country presentations

DESCRIPTION

Country Presentations. Canada. Canada’s Pharmaceutical DNA. and. Key Challenges and. Opportunities. Canada’s Pharmaceutical DNA. Health system. – Population aged 65 and over predicted to reach 25% of total by 2050 – Total expenditure on health (TEH) much higher than OECD average. - PowerPoint PPT PresentationTRANSCRIPT

Country Presentations

Canada

Canada’s Pharmaceutical DNAand

Key Challenges andOpportunities

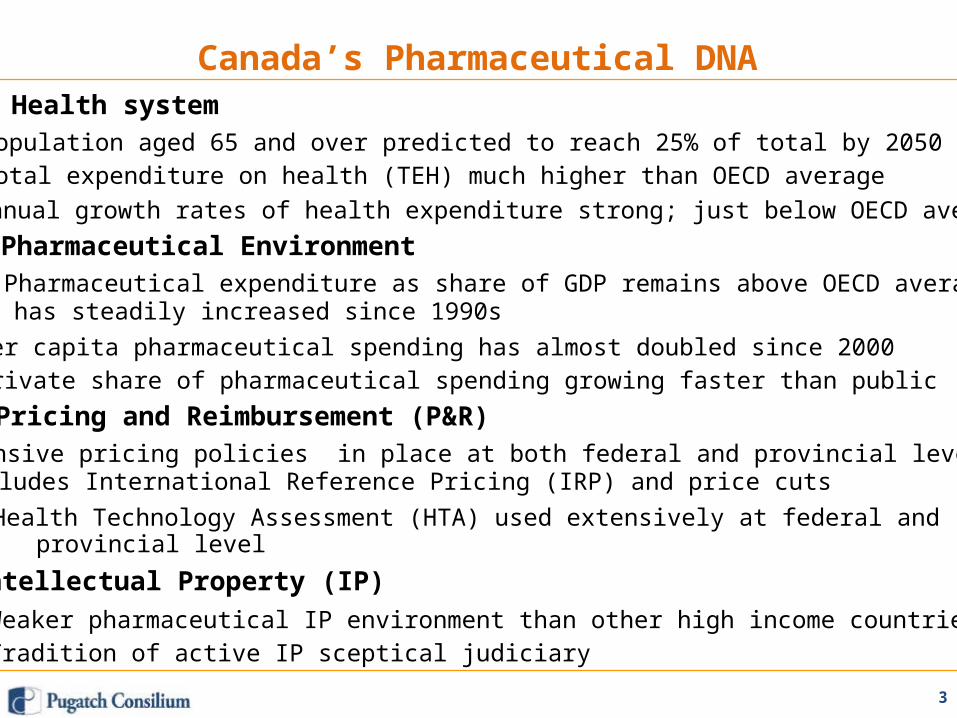

Canada’s Pharmaceutical DNAHealth system

– Population aged 65 and over predicted to reach 25% of total by 2050– Total expenditure on health (TEH) much higher than OECD average– Annual growth rates of health expenditure strong; just below OECD average

Pharmaceutical Environment– Pharmaceutical expenditure as share of GDP remains above OECD average:

has steadily increased since 1990s– Per capita pharmaceutical spending has almost doubled since 2000– Private share of pharmaceutical spending growing faster than public

Pricing and Reimbursement (P&R)– Extensive pricing policies in place at both federal and provincial level:includes International Reference Pricing (IRP) and price cuts– Health Technology Assessment (HTA) used extensively at federal and

provincial levelIntellectual Property (IP)

– Weaker pharmaceutical IP environment than other high income countries– Tradition of active IP sceptical judiciary

3

4

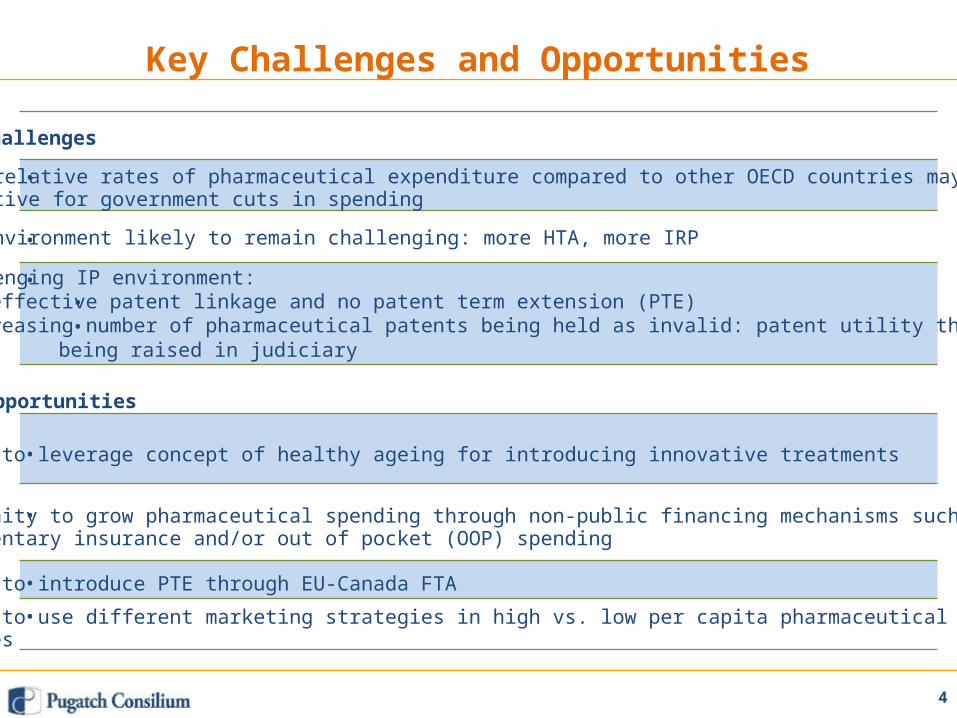

Key Challenges and Opportunities

Challenges

•

•

•

High relative rates of pharmaceutical expenditure compared to other OECD countries may provideincentive for government cuts in spending

P&R environment likely to remain challenging: more HTA, more IRP

Challenging IP environment:••

no effective patent linkage and no patent term extension (PTE)increasing number of pharmaceutical patents being held as invalid: patent utility threshold

being raised in judiciary

Opportunities

•

•

•

•

Ability to leverage concept of healthy ageing for introducing innovative treatments

Opportunity to grow pharmaceutical spending through non-public financing mechanisms such assupplementary insurance and/or out of pocket (OOP) spending

Ability to introduce PTE through EU-Canada FTA

Ability to use different marketing strategies in high vs. low per capita pharmaceutical spendingprovinces

