chapter iii growth and development of dairy industry...

TRANSCRIPT

CHAPTER – III

GROWTH AND DEVELOPMENT OF

DAIRY INDUSTRY IN INDIA

CHAPTER – III

GROWTH AND DEVELOPMENT OF DAIRY INDUSTRY IN INDIA

3.1 WORLD SCENARIO OF DAIRYING

The livestock sector plays a vital role in the economies of many developing

countries. It provides food (specifically, animal protein) to human beings, income,

employment and possibly foreign exchange to the nation. For low income

producers, livestock also serves as a store of wealth, provides organic fertilizer

for crop production and can even be a means of transport. More than 2,445 million

people economically active in agriculture in the world, probably 2/3 or even more

¾ of them are wholly or partly dependent on livestock farming. Consumption of

livestock products in developing countries, though starting from a low base, is

growing rapidly.

Milk provides relatively quick returns for small-scale livestock keepers. It

is a balanced nutritious food and is a key element in household food security.

Smallholders produce the vast majority of milk in developing countries where the

demand is expected to increase by 25 per cent by 2025. Over 80 per cent of milk

consumed in developing countries (200 billion litres annually) is handled by

informal market traders with inadequate regulation.

Globally, the dairy sector is probably one of the most distorted agricultural

sectors: producer subsidies are in place in many developed countries, encouraging

surplus production, export subsidies are paid by governments to place the excess

production on the world markets, and tariff and non-tariff barriers are erected both

by developed and developing countries to protect their dairy sector from ‘unfair’

competition.

These market distortions are having significant and different impacts on

producers and consumers in developing and developed countries, which are

however extremely difficult to quantify.

3.2 WORLD MILK PRODUCTION

Milk has certain features that distinguish it from other agricultural products

and shape its production, processing and trade. Milk is a bulky and heavy

commodity which requires high-cost storage and transportation as it gets spoiled

quickly without cooling. Due to this fact even the largest dairy farms cannot supply

adequate quantities to a processing plant. Each single dairy farm supplies only a

small share of the total milk processed. The dairy industries in many countries are

organized along co-operative lines. Milk producing cooperatives bundle the

interest and supply of a large number of dairy farmers and strengthen their

bargaining power towards processors or even run their own processing plants.

Over the last 24 years, total world milk production has increased by 32 per cent

whereas per capita world milk production has declined by nine per cent which

indicates that world milk production has not kept pace with the increase in world

population. The decline in global milk production per capita can be attributed to

falling production in the developed countries whereas per capita milk production in

the developing countries has slightly risen over the last 24 years. As opposed to the

trend towards intensification of milk production in developed countries, production

growth in developing countries is to a large part due to increasing numbers of milk

animals (and dairy farms) and only to a small part due to productivity gains.

India is the largest producer of dairy products in the world. There is a great

deal of variation in the pattern of dairy production worldwide. Many countries

which are large producers, consume this internally, while others — in particular

New Zealand — export a large percentage of their production. Internal

consumption is often in the form of liquid milk, while the bulk of international

trade is in processed dairy products such as milk powder. The world's largest

exporter of dairy products is New Zealand and dairy products are the largest export

earner for the country. Fonterra is the fifth-largest dairy company in the world and

New Zealand's largest company by turnover. Japan is the world's largest importer

of dairy products. Two thirds of total world milk is produced by Brazil, India,

Pakistan, Poland, the Russian Federation, the USA, and 15 EU member states.

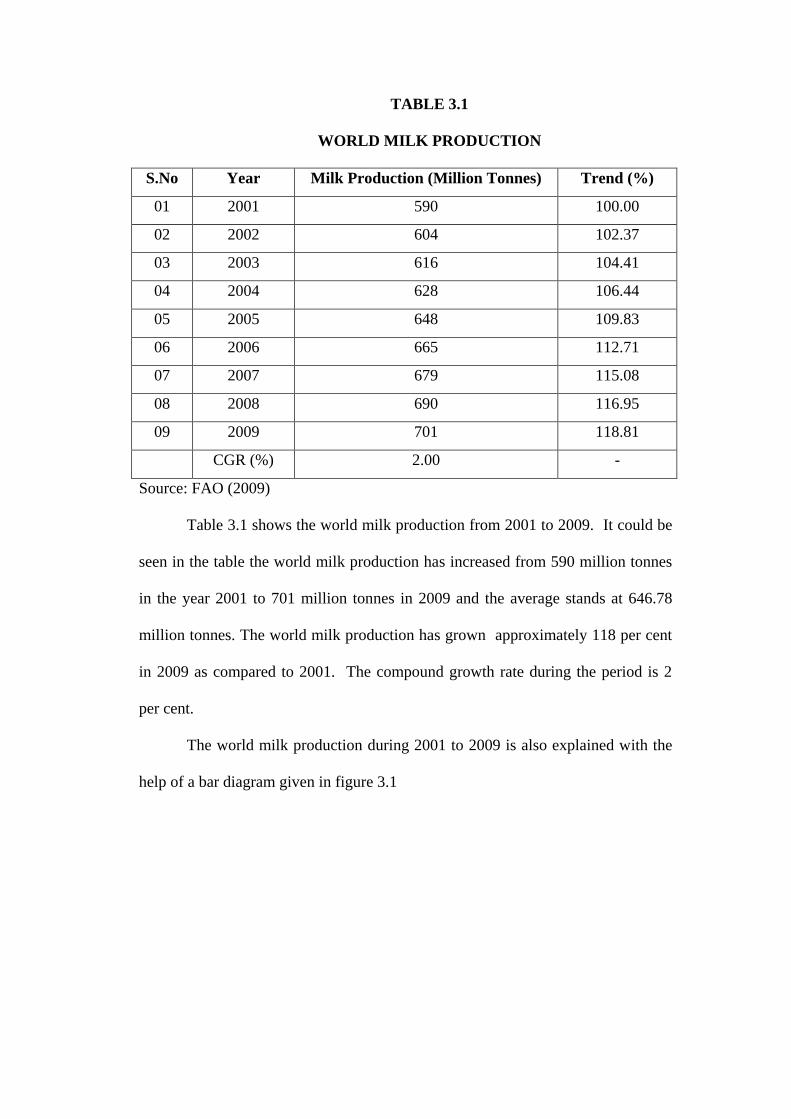

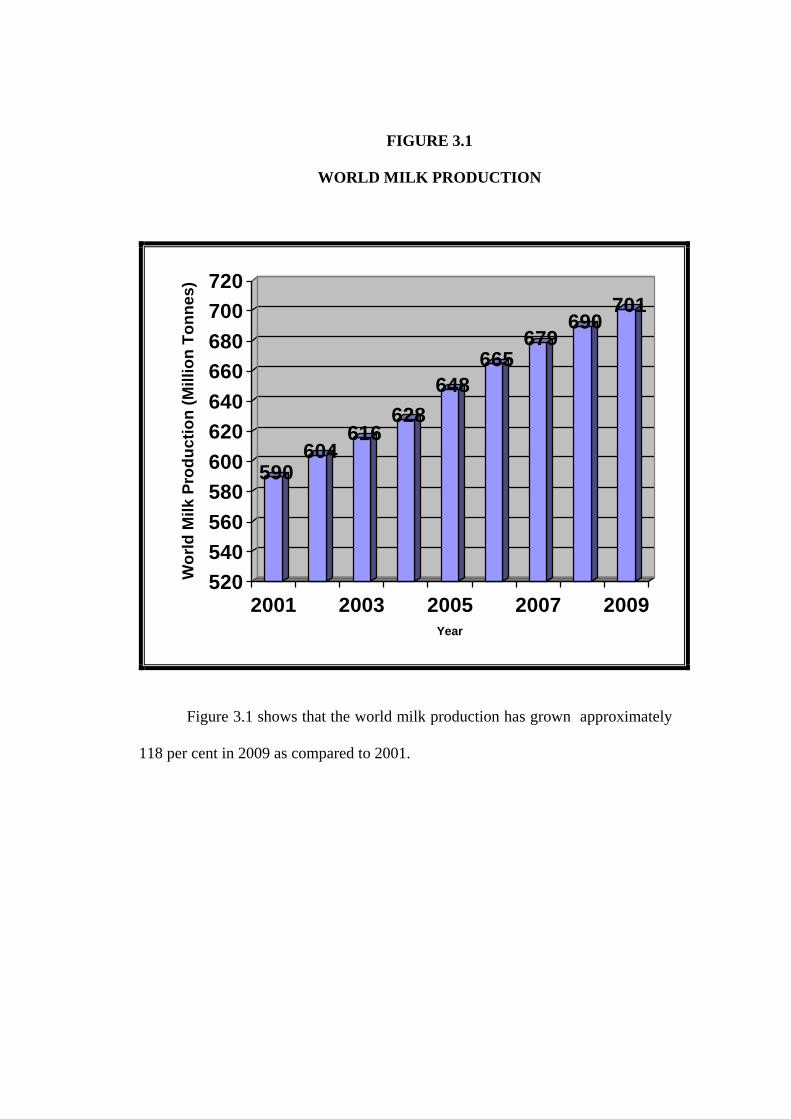

Table 3.1 shows world milk production during 2001 to 2009.

TABLE 3.1

WORLD MILK PRODUCTION

S.No Year Milk Production (Million Tonnes) Trend (%)

01 2001 590 100.00

02 2002 604 102.37

03 2003 616 104.41

04 2004 628 106.44

05 2005 648 109.83

06 2006 665 112.71

07 2007 679 115.08

08 2008 690 116.95

09 2009 701 118.81

CGR (%) 2.00 -

Source: FAO (2009)

Table 3.1 shows the world milk production from 2001 to 2009. It could be

seen in the table the world milk production has increased from 590 million tonnes

in the year 2001 to 701 million tonnes in 2009 and the average stands at 646.78

million tonnes. The world milk production has grown approximately 118 per cent

in 2009 as compared to 2001. The compound growth rate during the period is 2

per cent.

The world milk production during 2001 to 2009 is also explained with the

help of a bar diagram given in figure 3.1

FIGURE 3.1

WORLD MILK PRODUCTION

590604

616628

648

665679

690701

520

540

560

580

600

620

640

660

680

700

720

Wo

rld

Mil

k P

rod

uc

tio

n (

Mil

lio

n T

on

ne

s)

2001 2003 2005 2007 2009Year

Figure 3.1 shows that the world milk production has grown approximately

118 per cent in 2009 as compared to 2001.

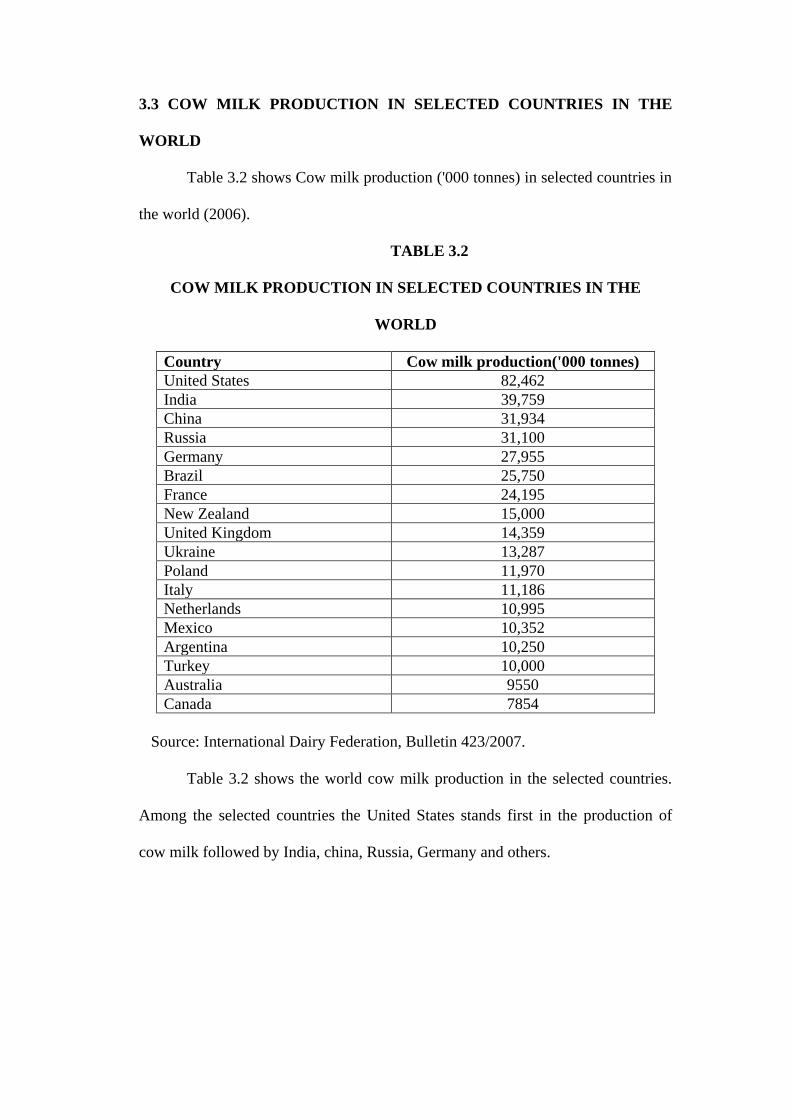

3.3 COW MILK PRODUCTION IN SELECTED COUNTRIES IN THE

WORLD

Table 3.2 shows Cow milk production ('000 tonnes) in selected countries in

the world (2006).

TABLE 3.2

COW MILK PRODUCTION IN SELECTED COUNTRIES IN THE

WORLD

Country Cow milk production('000 tonnes)

United States 82,462

India 39,759

China 31,934

Russia 31,100

Germany 27,955

Brazil 25,750

France 24,195

New Zealand 15,000

United Kingdom 14,359

Ukraine 13,287

Poland 11,970

Italy 11,186

Netherlands 10,995

Mexico 10,352

Argentina 10,250

Turkey 10,000

Australia 9550

Canada 7854

Source: International Dairy Federation, Bulletin 423/2007.

Table 3.2 shows the world cow milk production in the selected countries.

Among the selected countries the United States stands first in the production of

cow milk followed by India, china, Russia, Germany and others.

3.4 WORLD MILK CONSUMPTION

Total milk consumption in developed countries stayed more or less

constant over the last twenty years, significant increase in global milk consumption

is due to population growth and per capita income growth in developing countries.

The latter has led to the emergence of an affluent middle-class in many low and

middle income countries in Southeast Asia, Latin America and Central and Eastern

Europe.

Additional “westernization” trends leading to increasing preferences for

new value-added products in many of these economies generate additional dairy

market growth. The composition of dairy product consumption varies across

different regions with liquid milk as the overall most important product by volume.

However, processed dairy products become more important with increasing

incomes and living standards, and in developed countries the trend goes more and

more towards high value functional foods that require considerable research

investments and sophisticated processing.

