consumer finance survey - bangko sentral ng pilipinas · consumer finance survey 2014 a survey...

TRANSCRIPT

Consumer Finance Survey

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

TABLE OF CONTENTS

I. About the Survey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

II. Key Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

A. Demographic Characteristics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B. Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Respondent’s Residence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Other Real Property Ownership (Apart from Respondent’s Residence). .

3. Ownership of Vehicles and Other Non-Financial Assets . . . . . . . . . . . . .

4. Financial Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Insurance and Pension . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Inheritance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. Credit Cards and Other Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

C. Income and Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Work and Income of Respondents and Spouses. . . . . . . . . . . . . . . . . . . . .

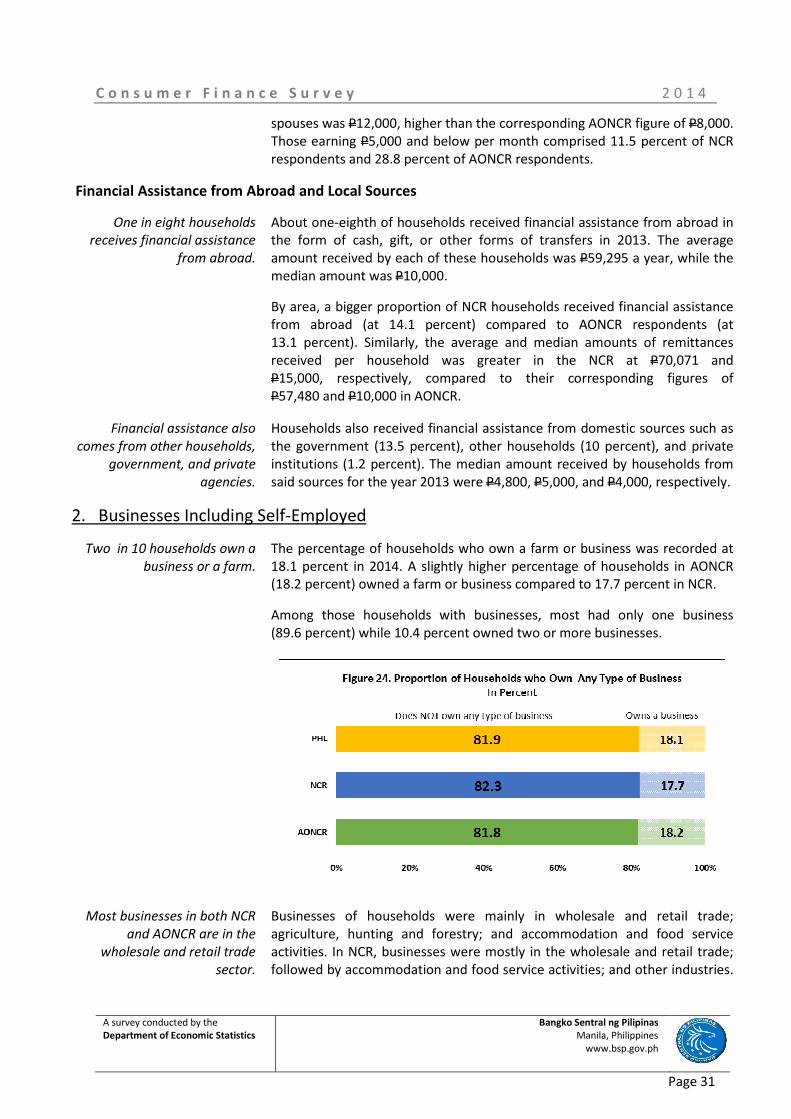

2. Businesses Including Self-Employed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

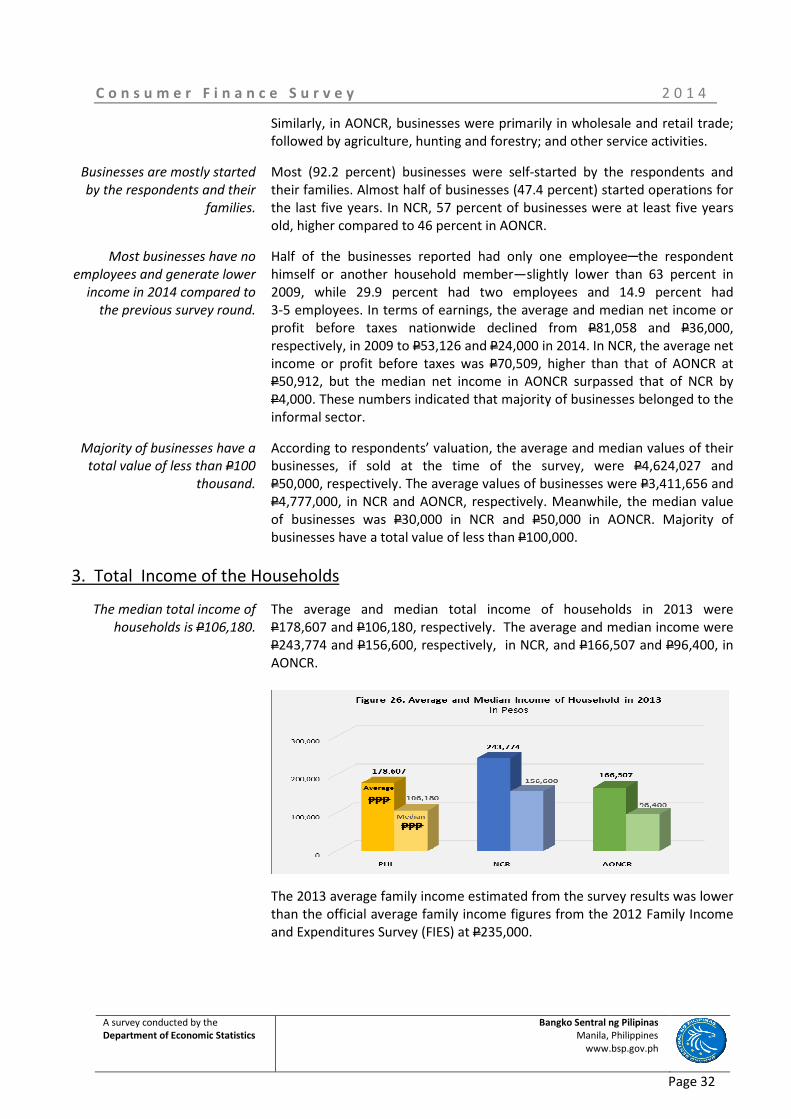

3. Total Income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

D. Preferences and Behaviors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

E. Respondents’ Profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

6

7

12

14

19

23

25

26

28

28

31

33

33

35

36

III. Policy Implications and Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

IV. Statistical Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

A. Demographic Characteristics. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

B. Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Respondent’s Residence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2. Other Real Property Ownership (Apart from Respondent’s Residence). .

3. Ownership of Vehicles and Other Non-Financial Assets . . . . . . . . . . . . .

4. Financial Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5. Insurance and Pension . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6. Inheritance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7. Credit Cards and Other Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

C. Income and Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1. Work and Income of Respondents and Spouses . . . . . . . . . . . . . . . . . . . .

2. Businesses Including Self-Employed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. Total Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4. Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

D. Preferences and Behaviors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

E. Respondents’ Profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

38

39

39

43

44

49

53

56

56

59

62

67

70

71

78

79

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 2

I. About the survey

The Consumer Finance Survey (CFS) is a nationwide quadrennial survey on consumer finances among

Filipino households. The CFS generates data on the financial conditions of households, including what

they own (financial and non-financial assets) as well as from whom and how much they borrow (sources

of credit and level of indebtedness). It also generates data on the income, spending and insurance

coverage of households.

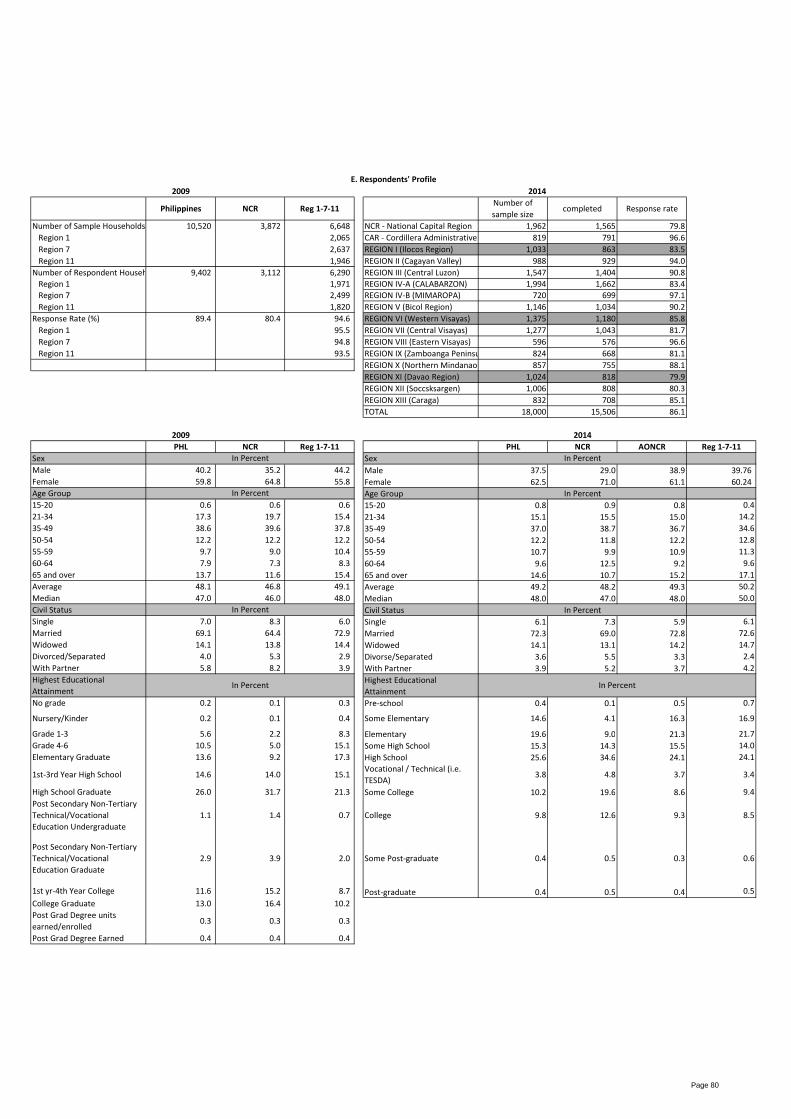

The 2014 CFS has a sample size of 18,000 households covering all regions in the country, except Leyte

province (displaced due to typhoon Yolanda) and Autonomous Region in Muslim Mindanao (ARMM). By

contrast, the inaugural 2009 CFS consisted of a smaller sample size of 10,520 households covering

Regions 1, 7 and 11 only. The bigger sample size for the 2014 survey is more representative of the

financial conditions of households in the country. The domains of the survey are National Capital Region

(NCR) and Areas Outside NCR (AONCR). The survey made use of the 2003 Master Sample (MS2003) of

the Philippine Statistics Authority (PSA). The MS2003 uses a two-stage sampling with stratification at

the Primary Sampling Unit (PSU) level. In the first stage, households were stratified in terms of

Enumeration Areas (EA)/Barangays. Random samples of EAs were drawn in each region with probability

proportional to the size (i.e., total number of households) of the EA. In the second sampling stage,

random samples of 12 households for NCR and 16 for AONCR were selected from each of the sample

EAs.

The PSA, through its Survey Review and Clearance System, gave the clearance to conduct the CFS after

their review of the CFS survey design and questionnaire. To encourage participation in the survey, a

letter signed by the BSP Governor was sent to each of the sample households, informing them of the

CFS and its objectives, inviting them to participate in the CFS and assuring them of the confidentiality of

their responses. The data collection was conducted starting July 2014 until end-January 2015. The

survey had an overall response rate of 86.2 percent. Details of response rates are as follows:

Area Sample

Households

Percent Share

of Sample

Households

Respondent

Households

Response

Rate

Philippines 18,000 100.0 15,503 86.1

NCR 1,962 10.9 1,565 79.8

AONCR 16,038 89.1 13,938 86.9

North/Central Luzon 4,387 24.4 3,987 90.9

South Luzon 3,860 21.4 3,395 88.0

Visayas 3,248 18.0 2,799 86.2

Mindanao 4,543 25.2 3,757 82.7

In each of the sample households, using a set of screening questions, the enumerator identified the

survey respondent―the person living in the household who is the most knowledgeable and credible to

answer questions about household finances. At anytime during the interview, the selected respondent

could consult any person in their household or look for a document that could help him answer

accurately the questions being asked by the interviewer.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 3

The CFS generally followed the PSA’s definition of household membership.1 Data on demographic

characteristics of sample households covered all the members of the household. For assets and

liabilities as well as income and expenditures of the household, only the Primary Economic Unit (PEU)

within the household was covered. The PEU consists of the survey respondent, his/her spouse (if any),

and other members of the household whose finances are interdependent with the respondent and/or

the spouse. Finances of other members of the household such as those of hired help, boarders, and

financially independent household members were not included.2 In the survey report, the term

“household” refers to the sample household.

Data on work, income and expenditures of households were for full year 2013 (the calendar year

preceding the survey) while the data pertaining to demographics, assets and liabilities, and preferences

and behaviors were reckoned on the date the household was interviewed (i.e., within the period from

July 2014 to end-January 2015).

Considering the differences in coverage of the 2009 and 2014 CFS, changes in the survey results

between the two periods were analyzed for comparative survey areas i.e., NCR and Regions 1, 7, and

11 in AONCR only.

The CFS questionnaire was translated in five dialects with the most number of respondents: Tagalog,

Ilonggo, Visayan, Bicolano and Ilocano, with English translation for each question. Questionnaires

translated in local dialects are back-translated to ensure that the translations and the essence of the

questions are consistent. Taylor Nelson Sofres (TNS), a research agency based in the Philippines which

provides consulting services in market research and household surveys, was contracted by the BSP to

perform the data collection, enumeration and data encoding of the results. They used the door-to-door

and face-to-face interview method in their data collection. Statistical tables of the CFS were generated

using Stata and SPSS software.

II. Key Findings

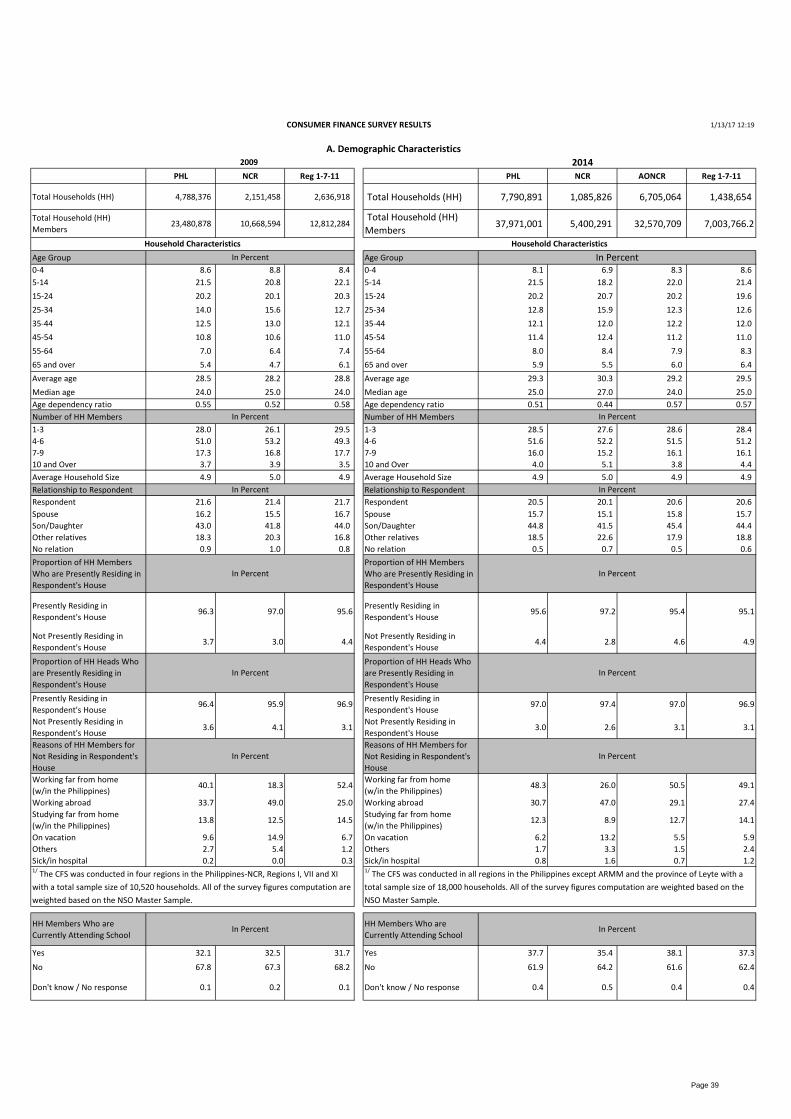

A. Demographic Characteristics

The age composition of

household members

indicates a significant

increase in the labor force

for the next ten years...

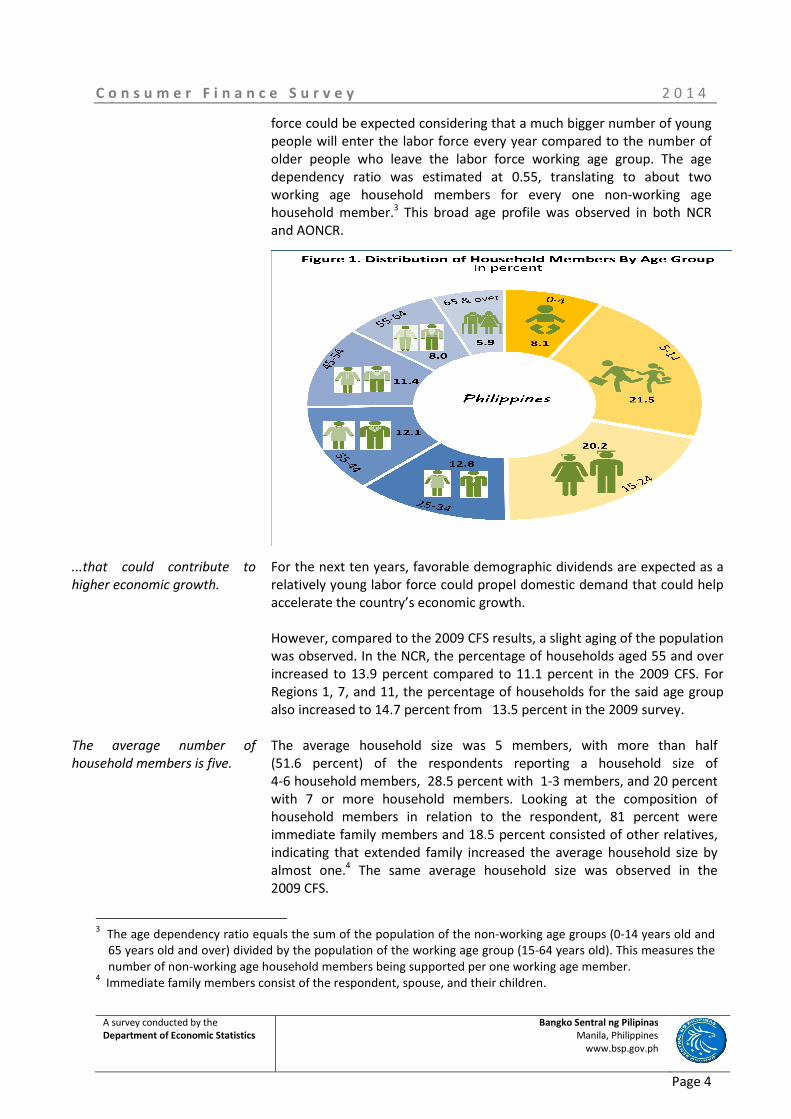

The results of the survey showed that the Philippines has a young

population. The age distribution of household members showed that

8.1 percent were 0-4 years old, 21.5 percent were 5-14 years old,

20.2 percent were 15-24 years old, 12.8 percent were 25-34 years old,

12.1 percent were 35 -44 years old and 11.4 percent were 45-54 years

old. Meanwhile, those who were about to retire or were close to

compulsory retirement (aged 55-64 years old) and the elderly (65 years

old and over) accounted for 8.0 percent and 5.9 percent of the household

members, respectively, at the time of the survey. The average and

median age of the population are 29.3 years and 25 years, respectively.

These figures indicated that a significant increase in the country’s labor

1 A household is a social unit consisting of a person living alone or a group of persons who sleep in the same

housing unit and have a common arrangement in the preparation and consumption of food. Meanwhile, in

determining household membership, a basic criterion is the usual place of residence or the place where the

person usually resides. This may be the same or different from the place where he is found at the time of the

census. 2 A household member is considered to be financially independent if he/she provides/pays for his/her expenses in

at least two of the three major expense categories: rent, food, and other living expenses.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 4

force could be expected considering that a much bigger number of young

people will enter the labor force every year compared to the number of

older people who leave the labor force working age group. The age

dependency ratio was estimated at 0.55, translating to about two

working age household members for every one non-working age

household member.3 This broad age profile was observed in both NCR

and AONCR.

...that could contribute to

higher economic growth.

For the next ten years, favorable demographic dividends are expected as a

relatively young labor force could propel domestic demand that could help

accelerate the country’s economic growth.

However, compared to the 2009 CFS results, a slight aging of the population

was observed. In the NCR, the percentage of households aged 55 and over

increased to 13.9 percent compared to 11.1 percent in the 2009 CFS. For

Regions 1, 7, and 11, the percentage of households for the said age group

also increased to 14.7 percent from 13.5 percent in the 2009 survey.

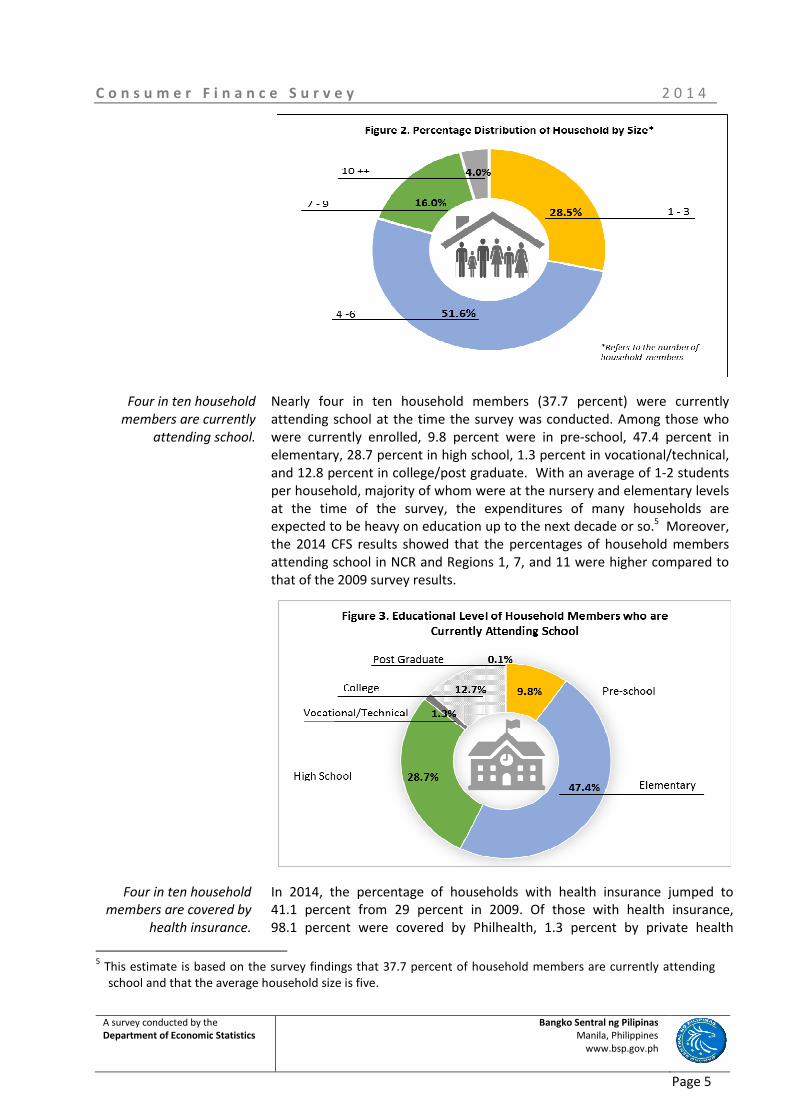

The average number of

household members is five.

