chapter 4 valuing bonds chapter 4 topic overview u bond characteristics u annual and semi-annual...

TRANSCRIPT

Chapter 4

Valuing Bonds

Chapter 4 Topic Overview

Bond Characteristics Annual and Semi-Annual Bond

Valuation Reading Bond Quotes Finding Returns on Bonds Bond Risk and Other Important Bond

Valuation Relationships

Bond Characteristics

Par (or Face) Value (F) = stated face value that is the amount the issuer must repay, usually $1,000

Coupon Interest Rate Coupon (C) = Coupon Rate x Face Value Maturity Date = when the face value is repaid. A legal contract called the bond indenture

specifies these values. This makes a bond’s cash flows look like this:

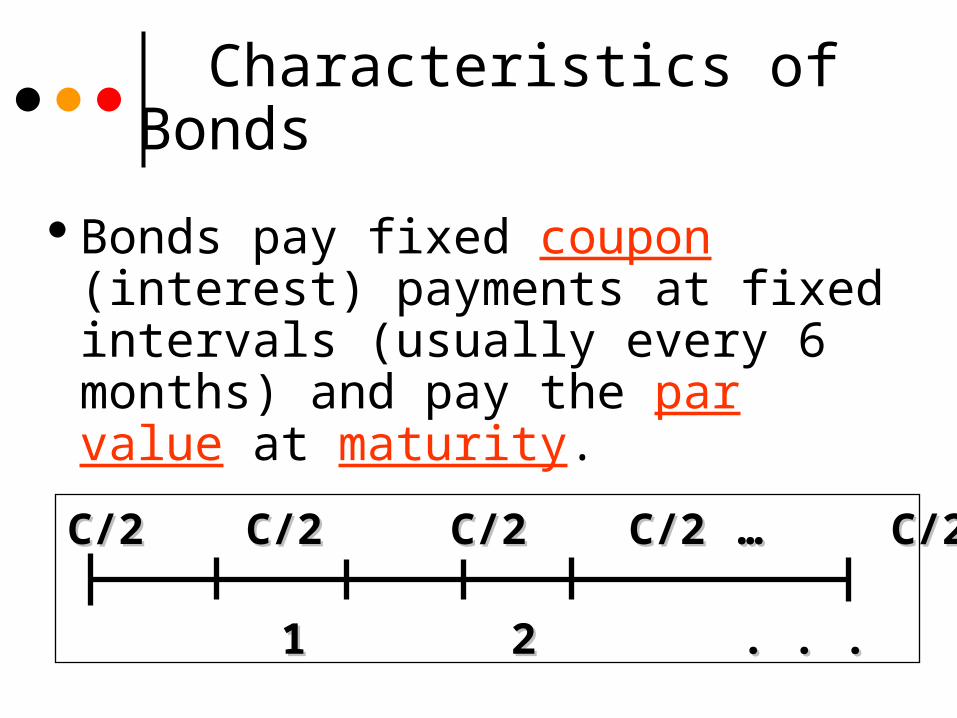

Characteristics of Bonds

Bonds pay fixed coupon (interest) payments at fixed intervals (usually every 6 months) and pay the par value at maturity.

00 1 1 2 . . .2 . . . nn

C/2 C/2 C/2 C/2C/2 C/2 C/2 C/2 … C/2+F… C/2+F

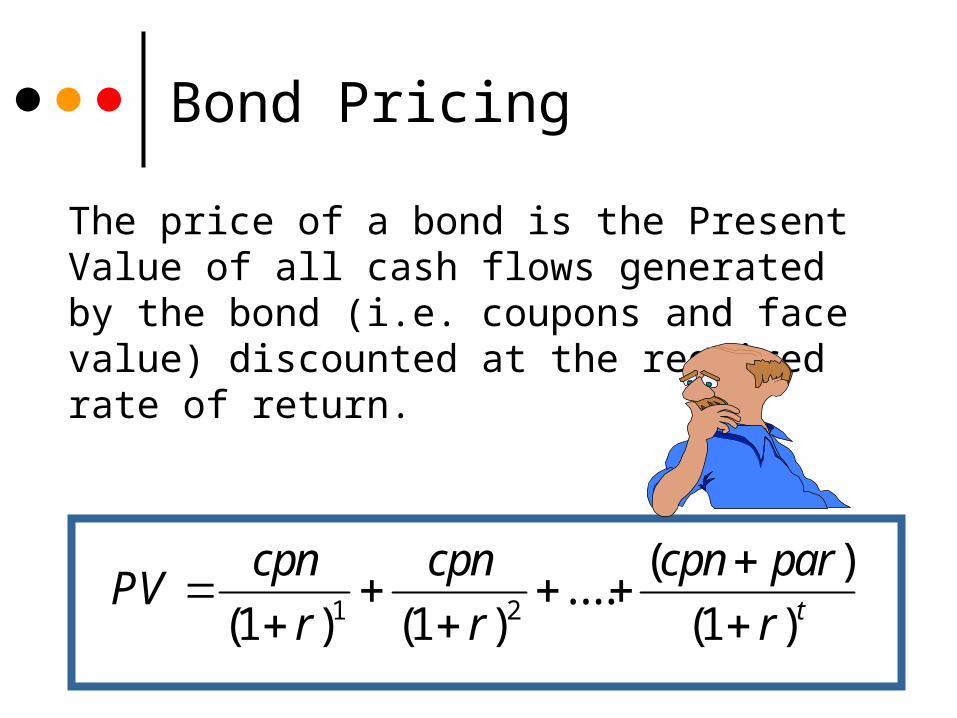

Bond Pricing

The price of a bond is the Present Value of all cash flows generated by the bond (i.e. coupons and face value) discounted at the required rate of return.