After years of relatively stable development of global supply and demand

on milk, the unexpected price fluctuations in 2007 and 2008 caused sufficient

changes both in the world demand and in the production of milk, creating big gaps,

which, in their turn, increased price instability. Since mid- 1990 the world milk

consumption is growing at an average of 10-15 million tones of milk per year,

based on the population growth and increasing income in many countries (IFCN,

2008). Since 1980 the demand for the dairy products grew especially in Asian

region from 32 kg per capita in 1981 to 64 kg per capita in 2007, the Asian

consumers presented almost a half of the world demand for milk and milk

products.

Growing income and change in food composition in China, India and other

Asian countries are the factors responsible for the increasing demand. The

governmental support of milk consumption like school milk programmes and new

dairyproducts supported this expansion (FAO, 2009). This growing demand and

higher prices created market opportunities for the local producers and in 2005 Asia

became the world’s largest milk producer with a growth of 35% in 1997-2007.

The total milk consumption (as fluid milk and processed products) per

person varies widely from highs in Europe and North America to lows in Asia.

However, as the various regions of the world become more integrated through

travel and migration, these trends are changing, a factor which needs to be

considered by product developers and marketers of milk and milk products in

various countries of the world.

Even within regions such as Europe, the custom of milk consumption has

varied greatly. Consider for example the high consumption of fluid milk in

countries like Finland, Norway and Sweden compared to France and Italy where

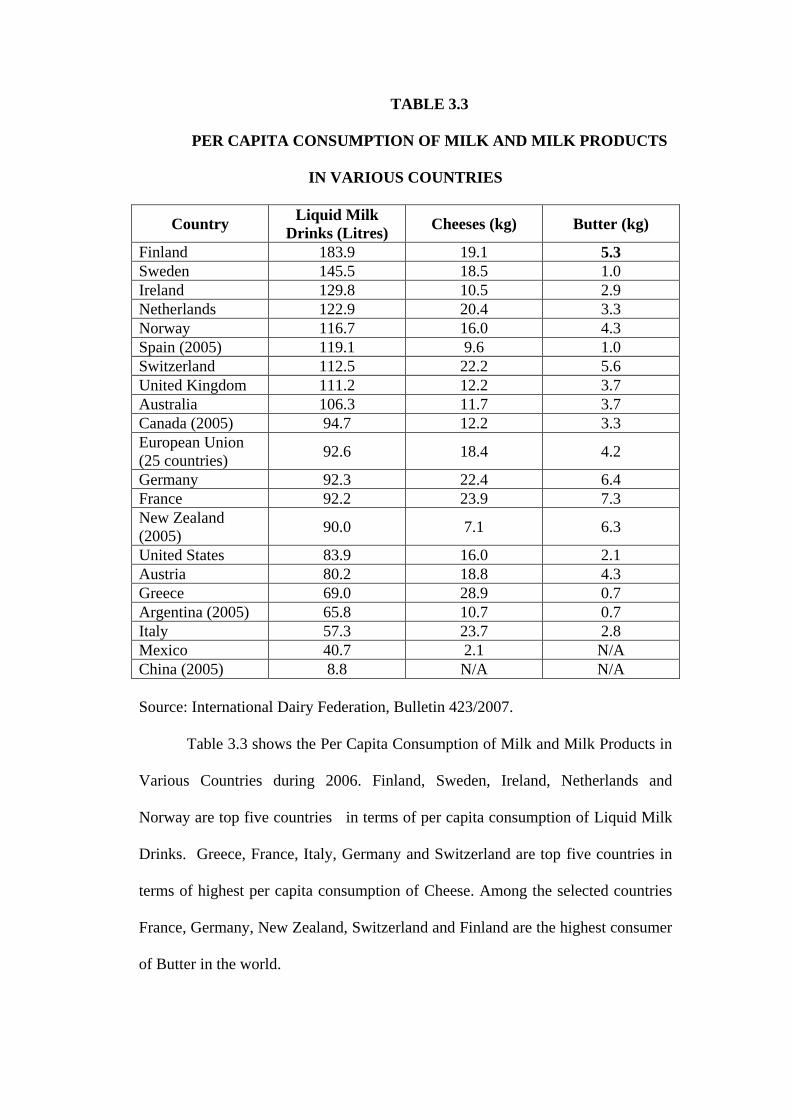

cheeses have tended to dominate milk consumption. Table 3.3 illustrates milk per

capita consumption information from various countries of the world.

TABLE 3.3

PER CAPITA CONSUMPTION OF MILK AND MILK PRODUCTS

IN VARIOUS COUNTRIES

Country Liquid Milk

Drinks (Litres) Cheeses (kg) Butter (kg)

Finland 183.9 19.1 5.3

Sweden 145.5 18.5 1.0

Ireland 129.8 10.5 2.9

Netherlands 122.9 20.4 3.3

Norway 116.7 16.0 4.3

Spain (2005) 119.1 9.6 1.0

Switzerland 112.5 22.2 5.6

United Kingdom 111.2 12.2 3.7

Australia 106.3 11.7 3.7

Canada (2005) 94.7 12.2 3.3

European Union

(25 countries) 92.6 18.4 4.2

Germany 92.3 22.4 6.4

France 92.2 23.9 7.3

New Zealand

(2005) 90.0 7.1 6.3

United States 83.9 16.0 2.1

Austria 80.2 18.8 4.3

Greece 69.0 28.9 0.7

Argentina (2005) 65.8 10.7 0.7

Italy 57.3 23.7 2.8

Mexico 40.7 2.1 N/A

China (2005) 8.8 N/A N/A

Source: International Dairy Federation, Bulletin 423/2007.

Table 3.3 shows the Per Capita Consumption of Milk and Milk Products in

Various Countries during 2006. Finland, Sweden, Ireland, Netherlands and

Norway are top five countries in terms of per capita consumption of Liquid Milk

Drinks. Greece, France, Italy, Germany and Switzerland are top five countries in

terms of highest per capita consumption of Cheese. Among the selected countries

France, Germany, New Zealand, Switzerland and Finland are the highest consumer

of Butter in the world.

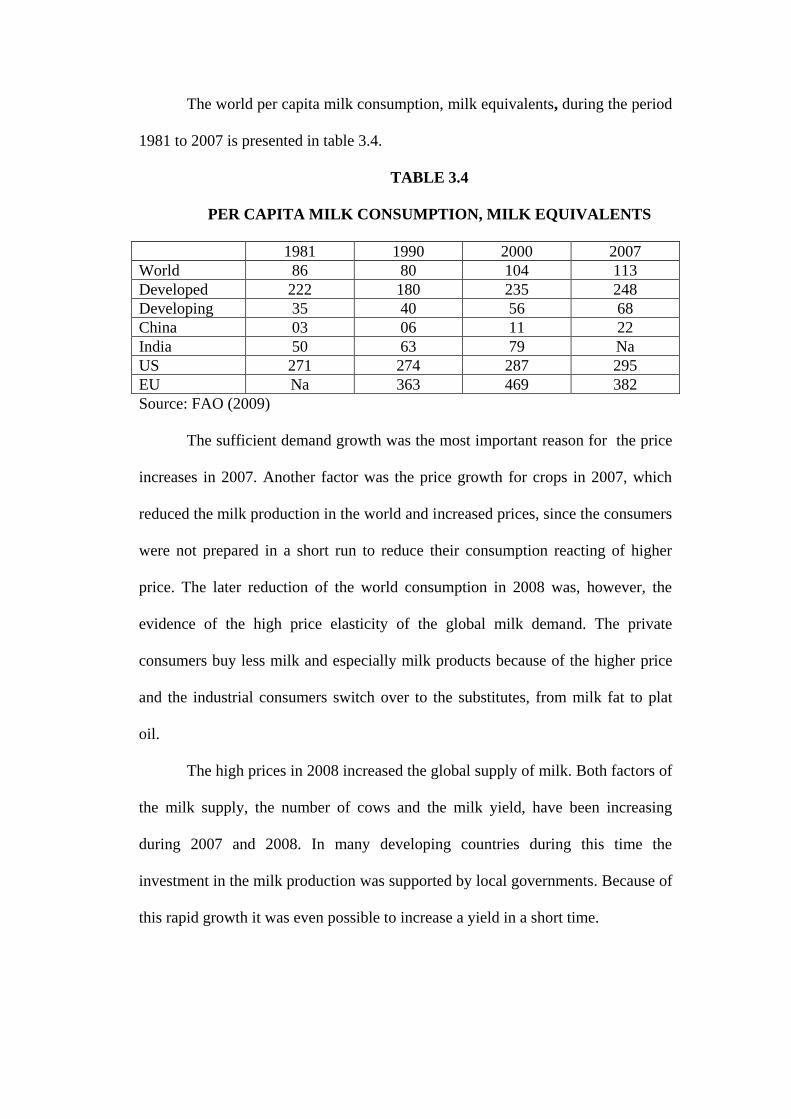

The world per capita milk consumption, milk equivalents, during the period

1981 to 2007 is presented in table 3.4.

TABLE 3.4

PER CAPITA MILK CONSUMPTION, MILK EQUIVALENTS

1981 1990 2000 2007

World 86 80 104 113

Developed 222 180 235 248

Developing 35 40 56 68

China 03 06 11 22

India 50 63 79 Na

US 271 274 287 295

EU Na 363 469 382

Source: FAO (2009)

The sufficient demand growth was the most important reason for the price

increases in 2007. Another factor was the price growth for crops in 2007, which

reduced the milk production in the world and increased prices, since the consumers

were not prepared in a short run to reduce their consumption reacting of higher

price. The later reduction of the world consumption in 2008 was, however, the

evidence of the high price elasticity of the global milk demand. The private

consumers buy less milk and especially milk products because of the higher price

and the industrial consumers switch over to the substitutes, from milk fat to plat

oil.

The high prices in 2008 increased the global supply of milk. Both factors of

the milk supply, the number of cows and the milk yield, have been increasing

during 2007 and 2008. In many developing countries during this time the

investment in the milk production was supported by local governments. Because of

this rapid growth it was even possible to increase a yield in a short time.

One important reason for the supply growth in late 2007 and the beginning

of 2008 was the export of the European intervention funds for milk and butter,

which increased supply on the world market. In terms of the liberalization of the

world milk market it appears that the price elasticity of milk supply in the short-run

is very high.

Reduction of global demand and growing supply of milk in 2008 created a

sufficient gap between production and consumption and therefore led to decreasing

of prices for milk since summer 2008. During the period of higher prices in 2007

many countries used the new built capacities in dairy production especially for the

export. With lower prices it became less attractive in 2008 to export. A part of the

production went down on the domestic markets and additionally lowered the

prices.

In 2008 the positions of the major exporters have been returned to the

traditional exporters like Australia, New Zeeland and USA. Asian market has

imported in 2008 about 19 million tonnes of dairy products, which amounts to half

of the global milk trade. The net export position of Oceania is 14 million tonnes

and of the EU is 7.8 million tonnes (FAO, 2009), which shows the dependency of

the EU from the consumption and import demand in the Asian countries.

In spite of the temporary supply overhang, the world market is still not able

to cover the growing demand for milk and dairy products because of low

productivity. For example, the average yield in Asia is still 0.91 tonnes per animal

per year, while in North America in 2007 it was 9,01 tonnes. Asia has 52% of

global livestock, but only 34% of the world production. Nearly 80 per cent of

overall milk production over the past decade were supplied by producers with two

to five cows (FAO, 2009).

Therefore it is expected that the middle and big sized farms would have the

cost advantages for the next years and would be the major exporters of milk. The

costs of milk production differ within regions and between regions. The last

research of IFCN shows significant cost advantages of larger dairy farms compared

to smaller ones (IFCN, 2008). However, the crop and energy price growth in 2007

and 2008 contributes more to the costs of the larger farms than that in smaller

farms and in some developing and transitional countries the smaller farms with self

- production of feed became more attractive. This could decline the amount of milk

production in the future in these regions and increase export chances for dairy

producers in developed countries.

The political protection of the milk producers during the past five years in

the EU and the USA kept domestic prices on a high level in 1990 and increased

production in these regions. The liberalization of the milk market according to

WTO agreements since 2000 increased the instability of prices, and pressure from

imported milk and dairy products. The milk production quote with guarantee price

in the EU will end in the EU by 2015, continuously growing in the previous years

in order to adjust the producers to the new market conditions. The result is

sufficient production in all EU-countries, because especially big companies tried to

use the new expanded production rights, hoping on the high market prices for milk.

The constant or in some of EU countries declining demand for milk is the reason

for the fast growing over production and decreasing price.

The higher prices in 2007 allowed the EU to cut the export subsidies for

milk, which was planned according to WTO obligations. As a result the European

milk producers were facing the problem of excess production and decrease in

demand in 2008 stronger over production and demand cutting, having no

possibility to sell this over production on the world markets, because the world

prices were still lower than that in the EU.

At the moment the marginal price covering the costs in the EU is about 25

Ct/kg, while in South America, Oceania, Poland it is below 17 US-$/100 kg milk,

in Argentina, India and Poland the larger farms can produce milk below 15 US-$

per 100 kg milk (IFCN, 2009). The milk prices in the EU in 2001-2007 had

seasonal fluctuations with the general declining trend. Since mid 2007 the EU

prices grew steadily and in August 2008 declined considerably in two other milk

producing countries. So the price instability seems to be higher in the EU than in

other producing countries.

The bad economical situation due to lower prices for milk in 2008/2009

affected primarily the small producers. The European politicians decided in 2009

after the protests of milk farmers in many EU countries to increase the direct

support of the production, which obviously will increase the milk prices in the EU

market. This would have similar effect as the protection policy in 1990th, when the

overproduction was sold on the world markets with export subsidy. The possible

scenario for milk production in the EU is that under increased price uncertainly the

investor’s confidence in the milk production will be lower and that the smaller

farmers, having lower yield and fewer chances for the reduction of cost production

will disappear from the market.

At the same time, it is expected that the import would grow, the investment

in milk production made during the price shock of 2007 will allow the developing

countries to produce more milk for export. The EU had lost already some positions

in export in 2004 – 2008.

German milk producers in February 2009 got only 24,4 Ct/kg, it was the

lowest price since 1980. The world finance crisis weakens the milk product sector

in the EU, because consumers in especially developing countries were not able to

pay for the relative expensive European dairy products. The forecast of Zentrale

Markt and Preisberichtstelle (ZMP) is that the milk production in 2009 would not

grow, even if the producers’ quotas will expand (ZMP, 2009). However, in the

long run the growing demand for the dairy products would be the major factor for

the price increase; the Food and Agriculture Organization of the United Nations

(FAO) and the Organization for Economic Co-operation and Development

(OECD) estimated that prices of skim and whole milk powder between US$3 000

and $3 700 per tone over the next decade, which is 50- 90 percent higher than the

previous five years’ average (FAO, 2009).

It is to expect that the quality of milk in combination with low prices will

be the most important factors of the global competitiveness of milk producers. The

differences in the technology and market infrastructure in the EU countries will be

critical for covering the milk demand with domestic supply and for the possibility

to gain from the milk export.

