chapter 19 completing the audit / post audit responsibilities spring 2007

Post on 20-Dec-2015

241 views

TRANSCRIPT

Chapter 19Completing The Audit /

Post Audit Responsibilities Spring 2007

Completing the Audit Main point: Procedures performed at

the end of the audit are your last chance to detect material misstatements.

There are a series of “standard procedures” to catch problems.

Mentally need to step back and “look at the forest”.

Auditor Responsibilities in Completing the Audit Complete fieldwork Evaluate findings Evaluate Going Concern Communications with clients

Completing Fieldwork Making subsequent events review. Reading minutes of meetings. Obtaining evidence concerning

litigation, claims and assessments. Obtaining a client representation

letter. Performing analytical procedures.

Subsequent Event’s Time Frame

Year EndEnd of

Field work Issue Report

Subsequent Events

Subsequent Events Period

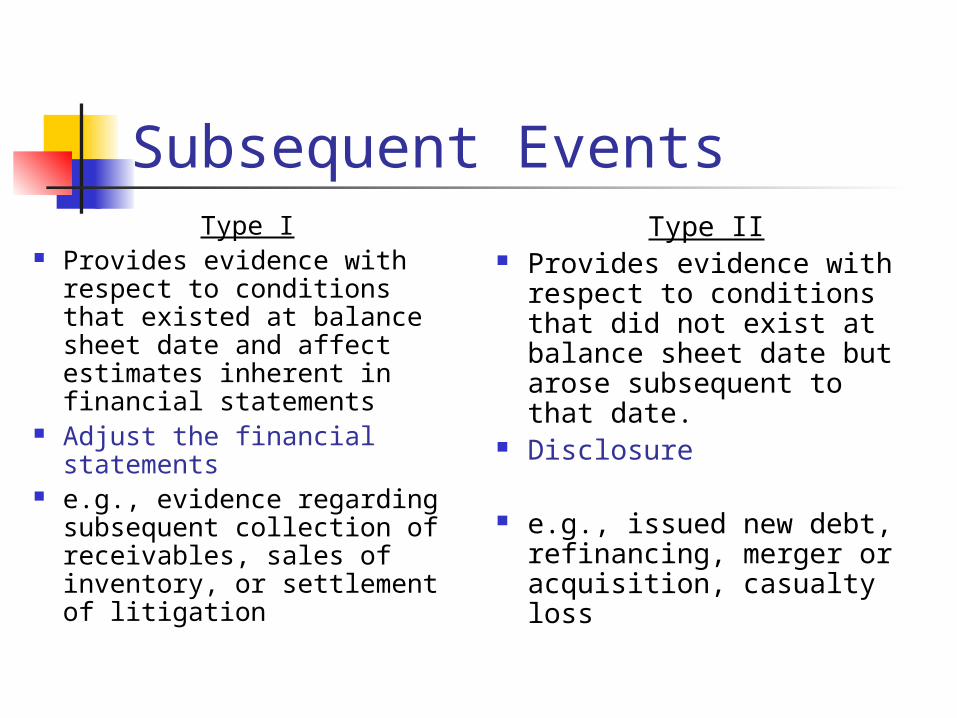

Subsequent EventsType I

Provides evidence with respect to conditions that existed at balance sheet date and affect estimates inherent in financial statements

Adjust the financial statements

e.g., evidence regarding subsequent collection of receivables, sales of inventory, or settlement of litigation

Type II Provides evidence with

respect to conditions that did not exist at balance sheet date but arose subsequent to that date.

Disclosure

e.g., issued new debt, refinancing, merger or acquisition, casualty loss

Subsequent Event’s Time Frame

Year EndEnd of

Field work Issue Report

Subsequent Events

Subsequent Events Period

Dual Date Report

Dual Dating Report Material Subsequent Event (usually

type II event ) which happens after the close of field work but prior to printing and issuing the report.

Audit Procedures for Subsequent Events Read interim financial statements

after year-end. Inquiry of management (Explain

what you are looking for) Read minutes of board of directors

meetings. Inquiry of client’s legal council. Representation letter from client.

