challenges to the ifrs adoption in china - apbersociety.org · asia pacific business &...

TRANSCRIPT

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

61

ChallengestotheIFRSAdoptioninChina

XinyunMiaoNationalInstituteofTechnology,UbeCollegeYamaguchi,[email protected]

ABSTRACTThe objective of this paper is to clarify the challenges to the adoption of InternationalFinancial Reporting Standards (IFRS) in China. By adopting the case study approach andusing data collected from various sources, this paper clarified challenges to the directadoptionofIFRSinChina,includingtheendorsementprocess,theinterpretationsofIFRSbythe Ministry of Finance (MOF) and Chinese accounting professionals, the costs of IFRSimplementation,thetranslationofIFRSintoMandarinChineseandtheIFRS-relatedtrainingand education. The unique Chinese institutions would mainly pose these challenges. Byunraveling the incompatibility between the direct adoption of IFRS and Chinese-specificinstitutionalframeworkoffinancialreporting,thispaperarguesthatevenIFRSareadoptedin all countries; the interpretations and applications of IFRS may be diversified acrosscountries.Thissuggeststhatinordertoachievethedefactoglobalconvergenceoffinancialreporting, the discussions should be extended from simple accounting issues to a moreholisticperspective,includingtheinstitutionaldiversitysurroundingtheaccountingsystemsinindividualcountries.Keywords: International Financial Reporting Standards (IFRS), institutionalcomplementarity

INTRODUCTION

The International Accounting Standards Board (IASB) has been developing theInternationalFinancialReportingStandards (IFRS)and facilitating the internationaluseofIFRS.Thepromotionofconvergencewithoradoptionof IFRShasbeen largelysupportedby the growth of multinational enterprises and the increasing globalization of capitalmarkets.Numerousresearchesindicatedthatthemultinationalenterpriseswouldbenefitfrom the adoption of IFRS. Specifically, international use of IFRSwill lowermultinationalenterprises’ cost of preparingmore than one set of accounts and consolidating financialstatementsunderdifferentaccountingstandards(Chand,2005;Irvine,2008;Phan,2014).Especially,becausethemultinationalaccountingfirmshavenecessaryknowledgeandskillstoapplyIFRS,theyarelikelytogainacomparativeadvantageoverlocalaccountingfirmsinthe IFRS adoption (Chand, 2005; Irvine, 2008). Furthermore, the globalization of capitalmarketsrequiresasinglesetofglobalfinancialstandardstoreducethefinancialreportingcosts and improve the comparability of financial information (Nobes and Parker, 2016).With these supports, theuseof IFRShas extended rapidly. The IASB’s surveyshows thatnearly 130 countries have required all or most domestic listed companies and financialinstitutionsintheircapitalmarketstopreparefinancialstatementsinaccordancewithIFRS(asofMarch30,2017).

InspiteoftheinternationaladoptionofIFRS,numerousstudiessuggestedthatmanycountries,especiallydevelopingcountries,lacknecessaryinfrastructuresfortheconsistent

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

62

applicationofIFRS.Thus,theconvergenceofaccountingstandardsondejurelevelmaynotnecessarily lead to convergencede facto. For instance,Poudeletal. (2014) clarified thatthedirect adoptionof IFRS inNepal doesnotnecessarily improve the comparability andtransparency of financial reporting prepared by Nepalese companies. That is becausecontextualfactorsinNepal,suchaswidespreadcorruption,underdevelopedcapitalmarket,and a lack of qualified and well-trained accountants, are likely to hinder consistentinterpretations and applications of IFRS inNepal.Mısırlıoğlu et al. (2013) illustrated thatTurkish listed companies have not applied IFRS consistently or made disclosure incompliance with IFRS requirements in spite of the mandatory IFRS adoption in 2005.Mısırlıoğlu et al. (2013) explained that Turkey’s distinct factors, such as the taxation-oriented financial reporting tradition, the lackof efficient enforcementmechanisms, andinadequate management information systems, are likely to pose an impediment to theconsistentimplementationofIFRS.

Inadditiontothenational-specificfactors,suchfirm-specificfactorsasfirmsizeandindustry are significant elements that determine the effective implementation of IFRS.Guerreiroetal.(2008)demonstratedthatfirmsizeisasignificantvariableindeterminingthepreparednessofcompaniesforapplyingIFRSandshowedthatlargercompanieshavestronger incentives to improve the quality of financial reporting. Moreover, as IFRSprovidedmanagersoptionsonaccounting treatments for thesamebusiness transactionsand economic events, different accounting policy choices under IFRS among enterpriseswould hinder the comparability of financial information. Stadler and Nobes (2014)illustratedthatindustryfactorswouldaffectIFRSpolicychoices,partlybecauseenterprisestendtokeeppolicychoicesalignmentwithindustrypeers.Furthermore,certainaccountingissues, such as fair valuemeasurement, would be problematic in certain industries. Forexample,Mulleretal.(2008)foundthattheadoptionofIAS40andtherequirementthatall enterprises owning investment properties should display fair values of these assets,whether through recognition or disclosure, have not fully eliminated differences ininformationasymmetryofEuropeanUnion(EU)listedcompaniesintherealestateindustry.That maybe due to investors’ concerns over the reliability of fair value estimates bymanagers.

TheincompatibilitybetweenIFRSandexistingnationalinstitutionalarrangementsandthe problems related to particular industries or firm size might result in unintendedconsequences,suchasadecrease inthereliabilityof financial reporting.ThismayhindertheachievementofintendedobjectivesofIFRSadoption(eithermandatoryorvoluntary),suchasimprovingthecomparabilityandtransparencyoffinancialinformation.

Althoughnumerous studies investigatedproblems related to theglobal adoptionofIFRS,fewstudiesrevealedobstaclestotheimplementationofIFRSinChina.Theobjectiveof this paper is to fill this gap and clarify the challenges to the IFRS adoption in China,including the endorsement process, the interpretations of IFRS, the costs of IFRSimplementation, the translation of IFRS into Mandarin Chinese, and the IFRS-relatedtrainingandeducation.

Chinaisoneofaminorityofcountriesthathavenotrequiredorpermitteddomesticcompanies to apply IFRS. The Chinese government requires listed companies in ChinesedomesticcapitalmarketsandChinesefinancialinstitutionstopreparefinancialstatementsin accordancewithChineseaccounting standards (CAS).Byanalyzing the challenges, thispaper would provide a rationale for the decision of the accounting standards setter inChina, the Ministry of Finance (MOF), concerning convergence with IFRS. This would

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

63

helpfulformakingforecastsaboutthepotentialadoptionofIFRSinChina.The remainder of this paper is organized as follows. Section two describes the

convergence process of CASwith IFRS since 2005. Section three elaborates the researchmethodsofthispaper,includingthetheoreticalframework,thecasestudyapproach,andthedatacollection.SectionfourinvestigatesthemainissuesthatarelikelytochallengetheIFRS implementation in China. Section five concludes this paper by summarizing theincompatibility between the direct adoption of IFRS1 and contemporary Chinese-specificinstitutionalarrangements.

THECONVERGENCEPROCESSOFCASWITHIFRS

Theconvergence towardsoradoptionof IFRSataglobal levelhadputChinaunderstrongexternal pressures to converge its accounting systemwith IFRS andhad triggeredaccountingreformsinChinasince2005.TheMOF,atthebeginningof2005,setupaplanto establish 22 new specific accounting standards and to revise the existing basicaccounting standard and 16 specific accounting standards until the end of 2005 or thebeginningof2006.Themainobjectiveofthereformduring2005and2006wastoimprovetheconvergenceofCASwithIFRS.Thus,inordertoestablishanewsetofCASinlinewithIFRS,theMOFenhancedcollaborationwiththeIASB.Thecollaborationresultedinajointstatement inNovember 2005, so-called the “2005Beijing Joint Statement.” TheMOF, inthestatement,announcedthatitwouldsettheconvergencewithratherthanadoptionofIFRS as “one of the fundamental goals of” its standard-setting program (CASC and IASB,2005).TheIASB,inturn,tookastepbackfromitsinitialstrongpositionthatconvergencemeantfulladoptionofIFRSwordforword(Wang,2006),andrecognizedthattheMOFhadtheauthoritytodeterminetheformandwaystoconvergeCASwithIFRS(CASCandIASB,2005).

Severalmonthsafterthisjointstatement,theMOFpromulgatedanewsetofCASinFebruary 2006, known as the Accounting Standards for Business Enterprises (ASBE). Thenew set of CAS issued in 2006 was acknowledged by the IASB as having achieved“substantial convergence” with IFRS (IASB, 2006). The “substantial convergence,” asdefinedbyofficialswithintheMOF,meantthattheprinciplesofrecognition,measurementand reporting in CASwere the same as those in IFRS, although the IFRS have not beenincorporated into CAS word for word (Liu, 2006). TheMOF and the IASB expected that“substantialconvergence”wouldresultinidenticalfinancialstatementsinaccordancewitheitherIFRSorCAS(CASCandIASB,2005).TheMOFrequiredalllistedcompaniesinChina’sdomestic capital markets to apply the new set of CAS for both consolidated and non-consolidatedfinancialstatementsfromthebeginningofthefiscalyear2007.TheMOFhasbeengraduallyextendingtheapplicationofthenewsetofCASforbothconsolidatedandnon-consolidated financial statements of unlisted large and medium-sized companies(MOF,2009).

