commodities as an asset class - swiss.cfaswiss.cfa/lists/events...

TRANSCRIPT

Commodities as an Asset ClassDelivering Beta & Beyond

Dr. David-Michael Lincke, CFA, FRMPicard Angst AG

Continuing Education SeminarCFA Society SwitzerlandZurich, 14 October 2016

Contents

October 16 Picard Angst AG

Commodities - State of the Market and Asset Class 3

Portfolio Contribution – Diversification, Inflation Sensitivity, Risk Premium 10

Evolution of Commodity Beta Strategies 17

Alternative Risk Premia in Commodities 31

Summary 36

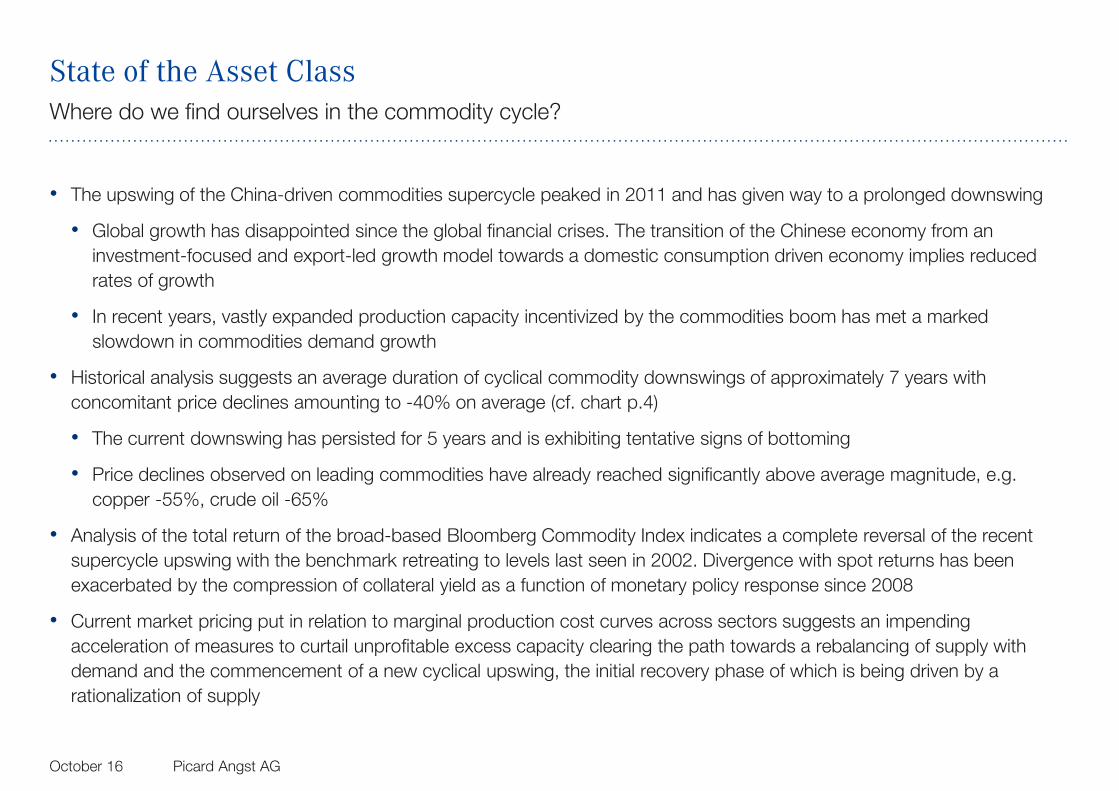

State of the Asset Class

October 16 Picard Angst AG

Where do we find ourselves in the commodity cycle?

• The upswing of the China-driven commodities supercycle peaked in 2011 and has given way to a prolonged downswing

• Global growth has disappointed since the global financial crises. The transition of the Chinese economy from an investment-focused and export-led growth model towards a domestic consumption driven economy implies reduced rates of growth

• In recent years, vastly expanded production capacity incentivized by the commodities boom has met a marked slowdown in commodities demand growth

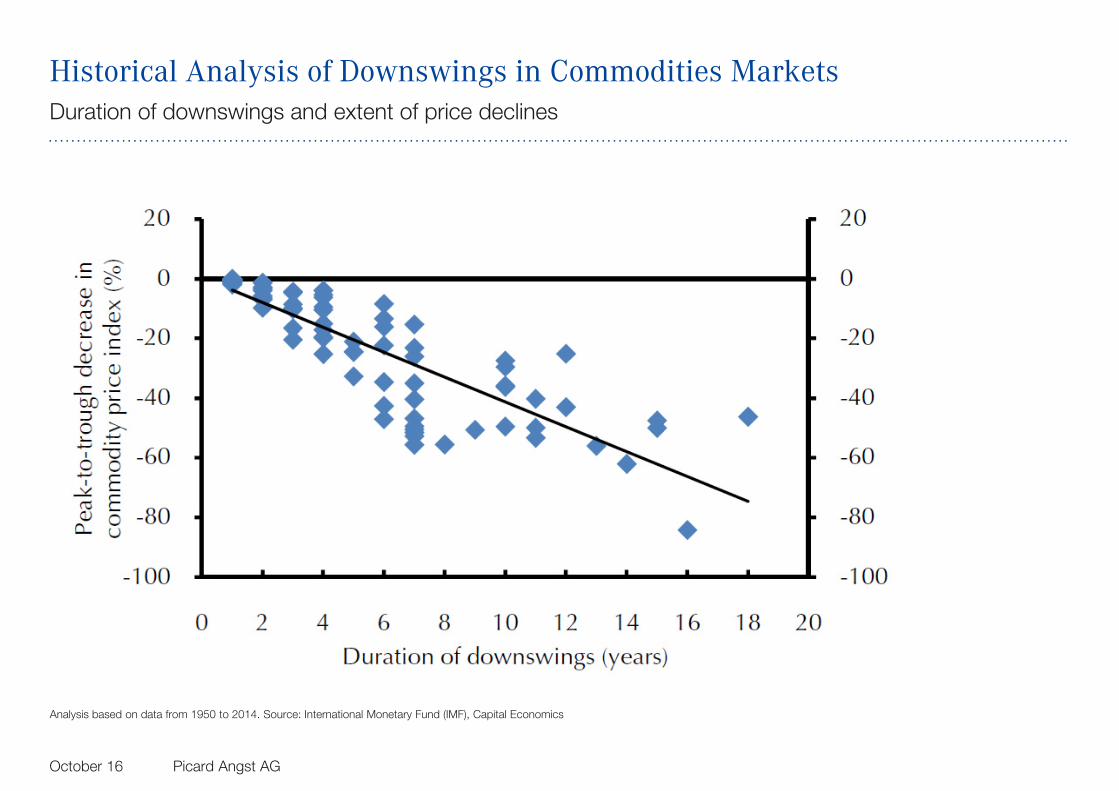

• Historical analysis suggests an average duration of cyclical commodity downswings of approximately 7 years with concomitant price declines amounting to -40% on average (cf. chart p.4)

• The current downswing has persisted for 5 years and is exhibiting tentative signs of bottoming

• Price declines observed on leading commodities have already reached significantly above average magnitude, e.g. copper -55%, crude oil -65%

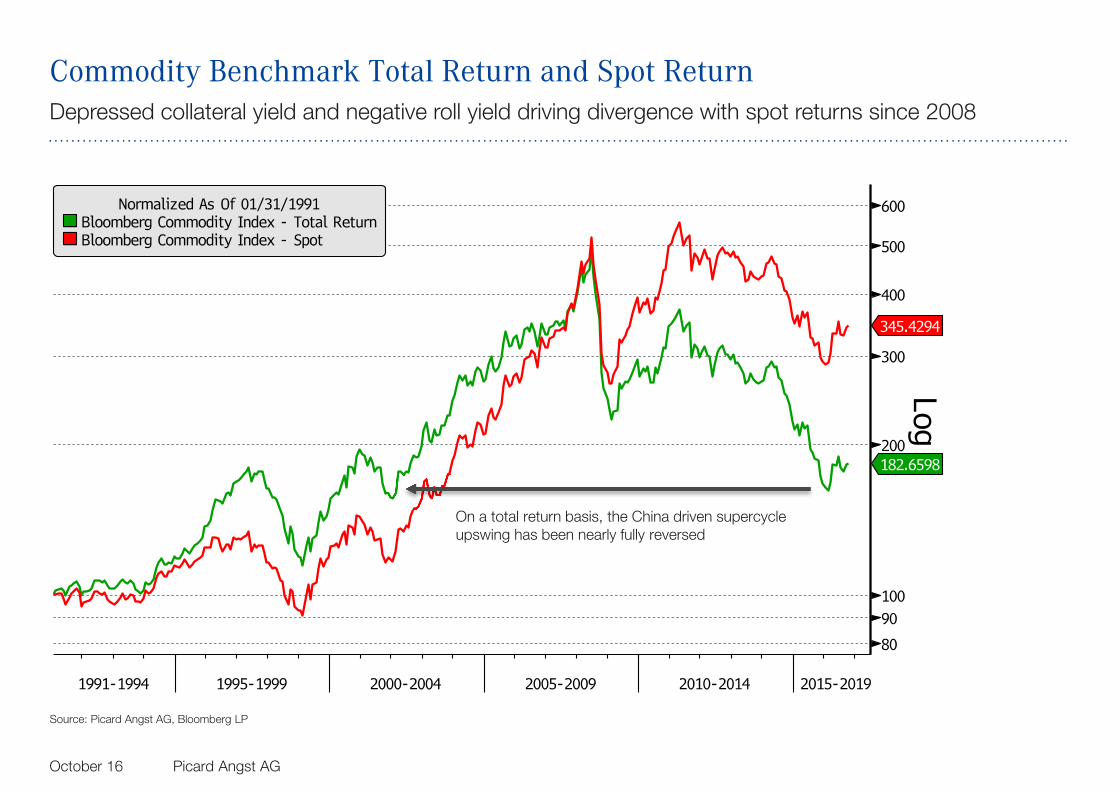

• Analysis of the total return of the broad-based Bloomberg Commodity Index indicates a complete reversal of the recent supercycle upswing with the benchmark retreating to levels last seen in 2002. Divergence with spot returns has been exacerbated by the compression of collateral yield as a function of monetary policy response since 2008

• Current market pricing put in relation to marginal production cost curves across sectors suggests an impending acceleration of measures to curtail unprofitable excess capacity clearing the path towards a rebalancing of supply with demand and the commencement of a new cyclical upswing, the initial recovery phase of which is being driven by a rationalization of supply

Historical Analysis of Downswings in Commodities Markets

October 16 Picard Angst AG

Duration of downswings and extent of price declines

Analysis based on data from 1950 to 2014. Source: International Monetary Fund (IMF), Capital Economics

Commodity Benchmark Total Return and Spot Return

October 16 Picard Angst AG

Depressed collateral yield and negative roll yield driving divergence with spot returns since 2008

Source: Picard Angst AG, Bloomberg LP

On a total return basis, the China driven supercycle upswing has been nearly fully reversed