Reading Minutes of Meetings Read all minutes of meetings

throughout the year as well as through the report release date

Look for significant items that have not been properly addressed

May indicate a significant subsequent event

Attorney’s Letters andRepresentation Letters

Primary concern is evidence regarding FASB No. 5 regarding Accounting for Contingencies on litigation, claims, assessments Management representations Direct communication with expert: Attorney

Possible Action Record a liability Disclose a contingency Nothing

Attorney’s Letters Attorney Letter

Client waives attorney - client privilege in the context of the audit.

Identify existence of litigation Need assessment of probability of material loss in

the context of FASB No. 5 The client’s lawyer is an expert with respect to:

Existence of a condition indicating an uncertainty as to possible loss from litigation, claims, and assessments.

Period of underlying cause for legal action. The degree of probability of unfavorable outcome. The amount or range of potential loss.

Representation Letter

If client representation is not competent evidence, what is the value of the representation letter?» Mgmt. acknowledges their primary

responsibility for the financial statements» Availability of ALL financial records» Completeness of minutes» Representation regarding irregularities

involving management or employees» Address all material accounting estimates!!

Representation Letter Two Key Representations

The client takes responsibility for the financial statements as their own.

The client indicates that no evidence has been withheld from the auditor.

Everything Else is Icing on the Cake Have management address every accounting

estimate. Discuss any issue of audit interest

REMEMBER! REP LETTER DOES NOT SUBSTITUTE FOR CORROBORATING EVIDENCE!

Analytical Procedures

Year-End Analytical Procedures (required) Compare this year to last year Trend analysis Comparison to budgets Comparison to underlying business activity ** Put it all together and determine if it makes

sense**

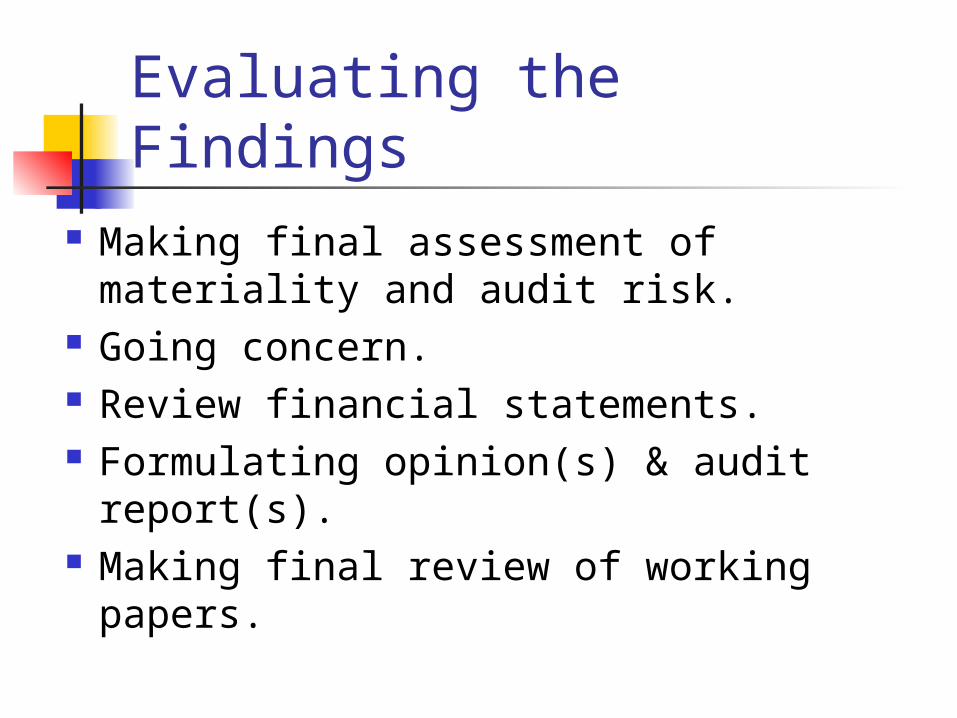

Evaluating the Findings Making final assessment of materiality

and audit risk. Going concern. Review financial statements. Formulating opinion(s) & audit

report(s). Making final review of working papers.

