certified customs specialist (ccs) · of cbp form 3461 or cbp form 7533 (inward cargo manifest for...

TRANSCRIPT

CERTIFIED CUSTOMS SPECIALIST (CCS)

COURSE MATERIALS

Module 12

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 2 of 23

Module 12: Entry Summary and Assessment of Duties The entry process can be broken down into steps that may be taken simultaneously or separately. The first is the filing of entry for release of goods. Second is the follow‐up Entry Summary within 10 working days of the release.

List of Lessons:

• Lesson 1: Entry Summary • Lesson 2: Assessment of Duties • Lesson 3: Discrepancies (Overages and Shortages) • Lesson 4: Travelers and Their Goods • Lesson 5: Instruments of International Traffic • Lesson 6: Check Digit Computation Formula • Lesson 7: Rules for Constructing the Manufacturer Identification Code (MID)

Lesson 1: Entry Summary

Topic 1: Entry Summary Documentation

Entry summary documentation consists of the entry summary (CBP Form 7501) and other documents (i.e. commercial invoice, packing list, evidence of right to make entry) necessary to assess duties, collect statistics and determine that all import requirements have been fulfilled. Use of the Automated Broker Interface (ABI) can reduce or eliminate some of these paper documentation requirements. Depending on the payment option employed, the entry summary may also include estimated duties to be paid.

The CBP Form 7501 (Entry Summary) is used by CBP to collect duties, taxes and fees on imported merchandise, to record statistical data on imports, and to provide a concise summary of the import transaction by classification and value. Generally, imported merchandise is released via CBP 3461 (Entry/Immediate Delivery) and the entry summary document follows. The entry summary must be presented to CBP within 10 working days of the release of the goods, along with the entry package. The entry package consists of a copy of the CBP Form 3461 (if used), an invoice which includes country of origin of the merchandise, the U.S. classification for the merchandise along with other information (ref: 19 CFR 141.86) on the shipment being imported, packing list, copy of the bill of lading or air waybill, and other pertinent documents based on the type of merchandise and any Government Agencies which have set forth import requirements for the merchandise being imported.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 3 of 23

Periodic Monthly Statement (PMS) was introduced in June, 2004 offering the ability to pay for shipments released during the previous calendar month by the 15th business day of the following month. Otherwise, duties and fees must be paid on a single pay transaction‐by-transaction basis or consolidated on a statement paid daily.

Topic 2: Entry Summary Scenarios

When the entry documentation for release (usually a CBP Form 3461) is filed before the entry summary documentation, the same commercial documents may be used in preparing the entry summary, CBP Form 7501, and should be filed with the entry summary documentation within the time period stated 19 CFR 142.12(b). The entry summary documentation shall also include any other required documents unless a bond for missing documents is on file.

When the entry summary documentation is filed at time of entry for release (ref: 19 CFR 142.13), the required commercial documents shall be filed at the same time, with the exception of CBP Form 3461 or CBP Form 7533 (Inward Cargo Manifest For Vessel Under Five Tons, Ferry, Train, Car, Vehicle, etc.) which is not required. The importer also shall file any additional invoice required for a particular shipment. The filing of the CBP Form 7501 as the entry release document is called an Entry/Entry summary.

Merchandise, for which an entry summary serves as both an entry and an entry summary, will not be released by CBP until a bond has been filed, or the entry has been liquidated - liquidation means that the entry has been “closed out” by CBP, as follows:

a) Merchandise not designated for examination may be released to, or upon the order of, the carrier if a bond is filed on CBP Form 301 containing the bond conditions set forth in 19 CFR 113.62. Merchandise designated for examination may be released under the bond after examination has been completed if:

1. It has been found to be truly and correctly invoiced 2. It is entitled to admission into the commerce of the United States 3. Its release is not precluded by any law or regulation.

If merchandise is entered by or on behalf of a United States Government department or agency, the stipulation prescribed in 19 CFR 141.102(d), shall be accepted in place of a bond.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 4 of 23

b) After entry - If a bond has not been filed in accordance with paragraph (a), the merchandise shall not be released before:

1. The entry has been liquidated and the full amount of all duties and taxes due,

including dumping or other special duties and charges, has been paid, or the right to free entry established;

2. The port director determines that the merchandise may be admitted into the commerce of the United States; and

3. All documents relating to the merchandise which are required by law or regulations have been filed.

When filing one entry summary for multiple entries for split arrivals of one shipment, the following applies:

a) Except as provided in paragraph 19 CFR 142.17(b), the port director may permit the filing of one entry summary for merchandise the subject of separate entries if:

1. The merchandise has the same country of exportation, and the same country of

origin; 2. The merchandise arrives by land, by the same vessel or by the same air carrier, 3. The merchandise is consigned to the same consignee; 4. The time between the date of the first entry and the date of the last entry does

not exceed 1 week; 5. The entry summary document is filed within 10 working days from the date of

the first entry; and 6. Each entry is identified separately by entry number on the entry summary.

b) One entry summary shall not be used for multiple entries of the following:

1. Quota-class merchandise; 2. Prohibited merchandise; 3. Merchandise subject to restrictions which require processing and documentation

more frequently than on a weekly basis; 4. Merchandise for which liquidation has been withheld; and 5. Merchandise classifiable under the same Harmonized Tariff Schedule of the

United States (HTSUS) subheading number, to the eight-digit level having

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 5 of 23

different rates of duty for which entries or immediate transportation entries have been filed. However, this provision is not applicable in the following circumstances:

(i) Entries may be consolidated if the time of entry is: (A) Before the date of change in rate of duty, or (B) On or after the date of change in rate of duty.

