chro cfo mmkt ebook

TRANSCRIPT

The CHRO/CFO Alliance: Nine Steps to a Powerful Partnership

In Search of Integrated Performance Management 1Five Areas Where CHROs and CFOs Agree 7Four Areas Where CHROs and CFOs Disagree 19

Our recent survey of more than 100 midsized company executives revealed clear intent for the finance and HR functions to work more closely and take advantage of opportunities to help teach and learn from each other.

We uncovered five areas where CHROs and CFOs completely agreed on how they should work together; we also identified four areas where CHROs and CFOs each thought their business partner has more to learn if he or she hopes to strengthen the partnership.

1

From a distance, the CHRO (chief HR officer) and CFO (chief financial officer) have a lot in common. First and foremost, they control the two most important resource streams in most organizations, money and people, as well as how those resources interact.

Both functions are non-revenue generating—serving at the “corporate center” on a mix of compliance and strategic value activities—and drive the performance management of the organization.

When CFOs and CHROs are tightly aligned, they wield great power and strategic influence. But when either function fails to assert its strategic impact or collaborate effectively, both often end up retreating to their functional comfort zones and talking in what might as well be Greek.

Even when CFOs and CHROs are working toward the same objectives and on the same initiatives, the unique functional expertise each position brings to the table often leaves them wondering “how my counterpart could possibly think that?”

In Search of Integrated Performance Management

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

2

When these two functions are not aligned, corporate performance suffers, which can often lead to finger pointing and frayed corporate culture.

In this challenging business environment, companies can no longer afford to have the heads of the two largest resource streams in the company misaligned. With pressure to achieve ever-increasing growth goals, a healthy working relationship between HR and Finance is no longer optional—it is essential.

3

CEB requested feedback and advice from CFOs and CHROs on business partner behavior that would improve their partnership. Across organizations and geographies, a common set of themes emerged.

This white paper shows which areas your peers and business partners said posed the greatest challenges, and it provides the tools and resources you can use to avoid future conflicts and form a productive business partnership.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