Presentation Overview

5

Presentation Overview

• Demographic background

• Macro-economic background

• Health system overview

• Pharmaceutical overview

• Pricing and reimbursement policies

• Intellectual property environment

• Biopharmaceutical regulatory requirements

• Public procurement policies – pharmaceuticals

6

Demographic Background

7

Demographics

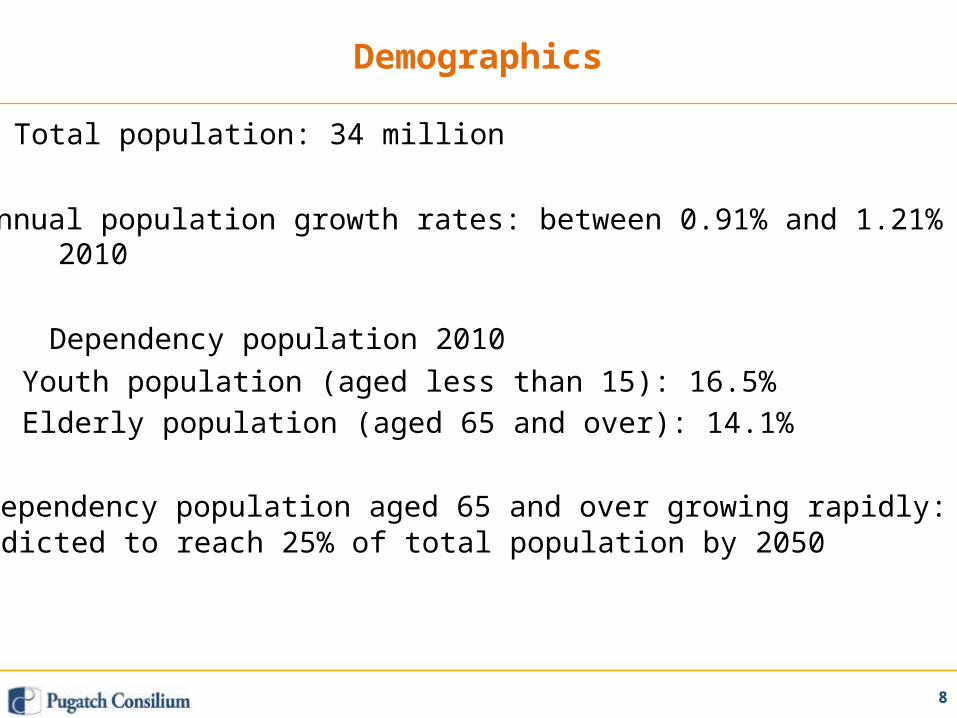

• Total population: 34 million

• Annual population growth rates: between 0.91% and 1.21% 2000-2010

• Dependency population 2010– Youth population (aged less than 15): 16.5%– Elderly population (aged 65 and over): 14.1%

• Dependency population aged 65 and over growing rapidly:predicted to reach 25% of total population by 2050

8

9

Source: OECD Stat (2012)

20

15

10

5

02000 2005 2010 2020 2030 2040 2050

Dependency Population, Trend and Forecast, 2000-2050

30

25

Youth Population(agedless than 15) % of total

Population

Elderly population (aged65 and over) % of totalPopulation

Macro-economic Background

10

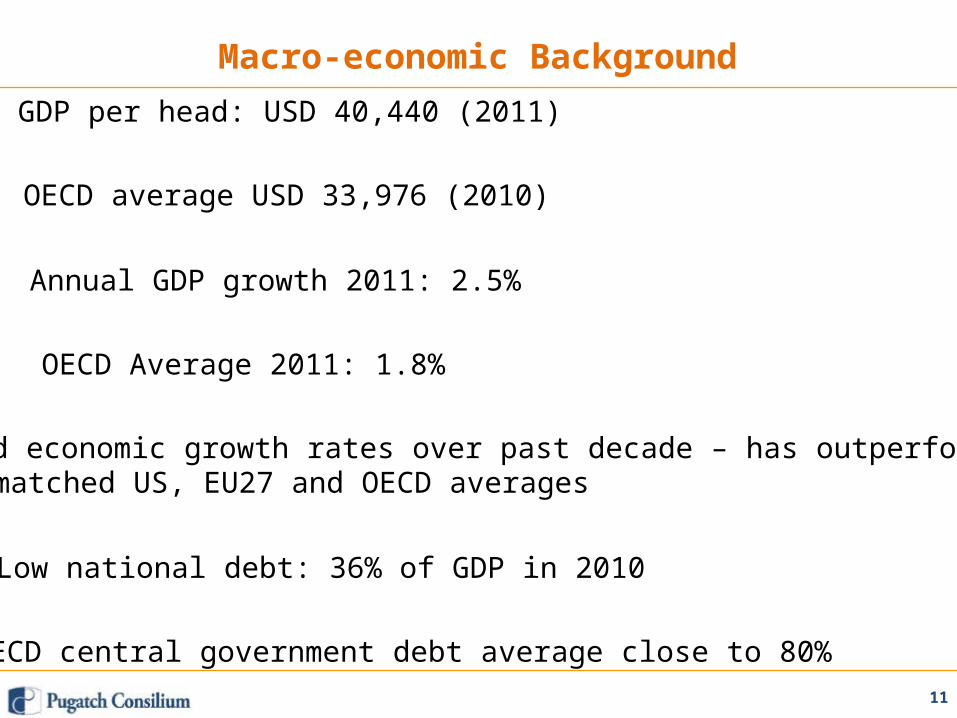

Macro-economic Background• GDP per head: USD 40,440 (2011)

• OECD average USD 33,976 (2010)

• Annual GDP growth 2011: 2.5%

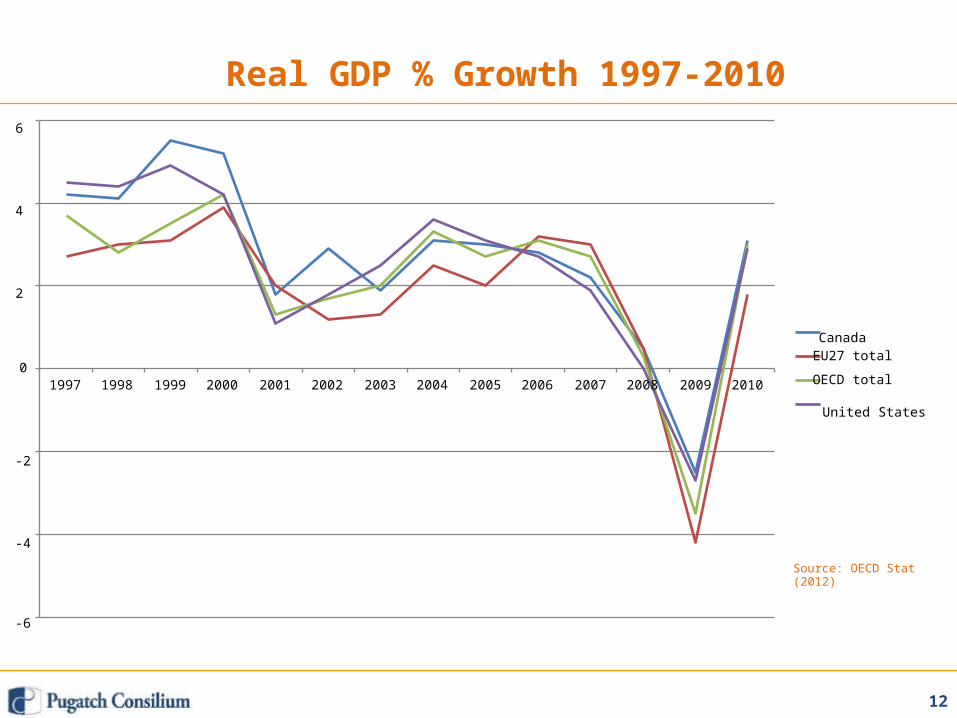

• OECD Average 2011: 1.8%

• Solid economic growth rates over past decade – has outperformed ormatched US, EU27 and OECD averages

• Low national debt: 36% of GDP in 2010

• OECD central government debt average close to 80%11

01997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Real GDP % Growth 1997-20106

4

2

CanadaEU27 total

OECD total

United States

-2

-4

Source: OECD Stat(2012)

-6

12

Health System Overview

13

General Health System Facts• National health insurance program (“Medicare”)

• Central Government sets insurance standards through CanadaHealth Act

• 13 provincial and territorial health insurance plans offers actualcoverage and medical services

• Traditional single-payer model, tax funded

• Health policy fragmented, divided between central and provincialgovernments, especially pharmaceutical policy (discussed below)