Final assessment of Materiality Determine whether known & projected

errors will influence a financial statement user’s decision (as called Summary of Unadjusted Differences in class).

See Figure 19-3 p. 906.

Consider implications of prior year’s “passed adjustments.”

Proposed Adjusting Journal Entries

Implications for • Balance Sheet• Pretax Income => Income Tax Expense• Statement of Cash Flows• Statement of Owner’s Equity• Any potential disclosures

Implications of Prior Year’s Passed Adjustments (corrected during this year)

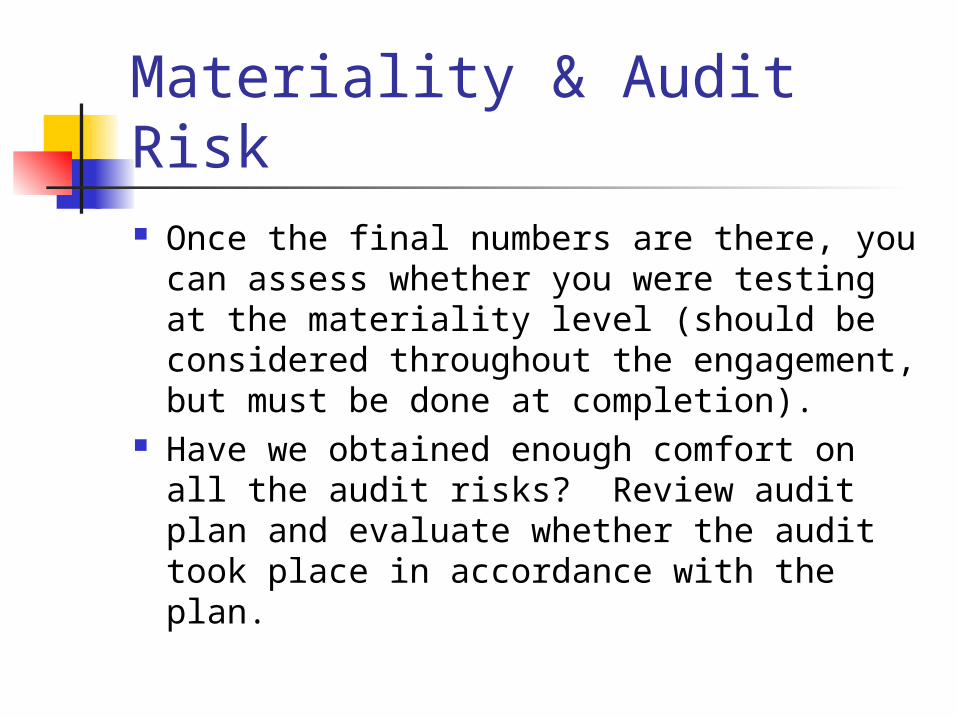

Materiality & Audit Risk Once the final numbers are there, you

can assess whether you were testing at the materiality level (should be considered throughout the engagement, but must be done at completion).

Have we obtained enough comfort on all the audit risks? Review audit plan and evaluate whether the audit took place in accordance with the plan.

Assess Going Concern The auditor has a responsibility to evaluate

whether there is substantial doubt about the entity’s ability to continue as a going concern for a reasonable period of time, not to exceed one year beyond the date of the financial statements being audited (AU 341)

The results of auditing procedures designed and performed to achieve other audit objectives should be sufficient for this purpose.