During and after the financial crisis of 2007-2008, the Group of Twenty (G20)addressed accounting as a critical issue for financial stability. It encouraged membercountries,includingChina,toconvergetheirnationalGAAPswithIFRSoradoptIFRS.WiththeG20’sendorsementofIFRSasthesinglesetofglobalfinancialreportingstandards,theIASBfurtherpressuredtheMOFtodirectlyadopt IFRS inChina.Forexample,since2011,thecurrentChairmanoftheIASB,HansHoogervorst,hasexertedpressuresontheMOFtofullyadoptIFRSinChinatoreplaceCAS.WhenvisitedChinain2011,hegaveaspeechandstated “there is a lingering suspicionamong thebroader international financial reporting

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

64

community about closeness between IFRS and Chinese accounting standards. In thisregard,theterm‘principallyinlinewithIFRS’doesChinanofavours”(Hoogervorst,2011).HefurthersuggestedthatChinashouldmakeadecisionto“fullyadoptIFRS”(Hoogervorst,2011)asBrazildid.

TheMOF,however,hadestablished the “convergenceapproach”as the strategy torespond to the pressures of the global convergence in financial reporting (see the 2005Beijing Joint Statement).Under this approach, theMOF continues todevelopCAS,whilegraduallyeliminatingdisparitiesbetweenCASandIFRSovertime.TheMOFhasnoplanstoaccept the “direct adoptionapproach” (eithermandatoryor voluntary) suggestedby theIASB,inwhichIFRSwouldreplaceCAS.YangMin,formerDirectorGeneral(2010-2015)ofthe Accounting Regulatory Department within the MOF argued, “the convergenceapproach is a pragmatic and effective way to meet the needs for establishing anddeveloping accounting standards” (Yang et al., 2011, p. 14) in China,which is a countrywithspecificlegalenvironment,codesoflanguage,andimplementationproblems.

Afteradecadeofsigningthe2005BeijingJointStatement,the IFRSFoundationandtheMOFheldabilateralmeeting,ontheoccasionoftheIFRSFoundationTrusteesmeetinginBeijingduringOctober13thto16th,2015.Thetwoorganizationsdiscussedsomeoptionsforhowtofurtherenhancethecooperationandrelationshipbetweentheminthefuture(IASB,2015b).ThebilateralmeetingresultedinaJointStatement,referredtoasthe“2015BeijingJointStatement,”toupdatethe2005BeijingJointStatement.Intheupdatedjointstatement,DaiBohua,AssistantMinisteroftheMOF,reaffirmedthatthegoaloftheCASestablishmentistoachievefullconvergencewithIFRS.Thiscommitmentisconsistentwiththe “G20-endorsedobjectiveof a single setofhighquality, global accounting standards”(IASB,2015a).TheIFRSFoundation, inturn,assentedtoensureChinesestakeholders’fullinvolvement “in the future development of IFRS” (MOF and IFRS Foundation, 2015).Furthermore, the twoorganizationsannouncedaplan toestablisha jointworkinggroup“to explore ways and steps to advance the use of IFRS within China and other relatedissues,especially for those internationallyorientatedChinesecompanies” (MOFand IFRSFoundation,2015).

Althoughthe2015BeijingJointStatementdidnotspecifythedirectadoptionofIFRS(eithermandatoryorvoluntary)inChina,itraisedthelikelihoodofdirectadoptionofIFRS(either mandatory or voluntary), at least in the “internationally orientated Chinesecompanies”(MOFandIFRSFoundation,2015),afterthelong-termadherenceoftheMOFtotheconvergenceapproach.Actually,WangJun,formerViceMinisteroftheMOF(2005-2013),suggestedthisprobability inhispresentation inthe3rd2009 IFRSAdvisoryCouncilmeetingasfollows:

Duetofactors,suchasthelawsystemandculture,atpresent,itisimpossibleforChinese accounting standards to be equivalent with International FinancialReporting Standards word for word. However, we do not disagree that it isattemptable to prepare financial statements of Chinese enterprises,which havelisted shares in overseas capital markets, or Chinese large multinationalcompanies, directly in accordance with International Financial ReportingStandardswhenconditionswillhavepermitted.(Wang,2009,p.4)

Actually, increasingoverseas financingbyChineseenterpriseshasbeena significantimpetusfortheconvergenceofCASwithIFRS.Attheendof2016,therewere394Chinese

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

65

companiesthathavelistedsharesontheStockExchangeofHongKong.Moreover,Chineseenterprises,in2016,raised941,273millionRMBbyissuingsharesontheStockExchangeofHong Kong, while raised 1,990,190 million RMB by issuing shares on Chinese domesticcapitalmarkets,namely theShenzhenStockExchangeand theShanghai StockExchange.Most Chinese enterprises that have listed shares on the Stock Exchange of Hong Kongpreparetwosetsofaccounts inaccordancewithCASandIFRSasadoptedbyHongKong.TheMOFacknowledgedthatconvergingCASwithIFRSwouldbenefitChineseenterprisesthat have raised or intend to raise funds in the global capital market by reducing theirfinancial reporting costs. This was one of the MOF’s motivations to promote theconvergenceofCASwithIFRS(Miao,2016).

In addition to overseas financing, Chinese enterprises have been expanding theirbusinessactivitiesworldwide.According to theWorldBank’s statistics, the foreigndirectinvestment (FDI) ofChineseenterprises in2015 reached174.391billionUSD, accountingfor about 9% of the global net outflows of FDI, which was 1.866 trillion USD in 2015.Chinesemultinationalenterpriseswouldhavestrongerincentivestopromotetheadoptionof IFRS inChina,as thiswould save their costs to consolidate financial statementsunderdifferentaccountingstandards.

RESEARCHMETHODS

TheoreticalFramework

The analyses of this paper are mainly based on the notion of institutionalcomplementarity. Aoki (2001) defined the institutional complementarities as “synchronicinterdependencies among institutions” (Aoki, 2001, p.225), such as “political,organizational, and social domains” (Aoki, 2001, p.3), and suggested that “one type ofinstitutionratherthananotherbecomesviableinonedomainwhenafittinginstitutionispresent in another domain, and vice versa” (Aoki, 2001, p.225). Applying this notion toaccounting,Hailetal. (2010)suggests,“accountingstandardsareoneofmany importantinstitutionalelementsaffectingfinancialreportingpracticesinacountry”(Hailetal.,2010,p.360).Furthermore,asaccountingsystemislikelytobecomplementarytoitssurroundinginstitutionalarrangementsthatvarygreatlyfromcountrytocountry,“changingsolelytheaccounting standards” (Hail et al., 2010, p.359) (e.g., adopting IFRS to replace nationalaccounting standards) may “have limited effects and, in some cases, can even haveundesirable effects” (Hail et al., 2010, p.359) on financial reporting practices in certaincountries.

CaseStudyApproach

Thispaperadoptsacasestudyapproach.CooperandMorgan(2008)suggestedthatthe case study approach is useful when the research aims to examine the details ofcontext-dependent, complex and significant events, such as the changes in accountingregulations. Cooper and Morgan (2008) further argued that the case study approach ishelpful for understanding the applicability and rationalization of certain accountingregulations in a specific context. Thus, the case study approach is appropriate for thispaper.ThisisbecausethispaperaimstoassesstheapplicabilityofdirectadoptionofIFRS(eithermandatoryorvoluntary)inChinabydiscussingthecompatibilityofIFRSwithmainelementsoftheChinese-specificcontext(e.g.,thepoliticalandtaxationsystems).

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

66

DataCollection

The data used in this paper was collected frommultiple sources including primarysources and secondary documents. The primary sources mainly include officialpublications, speeches, and pronouncements of senior officials within the MOF. This isbecause the MOF is the only authority responsible for establishing Chinese accountingstandardsandisoneofmajorsupervisorsoftheimplementation.ThestatementsofseniorofficialswithintheMOFhelpusexploretheirrationalityandvaluesregardingaccounting,and their opinions on the global convergence of financial reporting, especially, the IFRSadoption. We also reviewed documents related to the development and training ofChineseaccountingprofessionalsissuedbytheMOF.TheMOFisthemajoractortodesign,establishandimprovethedevelopmentofChineseaccountingprofessionals(Wang,2012),which is an essential infrastructure for the consistent and rigorous implementation ofaccountingstandards.