PVcpn

r

cpn

r

cpn par

r t

( ) ( )

....( )

( )1 1 11 2

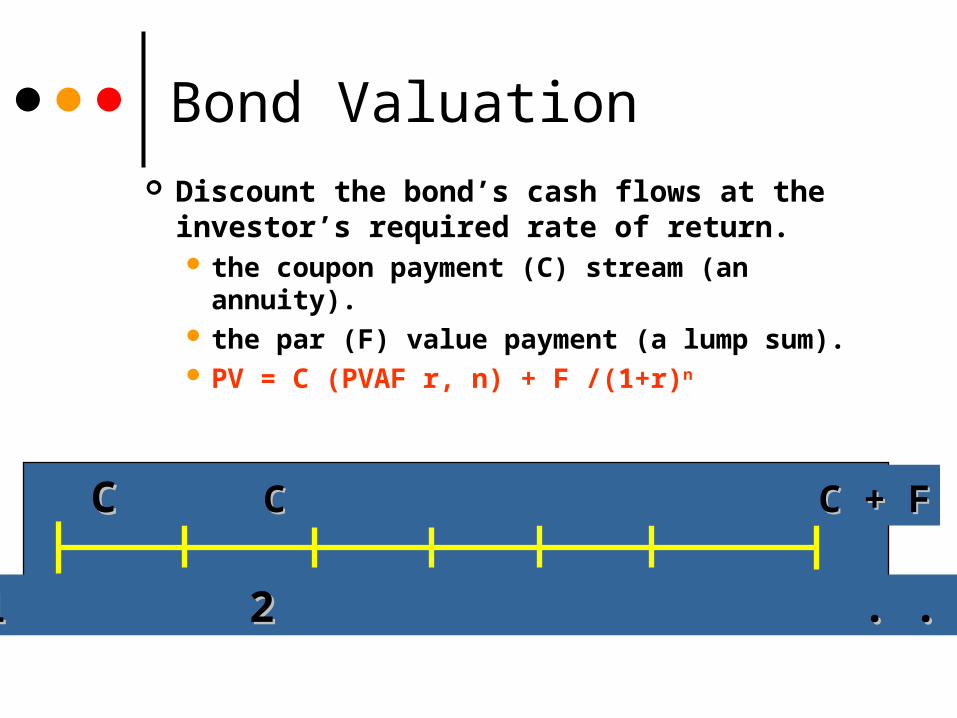

Bond Valuation Discount the bond’s cash flows at the

investor’s required rate of return. the coupon payment (C) stream (an annuity). the par (F) value payment (a lump sum). PV = C (PVAF r, n) + F /(1+r)n

00 1 1 2 . . . 2 . . . nn

C C CC C + FC + F

Bond Valuation Example #1

Duff’s Beer has $1,000 par value bonds outstanding that make annual coupon payments. These bonds have a 7.5% annual coupon rate and 15 years left to maturity. Bonds with similar risk have a required return of 9%, and Moe Szyslak thinks this required return is reasonable.

What’s the most that Moe is willing to pay for a Duff’s Beer bond?

0 1 2 3 . . . 15

1000 ? 75 75 75 . . . 75

r = 9%

Let’s Play with Example #1

Homer Simpson is interested in buying a Duff Beer bond but demands an 7.5 percent required return.

What is the most Homer would pay for this bond?

0 1 2 3 . . . 15

1000 ? 75 75 75 . . . 75

r = 7.5%

Let’s Play with Example #1 some more.

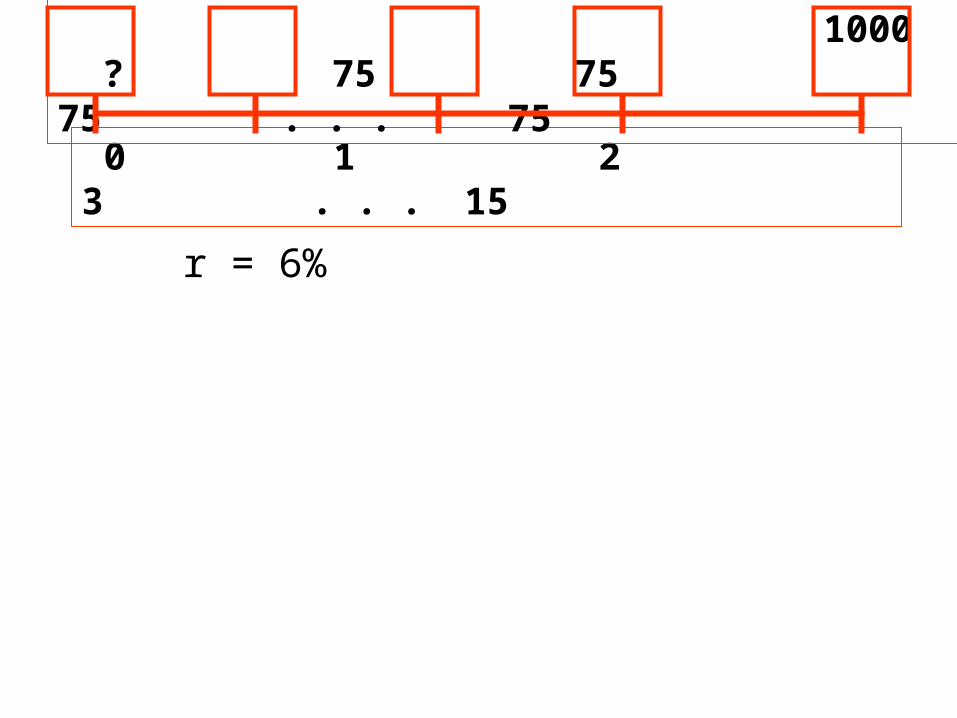

Barney (belch!) Gumble is interested in buying a Duff Beer bond and demands on a 6 percent required return.

What is the most Barney (belch!) would pay for this bond?

