costar template

TRANSCRIPT

© Copyright 2013 CoStar Group, Inc. All Rights Reserved. Although CoStar

makes efforts to ensure the accuracy and reliability of the information

contained herein, the following information includes projections that are

based on various assumptions by CoStar concerning future events and

circumstances, as well as historical and current data maintained in CoStar’s

database. Actual results may vary from the projections presented.

The information in this presentation is provided ‘as is’ and CoStar expressly

disclaims any guarantees, representations or warranties of any kind,

including those of merchantability and fitness for a particular purpose.

Webinar Presenters

Anthony Guma

Director

CoStar Group

© Copyright 2013 CoStar Group, Inc.

Greg Kats

President

Capital-E

Agenda

A brief review of emerging, relevant trends

The accelerating green transition and how to profit

from it

New products and services that cut real estate

operating costs and reduce risk

Questions

© Copyright 2013 CoStar Group, Inc.

Anthony Guma

© Copyright 2013 CoStar Group, Inc.

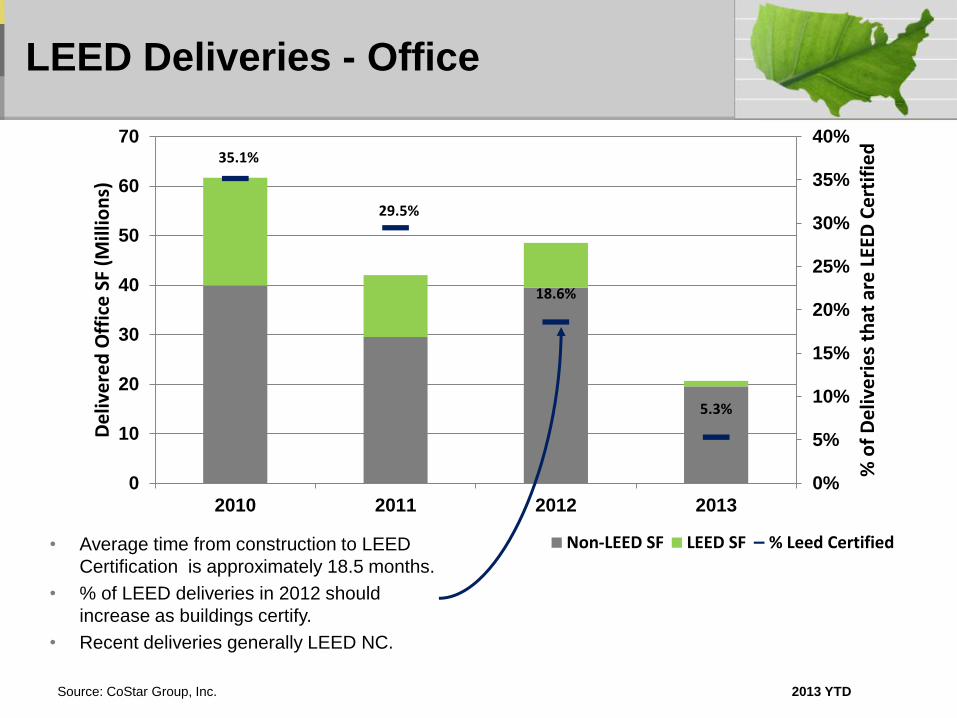

LEED Deliveries - Office

35.1%

29.5%

18.6%

5.3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

10

20

30

40

50

60

70

2010 2011 2012 2013

% o

f D

eliv

eri

es

that

are

LEE

D C

ert

ifie

d

De

live

red

Off

ice

SF

(Mill

ion

s)

Non-LEED SF LEED SF % Leed Certified• Average time from construction to LEED

Certification is approximately 18.5 months.

• % of LEED deliveries in 2012 should

increase as buildings certify.

• Recent deliveries generally LEED NC.

Source: CoStar Group, Inc. 2013 YTD

Major LEED Deliveries –

2012 & 2013

Devon Tower Oklahoma City

LEED Gold

1,800,000 SF, 2012

Endo Pharmaceuticals Philadelphia

LEED Silver

300,000 SF, 2013

1000 Connecticut Washington, DC

LEED Platinum

385,791 SF, 2012

Juniper Networks-

Bldg 2 South Bay/San Jose

LEED Gold

318,712 SF, 2013

BASF NA Headquarters Northern New Jersey

LEED Platinum

326,000 SF, 2012

Davita Headquarters Denver

LEED Gold

246,000, 2012

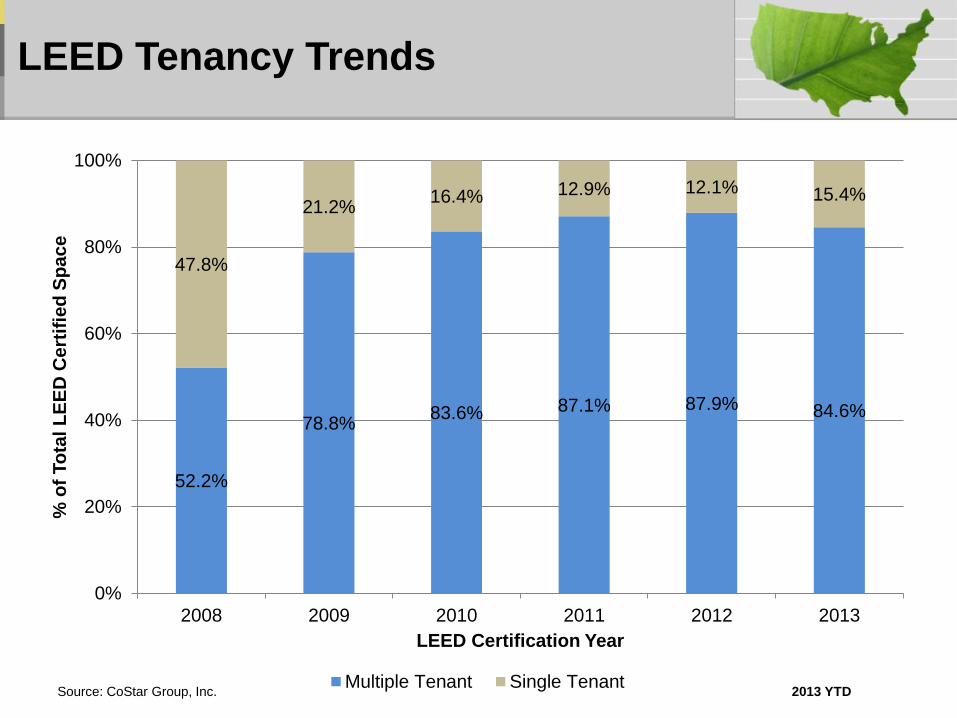

LEED Tenancy Trends

Source: CoStar Group, Inc. 2013 YTD

52.2%

78.8% 83.6% 87.1% 87.9% 84.6%

47.8%

21.2% 16.4% 12.9% 12.1% 15.4%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013

