chapter sixteen control: techniques for enhancing organizational effectiveness

TRANSCRIPT

Chapter Sixteen

Control: Techniques for Enhancing Organizational Effectiveness

B16-1

Panel 16.1

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

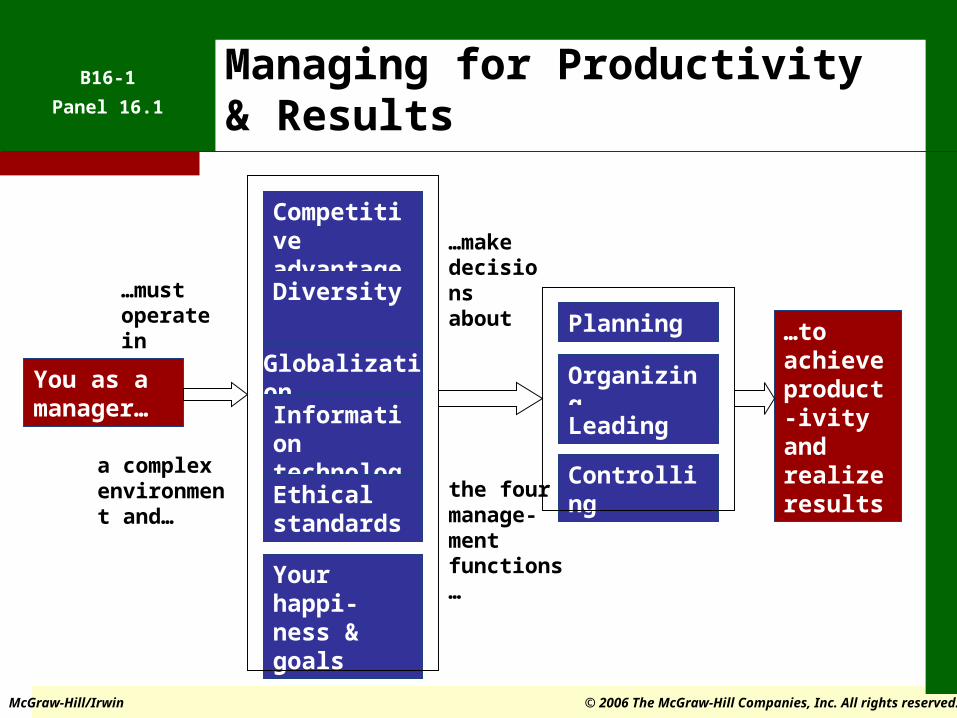

Managing for Productivity & Results

You as a manager…

Competitive advantage

Diversity

Globalization

Information technology

Ethical standards

Your happi- ness & goals

…must operate in

a complex environment and…

Planning

Organizing Leading

Controlling

…make decisions about

the four manage-ment functions…

…to achieve product-ivity and realize results

B16-2

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

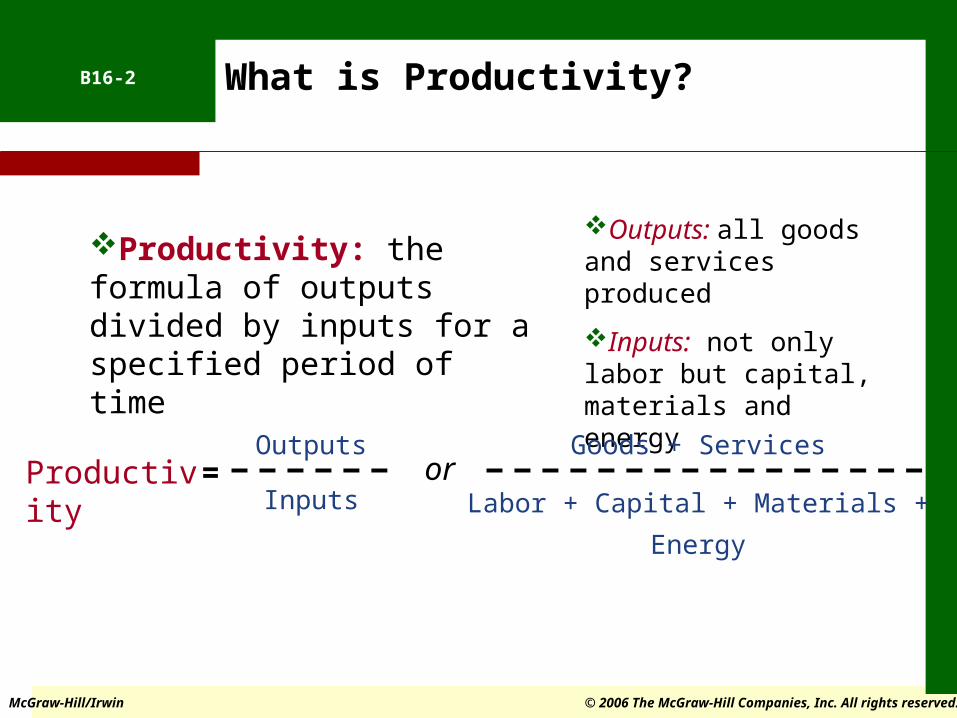

What is Productivity?

Productivity: the formula of outputs divided by inputs for a specified period of time