Regardingsecondarydocuments,wescrutinizedtheMOF’sanalytical reportsontheimplementationof thenewsetofCAS inorder todetect thepracticalproblemsand theinfluence of new accounting standards on financial statements of Chinese listedcompanies. We also examined the China Securities Regulatory Commission (CSRC)’sregulatoryreportsinordertounderstandtheproblemsrelatedtotheinterpretationsandapplicationsofthenewsetofCAS.TheCSRC’sreportsalsodealwithproblemsregardingauditingoffinancialstatementspreparedbyChineselistedcompaniesinaccordancewiththenewsetofCAS.AsthesetofCASissuedin2006wasacknowledgedashavingachieved“substantial convergence” with IFRS, it is expected that the implementation problemsalreadyidentifiedintheanalyticalreportsoftheMOFandtheCSRCwouldstillexistduringthe direct adoption of IFRS (either mandatory or voluntary) in China. Furthermore, theMOF hasmodified IFRS to accommodate Chinese-specific contextwhen setting CAS. Forexample,theMOFlimitedtheapplicationoffairvaluemeasurementinCAStoreducetheimpactof fairvaluemeasurement inmanyareas (BiondiandZhang,2007). It isexpectedthat implementation problems identified by the MOF and the CSRC may become moreacute if theMOF permits or requires Chinese enterprises to prepare financial reports inaccordancewithIFRS.

Additionally,thesecondarydocumentsincludearticlesandbookscontainingresearchand analyses of the Chinese accounting system and its surrounding institutions. Thesedocuments were written by Chinese and foreign academics, accounting professionals inChina, and officials in Chinese regulatory organizations. Other documents includeinvestigation reportsby internationalorganizations, suchas theWorldBank, and foreignorganizations,suchastheFinancialServicesAgencyinJapan.

Byanalyzingarchivedmaterials,thispaperclarifieschallengestotheimplementationofIFRSinChina,includingissuesconcerningtheendorsementprocess,theinterpretationsof IFRS, thecostsof IFRS implementation, the translationof IFRS intoMandarinChinese,andtheIFRS-relatedtrainingandeducation.

CHALLENGESTOTHEIMPLEMENTATIONOFIFRSINCHINA

Endorsement

AccordingtotheAccountingLaw (article7),theNationalPeople’sCongressofChinahasdelegatedChineseaccountingstandardssettingauthoritytotheMOF.SincetheIASBis

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

67

a private standard setter without the power to issue legally binding standards, IFRS asissued by the IASB are not simply applied in each country or region and need to beendorsedby localauthoritativeagencies.Actually,severalcountriesandregionalentities,suchasJapanandtheEU,haveappliedendorsementmechanismsforexistingIFRS,futureamendmentsofexistingIFRS,orthecreationofnewIFRS.

Endorsement mechanisms had been used as a safeguard against undue foreigninfluenceandtopreservelocallegislators’vetorights.Forexample,theEUhadconductedanendorsementmechanism to grant theEUa veto righton IFRS implementation in thisregion,andensureitsinfluenceinthestandards-settingprocessoftheIASB.Thishadbeenhighlighted by changes of IFRS in response to pressures from the EU during the globalfinancial crisis. One change is allowing reclassification of financial assets out of the “fairvaluethroughprofitorloss”and“available-for-sale”categories(Camfferman&Zeff,2015).Thus,itcanbeexpectedthatifIFRSareadoptedinChina,theMOFwillbelikelytoapplyanendorsementmechanismtocreate“IFRSasendorsedbytheMOF.”

The Chinese-specific institutional arrangements have several prominent features,suchasahighweightofthesecondarysectorinChina’seconomy,2theheavydependenceon bank loans3 for financing, and the scarcity of qualified accounting professionals.4 TheChinese reporting system has evolved in concert with these features. For instance, CAStake thehistorical costas theprincipalmeasurementattributeand restrict theextensiveapplicationoffairvalue.Assuch,eveniftheMOFdecidestoadoptIFRS,itisunlikelythattheMOFwillpermitor requireChinesecompanies toapply“IFRSas issuedbythe IASB.”The MOF will be likely to make modifications and exclusions to IFRS to accommodateChineseinterests.Forexample,althoughtheIASBprohibitsthepoolingofinterestsmethodfor business combinations, Yang Min, former Director General of the AccountingRegulatory Department, recognized that this method is necessary for businesscombinationsinChina,andstated:

In China, a large number of business combinations happened within the sameenterprise groups. These are business combinations under common control,regardingwhich IFRShavenotyetprovidedclearregulations.Supposingthatweacceptthe“directadoption”approach, thiswill result inagap intheaccountingstandards, leading to the absence of regulations for such accounting practices.Even if we wait for the IASB to establish a new standard or revise the extantstandardforthesetransactions,wewouldhavetowaitforalongtimebecauseofthedueprocess,suchasplanningtheproject,makingresearch,conductingpublicconsultation, voting, and publishing the standard. This is not conducive to theimprovement in accounting practices and financial information of Chineseenterprises.(Yangetal.,2011,p.15)

Additionally, Liu Yuting, former Director General (2002-2010) of the Accounting

Regulatory Department, pointed out that CAS excluded the accounting standard foremployeebenefits,andtheaccountingstandardforfinancialreportinginhyperinflationaryeconomies.ThisisbecauseemployeebenefitsarenotcommoninChina,andhyperinflationis not expected to occur in an economyunder themacroscopical control of the Chinesegovernment(Liu,2007).EveniftheMOFdecidestodirectlyadoptIFRS, itwillbelikelytoadd certain accounting regulations that are exempt in IFRS, or exclude certain IFRSregulations in theChinese-specificversionof IFRSduringanendorsementprocess.These

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

68

deliberate modifications would lead to a national set of IFRS in China. Such aregionalization of IFRS opposes the IASB’s intended goal of facilitating cross-bordercomparabilitybyestablishingasinglesetofglobalaccountingstandards.

Moreover,iftheMOFadoptsIFRS,theendorsementprocesswillpotentiallyleadtoatime lag between the release of standards or interpretations by the IASB andcorresponding regulations in “IFRSasendorsedby theMOF.”The time lagmaybeup toyears.Forexample,theIASBestablishedIFRS13,andmadeiteffectiveforannualperiodsbeginningonorafterJanuary1st,2013.TheMOFincorporatedIFRS13intoCAS,andissuedthe accounting standard for fair value measurement on January 26th, 2014, which waseffective for Chinese listed companies since July 1st, 2014. The time lag between theeffectivedatesoftheaccountingstandardforfairvaluemeasurementinIFRSandCASwasoneandahalfyears.Thetime lagbetweenthereleaseofastandardbythe IASBand itsendorsement by the MOF is likely to hinder the comparability of financial reportingbetweenenterprises inChinaand firms inother IFRS-adopting countries. This is becausethe MOF will be unlikely to permit Chinese enterprises to voluntarily apply an issuedstandardbeforeendorsementwhilefirmsinothercountriesmaybeapplyingthestandardalready.

InterpretationsofIFRS

Chineseaccountingprofessionalshaveexperiencedmerely30yearsofdevelopment.Moreover,mostofthemhavebeenaccustomedtotherules-basedapproachduringalongperiod of education and practice under the Chinese accounting system with detailedregulations. Thus, Chinese accounting professionals are considered to lack the necessaryeducationandexperience tomake consistent interpretationsandappropriate judgmentsunderprinciples-basedaccountingstandards(WorldBank,2009;ICAS,2010;Chen,2015).Actually, accountants in Chinese enterprises and auditors in accounting firms have beenlargely relying on guidance provided by the MOF, such as interpretations (jieshi) andexplications(jiangjie).ThiscausedcurrentCAStoprovidemorespecificrulesthanIFRSdo.Suchaprofessionalenvironment fostersprecise interpretationsandapplicationguidanceforaconsistentimplementationofIFRSinChina(Li,2011).

Chinese regulators, such as the CSRC, have been urging theMOF to providemoreprecise interpretations and implementation guidance. For example, Li Xiaoxue, formercommitteemember forDiscipline Inspectionwithin theCSRC, pointedout that theMOFhad not provided adequate interpretations to CAS, and suggested that theMOF shouldaccelerate the development of interpretations. Moreover, Li Xiaoxue suggested thatregulatorsoftheChinesefinancialsector,suchastheCSRC,theChinaBankingRegulatoryCommission (CBRC), and the China Insurance Regulatory Commission (CIRC), should alsoprovidedetailedguidancetoaccountingstandardsimplementation.LiXiaoxuestated:

Theinterpretationmechanismofaccountingstandardscannotmeettheneedsoffinancial reporting preparers and regulators [in China]. The MOF had claimedcontinuingconvergencewithIFRS.Thus, itconsultsregularlywiththeIASBwhendeveloping or modifying the implementation guidance. This process leads to alongperiodforissuingtheimplementationguidance,andinsomecases,theMOFand the IASBcannotcomeatdefinitiveconclusions.On theotherhand,Chinesecapitalmarketsareinanemergingandtransitionalperiod.Inthesemarkets,neweconomiceventsandtransactionshavebeencontinuouslyemerging.There isan

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

69

urgent need for uniform standards to regulate new economic events andtransactions.…RecentmodificationsofIFRS,suchasaccountingstandardsfortheimpairmentof financial instrumentsand lease,werecharacterizedas theoreticaland had a relatively lack of operability. … In order to regulate the [accountingstandards] implementation and improve the quality and comparability of[financial] information, regulators of the financial sector [in China] need toconsider how to provide detailed implementation guidance according to theactualsituationsin[business]entitiesundertheirsupervision.(Li,2011,pp.13-14)

Considering the currentChinese institutional factors, suchas the lackof accounting

professionals who are skilled in making appropriate interpretations and judgments ofprinciples-basedaccountingstandards,andthepoliticalpressuresfromtheChinesecapitalmarketsregulatorforimplementationguidance,theMOFwouldbelikelytoprovidemorepreciseguidelines, suchasbright-line thresholds,andexamples,even if itdirectlyadoptsIFRS.Moreover,Chineseenterpriseswillbe likely torelyonpreciseguidelinesofferedbytheMOFincaseswhereIFRShavegapsoraretoovague.

