costs and benefits of investing in ecoystem restoration...

TRANSCRIPT

Costs and Benefits of Investing in Ecoystem Restoration and Conservation: Green Growth Opportunities in Katingan Peatlands Technical Report

Component 1B: Green Growth Assessment of Capital Projects

Government of Indonesia - GGGI Green Growth Program

January 2015

2

Table of Contents

EXECUTIVE SUMMARY .................................................................................................................................. 6 1 INTRODUCTION .............................................................................................................................. 19 2 OPTIONS FOR LAND USE AT KATINGAN ......................................................................................... 27 3 METHODOLOGY ............................................................................................................................. 31 4 SCOPE OF ANALYSIS ....................................................................................................................... 36 5 RESULTS ......................................................................................................................................... 42 6 POLICY IMPLICATIONS ................................................................................................................... 62 APPENDIX A LITERATURE REVIEW ....................................................................................................... 77 APPENDIX B MODEL ARCHITECTURE .................................................................................................. 82 APPENDIX C ECOSYSTEM VALUATIONS .............................................................................................. 83

3

List of Figures

Figure 1: The five desired outcomes of green growth developed with key stakeholders in Indonesia . 6 Figure 2: Overview of Katingan Restoration and Conservation Project Area ......................................... 8 Figure 3: Illustration of findings ............................................................................................................ 10 Figure 4: Illustration of Net Present Value results ................................................................................ 12 Figure 5: The five desired outcomes of green growth developed with key stakeholders in Indonesia .............................................................................................................................................................. 20 Figure 6: Stages in conducting project-level eCBA ............................................................................... 22 Figure 7: Planned Project Activities against 5 outcomes of green growth ........................................... 24 Figure 8: Stylized overview of a ‘greened’ planning and project appraisal process in Indonesia ........ 26 Figure 9: Activities against 5 outcomes of green growth ..................................................................... 29 Figure 10: Hypothesis tested by this report ......................................................................................... 30 Figure 11: An impact pathway .............................................................................................................. 36 Figure 12: Illustration of Net Present Value results .............................................................................. 43 Figure 13: Financial analysis; comparison of the Green Growth and BAU scenario (undiscounted net benefits) ................................................................................................................................................ 45 Figure 14: Assumed Palm Oil Yield Curve (years since planting) .......................................................... 46 Figure 15: Palm Oil Financial Costs and Benefits .................................................................................. 47 Figure 16: Logging/Timber Plantation Financial Costs and Benefits..................................................... 48 Figure 17: Land cover map of the Katingan Conservation Area and surrounding region .................... 50 Figure 18: Map of forest biomass carbon stocks in the Katingan Conservation Area .......................... 50 Figure 19: Estimated actual - and assumed marketable - emissions reductions over 25 years ........... 50 Figure 20: PT RMU Ecosystem Restoration Concession Financial Costs and Benefits .......................... 51 Figure 21: eCBA analysis; comparison of the Green Growth and BAU scenario (undiscounted net benefits) ................................................................................................................................................ 52 Figure 22: eCBA Costs and Benefits for Palm Oil Plantations ............................................................... 54 Figure 23: eCBA Costs and Benefits for HTI Timber Plantations ........................................................... 54 Figure 24: eCBA Costs and Benefits for PT RMU project ...................................................................... 56 Figure 25: Variation in results (financial) .............................................................................................. 59 Figure 26: Variation in results (eCBA) ................................................................................................... 59 Figure 27: Palm Oil and Timber international price trends 2009-2014 ................................................ 60 Figure 28: Ecosystem service valuations............................................................................................... 61 Figure 29: Payment Mechanism under a Regional Incentive Fund ...................................................... 72

4

List of Tables Table 1: Summary of results (USD million) ........................................................................................... 11 Table 2: Matrix on Policy Barriers and Enablers of Green Growth Interventions ................................ 14 Table 3: Forest land-use zones in Indonesia ......................................................................................... 22 Table 4: Assumed land use in BAU scenario ......................................................................................... 27 Table 5: Key aspect of BAU Scenario, and identification of expected green growth impacts .............. 28 Table 6: Summary of the Green Growth scenario implementation, and identification of expected green growth impacts ........................................................................................................................... 29 Table 7: Key assumptions applied across the analysis .......................................................................... 33 Table 8: Impact Pathways for RMU ...................................................................................................... 38 Table 9: Summary of results (USD million) ........................................................................................... 43 Table 10: Summary of costs and benefits in each scenario .................................................................. 44 Table 11: Subsidence characteristics of peat land in Kalimantan and Sumatera ................................. 53 Table 12: Estimates for the Global Social Cost of Carbon ..................................................................... 56 Table 13: Variation of input variables in sensitivity analysis (financial) ............................................... 57 Table 14: Variation of input variables in sensitivity analysis (eCBA) .................................................... 58 Table 15: Seven ERC Licenses in Indonesia ........................................................................................... 63 Table 16: Summary of key policy suggestions ...................................................................................... 75

5

GoI-GGGI Green Growth Program

Our joint Government of Indonesia (GoI) and Global Green Growth Institute (GGGI) goal “To promote green growth in Indonesia that recognizes the value of natural capital, improves resilience, builds local economies and is inclusive and equitable”. To achieve this, GGGI provides technical support, research and capacity building that is in line with GoI’s vision and direction Our objectives The specific objectives of the GoI-GGGI Green Growth Program are:

1. To ensure the green growth vision matches or exceeds existing development targets;

2. To track the achievement of green growth priorities of Indonesia by providing relevant targets and indicators;

3. To evaluate the implications of the country’s current development path against green growth targets and indicators and assessing projects and potential policy and investment interventions against this baseline;

4. To identify the key sectors and high potential green growth projects and investment interventions that will help deliver green growth development;

5. To harness private sector engagement and investment in support of delivering green growth opportunities in Indonesia;

6. To undertake economic modeling to analyze each project showing their financial returns and identifying any gaps in the incremental spend required to secure green projects.

How GoI and GGGI will meet these objectives

1

2

“To mainstream green growth within Indonesia’s economic and development planning processes”

“To increase the use of green technology and increase capital investment in green industry” (GIMS)

“To support the development of a funding mechanism that disburses REDD+ finance to catalyze green growth”

“To support key provincial governments in prioritizing and implementing green growth”

Greening the planning process

REDD+ for green growth

Regional engagement

3

The combined work of these components will help to achieve the objectives and the overarching goal of GoI and GGGI.

6

Executive Summary Introduction

The Government of Indonesia (GoI)-Global Green Growth Institute (GGGI) Green Growth Program for Indonesia aims to promote green growth in Indonesia that recognizes the value of natural capital, improves resilience, builds local economies and is inclusive and equitable. A fundamental part of this will be mainstreaming green growth within Indonesia’s economic and development planning processes. To this end, GGGI with GoI are developing a framework and suite of tools that can be used by GoI to help embed green growth concepts into existing planning and investment appraisal instruments. Full details of the framework can be found in an accompanying report1, but the essence of the framework is to make green growth measurable along the desired five outcomes outlined in Figure 1 below. These outcomes are interrelated and a positive contribution to one can often simultaneously provide benefits to others. Only by making progress along all of these outcomes can Indonesia plan for inclusive and equitable growth that is sustainable over the course of generations. Figure 1: The five desired outcomes of green growth developed with key stakeholders in Indonesia

Similarly, full details of the range of tools needed to embed green growth within planning processes can be found in accompanying reports2, but at the heart of the suite of tools lies a comprehensive and integrated assessment of the monetary Costs and Benefits of capital projects in Indonesia. This includes, but is not limited to, those projects contained in the Master Plan for the Acceleration of Economic Development (MP3EI). This green growth assessment must not only look at financial costs and benefits but economic, social and environmental costs and benefits as well: Extended Cost Benefit Analysis (eCBA). An eCBA can be used by decision makers in government and the private sector to answer key questions such as:

1 GGGI (2015) Scoping green growth in Indonesia. Working Paper GGGI Indonesia Program 2 GGGI (2015) The Role of Extended Cost Benefit Analysis in Public Policy and Planning in Indonesia. Working Paper GGGI Indonesia Program

7

What is the green growth performance of the project compared to a Business As Usual scenario?

What is the value to the economy, society and the environment of this performance?

How can one re-design a project to improve its green growth performance?

What are the synergies and trade-offs among the different outcomes of green growth in doing this?

How much capital investment is required to achieve this improved performance?

What policy instruments are needed to drive investment and behavioural change?

Thus, a project-level eCBA can be viewed as an analytical tool that governments can use to identify the monetary values of public goods, environmental externalities and social returns associated with many projects. In this sense, results of an eCBA can be used as a base of evidence to determine the size of public and private investment flows needed to maximize these values over time.