The average household size was 5 members, with more than half

(51.6 percent) of the respondents reporting a household size of

4-6 household members, 28.5 percent with 1-3 members, and 20 percent

with 7 or more household members. Looking at the composition of

household members in relation to the respondent, 81 percent were

immediate family members and 18.5 percent consisted of other relatives,

indicating that extended family increased the average household size by

almost one.4 The same average household size was observed in the

2009 CFS.

3 The age dependency ratio equals the sum of the population of the non-working age groups (0-14 years old and

65 years old and over) divided by the population of the working age group (15-64 years old). This measures the

number of non-working age household members being supported per one working age member. 4 Immediate family members consist of the respondent, spouse, and their children.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 5

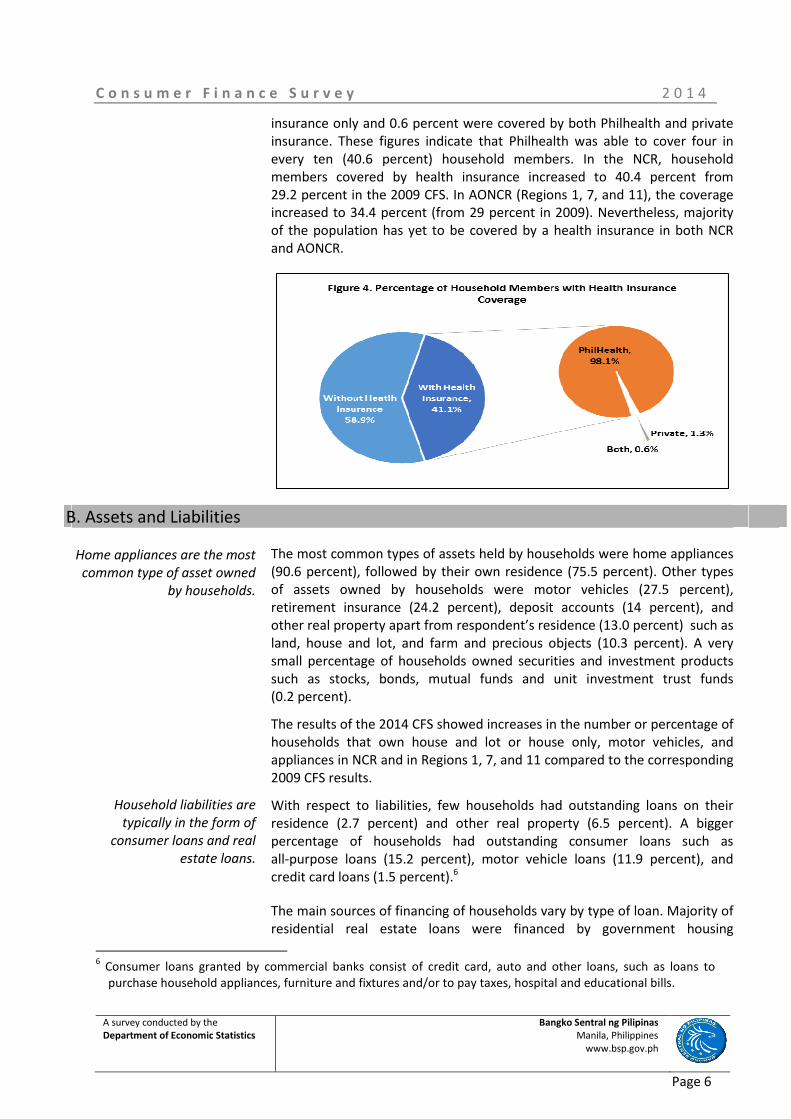

Four in ten household

members are currently

attending school.

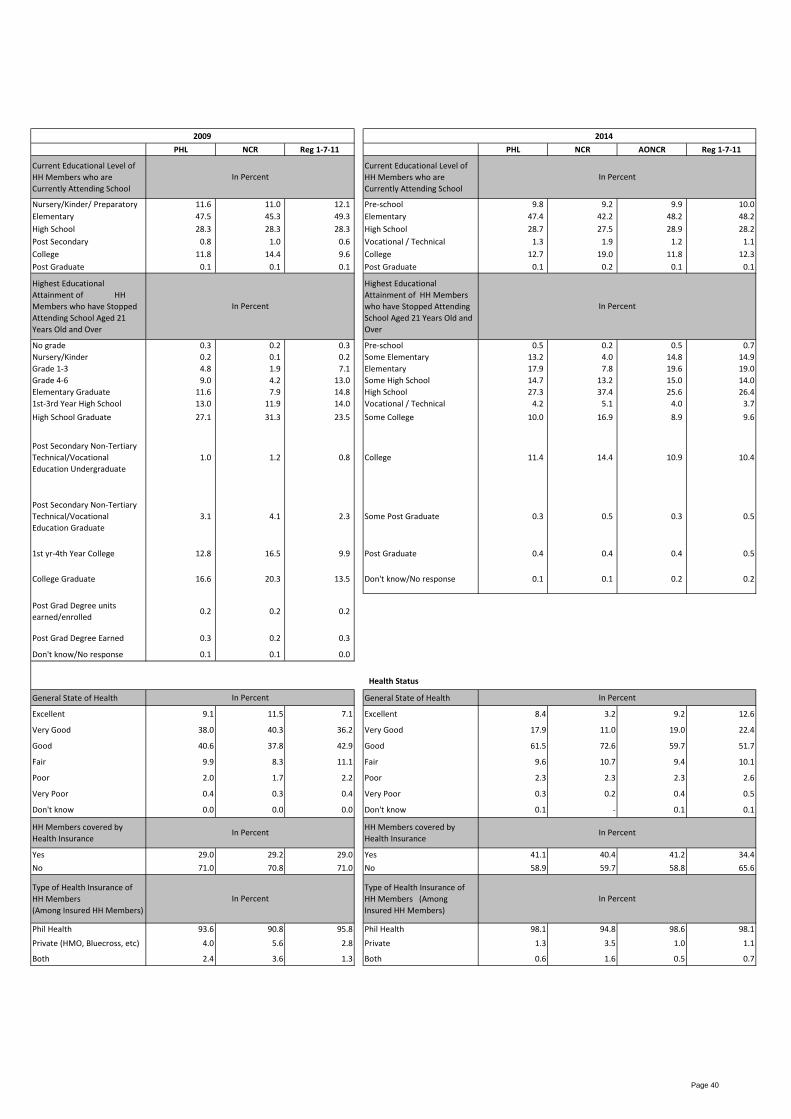

Nearly four in ten household members (37.7 percent) were currently

attending school at the time the survey was conducted. Among those who

were currently enrolled, 9.8 percent were in pre-school, 47.4 percent in

elementary, 28.7 percent in high school, 1.3 percent in vocational/technical,

and 12.8 percent in college/post graduate. With an average of 1-2 students

per household, majority of whom were at the nursery and elementary levels

at the time of the survey, the expenditures of many households are

expected to be heavy on education up to the next decade or so.5 Moreover,

the 2014 CFS results showed that the percentages of household members

attending school in NCR and Regions 1, 7, and 11 were higher compared to

that of the 2009 survey results.

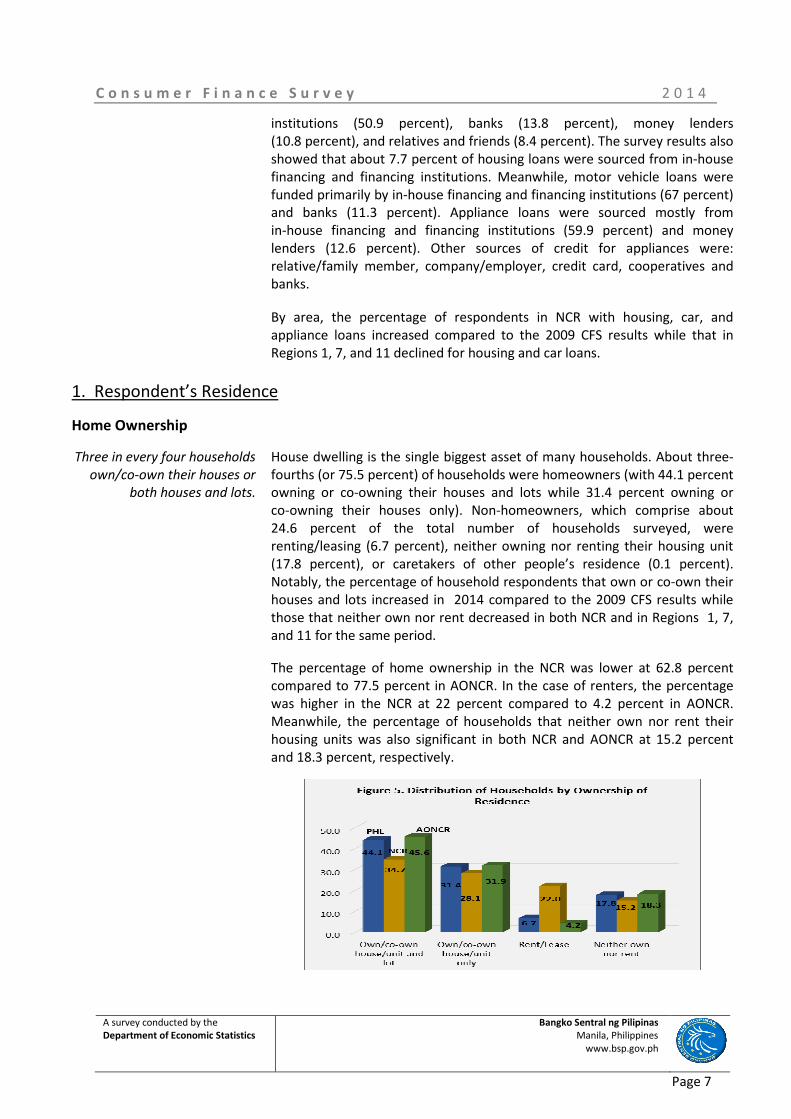

Four in ten household

members are covered by

health insurance.

In 2014, the percentage of households with health insurance jumped to

41.1 percent from 29 percent in 2009. Of those with health insurance,

98.1 percent were covered by Philhealth, 1.3 percent by private health

5 This estimate is based on the survey findings that 37.7 percent of household members are currently attending

school and that the average household size is five.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 6

insurance only and 0.6 percent were covered by both Philhealth and private

insurance. These figures indicate that Philhealth was able to cover four in

every ten (40.6 percent) household members. In the NCR, household

members covered by health insurance increased to 40.4 percent from

29.2 percent in the 2009 CFS. In AONCR (Regions 1, 7, and 11), the coverage

increased to 34.4 percent (from 29 percent in 2009). Nevertheless, majority

of the population has yet to be covered by a health insurance in both NCR

and AONCR.

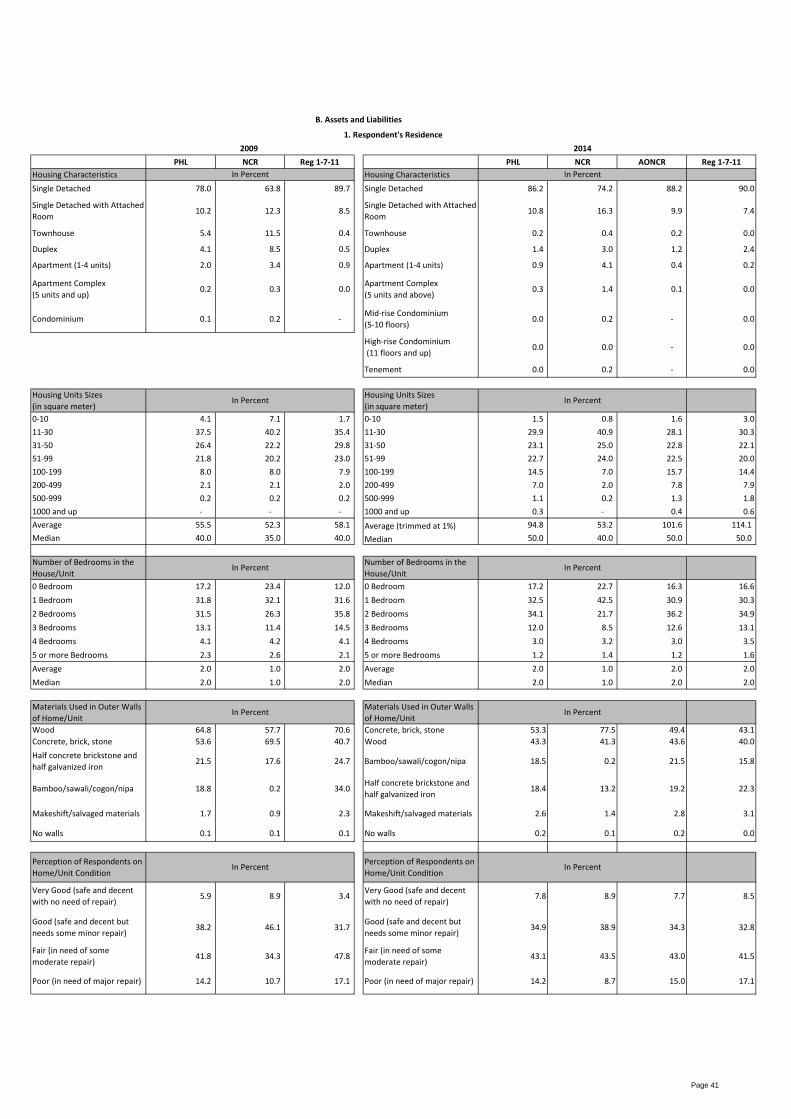

B. Assets and Liabilities

Home appliances are the most

common type of asset owned

by households.

Household liabilities are

typically in the form of

consumer loans and real

estate loans.

The most common types of assets held by households were home appliances

(90.6 percent), followed by their own residence (75.5 percent). Other types

of assets owned by households were motor vehicles (27.5 percent),

retirement insurance (24.2 percent), deposit accounts (14 percent), and

other real property apart from respondent’s residence (13.0 percent) such as

land, house and lot, and farm and precious objects (10.3 percent). A very

small percentage of households owned securities and investment products

such as stocks, bonds, mutual funds and unit investment trust funds

(0.2 percent).

The results of the 2014 CFS showed increases in the number or percentage of

households that own house and lot or house only, motor vehicles, and

appliances in NCR and in Regions 1, 7, and 11 compared to the corresponding

2009 CFS results.

With respect to liabilities, few households had outstanding loans on their

residence (2.7 percent) and other real property (6.5 percent). A bigger

percentage of households had outstanding consumer loans such as

all-purpose loans (15.2 percent), motor vehicle loans (11.9 percent), and

credit card loans (1.5 percent).6

The main sources of financing of households vary by type of loan. Majority of

residential real estate loans were financed by government housing

6 Consumer loans granted by commercial banks consist of credit card, auto and other loans, such as loans to

purchase household appliances, furniture and fixtures and/or to pay taxes, hospital and educational bills.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 7

institutions (50.9 percent), banks (13.8 percent), money lenders

(10.8 percent), and relatives and friends (8.4 percent). The survey results also

showed that about 7.7 percent of housing loans were sourced from in-house

financing and financing institutions. Meanwhile, motor vehicle loans were

funded primarily by in-house financing and financing institutions (67 percent)

and banks (11.3 percent). Appliance loans were sourced mostly from

in-house financing and financing institutions (59.9 percent) and money

lenders (12.6 percent). Other sources of credit for appliances were:

relative/family member, company/employer, credit card, cooperatives and

banks. By area, the percentage of respondents in NCR with housing, car, and

appliance loans increased compared to the 2009 CFS results while that in

Regions 1, 7, and 11 declined for housing and car loans.

1. Respondent’s Residence

Home Ownership

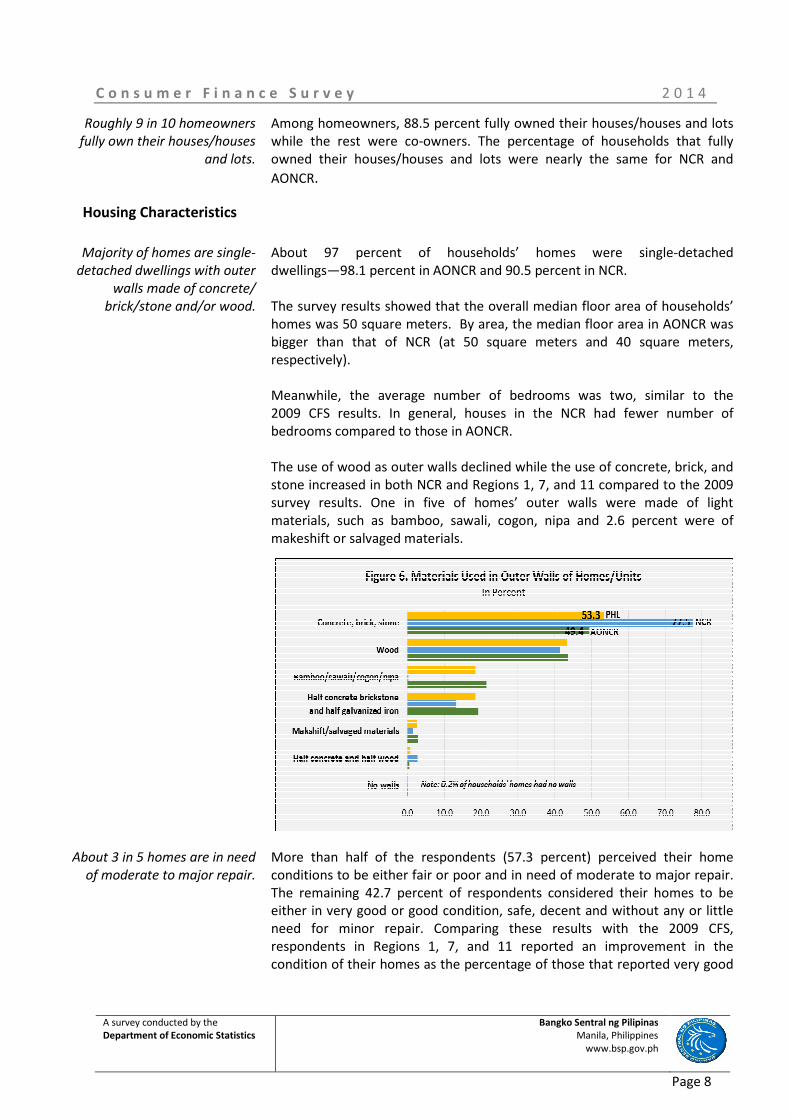

Three in every four households

own/co-own their houses or

both houses and lots.

House dwelling is the single biggest asset of many households. About three-

fourths (or 75.5 percent) of households were homeowners (with 44.1 percent

owning or co-owning their houses and lots while 31.4 percent owning or

co-owning their houses only). Non-homeowners, which comprise about

24.6 percent of the total number of households surveyed, were

renting/leasing (6.7 percent), neither owning nor renting their housing unit

(17.8 percent), or caretakers of other people’s residence (0.1 percent).

Notably, the percentage of household respondents that own or co-own their

houses and lots increased in 2014 compared to the 2009 CFS results while

those that neither own nor rent decreased in both NCR and in Regions 1, 7,

and 11 for the same period.

The percentage of home ownership in the NCR was lower at 62.8 percent

compared to 77.5 percent in AONCR. In the case of renters, the percentage

was higher in the NCR at 22 percent compared to 4.2 percent in AONCR.

Meanwhile, the percentage of households that neither own nor rent their

housing units was also significant in both NCR and AONCR at 15.2 percent

and 18.3 percent, respectively.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 8

Roughly 9 in 10 homeowners

fully own their houses/houses

and lots.

Among homeowners, 88.5 percent fully owned their houses/houses and lots

while the rest were co-owners. The percentage of households that fully

owned their houses/houses and lots were nearly the same for NCR and

AONCR.

Housing Characteristics

Majority of homes are single-

detached dwellings with outer

walls made of concrete/

brick/stone and/or wood.

About 97 percent of households’ homes were single-detached

dwellings―98.1 percent in AONCR and 90.5 percent in NCR.

The survey results showed that the overall median floor area of households’

homes was 50 square meters. By area, the median floor area in AONCR was

bigger than that of NCR (at 50 square meters and 40 square meters,

respectively).

Meanwhile, the average number of bedrooms was two, similar to the

2009 CFS results. In general, houses in the NCR had fewer number of

bedrooms compared to those in AONCR.

The use of wood as outer walls declined while the use of concrete, brick, and

stone increased in both NCR and Regions 1, 7, and 11 compared to the 2009

survey results. One in five of homes’ outer walls were made of light

materials, such as bamboo, sawali, cogon, nipa and 2.6 percent were of

makeshift or salvaged materials.

About 3 in 5 homes are in need

of moderate to major repair.

More than half of the respondents (57.3 percent) perceived their home

conditions to be either fair or poor and in need of moderate to major repair.

The remaining 42.7 percent of respondents considered their homes to be

either in very good or good condition, safe, decent and without any or little

need for minor repair. Comparing these results with the 2009 CFS,

respondents in Regions 1, 7, and 11 reported an improvement in the

condition of their homes as the percentage of those that reported very good

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 9

and good housing conditions increased while the percentage of those that

have fair or poor housing conditions decreased. The reverse was reported by

NCR respondents.

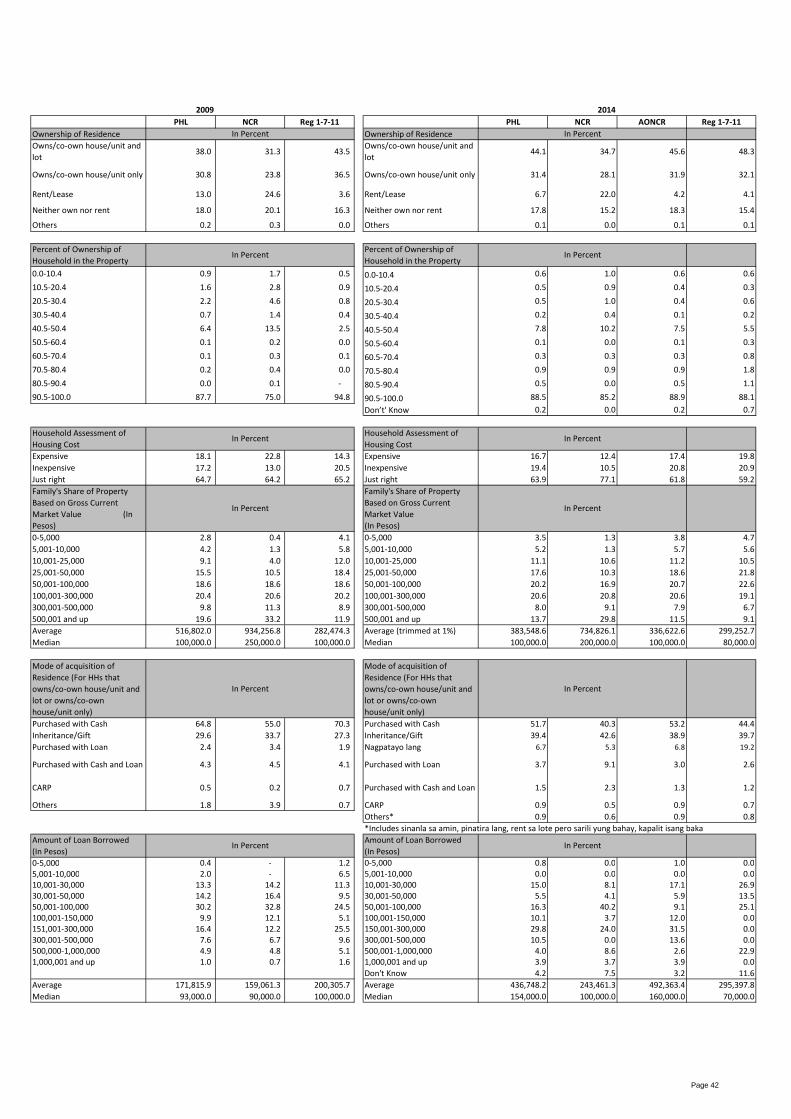

Housing Cost

About 4 in 5 respondents think

that the cost of buying/renting

their homes is not expensive.

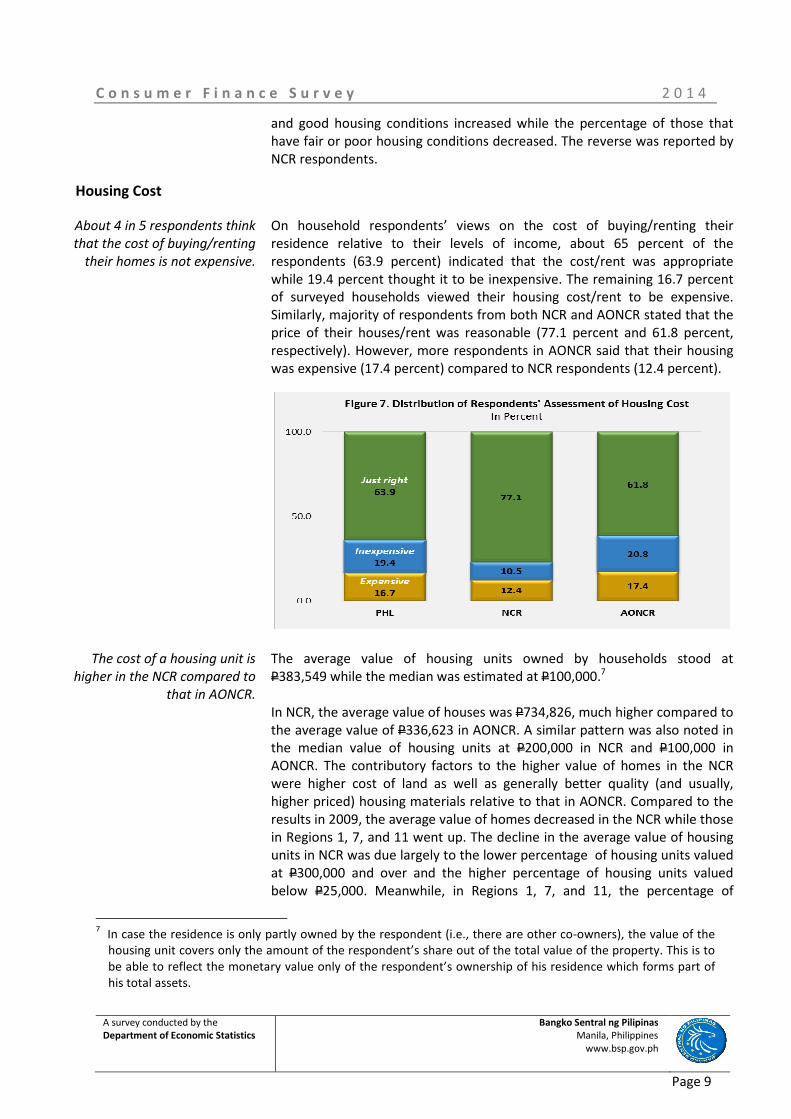

On household respondents’ views on the cost of buying/renting their

residence relative to their levels of income, about 65 percent of the

respondents (63.9 percent) indicated that the cost/rent was appropriate

while 19.4 percent thought it to be inexpensive. The remaining 16.7 percent

of surveyed households viewed their housing cost/rent to be expensive.