• Private provision of primary care limited but growing

14

Health Expenditure

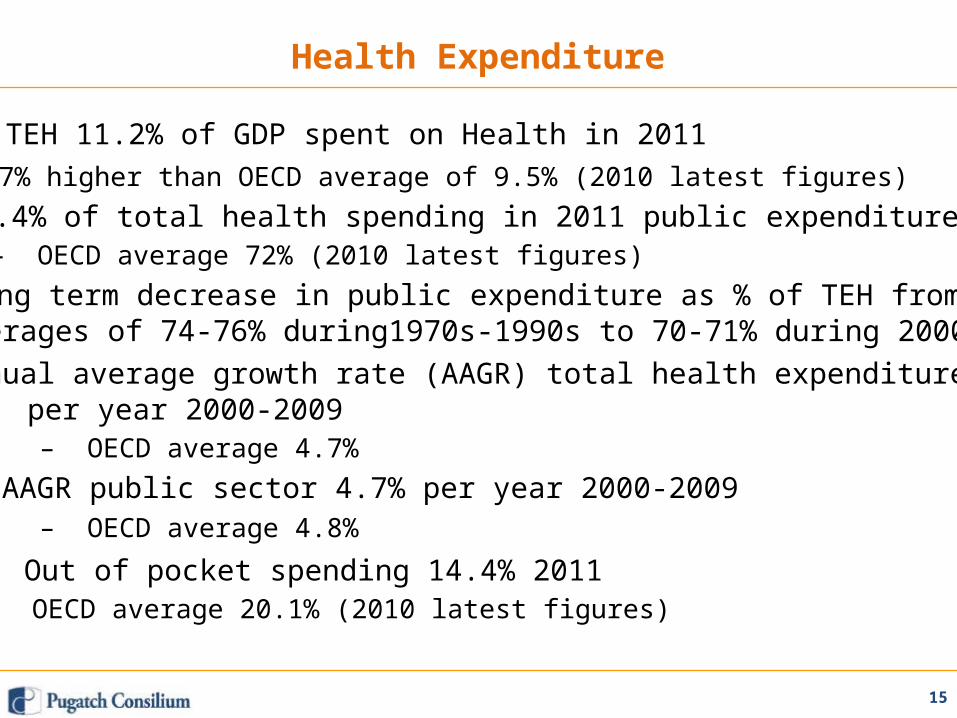

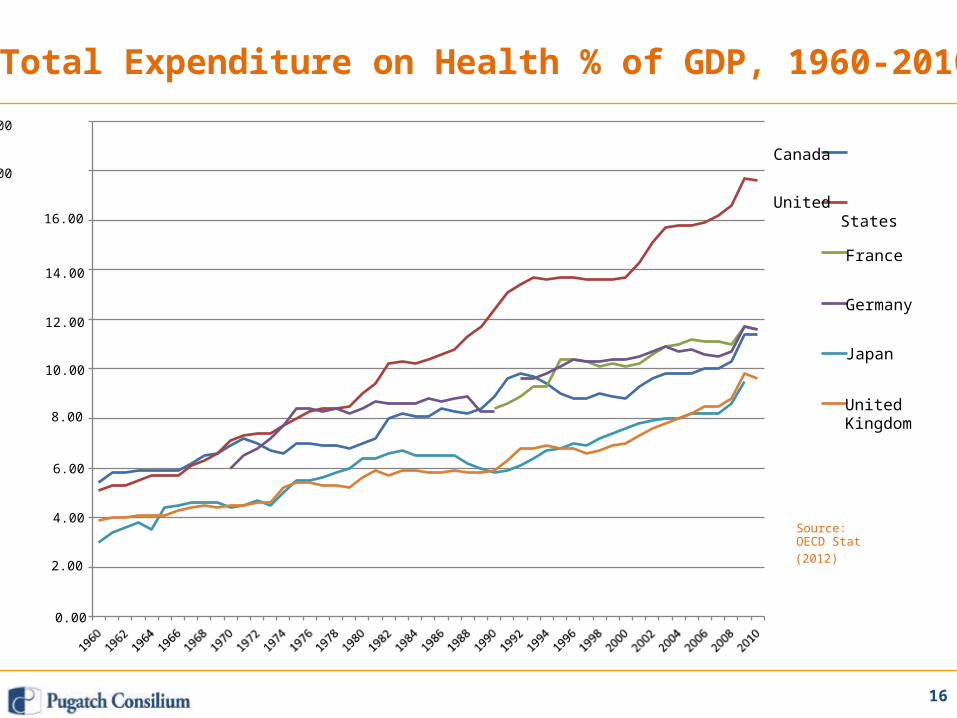

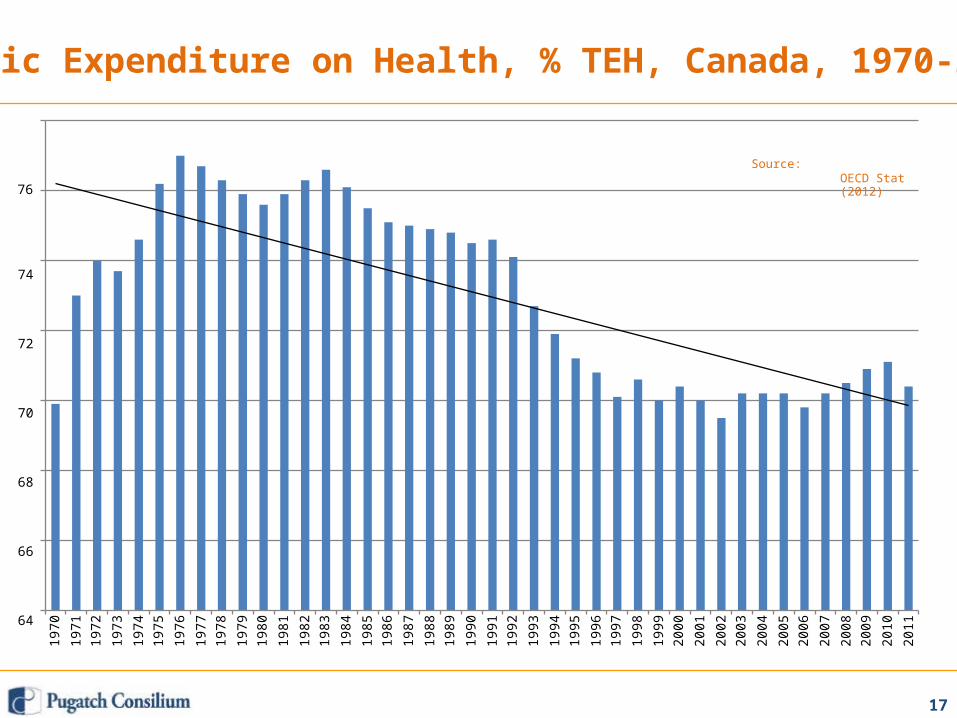

• TEH 11.2% of GDP spent on Health in 2011– 1.7% higher than OECD average of 9.5% (2010 latest figures)