This report is the third in a series performing project-level eCBAs on selected investments across Indonesia. For this analysis, we3 have selected the Katingan Restoration and Conservation Project (the ‘RMU’ project named after the project developers, PT Rimba Makmur Utama), at the request of the Central Kalimantan planning agency (Bappeda). The project is also representative of peat land issues and one on which we can pilot our eCBA methodologies in practice.

The project is located in the Katingan and Kotawaringin Timur Districts of Central Kalimantan, and covers 203,570 ha of peatland forest area including 150,650 ha of high-density swamp forest, home to large populations of endangered species such as the Bornean orangutan and proboscis monkeys.

The entire project area is classified as convertible and non-convertible Production Forest (HP).

Given the previous land-use classifications (HP, HPK4) and licenses issued (HTI, HPH), it is assumed that land would otherwise be logged, used for pulpwood plantations and/or converted to Palm Oil plantations. These uses of the land therefore constitute our ‘Business As Usual’ (BAU) scenario.

PT Rimba Makmur Utama (PT RMU) has obtained a License for the Commercial Use of Forest Products – Ecosystem Restoration - IUPHHK-RE (Ecosystem Restoration Concession, or ‘ERC’)

from the Ministry of Forestry of the Government of Indonesia5. ERCs are granted to private corporations seeking to conserve and restore Production Forests in Indonesia. In law, the ERC prevents the use of the project area for activities such as Palm Oil plantations, Industrial Timber plantations, selective logging etc. and obliges the developer to restore ecosystems through measures such as canal blocking, peat rewetting, reforestation and species reintroduction. Carbon storage and sequestration credits will be generated under the international Verified Carbon Standard (VCS) offset scheme, with Climate Carbon Biodiversity Alliance (CCBA) certification to reflect the wider social, environmental and biodiversity benefits of the project. The RMU project constitutes our ‘green growth’ scenario.

We note that the RMU project has been re-designed during its inception phase. The facts and figures used in this report relate to the original project design covering an area of 203,570 hectares, as set out in the CCBA Project Design Document, and consistent with the Financial Model provided to us by PT RMU. However, the exact nature of the new license/project design

3 Throughout this document “we”, “our” and “us” refers to the GGGI project team 4 HP: Production Forest, HTI: Industrial Timber Plantations, HPH: Logging Concessions and HPK: Convertible Production Forest (other uses including Palm Oil) 5 Source: Project Design Document

8

(expected to be between 108,000 and 157,000 ha) is not clear, and it is not possible to assess the exact impact of the revised plan on the eCBA results. It is likely though that the revised design will entail less benefit and greater cost per hectare since protecting a smaller area is less environmentally valuable than a larger area in the watershed, and management costs are largely fixed. Despite this change in project design, this report still contributes to the body of knowledge, and provides robust new understanding of the valuation of ERC projects in Indonesia. We are very grateful to PT RMU for sharing their data, insight and time, without which the analysis would not be possible. Figure 2: Overview of Katingan Restoration and Conservation Project Area

Source: Project Design Document

Findings

These two scenarios correspond to two different investment outcomes. Looking solely at the cashflows expected from a typical Palm Oil and HTI Plantation over 60 years, the findings of our financial analysis were that Business As Usual generates $43m higher return (Net Present Value discounted at 10%) even with the assumed carbon/biodiversity incentive of $2-8/tCO2 for the RMU

Proposed area in the watershed between

Mentaya and Katingan Rivers

9

project. And, given the current state of the global carbon markets, and opex escalation since the project design, the realized financial return is likely to be significantly lower. These findings correspond to the left hand side of the graphic in Figure 3. Conducting an Extended Cost Benefit Analysis tells a different story though. Accounting for the hidden costs of Business As Usual avoided under Green Growth, and valuing properly the full range of benefits occurring under an Ecosystem Restoration Concession, we estimate that the net societal benefit from the activities taking place at the Katingan site are $9.5bn higher than the Business As Usual scenario (in Net Present Value terms discounted at 5%). These findings correspond to the right hand side of the graphic in Figure 3. The benefits of the Green Growth scenario above can be broken down as follows:

Economic Growth benefits of $35m; value of 224 MtCO2 of avoided emissions credit sales at an average of $6.9/tCO2, $49m of sustainable (low impact, native species) logging revenues once PT RMU has restored the peat swamp forest, and $24m of agriculturally productive land bequeathed to the next generation. Minus capital and operational costs.

Social benefits of $4m; Socio-cultural value of the standing forest to local communities.

Ecosystem benefits of $232m; the value of standing forest to local communities including fuelwood, agricultural use, fisheries, and local and global biodiversity value (which in turn could drive eco-tourism).

GHG emission benefits of $9,702m; avoided climate change damages of rising sea levels, agricultural productivity loss, more frequent extreme weather events etc. (at $80/tCO2, minus credit monetized value above). This is the largest benefit category, although depends heavily on assumptions around carbon volumes and value.

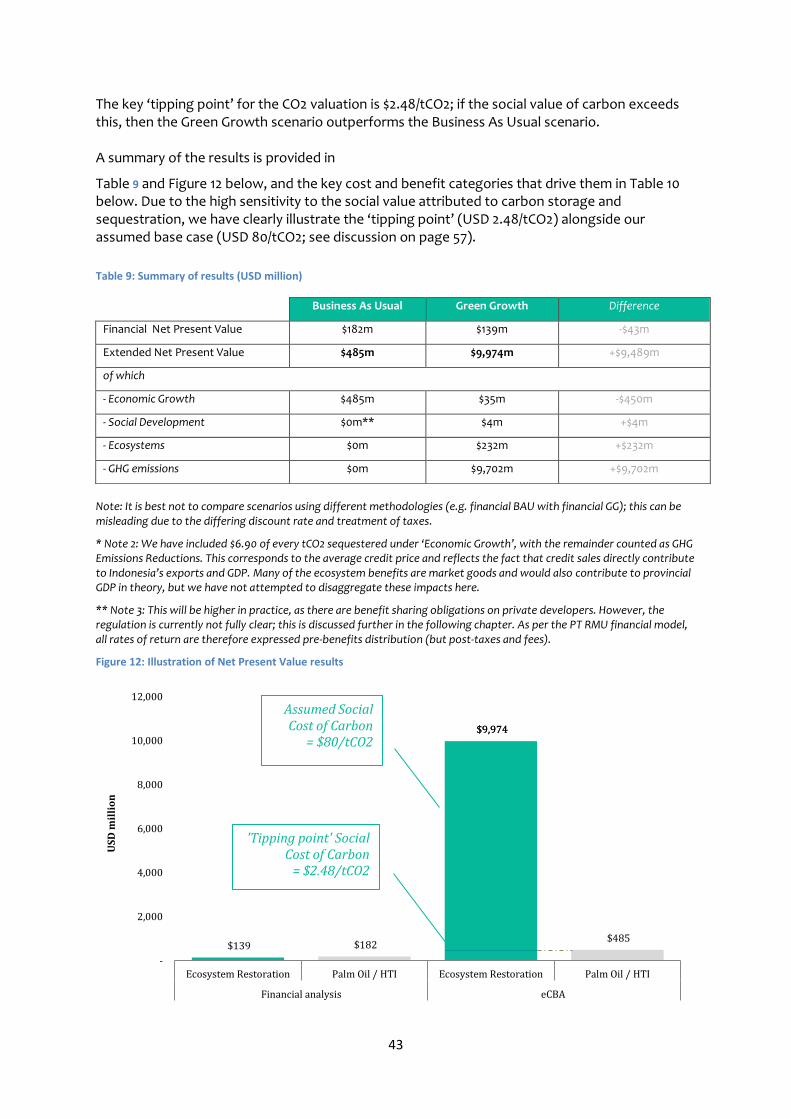

The key break-even point for the CO2 valuation is $2.48/tCO2; if the social value of carbon exceeds this, then the Green Growth scenario outperforms the Business As Usual scenario (see Figure 4). However, this is at the very lowest end of the range in the literature, suggesting that the real value will be shown to be higher than this (see discussion on page 57). In addition there are hidden costs included in the net value of the BAU scenario, including:

Peat soil drainage issues causing flooding and significant yield deteriorations over time (a net present cost of around $297m)

Negative knock-on impacts to surrounding agricultural landscapes within the same watershed (a net present cost of around $295m)

Figure 3: Illustration of findings

We note that our methodology for valuing ecosystem services is conservative and follows a local Ministry of Environment study focused on marketable goods and services. Some studies would have the total ecosystem benefits up to ten-times higher6. Furthermore, the RMU project sits in a relatively small watershed in a coastal location. In a more upstream location the soil/hydrology impacts would likely be significantly higher. Also, we have not quantitatively included stranded assets such as the palm oil mills that would likely be left idle as local concessions flood and become unproductive. If these were included, the BAU scenario would decline in value. At the same time, we have been generous to the Business As Usual scenario, where most benefits come from commodity revenues. These are volatile and unpredictable, and the price of Crude Palm Oil alone has fallen 18% since year-end 20137. In short, a full analysis reveals that Business As Usual generates only uncertain, short-term cash and a number of hidden costs for investors and the wider economy. Green growth, conversely, generates sustainable, stable benefits. Table 1 and Figure 4 below summarize these findings. Table 1: Summary of results (USD million)

Note: Resilience is not valued since it is a cross-cutting theme, impacted by the other 4 outcomes of green growth; for example communities are less vulnerable to commodity price shocks or flooding from climate change, which are ‘economic’ and ‘ecosystem’ impacts in their own right.