Similarly, majority of respondents from both NCR and AONCR stated that the

price of their houses/rent was reasonable (77.1 percent and 61.8 percent,

respectively). However, more respondents in AONCR said that their housing

was expensive (17.4 percent) compared to NCR respondents (12.4 percent).

The cost of a housing unit is

higher in the NCR compared to

that in AONCR.

The average value of housing units owned by households stood at

P383,549 while the median was estimated at P100,000.7

In NCR, the average value of houses was P734,826, much higher compared to

the average value of P336,623 in AONCR. A similar pattern was also noted in

the median value of housing units at P200,000 in NCR and P100,000 in

AONCR. The contributory factors to the higher value of homes in the NCR

were higher cost of land as well as generally better quality (and usually,

higher priced) housing materials relative to that in AONCR. Compared to the

results in 2009, the average value of homes decreased in the NCR while those

in Regions 1, 7, and 11 went up. The decline in the average value of housing

units in NCR was due largely to the lower percentage of housing units valued

at P300,000 and over and the higher percentage of housing units valued

below P25,000. Meanwhile, in Regions 1, 7, and 11, the percentage of

7 In case the residence is only partly owned by the respondent (i.e., there are other co-owners), the value of the

housing unit covers only the amount of the respondent’s share out of the total value of the property. This is to

be able to reflect the monetary value only of the respondent’s ownership of his residence which forms part of

his total assets.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 10

respondents with housing units valued at P50,000 to P300,000 increased.

These results could reflect the assessment of the quality of housing units of

the respondents in NCR and AONCR.

Housing Loans and Mode of Acquisition of Respondent’s Residence

Housing is generally acquired

by households either through

purchase in cash or

inheritance...

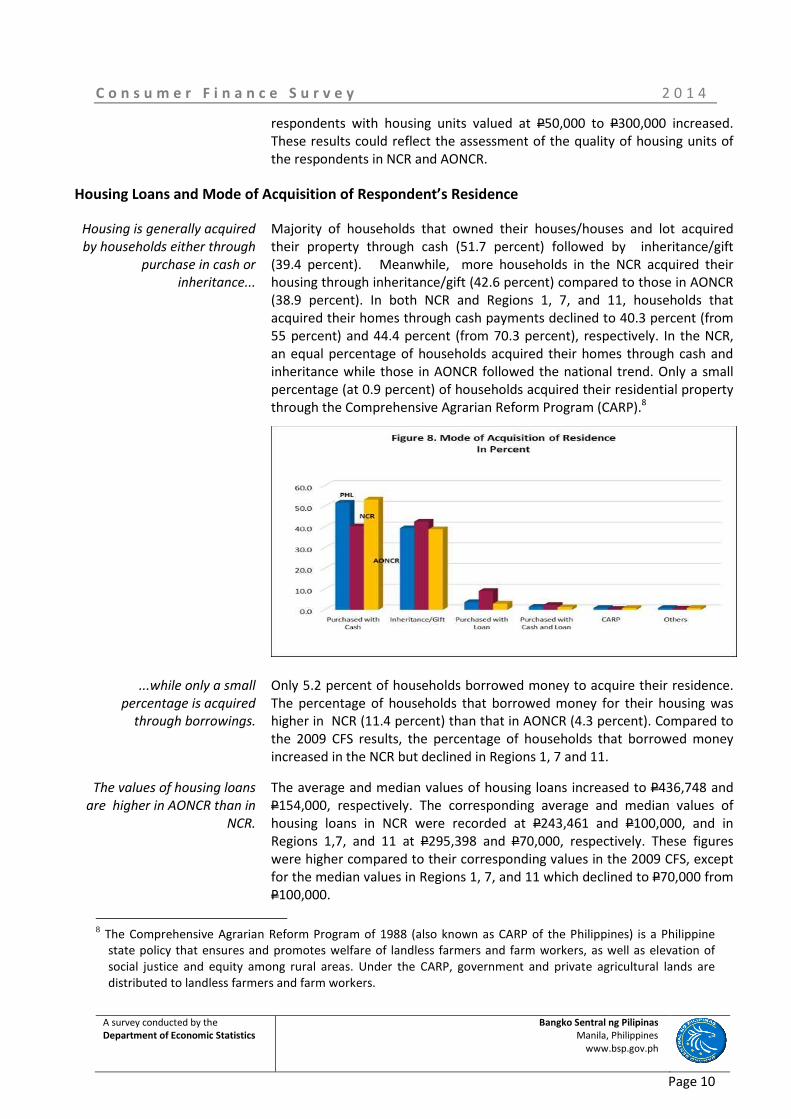

Majority of households that owned their houses/houses and lot acquired

their property through cash (51.7 percent) followed by inheritance/gift

(39.4 percent). Meanwhile, more households in the NCR acquired their

housing through inheritance/gift (42.6 percent) compared to those in AONCR

(38.9 percent). In both NCR and Regions 1, 7, and 11, households that

acquired their homes through cash payments declined to 40.3 percent (from

55 percent) and 44.4 percent (from 70.3 percent), respectively. In the NCR,

an equal percentage of households acquired their homes through cash and

inheritance while those in AONCR followed the national trend. Only a small

percentage (at 0.9 percent) of households acquired their residential property

through the Comprehensive Agrarian Reform Program (CARP).8

...while only a small

percentage is acquired

through borrowings.

Only 5.2 percent of households borrowed money to acquire their residence.

The percentage of households that borrowed money for their housing was

higher in NCR (11.4 percent) than that in AONCR (4.3 percent). Compared to

the 2009 CFS results, the percentage of households that borrowed money

increased in the NCR but declined in Regions 1, 7 and 11.

The values of housing loans

are higher in AONCR than in

NCR.

The average and median values of housing loans increased to P436,748 and

P154,000, respectively. The corresponding average and median values of

housing loans in NCR were recorded at P243,461 and P100,000, and in

Regions 1,7, and 11 at P295,398 and P70,000, respectively. These figures

were higher compared to their corresponding values in the 2009 CFS, except

for the median values in Regions 1, 7, and 11 which declined to P70,000 from

P100,000.

8 The Comprehensive Agrarian Reform Program of 1988 (also known as CARP of the Philippines) is a Philippine

state policy that ensures and promotes welfare of landless farmers and farm workers, as well as elevation of

social justice and equity among rural areas. Under the CARP, government and private agricultural lands are

distributed to landless farmers and farm workers.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 11

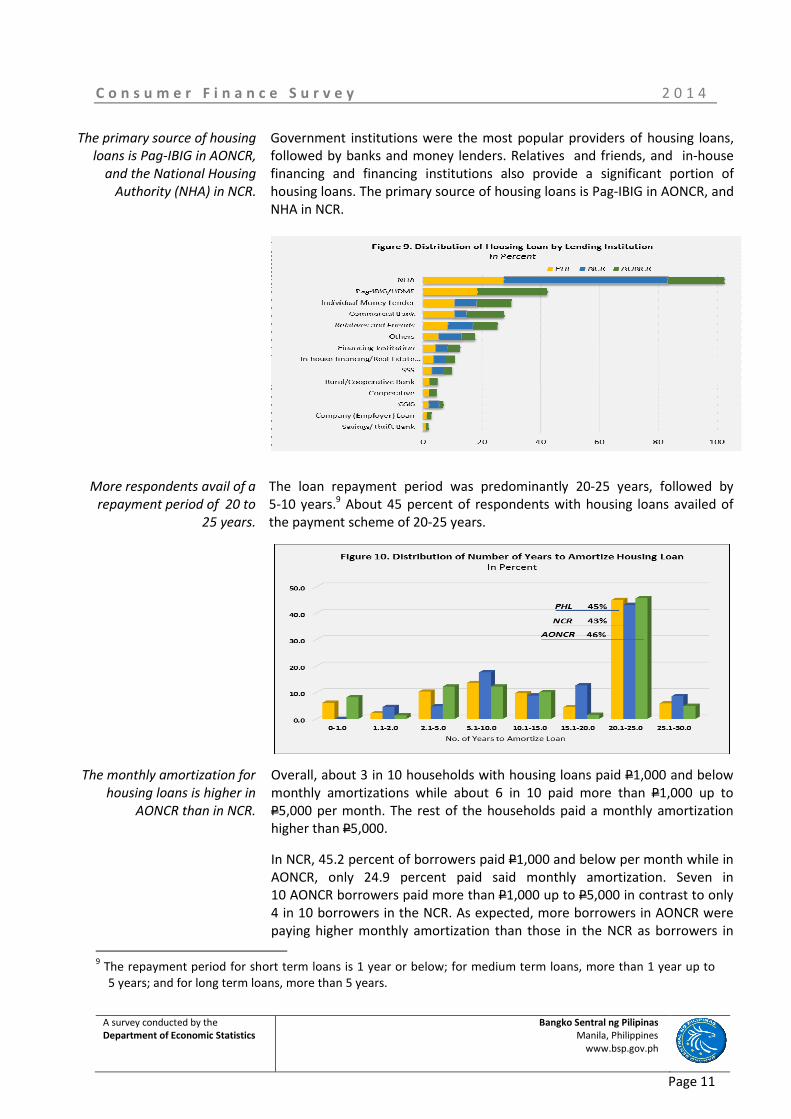

The primary source of housing

loans is Pag-IBIG in AONCR,

and the National Housing

Authority (NHA) in NCR.

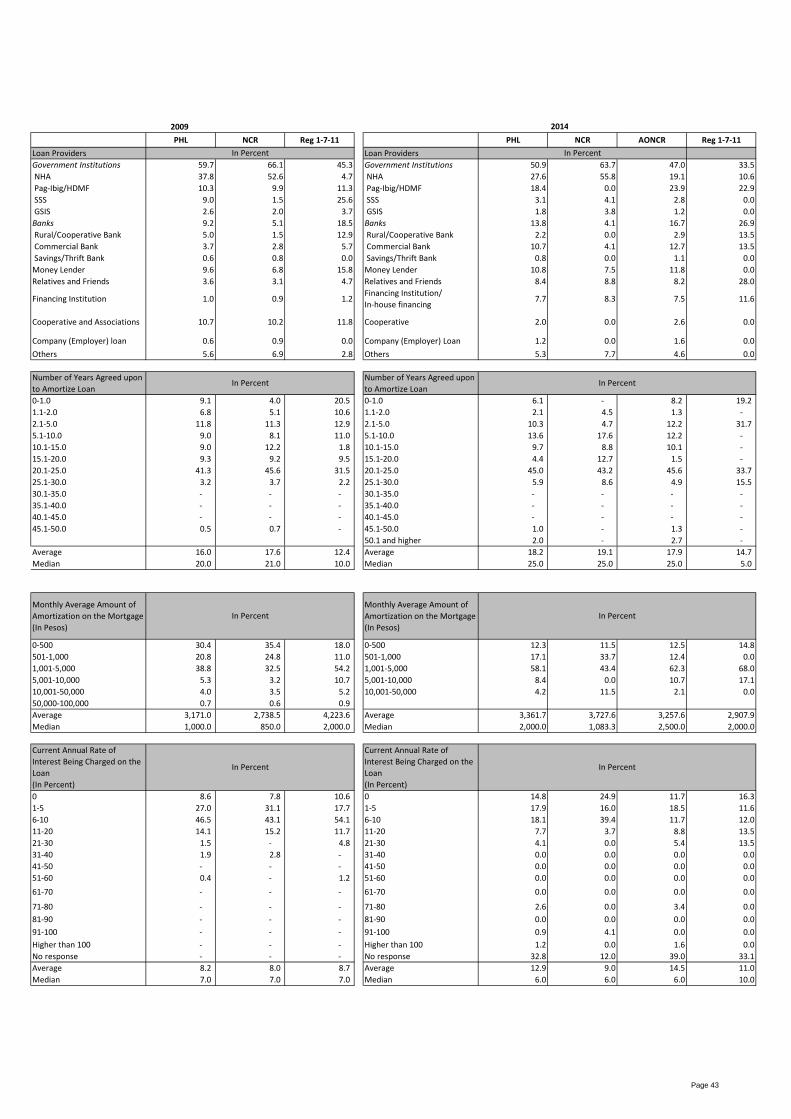

Government institutions were the most popular providers of housing loans,

followed by banks and money lenders. Relatives and friends, and in-house

financing and financing institutions also provide a significant portion of

housing loans. The primary source of housing loans is Pag-IBIG in AONCR, and

NHA in NCR.

More respondents avail of a

repayment period of 20 to

25 years.

The loan repayment period was predominantly 20-25 years, followed by

5-10 years.9 About 45 percent of respondents with housing loans availed of

the payment scheme of 20-25 years.

The monthly amortization for

housing loans is higher in

AONCR than in NCR.

Overall, about 3 in 10 households with housing loans paid P1,000 and below

monthly amortizations while about 6 in 10 paid more than P1,000 up to

P5,000 per month. The rest of the households paid a monthly amortization

higher than P5,000.

In NCR, 45.2 percent of borrowers paid P1,000 and below per month while in

AONCR, only 24.9 percent paid said monthly amortization. Seven in

10 AONCR borrowers paid more than P1,000 up to P5,000 in contrast to only

4 in 10 borrowers in the NCR. As expected, more borrowers in AONCR were

paying higher monthly amortization than those in the NCR as borrowers in

9 The repayment period for short term loans is 1 year or below; for medium term loans, more than 1 year up to

5 years; and for long term loans, more than 5 years.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 12

AONCR generally had bigger loans compared to respondents in NCR.

Moreover, majority of housing loans in NCR were low cost housing projects

of the NHA whereas in AONCR, housing loans were mostly borrowed from

Pag-IBIG, SSS and GSIS with bigger loanable amounts and higher value.

One in two households pay an

annual interest rate of

10 percent or

lower on housing loans.

In terms of lending rates, 50.8 percent of the households (with loans) paid

an annual interest rate of 10 percent and below on their housing loans. The

average rates on housing loans in NCR was lower at 9 percent compared to

14.5 percent in AONCR, while median rates were the same for both areas at

6 percent.

A small percentage of

households have outstanding

loans on their residential

property.

About 3 in 100 households (2.7 percent) had an outstanding loan on their

residential property. In NCR, the percentage was higher at 6.1 percent

compared to 2.2 percent in AONCR.

Nearly 6 in 10 households with

outstanding housing loans pay

ahead or on schedule.

More than half of households with outstanding loans (55.9 percent) paid

their monthly amortization either ahead of or on schedule, while the rest

were behind schedule. A bigger percentage of households in NCR paid their

loans on time or ahead of schedule compared to those in AONCR.

Notably, there was a marked improvement from the 2009 CFS in the

percentage of households that paid their housing loan amortizations ahead

of/on schedule. In NCR, 67.4 percent reported paying their amortizations

ahead of/on schedule in 2014 compared to 44.7 percent in 2009. The same

was observed for Regions 1, 7 and 11 (at 78.5 percent in 2014 from

55 percent in 2009).

Among households whose loan

payments are behind schedule,

about 2 in 5 are behind

schedule by more than

1 year.

Among households whose loan payments were behind schedule, less than

half or about 40.8 percent were in default.10

Of these, 29.9 percent were in

default by one to five years while 11 percent were in default by more than

5 years. Compared to the 2009 CFS results, the percentage of loan payments

in default declined in 2014 in NCR as well as in Regions 1, 7, and 11.

2. Other Real Property Ownership (Apart from Respondent’s Residence)

Other Real Property Ownership by Type and Use

One in eight households owns

other real property apart from

their residence…

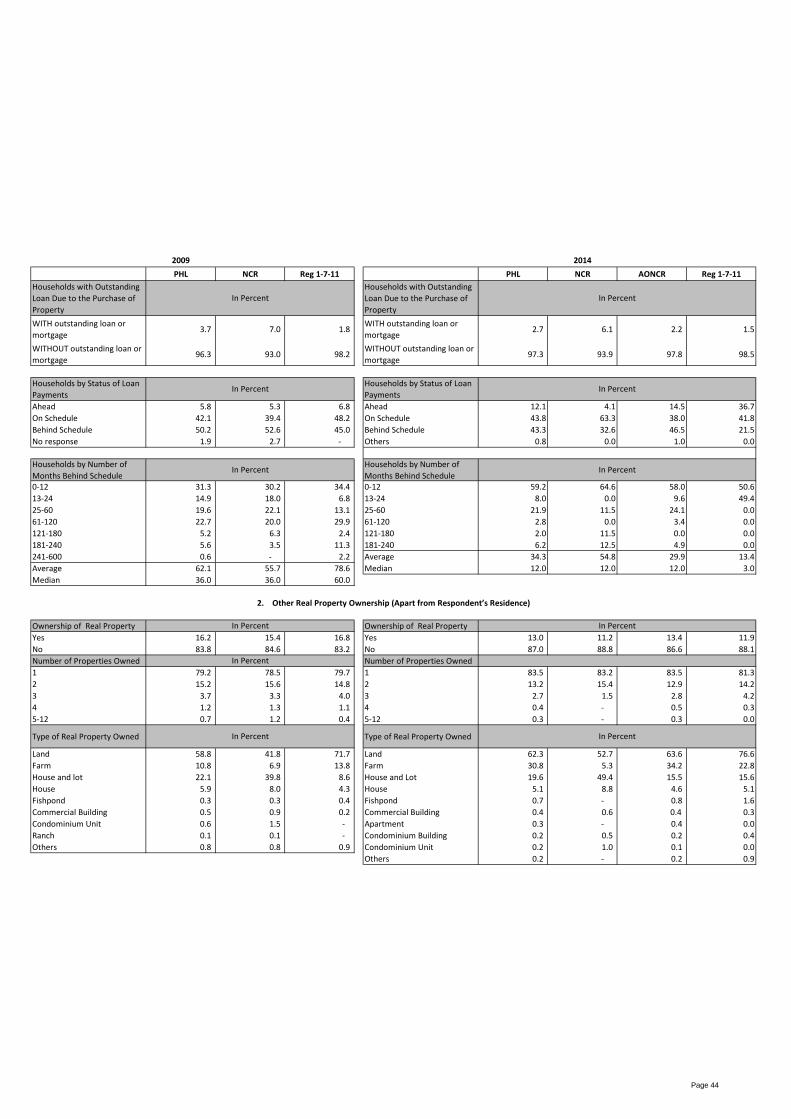

About 13 percent of households owned other real property (aside from their

residence) in 2014. Of these, 83.5 percent owned one other real property,

13.2 percent owned two, and 3.4 percent owned three or more. The

percentage of households in AONCR that owned other real property was

slightly higher compared to that in NCR.

10

Default loans in this survey are those for which amortization payments are behind schedule by more than one

year. However, the BSP defines non-performing loans (NPLs) as those with unpaid quarterly, semi-annual and

annual installments, 30 days or more after due date and loans with unpaid monthly installment for three or

more months. The non-repayment period of NPLs is thus much shorter compared to the survey’s definition of a

default loan.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 13

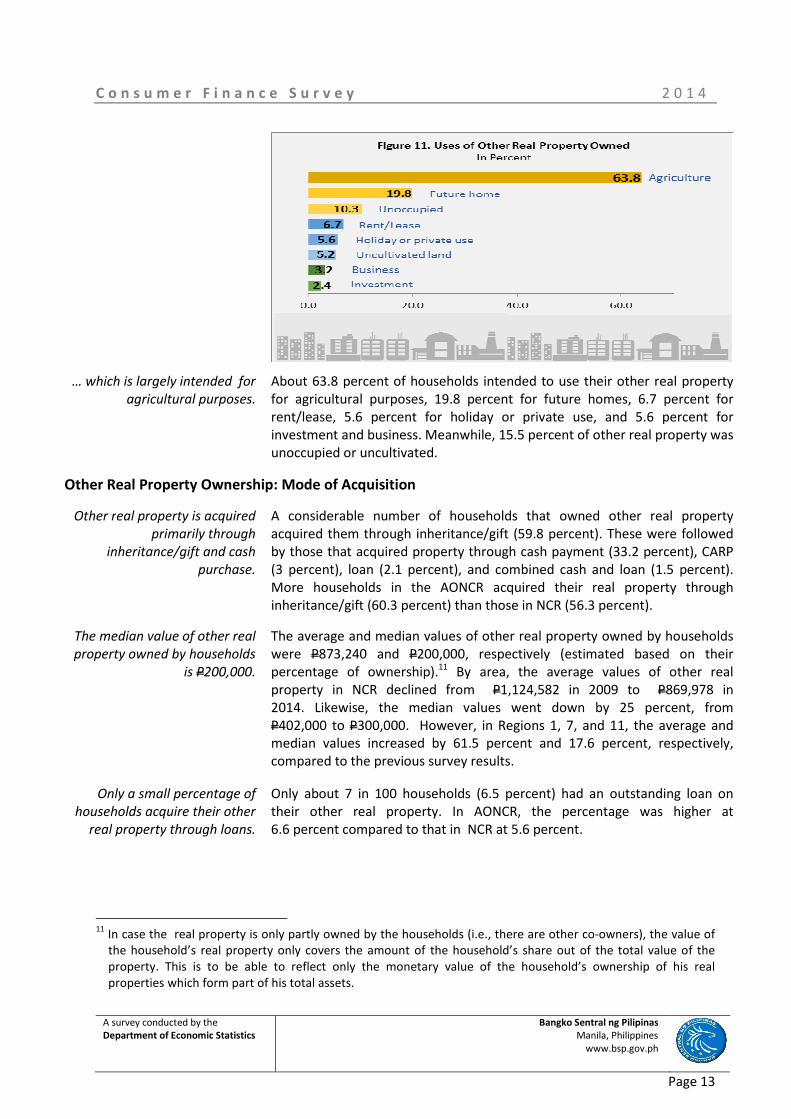

… which is largely intended for

agricultural purposes.

About 63.8 percent of households intended to use their other real property

for agricultural purposes, 19.8 percent for future homes, 6.7 percent for

rent/lease, 5.6 percent for holiday or private use, and 5.6 percent for

investment and business. Meanwhile, 15.5 percent of other real property was

unoccupied or uncultivated.

Other Real Property Ownership: Mode of Acquisition

Other real property is acquired

primarily through

inheritance/gift and cash

purchase.

A considerable number of households that owned other real property

acquired them through inheritance/gift (59.8 percent). These were followed

by those that acquired property through cash payment (33.2 percent), CARP

(3 percent), loan (2.1 percent), and combined cash and loan (1.5 percent).

More households in the AONCR acquired their real property through

inheritance/gift (60.3 percent) than those in NCR (56.3 percent).

The median value of other real

property owned by households

is P200,000.

The average and median values of other real property owned by households

were P873,240 and P200,000, respectively (estimated based on their

percentage of ownership).11

By area, the average values of other real

property in NCR declined from P1,124,582 in 2009 to P869,978 in

2014. Likewise, the median values went down by 25 percent, from

P402,000 to P300,000. However, in Regions 1, 7, and 11, the average and

median values increased by 61.5 percent and 17.6 percent, respectively,

compared to the previous survey results.

Only a small percentage of

households acquire their other

real property through loans.

Only about 7 in 100 households (6.5 percent) had an outstanding loan on

their other real property. In AONCR, the percentage was higher at

6.6 percent compared to that in NCR at 5.6 percent.

11

In case the real property is only partly owned by the households (i.e., there are other co-owners), the value of

the household’s real property only covers the amount of the household’s share out of the total value of the

property. This is to be able to reflect only the monetary value of the household’s ownership of his real

properties which form part of his total assets.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 14

The primary sources of other

real property loans in AONCR

are relatives and friends.

Relatives and friends were the most popular providers of other real property

loans, followed by money lenders and banks.12

They were also the main

providers of other real property loans in AONCR while NHA, Pag-IBIG/HDMF,

financing institutions and GSIS were the most common loan providers in

NCR.

