connectors: what we know about them and how they work?

DESCRIPTION

Connectors: What we know about them and how they work?. SCI - August 2, 2007. Agenda. How do you assess whether a Connector is what your state needs? What factors contributed to the design and functionality of the Connector in MA? - PowerPoint PPT PresentationTRANSCRIPT

Connectors: What we know about them and how they work?

SCI - August 2, 2007SCI - August 2, 2007

22

AgendaAgenda

How do you assess whether a Connector is what How do you assess whether a Connector is what your state needs?your state needs?– What factors contributed to the design and What factors contributed to the design and

functionality of the Connector in MA?functionality of the Connector in MA?– What data did MA use to think through the What data did MA use to think through the

Connector’s structure and functions?Connector’s structure and functions? Which model is right for your state? Which model is right for your state? – Massachusetts Model Massachusetts Model – Connecticut Model Connecticut Model – Washington DC ModelWashington DC Model

Implementation issues to considerImplementation issues to consider

33

DataData

Individual data (age, insurance status, Individual data (age, insurance status, employment, income, family status, health employment, income, family status, health status)status)

Employer data (average price of plan, % Employer data (average price of plan, % contribution, offer rate by size)contribution, offer rate by size)

Insurance market (number, price, type of plans Insurance market (number, price, type of plans in each market, benefit coverage)in each market, benefit coverage)

Medicaid and other public program cost and Medicaid and other public program cost and benefit databenefit data

Uncompensated Care Pool or safety net dataUncompensated Care Pool or safety net data

44

Questions to ask about insurance Questions to ask about insurance marketsmarkets

Are the nongroup and small group markets functioning Are the nongroup and small group markets functioning well?well?Is anything working well? Is anything working well? What are the barriers to entry?What are the barriers to entry?What is the product availability?What is the product availability?How many carriers are in the markets? Is there How many carriers are in the markets? Is there adequate competition?adequate competition?Is there choice, portability, flexibility?Is there choice, portability, flexibility?What is the state’s experience with adverse selection, What is the state’s experience with adverse selection, risk pooling, reinsurance?risk pooling, reinsurance?What reforms have been made to the markets in the What reforms have been made to the markets in the past? Were they successful?past? Were they successful?

55

What we learned about insurance What we learned about insurance marketsmarkets

Un-level playing field between employees of firms that don’t offer (nongroup purchase) and self-employed (small group purchase)

Little choice of product in nongroup market

No pre-tax payment for people purchasing in nongroup market

Small employers have minimum participation and contribution requirements that are barriers to entry

Very small groups are older and use more services

66

Questions to ask about the uninsured Questions to ask about the uninsured

Who are the uninsured?What does their care cost? How do they receive and pay for care?Why don’t they have health insurance?– Are they employed? Type of employment?– Are they offered insurance by employer?– If offered, why do they choose not to

purchase?What is their demographic profile?What is their health status?

77

What we learned about the uninsuredWhat we learned about the uninsuredThe uninsured are not a homogenous group; however, they are The uninsured are not a homogenous group; however, they are likely:likely:– to have been born in the U.S. to have been born in the U.S. – to be single and whiteto be single and white– to be between 25 and 64to be between 25 and 64– to have at least a high school educationto have at least a high school education– to be employed and work for small firmsto be employed and work for small firms– to have moderate incomes and reportedly willing to pay for to have moderate incomes and reportedly willing to pay for

health insurancehealth insurance– to turn down coverage when offered itto turn down coverage when offered it– to have good health status.to have good health status.

88

Questions to ask about employer Questions to ask about employer coveragecoverage

Who does and doesn’t offer? Are they dropping or likely to drop coverage?What are the barriers to offering?What benefits do they offer?How much do they subsidize?How many employees take up offer of coverage?Do they offer pre-tax payment of premium?How much choice do they have and how much choice do they provide to their employees?Do they discriminate among employees?

