certificate examination in investment-linked...

TRANSCRIPT

CEILLIC E R T I F I C A T E E X A M I N A T I O N I N I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

CERTIFICATE EXAMINATION IN INVESTMENT-LINKED LIFE INSURANCE

PREFACE

This course contains the study materials for the Certificate Examination in Investment-Linked Life Insurance. The book may look ominously thick but please bear in mind that the market out there, both, the product producers and clients market has undergonetremendous changes in the last 15 years. The sudden deluge of information found here as compared to the earlier version is to provide a slightly higher level of understanding amongst agents, so that they can be better prepared when facing a client.

The objective of this course is to provide basic fundamental knowledge of howinvestment-linked life insurance works and how to market it to the public. This coursealso introduces the agent to the world of Investment-Linked L i fe Insurance sales andit is also hoped that the agents will not stop with this course but empower themselveswith higher qualifications in the coming future.

The Chapters in this course are designed in such a way, that a new person will get a clearpicture of what Investment-Linked Life Insurance is all about and also sets a template for them to follow to a higher level in the future.

It is hoped that the agents will utilise this course effectively and carry out their sales activities with stronger conviction and heightened confidence.

CEILLIC E R T I F I C A T E E X A M I N A T I O N I N I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

CERTIFICATE EXAMINATION IN INVESTMENT-LINKED LIFE INSURANCE

1st Edition 1998 (First published by The Malaysian Insurance Institute)

2nd Edition 1999

3rd Edition 1999

4th Edition 2000

5th Edition 2002

6th Edition 2010

Study Text

CEILLIC E R T I F I C A T E E X A M I N A T I O N I N I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

CERTIFICATE EXAMINATION IN INVESTMENT-LINKED LIFE INSURANCE

Copyright The Malaysian Insurance Institute 2010

All rights reserved. No part of this publication may be reproduced, stored in a retrievalsystem, or transmitted in any form by any system, electronic, mechanical, photocopying,recording or otherwise, without the prior permission of The Malaysian Insurance Institute.

The Malaysian Insurance Institute would like to express our gratitude to Persatuan InsuransAm Malaysia, the Life Insurance Association of Malaysia and all the various individuals who contributed in various ways to make the publication of this course book possible.

Published by The Malaysian Insurance Institute (35445H)No. 5, Jalan Sri Semantan Satu, Damansara Heights

50490 Kuala LumpurWebsite : www.insurance.com.my

ISBN 978-983-2432-02-9

Pages

11.1 Introduction

2

3

C O N T E N T S

The Malaysian Insurance Institute

INTRODUCTION TO INVESTMENT - LINKEDLIFE INSURANCE

KEY CONSIDERATIONS IN INVESTMENT

2.1 Introduction2.2 Investment Objectives2.3 Funs Available2.4 Risk Or Security2.5 Investment Horizon2.6 Acessibility Of Funds2.7 Taxation Treatment2.8 Performance Of The Investment2.9 DiversificationSelf-assessment Questions

TYPES OF INVESTMENT ASSETS3.1 Introduction3.2 Investment Choices3.3 Cash And Deposits3.4 Fixed Income Securities3.5 Shares3.6 Unit Trusts 3.7 Investment Trusts3.8 Properties 3.9 Derivatives 3.10 Exchange Traded Funds 3.11 Sukuk Bonds3.12 Capital Guaranteed FundSelf-assessment Questions