3.5 THE DAIRY INDUSTRY

Dairy companies all over the world face a number of changes and

challenges which are forcing them to reconsider their strategies. The most

important challenges are a growing demand for dairy products, with world demand

growing by 2 per cent a year or a quantity equal to the entire annual production of

Australia, coupled with concerns about the milk supply growing at a slower pace

than demand. Furthermore, dairy companies face an increasing number of

consumer requirements in combination with increasing customer power. Food

retailers, the foodservice industry and the food processing industry are the key

customers for dairy products. The leading companies in this sector tend to be

significantly larger than the players in the dairy industry and the on-going global

consolidation process is further increasing their market power. Consequently, the

concentration process by means of mergers, acquisitions and strategic alliances in

the dairy industry has been very pronounced and is expected to continue. As

demand in dairy products is not rising at equal rates all over the world but hardly at

all in developed and strongly in some developing regions the challenges dairy

companies face vary depending on the market they operate in. Companies

operating in the big but mature dairy markets of Europe and the US face limited

market growth opportunities in terms volume as per capita consumption levels are

among the highest in the world and growth can only occur by increasing market

shares or switching to higher value-added products. Due to these limited market

opportunities in developed countries, multinational dairy companies are often

attracted by strong growth markets in developing countries. To benefit from the

growth of their own domestic markets, local companies will have to raise product

quality and efficiency to be able to withstand foreign competition.

3.6 DAIRY TRADE

The dairy sector is highly localized, as milk is a bulky and perishable

product, and dairy products are mostly consumed in the country or region where

they are produced. Only a small fraction of global production is traded

internationally. Despite the technological developments in refrigeration and

transportation only 7 per cent of the milk produced is traded internationally if intra-

EU trade is excluded.

Trade in dairy products is very volatile, as dairy trade flows can be affected

by (a) overall economic situation in a country, (b) fluctuations in supply and

demand, (c) changing exchange rates and (d) political measures. Additional

volatility is introduced by the fact that the global dairy market is extremely

concentrated in terms of buyers and sellers; hence, supply or demand shocks are

not easily absorbed. With demand for dairy products most rapidly rising in regions

that are not self-sufficient in milk production, volumes of dairy trade are growing.

Also the share of global dairy production that is traded will increase as trade will

grow at a faster pace than milk production. Since 1990, a shift in world dairy

exports from high export subsidizing countries, e.g. EU and US towards non-

subsidizing countries, e.g. New Zealand and Australia has been taking place. The

developed countries account for 62 per cent of the world’s dairy imports (measured

in milk equivalents) and 93 per cent of the exports, show clearly that the major part

of the global dairy trade takes place among developed countries.

3.7 DAIRY POLICIES

In many, and predominantly in developed countries, the dairy market is one

of the most heavily regulated agricultural markets. Government interventions in the

domestic dairy market are most commonly aimed at controlling quantities of

production, establishing minimum prices and guaranteeing farmers’ incomes.

Frequently, governments also intervene through public purchases and storage of

oversupply or apply policies to foster dairy consumption. In countries where

domestic prices for dairy products are supported well above world market prices,

as a consequence, the domestic market has to be protected against foreign

competition in order to ensure the market outlet for domestic farmers who would

otherwise have difficulties to sell their overpriced products. The major policies

countries put in place to limit imports are tariffs and tariff rate quotas (TRQs) and

other non-tariff barriers. Globally dairy products are among the agricultural

commodities with the highest tariff protection with an average protection level of

over 80 per cent (the average over all agricultural commodities being 62 percent).

The most important measure promoting exports are export subsidies. Under the

WTO Agreement on Agriculture, countries that used export subsidies on

agricultural products were required to set commitment levels on the volume and

value of export subsidies that could be provided. The most significant user of

export subsidies on dairy is the European Union, accounting for over 80 per cent of

the total value of export subsidies on dairy granted during the period 1995-2001.

Over the same period values of export subsidies have been reduced considerably,

and in the case of the EU, subsidies for dairy exports in 2001 were only slightly

more than 40 per cent of those in 1995.

3.8 INTERNATIONAL STANDARDS FOR DAIRY PRODUCTS

Though standards were initially developed by the public sector to reduce

transaction costs and ensure product quality and safety, they have become a

strategic instrument of competition of differentiated product markets, especially in

developing countries. It can be very difficult for farmers to meet private standards

for milk quality and safety which might require investment in mechanical milking,

on farm cooling, new feeds and genetic improvement. Apart from the initial

investment cost a dairy farmer faces to meet those standards, high operating costs

might render small and even medium-scale units unprofitable in the long run.

Different developments are occurring in the global dairy sector at the

moment: Production in developed countries is falling (together with the number of

dairy cows and farms), while productivity is rising. Simultaneously milk

production in developing countries is growing strongly and the number of cows are

increasing. This development is mirrored in consumption. Dairy consumption

levels in developed countries are constant or falling, whereas in many developing

countries, particularly in East and Southeast Asia and driven by population growth

and growing per capita incomes, dairy consumption is rapidly increasing. With

consumer demand in developing countries rising faster than domestic production,

global dairy trade volumes are increasing as well with import demand of

developing countries being the major driver. OECD dairy policies mainly result in

a financial transfer from consumers in OECD countries to producer and processors.

Actually, some benefits of the OECD dairy policies, through the depressed

world market prices to which they lead, probably also accrue to consumers in

developing countries in terms of increased supply of dairy products predominantly

in urban centres – especially considering that many developing countries are not

expected to be self-sufficient in dairy production in the future and therefore will

have to import increasing amounts of dairy products. However, the artificially low

world market price for dairy products, and here especially milk powder, might

have negative impacts on dairy farmers in developing countries who have to

compete on their local markets with imported milk powder.

3.9 DAIRYING IN INDIA

Dairy development in India has been acclaimed as one of modern India’s

most accomplished development programmes. The State like Gujarat,

Maharashtra, Uttar Pradesh, Haryana, Rajasthan, Andhra Pradesh, Karnataka and

Tamil Nadu are surplus in milk production. The consumption pattern indicates

that 45 per cent of milk is consumed in liquid form, while butter milk/separated

milk (butter and ghee) constitutes 34 per cent. The balance is in the form of milk

powder, ice creams, cheese and other products.

Indian dairying is emerging as a sunrise industry. India represents one of

the world’s largest and fastest growing markets for milk products due to the

increasing disposable incomes among the 250 million strong middle class.

The world dairy is zooming on India for its rapidly growing markets that

promise the ‘moon’. The changing international dairy trade pattern, following

General Agreement on Tariffs and Trade (GATT) and the emergence of the World

Trade Organisation (WTO), offer to the Indian dairy industry an opportunity to

take its bow as an exporter. India’s enthusiasm to integrate with the world

economy is reflected in technological upgradition, professional excellence and

cost-effective approach.

Today, Indian dairy co-operative network is very wide and large. Total 170

milk unions are operated in 346 districts in India and nearly about, 1,22,534 village

level dairy co-operative societies are working under this union. In India 12.96

million farmers are the members of Dairy Co-operative Societies of which 3.4

million are women. The dairy sector provides 70 million farm families triple

benefits of nutritive food, supplementary income and employment for family

labours who are mainly women.

Indian dairy industry is one of the fastest growing sectors in India. It has

seen incredible growth for the last several years. India holds number one position

in the world in milk production – 88 MT (2003-2004). The global milk production

in the year 2003 was reported at 600 million tonnes (FAO, 2003).

Indian dairy industry is growing very rapidly at 4.5 per cent per annum.

The world milk production by 2020 is expected to rise to 350-700 million tonnes.

India’s share to world milk production at that time would substantially increase to

175 MT and 200 MT of milk by the year 2015 and 2020 respectively.

From the present production figure of 108 MT, India’s dairy sector is

expected to triple its production in the next 10 years in view of expanding potential

for export to Europe, Middle East and South East. India’s dairy export share is

less than one per cent. The cost of production of milk per litre in India is the lowest

in the world. In order to take the advantage of lowest cost and increasing

production of milk in India, MNC’s are planning to expand their activities in India.

3.10 DAIRYING BEFORE INDEPENDENCE

Dairying before independence was in a very primitive and old form.

Private persons collected milk from the rural farmers twice a day and sold it door

to door in cities and towns by bicycle in raw conditions. This business was

generally practised around the city at a walkable distance, so that fresh milk would

reach within two to three hours of milking. Village grazers collect the animals,

cows and buffaloes from the backyards, take them out for the whole day for

grazing and bring them back in the evening. A member of the family may do the

feeding and milking. The farmers bring milk to the milk shop by carrying it on

head and shoulder. “A concept of movement of milk for long distance started in

India in 1945. Before 1947, there were some 60 dairy farms with thousands of

crossbred cows in them. The female ones were the best North Indian breed viz.,

the Sahiwal, Siondhi and Tharparker. India had a large number of Princely States,

known as native states, ruled over by the Rajas, Maharajas and Nawabs. Some of

these had state dairies called Palace Dairies and as a hobby, the princes maintained

excellent herd of Indian cows and buffaloes. The Hindus, the Jains and the

Persians’ are strictly against the killing of old animals like cows.

Government of India has established ‘Indian Agricultural Research

Institute’ at Delhi. The cooperative sector is involved in dairy farming activity

along with the private and public sector. The Cooperative Credit Society’s Act

was passed in 1912 and first cooperative dairy society was established at

Allahabad (U.P) in 1913.

Till 1938, there were 19 union societies with 264 primary societies of

11,600 producer members. Only one cooperative dairy in Calcutta was

pasteurizing small quantity of milk for local distribution around in 1925.

Initially people were unaware of purity, hygiene and quality of milk. In

1916, Bombay Municipality’s analyst Dr. L. Joshi for the first time exposed

publicly about unsatisfactory conditions of quality (Purity and hygiene). The

Government of Bombay was the first in the country to take steps to prevent

adulteration of food and by early 1930 every province had food adulteration laws,

analytical laboratories, standardized system of testing, sampling and punishing

offenders. During the Second World War, rationing of food grains had become

very critical and vague for the citizens of Bombay. Milk had also become scarce

and expensive for them. Then the government introduced in the city of Bombay a

subsidized milk distribution scheme from 17th

August 1944. The registered

customers had to fetch milk in their own vessels from the milk center in the

morning and afternoons. This was the starting point of public milk distribution

under a Milk Commissioner from 1st April 1945 who coordinated various activities

under the new department.

3.11 POST INDEPENDENCE DAIRY DEVELOPMENT

From the beginning of the first plan on 1st April 1951, there was cattle

colonization project for removal of 15,000 buffaloes with their owners and

attendants from Bombay city stable to Aarey milk colony. The largest processing

and bottling plant with 25,000 liters per day capacity was erected at Aarey milk

colony, which went into operation on 15th

December 1950.

Dairy cooperatives are in existence in the country since 1913; Most of them

are collecting and selling raw milk to the local consumers. But the first large scale

and systematic break-through in dairy cooperatives in India was made in 1948 by

Kaira Distict Cooperative Milk Producers Union, Anand, initially it was processing

and dispatching milk for distribution in loose form in Bombay. Later, it built its

own new dairy at Anand in which it was processing, manufacturing and packaging

milk products in its own brand name “Amul”.

During the first five years plan, the Milk Schemes at Bombay, Calcutta and

Delhi were on the way. Projects for collecting milk from villages, processing and

distribution were started in other states like Andhra Pradesh, Bihar, Madyha

Pradesh, Orissa, Tamil Nadu and Uttar Pradesh. In 1945 Dr. H.D. Kay of the

Dairy Research Institute, Shinfield (England) visited India to advise the

Government of India on dairy research. On his recommendation the National

Dairy Research Institute (NDRI) was set up at Karnal (then in Punjab, now in

Haryana). During the first five year plan, an allotment of Rs. 78 million was made

for dairy development. In second five-year plan, dairy development began to take

shape on an organized basis. The expenditure during this plan amounted to Rs.120

million.

A number of states created separate dairy development departments to give

exclusive attention to development of dairying. The programme envisaged

establishment of Thirty six fluid milk handling plants at large consuming centers,

six milk product factories and expansion of facilities for salvage of dry animals

from city stables. In addition to the existing one at Bangalore, two additional

Regional Dairy Research Stations were established at the Aaery Milk Colony,

Bombay and Kalyani near Calcutta.

Training to personnel in quality control issues was also undertaken. Seven

additional fluid milk handling plants were set up as pilot milk projects. It was

during this period that a gift of rail and road milk tankers from New Zealand was

received under Bombay Milk Scheme for transportation of milk between Anand

and Bombay. This was for the first time that bulk transport of milk was started in

India. The setting up of fifty five fluid milk projects for the cities having

population of 1,00,000 each, eight rural creameries, six milk product factories, two

cheese factories and four cattle feed compounding factories were taken in hand

during third five year plan. A Modern feed compounding mill was set up in

Anand area from the funds gifted by the United Kingdom. Some more states

established separate dairy departments. The National Dairy Development Board

(NDDB) was set up in September 1965 with headquarters in Anand in Gujarat

State. The major milk product manufacturing factories in India during the post

independence period is given in table 3.5.

