chapter – v determinants of customer...

TRANSCRIPT

150

Chapter – V

DETERMINANTS OF CUSTOMER SATISFACTION IN BANK: APPLICATION OF FACTOR ANALYSIS

5.1. INTRODUCTION

Satisfaction is an attitude or evaluation that is formed by the customer comparing

their pre-purchase expectations of what they would receive from the product to

their subjective perceptions of the performance they actually did receive. Several

authors have defined satisfaction in a different way. Satisfaction is a person’s

feeling of pleasure or disappointment resulting from comparing a product’s

perceived performance (or outcome) in relation to his or her expectations. It is a

function of consumer’s belief that he or she was treated fairly. Satisfaction is

determined by the discrepancy between perceived performance and cognitive

standards such as expectations and desires. Customers’ expectation can be defined

as customer’s pretrial beliefs about a product. Expectations are viewed as

predictions made by consumers about what is likely to happen during impending

transaction or exchange. Perceiver performance is defined as customer’s

perception of how product performance fulfills their needs, wants and desire.

Customer satisfaction is a function of perceived quality and disconfirmation – the

extent to which perceived quality fails to match repurchase expectations.

Customers compare the perceived performance of a product (service, goods) with

some performance standard. Customers are satisfied when the perceived

151

performance is greater than the standard (positively disconfirmed), whereas

dissatisfaction occurs when the performance falls short of the standard (negatively

disconfirmed). It is a collective outcome of perception, evaluation and

psychological reactions to the consumption experience with a product/service. It is

a measure of how products and services supplied by a company to meet or surpass

customer expectation. It is the provision or transfer of goods, services and ideas in

return for something of value.

Customer Satisfaction is the gratification or the state of feeling pleasure or the act

of fulfilling a need or desire of customers. It is the degree to which there is match

between the customer's expectations and the actual performance. Satisfying

customer means (i) knowing the customers, their needs, testes and preferences (ii)

delivering services as per their requirements with a view to minimize actual and

expectation gap for changing their perception towards the services, which will

pave the way to enhanced customer satisfaction level.

It is considered to be one of the most important competitive factors for the future,

and is the best indicator of a bank’s profitability, which drives a firm to improve

their reputation and image, to reduce customer turnover, and to increase attention

to customer needs. For a banking industry, the whole spectrum of activity and

income generation revolves round the customer. Customer service is of paramount

importance if banks have to survive and thrive in the present competitive

environment. The dynamic nature of the market, coupled with an increased

number of more demanding and affluent consumers, brought greater challenges to

bankers in retaining their customers.

Customer satisfaction is the only ‘mantra’ for banks for its sustainable growth and

152

development. In today’s competitive marketing environment, when customers

have many alternatives to choose from to better satisfy their needs, customer

loyalty is crucial for banks. Customers who are just satisfied find it easy to switch

service provider when a better offer comes along. As a result, the significance of

customer satisfaction is emphasized in markets where competition is intense. A

dissatisfied or merely satisfied customer is likely to switch over but highly

satisfied customer is likely to stay on due to brand loyalty. Customer satisfaction is

considered to affect customer retention and, therefore, competitiveness in banks.

Complete customer satisfaction is the key to securing customer loyalty and

generating superior long-term banking performance. It is also apparent that high

customer satisfaction leads to the strengthening of the relationship between a

customer and a bank, and this deep sense of collaboration has been found to be

profitable. The biggest challenge to Indian banks comes not from trade unions or

foreign banks but from customers who are demanding more. Rising expectations

from the customers and narrow margins of profit are challenges before the banking

industry as a whole.

There are overwhelming arguments that it is more expensive to win new

customers than to keep existing ones. Customer satisfaction is the base for

business expansion of the stiff competition prevalent in the banking industry. With

the advent of new banks in 1995, the concept of customer service has become an

important and pivotal issue in banks irrespective of public sector or private sector.

The survival of banking business is dependent on customer satisfaction. The focal

point of any service organization is customer satisfaction, more so in the banking

sector. The phrases such as ‘customer is the king of the businesses, ‘service to

customer is service to god’ is no more myth but turned out to reality for banking

153

sector. There are some controllable and uncontrollable factors directly or

indirectly affecting the level of customer satisfaction from the services rendered

by the banks.

Against this backdrop, the present chapter is exclusively aimed at identifying the

determinants of customer satisfaction from the services offered by the banks in the

area under study.

5.2. OBJECTIVE

The objective of the present chapter is –

To identify the factors responsible for determining the customer

satisfaction in respect of banking services.

5.3. METHODOLOGY: TOOL AND TECHNIQUES USED In order to determine the number of factors influencing customer satisfaction in

banks under the study and to know the relative strength of the each factor in

influencing the customer’s satisfaction level, the Factor Analysis (FA) was

performed with the help of SPSS software (version-15). To identify the common

dimensions of the variables, factor analysis technique has been applied. Factor

Analysis was used to identify the underlying dimensions or factors that actually

contribute to a number of observed attributes. It is a statistical approach that can

be used to analyze interrelationships among a large number of variables and to

explain these variables in terms of their common underlying dimensions (factors).

The statistical approach involves finding a way of condensing the information

contained in a number of original variables into a smaller set of dimensions

(factors) with a minimum loss of information.

154

5.4. FACTOR ANALYSIS The first step involves calculation of correlation matrix which exhibited the

interrelationship among the observed variables. To extract minimum number

of factors, Principal Component Analysis (PCA) with varimax rotation was

used. A Principal Component Analysis is a factor model in which the factors

are based upon the total variance. In addition to selecting the factor model, we

have specified how the factors are to be extracted in such a way that each factor

is independent of all other factors. Therefore, the correlation between the

factors is arbitrarily determined to be zero.