Outputs: all goods and services produced

Inputs: not only labor but capital, materials and energy

Productivity = orOutputs

Inputs

Goods + Services

Labor + Capital + Materials + Energy

B16-3

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

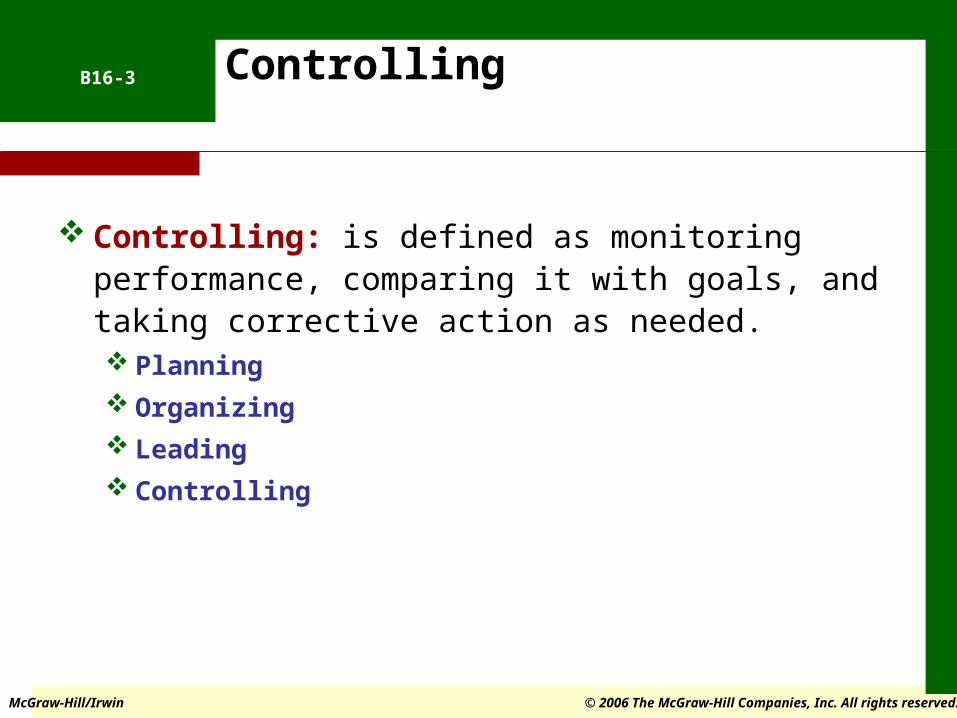

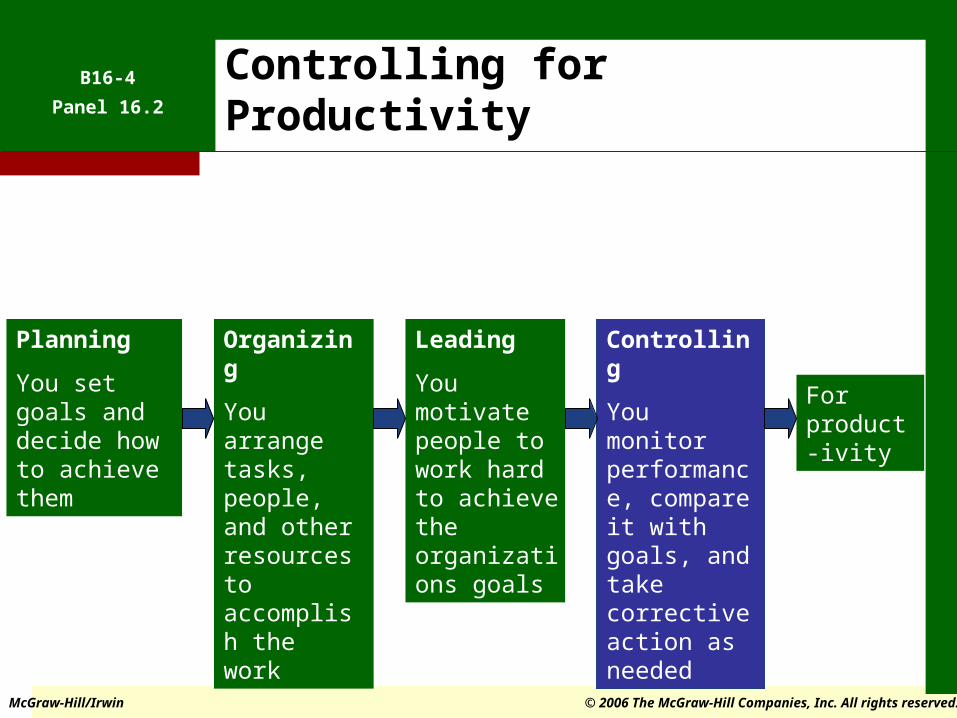

Controlling

Controlling: is defined as monitoring performance, comparing it with goals, and taking corrective action as needed. Planning

Organizing

Leading

Controlling

B16-4

Panel 16.2