6 Van Baukering et al (2008). See page 56 for details. 7 Source: World Bank Global Economic Monitor This is not reflected in our final results as we take a long-term assumption for the value of Fresh Fruit Bunches ($150/tonne).

Business As Usual Green Growth Difference

Financial Net Present Value $182m $139m -$43m

Extended Net Present Value $485m $9,974m +$9,489m

of which

- Economic Growth $485m $35m -$450m

- Social Development $0m $4m +$4m

- Ecosystems $0m $232m +$232m

- GHG emissions $0m $9,702m +$9,702m

12

Figure 4: Illustration of Net Present Value results

Policy

The quantitative analysis that took place for this study has two major conclusions:

1. From a societal perspective, ERC is an optimal use of land at this (and similar) site(s)

2. Under current market conditions, the cash incentive to invest in ERC is limited Given these two points, there is a clear rationale for public policy intervention. Based on our quantitative analysis, a literature review, stakeholder consultation and interviews with PT RMU, we have identified a number of supporting policy interventions that would be helpful to support ERC projects and drive investment across suitable degraded land sites across Indonesia. Individually, these are not new recommendations, but do need to be addressed in a novel and systematic way if ERC projects are to get off the ground:

Addressing regulatory issues; streamlining the licensing cost and process.

Reducing business and financial risks; ensuring a stable CO2 price with the help of Indonesian and international funds.

Improving financial performance; ensuring a reasonable CO2 price supported by multi-commodity strategies including Non-Timber Forest Products and Biodiversity monetization, as well as opening access to low-cost debt finance.

Improving land use governance; in the long-run, appropriately zoning potential ERC areas to avoid competition with commodity extraction activities and ensuring enforcement of the law.

Incentivizing local government to support ERC; compensating local government for land swap costs, and ensuring sufficient fiscal incentives exist to support ERC projects. This policy objective needs to be a priority.

The policy matrix in Table 2 below explains in more detail the identified barriers to the success of ERC projects and the potential policy remedies. These have been categorized according to whether they are for the benefit of (or incentivize) primarily investors, government or communities.

$139 $182

$9,974

$485

$9,974

-

2,000

4,000

6,000

8,000

10,000

12,000

Ecosystem Restoration Palm Oil / HTI Ecosystem Restoration Palm Oil / HTI

Financial analysis eCBA

US

D m

illi

on

Assumed Social Cost of Carbon

= $80/tCO2

'Tipping point' Social Cost of

Carbon = $2.48/tCO2

13

This is a complex list of policies, but the overarching story around ERCs and how to promote them in the short-term is simple. Tangible sources of finance, such as carbon finance, are needed to bridge the gap for investors while broader policy reforms and economic development takes place. The analogy the project developers, PT RMU, use is one of a patient with a broken leg: “The forests are broken. Carbon revenue is the 'crutch' needed to get them walking again after a period of rest and recovery. The more crutches investors can access, the faster the forest will recover. And as the forests recover eventually investment in wider sustainable economic activities such as non-timber forest products, eco-tourism will be viable and self-sustaining. But only then can the forests walk again on their own two feet and no longer need the crutch” Rezal Kusumaatmadja PT RMU COO

14

Table 2: Matrix on policy barriers and enablers of green growth interventions

Key Issue Proposed Policy Intervention Expected Outcome

Po

licy

fo

r In

vest

ors

Addressing Regulatory Issues

Uncertainty regarding licensing (time and cost)

Streamlining and increasing the transparency of the ERC licensing process Greater government participation in the project: local government acquires the land and/or licenses

Decreased legal uncertainty and implementation delays Reallocation of regulatory risks to local government and de-risking of the investment

Addressing Business/Financial Risks

Absence of proven business model

Additional one-off support for early stage projects such as tax holidays

Awareness raising of long-run impacts of peat drainage in the business community

Increased investor confidence that ERC projects are practical

Increased investor understanding of the hidden costs of BAU

Financial risks (uncertainty regarding CER/VCS prices / volumes)

National Carbon Market and stabilization fund (minimum price at which GoI would buy a guaranteed volume of credits)

Other bilateral and multilateral guarantees

Decreased financial risks

Improving financial performance

Low returns on investment relative to commodities

Land swap (land suitable for palm oil expansion vs. HCV land)

Application of Polluter Pays Principle through carbon pricing

Decreased (legal) opportunity cost of investing in ERC in degraded peat swap forest

Low absolute returns on investment

Mandate a government agency to monitor leakage or absorb risk of spiraling monitoring costs

Decreased operation costs and improved financial performance

Allow concession fee to be paid in installments

Lower capital costs and higher financial performance

15

Provide preferential long-term funding to ERC developers through REDD+ Fund

Reduced cost of capital and improved financial performance

Po

licy

fo

r G

ove

rnm

ent

Incentivizing Government

Perceived attractiveness of commodity revenues and fiscal opportunity cost of ERC (national/provincial)

Clear spatial plan, including zoning of HCV areas (validation of ‘one map’)

Increase in palm oil output without further deforestation

Fiscal opportunity cost of land swaps (especially at district level)

Redirect revenue flows from project developers from national to local government

Intergovernmental fiscal transfers

Compensate eventual losses in fiscal revenues for local governments

Costs and benefits (including future fiscal liabilities) not included in decision making

Include green growth tools and methodologies in project and planning appraisal

Internalization of ecosystem service values into planning and investment decisions

Po

licy

fo

r C

om

mu

nit

ies

Addressing Social Risks

Absence of socio-economic opportunity means land clearance activities continue (or are simply displaced elsewhere; leakage)

Clarify benefit sharing mechanisms and establishing guidelines for participatory processes

Benefits funneled into long-term trust funds used to support livelihood development

Establish guidelines to assist developers include livelihood development in project design

Viable alternative to land clearance activities and sustainable long-term livelihoods

Greater buy-in for project and reduced monitoring and enforcement costs

16

Final remarks

We believe that these results provide a valuable contribution to the evidence base for green growth policymaking in Indonesia, both at national and sub-national levels. However, there are some caveats. While the principles of the methodology are well-established, the application is experimental and only the third, pilot, analysis in a series of analyses to be refined with stakeholders. Despite the best efforts of the team to validate all assumptions and findings with stakeholders, inevitably the results are subject to a degree of uncertainty, especially the counterfactual Business As Usual scenario. Therefore, some data gaps had to be filled with national and international proxies.

The specific results of this analysis are not, by themselves, suitable for investment decision making. While effort has been made to use local information wherever possible, data has not been universally available, and international proxies have been used in the analysis. Business implications are drawn without detailed feasibility studies, and the analysis has been designed to inform the policy debate rather than capital allocation decisions. In addition, we have not assured the data provided to us by PT RMU. The Global Green Growth Institute, its partners and contractors, do not verify, validate or endorse the social, economic or environmental performance of individual investments or projects.

Nonetheless, we hope that the analysis provides a tangible example of how to quantify and monetize a broad range of impacts at the project-level, and provides inspiration for the practical embedding of green growth theory into everyday planning processes. All feedback and comments are gratefully received by the project team.

