chapter20 corporate restructuring

TRANSCRIPT

CONTEMPORARY FINANCIAL MANAGEMENT

Chapter 20:

Corporate Restructuring

INTRODUCTION

This chapter focuses on forms of corporate restructuring, including external expansion (mergers) and business failure (bankruptcy).

2

TYPES OF COMBINATIONS

Merger (or Acquisition) Vertical Horizontal Conglomerate

Geographic market Product extension Pure

Consolidation Holding company Joint venture

3

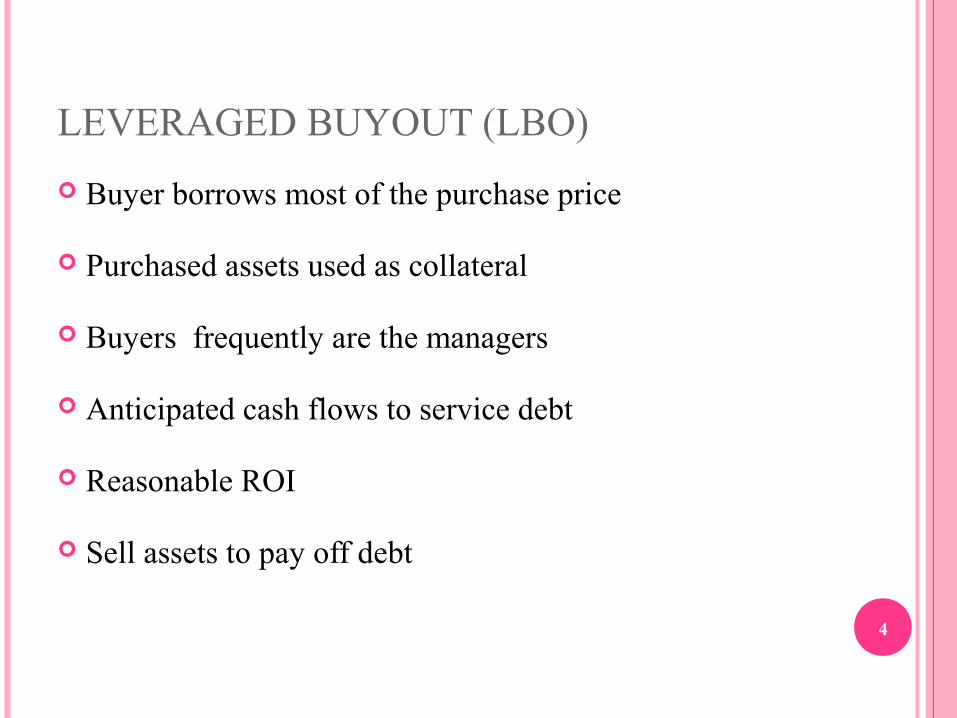

LEVERAGED BUYOUT (LBO)

Buyer borrows most of the purchase price

Purchased assets used as collateral

Buyers frequently are the managers

Anticipated cash flows to service debt

Reasonable ROI

Sell assets to pay off debt

4

TYPES OF MERGERS

Share Purchase

Acquiring company buys the stock of the target company. Assumes liabilities of the acquired firm

5

TYPES OF MERGERS

Asset Purchase

Acquiring company buys assets of target company NO assumption of liabilities

6

TYPES OF MERGERS

Tender Offer/Hostile Takeover

Purchase the common stock of the target company Offering price is greater than the market price

Induce shareholders to sell

7

WHAT HAPPENS AFTER A MERGER? Divestitures

Part of the company sold for cash Spin-off Equity carve-out

Restructurings Operational Financial

8

POPULARITY OF RESTRUCTURING

Failure of internal control mechanisms Unproductive investment Organizational inefficiencies