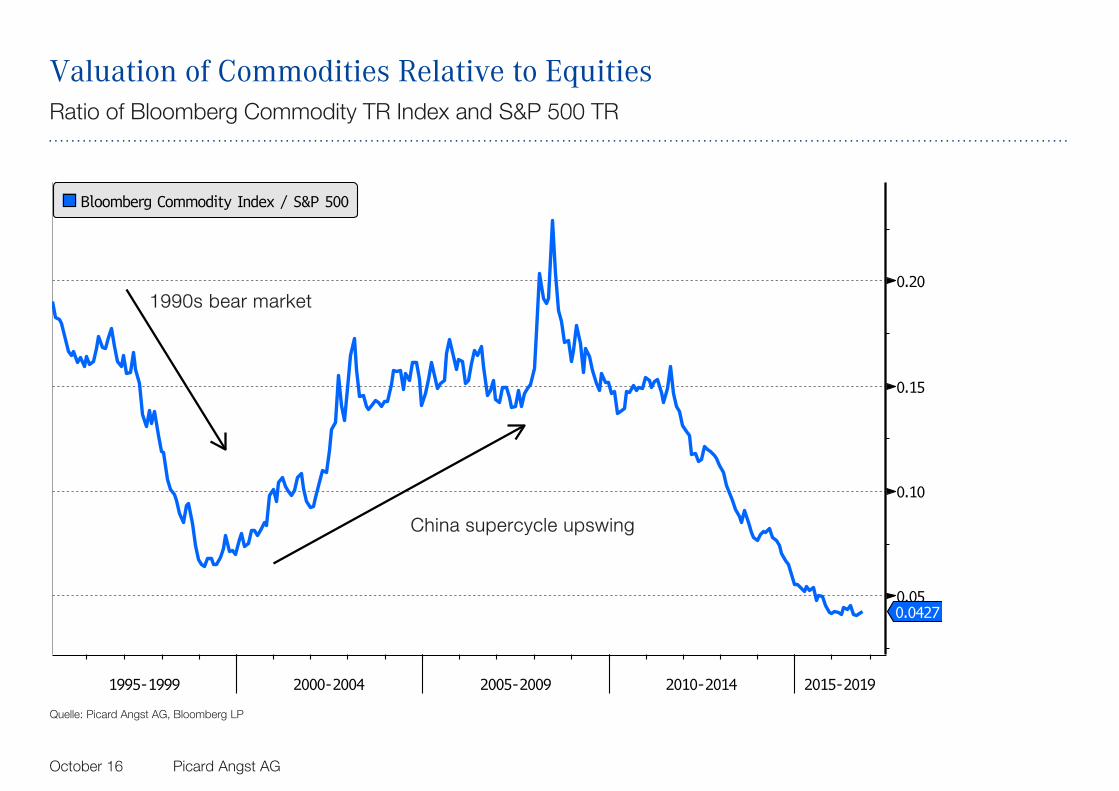

Valuation of Commodities Relative to Equities

October 16 Picard Angst AG

Ratio of Bloomberg Commodity TR Index and S&P 500 TR

Quelle: Picard Angst AG, Bloomberg LP

1990s bear market

China supercycle upswing

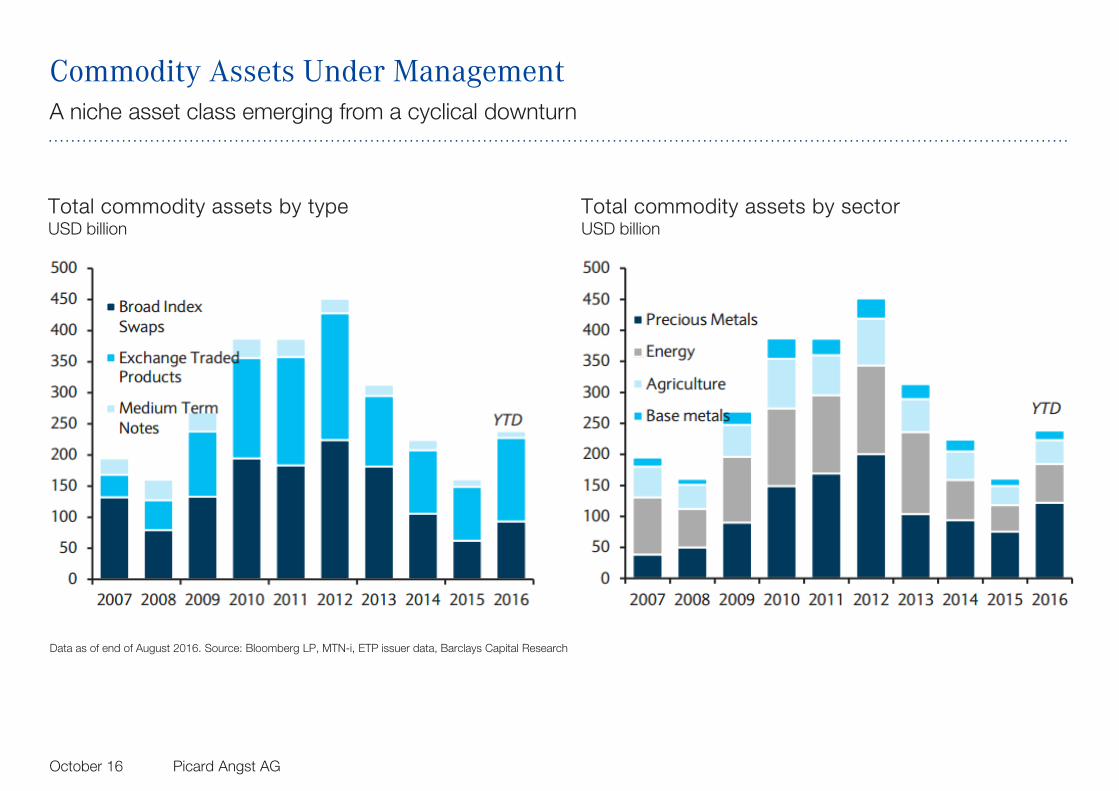

Commodity Assets Under Management

October 16 Picard Angst AG

A niche asset class emerging from a cyclical downturn

Total commodity assets by type USD billion

Total commodity assets by sector USD billion

Data as of end of August 2016. Source: Bloomberg LP, MTN-i, ETP issuer data, Barclays Capital Research

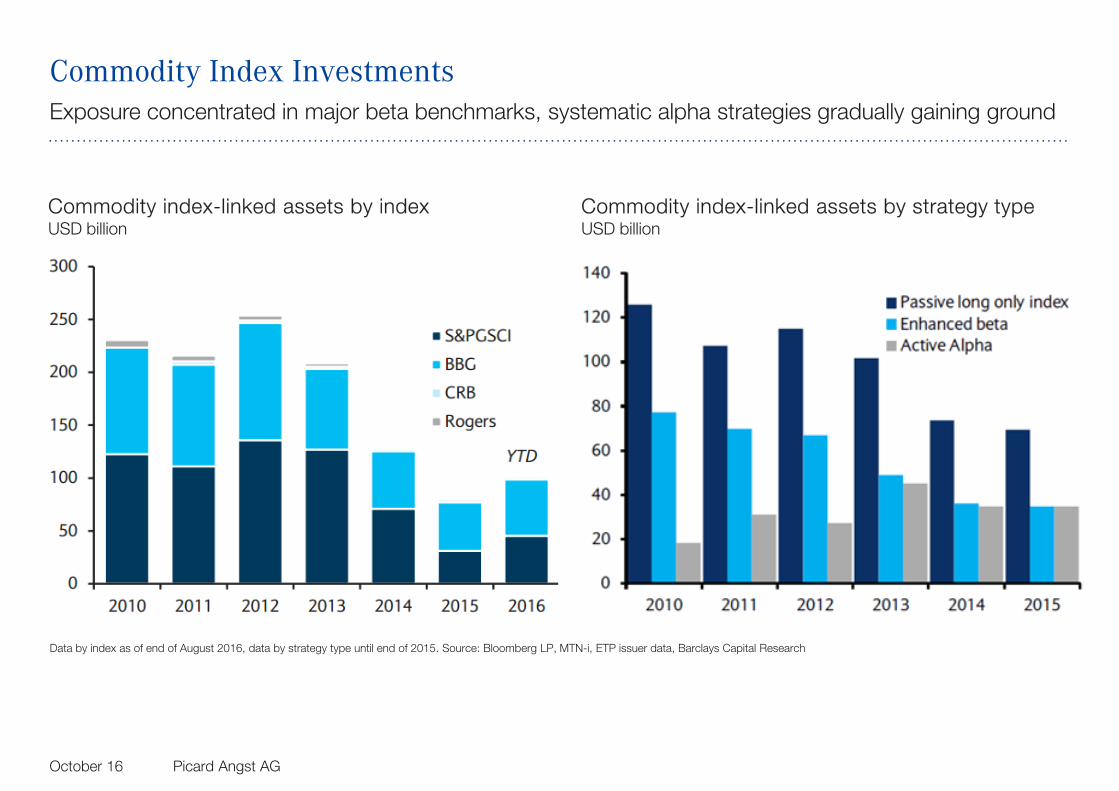

Commodity Index Investments

October 16 Picard Angst AG

Exposure concentrated in major beta benchmarks, systematic alpha strategies gradually gaining ground

Commodity index-linked assets by index USD billion

Commodity index-linked assets by strategy type USD billion

Data by index as of end of August 2016, data by strategy type until end of 2015. Source: Bloomberg LP, MTN-i, ETP issuer data, Barclays Capital Research

Contents

October 16 Picard Angst AG

Commodities - State of the Market and Asset Class 3

Portfolio Contribution – Diversification, Inflation Sensitivity, Risk Premium 10

Evolution of Commodity Beta Strategies 17

Alternative Risk Premia in Commodities 31

Summary 36

Why Consider Commodities in the Strategic Asset Allocation?Benefit to the portfolio

Diversification

• Low average correlation with major traditional asset classes equities and bonds

• Historically, the addition of commodities to an equity/bond portfolio has resulted in a sustained increase of risk-adjusted returns

Inflation Protection

• Among all asset classes, commodities exhibit the highest degree of sensitivity with respect to price pressures

Return – Earning the asset class risk premium (beta)

• The cyclicality and lack of cash flow yield from commodities investments raises questions regarding the existence of an asset class risk premium

• Historically, provided a suitable investment strategy that adequately accounts for the cyclicality of the asset class is chosen, a broadly diversified commodity portfolio has achieved equity-like risk-adjusted returns over the long term

October 16 Picard Angst AG

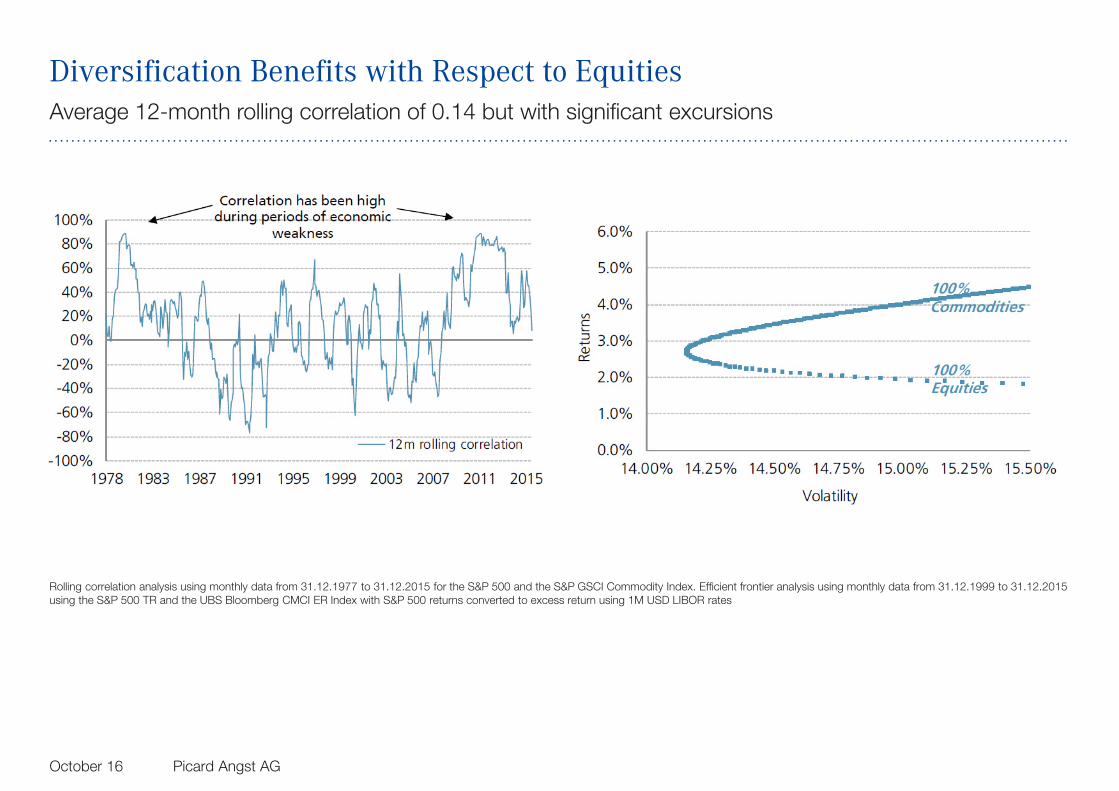

Diversification Benefits with Respect to EquitiesAverage 12-month rolling correlation of 0.14 but with significant excursions