Going Concern Considerations

The auditor must evaluate if: Negative trends (e.g., operating losses, negative

cash flow from operations) Other indications of possible financial difficulties

(e.g., denial of trade credit by suppliers, restructuring of debt)

Internal matters (e.g., work stoppages, uneconomic long-term commitments)

External matters (e.g., loss of license, patent, loss of principal customer/supplier)

Going Concern: Evaluate Management Plans

If, after consider the identified conditions and events in the aggregate, the auditor believes there is substantial doubt about the ability of the entity to continue as a going concern for a reasonable period of time, he should consider management’s plans for dealing with the adverse effects of the conditions and events. Plans to dispose of assets Plans to borrow money or restructure debt Plans to reduce or delay expenditures Plans to increase ownership equity

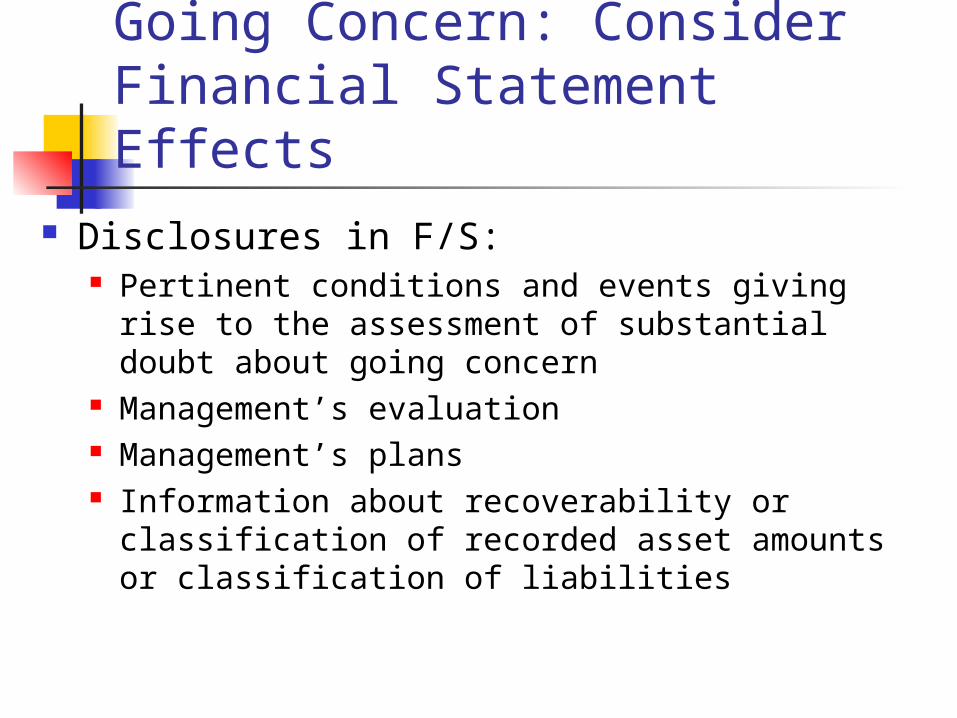

Going Concern: Consider Financial Statement Effects

Disclosures in F/S: Pertinent conditions and events giving rise to the

assessment of substantial doubt about going concern

Management’s evaluation Management’s plans Information about recoverability or classification

of recorded asset amounts or classification of liabilities

Going Concern: Impact on Audit Reports

Evaluate adequacy of disclosure in the financial statements.

Possible “except for” qualified opinion regarding inadequate disclosures

Possible explanatory paragraph regarding uncertainties.

If the auditor reaches a conclusion about substantial doubt, that is mitigated by management plans, disclosure is still necessary. The auditor may conclude that reference to going concern in the audit report is unnecessary.

Report of Independent Registered Public Accounting Firm – TRM Corp

We have completed an integrated audit of TRM Corporation’s 2005 consolidated financial statements and of its internal control over financial reporting as of December 31, 2005 and audits of its 2004 and 2003 consolidated financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Our opinions, based on our audits, are presented below.