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Controlling for Productivity

Planning

You set goals and decide how to achieve them

Organizing

You arrange tasks, people, and other resources to accomplish the work

Leading

You motivate people to work hard to achieve the organizations goals

Controlling

You monitor performance, compare it with goals, and take corrective action as needed

For product-ivity

B16-5

Panel 16.3

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

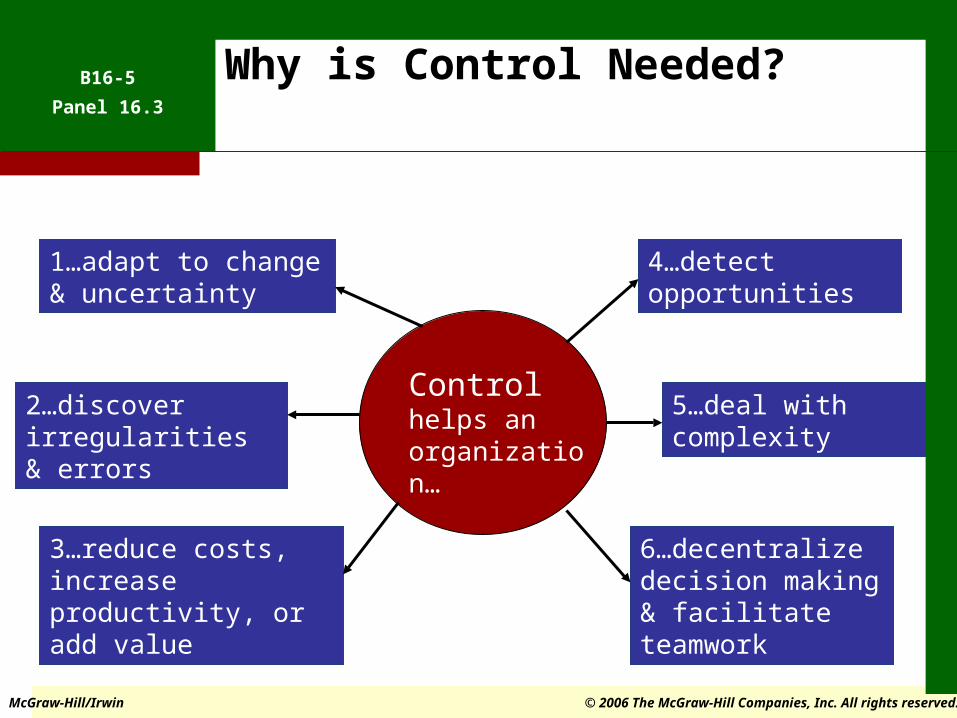

Why is Control Needed?