Rolling correlation analysis using monthly data from 31.12.1977 to 31.12.2015 for the S&P 500 and the S&P GSCI Commodity Index. Efficient frontier analysis using monthly data from 31.12.1999 to 31.12.2015 using the S&P 500 TR and the UBS Bloomberg CMCI ER Index with S&P 500 returns converted to excess return using 1M USD LIBOR rates

October 16 Picard Angst AG

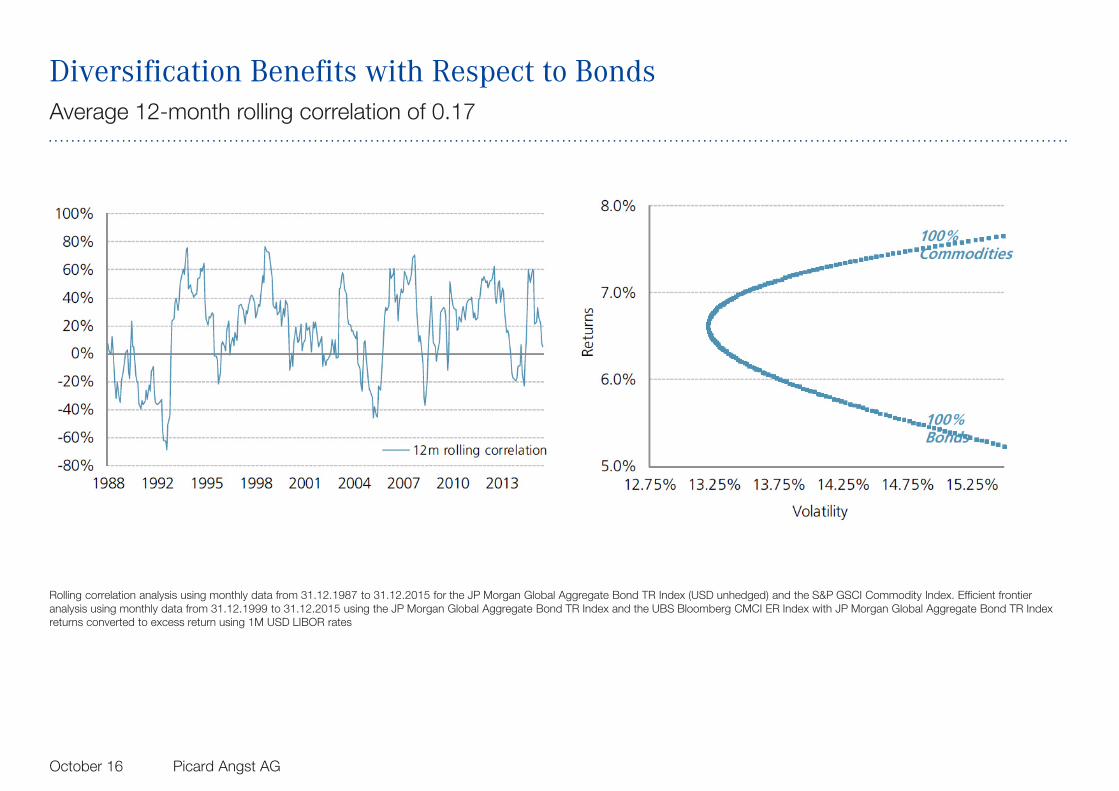

Diversification Benefits with Respect to BondsAverage 12-month rolling correlation of 0.17

Rolling correlation analysis using monthly data from 31.12.1987 to 31.12.2015 for the JP Morgan Global Aggregate Bond TR Index (USD unhedged) and the S&P GSCI Commodity Index. Efficient frontier analysis using monthly data from 31.12.1999 to 31.12.2015 using the JP Morgan Global Aggregate Bond TR Index and the UBS Bloomberg CMCI ER Index with JP Morgan Global Aggregate Bond TR Index returns converted to excess return using 1M USD LIBOR rates

October 16 Picard Angst AG

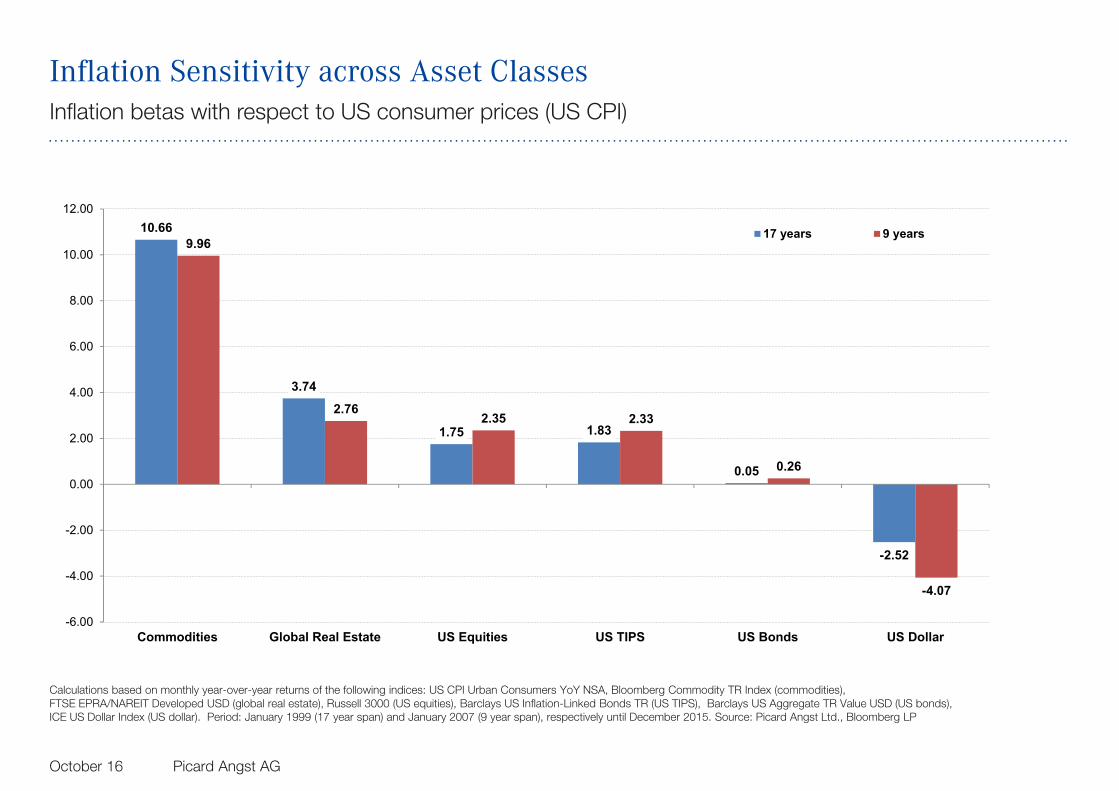

Inflation Sensitivity across Asset ClassesInflation betas with respect to US consumer prices (US CPI)

Calculations based on monthly year-over-year returns of the following indices: US CPI Urban Consumers YoY NSA, Bloomberg Commodity TR Index (commodities), FTSE EPRA/NAREIT Developed USD (global real estate), Russell 3000 (US equities), Barclays US Inflation-Linked Bonds TR (US TIPS), Barclays US Aggregate TR Value USD (US bonds), ICE US Dollar Index (US dollar). Period: January 1999 (17 year span) and January 2007 (9 year span), respectively until December 2015. Source: Picard Angst Ltd., Bloomberg LP

October 16 Picard Angst AG

10.66

3.74

1.75 1.83

0.05

-2.52

9.96

2.762.35 2.33

0.26

-4.07

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Commodities Global Real Estate US Equities US TIPS US Bonds US Dollar

17 years 9 years

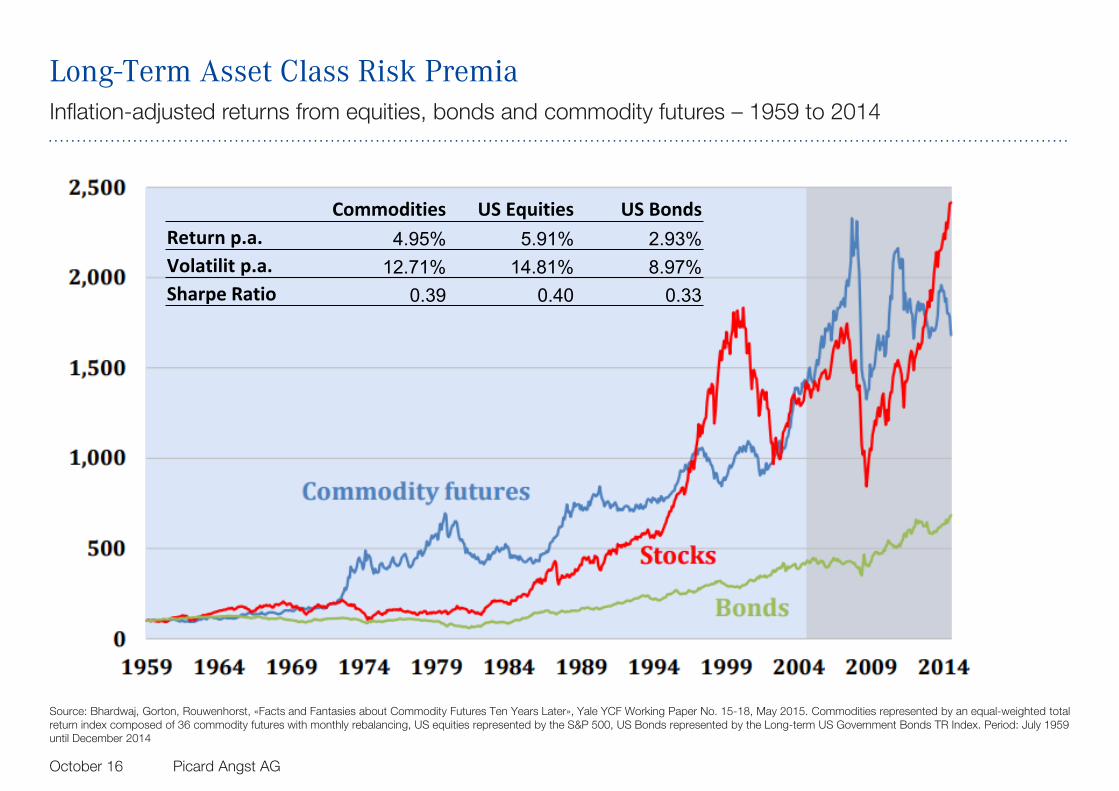

Long-Term Asset Class Risk PremiaInflation-adjusted returns from equities, bonds and commodity futures – 1959 to 2014

Source: Bhardwaj, Gorton, Rouwenhorst, «Facts and Fantasies about Commodity Futures Ten Years Later», Yale YCF Working Paper No. 15-18, May 2015. Commodities represented by an equal-weighted total return index composed of 36 commodity futures with monthly rebalancing, US equities represented by the S&P 500, US Bonds represented by the Long-term US Government Bonds TR Index. Period: July 1959 until December 2014

October 16 Picard Angst AG

Commodities US Equities US BondsReturn p.a. 4.95% 5.91% 2.93%Volatilit p.a. 12.71% 14.81% 8.97%Sharpe Ratio 0.39 0.40 0.33