Further, to decide the number of factors to be extracted, the most commonly

used technique is referred as the latent root (eigen values) representing the

extent of variance in data. Now we have to interpret the factors, i.e., with

factor loading which were greater then 0.30 (ignoring the negative sings) and

loaded them in the extracted factors (Hair et. al, 2008). A factor loading is the

correlation between the original variables and the factors squared factor loading

indicate what percentage of the variance in an original variable is explained by

a factor. Finally, the factors based on appropriateness for representing the

underlying dimensions of a particular interpretation were suitably named. They

strongly influence the name or level selected to represent a factor. The 25

variables used for the factor analysis were coded. Moreover, to study the

appropriateness of factor analysis Kaiser-Meyer-Olkin (KMO) and Bartlett's

test statistic was used. If, the KMO value is greater than 0.6 is considered as

adequate (Kaiser and Rice, 1974).

155

Further, KMO measures the magnitude of observed correlation coefficients. A

value of greater then 0.5 is desirable. Bartlett's test measures the correlation of

variables. A probability of less than 0.5 is acceptable (Singh and Jain, 2009).

Table - 5.1: KMO and Bartlett's Test Result for Customer Satisfaction

Kaiser-Meyer-Olkin Measure of Sampling Adequacy .861

Bartlett's Test of Sphericity Approx. Chi-Square 4044.193

df 300

Sig. .000

Source: Computed from Primary Data.

From the table, it can be seen that KMO value is acceptable. Bartlett’s test result

also showed that the values were significant and thus acceptable. The items in the

respective category were individually subjected to Principal Component Analysis

(PCA) with varimax rotation and Kaiser Normalization using SPSS (version 15).

The items having factor loading less than 0.30 were eliminated (Hair et. al., 1995).

Finally, 7 factors comprising 25 items, all having eigen values of unity and above

were extracted and the results are shown. Further, in order to assess the

appropriateness of the data for factor analysis, the commonalities derived from the

factor analysis were reviewed. These were relatively larger (greater than 0.5),

suggesting that the data were appropriate (Stewart, 1981). The individual

dimensions of proposed instruments explained total variance exceeding 60 per

cent, suggesting the appropriateness of the process.

We have also tested the reliability of items by computing the coefficient alpha

(Cronbach, 1951), measuring the internal consistency of the items.

156

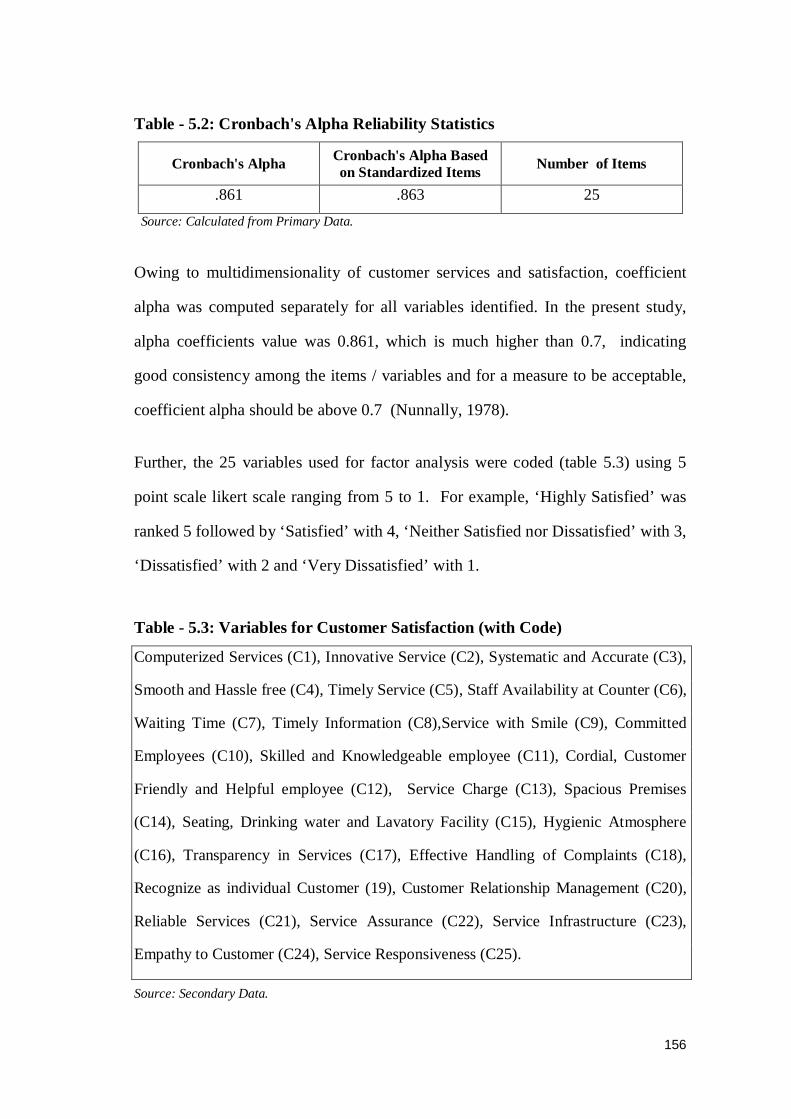

Table - 5.2: Cronbach's Alpha Reliability Statistics

Cronbach's Alpha Cronbach's Alpha Based on Standardized Items Number of Items

.861 .863 25 Source: Calculated from Primary Data.

Owing to multidimensionality of customer services and satisfaction, coefficient

alpha was computed separately for all variables identified. In the present study,

alpha coefficients value was 0.861, which is much higher than 0.7, indicating

good consistency among the items / variables and for a measure to be acceptable,

coefficient alpha should be above 0.7 (Nunnally, 1978).

Further, the 25 variables used for factor analysis were coded (table 5.3) using 5

point scale likert scale ranging from 5 to 1. For example, ‘Highly Satisfied’ was

ranked 5 followed by ‘Satisfied’ with 4, ‘Neither Satisfied nor Dissatisfied’ with 3,

‘Dissatisfied’ with 2 and ‘Very Dissatisfied’ with 1.