0 1 2 3 . . . 15

1000 ? 75 75 75 . . . 75

r = 6%

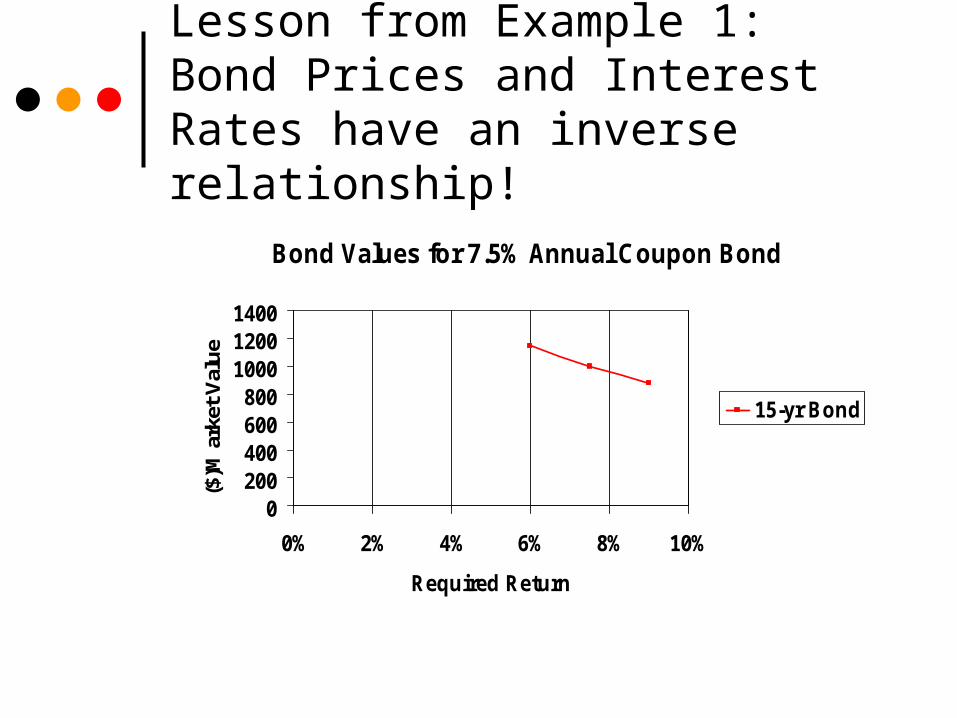

Lesson from Example 1: Bond Prices and Interest Rates have an inverse relationship!

Bond Values for 7.5% Annual Coupon Bond

0200400600800

100012001400

0% 2% 4% 6% 8% 10%

Required Return

($)M

ark

et V

alu

e

15-yr Bond

Another Example 1 Lesson: Bond Premiums and Discounts

What happens to bond values if required return is not equal to the coupon rate?

The bond's price will differ from its par value

P0 < par valuer > Coupon Interest Rate DISCOUNT =

P0 > par valuer < Coupon Interest Rate PREMIUM =

P0 = par valuer = Coupon Interest Rate PAR =

Bonds with Semiannual Coupons

Double the number of years, and divide required return and annual coupon by 2.

PP00 = = CC/2/2(PVFA(PVFAr/2,2nr/2,2n) + F ) + F /(1+r/2)2n

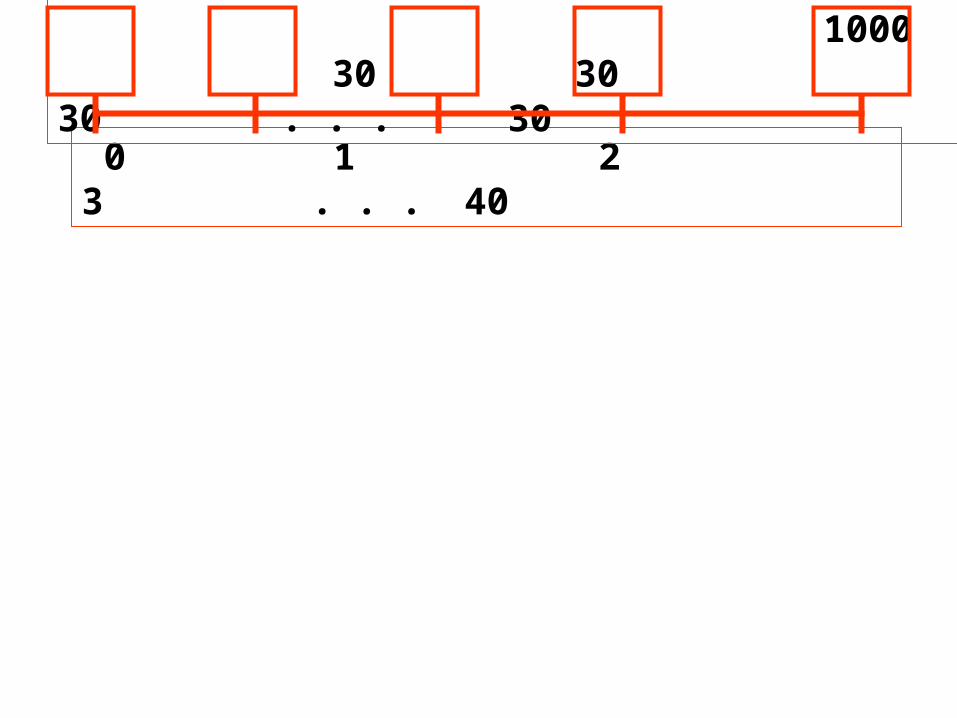

Semiannual Example

Kwickee-Mart has an $1000 par value bond with an annual coupon rate of 6% that pays coupons semiannually with 20 years left to maturity. What is the most you would be willing to pay for this bond if your required return is 7% APR?

Semiannual coupon = 6%/2($1000) = $30Semiannual coupon = 6%/2($1000) = $30 20x2 = 40 remaining coupons20x2 = 40 remaining coupons

0 1 2 3 . . . 40

1000 30 30 30 . . . 30

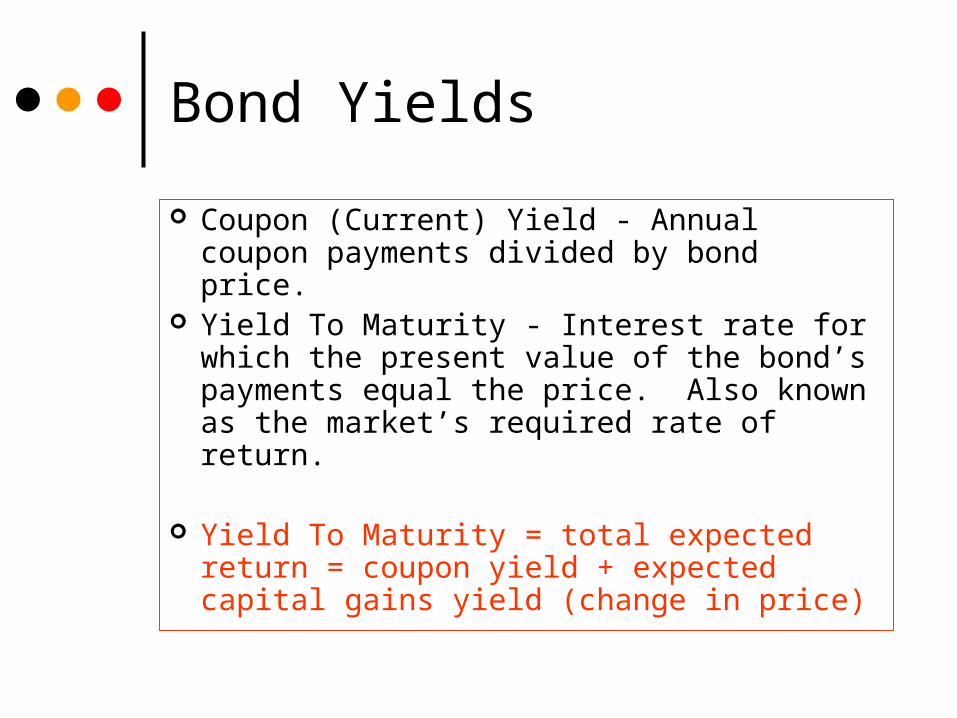

Bond Yields

Coupon (Current) Yield - Annual coupon payments divided by bond price.

