conquering the term sheet everything you need to know about deal terms part 3

TRANSCRIPT

Conquering the Term Sheet

Everything You Need to Know About Deal Terms

Part 3

David StarkPartner, OurCrowd

@starkupnation

Zack MillerPartner, OurCrowd

@newrulesinvest

OurCrowd

Leading equity crowdfunding platform with 8000+ investors

from over 100 countries

Mailbox: Liquidation preferences

It depends. Pro rata rights are a right, not an obligation. Things to remember: Lean on your winners. Avoid being crushed.

Important note: If you have the opportunity to buy up, why not?

Q: Should I exercise my pro rata rights?

Quick ReviewLesson 1 - Equity

Valuation Liquidation preferences

ESOP

Key takeawayNeed to look at the

WHOLE term sheet to see the full

picture

Lesson 2 - EquityPro rata rights

Anti-dilution protection Control provisions

Key takeawayNeed to have

opportunity to continue backing your winners

Today’s agenda

Convertible notes Pros and cons (investor/entrepreneur)

Amount/maturity Interest

Conversion Discount

Cap Auto/voluntary conversion

Repayment SAFE

Convertible Notes

Structured as a loan, converts to equity if certain events occur

(generally upon a future financing)

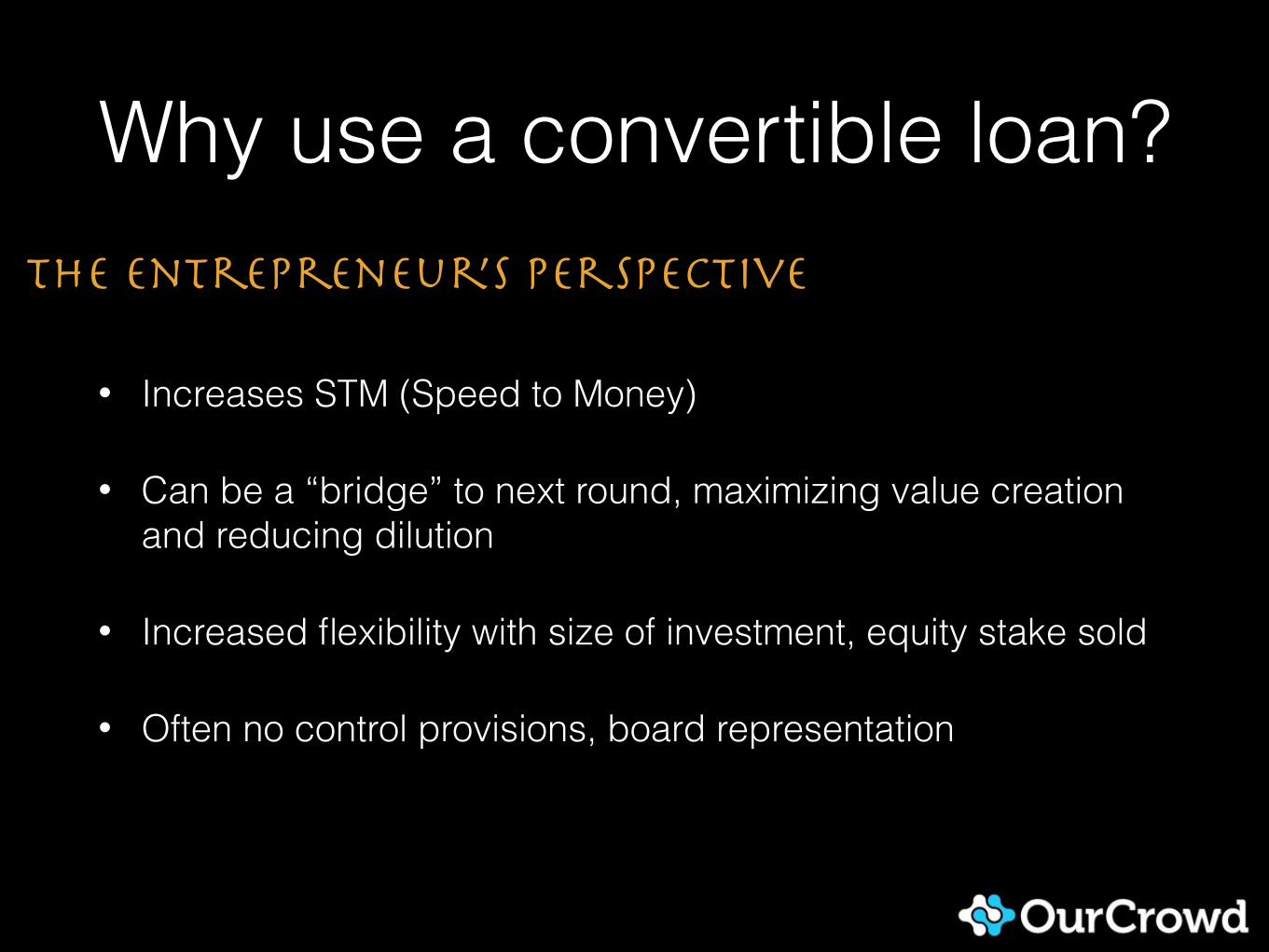

Why use a convertible loan?

• Increases STM (Speed to Money)

• Can be a “bridge” to next round, maximizing value creation and reducing dilution