(ii) Immediate transportation entries may be consolidated if the date of acceptance is:

(A) Before the date of change in the rate of duty, or (B) On or after the date of change in rate of duty.

If an entry summary covering multiple entries refers to entry documentation which is not in proper form, the entry summary and the entry documentation shall be returned for correction. If any merchandise released at time of entry is later found to be prohibited, the port director shall demand its return to Customs custody in accordance with 19 CFR 141.113, and an entry summary and the deposit of estimated duties, if any, shall not be required provided:

1. An entry for exportation, CBP Form 7512 (Transportation Entry and Manifest of

Goods Subject to Customs Inspection and Permit) or an application to destroy the merchandise using CBP Form 4613 under Customs supervision is made within 10 days after the time of entry, and the exportation or destruction is accomplished promptly, or

2. An entry for transportation and exportation, CBP Form 7512, is made within 10 days after the time of entry and domestic carriage of the merchandise does not conflict with the requirements of another Federal agency.

The exportation or destruction of prohibited or abandoned merchandise must be in accordance with 19 CFR 158.41 and 158.45(c), and 158.43

Topic 3: Failure to File Documentation on Time

If the applicable entry summary documentation set forth in 19 CFR 142.22(b) is not filed within the time provided in 19 CFR 142.23, the port director shall make an immediate demand for liquidated damages in the amount of the bond in the case of a single entry bond or when the

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 6 of 23

transaction has been charged against a continuous bond, the demand shall be for the amount that would have been demanded if the merchandise had been released under a single entry bond. Any application for cancellation of liquidated damages incurred shall be made in accordance with 19 CFR 172.2.

Lesson 2: Assessment of Duties

Topic 1: Liability for Duties

The liability for the payment of duties for goods imported into the United States is activated by the arrival of goods into the territory of the United States. These duties represent a debt of the importer that can only be discharged when the duties are paid in full. Payment of duties to a customs broker does not relieve the importer of liability if the duties are not paid by the customs broker to CBP. The liability to pay duties also includes the liability to pay any internal revenue taxes associated with the importation of goods.

In situations where the customs broker is the importer of record, the customs broker is responsible for the payment of duty. However, when acting as the importer of record, the customs broker may obtain relief from liability for potential increased or additional duties that are found owing if a declaration naming the actual owner of the goods and an owner’s declaration, whereby the owner agrees to pay the additional duty, and the owner’s bond are filed by the broker with the port director within 90 days of the date of entry.

The claim of the Government for unpaid duties against the estate of a deceased or insolvent importer has priority over obligations to creditors other than the United States. The liability for duties also constitutes a lien upon the merchandise imported, which may be enforced while such merchandise is in the custody or subject to the control of the United States. If imported goods are entered into a warehouse, the liability for duties can be transferred to the party who purchases the goods while they are in the warehouse and then enters the goods under their own name.

The liability to pay taxes on imported goods does not apply to imported merchandise that was not ordered by the consignee. These goods, once refused by the consignee, are deemed to be unclaimed goods.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 7 of 23

Topic 2: Continuation of Liability

The liability to pay duties also applies to duty-paid imported goods that are exported and then re- entered into the United States with the following limited exceptions: a) Personal and household effects taken abroad by a resident of the United States and brought back on his return to this country; b) Professional books, implements, instruments, and tools of trade, occupation, or employment taken abroad by an individual and brought back on his return to this country; c) Automobiles and other vehicles taken abroad for noncommercial use; d) Metal boxes, casks, barrels, carboys, bags, quicksilver flasks or bottles, metal drums, or other substantial outer containers exported from the United States empty and returned as usual containers or coverings of merchandise, or exported filled with products of the United States and returned empty or as the usual containers or coverings of merchandise; e) Articles exported from the United States for repairs or alterations, which may be returned upon the payment of duty on the value of repairs or alterations at the rate or rates which would otherwise apply to the articles in their repaired or altered conditions; f) Articles exported for exhibition under certain conditions; g) Domestic animals taken abroad for temporary pasturage purposes and returned within 8 months; h) Articles exported under lease to a foreign manufacturer; or i) Any other re-imported articles for which free entry is specifically provided. The rate of duty applied to imported merchandise is the rate of duty that is applicable at time of entry. Once duty liability amounts have been estimated, they must be deposited with CBP at the time of filing the entry documentation or entry summary documentation when it serves as both entry and entry summary. This obligation to submit duty deposits does not apply in certain circumstances such as informal mail entries, warehouse entries, in bond entries, and appraisement entries. Payment of duty liability amounts can be by check per entry or on daily or monthly statements, which are available through CBP.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 8 of 23

There are a series of additional special situations where duty and/or tax deposits are not required:

a) Cigars and cigarettes - A qualified dealer or manufacturer may enter or withdraw for consumption cigars, cigarettes, and cigarette papers and tubes without payment of internal- revenue tax in accordance with 19 CFR 11.2(a). b) Bulk distilled spirits transferred to the bonded premises of a distilled spirits plant - An importer may transfer distilled spirits in bulk to the bonded premises of a distilled spirits plant, without the payment of tax, under the provisions of section 5232(a), Internal Revenue Code of 1986 (26 USC 5232(a)), and the regulations of the Bureau of Alcohol, Tobacco and Firearms (27 CFR 251). c) Deferral of payment of taxes on alcoholic beverages - An importer may pay on a semimonthly basis the estimated internal revenue taxes on all the alcoholic beverages entered or withdrawn for consumption during that period, under the procedures set forth in 19 CFR 24.4.

d) Government entries - If a shipment is entered or withdrawn for consumption by a U.S. Government department or agency, or an authorized representative thereof, no deposit of estimated customs duties or taxes shall be required if a stipulation is furnished in lieu of the bond. The proper department or agency will then be billed after liquidation of the entry for any duties or charges due.

