corporate governance and - universität ulm · corporate governance and finance nino papiashvili...

TRANSCRIPT

Corporate Governance and Finance

Nino Papiashvili

Institute of FinanceUlm University

Corporate Governance and FinanceCorporate Governance and Finance

From Sole Proprietorship to Corporationso So e op eto s p to Co po at o s

Owners of the Assets ≠ Controllers of the AssetsOwners of the Assets ≠ Controllers of the Assets

Agency problems Agents and Principals do notAgency problems – Agents and Principals do not want the same things

=>The role of Corporate Governance enters the playplay

Corporate Governance and FinanceCorporate Governance and Finance

Class time and room:

Wednesdays at 16:00‐18:00 in Room H12Thursdays at 12:00‐14:00 in Room H8

Office Hours: Thursdays at 14:00‐17:00 or by appointmentRoom 1.21 ‐ Helmholtzstrasse 18

You can also contact me at: nino papiashvili@uni‐ulm denino.papiashvili@uni ulm.de

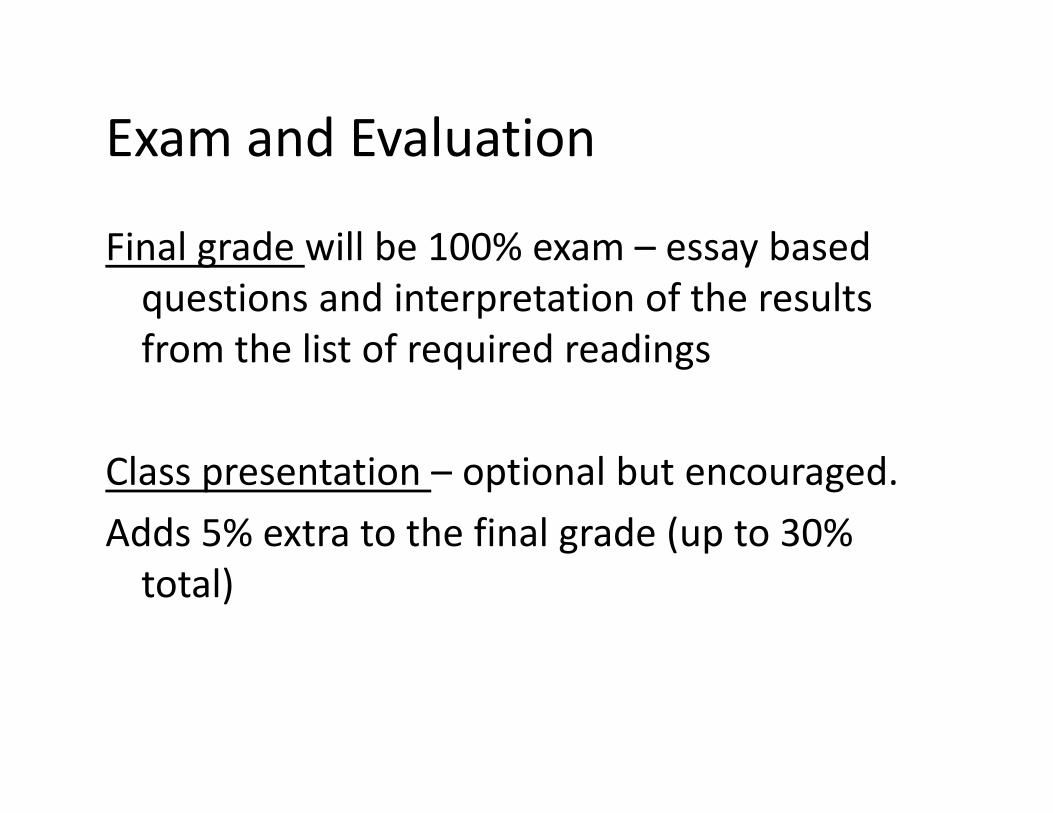

Exam and EvaluationExam and Evaluation

Final grade will be 100% exam – essay basedFinal grade will be 100% exam essay based questions and interpretation of the results from the list of required readingsfrom the list of required readings

Cl i i l b dClass presentation – optional but encouraged.Adds 5% extra to the final grade (up to 30% total)

Study MaterialStudy Material

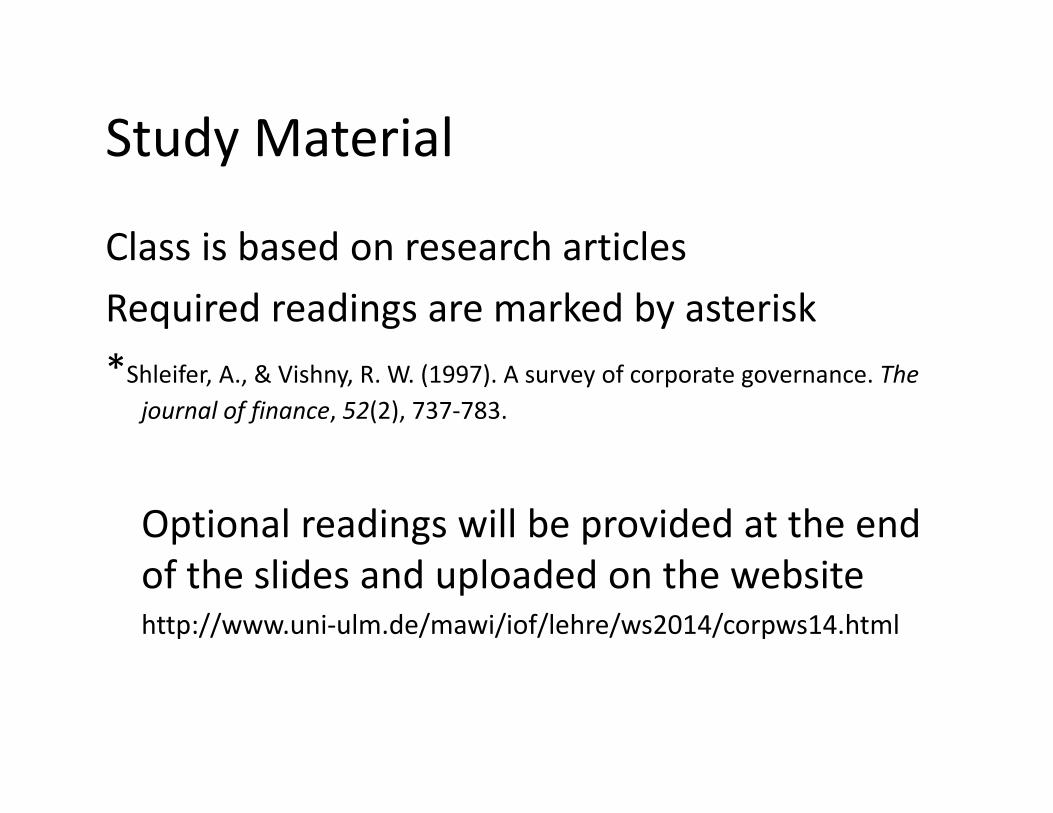

Class is based on research articlesClass is based on research articlesRequired readings are marked by asterisk**Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The

journal of finance, 52(2), 737‐783.

Optional readings will be provided at the end f h l d d l d d h bof the slides and uploaded on the website

http://www.uni‐ulm.de/mawi/iof/lehre/ws2014/corpws14.html

Searching ArticlesSearching ArticlesGo to uni‐ulm.de => kiz (Library/IT/Media) =>Library=>Digital

Library=>E‐Journalsy

Searching ArticlesSearching Articles

Searching ArticlesSearching Articles

CorporationsCorporations

Corporation – organization that allows differentCorporation organization that allows different parties to contribute capital, expertise and labor for the benefit for all of them.Investors – provide finances and participate in profits without responsibility over operationsprofits without responsibility over operationsManagers – run the company without providing fundsfunds=> Separation of ownership (investors) and control (managers)control (managers)

CorporationsCorporations

Investors own stock certificates and rights to:Investors own stock certificates and rights to:

ll h k1. sell the stock2. vote the proxy3. bring suit for damages 4 certain information4. certain information5. residual claims

CorporationsCorporationsIn order for the stock to be freely transferable:

1. shareholders have to have limited liability – give up controlcontrol

2. shares have to trade at a fairly low rate – issue millions of shares of stock

=>Loosened the connection between ownership and controlcontrol

=>No single shareholder can monitor effectively ‐sheer numbers rob shareholders of power

Corporate GovernanceCorporate GovernanceThe structure of modern corporations with widely dispersed i t l d tinvestors lead to:

1. Collective action problemsfl f b d h h ld2. Conflicts of interests between managers and shareholders

Corporate governance tries to answer the questions:

How do we make a manager as committed to the creation of long‐term shareholder value as he would be if it was his own money?