• Increased flexibility with size of investment, equity stake sold

• Often no control provisions, board representation

The entrepreneur’s Perspective

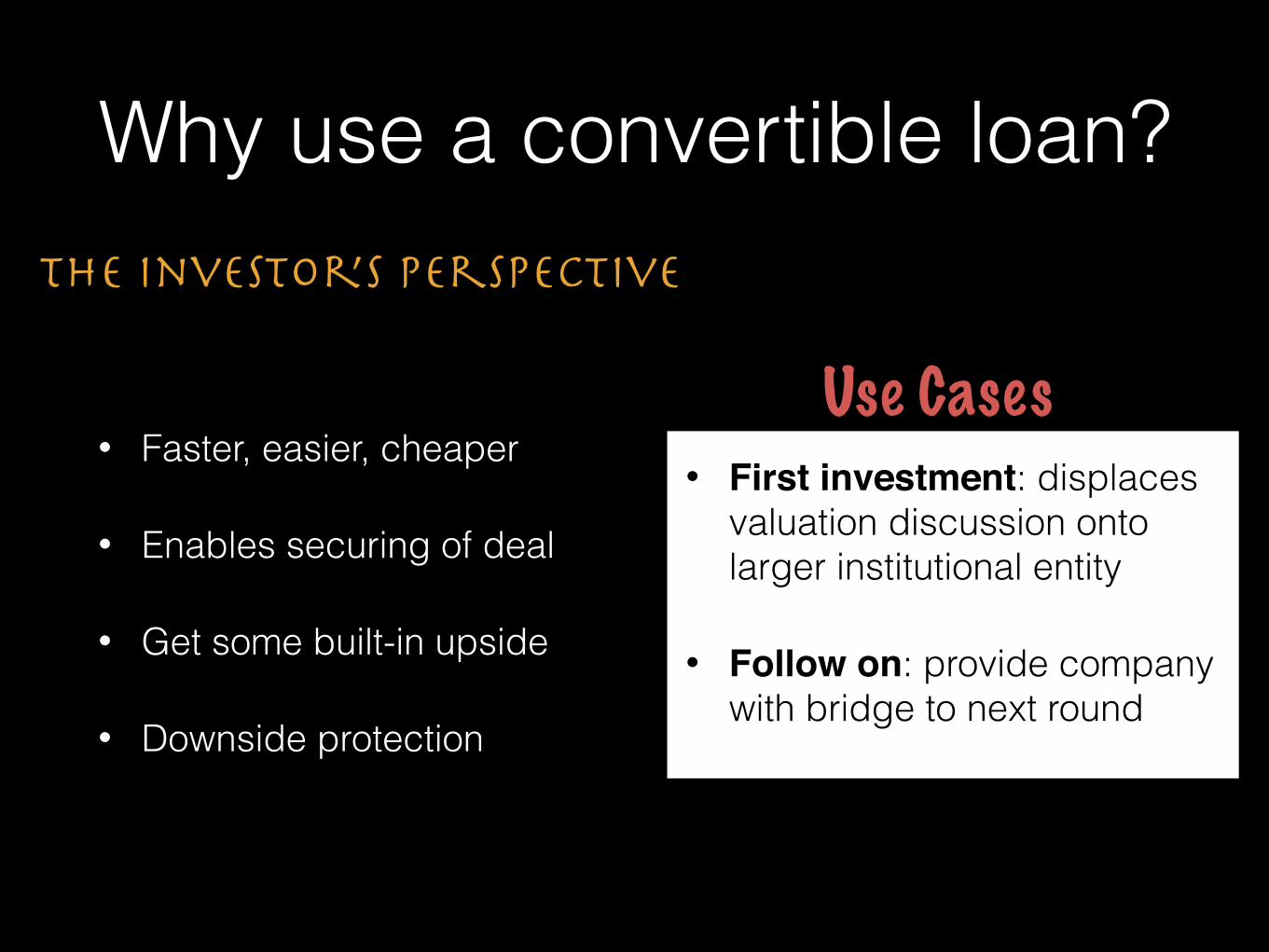

Why use a convertible loan?

• Faster, easier, cheaper

• Enables securing of deal

• Get some built-in upside

• Downside protection

The Investor’s Perspective

• First investment: displaces valuation discussion onto larger institutional entity

• Follow on: provide company with bridge to next round

Use Cases

Keeping the faithEventual rights and preferences are unknown at the time

of investment…

Loan AmountHow much money is going

to be invested by you +

How much money will be invested by others

(What is the timeframe for others to join)

MaturityLength of the loan period Typically 12-24 months

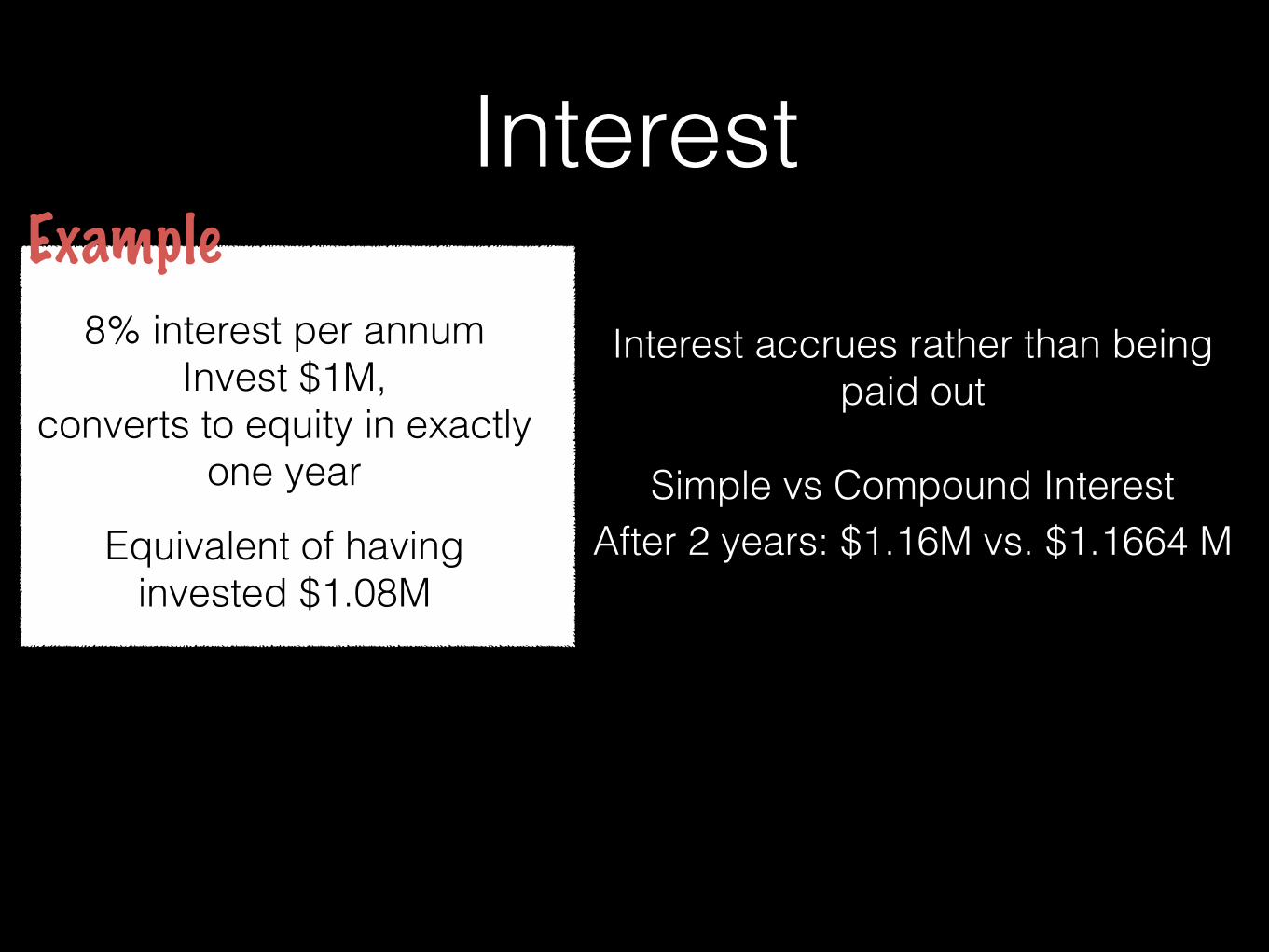

Interest

Convertibles are loans and have interest rate associated with them

Secured vs. Non-secured

Underlying assets to seize or personal guarantee

PrepaymentNote may not be prepaid without the consent of the

lender

Interest

Interest accrues rather than being paid out

Simple vs Compound Interest

8% interest per annum

Invest $1M, converts to equity in exactly

one year

Equivalent of having invested $1.08M

Example

After 2 years: $1.16M vs. $1.1664 M

Conversion

Move from debt to equity

Automatic vs. Voluntary Conversion

Exactly as it sounds, some conversions are forced when certain conditions are met