Agoglia et al. (2011) documented the effect of accounting standard precision onfinancial statement preparers’ judgments. Specifically, their results showed that financialstatement preparers were less likely to report aggressively (in Agoglia et al. (2011),preparers are more likely to capitalize the lease) when applying a less precise financialreporting standard (in Agoglia et al. (2011), that is the one with more principles-basedleaseclassificationcriteria),thanwhenapplyingamoreprecisestandard(inAgogliaetal.(2011) that is the onewithmore rules-based lease classification criteria).Given that theMOFisexpectedtoprovidemorepreciseguidancethantheIASB,accountingprofessionalsinChinawillbelikelytomakedifferentjudgmentsfromtheircounterpartiesinotherIFRS-adoptingcountries,evenifChinadirectlyadoptsIFRS.

Importantly, the MOF has adopted a perspective, focusing on the financial andproductive process generated by the whole entity, which leads to a matching-basedrepresentation and historical cost valuation. This differs from the IASB’s fair valueperspective,focusingonthenetworthoftheenterpriseastheresidualtotheshareholdersandanaccountingrepresentationofthemarket-basedvalueofthefirm(Biondi&Zhang,2007).Thus,theMOFislikelytoofferChinese-specificinterpretationsandimplementationguidelines,whichmay leadenterprises inChina tomakedifferentaccounting treatmentsforthesametransactionsandeconomiceventsfromIFRS-applyingfirmsinothercountriesdo. For example, although theMOF adopted the IFRS accounting treatments in currentCAS,allowingenterprisestochoosecostmodelorfairvaluemodelforthemeasurementofcertainassets(e.g.,investmentpropertiesandbiologicalassets)afterrecognition,theMOF“requiredenterprisestostrictlylimittheapplicationoffairvaluemeasurementduringtheimplementationofaccountingstandards”(Liu,2011,p.11).Thisevidenceshowsthatevenif China directly adopts IFRS, the MOF will be likely to provide interpretations andguidelines that are geared towards a local adaptation of IFRS, leading to differences inaccountingpracticesbetweenChinaandotherIFRS-applyingcountries.

Additionally, Chinese accounting professionals may face the challenge to interpretIFRS consistently as do counterparties in Anglo-American countries (World Bank, 2009).Specifically,principles-basedIFRScontainnumerousverbalprobabilityexpressions,suchas“sufficient certainty,” “reasonable assurance,” and “no longer probable” (Doupnik &Richter, 2004). These uncertainty and probability expressions need to be interpreted

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

70

appropriatelyandconsistentlytoenhancethecomparabilityoffinancialreporting(Chandet al., 2010). However, several previous studies (e.g., Doupnik & Richter, 2003, 2004;Doupnik & Riccio, 2006; Chand et al., 2010) documented the effects of country-specificfactors(e.g.,thenationalcultureandaccountingprofessionals’familiaritywithaccountingstandardsinIFRS)onaccountants’interpretationsofIFRS.Particularly,Chandetal.(2012)found that Chinese students showed greater conservatism and secrecy than Australianstudents inassigningprobabilitiestouncertaintyexpressions in IFRS.Furthermore,Chandetal. (2012)showedthatsimilarsecondaryandtertiaryeducationcouldnotmitigatetheeffects of the national culture on professional judgments of Australian (Anglo-Celtic)students and Chinese Australian students (who were born in China and migrated toAustraliatocompletetheirsecondaryandtertiaryeducation).EveniftheMOFadoptsIFRS,it would be expected that the unique Chinese national culture, such as long-termorientation and conservative virtues (Hofstede & Bond, 1988), would affect accountingprofessionals’ interpretations of IFRS. This would lead to different financial reportingbetweenChineseenterprisesandfirmsinAnglo-Americancountries.CostofIFRSImplementation

The MOF requires Chinese enterprises to prepare both consolidated and non-consolidated financial statements in accordance with the new set of CAS. The MOFconsiders that a single set of accounting standards for both consolidated and non-consolidatedfinancialstatementscanavoidmaintainingtwosetsofaccountsandreduceenterprises’ cost to prepare financial statements (FSA, 2012). Actually, non-consolidatedfinancial statements are important for Chinese enterprises. First, the CSRC requiredChinese listed companies to conduct profit distributions based on non-consolidatedfinancialstatements(CSRC,2008).Second,mostChineseenterprisescalculatethetaxableincome based on the accounting profits reported in the non-consolidated financialstatements. Traditionally in China, there has been a close relationship between taxationand accounting, and the calculation of taxable income has been a major purpose ofaccountingformostChineseenterprises,especiallysmallandmedium-sizedones(Doupnik&Perera,2012).Moreover,thecloselinkhasbeenspecifiedbytheEnterpriseIncomeTaxLaw,whichdefinesthefinancialstatementsasthebasisforcalculatingtaxableincome,andrequiresenterprises to submit financial statements to taxationauthoritiesalongwith taxreturns(article21,article54).

ConsideringthattheEnterpriseIncomeTaxLawuseshistoricalcostastaxbasisforallassets (article 56), if the MOF permits or requires Chinese enterprises to prepare bothconsolidated and non-consolidated financial statements in accordance with IFRS(hereinafter,“uniformityapproach”),thedivergencesbetweenaccountingregulationsandtaxation rules would be enlarged, leading to an increase in adjustment costs fromaccountingprofitstotaxableincomeforfirms(Daietal.,2005;Song,2013).Ontheotherhand, if theMOFpermitsor requires IFRSonly forconsolidated financial statementsandrequires CAS for non-consolidated financial statements (hereinafter, “separationapproach”),Chineseenterprisesshouldhavetoprepare twosetsof financial statements.OnewouldbeunderIFRSmainlyforthefinancialreportingpurpose,andtheotherwouldbe under CAS mainly for taxation purposes and profit distributions. This “separationapproach” would require skilled personnels who are competent to prepare financialstatements under IFRS and CAS. Considering the increasing complexity of both sets ofaccounting standards, Chinese firms should need to recruit new employees or re-train

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

71

existing employees. The costs to employ or re-train specialized staffs would be a heavyfinancial burden for companies, especially for small and medium-sized firms. Theimplementation costs led by the “separation approach” have been demonstrated inGermany(seeHellmannetal.,2010,p.113).Assuch,eitherthe“uniformityapproach”orthe “separation approach” would lead to high implementation costs for Chineseenterprises.

Additionally, the adoption of IFRS in China, either mandatory or voluntary, wouldlargelyincreasetheenforcementandregulationcostsofsupervisors,suchastheMOFandtheCSRC.First,eveniftheMOFadoptsIFRS,itisexpectedthattheMOFwouldcontinuetoweigh in on the implementation of IFRS. For example, considering the Chinese-specificcontext, there are insufficient qualified accounting professionals who are competentenoughtomakeappropriateinterpretationsofIFRSandjudgments.Thus,theMOFwouldhave to spend considerablebudgetary andpersonal resources toprovide interpretationsandpreciseimplementationguidanceforprinciples-basedaccountingstandards(Li,2011).

Second,theMOFandtheCSRCsupervisetheimplementationofaccountingstandardsin Chinese enterprises and the auditing of financial statements. The enforcementeffectiveness of the MOF and the CSRC largely depends on their funding, researchcapability, and officials’ professional knowledge. Actually, even for the new set of CAS,supervising capacity (e.g., human capacity) development for accounting standardsimplementationhasbeenanurgentissuefortheregulators.Forexample,theWorldBankpointedoutthatinordertoimprovethereviewofcompanies’financialstatementsaswellasthereviewofaccountingfirms’andCPAs’auditingpractices,regulatorsinChina,suchastheMOFandtheCSRC,needtorecruitmoretechnicallyqualifiedpersonnelswhohavetheexperience relatedwith accounting andauditing standards implementation (WorldBank,2009). If theMOFadopts IFRS, theMOFand theCSRCwouldhave to recruit specializedstaffsthathavepracticalexperiencerelatedwithIFRSimplementationandauditingofIFRS-basedfinancialstatements.ThiswouldbeabigchallengebecauseonlyasmallnumberofChinese accounting professionals have adequate exposure to IFRS-related reporting andauditingpractices(Wang,2012).