Table - 5.3: Variables for Customer Satisfaction (with Code)

Computerized Services (C1), Innovative Service (C2), Systematic and Accurate (C3),

Smooth and Hassle free (C4), Timely Service (C5), Staff Availability at Counter (C6),

Waiting Time (C7), Timely Information (C8),Service with Smile (C9), Committed

Employees (C10), Skilled and Knowledgeable employee (C11), Cordial, Customer

Friendly and Helpful employee (C12), Service Charge (C13), Spacious Premises

(C14), Seating, Drinking water and Lavatory Facility (C15), Hygienic Atmosphere

(C16), Transparency in Services (C17), Effective Handling of Complaints (C18),

Recognize as individual Customer (19), Customer Relationship Management (C20),

Reliable Services (C21), Service Assurance (C22), Service Infrastructure (C23),

Empathy to Customer (C24), Service Responsiveness (C25).

Source: Secondary Data.

157

5.4.1. Inter-correlation Matrix

The results of factor analysis are shown here and initially the inter-correlation

among the variables were calculated and presented in the table (table 5.4). Almost

all the cases, correlation coefficient of variables were found statistically

significant, hence included as the factor influencing the level of customer

satisfaction in respect of banking services.

Further, the table (table 5.5) exhibited the variable of column 1, which was not

correlated with or negatively correlated with the specific variable(s) of column 2.

Table - 5.5: Variables not Correlated with

Variables Not correlated with the variable(s) Computerized services (C1) (C19), Innovative service (C2) (C11), (C13)*, (C17), (C18), (C21)*, (C22) Systematic and Accurate services (C3) (C11), (C13), (C17), (C18), Smooth, hassle free (C4) (C17), (C21) Timely services (C5) (C7) Staff availability at counter (C6) (C20) Waiting time (C7) (C11), (C13) Timely information (C8) (C11)*, (C13), (C17), (C21) Service with smile (C9) (C17)* Commitment of Employee (C10) (C24) Skilled, Knowledgeable Employee (C11) (C16)*, (C19)*, (C20)*, (C23) Cordial, customer friendly, helpful employee (C12) (C20) Service charge (C13) (C19), (C20) Hygienic atmosphere (C16) (C17), (C21)* Transparency in services (C17) (C20)* Effective handling of complaint (C18) (C19), (C20) Recognize as individual customer (C19) (C21) CRM (C20) (C21)*

Figures in parentheses showing code number of variable. * Negatively correlated variable. Source: Computed from Primary Data.

158

Figure - 5.1: Scree Plot showing the Eigen Values

The scree test was used to identify the optimum number of factors that can be

extracted before the amount of unique variance begins to dominate the common

variance structure. The scree test was derived by plotting the latent roots against

the number of factors in their order of extraction, and the shape of the resulting

curve was used to evaluate the cutoff point (Cattel, 1966). The scree plot

demonstrated (Figure 5.1) the eigen values for initial 25 components or factors

extracted in the study. Starting with the first factor, the plot slopes steeply

downward initially and then slowly became an approximately horizontal line. The

point at which the curve first begins to straighten out was considered to indicate

the number of factors to extract. In the present case, as we have the eigen value

more than 1, hence, 7 factors have been considered. All factors beyond 1 for

which these eigen value level off were excluded from consideration (Cattel and

Vogelman, 1977).

159

Table - 5.4: Inter-Correlation of Variables C1 C2 C3 C4 C5 C6 C7 C8 C9 C10 C11 C12 C13 C14 C15 C16 C17 C18 C19 C20 C21 C22 C23 C24 C25

C1 1

C2 .47* 1

C3 .36* .39* 1

C4 .31* .34* .25* 1

C5 .20* .22* .24* .16* 1

C6 .18* .11* .16* .26* .21* 1

C7 .28* .24* .29* .16* .25 .01* 1

C8 .30* .34* .26* .22* .19* .08* .42* 1

C9 .25* .32* .37* .26* .20* .21* .30* .26* 1

C10 .16* .13* .18* .16* .30* .26* .21* .18* .25* 1

C11 .16* .04 .01 .23* .21* .34* .07 -.02 .17* .18* 1

C12 .18* .13* .09* .10* .20* .28* .10* .10* .13* .18* .32* 1

C13 .08* -.01 .01 .16* .18* .21* .08 .04 .13* .12* .40* .24* 1

C14 .23* .14* .23* .20* .13* .17* .16* .19* .24* .14* .12* .15* .08* 1

C15 .35* .30* .24* .28* .21* .17* .18* .46* .20* .26* .16* .23* .14* .18* 1

C16 .40* .32* .31* .36* .20* .08* .21* .34* .32* .12* -.02 .14* .10* .36* .28* 1

C17 .15* .01 .06 .06 .21* .27* .13* .02 -.0 .10* .28* .37* .31* .11* .11* .08 1

C18 .18* .06 .08 .15* .12* .16* .11* .11* .14* .21* .36* .30* .44* .13* .25* .09* .28* 1

C19 .06 .21* .18* .22* .20* .11* .20* .28* .29* .27* -.01 .15* .02 .19* .17* .25* .02* .04 1

C20 .28* .38* .27* .27* .11* .06 .26* .49* .32* .11* -.04 .03 .00 .23* .30* .37* -.05 .01 .34* 1

C21 .10* -.00 .09* .07 .15* .29* .11* .06 .09* .23* .25* .26* .29* .11* .15* -.03 .41* .35* .00 -.03 1

C22 .12* .08 .21* .09* .30* .18* .26* .21* .15* .19* .14* .12* .24* .22* .25* .14* .21* .24* .19* .16* .27* 1

C23 .38* .31* .24* .29* .26* .25* .17* .31* .22* .24* .05 .18* .13* .23* .38* .37* .13* .11* .24* .36* .12* .14* 1

C24 .14* .15* .20* 0.20* .12* .25* .26* .35* .23* .07 .15* .21* .12* .18* .28* .19* .22* .28* .19* .19* .18* .29* .24* 1

C25 .33* .24* .26* .30* .27* .22* .27* .37* .29* .24* .13* .35* .20* .25* .38* .35* .23* .22* .27* .28* .21* .25* .41* .41* 1

*Correlation is significant at the 0.05 level (2-tailed). N=612. Source: Calculated from Primary Data.