How to achieve the right balance between management discretion and small shareholder protection?

Corporate GovernanceCorporate Governance

Mechanisms that can mitigate the agencyMechanisms that can mitigate the agency problems:

1. Concentration of Ownership2. Hostile Takeovers3. Boards of Directors4. Managerial Incentives

OwnershipOwnershipConcentrated vs. dispersed ownership:

1. Power and resources for monitoring2. Diversification2. Diversification3. Liquidity of stock market

4 Another so rce of conflicts of interests redistrib te rents4. Another source of conflicts of interests – redistribute rents from small shareholders and employees to them

5. Where investor protection law is weak concentration of ownership leverages up legal protectionownership leverages up legal protection

6. When small investor expropriation is expected (or minority investor rights are not protected) – external finance declines: small investors are unwilling to invest (Europe)declines: small investors are unwilling to invest (Europe)

OwnershipOwnershipCreditors as owners:

1. Limits managerial discretion by minimizing free cash flow available to themh f h f2. Threat of termination when performance is poor

3. Legal protection of creditors is more effective (debt contract violations are more straightforward)

4. Highly levered firms may incur large costs of financial distress and bankruptcy

5 Since creditors bear all the costs of failure but no share in success5. Since creditors bear all the costs of failure but no share in success they might cause the firms to forego good (risky) investment projects

TakeoversTakeovers

Threat of takeover ‐mechanism to discipline the pmanagers

When large blockholding is regulated by the law then the system of dispersed shareholders relying on hostile takeovers emerge (USA).on hostile takeovers emerge (USA).

=>rapid mechanism to concentrate ownership p ptemporarily to remove poor performing managers.

TakeoversTakeovers

Are costly – raider has to pay to targetAre costly raider has to pay to target shareholders the potential benefits

Leads to anti takeover defenses – which may lead to management entrenchment and self‐lead to management entrenchment and selfdealing and possible negative impact on firm value

Pre‐bid and post‐bid defensesPre bid and post bid defenses

Board of DirectorsBoard of Directors

Dispersed shareholders have the right to electDispersed shareholders have the right to elect directors whose mission is to:

1. protect their rights 2 select managers2. select managers3. design CEO compensation 4 it t4. monitor management 5. vote on important decisions.

Board of DirectorsBoard of Directors

Board characteristics:

1. Board is nominated by the management –Source of conflicts of interests: potential collusion with managers

2 Chairman of the Board=Chief Executive Officer?2. Chairman of the Board=Chief Executive Officer?3. Independence of the board => incompetence4 Staggered/classified board4. Staggered/classified board5. Monitoring of the board: Incentives of the

directors

CEO IncentivesCEO IncentivesCEO compensation should align interests of managers and shareholders

Give managers the right incentives – the stake in firmGive managers the right incentives the stake in firm value

Typical structure of CEO compensation: basic salaryTypical structure of CEO compensation: basic salary, bonuses, stocks, options, other benefits

E i ti d i=>Excessive option awards may give managers wrong incentives of market timing their contracts in advance or later engage in manipulating accounting numbers to increase their payincrease their pay.

Corporate Governance and Equity PricesCorporate Governance and Equity Prices

Gompers, P. A., Ishii, J. L., & Metrick, A. (2001). Corporate governance andGompers, P. A., Ishii, J. L., & Metrick, A. (2001). Corporate governance and equity prices (No. w8449). National bureau of economic research.

Empirical Q: Is there a relationship between corporate governance and firm performance?

They constructed a “Governance Index” based on 24 characteristics related to shareholder rights on 1500 firms during 1990s

The results show that an investment strategy that bought shares in the firms with strongest shareholder rights and sold in the weakest shareholder rights would have earned abnormal returns of 8.5% per year in the sample period

Construction of the IndexConstruction of the Index

Index is a proxy for the balance of power between p y pshareholders and managers: for every provision that reduces shareholder rights (increases managerial power) one point is added to the firm’s G Indexp

So firms in the highest decile of the Index are placed in the “Dictatorship Portfolio”( weakest shareholder rights)the Dictatorship Portfolio ( weakest shareholder rights) and the ones in the lowest decile in “Democracy Portfolio” (strongest shareholder rights).

Result: democracy portfolio (G≤5) outperformed Dictatorship portfolio (G≥14) by 8.5% per year

The Provisions of the G IndexThe Provisions of the G Index

Provisions are divided into five groups/subindices:Provisions are divided into five groups/subindices:

i f d l i h il bidd1. Tactics for delaying hostile bidders2. Limiting shareholder voting rights3. Manager/Director protection 4 Other takeover defenses4. Other takeover defenses5. State laws limiting takeovers

The ProvisionsThe ProvisionsTactics for delaying hostile bidders: 1. blank check preferred stock2. classified board3 limitation to special meeting3. limitation to special meeting4. limitation to written consent

Other takeover defenses:1. anti‐greenmail 2. directors’ duties2. directors duties 3. fair price requirements4. pension parachutes 5 i ill5. poison pill 6. silver parachutes

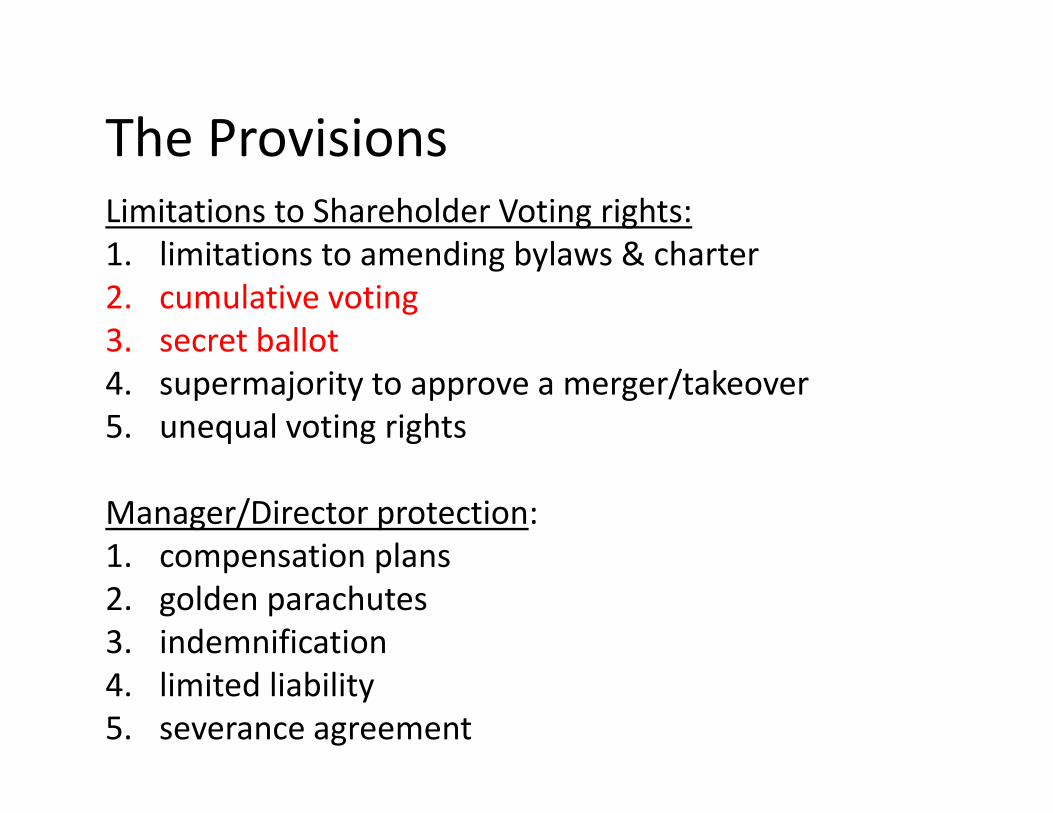

The ProvisionsThe ProvisionsLimitations to Shareholder Voting rights:1 limitations to amending bylaws & charter1. limitations to amending bylaws & charter2. cumulative voting 3. secret ballot 4. supermajority to approve a merger/takeover5. unequal voting rights