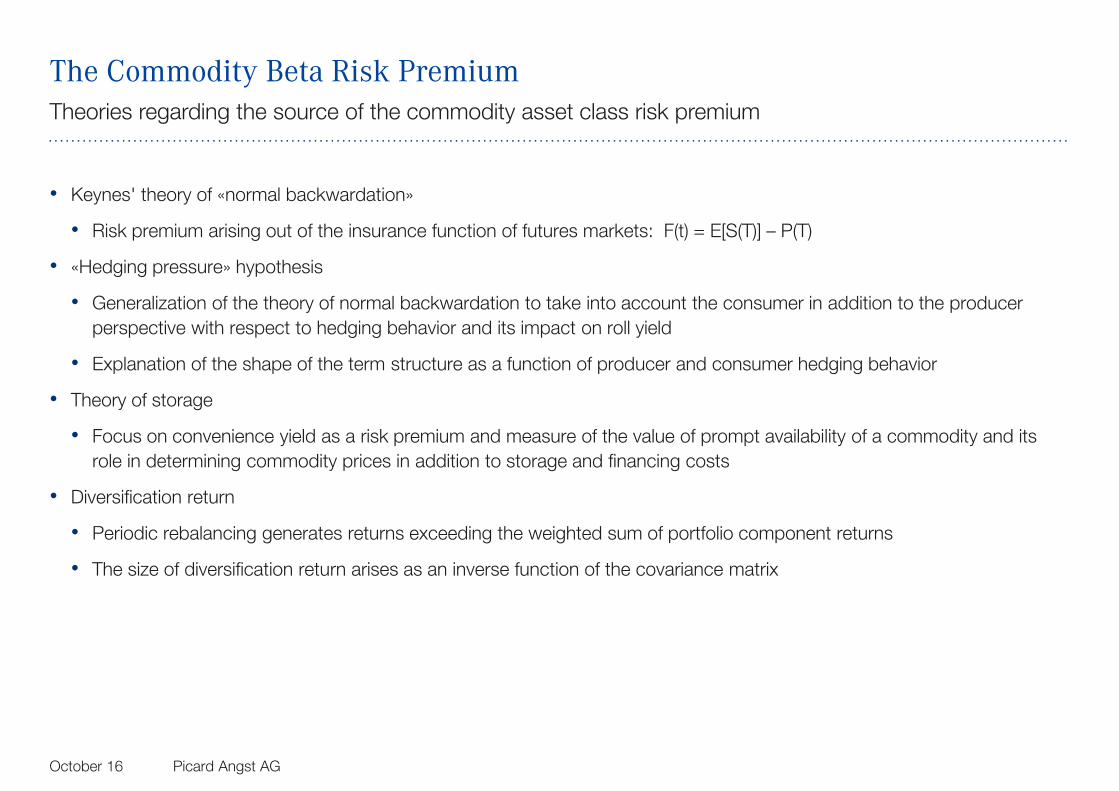

The Commodity Beta Risk Premium

October 16 Picard Angst AG

Theories regarding the source of the commodity asset class risk premium

• Keynes' theory of «normal backwardation»

• Risk premium arising out of the insurance function of futures markets: F(t) = E[S(T)] – P(T)

• «Hedging pressure» hypothesis

• Generalization of the theory of normal backwardation to take into account the consumer in addition to the producer perspective with respect to hedging behavior and its impact on roll yield

• Explanation of the shape of the term structure as a function of producer and consumer hedging behavior

• Theory of storage

• Focus on convenience yield as a risk premium and measure of the value of prompt availability of a commodity and its role in determining commodity prices in addition to storage and financing costs

• Diversification return

• Periodic rebalancing generates returns exceeding the weighted sum of portfolio component returns

• The size of diversification return arises as an inverse function of the covariance matrix

Contents

October 16 Picard Angst AG

Commodities - State of the Market and Asset Class 3

Portfolio Contribution – Diversification, Inflation Sensitivity, Risk Premium 10

Evolution of Commodity Beta Strategies 17

Alternative Risk Premia in Commodities 31

Summary 36

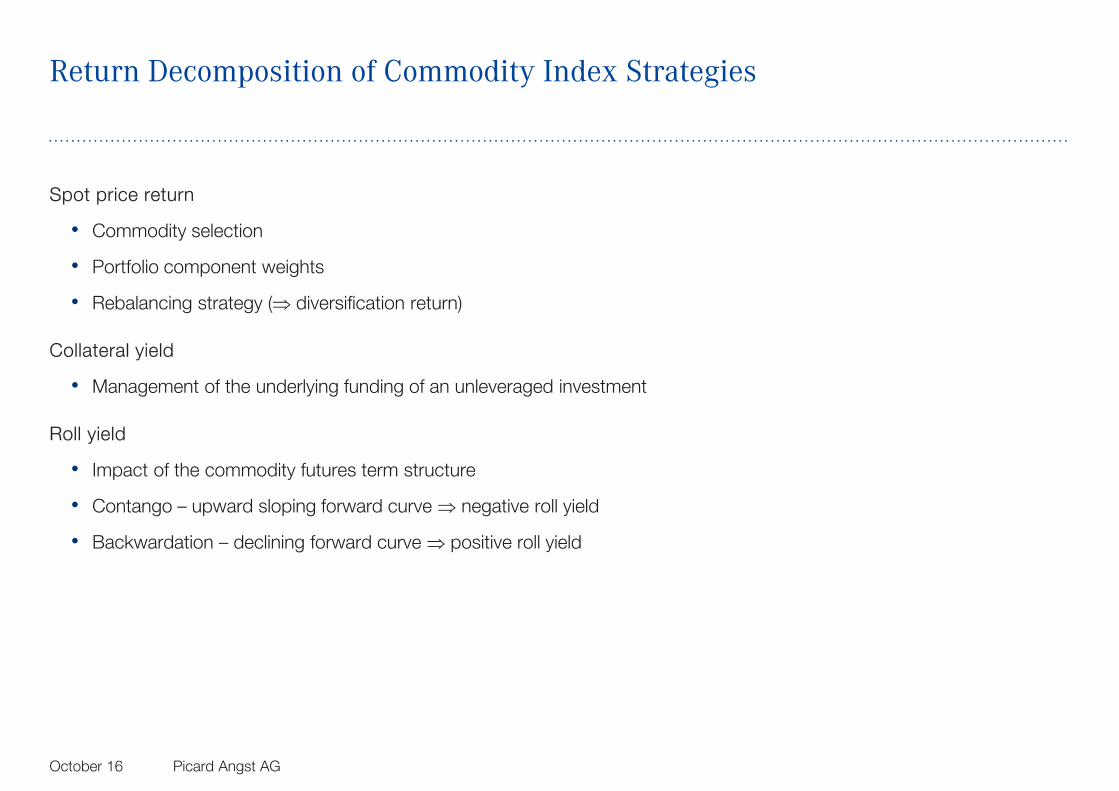

Return Decomposition of Commodity Index Strategies

October 16 Picard Angst AG

Spot price return

• Commodity selection

• Portfolio component weights

• Rebalancing strategy ( diversification return)

Collateral yield

• Management of the underlying funding of an unleveraged investment

Roll yield

• Impact of the commodity futures term structure

• Contango – upward sloping forward curve negative roll yield

• Backwardation – declining forward curve positive roll yield

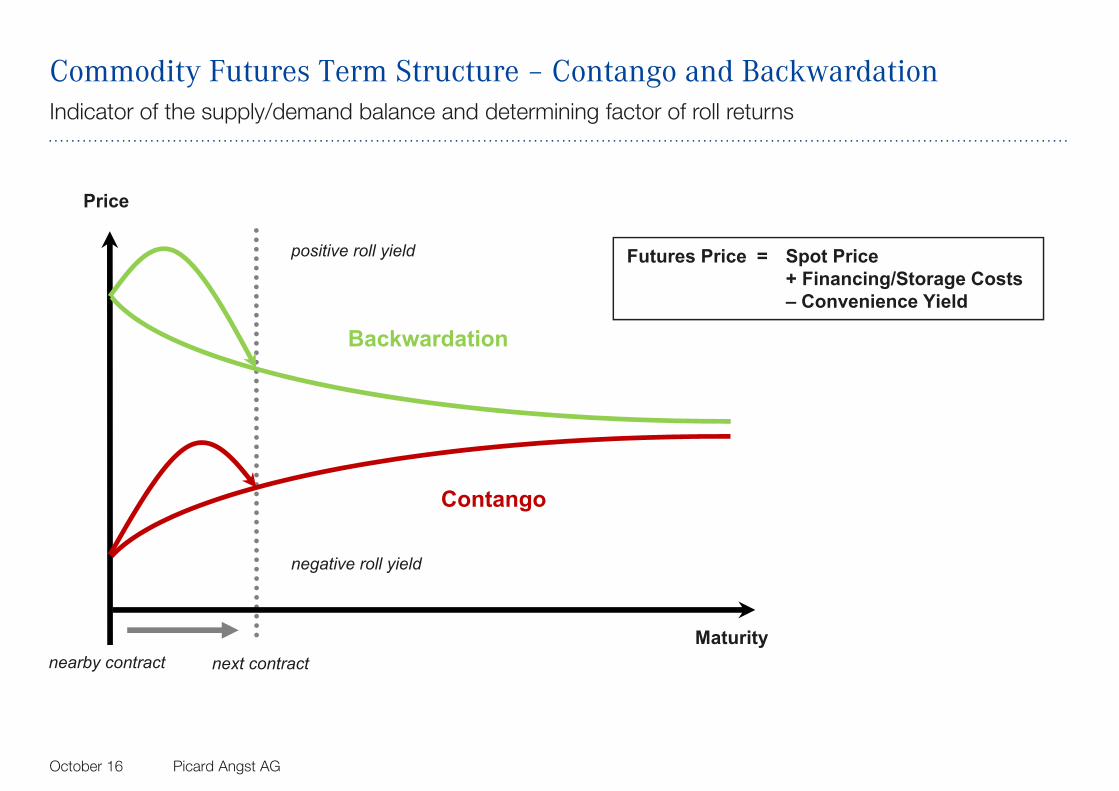

Commodity Futures Term Structure – Contango and Backwardation

October 16 Picard Angst AG

Indicator of the supply/demand balance and determining factor of roll returns

positive roll yield

Backwardation

Contango

nearby contract next contractMaturity

Price

negative roll yield

Futures Price = Spot Price+ Financing/Storage Costs– Convenience Yield

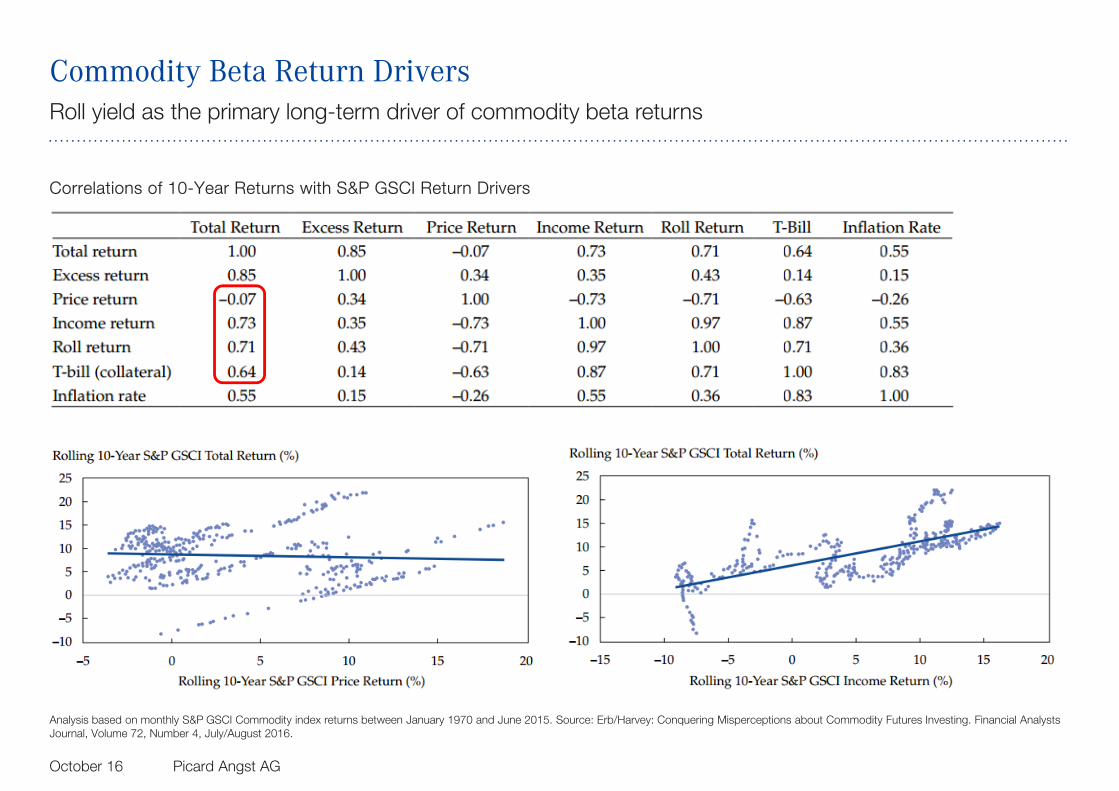

Commodity Beta Return Drivers

October 16 Picard Angst AG

Roll yield as the primary long-term driver of commodity beta returns

Correlations of 10-Year Returns with S&P GSCI Return Drivers

Analysis based on monthly S&P GSCI Commodity index returns between January 1970 and June 2015. Source: Erb/Harvey: Conquering Misperceptions about Commodity Futures Investing. Financial Analysts Journal, Volume 72, Number 4, July/August 2016.