% o

f To

tal L

EE

D C

ert

ifie

d S

pa

ce

LEED Certification Year

Multiple Tenant Single Tenant

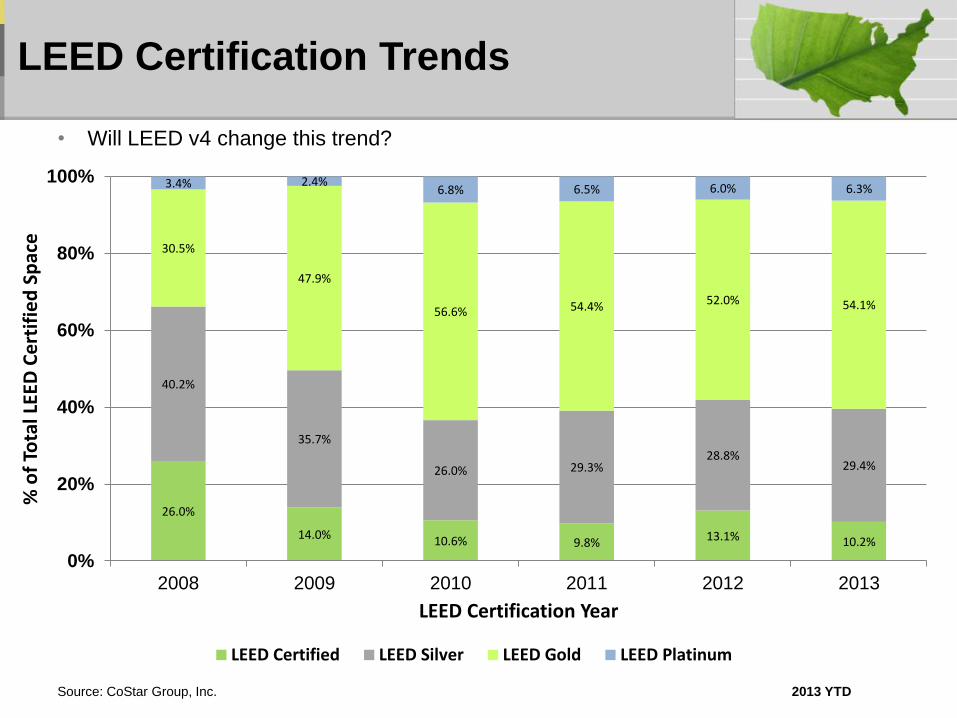

LEED Certification Trends

Source: CoStar Group, Inc.

26.0%

14.0% 10.6% 9.8% 13.1% 10.2%

40.2%

35.7%

26.0% 29.3% 28.8%

29.4%

30.5%

47.9%

56.6% 54.4% 52.0% 54.1%

3.4% 2.4% 6.8% 6.5% 6.0% 6.3%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013

% o

f To

tal L

EED

Ce

rtif

ied

Sp

ace

LEED Certification Year

LEED Certified LEED Silver LEED Gold LEED Platinum

2013 YTD

• Will LEED v4 change this trend?

Green Office Markets

23%

20%

17% 16% 16%

15%

13% 12% 12%

11% 11% 11% 10%

9% 9% 8% 8% 8%

7% 7%

0%

5%

10%

15%

20%

25%

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

LEED

% o

f To

tal O

ffic

e S

F

Ave

rage

Off

ice

Re

nt

(50

K+

SF, B

uilt

in L

ast

10

Ye

ars)

Non LEED Rent LEED Rent % LEED SF

Source: CoStar Group, Inc. (Rent comparison based on

50K+ SF, Built in Last 10 Years)

Greg Kats

© Copyright 2013 CoStar Group, Inc.

N ew t e c h n o l o g i e s / s o l u t i o n s

L ow e r C o s t G r e e n e r B u i l d i n g s a n d C i t i e s

COSTAR 2013

Greg Ka ts, Capi ta l E

Comcast Building

All Building Types are Greening

Wentworth Commons - IL

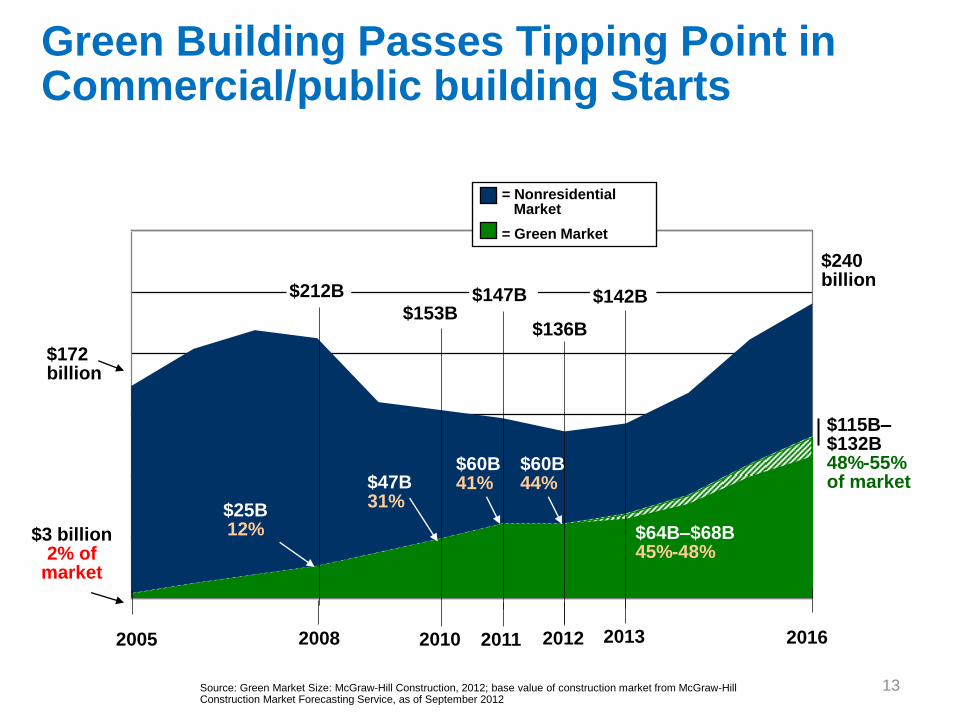

13 13

2005 2008 2010 2016

= Nonresidential Market

$172 billion

$3 billion 2% of

market

$60B 41%

$212B

= Green Market

$153B

$240 billion

$25B 12%

Green Building Passes Tipping Point in Commercial/public building Starts

$136B

$47B 31%

2011 2013

$60B 44%

$64B–$68B 45%-48%

$115B– $132B 48%-55% of market

$142B $147B

2012

Source: Green Market Size: McGraw-Hill Construction, 2012; base value of construction market from McGraw-Hill Construction Market Forecasting Service, as of September 2012