Control helps an organization…

1…adapt to change & uncertainty

2…discover irregularities & errors

3…reduce costs, increase productivity, or add value

4…detect opportunities

5…deal with complexity

6…decentralize decision making & facilitate teamwork

B16-6

Panel 16.4

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

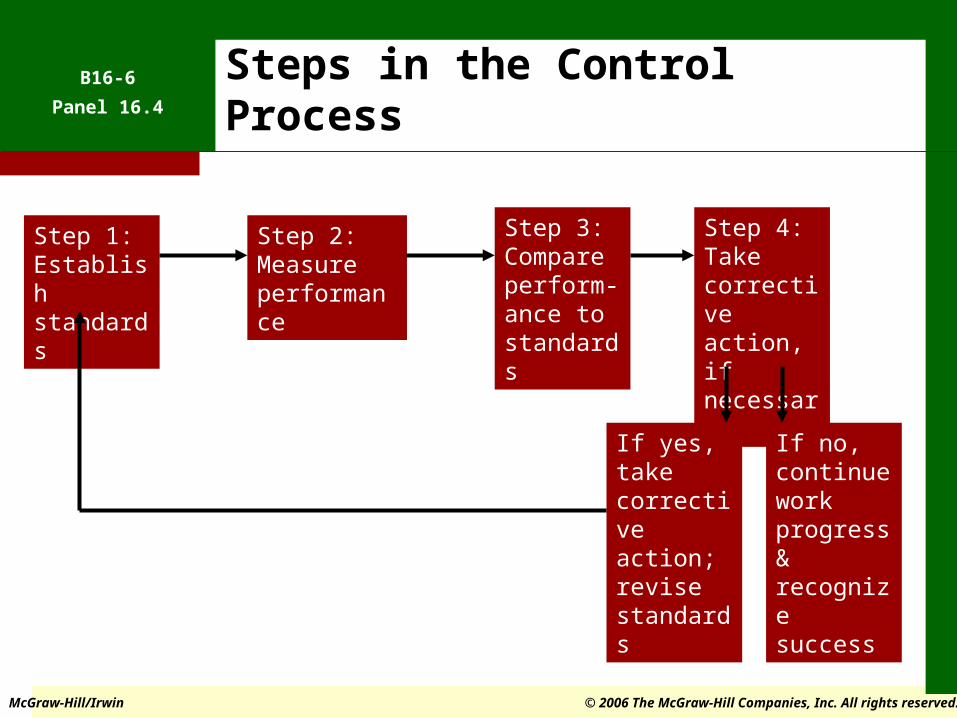

Steps in the Control Process

Step 1: Establish standards

Step 2: Measure performance

Step 3: Compare perform-ance to standards

Step 4: Take corrective action, if necessary

If yes, take corrective action; revise standards

If no, continue work progress & recognize success

B16-7

Panel 16.5

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

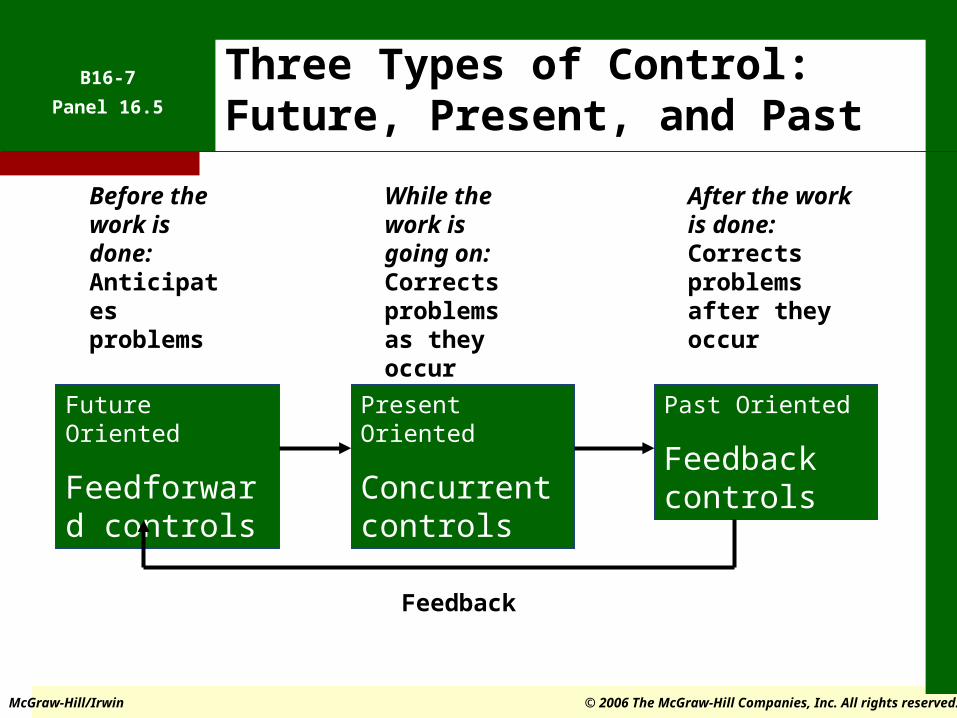

Three Types of Control: Future, Present, and Past

Future Oriented

Feedforward controls

Present Oriented

Concurrent controls

Past Oriented

Feedback controls

Before the work is done: Anticipates problems

While the work is going on: Corrects problems as they occur

After the work is done: Corrects problems after they occur

Feedback

B16-8

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Levels & Areas of Control

Strategic control

Tactical control

Operational control

Physical resources

Human resources

Informational resources

Financial resources

B16-9

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Styles of Implementing Controls

Bureaucratic control

Market control

Clan control

B16-10

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Budget

Budget: is a formal financial projection

B16-11

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Financial Statements

Financial Statement: summary of some aspects of an organization’s financial status

B16-12

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Ratio Analysis

Ratio Analysis: practice of evaluating financial ratios

B16-13

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Audits

Audits: formal variations of on organization’s financial and operational systems

B16-14

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

TQM and Its Components

Total Quality Management (TQM): a comprehensive approach led by top management and supported throughout the organization—dedicated to continuous quality improvement, training, and customer satisfaction

Make continuous improvement a priority Get every employee involved Listen to and learn from customers and

employees Use accurate standards to identify and

eliminate problems

B16-15

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Core Principles of TQM

1) People Orientation- Focusing Everyone on Delivering Customer Value

2) Improving Orientation—Focusing Everyone on Continuously Improving Work Processes