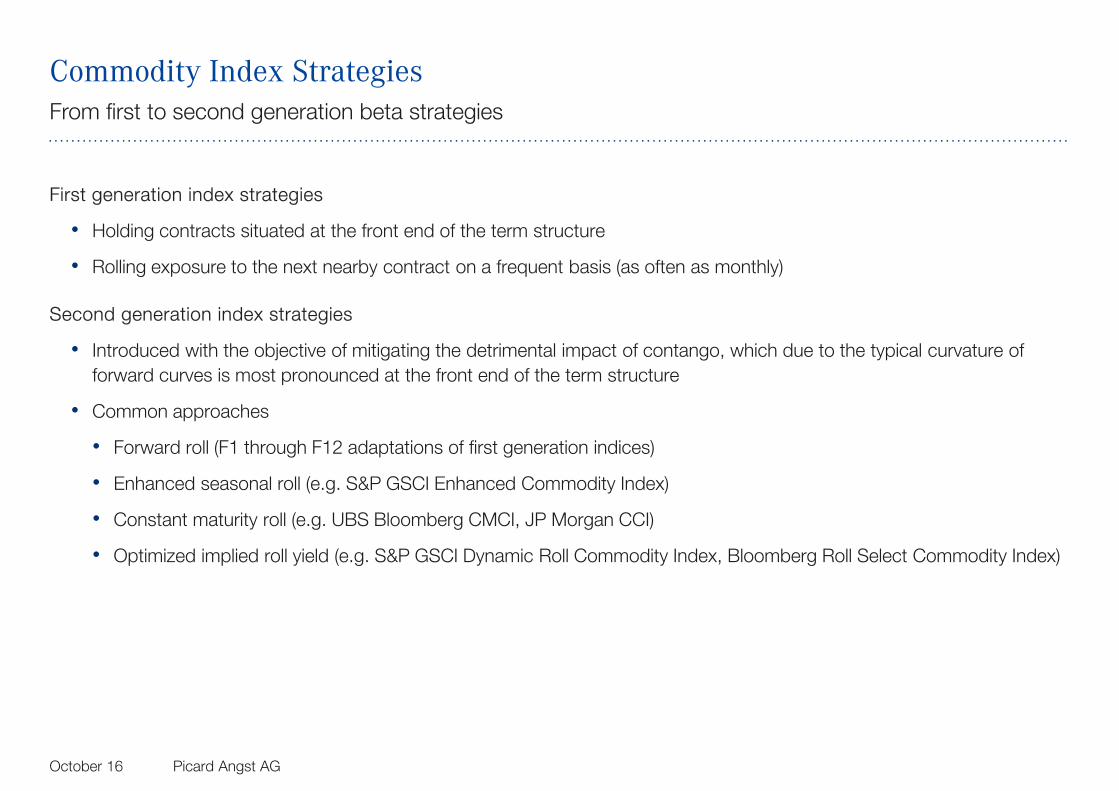

Commodity Index Strategies

October 16 Picard Angst AG

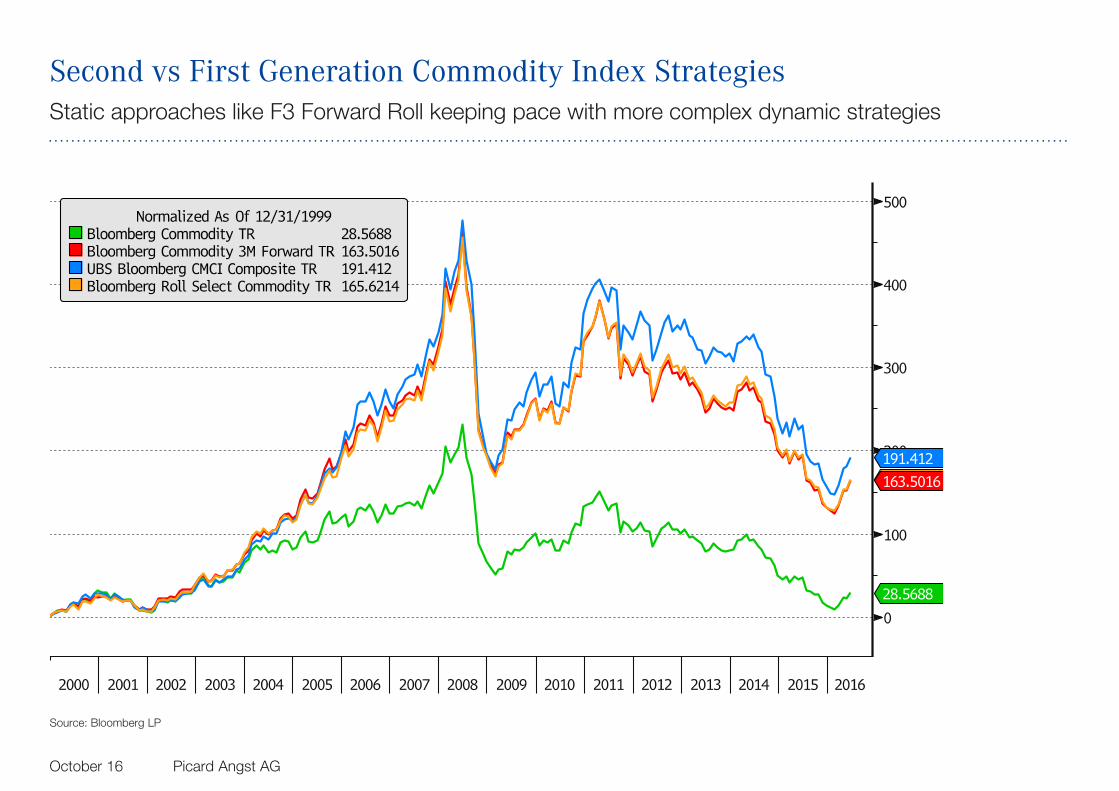

From first to second generation beta strategies

First generation index strategies

• Holding contracts situated at the front end of the term structure

• Rolling exposure to the next nearby contract on a frequent basis (as often as monthly)

Second generation index strategies

• Introduced with the objective of mitigating the detrimental impact of contango, which due to the typical curvature of forward curves is most pronounced at the front end of the term structure

• Common approaches

• Forward roll (F1 through F12 adaptations of first generation indices)

• Enhanced seasonal roll (e.g. S&P GSCI Enhanced Commodity Index)

• Constant maturity roll (e.g. UBS Bloomberg CMCI, JP Morgan CCI)

• Optimized implied roll yield (e.g. S&P GSCI Dynamic Roll Commodity Index, Bloomberg Roll Select Commodity Index)

Second vs First Generation Commodity Index Strategies

October 16 Picard Angst AG

Static approaches like F3 Forward Roll keeping pace with more complex dynamic strategies

Source: Bloomberg LP

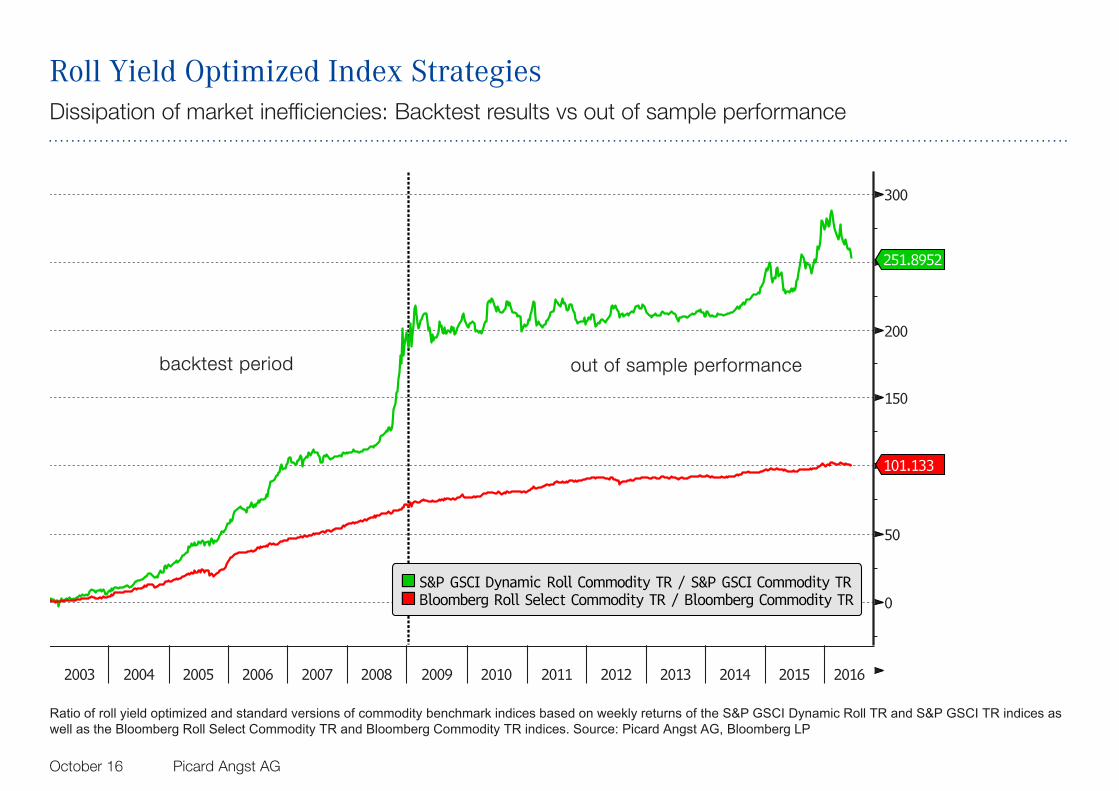

Roll Yield Optimized Index Strategies

October 16 Picard Angst AG

Dissipation of market inefficiencies: Backtest results vs out of sample performance

Ratio of roll yield optimized and standard versions of commodity benchmark indices based on weekly returns of the S&P GSCI Dynamic Roll TR and S&P GSCI TR indices as well as the Bloomberg Roll Select Commodity TR and Bloomberg Commodity TR indices. Source: Picard Angst AG, Bloomberg LP

backtest period out of sample performance

Compositional Deficits of Common Commodity Benchmarks

October 16 Picard Angst AG

Eliminating structural drag and aligning basis risks

• In terms of portfolio composition, standard commodity benchmarks, such as the S&P GSCI and Bloomberg index families, suffer from inadequate construction methodologies focused on production and liquidity statistics

• Disparate sector weightings, e.g. extreme energy overweight in the S&P GSCI due to exclusively taking into account production volume data

• Inclusion of commodity contracts, e.g. US natural gas, whose economic characteristics guarantee losses if held over the long term

• Disregard for the correlation structure among as well as within commodity sectors resulting in unnecessarily high volatility levels or overly expansive portfolio size

• The US dollar based nature of commodities markets raises challenges for European investors looking to take commodity exposure as an inflation hedge

• Basis risks abound with standard commodity benchmarks (e.g. US natural gas, US livestock)

• A dynamic approach to sector allocation can improve significantly on the inflation hedging suitability of commodity investments