Consolidated financial statements and financial statement schedule

In our opinion, the consolidated financial statements listed in the index appearing under Item 15(a)(1) present fairly, in all material respects, the financial position of TRM Corporation and its subsidiaries at December 31, 2005 and 2004, and the results of their operations and their cash flows for each of the three years in the period ended December 31, 2005 in conformity with accounting principles generally accepted in the United States of America. In addition, in our opinion, the accompanying financial statement schedule listed in the index appearing under Item 15(a)(2) presents fairly, in all material respects, the information set forth therein when read in conjunction with the related consolidated financial statements. These financial statements and financial statement schedule are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements and financial statement schedule based on our audits. We conducted our audits of these statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit of financial statements includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

Report of Independent Registered Public Accounting Firm – TRM Corp

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, the Company incurred a net loss for 2005 resulting in its failure to meet certain financial covenants of its financing agreement with Bank of America, N.A. and other lenders. The Company does not expect to meet the required financial covenants during 2006, which may render the debt callable by the bank. This raises substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Internal control over financial reporting

Also, we have audited management’s assessment, included in Management’s Report on Internal Control Over Financial Reporting appearing under Item 9A, that the Company did not maintain effective internal control over financial reporting as of December 31, 2005, because the Company did not maintain effective controls over the a) valuation of its accounts receivable including the related allowance for doubtful accounts, b) completeness and accuracy of certain of its equipment, including the related depreciation expense, and c) completeness and accuracy of its accrued liabilities and related expense accounts, including cost of goods sold, based on criteria established in Internal Control — Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The Company’s management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting. Our responsibility is to express opinions on management’s assessment and on the effectiveness of the Company’s internal control over financial reporting based on our audit.

We conducted our audit of internal control over financial reporting in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. An audit of internal control over financial reporting includes obtaining an understanding of internal control over financial reporting, evaluating management’s assessment, testing and evaluating the design and operating effectiveness of internal control, and performing such other procedures as we consider necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinions.

Cont…A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Cont…A material weakness is a control deficiency, or combination of control deficiencies, that results in more than a remote likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected. The following material weaknesses have been identified and included in management’s assessment as of December 31, 2005:

Ineffective controls over accounts receivable . The Company did not maintain effective controls over the valuation of its accounts receivable. Specifically, the Company failed to properly review its aged customers’ accounts receivable in order to value such receivables in accordance with generally accepted accounting principles. This control deficiency resulted in audit adjustments to the Company’s 2005 annual consolidated financial statements. Additionally, this control deficiency could result in a misstatement in the accounts receivable, allowance for doubtful accounts and the related general and administrative expense accounts that would result in a material misstatement to the annual or interim consolidated financial statements that would not be prevented or detected. Accordingly, the Company’s management has determined that this control deficiency constitutes a material weakness.

Ineffective controls over equipment . The Company did not maintain effective controls over the completeness and accuracy of certain of its equipment, including the related depreciation expense. Specifically, a United Kingdom subsidiary failed to ensure the completeness and accuracy of costs used to capitalize security and processing compliance enhancements made to its ATM equipment. This control deficiency resulted in an audit adjustment to the Company’s 2005 consolidated financial statements. Additionally, this control deficiency could result in a misstatement in the equipment, accumulated depreciation, and the related depreciation expense accounts that would result in a material misstatement to the annual or interim consolidated financial statements that would not be prevented or detected. Accordingly, the Company’s management has determined that this control deficiency constitutes a material weakness.

Cont…Ineffective controls over accrued liabilities . The Company did not maintain effective controls over the completeness and accuracy of certain of its accrued liabilities and related expense accounts, including cost of goods sold. Specifically, a United Kingdom subsidiary failed to ensure the completeness and accuracy of its customer discounts and accruals for processing costs and services. This control deficiency resulted in audit adjustments to the Company’s 2005 annual consolidated financial statements. Additionally, this control deficiency could result in a misstatement in the accrued liabilities and related expense accounts, including cost of sales that would result in a material misstatement to the annual or interim consolidated financial statements that would not be prevented or detected. Accordingly, the Company’s management has determined that this control deficiency constitutes a material weakness.

These material weaknesses were considered in determining the nature, timing, and extent of audit tests applied in our audit of the 2005 consolidated financial statements, and our opinion regarding the effectiveness of the Company’s internal control over financial reporting does not affect our opinion on those consolidated financial statements.