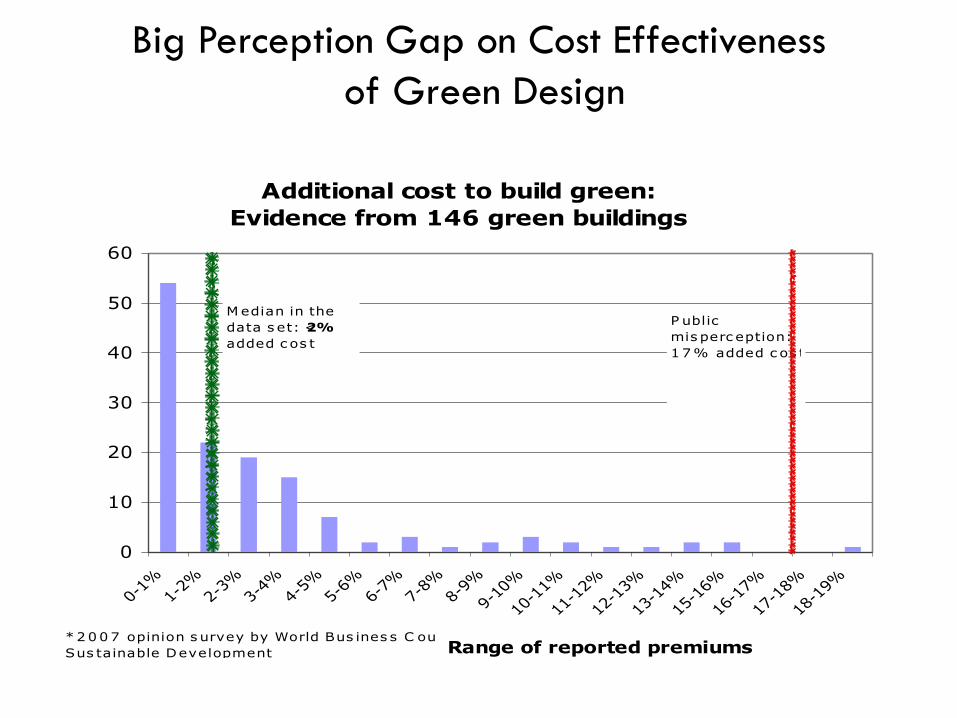

Big Perception Gap on Cost Effectiveness

of Green Design

Additional cost to build green:

Evidence from 146 green buildings

0

10

20

30

40

50

60

0-1%

1-2%

2-3%

3-4%

4-5%

5-6%

6-7%

7-8%

8-9%

9-10

%

10-1

1%

11-1

2%

12-1

3%

13-1

4%

15-1

6%

16-1

7%

17-1

8%

18-1

9%

Range of reported premiums

# o

f bu

ildin

gs in

data

set

M edian in the

data s et: <2%

added c os t

P ublic

mis perc eption:

17% added c os t*

*2007 opinion s urvey by World Bus ines s C ounc il for

Sus tainable Development

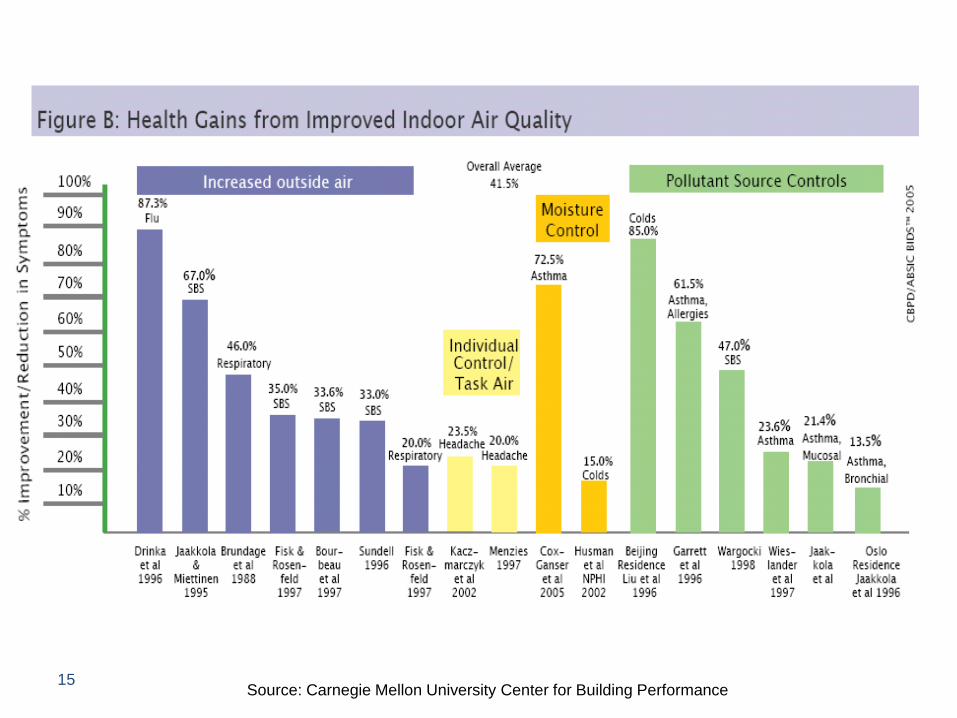

15 Source: Carnegie Mellon University Center for Building Performance

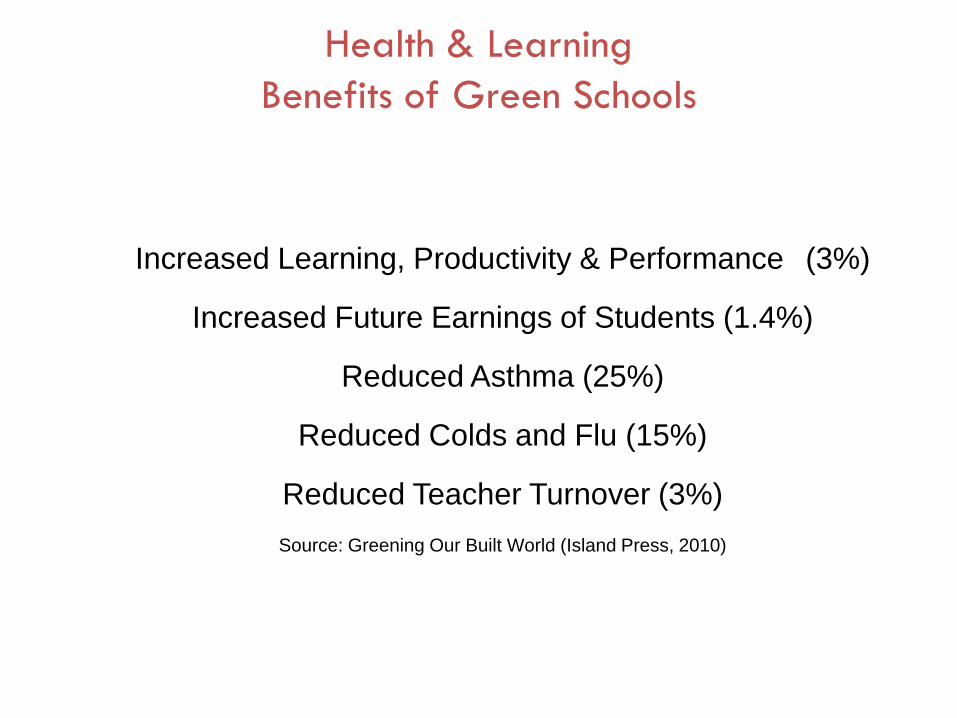

Health & Learning

Benefits of Green Schools

Increased Learning, Productivity & Performance (3%)