Large active investors

Available financing

Long economic expansion Increased revenues Increased asset values

9

ANTI-TAKEOVER MEASURES

10

Staggering board

Golden parachutes

Supermajority rule

Poison pills

White knight

Standstill agreement

“Pacman” defense

Litigation

Asset/Liability restructuring

BOARDMAIL Institutional investors use it to fight

anti-takeover devices

Requires the board of directors to adopt weaker anti-takeover measures

In exchange for voting support from institutional owners

Vote in sympathetic board members

11

WHY FIRMS SEEK EXTERNAL GROWTH Less Expensive

Achieve economies of scale

Vertical merger

Rapid growth

Diversification

Tax-loss carryforward

12

TAXES ON MERGERS Cash or debt securities

Gains are usually taxable at the time of the merger

Equity securities Usually tax-free

13

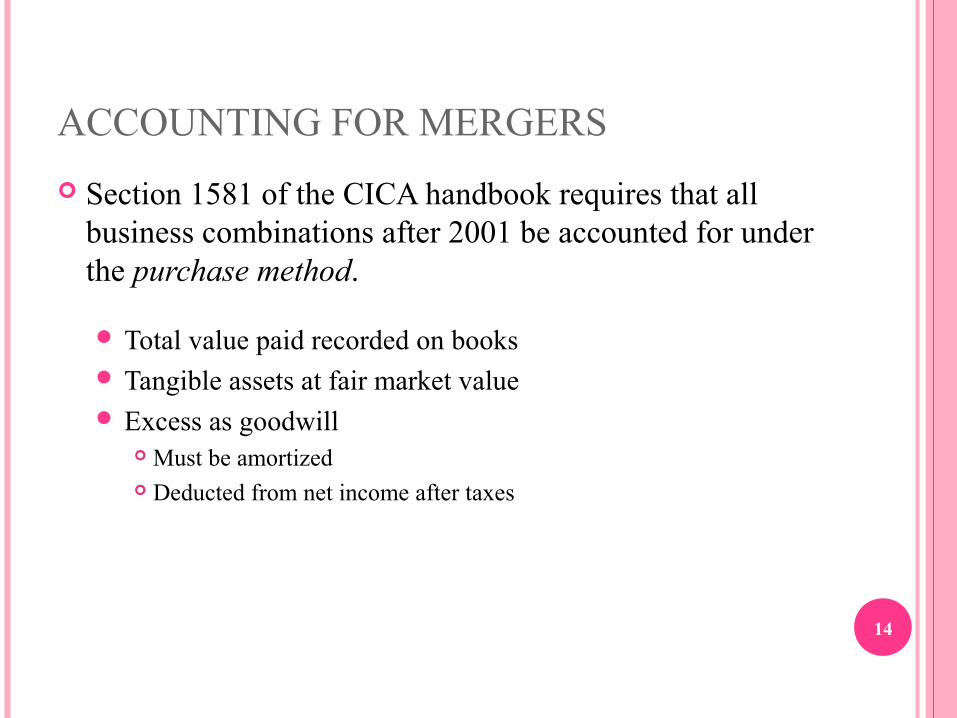

ACCOUNTING FOR MERGERS

Section 1581 of the CICA handbook requires that all business combinations after 2001 be accounted for under the purchase method.

Total value paid recorded on books Tangible assets at fair market value Excess as goodwill

Must be amortized Deducted from net income after taxes

14

VALUATION OF A MERGER CANDIDATE

Comparative P/E Ratio Method Examines prices and P/E ratios of similar companies

Adjusted Book Value Method Determine market value of the company’s assets

Discounted Cash Flow Method Uses capital budgeting techniques to find the Present value of

the free cash flows

15

EPS OF THE SURVIVING COMPANY

( )1 2 1,2

C1 2

EAT + EAT + EATEPS =

NS + NS ER

16

EPSc = Earnings per share (combined companies)EAT1 = Earnings after taxes (acquiring company)EAT2 = Earnings after taxes (target company)EAT1,2 = Synergistic earnings from mergerNS1 = Shares outstanding (acquiring company)NS2 = Shares outstanding (target company)ER = Exchange ratio

Post-merger common share price and P/E ratio determined by the financial markets

BUSINESS FAILURE

Two federal laws govern business failure:

The Bankruptcy and Insolvency Act (BA) Companies’ Creditors Arrangement Act (CCAA)

17

FAILURES Technically insolvent

Unable to meet current obligations

Legally insolvent Assets are less than liabilities

Bankrupt Unable to pay debts Files for protection under federal bankruptcy laws

18

REASONS WHY FIRMS FAIL

Business risk

Industry downturns Over expansion Inadequate sales Increased competition Technological change

19

REASONS WHY FIRMS FAIL

Financial risk

Excessive leverage Too much short-term debt Poor management of accounts receivable Poor management of accounts payable Incompetent management

20

ALTERNATIVES FOR FAILING BUSINESSES

21

Resolve itsDifficulties(informally) Declare

Bankruptcy(formally)

REORGANIZATION VS LIQUIDATION Legal bankruptcy proceedings focus on whether the failing