Manager/Director protection: 1 compensation plans1. compensation plans 2. golden parachutes3. indemnification4. limited liability5. severance agreement

The ProvisionsThe Provisions

State laws:State laws:

1 anti‐greenmail law1. anti‐greenmail law 2. business combination law 3 h t l3. cash‐out law 4. directors’ duties law 5. fair price law 6. control share (supermajority) acquisition law

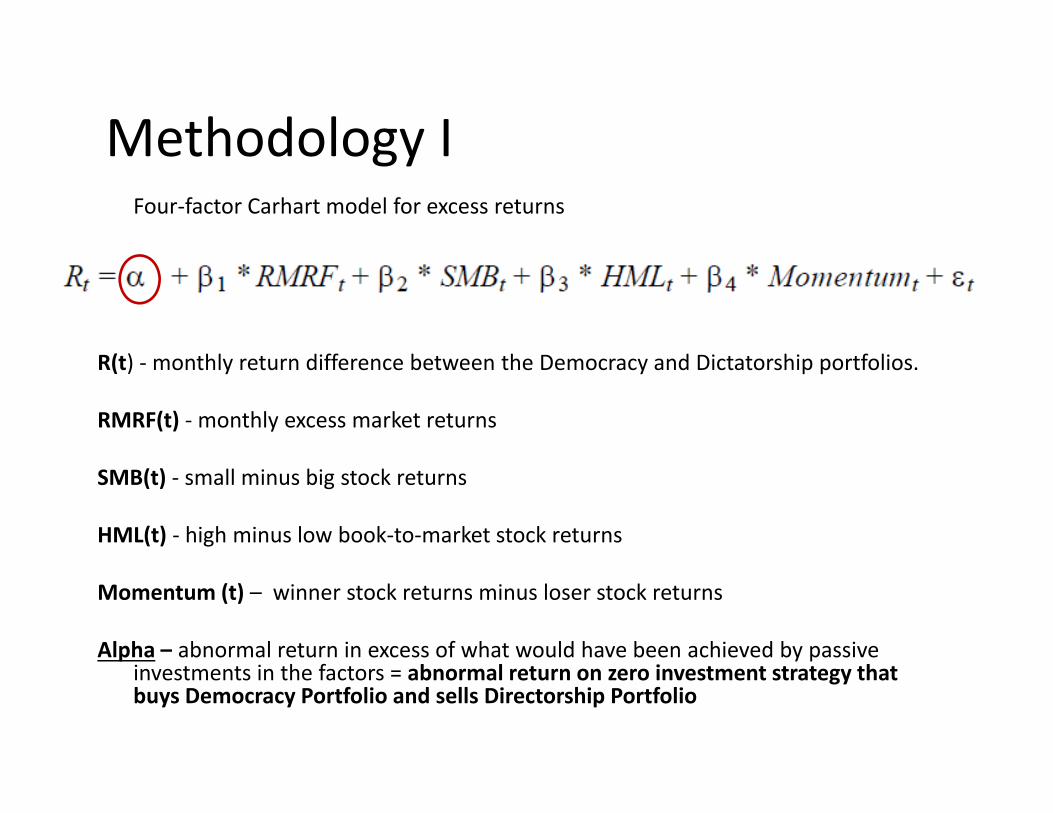

Methodology IMethodology IFour‐factor Carhart model for excess returns

R( ) hl diff b h D d Di hi f liR(t) ‐monthly return difference between the Democracy and Dictatorship portfolios.

RMRF(t) ‐monthly excess market returns

SMB(t) ‐ small minus big stock returns

HML(t) ‐ high minus low book‐to‐market stock returns

Momentum (t) – winner stock returns minus loser stock returns

Alpha – abnormal return in excess of what would have been achieved by passive investments in the factors = abnormal return on zero investment strategy that buys Democracy Portfolio and sells Directorship Portfolio

Results

Annual 8.5%

Annual 3.5%

Ann al 5 0%Annual ‐5.0%

Methodology IIMethodology II

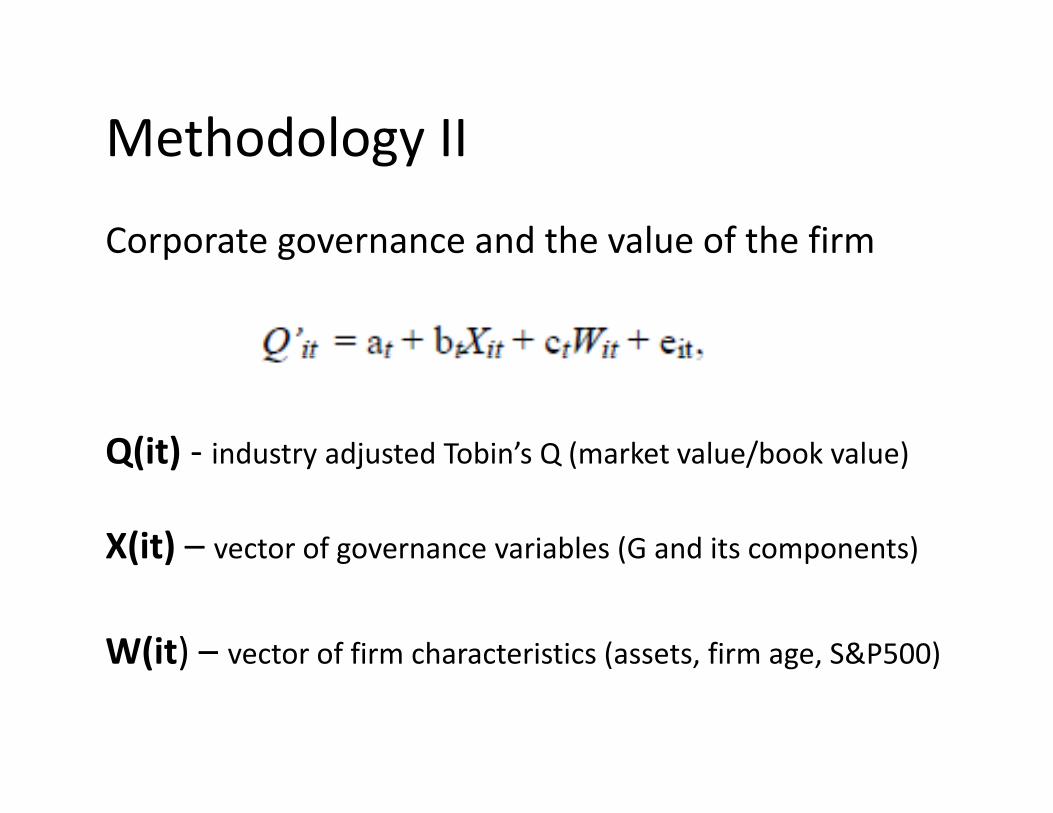

Corporate governance and the value of the firm Co po ate go e a ce a d t e a ue o t e

Q(it) ‐ industry adjusted Tobin’s Q (market value/book value)Q(it) industry adjusted Tobin s Q (market value/book value)

X(it) – vector of governance variables (G and its components)( ) g ( p )

W(it) – vector of firm characteristics (assets, firm age, S&P500)W(it) vector of firm characteristics (assets, firm age, S&P500)

