complete thesis - ruchi sagarshodhganga.inflibnet.ac.in/bitstream/10603/45020/13/13...136 mahila...

TRANSCRIPT

134

CHAPTER 5

THE PATTERN OF UTILISATION OF LOANS

5.1 INTRODUCTION

Microfinance has made great

to financial services and developing ways to overcome these barriers. It is assumed

the household and the access to income for both production and consumption.

particularly with that of children. In this context the present chapter examines the

borrowing behaviour of the respondents. The saving as well as borrowing activity has

multiple aspects. It initiates the process of bringing up the households above their

subsistence level living. The process is rather gradual but it certainly indicates that

this activity has tremendous potential.

This chapter brings forth the utilisation of SHG loans by the respondents, analyses the

relation between various socio-economic indicators like income of the respondents

and their families, education levels, working status, age etc. with the loan utilisation

patterns of the respondents. The utilisation pattern has revealed very interesting

aspects about the role played by the SHGs in the livelihoods of their members. The

major part of the total loans advanced by the groups was for fulfilling their

consumption requirements. However, some of the women have shown enterprising

spirit. These women have not only used the loans for their consumption requirements

135

but they also moved on to gain more stability into their lives. They have taken loans

for various kinds of income generating activities which they have been pursuing to

support their families.

5.2 BORROWING STATUS OF WOMEN

The present section examines the total number of respondents who borrowed from the

groups and the amount of loans availed by them. It also analyses the frequency of

borrowings by the respondents.

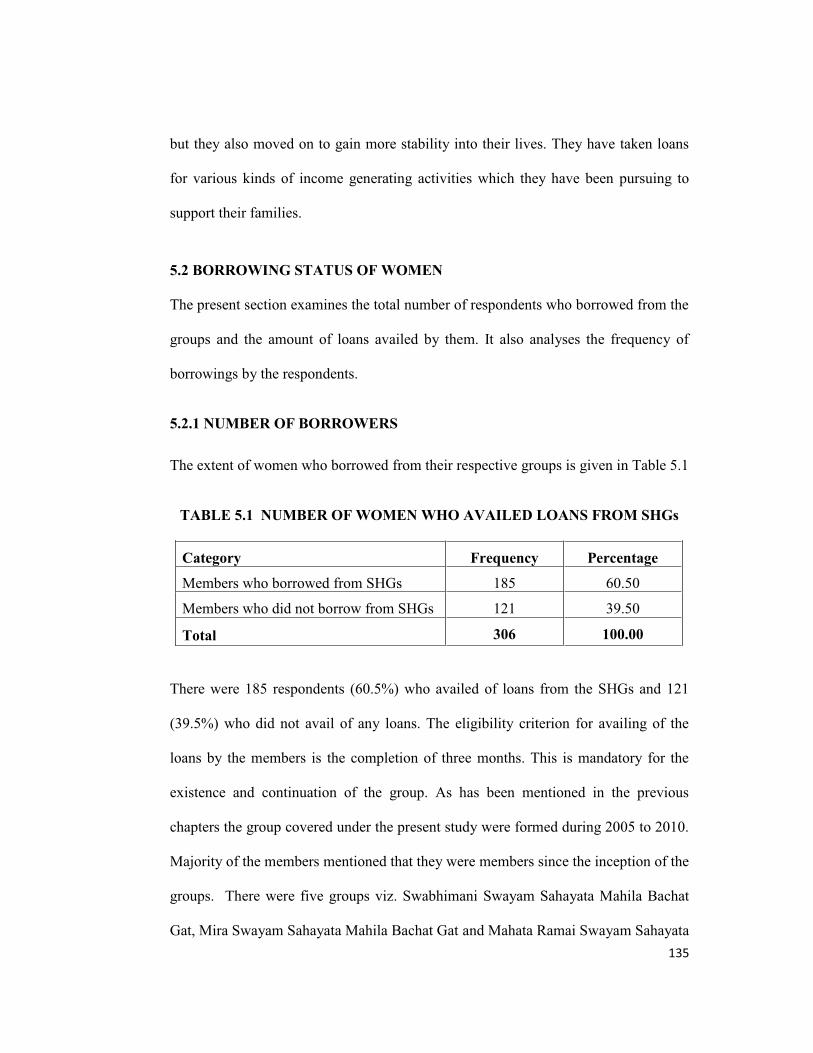

5.2.1 NUMBER OF BORROWERS

The extent of women who borrowed from their respective groups is given in Table 5.1

TABLE 5.1 NUMBER OF WOMEN WHO AVAILED LOANS FROM SHGs

Category Frequency Percentage

Members who borrowed from SHGs 185 60.50

Members who did not borrow from SHGs 121 39.50

Total 306 100.00

There were 185 respondents (60.5%) who availed of loans from the SHGs and 121

(39.5%) who did not avail of any loans. The eligibility criterion for availing of the

loans by the members is the completion of three months. This is mandatory for the

existence and continuation of the group. As has been mentioned in the previous

chapters the group covered under the present study were formed during 2005 to 2010.

Majority of the members mentioned that they were members since the inception of the

groups. There were five groups viz. Swabhimani Swayam Sahayata Mahila Bachat

Gat, Mira Swayam Sahayata Mahila Bachat Gat and Mahata Ramai Swayam Sahayata

136

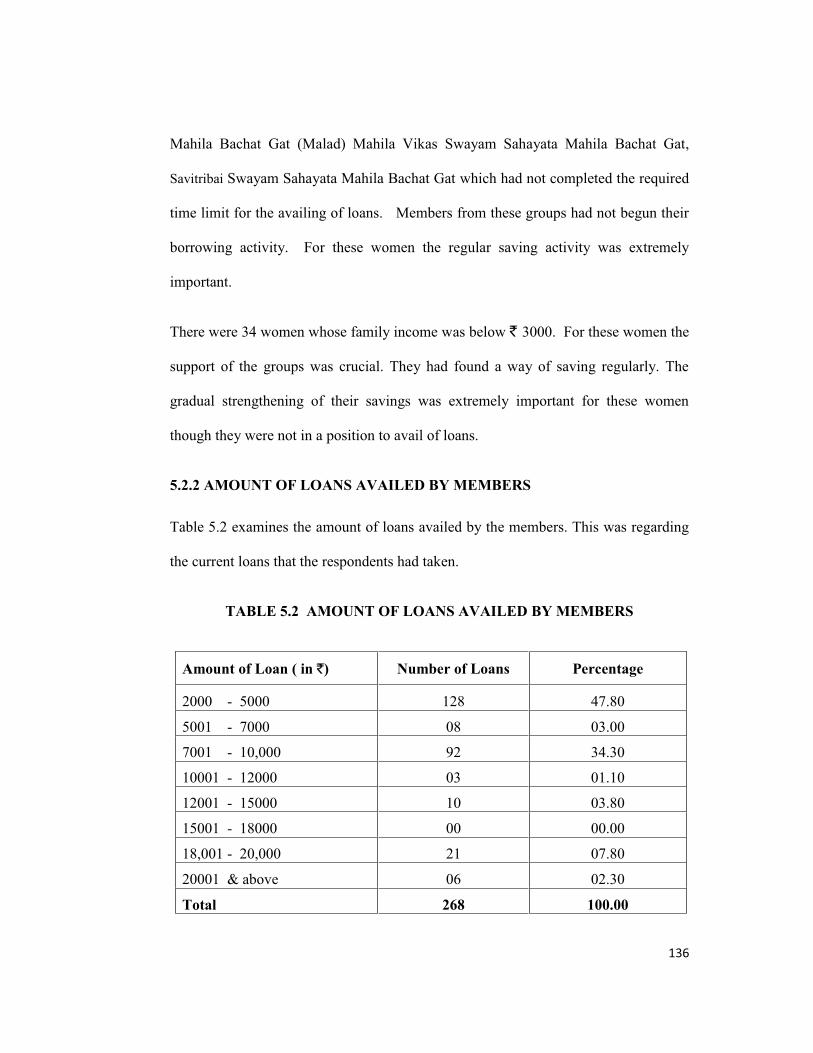

Mahila Bachat Gat (Malad) Mahila Vikas Swayam Sahayata Mahila Bachat Gat,

Savitribai Swayam Sahayata Mahila Bachat Gat which had not completed the required

time limit for the availing of loans. Members from these groups had not begun their

borrowing activity. For these women the regular saving activity was extremely

important.

There were 34 women whose family income was below ` 3000. For these women the

support of the groups was crucial. They had found a way of saving regularly. The

gradual strengthening of their savings was extremely important for these women

though they were not in a position to avail of loans.

5.2.2 AMOUNT OF LOANS AVAILED BY MEMBERS

Table 5.2 examines the amount of loans availed by the members. This was regarding

the current loans that the respondents had taken.