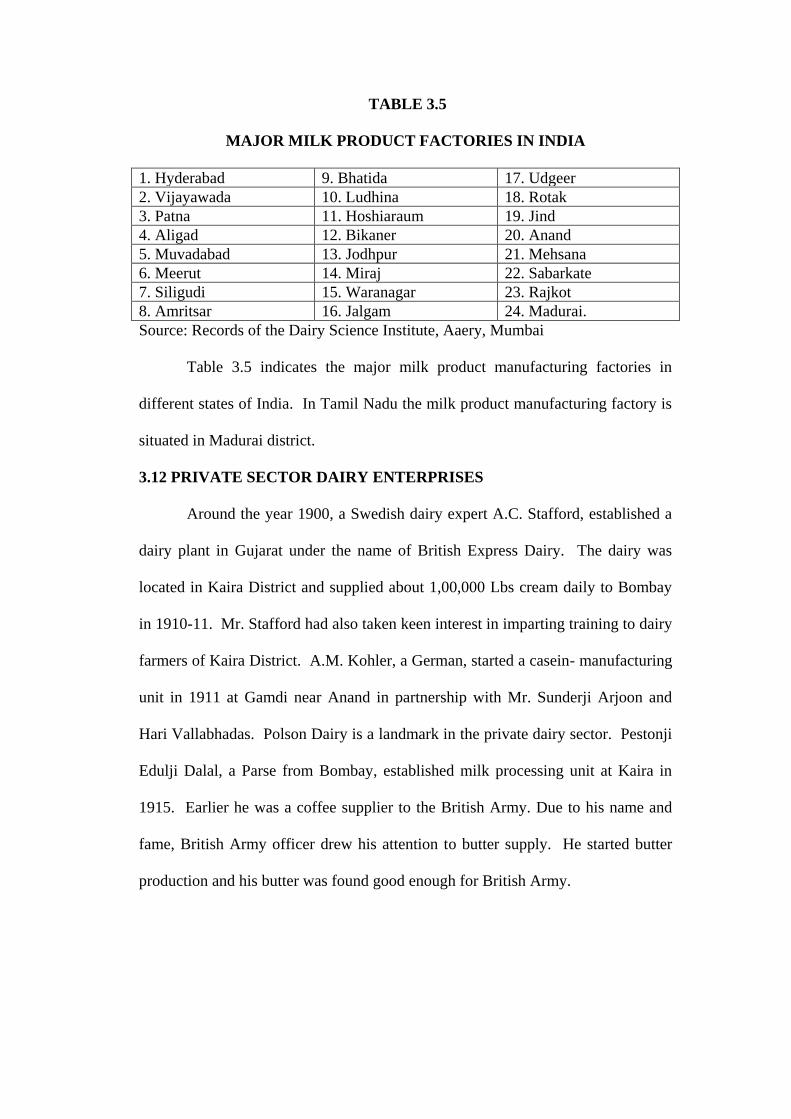

TABLE 3.5

MAJOR MILK PRODUCT FACTORIES IN INDIA

1. Hyderabad 9. Bhatida 17. Udgeer

2. Vijayawada 10. Ludhina 18. Rotak

3. Patna 11. Hoshiaraum 19. Jind

4. Aligad 12. Bikaner 20. Anand

5. Muvadabad 13. Jodhpur 21. Mehsana

6. Meerut 14. Miraj 22. Sabarkate

7. Siligudi 15. Waranagar 23. Rajkot

8. Amritsar 16. Jalgam 24. Madurai.

Source: Records of the Dairy Science Institute, Aaery, Mumbai

Table 3.5 indicates the major milk product manufacturing factories in

different states of India. In Tamil Nadu the milk product manufacturing factory is

situated in Madurai district.

3.12 PRIVATE SECTOR DAIRY ENTERPRISES

Around the year 1900, a Swedish dairy expert A.C. Stafford, established a

dairy plant in Gujarat under the name of British Express Dairy. The dairy was

located in Kaira District and supplied about 1,00,000 Lbs cream daily to Bombay

in 1910-11. Mr. Stafford had also taken keen interest in imparting training to dairy

farmers of Kaira District. A.M. Kohler, a German, started a casein- manufacturing

unit in 1911 at Gamdi near Anand in partnership with Mr. Sunderji Arjoon and

Hari Vallabhadas. Polson Dairy is a landmark in the private dairy sector. Pestonji

Edulji Dalal, a Parse from Bombay, established milk processing unit at Kaira in

1915. Earlier he was a coffee supplier to the British Army. Due to his name and

fame, British Army officer drew his attention to butter supply. He started butter

production and his butter was found good enough for British Army.

3.13 PERFORMANCE OF INDIAN DAIRY SECTOR OVER THE YEARS

During the early decade of 50s and 60s, milk production in India was

stagnant and the scarcities of resources in terms of livestock led to the need for

major policy reforms in the dairy sector. The strategy for organized dairy

development in India was actually conceived in the late 1960s, within a few years

after the National Dairy Development Board (NDDB) was founded in 1965.

NDDB began its operation with an objective of making dairying a means for a

better future for the millions of milk producers at the grass root level with its

consistent efforts. It rested on the Operation Flood Programme (OFP). The OFP

was a major policy development designed to develop dairying by replicating the

Anand Model for dairy development so as to provide the missing market link in the

formal milk sector between the urban milk consumer and the rural producer

through a network of cooperatives. The OFP was instrumental in creating strong

linkages among millions of smallholders producers and urban consumers. Prior

to OFP, the link between the producer and consumer was completely missing.

OFP in India helped to bridge the gap between formal dairy sector and rural

producers by developing gradual and concrete slabs of co-operatives and plants in

India. It was the first ever step being taken toward dairy infrastructure

development in India. OFP for the first time recognized the need of the rural milk

producers and paid attention towards their thorough development.

It played the key role in bringing about the transformation in dairy

development in the country. The OFP established milk producers’ cooperatives in

villages and made modern technology available to them. The broad objectives

were to increase milk production, augment rural incomes, and transfer to milk

producers, the profits of milk marketing.

The performance of Indian dairy sector during the 50s and 60s was not

remarkable. However with the successful implementation of OFP during the 70s,

the dairy sector achieved four fold growths rate by touching the mark of 4.51

during a single decade from 1971-81. Since then a gradual increase in growth rate

has been observed with 5.21 till 1996 in an era which acknowledged the

emergence of more globalized and liberalized policies in world trade. Soon after

this, growth of Indian dairy sector declined by the end of the year 2005 and moved

down to the mark of 4.42. To sum up, it may be inferred that the Indian dairy

sector during the past 6 decades has shown consistent growth trends which in turn

resulted in the best ranking in world dairy scenario. Moreover, after globalization,

the milk production in India has increased but even then it is yet waiting for land

mark achievement in world milk trade which could only be possible with balanced

growth of livestock and proper dairy infrastructure development throughout India.

India has a sound base for infrastructure development with an existing 1.9 lakh of

dairy plants and co-operatives. In spite of all hypes and publicity being projected

towards two vital segments of Indian dairy sector viz., organized and unorganized,

the contribution of both is 14:45 per cent respectively. This clearly shows an

increase of three folds in productivity by the latter segment. What is needed at this

stage is to bridge the gap between these two sectors on a moderate basis in order to

get the desired output.

With the successful implementation of the OFP in 1970 and other dairy

development programmes implemented by the State and Central Governments,

increased demand driven by increased population, higher incomes and

urbanization, milk output increased substantially in India. As a result, India has

emerged as the world’s largest milk producing nation. Milk production has

increased by about 4 per cent a year, and it has increased from 22 million tonnes in

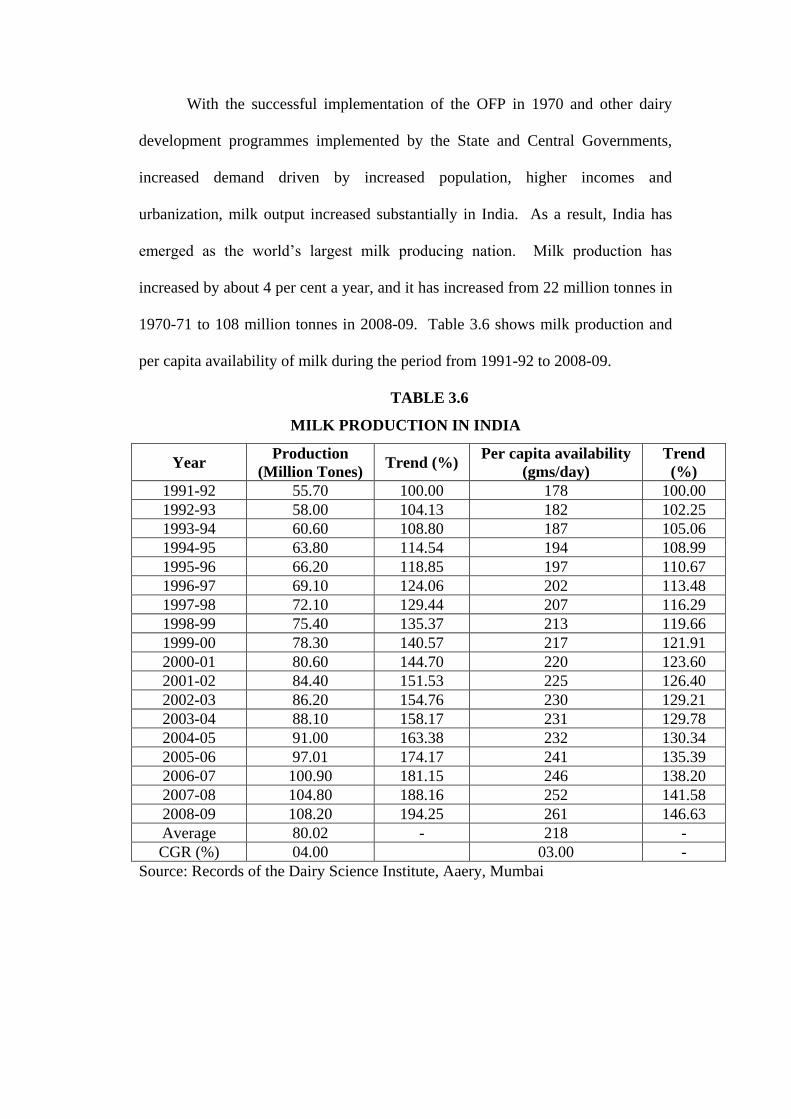

1970-71 to 108 million tonnes in 2008-09. Table 3.6 shows milk production and

per capita availability of milk during the period from 1991-92 to 2008-09.

TABLE 3.6

MILK PRODUCTION IN INDIA

Year Production

(Million Tones) Trend (%)

Per capita availability

(gms/day)

Trend

(%)

1991-92 55.70 100.00 178 100.00

1992-93 58.00 104.13 182 102.25

1993-94 60.60 108.80 187 105.06

1994-95 63.80 114.54 194 108.99

1995-96 66.20 118.85 197 110.67

1996-97 69.10 124.06 202 113.48

1997-98 72.10 129.44 207 116.29

1998-99 75.40 135.37 213 119.66

1999-00 78.30 140.57 217 121.91

2000-01 80.60 144.70 220 123.60

2001-02 84.40 151.53 225 126.40

2002-03 86.20 154.76 230 129.21

2003-04 88.10 158.17 231 129.78

2004-05 91.00 163.38 232 130.34

2005-06 97.01 174.17 241 135.39

2006-07 100.90 181.15 246 138.20

2007-08 104.80 188.16 252 141.58

2008-09 108.20 194.25 261 146.63

Average 80.02 - 218 -

CGR (%) 04.00 03.00 -

Source: Records of the Dairy Science Institute, Aaery, Mumbai

As per table 3.6 the milk production in India has increased to 108.20 per cent

in 2008-09 as compared to 1991-92. The per capita availability of milk has increased

to 146.63 per cent during the same period. The compound growth rate milk

production is 4 per cent and per capita availability of milk is 3 per cent during the

period.

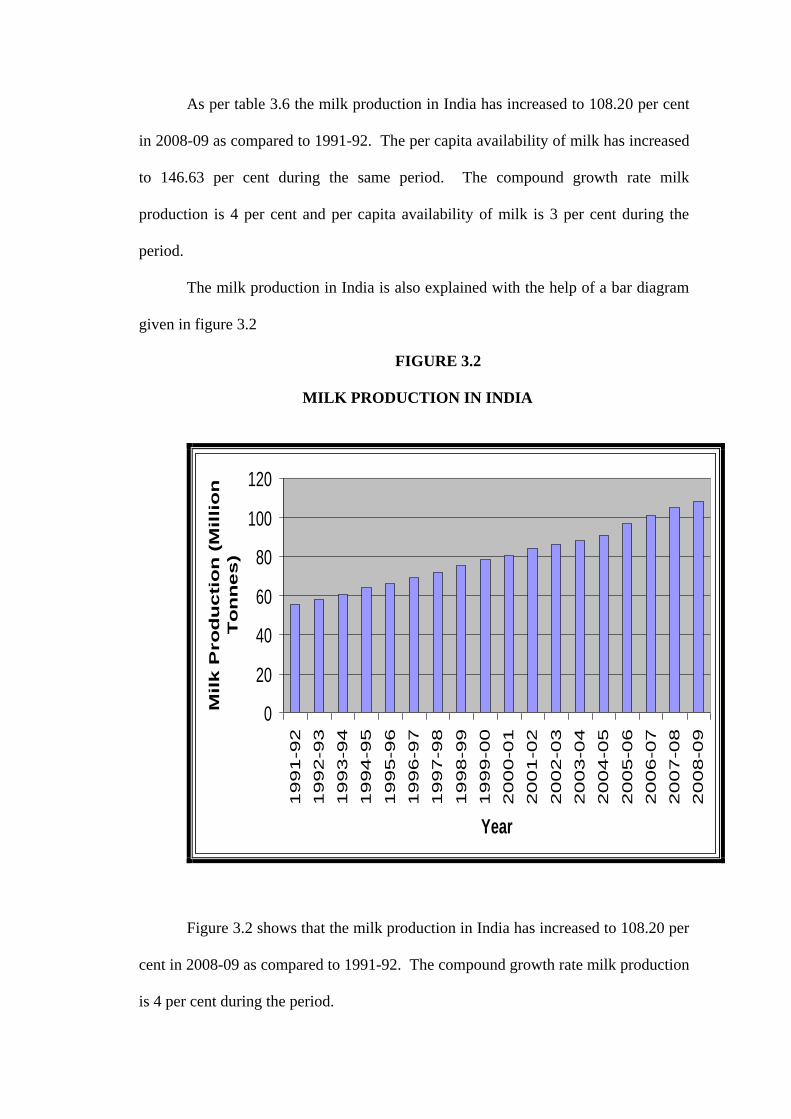

The milk production in India is also explained with the help of a bar diagram

given in figure 3.2

FIGURE 3.2

MILK PRODUCTION IN INDIA

0

20

40

60

80

100

120

19

91

-92

19

92

-93

19

93

-94

19

94

-95

19

95

-96

19

96

-97

19

97

-98

19

98

-99

19

99

-00

20

00

-01

20

01

-02

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

20

08

-09

Year

Mil

k P

ro

du

cti

on

(M

illi

on

To

nn

es

)

Figure 3.2 shows that the milk production in India has increased to 108.20 per

cent in 2008-09 as compared to 1991-92. The compound growth rate milk production

is 4 per cent during the period.