The stipulation shall be in the following form:

I ________________ (title), a duly authorized representative of the (name of U.S. Government department or agency) stipulate and agree on behalf of such department or agency that all applicable provisions of the Tariff Act of 1930, as amended, and the regulations thereunder, and of all other laws and regulations, relating to _____________ (type of entry) entry No. ______, of ______ (date) will be observed and complied with in all respects.

(Signature) _______________________

In those instances where the port director is of the opinion that the goods are undervalued, and/or that the number or quantity of goods entered is greater than the volume declared, and the estimated increase of duty on an entry exceeds $15, CBP will issue Notice of Action (CBP Form 29) for additional duties. These additional duties also represent a liability on the part of the importer.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 9 of 23

The importer has 20 calendar days to reply to the Notice of Action (CBP Form 29) from issue date of the form, by tendering the additional duties requested or presenting evidence to justify the initial declaration and payment of duties.

When an examining officer finds goods that do not match the description given in the invoice, duties are assessed on the goods actually found. If there is no doubt that the discrepancy appears to be the result of a mistake and not of any intent to defraud, no proceedings for forfeiture shall be taken. When the entire shipment does not agree with the invoice and there is no evidence of any intent to defraud, a new entry shall be required and the estimated duty-paid on the original entry shall be refunded on liquidation as in the case of a non-importation.

Lesson 3: Discrepancies (Overages and Shortages)

A shortage is defined as the difference between the actual available or deliverable quantity of a good and the higher required quantity. An overage is when goods are found that have not been noted on the cargo manifest. The Manifest Discrepancy Report (MDR) in ACE is a record filed with an amendment code for the e-manifest according to the Frequently Asked Questions for Automated Commercial Environment dated July 2011.

All manifest discrepancies must be reported to CBP. Anyone may report a discrepancy. In ACE, the broker has the ability to do a “bill of lading update” to correct entry manifest quantities. The carrier can also amend the manifest to correct manifest quantities. The ultimate responsibility for the reporting of discrepancies rests with the importing carrier and with the party that last receipted for the full amount of merchandise listed on the manifest, in-bond or transfer document. An importing carrier who cannot show that landed imported merchandise was properly released from CBP custody may be liable for liquidated damages and payment of duty on that merchandise. A custodian of bonded merchandise who cannot account for merchandise in its custody may be liable for liquidated damages under his bond.

Discrepancies usually include changes to manifested quantities, but can include changes to other manifest information. A corrected manifest is not required where there are discrepancies between marks or numbers on a package and the marks or numbers shown on the manifest, when the quantity and description are correct. Except discrepancies in bulk petroleum or petroleum products exceeding one percent, a MDR will not be required when the port director is satisfied that the difference between the quantity of bulk merchandise listed on the manifest or bill of lading or air waybill, and the quantity unladen, is the usual difference caused by

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 10 of 23

absorption or loss of moisture, temperature, faulty weighing at the port of lading or other such reason. In all other cases, the time period for filing a MDR is 60 from date of entry or before liquidation 19 CFR 158 days for vessel, 30 days from Aircraft entry 19 CFR 122.49 (a)(2) for aircraft, and 60 days, from date of arrival 19 CFR 132 (b) for vehicle carrier.

The primary document comprising the MDR for importing carriers and express consignment carriers is the original manifest page or the electronic equivalent for automated carriers, or a newly prepared manifest page for merchandise omitted in total from the manifest. Other documents may be used as the MDR in lieu of a manifest page.

The MDR will be annotated at the top, “Manifest Discrepancy Report”. The MDR must also contain in close proximity to the original quantity or description the statement, “AMENDED (QUANTITY or DESCRIPTION) _________”. The filer must include a clear and concise statement as to the reason for the discrepancy and must include a signed statement of the owner/operator/agent or responsible party for the inward or bonded carrier or other entity preparing the MDR. The statement shown must read as follows:

"I declare that the information contained on this document is true and correct to the best of my knowledge and belief and that the discrepancy described herein occurred for the reason stated".

Also included should be a signature of a company representative, the company name, and date.

Bonded carriers may use a modified copy of the in-bond document (bill of lading, and air waybill) as the MDR. A copy of the MDR must be provided to the importing carrier for use in the correction of the Inward Foreign Manifest (IFM). Container Freight Stations (CFS) and Bonded Cartmen (CHL) may use a modified copy of the transfer document, cartage document, manifest, bill of lading, or air waybill as an MDR. A copy of the MDR must be provided to the importing carrier for use in the correction of the IFM.

Foreign Trade Zone (FTZ) proprietors may file MDRs on company letterhead or on an Application for Foreign Trade Zone Admission on CBP Form 214. A copy of the MDR must be provided to the importing carrier for use in the correction of the IFM.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 11 of 23

Importers/brokers/filers may file an MDR by letter to CBP. A copy of the MDR must be provided to the importing carrier for use in the correction of the IFM. Entries filed prior to the discovery of a discrepancy may be canceled or relieved from duty if a copy of the carrier’s MDR is attached to a copy of the letter to non-importation or non-delivery to the satisfaction of the port director.

All carriers, whether automated or not, including Express Courier Consignment Facility operators, in- bond carriers, bonded warehouse proprietors, Foreign Trade Zone operators, and Container Freight Station operators must electronically transmit or otherwise submit MDRs immediately upon discovery of the discrepancy. MDRs can be electronically transmitted or otherwise submitted within the reporting period as prescribed by regulation after entry of the importing conveyance or receipt of the merchandise to avoid penalty actions.