In our opinion, management’s assessment that TRM Corporation did not maintain effective internal control over financial reporting as of December 31, 2005, is fairly stated, in all material respects, based on criteria established in Internal Control — Integrated Framework issued by the COSO. Also, in our opinion, because of the effects of the material weaknesses described above on the achievement of the objectives of the control criteria, TRM Corporation has not maintained effective internal control over financial reporting as of December 31, 2005, based on criteria established in Internal Control — Integrated Framework issued by the COSO. /s/ PricewaterhouseCoopers LLP Portland, Oregon March 30, 2006

TRM: Notes to Consolidated Financial Statements

1. Description of Business and Summary of Significant Accounting Policies (portion of)

Our consolidated financial statements have been prepared on a going concern basis which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. We incurred a net loss of $8.9 million in 2005. As a result of our 2005 financial performance, we have failed to meet certain financial covenants of our financing agreement with Bank of America, N.A. and other lenders. As discussed further in Note 8 we have entered into a Forbearance Agreement and Amendment with our lenders pursuant to which they have agreed not to take any action with regard to our covenant violations prior to June 15, 2006. However, we do not expect to meet all of our financial covenants for the second quarter of 2006, because some of the covenant calculations include results of operations for the most recent twelve-month period, and we incurred substantial losses in the fourth quarter of 2005. Therefore, we expect that the lenders will have the right to require payment in full of our outstanding debt under our financing agreement ($91.6 million at December 31, 2005). Because there are claimed cross-default provisions in TRM Inventory Funding Trust’s Loan and Servicing Agreement, if we do not refinance the outstanding debt under our financing agreement or obtain an additional forbearance period we expect to be declared in default of the provisions of the Loan and Servicing Agreement as well, and the lender will be able to demand payment. These factors, among others, may indicate that we may be unable to continue as a going concern for a reasonable period of time. Our financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or the amounts and classification of liabilities that may be necessary should the Company be unable to continue as a going concern. The Company’s continuation as a going concern is contingent upon our ability to continue to defer payment of our liabilities under our financing agreement, or to refinance the debt.

We expect to be able to refinance the outstanding balances under our financing agreement and have begun initial efforts to do so. However, we can provide no assurance that we will be able to do so. If we are unable to refinance our debt or to get our lenders to agree to any further forbearance from calling our loans, we might be forced to seek protection of the courts through reorganization, bankruptcy or insolvency proceedings.

If we refinance the outstanding balances under our financing agreement, or if the balance is demanded by the lender, the remaining unamortized deferred financing costs of $2.5 million as of December 31, 2005 associated with this credit facility may be written off in the period of refinancing or demand.

Technical review of Financial Statements

Use Disclosure Checklist If this is subject to 404…what

happens if you find something wrong with the statements?