4

1. Strategy 2. Planning

Financial Objective

Strategic Objective Budgets

MetricsPlanning

HR Capability Planning

Performance Goals

Exec Comp

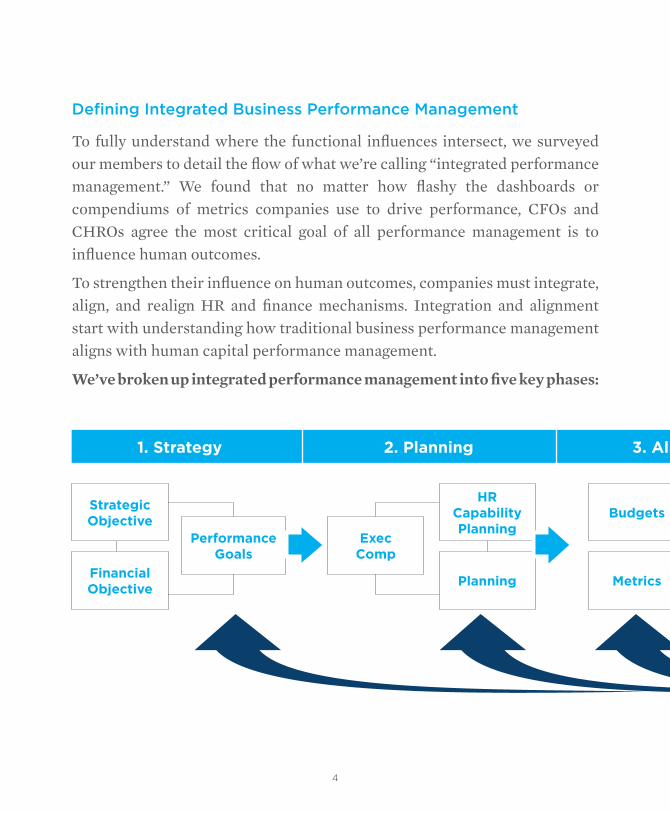

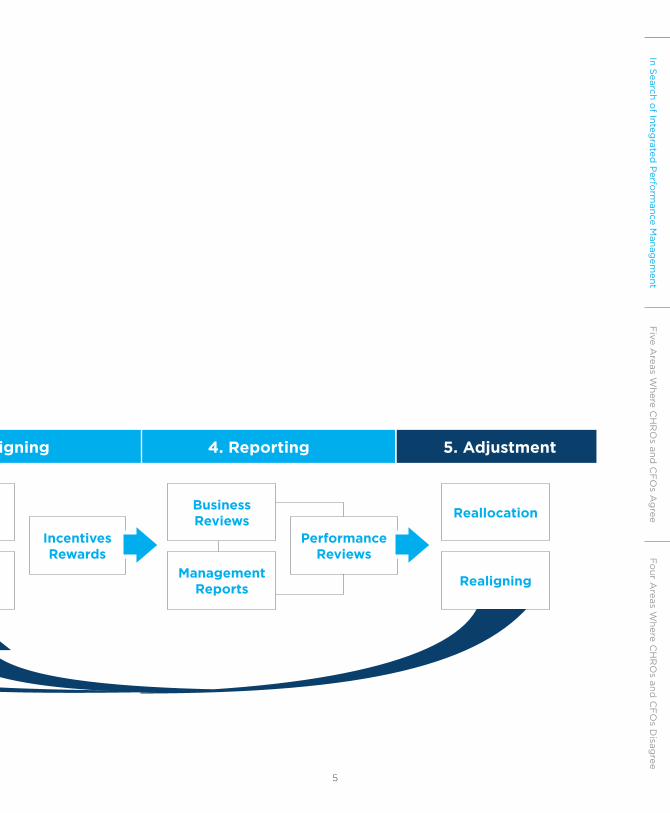

Defining Integrated Business Performance Management

To fully understand where the functional influences intersect, we surveyed our members to detail the flow of what we’re calling “integrated performance management.” We found that no matter how flashy the dashboards or compendiums of metrics companies use to drive performance, CFOs and CHROs agree the most critical goal of all performance management is to influence human outcomes.

To strengthen their influence on human outcomes, companies must integrate, align, and realign HR and finance mechanisms. Integration and alignment start with understanding how traditional business performance management aligns with human capital performance management.

We’ve broken up integrated performance management into five key phases:

3. Aligning

5

Budgets

Metrics

5. Adjustment

Reallocation

Realigning

3. Aligning 4. Reporting

Management Reports

Business Reviews

Incentives Rewards

Performance Reviews

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

6

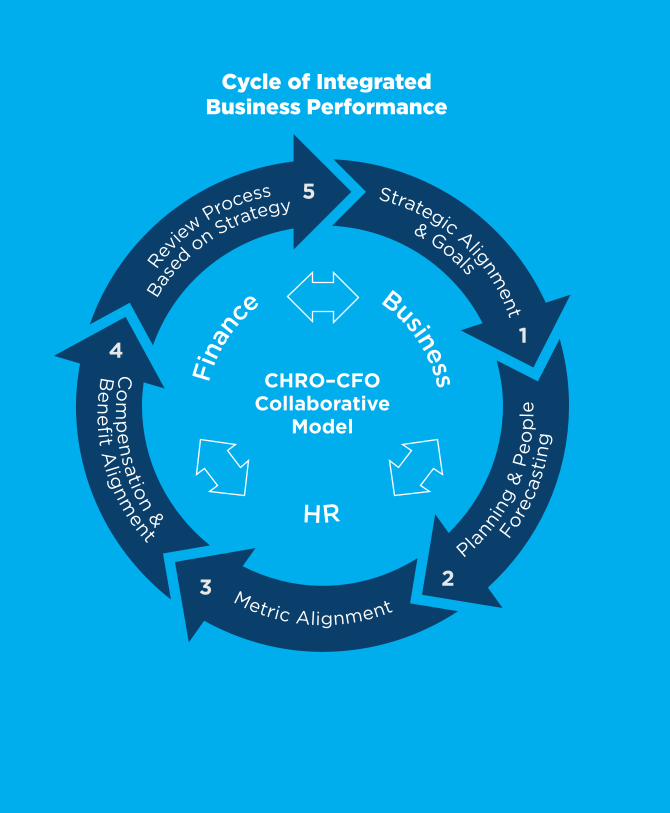

CHRO–CFO Collaborative

Model

4

3

1

2

5

Cycle of Integrated Business Performance

7

1. Engage and ally early in strategic planning to drive focus on a set of limited, realistic, and clearly defined strategic goals.

2. Integrate operational and workforce planning to create a connected, transparent process for resource allocation.

3. Teach the value of HR- and finance-functional metrics, and then collaborate to align metrics against company objectives.

4. Focus compensation and benefits decisions on driving behaviors aligned with strategic priorities.

5. Implement an ongoing review process that enables HR and Finance to coordinate on critical people decisions.

Five Areas Where CHROs and CFOs Agree

The model for integrated performance management is composed of five areas where both CFOs and CHROs realize the need to work together.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

8

1. Engage and ally early in strategic planning to drive focus on a set of limited, realistic, and clearly defined strategic goals.

In my experience, if Finance and HR aren’t highly involved in strategy formulation, the organization will make too

many uninformed bets and miss opportunities to drive value in new and innovative ways.” CFO, Electronics Industry

Successful collaboration begins with strategic alignment. To do that effectively requires CFOs and CHROs to rise above any functional viewpoint and recognize (whether there’s formal strategic planning or not) and agree on how the company intends to drive value. Then both functions have to be “at the table” as they co-own the management of the largest resource streams for the organization.

The functional heads must share a unified vision for corporate performance. Without clear goals, both sides often plan independently, adjustments are unclear, and both CFOs and CHROs retreat to running their functions instead of aligning their functions to drive business value.

CEB View

9

Potential Value of Strategy Versus Realized ValueIndexed

63%

100%

50%

0%Potential

ValueRealized

Value

100%

Source: McKinsey & Company; CEB analysis.

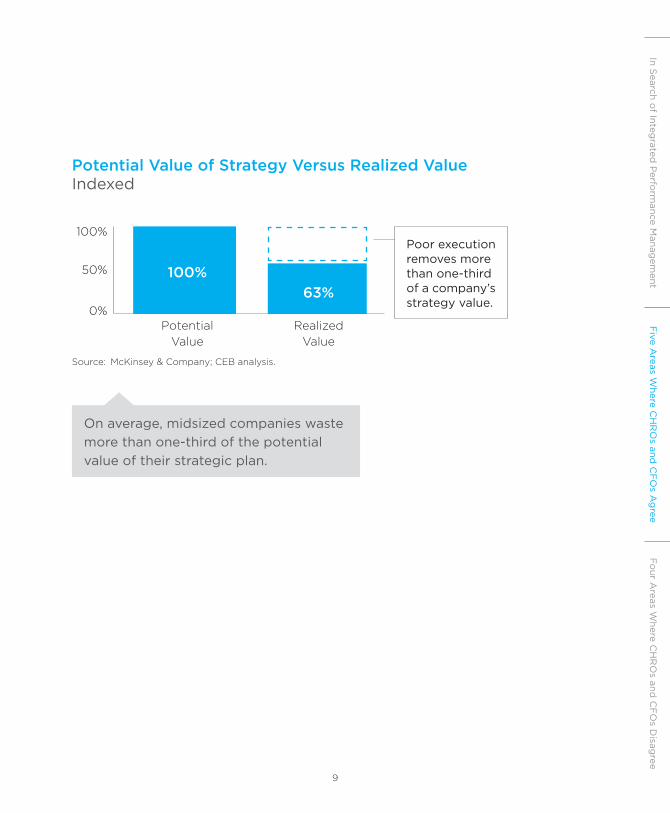

Poor execution removes more than one-third of a company’s strategy value.