3. Ownership of Vehicles and Other Non-Financial Assets

Vehicles

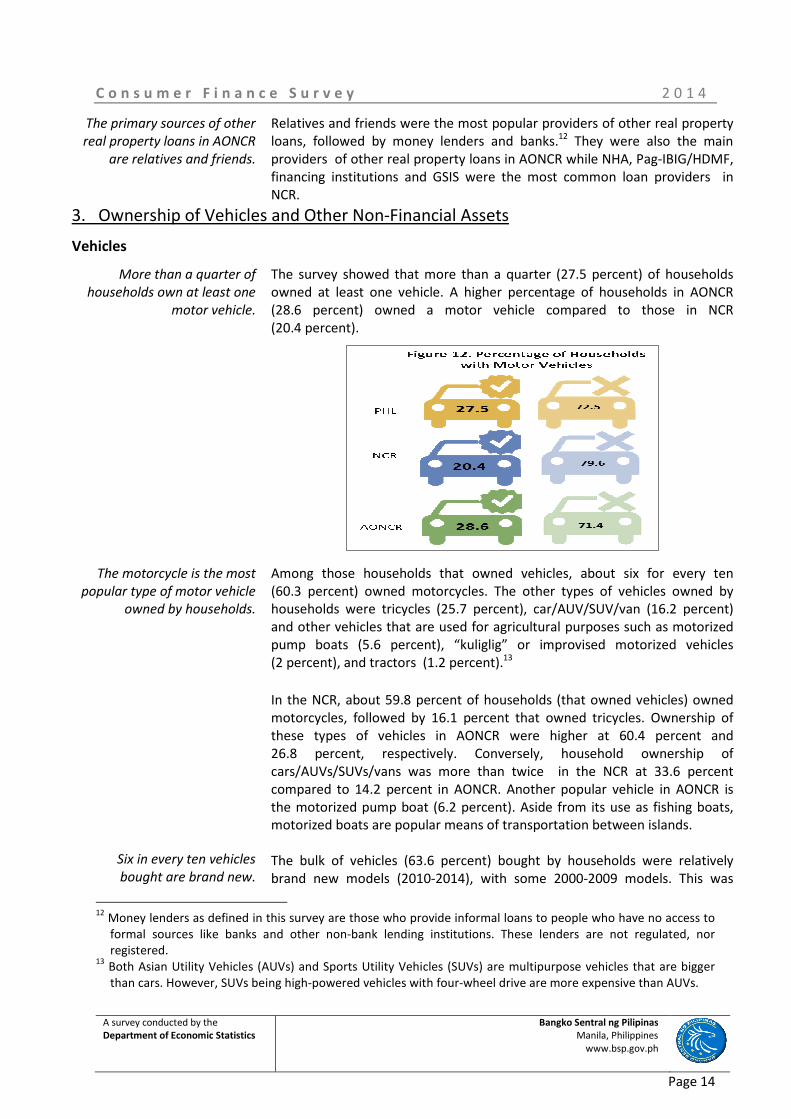

More than a quarter of

households own at least one

motor vehicle.

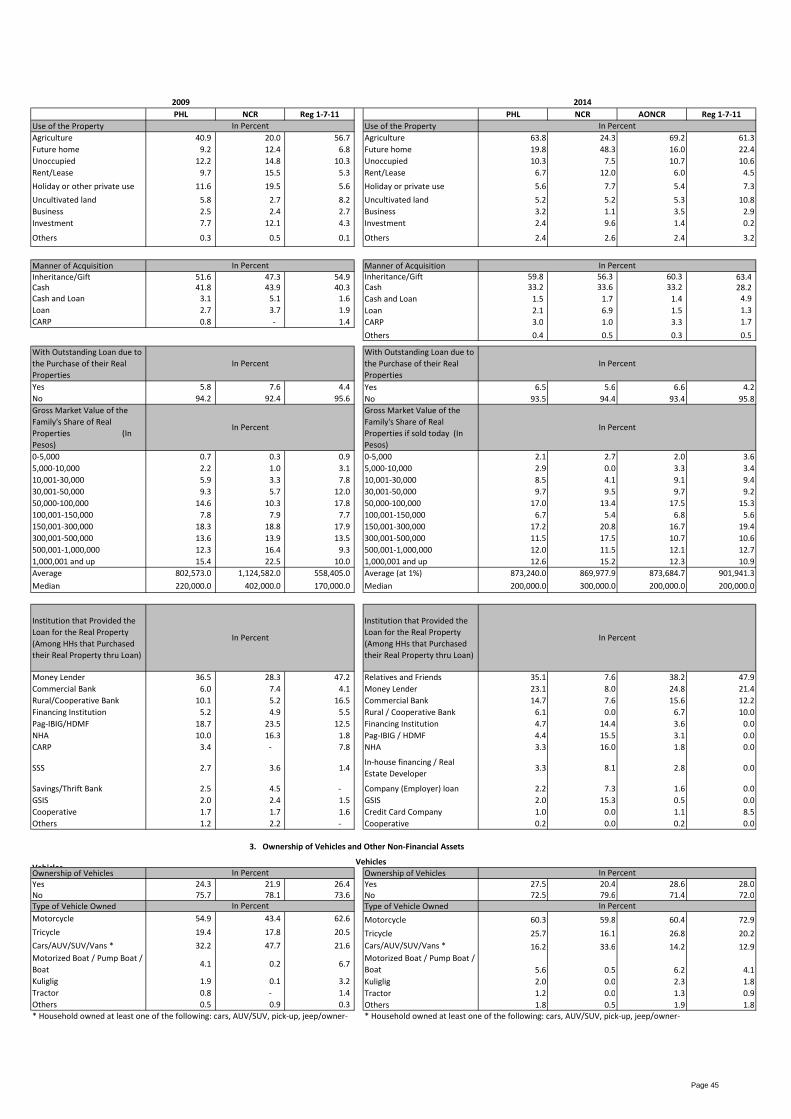

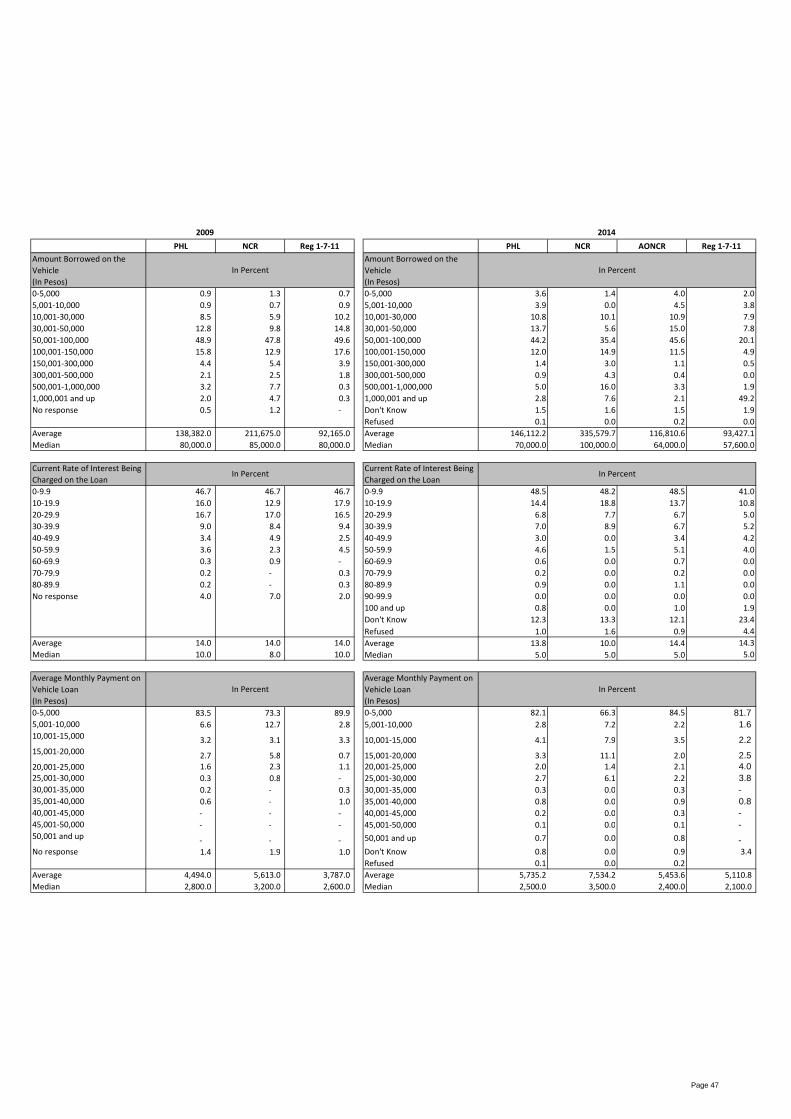

The survey showed that more than a quarter (27.5 percent) of households

owned at least one vehicle. A higher percentage of households in AONCR

(28.6 percent) owned a motor vehicle compared to those in NCR

(20.4 percent).

The motorcycle is the most

popular type of motor vehicle

owned by households.

Six in every ten vehicles

bought are brand new.

Among those households that owned vehicles, about six for every ten

(60.3 percent) owned motorcycles. The other types of vehicles owned by

households were tricycles (25.7 percent), car/AUV/SUV/van (16.2 percent)

and other vehicles that are used for agricultural purposes such as motorized

pump boats (5.6 percent), “kuliglig” or improvised motorized vehicles

(2 percent), and tractors (1.2 percent).13

In the NCR, about 59.8 percent of households (that owned vehicles) owned

motorcycles, followed by 16.1 percent that owned tricycles. Ownership of

these types of vehicles in AONCR were higher at 60.4 percent and

26.8 percent, respectively. Conversely, household ownership of

cars/AUVs/SUVs/vans was more than twice in the NCR at 33.6 percent

compared to 14.2 percent in AONCR. Another popular vehicle in AONCR is

the motorized pump boat (6.2 percent). Aside from its use as fishing boats,

motorized boats are popular means of transportation between islands.

The bulk of vehicles (63.6 percent) bought by households were relatively

brand new models (2010-2014), with some 2000-2009 models. This was

12

Money lenders as defined in this survey are those who provide informal loans to people who have no access to

formal sources like banks and other non-bank lending institutions. These lenders are not regulated, nor

registered. 13

Both Asian Utility Vehicles (AUVs) and Sports Utility Vehicles (SUVs) are multipurpose vehicles that are bigger

than cars. However, SUVs being high-powered vehicles with four-wheel drive are more expensive than AUVs.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 15

observed in both NCR and AONCR. The percentage of households that bought

new models increased to 64.4 percent (from 53.7 percent in the previous CFS

results) in NCR and 62.7 percent (from 58.6 percent in 2009) in

Regions 1, 7, and 11.

Vehicles bought are primarily

for personal use.

Vehicles bought by households were largely for personal use (80.4 percent).

Some households (9.1 percent) bought vehicles for hire/rent to generate

income while 9.6 percent of households purchased vehicles for both personal

and business use. Utilization of vehicles in both NCR and AONCR broadly

followed the national pattern.

The estimated median

monthly income from vehicles

for hire is P4,350.

The average monthly income derived from vehicles for hire was

P5,962.3 with a median income of P4,350. These were lower compared to

the 2009 CFS results. This could be due to the higher number of motorcycles

and lower number of cars/UAVS/SUVs/vans owned and for hire recorded in

the 2014 CFS.

The average value of vehicles owned by households (if sold at the time of the

survey) was P71,188.90, with a median of P30,000. The average and median

values of vehicles were much higher in the NCR given the bigger percentage

of ownership of cars/AUVs/SUVs/vans compared to that in AONCR.

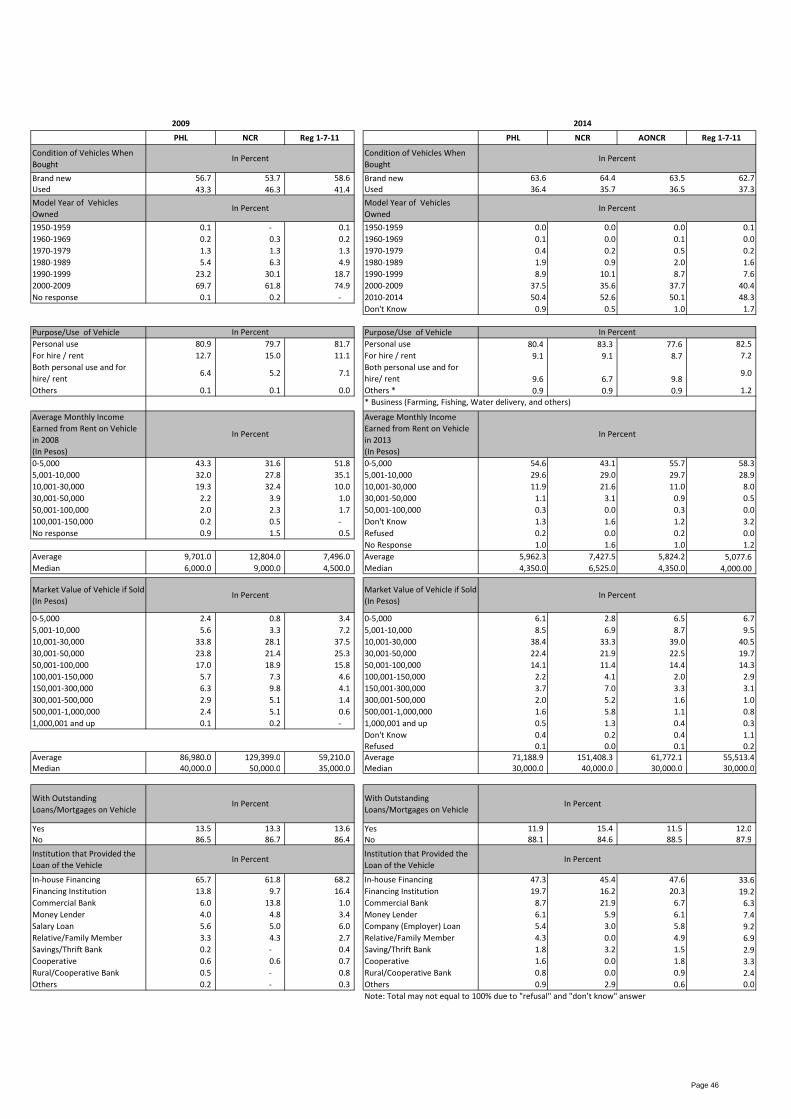

One in eight households that

own a motor vehicle avail

themselves of a motor vehicle

loan.

About 11.9 percent of households that owned motor vehicles had

outstanding loans on their vehicles. A bigger percentage of NCR households

had outstanding loans on vehicles (15.4 percent) compared to those in

AONCR (11.5 percent).

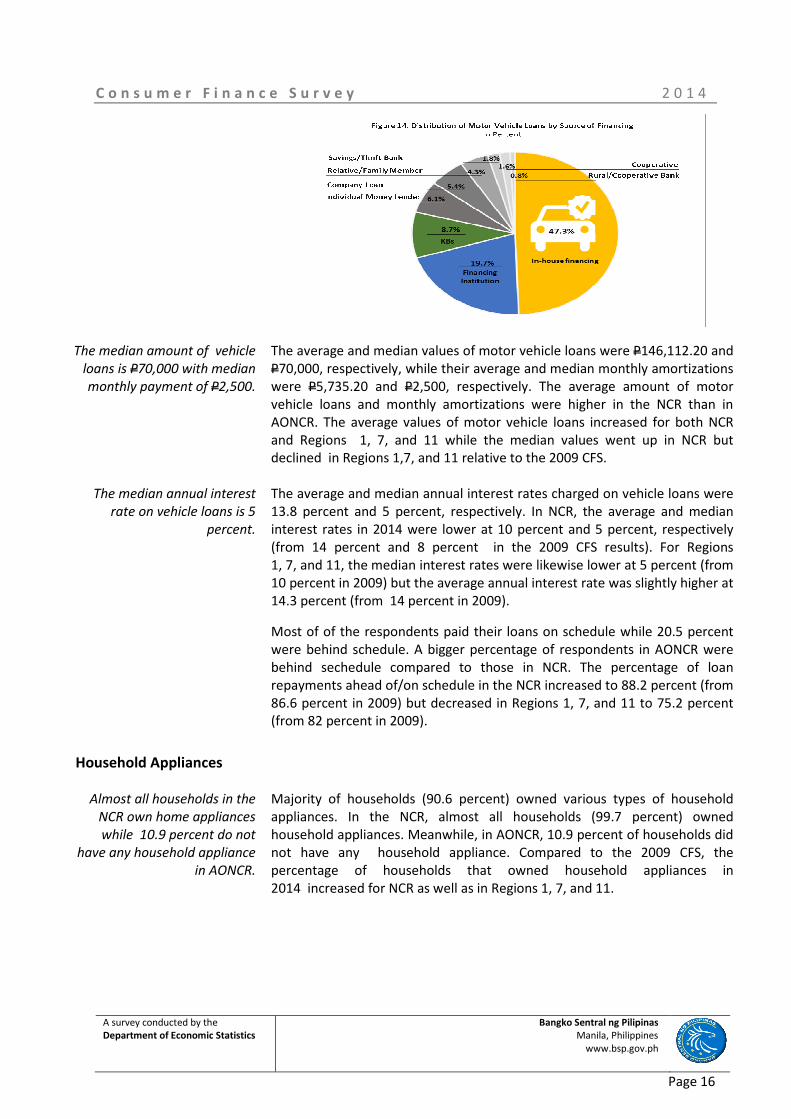

In-house financing and

financing institutions are the

top sources of motor vehicle

loans.

In-house financing and financing institutions (67 percent) were the two most

popular modes/sources of motor vehicle loans. This was observed both for

NCR and AONCR households. Other providers of motor vehicle loans were

commercial banks, individual money lenders, company (employer) loans,

relative/family members, saving/thrift banks, and cooperatives/rural banks.

The percentage of respondents in the NCR who availed of motor vehicle

loans from banks in 2014 increased to 25.1 percent (from 13.8 percent in the

2009 CFS). Likewise, the percentage of car loans availed from banks by the

households in Regions 1, 7, and 11 increased to 11.6 percent (from

2.2 percent in 2009).

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 16

The median amount of vehicle

loans is P70,000 with median

monthly payment of P2,500.

The average and median values of motor vehicle loans were P146,112.20 and

P70,000, respectively, while their average and median monthly amortizations

were P5,735.20 and P2,500, respectively. The average amount of motor

vehicle loans and monthly amortizations were higher in the NCR than in

AONCR. The average values of motor vehicle loans increased for both NCR

and Regions 1, 7, and 11 while the median values went up in NCR but

declined in Regions 1,7, and 11 relative to the 2009 CFS.

The median annual interest

rate on vehicle loans is 5

percent.

The average and median annual interest rates charged on vehicle loans were

13.8 percent and 5 percent, respectively. In NCR, the average and median

interest rates in 2014 were lower at 10 percent and 5 percent, respectively

(from 14 percent and 8 percent in the 2009 CFS results). For Regions

1, 7, and 11, the median interest rates were likewise lower at 5 percent (from

10 percent in 2009) but the average annual interest rate was slightly higher at

14.3 percent (from 14 percent in 2009).

Most of of the respondents paid their loans on schedule while 20.5 percent

were behind schedule. A bigger percentage of respondents in AONCR were

behind sechedule compared to those in NCR. The percentage of loan

repayments ahead of/on schedule in the NCR increased to 88.2 percent (from

86.6 percent in 2009) but decreased in Regions 1, 7, and 11 to 75.2 percent

(from 82 percent in 2009).

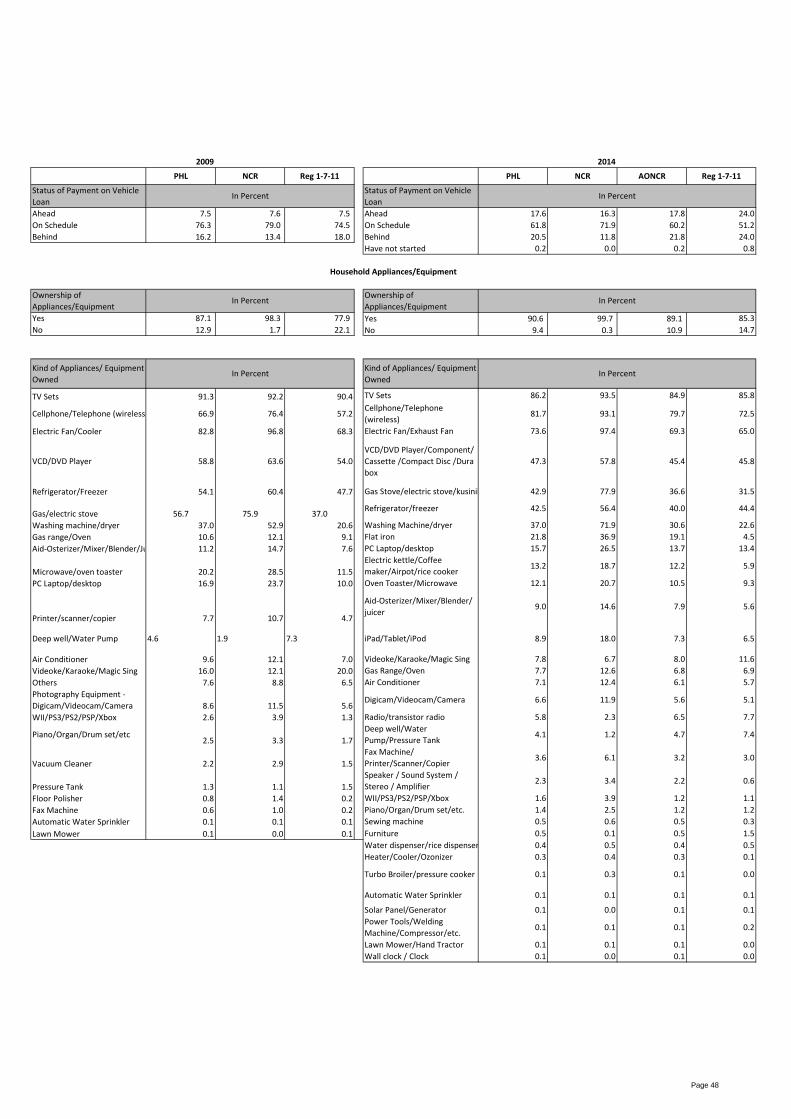

Household Appliances

Almost all households in the

NCR own home appliances

while 10.9 percent do not

have any household appliance

in AONCR.

Majority of households (90.6 percent) owned various types of household

appliances. In the NCR, almost all households (99.7 percent) owned

household appliances. Meanwhile, in AONCR, 10.9 percent of households did

not have any household appliance. Compared to the 2009 CFS, the

percentage of households that owned household appliances in

2014 increased for NCR as well as in Regions 1, 7, and 11.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 17

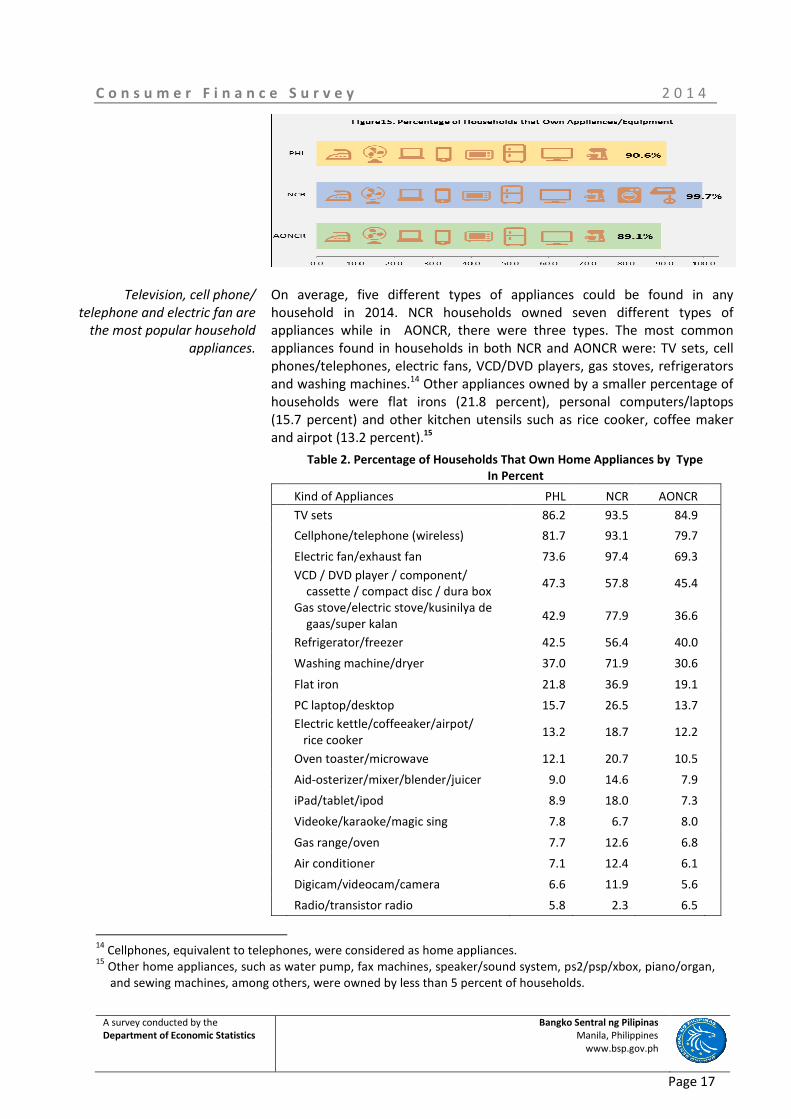

Television, cell phone/

telephone and electric fan are

the most popular household

appliances.