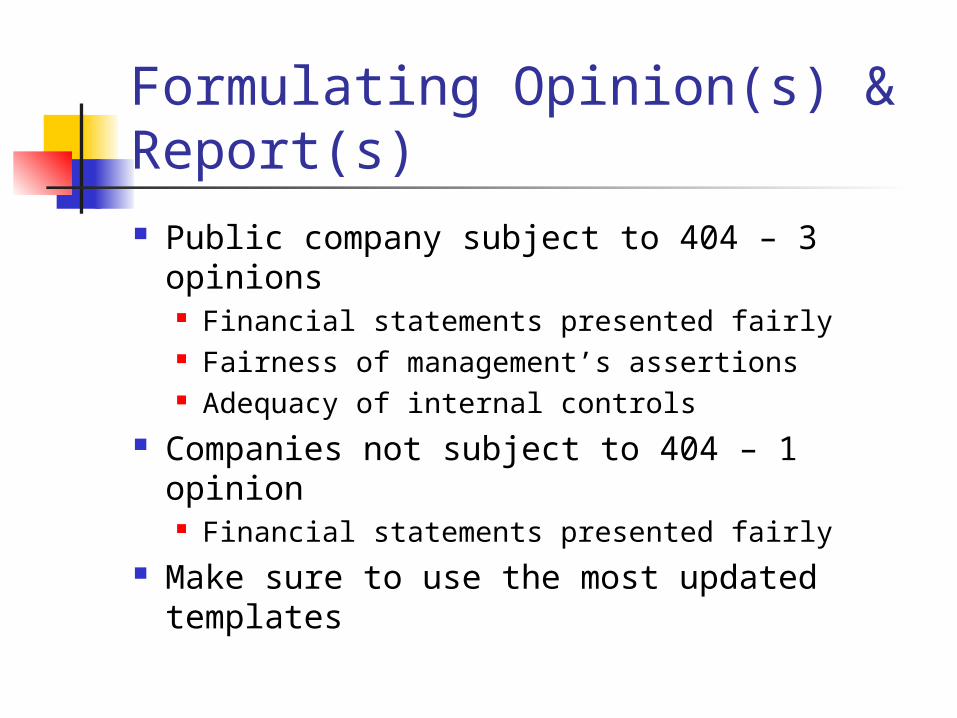

Formulating Opinion(s) & Report(s) Public company subject to 404 – 3

opinions Financial statements presented fairly Fairness of management’s assertions Adequacy of internal controls

Companies not subject to 404 – 1 opinion Financial statements presented fairly

Make sure to use the most updated templates

Communicating with the Client Communicating internal control

matters (AU 325 and PCAOB Standard No. 2)

Communicating matters of audit conduct (AU 380)

Management letter

Internal Control Matters REQUIRED for companies if significant

deficiencies are noted. Public companies subject to 404 – All

significant deficiencies are reported Private companies – not required to

search for significant deficiencies, but if they are found, must report

Control Deficiencies Significant deficiency

Internal control deficiency that adversely affects the company’s ability to initiate, record, process, or report external financial data reliably in accordance with GAAP…results in more than a remote likelihood that a misstatement of the annual or interim financial statements, that is more than inconsequential in amount, will not be prevented or detected.