On average, midsized companies waste more than one-third of the potential value of their strategic plan.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

10

Making resource decisions without HR’s input can lead to strategic failure with costly effects to the business in

terms of morale, productivity, and retention.” CHRO, Education Industry

CFOs and CHROs both must drive the business planning process by engaging the business, estimating resource risks, and discovering critical roadblocks. Workforce planning and operational planning cannot be done effectively in a separate environment. CFOs must learn the basics of workforce planning just as CHROs must learn the basics of business operational planning. Both heads must direct responsibility down to the business and assume the role of functional coaches. They must also work with the compensation committee to align senior leader compensation with long-term strategic objectives. Because it is almost impossible to align compensation perfectly to strategy, organizations should aim for directional fit and plan to review this alignment annually. Both CFO financial expertise and CHRO compensation and benefits expertise are necessary to execute and drive this process.

2. Integrate operational and workforce planning to create a connected, transparent process for resource allocation.

CEB View

11

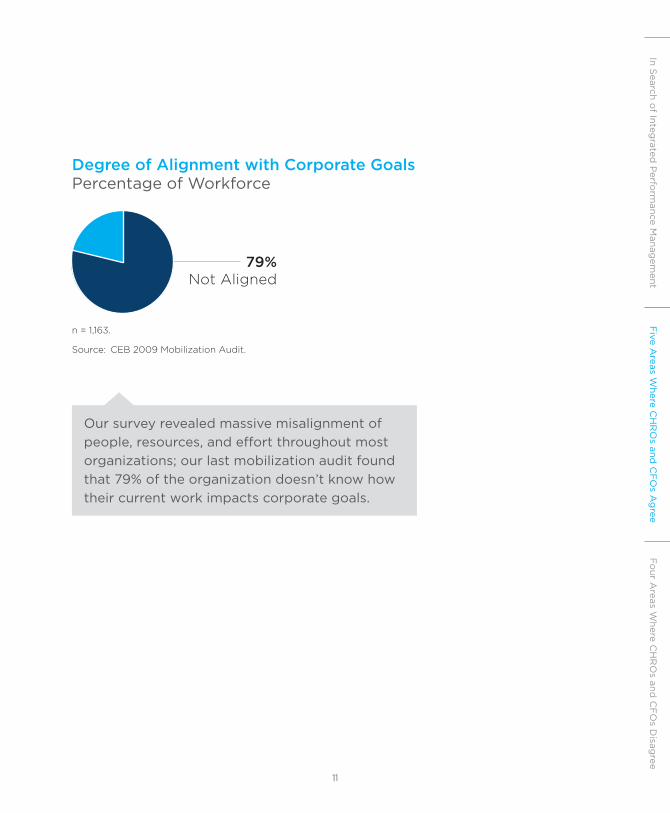

Our survey revealed massive misalignment of people, resources, and effort throughout most organizations; our last mobilization audit found that 79% of the organization doesn’t know how their current work impacts corporate goals.

79% Not Aligned

n = 1,163.

Source: CEB 2009 Mobilization Audit.

Degree of Alignment with Corporate GoalsPercentage of Workforce

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

12

3. Teach the value of HR- and finance-functional metrics, and then collaborate to align metrics against company objectives.

Companies that overly focus on financial metrics may achieve their short-term goals but neglect the capability building needed to drive long-term strategic direction. Finance must work with HR to engage the business in developing operational and human capital metrics that speak to the health of the organization, not just the financial goals. Success in this engagement requires both Finance and HR to understand metrics in all three areas, pressure-test them against the business, and adjust them as needed.

Many companies find success by implementing a balanced scorecard approach that Finance, HR, and the business review and update for relevance each quarter.