B16-16

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

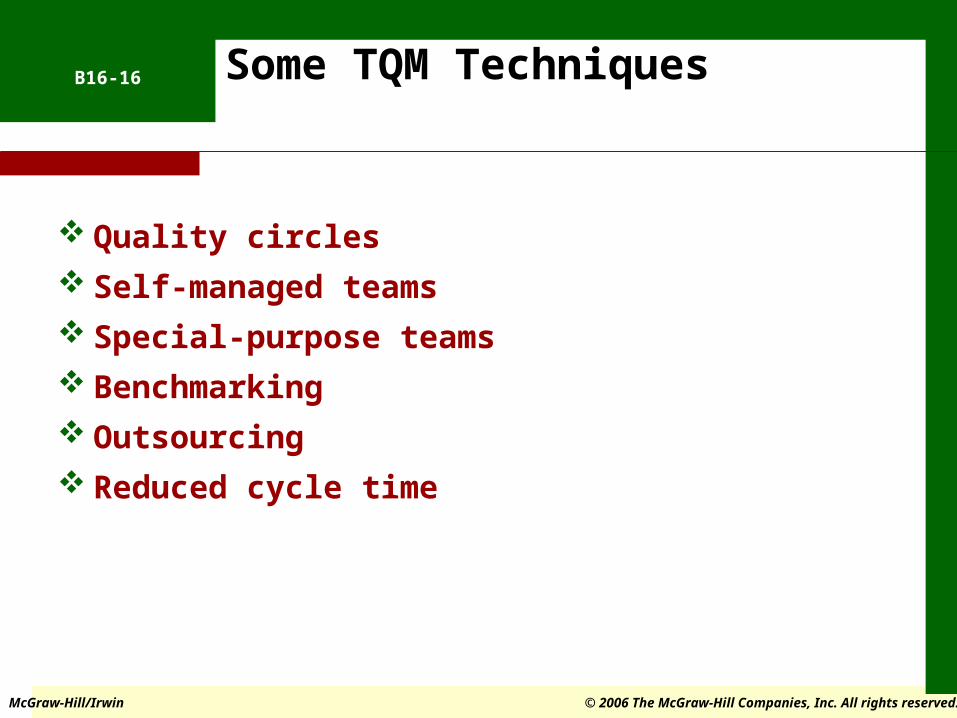

Some TQM Techniques

Quality circles

Self-managed teams

Special-purpose teams

Benchmarking

Outsourcing

Reduced cycle time

B16-17

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

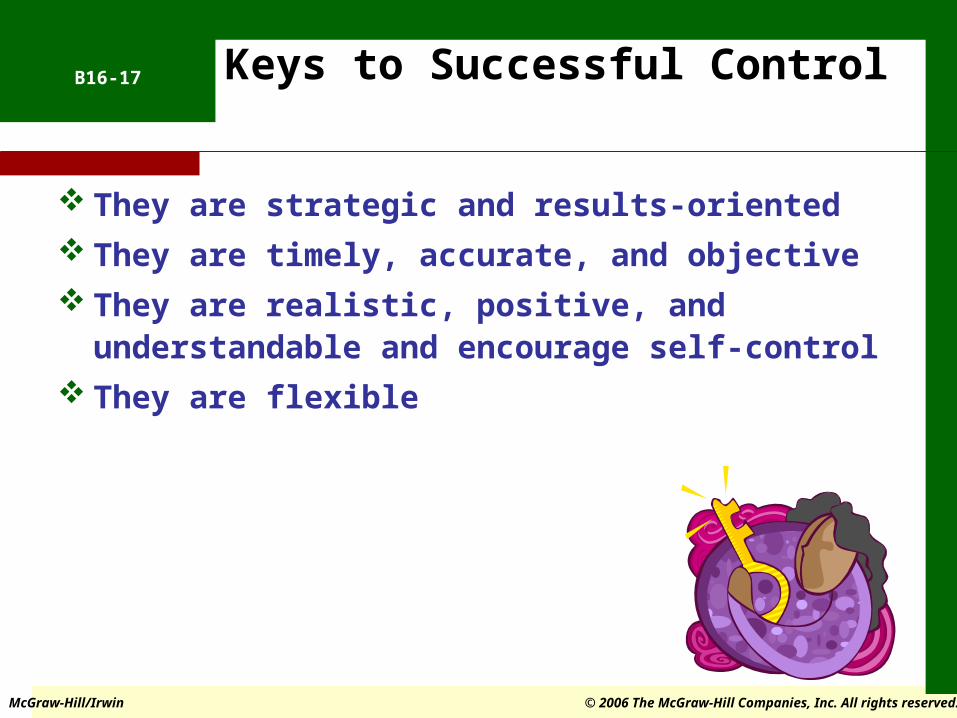

Keys to Successful Control

They are strategic and results-oriented

They are timely, accurate, and objective

They are realistic, positive, and understandable and encourage self-control

They are flexible

B16-18

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

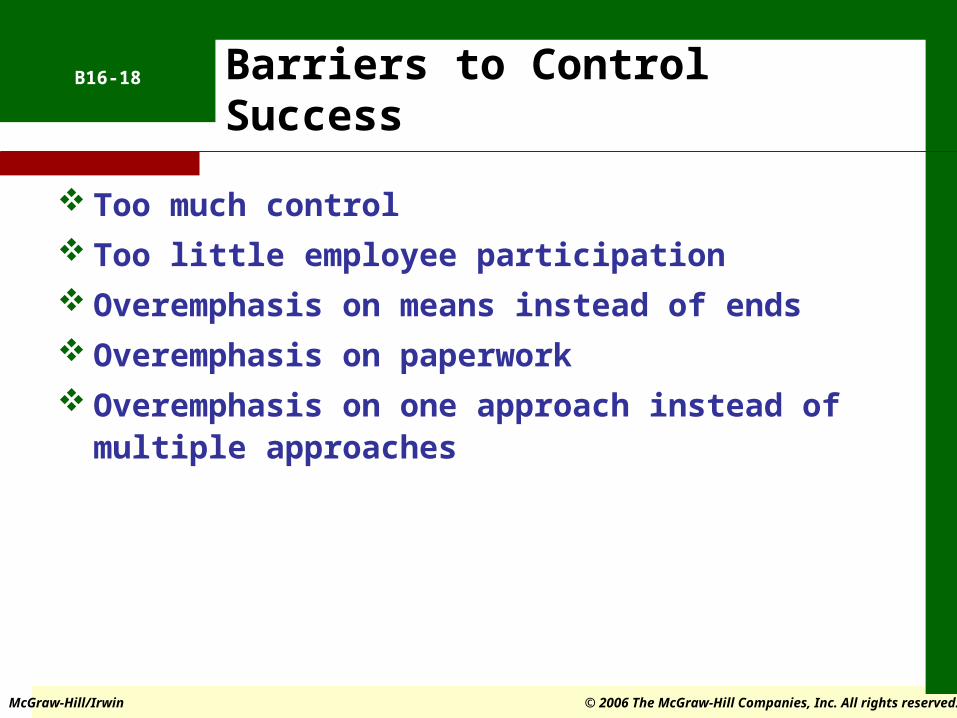

Barriers to Control Success

Too much control

Too little employee participation

Overemphasis on means instead of ends

Overemphasis on paperwork

Overemphasis on one approach instead of multiple approaches