On average, five different types of appliances could be found in any

household in 2014. NCR households owned seven different types of

appliances while in AONCR, there were three types. The most common

appliances found in households in both NCR and AONCR were: TV sets, cell

phones/telephones, electric fans, VCD/DVD players, gas stoves, refrigerators

and washing machines.14

Other appliances owned by a smaller percentage of

households were flat irons (21.8 percent), personal computers/laptops

(15.7 percent) and other kitchen utensils such as rice cooker, coffee maker

and airpot (13.2 percent).15

Table 2. Percentage of Households That Own Home Appliances by Type

In Percent

Kind of Appliances PHL NCR AONCR

TV sets 86.2 93.5 84.9

Cellphone/telephone (wireless) 81.7 93.1 79.7

Electric fan/exhaust fan 73.6 97.4 69.3

VCD / DVD player / component/

cassette / compact disc / dura box 47.3 57.8 45.4

Gas stove/electric stove/kusinilya de

gaas/super kalan 42.9 77.9 36.6

Refrigerator/freezer 42.5 56.4 40.0

Washing machine/dryer 37.0 71.9 30.6

Flat iron 21.8 36.9 19.1

PC laptop/desktop 15.7 26.5 13.7

Electric kettle/coffeeaker/airpot/

rice cooker 13.2 18.7 12.2

Oven toaster/microwave 12.1 20.7 10.5

Aid-osterizer/mixer/blender/juicer 9.0 14.6 7.9

iPad/tablet/ipod 8.9 18.0 7.3

Videoke/karaoke/magic sing 7.8 6.7 8.0

Gas range/oven 7.7 12.6 6.8

Air conditioner 7.1 12.4 6.1

Digicam/videocam/camera 6.6 11.9 5.6

Radio/transistor radio 5.8 2.3 6.5

14

Cellphones, equivalent to telephones, were considered as home appliances. 15

Other home appliances, such as water pump, fax machines, speaker/sound system, ps2/psp/xbox, piano/organ,

and sewing machines, among others, were owned by less than 5 percent of households.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 18

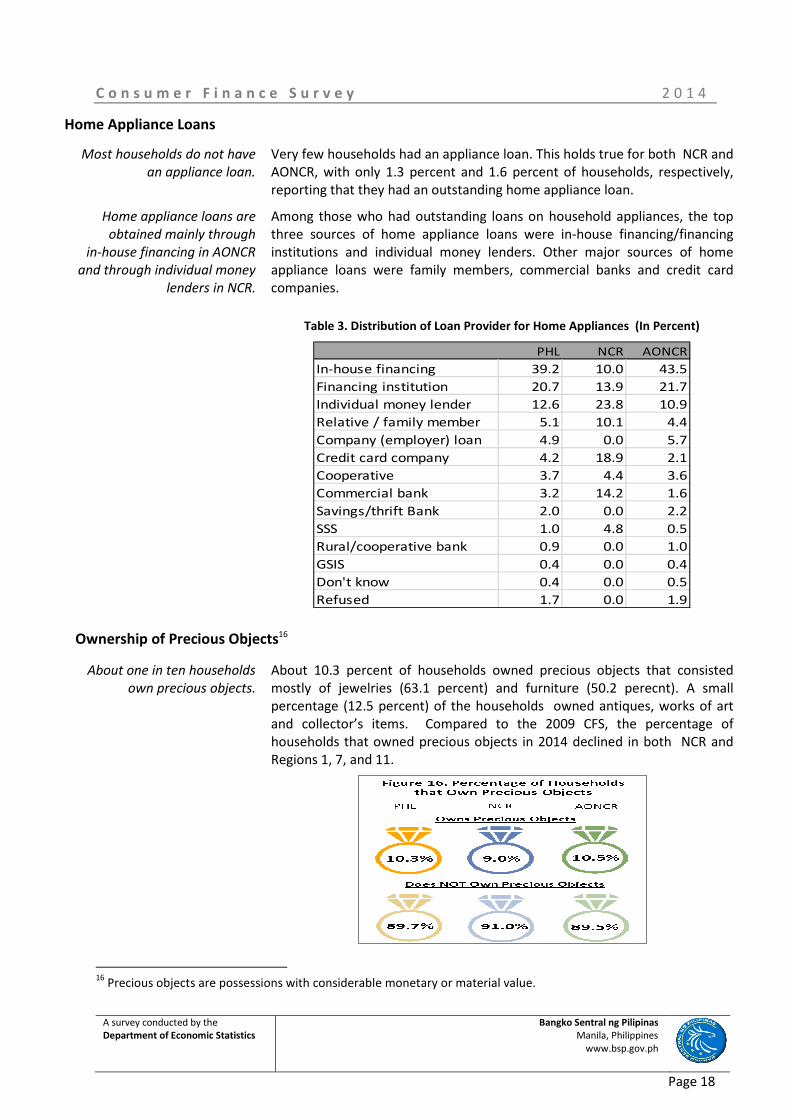

Home Appliance Loans

Most households do not have

an appliance loan.

Very few households had an appliance loan. This holds true for both NCR and

AONCR, with only 1.3 percent and 1.6 percent of households, respectively,

reporting that they had an outstanding home appliance loan.

Home appliance loans are

obtained mainly through

in-house financing in AONCR

and through individual money

lenders in NCR.

Among those who had outstanding loans on household appliances, the top

three sources of home appliance loans were in-house financing/financing

institutions and individual money lenders. Other major sources of home

appliance loans were family members, commercial banks and credit card

companies.

Table 3. Distribution of Loan Provider for Home Appliances (In Percent)

PHL NCR AONCR

In-house financing 39.2 10.0 43.5

Financing institution 20.7 13.9 21.7

Individual money lender 12.6 23.8 10.9

Relative / family member 5.1 10.1 4.4

Company (employer) loan 4.9 0.0 5.7

Credit card company 4.2 18.9 2.1

Cooperative 3.7 4.4 3.6

Commercial bank 3.2 14.2 1.6

Savings/thrift Bank 2.0 0.0 2.2

SSS 1.0 4.8 0.5

Rural/cooperative bank 0.9 0.0 1.0

GSIS 0.4 0.0 0.4

Don't know 0.4 0.0 0.5

Refused 1.7 0.0 1.9

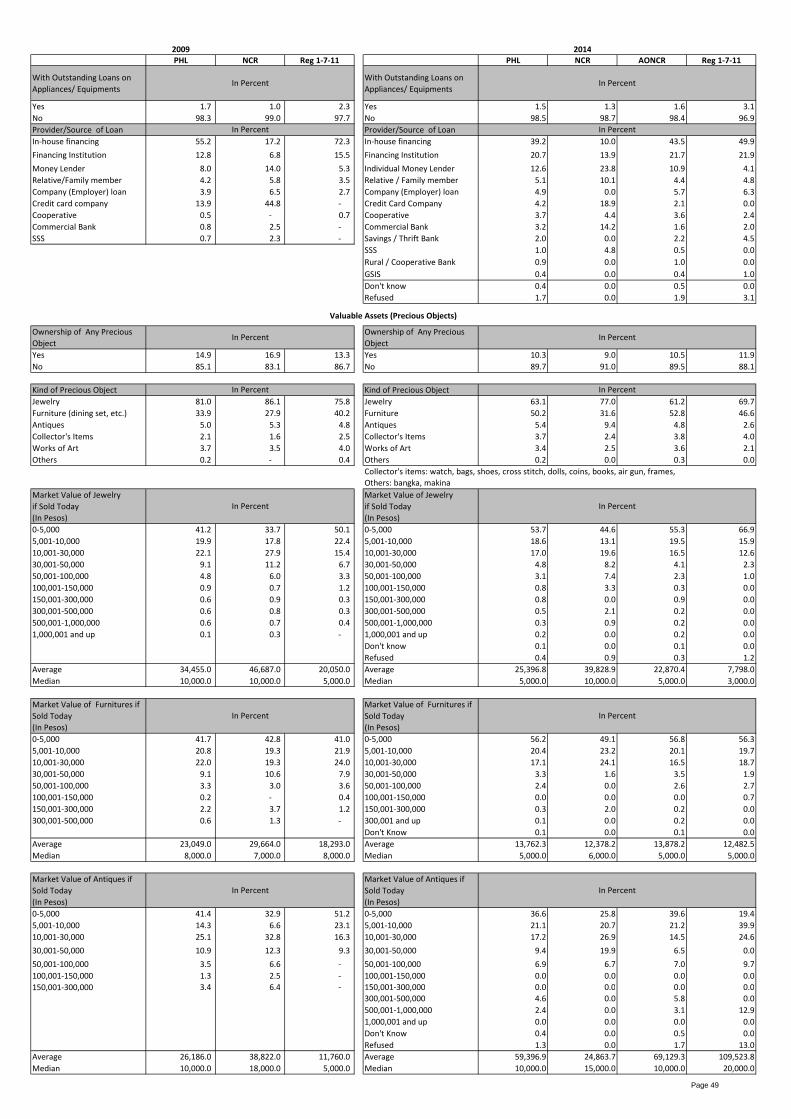

Ownership of Precious Objects16

About one in ten households

own precious objects.

About 10.3 percent of households owned precious objects that consisted

mostly of jewelries (63.1 percent) and furniture (50.2 perecnt). A small

percentage (12.5 percent) of the households owned antiques, works of art

and collector’s items. Compared to the 2009 CFS, the percentage of

households that owned precious objects in 2014 declined in both NCR and

Regions 1, 7, and 11.

16

Precious objects are possessions with considerable monetary or material value.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 19

Antiques are the most

valuable precious objects

owned by households.

The highest estimated average and median values among precious objects

were those of antiques at P59,396.90 and P10,000, respectively. The second

highest average value pertained to jewelries (P25,396.80), followed by works

of art (P23,176.70) and furnitures (P13,762.30).

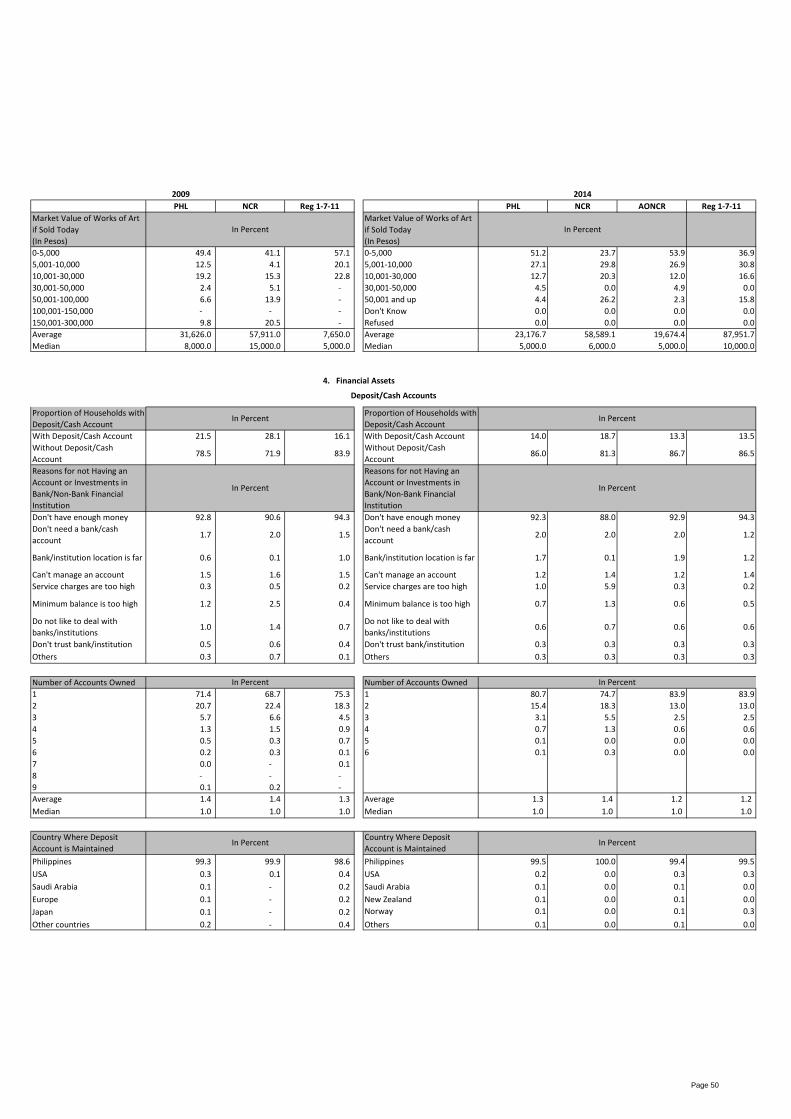

4. Financial Assets

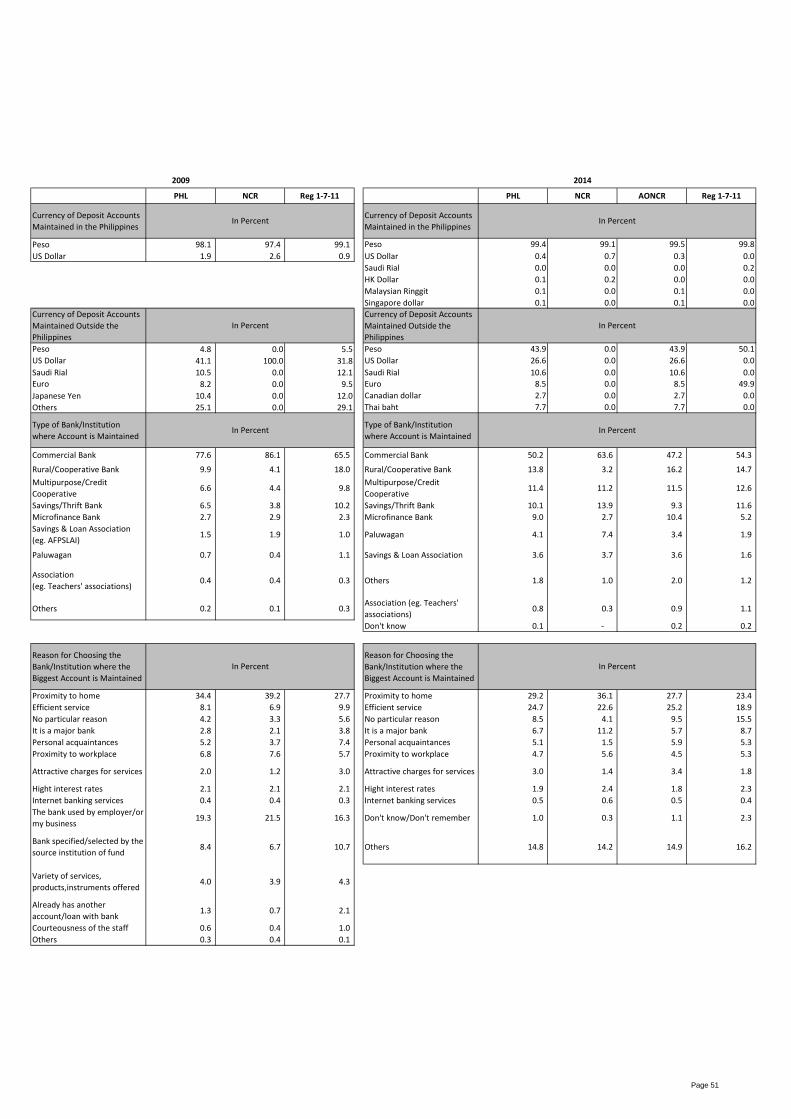

Deposit/Cash Accounts

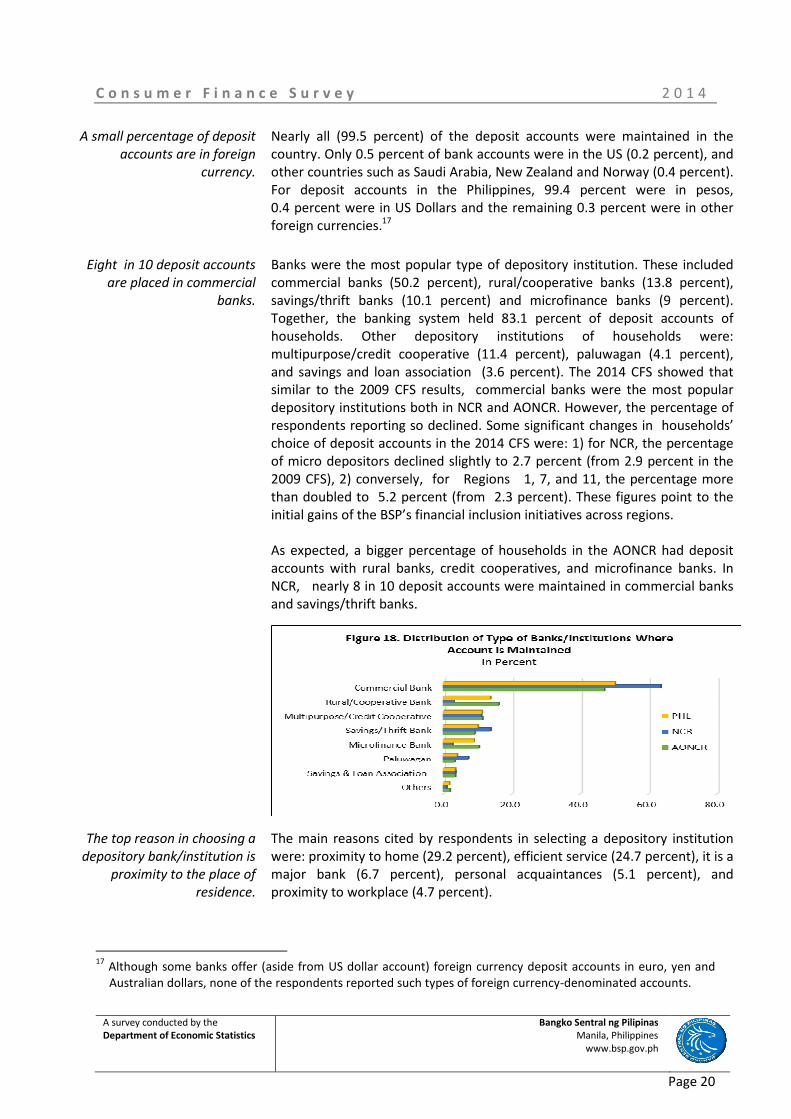

Eighty six percent of

households are unbanked.

Majority of households or 86 percent did not have a deposit account. This

means that only the remaining 14 percent save their money in banks,

consistent with the results of the National Baseline Survey on Financial

Inclusion (NBSFI) conducted by the Inclusive Finance Advocacy Staff (IFAS) in

2014. The said survey showed that out of the 43.2 percent adults who

currently have savings either through banks or cooperatives, 32.7 percent put

their money in banks. The results therefore indicated that only 14.1 percent

of adults save in banks.

The foremost reason cited by households for not having a deposit account

was not having enough money to keep an account (92.3 percent). Other

reasons cited by households were: (1) do not need a bank/cash account

(2 percent), (2) bank/institution location is far (1.7 percent), (3) cannot

manage an account (1.2 percent), (4) service charges are too high

(1.0 percent), and other reasons (1.6 percent) such as minimum balance is

too high, do not like to deal with banks/institutions and do not trust

banks/institutions.

By area, both the 2009 and 2014 CFS results showed that a bigger number of

households in the NCR have deposit accounts compared to those in AONCR.

Compared however to the 2009 CFS, the percentage of households with

deposit accounts declined both in the NCR (to 18.7 percent from

28.1 percent) and Regions 1, 7, and 11 (to 13.5 percent from 16.1 percent),

respectively. Meanwhile, the average number of deposit accounts owned by

households remained steady at 1.4 accounts in the NCR and 1.2 accounts in

the comparative regions in AONCR.

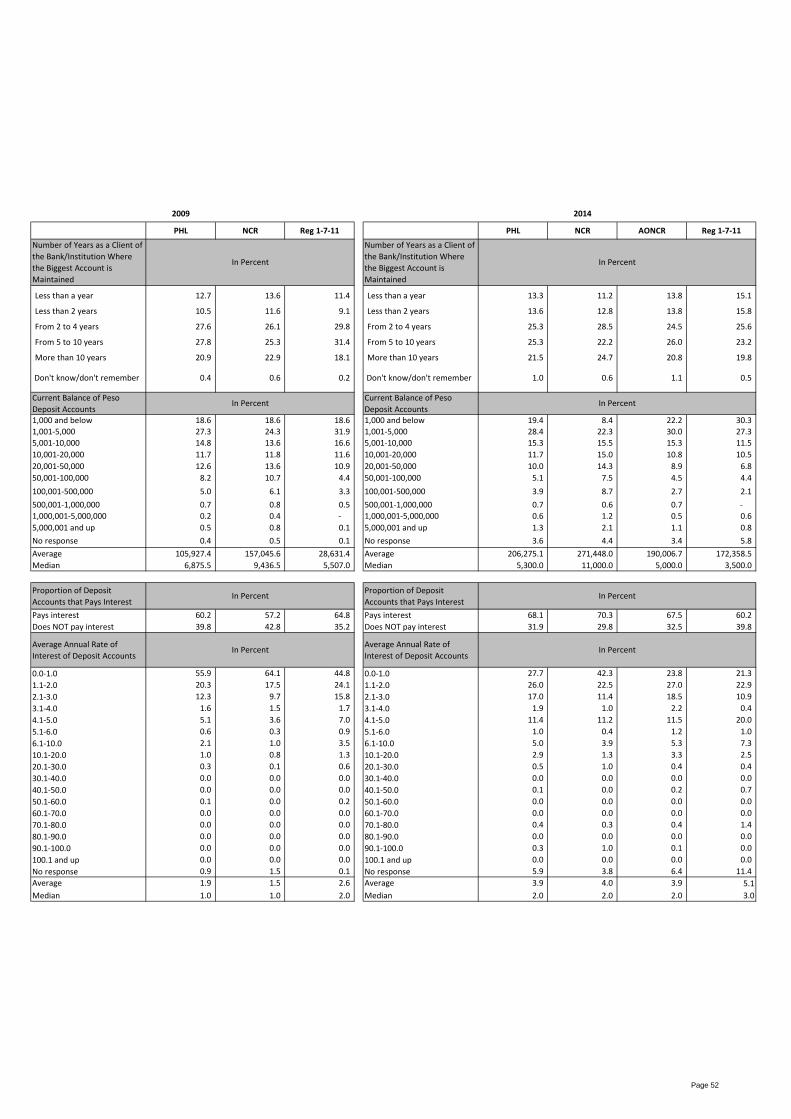

Most households have only

one deposit account.

Among households with deposit accounts, 80.7 percent had only one deposit

account, 15.4 percent had two, and 4.0 percent had three or more.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 20

A small percentage of deposit

accounts are in foreign

currency.

Nearly all (99.5 percent) of the deposit accounts were maintained in the

country. Only 0.5 percent of bank accounts were in the US (0.2 percent), and

other countries such as Saudi Arabia, New Zealand and Norway (0.4 percent).

For deposit accounts in the Philippines, 99.4 percent were in pesos,

0.4 percent were in US Dollars and the remaining 0.3 percent were in other

foreign currencies.17

Eight in 10 deposit accounts

are placed in commercial

banks.

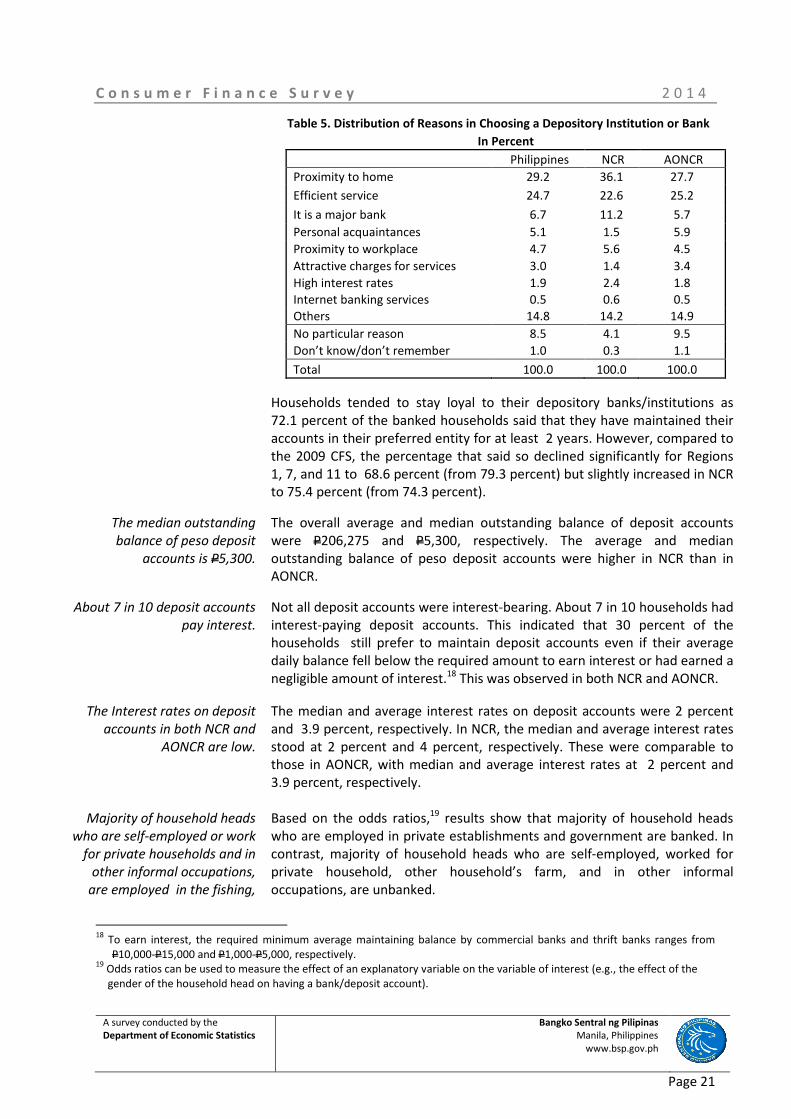

Banks were the most popular type of depository institution. These included

commercial banks (50.2 percent), rural/cooperative banks (13.8 percent),

savings/thrift banks (10.1 percent) and microfinance banks (9 percent).