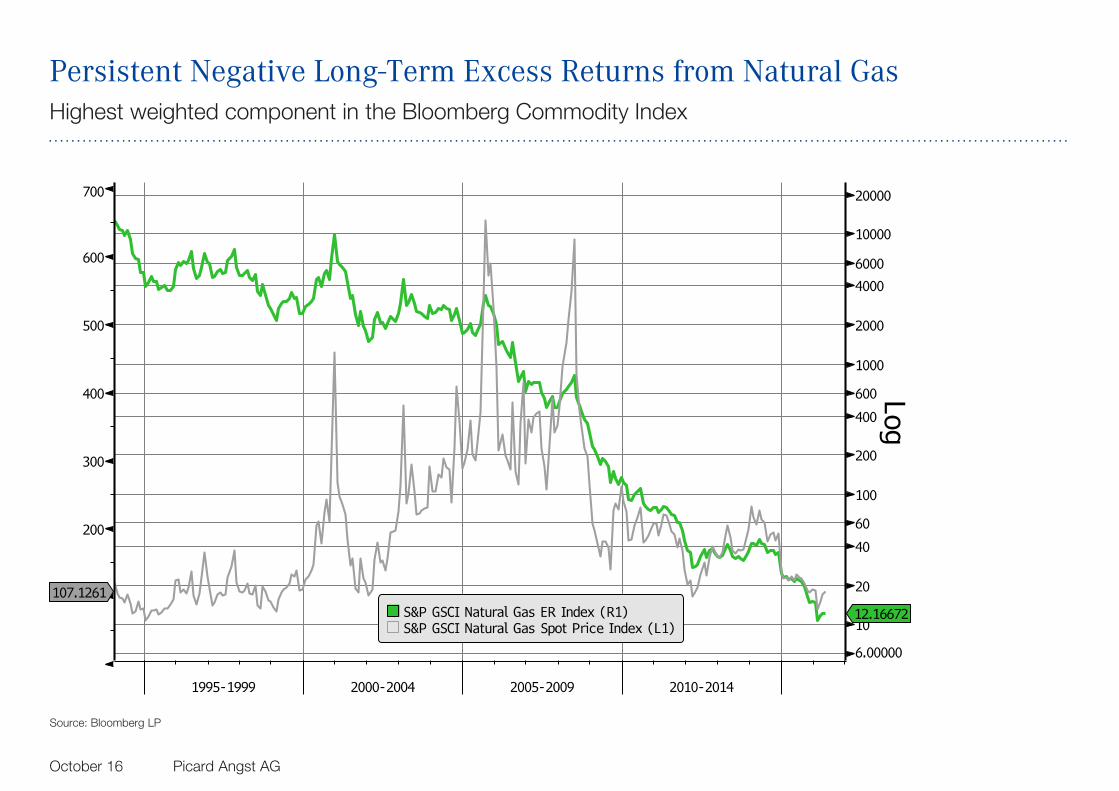

Persistent Negative Long-Term Excess Returns from Natural Gas

October 16 Picard Angst AG

Highest weighted component in the Bloomberg Commodity Index

Source: Bloomberg LP

Optimizing Commodity Exposure for Inflation Hedging

October 16 Picard Angst AG

Taking into account time-varying inflation sensitivity across commodity sectors

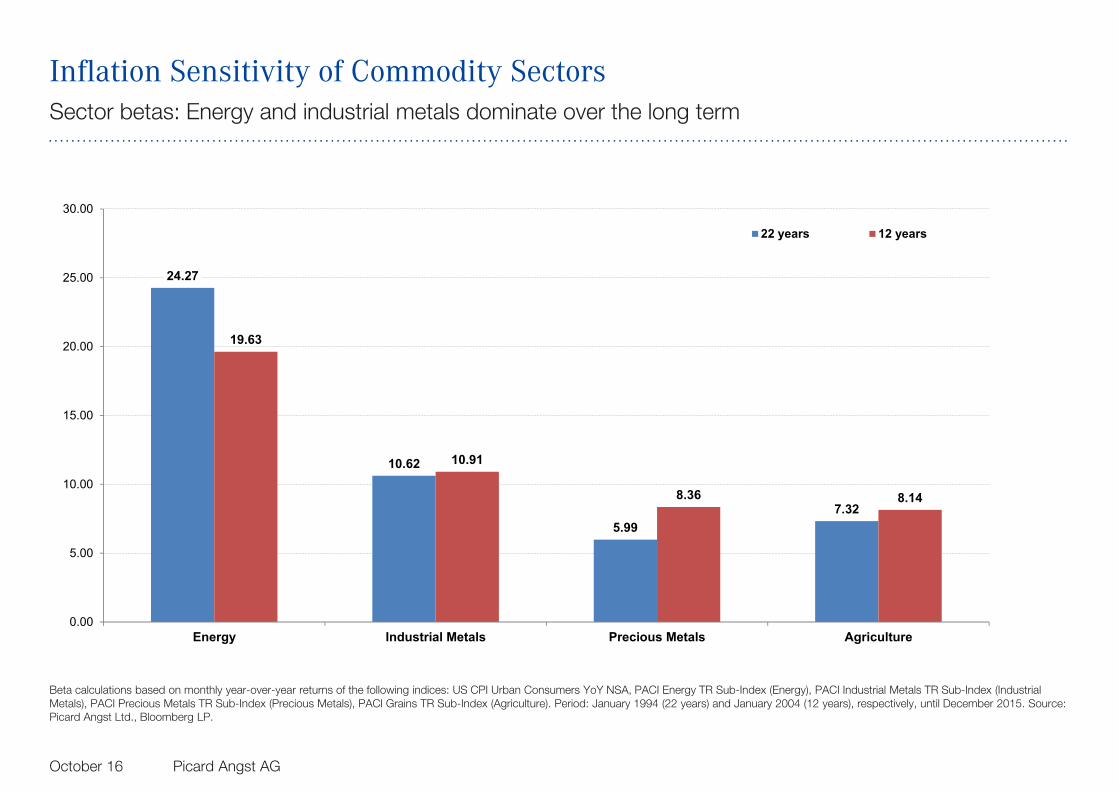

• Inflation sensitivity varies across commodity sectors

• Over the long term, energy and industrial metals exhibit the highest inflation betas

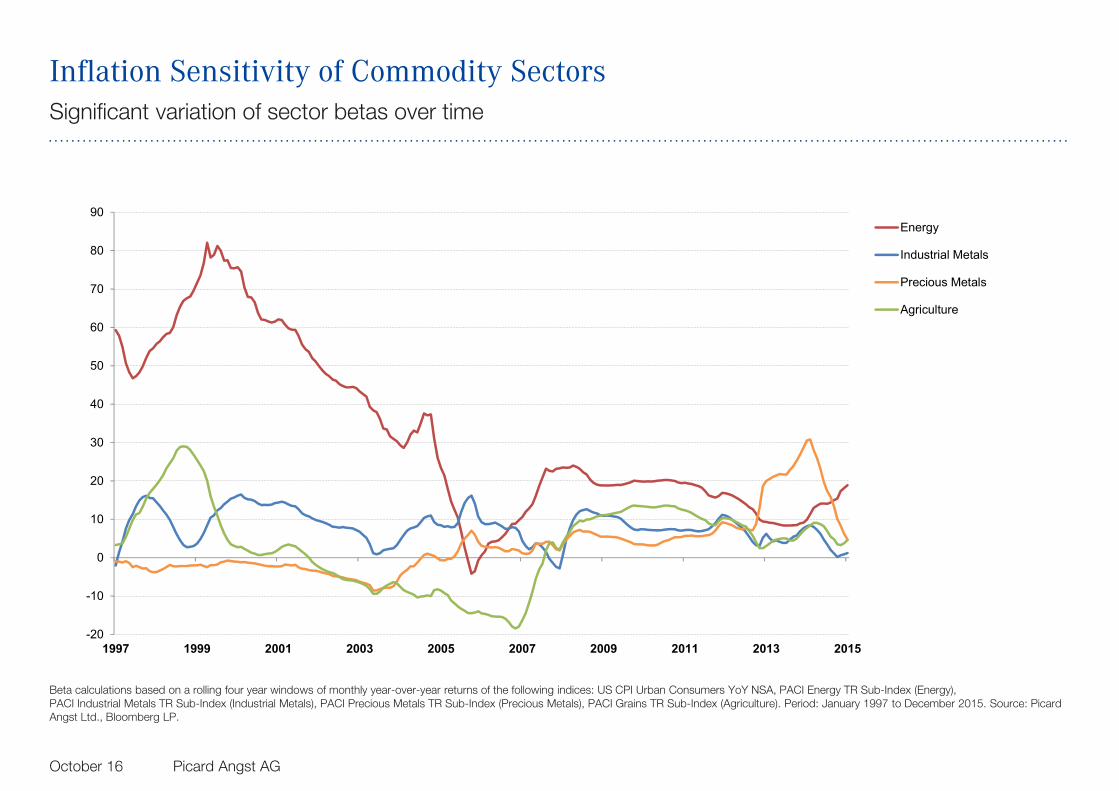

• However, betas do not remain stable over time and are subject to substantial volatility as a function of the economic cycle

