challenges and opportunities for the eu beet growers · challenges and opportunities for the eu...

TRANSCRIPT

CHALLENGES AND OPPORTUNITIES

FOR THE EU BEET GROWERS

By Roland CUNI

Deputy General Manager Sugarbeet growers’association

Challenges and opportunities for the EU beet growers

Great future for all arable crops in the EU.

Sugar beet has a great potential in the EU.

Beet farmers have the choice to switch to others crops if beet profitability is too low.

Therefore more opportunities than challenges for beet growers.

Post 2016-2017 market analysis

necessary to analyse

opportunities for beet growers

Post 2016-2017 EU beet sugar production

Most sugar companies target higher production by increasing campaign duration, without investments:

o Current sugar production = 17 Mt sugar.eq

o Post 2016-2017 production = 18 - 19 Mt • + 15% in France • Increase in Poland, Germany, Belgium,… • Possible decrease in southern EU • + 5-10% in the EU

Target achievement will depend on sugar prices.

Tough competition between EU sugar companies.

Post 2016-2017 EU sugar consumption

Isoglucose companies target higher production, which need investments.

Sugar / isoglucose tough competition.

Isoglucose target achievement will depend on sugar prices.

Whatever EU sugar price, EU sugar consumption will decrease, by 0,5 to 2,5 Mt.

Post 2016-2017 EU sugar imports

Competition beet sugar producers / refiners.

EU markets less attractive for ACPs / LDCs.

Further tariff quotas through FTA (Canada, Mercosur ?, Georgia ?, Thailand ?) and preferential access (Ukraine).

Imports will depend on the gap between EU and world sugar prices.

Few countries worldwide are both importer and exporter.

Consequences on EU sugar prices

Reduced gap between EU and world prices.

« Invisible hand of the market » to find appropriate EU price to balance:

isoglucose expansion beet sugar expansion imports and refining

± ? €/t white ex factory ?

↗ sugar production

↘ sugar consumption

↗ exports on world market: 1 to 3 Mt

↘ EU sugar prices

EU sugar competitiveness on the world market Production Costs

Brazil: 2013/14 raw, fob

Thailand: 2013/14 raw, fob

France: 2013/14 raw equivalent, fob

Exchange rate US$/BRL Production Cost

Mars 2013 1,98 19,0 cts/lb

Octobre 2013 2,19 17,2 cts/lb

Mars 2014 2,34 16,1 cts/lb

Exchange rate US$/Baht Production Cost

Mars 2013 29,5 18 cts/lb

Octobre 2013 31,2 17 cts/lb

Mars 2014 32,4 16,4 cts/lb

Exchange rate €/US$ Production Cost

Mars 2013 1,30 19,5 cts/lb

Mars 2014 1,38 21,0 cts/lb

EU sugar Production Costs

No very significative differences in sugar production

costs, delivered, between UK, France, Belgium,

Netherland, Germany, Poland?

Some countries are more competitive in beet (F) and others more competitive in process (UK).

Some countries (Germany) are closer to main markets than others (F).

Beet supply by growers

Will beet growers produce more?

Beet growers can produce much more, but… beet growers can switch to many others crops whereas sugar producers cannot switch to another product.

Beet growers decisions will depend on: beet prices, alternative crops prices, quality and transparency of contractual

relationship with sugar companies.

Sugar producers enter a new paradigm in which beet supply may be at risk.

If beet prices required by growers are to high for

sugar producers to make profit because of too low

sugar prices sugar production to be adjusted.

Some sugar producers will calculate the profitability

of marginal production on a marginal cost basis and

others on a average cost basis, depending on their

strategy.

Will beet growers produce more?

Beet prices versus Sugar prices under the current sugar regime

Quota (food usages)

26,29 €/t minimum price ± equivalent to 404 €/t reference price.

If market price > 404 €/t beet price > 26,29 €/t according to pricing mechanism based on a win/win approach.

Out of quota (non food usages + world market)

Beet prices depend on world sugar prices and/or grower price requirements.