Together, the banking system held 83.1 percent of deposit accounts of

households. Other depository institutions of households were:

multipurpose/credit cooperative (11.4 percent), paluwagan (4.1 percent),

and savings and loan association (3.6 percent). The 2014 CFS showed that

similar to the 2009 CFS results, commercial banks were the most popular

depository institutions both in NCR and AONCR. However, the percentage of

respondents reporting so declined. Some significant changes in households’

choice of deposit accounts in the 2014 CFS were: 1) for NCR, the percentage

of micro depositors declined slightly to 2.7 percent (from 2.9 percent in the

2009 CFS), 2) conversely, for Regions 1, 7, and 11, the percentage more

than doubled to 5.2 percent (from 2.3 percent). These figures point to the

initial gains of the BSP’s financial inclusion initiatives across regions.

As expected, a bigger percentage of households in the AONCR had deposit

accounts with rural banks, credit cooperatives, and microfinance banks. In

NCR, nearly 8 in 10 deposit accounts were maintained in commercial banks

and savings/thrift banks.

The top reason in choosing a

depository bank/institution is

proximity to the place of

residence.

The main reasons cited by respondents in selecting a depository institution

were: proximity to home (29.2 percent), efficient service (24.7 percent), it is a

major bank (6.7 percent), personal acquaintances (5.1 percent), and

proximity to workplace (4.7 percent).

17

Although some banks offer (aside from US dollar account) foreign currency deposit accounts in euro, yen and

Australian dollars, none of the respondents reported such types of foreign currency-denominated accounts.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 21

Table 5. Distribution of Reasons in Choosing a Depository Institution or Bank

In Percent

Philippines NCR AONCR

Proximity to home 29.2 36.1 27.7

Efficient service 24.7 22.6 25.2

It is a major bank 6.7 11.2 5.7

Personal acquaintances 5.1 1.5 5.9

Proximity to workplace 4.7 5.6 4.5

Attractive charges for services 3.0 1.4 3.4

High interest rates 1.9 2.4 1.8

Internet banking services 0.5 0.6 0.5

Others 14.8 14.2 14.9

No particular reason 8.5 4.1 9.5

Don’t know/don’t remember 1.0 0.3 1.1

Total 100.0 100.0 100.0

Households tended to stay loyal to their depository banks/institutions as

72.1 percent of the banked households said that they have maintained their

accounts in their preferred entity for at least 2 years. However, compared to

the 2009 CFS, the percentage that said so declined significantly for Regions

1, 7, and 11 to 68.6 percent (from 79.3 percent) but slightly increased in NCR

to 75.4 percent (from 74.3 percent).

The median outstanding

balance of peso deposit

accounts is P5,300.

The overall average and median outstanding balance of deposit accounts

were P206,275 and P5,300, respectively. The average and median

outstanding balance of peso deposit accounts were higher in NCR than in

AONCR.

About 7 in 10 deposit accounts

pay interest.

Not all deposit accounts were interest-bearing. About 7 in 10 households had

interest-paying deposit accounts. This indicated that 30 percent of the

households still prefer to maintain deposit accounts even if their average

daily balance fell below the required amount to earn interest or had earned a

negligible amount of interest.18

This was observed in both NCR and AONCR.

The Interest rates on deposit

accounts in both NCR and

AONCR are low.

Majority of household heads

who are self-employed or work

for private households and in

other informal occupations,

are employed in the fishing,

The median and average interest rates on deposit accounts were 2 percent

and 3.9 percent, respectively. In NCR, the median and average interest rates

stood at 2 percent and 4 percent, respectively. These were comparable to

those in AONCR, with median and average interest rates at 2 percent and

3.9 percent, respectively.

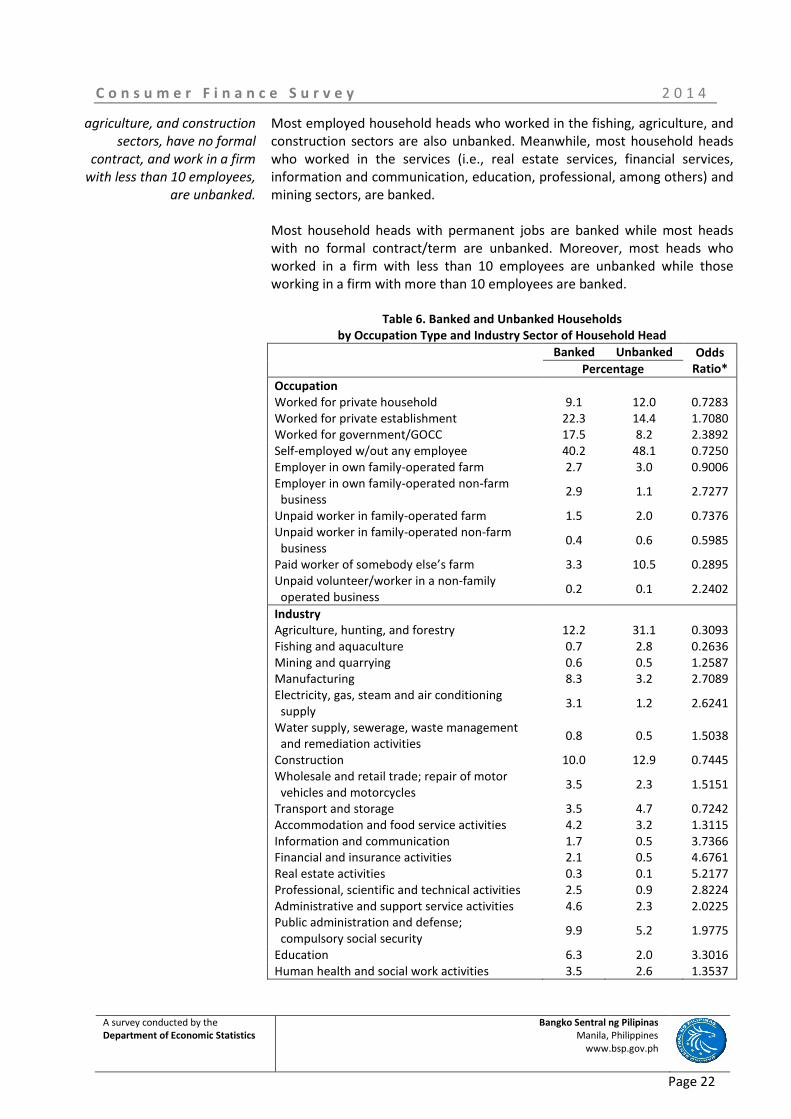

Based on the odds ratios,19

results show that majority of household heads

who are employed in private establishments and government are banked. In

contrast, majority of household heads who are self-employed, worked for

private household, other household’s farm, and in other informal

occupations, are unbanked.

18

To earn interest, the required minimum average maintaining balance by commercial banks and thrift banks ranges from

P10,000-P15,000 and P1,000-P5,000, respectively. 19

Odds ratios can be used to measure the effect of an explanatory variable on the variable of interest (e.g., the effect of the

gender of the household head on having a bank/deposit account).

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 22

agriculture, and construction

sectors, have no formal

contract, and work in a firm

with less than 10 employees,

are unbanked.

Most employed household heads who worked in the fishing, agriculture, and

construction sectors are also unbanked. Meanwhile, most household heads

who worked in the services (i.e., real estate services, financial services,

information and communication, education, professional, among others) and

mining sectors, are banked.

Most household heads with permanent jobs are banked while most heads

with no formal contract/term are unbanked. Moreover, most heads who

worked in a firm with less than 10 employees are unbanked while those

working in a firm with more than 10 employees are banked.

Table 6. Banked and Unbanked Households

by Occupation Type and Industry Sector of Household Head

Banked Unbanked Odds

Ratio* Percentage

Occupation

Worked for private household 9.1 12.0 0.7283

Worked for private establishment 22.3 14.4 1.7080

Worked for government/GOCC 17.5 8.2 2.3892

Self-employed w/out any employee 40.2 48.1 0.7250

Employer in own family-operated farm 2.7 3.0 0.9006

Employer in own family-operated non-farm

business 2.9 1.1 2.7277

Unpaid worker in family-operated farm 1.5 2.0 0.7376

Unpaid worker in family-operated non-farm

business 0.4 0.6 0.5985

Paid worker of somebody else’s farm 3.3 10.5 0.2895

Unpaid volunteer/worker in a non-family

operated business 0.2 0.1 2.2402

Industry

Agriculture, hunting, and forestry 12.2 31.1 0.3093

Fishing and aquaculture 0.7 2.8 0.2636

Mining and quarrying 0.6 0.5 1.2587

Manufacturing 8.3 3.2 2.7089

Electricity, gas, steam and air conditioning

supply 3.1 1.2 2.6241

Water supply, sewerage, waste management

and remediation activities 0.8 0.5 1.5038

Construction 10.0 12.9 0.7445

Wholesale and retail trade; repair of motor

vehicles and motorcycles 3.5 2.3 1.5151

Transport and storage 3.5 4.7 0.7242

Accommodation and food service activities 4.2 3.2 1.3115

Information and communication 1.7 0.5 3.7366

Financial and insurance activities 2.1 0.5 4.6761

Real estate activities 0.3 0.1 5.2177

Professional, scientific and technical activities 2.5 0.9 2.8224

Administrative and support service activities 4.6 2.3 2.0225

Public administration and defense;

compulsory social security 9.9 5.2 1.9775

Education 6.3 2.0 3.3016

Human health and social work activities 3.5 2.6 1.3537

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 23

Arts, entertainment and recreation 0.0 0.5 -

Other service activities 15.9 16.7 0.9448

Activities of households as employers;

Undifferentiated goods and services-

producing Activities of households for own use

0.9 1.6 0.5423

Activities of extraterritorial organizations and

bodies 0.3 0.0 -

Industry not elsewhere classified 5.2 4.7 1.1123

Type of Contract

Permanent 53.1 27.2 3.0312

Temporary/fixed-term contract (OFW,

consultant) 9.3 9.1 1.0304

No formal contract/term 31.3 53.8 0.3913

Other employment agreement 1.9 2.6 0.7389

Not applicable/Self-employed 3.9 6.2 0.6120

Don’t know 0.6 1.3 -

Firm size

Less than 10 employees 28.7 49.8 0.4061

10 to 19 19.8 16.1 1.2861

20 to 99 26.5 18.3 1.6114

100 to 499 14.1 6.5 2.3766

500 or more 7.6 2.9 2.7935

None 3.2 6.4 0.4857 *Note: Given a 2x2 table, the odds ratio is computed as follows:

Banked Unbanked

Presence of Characteristic a b

Absence of Characteristic c d

The odds ratio is computed as: OR = ad/cb

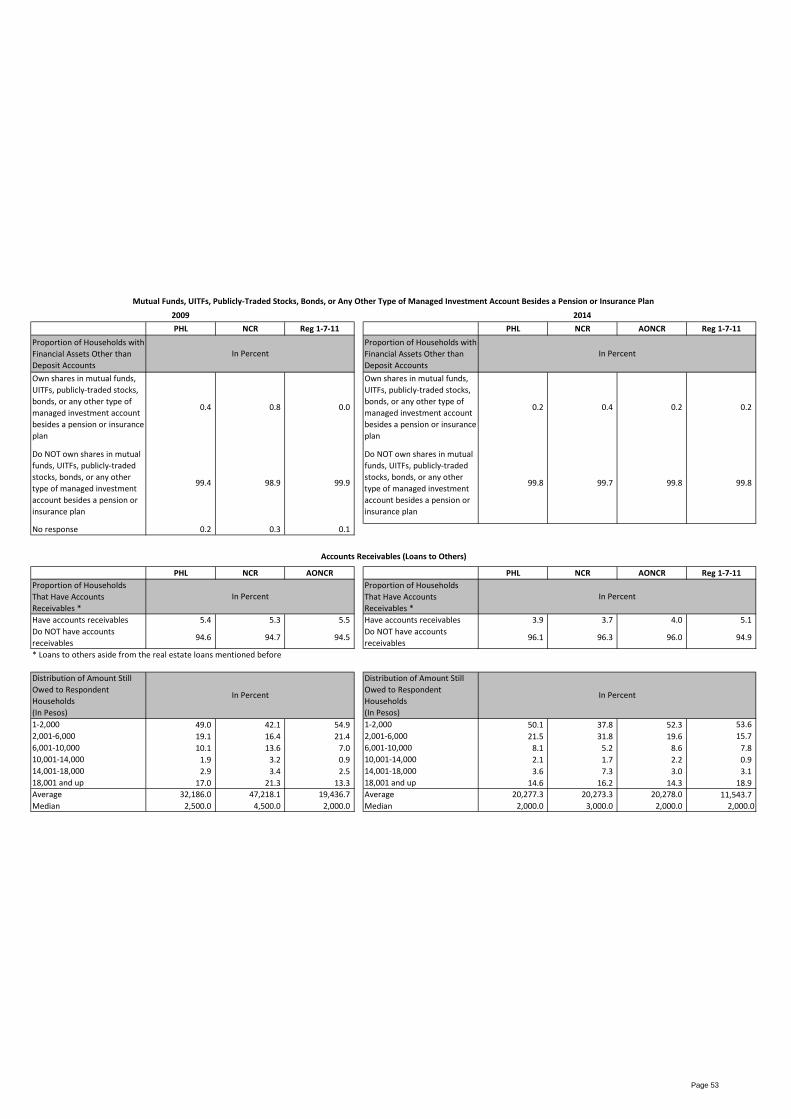

Financial Assets Other Than Deposit Accounts

A very small percentage of

households have investments

in mutual funds and stocks.

A very small percentage of households had investments in stocks, mutual

funds, and/or fixed-income securities, including government securities. In

NCR, less than one percent of households had invested in any of these

financial instruments while in AONCR, the percentage was negligible.

Nearly 1 in 25 households have

accounts receivables from

other households/ businesses.

Aside from deposit accounts, loans made to other households/businesses

were considered to be part of the financial asset of the lender. About

3.9 percent of households had outstanding loan collections. The average and

median values of the outstanding accounts receivables were P20,277 and

P2,000, respectively. The percentage of households that had accounts

receivables declined in both NCR and Regions 1, 7, and 11 compared to the

2009 CFS. The average amount of accounts receivables decreased for both

areas relative to the 2009 CFS results.

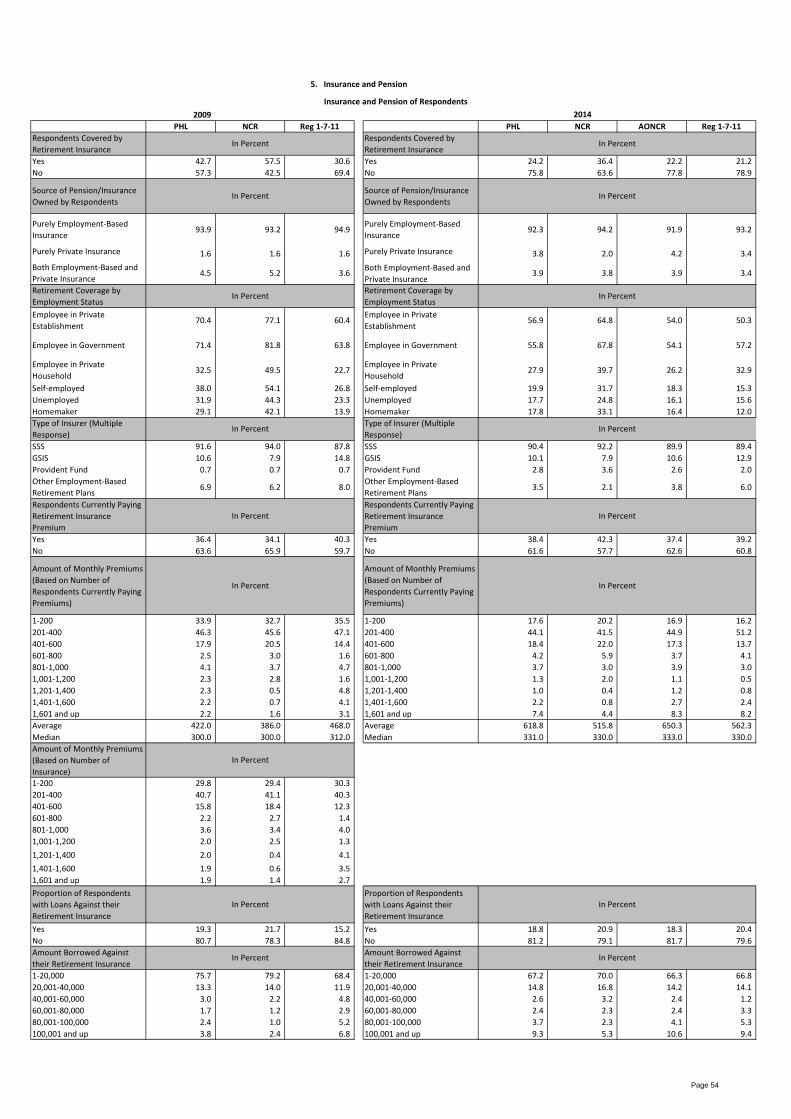

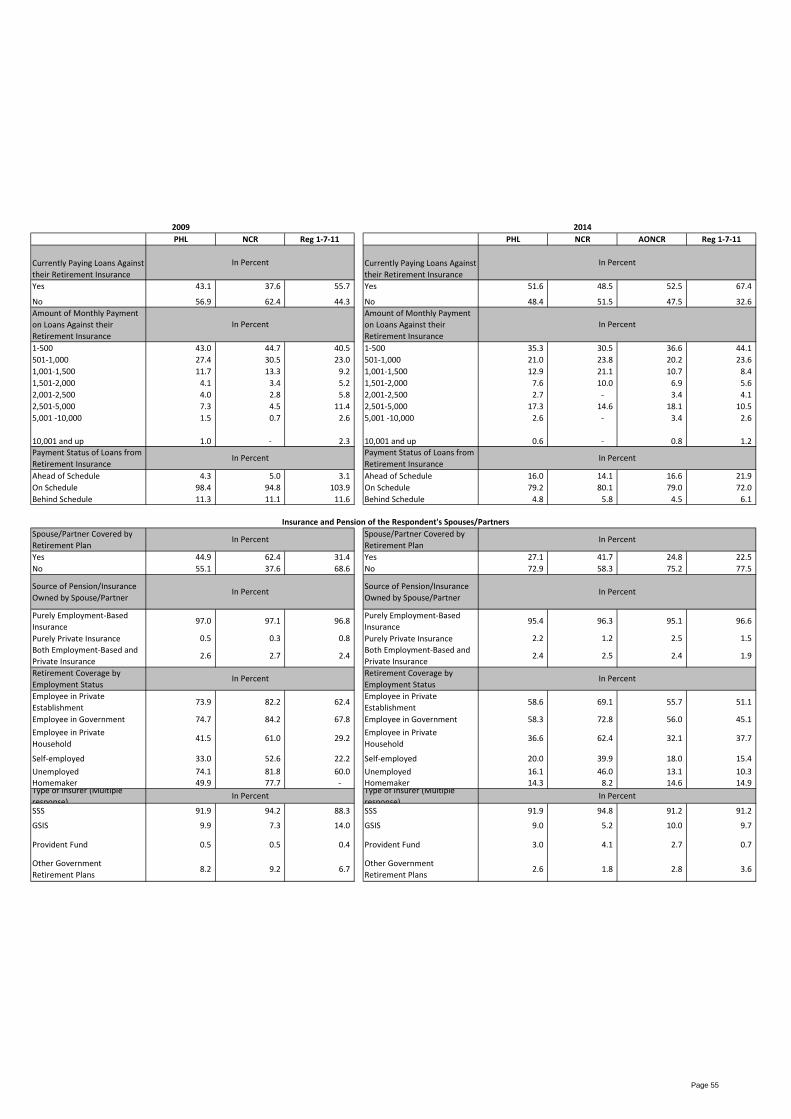

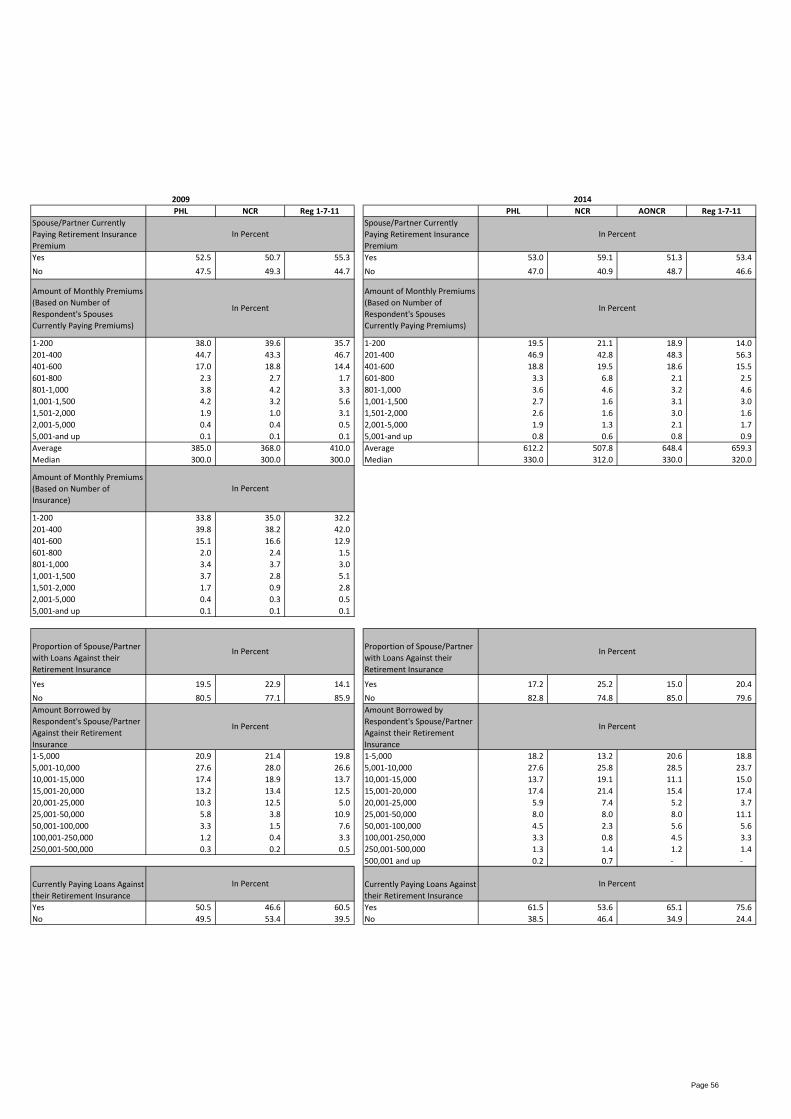

5. Insurance and Pension

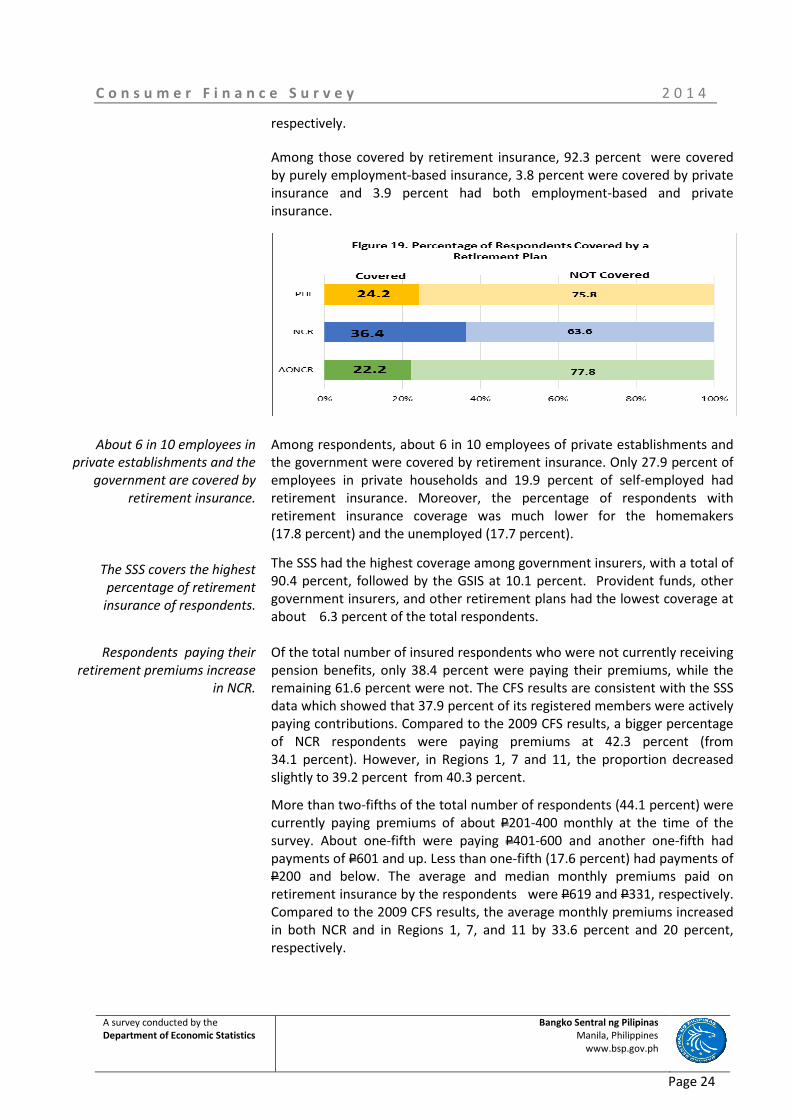

The percentage of respondents

who have one or more

retirement plan/s

declines.