Others are optional

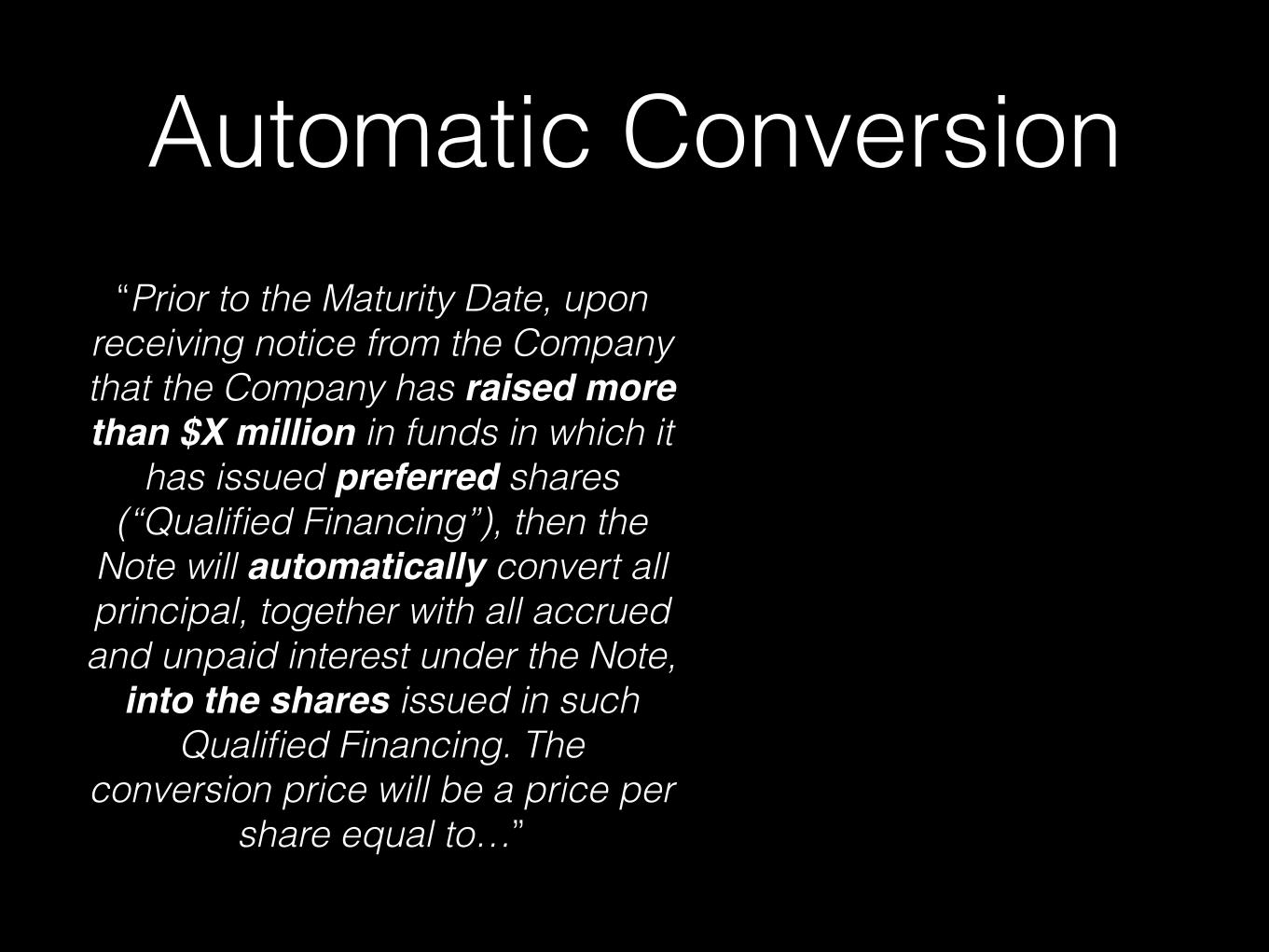

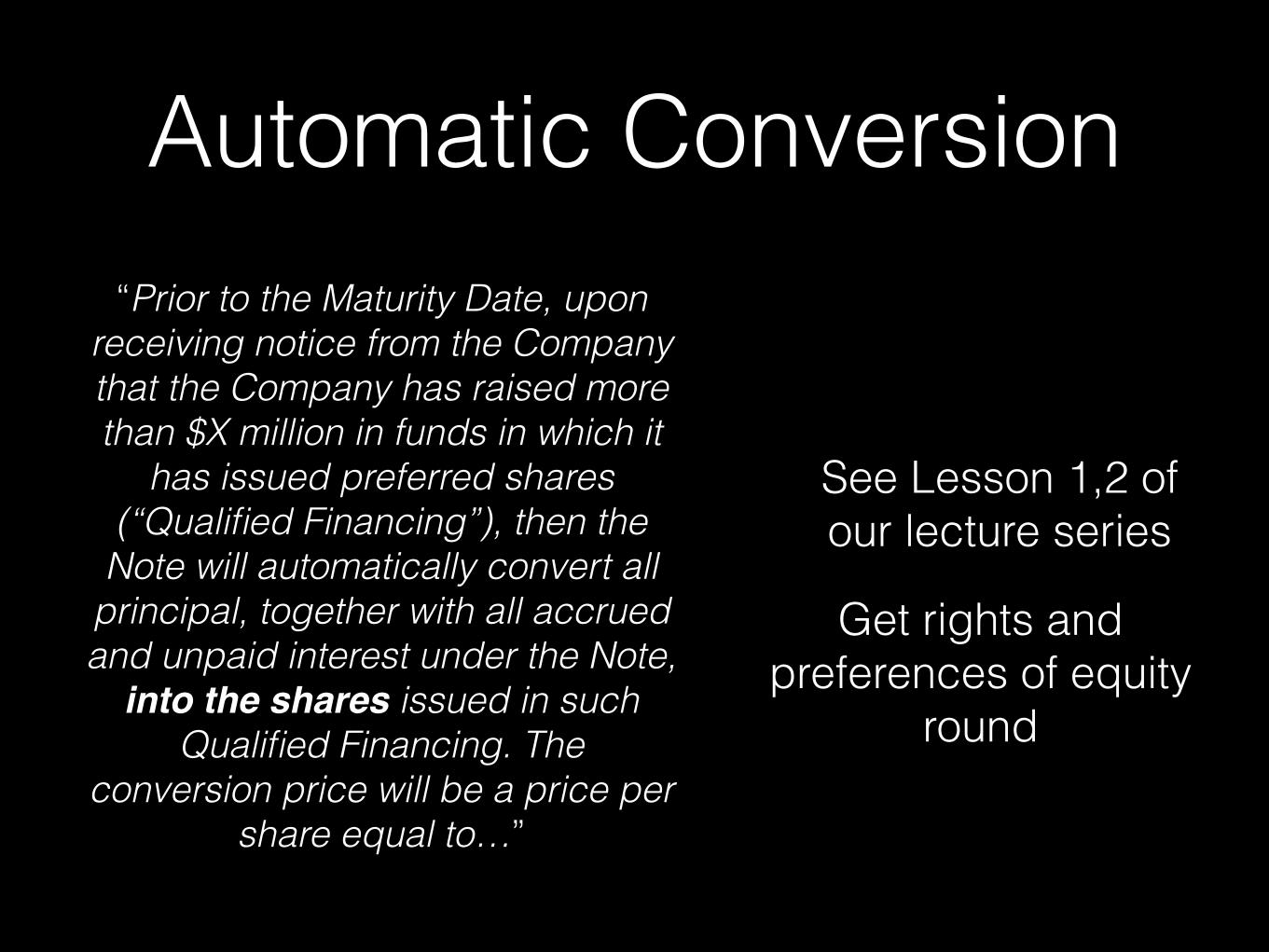

Automatic Conversion“Prior to the Maturity Date, upon

receiving notice from the Company that the Company has raised more than $X million in funds in which it

has issued preferred shares (“Qualified Financing”), then the

Note will automatically convert all principal, together with all accrued and unpaid interest under the Note,

into the shares issued in such Qualified Financing. The

conversion price will be a price per share equal to…”

