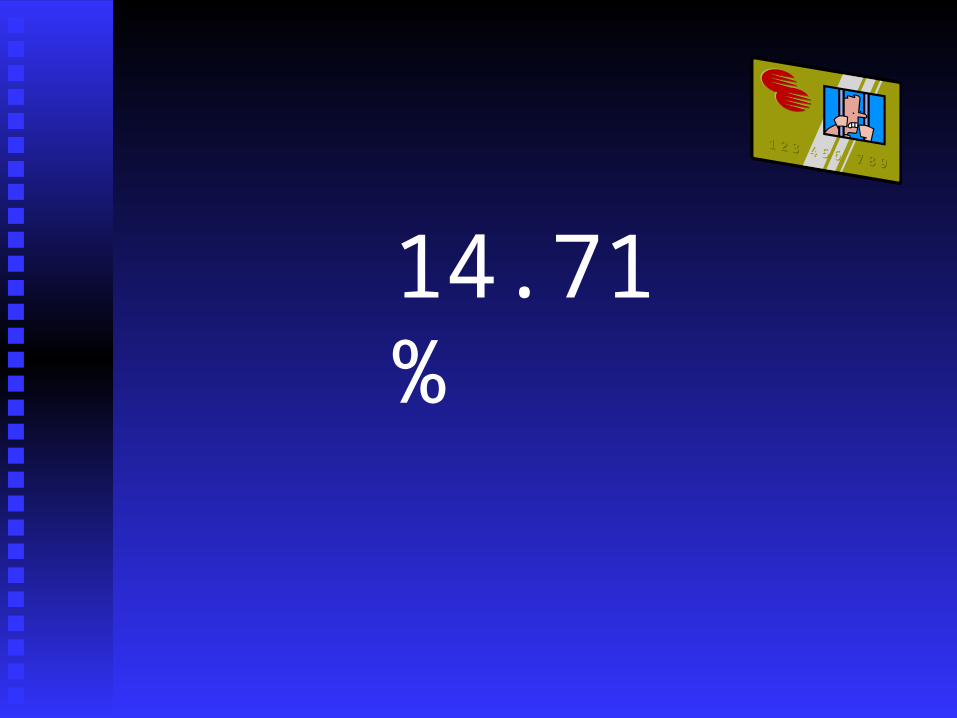

What is the average rate for a credit card?

14.71%

What is the highest interest rate currently

charged on a credit card?

41%That’s almost half!!!

Credit Cards: The Basics

Fees, fees, and more feesFees, fees, and more fees Annual fee for just having the credit cardAnnual fee for just having the credit card Over the limit fees, charged whenever you Over the limit fees, charged whenever you

exceed your credit limitexceed your credit limit Late payment feesLate payment fees Transaction feesTransaction fees Other miscellaneous feesOther miscellaneous fees

read the fine print!!!read the fine print!!!