TABLE 5.2 AMOUNT OF LOANS AVAILED BY MEMBERS

Amount of Loan ( in `) Number of Loans Percentage

2000 - 5000 128 47.80

5001 - 7000 08 03.00

7001 - 10,000 92 34.30

10001 - 12000 03 01.10

12001 - 15000 10 03.80

15001 - 18000 00 00.00

18,001 - 20,000 21 07.80

20001 & above 06 02.30

Total 268 100.00

137

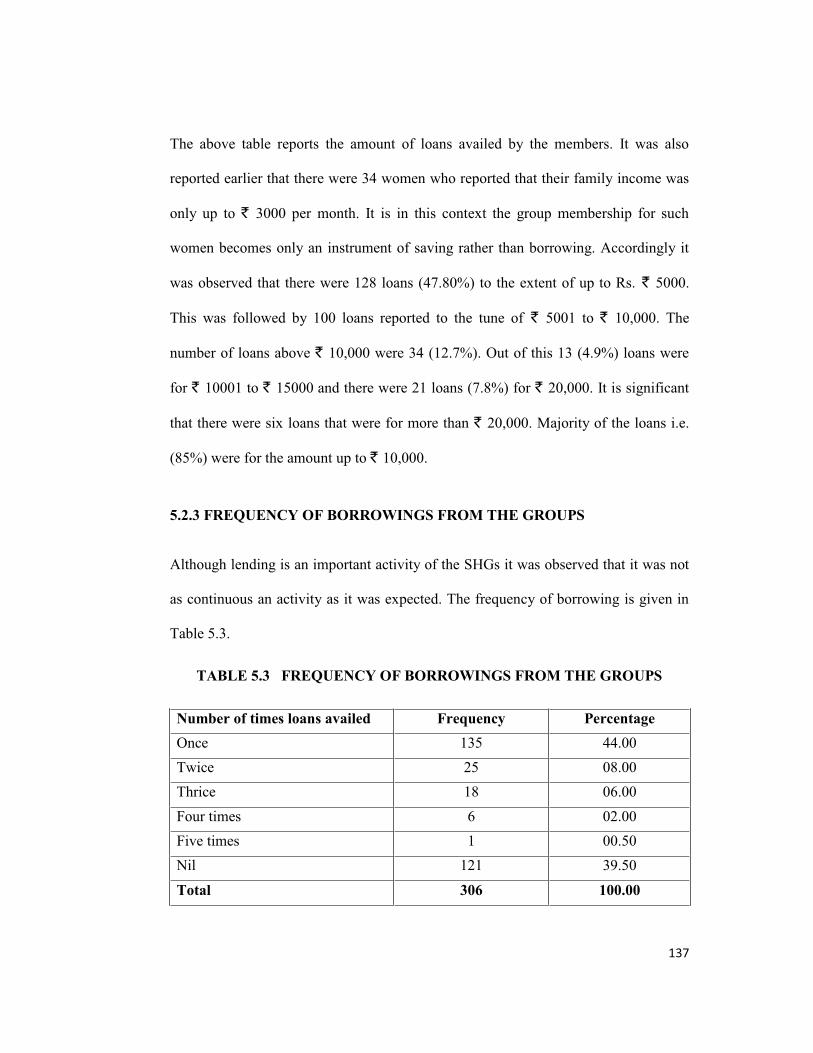

The above table reports the amount of loans availed by the members. It was also

reported earlier that there were 34 women who reported that their family income was

only up to ` 3000 per month. It is in this context the group membership for such

women becomes only an instrument of saving rather than borrowing. Accordingly it

was observed that there were 128 loans (47.80%) to the extent of up to Rs. ` 5000.

This was followed by 100 loans reported to the tune of ` 5001 to ` 10,000. The

number of loans above ` 10,000 were 34 (12.7%). Out of this 13 (4.9%) loans were

for ` 10001 to ` 15000 and there were 21 loans (7.8%) for ` 20,000. It is significant

that there were six loans that were for more than ` 20,000. Majority of the loans i.e.

(85%) were for the amount up to ` 10,000.

5.2.3 FREQUENCY OF BORROWINGS FROM THE GROUPS

Although lending is an important activity of the SHGs it was observed that it was not

as continuous an activity as it was expected. The frequency of borrowing is given in

Table 5.3.

TABLE 5.3 FREQUENCY OF BORROWINGS FROM THE GROUPS

Number of times loans availed Frequency Percentage

Once 135 44.00

Twice 25 08.00

Thrice 18 06.00

Four times 6 02.00

Five times 1 00.50

Nil 121 39.50

Total 306 100.00

138

There were 185 respondents who borrowed from the groups. The largest number of

borrowers i.e. 135 respondents had borrowed only once from their respective groups.

There were 25 respondents who had borrowed twice and 18 respondents who had

borrowed three times. The number of respondents who borrowed more than three

times was only seven. While six respondents had borrowed four times only one

respondent had borrowed five times. There were 121 respondents who did not borrow

even once. These were the women who had focused on the strengthening of their

savings. The reason largely for not availing of loans was because of the low capacity

to repay the loans. Also some of the members belonged to the newly formed groups

so they could not borrow. Frequency of borrowing was mainly related to the maturity

of the groups. Members belonging to older groups borrowed more frequently.

5.3 UTILISATION OF THE LOANS

The various aspects of utilisation of loans such as the purpose of borrowing,

relationship between the purpose of loan and the frequency of the borrowing, working

status of respondents, age of the respondents, their educational levels etc. have been

discussed in the present section.

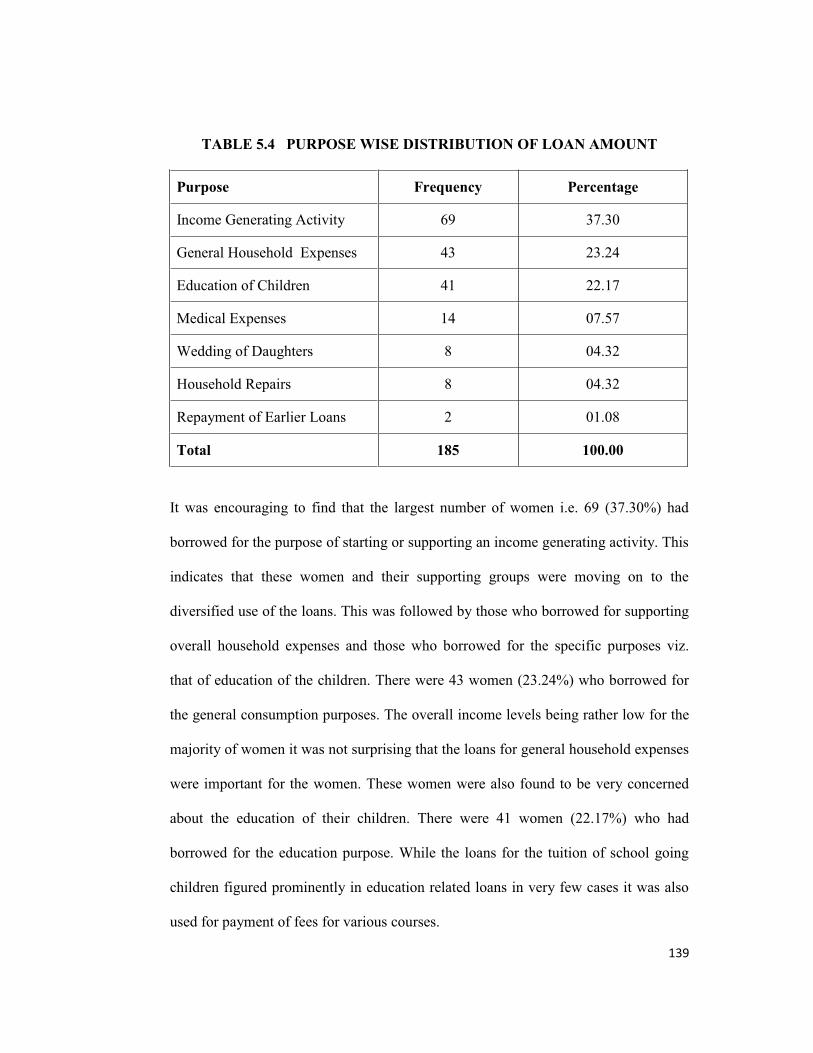

5.3.1 PURPOSE WISE DISTRIBUTION OF LOANS

Table 5.4 gives information on the purpose of borrowing and the number of

respondents availing loans for the specified purpose. Since loans could be for more

than one purpose, the purpose with largest amount has been taken as the main reason

of borrowing. It was observed that the loans for the general household expenses were

availed by those members who had borrowed more than once from the groups.

139

TABLE 5.4 PURPOSE WISE DISTRIBUTION OF LOAN AMOUNT

Purpose Frequency Percentage

Income Generating Activity 69 37.30

General Household Expenses 43 23.24

Education of Children 41 22.17

Medical Expenses 14 07.57

Wedding of Daughters 8 04.32

Household Repairs 8 04.32

Repayment of Earlier Loans 2 01.08

Total 185 100.00

It was encouraging to find that the largest number of women i.e. 69 (37.30%) had

borrowed for the purpose of starting or supporting an income generating activity. This

indicates that these women and their supporting groups were moving on to the

diversified use of the loans. This was followed by those who borrowed for supporting

overall household expenses and those who borrowed for the specific purposes viz.

that of education of the children. There were 43 women (23.24%) who borrowed for

the general consumption purposes. The overall income levels being rather low for the

majority of women it was not surprising that the loans for general household expenses

were important for the women. These women were also found to be very concerned

about the education of their children. There were 41 women (22.17%) who had

borrowed for the education purpose. While the loans for the tuition of school going

children figured prominently in education related loans in very few cases it was also

used for payment of fees for various courses.

140

The remaining 32 women (17.29%) borrowed for various other purposes. These were

the contingencies which the households have to face frequently. There were 14

women (7.57%) who had borrowed on account of medical contingency. There were

eight women who had borrowed for wedding expenses and the other eight women

borrowed for undertaking household repairs. There were only two women who

borrowed to repay the earlier loans.