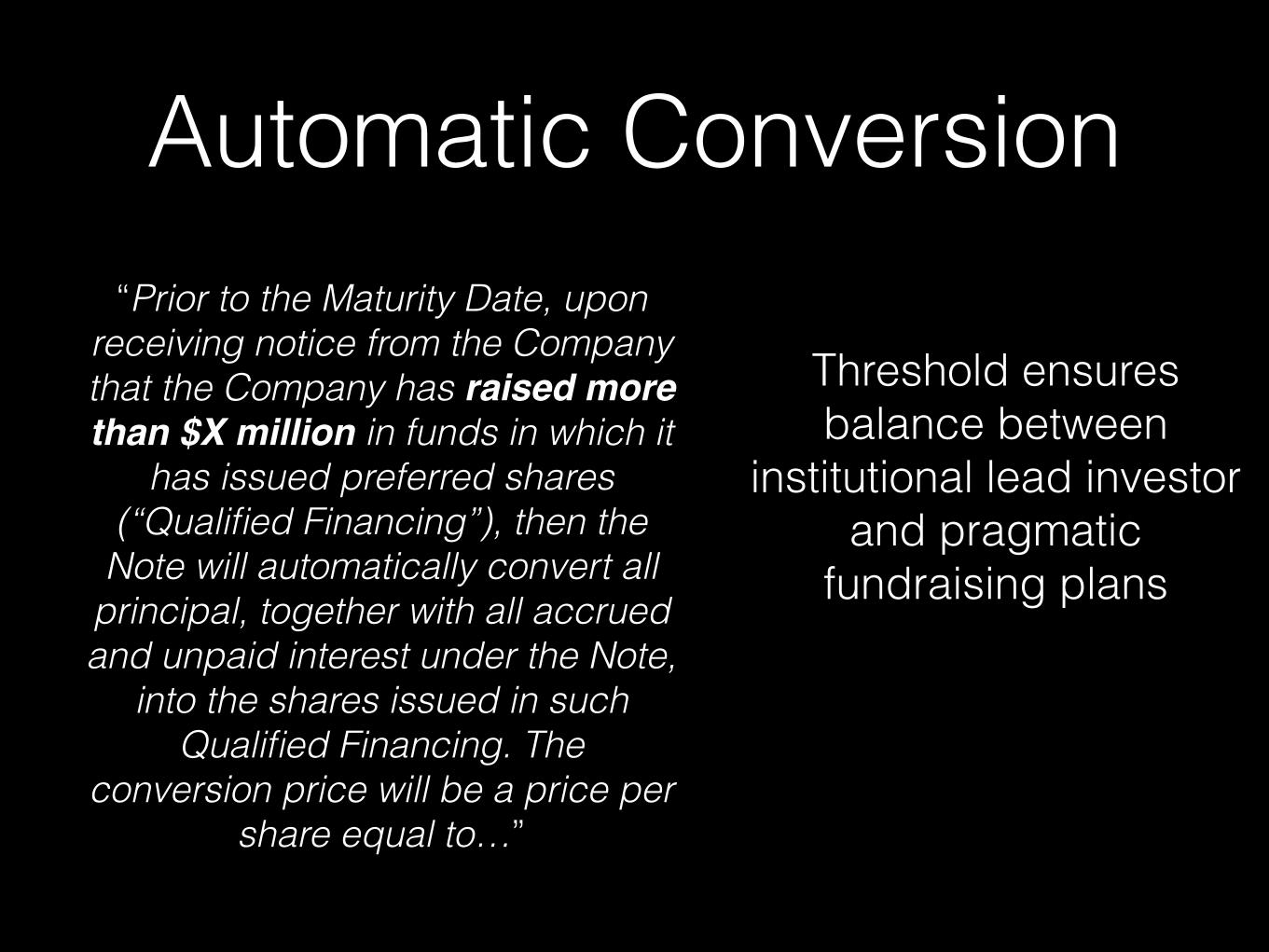

Automatic Conversion“Prior to the Maturity Date, upon

receiving notice from the Company that the Company has raised more than $X million in funds in which it

has issued preferred shares (“Qualified Financing”), then the

Note will automatically convert all principal, together with all accrued and unpaid interest under the Note,

into the shares issued in such Qualified Financing. The

conversion price will be a price per share equal to…”