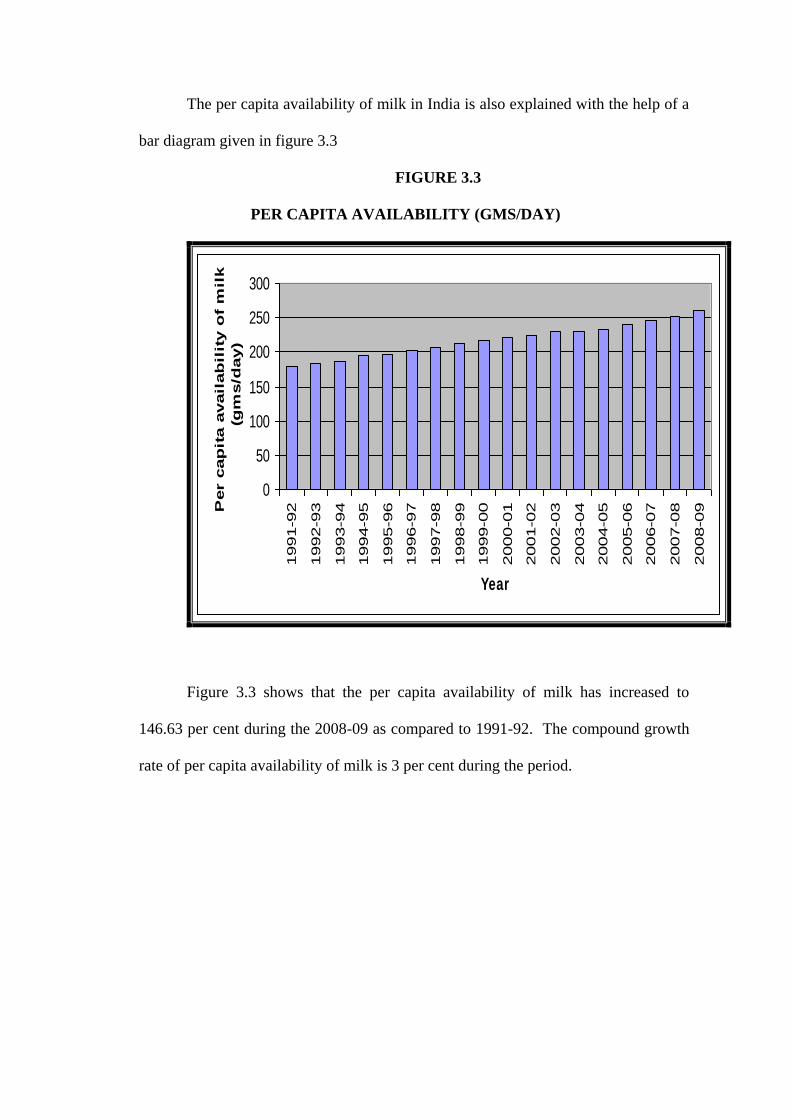

The per capita availability of milk in India is also explained with the help of a

bar diagram given in figure 3.3

FIGURE 3.3

PER CAPITA AVAILABILITY (GMS/DAY)

0

50

100

150

200

250

3001991-9

2

1992-9

3

1993-9

4

1994-9

5

1995-9

6

1996-9

7

1997-9

8

1998-9

9

1999-0

0

2000-0

1

2001-0

2

2002-0

3

2003-0

4

2004-0

5

2005-0

6

2006-0

7

2007-0

8

2008-0

9

Year

Per c

ap

ita a

vail

ab

ilit

y o

f m

ilk

(gm

s/d

ay)

Figure 3.3 shows that the per capita availability of milk has increased to

146.63 per cent during the 2008-09 as compared to 1991-92. The compound growth

rate of per capita availability of milk is 3 per cent during the period.

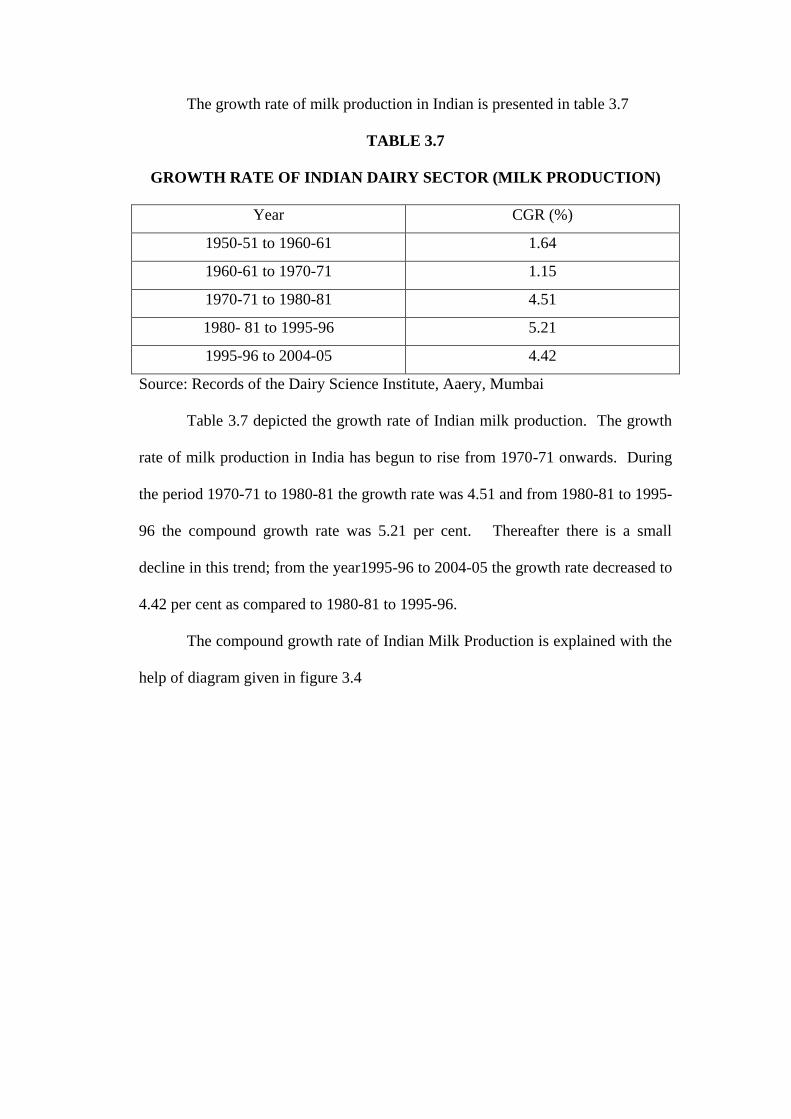

The growth rate of milk production in Indian is presented in table 3.7

TABLE 3.7

GROWTH RATE OF INDIAN DAIRY SECTOR (MILK PRODUCTION)

Year CGR (%)

1950-51 to 1960-61 1.64

1960-61 to 1970-71 1.15

1970-71 to 1980-81 4.51

1980- 81 to 1995-96 5.21

1995-96 to 2004-05 4.42

Source: Records of the Dairy Science Institute, Aaery, Mumbai

Table 3.7 depicted the growth rate of Indian milk production. The growth

rate of milk production in India has begun to rise from 1970-71 onwards. During

the period 1970-71 to 1980-81 the growth rate was 4.51 and from 1980-81 to 1995-

96 the compound growth rate was 5.21 per cent. Thereafter there is a small

decline in this trend; from the year1995-96 to 2004-05 the growth rate decreased to

4.42 per cent as compared to 1980-81 to 1995-96.

The compound growth rate of Indian Milk Production is explained with the

help of diagram given in figure 3.4

FIGURE 3.4

GROWTH RATE OF INDIAN DAIRY SECTOR (MILK PRODUCTION)

1.641.15

4.51

5.21

4.42

0

1

2

3

4

5

6

1950-51 to

1960-61

1960-61 to

1970-71

1970-71 to

1980-81

1980- 81 to

1995-96

1995-96 to

2004-05

Year

Gro

wth

rate

of

Ind

ian

Dair

y

Secto

r -

Mil

k P

ro

du

cti

on

Figure shows that during the period 1950-51 to 1960-61 the compound

growth rate of milk production was 1.64 per cent and during 1960-61 to 1970-71

the growth rate was 1.15. From the year1995-96 to 2004-05 the growth rate

decreased to 4.42 per cent as compared to 1980-81 to 1995-96.

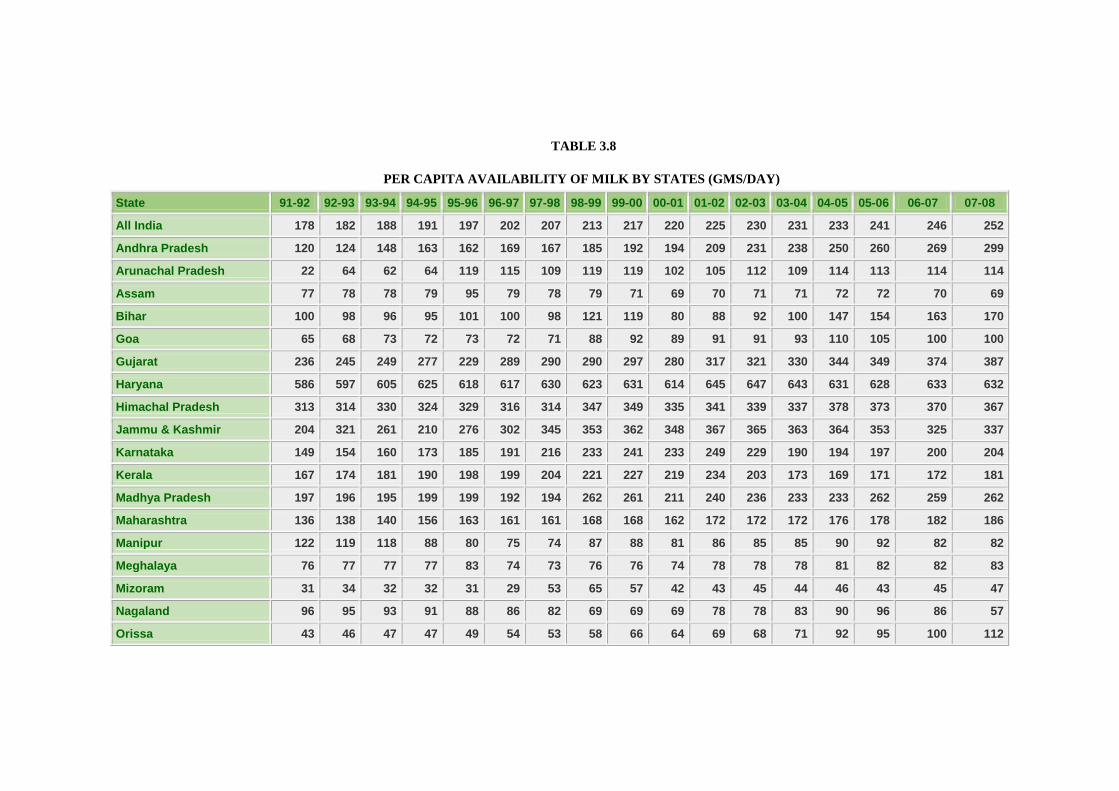

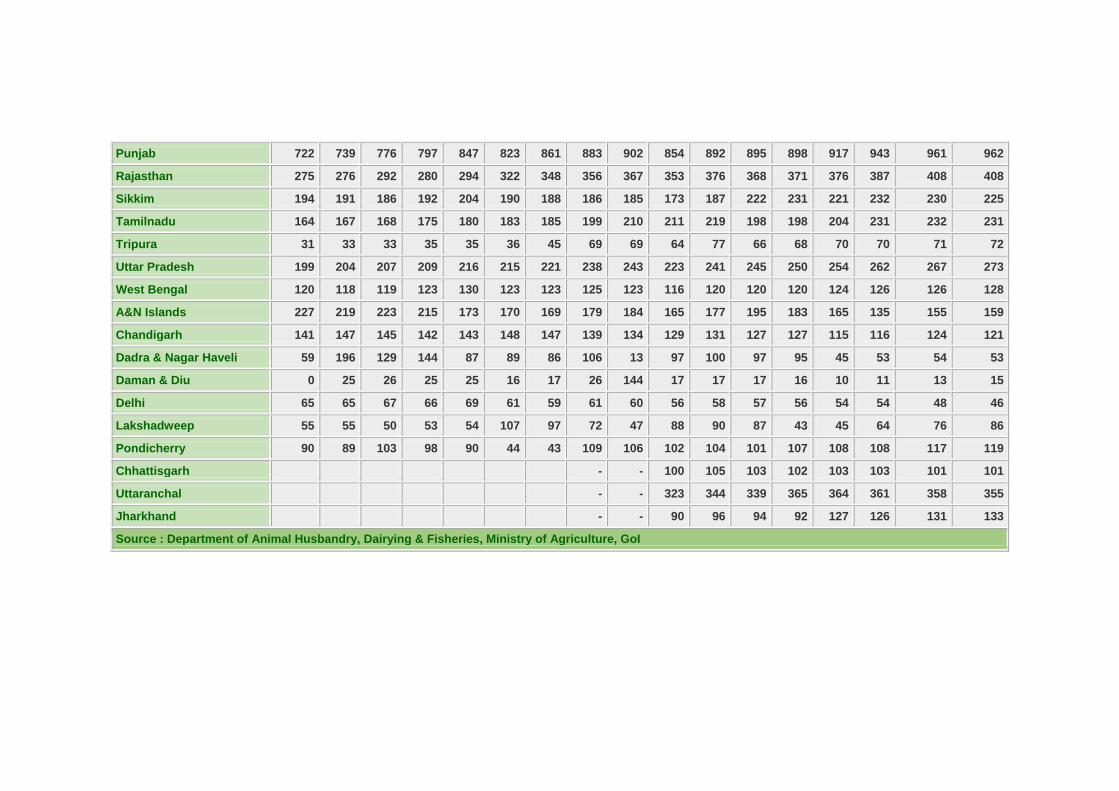

3.14 PER CAPITA AVAILABILITY OF MILK BY STATES

The per capita availability of milk in Indian states is given in table 3.8

TABLE 3.8

PER CAPITA AVAILABILITY OF MILK BY STATES (GMS/DAY)

State 91-92 92-93 93-94 94-95 95-96 96-97 97-98 98-99 99-00 00-01 01-02 02-03 03-04 04-05 05-06 06-07 07-08

All India 178 182 188 191 197 202 207 213 217 220 225 230 231 233 241 246 252

Andhra Pradesh 120 124 148 163 162 169 167 185 192 194 209 231 238 250 260 269 299

Arunachal Pradesh 22 64 62 64 119 115 109 119 119 102 105 112 109 114 113 114 114

Assam 77 78 78 79 95 79 78 79 71 69 70 71 71 72 72 70 69

Bihar 100 98 96 95 101 100 98 121 119 80 88 92 100 147 154 163 170

Goa 65 68 73 72 73 72 71 88 92 89 91 91 93 110 105 100 100

Gujarat 236 245 249 277 229 289 290 290 297 280 317 321 330 344 349 374 387

Haryana 586 597 605 625 618 617 630 623 631 614 645 647 643 631 628 633 632

Himachal Pradesh 313 314 330 324 329 316 314 347 349 335 341 339 337 378 373 370 367

Jammu & Kashmir 204 321 261 210 276 302 345 353 362 348 367 365 363 364 353 325 337

Karnataka 149 154 160 173 185 191 216 233 241 233 249 229 190 194 197 200 204

Kerala 167 174 181 190 198 199 204 221 227 219 234 203 173 169 171 172 181

Madhya Pradesh 197 196 195 199 199 192 194 262 261 211 240 236 233 233 262 259 262

Maharashtra 136 138 140 156 163 161 161 168 168 162 172 172 172 176 178 182 186

Manipur 122 119 118 88 80 75 74 87 88 81 86 85 85 90 92 82 82

Meghalaya 76 77 77 77 83 74 73 76 76 74 78 78 78 81 82 82 83

Mizoram 31 34 32 32 31 29 53 65 57 42 43 45 44 46 43 45 47

Nagaland 96 95 93 91 88 86 82 69 69 69 78 78 83 90 96 86 57

Orissa 43 46 47 47 49 54 53 58 66 64 69 68 71 92 95 100 112

Punjab 722 739 776 797 847 823 861 883 902 854 892 895 898 917 943 961 962

Rajasthan 275 276 292 280 294 322 348 356 367 353 376 368 371 376 387 408 408

Sikkim 194 191 186 192 204 190 188 186 185 173 187 222 231 221 232 230 225

Tamilnadu 164 167 168 175 180 183 185 199 210 211 219 198 198 204 231 232 231

Tripura 31 33 33 35 35 36 45 69 69 64 77 66 68 70 70 71 72

Uttar Pradesh 199 204 207 209 216 215 221 238 243 223 241 245 250 254 262 267 273

West Bengal 120 118 119 123 130 123 123 125 123 116 120 120 120 124 126 126 128

A&N Islands 227 219 223 215 173 170 169 179 184 165 177 195 183 165 135 155 159

Chandigarh 141 147 145 142 143 148 147 139 134 129 131 127 127 115 116 124 121

Dadra & Nagar Haveli 59 196 129 144 87 89 86 106 13 97 100 97 95 45 53 54 53

Daman & Diu 0 25 26 25 25 16 17 26 144 17 17 17 16 10 11 13 15

Delhi 65 65 67 66 69 61 59 61 60 56 58 57 56 54 54 48 46

Lakshadweep 55 55 50 53 54 107 97 72 47 88 90 87 43 45 64 76 86

Pondicherry 90 89 103 98 90 44 43 109 106 102 104 101 107 108 108 117 119

Chhattisgarh - - 100 105 103 102 103 103 101 101

Uttaranchal - - 323 344 339 365 364 361 358 355

Jharkhand - - 90 96 94 92 127 126 131 133

Source : Department of Animal Husbandry, Dairying & Fisheries, Ministry of Agriculture, GoI

97

The state wise per capita availability of milk in India during 1991-92 to

2007-08 is shown in table 3.8. All India per capita availability of milk has

increased to about 142 per cent in the year 2007-08 as compared to 1991-92, it is

pertinent to mention that the per capita availability of milk in Tamil Nadu has also

increased to 141 per cent during the same period, which is more or less same in the

all India consumption rate.