Almost all the loans other than those taken for the income generating activities were

for the important phases in the life cycle. Some of the requirements were unexpected

such as the medical expenses whereas some of them were expected ones like

education and marriage expenses. These loans were extremely important to the

women as in the absence of them they would have had to go to the money lenders and

consequently would have become indebted for an unspecified period of life. These

loans were a kind of much needed safety nets for the women.

5.3.2 LOANS FROM SHGS AND FROM SOURCES OTHER THAN SHGs

It was observed that there were some members who borrowed from SHGs as well as

from other sources. Table 5.5 gives the information on the extent of borrowing from

SHGs as well as from other sources.

TABLE 5.5 LOANS TAKEN FROM SHGs AND OTHER SOURCES

Category No. of Women Percentage

Those who availed loans only

from SHGs 151 81.62

Those who availed from SHGs and

other sources 34 18.38

Total 185 100.00

141

What needs to be noted here is that 34 (18.38%) women who had to borrow from

other sources had also borrowed from their respective SHGs. Thus they were also

part of the number of women who borrowed from SHGs. The SHGs had their own

policy in disbursing the loans. If the SHGs could not sanction loans for these

members, they had to borrow from other sources. For 151 women (81.62%) SHGs

were the only source.

5.3.3 COMPARATIVE ANALYSIS BETWEEN THE UTILISATION OF

LOANS TAKEN FROM SHGs AND LOANS TAKEN FOM OTHER

SOURCES

The present section undertakes the comparative analysis of the utilisation of loans

taken from SHGs and from other sources.

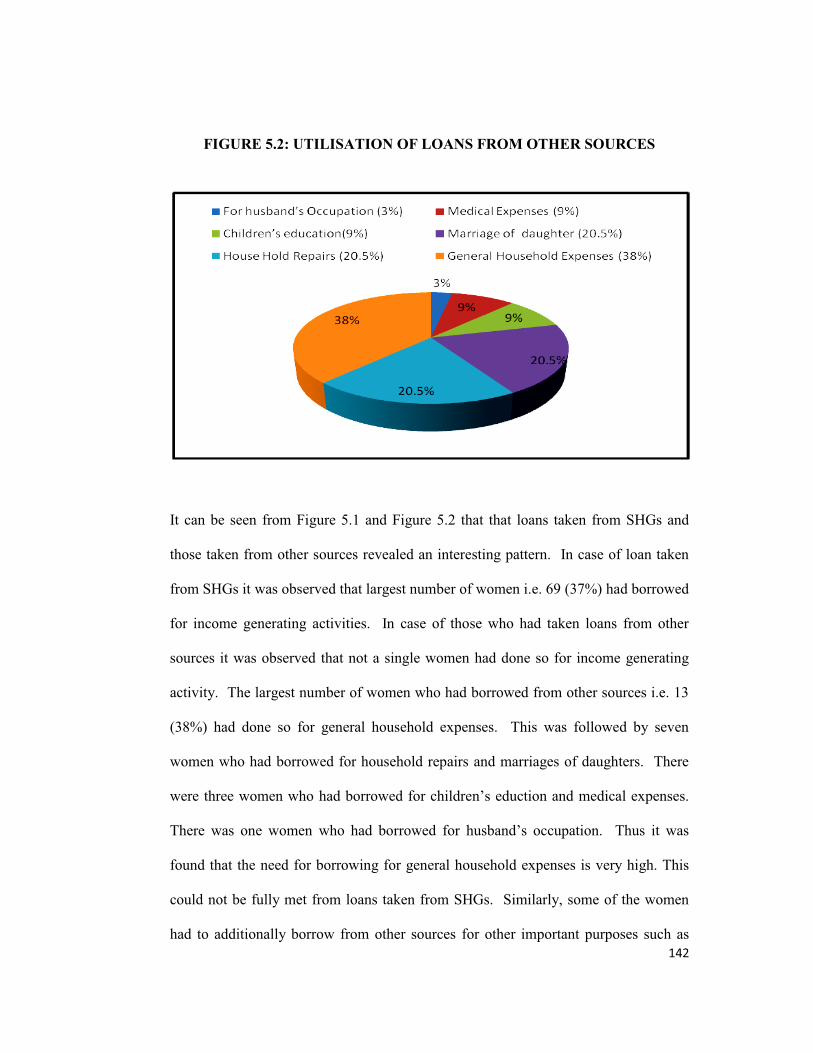

FIGURE 5.1: UTILISATION OF LOANS FROM SHGs

142

FIGURE 5.2: UTILISATION OF LOANS FROM OTHER SOURCES

It can be seen from Figure 5.1 and Figure 5.2 that that loans taken from SHGs and

those taken from other sources revealed an interesting pattern. In case of loan taken

from SHGs it was observed that largest number of women i.e. 69 (37%) had borrowed

for income generating activities. In case of those who had taken loans from other

sources it was observed that not a single women had done so for income generating

activity. The largest number of women who had borrowed from other sources i.e. 13

(38%) had done so for general household expenses. This was followed by seven

women who had borrowed for household repairs and marriages of daughters. There

There was one women who had bor

found that the need for borrowing for general household expenses is very high. This

could not be fully met from loans taken from SHGs. Similarly, some of the women

had to additionally borrow from other sources for other important purposes such as

143

education. SHGs still have to go a long way to completely eliminate the needs of

their member to borrow from other sources.

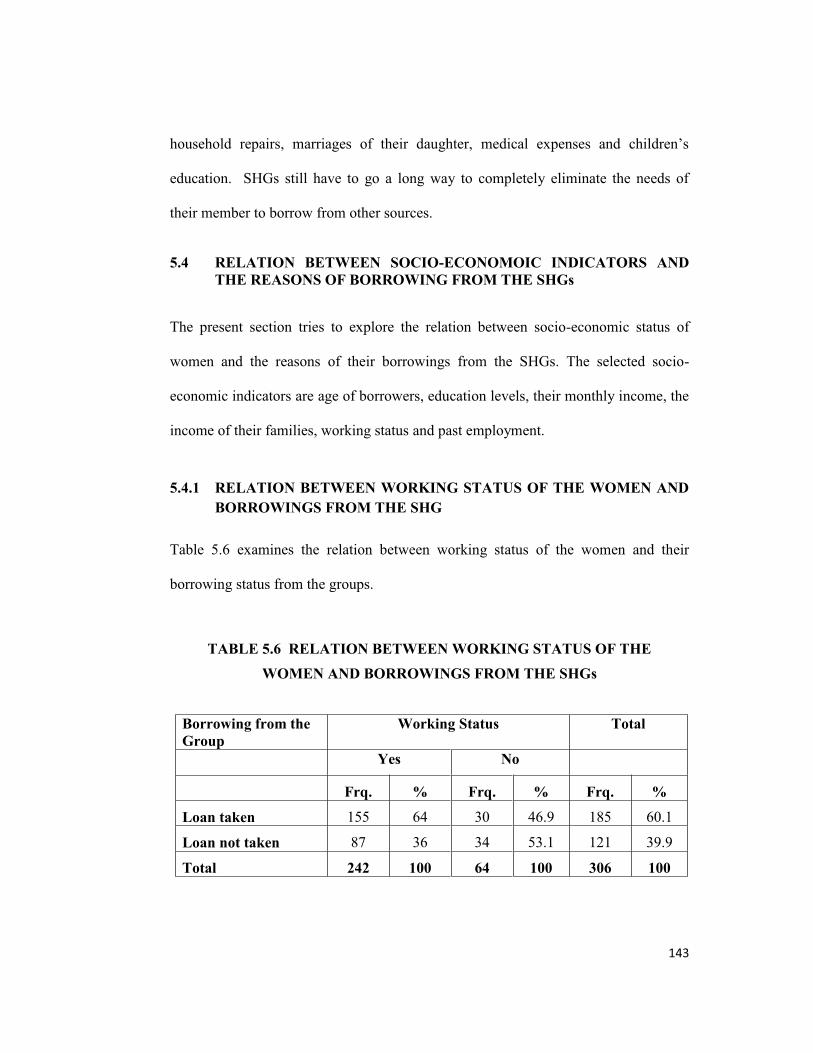

5.4 RELATION BETWEEN SOCIO-ECONOMOIC INDICATORS AND

THE REASONS OF BORROWING FROM THE SHGs

The present section tries to explore the relation between socio-economic status of

women and the reasons of their borrowings from the SHGs. The selected socio-

economic indicators are age of borrowers, education levels, their monthly income, the

income of their families, working status and past employment.

5.4.1 RELATION BETWEEN WORKING STATUS OF THE WOMEN AND

BORROWINGS FROM THE SHG

Table 5.6 examines the relation between working status of the women and their

borrowing status from the groups.

TABLE 5.6 RELATION BETWEEN WORKING STATUS OF THE

WOMEN AND BORROWINGS FROM THE SHGs

Borrowing from the

Group

Working Status Total

Yes No

Frq. % Frq. % Frq. %

Loan taken 155 64 30 46.9 185 60.1

Loan not taken 87 36 34 53.1 121 39.9

Total 242 100 64 100 306 100

144

From Table 5.6 it can be seen that 242 women were working. As had been reported

earlier these women were largely domestic workers, anganwadi helpers and petty

vendors. There were 155 working women who had availed of loans. But there was

also a significant number of working women i.e. 87 who did not borrow from the

groups. There were 64 women who reported that they were not engaged in any work.

Out of this 30 women had availed of loans and 34 women did not take any loans. It

indicates that the working status did not have any significant relationship with the

borrowing status of the respondents. Those women who were not working had to

depend on the earning members of their household to contribute to the savings.