CERTIFICATE EXAMINATION ININVESTMENT - LINKED LIFE INSURANCE

Self-assessment Questions13

5589

101011

1111

12

14141417192123242529293032

Pages

4

5

6

C O N T E N T S

The Malaysian Insurance Institute

INVESTMENT - LINKED LIFE INSURANCE PRODUCTS– A WORLD SCENARIO

4.1 Introduction

4.2 In The United Kingdom

4.3 In The United States Of America

4.4 In Singapore

4.5 In MalaysiaSelf-assessment Questions

5.1 Introduction

5.2 Definitions

5.3 Characteristics Of Investment - Linked Insurance Policies

5.4 Types Of Investment - Linked Insurance Policies

5.5 Loans And Withdrawals Of Investment - Linked Insurance Policies

5.6 Risk Base Capital GuidelinesSelf-assessment Questions

TYPES OF INVESTMENT - LINKEDLIFE INSURANCE PRODUCTS

STRUCTURE OF INVESTMENT - LINKED FUNDS

6.1 Introduction

6.2 Accumulation Units 6.3 Distribution Units

6.4 Types Of Investment - Linked Funds

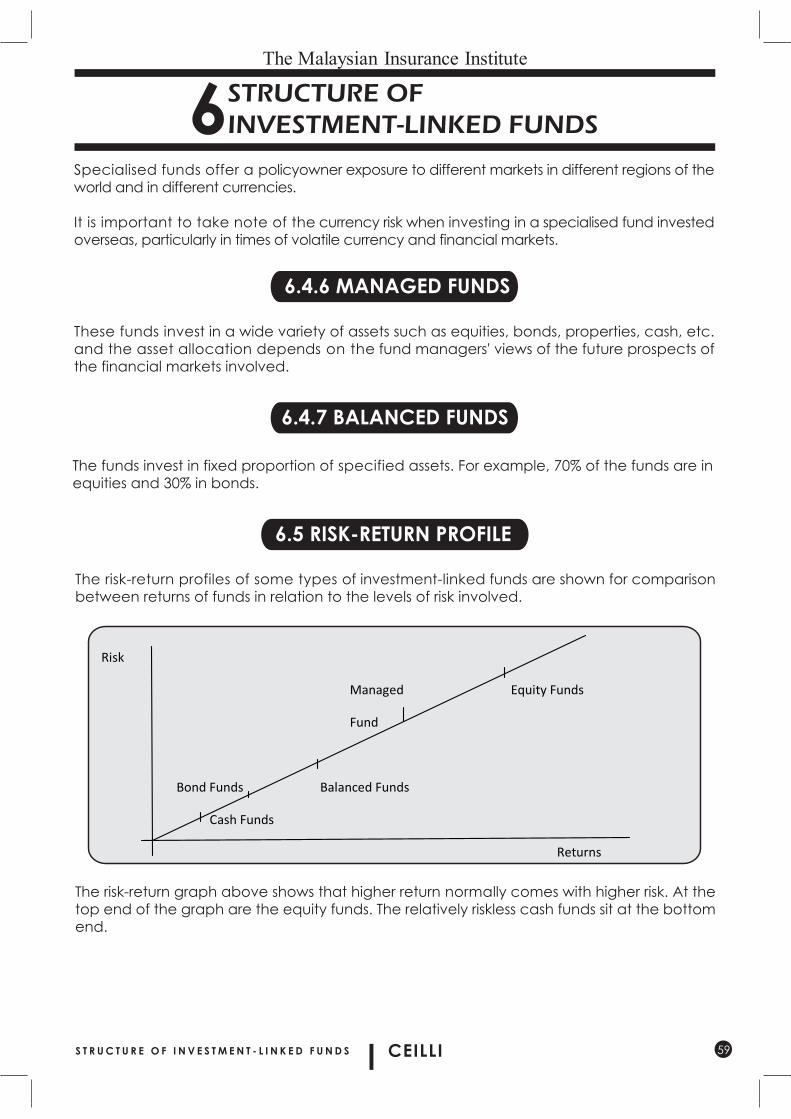

6.5 Risk - Return Profile

6.6 SwitchingSelf-assessment Questions

34

34

40

42

36

36

3739

4444505055

57

5757

57