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

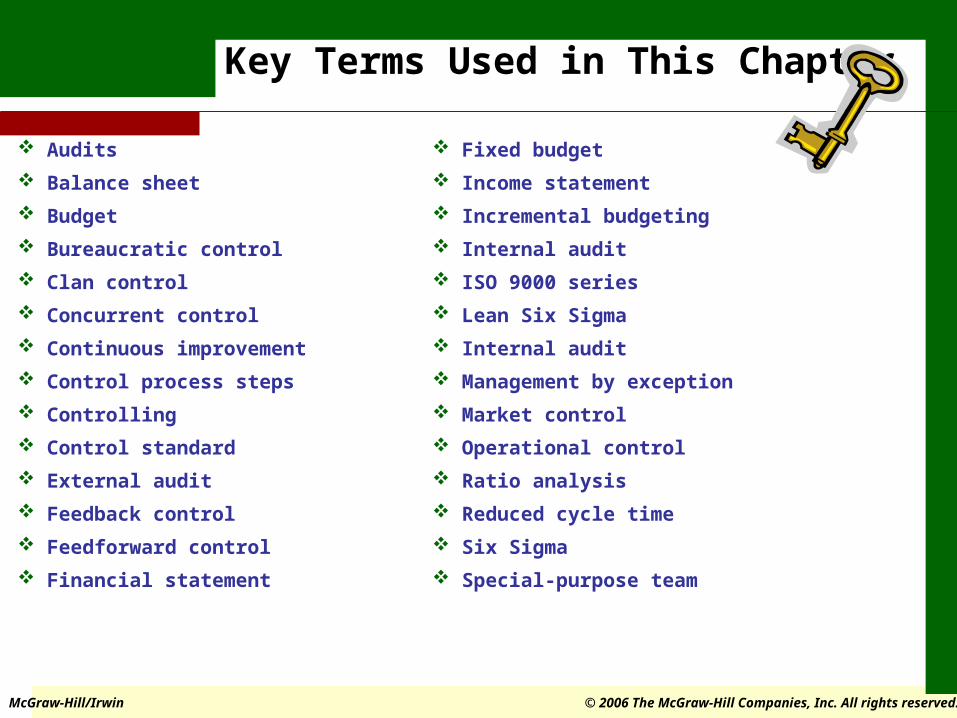

Key Terms Used in This Chapter

Audits

Balance sheet

Budget

Bureaucratic control

Clan control

Concurrent control

Continuous improvement

Control process steps

Controlling

Control standard

External audit

Feedback control

Feedforward control

Financial statement

Fixed budget

Income statement

Incremental budgeting

Internal audit

ISO 9000 series

Lean Six Sigma

Internal audit

Management by exception

Market control

Operational control

Ratio analysis

Reduced cycle time

Six Sigma

Special-purpose team

McGraw-Hill/Irwin © 2006 The McGraw-Hill Companies, Inc. All rights reserved.

Key Terms Used in This Chapter

Statistical process control

Strategic control

Tactical control

Total Quality Management

(TQM)

Two core principles of TQM

Variable budget

Zero-based budgeting