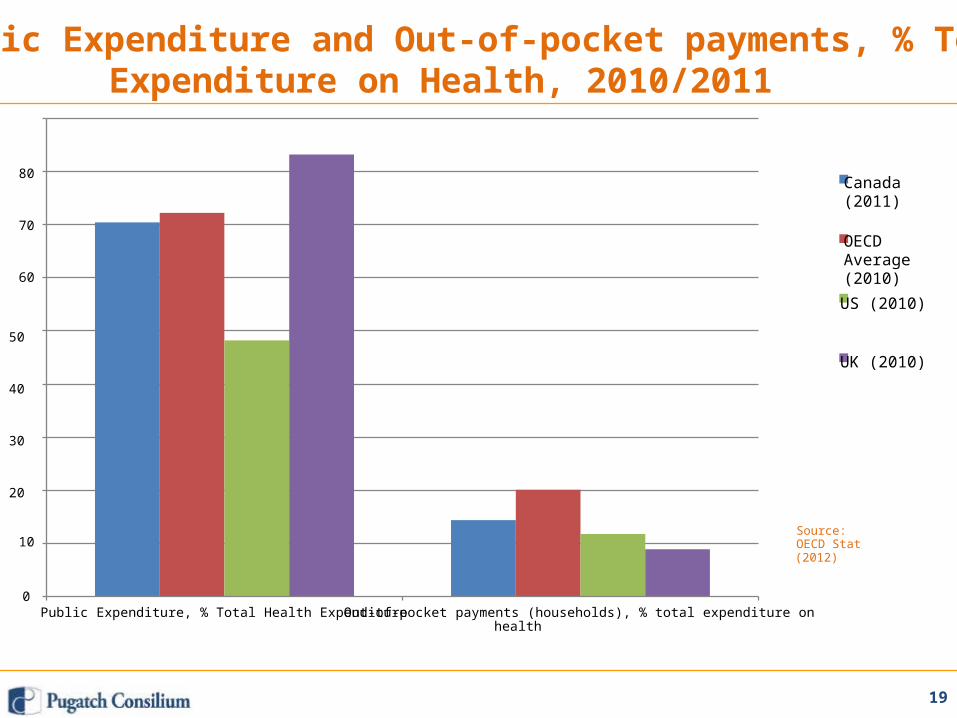

• 70.4% of total health spending in 2011 public expenditure– OECD average 72% (2010 latest figures)

• Long term decrease in public expenditure as % of TEH fromaverages of 74-76% during1970s-1990s to 70-71% during 2000s

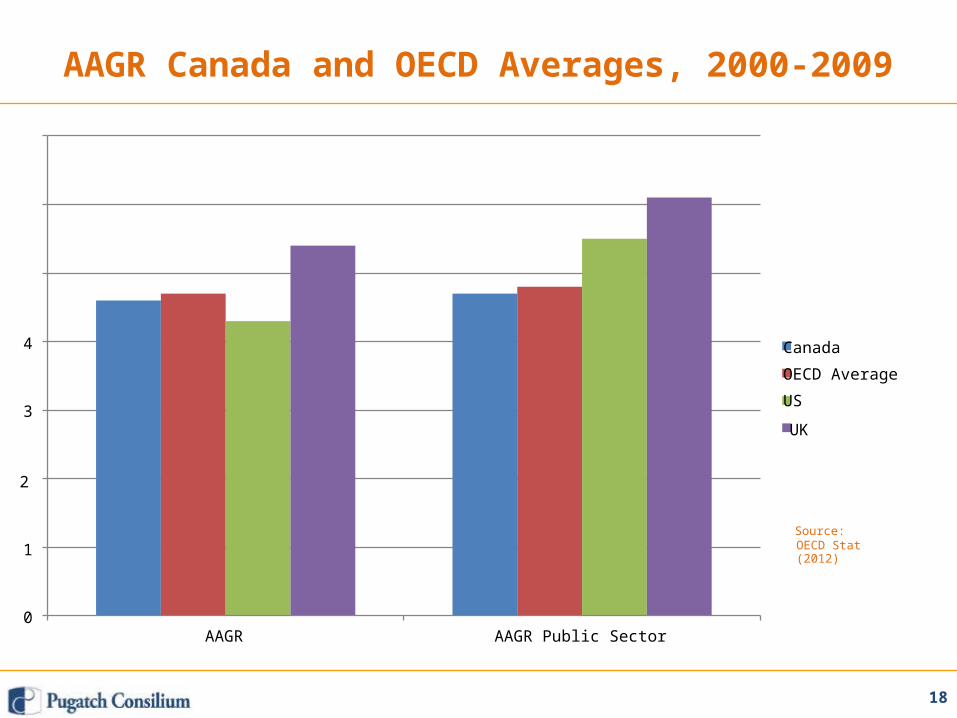

• Annual average growth rate (AAGR) total health expenditure 4.6%per year 2000-2009– OECD average 4.7%

• AAGR public sector 4.7% per year 2000-2009– OECD average 4.8%

• Out of pocket spending 14.4% 2011– OECD average 20.1% (2010 latest figures)

15

(2012)

0.00

16

2.00

6.00

4.00Source:OECD Stat

8.00

16.00

Total Expenditure on Health % of GDP, 1960-201020.00

Canada18.00

UnitedStates

France14.00

Germany12.00

Japan10.00

UnitedKingdom

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

OECD Stat(2012)

74

72

70

68

66

64

17

76

Public Expenditure on Health, % TEH, Canada, 1970-201178

Source:

18

OECD Stat(2012)1

0

4

3

AAGR Canada and OECD Averages, 2000-2009

7

6

5

AAGR AAGR Public Sector

Canada

OECD Average

US

UK

2

Source:

19

Source:OECD Stat(2012)

0

10

80

70

60

Public Expenditure and Out-of-pocket payments, % TotalExpenditure on Health, 2010/2011

90

Public Expenditure, % Total Health Expenditure Out-of-pocket payments (households), % total expenditure onhealth

Canada(2011)

OECDAverage(2010)US (2010)

50

UK (2010)

40

30

20

Pharmaceutical Overview

20

Pharmaceutical Overview

• Pharmaceuticals are covered through public or private insurance• Within a hospital setting drugs administered are covered throughpublic insurance

• Provinces and territories offer pharmaceutical insurance plans• Plans differ in eligibility, premiums, coverage and formularydesign• Canada top-10 pharmaceutical market in the world – per capita

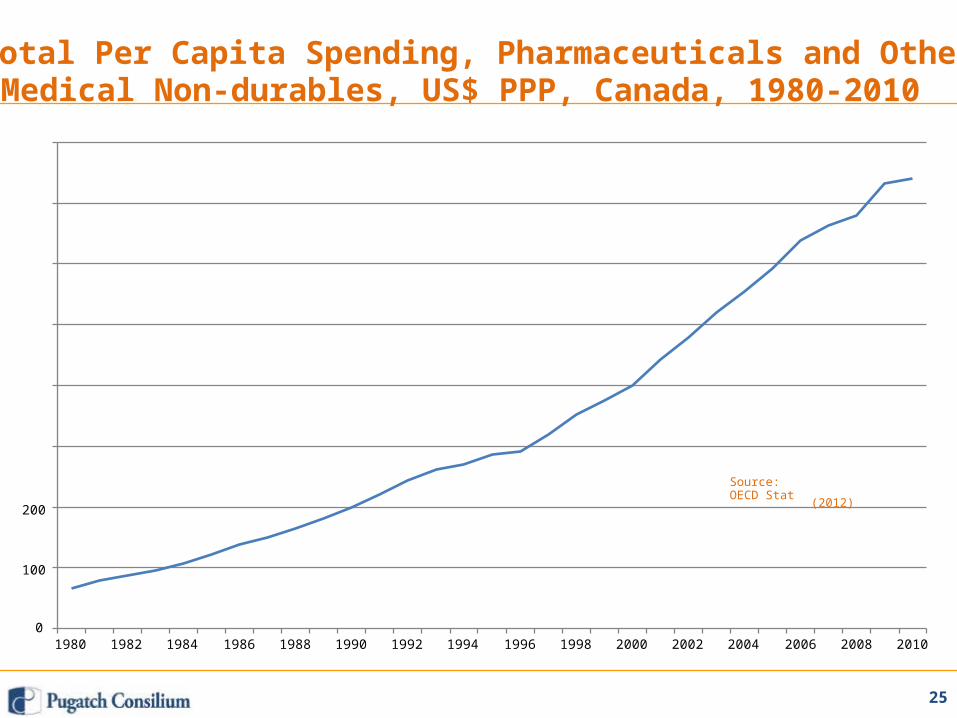

spending 2nd highest in the world• Strong growth in per capita pharmaceutical spending since1990s• Between 2000-2010 per capita spending almost doubled from