596061

CERTIFICATE EXAMINATION ININVESTMENT - LINKED LIFE INSURANCE

Pages

8

9

C O N T E N T S

The Malaysian Insurance Institute

BENEFITS AND RISKS OF INVESTING ININVESTMENT - LINKED FUNDS

8.1 Introduction8.2 Benefits8.3 Risks Of Investing In Investment - Linked FundsSelf-assessment Questions

COMPARISONS BETWEEN INVESTMENT - LINKEDLIFE INSURANCE AND TRADITIONAL WITHPROFIT LIFE INSURANCE PRODUCTS

9.1 Introduction

9.2 Traditional Guaranteed Without - Profit Life Insurance Products

9.3 Traditional With - Profit Life Insurance Products

9.4 Investment - Linked Life Insurance Products

9.5 Other Comparison - TransparencySelf-assessment Questions

7 HOW INVESTMENT-LINKED LIFEINSURANCE PRODUCTS WORK

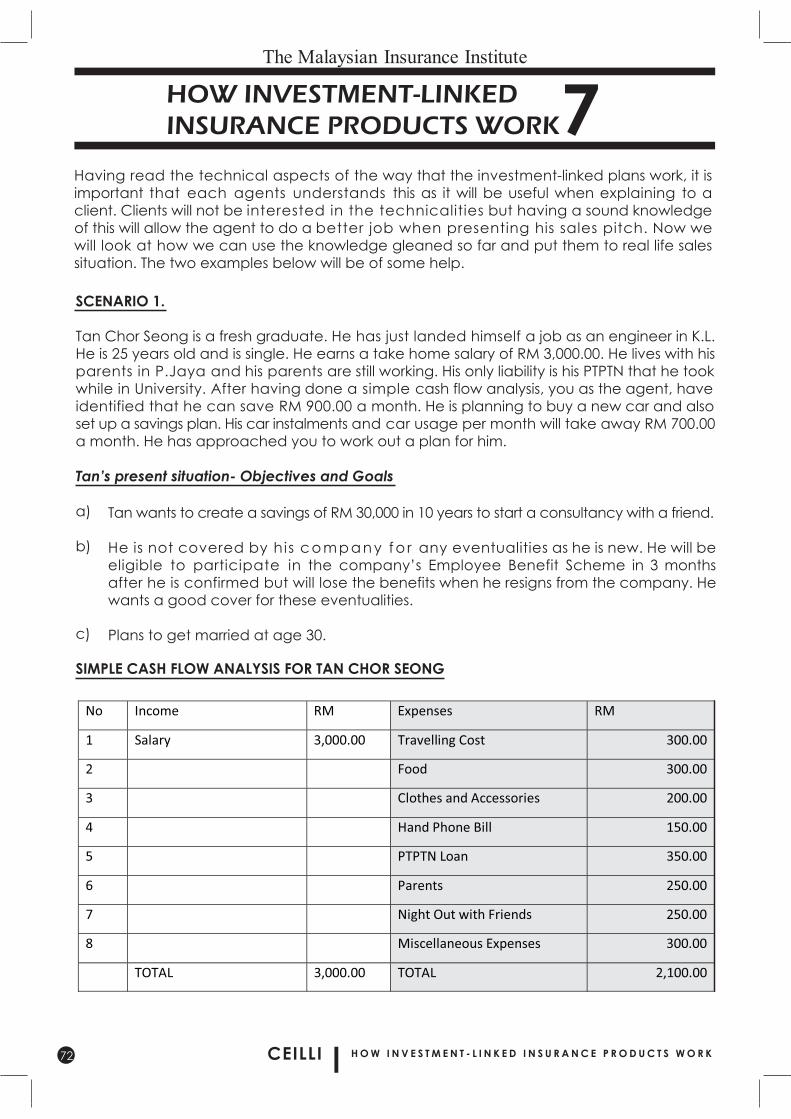

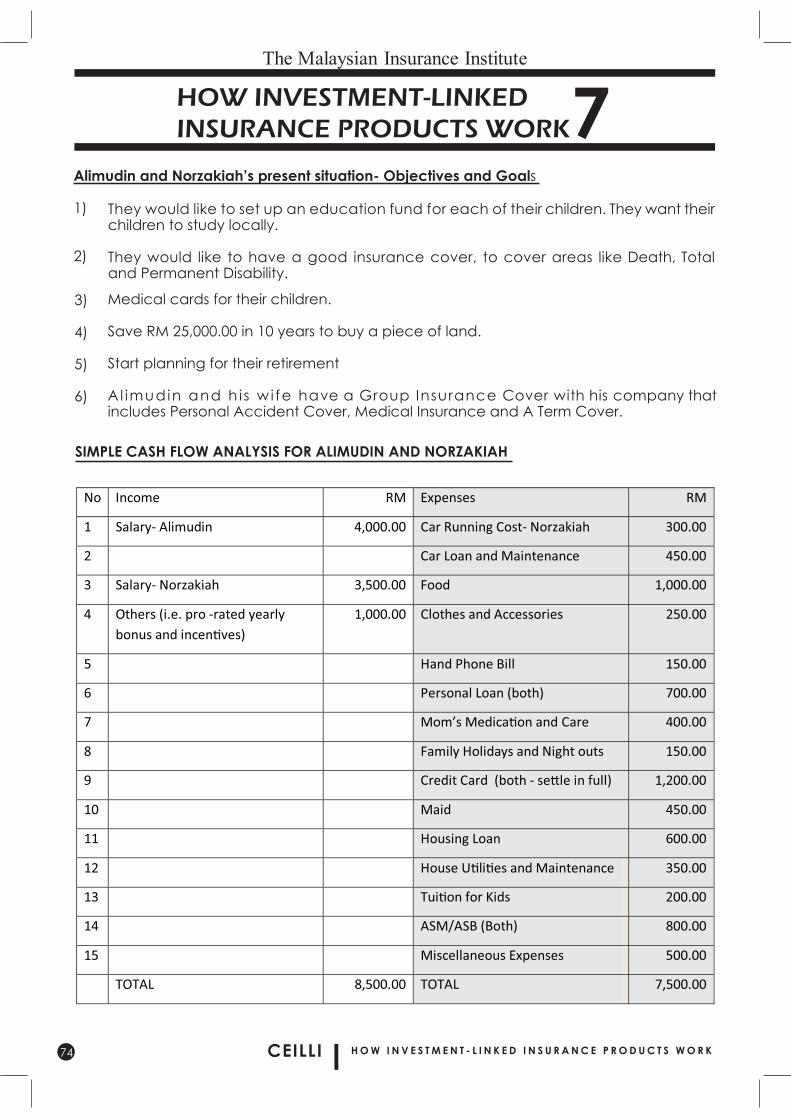

7.1 Introduction 7.2 The Working Of Investment - Linked Life Insurance 7.3 Top - Ups 7.4 Single Premium Policies - Methods Of Calculating Benefits 7.5 Withdrawal Benefit 7.6 Surrender Value 7.7 Death Benefit7.8 Regular Premium PoliciesSelf-assessment Questions