Yield To Maturity - Interest rate for which the present value of the bond’s payments equal the price. Also known as the market’s required rate of return.

Yield To Maturity = total expected return = coupon yield + expected capital gains yield (change in price)

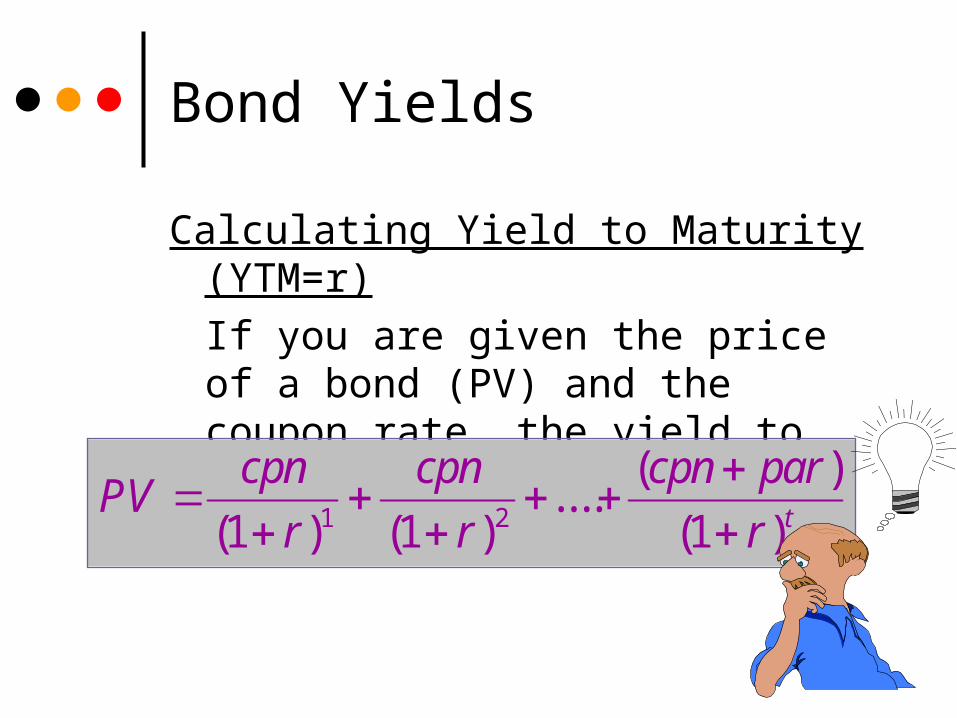

Bond Yields

Calculating Yield to Maturity (YTM=r)

If you are given the price of a bond (PV) and the coupon rate, the yield to maturity can be found by solving for r.

PVcpn

r

cpn

r

cpn par

r t

( ) ( )

....( )

( )1 1 11 2

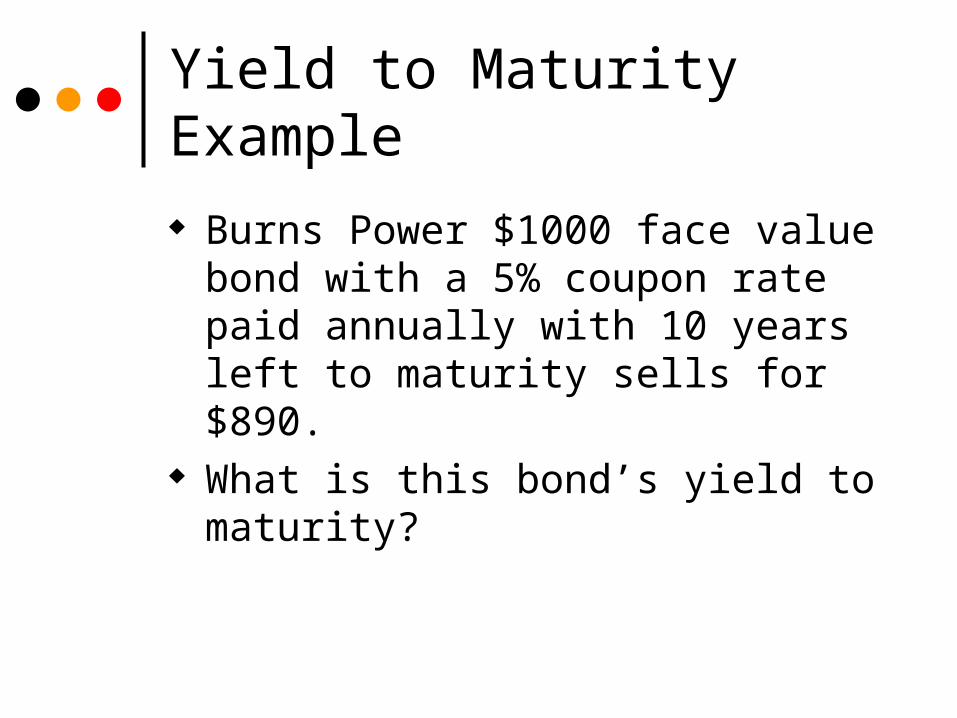

Yield to Maturity Example

Burns Power $1000 face value bond with a 5% coupon rate paid annually with 10 years left to maturity sells for $890.

What is this bond’s yield to maturity?

0 1 2 3 . . . 10

1000-890 50 50 50 . . . 50

What is bond’s YTM?

What is the bond’s current yield?

U.S. Treasury Bond QuotationsRATE

MATURITY

MO/YRBID ASKED CHG

ASK

YLD

Government Bonds & Notes8.875 Feb 19 139:27 139:28 3 4.73

Rate Coupon rate of 8.875%

Bid pricesAsk prices

(percentage of par value)

Bid price: the price traders receive if they sell a bond to the dealer.