USD 400.7 to USD 740.7 (PPP)

21

Pharmaceutical Snapshot

•••••

Total spending on pharmaceuticals in 2011 C$32billion (CIHI)Growth of 4% 2010-2011Lower growth than in the past but still close to TEH AAGRPrescription drugs account for close to 85% of total spendingRelatively even split between public and private financing of

prescription drugs: 45% vs. 55%• Stronger growth rates in private financing (6.8%) vs. public

financing (2.2%)• Large variations in per capita spending from province to

province: C$576 in British Columbia and C$710 in Manitoba vs.C$937 in New Brunswick and C$985 in Nova Scotia

• Large variations in spending growth from province to province:1.4% in British Columbia and 2% in Ontario vs. 7.4% inSaskatchewan and 9.4% in Newfoundland and Labrador

22

Total Expenditure on Pharmaceuticals and Other MedicalNon-durables, % TEH, Canada, 1960-2010

23

Source:OECD Stat

(2012)

18

16

14

12

10

8

6

4

2

0

20

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

15

10

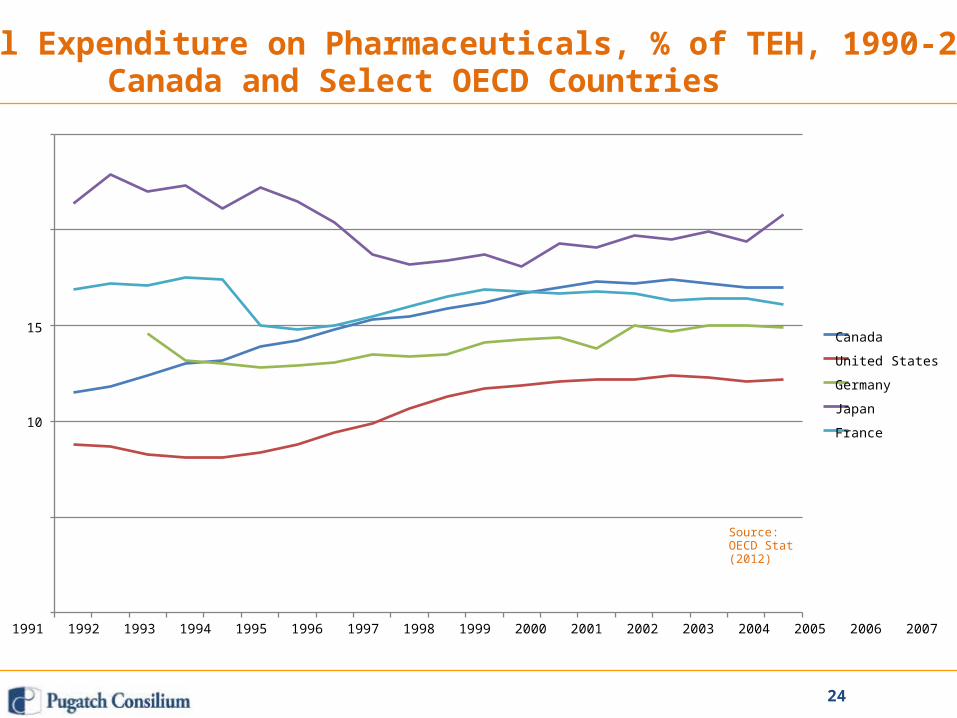

Total Expenditure on Pharmaceuticals, % of TEH, 1990-2009,Canada and Select OECD Countries

25

20

5Source:OECD Stat(2012)

01990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

24

Canada

United States

Germany

Japan

France

25

(2012)200

100

0

Total Per Capita Spending, Pharmaceuticals and OtherMedical Non-durables, US$ PPP, Canada, 1980-2010

800

700

600

500

400

300

Source:OECD Stat

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

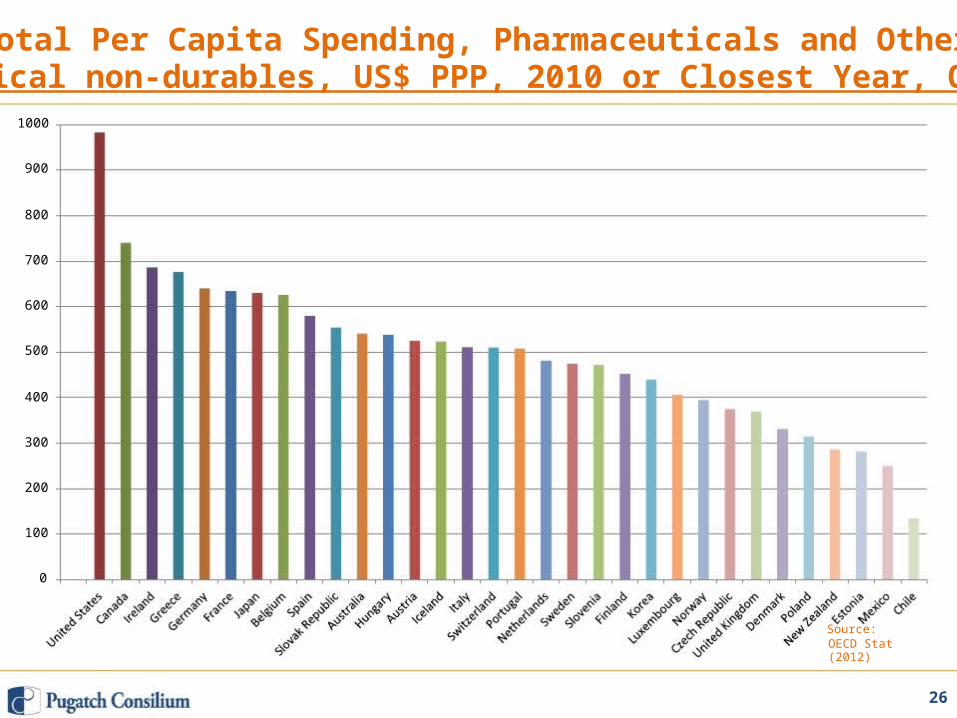

Total Per Capita Spending, Pharmaceuticals and OtherMedical non-durables, US$ PPP, 2010 or Closest Year, OECD

26

Source:OECD Stat(2012)

0

100

200

300

400

500

600

700

800

900

1000

Pricing and ReimbursementPolicies

27

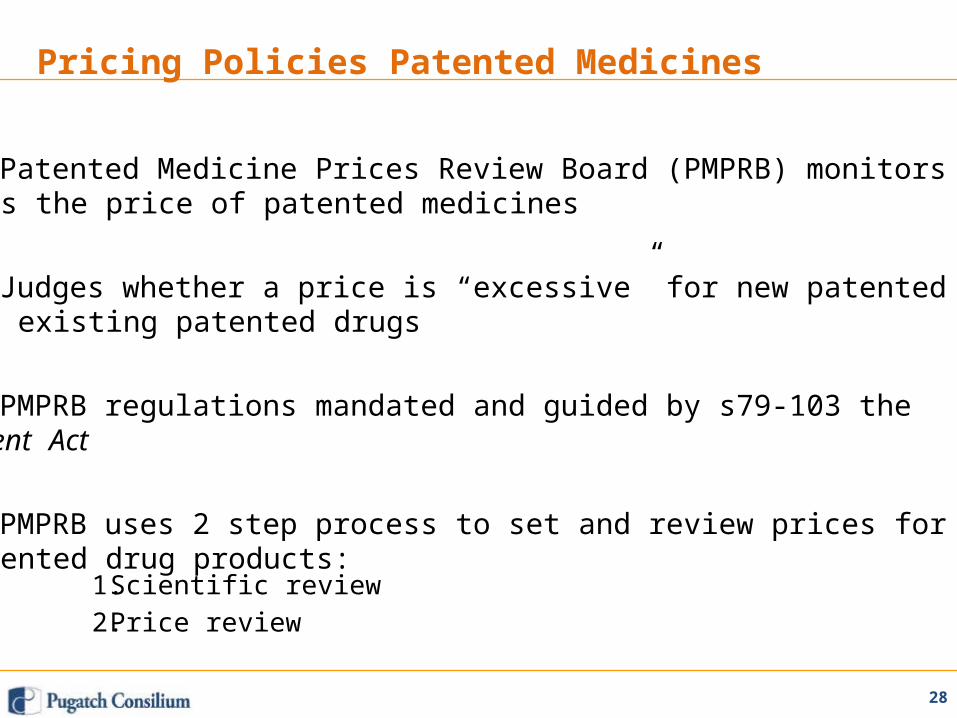

Pricing Policies Patented Medicines

• Patented Medicine Prices Review Board (PMPRB) monitors andsets the price of patented medicines