Third, the CSRC anticipates that extensive application of fair value measurementwould lead to a significant increase in supervision costs for financial reporting of listedcompanies.Forexample,JiaWenqin,theChiefAccountantandtheheadoftheAccountingDepartmentwithintheCSRC,stated:

ItisforeseeablethatiffairvaluemeasurementisappliedinChinainawiderangeas its application in the United States, this would lead to a large fluctuation incompanies’ net assets and net profits in different accounting periods, andmayprovide more earnings manipulation opportunities to companies. This wouldsignificantlyincreaseoursupervisioncostsandbringunprecedentedchallengestoregulation.(Jia,2010,p.9)

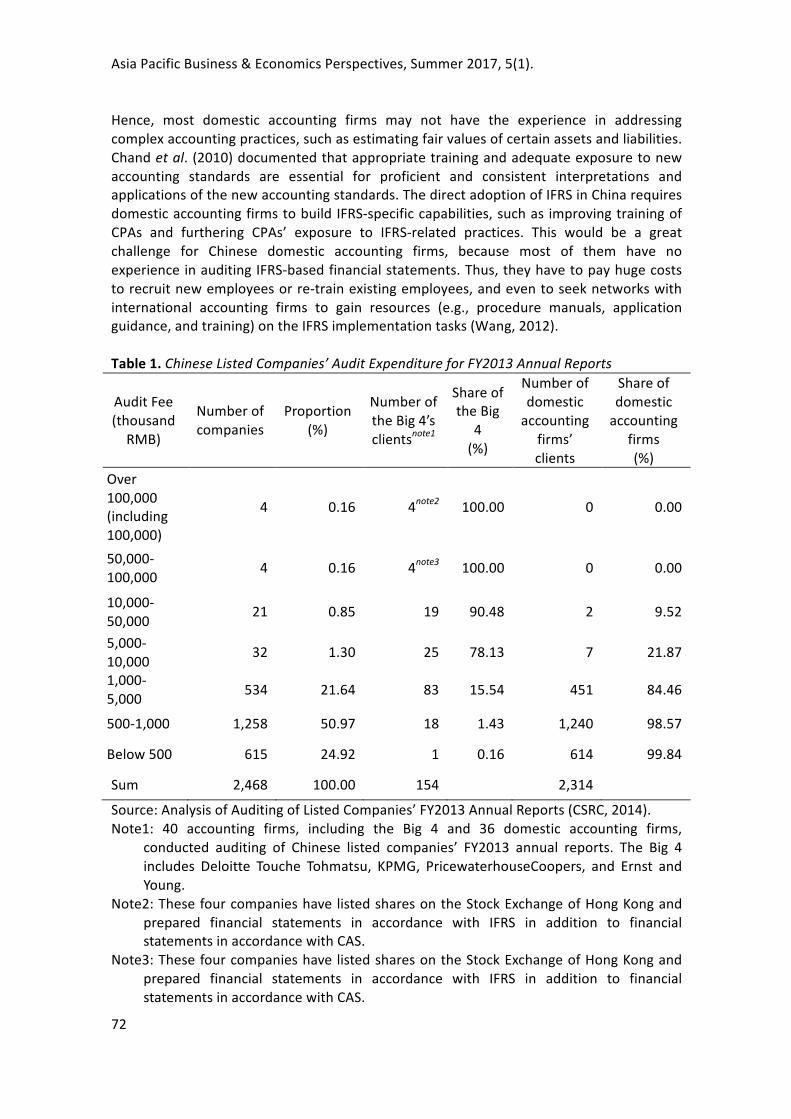

Moreover,thedirectadoptionof IFRSwouldbringasubstantial financialburdenforaccounting firms, especially for Chinese domestic ones. Table 1 describes the auditingexpenditure distribution for Chinese listed companies’ FY2013 annual reports. Table 1shows that themajor proportion (1,854 of 2,314) of Chinese domestic accounting firms’clients paid audit fees under onemillion RMB. This data shows that themain clients ofmost domestic accounting firms were relatively small and medium-sized enterprises.

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

72

Hence, most domestic accounting firms may not have the experience in addressingcomplexaccountingpractices,suchasestimatingfairvaluesofcertainassetsandliabilities.Chandetal.(2010)documentedthatappropriatetrainingandadequateexposuretonewaccounting standards are essential for proficient and consistent interpretations andapplicationsofthenewaccountingstandards.ThedirectadoptionofIFRSinChinarequiresdomesticaccountingfirmstobuildIFRS-specificcapabilities,suchas improvingtrainingofCPAs and furthering CPAs’ exposure to IFRS-related practices. This would be a greatchallenge for Chinese domestic accounting firms, because most of them have noexperienceinauditingIFRS-basedfinancialstatements.Thus,theyhavetopayhugecoststorecruitnewemployeesorre-trainexistingemployees,andeventoseeknetworkswithinternational accounting firms to gain resources (e.g., procedure manuals, applicationguidance,andtraining)ontheIFRSimplementationtasks(Wang,2012).Table1.ChineseListedCompanies’AuditExpenditureforFY2013AnnualReports

AuditFee(thousandRMB)

Numberofcompanies

Proportion(%)

NumberoftheBig4’sclientsnote1

ShareoftheBig

4(%)

Numberofdomesticaccounting

firms’clients

Shareofdomesticaccounting

firms(%)

Over100,000(including100,000)

4 0.16 4note2 100.00 0 0.00

50,000-100,000 4 0.16 4note3 100.00 0 0.00

10,000-50,000 21 0.85 19 90.48 2 9.52

5,000-10,000 32 1.30 25 78.13 7 21.87

1,000-5,000 534 21.64 83 15.54 451 84.46

500-1,000 1,258 50.97 18 1.43 1,240 98.57

Below500 615 24.92 1 0.16 614 99.84

Sum 2,468 100.00� 154 � 2,314 �

Source:AnalysisofAuditingofListedCompanies’FY2013AnnualReports(CSRC,2014).Note1: 40 accounting firms, including the Big 4 and 36 domestic accounting firms,

conducted auditing of Chinese listed companies’ FY2013 annual reports. The Big 4includes Deloitte Touche Tohmatsu, KPMG, PricewaterhouseCoopers, and Ernst andYoung.

Note2:ThesefourcompanieshavelistedsharesontheStockExchangeofHongKongandprepared financial statements in accordance with IFRS in addition to financialstatementsinaccordancewithCAS.

Note3:ThesefourcompanieshavelistedsharesontheStockExchangeofHongKongandprepared financial statements in accordance with IFRS in addition to financialstatementsinaccordancewithCAS.

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

73

Table 1 also shows thatmost Chinese listed companies (2,314 of 2,468) have beenauditedbydomesticaccountingfirms.Thus,thelackofChinesedomesticaccountingfirms’IFRS-specific capabilities would largely affect the entire auditing quality in China. ThiswouldhindertheIFRSadoptioninChina,becausehighqualityauditingisoneofeffectiveenforcementmechanismsfortheconsistentimplementationofIFRS.TranslationofIFRS

LiteraltranslationofsomeaccountingconceptsandtermsinIFRSisdifficultbecausefull equivalence in translation between English andMandarin Chinese is rare.When anexact accounting terminology equivalent to an IFRS concept does not exist inMandarinChinese, translators tend to use the nearest equivalent. Thismay “lead to a blurring ofmeaningor loss of significant differences in the concepts” (Evans, 2004, p.211), becausethe nearest equivalent may be already applied in the Chinese context and defineddifferentlyfromtheconceptinIFRS.

For example, there is no exact equivalent terminology in CAS to the accountingconceptof“income”,thus,theChinaAccountingStandardsCommission(CASC)withintheMOF used the nearest comparable terminology, and translated “income” intoMandarinChineseas“shouyi”(CASC,2013,p.10).Theterminologyof“shouyi”inCASistraditionallyequivalent to profit or loss. For instance, “earnings per share” was translated intoMandarinChineseas“meigu(meanspershare)shouyi(meansearnings)”(MOF,2006),andthe concept of “earnings” is defined as “profit or loss from continuing operationsattributable to the parent entity” and “profit or loss attributable to the parent entity”(IASB, 2016b, para.12). On the contrary, as the IASB stated that “an entitymay use theterm ‘net income’ to describe profit or loss” (IASB, 2016a, para.8), “income” does notnecessarilymeananetamountdeductingexpenses,namelyprofitorloss.Thus,“shouyi”isnottheexactChineseequivalentto“income.”ThisexampleprovidesevidencethatduringthetranslationprocessfromEnglishtoMandarinChinese,translatorsmayuseaccountingterminologiesthathavealreadybeenlinkedwithotherconceptsorideasinCAS.Thismaylead users of the Mandarin Chinese-version of IFRS, such as preparers of financialreporting, auditors, investors, and regulators in China, to understand some importantaccountingconceptsinadifferentwayfromtheusersoftheEnglish-versionofIFRS.

In addition to the misunderstandings caused by literal translation, word used intranslationmaycorrespondtodifferentconnotationsintheChinesecontext.ThisalsomayleadusersoftheMandarinChinese-versionofIFRStomakedifferentinterpretationsofanaccounting concept from the ones made by users of the English-version of IFRS. Forexample, Pan et al. (2015) found that Chinese students made significantly differentinterpretationsoftheprincipleof“control”andconsolidationjudgments,whentheyweregiven research instruments in English from when they were offered the same researchinstrumentstranslatedintoMandarinChinese.Panetal.(2015)furtherfoundthecauseforthe differences. The reason was that the word used in translation of “control,” namely“kongzhi,”hasaconnotationoftheChinesegovernment’s“invisiblepower”overeconomyand accounting. This connotation affected Chinese students’ interpretations of theprincipleof“control”andconsolidationjudgments.