3.15 EMERGING GLOBAL SCENARIO VIS-À-VIS INDIAN DAIRY

SCENARIO

In the global context, the production of cow milk is highest though its share

has declined from 85.54 per cent in 1996 to 84 per cent in 2006; while the share of

buffalo milk increased from 10.54 per cent in 1996 to 12.5 per cent in 2006. The

share of sheep and goat milk also declined to the marginal level during the same

period. However, gap in production rate do exist between developing and

developed countries. Over the last 24 years, total world milk production has

increased while the per capita has declined and it can be attributed to falling

production in the developed countries. (Rutherford 1999). India’s status in world

scenario could be acknowledged with the fact that it has become the leader in milk

production. The share of India in the world milk production has increased over the

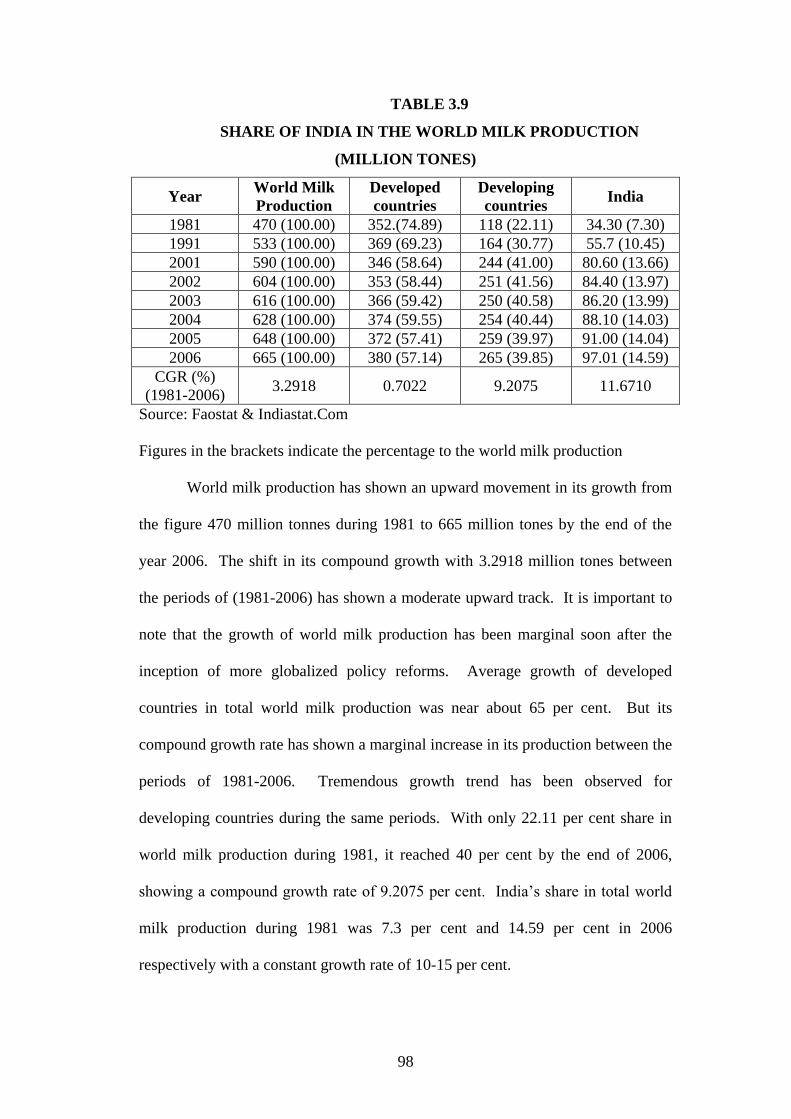

years as is discernible from table 3.9.

98

TABLE 3.9

SHARE OF INDIA IN THE WORLD MILK PRODUCTION

(MILLION TONES)

Year World Milk

Production

Developed

countries

Developing

countries India

1981 470 (100.00) 352.(74.89) 118 (22.11) 34.30 (7.30)

1991 533 (100.00) 369 (69.23) 164 (30.77) 55.7 (10.45)

2001 590 (100.00) 346 (58.64) 244 (41.00) 80.60 (13.66)

2002 604 (100.00) 353 (58.44) 251 (41.56) 84.40 (13.97)

2003 616 (100.00) 366 (59.42) 250 (40.58) 86.20 (13.99)

2004 628 (100.00) 374 (59.55) 254 (40.44) 88.10 (14.03)

2005 648 (100.00) 372 (57.41) 259 (39.97) 91.00 (14.04)

2006 665 (100.00) 380 (57.14) 265 (39.85) 97.01 (14.59)

CGR (%)

(1981-2006) 3.2918 0.7022 9.2075 11.6710

Source: Faostat & Indiastat.Com

Figures in the brackets indicate the percentage to the world milk production

World milk production has shown an upward movement in its growth from

the figure 470 million tonnes during 1981 to 665 million tones by the end of the

year 2006. The shift in its compound growth with 3.2918 million tones between

the periods of (1981-2006) has shown a moderate upward track. It is important to

note that the growth of world milk production has been marginal soon after the

inception of more globalized policy reforms. Average growth of developed

countries in total world milk production was near about 65 per cent. But its

compound growth rate has shown a marginal increase in its production between the

periods of 1981-2006. Tremendous growth trend has been observed for

developing countries during the same periods. With only 22.11 per cent share in

world milk production during 1981, it reached 40 per cent by the end of 2006,

showing a compound growth rate of 9.2075 per cent. India’s share in total world

milk production during 1981 was 7.3 per cent and 14.59 per cent in 2006

respectively with a constant growth rate of 10-15 per cent.

99

Its compound growth has touched the mark of 11.6710 per cent. From the

above table it has been observed that in the past three decades, the percentage share

of developed countries in world milk production has gone down while the

percentage share of developing countries has shown positive results. However, the

Indian dairy sector has shown marginal shift in its production during the same

period. The six major milk producers of the world are India, EU, Russian

Federation, Pakistan and Brazil. Major thrust in production has been seen during

1980-2003 with remarkable growth of 176 per cent in India. In 1980, the share of

six biggest milk producers was 57 per cent of global market and reached 63 per

cent in 2003. It is interesting to note that during the past three decades, the total

milk production has increased but per capita milk production declined from 105 kg

in 1980 to 96 kg in 2004 showing the decline rate of 9 per cent.

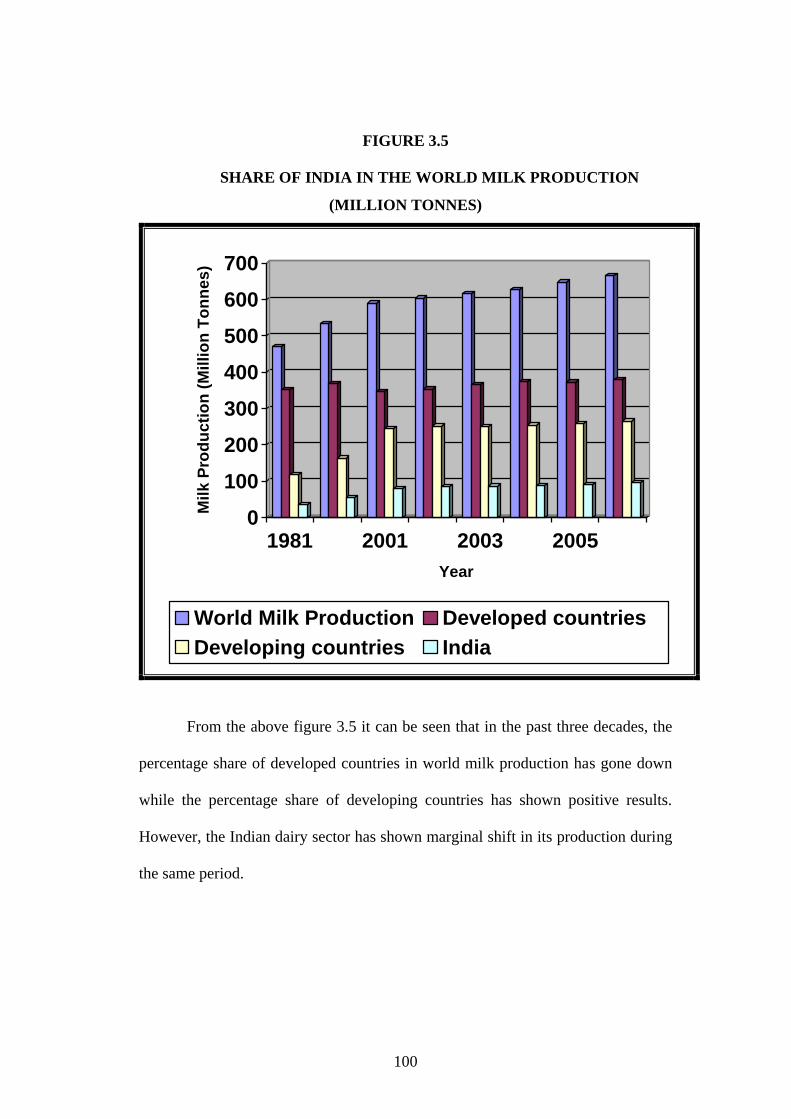

The share of India in the world milk production (million tones) is also

explained with the help of a bar diagram given in figure 3.5

100

FIGURE 3.5

SHARE OF INDIA IN THE WORLD MILK PRODUCTION

(MILLION TONNES)

0

100

200

300

400

500

600

700

Mil

k P

rod

uc

tio

n (

Mil

lio

n T

on

ne

s)

1981 2001 2003 2005

Year

World Milk Production Developed countries

Developing countries India

From the above figure 3.5 it can be seen that in the past three decades, the

percentage share of developed countries in world milk production has gone down

while the percentage share of developing countries has shown positive results.

However, the Indian dairy sector has shown marginal shift in its production during

the same period.

101

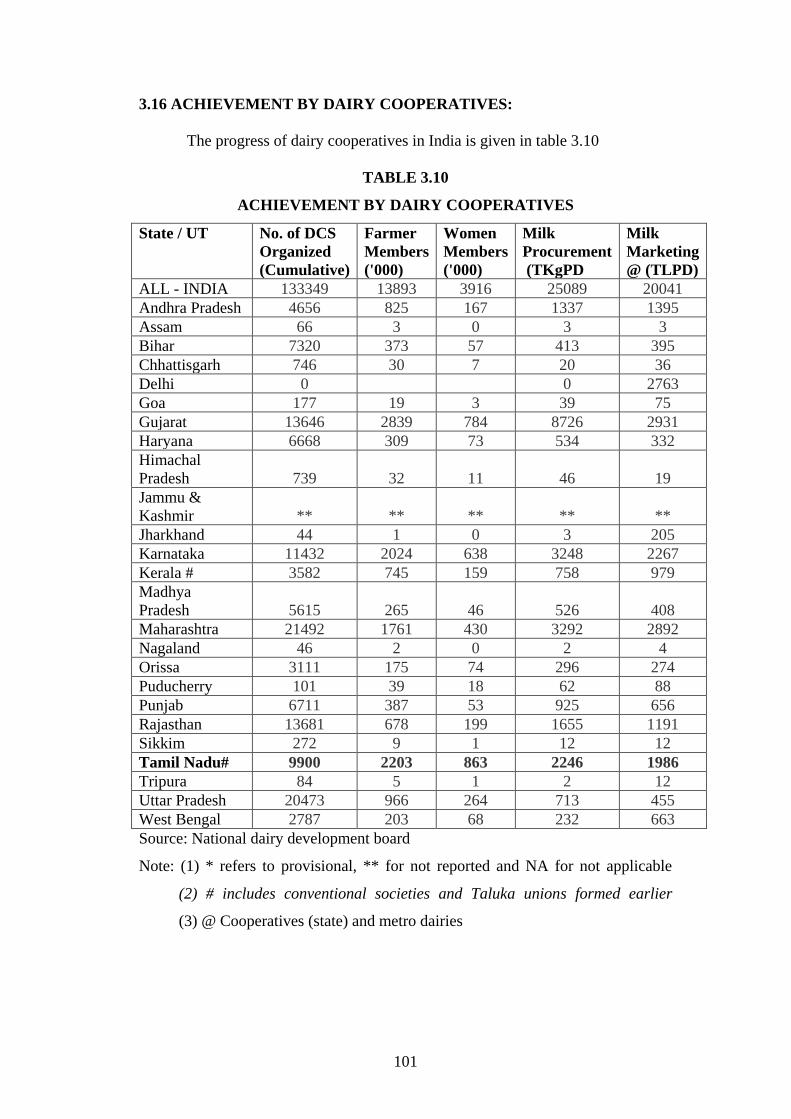

3.16 ACHIEVEMENT BY DAIRY COOPERATIVES:

The progress of dairy cooperatives in India is given in table 3.10

TABLE 3.10

ACHIEVEMENT BY DAIRY COOPERATIVES

State / UT No. of DCS

Organized

(Cumulative)

Farmer

Members

('000)

Women

Members

('000)

Milk

Procurement

(TKgPD

Milk

Marketing

@ (TLPD)

ALL - INDIA 133349 13893 3916 25089 20041

Andhra Pradesh 4656 825 167 1337 1395

Assam 66 3 0 3 3

Bihar 7320 373 57 413 395

Chhattisgarh 746 30 7 20 36

Delhi 0 0 2763

Goa 177 19 3 39 75

Gujarat 13646 2839 784 8726 2931

Haryana 6668 309 73 534 332

Himachal

Pradesh 739 32 11 46 19

Jammu &

Kashmir ** ** ** ** **

Jharkhand 44 1 0 3 205

Karnataka 11432 2024 638 3248 2267

Kerala # 3582 745 159 758 979

Madhya

Pradesh 5615 265 46 526 408

Maharashtra 21492 1761 430 3292 2892

Nagaland 46 2 0 2 4

Orissa 3111 175 74 296 274

Puducherry 101 39 18 62 88

Punjab 6711 387 53 925 656

Rajasthan 13681 678 199 1655 1191

Sikkim 272 9 1 12 12

Tamil Nadu# 9900 2203 863 2246 1986

Tripura 84 5 1 2 12

Uttar Pradesh 20473 966 264 713 455

West Bengal 2787 203 68 232 663

Source: National dairy development board

Note: (1) * refers to provisional, ** for not reported and NA for not applicable

(2) # includes conventional societies and Taluka unions formed earlier

(3) @ Cooperatives (state) and metro dairies

102

Table 3.10 shows the progress of Indian dairy co-operatives. There are

133349 dairy cooperatives, 13893000 Farmer Members of which 3916000 are

Women Members in India. On an average the Indian co-operatives procured 25089

Tonne Kg per Day and marketed 20041Tonne Liters per Day. In Tamil Nadu,

there are 9900 dairy cooperatives including conventional societies and Taluka

unions formed earlier, 2203000 farmer members of which 863000 are women

members. The average milk procured by dairy co-operatives in Tamil Nadu is 2246

Tonne Kg per day and the average milk marketed is 1986 Tonne Liters per day.