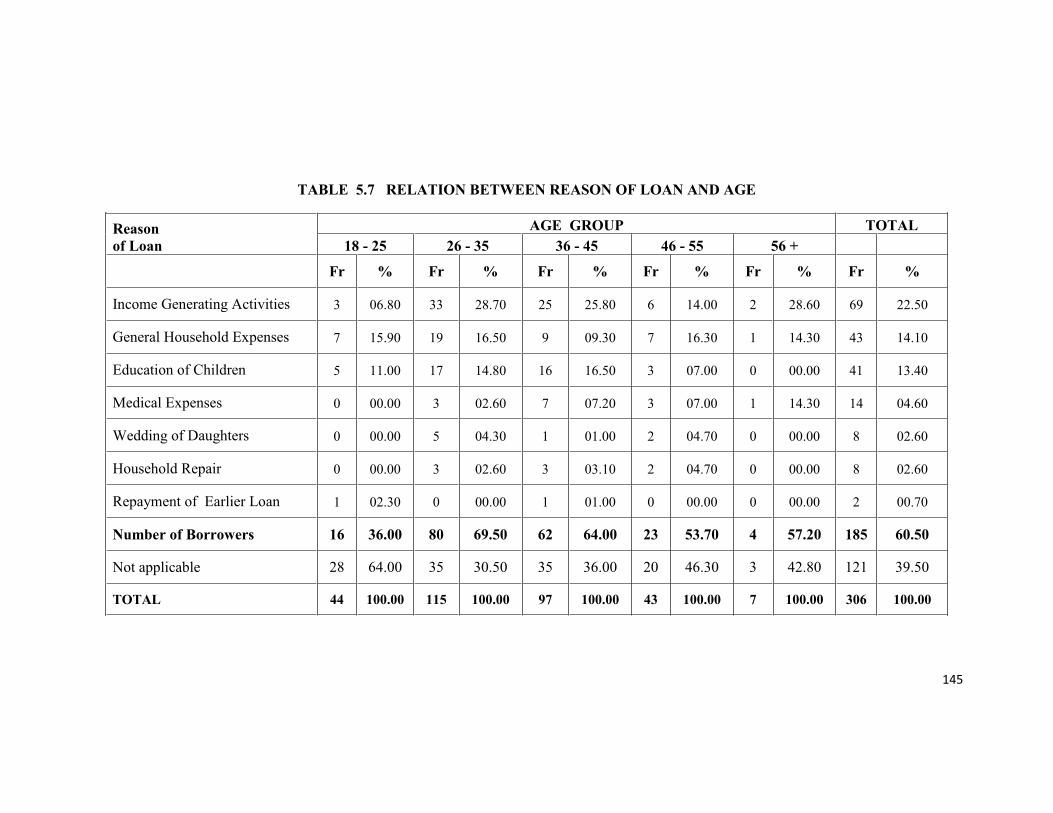

5.4.2 RELATION BETWEEN REASON OF LOAN AND AGE

Table 5.7 presents the relationship between the reason of SHG loans and the age of

respondents.

This table brings out an interesting relationship between the age of the respondents

and the purpose of borrowing. It was observed that the largest number of borrowers

i.e. 80 (43.24%) were in the age group of 26 35 years. This was followed by 62

women (33.51%) who were in the age group of 36 to 45 years. Thus there were 142

borrowers (76.75%) who were in the age group of 26 45 years. Among the

remaining borrowers 23 (12.43%) were in the higher age group of 46 55 years and

16 borrowers (8.65%) in the youngest age group of 18 25 years. There were only

four borrowers in the oldest age group of 56 years and above.

145

TABLE 5.7 RELATION BETWEEN REASON OF LOAN AND AGE

Reason

of Loan

AGE GROUP TOTAL

18 - 25 26 - 35 36 - 45 46 - 55 56 +

Fr % Fr % Fr % Fr % Fr % Fr %

Income Generating Activities 3 06.80 33 28.70 25 25.80 6 14.00 2 28.60 69 22.50

General Household Expenses 7 15.90 19 16.50 9 09.30 7 16.30 1 14.30 43 14.10

Education of Children 5 11.00 17 14.80 16 16.50 3 07.00 0 00.00 41 13.40

Medical Expenses 0 00.00 3 02.60 7 07.20 3 07.00 1 14.30 14 04.60

Wedding of Daughters 0 00.00 5 04.30 1 01.00 2 04.70 0 00.00 8 02.60

Household Repair 0 00.00 3 02.60 3 03.10 2 04.70 0 00.00 8 02.60

Repayment of Earlier Loan 1 02.30 0 00.00 1 01.00 0 00.00 0 00.00 2 00.70

Number of Borrowers 16 36.00 80 69.50 62 64.00 23 53.70 4 57.20 185 60.50

Not applicable 28 64.00 35 30.50 35 36.00 20 46.30 3 42.80 121 39.50

TOTAL 44 100.00 115 100.00 97 100.00 43 100.00 7 100.00 306 100.00

146

There were 44 women in the youngest age group of 18-25 years. There were 16

women who had availed loans from this age group. They had mainly borrowed for

consumption needs followed by education, income generating activities and the

repayment of earlier loans.

Out of 115 women in the age group of 26-35 years, 80 women had availed of loans

and large number of them i.e. 33 women had borrowed for income generating activity.

There were 19 and 17 women who had borrowed for consumption and educational

needs respectively. The remaining 11 women borrowed for marriage, medical

expenses and repairing of the house.

Out of 97 women in the age group of 36-45 years there were 62 women who had

availed of loans. In this age group also as in the case of the age group 26-35 years

largest number of borrowers had taken loans for income generating activity. This was

followed by 16 women who had borrowed for education purpose. Remaining

21women had borrowed for consumption (9), medical expenses (7), repairing of the

house (3), marriage (1), repayment of previous loan (1).

Out of 43 women in the age group of 46-55 years, largest number borrowed for

consumption purposes. This was closely followed by six women who borrowed for

income generating activities. The remaining 10 women were all spread out in

borrowing for education (3), medical expenses (3), marriage (2), and house repair (2).

There were only seven women in the age group of 56 years and above. Out of these

four women had taken loans. There were two women from this category who

147

borrowed for income generating activities and one each had taken loans for

consumption and medical expenses respectively.

It was observed that borrowing for income generating activity figured prominently for

each of the age groups. This was followed by consumption needs and educational

expenses.

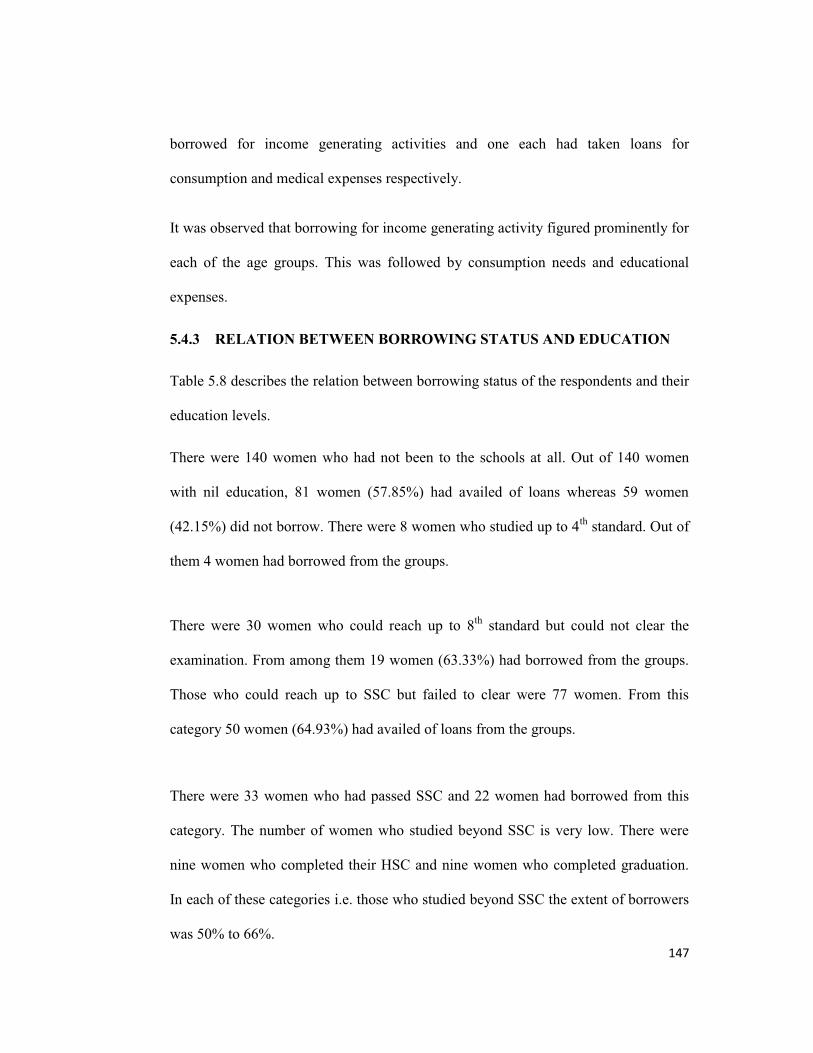

5.4.3 RELATION BETWEEN BORROWING STATUS AND EDUCATION

Table 5.8 describes the relation between borrowing status of the respondents and their

education levels.