firm should be reorganized or liquidated

Reorganize if going-concern value exceeds its liquidation value

Liquidate if liquidation value is more than its going-concern value

22

ALTERNATIVES FOR CASH FLOW PROBLEMS

Negotiate accounts payable deferrals

Restructure debt Extension Composition

Sell off assets Real estate/operating divisions

Sale and leaseback

Creditors’ committee

Assignment23

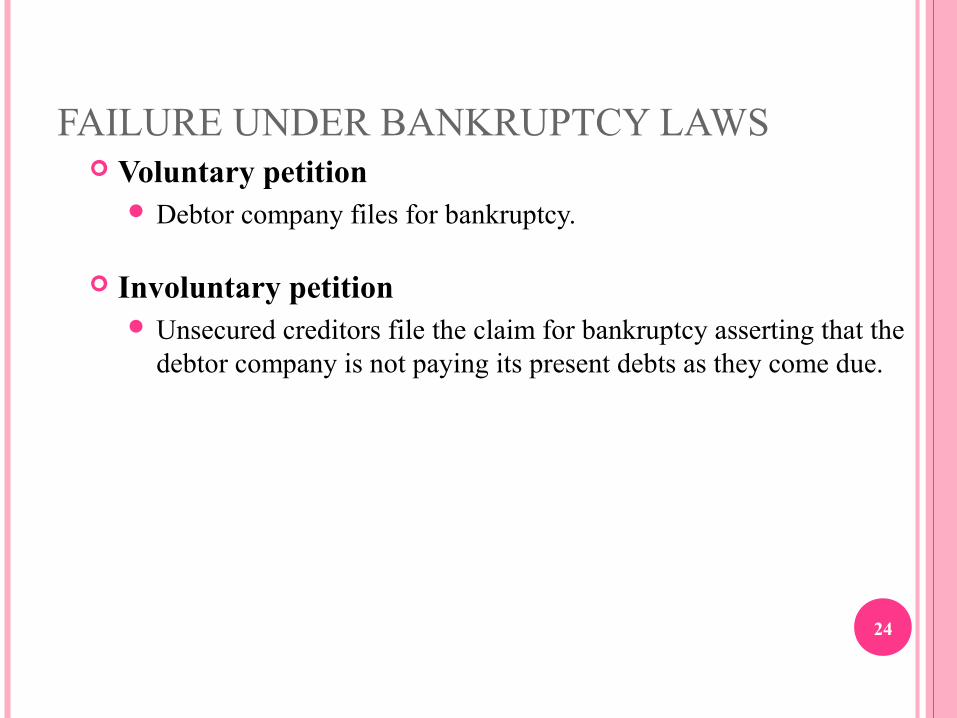

FAILURE UNDER BANKRUPTCY LAWS Voluntary petition

Debtor company files for bankruptcy.

Involuntary petition Unsecured creditors file the claim for bankruptcy asserting that the

debtor company is not paying its present debts as they come due.

24

PRIORITIES Administration expenses Wages owed six months prior to bankruptcy (maximum

$2000) Municipal taxes owed within 2 years preceding bankruptcy Rent for preceding 3-month period General/unsecured claims, including taxes due the Crown Preferred shareholders Common share holders

25

MAJOR POINTS

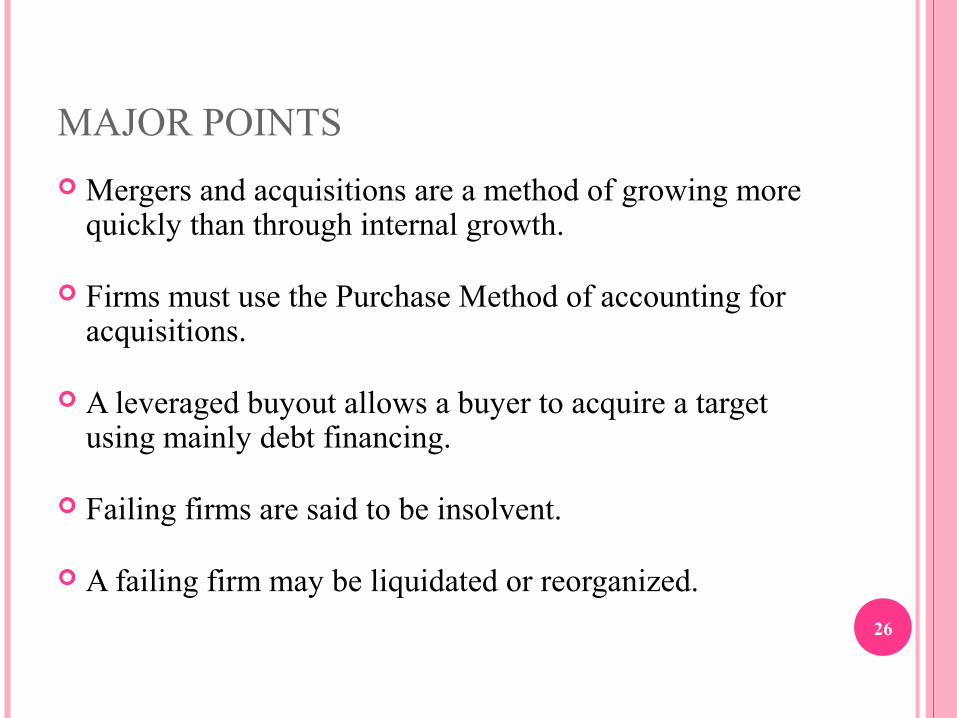

Mergers and acquisitions are a method of growing more quickly than through internal growth.

Firms must use the Purchase Method of accounting for acquisitions.

A leveraged buyout allows a buyer to acquire a target using mainly debt financing.

Failing firms are said to be insolvent.

A failing firm may be liquidated or reorganized.26