All importers, whether automated or not, can transmit or paper file MDRs immediately upon discovery of the discrepancy. Manifest Discrepancy Reports may be electronically transmitted or otherwise submitted within the reporting period as prescribed by regulation after permit or entry of the merchandise to avoid penalty action. A penalty for late reporting may be assessed when the MDRs are received by CBP after the reporting period.

Pre-existing commercial documents related to the merchandise in question may be used as supporting documents to substantiate an MDR. These documents may include bills of lading, signed affidavits, exporter’s and shipper’s messages and telexes, and any other document that would substantiate the filer’s claim. In accordance with CBP recordkeeping requirements, documents supporting claims of discrepancy must be retained for a period of five years from the date of entry or exportation.

Documents supporting the claim of discrepancy should be attached to the MDR. The MDR will be accepted whether or not documentation substantiating the reason for the discrepancy is attached to the MDR. However, penalties may be assessed for lack of this substantiation. If documents are not attached, the filer should collect and retain the documents to substantiate claims for post audit reviews.

Post Audit Teams are responsible for the enforcement of manifest accuracy. Post Audit Teams must audit carrier records to ensure that substantiating documentation is obtained by the carriers and held on file whether or not an MDR was required or filed. Post Audit Teams will assess penalties and/or liquidated damages when audits reveal discrepancies that violate CBP

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 12 of 23

laws or regulations, or when documents that are used to support discrepancy claims are found to be unacceptable or not present. Post Audit Teams must also ensure coordination with the Manifest Review Units (MRU) so that local guidelines are developed for MRU review of appropriate MDRs.

CBP officers (including the Contraband Enforcement Team (CET)), discovering any discrepancy as listed in this directive should prepare an MDR. A copy must be provided to the carrier and to the Post Audit Team.

Lesson 4: Travelers and Their Goods

Topic 1: Residents and Nonresidents

For CBP purposes, persons arriving from foreign countries are divided into two classes:

1) Residents of the United States returning from abroad (returning residents), and 2) All other persons, hereinafter referred to as nonresidents.

Returning residents are defined as:

• Citizens of the United States (including American citizens who are residents of American Samoa, Guam, the Commonwealth of the Northern Mariana Islands or the Virgin Islands of the United States)

• Persons who have formerly resided in the United States

As a rule, articles are considered to accompany a passenger or to have been brought into the country by a passenger if the articles arrive on the same vessel, vehicle, or aircraft on the same date as the passenger’s arrival in the United States. Articles in baggage that are shipped as freight on a bill of lading or airway bill are considered to accompany a passenger when the baggage arrives on the conveyance on which the passenger arrives in the United States. Articles in baggage, or in baggage shipped as freight, are considered to accompany a passenger if examined at an established preclearance station and the baggage is hand-carried, checked or manifested on the conveyance on which the passenger arrives in the United States.

Subject to any personal exemption from entry requirements, articles imported as baggage but not passed under a baggage declaration or under the procedure provided for unaccompanied

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 13 of 23

shipments of effects subject to personal exemptions, are entered in the same manner as a cargo importation of like goods. When making a regular entry –as freight and not personnel effects- for articles imported in baggage, the value of articles entitled to free entry under subheadings 9804.00.10 or 9804.00.45 HTSUS, are disregarded in determining whether a formal or informal entry is required.

Topic 2: Personal Exemptions and Declarations

The regulations on personal exemptions outline a variety of situations where duty exemptions apply and entry declaration formalities may be waived or simplified including but not limited to:

• Residents of the United States returning from abroad • Baggage considered to be accompanying a passenger • Temporary imports by non-residents • Certain articles taken abroad and/or acquired abroad • Exemptions for resident and non-resident crew members • Diplomatic, consular and other named personnel of foreign governments or

international organizations • Tools of trade classifiable under the provisions of HTSUS 9804.00.15 or 9804.00.10

The Regulations also specify what merchandise must be declared upon arrival into the U.S.:

• Items you purchased and are carrying with you upon return to the United States • Items you received as gifts, such as wedding or birthday presents • Items you inherited • Items you bought in duty-free shops, on the ship, or on the plane • Repairs or alterations to any items you took abroad and then brought back, even if

the repairs/alterations were performed free of charge • Items you brought home for someone else • Items you intend to sell or use in your business • Items you acquired— whether purchased or received as gifts in the U.S. Virgin

Islands, American Samoa, Guam, or in a Caribbean Basin Economic Recovery Act country that are not in your possession when you return. In other words, if you acquired items in any of these island nations and asked the merchant to send them to you, you must still declare them when you go through CBP. This differs from the usual procedure for mailed items.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 14 of 23

Also, the CBP declaration must include the value paid for each item in U.S. dollars; including taxes paid. If the item was not purchased but provided, for example, as a gift, the value declared on the declaration should be the item’s fair retail value in the country where the item was received.

Topic 3: Types of Exemptions 19 CFR 148 and USHTS chapter 98 IV to VII

Whether or not a personal exemption applies and the amount depends on citizenship, the country the person is coming from, how long they were there, what was purchased or received, the country in which the goods were made, and the price paid for the goods. When entering the United States or returning to the United States from a foreign country with your personal belongings and goods you purchased or received you must declare them on a CBP Declaration Form 6059B.