99

What we learned about employer What we learned about employer coveragecoverage

Employers have not been dropping coverage in MAEmployers have not been dropping coverage in MA

Many small employers who offer hi do not offer pre-tax Many small employers who offer hi do not offer pre-tax treatment of premium paymentstreatment of premium payments

Many employers have difficulty providing hi for part time Many employers have difficulty providing hi for part time workersworkers

Waiting periods have increased slightly Waiting periods have increased slightly

Most employers do not vary contribution or cost sharing by Most employers do not vary contribution or cost sharing by employee characteristicsemployee characteristics

Employers who do not offer insurance are looking for lower Employers who do not offer insurance are looking for lower cost alternativescost alternatives

Most employers do not ask for proof of coverage if Most employers do not ask for proof of coverage if employees turn down coverageemployees turn down coverage

1010

Different models Different models

Massachusetts – combine market forces Massachusetts – combine market forces with public subsidieswith public subsidies

ConnecticutConnecticut

Washington DCWashington DC

1111

Medicaid

Cost/QualityImprovements

CommonwealthCare

InsuranceReforms

SharedResponsibility

ConnectorAuthority

MassachusettsHealth Care Reform

1212

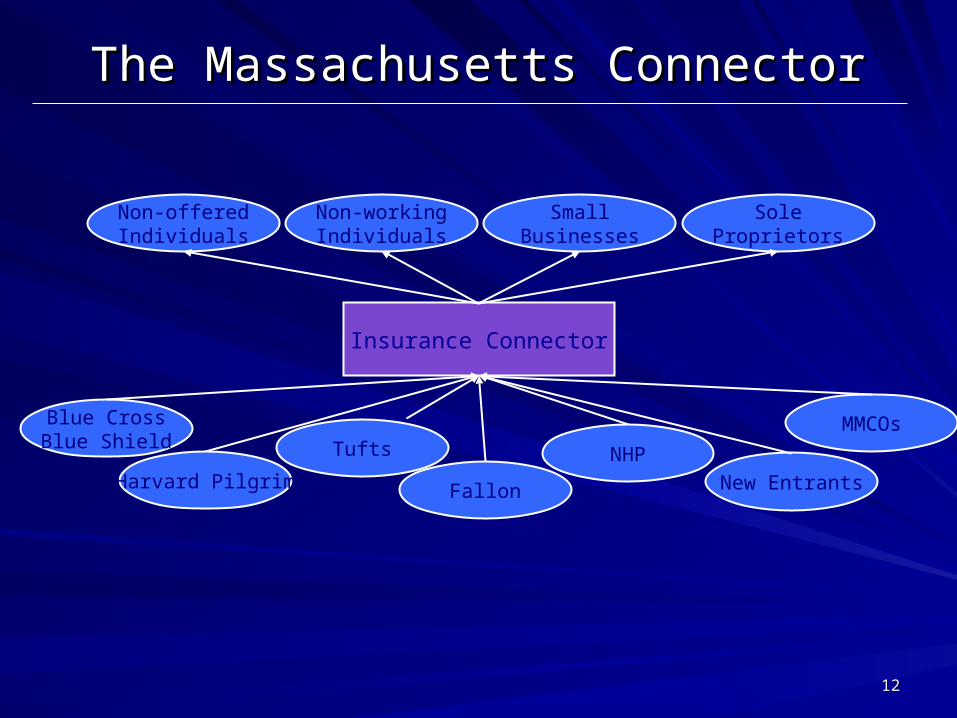

Non-offeredIndividuals

SmallBusinesses

SoleProprietors

Non-workingIndividuals

Blue CrossBlue Shield

FallonHarvard Pilgrim

Insurance Connector

The Massachusetts Connector The Massachusetts Connector

New Entrants

MMCOsTufts NHP

1313

Former governor’s vision for the Connector

Nexus between buyers and sellers Nexus between buyers and sellers – Premiums paid with pre-tax dollars (125 Cafeteria Premiums paid with pre-tax dollars (125 Cafeteria

Plan)Plan)– Facilitate premium assistance for 100-300% FPL Facilitate premium assistance for 100-300% FPL

Mechanism for reaching non-traditional workersMechanism for reaching non-traditional workers– Part-timers and seasonal workersPart-timers and seasonal workers– Contractors and sole-proprietorsContractors and sole-proprietors– Spouses with two employers wanting to contribute Spouses with two employers wanting to contribute

towards family plantowards family plan– Individuals with more than one jobIndividuals with more than one job

Alternative distribution systemAlternative distribution systemPromotes shift to defined contributionPromotes shift to defined contribution

1414

Business detailsBusiness details

Serves small businesses and individualsServes small businesses and individualsOffers subsidized and nonsubsidized plansOffers subsidized and nonsubsidized plansEligibility: firms up to 50, individuals without Eligibility: firms up to 50, individuals without access to subsidized coverageaccess to subsidized coverage7 health plans types offered by 6 carriers7 health plans types offered by 6 carriersStandard benefits with consumer choice: price Standard benefits with consumer choice: price (cost sharing and premiums, network, (cost sharing and premiums, network, formulariesformularies