There were 140 women who had not been to the schools at all. Out of 140 women

with nil education, 81 women (57.85%) had availed of loans whereas 59 women

(42.15%) did not borrow. There were 8 women who studied up to 4th

standard. Out of

them 4 women had borrowed from the groups.

There were 30 women who could reach up to 8th

standard but could not clear the

examination. From among them 19 women (63.33%) had borrowed from the groups.

Those who could reach up to SSC but failed to clear were 77 women. From this

category 50 women (64.93%) had availed of loans from the groups.

There were 33 women who had passed SSC and 22 women had borrowed from this

category. The number of women who studied beyond SSC is very low. There were

nine women who completed their HSC and nine women who completed graduation.

In each of these categories i.e. those who studied beyond SSC the extent of borrowers

was 50% to 66%.

148

TABLE 5.8 RELATION BETWEEN BORROWING STATUS AND EDUCATION

Loan taken

or not Nil

Up to 4th

Up to 8th

Up to SSC SSC HSC Graduate TOTAL

Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. %

Loan taken 81 57.85 4 50.00 19 63.33 50 64.93 22 66.70 5 55.60 6 66.70 185 60.50

Loan Not taken 59 42.14 4 50.00 11 36.67 27 35.07 11 33.30 4 44.40 3 33.30 121 39.50

Total 140 100.00 8 100.00 30 100.00 77 100.00 33 100.00 9 100.00 9 100.00 306 100.00

147

149

At each level of education from up to 4th

Standard till the graduate level it was found

that the number of women who had taken loans was more than those who had not

availed of loans. This was so even for illiterate women. Overall it was observed that

the extent of borrowers across the different categories of educational levels ranged

from 50% to 66%.

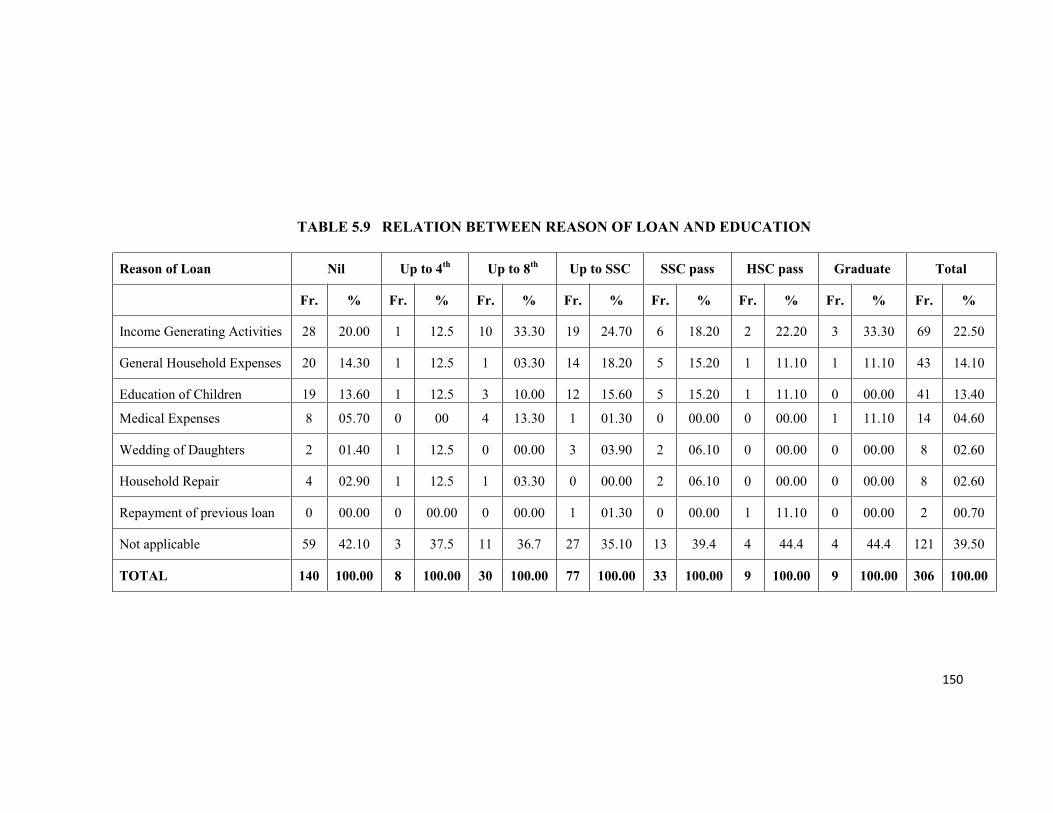

5.4.4 RELATION BETWEEN REASON OF LOAN AND EDUCATION

Table 5.9 examines the relation between purpose of borrowing and the education

levels of the respondents.

This table explains that out of 140 women who were illiterate 81 women had

borrowed from their groups. The largest number of women i.e. 28 had taken the loans

for income generating activities. This was closely followed by the number of

borrowers for consumption purposes (20) as well as for education (19). The remaining

14 women borrowed for medical purposes (8), house repairing (4) and marriage

expenses (2).

In case of women who studied up to 4th

standard one each borrowed for marriage

expenses, education, house repair, consumption and income generating activity.

In case of respondents who studied up to 8th

standard it was found that the majority

i.e. 10 women borrowed for income generating activities whereas remaining women

borrowed for medical expenses (4), education (3), house repair (1) and

consumption (1).

150

TABLE 5.9 RELATION BETWEEN REASON OF LOAN AND EDUCATION

Reason of Loan Nil Up to 4th

Up to 8th

Up to SSC SSC pass HSC pass Graduate Total

Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. %

Income Generating Activities 28 20.00 1 12.5 10 33.30 19 24.70 6 18.20 2 22.20 3 33.30 69 22.50

General Household Expenses 20 14.30 1 12.5 1 03.30 14 18.20 5 15.20 1 11.10 1 11.10 43 14.10

Education of Children 19 13.60 1 12.5 3 10.00 12 15.60 5 15.20 1 11.10 0 00.00 41 13.40

Medical Expenses 8 05.70 0 00 4 13.30 1 01.30 0 00.00 0 00.00 1 11.10 14 04.60

Wedding of Daughters 2 01.40 1 12.5 0 00.00 3 03.90 2 06.10 0 00.00 0 00.00 8 02.60

Household Repair 4 02.90 1 12.5 1 03.30 0 00.00 2 06.10 0 00.00 0 00.00 8 02.60

Repayment of previous loan 0 00.00 0 00.00 0 00.00 1 01.30 0 00.00 1 11.10 0 00.00 2 00.70

Not applicable 59 42.10 3 37.5 11 36.7 27 35.10 13 39.4 4 44.4 4 44.4 121 39.50

TOTAL 140 100.00 8 100.00 30 100.00 77 100.00 33 100.00 9 100.00 9 100.00 306 100.00

151

Similar pattern was observed for those who studied up to SSC. Out of 50 women from

this category who had borrowed from the groups 19 women had borrowed for income

generating activities. This was closely followed by 14 women who borrowed for

consumption needs and 12 women who borrowed for educational needs. Remaining

women borrowed for marriage (3), medical expenses (1) and the repayment of earlier

debts (1).

There were 33 women who had passed SSC examination. Out of them largest number

of women i.e. six had borrowed for income generating activities. This was closely

followed by five women each who borrowed for education and consumption

purposes. From this category two women each borrowed for medical expenses and

house repair.

There were only 18 women who had studied beyond SSC. The borrowing pattern of

these women was found to be mixed and spread over the requirements primarily on

income generating activities, consumption and education and followed by medical

expenses, marriage, house repair and repayment of earlier loans. Thus it was observed

that the pattern of borrowing as per the educational status followed the overall pattern

of purpose of loans.

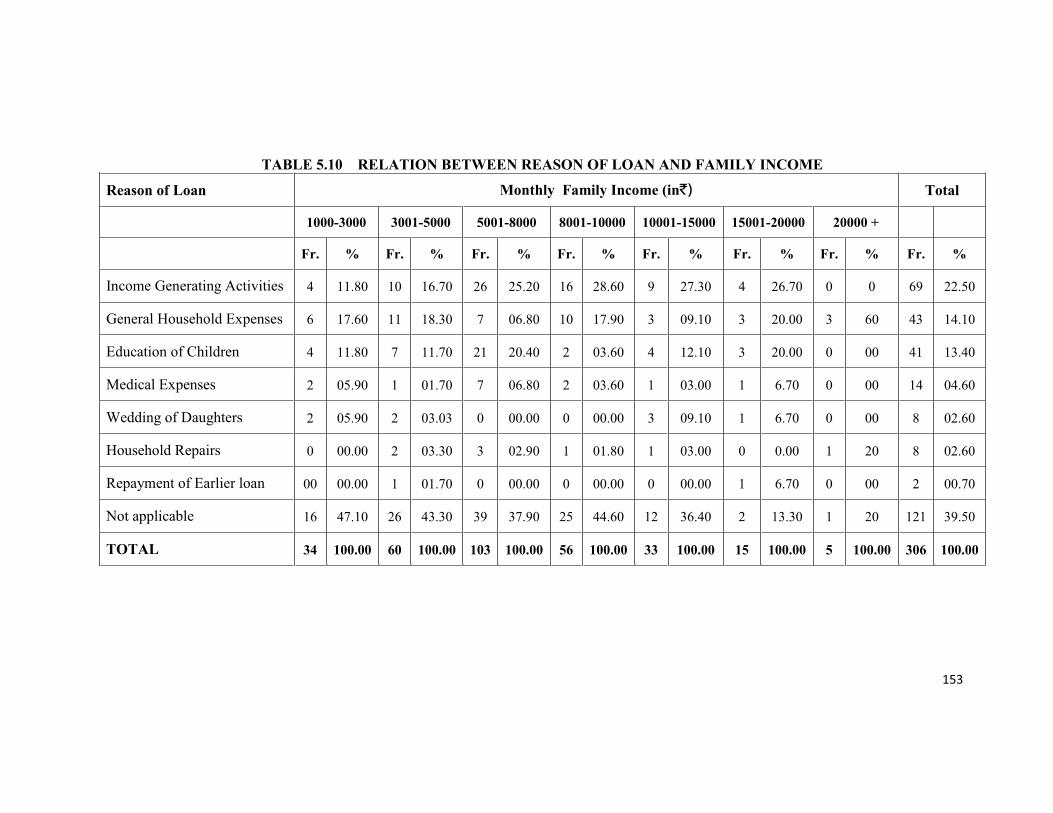

5.4.5 RELATION BETWEEN REASON OF LOAN AND FAMILY INCOME

Table 5.10 explains the relation between the purpose of borrowings and monthly

family income of the respondents

152

This table exhibits the relation between monthly family income of the respondents

and the reason of their SHG loan. There were 34 women with family income of up to