A U.S. resident returning from a foreign country with goods acquired abroad after a stay of 48-hours or more may be eligible for a personal duty-free exemption however, the 48 hours rule does not apply when returning from Mexico or the U.S. Virgin Islands 19 CFR 148.35. The availability of the personal exemption depends upon the country from which the person is returning. For instance, if returning from countries other than U.S. insular possessions a person is entitled to an $800 duty-free exemption and the next $1,000 worth of the goods purchased is subject to a flat rate of 3%. If you are returning from a U.S. insular possession (i.e., U.S. Virgin Islands or Guam) you are entitled to a $1,600 duty-free exemption and the next $1,000 worth of the goods you purchased is subject to a flat rate of 1.5%. If the value exceeds the total of the duty-free exemption plus the flat-rate, the remaining duty will be determined based on duty rates in the HTSUS, which are generally between 0 to10% (except for clothing and textiles, which can be much higher, up to 25%) from countries that have normal trade relations status with the United States. Further, if returning from a foreign country other than Mexico and it has been less than 48 hours, a $200 duty-free exemption is allowed. Anything above that amount will be dutiable at the rate in the HTSUS. If any purchases include alcoholic beverages or tobacco products, only a certain amount may be brought in duty-free under the exemption. The amount depends on the country returning from.

Regarding alcohol, generally, only 5 fl. oz per person may be entered into the United States duty-free by travelers who are 21 or older, although travelers coming from the U.S. Virgin

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 15 of 23

Islands or other Caribbean countries are entitled to a larger quantity 19 CFR 148.33(b)(3(i)). Additional quantities may be entered, although they will be subject to duty and Internal Revenue Service taxes. It is not legal for travelers under the age of 21 to import alcohol - even as a gift. The total amount of alcohol that may enter the country is determined primarily by the laws of the State where re-entry to the United States takes place.

Some commodities are not subject to duty (e.g., original paintings or antiques that are over 100 years old) or that may have originated in a country eligible for a special trade program (e.g., GSP, NAFTA, etc.). Also, the $200, $800, or $1,600 exemption for articles acquired abroad shall not be granted to a returning resident who has taken advantage of such exemption within the 30 days immediately preceding his current return to the United States.

A passenger who makes any false or fraudulent statement or who engages in other unsavory conduct whereby a CBP officer is or may be induced to pass an article free of duty or at less than the proper amount of duty, or to treat an article in some other manner in order to obtain a benefit, shall be penalized for fraud, gross negligence, and negligence.

In this case, the article involved shall be seized only if one or more of the conditions set forth under regulation are present 19 CFR 162.75(a). If a seizure is not made, an amount equivalent to the maximum penalty which may be assessed in accordance with the passenger's degree of culpability shall be demanded from the passenger. The amount demanded in lieu of seizure shall be determined in accordance with the regulatory guidelines. In all cases, the estimated duties shall be demanded of the passenger as soon as possible after the discovery of the violation. Any applicable internal revenue tax shall also be demanded unless the merchandise is to be, or has been, forfeited.

Lesson 5: Instruments of International Traffic

As a general rule, all merchandise imported into the United States is required to be entered, unless specifically excepted. Importation occurs when a vessel or aircraft laden with goods arrives within a port of entry with the intent to discharge its cargo, or upon arrival within the Customs territory of the United States if by vehicle or train. The “Customs territory of the United States” includes only the States, the District of Columbia, and Puerto Rico.

Specific exemptions from entry apply to merchandise described in General Note 3(e) of the Harmonized Tariff Schedule of the United States (HTSUS), which includes instruments of

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 16 of 23

international traffic. Since formal entry and payment of duty are not required for instruments of international traffic, importers may benefit from having articles, which they use for shipping merchandise designated as instruments of international traffic. This would allow importers more efficient and economic use of their containers, vehicles, locomotives and other railroad equipment in local traffic as well as in foreign countries.

Instruments of International Traffic are lift vans, cargo vans, shipping tanks, skids, pallets, and similar instruments, including containers, and repair components. As defined in 19 CFR 10.41a and Article 1 of the Customs Convention on Containers, the term "container" means an article of transport equipment (e.g. lift-van, movable tank or other similar structure), that is:

i. Fully or partially enclosed to constitute a compartment intended for containing goods;

ii. Of a permanent character and accordingly strong enough to be suitable for repeated use;

iii. Specially designed to facilitate the carriage of goods, by one or more modes of transport, without intermediate reloading;

iv. Designed for ready handling, particularly when being transferred from one mode of transport to another;

v. Designed to be easy to fill and to empty; and

vi. Having an internal volume of one cubic meter or more.

This definition applies whether the instruments of international traffic are loaded or empty. Duty is payable only on foreign-origin instruments of international traffic and not on those of U.S. origin. The importer may request a Prospective Interpretation Ruling from CBP to determine whether an article and its proposed use meet the criteria of an Instrument of International traffic.

These instruments may be released once the party requesting release has filed a Continuous bond for control of containers and instruments of international traffic. The request for release can be filed at the port of arrival or at a subsequent port where the instrument will travel in-bond or where a container has moved under the terms of a carnet. If all requirements are met, the regulations allow for the instruments to be released without entry or payment of duty. The person who files the application for release is responsible for keeping and maintaining records regarding the international movement of the containers.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 17 of 23

When the instruments are taken out of international traffic, the regulations require that an entry be made. A container that is designated as an instrument of international traffic is deemed to remain in international traffic as long as it exits the United States within 365 days of the date it was admitted and not diverted to point-to-point traffic. If a container does not exit the United States within 365 days of the date on which it is admitted, it is deemed to have been removed from international traffic, and an entry for consumption must be made within 10 business days after the end of the month in which the container is deemed removed from international traffic.

When entry is required under this section, any containers considered removed from international traffic in the same month may be listed on one entry, and the entry may be made at any port of entry. The importer of record is required, using reasonable care, to complete the entry by filing with CBP the declared value, classification and rate of duty applicable to the merchandise.