• Judges whether a price is “excessive” for new patented drugsand existing patented drugs

• PMPRB regulations mandated and guided by s79-103 thePatent Act

• PMPRB uses 2 step process to set and review prices for newpatented drug products:

1.2.

Scientific reviewPrice review

28

Scientific Review

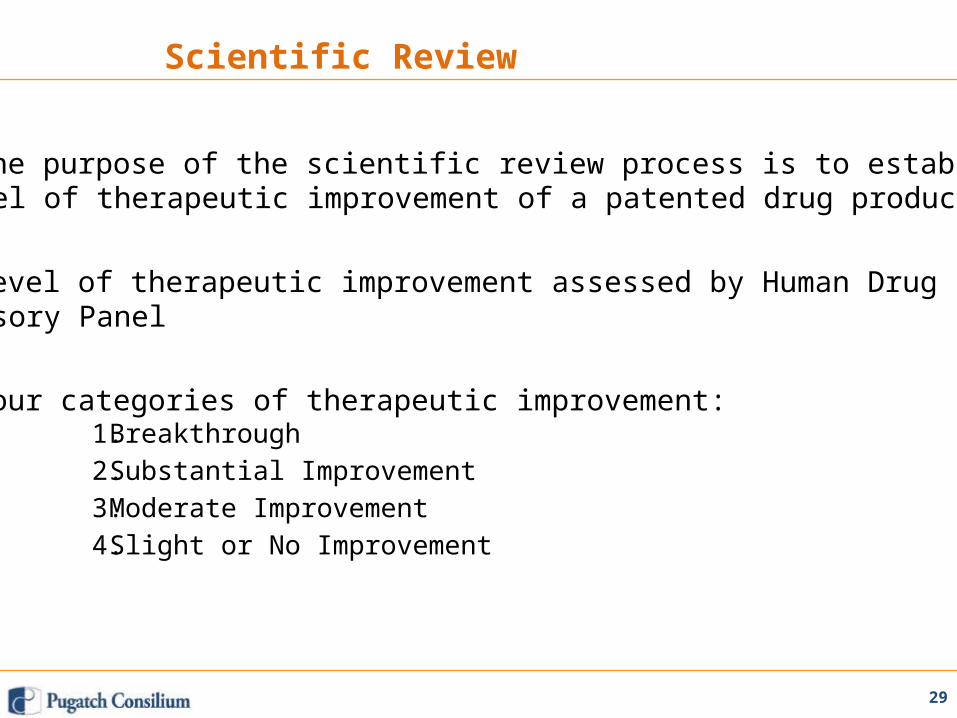

• The purpose of the scientific review process is to establish:“level of therapeutic improvement of a patented drug product”

• Level of therapeutic improvement assessed by Human DrugAdvisory Panel

• Four categories of therapeutic improvement:1.2.3.4.

BreakthroughSubstantial ImprovementModerate ImprovementSlight or No Improvement

29

Price Review Process

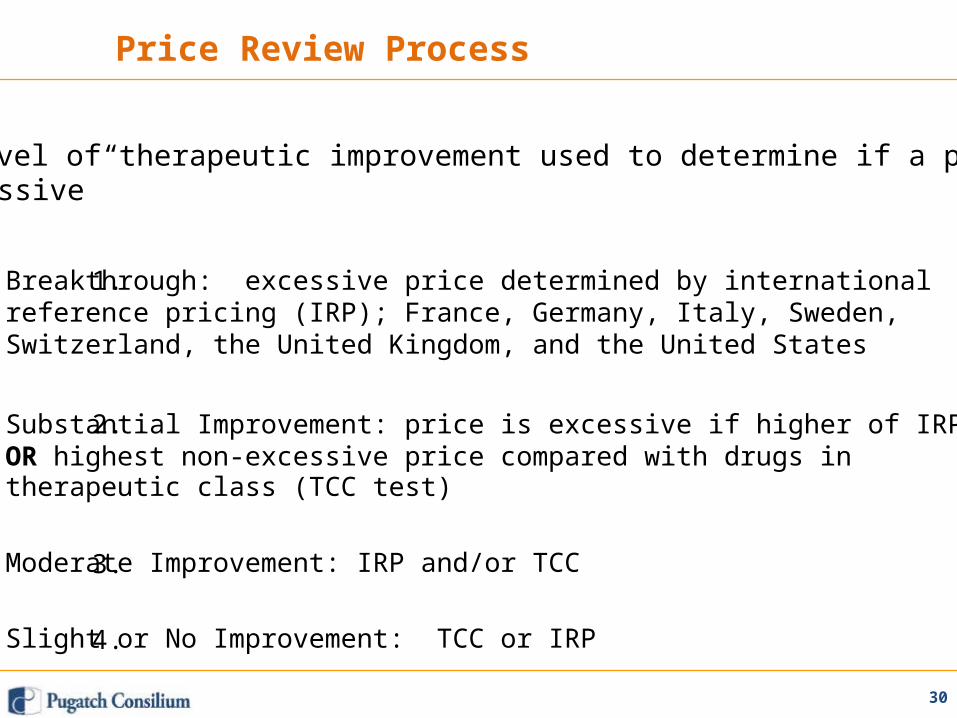

• Level of therapeutic improvement used to determine if a price is“excessive”

1.

2.

3.

4.

Breakthrough: excessive price determined by internationalreference pricing (IRP); France, Germany, Italy, Sweden,Switzerland, the United Kingdom, and the United States

Substantial Improvement: price is excessive if higher of IRP priceOR highest non-excessive price compared with drugs intherapeutic class (TCC test)