Increased Future Earnings of Students (1.4%)

Reduced Asthma (25%)

Reduced Colds and Flu (15%)

Reduced Teacher Turnover (3%)

Source: Greening Our Built World (Island Press, 2010)

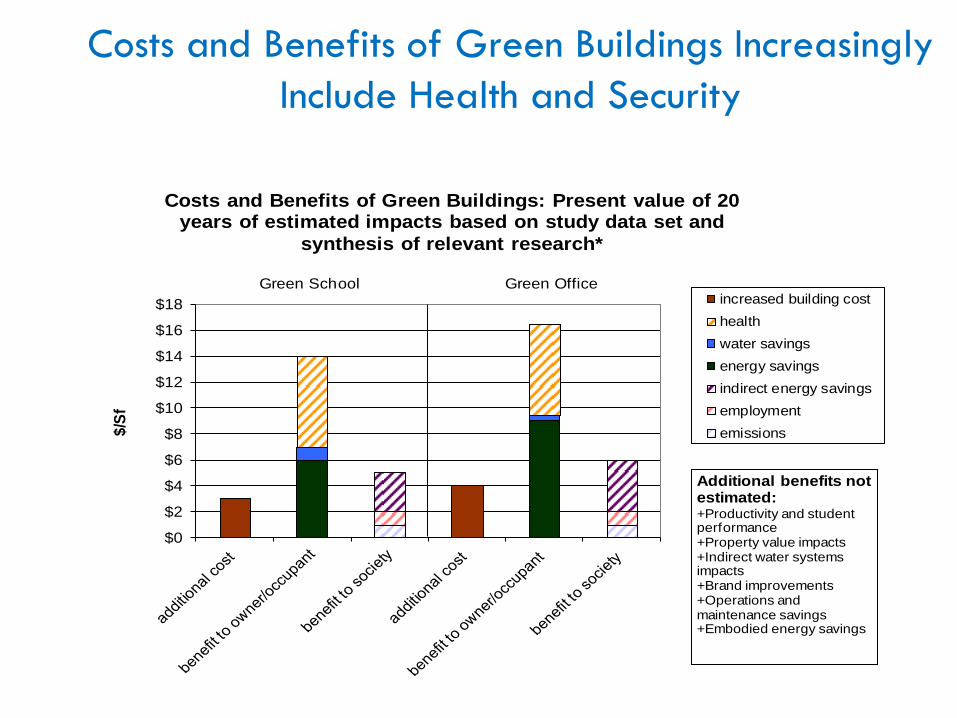

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$/S

f

Costs and Benefits of Green Buildings: Present value of 20 years of estimated impacts based on study data set and

synthesis of relevant research*

increased building cost

health

water savings

energy savings

indirect energy savings

employment

emissions

Green School Green Office

Additional benefits not estimated:+Productivity and student performance+Property value impacts+Indirect water systems impacts+Brand improvements+Operations and maintenance savings+Embodied energy savings