Quoted in increments of 32nds of a dollar

Ask price: the price traders pay to the dealer to buy a bond

Bid-ask spread: difference between ask and bid prices.

Ask Yield Yield to maturity on the ask price

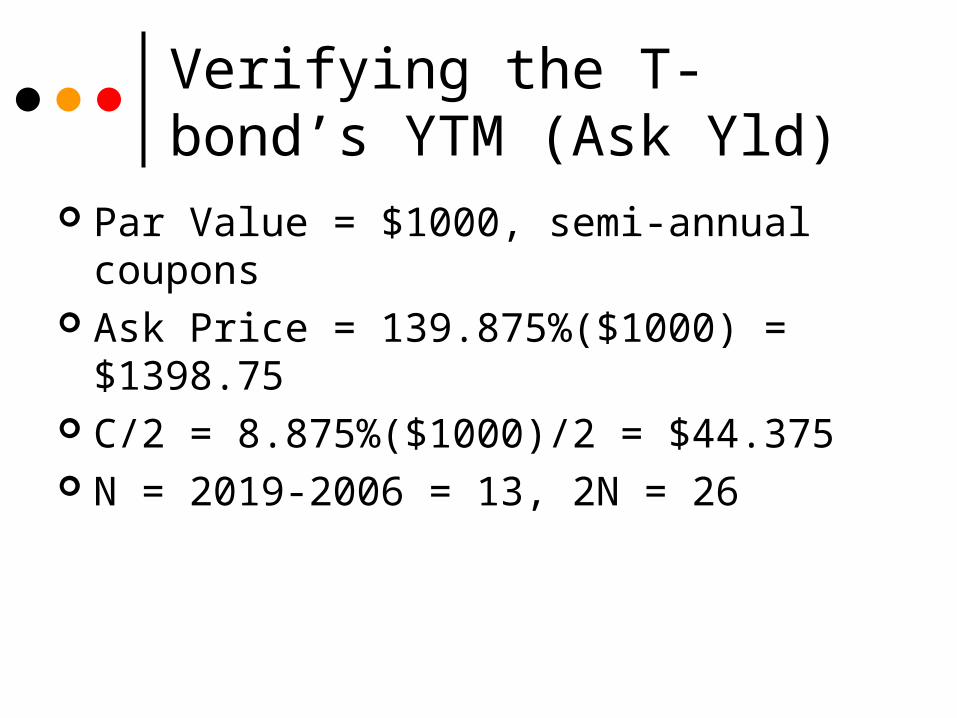

Verifying the T-bond’s YTM (Ask Yld)

Par Value = $1000, semi-annual coupons Ask Price = 139.875%($1000) = $1398.75 C/2 = 8.875%($1000)/2 = $44.375 N = 2019-2006 = 13, 2N = 26

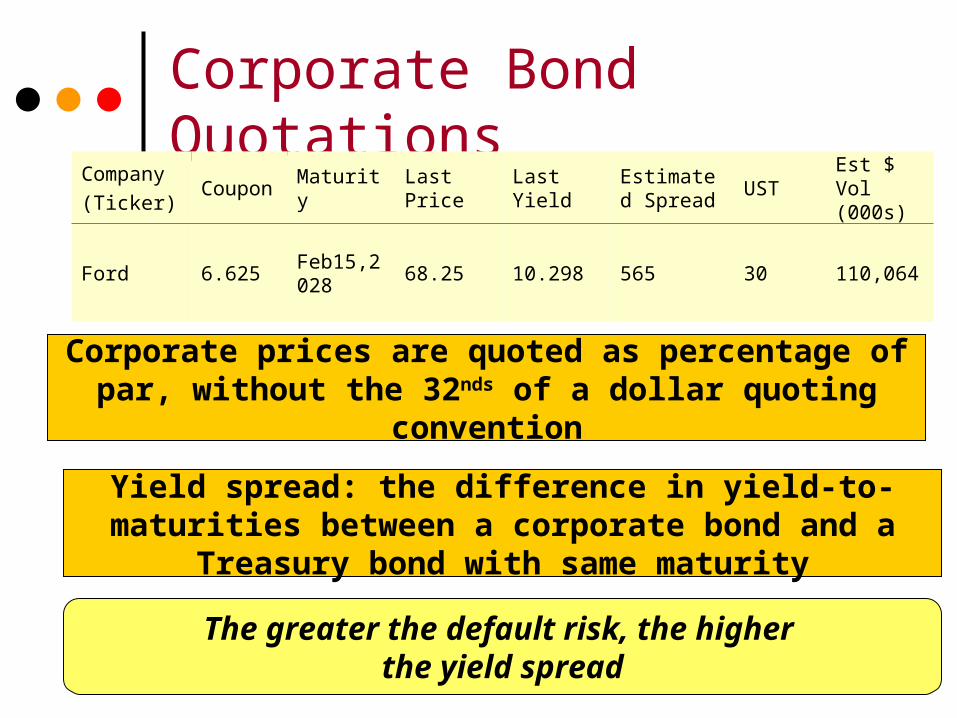

Corporate Bond QuotationsCompany

(Ticker)Coupon Maturity

Last Price

Last YieldEstimated Spread

USTEst $ Vol (000s)

Ford 6.625Feb15,2028

68.25 10.298 565 30 110,064

Corporate prices are quoted as percentage of par, without the 32nds of a dollar quoting

convention

Yield spread: the difference in yield-to-maturities between a corporate bond and a

Treasury bond with same maturity

The greater the default risk, the higher the yield spread

Causes of Bond Price Changes

Since a bond’s cash flows are fixed:

1. Changes in interest rates, and

2. Passage of time.

cause changes in a bond’s price.