17

Glossary Acronym Explanation

AMDAL Environment Impact Assessment

BAU Business As Usual

BCR Benefit-Cost ratio

BMP Best Management Practices

c.i.f Cost insured freight

CCBA Climate, Community and Biodiversity Alliance

CER Certified Emission Reduction

CO2 Carbon Dioxide

CPI Consumer Price Index

CPO Crude Palm Oil

eCBA Extended Cost Benefit Analysis

ERC Ecosystem Restoration Concession

f.o.b Free on board

FFB Fresh Fruit Bunch

FREDDI Fund for REDD+ Indonesia

GDP Gross Domestic Product

GIMS Green Industry Mapping Strategy

GGA Green Growth Assessment

GGAP Green Growth Assessment Process

GGF Green Growth Framework

GGGI Global Green Growth Institute

GHG Green House Gas

GoI Government of Indonesia

ha Hectare

HCV High Conservation Value

HP Hutan Produksi Production Forest Concession

HPK Hutan Produksi Conversi Production Forest Concession: Convertible

HTI Hutan Tanaman Industri Production Forest Concession: Industrial Timber

HPH Hak Pengusahaan Hutan Production Forest Concession: Selective Logging

IPB Bogor Agricultural University

IPCC Intergovernmental Panel on Climate Change

IUP-PAN-KARBON Business License for Carbon Sequestration and/or carbon storage

IUPHHK-RE Ecosystem Restoration Concession

Kalteng Central Kalimantan

KEK Special Economic Zone

18

KFCP Kalimantan Forest and Climate Partnership

KLH Ministry of Environment

KSN Strategic National Zone

kWh Kilowatt hour

LCOE Levelized Cost Of Electricity

LULUCF Land Use, Land Use Change and Forestry

Menhut Ministry of Forestry

MP3EI Master Plan for the Acceleration of Economic Development

MSL Mean Sea Level

Mt Megatonne (1 million tonnes)

MtCO2 Megatonne Carbon Dioxide

MTHW Mixed Tropical Hardwood

NPV Net Present Value

NTFP Non-Timber Forest Products

PDD Project Design Document

PES Program for Ecosystem Services

PPP Public Private Partnership

PT REKI Ecosystem Conservation and Restoration Indonesia Ltd.

PwC Pricewaterhouse Coopers

RAN/D-GRK National/Regional Action Plan for Reducing Greenhouse Gas Emission s

REDD+ Reducing Emissions from Deforestation and Forest Degradation

RMU PT Rimba Makmur Utama

RPJMD Region Medium Term Development Plan

RPJMN National Medium Term Development Plan

RSPO Roundtable on Sustainable Palm Oil

SDR Social Discount Rate

SOC Social Opportunity Cost

tCO2 Tons of Carbon Dioxide

TEV Total Economic Value

TNC The Nature Conservancy

TV Terminal Value

UNORCID UN Office for REDD+ Coordination in Indonesia

VAT Value Added Tax

VCS Verified Carbon Standard

WACC Weighted Average Cost of Capital

19

1 Introduction

Indonesia Green Growth Program

The Government of Indonesia (GoI) and Global Green Growth Institute (GGGI) have developed a program of activity that is aligned and wholly supportive of achieving Indonesia’s existing vision for economic development planning. The aim is to show, using real examples of Indonesia’s development and investment plans at national, provincial and district levels, how economic growth can be maintained while reducing poverty and social inequality, maximizing the value of ecosystem services, reducing GHG emissions, and making communities, economies, and the enviroment more resilient to economic and climate shocks.

The overarching goal of the Government of Indonesia-Global Green Growth Institute Green Growth Program for Indonesia is to promote green growth in Indonesia that recognizes the value of natural capital, improves resilience, builds local economies and is inclusive and equitable.

The program has a number of specific objectives (see page 5), and three complementary components:

1. Greening the Planning process. Aim: ‘To mainstream green growth within Indonesia’s economic and development planning processes’ and ‘To increase the use of green technology and increase capital investment in green industry’

2. REDD+ for green growth. Aim: ‘To support the development of a funding mechanism that disburses REDD+ finance to catalyze green growth’

3. Regional engagement. Aim: ‘To support key provincial governments in prioritizing and implementing green growth’

This report supports Component 1 in mainstreaming green growth in planning processes. As part of this component, the GoI and GGGI are developing a framework and suite of tools that can be used by GoI to help embed green growth principles into existing planning and investment appraisal instruments and processes.

Mainstreaming green growth in planning processes

Currently there is no single, internationally accepted analytical framework or set of indicators to monitor green growth performance8. As a starting point, GoI and GGGI have initiated a discussion with key stakeholders on what represents an appropriate framework to define what green growth means to stakeholders in Indonesia. Green growth planning needs to be undertaken in an integrated manner and on a comprehensive basis. It is important to understand the interdependencies between the country’s economic competitiveness drivers and their implications for social development and environmental performance.

A Green Growth Framework (GGF) is being developed which brings together a set of social, economic and environmental indicators across 5 outcomes of green growth. These are all quantifiable and measurable, and provide a relevant framework for Indonesia to think about what green growth means to the country and the desired outcomes to be achieved through green growth.

8 Green Growth Knowledge Platform, 2013

20

Figure 5: The five desired outcomes of green growth developed with key stakeholders in Indonesia

This Green Growth Framework can support decision making and prioritization of economic planning instruments, across national and sub-national government. A key part of decision making in this context is the selection and improvement of capital projects, such as those found in the Master Plan for the Acceleration of Economic Development (MP3EI).

The GoI together with the GGGI is developing a tool to help operationalize the GGF within government and measure the green growth performance of investments. This tool is called the Green Growth Assessment Process (GGAP). GGAP is a 9-step process using indicators specific to projects, sectors, districts, provinces and Indonesia as a nation, as well as a range of other tools, and can be used by government:

To allocate resources to the projects with the highest green growth potential;

To re-design and optimize publicly-funded projects; and,

To build a business case for projects with green growth benefits in order to attract private investment.

A full overview of the GGF and GGAP is available in an accompanying report9, but in brief the GGAP is fed with proposed capital projects from different government economic development strategies and sectoral development plans, and applies indicators under the GGF to prioritize those that contribute most to green growth. Different design options for this shortlist of prioritized investments undergo a Green Growth Assessment. For the purpose of capital project assessments we apply a project-level Extended Cost Benefit Analysis (eCBA) methodology. The project-level eCBA is intended to provide a holistic and comprehensive understanding of the impacts of investments through a focus on the measurement and valuation of their green growth implications in rigorous, economic terms. It is often used in the application of Multi Criteria Analysis (see page 26), providing the social, economic and environmental valuations needed to make decisions.

Based on the results of the project-level eCBA, and ongoing monitoring of green growth performance, aspects of these investments can potentially be re-designed. The identification of potential project re-designs can help inform policy developments and other enablers.

9 GGGI (2015) Scoping green growth in Indonesia. Working Paper GGGI Indonesia Program

21

This paper is the third in a series of papers conducting project-level eCBAs on a range of individual investments.

Box 1: Green Growth Indicators

The Green Growth Framework ultimately rests on the indicators used to define and measure green growth in practice. There are three broad functions/types of these indicators:

1. Diagnostic indicators: designed to assess the overall sustainability of Indonesia and to identify key issues that should be considered in the mainstreaming of the green growth Planning process;

2. Planning indicators: designed in accordance with the Pressure-State-Response approach and so useful for assessing the cause-effect linkages between sustainability issues highlighted by diagnostic indicators and their pressures and impacts;

3. Monitoring and Evaluation (M&E) indicators: designed to help track green growth progress and performance of Indonesia.

Indicators can be applied at different levels, including at the national, regional, sectoral and micro (project) levels (see Figure 5). All indicators within this report fall under the category of ‘project-level’ indicators.

The methodology applied at project level naturally supports functions 1 and 3 above: Diagnosis and M&E. eCBA provides a set of indicators that can be used for diagnosis of the project baseline across each of the five outcomes of green growth, and also sets out rigorous indicators that can be used for future project Monitoring and Evaluation. When aggregated across a number of projects, or particularly large projects, they may also support planning functions (Function 2).

For further details on indicators and their role in the planning framework, the reader is referred to the references footnoted on the previous page10.

Green Growth Assessment

Within the Green Growth Assessment of Capital Projects, eCBA is the key methodology used to value social, economic and environmental costs and benefits. Cost Benefit Analysis (CBA) is a toolkit used by economists and other decision makers to evaluate the desirability of a policy or project by systematically comparing costs and benefits. These costs and benefits are measured in terms of ‘social welfare’.

Social welfare is a technical term used by economists to measure the ‘utility’ of a population, as opposed to ‘private welfare’ which is just the utility of the individual. Social welfare includes all economic (material goods), social (community cohesion), and environmental (ecosystem services) benefits that an economy, society and nature provide.

In practice, calculating social welfare entails focusing on measurable economic costs and benefits, and including social and environmental factors not accounted for in market prices. We use the term Extended CBA (eCBA) to emphasize that our methodology assesses these non-market, social and environmental externalities as much as is practical and takes account of redesign options for the project to improve its green growth performance (this latter point differentiates eCBA from Social Cost Benefit Analysis (SCBA).

A project-level eCBA provides evidence for decision makers to inform decisions on whether a project should go ahead. If the total benefits exceed the total costs, then the project can be considered to be justified in net social welfare terms although the decision to proceed will inevitably be subject to a wider range of considerations (such as affordability). But, investors will usually only take forward projects where the private benefits exceed the private costs. Due to

22

the presence of market imperfections and ‘missing’ markets (e.g. ‘public goods’ such as clean air), private incentives are not always aligned with achieving optimal social outcomes. Therefore, a key objective of the project-level eCBA is to cast light on the difference between these and suggest policies to help align them.