Results IIAll negative and significant99’‐ 1 point up in G

Dummy for Democracy P Always positive Components of 99 ‐ 1 point up in G

11.4pp down in QAlways positive but insignificant

pGovernance are negative

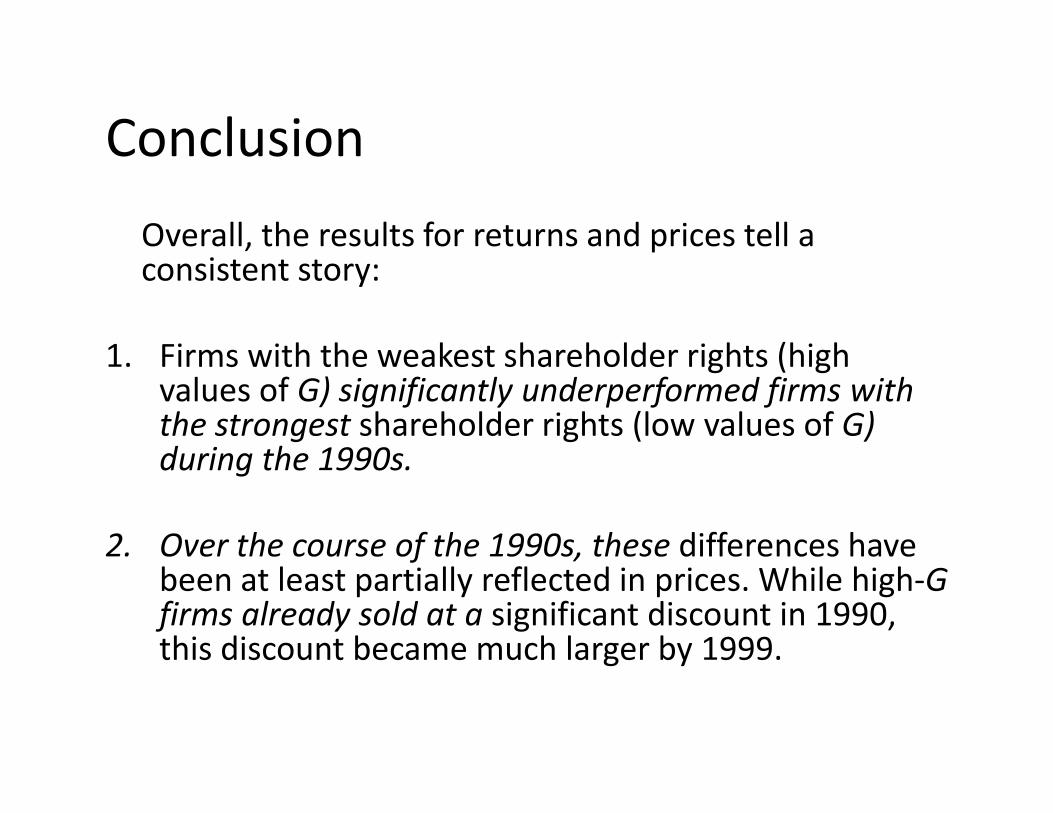

ConclusionConclusionOverall, the results for returns and prices tell a consistent story:

1 Firms with the weakest shareholder rights (high1. Firms with the weakest shareholder rights (high values of G) significantly underperformed firms with the strongest shareholder rights (low values of G) during the 1990sduring the 1990s.

2. Over the course of the 1990s, these differences have f ,been at least partially reflected in prices. While high‐G firms already sold at a significant discount in 1990, this discount became much larger by 1999.g y

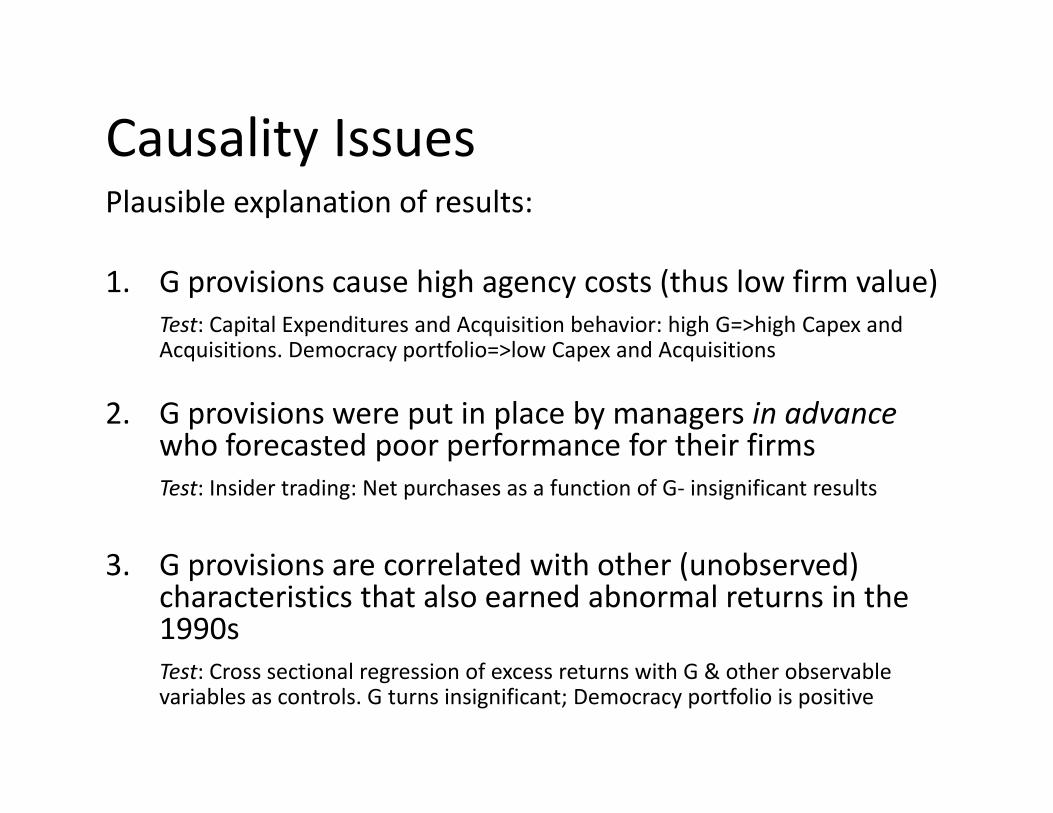

Causality IssuesCausality IssuesPlausible explanation of results:

1. G provisions cause high agency costs (thus low firm value)Test: Capital Expenditures and Acquisition behavior: high G=>high Capex and Acquisitions. Democracy portfolio=>low Capex and AcquisitionsAcquisitions. Democracy portfolio >low Capex and Acquisitions

2. G provisions were put in place by managers in advance who forecasted poor performance for their firmsp pTest: Insider trading: Net purchases as a function of G‐ insignificant results

3 G provisions are correlated with other (unobserved)3. G provisions are correlated with other (unobserved) characteristics that also earned abnormal returns in the 1990s

l f h & h b blTest: Cross sectional regression of excess returns with G & other observable variables as controls. G turns insignificant; Democracy portfolio is positive

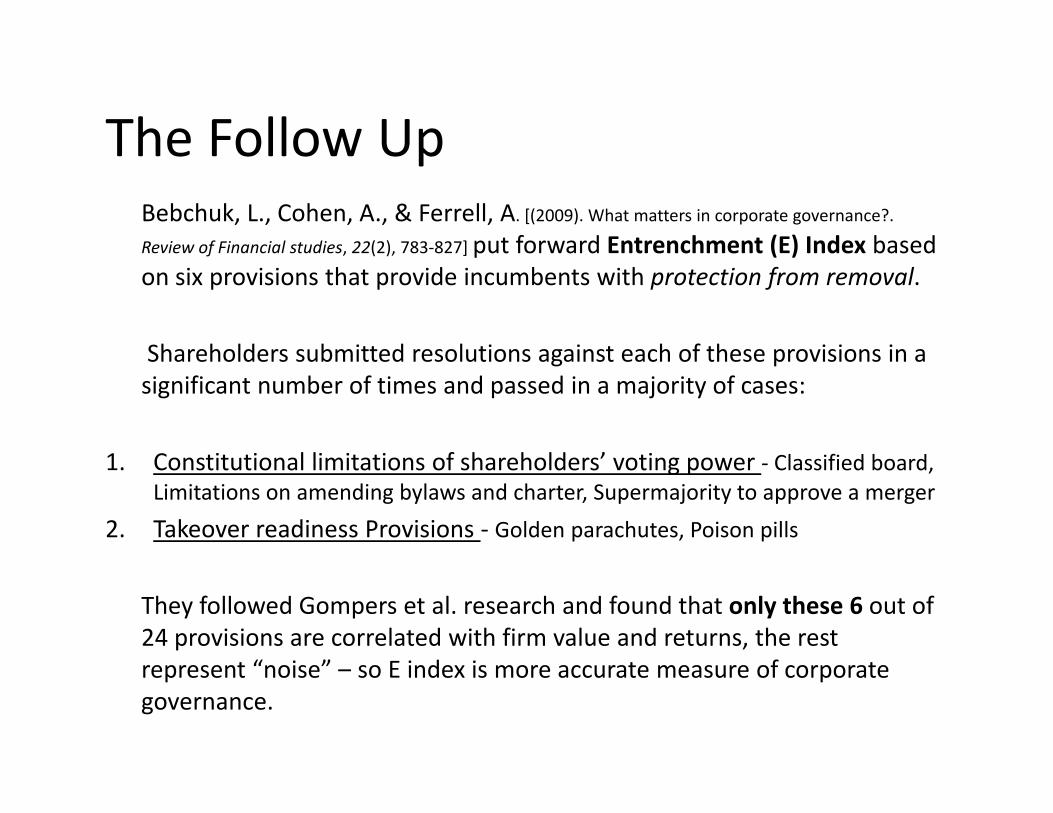

The Follow UpThe Follow UpBebchuk, L., Cohen, A., & Ferrell, A. [(2009). What matters in corporate governance?.