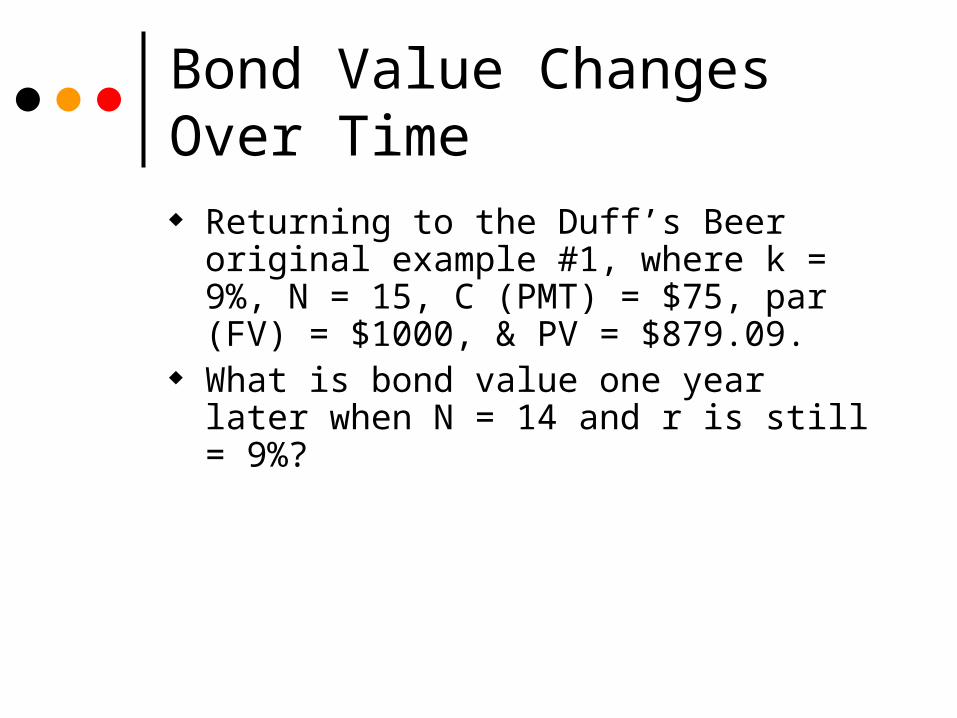

Bond Value Changes Over Time Returning to the Duff’s Beer original

example #1, where k = 9%, N = 15, C (PMT) = $75, par (FV) = $1000, & PV = $879.09.

What is bond value one year later when N = 14 and r is still = 9%?

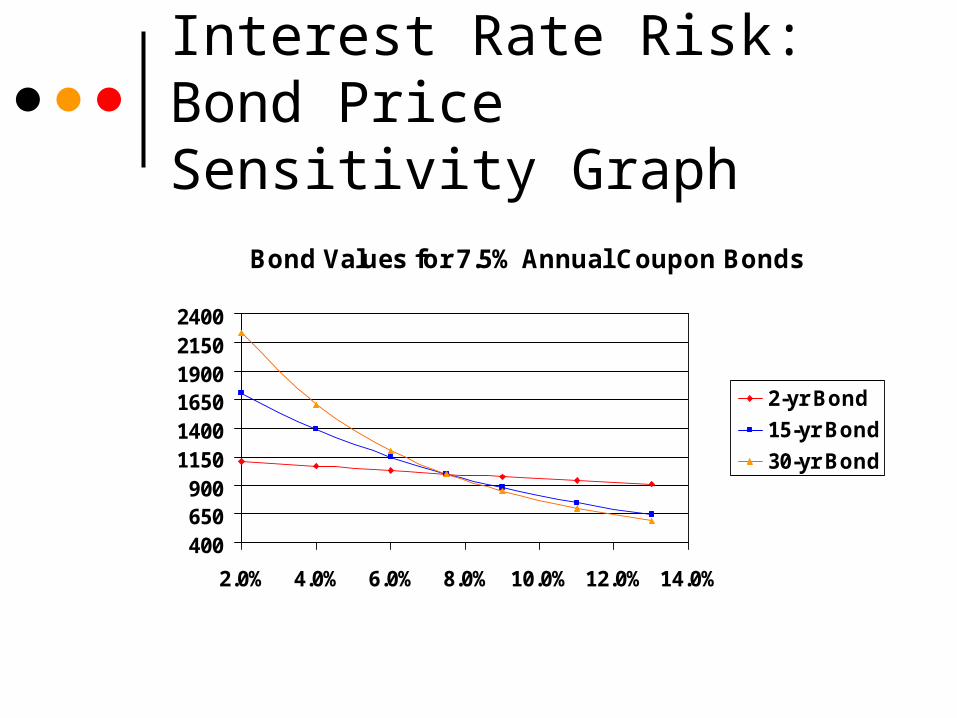

Interest Rate Risk

Measures Bond Price Sensitivity to changes in interest rates.

In general, long-term bonds have more interest rate risk than short-term bonds.

Also, for bonds with same time to maturity, lower coupon bonds have more interest rate risk than higher coupon bonds.

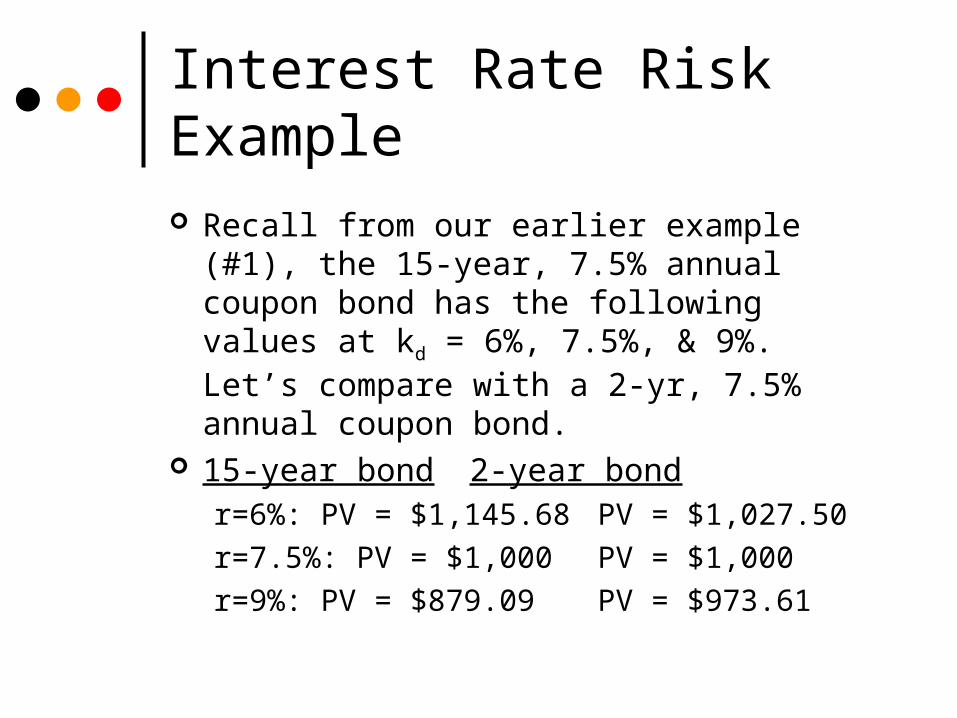

Interest Rate Risk Example

Recall from our earlier example (#1), the 15-year, 7.5% annual coupon bond has the following values at kd = 6%, 7.5%, & 9%. Let’s compare with a 2-yr, 7.5% annual coupon bond.