Besides translating IFRS into various national languages verbatim, adding preciseguidance to IFRS by national accounting standards setters is another challenge for theglobal implementation of a single set of accounting standards. IFRS contain broad

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

74

principlesand“uncertaintyexpressions”withtheaimtoguide judgments inpractice.Forexample, IAS 17 Leases adopted uncertainty expressions, namely “major part” and“substantiallyall,”5toprescribethecriteriafortheclassificationofaleaseasoperatingorcapital lease. The MOF developed the accounting standard for leases by substantiallyadoptingIAS17,andincluded“forthemajorpartoftheeconomiclife”and“substantiallyall of the fair value of the leased assets” criteria. TheMOF translated “major part” into“dabufen”and“substantiallyall”into“jihuxiangdangyu.”TheMOFalsoprovidedguidancefortheinterpretationof“dabufen”and“jihuxiangdangyu”asfollows:“generally,‘dabufen’shouldbeabove75%(including75%)…‘jihuxiangdangyu’shouldbeabove90%(including90%)” (MOF, 2006b). Previous studies have documented that the guidance added intoprinciples-based accounting standards may affect accounting professionals’ judgments(e.g.,Agogliaetal., 2011). Thus, precise guidanceandbright-line thresholdsprovidedbytheMOFmay lead to inconsistent judgments between Chinese accounting professionalsandcounterpartsincountrieswithoutpreciseguidancetoIFRS.TrainingandEducation

If the MOF adopts IFRS, it should strengthen IFRS-related training and education,which are essential to ensure the consistent interpretations and applications of IFRS inChina. Indeed, the costof IFRS-related trainingandeducation inChina is expected tobehigher than in Anglo-American countries, whose concepts and principles are mostlyreflected in IFRS (Feng, 2001). The understanding of concepts behind each standard isessential toproperly interpret IFRS, tomakeappropriate judgments,andtoapply IFRS inthe way intended by the IASB (ICAS, 2010). Actually, financial reporting preparers inChinesecompaniesandChineseCPAshavebeenfacingconsiderabledifficultiesinapplyingtheIFRSconcepts,suchasfairvalueandimpairmentlosses(WorldBank,2009).

The education about the reasoning and accountingmodels behind IFRS, which aredifferent fromthoseofCAS, is likely tobeachallenge forChina.This isbecause inmostChineseuniversities, there isa lackofwell-trainedandhighlyknowledgeable teachers togive instruction in the accounting environment andmodels in Anglo-American countries(World Bank, 2009). Furthermore, the accounting curricula in some Chinese universitiesfocusedonlyonCASandChinese auditing standards (WorldBank, 2009). Theuniversity-level education in China has not yet significantly encompassed IFRS content to provideenough accounting professionals skilled in applying IFRS. Thus, the training burden willlargelyfallontheindividualChineseenterprisesiftheMOFadoptsIFRS.

Actually,theMOFhasacknowledgedtheshortageofskilledIFRSusersasoneoftheurgent issues concerning IFRS implementation in China. In order to develop humanresources to address the challenge of the global convergence of financial reporting, theMOF launched a 10-year plan in 2005, called ‘Leading Accounting Talent Project’(lingjunrencaipeiyangguihua),andtrained1,327leadingaccountingtalentswhocanapplybothCASandIFRS(MOF,2016b).Candidatesforthisprojecthavebeenselectedfrombothpublic and private sectors, such as large companies, regulatory agencies, CPAs, andaccountingacademics(MOF,2007).TheMOF, in2016,establishedthenext10-yearplan,intendingtoincreasethenumberoftraineesinthisprojecttoover12,000until2020,andover17,000until2025 (MOF,2016a). Indevelopinghighquality trainingandeducationalprograms, the MOF has provided funds and played a leading role. The MOF also hascollaborated with three National Accounting Institutes (NAIs),6 the Chinese Institute ofCertified Public Accountants (CICPA),7 and the Accounting Society of China (ASC).8

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

75

Furthermore, in order to implement the next 10-year plan, the MOF have to seek thecooperation of universities, nationalministries, large companies, local governments, andaccountingfirms(MOF,2016a).

Although the national talent training programs contribute to an increase in thenumberofskilledIFRSspecialists,theamountoftraineesislimited,andcanonlymeetthehuman resources needs of a small cadre of Chinese enterprises, such as internationallyorientedcompanies (Wang,2012).TheMOFshowed its intention“toadvancetheuseofIFRSwithinChinaandother related issues,especially for those internationallyorientatedChinesecompanies”(MOFandIFRSFoundation,2015)inthe2015BeijingJointStatement.ThisintentionisconsistentwiththecontemporaryprofessionalinfrastructureinChina.ItiscanbeexpectedthattheMOF’sdecisionconcerningtheadoptionof IFRS inChinawouldbe cautious, in order to keep the accounting system compatible with the professionalinfrastructure.

SUMMARYANDCONCLUSIONS

This paper clarified several factors that may prove to be challenges in the directadoptionof IFRS inChina, includingtheendorsementprocess, the interpretationsof IFRSby theMOFandChineseaccountingprofessionals, thecostsof IFRS implementation, thetranslation of IFRS into Mandarin Chinese, and the IFRS-related training and education.ThesefactorsarerelatedwiththeChinese-specificinstitutionalarrangementssurroundingaccounting,suchasthepoliticalsystem,taxation,andprofessionalenvironment.

Even if theMOFdirectlyadopts IFRS, theendorsementprocessmaycreate“IFRSasendorsedbytheMOF”withmodificationsandexclusionsofIFRStoaccommodateChineseinterests.Additionally,thetimelagbetweenthereleaseofastandardbytheIASBanditsendorsement by the MOF is likely to hinder the comparability of financial reportingbetweenChineseenterprisesandfirmsinotherIFRS-adoptingcountries.

Findings of this paper suggest that Chinese accounting professionals may faceproblemsinconsistentlyinterpretingandapplyingIFRSiftheMOFdirectlyadoptsIFRS.TheMOF is likely to provide interpretations and guidance to facilitate the consistentimplementation of IFRS in China. However, precise guidance by the MOF may affectaccounting professionals’ independent judgments, and lead to different accountingtreatments for the same transactions and economic events in Chinese enterprisescomparedtothoseinotherIFRS-applyingenterprises.Thus,directIFRSadoptionmaynotnecessarily lead to an improvement in the comparability of financial reporting acrosscountries.

The direct adoption of IFRS is expected to cause high implementation costs forChinese enterprises. The costs would be prompted by the need to recruit accountantsqualifiedatapplyingIFRSorre-trainexitingaccountantswithIFRS-relatedknowledgeandskills.Additionally,thedirectadoptionofIFRSwouldlargelyincreasetheenforcementandregulation costs of regulators, such as theMOFand theCSRC. Themain costs that havebeen identified by this paper are led by establishing interpretations and preciseimplementationguidanceforprinciples-basedaccountingstandards,updatingtheofficials’professionalknowledge,andpreventingopportunisticapplicationsofaccountingstandardsthatgivemorediscretiontomanagers.Furthermore,asmostChinesedomesticaccountingfirms have no experience in auditing financial statements prepared in accordance withIFRS,theyneedtodevotegreatfinancialresourcestofosterIFRS-specificcapabilities,suchastrainingCPAsanddevelopingproceduremanuals.

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

76

The proper translation of IFRS from English to Mandarin Chinese would also be achallengeforthedirectadoptionof IFRS inChina.This isbecausethewords inMandarinChinese used to translate the concepts in IFRS may have been already applied in theChinese context and defined differently from the original meanings in IFRS. ImpropertranslationmayleadtoinappropriateinterpretationsandapplicationsofIFRS.

TheIFRS-relatedtrainingandeducationwouldposeanotherchallenge.AlthoughtheMOFconductedtrainingprogramstofosterChineseaccountingprofessionals’competenceinapplyingIFRS,thetraineesintheseprogramshavebeenlimitedtoasmallcadreofelites.InordertoenlargethesupplyofqualifiedaccountantsandauditorstoapplyIFRS,theMOFshouldseekthecooperationofvariousorganizations,suchasuniversities,largecompanies,andaccountingfirms.

This paper clarifiedChinese institutions’ constraints on the implementationof IFRS.Findingsof thispaper showed that IFRS couldbe incompatiblewith the currentpolitical,professional,andsocietalenvironmentsinChina.Theincompatibilitycouldbringpracticalproblems,suchastheinconsistentinterpretationsofIFRSandimpropertranslationofIFRSfrom English to Mandarin Chinese. Moreover, the incompatibility might produceunintended consequences in China, such as opportunistic applications of accountingstandards. Certain adjustments to Chinese-specific institutions should bemade to adaptthemtoIFRSimplementation.TheseadjustmentswouldbringsignificantcoststoChinesestakeholders,includingenterprises,regulators,andaccountingfirms.

Findings of this paper have important application for the IASB, which has beenpromotingtheglobaladoption(eithermandatoryorvoluntary)ofIFRS.Giventhecomplexinteractionsbetweenaccountingand surrounding institutions, inorder toachieve thedefacto global convergence of financial reporting, the IASB should extend discussionsconcerningtheconvergenceoffinancialreportingfromsimpleaccountingissuestoamoreholisticperspective, including institutionaldiversity surrounding the financial reporting inindividual countries,andhowto improve theadaptabilityofnational-specific contexts toIFRS.