The survey results showed that the percentage of respondents that had at

least one retirement or insurance plan from both/either the government

and/or private companies stood at 24.2 percent in 2014. The percentage of

respondents who were covered with either employment-based or private

insurance plans decreased in both NCR and Regions 1, 7, and 11 to

36.4 percent (from 57.5 percent) and 21.2 percent (from 30.6 percent),

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 24

respectively.

Among those covered by retirement insurance, 92.3 percent were covered

by purely employment-based insurance, 3.8 percent were covered by private

insurance and 3.9 percent had both employment-based and private

insurance.

About 6 in 10 employees in

private establishments and the

government are covered by

retirement insurance.

The SSS covers the highest

percentage of retirement

insurance of respondents.

Among respondents, about 6 in 10 employees of private establishments and

the government were covered by retirement insurance. Only 27.9 percent of

employees in private households and 19.9 percent of self-employed had

retirement insurance. Moreover, the percentage of respondents with

retirement insurance coverage was much lower for the homemakers

(17.8 percent) and the unemployed (17.7 percent).

The SSS had the highest coverage among government insurers, with a total of

90.4 percent, followed by the GSIS at 10.1 percent. Provident funds, other

government insurers, and other retirement plans had the lowest coverage at

about 6.3 percent of the total respondents.

Respondents paying their

retirement premiums increase

in NCR.

Of the total number of insured respondents who were not currently receiving

pension benefits, only 38.4 percent were paying their premiums, while the

remaining 61.6 percent were not. The CFS results are consistent with the SSS

data which showed that 37.9 percent of its registered members were actively

paying contributions. Compared to the 2009 CFS results, a bigger percentage

of NCR respondents were paying premiums at 42.3 percent (from

34.1 percent). However, in Regions 1, 7 and 11, the proportion decreased

slightly to 39.2 percent from 40.3 percent.

More than two-fifths of the total number of respondents (44.1 percent) were

currently paying premiums of about P201-400 monthly at the time of the

survey. About one-fifth were paying P401-600 and another one-fifth had

payments of P601 and up. Less than one-fifth (17.6 percent) had payments of

P200 and below. The average and median monthly premiums paid on

retirement insurance by the respondents were P619 and P331, respectively.

Compared to the 2009 CFS results, the average monthly premiums increased

in both NCR and in Regions 1, 7, and 11 by 33.6 percent and 20 percent,

respectively.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 25

The percentage of

respondents’ spouses who

have one

or more retirement

plans declines to

27.1 percent.

The percentage of respondents’ spouses who had at least one retirement or

insurance plan from both/either the government and/or private companies

declined to 27.1 percent in 2014 from 44.9 percent in 2009. The same trend

was evident in both the NCR and AONCR as the percentage of respondents’

spouses who were covered with either employment-based or private

insurance plans dropped to 41.7 percent from 62.4 percent in NCR and to

22.5 percent from 31.4 percent in Regions 1, 7 and 11.

Among respondents’ spouses employed in private establishments and the

government, about 6 in 10 are covered by retirement insurance. About

36.6 percent of respondents’ spouses employed in private households had

retirement insurance. Retirement insurance coverage among respondents’

spouses who are homemakers and unemployed were lower at 14.3 percent

and 16.1 percent, respectively.

The SSS covers the highest

percentage of retirement

insurance of respondents’

spouses.

Among respondents’ spouses, the SSS had the highest coverage among

government insurers with a total of 91.9 percent. This was followed by the

GSIS at 9 percent, and provident funds and other government insurers

accounting for 5.6 percent of the total respondents’ spouses covered by

insurance.

Almost half of respondents’

spouses are paying premiums

of about P201-400 monthly.

Forty-seven percent of the respondents’ spouses were currently paying

premiums of about P201-400 monthly at the time of the survey while

19.5 percent were paying P200 and below. About 19 percent were paying

P401-600 while 14.9 percent had payments of P600 and above. The average

and median monthly premiums paid by the respondents’ spouses through

employment-based insurers were P612 and P330, respectively. Compared to

the 2009 CFS, the average monthly premiums of respondents’ spouses

increased by 38 percent in NCR and 60.8 percent in Regions 1, 7, and 11.

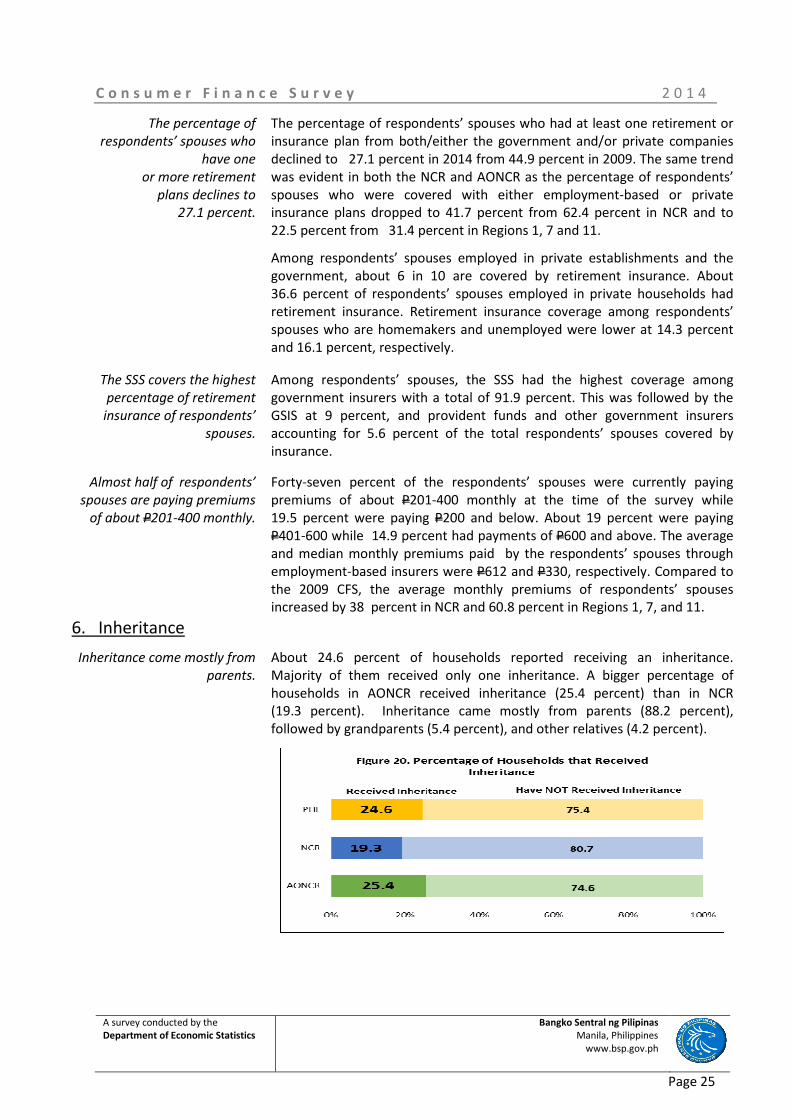

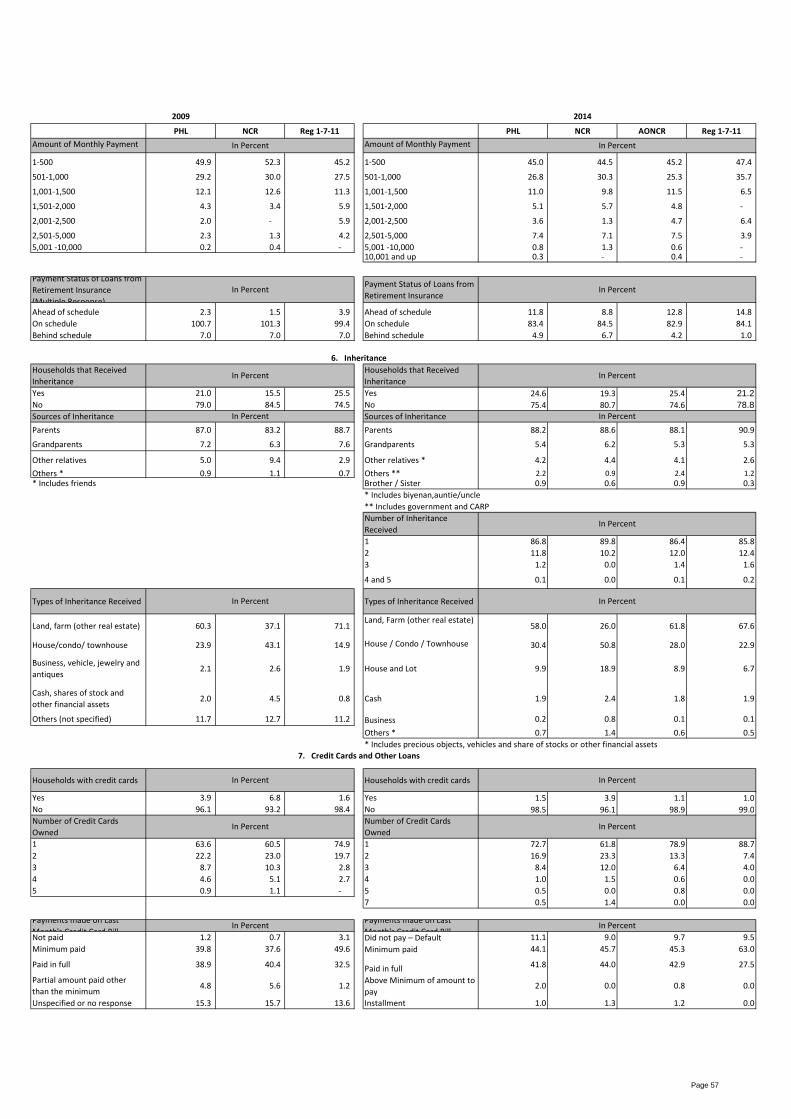

6. Inheritance

Inheritance come mostly from

parents.

About 24.6 percent of households reported receiving an inheritance.

Majority of them received only one inheritance. A bigger percentage of

households in AONCR received inheritance (25.4 percent) than in NCR

(19.3 percent). Inheritance came mostly from parents (88.2 percent),

followed by grandparents (5.4 percent), and other relatives (4.2 percent).

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 26

The most common inheritance

received is in the form of land,

farm, and house.

The most common inheritance received was real estate such as land or farm

(58.0 percent), and houses, condominiums, and townhouses (30.4 percent).

Households also received inheritance in the form of house and lot

(9.9 percent), cash (1.9 percent) and others (0.9 percent). Inheritance

received by both NCR and AONCR households followed the national pattern.

7. Credit Cards and Other Loans

Two percent of households

have credit cards.

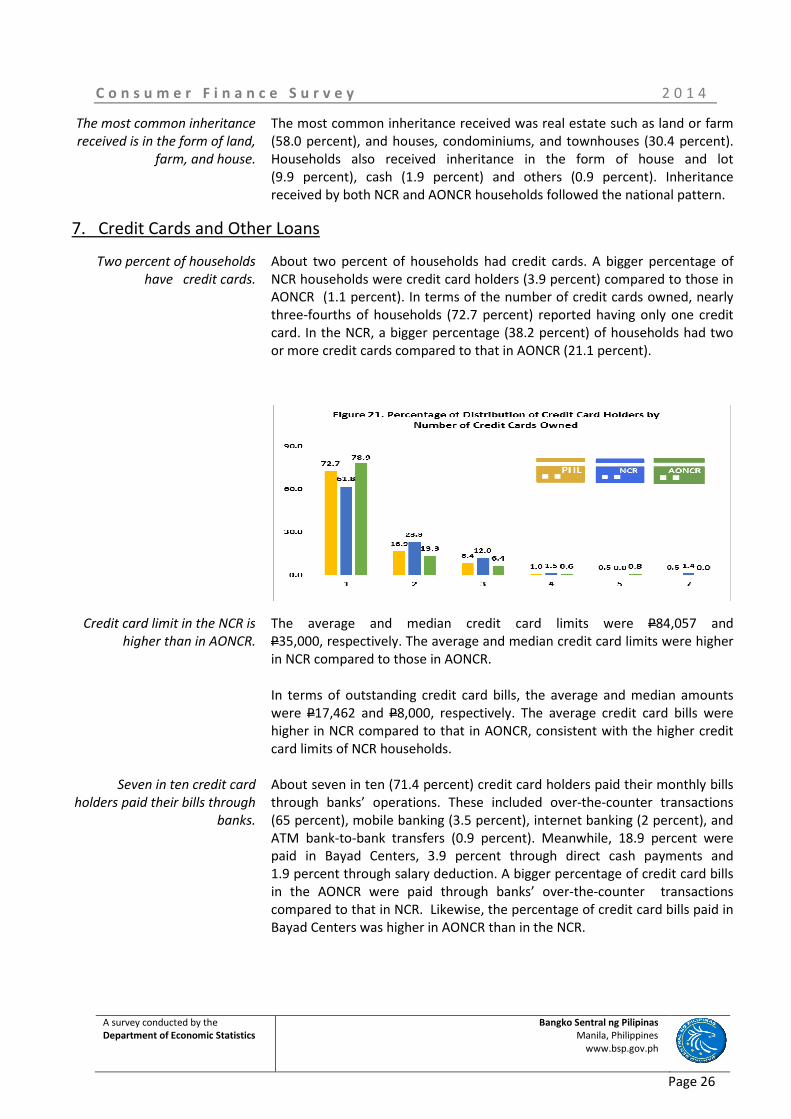

About two percent of households had credit cards. A bigger percentage of

NCR households were credit card holders (3.9 percent) compared to those in

AONCR (1.1 percent). In terms of the number of credit cards owned, nearly

three-fourths of households (72.7 percent) reported having only one credit

card. In the NCR, a bigger percentage (38.2 percent) of households had two

or more credit cards compared to that in AONCR (21.1 percent).

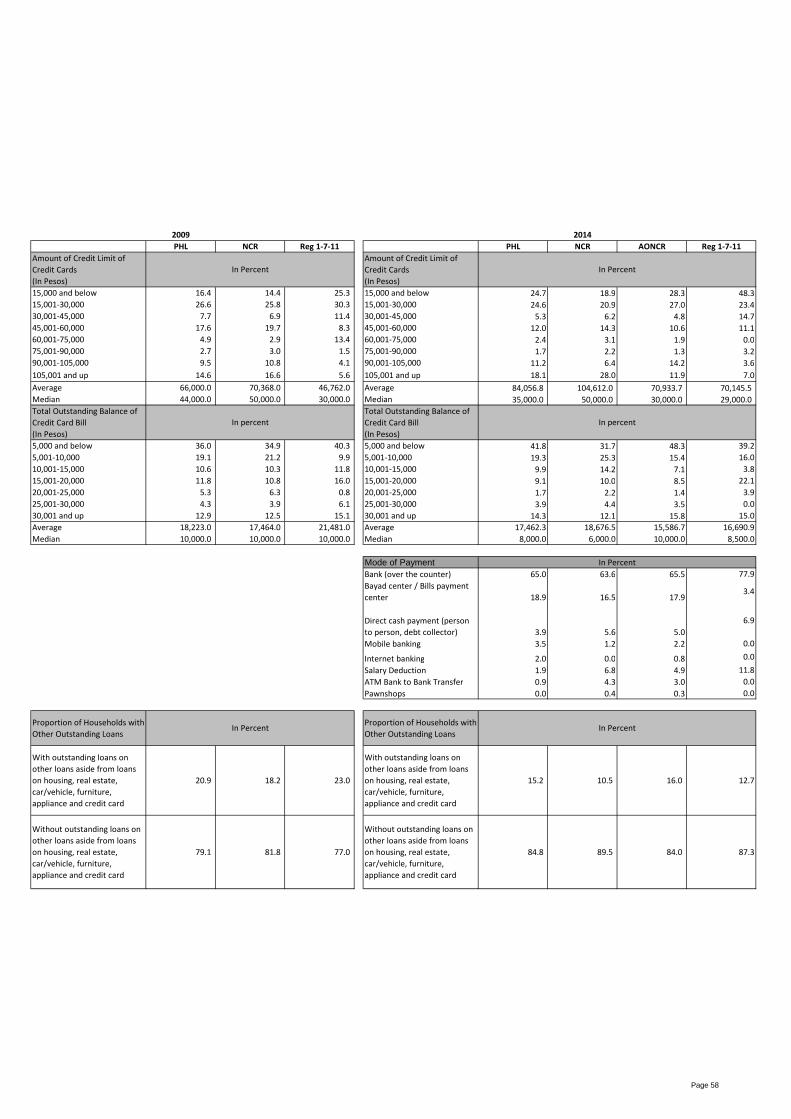

Credit card limit in the NCR is

higher than in AONCR.

The average and median credit card limits were P84,057 and

P35,000, respectively. The average and median credit card limits were higher

in NCR compared to those in AONCR.

Seven in ten credit card

holders paid their bills through

banks.

In terms of outstanding credit card bills, the average and median amounts

were P17,462 and P8,000, respectively. The average credit card bills were

higher in NCR compared to that in AONCR, consistent with the higher credit

card limits of NCR households.

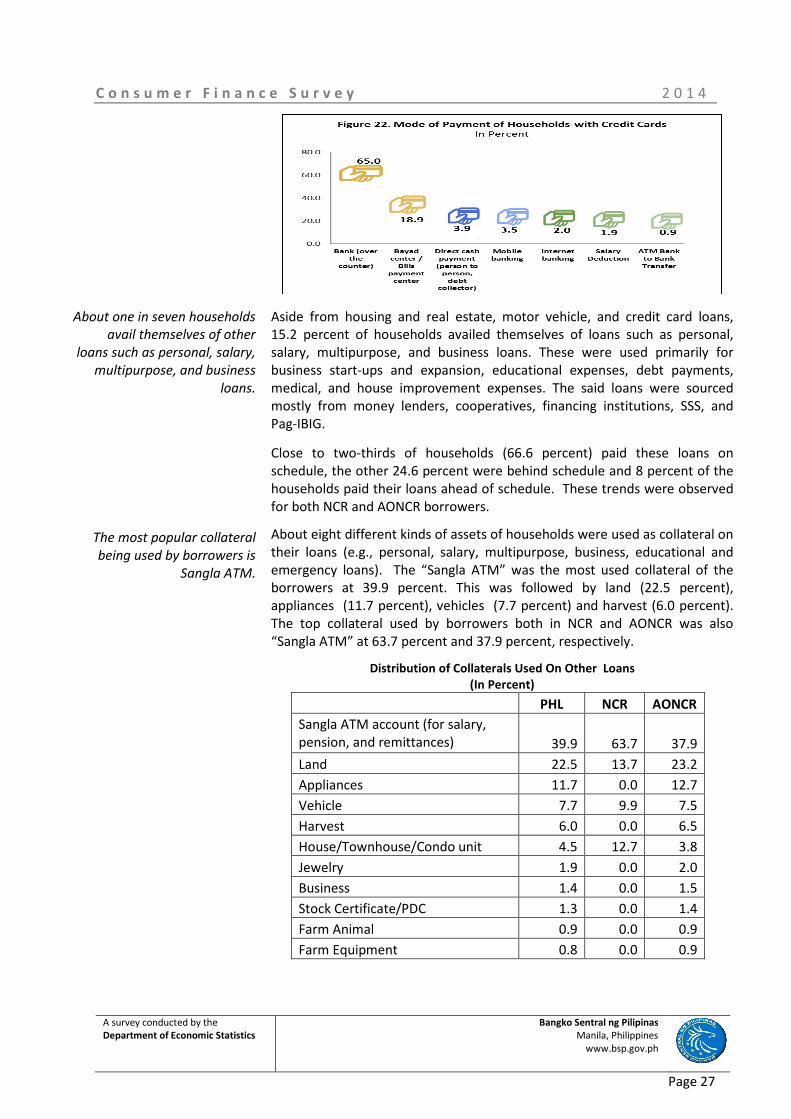

About seven in ten (71.4 percent) credit card holders paid their monthly bills

through banks’ operations. These included over-the-counter transactions

(65 percent), mobile banking (3.5 percent), internet banking (2 percent), and

ATM bank-to-bank transfers (0.9 percent). Meanwhile, 18.9 percent were

paid in Bayad Centers, 3.9 percent through direct cash payments and

1.9 percent through salary deduction. A bigger percentage of credit card bills

in the AONCR were paid through banks’ over-the-counter transactions

compared to that in NCR. Likewise, the percentage of credit card bills paid in

Bayad Centers was higher in AONCR than in the NCR.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 27

About one in seven households

avail themselves of other

loans such as personal, salary,

multipurpose, and business

loans.

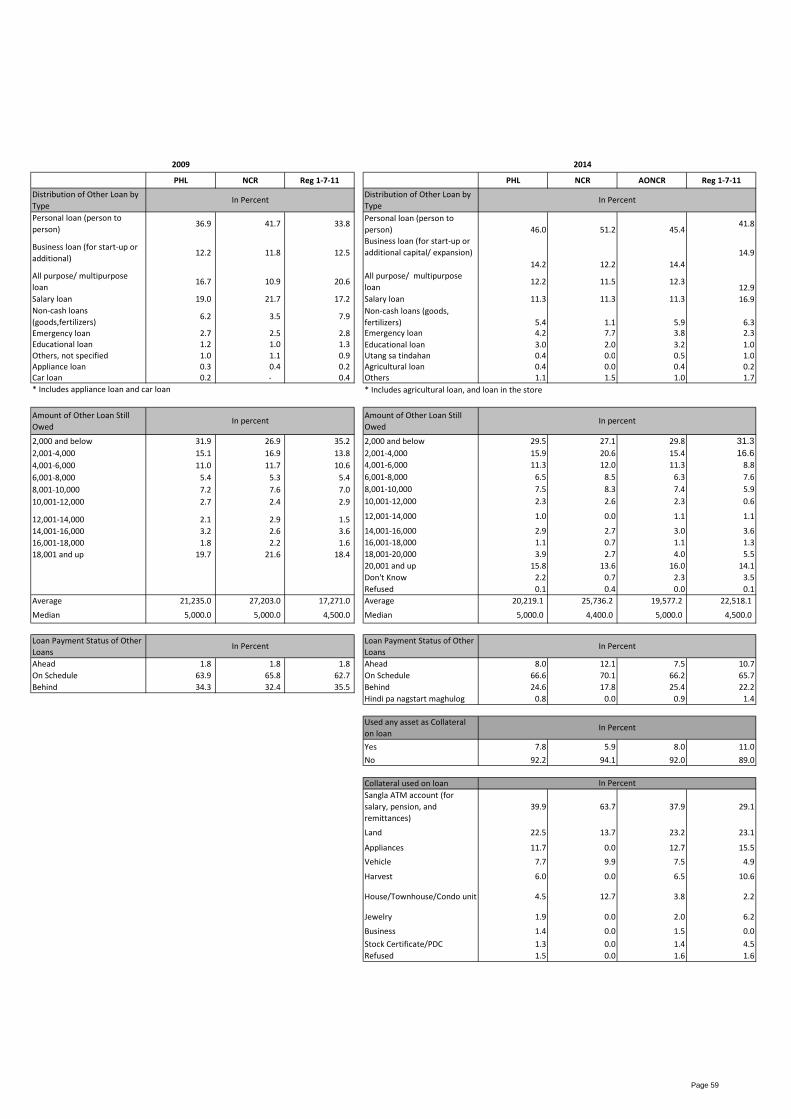

Aside from housing and real estate, motor vehicle, and credit card loans,

15.2 percent of households availed themselves of loans such as personal,

salary, multipurpose, and business loans. These were used primarily for

business start-ups and expansion, educational expenses, debt payments,

medical, and house improvement expenses. The said loans were sourced

mostly from money lenders, cooperatives, financing institutions, SSS, and

Pag-IBIG.

The most popular collateral

being used by borrowers is

Sangla ATM.

Close to two-thirds of households (66.6 percent) paid these loans on

schedule, the other 24.6 percent were behind schedule and 8 percent of the

households paid their loans ahead of schedule. These trends were observed

for both NCR and AONCR borrowers.

About eight different kinds of assets of households were used as collateral on

their loans (e.g., personal, salary, multipurpose, business, educational and

emergency loans). The “Sangla ATM” was the most used collateral of the

borrowers at 39.9 percent. This was followed by land (22.5 percent),

appliances (11.7 percent), vehicles (7.7 percent) and harvest (6.0 percent).

The top collateral used by borrowers both in NCR and AONCR was also

“Sangla ATM” at 63.7 percent and 37.9 percent, respectively.

Distribution of Collaterals Used On Other Loans

(In Percent)

PHL NCR AONCR

Sangla ATM account (for salary,

pension, and remittances) 39.9 63.7 37.9

Land 22.5 13.7 23.2

Appliances 11.7 0.0 12.7

Vehicle 7.7 9.9 7.5

Harvest 6.0 0.0 6.5

House/Townhouse/Condo unit 4.5 12.7 3.8

Jewelry 1.9 0.0 2.0

Business 1.4 0.0 1.5

Stock Certificate/PDC 1.3 0.0 1.4

Farm Animal 0.9 0.0 0.9

Farm Equipment 0.8 0.0 0.9

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 28

C. Income and Expenditures

The main sources of household

income are wages and

salaries.

Food and beverage consumed

at home is the main household

expenditure.