Review of Financial studies, 22(2), 783‐827] put forward Entrenchment (E) Index basedReview of Financial studies, 22(2), 783 827] put forward Entrenchment (E) Index based on six provisions that provide incumbents with protection from removal.

Shareholders submitted resolutions against each of these provisions in aShareholders submitted resolutions against each of these provisions in a significant number of times and passed in a majority of cases:

1 Constitutional limitations of shareholders’ voting power Cl ifi d b d1. Constitutional limitations of shareholders’ voting power ‐ Classified board, Limitations on amending bylaws and charter, Supermajority to approve a merger

2. Takeover readiness Provisions ‐ Golden parachutes, Poison pills

They followed Gompers et al. research and found that only these 6 out of 24 provisions are correlated with firm value and returns, the rest

t “ i ” E i d i t f trepresent “noise” – so E index is more accurate measure of corporate governance.

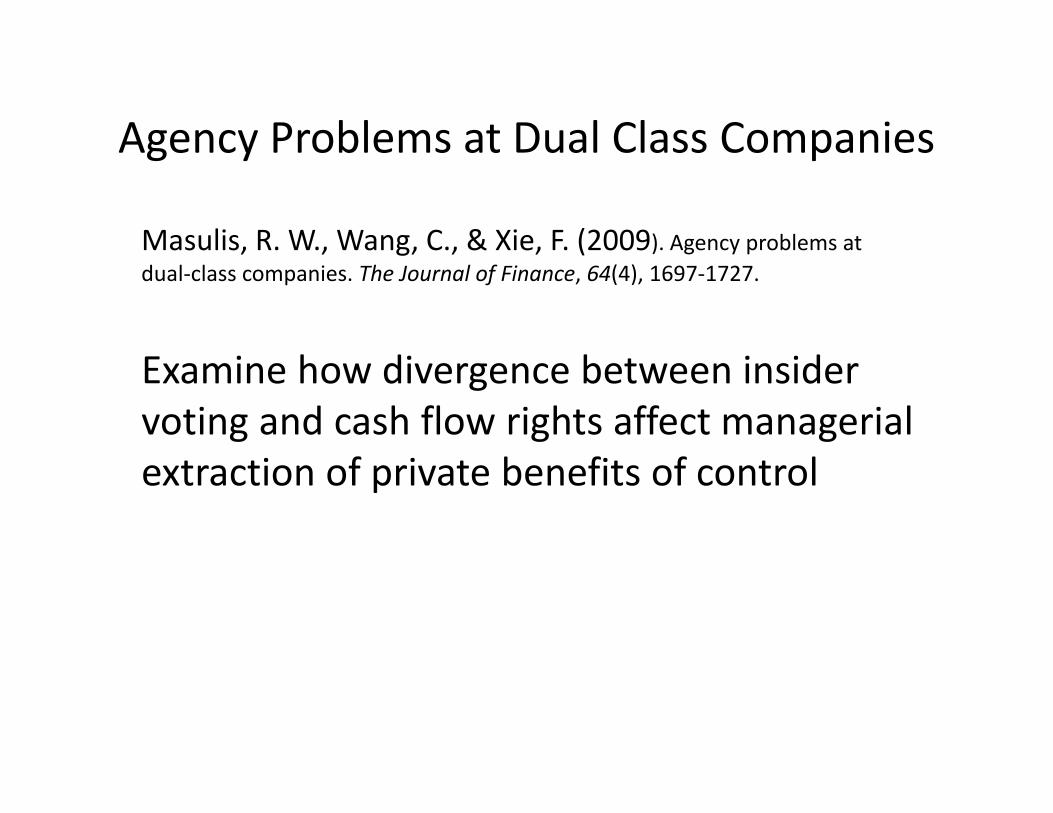

Agency Problems at Dual Class CompaniesAgency Problems at Dual Class Companies

Masulis, R. W., Wang, C., & Xie, F. (2009). Agency problems at , , g, , , ( ) g y pdual‐class companies. The Journal of Finance, 64(4), 1697‐1727.

h d b dExamine how divergence between insider voting and cash flow rights affect managerial

i f i b fi f lextraction of private benefits of control

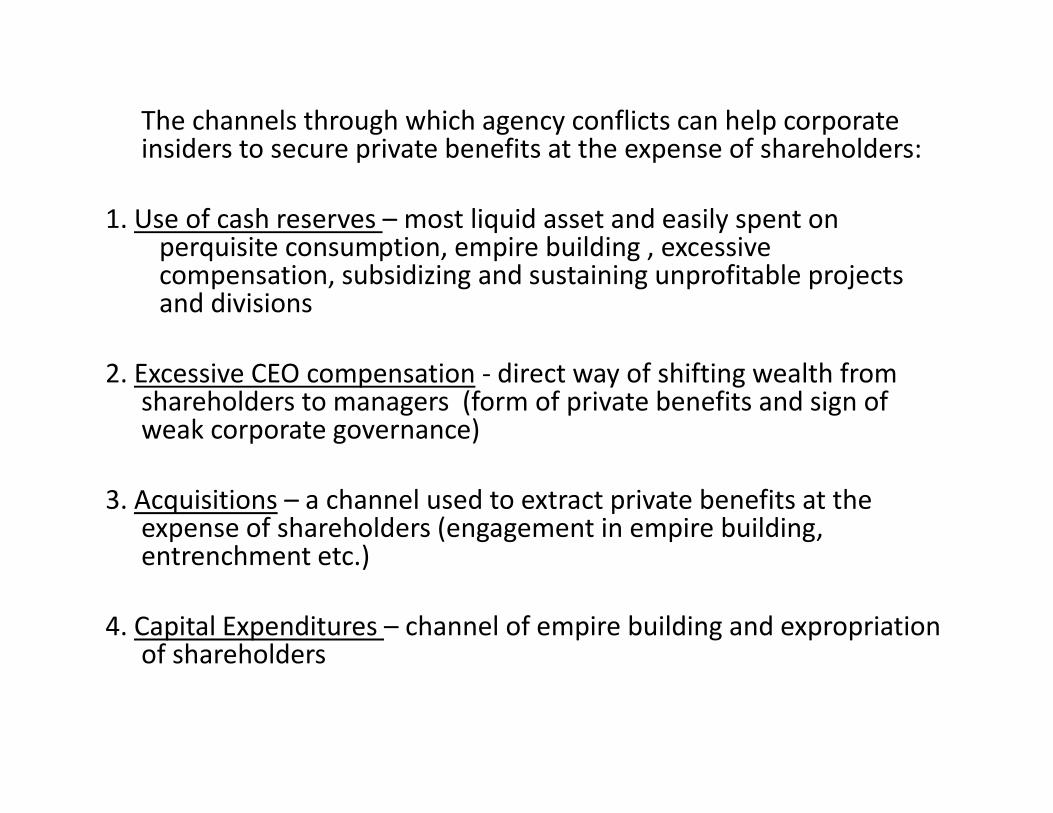

The channels through which agency conflicts can help corporate insiders to secure private benefits at the expense of shareholders:insiders to secure private benefits at the expense of shareholders:

1. Use of cash reserves – most liquid asset and easily spent on perquisite consumption, empire building , excessiveperquisite consumption, empire building , excessive compensation, subsidizing and sustaining unprofitable projects and divisions

2. Excessive CEO compensation ‐ direct way of shifting wealth from shareholders to managers (form of private benefits and sign of weak corporate governance)

3. Acquisitions – a channel used to extract private benefits at the expense of shareholders (engagement in empire building, entrenchment etc )entrenchment etc.)