160

5.4.2. Principal Factors

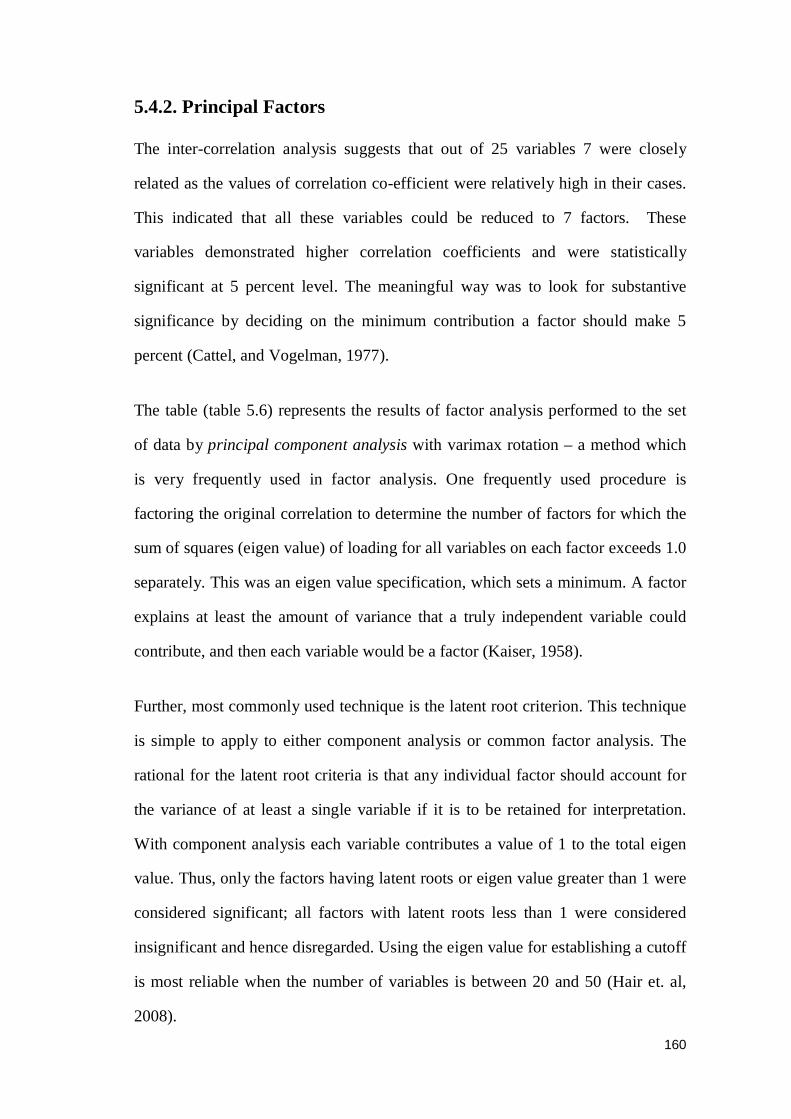

The inter-correlation analysis suggests that out of 25 variables 7 were closely

related as the values of correlation co-efficient were relatively high in their cases.

This indicated that all these variables could be reduced to 7 factors. These

variables demonstrated higher correlation coefficients and were statistically

significant at 5 percent level. The meaningful way was to look for substantive

significance by deciding on the minimum contribution a factor should make 5

percent (Cattel, and Vogelman, 1977).

The table (table 5.6) represents the results of factor analysis performed to the set

of data by principal component analysis with varimax rotation – a method which

is very frequently used in factor analysis. One frequently used procedure is

factoring the original correlation to determine the number of factors for which the

sum of squares (eigen value) of loading for all variables on each factor exceeds 1.0

separately. This was an eigen value specification, which sets a minimum. A factor

explains at least the amount of variance that a truly independent variable could

contribute, and then each variable would be a factor (Kaiser, 1958).

Further, most commonly used technique is the latent root criterion. This technique

is simple to apply to either component analysis or common factor analysis. The

rational for the latent root criteria is that any individual factor should account for

the variance of at least a single variable if it is to be retained for interpretation.

With component analysis each variable contributes a value of 1 to the total eigen

value. Thus, only the factors having latent roots or eigen value greater than 1 were

considered significant; all factors with latent roots less than 1 were considered

insignificant and hence disregarded. Using the eigen value for establishing a cutoff

is most reliable when the number of variables is between 20 and 50 (Hair et. al,

2008).

161

In the present study 25 variables were considered. Hence, based on the eigen value

(above 1), 7 factors were identified (table 5.6). The output of the factor analysis

was obtained by requesting principal component analysis and specifying rotation.

The table gives eigen values, variance explained, and cumulative variance

explained for our factor solution. The Extraction Sums of Squared Loadings group

gives information regarding the extracted factors or components. Again, we have

requested a factor rotation; therefore we see the results in the “Rotation Sums of

Squared Loadings” group.

Table - 5.6: Total Variance Explained

Component Initial Eigen values Extraction Sums of

Squared Loadings Rotation Sums of Squared Loadings

Total % of Variance

Cumulative % Total % of

Variance Cumulative

% Total % of Variance

Cumulative %

1 5.958 23.831 23.831 5.958 23.831 23.831 2.757 11.029 11.029

2 2.658 10.630 34.461 2.658 10.630 34.461 2.340 9.359 20.388

3 1.306 5.223 39.684 1.306 5.223 39.684 2.135 8.540 28.929

4 1.187 4.746 44.430 1.187 4.746 44.430 2.087 8.347 37.276

5 1.084 4.338 48.768 1.084 4.338 48.768 1.727 6.910 44.186

6 1.045 4.181 52.949 1.045 4.181 52.949 1.674 6.697 50.883

7 1.010 4.042 56.990 1.010 4.042 56.990 1.527 6.108 56.990 8 .925 3.701 60.691

9 .882 3.529 64.220

10 .841 3.363 67.583

11 .763 3.051 70.634

12 .733 2.933 73.567

13 .710 2.841 76.408

14 .672 2.689 79.098

15 .592 2.368 81.466

16 .560 2.241 83.707

17 .552 2.208 85.915

18 .529 2.117 88.032

19 .507 2.028 90.059

20 .475 1.900 91.960

21 .464 1.858 93.817

22 .457 1.829 95.647

23 .405 1.618 97.265

24 .346 1.383 98.648

25 .338 1.352 100.000

Extraction Method: Principal Component Analysis. Source: Calculated from Primary Data.