We should have joint buy-in on key people metrics linked to financial goals and strategic objectives so that we can

measure success and act quickly when we go off plan.” CHRO, Electronics

CEB View

13

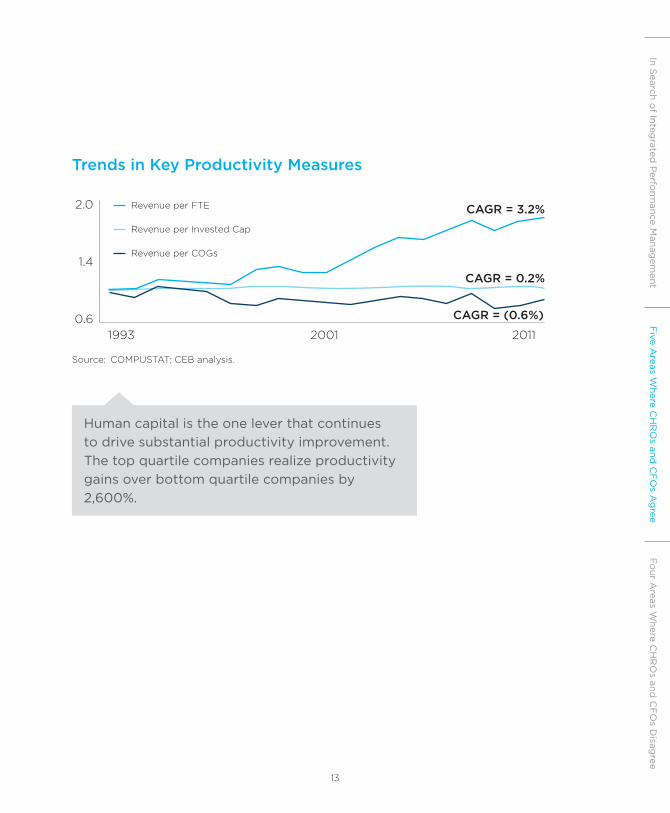

Source: COMPUSTAT; CEB analysis.

CAGR = 3.2%

CAGR = 0.2%

CAGR = (0.6%)

1993 2001 2011

2.0

1.4

0.6

Revenue per FTE

Revenue per Invested Cap

Revenue per COGs

Trends in Key Productivity Measures

Human capital is the one lever that continues to drive substantial productivity improvement. The top quartile companies realize productivity gains over bottom quartile companies by 2,600%.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

14

Compensation and benefits decisions have to originate from strategic intent and capability analysis. After clear goals are set, companies must understand the behaviors that will drive short- and long-term success and then align compensation with MBOs, clearly connecting outcomes to pay and STI payouts. The best companies are taking a step further by having leaders identify key collaboration points and tying those to outcomes as well. CHROs and CFOs must work closely together to ensure compensation and benefits are driving the right outcomes and behaviors. At leading companies, HR provides regular reporting on HR metrics and Finance analyzes effectiveness, the results of which drive collaboration. While it is important to focus on traditional compensation and benefits, our research shows that public recognition has double the impact on performance as that of rewards.

4. Focus compensation and benefits decisions on driving behaviors aligned with strategic priorities.

When compensation misaligns with strategic objectives, it often drives the wrong behaviors, such as rewarding salespeople for

bringing in revenue even if the customer is a poor strategic fit and/or costs too much to service.” CFO, Consumer Products Manufacturing Industry

CEB View

15

28% Agree

n = 294.

Source: CEB 2012 High Performance Survey.

Leaders Who Agree They Have Strong Line of Sight from Their Actions to Their RewardsPercentage of Leaders

Compensation fails to drive strategic value in most companies and actually incentivizes counterproductive decision making that degrades shareholder value. Only 28% of leaders believe they have a strong line of sight between their actions and rewards.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

16

Open communication begins with collaborating on key objectives and understanding how they translate into functional metrics and goals. Beyond that, CHROs and CFOs must understand that functional expertise doesn’t translate easily. CFOs need to understand that effective financial analysis exists to start the right conversations and drive the right behaviors. If the numbers aren’t starting the right conversations, being understood, or driving the right behaviors, they aren’t helping the business. CHROs must realize that the value of HR processes isn’t easily understood outside the HR world; if you’re talking or reporting in functional jargon or being too functionally specific, you’re likely having the wrong conversations and creating misunderstanding.