15-year bond 2-year bondr=6%: PV = $1,145.68 PV = $1,027.50

r=7.5%: PV = $1,000 PV = $1,000

r=9%: PV = $879.09 PV = $973.61

Interest Rate Risk: Bond Price Sensitivity Graph

Bond Values for 7.5% Annual Coupon Bonds

400650900

115014001650190021502400

2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

2-yr Bond

15-yr Bond

30-yr Bond

Default Risk

Credit risk Default premium Investment grade Speculative grade (Junk bonds)

Default RiskStandard

Moody' s & Poor's Safety

Aaa AAA The strongest rating; ability to repay interest and principalis very strong.

Aa AA Very strong likelihood that interest and principal will berepaid

A A Strong ability to repay, but some vulnerability to changes incircumstances

Baa BBB Adequate capacity to repay; more vulnerability to changesin economic circumstances

Ba BB Considerable uncertainty about ability to repay.B B Likelihood of interest and principal payments over

sustained periods is questionable.Caa CCC Bonds in the Caa/CCC and Ca/CC classes may already beCa CC in default or in danger of imminent defaultC C C-rated bonds offer little prospect for interest or principal

on the debt ever to be repaid.

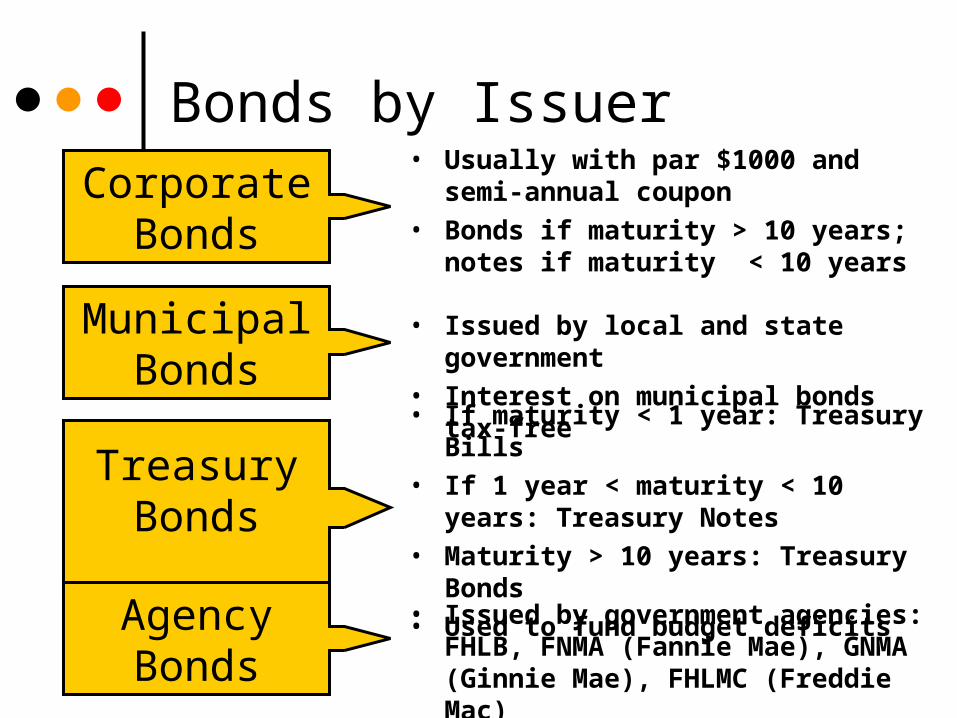

Bonds by IssuerCorporate

Bonds

• Usually with par $1000 and semi-annual coupon

• Bonds if maturity > 10 years; notes if maturity < 10 years

Municipal Bonds

• Issued by local and state government

• Interest on municipal bonds tax-free

Treasury Bonds

• If maturity < 1 year: Treasury Bills

• If 1 year < maturity < 10 years: Treasury Notes

• Maturity > 10 years: Treasury Bonds

• Used to fund budget deficitsAgency Bonds

• Issued by government agencies: FHLB, FNMA (Fannie Mae), GNMA (Ginnie Mae), FHLMC (Freddie Mac)

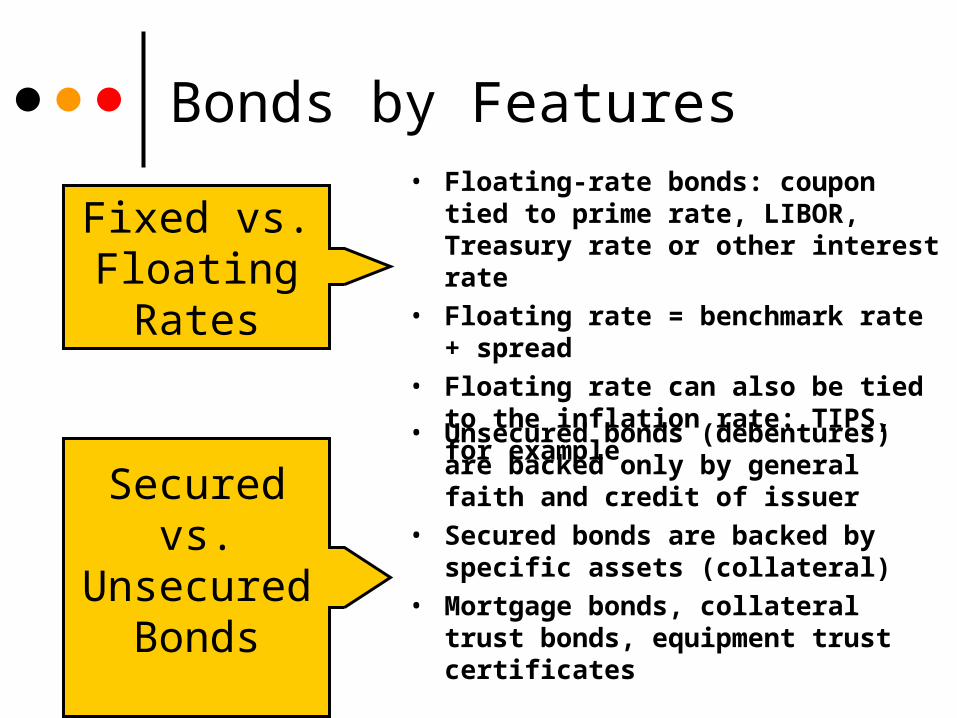

Bonds by Features

Fixed vs. Floating Rates

• Floating-rate bonds: coupon tied to prime rate, LIBOR, Treasury rate or other interest rate

• Floating rate = benchmark rate + spread

• Floating rate can also be tied to the inflation rate: TIPS, for example

Secured vs.