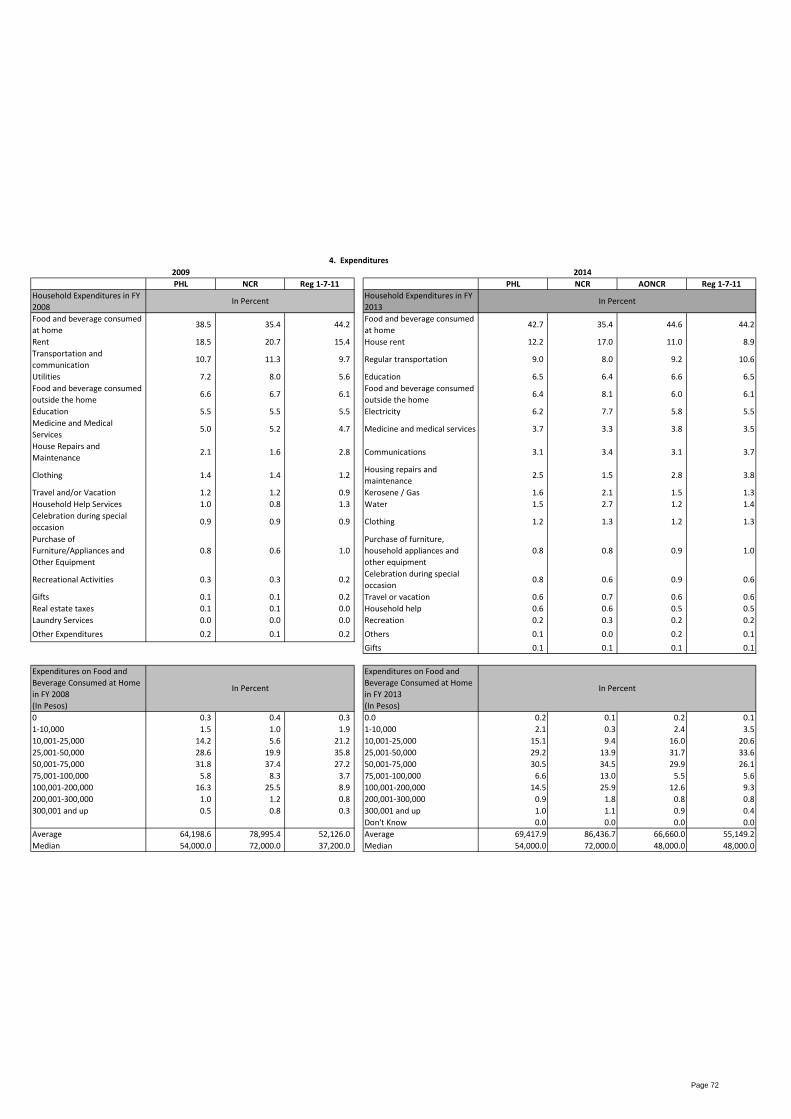

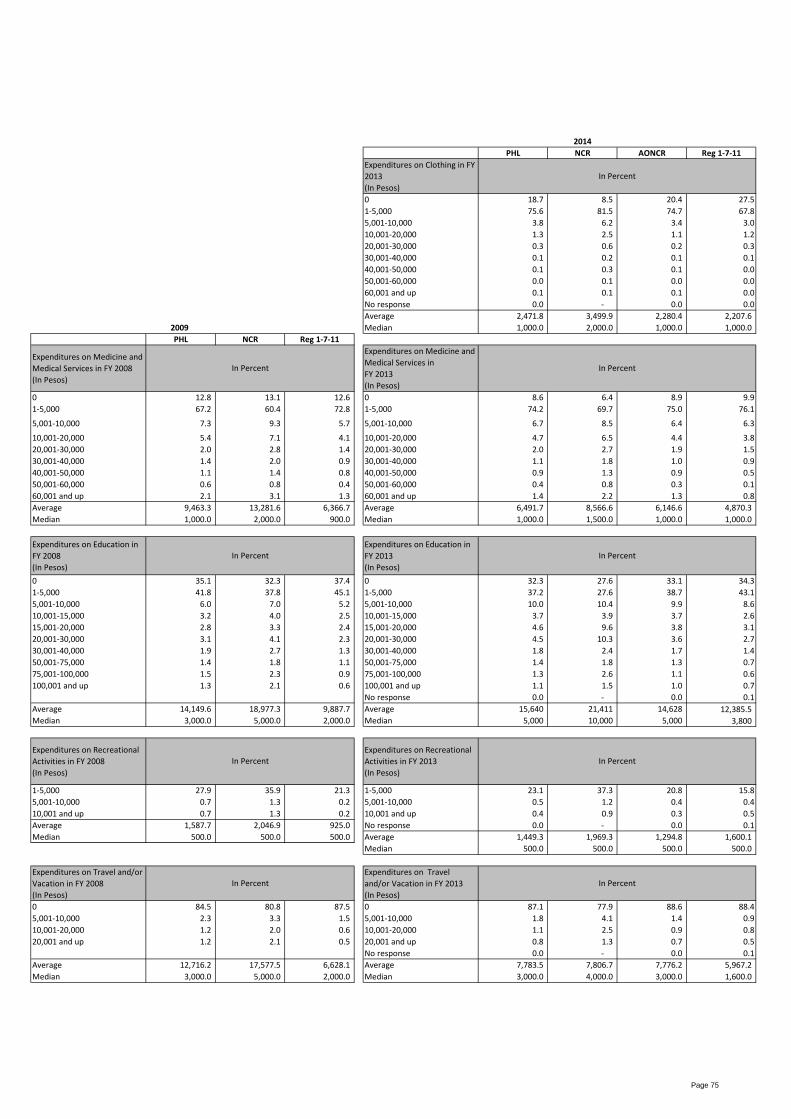

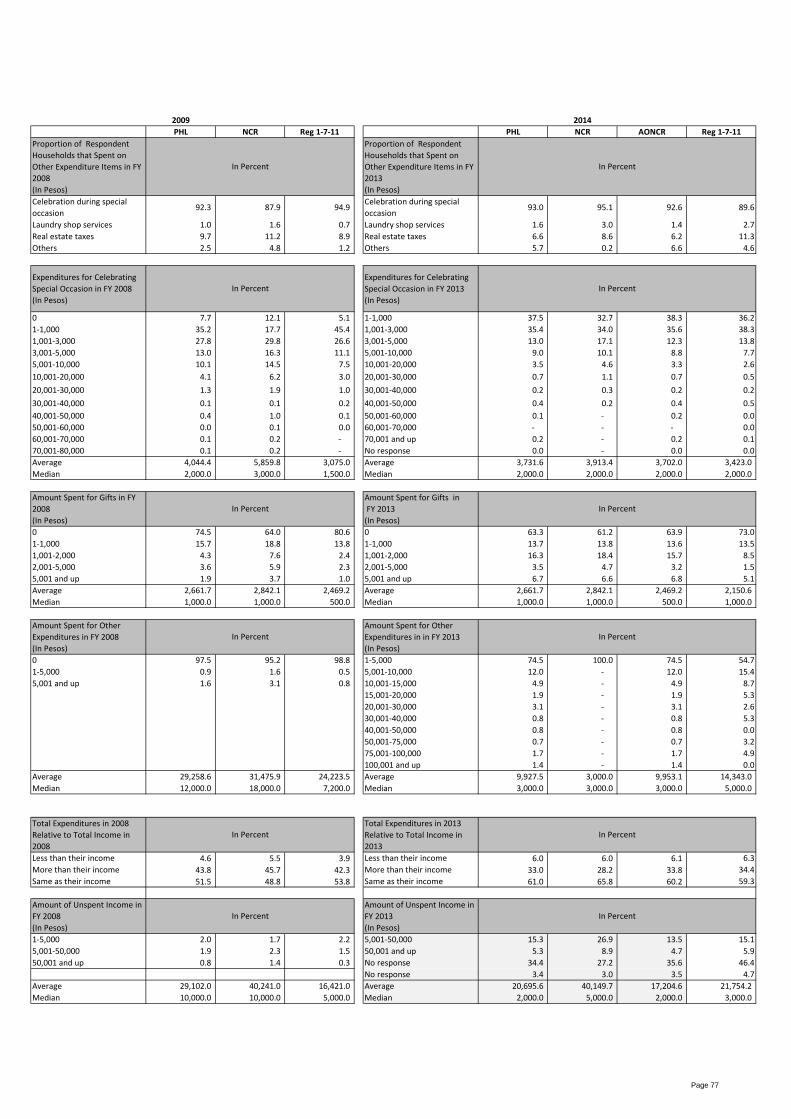

More than half (50.5 percent) of the respondents’ household income came

from wages and salaries. Other sources of household income were

businesses including self-employment (18.1 percent), financial assistance

from government (13.5 percent), financial assistance from abroad

(13.2 percent) and financial assistance from other households (10 percent).20

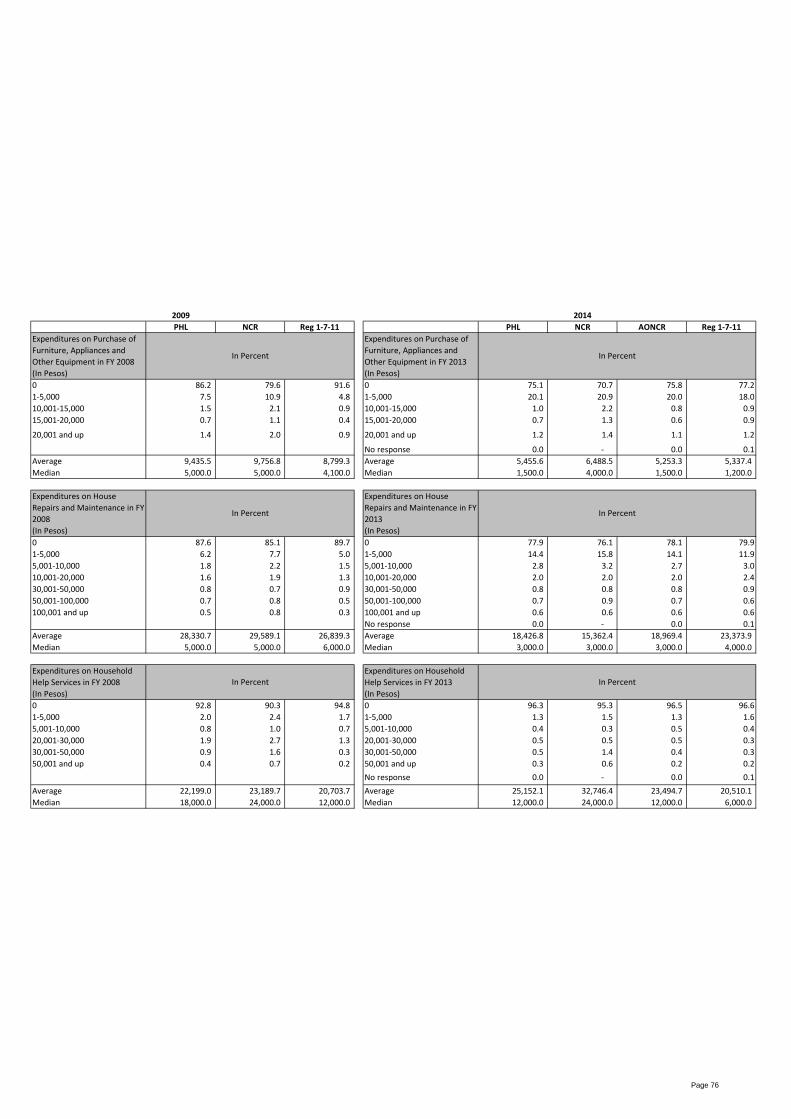

Food and beverages consumed at home accounted for 42.7 percent of the

annual household expenditures. This was followed by rent (12.2 percent),

regular transportation (9 percent), education (6.5 percent), food and

beverage consumed outside the home (6.4 percent), electricity (6.2 percent),

medicine and medical services (3.7 percent), utilities such as gas and water

(3.1 percent), communication (3.1 percent), house repairs and maintenance

(2.5 percent), clothing (1.2 percent), travel and recreation, celebration during

special occasions, and purchase of furniture and appliances at 0.8 percent

each,21

and household help services (0.6 percent).

1. Work and Income

Work and Income of Respondent

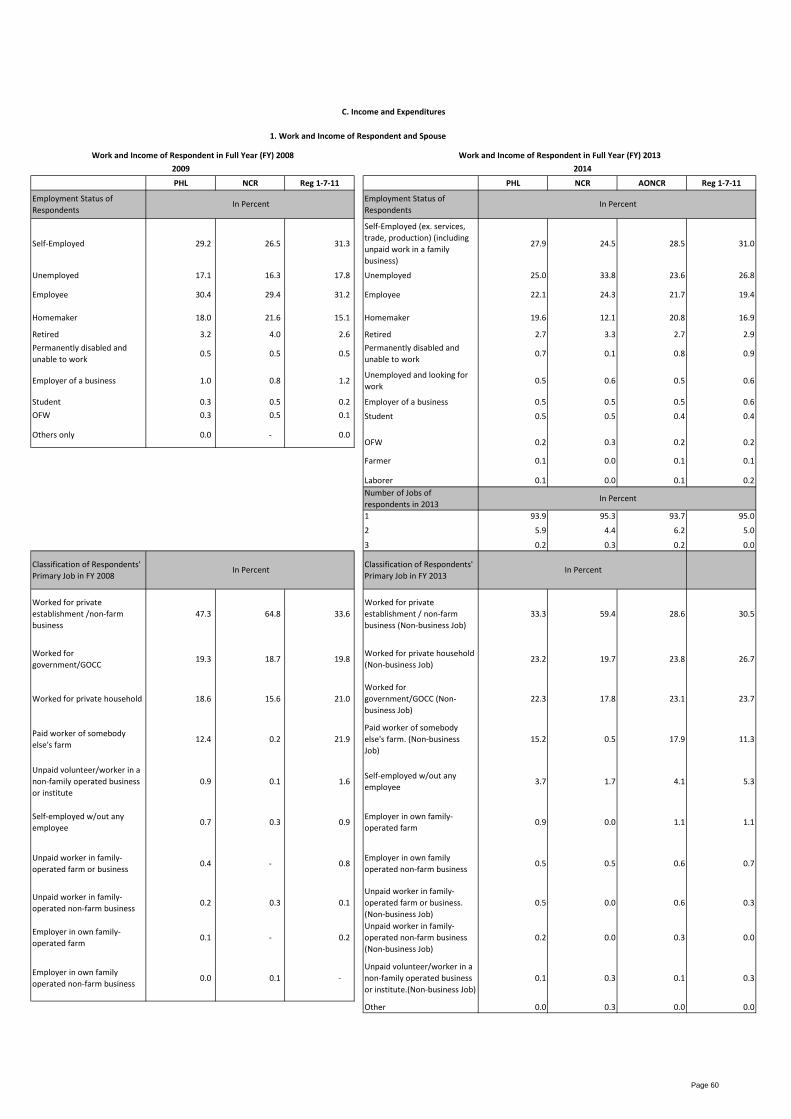

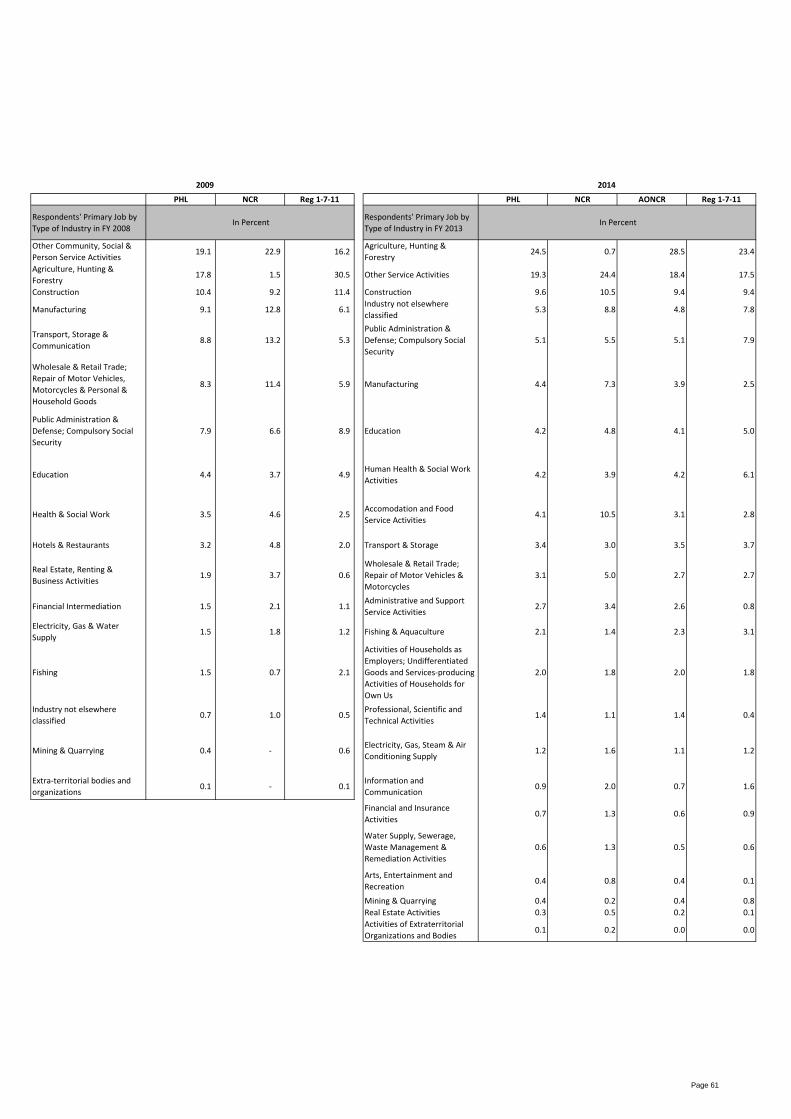

More than 50 percent of

respondents are working.

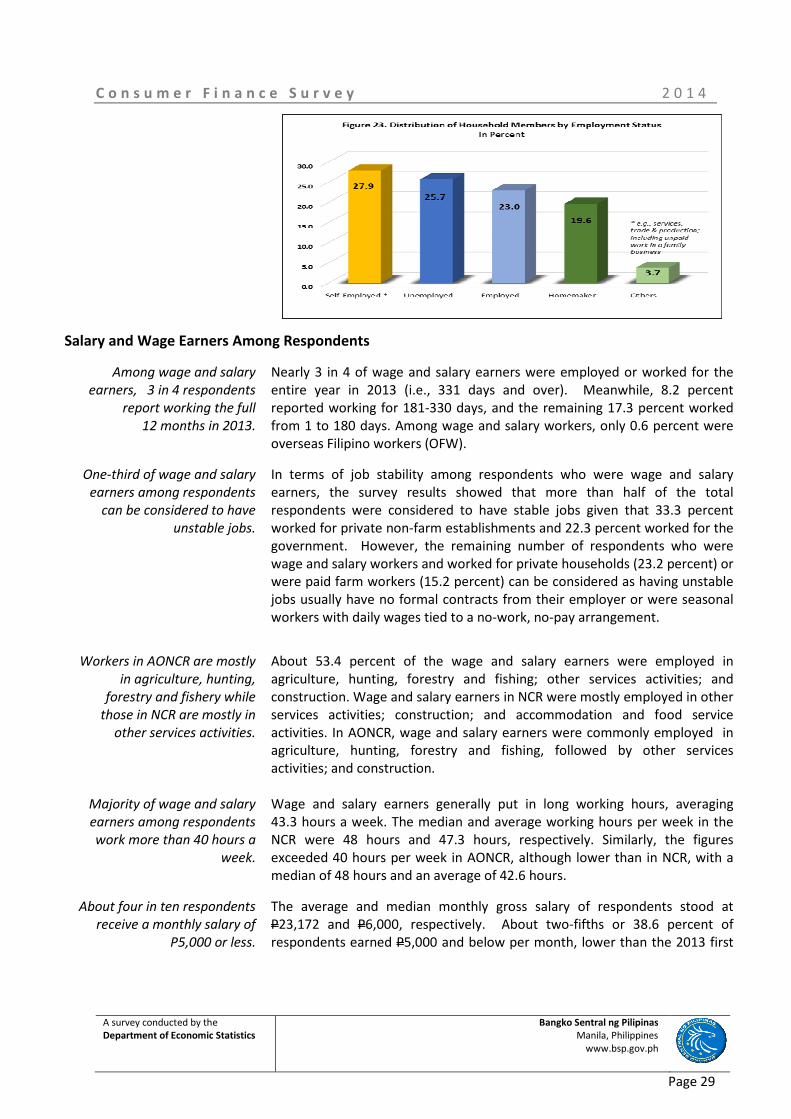

About 50.5 percent of respondents were working and reported the following

as their work status: self-employed (27.9 percent), employee or wage and

salary worker (22.1 percent), employer of a business (0.5 percent) and other

such as OFW (0.2 percent), farmer (0.1 percent) and labourer (0.1 percent)

Homemakers accounted for 19.6 percent, while a significant proportion of

respondents were unemployed (25.0 percent).22

Other respondents were

retired employees, permanently disabled persons and students (2.7 percent,

0.7 percent, and 0.5 percent, respectively). The higher percentage of

respondents that reported their status to be unemployed relative to the

PSA’s official unemployment figures can be attributed to the

“underemployed” respondents who considered themselves as unemployed

during the survey.23

Most respondents who were working had only one type of job (96 percent),

while 3.9 percent held two types of jobs, e.g., the respondent worked both as

an employee and as self-employed in a farm or business.

20

The total adds up to more than 100 percent inasmuch as some households had multiple sources of income. 21

Rent included imputed rental values for residences owned by households. 22

The unemployment and underemployment rates recorded by the PSA in the last quarter of 2013 and first

quarter of 2014 were 24.4 percent and 27 percent, respectively. 23

Based on PSA’s definition, underemployed persons include all employed persons who expressed the desire to

have additional hours of work in their present job or an additional job, or to have a new job with longer working

hours. Visibly underemployed persons are those who work for less than 40 hours during the reference period

and want additional hours of work.

C o n s u m e r F i n a n c e S u r v e y 2 0 1 4

A survey conducted by the

Department of Economic Statistics Bangko Sentral ng Pilipinas

Manila, Philippines

www.bsp.gov.ph

Page 29

Salary and Wage Earners Among Respondents

Among wage and salary

earners, 3 in 4 respondents

report working the full

12 months in 2013.

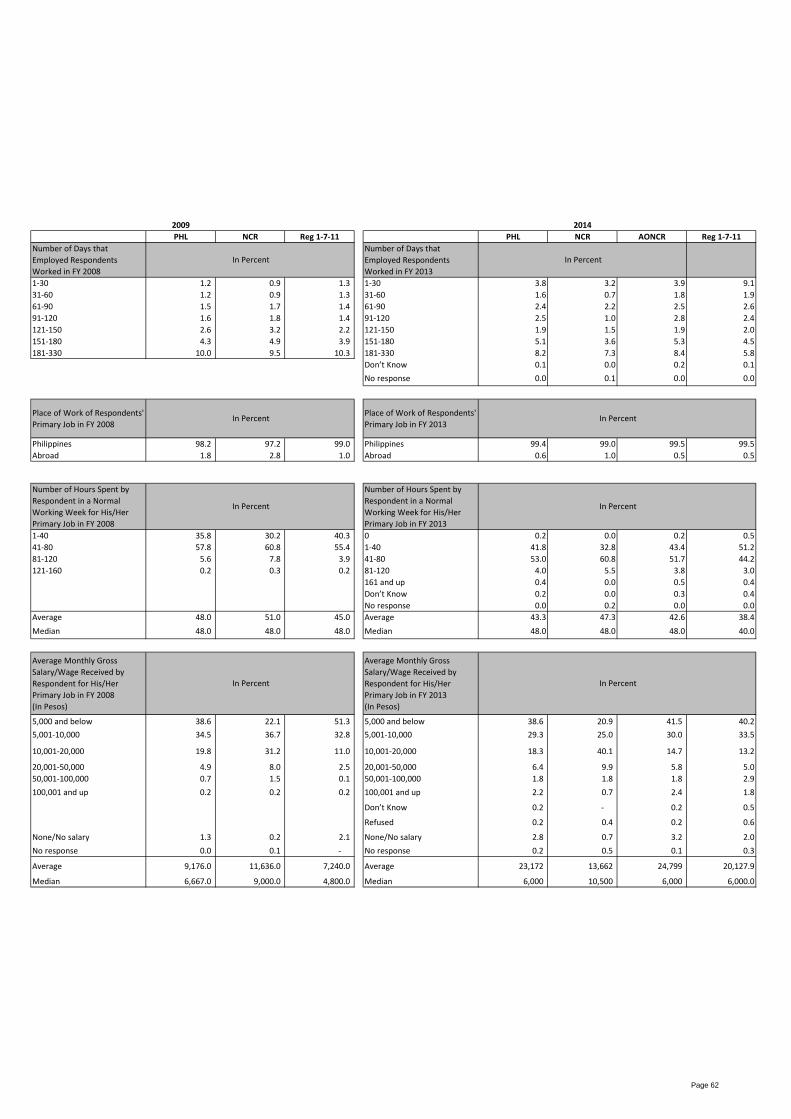

Nearly 3 in 4 of wage and salary earners were employed or worked for the

entire year in 2013 (i.e., 331 days and over). Meanwhile, 8.2 percent