CFOs and CHROs both need to be involved, at the very least, in joint quarterly meetings with the business to understand what shifts are occurring and what those shifts mean from a human capital and finance perspective. Many companies are holding monthly strategy reviews, run by the CFO, to help CHROs understand where risks and opportunities lie.

5. Implement an ongoing review process that enables HR and Finance to coordinate on critical people decisions.

When we’re chasing our quarterly targets, HR often becomes disconnected from the day-to-day business operations and financial

outcomes, which results in poor decision making and an inability to adjust to changes in the environment.” CHRO, Financial Services Industry

CEB View

17

n = 294.

Source: CEB Customer Effort Reduction Survey.

65.4% Interpretation

34.6% Actual Delivery

Interpretation Drives Effectiveness

Our research shows that 66% of perceived value from service resides in the way service is communicated; yet CFOs and CHROs often default to functional speak, and most don’t set up a cadence of review cycles to ensure alignment of key objectives.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

18

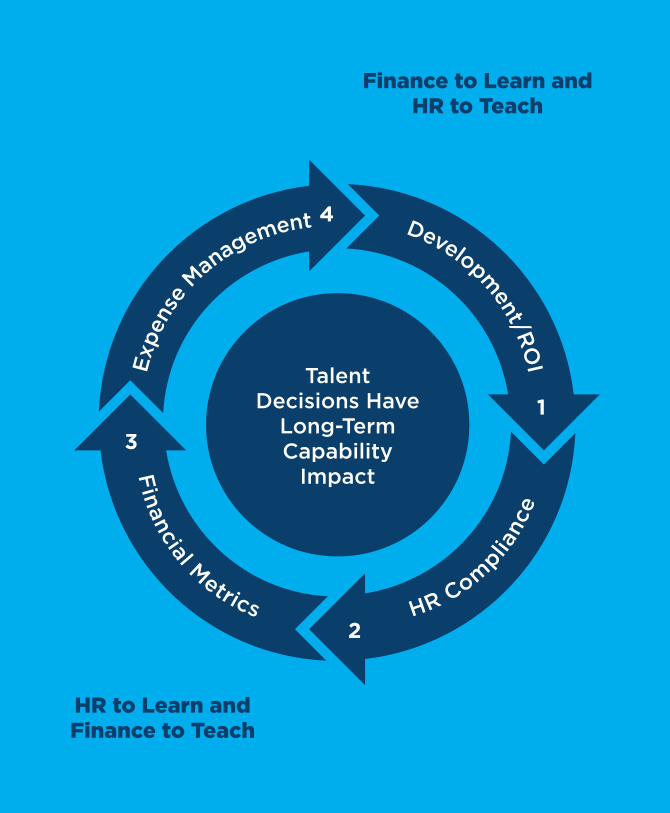

HR to Learn and Finance to Teach

Finance to Learn and HR to Teach

4

31

2

TalentDecisions Have

Long-Term Capability

Impact

19

Four Areas Where CHROs and CFOs Disagree

1. CHROs want CFOs to understand that development has strategic value beyond a direct ROI.

2. CHROs want CFOs to understand that labor laws can limit HR action.

3. CFOs believe the HR team needs to strengthen its knowledge of quantitative metrics.

4. CFOs want assurance that CHROs closely monitor and report details on head count and expenses.

Our survey also uncovered four areas that CFOs and CHROs view differently and believe their partner should strengthen their expertise in for better collaboration.

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

20

HR needs to understand the complexity in the way Finance thinks about things—cash cost versus allocated cost, current year spend versus run-rate

spend, etc. Often, meetings with HR take five tries because the analysis or presentation isn’t thought through.” CFO, Business Services Industry

1. CFOs believe the HR team needs to strengthen its knowledge of quantitative metrics.

CFOs should expect CHROs to have the financial expertise to engage in cost–benefit analysis and, if necessary, should assist in strengthening the financial acumen of the HR team.