Lesson 6: Check Digit Computation Formula

Check digits are computed from the filer code and transaction numbers (the first 7 digits of the entry number). Entry filer codes containing alpha characters must be transformed to a numeric equivalent prior to computing the check digit. The numeric equivalent for each alpha charter is as follows:

A=1

B=2

C=3

D=4

E=5

F=6

G=7

H=8

I=9

J=1

K=2

L=3

M=4

N=5

O=6

P=7

Q=8

R=9

S=2

T=3

U=4

V=5

W=6

X=7

Y=8

Z=9

Example: Entry filer code B76 would transform to 276 for check digit computation purposes.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 18 of 23

A. Using entry filer code B76 (276) and a transaction number 0324527 as an example,

the check digit is computed as follows:

Number for which check digit will be computed is: 2760324527

B. Start the calculation process by multiplying every other position by 2. (Essentially, all even positions will be multiplied by 2.)

*Note: High order zeros are a significant element in the computation process and must be included in the transaction number. If the result of the multiplication is greater than 9, add 1 to the sum, but disregard the digit in the tens column.

7 0 2 5 7

x2 x2 x2 x2 x2 (Multiply by 2)

14 0 4 10 14

+1

+1 +1 (Add 1 if total is greater than 9)

C. Add results

5+0+4+1+5=15

D. Total all odd positions starting at the beginning 2760324527 2+6+3+4+2=17

E. Add the sums from steps C and D.

15+17 = 32

F. Subtract the units digit (last digit) derived in step E (32) from 10. The result is the check digit.

10 - 2 = 8

G. Normally, the result of the arithmetic will be a single digit. In instances when the units digit subtracted from the sum in step E is a 0, the check digit will be 0.

15 + 0 + 4 + 11 + 15 (Disregard digits in the tens column)

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 19 of 23

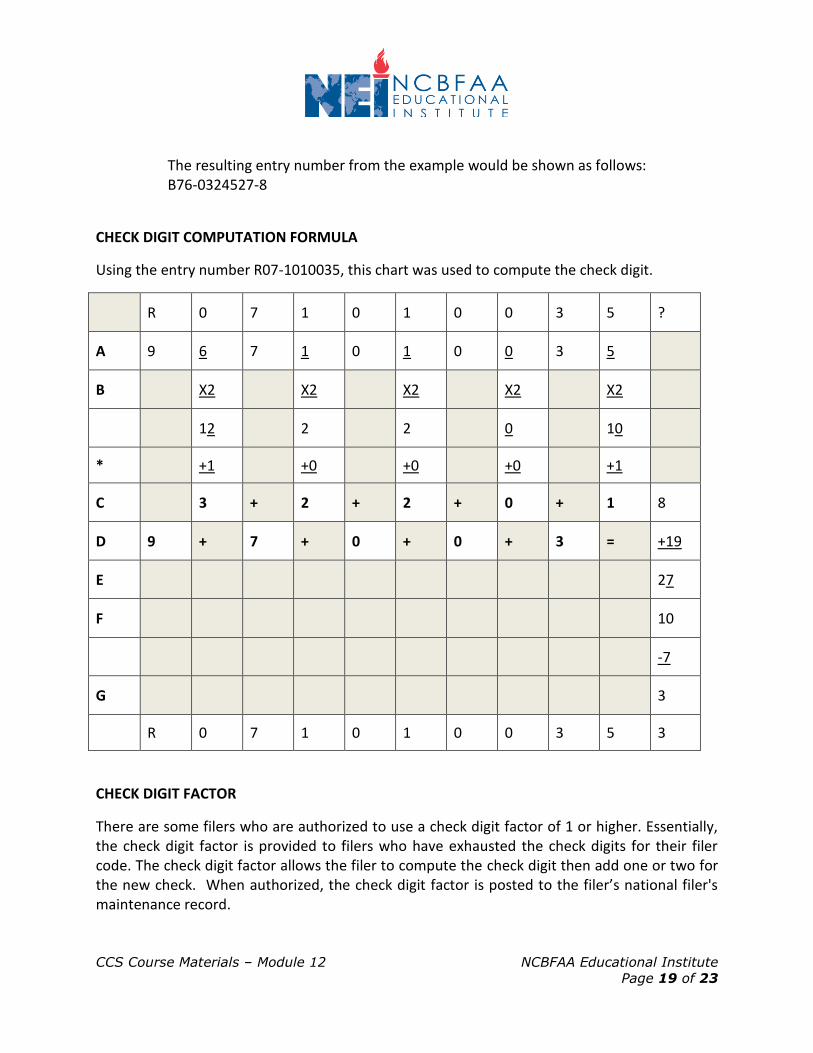

The resulting entry number from the example would be shown as follows: B76-0324527-8

CHECK DIGIT COMPUTATION FORMULA

Using the entry number R07-1010035, this chart was used to compute the check digit.

R 0 7 1 0 1 0 0 3 5 ?

A 9 6 7 1 0 1 0 0 3 5

B X2 X2 X2 X2 X2

12 2 2 0 10

* +1 +0 +0 +0 +1

C 3 + 2 + 2 + 0 + 1 8

D 9 + 7 + 0 + 0 + 3 = +19

E 27

F 10

-7

G 3

R 0 7 1 0 1 0 0 3 5 3

CHECK DIGIT FACTOR

There are some filers who are authorized to use a check digit factor of 1 or higher. Essentially, the check digit factor is provided to filers who have exhausted the check digits for their filer code. The check digit factor allows the filer to compute the check digit then add one or two for the new check. When authorized, the check digit factor is posted to the filer’s national filer's maintenance record.