The production of milk by dairy co-operatives in Tamil Nadu is approximately 9

per cent of milk procured by the dairy co-operatives in India.

3.17 MILK CONSUMING PATTERN IN INDIA

In India about 46 % of the total milk produced is consumed in liquid form

and 47 % is converted into traditional products like cottage butter, ghee, paneer,

khoya, curd, malai, etc. Only 7 % of the milk goes into the production of western

products like milk powders, processed butter and processed cheese. Among the

milk products manufactured by the organized sector some of the prominent ones

are ghee, butter, cheese, ice creams, milk powders, malted milk food, condensed

milk infants foods etc. Of these ghee alone accounts for 85%. It is estimated that

around 20% of the total milk produced in the country is consumed at producer-

household level and the remaining is marketed through various cooperatives,

private dairies and vendors.

103

Also of the total produce more than 50 per cent is procured by cooperatives

and other private dairies. 60 per cent of the total milk procured by co-operatives is

consumed in fluid form and the rest is used for manufacturing processed value

added dairy products; As far as private dairies are concerned only 45 per cent is

marketed in fluid form and the rest is processed into value added dairy products

like ghee, makhan etc.

Still, several consumers in urban areas prefer to buy loose milk from

vendors due to the strong perception that loose milk is fresh. Also, the current level

of processing and packaging capacity limits the availability of packaged milk. As

high as 98 per cent of milk is produced in rural India and it caters to 72 per cent of

the total population. In the urban sector 28 per cent population consumes 56 per

cent of total milk produced. Even in urban India, as high as 83 per cent of the

consumed milk comes from the unorganized traditional sector. Presently only 12

per cent of the milk market is represented by packaged and branded pasteurised

milk, valued at about Rs. 8,000 crores. Quality of milk sold by the unorganized

sector, however, is inconsistent and so is the price across the season in local areas.

Adulteration of milk with water, caustic soda, and some whitening agents is a

common complaint.

India's dairy market is multi-layered. It's shaped like a pyramid with a vast

market for low-cost milk. The bulk of the demand for milk is from the poor in

urban areas whose individual requirement is small, maybe a glassful for use as

whitener for their tea and coffee. Nevertheless, it adds up to a sizable volume -

millions of litres per day.

104

In the major cities lies an immense growth potential for the modern sector.

Presently, barely 778 out of 3,700 cities and towns are served by its milk

distribution network, dispensing hygienically packed wholesome, quality

pasteurised milk. According to one estimate, the packed milk segment would

double in the next five years, giving both strength and volume to the modern

sector. The narrow tip at the top is a small but affluent market for western type

milk products.

3.18 EXPORT POTENTIAL

India has the potential to become one of the leading players in milk and

milk product exports because of its location. India is located amidst major milk

deficit countries in Asia and Africa. Major importers of milk and milk products are

Bangladesh, China, Hong Kong, Singapore, Thailand, Malaysia, Philippines,

Japan, UAE, Oman and other gulf countries, all located close to India.

India's exports of milk and milk-based products showed a significant drop

of nearly 55% during the past year and was estimated at Rs 436 crore in 2006-07.

Concentrated milk and cream products such as skimmed milk powder continues to

be the largest item of export, which together accounts for nearly 78% of net milk

and milk products exports during the year 2006-07. The exports of skimmed milk

power reached Rs 343 crore in 2006-07 as against Rs 78 crore in 2001-02. On the

other hand butter, butter oil, ghee and other milk fat together accounted for just

over 10% of the net milk and milk product exports from India during 2006-07.

105

3.19 DAIRYING IN TAMIL NADU

Dairying, by playing a significant role in strengthening rural economy has

brought about socio-economic transformation in Tamil Nadu. Small farmers,

marginal farmers and downtrodden constitute majority of milk producers. Dairying

has vast potential to generate employment and has helped in poverty alleviation in

the rural belt. Dairying provides definite and regular income and employment to

millions of rural families throughout the year, especially to women thereby

improving the quality of their life. The milk producers in the State in the Co-

operative sector on an average get daily income of Rs.329.00 lakhs collectively

(Rs.1,20,085 lakhs annually) for the milk they pour to the dairy societies which

indicate the importance of this sector in the rural economy. While India is the

largest milk producing country in the world, Tamil Nadu is one of the frontline

States in milk production and ranks as number one in the country in the coverage

of more than 50% of revenue villages under Co-operative ambit. There are 8012

functional primary milk societies with 22.09 lakhs members.

During 2008-09, average milk procurement by Dairy Co-operatives was

26.30 lakhs litres per day (LLPD). On 12.02.2009, a record milk sale of 11.03

lakhs litres was achieved in the history of Chennai Metro Dairies. The market

shares of Dairy Co-operatives have increased considerably and aavin brand holds

the major market share in Tamil Nadu.

106

3.20 DAIRY DEVELOPMENT DEPARTMENT

The growth of dairying in Tamil Nadu is laudable ever since the Dairy

Development Department was established in 1958 in Tamil Nadu. The

administrative and statutory control of all the dairy cooperatives in the State was

transferred to this department on 01.08.1965. The Commissioner for Milk

Production and Dairy Development is the Head of the Department and also

officiates as the Functional Registrar of Dairy Co-operatives. He also functions as

the Managing Director of the Tamil Nadu Co-operative Milk Producers’

Federation Limited and State Registering authority under Milk and Milk Products

Order, 1992 for the State of Tamil Nadu.

Under the relevant provisions of the Tamil Nadu Co-operative Societies

Act, 1983 and Tamil Nadu Co-operative Societies Rules, 1988, he exercises

statutory functions like registration of new societies, revival of dormant societies,

inspection of societies, settlement of disputes, conduct of election to the boards of

management, constitution of boards, issue of direction to societies in the interest of

public etc., The Commissioner for Milk Production and Dairy Development is

assisted by Deputy Milk Commissioner (Co-operation) and 23 Deputy Registrars

(Dairying) at the regional level for discharging the statutory and administrative

functions.

107

3.21 PRIMARY MILK CO-OPERATIVE SOCIETIES

There are 8012 Milk Producers’ Societies including 1408 Milk Producers

Co-operatives exclusively for women and 61 Primary Milk Consumer Co-

operative societies in Tamil Nadu. During 2008-09, 208 societies were newly

registered, including 48 milk Co-operative societies exclusively managed by

women. Apart from this, 153 dormant societies were also revived.

For the benefit of the members, farmer induction programmes are

conducted on modern animal husbandry practices for upgrading milch animals and

their productivity. Since members of the milk producers’ Co-operative societies are

stakeholders, when the society earns profit, the member producers are paid

dividend on share capital, patronage rebate and bonus for the services rendered by

them to the society .This ploughing back of profit for the benefit of producers is

unique in the dairy co-operative sector and this has created a close bond between

the producers and the co-operative societies.

3.22 DISTRICT CO-OPERATIVE MILK PRODUCERS’ UNION LIMITED

There are 17 District Co-operative Milk Producers' Unions are functioning

covering all the districts of Tamil Nadu with primary milk co-operatives as

affiliated members to the district unions. The District Collectors are the Special

Officers of the Unions. The main functions of these Unions are procurement of

milk from primary societies by ensuring clean milk production, quality based milk

cost payment, supply of input services, animal health coverage, development and

supply of feed and fodder, implementation of State and Central Government

schemes at District level, marketing of liquid milk locally and through metro

dairies and conversion of surplus milk into traditional and value added products.

108

3.23 FUNCTIONS OF MILK PRODUCERS UNIONS

The milk producers unions have the following functionalities:

Establishing chilling centers.

Finding new milk routes for collecting milk produced by the members.

Collecting milk from societies and then processing and packing those in

modern dairy plants.

Determining the procurement and selling price of milk.

Increasing the liquid milk sales by undertaking innovative promotional

activities.

Supplying inputs to the members.

Providing veterinary health services and emergency services to the

members' cattle.

Providing Artificial Insemination services to the members' cattle.

Supplying quality milk to Chennai Metro.

3.24 TAMIL NADU CO-OPERATIVE MILK PRODUCERS’ FEDERATION

The Tamil Nadu Co-operative Milk Producers' Federation Limited, the

Apex body of 17 District Co-operative Milk Producers' Unions, was established on

1st February of 1981. The Federation has 3 dairy plants in Chennai which collect

milk from District Unions, process and pack in sachets and send for sale to

consumers in and around Chennai City. Ambathur product dairy is engaged in the

manufacturing of milk products. Recently, closed circuit T.V monitoring system

has been installed at Ambattur Metro Dairy for effective supervision. Further, 5

numbers of new Road Milk Tankers were purchased at an estimated cost of

Rs.71.60 lakhs by Tamil Nadu Cooperative Milk Producers’ Federation Limited to

maintain cold chain of transportation of milk.