But Finance has to understand the limitations of “communication by metrics.” Executives at forward-thinking companies work together to identify knowledge gaps and to develop metric fluency in HR, and doing so helps Finance understand when it is failing to communicate effectively.

The CFO View

CEB View

21

Many HR leaders do not feel responsible for the overall costs of personnel and simply follow requests for hiring from other senior managers within

the company. One of the critical dependencies between HR and Finance relates to head count planning. HR should be regularly aware of near- and mid-term hiring plans, not only for recruiting and sourcing but also so they can regularly evaluate the organizational structure for necessary adjustments.” CFO, Business Services Industry

2. CFOs want assurance that CHROs closely monitor and report details on head count and expenses.

CFOs and CHROs need to involve the line not only in business planning but also in workforce planning. CHROs and CFOs often start out on different pages, resulting in budget-busting siloed decisions throughout the year. CHROs have to work with the line to set realistic expectations and then continually update and communicate workforce needs—from a business perspective—to Finance to allow for disciplined decision making.

The CFO View

CEB View

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

22

HR navigates compliance issues at federal, state, and local levels. Our compliance with those regulations drives how we handle various pay

issues. Complacency in dealing with policy and procedural adherence can create unnecessary additional expense, and sometimes problems can surface later when the cost has become substantial.” CHRO, Food Industry

3. CHROs want CFOs to understand that labor laws can limit HR action.

CFOs must understand that there are mandatory HR compliance expenses that can’t be shortchanged. The legal expenses resulting from noncompliance can far outweigh any preventative expenses. However, HR has to understand that leading with “no” can frustrate business. Executives can collaborate to find a way around the compliance issue that saves money and drives business value.

CEB View

The CHRO View

23

The ROI of HR initiatives is very difficult to accurately demonstrate and easy to shoot holes through. On some level, CFOs must believe that

investing in people initiatives has payback in employee engagement and satisfaction. CFOs need to be open to the intangible value of an engaged, motivated, and committed workforce.” CHRO, Banking Industry

4. CHROs want CFOs to understand that development has strategic value beyond a direct ROI.

To hit aggressive growth targets, most companies must invest in training to fill critical capability gaps. Often that training is essential to strategy, but it lacks a clear, hard ROI. CFOs should recognize the value in strategic development and the critical business risk that skill capability gaps and succession represent. CHROs should teach the business how to identify capability gaps and work with it to create a clear and compelling case for development dollars based on business risk and opportunity rather than “development for development’s sake.”

CEB View

The CHRO View

In Search o

f Integrated

Perfo

rmance M

anagem

entF

ive Areas W

here CH

RO

s and C

FO

s Ag

reeF

our A

reas Where C

HR

Os and

CF

Os D

isagree

© 2014 CEB. All rights reserved. CEB8461914SYN

Scott EnglerManaging Director

Scott Engler is a senior member of CEB’s advisory team, working with CEB’s strategy, finance, and leadership programs for midsized companies.

Scott specializes in C-Level executive advisement in strategy development, alignment, leadership, and execution. He has advised senior leadership at over 100 organizations in strategy development and innovation, M&A targeting and integration, risk management, and talent management.

In addition to his advisory work, Scott creates and leads leadership training for senior executives, managers, and finance professionals, and he regularly speaks at conferences and leads CFO and CHRO executive retreats. Scott is consistently rated as one of CEB’s most effective speakers.

Isabel EcksteinResearch Analyst

Isabel Eckstein is a research analyst with CEB HR Leadership Council™ for Midsized Companies. She works with HR leaders at midsized companies worldwide to determine solutions to their greatest organizational challenges. She works with HR leaders at midsized companies worldwide to determine solutions to their greatest organizational challenges. In addition, Isabel publishes a membership-wide monthly newsletter, recommending tailored tools and research to thousands of HR leaders and their teams.

CEB Staff