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 20 of 23

Example: If a filer has been authorized to use a check digit factor of 1, using the example above, B76-0324527-8, the check digit (8) would be changed to (9). The Office of Field Operations, Trade Compliance and Facilitation, Broker Management Branch authorizes the Check Digit Factor. Lesson 7: Rules for Constructing the Manufacturer Identification Code (MID)

These instructions provide for the construction of an identifying code for a manufacturer or shipper from its name and address. The code can be up to 15 characters in length, with no inserted spaces.

To begin, for the first 2 characters, use the ISO code for the actual country of origin of the goods. The exception to this rule is Canada. “CA” is NOT a valid country for the manufacturer code. Instead, one of the appropriate province codes listed to the left should be the prefix to the Canadian MID.

ALBERTA XA

BRITISH COLUMBIA XC

MANITOBA XM

NEW BRUNSWICK XB

NEWFOUNDLAND (LABRADOR) XW

NORTHWEST TERRITORIES XT

NOVA SCOTIA XN

NUNAVUT XV

ONTARIO XO

PRINCE EDWARD ISLAND XP

QUEBEC XQ

SASKATCHEWAN XS

YUKON TERRITORY XY

Next, use the first three characters from the first two “words” of the name. If there is only one “word” in the name, then use only the first three characters from the first name. For example, Amalgamated Plastics Corp. would be “AMAPLA;” Bergstrom would be “BER.”

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 21 of 23

If there are two or more initials together, treat them as a single word. For example, A.B.C. Company or A B C Company would yield “ABCCOM.” O.A.S.I.S. Corp. would yield “OASCOR.” Dr. S.A. Smith yields “DRSA,” Shavings B L Inc. yields “SHABL.”

In the manufacturer name, ignore the English words a, an, and, of, and the. For example, “The Embassy of Spain” would yield “EMBSPA.”

Portions of a name separated by a hyphen are to be treated as a single word. For example, “Rawles- Aden Corp.” or “Rawles – Aden Corp.” would both yield “RAWCOR.”

Some names will include numbers. For examples, “20th Century Fox” would yield “20TCEN” and “Concept 2000” yields “CON200.”

Some words in the title of the foreign manufacturer’s name should not be used for the purpose of constructing the MID. For example, most textile factories in Macau start with the same words, “Fabrica de Artigos de Vestuario” which means “Factory of Clothing.” For a factory named “Fabrica de Artigos de Vestuario JUMP HIGH Ltd,” the portion of the factory name that identifies it as a unique entity is “JUMP HIGH.” This is the portion of the name that should be used to construct the MID. Otherwise, all of the MIDs from Macau would be the same, using “FABDE,” which is incorrect.

Similarly, many factories in Indonesia begin with the prefix PT, such as “PT Morich Indo Fashion.” In Russia, other prefixes are used, such as “JSC,” “OAO,” “OOO,” and “ZAO.” These prefixes should be eliminated for the purpose of constructing the MID.

Next, find the largest number on the street address line and use up to the first four numbers. For example, “11455 Main Street Suite 9999” would yield “1145.” A suite number or a post office box should be used if it contains the largest number. For example, “232 Main Street Suite 1234” would yield “1234.” If the numbers in the street address are spelled out, such as “One Thousand Century Plaza,” there will be no numbers in this section of the MID. However, if the address is “One Thousand Century Plaza Suite 345,” this would yield “345.”

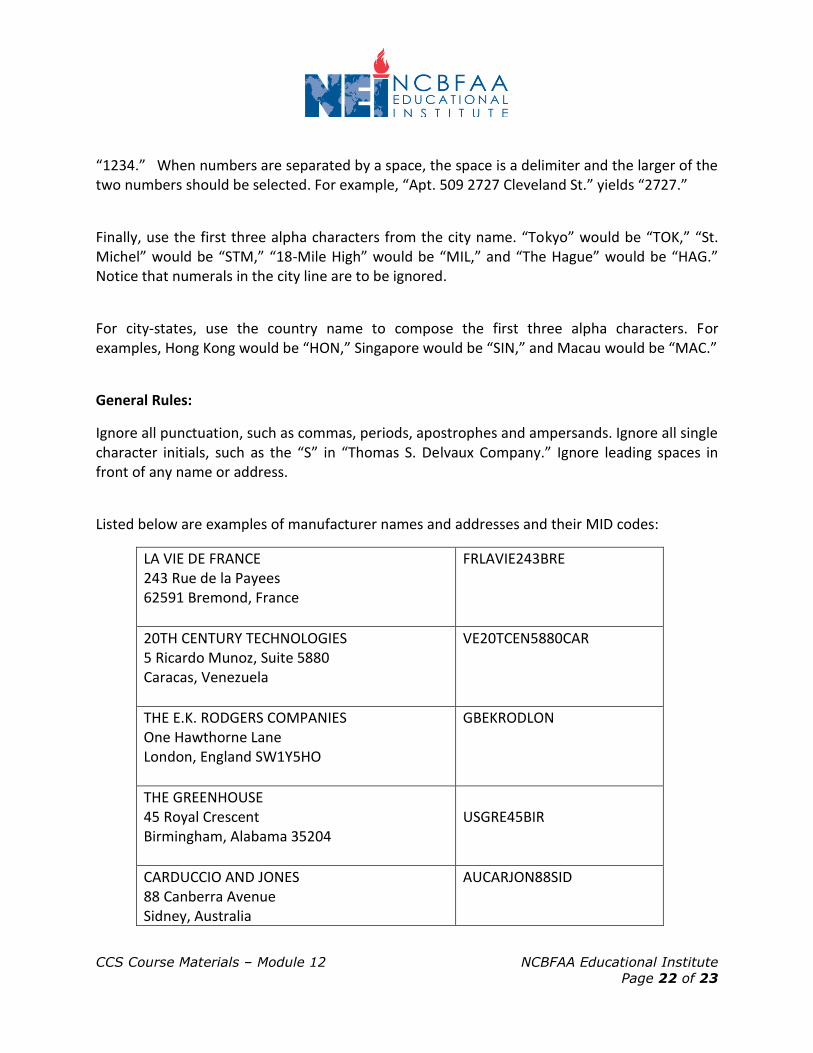

When commas or hyphens separate numbers, ignore all punctuation and use the number that remains. For examples, “12,34,56 Alaska Road” and “12-34-56 Alaska Road” would yield

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 22 of 23

“1234.” When numbers are separated by a space, the space is a delimiter and the larger of the two numbers should be selected. For example, “Apt. 509 2727 Cleveland St.” yields “2727.”