The practical process of conducting a project-level eCBA requires 6 stages as outlined in the Figure 6 below.

Figure 6: Stages in conducting project-level eCBA

Identify and consult project stakeholders

Review project documentation

Establish project rationale and need

Consult project stakeholders

Consult experts

Literature review

Identify outputs, outcomes and impacts

Identify potential scope for eCBA

Assess materiality: Identify actual scope for eCBA

Collect data from project documentation

Collect local market data

Collect international technology data

Value costs and benefits of green growth interventions

Consider implications of results for policy

Consider implications for project re-design and investment

Validate findings with stakeholders

The Katingan Restoration and Conservation Project (the RMU project)

The RMU project is located in the Katingan and Kotawaringin Timur Districts of Central Kalimantan, and covers a total area of 203,570ha of peatland forest area – including 154,892 ha of peat swamp forest, home to large populations of endangered species including the Bornean orangutan and proboscis monkeys. The entire project area is located in convertible and non-convertible Production Forest split between two functions: commercial logging; and palm oil production.

Around 12% of the project area (24,428 hectares) is classified as HPK and legally eligible for conversion to an oil palm plantation. The remaining 88% of the project area (179,142 hectares) is legally eligible for selective logging, and, for those areas containing peat soil less than 3 meters deep, to become HTI plantations.

Numerous HTI and HPH licenses have been issued in the project reference region, suggesting that the project areas classified under HP would be highly likely to be commercially developed. Recalling that 33 large palm oil plantations have already been developed in the vicinity of the project area, covering around 278,000 ha in areas with similar biophysical characteristics to the project area, it is reasonable to assume that the project areas classified as HPK would undergo conversion into palm oil plantations.

Table 3: Forest land-uses in Indonesia

Acronym Bahasa Indonesia English

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5 Stage 6

Identify project baseline

Identify Green Growth options

Map Impact Pathways

Collect data

Cost Benefit Analysis

Validate Findings

23

HP Hutan Produksi Production Forest Concession

HPK Hutan Produksi Conversi Production Forest Concession: Convertible

HTI Hutan Tanaman Industri Production Forest Concession: Industrial Timber

HPH Hak Pengusahaan Hutan Production Forest Concession: Selective Logging

Conversion to an oil palm plantation would entail the drainage of the peat areas and clearance of the above-ground biomass to enable the planting of oil palms. Peat drainage involves the digging of canals, allowing water to gradually drain away from the wet soil. Drainage results in the oxidation of carbonic matter, which releases large amounts of GHG into the atmosphere. Moreover, ‘peatland drainage leads to subsidence, which in turn leads to reduced drainability [increased flooding], declining productivity and in lowland areas often eventually results in abandonment of land for agricultural production’10.

It is already well-known internationally that the conversion of peatland to agricultural and other plantation uses can have serious adverse consequences for peat soil drainage and subsidence11. For example, the Sacramento-San Joaquin Delta in California was drained “over a century ago for agriculture and human settlement and has since experience subsidence rates that are among the highest in the world”12. Evidence on the topic is less available in South East Asia due to less published research, but the mechanisms are the same and according to some literature, subsidence on drained peatland may exceed two meters within a few decades, supporting the case that areas with peat over 2 metres in thickness are unsuitable for conversion to agriculture13.

In other words, palm oil development and drainage on peatland may permanently impair the agricultural potential of the land. In the short term, it will increase risks of flash floods during the rainy season, and water scarcity during the dry season, affecting plantation yields and production costs.

The creation of industrial timber plantation (HTI) for pulpwood would entail very similar activities with the same results14.

Selective logging (the harvesting of select tress for sale as timber) would also require canals for wood transport, as is already evident at the site15. However, these are generally smaller than the canals used to deliberately drain land for planting and so are less hydrologically disruptive. In this area it is also likely that selective logging would happen on a ‘less commercial’ scale (i.e., less intense are more driven by local communities rather than large corporates), since the area has already been significantly logged over.

PT Rimba Makmur Utama (PT RMU) has obtained a License for the Commercial Use of Forest Products – Ecosystem Restoration – IUPHHK-RE (Ecosystem Restoration Concession, or ‘ERC’) from the Ministry of Forestry of the Government of Indonesia16. ERCs are granted to private corporations seeking to conserve and restore Production Forests in Indonesia. In law, the ERC prevents the conversion of the project area to non-forest use for 35 years.

10 Deltares, 2012, Subsidence in drained coastal peatlands in SE Asia: implications for sustainability 11 Stephens et al (1984), Rojstaczer & Deverel (1993), Hirano et al (2012) 12 Knox et al (20140) Agricultural peatland restoration: effects of land-use change on greenhouse gas fluxes in the Sacramento-San Joaquin Delta. 13 Deltares, 2012, Subsidence in drained coastal peatlands in SE Asia: implications for sustainability 14 Source: Project Design Document. See also IPCC (2013) Supplement to the 2006 IPCC Guidelines for National GHG Inventories: Wetlands for further details on the GHG emissions process, as well as FAO (2014) Towards Climate-responsible Peatlands Management 15 Source: Project Design Document 16 Source: Project Design Document

24

Figure 7 below summarizes the key Katingan Restoration and Conservation project activities. Figure 7: Planned Project Activities against 5 outcomes of green growth

Source: Project Design Document, Team Analysis

Understanding the Results

In this report we calculate the costs and benefits of the Katingan Restoration and Conservation Project compared to BAU scenario. Our headline finding is that implementing eighteen project activities that make up the Katingan Restoration and Conservation Project would result in significant net societal benefits. The full quantitative results are presented in Section 6. The details of scope and methodology are presented in Sections 4 and 5, but it is important to provide context for interpretation of the headline results.

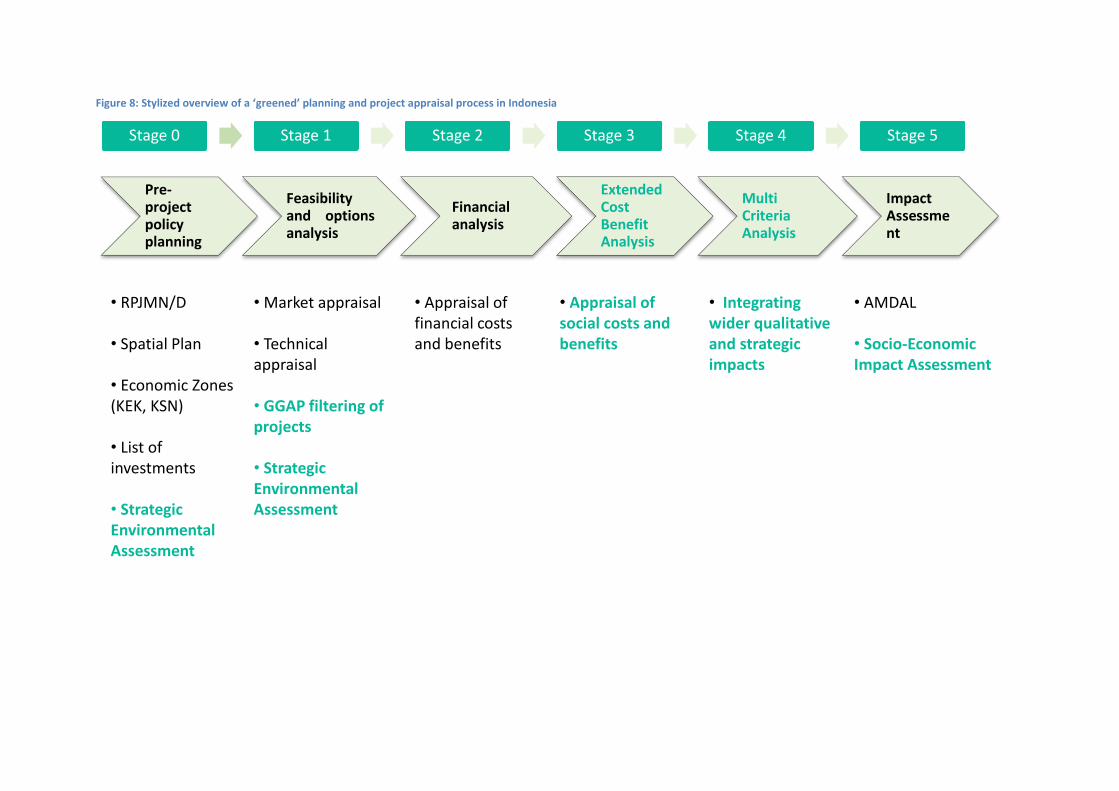

Cost Benefit Analysis is part of a broader project appraisal process and can fit into existing process as explained in Figure 8 on the following page. This allows for key decisions to be made before implementation:

Does it offer net positive benefits and should it proceed?