` 3000. From this category largest number of women borrowed for consumption

needs. This was followed by four women each who borrowed for educational needs

and for starting income generating activities. There were 2 women from this category

who borrowed for medical expenses.

There were 60 women who had family income in the range of ` 3001 to ` 5000.

From among them the largest number of women i.e. 11 borrowed for consumption

needs, closely followed by 10 women who borrowed for income generating activities.

There were seven women form this category who borrowed for educational needs ,

two women each borrowed for marriage expenses and house repair and one each who

borrowed for medical expenses and repayment of earlier loans. There were 26 women

from this category who had not availed of borrowing from the groups.

There were 103 women who had family income in the range of ` 5001 to ` 8000.

From among them largest number of women i.e. 26 borrowed for starting income

generating activities. This was followed by 21 women who borrowed for educational

needs. There were 7 women each from this category who borrowed for medical

expenses and consumption needs, followed by 3 women who borrowed for house

repairs. Thus in all there were 197 respondents with family income up to `8000 per

month. This is 64% of the total respondents. Out of them more than 40 respondents

borrowed for starting income generating activity. This constitutes more than 50% of

total respondents who borrowed to start income generating activity.

153

TABLE 5.10 RELATION BETWEEN REASON OF LOAN AND FAMILY INCOME

Reason of Loan Monthly Family Income (in`) Total

1000-3000 3001-5000 5001-8000 8001-10000 10001-15000 15001-20000 20000 +

Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. % Fr. %

Income Generating Activities 4 11.80 10 16.70 26 25.20 16 28.60 9 27.30 4 26.70 0 0 69 22.50

General Household Expenses 6 17.60 11 18.30 7 06.80 10 17.90 3 09.10 3 20.00 3 60 43 14.10

Education of Children 4 11.80 7 11.70 21 20.40 2 03.60 4 12.10 3 20.00 0 00 41 13.40

Medical Expenses 2 05.90 1 01.70 7 06.80 2 03.60 1 03.00 1 6.70 0 00 14 04.60

Wedding of Daughters 2 05.90 2 03.03 0 00.00 0 00.00 3 09.10 1 6.70 0 00 8 02.60

Household Repairs 0 00.00 2 03.30 3 02.90 1 01.80 1 03.00 0 0.00 1 20 8 02.60

Repayment of Earlier loan 00 00.00 1 01.70 0 00.00 0 00.00 0 00.00 1 6.70 0 00 2 00.70

Not applicable 16 47.10 26 43.30 39 37.90 25 44.60 12 36.40 2 13.30 1 20 121 39.50

TOTAL 34 100.00 60 100.00 103 100.00 56 100.00 33 100.00 15 100.00 5 100.00 306 100.00

154

The number of women who had family income in the range of ` 8001 to ` 10000 was

56. From among them also largest number of women i.e. 16 borrowed for income

generating activities. This was followed by 10 women who borrowed for consumption

needs. There were two women each who borrowed for educational expenses and

medical expenses and only one woman from this category borrowed for house repair.

There were 48 women who had family income of ` 10001 to ` 20,000 per month.

From among them 13 respondents borrowed to start some income generating activity.

There were only five women with monthly income of more than ` 20,000. Those

having comparatively higher monthly family income mainly borrowed for the

education of their children, house repair and for general household expenses.

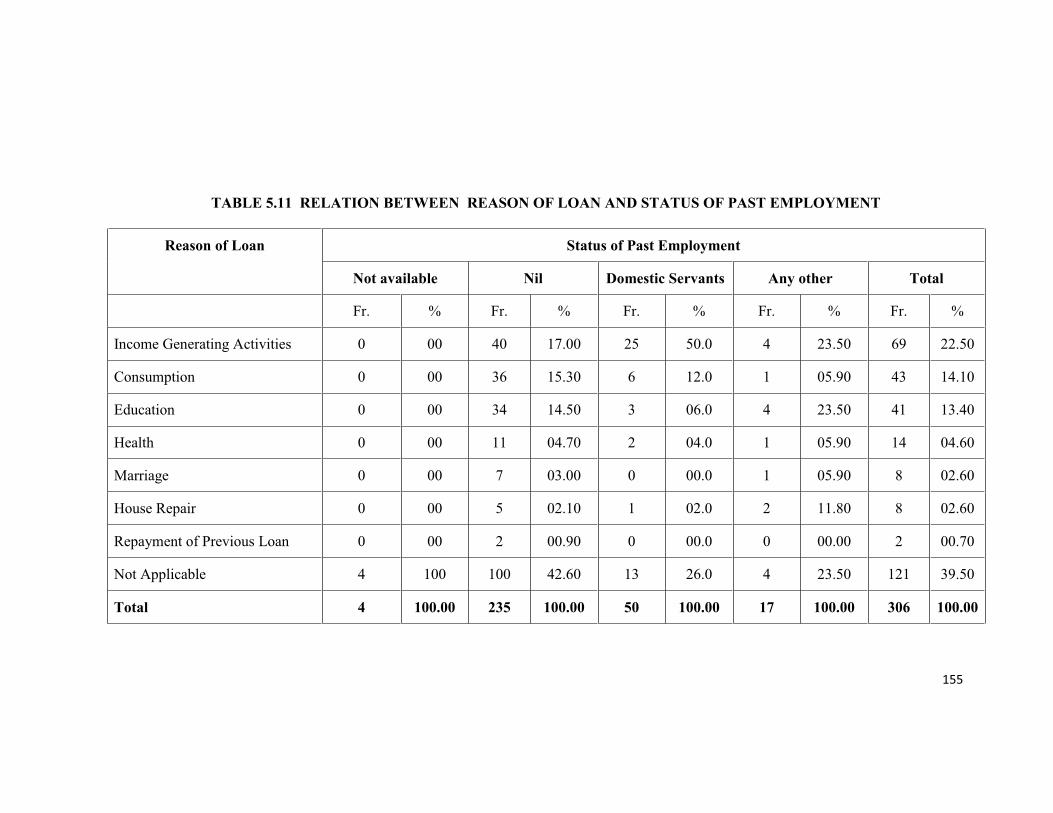

5.4.6 RELATION BETWEEN REASON OF LOAN AND PAST

EMPLOYMENT

Past employment status describes the work the respondents were doing prior to start

their own income generating activity. Table 5.11 describes the relation between the

category indicates those women who did not borrow from the groups. category

indicates those women who were not working earlier. It is noteworthy that a large

majority i.e. 50% of the women who were earlier working as domestic servants,

borrowed from the groups to start some income generating activity in the form of

small business. It helps us to understand the impact of microfinance on economic

empowerment of respondents. Around 24% of those women who were earlier

working as causal workers etc. borrowed from the group to start their own business.

155

TABLE 5.11 RELATION BETWEEN REASON OF LOAN AND STATUS OF PAST EMPLOYMENT

Reason of Loan Status of Past Employment

Not available Nil Domestic Servants Any other Total

Fr. % Fr. % Fr. % Fr. % Fr. %

Income Generating Activities 0 00 40 17.00 25 50.0 4 23.50 69 22.50

Consumption 0 00 36 15.30 6 12.0 1 05.90 43 14.10

Education 0 00 34 14.50 3 06.0 4 23.50 41 13.40

Health 0 00 11 04.70 2 04.0 1 05.90 14 04.60

Marriage 0 00 7 03.00 0 00.0 1 05.90 8 02.60

House Repair 0 00 5 02.10 1 02.0 2 11.80 8 02.60

Repayment of Previous Loan 0 00 2 00.90 0 00.0 0 00.00 2 00.70

Not Applicable 4 100 100 42.60 13 26.0 4 23.50 121 39.50

Total 4 100.00 235 100.00 50 100.00 17 100.00 306 100.00

156

Almost 40 women who were not working earlier borrowed to start their small

business. Four women did not disclose their earlier work status. Among those who

were not working earlier 3% borrowed for marriage in the family, 14.5% for the

education of their children, 5% for health purposes, 2% for the repair of their houses

and 1% for the repayment of earlier loans.

5.5 ROLE OF SHGs IN SUPPORTING ECONOMIC CONDITIONS

The SHGs have played a very important role in supporting the economic conditions of

the members. The thrust of SHGs is on two major activities viz. savings and loans.