Moderate Improvement: IRP and/or TCC

Slight or No Improvement: TCC or IRP

30

PMPRB Investigations and Hearings

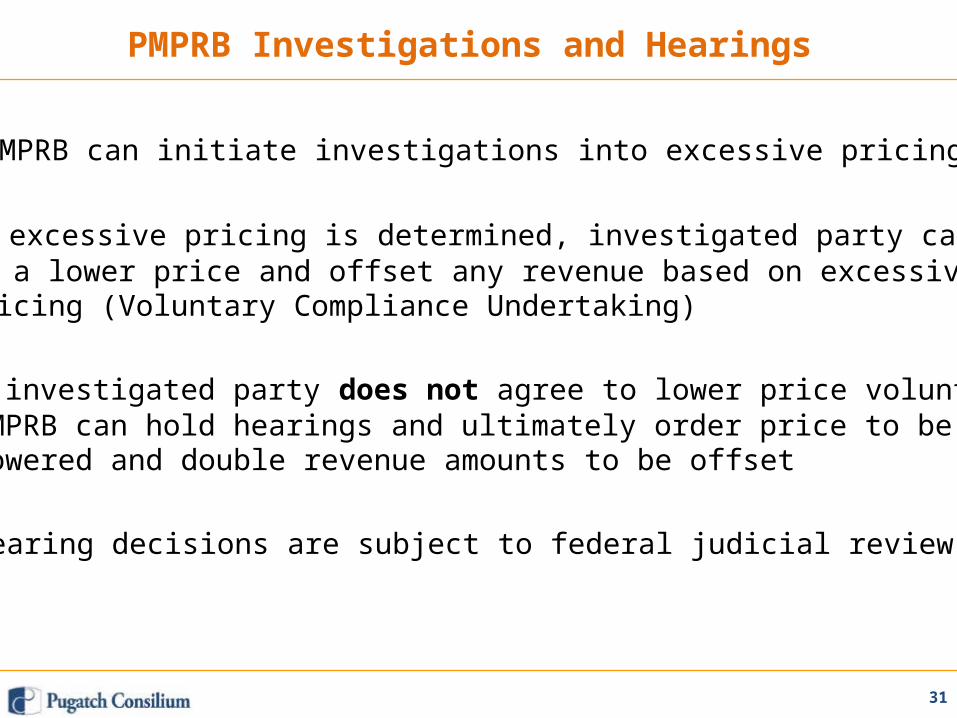

• PMPRB can initiate investigations into excessive pricing

• If excessive pricing is determined, investigated party can agreeto a lower price and offset any revenue based on excessivepricing (Voluntary Compliance Undertaking)

• If investigated party does not agree to lower price voluntarilyPMPRB can hold hearings and ultimately order price to belowered and double revenue amounts to be offset

• Hearing decisions are subject to federal judicial review

31

Reimbursement Policies

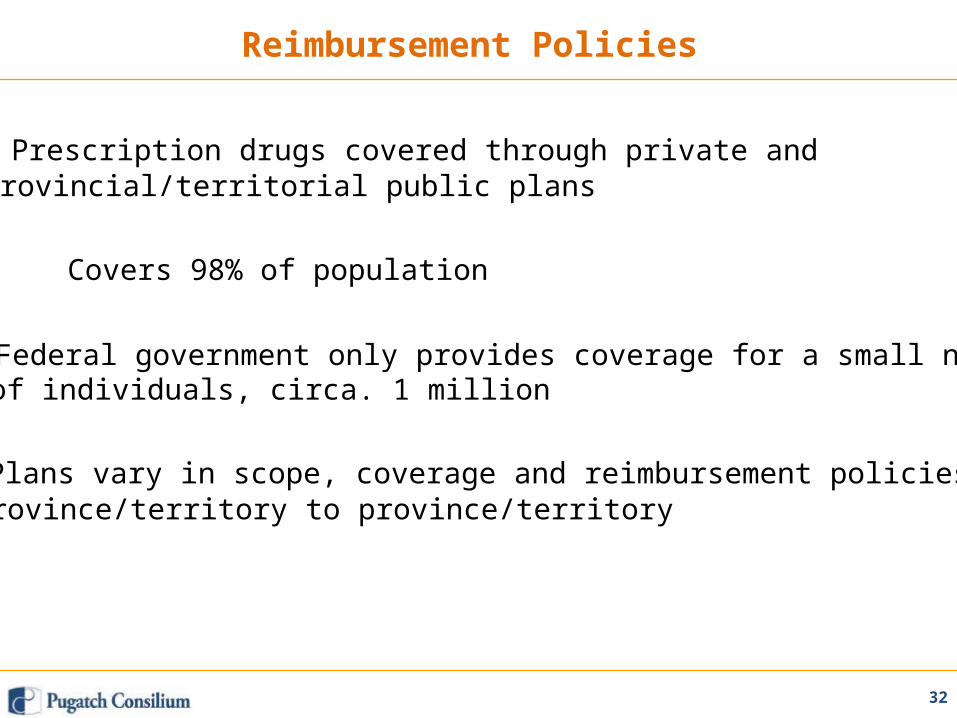

• Prescription drugs covered through private andprovincial/territorial public plans

• Covers 98% of population

• Federal government only provides coverage for a small numberof individuals, circa. 1 million

• Plans vary in scope, coverage and reimbursement policies fromprovince/territory to province/territory

32

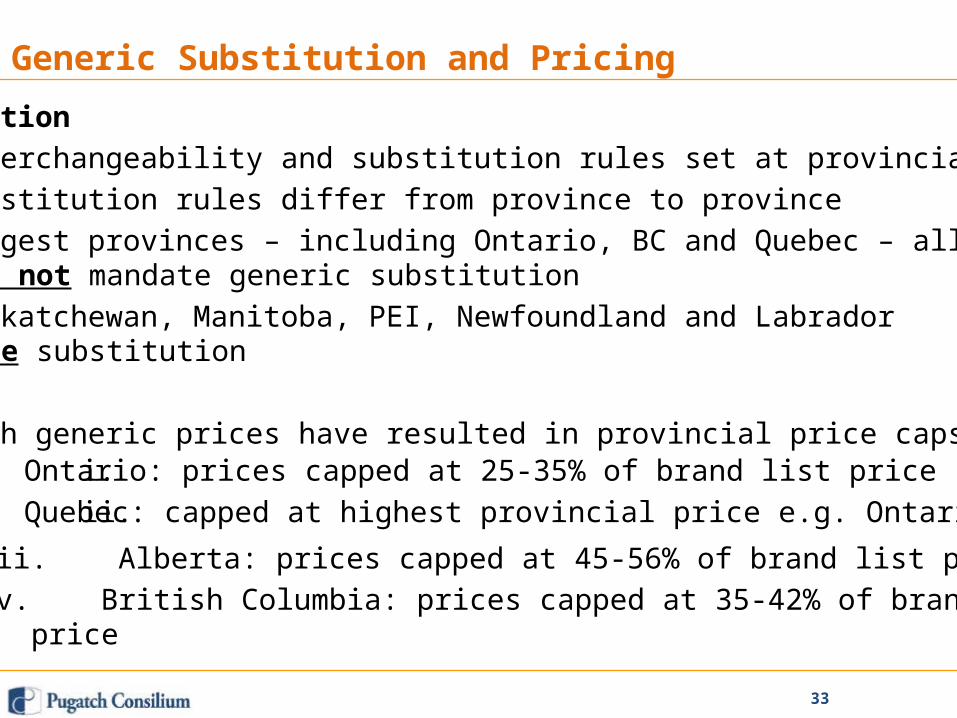

Generic Substitution and Pricing

Substitution• Interchangeability and substitution rules set at provincial level• Substitution rules differ from province to province• Biggest provinces – including Ontario, BC and Quebec – allow,

but do not mandate generic substitution• Saskatchewan, Manitoba, PEI, Newfoundland and Labrador

mandate substitutionPricing• High generic prices have resulted in provincial price caps:i.ii.