Are there opportunities to re-design this project to enhance green growth performance?

Are there policies that might drive better outcomes for this and other projects (see next chapter)?

We note that Social Cost Benefit Analysis (sCBA) is already mandatory for Public Private Partnership (PPP) projects in Indonesia, but not necessarily for other investments. Moreover, sCBA is often limited in scope and transparency (see page 64 for more discussion of PPPs).

25

The aim of the project-level eCBA in this report is to test the tool in development on a real project design17 and to contribute to the evidence base for green growth policy in Indonesia, highlighting potential options for improving green growth performance but more importantly demonstrating that valuing the wider implications of decision making, and internalizing them into the project appraisal process, can lead to improved policy outcomes. The project-level eCBA does not substitute for a full feasibility analysis and/or financial appraisal - rather it complements them.

For maximum impact, the project-level eCBA should be combined alongside other green growth tools such as Green Project Prioritization tools, Strategic Environmental Assessment and impact assessment techniques.

The specific results of this analysis are not, by themselves, suitable for investment decision making. While effort has been made to use local information wherever possible, data has not been universally available, and international proxies have been used in the analysis. Business implications are drawn without detailed feasibility studies, and the analysis has been designed to inform the policy debate rather than capital allocation decisions. In addition, we have not assured the data provided to us by PT RMU. The Global Green Growth Institute, its partners and contractors, do not verify, validate or endorse the social, economic or environmental performance of individual investments or projects.

Structure of this report

The rest of this report is structured as follows:

- Section 2 provides different options for delivery and introduces the Green Growth scenarios

- Section 3 provides detailed methodology and reporting framework used in this report

- Section 4 provides a detailed scope of analysis

- Section 5 presents the quantitative results of the Cost Benefit Analysis

- Section 6 outlines some policy implications of the results

- Appendix A provides an overview of literature review

- Appendix B outlines the architecture of the eCBA model

- Appendix C provides key ecosystem valuation coefficients

17 Notwithstanding the project re-design discussed on page 8

Figure 8: Stylized overview of a ‘greened’ planning and project appraisal process in Indonesia

Pre-projectpolicyplanning

Feasibilityand optionsanalysis

Financialanalysis

ExtendedCostBenefitAnalysis

MultiCriteriaAnalysis

ImpactAssessment

Stage 0 Stage 1 Stage 2 Stage 3 Stage 4 Stage 5

• Market appraisal

• Technical appraisal

• GGAP filtering of projects

• Strategic Environmental Assessment

• Appraisal of financial costs and benefits

• Appraisal of social costs and benefits

• Integrating wider qualitative and strategic impacts

• AMDAL

• Socio-Economic Impact Assessment

• RPJMN/D

• Spatial Plan

• Economic Zones (KEK, KSN)

• List of investments

• Strategic Environmental Assessment

2 Options for Land Use at Katingan

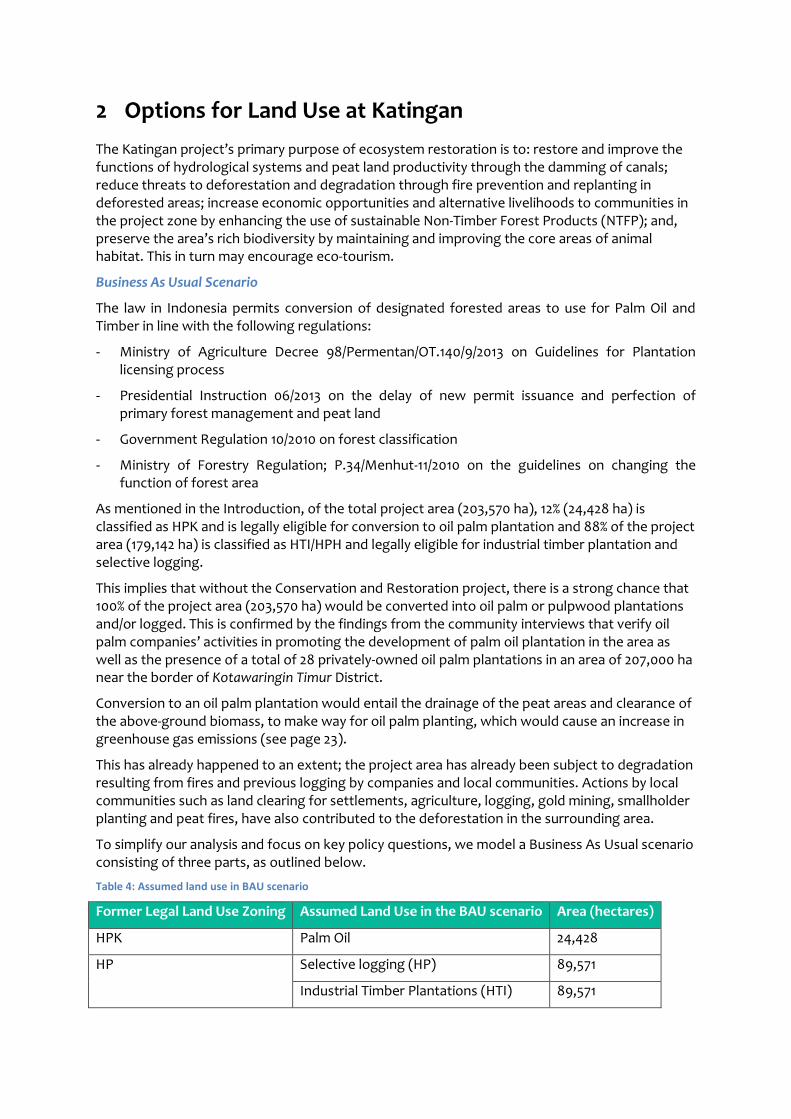

The Katingan project’s primary purpose of ecosystem restoration is to: restore and improve the functions of hydrological systems and peat land productivity through the damming of canals; reduce threats to deforestation and degradation through fire prevention and replanting in deforested areas; increase economic opportunities and alternative livelihoods to communities in the project zone by enhancing the use of sustainable Non-Timber Forest Products (NTFP); and, preserve the area’s rich biodiversity by maintaining and improving the core areas of animal habitat. This in turn may encourage eco-tourism.

Business As Usual Scenario

The law in Indonesia permits conversion of designated forested areas to use for Palm Oil and Timber in line with the following regulations:

- Ministry of Agriculture Decree 98/Permentan/OT.140/9/2013 on Guidelines for Plantation licensing process

- Presidential Instruction 06/2013 on the delay of new permit issuance and perfection of primary forest management and peat land

- Government Regulation 10/2010 on forest classification

- Ministry of Forestry Regulation; P.34/Menhut-11/2010 on the guidelines on changing the function of forest area

As mentioned in the Introduction, of the total project area (203,570 ha), 12% (24,428 ha) is classified as HPK and is legally eligible for conversion to oil palm plantation and 88% of the project area (179,142 ha) is classified as HTI/HPH and legally eligible for industrial timber plantation and selective logging.

This implies that without the Conservation and Restoration project, there is a strong chance that 100% of the project area (203,570 ha) would be converted into oil palm or pulpwood plantations and/or logged. This is confirmed by the findings from the community interviews that verify oil palm companies’ activities in promoting the development of palm oil plantation in the area as well as the presence of a total of 28 privately-owned oil palm plantations in an area of 207,000 ha near the border of Kotawaringin Timur District.

Conversion to an oil palm plantation would entail the drainage of the peat areas and clearance of the above-ground biomass, to make way for oil palm planting, which would cause an increase in greenhouse gas emissions (see page 23).

This has already happened to an extent; the project area has already been subject to degradation resulting from fires and previous logging by companies and local communities. Actions by local communities such as land clearing for settlements, agriculture, logging, gold mining, smallholder planting and peat fires, have also contributed to the deforestation in the surrounding area.

To simplify our analysis and focus on key policy questions, we model a Business As Usual scenario consisting of three parts, as outlined below.

Table 4: Assumed land use in BAU scenario

Former Legal Land Use Zoning Assumed Land Use in the BAU scenario Area (hectares)

HPK Palm Oil 24,428

HP Selective logging (HP) 89,571

Industrial Timber Plantations (HTI) 89,571

28

Table 5 below outlines what the hypothesized impacts of such a scenario might be, based on qualitative team expectations without reference to the quantitative analysis later in this report.

Table 5: Key aspect of BAU Scenario, and identification of expected green growth impacts

Activities under the BAU scenario

Description of expected impact on project area

Expected Green Growth Impact

Conversion to palm oil plantations

Total clearing of forest cover and drainage of the peat. Loss of biodiversity.