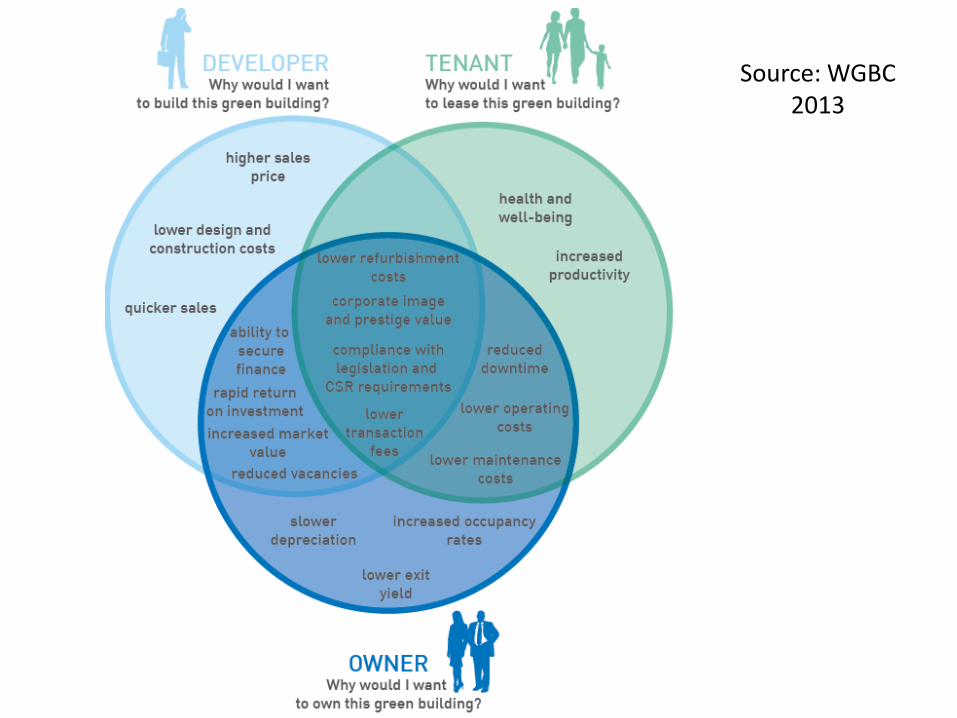

Costs and Benefits of Green Buildings Increasingly

Include Health and Security

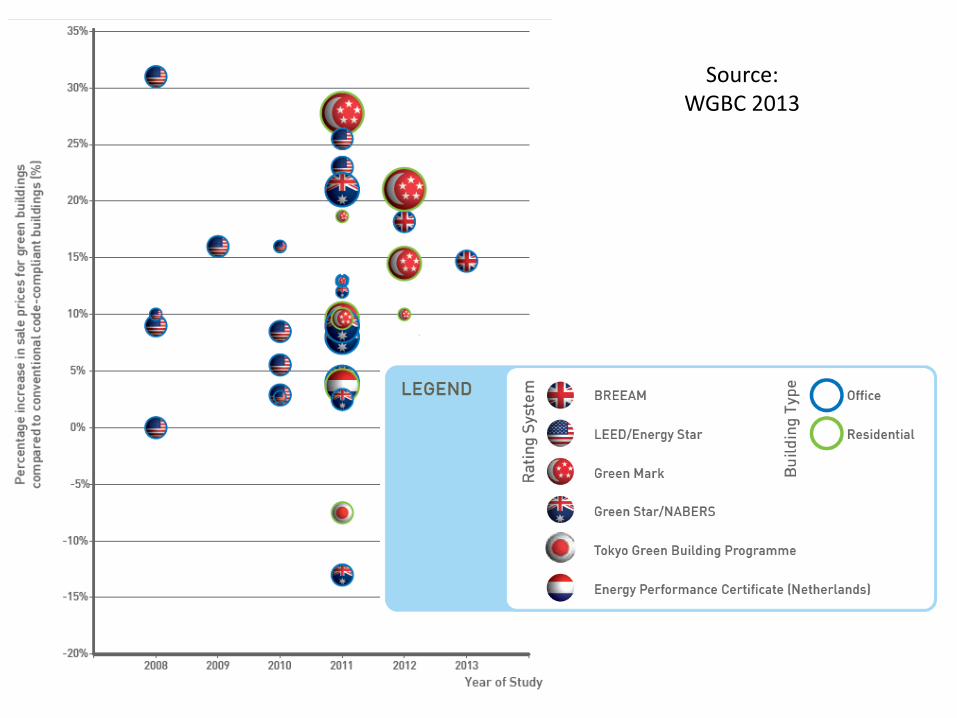

Source: WGBC 2013

Source: WGBC 2013

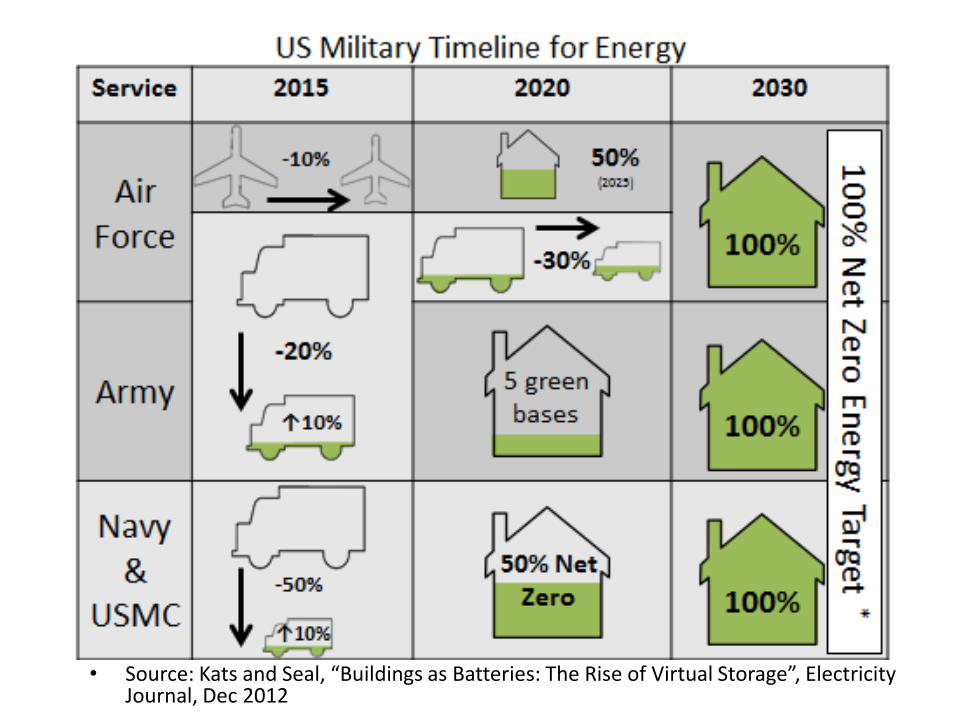

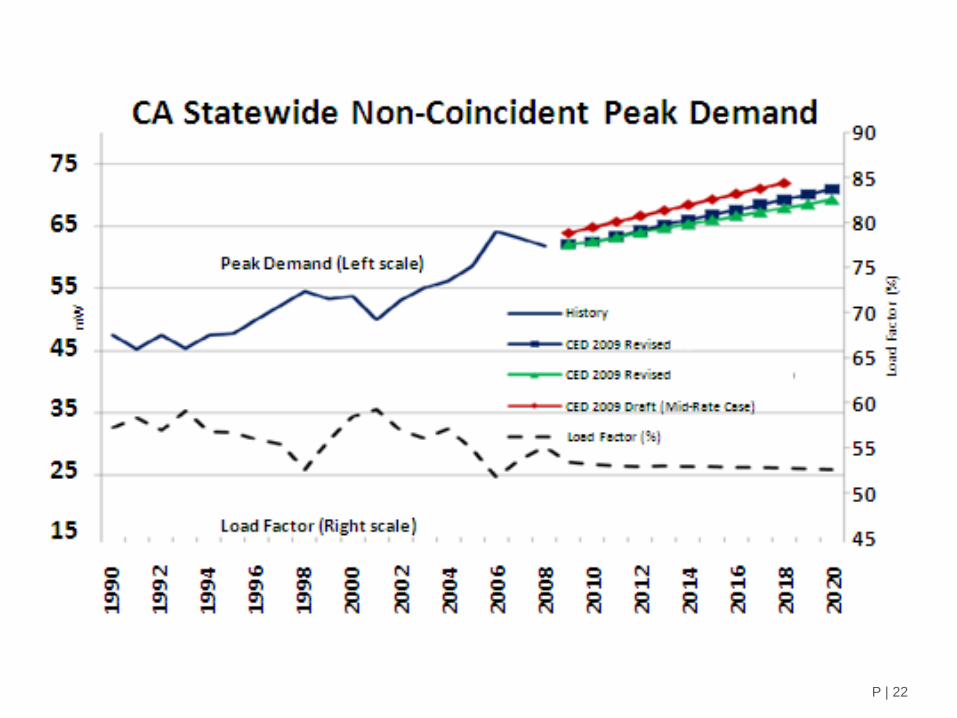

• Source: Kats and Seal, “Buildings as Batteries: The Rise of Virtual Storage”, Electricity Journal, Dec 2012

Shanghai

1989

2010

P | 22

Buildings as Batteries: The Rise of Virtual Storage (Kats and Seal, Electricity Journal, Dec 2012)

Most storage services can be far more cheaply provided by software+ controls on buildings

• Building reshapes its load to anticipate and respond to future weather, renewable energy and utility power needs/signals

– Building IQ: smart, linked, thermal mass: substantial energy savings even in new LEED buildings!