4. Capital Expenditures – channel of empire building and expropriation of shareholdersof shareholders

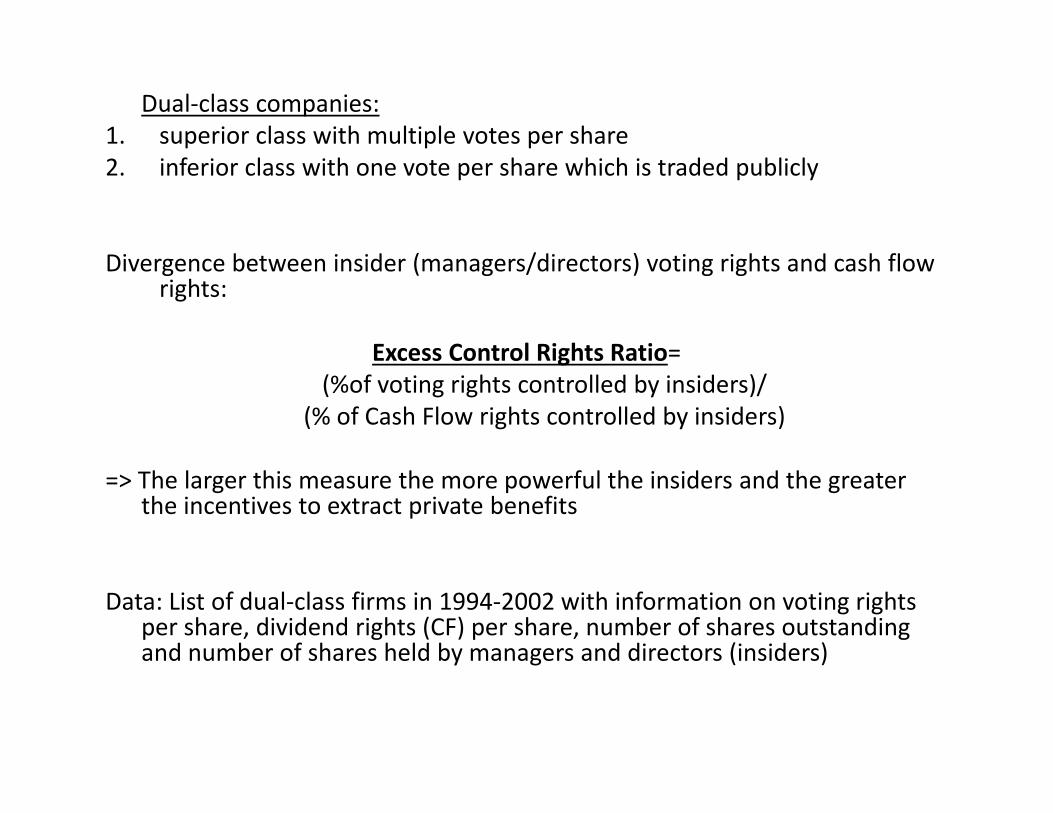

Dual‐class companies: 1. superior class with multiple votes per share2. inferior class with one vote per share which is traded publicly

( / )Divergence between insider (managers/directors) voting rights and cash flow rights:

Excess Control Rights Ratio=Excess Control Rights Ratio=(%of voting rights controlled by insiders)/

(% of Cash Flow rights controlled by insiders)

=> The larger this measure the more powerful the insiders and the greater the incentives to extract private benefits

Data: List of dual‐class firms in 1994‐2002 with information on voting rights per share, dividend rights (CF) per share, number of shares outstanding and number of shares held by managers and directors (insiders)y g ( )

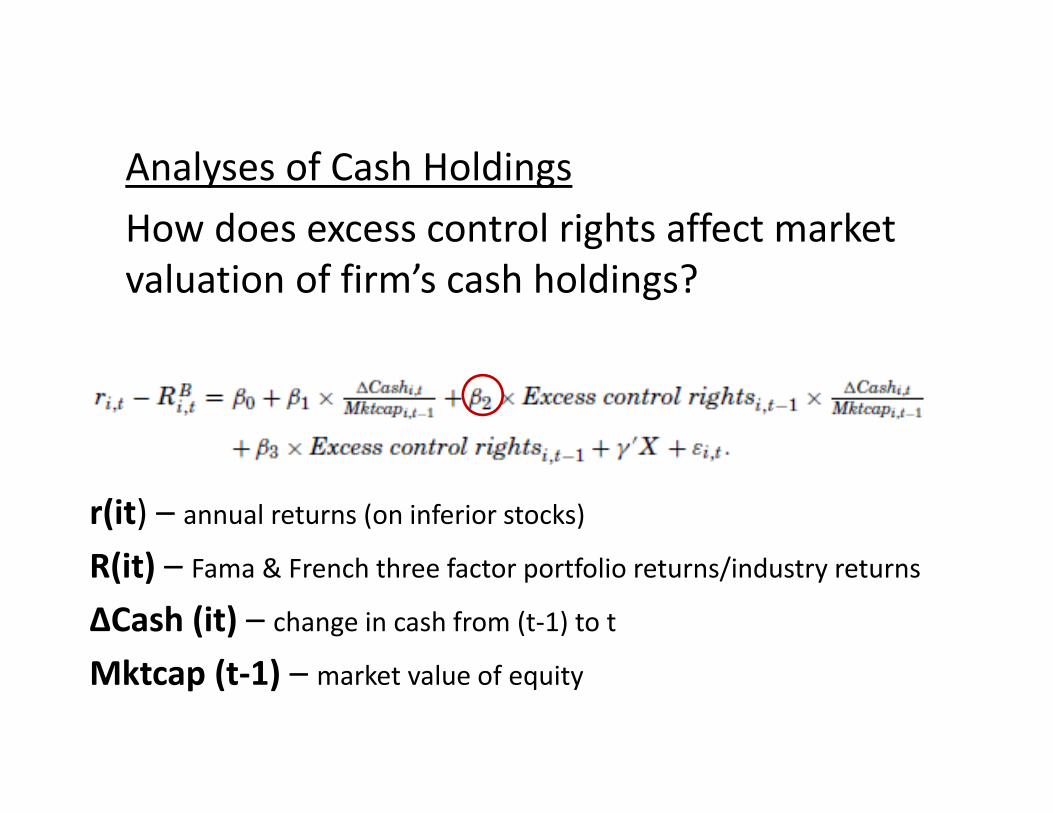

Analyses of Cash HoldingsHow does excess control rights affect market valuation of firm’s cash holdings?

r(it) – annual returns (on inferior stocks)

R(it) F & F h th f t tf li t /i d t tR(it) – Fama & French three factor portfolio returns/industry returns

∆Cash (it) – change in cash from (t‐1) to t

Mkt (t 1)Mktcap (t‐1) – market value of equity

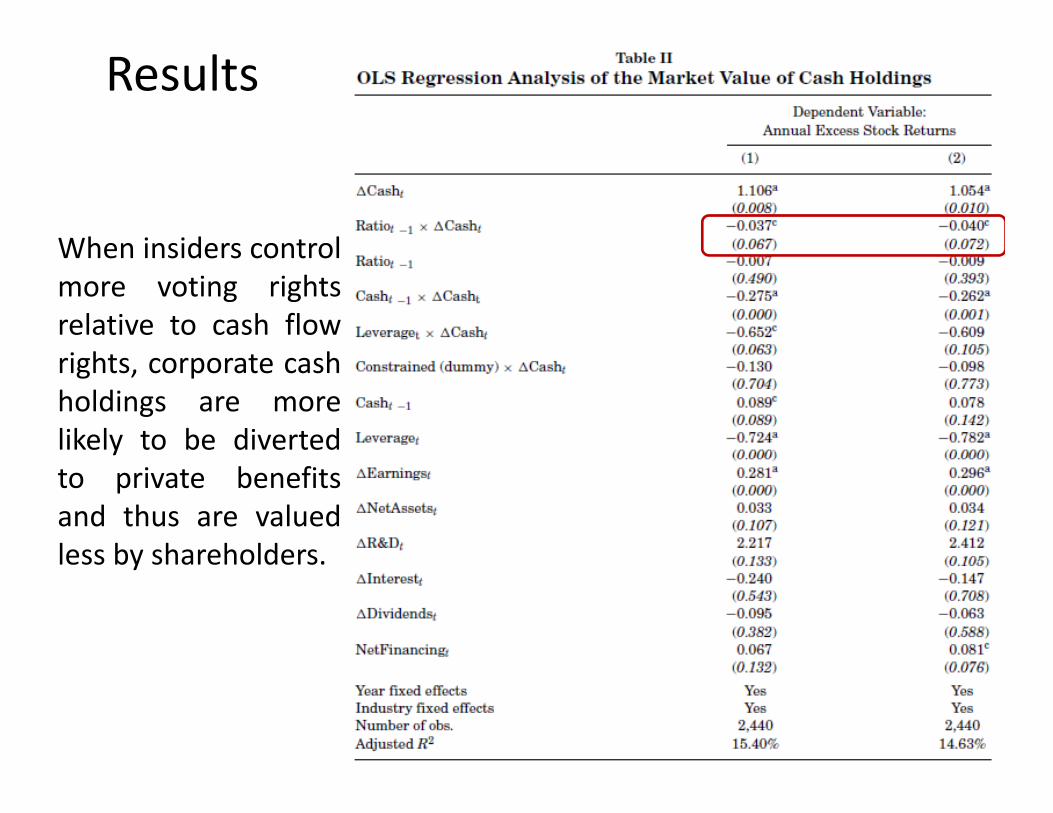

Results

When insiders controlWhen insiders controlmore voting rightsrelative to cash flowi ht t hrights, corporate cashholdings are morelikely to be divertedto private benefitsand thus are valuedless by shareholdersless by shareholders.