Ontario: prices capped at 25-35% of brand list priceQuebec: capped at highest provincial price e.g. Ontario

iii. Alberta: prices capped at 45-56% of brand list priceiv. British Columbia: prices capped at 35-42% of brand list

price

33

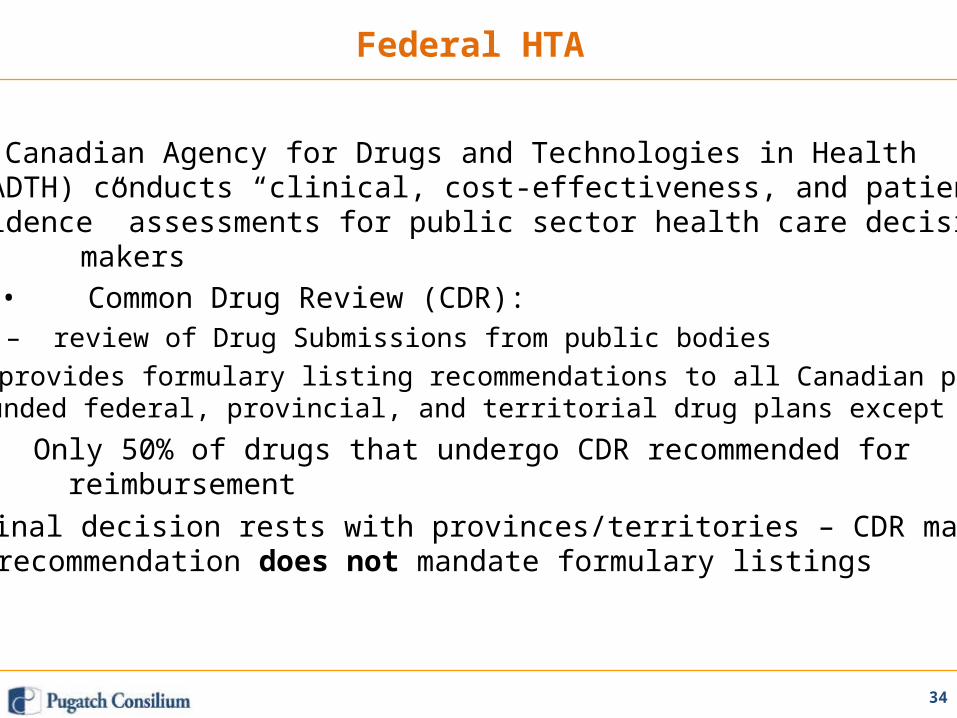

Federal HTA

• Canadian Agency for Drugs and Technologies in Health(CADTH) conducts “clinical, cost-effectiveness, and patientevidence” assessments for public sector health care decision

makers• Common Drug Review (CDR):

– review of Drug Submissions from public bodies– provides formulary listing recommendations to all Canadian publicly

funded federal, provincial, and territorial drug plans except Quebec.• Only 50% of drugs that undergo CDR recommended for

reimbursement• Final decision rests with provinces/territories – CDR makes

recommendation does not mandate formulary listings

34

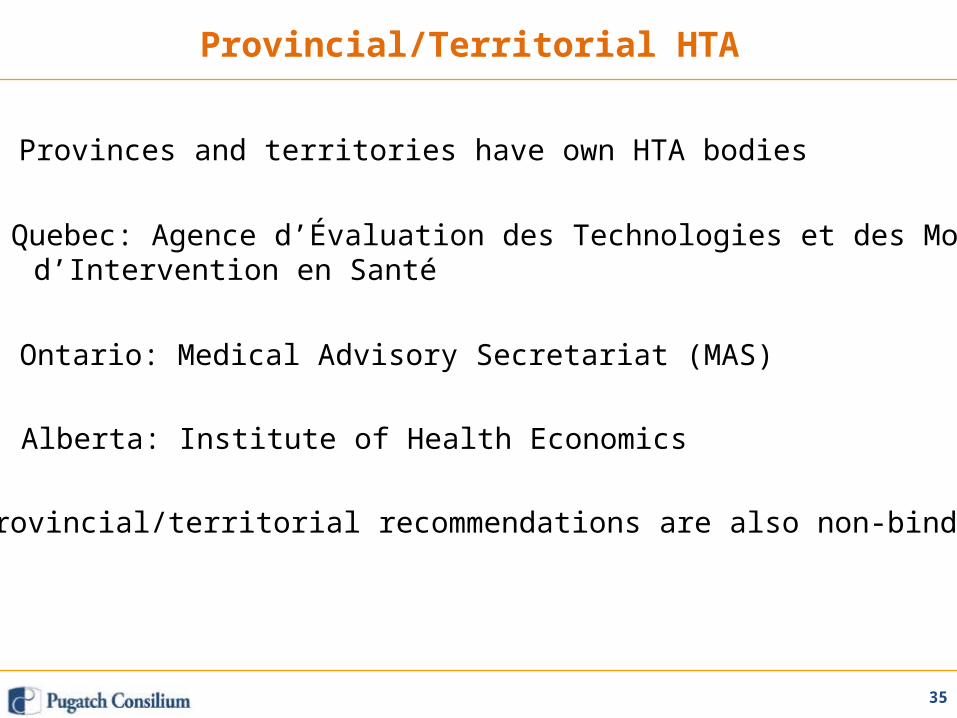

Provincial/Territorial HTA

• Provinces and territories have own HTA bodies

• Quebec: Agence d’Évaluation des Technologies et des Modesd’Intervention en Santé

• Ontario: Medical Advisory Secretariat (MAS)

• Alberta: Institute of Health Economics

• Provincial/territorial recommendations are also non-binding

35

Intellectual PropertyEnvironment

36

Pharmaceutical IP Overview

• History of compulsory licensing up to 1980s – limited R&Dactivity• Compared to other OECD countries Canada has limited

biopharmaceutical IP protection• Judiciary active in field of pharmaceutical IP – rulings often

contradict existing regulations e.g. Bayer (1998), Biolyse v. BMS(2005)

• Utility requirement– growing number of court decisions on the basis of patent utility in

relation to pharmaceutical patents.– High percentage of cases have ruled that pharmaceutical patents

were invalid.– The Canadian standard of utility being established through this

growing case law differs from US and EU as well as TRIPS.

37

Pharmaceutical ‘Patent Linkage’ Mechanism

• Notice of Compliance mechanism in place

• Requires generic applicants to comment on the patent status ofthe reference product

• Significant weaknesses:– does not provide the patent holder (“first person”) with a right ofappeal– the judicial proceedings determining the merits of the disputed

patent(s) is a summary not full process

38

PTE and RDP

• Canada does not offer patent term extensions forpharmaceutical products – currently under discussion in EU-

Canada FTA

• Canada offers a 8 year regulatory data protection term with thepossibility of a six-month pediatric extension

• RDP regulatory changes in 2006 response to Bayer case –reliance is grounds for data protection

39

Biopharmaceutical RegulatoryRequirements

40

Marketing Authorization for New Chemical Entities

• Health Canada’s (HC) Therapeutic Products Directorate (TPD)responsible for drug testing and approval

• New drug submissions required to undergo safety, efficacy andquality testing by TPD

• Average approval time: 18 months from submission of New DrugSubmission (NDS) until the TPD makes a marketing decision

• Priority review (target of 180 days) available for certain drugs(“extraordinary use new drug submission”)

• HC is an official observer and active participant in InternationalConference on Harmonisation of Technical Requirements forRegistration of Pharmaceuticals for Human Use (ICH)

• ICH guidelines and standards adopted by HC

41

Marketing Authorization for Biologics and Biosimilars

• Biological drugs undergo the same procedure and testingrequirements as new chemical entities

• Subsequent entry biologics (biosimilars) pathway introduced in2010

• Canadian biosimilar pathway resembles that used by theEuropean Medicines Agency (EMA)

• Key difference: Applicants may use biological reference productsthat have not received market approval in Canada

• RDP protection/periods the same for biologics and biosimilars asfor small molecule drugs

42

Public Procurement Policies –Pharmaceuticals

43

Public Procurement Policies – Pharmaceuticals

Overview• Pharmaceutical public procurement carried out at provincial and

hospital level – federal purchasing limited• Procurement guidelines issued by provincial governments• Group purchasing common – circa. 90% of hospital/health care

provider procurement through group purchasing organizationPan-Canadian Purchasing Alliance

• 2010 saw agreement between all provinces (expect Quebec) onestablishment of purchasing alliance

• Stated purpose to “consolidate public sector procurement ofcommon drugs and medical supplies and equipment”

• Relatively few drugs purchased so far• 2012 report of Council of Federation announced acceleration of

purchasing of branded drugs and expansion to include generics

44

Thank you!

45