Unsecured Bonds

• Unsecured bonds (debentures) are backed only by general faith and credit of issuer

• Secured bonds are backed by specific assets (collateral)

• Mortgage bonds, collateral trust bonds, equipment trust certificates

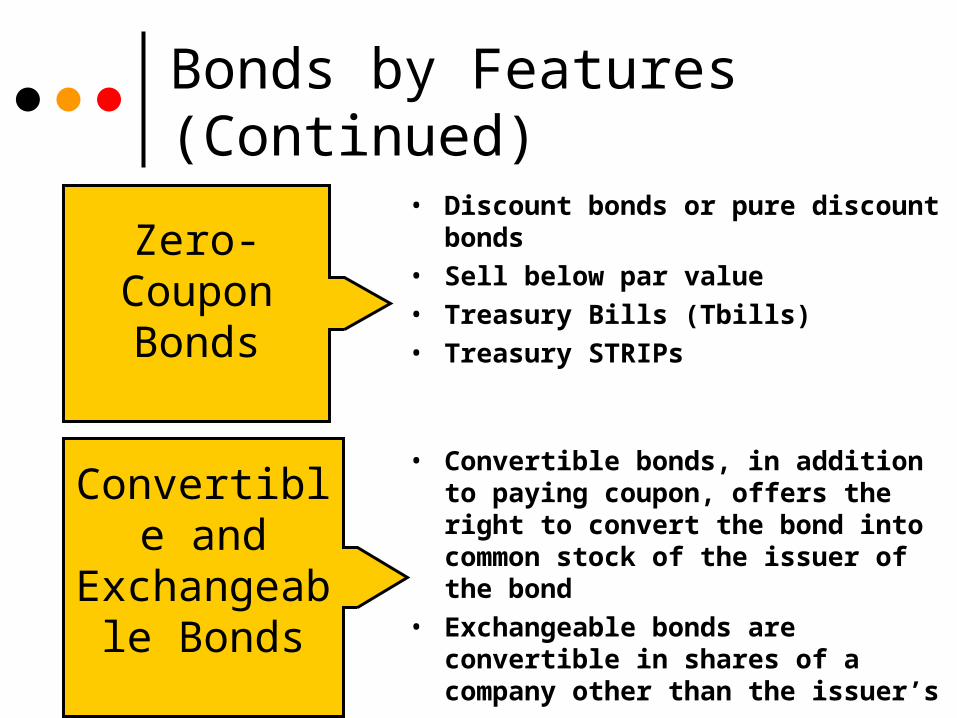

Bonds by Features (Continued)

Zero-Coupon Bonds

• Discount bonds or pure discount bonds

• Sell below par value• Treasury Bills (Tbills) • Treasury STRIPs

Convertible and

Exchangeable Bonds

• Convertible bonds, in addition to paying coupon, offers the right to convert the bond into common stock of the issuer of the bond

• Exchangeable bonds are convertible in shares of a company other than the issuer’s

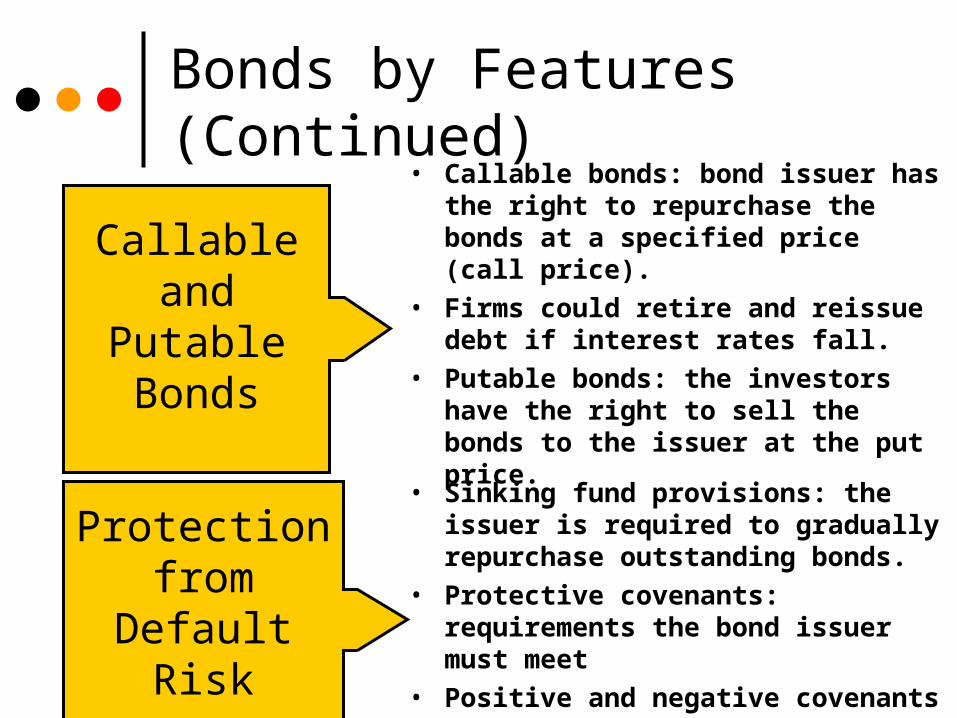

Bonds by Features (Continued)

Callable and

Putable Bonds

• Callable bonds: bond issuer has the right to repurchase the bonds at a specified price (call price).

• Firms could retire and reissue debt if interest rates fall.

• Putable bonds: the investors have the right to sell the bonds to the issuer at the put price.

Protection from

Default Risk

• Sinking fund provisions: the issuer is required to gradually repurchase outstanding bonds.

• Protective covenants: requirements the bond issuer must meet

• Positive and negative covenants