636365

6969

71

65

70

76

78787980

82

8283

858687

CERTIFICATE EXAMINATION ININVESTMENT - LINKED LIFE INSURANCE

Pages

11

12

C O N T E N T S

The Malaysian Insurance Institute

10 TAXATION AND LAW COVERINGINVESTMENT - LINKED LIFE INSURANCE PRODUCTS

10.1 Introduction10.2 Taxation Of Investment - Linked Life Insurance

10.3 Law Covering Investment - Linked Life Insurance

10.4 Other Legal RequirementsSelf-assessment Questions

IDENTIFYING AND ESTABLISHING CUSTOMER NEEDS

11.1 Introduction

11.2 Establishing Relationship With The Client

11.3 Gathering All Relevant Financial Data

11.4 Establishing Current Financial Position And Goals

11.5 Developing Plans And Strategies To Meet The Goals

11.6 Discuss Possible Recommendations

11.7 Implementation Of The Agreed Recommendations

11.8 Monitoring The PortfolioSelf-assessment Questions

MARKETING AND AFTER SALES SERVICES, ETHICS AND CODE OF CONDUCT

12.1 Introduction

12.2 Marketing 12.3 Ethics And ConductSelf-assessment Questions

ANSWERS TO SELF - ASSESSMENT QUESTIONS

8989

909596

9898

9999

99

100100

100102

104

104110

119

121

CERTIFICATE EXAMINATION ININVESTMENT - LINKED LIFE INSURANCE

p a g e

1CEILLI

1INTRODUCTION TO INVESTMENT - LINKED LIFE INSURANCE

I N T R O D U C T I O N T O I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

1.1 INTRODUCTION The insurance industry in Malaysia has experienced a steady growth in the last 15 years. Part of this growth is due to the fact that, Insurance companies in Malaysia have stepped up their efforts in designing and offering very good plans that are more customer-centric. These changes have augured well for the whole industry. The new plans have been well received by the market and one of the most popular products is the Investment-Linked Life Insurance plans. It is reported, according to Bank Negara’s DGI report 2009, that the total number of new life insurance policies has grown from 498,338 policies in 1990 to 1,403,562 policies in 2009.

One very interesting fact is that, part of the reason for this growth was the introduction of Investment-Linked Insurance plans in Malaysia. This plan was first introduced in the late 1990s and has seen a very steady growth. Bank Negara’s report also shows that, distribution of annual premiums that has gone into Investment-Linked Insurance policies has gone from 25.7 % in 2005 to 30.6% in 2009.

We have also seen that more and more insurance companies are moving away from sellingtheir traditional Whole Life and Endowment plans and have included many Investment-Linked plans in their portfolios. We see this as a positive move. Malaysians are becoming more discerning and now, they want to make sure that they are in control of the kinds of investments they choose. The Investment-Linked insurance policies, allows them to do this. Policyholders are quite happy to buy Investment- Linked policies because they can choose the amount of coverage needed and still enjoy a sizeable return on their savings.

So, what is an Investment-Linked Insurance policy? An Investment-Linked insurance plan offers a policyholder or investor a policy that is directly connected to investment performance.In other words, this plan not only offers the policyholder, a chosen amount of insurance cover but also provides that a portion of the premiums paid, is used to purchase funds in one or an array of investments offered by the insurance company.

Policyholders must be told and made aware of one very important fact when they choose the Investment-Linked policy, that the policy is directly linked to investment performance. The value of the policy is translated into units in a chosen fund or funds that is/are operated by the insurer. Sometimes, the insurance company may also channel these funds to an appointed fund manager to manage these funds. Thus it must be made known to the policyholder that these funds are exposed to the everyday fluctuations of market forces and they will and can fluctuate accordingly.

Policyholders must be made aware that the value of the units, directly reflects the values of the underlying funds. Benefits are therefore expressed in investment at their market value at the time the benefits are paid. To put it simply, policyholders must be made aware that their Investment-Linked plan can go to zero or grow at a good rate over time. There is a possibility that if the funds do badly, they can lose all the premiums paid and also the coverage provided. It is also important to know that the opposite of this can also take place and they can reap a good rate of return in the future.

This policy is designed to shift the uncertainty of investment gains or losses to policyholders and it does not provide any guarantee of either interest rates or minimum cash values. Theoretically, the cash value can go down to zero, and if so, the policy will terminate. This is because the policyholder must realise, that in order to gain the additional benefit of better-than-expected investment returns, they also have to assume all the possibility of investment losses.

The investment fund that is used for the Investment-Linked policy can have a wide range of investment modes. It also can cover a wide area of investments like equities or stocks, bonds , fixed interest , foreign funds , real estate, currency and so on. These funds can either be ‘external unit trusts’ or an ‘internal unitised investment -linked fund’ Please remember that an internal unitised investment-linked fund is part of the life insurance fund of a life insurancecompany. Thus, the policyholders are offered a range of unit-linked funds in which they can invest.

Investment-Linked Insurance plans are not a new phenomenon in the Insurance industry. Investment-Linked policies have been around for a long time but it was only introduced in Malaysia in the late 1990s. For the purpose of this study, we will use the term “Investment-Linked” to mean the same plans sold in Singapore and also similar to the term “Unit-Linked” in the United Kingdom and to the term “Variable Life” in the United States.

2 CEILLI I N T R O D U C T I O N T O I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

1INTRODUCTION TO INVESTMENT - LINKED LIFE INSURANCE

p a g e

3CEILLII N T R O D U C T I O N T O I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

SELF-ASSESSMENT QUESTIONS

CHAPTER 1

1. What was the main reason for the steady growth of the Insurance Industry in Malaysia?

a. The liberalisation of regulations by the Ministry of Finance and Bank Negara Malaysia. b. The introduction of Investment-Linked policies. c. The efforts by insurance companies to design and offer customer-centric and good plans. d. The robust growth of the country’s economy.