Threshold ensures balance between

institutional lead investor and pragmatic

fundraising plans

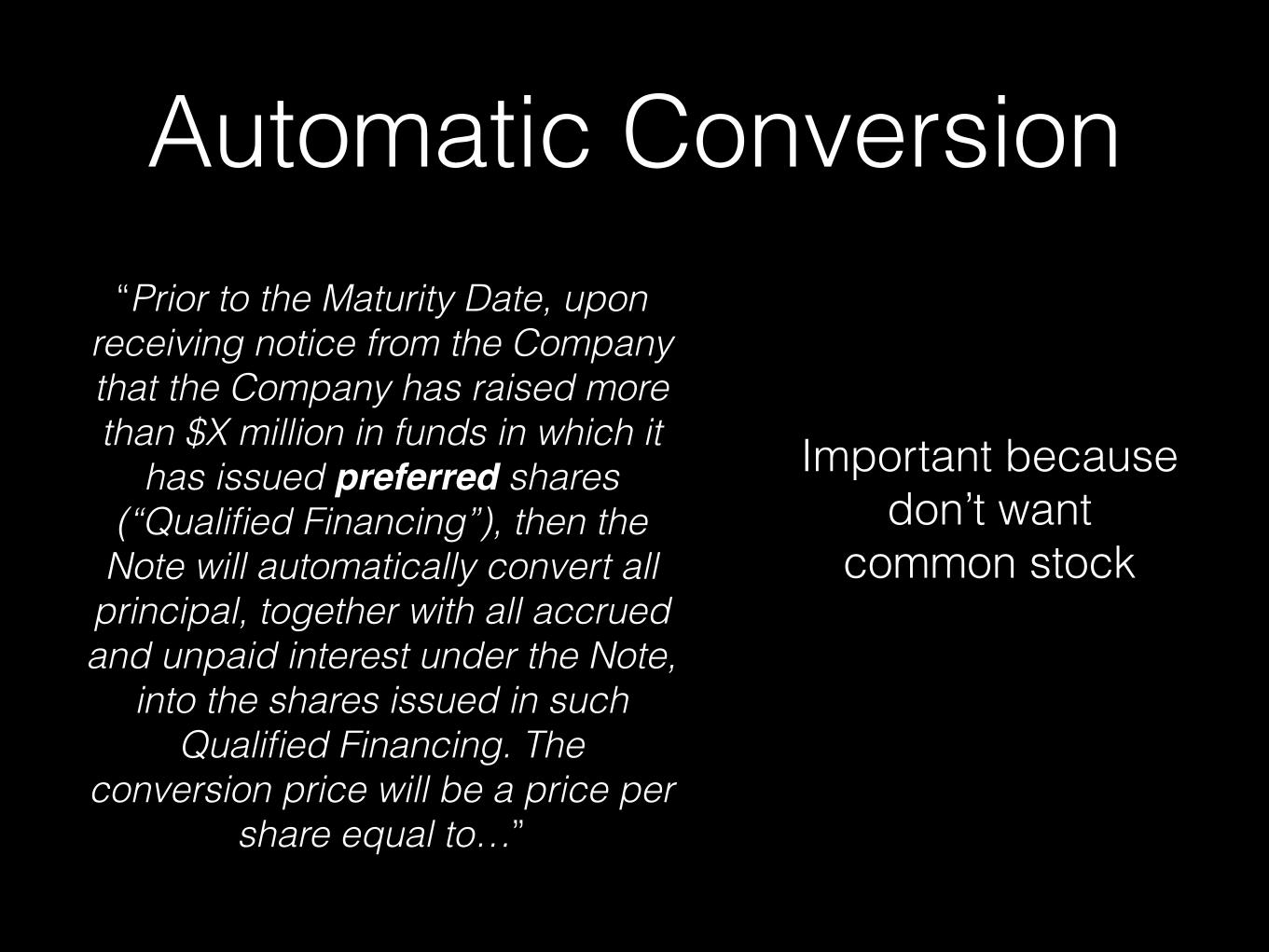

Automatic Conversion“Prior to the Maturity Date, upon

receiving notice from the Company that the Company has raised more than $X million in funds in which it

has issued preferred shares (“Qualified Financing”), then the

Note will automatically convert all principal, together with all accrued and unpaid interest under the Note,

into the shares issued in such Qualified Financing. The

conversion price will be a price per share equal to…”

Important because don’t want

common stock

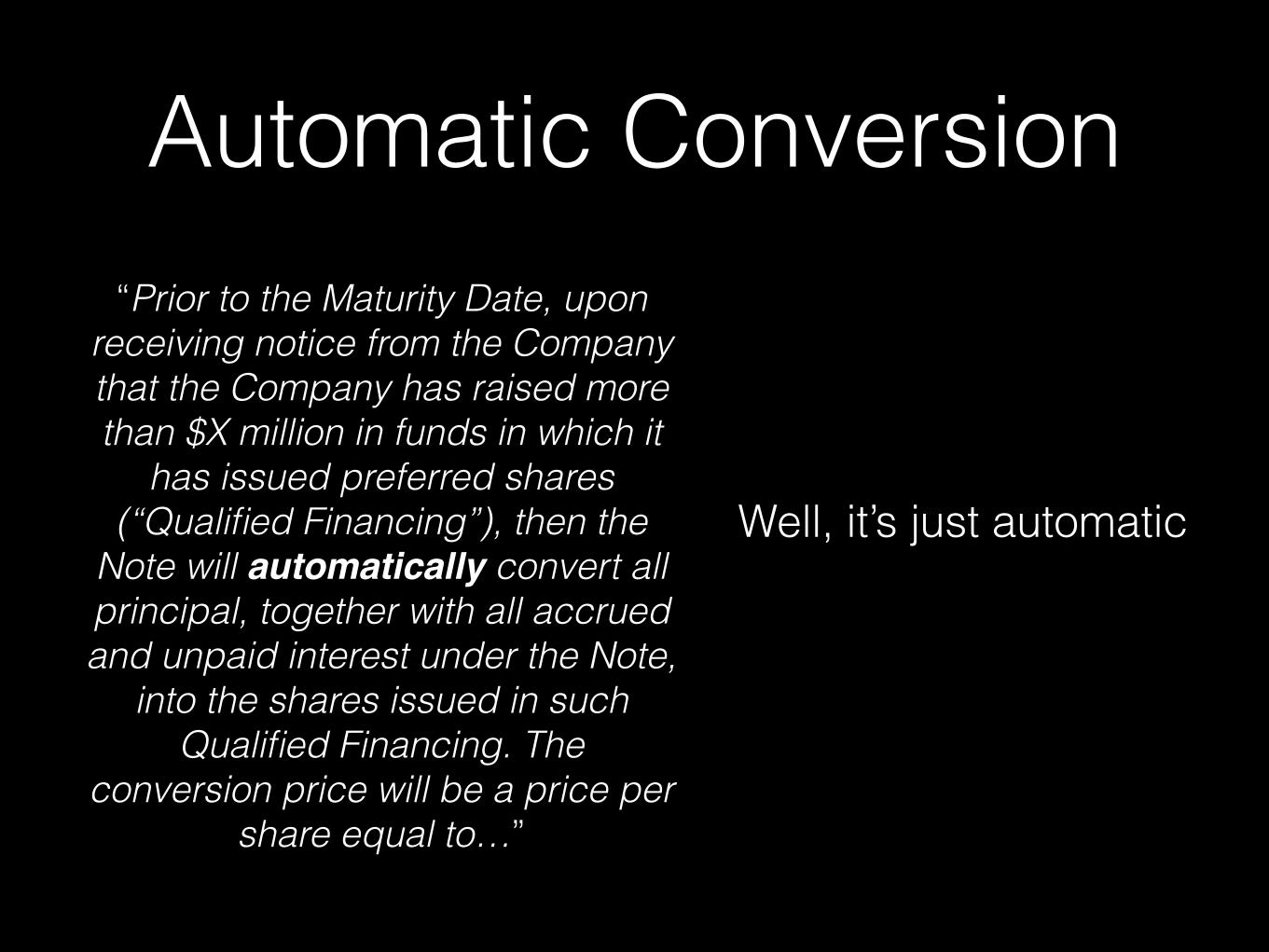

Automatic Conversion“Prior to the Maturity Date, upon

receiving notice from the Company that the Company has raised more than $X million in funds in which it

has issued preferred shares (“Qualified Financing”), then the

Note will automatically convert all principal, together with all accrued and unpaid interest under the Note,

into the shares issued in such Qualified Financing. The

conversion price will be a price per share equal to…”

Well, it’s just automatic

Automatic Conversion“Prior to the Maturity Date, upon

receiving notice from the Company that the Company has raised more than $X million in funds in which it

has issued preferred shares (“Qualified Financing”), then the

Note will automatically convert all principal, together with all accrued and unpaid interest under the Note,

into the shares issued in such Qualified Financing. The

conversion price will be a price per share equal to…”

See Lesson 1,2 of our lecture series

Get rights and preferences of equity

round

So, now you know which shares you’ll receive.

But what are you paying for them??

