certificate for sequestration annette burns & diane dunn

TRANSCRIPT

Certificate for Sequestration

Annette Burns & Diane Dunn

• Introduction• Background• Analysis of statistics• Common themes• Case studies• Review and discussion

Certificate For Sequestration

Background

• Stakeholder feedback identified a group of debtors who did not meet the LILA criteria or have proof of Apparent Insolvency

• Certificate for Sequestration (CFS) came into effect as part of the Home Owner and Debtor Protection (Scotland) Act 2010

- Authorised Persons: prescribed criteria to be able to grant a certificate

- the 30-day rule

Some statistics

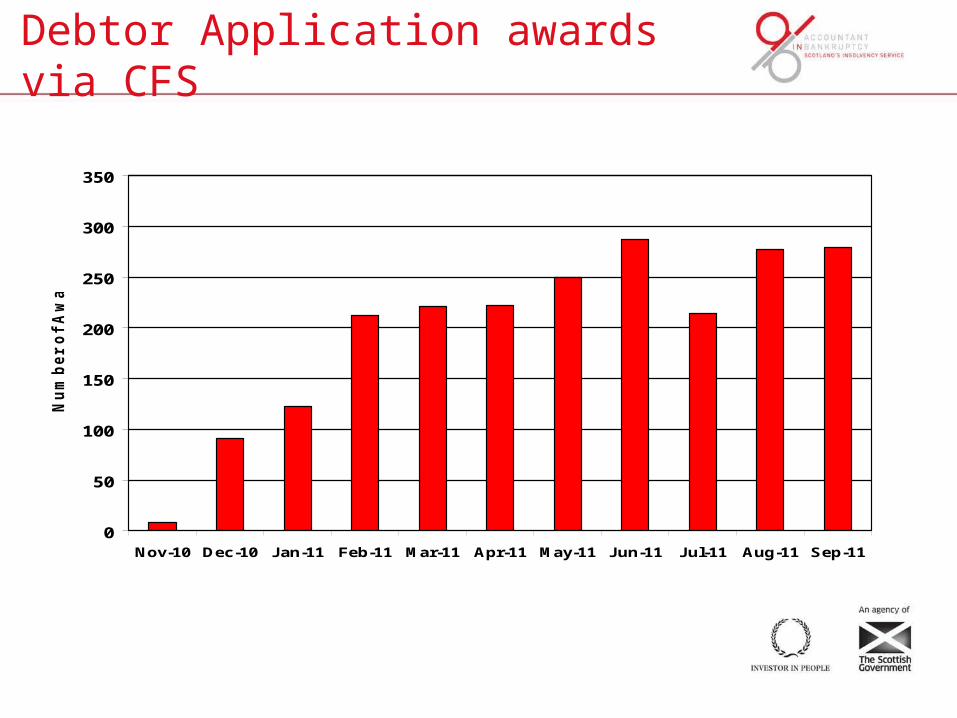

• From December 2010 until the end of September 2011, there were 2,183 debtor applications awarded with a CFS (29% of all debtor applications awarded)

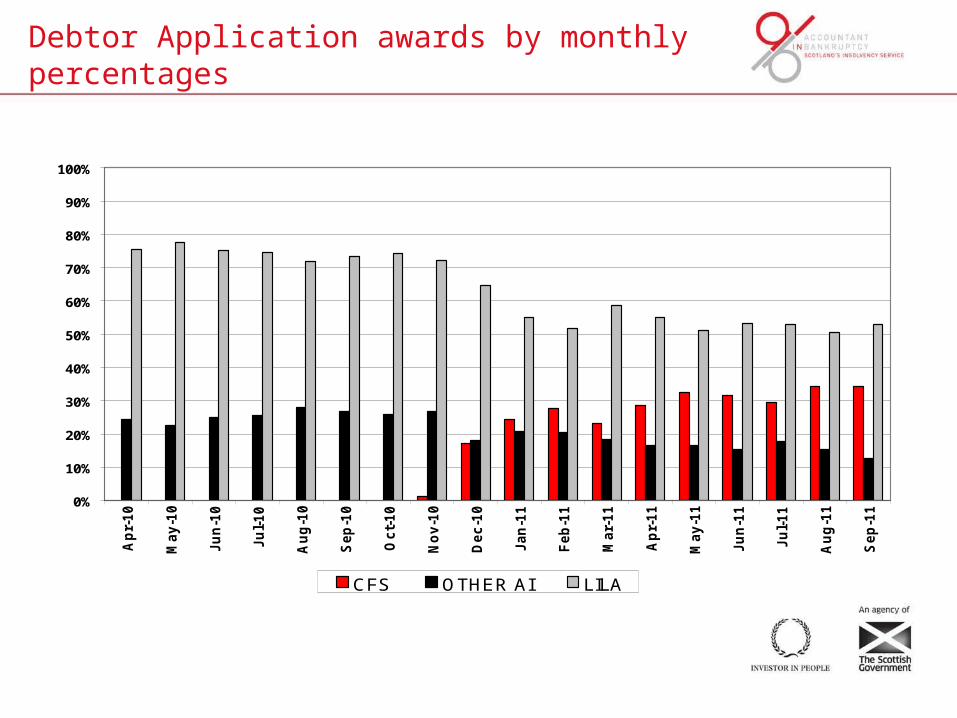

• LILA and Apparent Insolvency awards have dropped

• 207 Apparent Insolvency awards in September 2010, 103 in September 2011

Debtor Application awards via CFS

0

50

100

150

200

250

300

350

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11

Nu

mb

er

of

Aw

ard

s

Debtor Application awards by monthly percentages

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ap

r-1

0

Ma

y-1

0

Ju

n-1

0

Ju

l-1

0

Au

g-1

0

Se

p-1

0

Oc

t-1

0

No

v-1

0

De

c-1

0

Ja

n-1

1

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Ju

n-1

1

Ju

l-1

1

Au

g-1

1

Se

p-1

1

CFS OTHER AI LILA

• Inconsistent dates on CFS and debtor application

• Receipt of retrospective CFS– Application form received with no CFS, and question 7 ticked

‘no’ on the debtor application but CFS is submitted later– CFS received after debtor has been sent alternate routes letter– Where money adviser has not had full details of debtor’s

financial circumstances (e.g. mortgage to rent, life policy surrender value)

• CFS provided or trustee nominated where debtor meets LILA or AI criteria

• CFS not on headed notepaper

Common trends identified

Case Study 1

• Total debt circa £180k– Debtor earns £70k per annum– Has car valued at £20k– Has over £15k in bank– Company still trading– CFS issued

Case Study 2

• Total debt circa £9k– Non householder– Earns £21k per annum– CFS issued

Case Study 3

• Total debt circa £20k– Debtor owns property– Debtor earns £36k per annum– CFS issued

Review and Discussion

• How do you measure success?• Has the CFS met the needs of the debtors it

was intended to?• Does the 30-day rule assist or hinder?• Authorised Persons• In which ways does it work?• In which ways does it not work?• Areas for improvement?

Diane DunnPolicy Development Team Leader0300 200 2701 [email protected]

Annette BurnsHead of Case Administration0300 200 [email protected]

1 PENNYBURN ROAD, KILWINNING, AYRSHIRE, KA13 6SAT 0300 200 2600 F 0300 200 2601 W WWW.AIB.GOV.UK

THANK YOU