2. What is an Investment-Linked policy?

a. A participating Whole Life Policy. b. A Capital and returns guaranteed policy. c. An endowment policy only. d. A plan that offers clients’ coverage and investment returns.

3. All the following statements are True, except;

a. The Investment-Linked policy is directly linked to investment performance. b. Once the policy is in force, the clients’ investments will grow steadily. c. Fund Managers will make sure that the Investment Linked policy is shielded from market fluctuations. d. The Investment Linked policy only provides coverage and nothing else.

4. Investment-Linked Insurance policy is named as the following around the world except

a. Mutual Fund-Linked Policy. b. Unit-Linked Policy. c. Variable Life Policy. d. Takaful Investment-Linked life.

5. “... is designed to shift the uncertainties of investment gains or losses to the policy holders...” The excerpt describes what of the following accurately?

Policyholders who choose to take Investment-Linked policies must realise that they are also responsible to monitor the performance of their policy to ensure areasonable return.The chances that the policy values going to zero is impossible because the FundManagers, companies and agents will ensure that the policy is profitable at all times.Insurance companies, Fund Managers will wash their hands off the policy oncethe policy is taken and leave it solely to the agents and policy holders to monitor it.Agents are responsible to the clients’ only and must ensure that they monitor the policy atall times.

a.

b.

c.

d.

1INTRODUCTION TO INVESTMENT - LINKED LIFE INSURANCE

4

An Investment-Linked plan has the following features :- 6.

Provide cover for death and Total Permanent Disability.Participate in investments managed by the Insurer.Can provide a good return if monitored well.Largely depends on the clients’ ability to be good at investing in equities market.

i.ii.iii.iv.

i,ii,iv only.i,iii,iv only.ii,iii,iv only.i,ii,iii only.

a.b.c.d.

YOU WILL FIND THE ANSWERS AT THE BACK OF THE BOOK.

CEILLI I N T R O D U C T I O N T O I N V E S T M E N T - L I N K E D L I F E I N S U R A N C E

1INTRODUCTION TO INVESTMENT - LINKED LIFE INSURANCE

5CEILLI

2KEY CONSIDERATIONS IN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

2.1 INTRODUCTION

Many people were adversely affected by the 1997 Asian Financial Crisis. They were subjected to a greater loss when the Global Financial Crisis took place recently. Economies collapsed and governments were sent reeling. Drastic actions by governments andindustries were taken to stem the flow and in the overall scenario, many people lost their life savings or saw their savings coming to nothing.

Having been through all these economic upheavals, it is quite a challenge to speak about investments to a client. Clients over the years have become more proficient in investing and most of them learnt it the hard way after being ‘burnt’. Having these economic ‘disasters’ in the back of the head, we must realise that there is an increasing need forsound and proper advice. The majority of Malaysian investors are small time investors, usually investing as retail investors. Most of the time, very little investment research and analysis is done by them. They usually base their investment decisions on hear say news, rumours, gossips, ‘tips’ from their friends and early morning coffee shop conversations.

The main aim of this course is to empower the agent to have some basic knowledge ofhow, what, when, where and why investments must be done. The agent owes the client a moral obligation to educate them with some basic sound investment principles, so thatthe client will be able to make a sound judgement on investments.

There are some basic fundamental considerations that must be taken into account when making a decision on investment. The following key considerations must be made known to the client. A good understanding of these considerations is important before we get into an investment. The key considerations are as follows;

.

2.2 INVESTMENT OBJECTIVES

The objectives for investing our savings are continuously increasing, yet every single investmentvehicle can be easily categorised according to 3 fundamental characteristics i.e.;

a) Safety.b) Income. c) Growth.

1. Investment Objectives2. Availability of Funds3. Risk or Security4. Investment Horizon5. Accessibility of Funds6. Taxation Treatment7. Performance of the Investment8. Diversification

6 CEILLI

2KEY CONSIDERATIONSIN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

While it is possible for an investor to have more than 1 of the objectives above, the success of one must come at the expense of the others. Let’s look at the 3 fundamental characteristicsmentioned above a little more closely;

a) SAFETY

It is not wrong to say that there is no such thing as a completely safe and secure investment. We can get close to ultimate safety for our investment through the purchase of Governmentissued bonds or sukuk bonds and also from those found in the money market such as TreasuryBills or Fixed Deposit accounts. (These instruments will be discussed at length in Chapter 3).