162

The first step in interpreting the output was to look at the factors extracted, their

eigen values and the cumulative percentage of variance. We could see from the

cumulative percentage column that the importance of the attributes (i.e. 7 factors)

extracted together account for 57 % of the total variance (information contained in

the original 25 variables). This indicates that we lost only 43% of the information

contained into the original variable. Now, the most important thing was that of

interpreting what these 7 extracted factors represent.

In a sample of 100 respondents, factor loading of 0.55 and above are significant.

However, in a sample of 50, a factor loading of 0.75 is required for significance.

In comparison with the prior rule of thumb, which denoted all loadings of 0.30 and

above as having practical significance, this approach would consider loadings of

0.30 significant only for sample sizes of 350 or greater (Hair et. al, 2008).

In the present context, since 612 numbers of respondents from banks were

considered, hence all loadings (ignoring sign) of 0.30 and above were having

practical significance and relevance. But, in a given row, against a specific

variable, the highest value has been considered as per the rule of thumb (table 5.7).

Table - 5.7: Factor Loadings along with Eigen Values

Code Variables Factor (F)

F1 F2 F3 F4 F5 F6 F7

C8 Timely Information 0.711 0.209 -0.074 0.004 0.03 0.06 0.324

C15 Seating, Drinking water, Lavatory facility 0.641 0.287 0.148 0.192 -0.133 0.143 0.036

C20 Customer Relationship Management 0.584 0.241 -0.222 -0.038 0.276 0.084 0.114

C25 Service Responsiveness 0.544 0.162 0.374 0.075 0.236 0.127 0.093

C23 Service Infrastructure 0.514 0.344 0.268 -0.061 0.133 0.242 -0.16

C24 Empathy to Customer 0.504 -0.097 0.256 0.196 0.286 -0.115 0.267

C1 Computerized Services 0.206 0.775 0.19 0.086 0.057 -0.019 0.054

C2 Innovative Service 0.266 0.686 -0.094 0.022 0.083 0.141 0.048

C3 Systematic and Accurate Service 0.02 0.554 0.036 -0.055 0.315 0.167 0.362

C4 Smooth and Hassle free Service 0.269 0.381 -0.098 0.353 0.347 0.145 -0.206

C17 Transparency in Services -0.01 0.041 0.739 0.19 0.039 -0.022 0.129

C12 Cordial, Customer Friendly Helpful Employee 0.193 0.066 0.565 0.223 0.081 0.163 -0.11

C21 Reliable Services -0.013 -0.03 0.56 0.294 -0.024 0.139 0.233

163

C6 Staff Availability at Counter 0.018 0.077 0.402 0.258 0.306 0.384 -0.212

C11 Skilled and Knowledgeable Employee -0.101 0.093 0.191 0.734 0.064 0.183 -0.069

C13 Service Charge 0.052 -0.03 0.201 0.709 0.037 0.027 0.086

C18 Effective Handling of Complaints 0.186 0.014 0.239 0.683 -0.044 -0.043 0.18

C14 Spacious Premises 0.08 0.134 0.209 0.006 0.698 -0.036 0.126

C16 Hygienic Atmosphere 0.354 0.431 0.059 -0.043 0.483 -0.039 0.009

C9 Service with Smile 0.122 0.279 -0.204 0.265 0.474 0.294 0.236

C10 Committed Employees 0.136 0.078 0.096 0.131 -0.037 0.751 0.112

C5 Timely Service 0.031 0.263 0.265 0.029 -0.007 0.558 0.267

C19 Recognize as individual Customer 0.415 -0.154 -0.12 -0.065 0.399 0.497 0.07

C7 Waiting Time 0.222 0.261 -0.017 0.051 0.055 0.115 0.676

C22 Service Assurance 0.161 -0.08 0.259 0.148 0.168 0.177 0.577

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization. Source: Computed from Primary Data.

It is noticed from the above table that timely information; seating, drinking

water and lavatory facility; CRM; service responsiveness; service

infrastructure; and empathy to customer; had loadings 0.711, 0.641, 0.584,

0.544, 0.514 and 0.504 respectively on factor 1 (F1) which suggested that

factor 1 was a combination of these six variables.

Again, factor 2 (F2) is a group of 4 variables include computerized

services; innovative service; systematic and accurate service; and smooth

and hassle free service; with loadings 0.775, 0.686, 0.554, and 0.381

respectively.

The 3rd factor (F3) constitutes of transparency in services; cordial customer

friendly and helpful employee; reliable services; and staff availability at

counter; had loads 0.739, 0.565, 0.560 and 0.402 respectively.

In factor 4 (F4) we find that it is a blending of skilled and knowledgeable

employee; service charge; and effective handling of complaints; had loads

0.734, 0.709 and 0.683 respectively.

Again, factor 5 (F5) is a combination of spacious premises; hygienic

atmosphere; and service with smile; had loads 0.698, 0.483, and 0.474

respectively.

164

For factor 6 (F6) we find that it is grouping of committed employees;

timely service; and recognize as individual customer; had loadings 0.751,

0.558 and 0.497 respectively.

In factor 7 (F7) we see that it is a combination of waiting time; and service

assurance; had loads 0.676 and 0.577 respectively.