Green House Gas Emissions: Forest clearance and peat drainage would release significant quantities of GHG in the atmosphere, increasing climate change risks such as extreme weather events.

Sustained Economic Growth: Significant revenues generated by palm oil, logging and pulpwood plantation activities, although it is unclear for how long these can be sustained given likely flooding from peat soil drainage.

Healthy and productive ecosystems: HPH will contribute to partial loss of forest cover and significant loss of biodiversity. HTI/Palm Oil will cause greater losses of natural forest cover and even greater loss of biodiversity. Drainage of peat generally leads to on-site and downstream flooding.

Inclusive and equitable growth: the development of palm oil and timber activities would generate economic opportunities for local communities but deprive them of ecosystem services upon which their livelihoods were historically built.

Social, economic and environmental resilience: Local communities will be affected by the loss of biodiversity and ecosystem services. They had been relying on such services to provide livelihoods and subsistence opportunities, as well as resilience to climate and socio-economic shocks. However, this may be significantly offset if substantial CSR programs are run by plantation owners.

Conversion to timber plantations

Total clearing of forest cover and drainage of the peat. Loss of biodiversity.

Logging (HPH)

Partial loss of forest cover and (likely) drainage of the peat. Loss of biodiversity.

Key:

Red = Negative impact expected

Orange = Unknown or mild positive / negative impact expected

Green = Positive impact expected

Green Growth Scenario

The Green Growth scenario considered in this analysis refers to the implementation of the Katingan Restoration and Conservation Project. The Project will be managed and implemented within the 203,570 hectare project area, under the Ecosystem Restoration Concession (ERC) business model. ERC license holders are expected to invest in returning degraded or damaged production forests to their biological equilibrium, and preventing deforestation and degradation within their concession area18. Figure 9 below shows which Katingan Restoration and Conservation activities may impact each of the five outcomes of green growth.

In addition to these 18 activities undertaken by PT RMU, we assume in our Green Growth scenario that the land will be suitable for selective logging at the end of the Ecosystem Restoration Concession period. This would entail making use of the hydrologically restored peat swamp forest to nurture native species and use low impact silvicultural methods to harvest.

18 ERCs are regulated by Ministerial Decree 159/Menhut-II/2004 and Ministerial Regulation No 61/2008

29

Figure 9: Activities against 5 outcomes of green growth

Source: Project Design Document, Team Analysis

Grouping these activities into 5 themes, Table 6 below outlines what the hypothesized impacts of the Green Growth scenario might be. Again, this is based on qualitative team expectations without reference to the quantitative analysis later in this report.

Table 6: Summary of the Green Growth scenario implementation, and identification of expected green growth impacts

Activities under Green Growth Scenario

Description of expected impact on project area

Expected Green Growth Impact

Ecosystem Restoration

Maintenance of hydrological regulation functions, reforestation and enrichment in degraded areas

Green House Gas Emissions: The project implementation will support climate change mitigation as it avoids further forest clearance and peat drainage, and associated GHG emissions discussed in the BAU scenario. Better forest management will also increase biomass and carbon storage.

Sustained Economic Growth: In the short-term the Green Growth scenario may not contribute significantly to GDP. However, the project is expected to generate revenues from the sale of carbon credits and create income from other social and environmental activities. Prevention of drainage provides soil suitable for long-run selective logging.

Healthy and productive ecosystems: Maintenance of forest cover and soil integrity will enable hydrological balance in the project and surrounding area; it will also preserve local species’ habitat.

Inclusive and equitable growth: Local communities will be playing a central role in the Green Growth scenario, and

Forest Resource Conservation

Avoidance of biodiversity and ecosystem services losses

Research and Development

Enhancing knowledge and capacity on ecosystem restoration

30

Livelihood Development

Access to economic opportunities

benefit from a wide range of economic empowerment initiatives.

Social, economic and environmental resilience: Local communities will enjoy decreased vulnerability to climate shocks, potentially better access to public services, less volatile incomes, and more resilient ecosystem services providing products for local communities.

Community resilience

Decreased vulnerability to climate and socio-economic shocks

Key:

Red = Negative impact expected

Orange = Unknown or mild positive / negative impact expected

Green = Positive impact expected

Pulling the expected or hypothetical impacts of the two scenarios together, we are therefore testing the hypothesis in this report that green growth will provide a broader range of positive social, economic and environmental outcomes, whereas Business As Usual will generate only short-run financial gain. This hypothesis is illustrated below in Figure 10.

Figure 10: Hypothesis tested by this report

RMU scenarios

Initial conditions

$

Baseline : including negative social and environmental costs

Baseline : excluding negative social and environmental costs

Green Growth Scenario: Ecosystem Restoration Concession

Time

31

3 Methodology

This section summarises the methodological approach used to evaluate the societal costs and benefits likely to be generated by the green growth activities at Katingan.

Introduction to Green Growth Assessment

Within the Green Growth Assessment of Capital Projects, eCBA is the key methodology used to value social, economic and environmental costs and benefits, and underpins the results in this report. These costs and benefits are not always taken into account in decision making as individuals maximize their own private welfare, not necessarily social welfare. Private costs and benefits and social costs and benefits diverge due to the presence of market imperfections. For example, an investor does not always pay for the health damage that industrial effluent from their factory generates to communities downstream so the factory over-produces relative to what would be ‘best for society’, or does not pay for pollution-control technology even though this is cheaper than paying for the health damages inflicted. Principles of Cost Benefit Analysis

It is necessary to consider a much wider range of prices than pure market prices to arrive at the social costs and benefits of a decision (the social opportunity cost (SOC)). We note that these principles are crucial in differentiating eCBA (similar to ‘social cost benefit analysis’) from ‘financial appraisal’ or ‘financial cost-benefit analysis’, which only considers market costs and benefits from the perspective of a private investor.

Social discounting: Discounting is used to compare costs and benefits that occur in different time periods. Society generally prefers one dollar now to one dollar next year. The rate at which costs

and benefits are compared across time (‘discounted’) is called the Social Discount Rate (SDR19). We use a (real) SDR of 5% in our analysis, which is slightly below the standard range for

developing countries (8-15%)20

. This reflects the dominance of climate change and long-term environmental impacts in the analysis, and clearly differentiates the eCBA analysis from a financial appraisal Weighted Average Cost of Capital (WACC). The financial appraisal, on the other hand, uses a WACC of 10%, which is a weighted average of some assumed cost of debt and equity, and depends on corporate/project risk, access to finance, investor characteristics etc. PT RMU uses 12% in its financial appraisal and it is likely that Palm Oil or Timber companies would use a different WACC to reflect their own opportunity cost of capital. In order to facilitate direct comparisons between scenarios, we use 10%, which in real terms is a reasonably standard corporate discount rate in Indonesia. Taxes and subsidies: If there are significant taxes or subsidies present, then market prices will not represent the SOC of a resource (since taxes/subsidies are simply a transfer payment to/from government). In practice, it is not necessary to remove taxes and subsidies from all market prices in the analysis, but only where it makes a material difference to decision making. This is generally where markets are highly distorted. In the context of the RMU project, the main taxes are

19 Or: Social Rate of Time Preference. In the Ramsey (1928) model, SDR is defined as the sum of: the Pure Rate of Time Preference; and the Marginal Elasticity of Utility with respect to Income, multiplied by expected Income Growth. 20 Zhuang et al (2007) ‘Theory and Practice in the Choice of Social Discount Rate for Cost Benefit Analysis’

32

corporate income tax, and local licenses/concession fees, which are removed in the calculation of shadow prices.

Externalities: Where the social cost of the extraction or consumption of a resource differs from the private cost (or equivalently, the benefits), there is said to be an ‘externality’. In extremis, where everyone is affected by the externality, there is said to be a ‘public good’ (clean air) or ‘public bad’ (climate change). Again the market price, determined solely by private costs and benefits, will not reflect the true SOC of the resource or activity. Environmental externalities are pervasive in Kalimantan, with natural capital depletion taking place without account for the effects of:

Carbon release driving global climate change;

Disruption to hydrological cycle;

Destruction of biodiverse habitats;

Degradation of soil; and, other impacts.

Market power: Similarly, if a market is distorted due to oligopolistic or monopolistic market structures, then the market prices will fail to reflect the true opportunity cost of a resource. The most likely relevant distortion is in the palm oil sector where Fresh Fruit Bunch (FFB) prices are not set by market forces, but by provincial government commissions including representations from large palm oil estates and mills21. Yusuf et al (2004) estimated that this distortion to the FFB price is around 23% of the private price22. We have therefore uprated the market price of FFB by 23% for the shadow price calculation.