These instruments lend a relatively safe investment return but the client has to forego growth and income stream. The returns from these instruments are quite conservative and at best would help the client to create a hedge against inflation.

b) INCOME

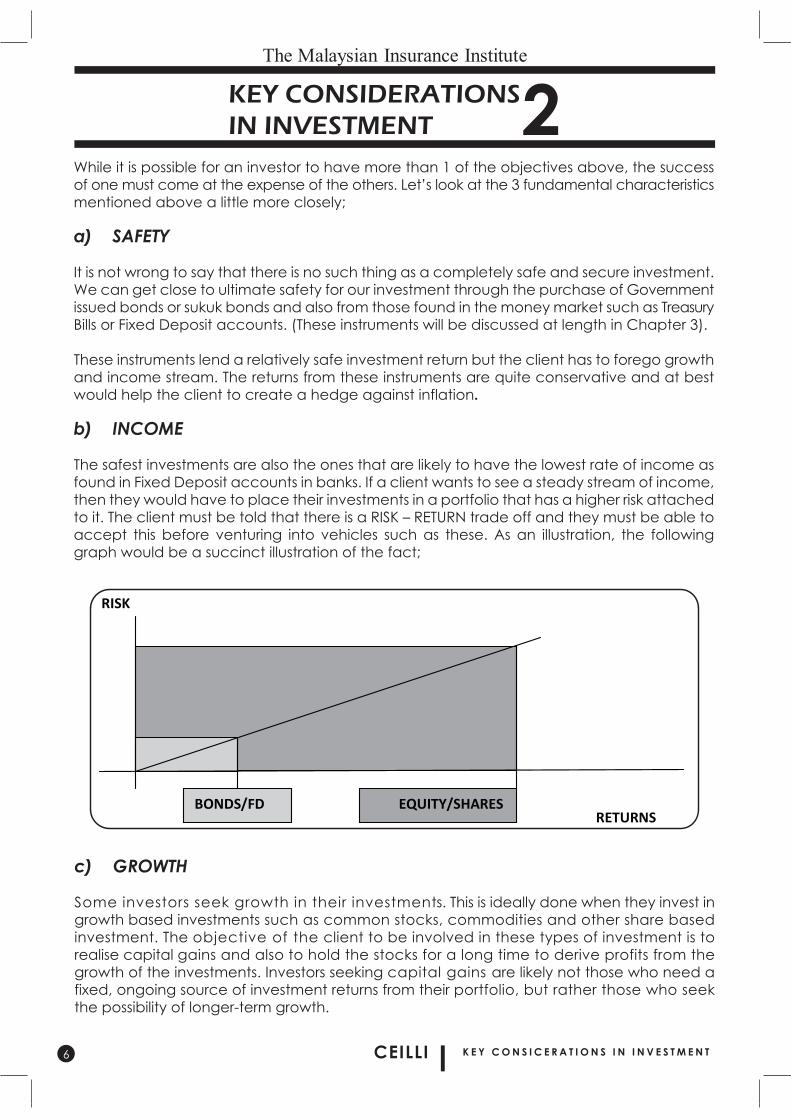

The safest investments are also the ones that are likely to have the lowest rate of income as found in Fixed Deposit accounts in banks. If a client wants to see a steady stream of income, then they would have to place their investments in a portfolio that has a higher risk attached to it. The client must be told that there is a RISK – RETURN trade off and they must be able to accept this before venturing into vehicles such as these. As an illustration, the following graph would be a succinct illustration of the fact;

RISK

RETURNSBONDS/FD EQUITY/SHARES

c) GROWTH

Some investors seek growth in their investments. This is ideally done when they invest in growth based investments such as common stocks, commodities and other share based investment. The objective of the client to be involved in these types of investment is to realise capital gains and also to hold the stocks for a long time to derive profits from the growth of the investments. Investors seeking capital gains are likely not those who need a fixed, ongoing source of investment returns from their portfolio, but rather those who seekthe possibility of longer-term growth.

7CEILLI

2KEY CONSIDERATIONS IN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

Depending on the objectives identified above, the person would need to choose between investing in income producing instruments or growth weighted instruments. It must be made known to the client, that different types of investments produce different combinations of income and also the risk factors involved in them.

The agent now has to ascertain, the correct mix of objectives that the client has and the agent has to also analyse the risk-return factors, to realise the completion of these objectives.It is by no means an easy task but it is not impossible either. Making sure that the clients are given a sound understanding of how investments work is the crux of the matter. Identifying the surplus funds that will be utilised to reach these objectives is what the agent must strive to do. In doing so, the agent not only wins the conf idence of the clients but he is in a position to offer proper advice that can be accepted by the clients.

Growth of capital is most closely associated with the purchase of common stocks, particularly growth securities, which offer considerable opportunity for increase in value. For this reason, common stock generally ranks among the most speculative of investments as their return depends on what will happen in an unpredictable future. Blue-chip stocks, by contrast, can potentially offer the best of all worlds by possessing reasonable safety, modest income and potential for growth in capital, generated by long-term increases in corporate revenues and earnings as the company matures.

OTHER INVESTMENT OBJECTIVES

Whilst the basic objective of every investor can fall into one or more of the 3 categories discussed above, investors also have secondary objectives that are more close to their hearts, that are more focussed for specific needs. The specific objectives of the investor can fall into the following headings;

a) Ensuring a comfortable standard of living.b) Providing funds for their dependents.c) Providing funds for education and up bringing of their children.d) Improving their financial position.e) Hedging inflation.f ) Liability cancellation.g) Retirement income.h)Achieving Financial Freedom.i ) Achieving a state – Beyond Financial Freedom.j ) Funds for paying necessary expenses and taxes when a person dies.