109

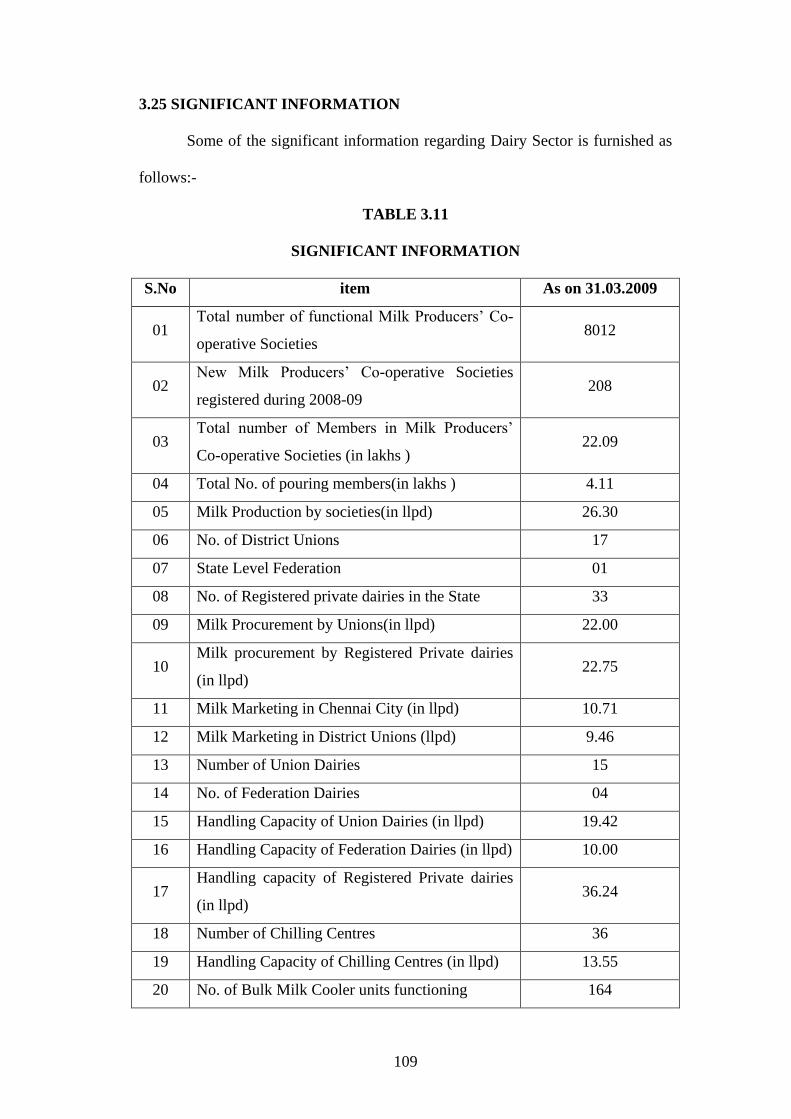

3.25 SIGNIFICANT INFORMATION

Some of the significant information regarding Dairy Sector is furnished as

follows:-

TABLE 3.11

SIGNIFICANT INFORMATION

S.No item As on 31.03.2009

01 Total number of functional Milk Producers’ Co-

operative Societies 8012

02 New Milk Producers’ Co-operative Societies

registered during 2008-09 208

03 Total number of Members in Milk Producers’

Co-operative Societies (in lakhs ) 22.09

04 Total No. of pouring members(in lakhs ) 4.11

05 Milk Production by societies(in llpd) 26.30

06 No. of District Unions 17

07 State Level Federation 01

08 No. of Registered private dairies in the State 33

09 Milk Procurement by Unions(in llpd) 22.00

10 Milk procurement by Registered Private dairies

(in llpd) 22.75

11 Milk Marketing in Chennai City (in llpd) 10.71

12 Milk Marketing in District Unions (llpd) 9.46

13 Number of Union Dairies 15

14 No. of Federation Dairies 04

15 Handling Capacity of Union Dairies (in llpd) 19.42

16 Handling Capacity of Federation Dairies (in llpd) 10.00

17 Handling capacity of Registered Private dairies

(in llpd) 36.24

18 Number of Chilling Centres 36

19 Handling Capacity of Chilling Centres (in llpd) 13.55

20 No. of Bulk Milk Cooler units functioning 164

110

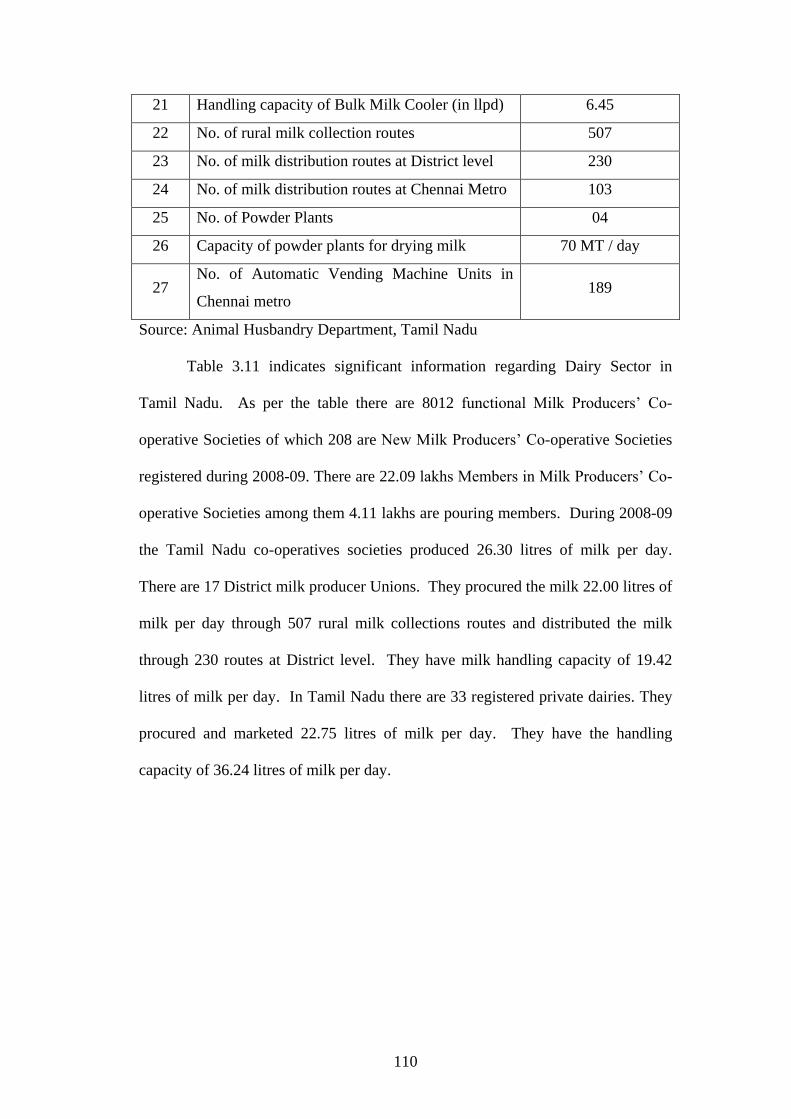

21 Handling capacity of Bulk Milk Cooler (in llpd) 6.45

22 No. of rural milk collection routes 507

23 No. of milk distribution routes at District level 230

24 No. of milk distribution routes at Chennai Metro 103

25 No. of Powder Plants 04

26 Capacity of powder plants for drying milk 70 MT / day

27 No. of Automatic Vending Machine Units in

Chennai metro 189

Source: Animal Husbandry Department, Tamil Nadu

Table 3.11 indicates significant information regarding Dairy Sector in

Tamil Nadu. As per the table there are 8012 functional Milk Producers’ Co-

operative Societies of which 208 are New Milk Producers’ Co-operative Societies

registered during 2008-09. There are 22.09 lakhs Members in Milk Producers’ Co-

operative Societies among them 4.11 lakhs are pouring members. During 2008-09

the Tamil Nadu co-operatives societies produced 26.30 litres of milk per day.

There are 17 District milk producer Unions. They procured the milk 22.00 litres of

milk per day through 507 rural milk collections routes and distributed the milk

through 230 routes at District level. They have milk handling capacity of 19.42

litres of milk per day. In Tamil Nadu there are 33 registered private dairies. They

procured and marketed 22.75 litres of milk per day. They have the handling

capacity of 36.24 litres of milk per day.

111

3.26 PERFORMANCE OF TAMIL NADU MILK COOPERATIVES

Tamil Nadu, with a daily milk production of 145.88 lakh litres,

is one of the leading states in milk production in India and the Tamil Nadu milk

cooperatives play a major role in the development of dairy within the state. The

milk cooperatives of Tamil Nadu, with the help from the government and National

Dairy Development Board (NDDB), have played substantial roles in taking the

state to the current position. Besides, NDDB also undertakes methodical approach

and appropriate strategy for the upliftment of Tamil Nadu milk cooperatives.

3.26.1 The Model

The dairy development programmes in Tamil Nadu have been implemented

through a wide network of co-operatives, which follow the ‘Anand Model’ of the

state of Gujarat. The model follows three-tier structure where primary milk

producers' co-operative societies remain at the base level. In the district level, there

is a union of producers' co-operative societies, whereas, Federation of District Co-

operative Milk Producers' Union remains at the top (state) level of the structure.

In Tamil Nadu, Milk Producers' Cooperative Societies function at the village level,

where milk producers get enrolled as members. The members get animal health

cover for their animals; breed improvement is also carried out. District unions

collect the milk produced at the village societies.

3.26.2 List of Tamil Nadu Milk Co-operatives

There are 17 district co-operative milk producer's unions in Tamil Nadu.

These milk co-operatives cover 32 districts across the state. There are also 15

diaries with a processing capacity of 19.42 LPD and 36 chilling centers with

chilling capacities of 13.55 LPD. The milk procurement by district Co-operative

milk producers’ unions in Tamil Nadu is presented in table 3.12

112

TABLE 3.12

MILK PROCUREMENT BY DISTRICT CO-OPERATIVE MILK

PRODUCERS’ UNIONS

(As on 31.03.2009)

S.No Name of the Union 2007-08 2008-09 Change (%)

(In thousand litres per day)

01 Kancheepuram-Tiruvallur 48 43 -10.42

02 Villupuram 165 164 -0.61

03 Vellore 276 291 -05.43

04 Dharmapuri 139 143 02.88

05 Salem 407 436 07.13

06 Erode 193 203 05.18

07 Coimbatore 208 203 -02.40

08 The Nilgiris 22 21 -04.55

09 Madurai 227 222 -02.20

10 Dindigul 40 42 05.00

11 Tiruchirapalli 286 279 -02.45

12 Thanjavur 34 30 -11.76

13 Pudukottai 11 13 18.18

14 Sivagangai 30 30 -

15 Virudhunagar 11 09 18.18

16 Tirunelveli 61 64 04.92

17 Kanyakumari 06 07 16.67

Total 2164 2200 01.66

Source: Animal Husbandry Department, Tamil Nadu

Table 3.12 shows the Milk procurement by District Co-operative Milk

Producers’ Unions as on 31.03.2009. The district co-operative milk producers’

unions in Tamil Nadu have procured 2200 thousand litres of milk per day during

the year 2009, which is 1.66 per cent higher than that of the previous year 2008.

113

Among the 17 district co-operative milk producers’ union, eight unions

namely Kancheepuram-Tiruvallur, Villupuram, Vellore, Coimbatore, The Nilgiris,

Madurai, Tiruchirapalli, and Thanjavur have negative growth for procurement of

milk per day during 2009 as compared to 2008.

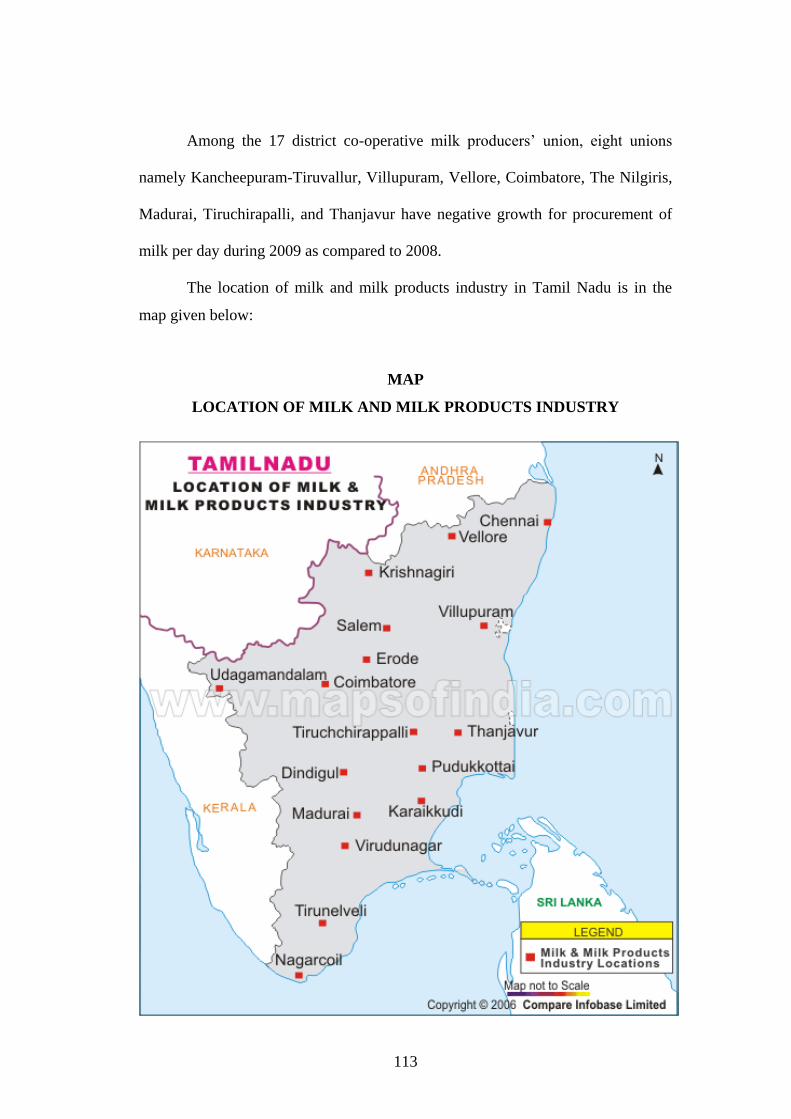

The location of milk and milk products industry in Tamil Nadu is in the

map given below:

MAP

LOCATION OF MILK AND MILK PRODUCTS INDUSTRY

114

3.27 PROFILE OF THE MADURAI DISTRICT CO-OPERATIVE MILK

PRODUCERS' UNION LTD

The Madurai District Co-operative Milk Producers’ Union Ltd, is popularly

known as Madurai Aavin. This is one of the largest dairies in the southern part of

Tamilnadu. Madurai Aavin was started in the year 1967 as Madurai Milk Project.

The project and the dairy machinery were funded by the UNICEF under New

Zealand free from Hunger Campaign Committee.

From 01.01.1974 Madurai Aavin brought under the control of Tamilnadu

Dairy Development Corporation Ltd, Chennai. From 1982 onwards Madurai

Aavin was converted in to and functioning as a District Co-operative Unit. The

members of this Co-operative unit are the Milk Producers’ Coop society at the

village level in both Madurai and Theni Districts.

Madurai Aavin is a Co-operative organization statutorily controlled by the

Commissioner for Milk Production and Dairy Development, Government of

Tamilnnadu. The apex body for this unit is the Tamilnadu Co-operative Milk

Producers’ Federation Ltd, Chennai.

3.27.1 LOCATION

The Madurai Aavin is located in an area of 39.42 acres of land at the

junction of the K. K. Nagar and Annanagar in the Madurai-Sivagangai Highways,

nearer to the Office of the Madurai District Collector.

115

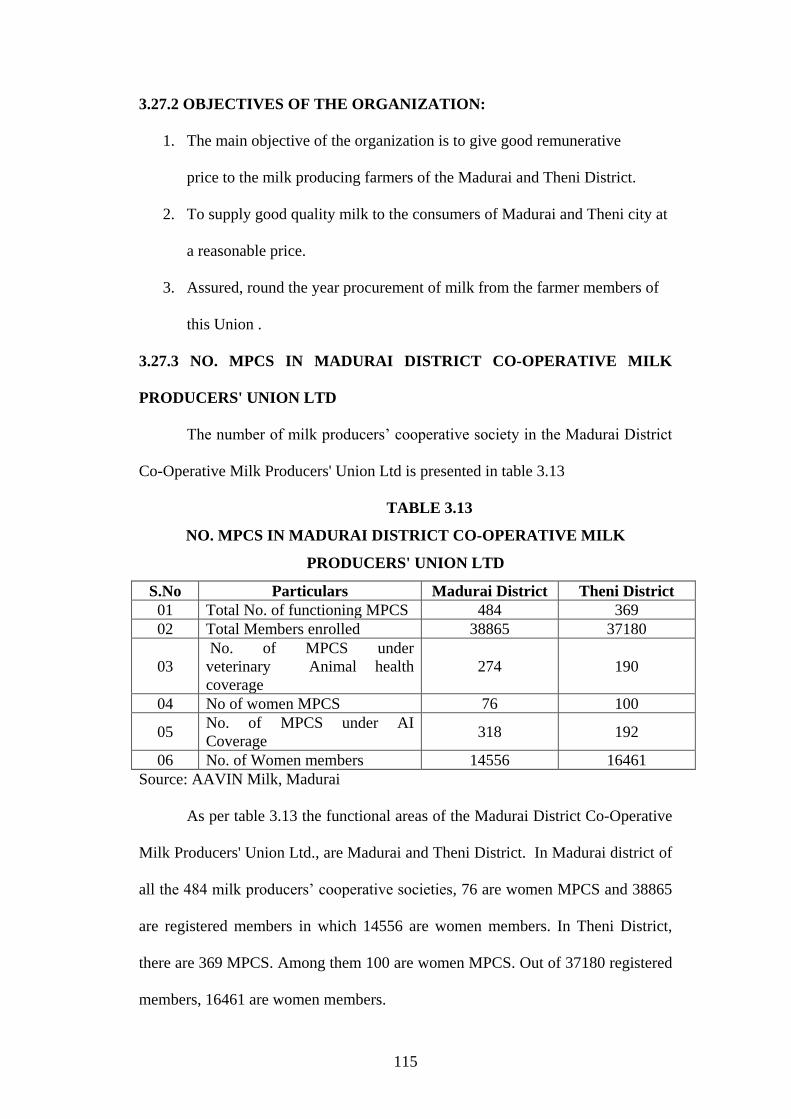

3.27.2 OBJECTIVES OF THE ORGANIZATION:

1. The main objective of the organization is to give good remunerative

price to the milk producing farmers of the Madurai and Theni District.

2. To supply good quality milk to the consumers of Madurai and Theni city at

a reasonable price.