ACKNOWLEDGEMENT

The author would like to appreciate the supports from the Mishima Kaiun MemorialFoundation, the Fuji Xerox Corporation Kobayashi Foundation, and the Murata ScienceFoundation.

ENDNOTES

1.Thedirectadoptionof IFRS in thispaper indicates that:applying IFRSas issuedby theIASB without modifications, or applying IFRS as endorsed by regional or nationalregulators(e.g.theEuropeanCommission)withpotentialdeletionsormodifications(e.g.the“carve-out”fromIAS39FinancialInstrumentsbytheEU).

2.Thesecondarysector,suchasminingandmanufacturing industries,contributed largelyto ChineseGDP. For example, 42.7 percent of ChineseGDP in FY 2014 came from thesecondarysector(NationalBureauofStatisticsofChina,2015).

3.TheamountoffundsraisedinChinesedomesticcapitalmarketsthroughdirectfinancingreachedapeakof10,190.93millionRMBin2010.Thisamountonlyaccountedfor12.8percentofbankloansinthesameyear(CSRC,2013).

4.ThenumberofCPAsperonemillioninChinaisapproximately159(215,091/1,350mil.),while in theUnited States, it is 1,087 (342,490/315mil.),meaning thatChinaonlyhas

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

77

one-seventh the number of CPAs per one million as the United States. Importantly,according to the regulations of the MOF and the CSRC, less than 0.5 percent ofaccountingfirms(40of8,350),andconsequently,onlyabout11percentofCPAs(about24,146of213,376)inChinaareeligibletoauditlistedcompanies(Miao,2016,p.152).

5.InJanuary,2016,theIASBissuedIFRS16LeasestoreplaceIAS17Leases.IFRS16Leasesalsoadoptedprobabilityexpressionsof“majorpart”and“substantiallyall”toprescribethe criteria for the classification of a lease as operating or capital lease (IASB, 2016c,para.63).

6. ThreeNAIswere established in the early 2000s in Beijing, Shanghai, and Xiamen. TheNAIs are government-funded institutes to provide accounting-centered trainings toChineseaccountingprofessionals.

7. The CICPA is a self-regulatory organization of Chinese CPAs. The CICPA is under theguidanceoftheMOFandtheStateCouncil.

8.TheASCisaself-regulatoryorganizationofChineseaccountingacademics,andisundertheguidanceoftheMOF.

REFERENCES

Agoglia, C.P.,Doupnik, T.S.,&Tsakumis,G.T. (2011). Principles-Based versusRules-basedAccountingStandards:The InfluenceofStandardPrecisionandAuditCommitteeStrengthonFinancialReportingDecisions.TheAccountingReview,86(3),747-767.

Aoki,M. (2001).TowaredsAComparative InstitutionalAnalysis. Cambridge,MA,US: TheMITPress.

Baker, C.R., Biondi, Y., & Zhang, Q. (2010). Disharmony in International AccountingStandardsSetting:TheChineseApproachtoAccountingforBusinessCombinations.CriticalPerspectiveonAccounting,21(2),107-117.

Biondi, Y. and Zhang, Q. (2007). Accounting for the Chinese Context: A ComparativeAnalysisof InternationalandChineseAccountingStandardsFocusingonBusinessCombinations.Socio-EconomicReview,5(4),695-724.

Brüggemann,U.,Hitz,J.,&Sellhorn,T.(2013).IntendedandUnintendedConsequencesofMandatoryIFRSAdoption:AReviewofExtantEvidenceandSuggestionsforFutureResearch.EuropeanAccountingReview,22(1),1-37.

Camfferman, K., & Zeff, S.A. (2015). Aiming for Global Accounting Standards: theInternationalAccounting StandardsBoard, 2001-2011.Oxford:OxfordUniversityPress.

Chand,P.(2005).ImpetustotheSuccessofHarmonization:theCaseofSouthPacificIslandNations.CriticalPerspectivesonAccounting,16,209-226.

Chand,P.(2012).TheEffectsofEthicCultureandOrganizationalCultureonJudgmentsofAccountants. Advances in Accounting, incorporating Advances in InternationalAccounting,28(2),298-306.

Chand, P., Cummings, L., and Patel, C. (2012). The Effect of Accounting Education andNationalCultureonAccounting Judgments:AComparative StudyofAnglo-CelticandChineseCulture.EuropeanAccountingReview,21(1),153-182.

Chand, P., Patel, C., & Patel, A. (2010). Interpretation and Application of “new” and“complex” International Financial Reporting Standards in Fiji: Implications forConvergence of Accounting Standards. Advances in Accounting, incorporatingAdvancesinInternationalAccounting,26(2),280-289.

Chen, Y. (2015). Devote Great Effort to Promote the Competence of Accounting

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

78

Professionals(thekeynotespeechatthe2015AnnualSummitoftheAssociationofCharteredCertifiedAccountants (ACCA)onMay21,2005,Beijing,China).TheChineseCertifiedPublicAccountant,7,5-6.(inChinese)

ChinaAccountingStandardsCommittee:CASC(2013).InternationalAccountingStandard1:PresentationofFinancial Statements (English-Chinese).Beijing:ChinaFinancial&EconomicPublishingHouse.

China Accounting Standards Committee and International Accounting Standards Board:CASC and IASB (2005). Joint Statement of the Secretary-general of the ChinaAccounting standards Committee and the Chairman of the InternationalAccounting Standards Board. Retrieved on June 30, 2016, fromhttp://www.ifrs.org/Alerts/PressRelease/Documents/2015/2005%20Beijing%20Statement.pdf

China Securities Regulatory Commission: CSRC (2008). Supervision Report on theImplementation of Accounting Standards for Business Enterprises in ListedCompanies(2007).FinanceandAccountingforInternationalCommerce,12,5-14.(inChinese)

China Securities Regulatory Commission: CSRC (2013). China Securities and FuturesStatisticalYearbook2012,Shanghai:XuelinPublishingHouse.(inChinese)

China Securities Regulatory Commission: CSRC (2014). Analysis of Auditing of ListedCompanies’ FY2013 Annual Reports. Retrieved on June 30, 2016, fromhttp://www.csrc.gov.cn/pub/newsite/kjb/gzdt/201505/t20150513_276779.html(inChinese)

Cooper,D.J.&Morgan,W.(2008).CaseStudyResearchinAccounting.AccountingHorizons,22(2),159-178.

Dai, D., Zhang, Y., & He, Y. (2005). Research on the Coordination between AccountingRegulationandTaxLawsinChina.AccountingResearch,1,50-54.(inChinese)

Doupnik, T.S., & Perera, H. (2012). International Accounting (Third Edition). New York:McGraw-Hill/Irwion.

Doupnik, T.S., & Riccio, E.L. (2006). The Influence of Conservatism and Secrecy on theInterpretation of Verbal Probability Expressions in the Anglo and Latin CulturalAreas.TheInternationalJournalofAccounting,41,237-261.

Doupnik, T.S. & Richter, M. (2003). Interpretation of Uncertainty Expressions: A Cross-nationalStudy.Accounting,OrganizationandSociety,28(1),15-35.

Doupnik, T.S. & Richter, M. (2004). The Impact of Culture on the Interpretation of “incontext” Verbal Probability Expressions. Journal of International AccountingResearch,3(1),1-20.

Evans, L. (2004). Language, Translation and the Problem of International AccountingCommunication.Accounting,AuditingandAccountabilityJournal,17(2),210-248.

Ezzamel,M., Xiao, J.Z., & Pan, A. (2007). Political Ideology and Accounting Regulation inChina.Accounting,OrganizationsandSociety,32(7-8),669-700.

Feng, S. (2001). The Issue Concerning the Internationalization of Chinese AccountingStandards.AccountingResearch,11,3-8.(inChinese)

FinancialServiceAgency:FSA(2012).InvestigationReportonAsian(China)ConcerningIFRS.(inJapanese)

Guerreiro,M.,Rodrigues,L.,&Craig,R.(2008).ThePreparednessofCompaniestoAdoptInternational Financial Reporting Standards: Portuguese Evidence. AccountingForum,32,75-88.

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

79

Hail, L., Leuz,C.,&Wysocki,P. (2010).GlobalAccountingConvergenceand thePotentialAdoption of IFRS by the U.S. (Part I): Conceptual Underpinning and EconomicAnalysis.AccountingHorizons,24(3),355-394.

Hellmann, A., Perera, H., & Patel, C. (2010). Contextual issues of the Convergence ofInternational Financial Reporting Standards: The Case of Germany. Advances inAccounting,IncorporatingAdvancesinInternationalAccounting,26(1),108-116.

Hofstede, G. & Bond, M.H. (1988). The Confucius Connection: From Cultural Roots toEconomicGrowth.OrganizationalDynamics,16(4),5-21.