5.5. DETERMINANTS OF CUSTOMER SATISFACTION The table (table 5.7) exhibited the factor loadings along with eigen values. It

confirmed close relationship of all variables with 7 underlined factors. These are

clustered as under (table 5.8).

Table - 5.8: Influencing Factors of Bank Customer Satisfaction

Factor – 1 Factor – 2 Factor – 3 Factor – 4 Factor – 5 Factor – 6 Factor – 7 Routine

Operation factor

Technology Factor

Human Factor

Management Factor

Environmental Factor

Behavioral Factor

Interactive Factor

C8. Timely information

C1. Computerized services

C17. Transparenc

y in services

C11. Skilled and knowledgeable people

C14. Spacious premises

C10. Committed employees

C7. Waiting time

C15. Seating, drinking water,

lavatory facility

C2. Innovative

services

C12. Cordial, customer friendly helpful

employee

C13. Service charge

C16. Hygienic

atmosphere

C5. Timely service

C22. Service

assurance

C20. Customer

relationship management

C3. Systematic

and accurate service

C21. Reliable services

C18. Effective

handling of complaints

C9. Service with smile

C19. Recognize

as individual customer

C25. Service

responsive ness

C4. Smooth and hassle free service

C6. Staff availability at counter

C23. Service

infrastructure

C24. Empathy to customer

Source: Determined from Primary Data.

165

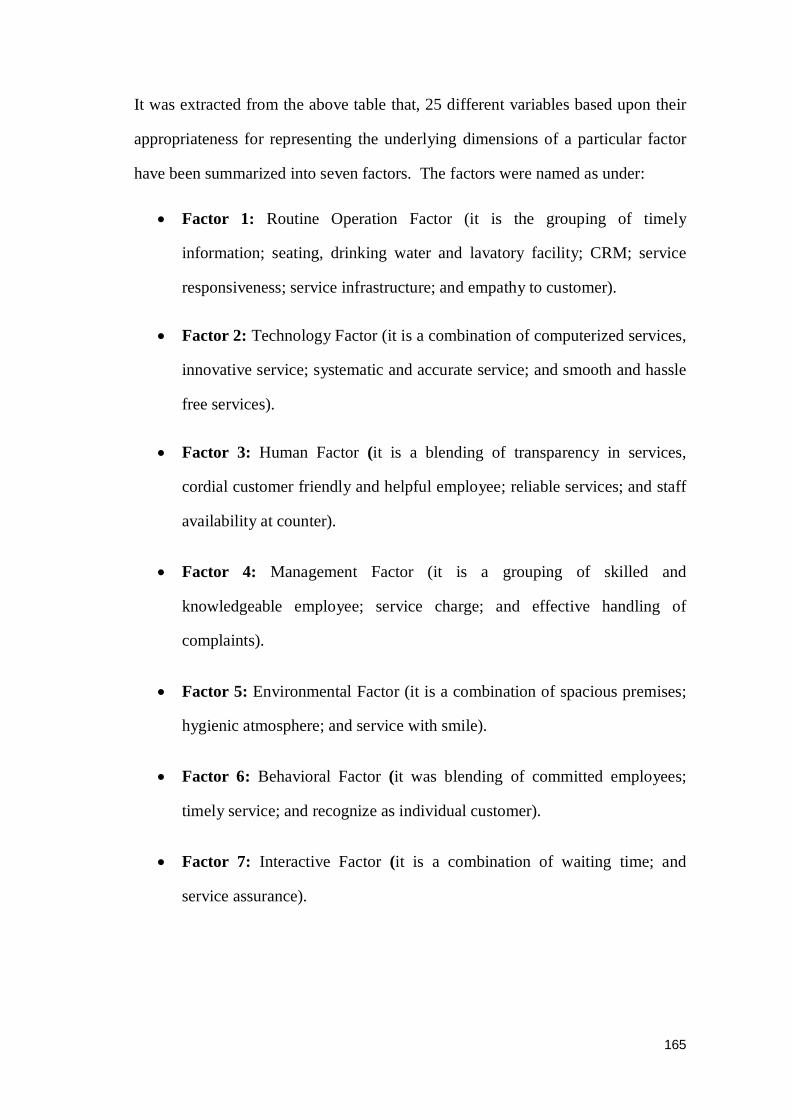

It was extracted from the above table that, 25 different variables based upon their

appropriateness for representing the underlying dimensions of a particular factor

have been summarized into seven factors. The factors were named as under:

Factor 1: Routine Operation Factor (it is the grouping of timely

information; seating, drinking water and lavatory facility; CRM; service

responsiveness; service infrastructure; and empathy to customer).

Factor 2: Technology Factor (it is a combination of computerized services,

innovative service; systematic and accurate service; and smooth and hassle

free services).

Factor 3: Human Factor (it is a blending of transparency in services,

cordial customer friendly and helpful employee; reliable services; and staff

availability at counter).

Factor 4: Management Factor (it is a grouping of skilled and

knowledgeable employee; service charge; and effective handling of

complaints).

Factor 5: Environmental Factor (it is a combination of spacious premises;

hygienic atmosphere; and service with smile).

Factor 6: Behavioral Factor (it was blending of committed employees;

timely service; and recognize as individual customer).

Factor 7: Interactive Factor (it is a combination of waiting time; and

service assurance).