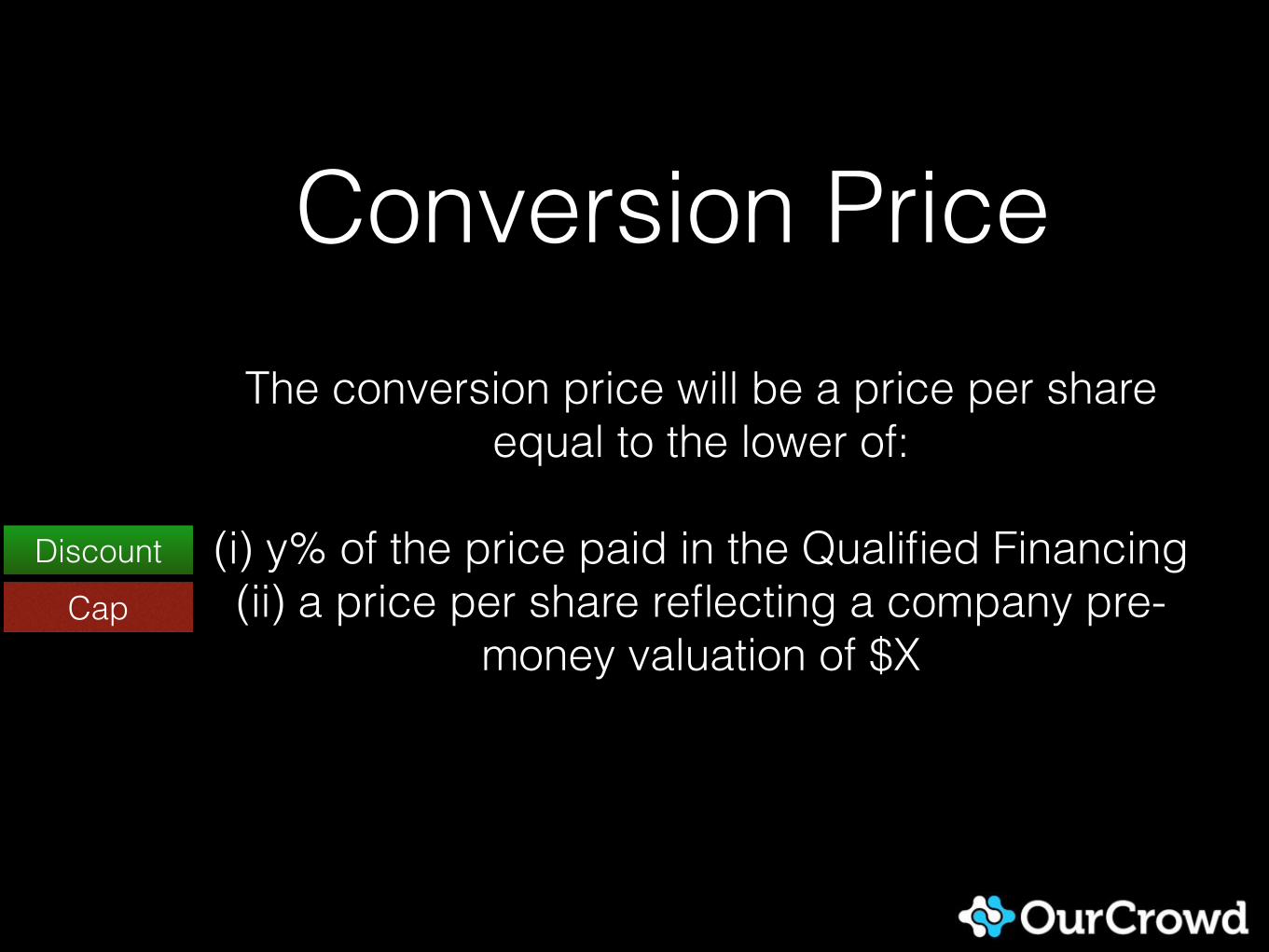

Conversion PriceThe conversion price will be a price per share

equal to the lower of:

(i) y% of the price paid in the Qualified Financing (ii) a price per share reflecting a company pre-

money valuation of $X

DiscountCap

Conversion Price

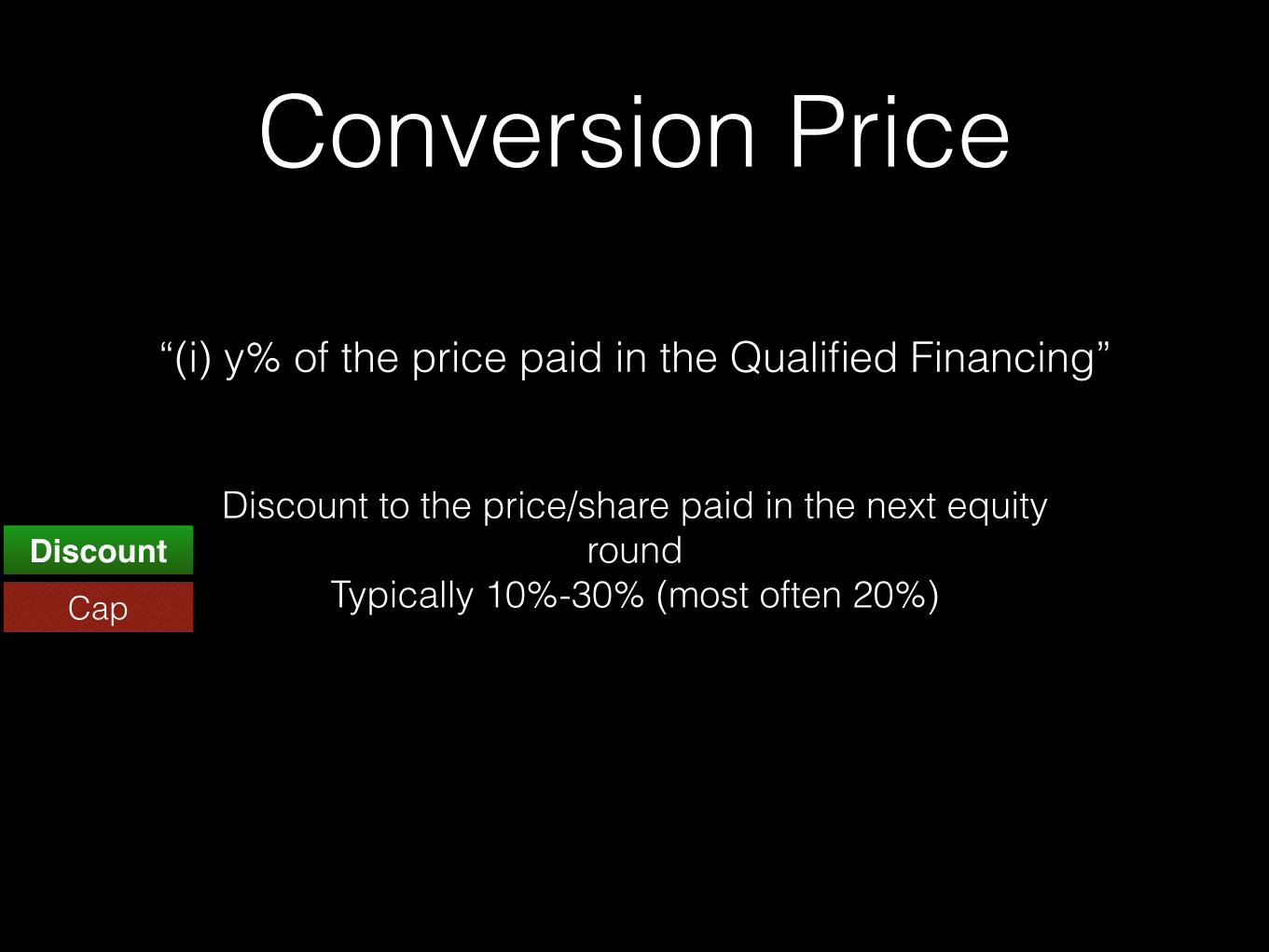

Discount to the price/share paid in the next equity round

Typically 10%-30% (most often 20%)Discount

Cap

“(i) y% of the price paid in the Qualified Financing”

Conversion Price

DiscountCap

“(i) y% of the price paid in the Qualified Financing”

Time-triggered discount: no discount if next round w/in 90 days from closing

Escalating discount: 15% within 90 days, 25% after 90 days but prior to 180 days, 35% after 180

days

Examples of variations

Real Life Example

Conversion Price

20% discount:next round = $1.00 per share, then the note will

convert into the same shares at a 20% discount, or $0.80 per share.