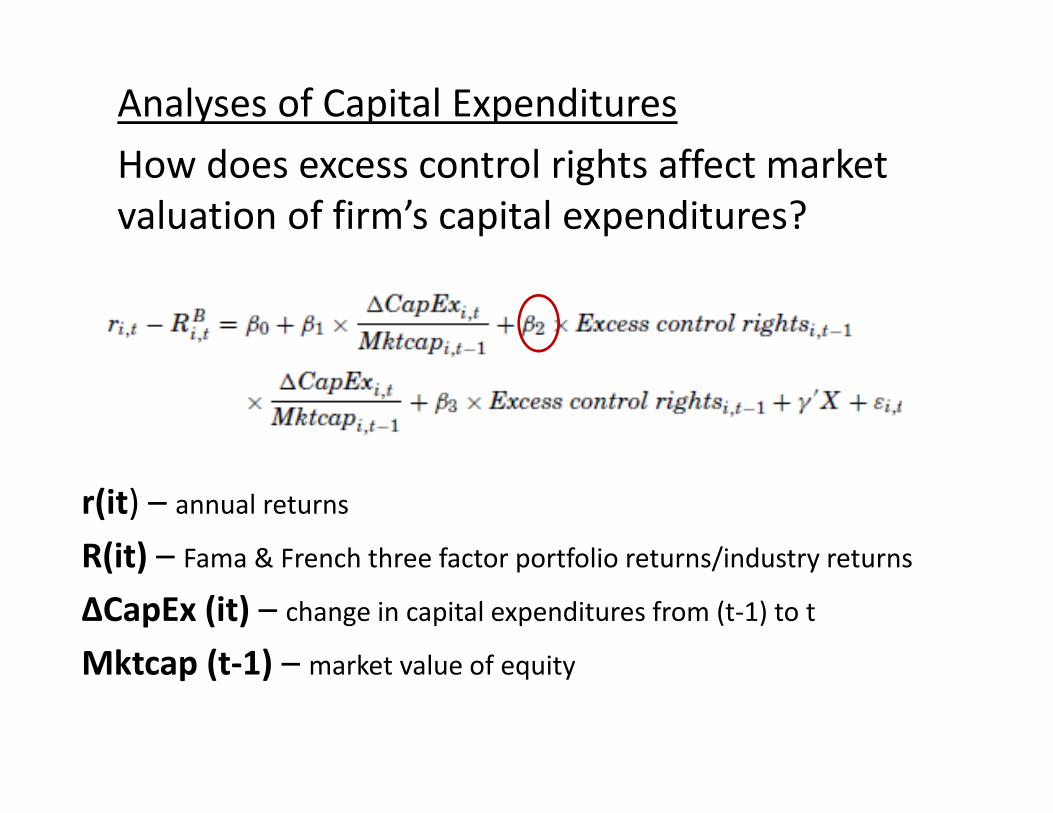

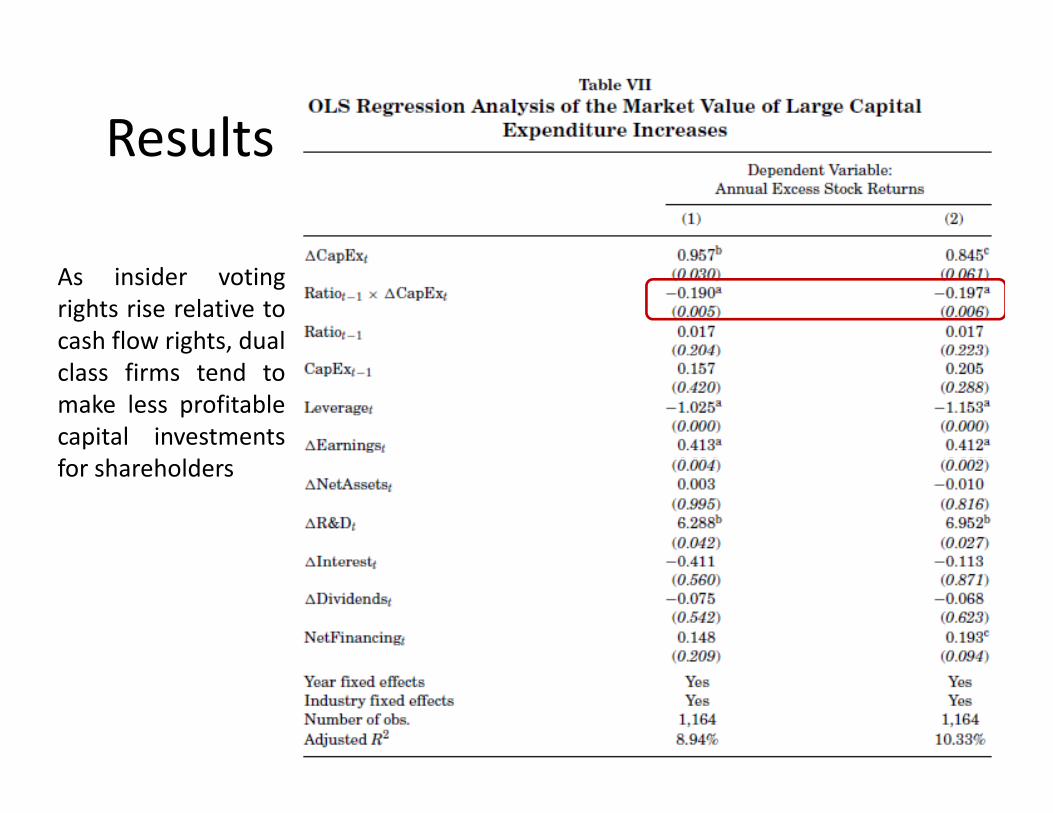

Analyses of Capital Expendituresd l i h ff kHow does excess control rights affect market

valuation of firm’s capital expenditures?

r(it) – annual returns

R(it) – Fama & French three factor portfolio returns/industry returnsR(it) Fama & French three factor portfolio returns/industry returns

∆CapEx (it) – change in capital expenditures from (t‐1) to t

Mktcap (t 1) – market value of equityMktcap (t‐1) – market value of equity

ResultsResults

As insider votingrights rise relative tocash flow rights, dualclass firms tend tomake less profitablecapital investmentsfor shareholders