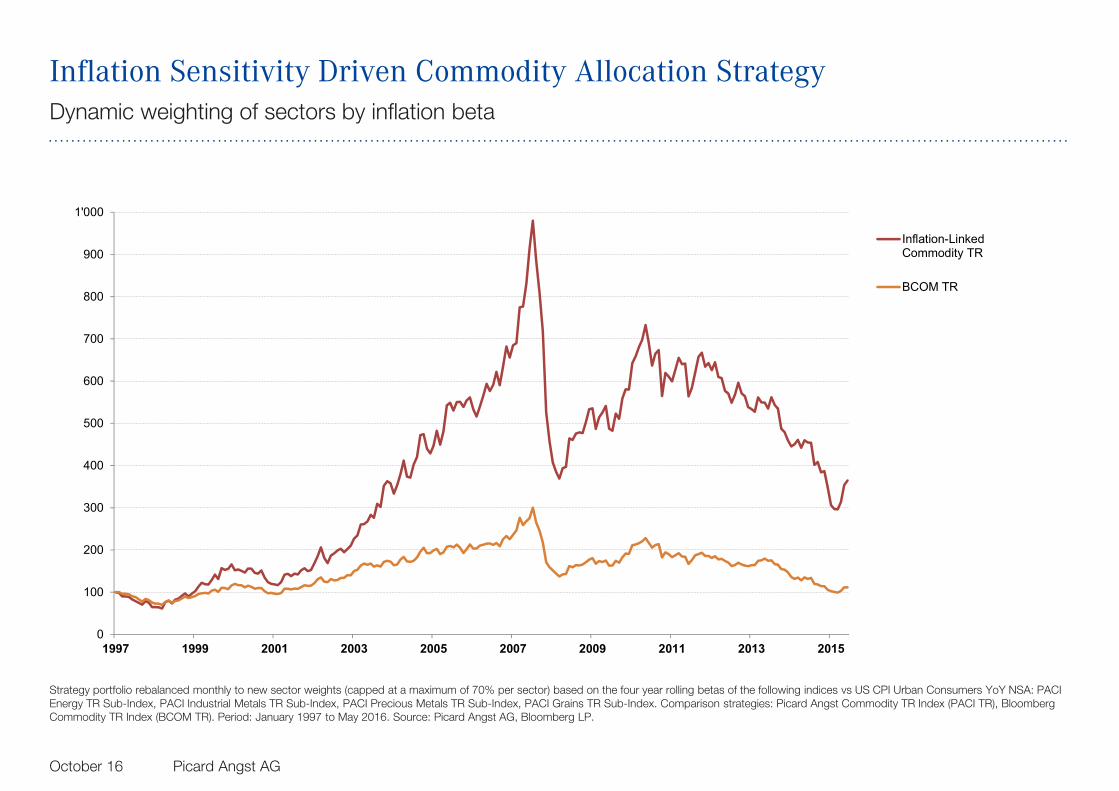

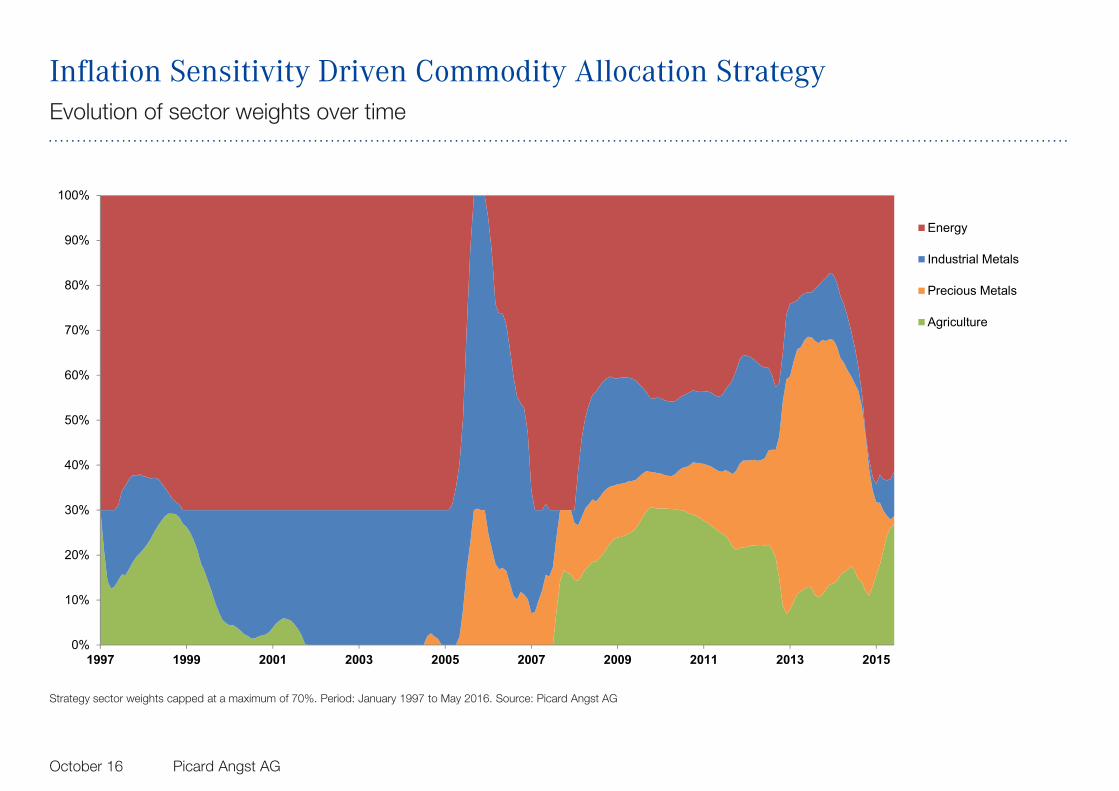

• Thus, if exposure to commodities is sought primarily as a defensive investment to take advantage of the pronounced inflation sensitivity of the asset class, portfolio construction should be driven by the time-varying inflation betas of the investment universe, e.g.

• Weighting of sectors energy, industrial metals, precious metals and agriculture (grains, softs) as a function of their respective dynamic inflation betas (subject to a sector weight cap of 70%)

• Monthly rebalancing of sector allocations

• Exclusion of commodity futures contracts from the investment universe that bear no relation to the European economy (notably NYMEX natural gas and the entire livestock sector)

Inflation Sensitivity of Commodity SectorsSector betas: Energy and industrial metals dominate over the long term

Beta calculations based on monthly year-over-year returns of the following indices: US CPI Urban Consumers YoY NSA, PACI Energy TR Sub-Index (Energy), PACI Industrial Metals TR Sub-Index (Industrial Metals), PACI Precious Metals TR Sub-Index (Precious Metals), PACI Grains TR Sub-Index (Agriculture). Period: January 1994 (22 years) and January 2004 (12 years), respectively, until December 2015. Source: Picard Angst Ltd., Bloomberg LP.

October 16 Picard Angst AG

24.27

10.62

5.997.32

19.63

10.91

8.36 8.14

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Energy Industrial Metals Precious Metals Agriculture

22 years 12 years

Inflation Sensitivity of Commodity SectorsSignificant variation of sector betas over time

Beta calculations based on a rolling four year windows of monthly year-over-year returns of the following indices: US CPI Urban Consumers YoY NSA, PACI Energy TR Sub-Index (Energy), PACI Industrial Metals TR Sub-Index (Industrial Metals), PACI Precious Metals TR Sub-Index (Precious Metals), PACI Grains TR Sub-Index (Agriculture). Period: January 1997 to December 2015. Source: Picard Angst Ltd., Bloomberg LP.

October 16 Picard Angst AG

-20

-10

0

10

20

30

40

50

60

70

80

90

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Energy

Industrial Metals

Precious Metals

Agriculture

Inflation Sensitivity Driven Commodity Allocation StrategyDynamic weighting of sectors by inflation beta

Strategy portfolio rebalanced monthly to new sector weights (capped at a maximum of 70% per sector) based on the four year rolling betas of the following indices vs US CPI Urban Consumers YoY NSA: PACI Energy TR Sub-Index, PACI Industrial Metals TR Sub-Index, PACI Precious Metals TR Sub-Index, PACI Grains TR Sub-Index. Comparison strategies: Picard Angst Commodity TR Index (PACI TR), Bloomberg Commodity TR Index (BCOM TR). Period: January 1997 to May 2016. Source: Picard Angst AG, Bloomberg LP.

October 16 Picard Angst AG

0

100

200

300

400

500

600

700

800

900

1'000

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Inflation-LinkedCommodity TR

BCOM TR

Inflation Sensitivity Driven Commodity Allocation StrategyEvolution of sector weights over time

Strategy sector weights capped at a maximum of 70%. Period: January 1997 to May 2016. Source: Picard Angst AG

October 16 Picard Angst AG

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Energy

Industrial Metals

Precious Metals

Agriculture

Contents

October 16 Picard Angst AG

Commodities - State of the Market and Asset Class 3

Portfolio Contribution – Diversification, Inflation Sensitivity, Risk Premium 10

Evolution of Commodity Beta Strategies 17

Alternative Risk Premia in Commodities 31

Summary 36

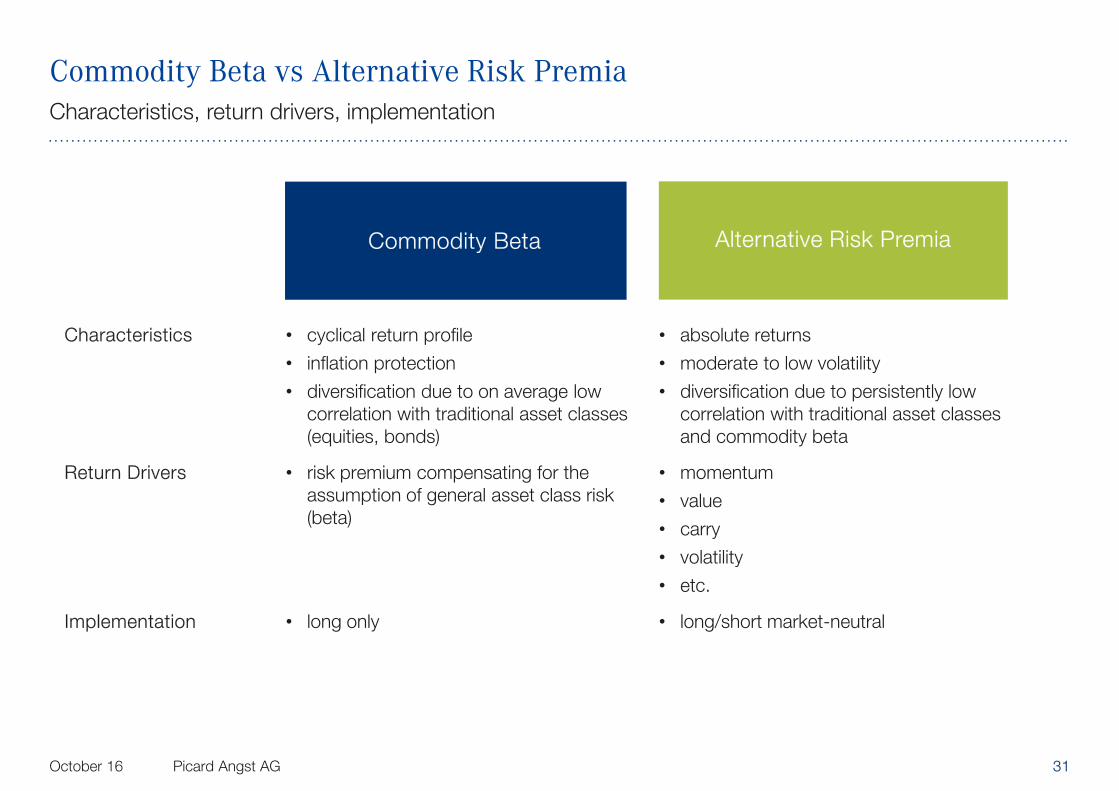

Commodity Beta vs Alternative Risk Premia

October 16 Picard Angst AG 31

Characteristics, return drivers, implementation

Commodity Beta Alternative Risk Premia

Characteristics • cyclical return profile

• inflation protection

• diversification due to on average low correlation with traditional asset classes (equities, bonds)

• absolute returns

• moderate to low volatility

• diversification due to persistently low correlation with traditional asset classes and commodity beta

Return Drivers • risk premium compensating for the assumption of general asset class risk (beta)

• momentum

• value

• carry

• volatility

• etc.

Implementation • long only • long/short market-neutral

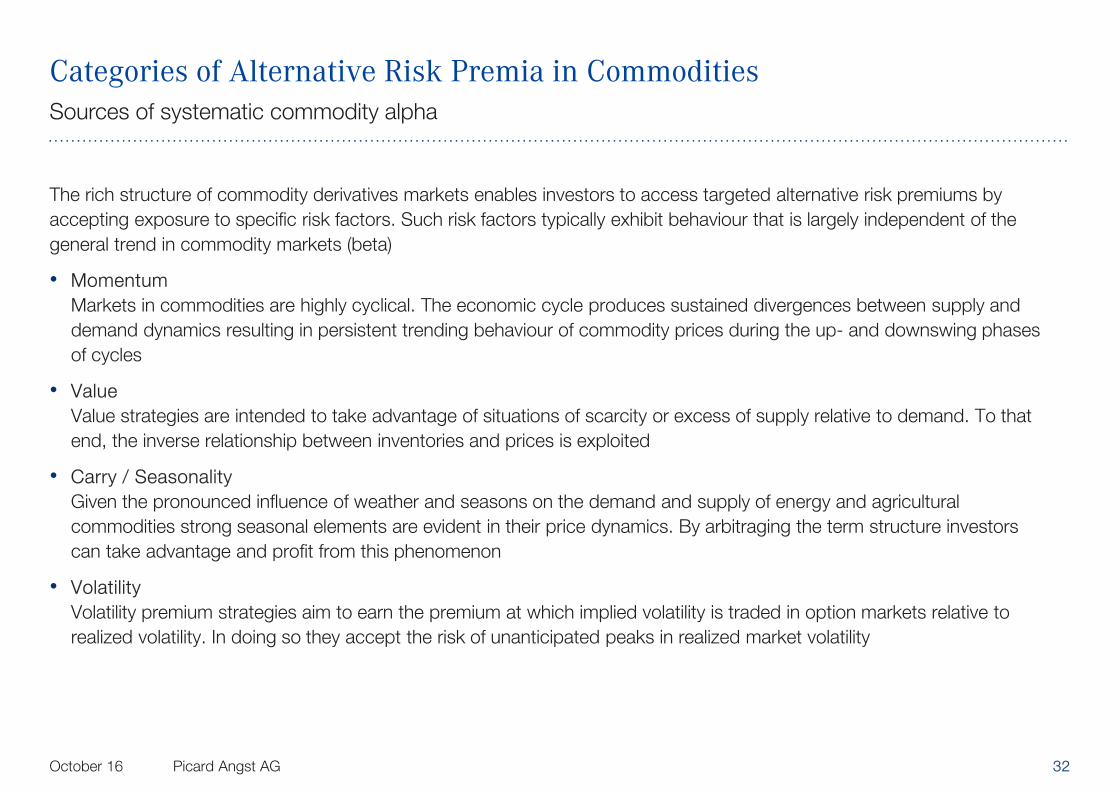

Categories of Alternative Risk Premia in Commodities

October 16 Picard Angst AG 32

Sources of systematic commodity alpha

The rich structure of commodity derivatives markets enables investors to access targeted alternative risk premiums by accepting exposure to specific risk factors. Such risk factors typically exhibit behaviour that is largely independent of thegeneral trend in commodity markets (beta)

• MomentumMarkets in commodities are highly cyclical. The economic cycle produces sustained divergences between supply and demand dynamics resulting in persistent trending behaviour of commodity prices during the up- and downswing phases of cycles

• ValueValue strategies are intended to take advantage of situations of scarcity or excess of supply relative to demand. To that end, the inverse relationship between inventories and prices is exploited