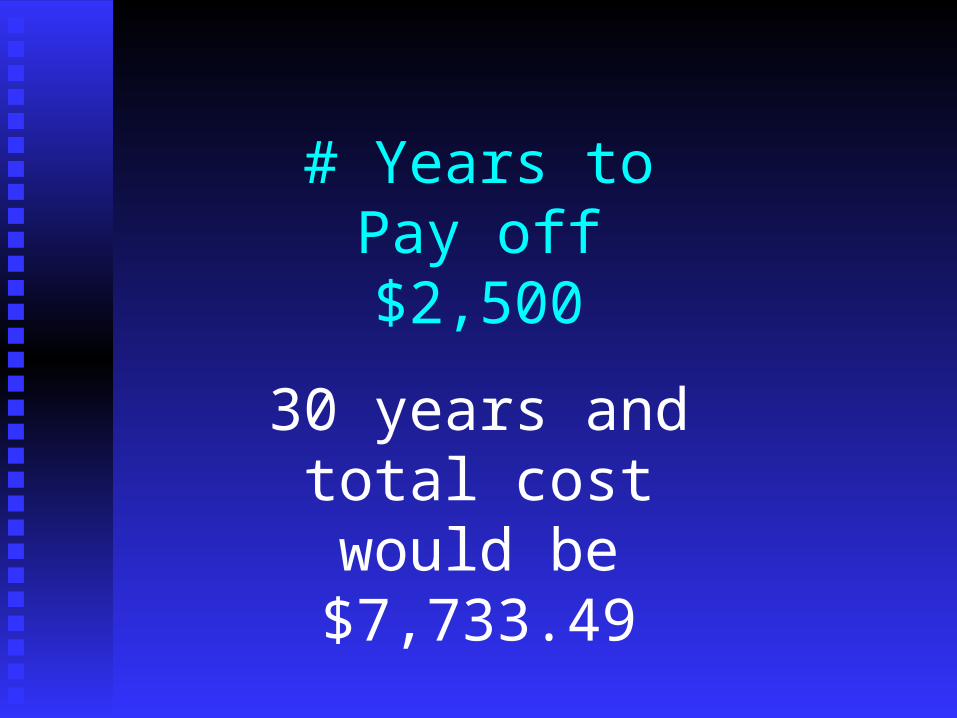

Credit Card Debt•How long will it take to pay off

$2,500 at an interest rate of 17% if you pay only the minimum

balance due?

# Years to Pay off $2,500

30 years and total cost would be $7,733.49

Credit Cards: The Risks

Characteristics of high-risk useCharacteristics of high-risk use Average credit card balances over $1,000Average credit card balances over $1,000 Owning four or more credit cardsOwning four or more credit cards Carrying a balance each monthCarrying a balance each month

What is the average # of credit cards a person holds?

14

Credit Cards: The Risks

Career choices can be limitedCareer choices can be limited Some are forced to file bankruptcy (1.3 million Some are forced to file bankruptcy (1.3 million

cardholders filed for bankruptcy last year)cardholders filed for bankruptcy last year) A few students, so overwhelmed with debt, have A few students, so overwhelmed with debt, have

committed suicidecommitted suicide

Credit Card Don’ts

Don’t get one, if you do - only get oneDon’t get one, if you do - only get one Don’t use them for cash advancesDon’t use them for cash advances Don’t charge more than you can pay off Don’t charge more than you can pay off

in a monthin a month Don’t let banks increase your credit limitDon’t let banks increase your credit limit

Source: USA Funds Life Skills -Module 1

Credit Card Do’s

Limit the number of cards you haveLimit the number of cards you have Use a debit card vs. a credit cardUse a debit card vs. a credit card Use a card that has no annual fee Use a card that has no annual fee

and lower interest ratesand lower interest rates Know all of your card’s hidden feesKnow all of your card’s hidden fees Always pay more than the Always pay more than the

minimum amount each monthminimum amount each month Pay on time, all the time.Pay on time, all the time.

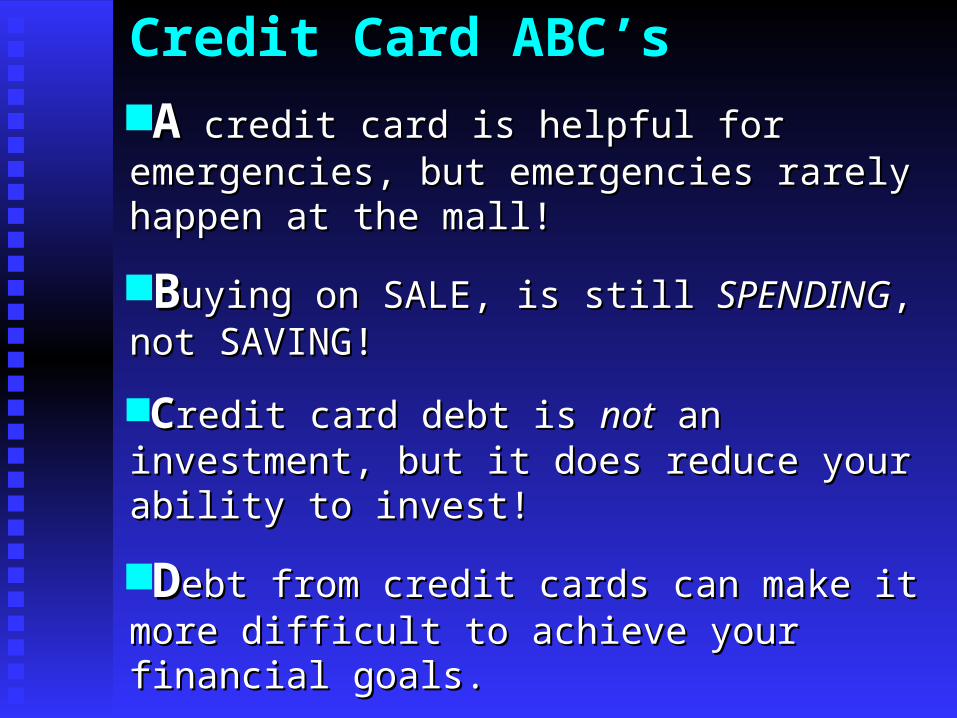

Credit Card ABC’sAA credit card is helpful for emergencies, but credit card is helpful for emergencies, but emergencies rarely happen at the mall!emergencies rarely happen at the mall!