– Digitally addressable buildings/cities: Honest Buildings

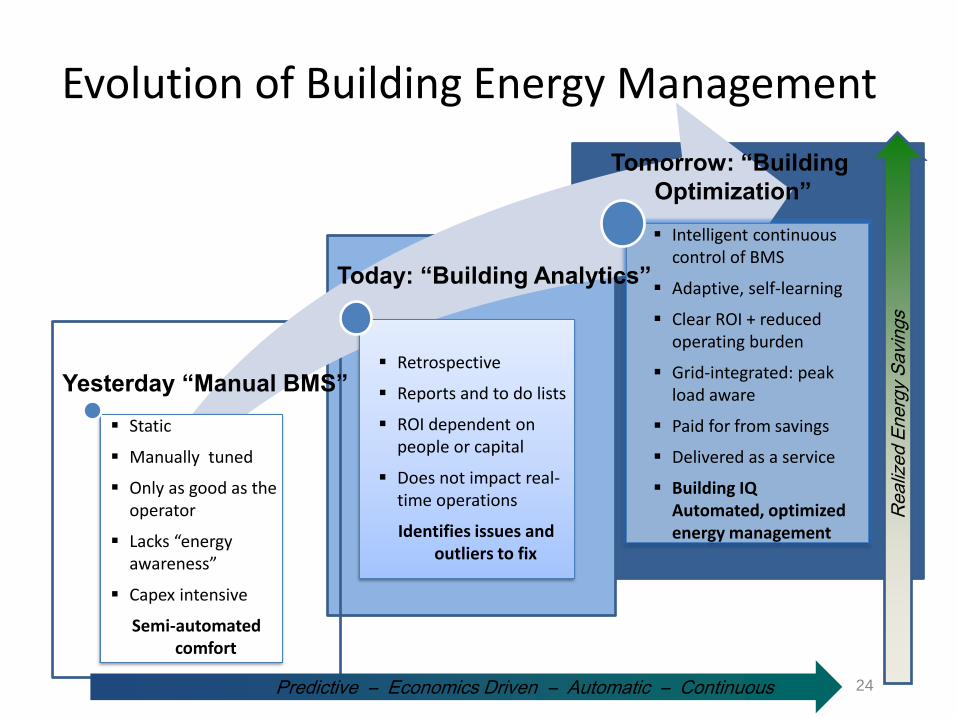

Evolution of Building Energy Management

BuildingIQ 24

Static

Manually tuned

Only as good as the operator

Lacks “energy awareness”

Capex intensive

Semi-automated comfort

Retrospective

Reports and to do lists

ROI dependent on people or capital

Does not impact real-time operations

Identifies issues and outliers to fix

Intelligent continuous control of BMS

Adaptive, self-learning

Clear ROI + reduced operating burden

Grid-integrated: peak load aware

Paid for from savings

Delivered as a service

Building IQ Automated, optimized energy management

Yesterday “Manual BMS”

Today: “Building Analytics”

Tomorrow: “Building

Optimization”

Re

aliz

ed

En

erg

y S

avin

gs

Predictive – Economics Driven – Automatic – Continuous

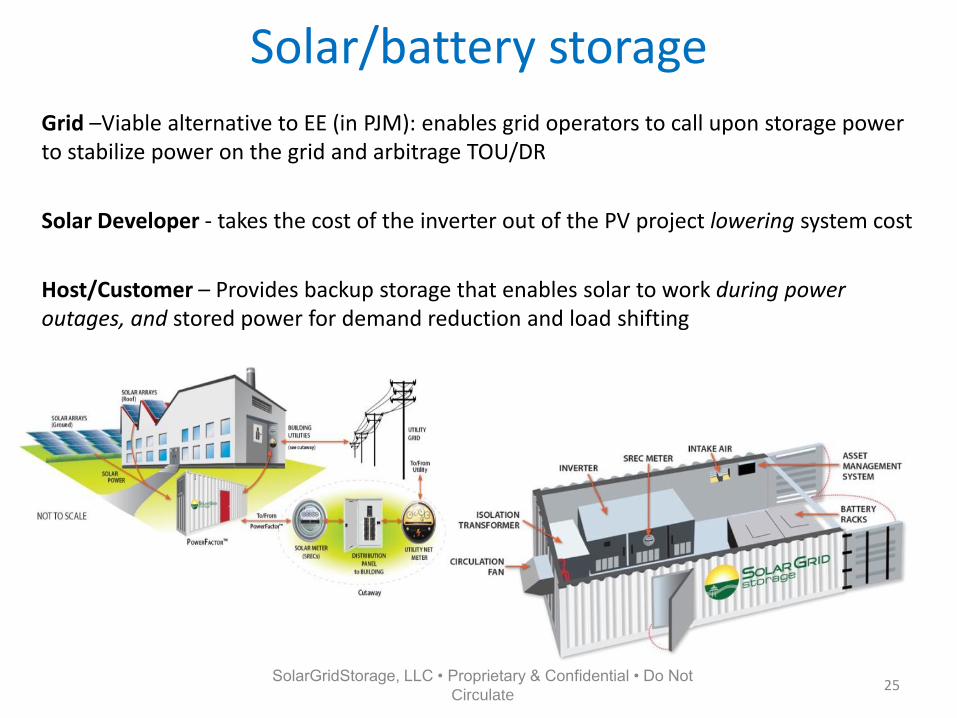

Solar/battery storage

Grid –Viable alternative to EE (in PJM): enables grid operators to call upon storage power to stabilize power on the grid and arbitrage TOU/DR

Solar Developer - takes the cost of the inverter out of the PV project lowering system cost

Host/Customer – Provides backup storage that enables solar to work during power outages, and stored power for demand reduction and load shifting