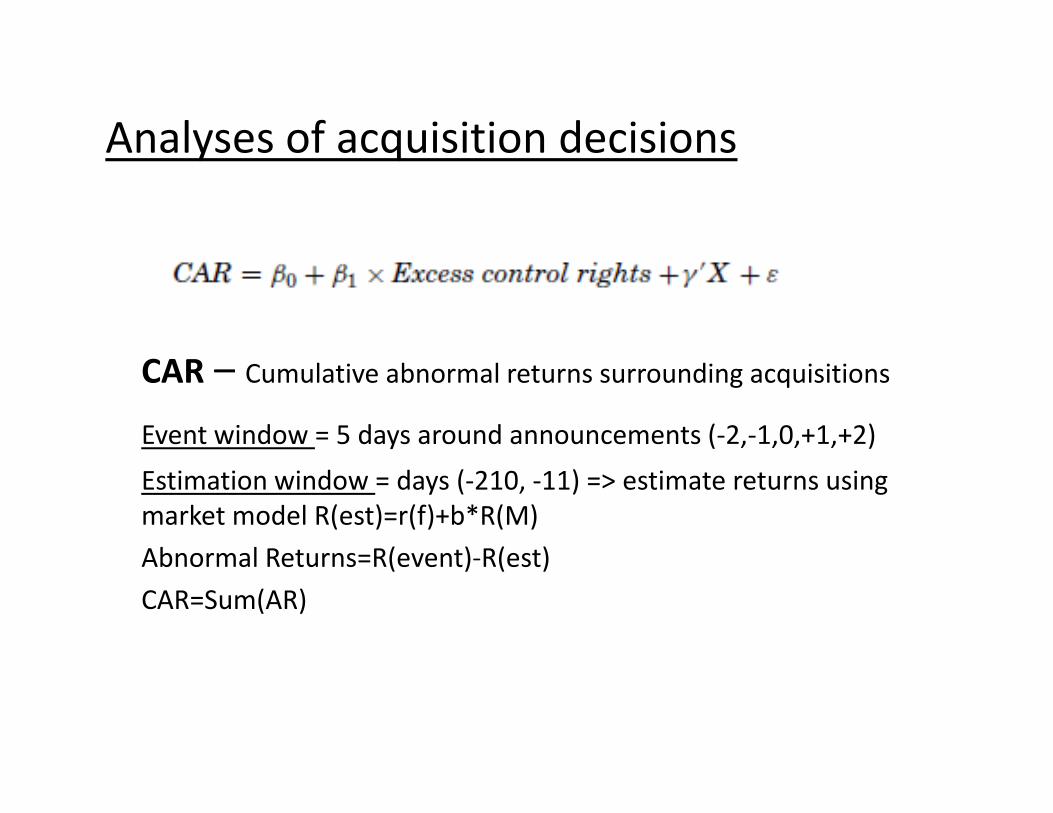

Analyses of acquisition decisionsAnalyses of acquisition decisions

CAR – Cumulative abnormal returns surrounding acquisitions

Event window = 5 days around announcements (‐2,‐1,0,+1,+2)Estimation window = days (‐210, ‐11) => estimate returns using market model R(est)=r(f)+b*R(M)Abnormal Returns=R(event)‐R(est)Abnormal Returns=R(event) R(est)CAR=Sum(AR)

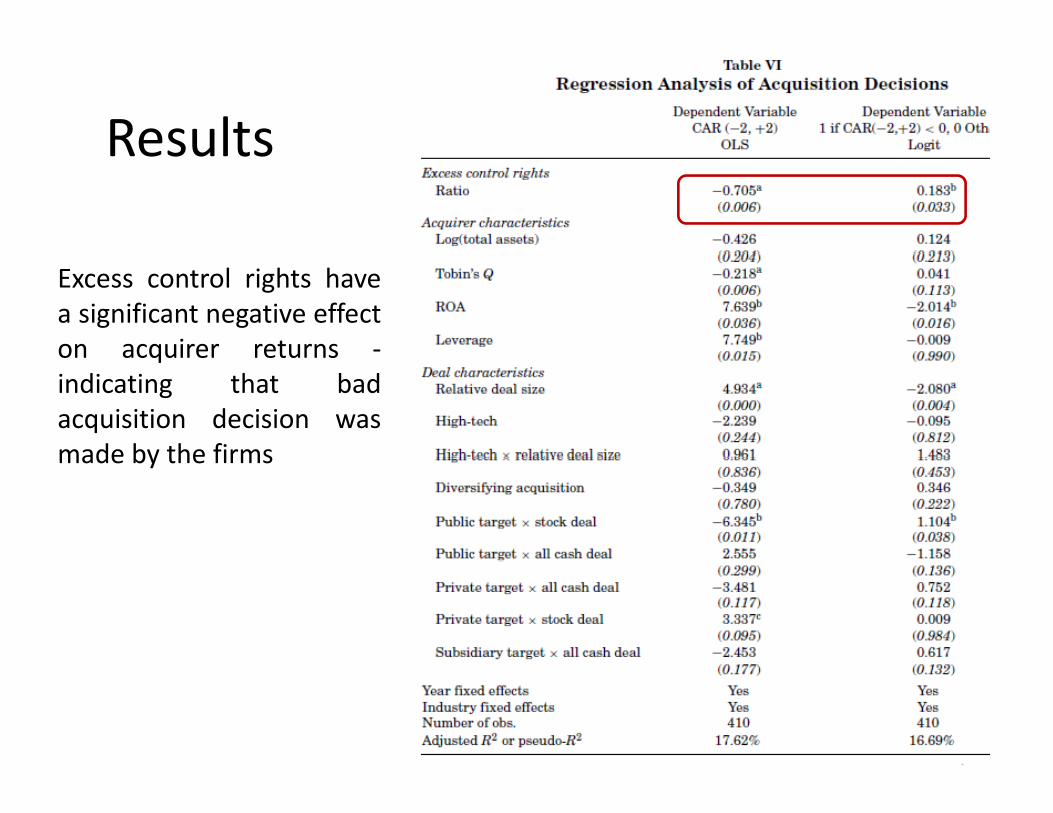

ResultsResults

Excess control rights havea significant negative effecton acquirer returns ‐on acquirer returnsindicating that badacquisition decision wasmade by the firmsmade by the firms

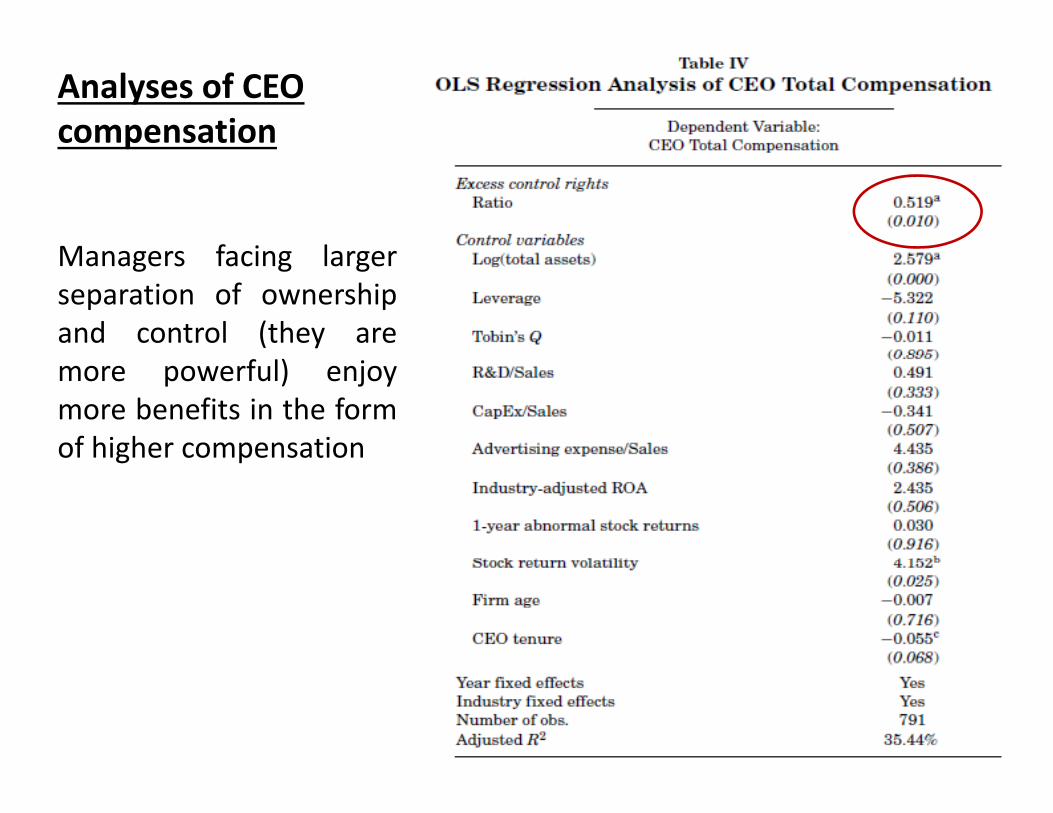

Analyses of CEO compensation

Managers facing largerManagers facing largerseparation of ownershipand control (they aremore powerful) enjoymore benefits in the formof higher compensationg p

References:References: *Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance.

The journal of finance, 52(2), 737‐783.

*Gompers, P. A., Ishii, J. L., & Metrick, A. (2001). Corporate governance p , , , , , ( ) p gand equity prices (No. w8449). National bureau of economic research.

*Masulis, R. W., Wang, C., & Xie, F. (2009). Agency problems at dual‐class companies. The Journal of Finance, 64(4), 1697‐1727.

Bebchuk, L., Cohen, A., & Ferrell, A. (2009). What matters in corporate governance?. Review of Financial studies, 22(2), 783‐827.