166

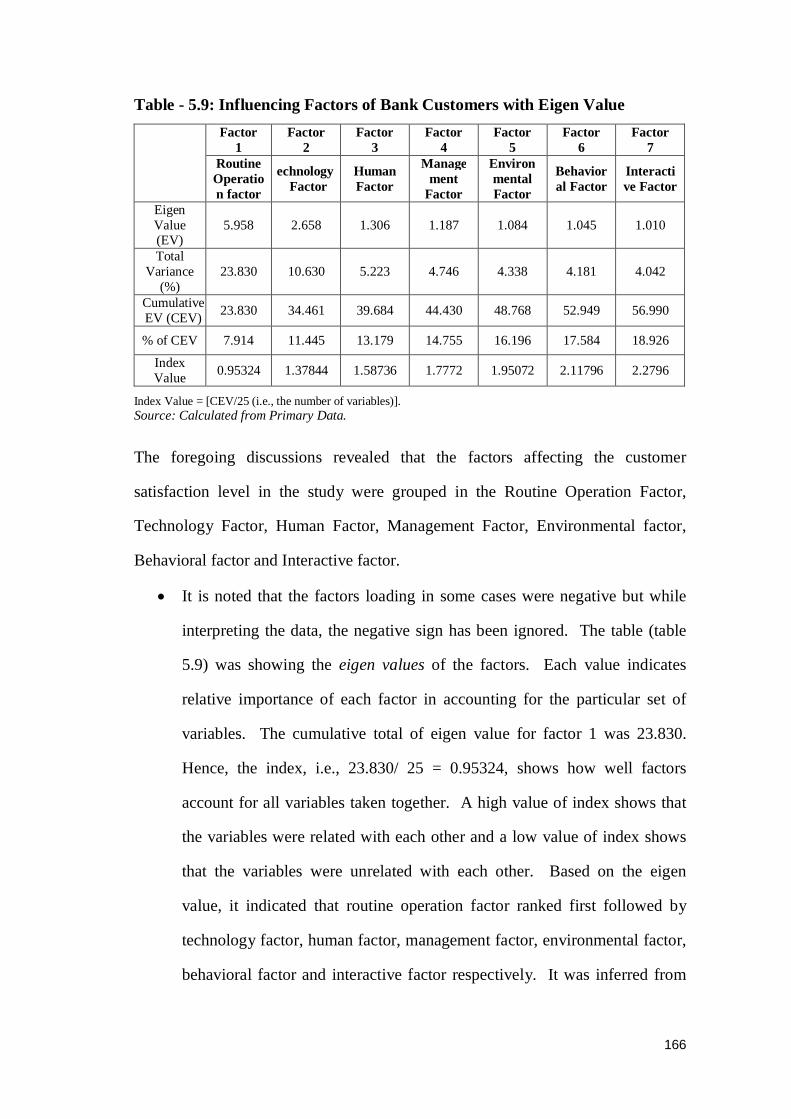

Table - 5.9: Influencing Factors of Bank Customers with Eigen Value

Factor 1

Factor 2

Factor 3

Factor 4

Factor 5

Factor 6

Factor 7

Routine Operation factor

echnology Factor

Human Factor

Management

Factor

Environmental Factor

Behavioral Factor

Interactive Factor

Eigen Value (EV)

5.958 2.658 1.306 1.187 1.084 1.045 1.010

Total Variance

(%) 23.830 10.630 5.223 4.746 4.338 4.181 4.042

Cumulative EV (CEV) 23.830 34.461 39.684 44.430 48.768 52.949 56.990

% of CEV 7.914 11.445 13.179 14.755 16.196 17.584 18.926

Index Value 0.95324 1.37844 1.58736 1.7772 1.95072 2.11796 2.2796

Index Value = [CEV/25 (i.e., the number of variables)]. Source: Calculated from Primary Data.

The foregoing discussions revealed that the factors affecting the customer

satisfaction level in the study were grouped in the Routine Operation Factor,

Technology Factor, Human Factor, Management Factor, Environmental factor,

Behavioral factor and Interactive factor.

It is noted that the factors loading in some cases were negative but while

interpreting the data, the negative sign has been ignored. The table (table

5.9) was showing the eigen values of the factors. Each value indicates

relative importance of each factor in accounting for the particular set of

variables. The cumulative total of eigen value for factor 1 was 23.830.

Hence, the index, i.e., 23.830/ 25 = 0.95324, shows how well factors

account for all variables taken together. A high value of index shows that

the variables were related with each other and a low value of index shows

that the variables were unrelated with each other. Based on the eigen

value, it indicated that routine operation factor ranked first followed by

technology factor, human factor, management factor, environmental factor,

behavioral factor and interactive factor respectively. It was inferred from

167

the analysis that the respondents were emphasizing more on Routine

Operations of banks offering services in the area under study.

The eigen value of Routine Operation Factor ranked the highest (eigen

value = 5.958) indicating the satisfactions level of the customers. In regard

to timely information; seating, drinking water and lavatory facility; CRM;

service responsiveness; service infrastructure; and empathy to customer etc.

were not appreciable.

The Technology Factor which was second in the list (eigen value = 2.658)

generates slight satisfaction because the customers feel that they were not

getting enough through computerized services. Innovative services were

not offered them frequently and banking services were not very systematic

and accurate in true sense. Services rendered by the banks were not very

smooth and hassle free. In connection with the technology factor, much had

not been done and banks in the area under study are yet to step forward in

adopting modern technology up-gradation in the bank branches like full-

computerization, innovativeness in offering new services etc. to survive in

the present day world of competition. Innovativeness and mechanization is

the need of the hour, but banks in the districts under study was showing a

dismal service performance in this respect. All the branches of all the

banks had not fully computerized their operations and were stuck on to

manual computations and calculations which increased the work load and

reduced the efficiency of the staff. The technology up-gradation,

innovativeness of new services etc. were essential in this respect.

In the context of Human Factor (eigen value = 1.306), again the satisfaction

level was slight. It included transparency in services; cordial, customer

friendly and helpful employees; reliable services and staff availability at

counter. It means that, banks in the area under study were not making an

168

extra effort to ensure transparency in services. The employees were not

very cordial, customer friendly and helpful. The banks could not offer

reliable services in actual sense. Availability of staff at the counter was not

very satisfactory. So, the customers were slightly satisfied as far as human

factor of the bank came into picture.

The Management Factor (eigen value = 1.187), which included skilled and

knowledgeable employees; service charge and effective handling of

complaints. In this context it can be stated that, the skill and knowledge

level of the service provider was not up to the customer’s expectation. In

connection with the service charge, in some cases it was relatively higher.

Sometimes, the banks fail to handle the customer’s complaints effectively

and efficiently.