$500,000 convertible note —> 625,000 shares ($500,000 / $0.80)

New $500,000 equity investor —> 500,000 shares ($500,000 / $1.00)

DiscountCap

Conversion Price

DiscountCap

(ii) a price per share reflecting a company pre-money valuation of $X

Maximum conversion valuation(regardless of valuation of next round)

Conversion Price

DiscountCap

(ii) a price per share reflecting a company pre-money valuation of $X

breakeven point is $X/Y%eg. lower of 80% of pps or $20M cap —>

$20M/8% = $25M

<$25M 20% discount

>$25M $20M cap (discount > 20%)

Next round valuation

Conversion Price

DiscountCap

Importance of a cap for investors• Protect upside on risk-adj basis • Align interests • Protection vs. tail risk

Balance with management not wanting cap to set next round’s valuation

Non Qualified Financing

Financing round that doesn’t meet the criteria

Can voluntarily convert

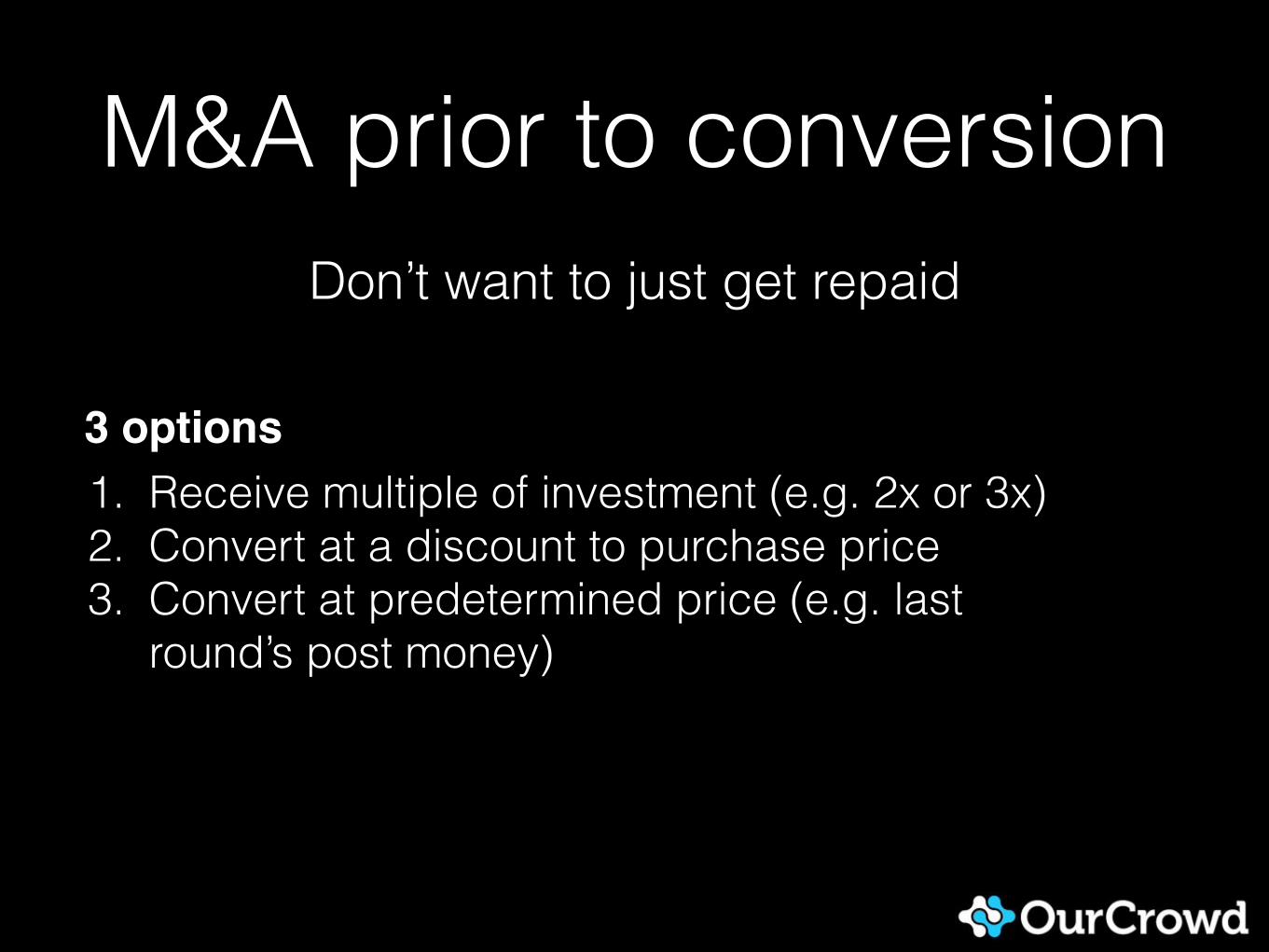

M&A prior to conversionDon’t want to just get repaid

1. Receive multiple of investment (e.g. 2x or 3x) 2. Convert at a discount to purchase price 3. Convert at predetermined price (e.g. last

round’s post money)