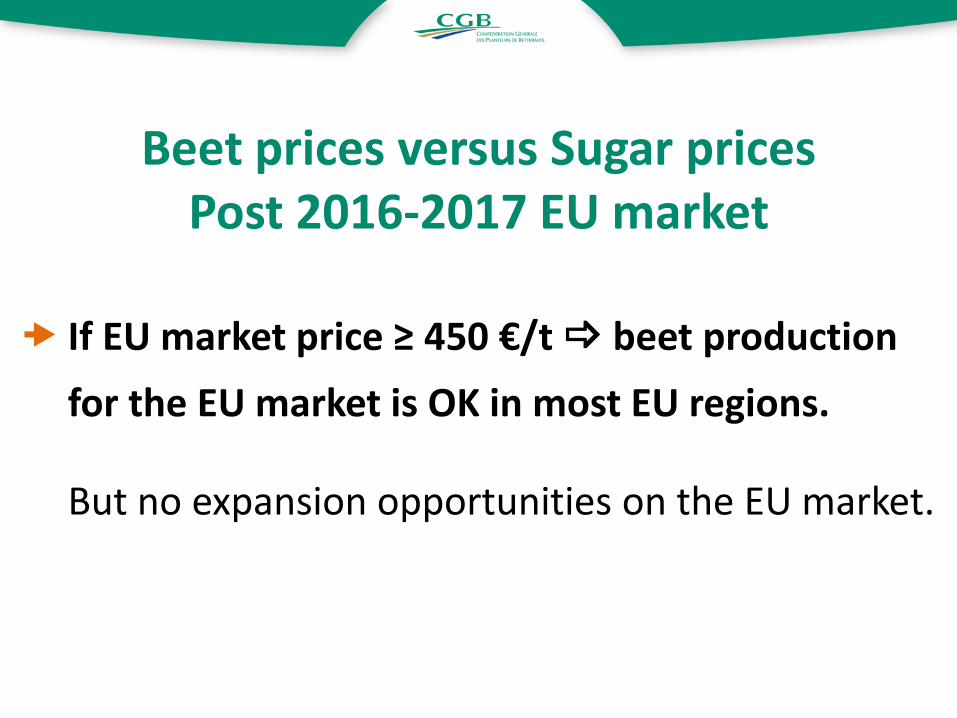

Beet prices versus Sugar prices

Post 2016-2017 EU market

If EU market price ≥ 450 €/t beet production

for the EU market is OK in most EU regions.

But no expansion opportunities on the EU market.

Beet prices versus Sugar prices Post 2016-2017 world market

If world raw sugar price > 20 cts/lb beet expansion opportunities.

If world raw sugar price ≤ 20 cts/lb beet supply for export on the world market not sustainable without a strong reduction in costs.

20 cts is the upper range of average world market prices, based on current brazilian costs of production and US$/BRL exchange rates.

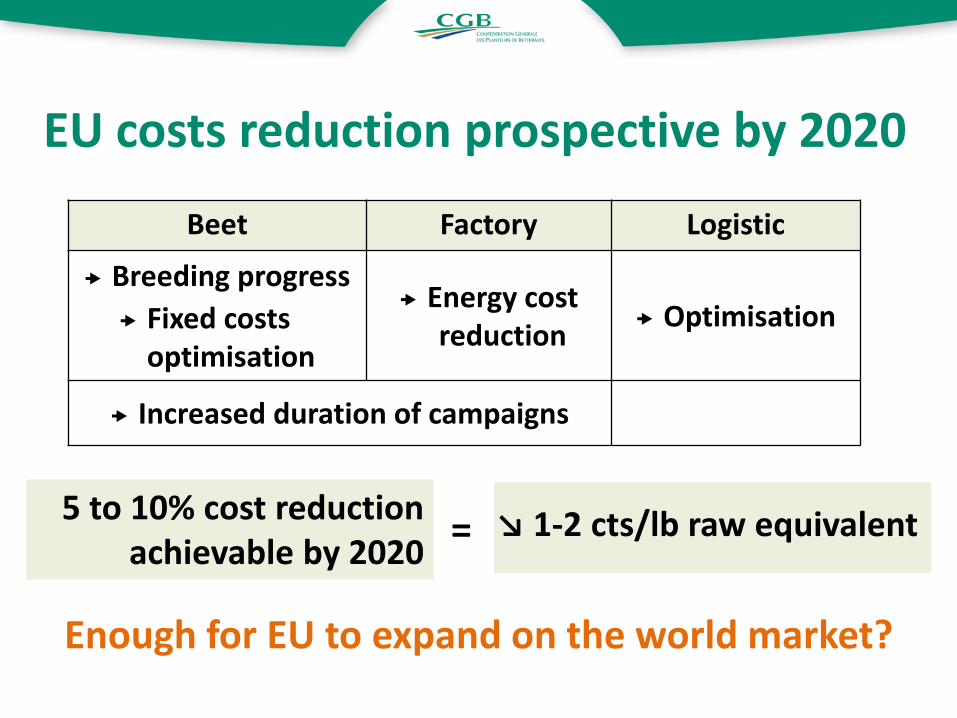

EU costs reduction prospective by 2020

Beet Factory Logistic

Breeding progress

Fixed costs optimisation

Energy cost reduction

Optimisation

Increased duration of campaigns

Enough for EU to expand on the world market?

5 to 10% cost reduction achievable by 2020

↘ 1-2 cts/lb raw equivalent =

Challenges and opportunities for the EU beet growers

Beet growers can increase production provided it is

profitable.

Too low beet profitability to export on the world

market with current competitiveness at world

prices < 20 cts/lb.

EU competitiveness to improve, which is possible.

Beet growers confident for the future

of arable crops including sugar beet.

Challenges and opportunities for the EU beet growers