• Carry / SeasonalityGiven the pronounced influence of weather and seasons on the demand and supply of energy and agricultural commodities strong seasonal elements are evident in their price dynamics. By arbitraging the term structure investors can take advantage and profit from this phenomenon

• VolatilityVolatility premium strategies aim to earn the premium at which implied volatility is traded in option markets relative to realized volatility. In doing so they accept the risk of unanticipated peaks in realized market volatility

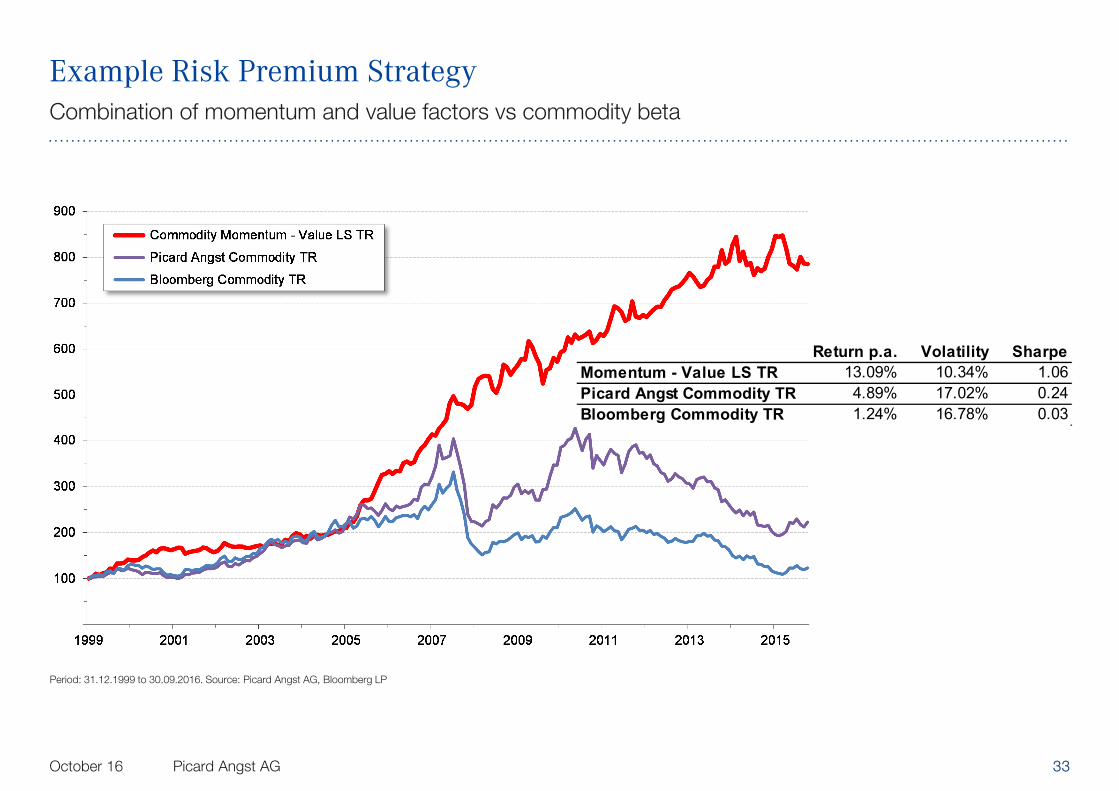

Example Risk Premium Strategy

October 16 Picard Angst AG 33

Combination of momentum and value factors vs commodity beta

Period: 31.12.1999 to 30.09.2016. Source: Picard Angst AG, Bloomberg LP

Return p.a. Volatility SharpeMomentum - Value LS TR 13.09% 10.34% 1.06Picard Angst Commodity TR 4.89% 17.02% 0.24Bloomberg Commodity TR 1.24% 16.78% 0.03

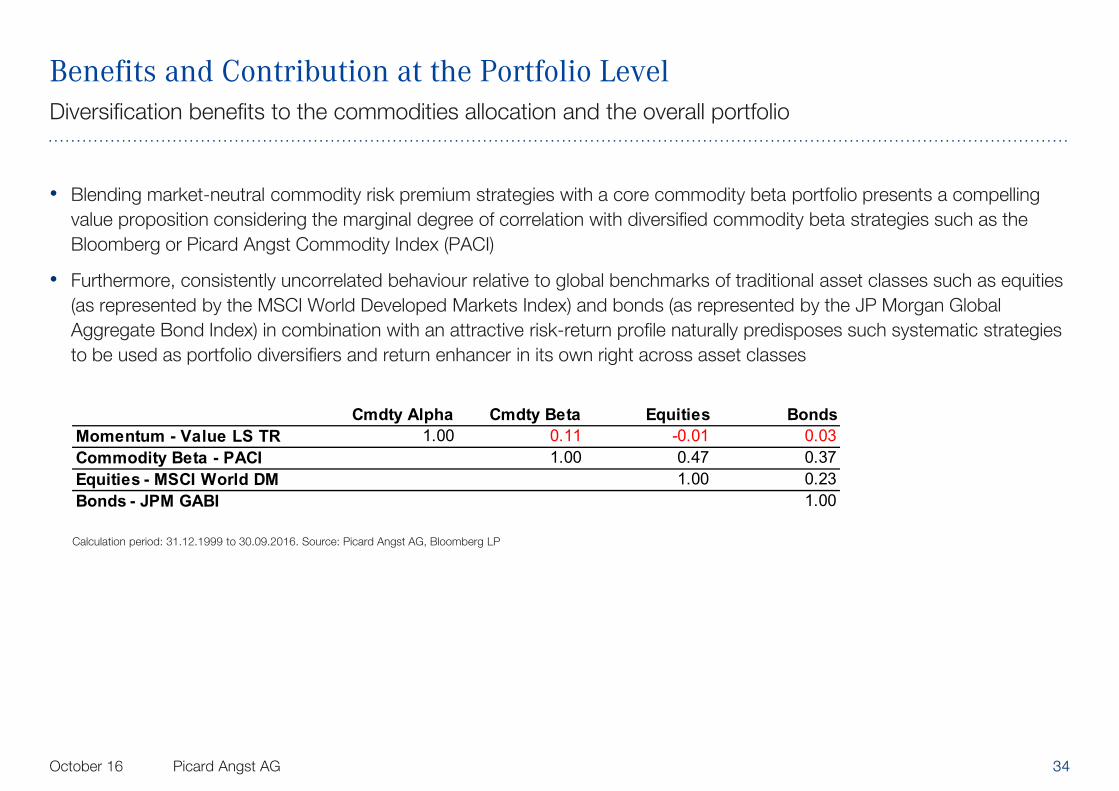

Benefits and Contribution at the Portfolio Level

October 16 Picard Angst AG 34

Diversification benefits to the commodities allocation and the overall portfolio

Calculation period: 31.12.1999 to 30.09.2016. Source: Picard Angst AG, Bloomberg LP

• Blending market-neutral commodity risk premium strategies with a core commodity beta portfolio presents a compelling value proposition considering the marginal degree of correlation with diversified commodity beta strategies such as the Bloomberg or Picard Angst Commodity Index (PACI)

• Furthermore, consistently uncorrelated behaviour relative to global benchmarks of traditional asset classes such as equities (as represented by the MSCI World Developed Markets Index) and bonds (as represented by the JP Morgan Global Aggregate Bond Index) in combination with an attractive risk-return profile naturally predisposes such systematic strategies to be used as portfolio diversifiers and return enhancer in its own right across asset classes

Cmdty Alpha Cmdty Beta Equities BondsMomentum - Value LS TR 1.00 0.11 -0.01 0.03Commodity Beta - PACI 1.00 0.47 0.37Equities - MSCI World DM 1.00 0.23Bonds - JPM GABI 1.00

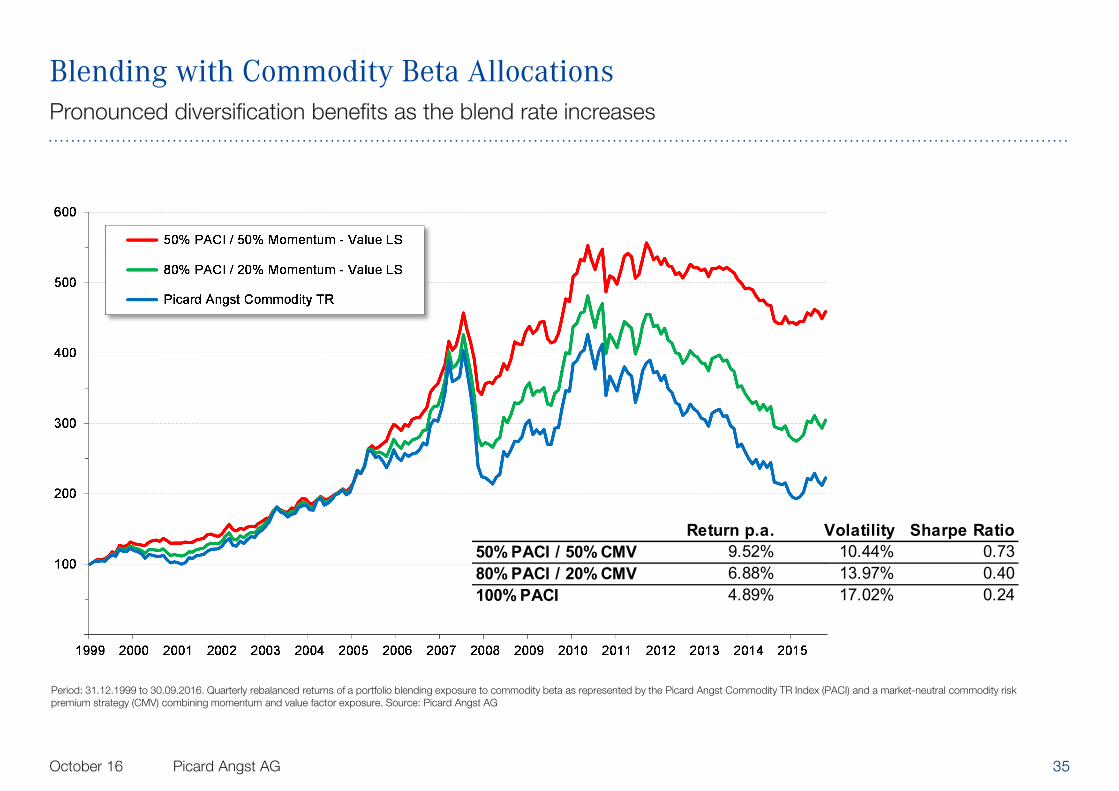

Blending with Commodity Beta Allocations

October 16 Picard Angst AG 35

Pronounced diversification benefits as the blend rate increases

Period: 31.12.1999 to 30.09.2016. Quarterly rebalanced returns of a portfolio blending exposure to commodity beta as represented by the Picard Angst Commodity TR Index (PACI) and a market-neutral commodity risk premium strategy (CMV) combining momentum and value factor exposure. Source: Picard Angst AG

Return p.a. Volatility Sharpe Ratio50% PACI / 50% CMV 9.52% 10.44% 0.7380% PACI / 20% CMV 6.88% 13.97% 0.40100% PACI 4.89% 17.02% 0.24

Summary

October 16 Picard Angst AG

• From a price perspective commodities markets may be near a cycle low. Market prices of the majority of commodities have declined deep into marginal production cost curves. Given the tepid global growth outlook, however, any sustained recovery will be driven initially by rationalization of excess supply

• The recent cycle downswing is not out of line with the historical record. Factors such as diversification potential and inflation sensitivity that originally prompted pension funds to include commodities in their strategic asset allocation retain validity

• The overwhelming majority of institutional asset invested in commodities continue to track standard benchmarks such as the Bloomberg or S&P GSCI Commodity indexes or enhanced variations thereof despite obvious deficiencies in their construction

• In order to mitigate the pronounced return cyclicality inherent to the asset class, institutional investors are well-advised to look beyond pure beta investment solutions to commodities and consider adding exposure to targeted alternative risk premia offered by the asset class

Thank you for your attention

37

Contact InformationDr. David-Michael Lincke, CFA, FRMHead of Portfolio Management

Picard Angst AGBahnhofstrasse 13 - 158808 Pfäffikon SZ, Switzerland

E-Mail: [email protected]: www.picardangst.com