Material weakness Significant deficiency that results in more than a

remote likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected

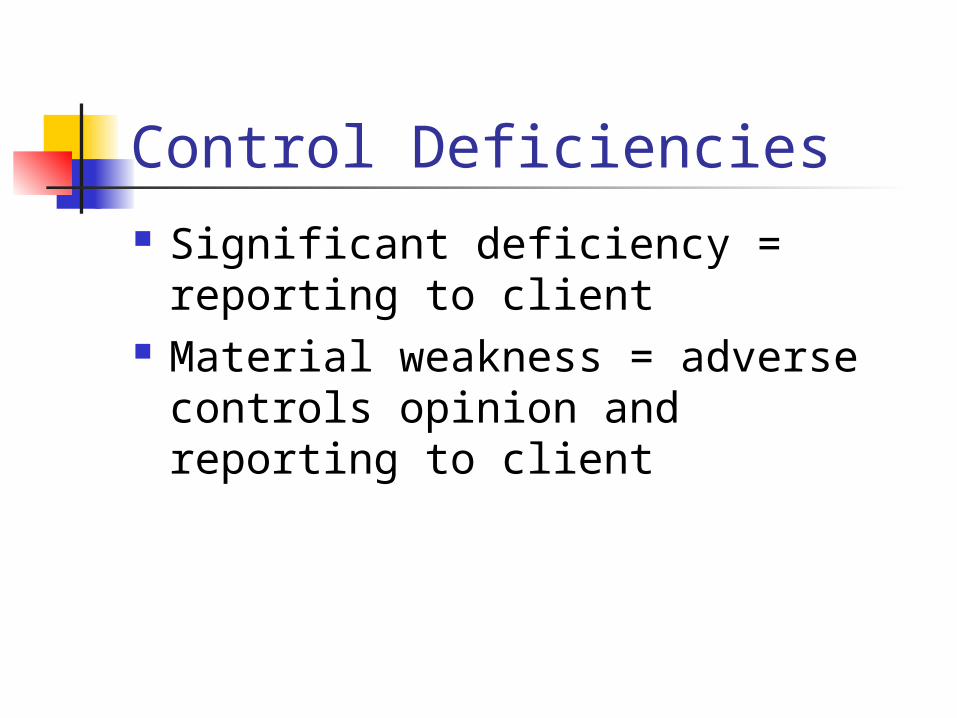

Control Deficiencies Significant deficiency = reporting

to client Material weakness = adverse

controls opinion and reporting to client

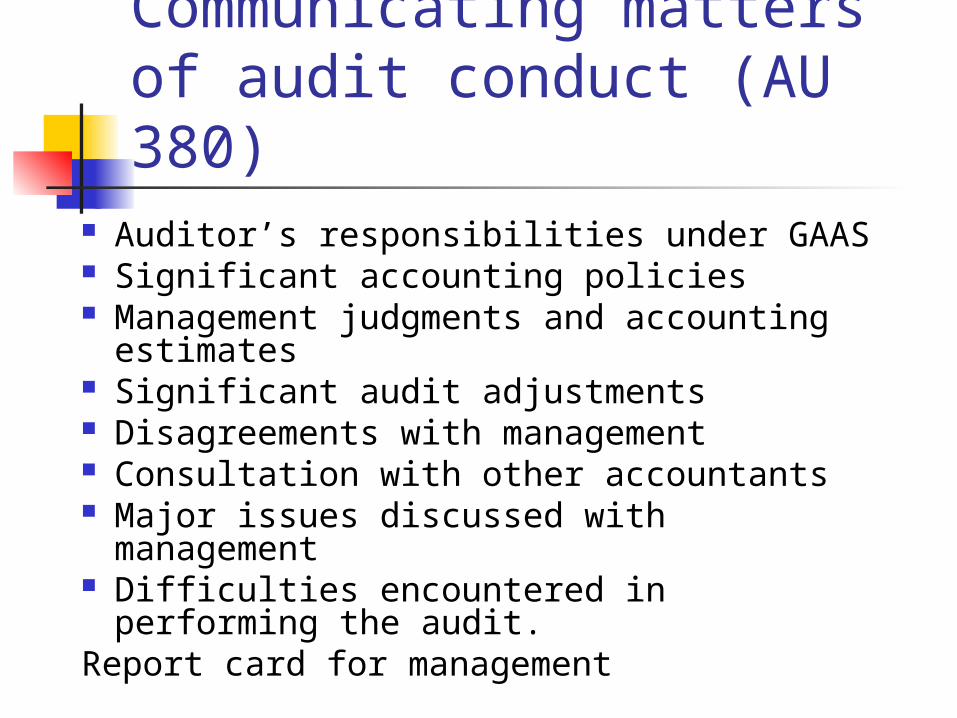

Communicating matters of audit conduct (AU 380)

Auditor’s responsibilities under GAAS Significant accounting policies Management judgments and accounting

estimates Significant audit adjustments Disagreements with management Consultation with other accountants Major issues discussed with

management Difficulties encountered in performing

the audit.Report card for management

Management Letter Recommendations not otherwise

communicated/reported. Improved efficiency and

effectiveness Way to add value to your clients.

Post-Audit Responsibilities Discovery of facts between report date

and issuance of report –> dual dating of report

Example, follows original date:“February 28, 20xx, except for the

information in Note A for which the date is March 7, 20xx.”

Post-Audit Responsibilities Do the facts affect the report that was issued?

If yes: Time for restatement and must take steps to

prevent future reliance on the audit report. Consult attorney and insurance carrier. Notify the client that the audit report must no longer be

associated with the financial statements. Notify the regulatory agencies having jurisdiction over

the client that the report should no longer be relied on. Notify each individual known to be relying on the

financial statements that the report should no longer be relied on.

Discovery of Omitted Procedure

Assess the importance of the procedure in relation to ability to currently support opinion expressed on the financial statements.

If needed, perform procedure and obtain evidence.

If evidence does not support opinion previously issued on the financial statements, follow procedures related to subsequent discovery of facts existing at report date.

Audit’s done!