Hoogervorst,H.(2011).SpeechbyHansHoogervorstonJuly29,2011inBeijing.RetrievedonJanuary25,2016,fromhttp://www.ifrs.org/News/Announcements-and-Speeches/Pages/Hans-Hoogervorst-Beijing-speech-July-2011.aspx

Institute of CharteredAccountants of Scotland: ICAS (2010).ChineseAccounting Reform:TowardsAPrinciples-basedGlobalRegime.RetrievedonJanuary25,2016,fromhttp://icas.org.uk/home/technical-and-research/technical-information-and-guidance/financial-reporting/chinese-accounting-reform-towards-a-principles-based-global-regime/

International Accounting Standards Board: IASB (2006). China Affirms Commitment toConverge with IFRS. Retrieved on January 25, 2016, fromhttp://www.ifrs.org/News/Announcements-and-Speeches/Pages/China-affirms-commitment-to-converge-with-IFRSs.aspx

International Accounting Standards Board: IASB (2015a).China to Explore FurtherUse ofIFRS. Retrieved on November 27, 2016, fromhttp://www.ifrs.org/Alerts/PressRelease/Pages/China-to-explore-further-use-of-IFRS.aspx

InternationalAccountingStandardsBoard:IASB(2015b).SummaryoftheIFRSFoundationTrustees’Meeting(October2015,Beijing).RetrievedonNovember26,2016,fromhttp://www.ifrs.org/About-us/IFRS-Foundation/ Oversight/Trustees/Trustee-meetings/Documents/20151015-SummaryTrusteesmeeting.pdf

International Accounting Standards Board: IASB (2016a). IAS 1: Presentation of FinancialStatement. Retrieved on July 21, 2016, fromhttp://www.ifrs.org/IFRSs/Pages/IFRS.aspx

International Accounting Standards Board: IASB (2016b). IAS 33: Earnings per Share.RetrievedonJuly21,2016,fromhttp://www.ifrs.org/IFRSs/Pages/IFRS.aspx

International Accounting Standards Board: IASB (2016c). IFRS 16: Leases. Retrieved onNovember27,2016,fromhttp://www.ifrs.org/IFRSs/Pages/IFRS.aspx

Irvine, H. (2008). The Global Institutionalization of Financial Reporting: The Case of theUnitedArabEmirates.AccountingForum,32,125-142.

Jia, W. (2010). Understanding on Accounting Standard for Financial Instruments andConvergenceofAccountingStandards.FinanciaAccounting,10,6-13.(inChinese)

Li,X.(2011).TheDevelopmentofInternationalAccountingStandardsandItsInfluenceonFinancialSupervisioninChinainthePostFinancialCrisisEra.FinancialAccounting,7,13-14.(inChinese)

Li, Y. (2011). Researchon theEstablishingOrientation forChineseAccounting Standards.JournalofBeijingTechnologyandBusinessUniversity(SocialScience),26(3),1-6.

Liu, Y. (2006). The Process of the Establishment of Chinese Accounting Standards.

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

80

Presentationatthe6thChina-Japan-KoreaAccountingStandardsSetters'Meetingheld inSeoul,KoreaonAugust30,2006.RetrievedonNovember27,2016,fromhttp://kjs.mof.gov.cn/zhengwuxinxi/lingdaojianghua/200807/t20080709_56580.html

Liu, Y. (2007). Establishment, Convergence and Equivalence of Chinese AccountingStandardsforBusinessEnterprises.AccountingResearch,3,2-8.(inChinese)

Liu, Y. (2011). The Influence of Major Revisions of the International Financial ReportingPrinciplesonChinaafter theFinancialCrisis.Finance&Accounting,12, 8-12. (inChinese)

Miao,X.(2016). IssuesAffectingConvergenceofNationalAccountingStandardswithIFRSinaTransitionalCountry:TheCaseofChina.AcademyofAccountingandFinancialStudiesJournal,20(2),142-165.

MinistryofFinanceofChina:MOF (2006).AccountingStandards forBusinessEnterprises:Specific Standards. Retrieved on June 6, 2016, fromhttp://www.casplus.com/rules/rules.asp(inChinese)

Ministry of Financeof China:MOF (2007).TheNotice by theMOFabout the Issuance of“10-YearPlanforLeadingAccountingTalentProject.”RetrievedonJune6,2016,fromwww.cicpa.org.cn/news/newsaffix/8417_20075303417_1.doc(inChinese)

Ministry of Finance of China: MOF (2009). Analytical Report on the ImplementationSituation of the Accounting Standards for Business Enterprises in China's ListedCompanies in 2008. Retrieved on June 6, 2016, fromhttp://kjs.mof.gov.cn/zhengwuxinxi/diaochayananjiu/200908/t20090803_189997.html(inChinese)

MinistryofFinanceofChina:MOF(2016a).PlanforNationwideLeadingAccountingTalentProject (Exposure Draft). Retrieved on June 6, 2016, fromhttp://kjs.mof.gov.cn/zhengwuxinxi/gongzuotongzhi/201604/t20160407_1940265.html(inChinese)

Ministry of Finance of China: MOF (2016b). Explanation for the Revision of “Plan forNationwideLeadingAccountingTalentProject(ExposureDraft).RetrievedonJune6,2016,fromhttp://kjs.mof.gov.cn/zhengwuxinxi/gongzuotongzhi/201604/t20160407_1940265.html(inChinese)

Ministry of Finance of China and IFRS Foundation: MOF and IFRS Foundation (2015).Ministry of Finance of China and IFRS Foundation Joint Statement. Signed onNovember 18,2015 in Beijing. Retrieved on April 23, 2016, fromhttp://kjs.mof.gov.cn/zhengwuxinxi/gongzuodongtai/201511/t20151120_1574639.html

Mısırlıoğlu, İ., Tucker, J., & Yükseltürk, O. (2013). Does Mandatory Adoption of IFRSGuaranteeCompliance?TheInternationalJournalofAccounting,48,327-363.

Muller,K.,Riedl,E.,&Selhorn,T. (2008).ConsequencesofVoluntaryandMandatoryFairValue Accounting: Evidence Surrounding IFRS Adoption in the EU Real EstateIndustry.HarvardBusinessSchoolWorkingPaper.

NationalBureauofStatisticsofChina(2015).ChinaStatisticalYearbook2015.RetrievedonJanuary 25, 2016, from http://www.stats.gov.cn/tjsj/ndsj/2015/indexch.htm (inChinese)

NationalPeople’sCongressofChina(1999).TheAccountingLawofthePeople’sRepublicofChina.(inChinese)

AsiaPacificBusiness&EconomicsPerspectives,Summer2017,5(1).

81

NationalPeople’sCongressofChina(2007).TheEnterpriseIncomeTaxLawofthePeople’sRepublicofChina.(inChinese)

Nobes,C.,&Parker,R.(2016).ComparativeInternationalAccounting(13thEdition).Harlow:PearsonEducationLimited.

Pan,P.,Patel,C.,&Mala,R. (2015).Questioning theUncriticalApplicationofTranslationandBack-TranslationMethodologyinAccounting:EvidencefromChina.CorporateOwnershipofControl,12(4),480-492.

Peng, S., & Bewley, K. (2010). Adaptability to Fair Value Accounting in An EmergingEconomy: A Case Study of China’s IFRS Convergence. Accounting, Auditing &AccountabilityJournal,23(8),982-1011.

Perera, H., Cummings, L., & Chua, F. (2012). Cultural Relativity of AccountingProfessionalism:EvidencefromNewZealandandSamoa.AdvancesinAccounting,IncorporatingAdvancesinInternationalAccounting,28,138-146.

Phan,D.(2014).WhatFactorsarePerceivedtoInfluenceConsiderationofIFRSAdoptionbyVietnamese Policymakers? Contemporary Issues in Business and Government,20(1),27-40.

Song,J.(2013).SeparationandCoordinationbetweenAccountingandTaxationRegardingFairValue:AnAnalysisBasedonAccountingStandardforFairValueMeasurement(ExposureDraft).TaxationResearch,10,83-86.(inChinese)

Stadler, C.,&Nobes, C. (2014). The Influenceof Country, Industry, and Topic Factors onIFRSPolicyChoice.Abacus,50(4),386-421.

Wang, J. (2006). Issues about Accounting Reform and Development. Presented to theFourth Meeting of the Third Council of the China Association of Chief FinancialOfficers,Yichang,China.(inChinese)

Wang, J. (2009).Make Concerted Efforts to Begin aNewChapter in the Convergence ofAccounting Standards (the presentation in the 3rd 2009 IFRS Advisory CouncilmeetingonNovember12,2009).AccountingResearch,12,3-4.(inChinese)

Wang, J. (2012). Continue Emancipating the Mind, Insist on Scientific Development,Achieve the Movement from A Big Country to A Powerful Country concerningAccounting (the speech at theNationalAccountingManagementConferenceonFebruary14,2012).AccountingResearch,3,3-14.(inChinese)

WorldBank(2009).ReportontheObservanceofStandardsandCodes(ROSC)-AccountingandAuditing:People’sRepublicofChina.

Yang,M.,Lu,J.,&Xu,H.(2011).TheCurrentSituationoftheInternationalConvergenceofAccountingStandardsandChina’sStrategyforConvergencewithIFRS.AccountingResearch,10,9-15.(inChinese)