8 CEILLI

2KEY CONSIDERATIONSIN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

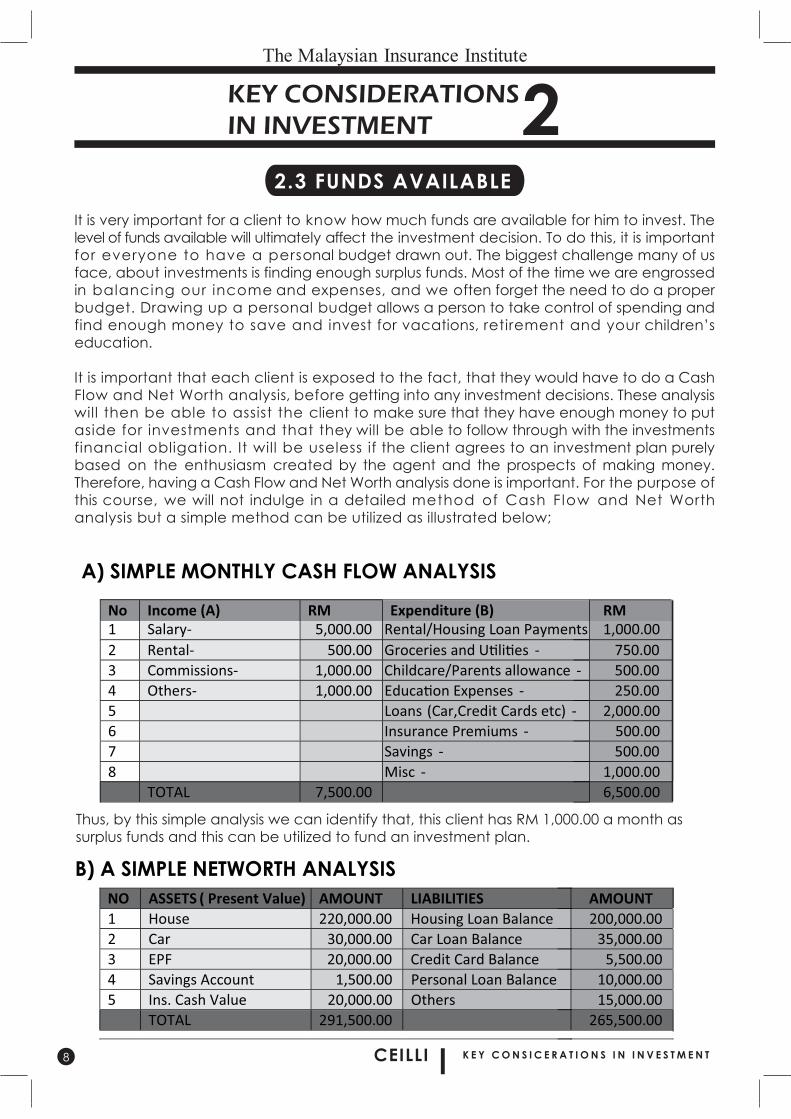

A) SIMPLE MONTHLY CASH FLOW ANALYSIS

No Income (A)

RM Expenditure (B) RM1 Salary- 5,000.00 Rental/Housing Loan Payments 2 Rental- 500.00 Groceries and U�li�es -3 Commissions- 1,000.00 Childcare/Parents allowance -4 Others- 1,000.00 Educa�on Expenses -5 Loans (Car,Credit Cards etc) -6 Insurance Premiums -7 Savings -8 Misc -

TOTAL 7,500.00

1,000.00750.00500.00250.00

2,000.00500.00500.00

1,000.006,500.00

Thus, by this simple analysis we can identify that, this client has RM 1,000.00 a month as surplus funds and this can be utilized to fund an investment plan.

B) A SIMPLE NETWORTH ANALYSISNO ASSETS ( Present Value) AMOUNT LIABILITIES AMOUNT1 House 220,000.00 Housing Loan Balance 200,000.002 Car 30,000.00 Car Loan Balance 35,000.003 EPF 20,000.00 Credit Card Balance 5,500.004 Savings Account 1,500.00 Personal Loan Balance 10,000.005 Ins. Cash Value 20,000.00 Others 15,000.00

TOTAL 291,500.00 265,500.00

2.3 FUNDS AVAILABLE

It is very important for a client to know how much funds are available for him to invest. The level of funds available will ultimately affect the investment decision. To do this, it is important for everyone to have a personal budget drawn out. The biggest challenge many of us face, about investments is finding enough surplus funds. Most of the time we are engrossed in balancing our income and expenses, and we often forget the need to do a proper budget. Drawing up a personal budget allows a person to take control of spending and find enough money to save and invest for vacations, retirement and your children’s education.