Finally, use the first three alpha characters from the city name. “Tokyo” would be “TOK,” “St. Michel” would be “STM,” “18-Mile High” would be “MIL,” and “The Hague” would be “HAG.” Notice that numerals in the city line are to be ignored.

For city-states, use the country name to compose the first three alpha characters. For examples, Hong Kong would be “HON,” Singapore would be “SIN,” and Macau would be “MAC.”

General Rules:

Ignore all punctuation, such as commas, periods, apostrophes and ampersands. Ignore all single character initials, such as the “S” in “Thomas S. Delvaux Company.” Ignore leading spaces in front of any name or address.

Listed below are examples of manufacturer names and addresses and their MID codes:

LA VIE DE FRANCE 243 Rue de la Payees 62591 Bremond, France

FRLAVIE243BRE

20TH CENTURY TECHNOLOGIES 5 Ricardo Munoz, Suite 5880 Caracas, Venezuela

VE20TCEN5880CAR

THE E.K. RODGERS COMPANIES One Hawthorne Lane London, England SW1Y5HO

GBEKRODLON

THE GREENHOUSE 45 Royal Crescent Birmingham, Alabama 35204

USGRE45BIR

CARDUCCIO AND JONES 88 Canberra Avenue Sidney, Australia

AUCARJON88SID

CCS Course Materials – Module 12 NCBFAA Educational Institute Page 23 of 23

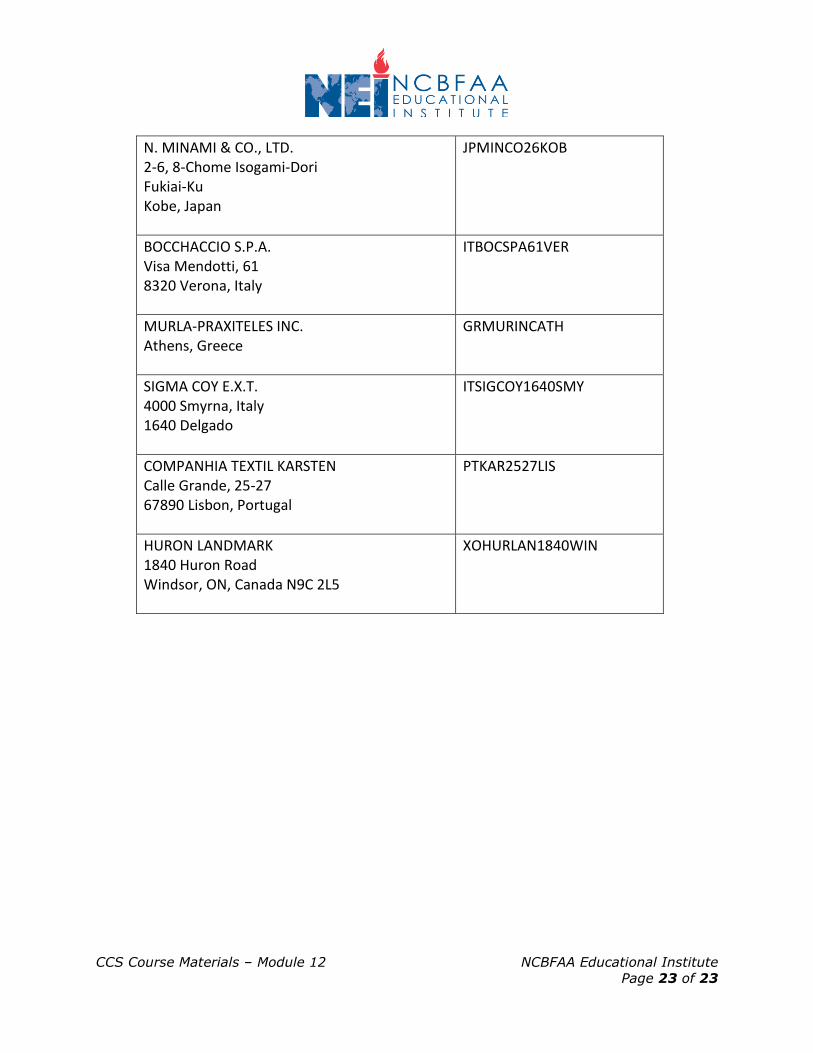

N. MINAMI & CO., LTD. 2-6, 8-Chome Isogami-Dori Fukiai-Ku Kobe, Japan

JPMINCO26KOB

BOCCHACCIO S.P.A. Visa Mendotti, 61 8320 Verona, Italy

ITBOCSPA61VER

MURLA-PRAXITELES INC. Athens, Greece

GRMURINCATH

SIGMA COY E.X.T. 4000 Smyrna, Italy 1640 Delgado

ITSIGCOY1640SMY

COMPANHIA TEXTIL KARSTEN Calle Grande, 25-27 67890 Lisbon, Portugal

PTKAR2527LIS

HURON LANDMARK 1840 Huron Road Windsor, ON, Canada N9C 2L5

XOHURLAN1840WIN