Tradable goods and Exchange Rates: Tradable goods must be valued as if there are no impediments to trade (i.e., no quantitative restrictions, no import/export tariffs or subsidies). In Indonesia, although timber and CPO are both subject to export VAT and export duty

respectively23,24, we note that pulpwood and FFB are either ineligible or impractical to export and therefore can be treated as non-tradable goods.

We assume that the official exchange rate represents the true opportunity cost of foreign exchange. All dollar values will be uplifted as needed to a 2014 base year using the United States GDP Deflator.

Costs relating to finance: The payment of interest and repayment of principal is often a key part of financial analyses. But, debt service is not relevant for economic and financial analysis in this context because “in both cases what matters is assessing the quality of the project independently of its financing mode”25. Debt service also represents a transfer rather than a use of resources.

Key data and assumptions for this project

The project-level eCBA relies on a wide range of physical and monetary data. It is not always clear cut as to which value to use in a particular calculation due to the constant evolution of markets, uncertainty about the future, missing or inaccessible data, unknown project operational details and so on.

21 Forest Peoples Programme (2006) Ghosts on our Own Land: Indonesian Oil Palm Smallholders and the Roundtable on Sustainable Palm Oil 22 Yusuf et al (2004) Pricing of Palm Oil Fresh Fruit Bunches for Smallholders in South Sumatera 23 PwC Indonesia (2014) “Indonesian Pocket Tax Book 2014” 24 Bloomberg (2013) “Indonesia cuts Palm Oil Export-Tax to Boost Sales as Prices Drop” 25 World Bank Handbook on Economic Analysis of Investment Operations

33

As a general rule, and all other considerations being equal (e.g. data quality), preference was given to data in the following order:

1) Project-specific data (e.g. from PT RMU financial model and Project Design Document)

2) Province-specific data (e.g. FFB prices from Kalteng, ecosystem products from Kalteng)

3) Indonesia-specific data (e.g. timber plantation operating costs from Sumatera)

4) South East Asia-specific data

5) Other comparable international technology or market data

In addition to these quantitative assumptions below, there were two qualitative assumptions made across all areas of analysis.

The first of these was that demand curves are inelastic. That is to say, in no scenario are market prices expected to shift; all prices were held constant in the BAU and Green Growth scenario. At the same time productivity and technology outside of the direct scope of analysis have been held constant.

The second is that the relevant geographical scope of analysis is Central Kalimantan – direct costs and benefits to other provinces are excluded (although for example it is possible that East Kalimantan or Java would benefit from activity later in the same supply-chain or transport of the produced commodities). The only exception to this was in relation to climate change. As this is considered a global problem, the valuations were made on the basis of the global damages attributable to one tonne of carbon emitted in Indonesia, not just the Indonesia-specific damages.

We note that a draft version of this report was presented to stakeholders for data and assumption validation.

Table 7: Key assumptions applied across the analysis26

Parameter Value Source

Weighted Average Cost of Capital (‘WACC’)

10%

Corporate Income Tax 25%

Social discount rate 5% Team Assumption

Social cost of carbon $80/tCO2 Tol (2009) assuming 0% Pure Rate of Time Preference

Forest Area 203,570 ha

Based on discussions with RMU project team

Percentage of forest area used for palm oil (HPK)

12%

Percentage of forest area used for HTI plantations

44%

Percentage of forest area used for selective logging

44%

HT

I D

eve

lop

me

nt

foll

ow

ing

cle

arin

g

Phase 1: Logging/clearing (clear cutting)

Number of years 10 years Team assumption based on SME input

Average logging yield 31.7 m3/ ha International Tropical Timber Council (2004)

Average price of logged $1o4/m3 Based on: Klassen (2010) Domestic Demand: the black hole in

26 Note: In this table and the following table, units are generally quoted in their source year currency units. In the actual CBA calculations, all values were automatically adjusted for inflation using the US GDP deflator as published by the World Bank World Development Indicators.

34

timber Indonesia’s forest policy

Log production cost $51/m3 Klassen (2010) Domestic Demand: the black hole in Indonesia’s forest policy, net of formal and informal taxes

Phase 2: HTI Development

Land preparation/planting 2 years International Finance Corporation. Note: Not on peatland.

Years to harvest after planting

5 years International Finance Corporation. Note: Not on peatland.

Average pulpwood yield 100 m3/ha International Finance Corporation. Note: Not on peatland.

Net revenue $25/m3 Using Climate Change Revenues to Grow More Wood and Reduce Net Carbon Emissions: Dual-Purpose Forest Plantations

International Finance Corporation. Note: Not on peatland.

Land preparation/planting cost

$1200/ha

Sel

ecti

ve

Log

gin

g

Selective Logging: As above (Phase 1 only)

Pa

lm O

il A

rea

Cycle 25 years

Average price of FFB $150/tonne http://www.bappebti.go.id/en/topdf/create/2040.html

Average production yield 25 tonne/ha

Reducing agricultural expansion into forests in Central Kalimantan Indonesia: Analysis of implementation and financing gap. Note: includes adjustment for costs of planting on peat. Rizaldi Boer, Dodik Ridho Nurrochmat, M. Ardiansyah, Hariyadi, Handian Purwawangsa, and Gito Ginting

Capital expenditure $9,006/ha/25

years

Operating expense (years 1 – 3)

$315/ha/yr

Operating expense (years 4 - 25)

$1,565/ha/yr

Hydrology Impacts starting year

Year 1

Wider watershed area – Area between Katingan and Mentaya river, bounded by Northern concession limit

200,000 ha Approximation based on Google Map distance tool

Wider watershed area –NPV of agricultural land

$3,424/ha

TNC Project

Note: Not on peatland.

Wider watershed area – NPV of sustainable forest management

$398/ha

TNC Project

Note: Not on peatland.

PT

R

MU

Pro

je

ct

Are

a Estimated Emissions Reductions

224 MtCO2/25

years Calculated using IPCC (2013) emissions factors below

35

Net emissions reduction factor for Timber Plantation (HTI)

73 tCO2/ha/yr Source: IPCC (2013) Note 95% Confidence Interval of 59 – 98 tCO2/ha/yr

Net emissions reduction factor for Oil Palm Plantation

40 tCO2/ha/yr

Source: IPCC (2013) Note 95% Confidence Interval of 21 – 62 tCO2/ha/yr

Net emissions reduction factor for Selective Logging

19 tCO2/ha/yr Source: IPCC (2013) Note 95% Confidence Interval of 14 – 25 tCO2/ha/yr

Marketable Emissions Reductions

134 MtCO2/25

years PT RMU Financial Model

Carbon credit price $2 - $8/tCO2

Economic value for forestry $5.6/ha/year

Peraturan Menteri Negara Lingkungan Hidup Republik Indonesia Nomor 14 Tahun 2012 tentang Panduan Valuasi Ekonomi Ekosistem Gambut (Ministerial Regulation)

Economic value for agriculture

$7.0/ha/year

Economic value for freshwater fish

$17.6/ha/year

Economic value for hydrology

$1.1/ha/year

Economic value for social cultural

$1.1/ha/year

Biodiversity and tourism $27/ha/year WWF Heart of Borneo: Investing in Nature for a Green Economy

36

Inputs

What resources have been committed?

Activities

How are the resources used?

Outputs

What are the direct results of

those activities?

Outcomes

How are stakeholders affected as a result of the outputs?

Impacts

The net change to stakeholders as a result of outputs

4 Scope of Analysis

This section explains the impact pathway approach that we use to structure our valuation. Impact pathways provide a rigorous ways of categorizing activities, outcomes and stakeholders and deciding which items to include in the quantitative scope of analysis.

Impact pathways and Indicators

In order to determine the net benefit that each of our ‘green growth interventions’ will generate, we must first establish how each intervention is likely to affect the environment, the economy and society as a whole. We use ‘impact pathways’ to describe the linkages between interventions (activities), the expected outputs from those activities, and the positive and negative outcomes that are generated in both the short and longer term.

The structure of an impact pathway is outlined in Figure 11 below. Beneath Figure 11 there is an example for the Katingan Restoration and Conservation project actually used in the Extended Cost Benefit Analysis. By explicitly outlining this ‘theory of change’, we make sure that each outcome is clearly defined and that they are derived from tangible activities and outputs. Outcomes must be expressed in monetary terms to ensure that they are compatible with a monetary Cost Benefit Analysis.

Figure 11: An impact pathway

Illustrative example for RMU:

Investment in restoration activities and ongoing monitoring

Forest resource conservation

Avoided deforestation

Increased timber and NTFP yield for local communities

Water supply and disturbance regulation for downstream communities and businesses

Better erosion control, soil formation and nutrient cycling for downstream Better waste treatment for downstream communities and businesses

Increased carbon storage/sequestration benefit to global stakeholders and businesses

Biodiversity and intangible value to global stakeholders

Deduct BAU outcome from project outcomes to get net impact

37