25 SolarGridStorage, LLC • Proprietary & Confidential • Do Not

Circulate

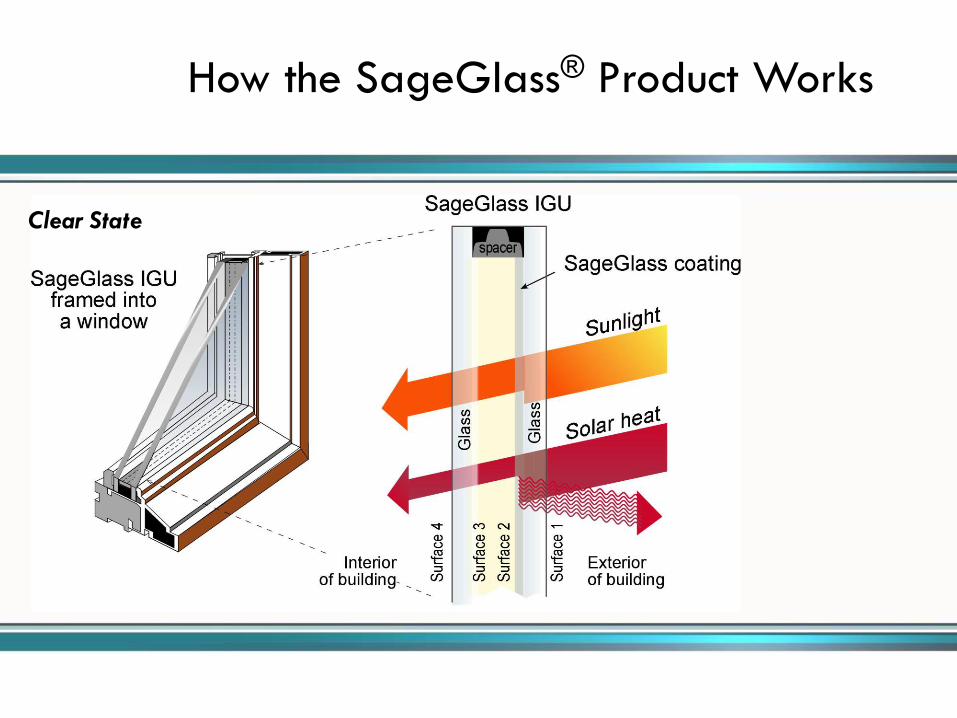

How the SageGlass® Product Works

Clear State

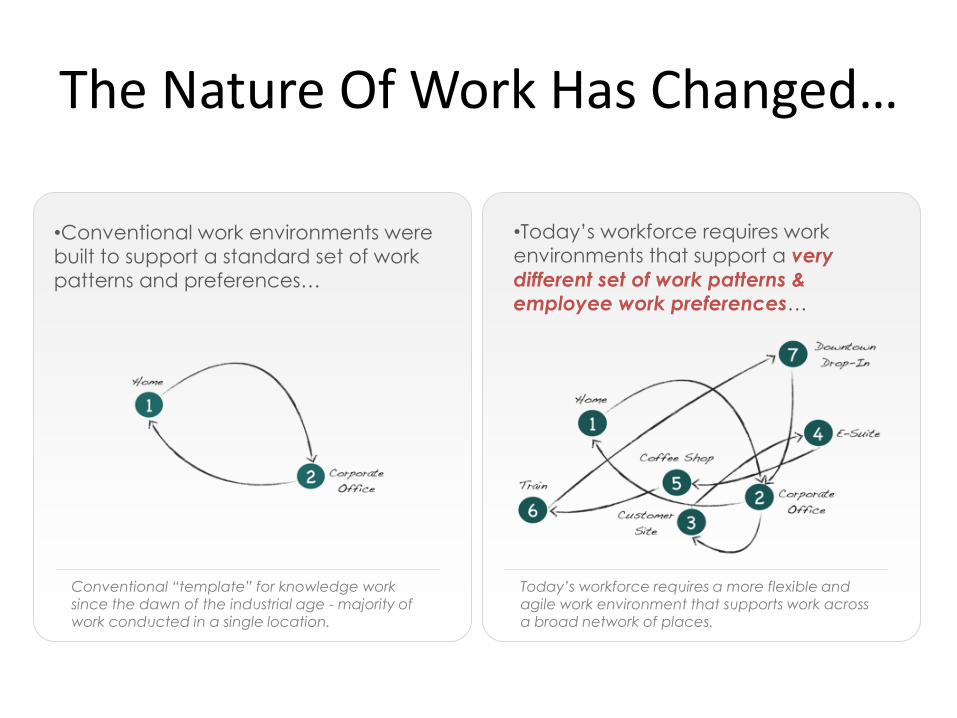

The Nature Of Work Has Changed…

Conventional “template” for knowledge work

since the dawn of the industrial age - majority of work conducted in a single location.

Today’s workforce requires a more flexible and

agile work environment that supports work across a broad network of places.

•Today’s workforce requires work

environments that support a very

different set of work patterns & employee work preferences…

•Conventional work environments were

built to support a standard set of work

patterns and preferences…

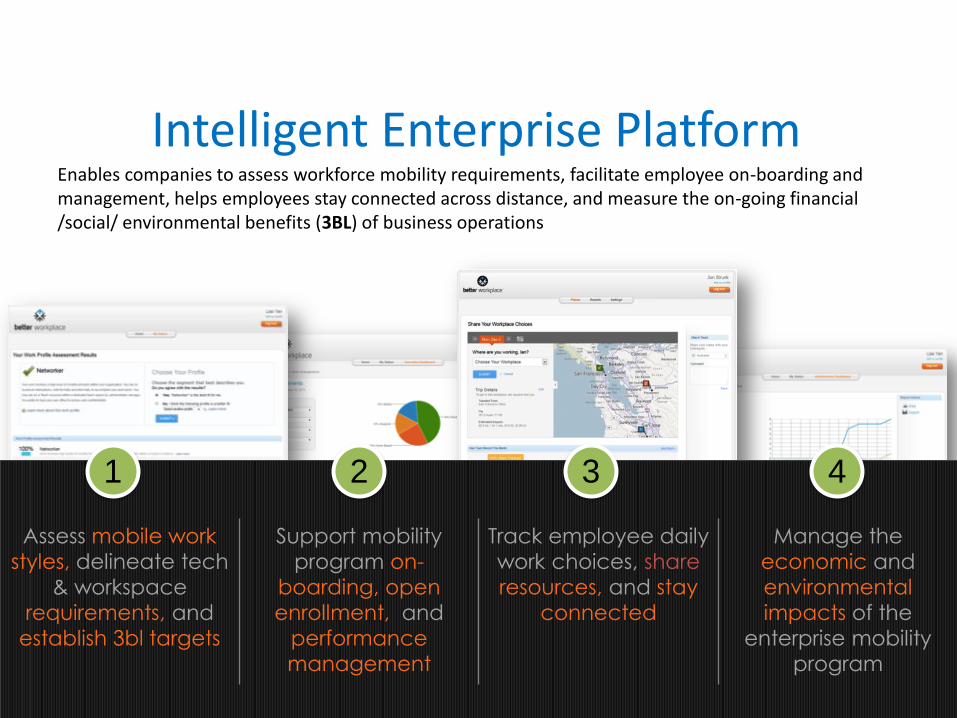

Assess mobile work

styles, delineate tech

& workspace

requirements, and

establish 3bl targets

Support mobility

program on-

boarding, open

enrollment, and

performance

management

Track employee daily

work choices, share

resources, and stay

connected

Manage the

economic and

environmental

impacts of the

enterprise mobility

program

1 2 3 4

Intelligent Enterprise Platform Enables companies to assess workforce mobility requirements, facilitate employee on-boarding and management, helps employees stay connected across distance, and measure the on-going financial /social/ environmental benefits (3BL) of business operations

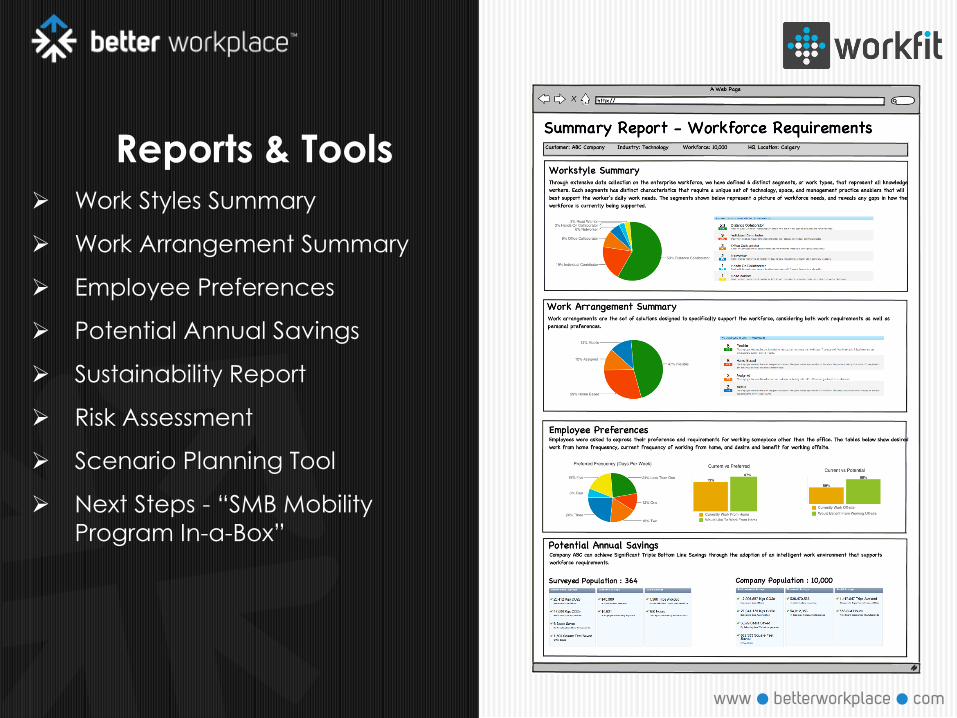

Reports & Tools

Work Styles Summary

Work Arrangement Summary

Employee Preferences

Potential Annual Savings

Sustainability Report

Risk Assessment

Scenario Planning Tool

Next Steps - “SMB Mobility

Program In-a-Box”