BBuying on SALE, is still uying on SALE, is still SPENDINGSPENDING, not , not SAVING!SAVING!

CCredit card debt is redit card debt is notnot an investment, but it does an investment, but it does reduce your ability to invest!reduce your ability to invest!

DDebt from credit cards can make it more difficult to ebt from credit cards can make it more difficult to achieve your financial goals.achieve your financial goals.

Credit Worthiness

Before creditors lend money, they need to Before creditors lend money, they need to be assured that the funds will be repaid. be assured that the funds will be repaid. In other words, is the prospective borrower In other words, is the prospective borrower

creditworthy?creditworthy?

Fill out the 3 C’s of Credit Web using the Fill out the 3 C’s of Credit Web using the bookbook

Common Reasons for Denying Credit

Too little time in current job or at current residenceToo little time in current job or at current residence

Too much outstanding debtToo much outstanding debt

Unreasonable purpose for requesting creditUnreasonable purpose for requesting credit

Cosigner cannot take on additional debt liabilityCosigner cannot take on additional debt liability

Errors on applicant’s credit reportErrors on applicant’s credit report

Strict creditor’s standardsStrict creditor’s standards

Improving Poor Credit

Face up to the problemFace up to the problem

Work with creditors to maintain payment scheduleWork with creditors to maintain payment schedule

Consider consolidating debtsConsider consolidating debts

Make a single payment rather than severalMake a single payment rather than several

Contact a credit counseling organizationContact a credit counseling organization

800-388-2227 = National Foundation for Credit Counseling800-388-2227 = National Foundation for Credit Counseling

Don’t expect miraclesDon’t expect miracles

It takes time and patience to fix a poor credit ratingIt takes time and patience to fix a poor credit rating

Credit Score & Report

Complete the worksheet Credit report using Complete the worksheet Credit report using the booksthe books

Checking Your Report

• Make sure info in credit report is correctMake sure info in credit report is correct

• Review at least once a yearReview at least once a year

– If you check too often, it reduces your credit scoreIf you check too often, it reduces your credit score

• Errors: credit reporting agency must investigate and respond to you Errors: credit reporting agency must investigate and respond to you

in 30 daysin 30 days

• Credit reporting agenciesCredit reporting agencies::

– Equifax Equifax www.equifax.com

– Experian Experian www.experian.com

– TransUnion TransUnion www.transunion.com

How to Establish Credit Open an individual savings and checking account in your name.Open an individual savings and checking account in your name.

Over time your transactions demonstrate responsible money Over time your transactions demonstrate responsible money handlinghandling

Apply for a loan Apply for a loan (Careful for costs and interest)(Careful for costs and interest)

Apply for department store/gasoline credit cards Apply for department store/gasoline credit cards (Easier to obtain, but (Easier to obtain, but choose carefully)choose carefully)

PatiencePatience (It takes time to establish credit)(It takes time to establish credit)

Start slow Start slow (Be cautious, keep track of overall debt and pay on time!)(Be cautious, keep track of overall debt and pay on time!)

What’s In Your Credit Report?! Identifying InformationIdentifying Information

Name, address, SS #, date of birth, employment infoName, address, SS #, date of birth, employment info

Trade LinesTrade Lines

Your credit accounts. Lenders report on each account (bankcard, Your credit accounts. Lenders report on each account (bankcard,

auto loan, mortgage)auto loan, mortgage)

InquiriesInquiries

Who, in the past 2 years, has inquires about your credit report. Who, in the past 2 years, has inquires about your credit report.