The other factor which yields poor satisfaction was Environmental Factor

(eigen value = 1.084). It was observed that the banks operating in the area

under the study are yet to make full efforts to improve the environmental

factors which included spacious premises; hygienic atmosphere; and

service rendered with smile by the bank employees etc. The bank’s

condition with regard to the environmental factors which are well within

the control of the banks. But, necessary steps have not been taken to

improve the environmental condition of banks in general.

Behavioral Factor (eigen value= 1.045) is the combinations of variables

like committed employees; timely service; and recognize as individual

customer. As far as the behavioral factor of employees is concerned, the

commitment level of employees in rendering services and with a view to

satisfy customer, more efforts are needed to put. Services must be rendered

without wasting the valuable time of customers. Bank employee should try

169

to recognize the individual customer which was not prominently visible in

the bank.

The Interactive Factor (eigen value = 1.010) pertaining to waiting time and

service assurance by the bank employees indicating moderate level of

satisfaction. It revealed that waiting time for having services in the banks is

more than expected and service assurance from the employees is less than

customer’s expectation.

5.6. FACTOR WISE CUSTOMER SATISFACTION LEVEL

Factor wise satisfaction level of customers is calculated using mean/average score,

which reflected that in some cases customers are modestly satisfied and some

cases they are slightly satisfied from the services delivered by the bank in the area

under the study. Following table (table 5.10) exhibited the mean value/average

score of all the underlying factors. It also highlighted the level of satisfaction

(LOS) and factor ranking based on mean value.

Table - 5.10: Factor Ranking

Factor Name of the Factor Mean Value LOS Factor Ranking

Factor – 1 Routine Operation Factor 2.81 Slight 1

Factor – 2 Technology Factor 2.82 Slight 2 Factor – 3 Human Factor 3.28 Modest 7 Factor – 4 Management Factor 3.24 Modest 6 Factor – 5 Environmental Factor 2.9 Slight 3 Factor – 6 Behavioral Factor 3.02 Modest 4 Factor – 7 Interactive Factor 3.03 Moderate 5

Mean value is calculated against all the variables under a particular factor. Factor ranking is based on mean value of all the variables under a particular factor. Source: Calculated from Primary Data.

Mean value of each factor is calculated based on the average/mean value of all

variables included under a particular factor. Further, factor ranking has been done

170

based on lowest mean value. More emphasis should be given on the factor having

relatively low mean value when strategies would be adopted.

The factor wise average score revealed that none of the variables ranked 4.00 and

above which indicates that the customers of banks in regard to the service

rendered was quite dismal. They are either modestly satisfied or slightly satisfied

from the services. The routine operation factor indicates the daily functional

processes that the banks failed to serve the customers fully. The factor wise

average scores in respect of technology factors and environmental factors revealed

that the customers are turned to be dissatisfied lot. It is because of the fact that,

banks are unable to improve the quality standards. In technology front, banks in

the area under the study are lagging behind. The rural areas of the districts under

study are still un-varied for by the banks and rural masses are yet to enjoy modern

banking facilities. From the above analysis it is evident that banks in the districts

need to adopt certain specific marketing strategies in order to survive in the

present globalization environment and in the world of competition.

5.7. CONCLUSION

Majority of the service variables are correlated with each other in connection with

the banking services. But, some of the specific variables are not correlated with

each other and some of them are negatively correlated. All 25 service variables are

categorized under 7 major factors responsible for customer satisfaction from the

banking services. These factors are named as routine operation factor (factor 1);

technology factor (factor 2); human factor (factor 3); management factor (factor

4); environment factor (factor 5); behavioral factor (factor 6); and interactive

factor (factor 7). Further, based on mean value of all the variables under a

particular factor, factor ranking has been made. Factor with lowest mean value is

171

given the first priority as far as strategic issues of banks are concerned.

Accordingly, the routine operation factor ranked first out of 7 factors. So, more

emphasis should be given to routine operation factor followed by technology

factor, environmental factor, behavioral factor, interactive factor, management

factor and human factor of the bank respectively.

From the foregoing analysis it is inferred that 7 factors or determinants give the

shape to the customer satisfaction in respect of services rendered by the banks

operating in the area under the study. This indicates, in the hypercompetitive

environment, survival of banks depends on to what extent they are adapted to

these changing environment and emphasized on the principal factors that

determine the plight of banking operations. The strategy therefore would be to

immediately address the issue.

REFERENCES

Cattel, R. B. (1966). The Scree Test for the Number of Factors.

Multivariate Behavioral Research, April, 1, 245-276.

Cattel, R. B. & Vogelman, S. (1977). A Comprehensive trial of the Scree

and the K G Criteria for Determining the Number of Factors. Multivariate

Behavioral Research, 289-325.

Cronbach, L. J. (1951). Coeffiecient Alpha and the Internal Structures of

Tests. Psychrometrika, 16 (3), 297-333.

Hair, J. F. Jr.; Anderson, R. E.; Tatham, R. L. & Black, W. C. (1995).

Multivariate Data Analysis. NJ: Printice-Hall, Engelwood Cliffs, 4th

edition.

172

Hair, J. F. Jr.; Anderson, R. E.; Tatham, R. L.; Black, W. C. & Babin, B. J.

(2008). Multivariate Data Analysis. New Delhi: Pearson Education, 6th

edition.

Kaiser, H. F. (1958). Varimax Criterion for Analytical Rotation in Factor

Analysis. Psychrometrica, 23, 187-200.

Kaiser, H. F. and Rice, J. (1974). Little Jiffy Mark IV. Educational and

Psychological Measurement, 34(1), 111-17.

Nunnally, J. C. (1978). Psychometric Theory. New York: McGraw-Hill.

Singh, R. and Jain, M. (2009). Metro Trains and Customer Satisfaction- an

Empirical Study in Delhi. Cabell’s Management Directory, USA, 6(2).

Stewart, D. W. (1981). The Application and Misapplication of Factor

Analysis in Marketing Research. Journal of Marketing Research, February,

38, 51-56.