1515

ChallengesChallenges

Some really wanted purchasing poolSome really wanted purchasing pool

Final legislation did not allow as much flexibility in Final legislation did not allow as much flexibility in product design as we would have likedproduct design as we would have liked

Open meetingsOpen meetings

Ambitious timelines Ambitious timelines

Change in administration Change in administration

Tension between the “business plan” of connector Tension between the “business plan” of connector and regulatory authorityand regulatory authority– Defining affordabilityDefining affordability

– Defining minimum creditable coverageDefining minimum creditable coverage

1616

Different models Different models

MassachusettsMassachusetts

Connecticut – employee choice pool with Connecticut – employee choice pool with full HR functionalityfull HR functionality

Washington DCWashington DC

1717

BusinessBusinessPartners &Partners &CustomersCustomers

RequestRequestMediumsMediums

CBIACBIA

CarriersCarriers

AgentsAgentsAgentsAgents

EmployersEmployersEmployersEmployers

EmployeesEmployeesEmployeesEmployees

E-MailE-MailE-MailE-Mail

PaperPaperPaperPaper

WebWebWebWeb

PhonePhonePhonePhone

FaxFaxFaxFax

ContactContactManagemtManagemt

Billing &Billing &AdminAdmin

Health Health PlansPlans

Health Health PlansPlans

AncillaryAncillaryCarriersCarriers

AncillaryAncillaryCarriersCarriers

CustomerCustomerServiceService

CustomerCustomerServiceService

DataData EntryEntry

DataData EntryEntry

AgentAgentRepsReps

AgentAgentRepsReps

Action & Follow-upAction & Follow-up

Request CoordinationRequest Coordination

CBIA HC administration

WorkflowWorkflow

1818

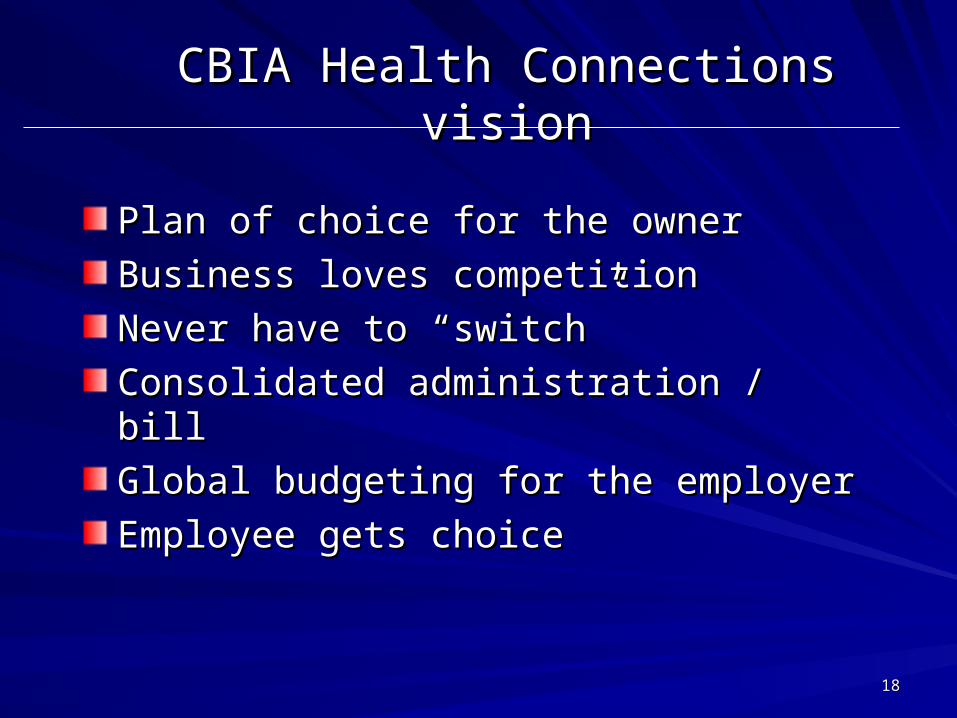

CBIA Health Connections visionCBIA Health Connections vision

Plan of choice for the owner Plan of choice for the owner

Business loves competitionBusiness loves competition

Never have to “switch” Never have to “switch”

Consolidated administration / billConsolidated administration / bill

Global budgeting for the employerGlobal budgeting for the employer

Employee gets choiceEmployee gets choice

1919

Business detailsBusiness details

Serves small businessesServes small businesses

6000 companies, 88,000 members6000 companies, 88,000 members

Eligibility: firms of 3-100Eligibility: firms of 3-100

4 health plans with up to 38 options4 health plans with up to 38 options

Standard benefits with consumer choice: price, Standard benefits with consumer choice: price, network, formulariesnetwork, formularies