3 options

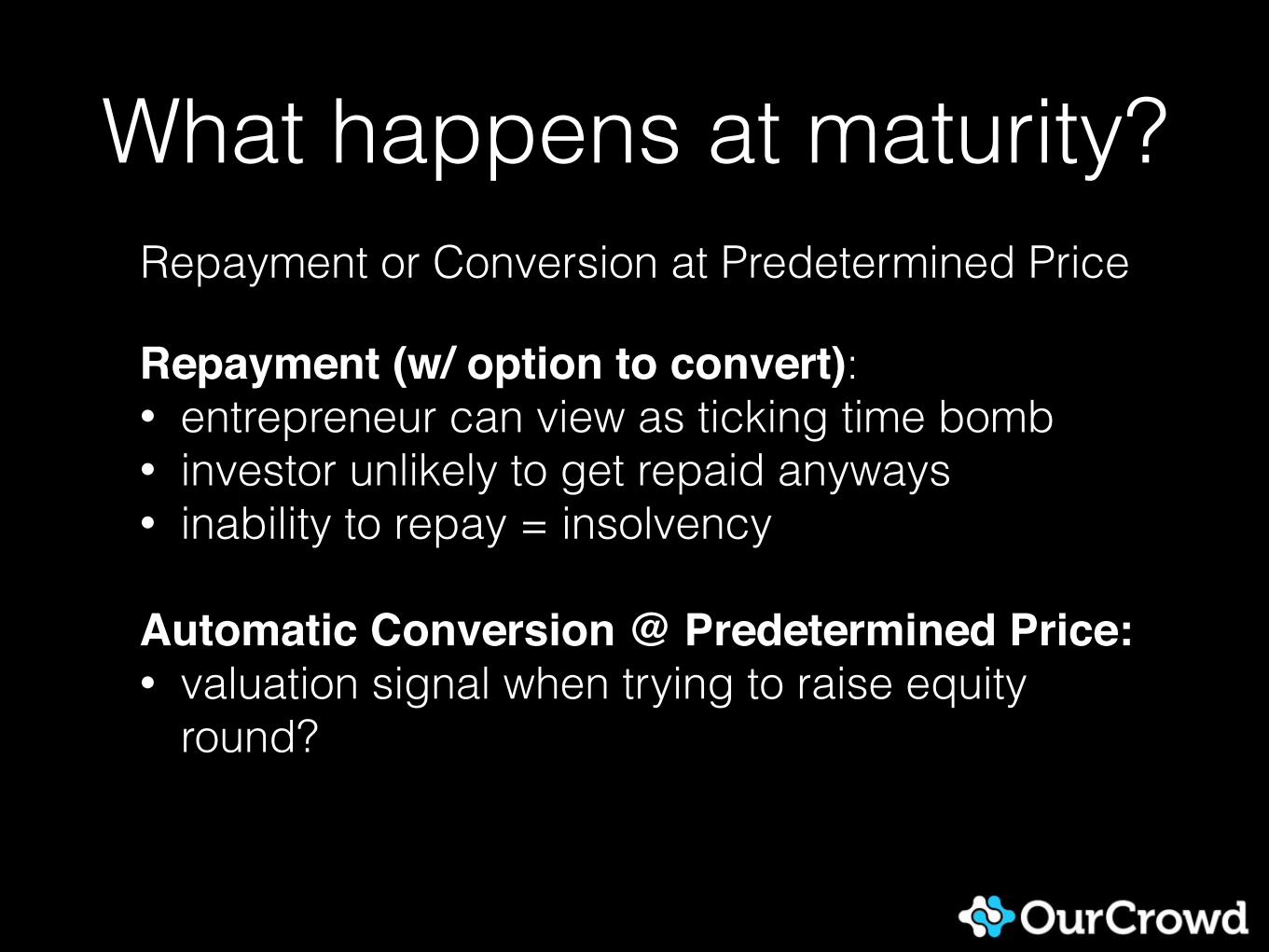

What happens at maturity?

What happens at maturity?Repayment or Conversion at Predetermined Price

Repayment (w/ option to convert): • entrepreneur can view as ticking time bomb • investor unlikely to get repaid anyways • inability to repay = insolvency

Automatic Conversion @ Predetermined Price:• valuation signal when trying to raise equity

round?

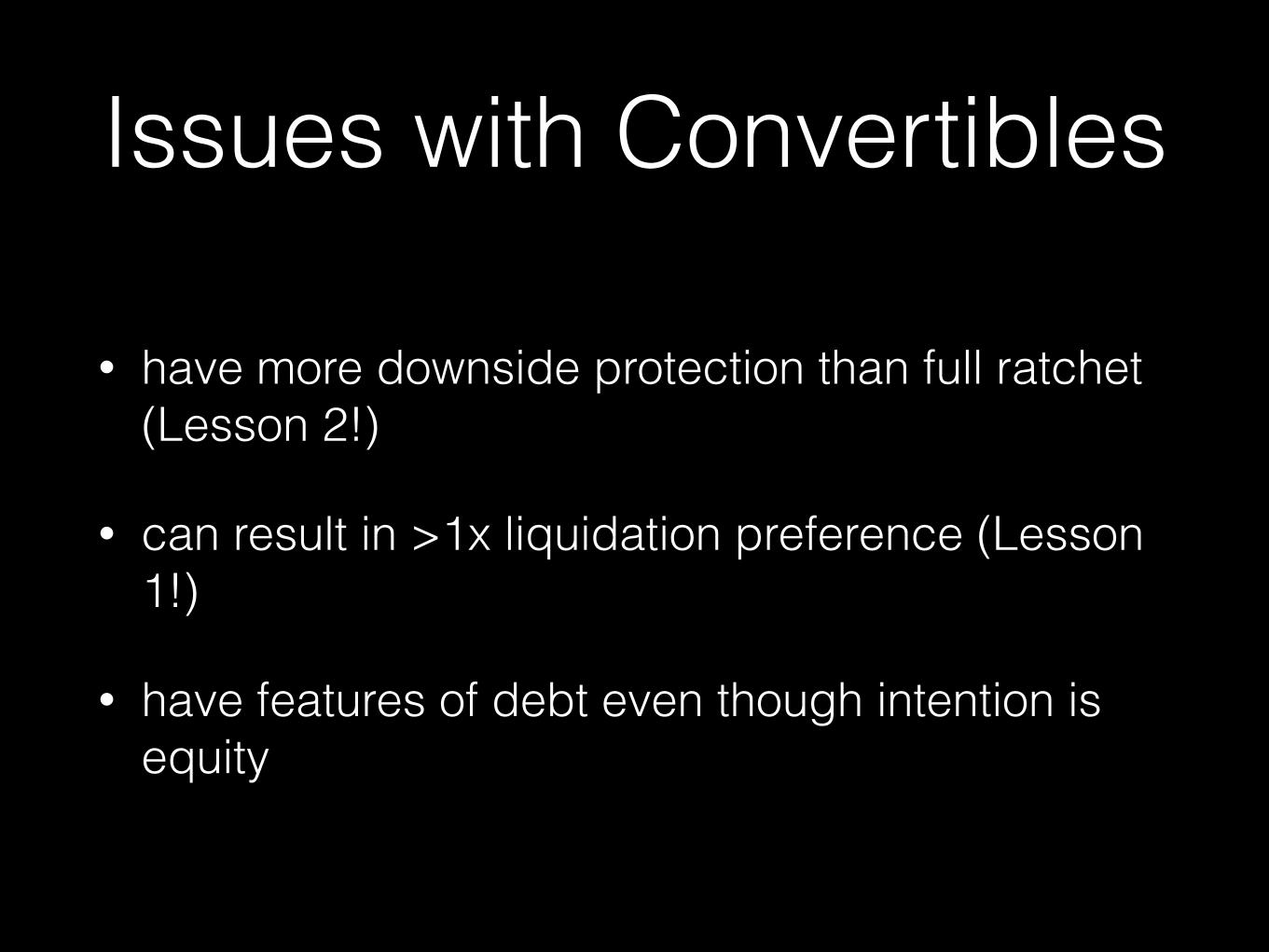

Issues with Convertibles

• have more downside protection than full ratchet (Lesson 2!)

• can result in >1x liquidation preference (Lesson 1!)

• have features of debt even though intention is equity

Alternatives

Priced Convertible

DebtFloor to go with the ceiling

SAFEs: Simple Agreement for Future Equity

SAFEs

Next step?

Thanks for joining us for our Term Sheet series

OurCrowd.com

Check out our real-life term sheets by

accrediting on our website