Both were very important for the respondents.

5.5.1 ROLE OF SAVINGS

As mentioned earlier the SHGs to which the respondents belonged were formed

during 2005 to 2010. There were five groups that were engaged only in saving

activities. Each respondent of those groups shared that the regular saving was an

extremely important part of their routine. Those who were earning found that the

regular saving activity gave them some kind of security and stability. For those who

were not engaged in any activity also shared that the regular savings enabled them to

have a glimpse of hope to improve their condition. There was a steady increase in the

savings balance of all the groups. All the respondents reported that they were very

keen to remain members of their SHGs and continue to save regularly. They were all

aware of the need to build up savings without any interruption. This they all

considered as a starting point towards ensuring a better future for themselves.

157

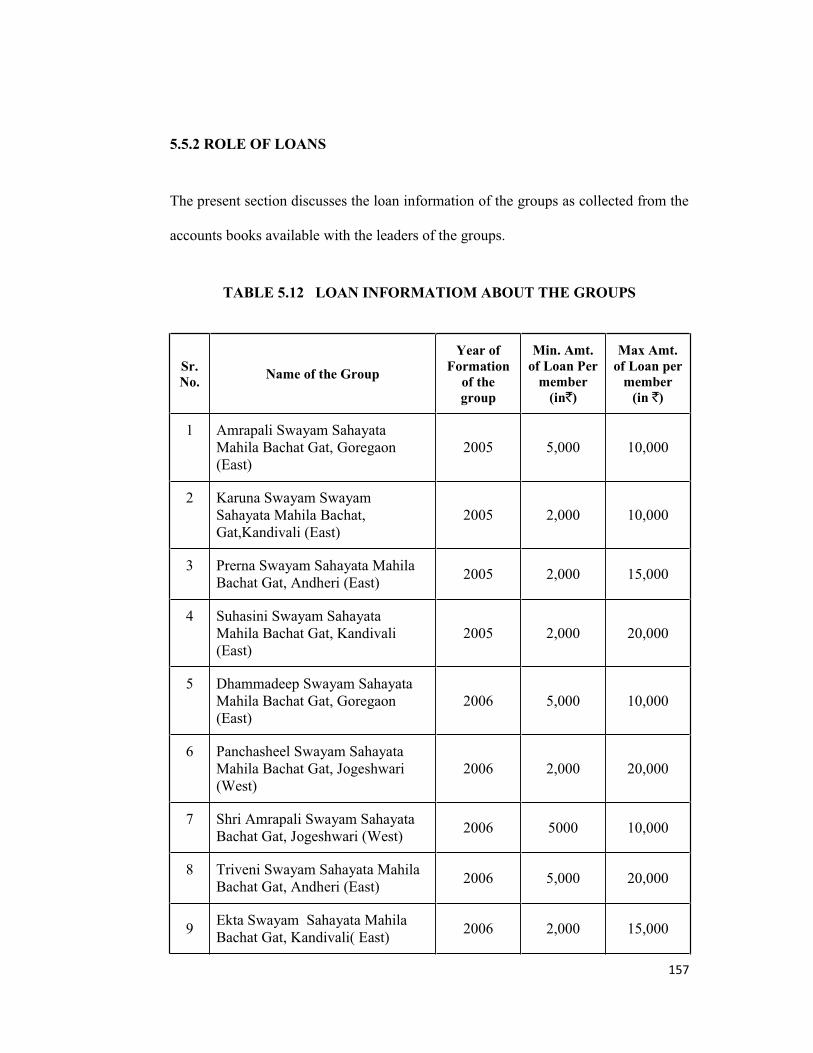

5.5.2 ROLE OF LOANS

The present section discusses the loan information of the groups as collected from the

accounts books available with the leaders of the groups.

TABLE 5.12 LOAN INFORMATIOM ABOUT THE GROUPS

Sr.

No. Name of the Group

Year of

Formation

of the

group

Min. Amt.

of Loan Per

member

(in`)

Max Amt.

of Loan per

member

(in `)

1 Amrapali Swayam Sahayata

Mahila Bachat Gat, Goregaon

(East)

2005 5,000 10,000

2 Karuna Swayam Swayam

Sahayata Mahila Bachat,

Gat,Kandivali (East)

2005 2,000 10,000

3 Prerna Swayam Sahayata Mahila

Bachat Gat, Andheri (East) 2005 2,000 15,000

4 Suhasini Swayam Sahayata

Mahila Bachat Gat, Kandivali

(East)

2005 2,000 20,000

5 Dhammadeep Swayam Sahayata

Mahila Bachat Gat, Goregaon

(East)

2006 5,000 10,000

6 Panchasheel Swayam Sahayata

Mahila Bachat Gat, Jogeshwari

(West)

2006 2,000 20,000

7 Shri Amrapali Swayam Sahayata

Bachat Gat, Jogeshwari (West) 2006 5000 10,000

8 Triveni Swayam Sahayata Mahila

Bachat Gat, Andheri (East) 2006 5,000 20,000

9 Ekta Swayam Sahayata Mahila

Bachat Gat, Kandivali( East) 2006 2,000 15,000

158

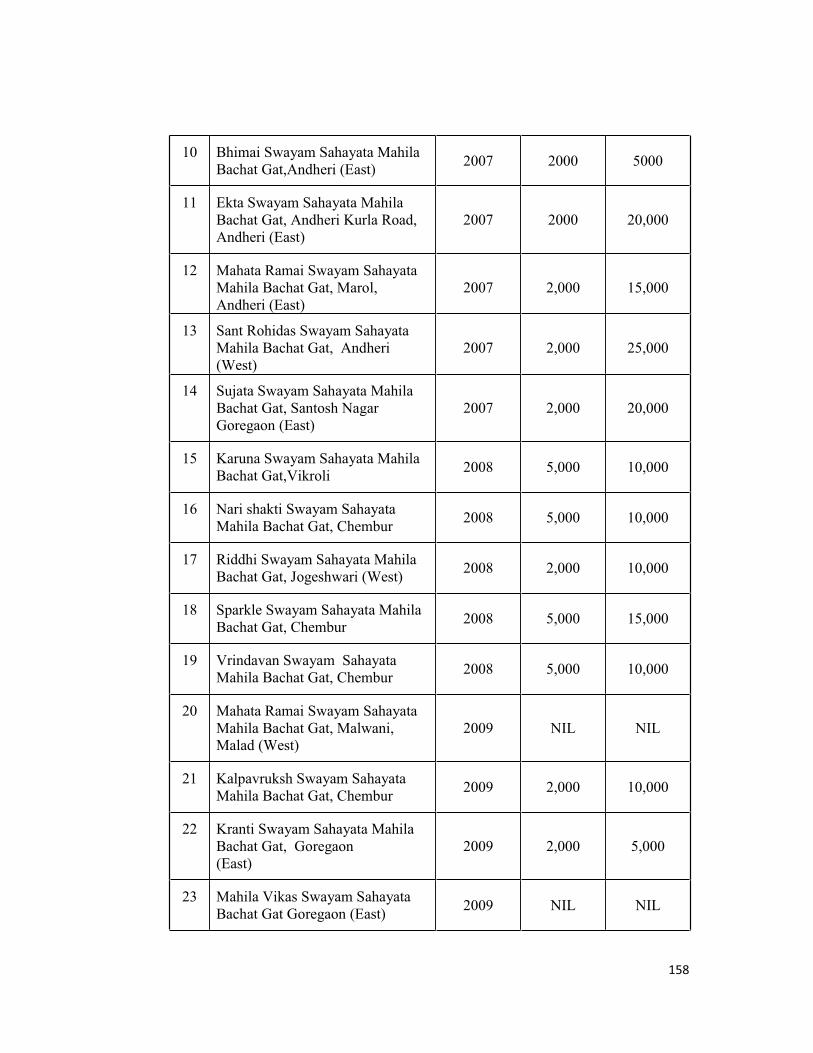

10 Bhimai Swayam Sahayata Mahila

Bachat Gat,Andheri (East) 2007 2000 5000

11 Ekta Swayam Sahayata Mahila

Bachat Gat, Andheri Kurla Road,

Andheri (East)

2007 2000 20,000

12 Mahata Ramai Swayam Sahayata

Mahila Bachat Gat, Marol,

Andheri (East)

2007 2,000 15,000

13 Sant Rohidas Swayam Sahayata

Mahila Bachat Gat, Andheri

(West)

2007 2,000 25,000

14 Sujata Swayam Sahayata Mahila

Bachat Gat, Santosh Nagar

Goregaon (East)

2007 2,000 20,000

15 Karuna Swayam Sahayata Mahila

Bachat Gat,Vikroli 2008 5,000 10,000

16 Nari shakti Swayam Sahayata

Mahila Bachat Gat, Chembur 2008 5,000 10,000

17 Riddhi Swayam Sahayata Mahila

Bachat Gat, Jogeshwari (West) 2008 2,000 10,000

18 Sparkle Swayam Sahayata Mahila

Bachat Gat, Chembur 2008 5,000 15,000

19 Vrindavan Swayam Sahayata

Mahila Bachat Gat, Chembur 2008 5,000 10,000

20 Mahata Ramai Swayam Sahayata

Mahila Bachat Gat, Malwani,

Malad (West)

2009 NIL NIL

21 Kalpavruksh Swayam Sahayata

Mahila Bachat Gat, Chembur 2009 2,000 10,000

22 Kranti Swayam Sahayata Mahila

Bachat Gat, Goregaon

(East)