2020

Why HC works in the private sectorWhy HC works in the private sector

Common benefits (standardized but not exact)Common benefits (standardized but not exact)Private sector approach: businesses wary of Private sector approach: businesses wary of government involvementgovernment involvementOther services (Life, STD, LTD, Dental, COBRA, Other services (Life, STD, LTD, Dental, COBRA, Section 125, HRA’s, HSA’s)Section 125, HRA’s, HSA’s)Ability to change and adapt quicklyAbility to change and adapt quicklyUtilization management and reportingUtilization management and reportingWellness initiativesWellness initiativesCommunicationsCommunications

2121

ChallengesChallenges

Rapidly changing marketplaceRapidly changing marketplace

Cost PressuresCost Pressures

Legislative ChallengesLegislative Challenges

Consolidation of Health PlansConsolidation of Health Plans

Consumer Driven OptionsConsumer Driven Options

Wellness / LifestyleWellness / Lifestyle

2222

Different models Different models

MassachusettsMassachusetts

ConnecticutConnecticut

Washington DC – full market reform – Washington DC – full market reform – health insurance is an individual purchasehealth insurance is an individual purchase

2323

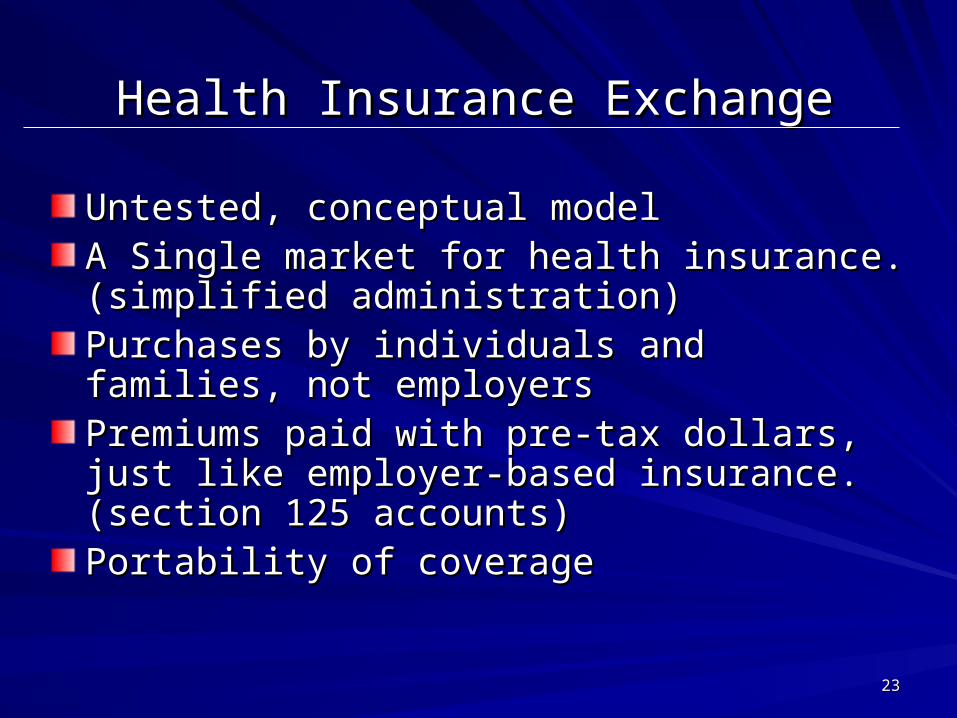

Health Insurance ExchangeHealth Insurance Exchange

Untested, conceptual modelUntested, conceptual modelA Single market for health insurance. (simplified A Single market for health insurance. (simplified administration)administration)Purchases by individuals and families, not Purchases by individuals and families, not employersemployersPremiums paid with pre-tax dollars, just like Premiums paid with pre-tax dollars, just like employer-based insurance. (section 125 employer-based insurance. (section 125 accounts) accounts) Portability of coveragePortability of coverage

2424

Implementation issuesImplementation issues

Number of plansNumber of plans

Coverage requirementsCoverage requirements

Underwriting/rating rulesUnderwriting/rating rules

Risk managementRisk management

EligibilityEligibility

FunctionalityFunctionality

Thorny issues (COBRA, HIPAA, ERISA)Thorny issues (COBRA, HIPAA, ERISA)