Report lists “Voluntary” (you) & “Involuntary” (lenders) Report lists “Voluntary” (you) & “Involuntary” (lenders)

inquiriesinquiries

Public Record & Collection ItemsPublic Record & Collection Items

Public record info from state and countyPublic record info from state and county

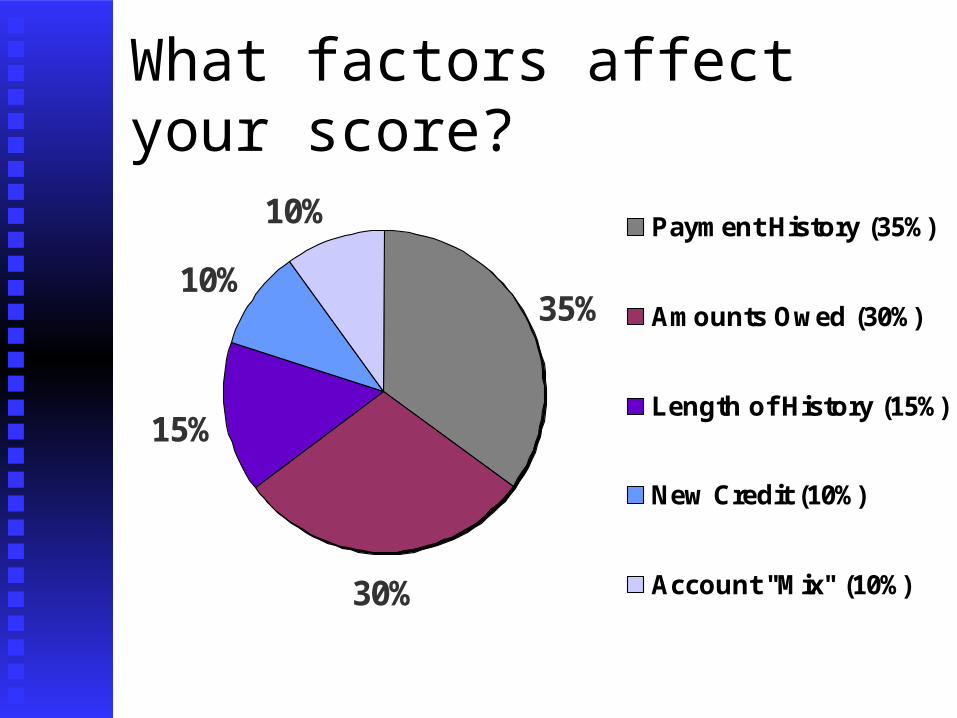

What factors affect your score?

35%

30%

15%

10%

10%Payment History (35%)

Amounts Owed (30%)

Length of History (15%)

New Credit (10%)

Account "Mix" (10%)

What Is NOT In Your Score

Race, color, religion, national origin, sex and marital Race, color, religion, national origin, sex and marital

statusstatus

AgeAge

Salary, occupation, title, employer, date employed or Salary, occupation, title, employer, date employed or

employment historyemployment history

Where you liveWhere you live

Interest rates for particular accounts/credit cardsInterest rates for particular accounts/credit cards

Child/family support obligations or rental agreementsChild/family support obligations or rental agreements

How Credit Scoring Helps You

People can get loans fasterPeople can get loans faster

Credit decisions are fairerCredit decisions are fairer

Credit “mistakes” count for lessCredit “mistakes” count for less

More credit is availableMore credit is available

Credit rates are lower overall.Credit rates are lower overall.

To Maximize Your Score . . .

Don’t procrastinate – pay all your bills on timeDon’t procrastinate – pay all your bills on time

Avoid owing more than 30% of your available Avoid owing more than 30% of your available revolving creditrevolving credit

““Less is more” – Less is more” – keep your revolving debt as low as keep your revolving debt as low as possiblepossible

““Older is better” – Older is better” – older accounts score more older accounts score more favorablyfavorably

Minimize the opening of new revolving accountsMinimize the opening of new revolving accounts

What is the true cost of paying the “minimum” Suppose:Suppose:

Credit card balance = $8,000Credit card balance = $8,000

Interest rate (APR) = 18%Interest rate (APR) = 18%

Minimum payment = 2% of balanceMinimum payment = 2% of balance

How long would it take to pay it off?How long would it take to pay it off?

647 months / 54 years647 months / 54 years

Total interest paid = $22,931Total interest paid = $22,931

This assumes you STOP using the credit cards! This assumes you STOP using the credit cards!

It will take even longer if you don’t stop!It will take even longer if you don’t stop!