2009 2,000 5,000

23 Mahila Vikas Swayam Sahayata

Bachat Gat Goregaon (East) 2009 NIL NIL

159

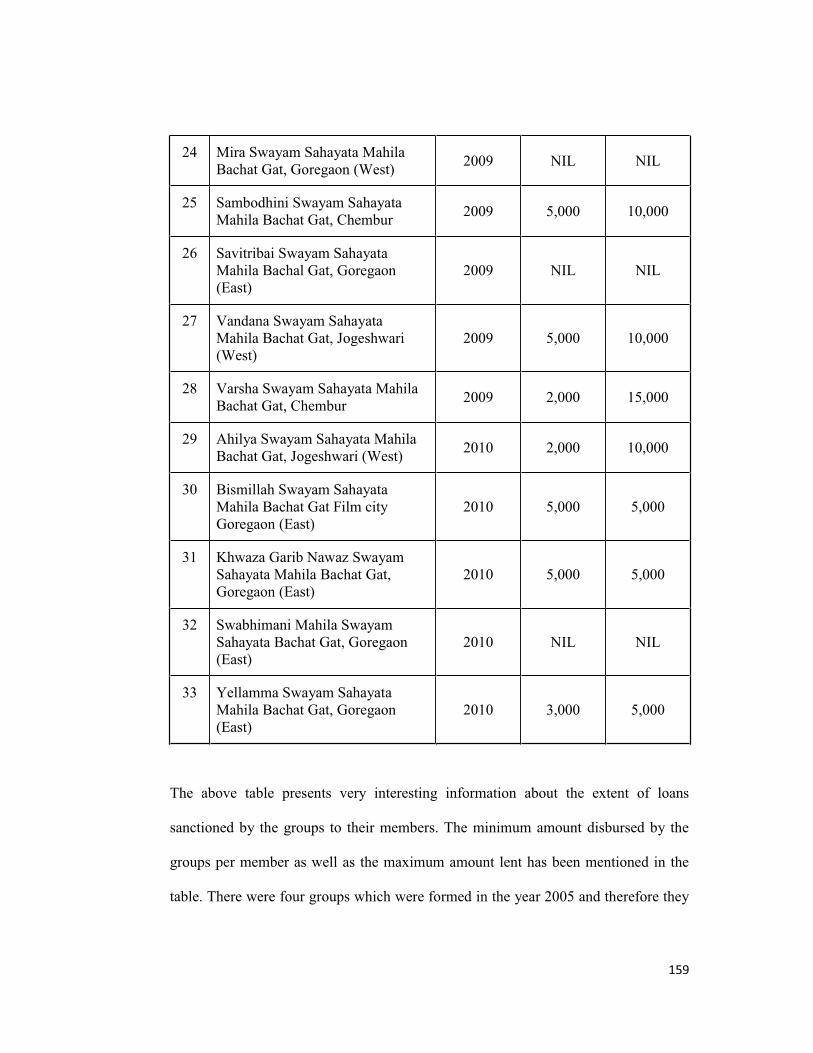

24 Mira Swayam Sahayata Mahila

Bachat Gat, Goregaon (West) 2009 NIL NIL

25 Sambodhini Swayam Sahayata

Mahila Bachat Gat, Chembur 2009 5,000 10,000

26 Savitribai Swayam Sahayata

Mahila Bachal Gat, Goregaon

(East)

2009 NIL NIL

27 Vandana Swayam Sahayata

Mahila Bachat Gat, Jogeshwari

(West)

2009 5,000 10,000

28 Varsha Swayam Sahayata Mahila

Bachat Gat, Chembur 2009 2,000 15,000

29 Ahilya Swayam Sahayata Mahila

Bachat Gat, Jogeshwari (West) 2010 2,000 10,000

30 Bismillah Swayam Sahayata

Mahila Bachat Gat Film city

Goregaon (East)

2010 5,000 5,000

31 Khwaza Garib Nawaz Swayam

Sahayata Mahila Bachat Gat,

Goregaon (East)

2010 5,000 5,000

32 Swabhimani Mahila Swayam

Sahayata Bachat Gat, Goregaon

(East)

2010 NIL NIL

33 Yellamma Swayam Sahayata

Mahila Bachat Gat, Goregaon

(East)

2010 3,000 5,000

The above table presents very interesting information about the extent of loans

sanctioned by the groups to their members. The minimum amount disbursed by the

groups per member as well as the maximum amount lent has been mentioned in the

table. There were four groups which were formed in the year 2005 and therefore they

160

were the oldest groups covered in the study. The minimum amount ranged between

`2000 to `5000 whereas the maximum amount was between `10,000 to `20,000.

Five groups were formed in the year 2006. In case of these groups also it was found

that the minimum amount of loan disbursed was between `2000 to `5000 whereas the

maximum amount was between `10,000 to `20,000.

There were five groups that were established in 2007. The minimum amount for each

of the group was uniform i.e. `2000. The maximum amount ranged between `10,000

to `25,000. It was on account of catering to the diverse needs of the members by these

groups. These were primarily for income generating activities as well as for

consumption needs.

Five groups were formed in 2008. Though the minimum amount of loan was reported

between `2000 to `5000 it was observed that for four groups it was `5000 and only

for one group it was `2000. The maximum amount was `10,000 for four groups and

`15,000 for one group.

There were nine groups that were formed in 2009. At the time of collecting data it

was found that four groups had not disbursed any loans. However all these groups had

recorded steady savings by the members. There were five groups that were formed in

2010. Out of these groups only one group had not started lending operations. The

minimum amount lent per member by these groups was between `2000 to `5000 and

the maximum amount was between `5000 to `10,000.

161

All the members who had borrowed for above ` 10,000 had done so for income

generating activities. There were five groups each who had given loans to the extent

of ` 15,000 and ` 20,000. There was only one group that had given up to ` 25,000.

It was observed that women had formed a very close bond with their groups. The

groups had helped the members to reduce their dependence on the external sources of

loan considerably. The older groups went on expanding their savings base. With

larger savings the frequency of loans also increased. Thus timely loans were made

available to the members.

Over the period of time the groups were stabilised and they could also borrow from

the banks in which they had accounts. The sources of external loans were NGOs. The

NGO with respect to external funding of the groups was Rotary Club, Mumbai.

There were four groups which had received loans from the banks. These were

Yellamma Swayam Sahayata Mahila Bachat Gat, Sant Rohidas Swayam Sahayata

Mahila Bachat Gat, Varsha Swayam Sahayata Mahila Bachat Gat and Vasti Vikas

Samiti. Other than these there were three groups which had already applied for bank

loans. These were Khwaza Garib Nawaz Swayam Sahayata Mahila Bachat Gat,

Mahata Ramai Swayam Sahayata Mahila Bachat Gat and Bismillah Swayam Sahayata

Mahila Bachat Gat.

There were four groups which received external loans for initiating income generating

activities from Rotary Club, Mumbai. These groups were Prerna Swayam Sahayata

Mahila Bachat Gat, Triveni Swayam Sahayata Mahila Bachat Gat, Sant Rohidas

Swayam Sahayata Mahila Bachat Gat and Vasti Vikas Samiti consisting of one

162

member each from Vrindavan Swayam Sahayata Mahila Bachat Gat Nari Shakti

Swayam Sahayata Mahila Bachat Gat and Sambodhini Swayam Sahayata Mahila

Bachat Gat and two members from Sparkle Swayam Sahayata Mahila Bachat Gat.

The loans which were received from Rotary Club did not require the payment of

installments for the first three months. Thereafter the borrowers were required to pay

some amount from the principal in the form of installments.

Thus it was observed that both the savings as well as lending activities of the groups

played an extremely important role in supporting economic activities of the

respondents. The members were in a position to save on a regular basis. Timely loans

for various consumption needs were extremely important for them. This also reduced

their dependence on the money lenders. The interest on SHG loans being

comparatively less than the money lenders the loans were further instrumental in

saving in terms of interest. A move towards further enhancement of economic

conditions has already begun by way availing loans for income generating activities.

The largest numbers of loans were taken for income generating activities. Thus both

saving and lending by SHGs have enabled the members to gain some security.

5.6 SUMMARY

The present chapter focused on the borrowing behavior of the respondents. It has

highlighted the role of SHGs with respect to savings and credit operations. Majority

of the members availed loans from the group while some were content with savings

and some others could not borrow as the groups were in the initial stages of

formation. Even those women who had still not borrowed from the groups appreciated

163

the fact that they could save some amount of money after becoming members of the

SHGs. It helped in raising their self esteem.

Interest rates on SHG loans as reported by the members were less than interest rates

charged by the money lenders. However, compared to the interest rates charged by

sources other than money lenders, SHG loans were not cheap. Majority of the

members borrowed loans in the amounts of ` 5000 and ` 10, 000. In the instance of

loans arranged from NGOs they could also borrow up to ` 20,000 or more. However,

in some cases the groups also allowed some members to borrow more than ` 20,000

depending upon the need and circumstances of the members.

The study also revealed that majority of the members had borrowed only once from

the group. It is noteworthy that almost 40% of the borrowers utilised the loans to start

income generating activities. Remaining borrowers used the loans for risk situations

like illnesses, marriages, repayment of earlier loans house repairs and for the payment

of school or college fees or tuition fees of their children.

Thus, it can be concluded that SHG loans helped the women from vulnerable sections

of the society, enabling them to deal with risk situations of various types and also

helping some of them to become economically empowered.