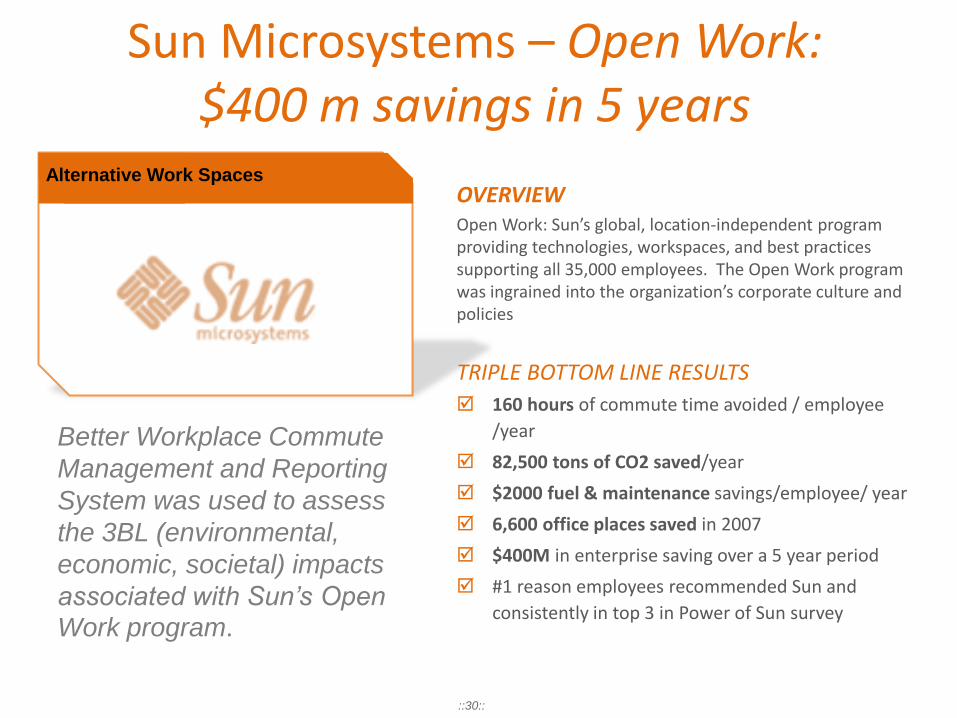

Sun Microsystems – Open Work: $400 m savings in 5 years

Better Workplace Commute

Management and Reporting

System was used to assess

the 3BL (environmental,

economic, societal) impacts

associated with Sun’s Open Work program.

OVERVIEW Open Work: Sun’s global, location-independent program providing technologies, workspaces, and best practices supporting all 35,000 employees. The Open Work program was ingrained into the organization’s corporate culture and policies

TRIPLE BOTTOM LINE RESULTS

160 hours of commute time avoided / employee

/year

82,500 tons of CO2 saved/year

$2000 fuel & maintenance savings/employee/ year

6,600 office places saved in 2007

$400M in enterprise saving over a 5 year period

#1 reason employees recommended Sun and

consistently in top 3 in Power of Sun survey

Alternative Work Spaces

::30::

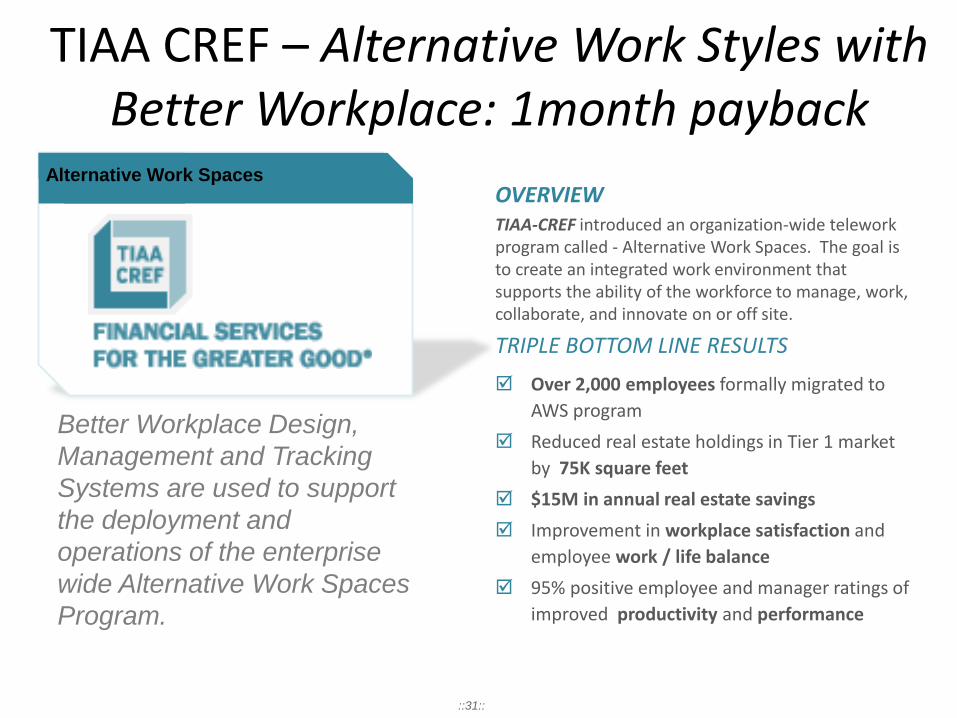

TIAA CREF – Alternative Work Styles with Better Workplace: 1month payback

Better Workplace Design,

Management and Tracking

Systems are used to support

the deployment and

operations of the enterprise

wide Alternative Work Spaces

Program.

OVERVIEW TIAA-CREF introduced an organization-wide telework program called - Alternative Work Spaces. The goal is to create an integrated work environment that supports the ability of the workforce to manage, work, collaborate, and innovate on or off site.

TRIPLE BOTTOM LINE RESULTS

Over 2,000 employees formally migrated to

AWS program

Reduced real estate holdings in Tier 1 market

by 75K square feet

$15M in annual real estate savings

Improvement in workplace satisfaction and

employee work / life balance

95% positive employee and manager ratings of

improved productivity and performance

Alternative Work Spaces

::31::

Thank you!

www.cap-e.com

www.betterworkplace.com

Your Questions

© Copyright 2013 CoStar Group, Inc.