It is important that each client is exposed to the fact, that they would have to do a Cash Flow and Net Worth analysis, before getting into any investment decisions. These analysis will then be able to assist the client to make sure that they have enough money to put aside for investments and that they will be able to follow through with the investments financial obligation. It will be useless if the client agrees to an investment plan purely based on the enthusiasm created by the agent and the prospects of making money. Therefore, having a Cash Flow and Net Worth analysis done is important. For the purpose of this course, we will not indulge in a detailed method of Cash F low and Net Worth analysis but a simple method can be utilized as illustrated below;

9CEILLI

2KEY CONSIDERATIONS IN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

2.4 RISK OR SECURITY

There is a trade-off between expected return and risk that should prevail in a rationalenvironment. Investors unwilling to assume risk must be satisfied with the risk-free rate ofreturn. If they wish to try to earn a larger rate of return, they must be willing to assume a larger risk.

The first thing about learning how to invest in the stock market is to know what kind ofinvestor risk profile you have. In so doing, you will determine how best to allocate your savings amongst various asset classes. Not knowing what kind of risk profile you have or what you are investing in may cost you financially. For example, if an 80 year old is found to own very aggressive funds, or a single person in their twenties has investedpurely in bonds, shows that a risk profiling exercise has not been done. Not having the stomach or r ight disposition may make you cut in and out of investments, that is detrimental to your portfolio and before long, you will find yourself wondering why you are left with a so little money of what you had initially.

What’s Your Investment Risk Profile? Know Yourself!

Investing is a way to make your money work for you so that you can take calculated risks for the promise of a better reward: much better than simply stuffing your money in ahidden corner somewhere in your house. The more you know about risk and how it can affect you and your situation, the better off you will be. Bottom-line: there is a law that states that your returns are directly proportional to the risk you take. I found this definition of risk to be quite adequate:

The concept of “risk” in investment has to do with volatility or how widely the price of a stock or mutual fund fluctuates. The wider the fluctuations, the higher the risk. This isbecause you stand to make and also lose more money, compared to a fund that doesn’t fluctuate as wildly.

Based on the example above, we can say that the client has a positive Net Worth position whereby, we subtract the ASSETS with the LIABILITIES i.e. RM 291,500 – RM 265,500 = RM 26,000.Based on this analysis we can then offer a viable and simple plan that will meet the client’s investment objectives.

We can save some money even if a major portion of our income goes into servicing various debts e.g. home loan, personal loan or for that matter Credit Card bills we have accumulated. As Warren Buffet advises ”you need to first set aside m o n e y f o r investments before thinking about spending it”. You don’t need a million to start investing. You can start with a humble sum of RM 500 per month and see it grow. Based on the availability of funds, the client can then decide which investments should be chosen and invested regularly. If the client can set aside a fixed amount of current income which is a surplus to his needs, then investment options like investment-linked insurance plans, unit trust and the like can be considered.

10 CEILLI

2KEY CONSIDERATIONSIN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

2.5 INVESTMENT HORIZON

Investment horizon can be defined as; the length of time a sum of money is expected to be invested. An individual's investment horizon depends on when and how much money will be needed, and the horizon influences the optimal investment strategy. In general, the shorter the investor's horizon, the less risk he/she should be willing to accept.

Basically Investment horizon can be defined as the total length of time that an investorexpects to hold a security or a portfolio. The investment horizon is used to determine the investor's income needs and desired risk exposure, which is then used to aid insecurity selection.

2.6 ACCESSIBILITY OF FUNDS

We should understand that a client will invest with an objective to make money and he will need the money to settle a specific event. With this in mind, we can divide the accessibilityof funds into 3 clear components;

Risk profiling test and many others like it tend to concentrate on finding out your age, strength of income, family situation, current financial picture, overall tendencies and investment disposition. I would say that one other important element in figuring out where you stand as an investor is, how sophisticated you are and what kind of experience you have with investing. Ultimately, your overall background and attitude about investing will affect how you should proceed.

Following on from this investment concept, “aggressive” or “high risk” means that a mutual fund or stock can potentially achieve higher returns because of greater volatility. In contrast, “low risk” or “conservative” means that a stock or mutual fund will trade close to itshistorical average prices and will tend to be quite stable.

If a client needs the fund in a short p e r i o d o f time, the client would not want to place his money in an investment, that will not allow him to unlock it in a time frame that is short. It would be meaningless for him to place his investments in a long terminvestments like real estate or long term bond funds. When he decides to take the money back, he might not be able to realize the returns expected and at times might have to pay a penalty for exiting early.

The second element is the cost or penalty that the client has to pay if he exits early. This is important because if the cost is going to be very big then it defeats the purpose of the investment objectives. Thus it is important to make sure that the funds can be taken out without having to pay hefty penalties.

The third considerat ion is how much is i t going to cost the client to get into an investment? It is important for us to tell the client the exact amount of money that is needed to set up the investment account and its cost. It would be very helpful if we can clear this upfront with the client before the investment is set up.

a)

b)

c)

11CEILLI

2KEY CONSIDERATIONS IN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

2.7 TAXATION TREATMENT

A client should consider the different tax treatment on different types of investmentsbefore making a decision on what to invest. Different types of investment portfolios attract or enjoy a wide range of tax treatment. Knowing how the tax treatment for the particular investment portfolio is important before the investment decisions are made.

As far as Investment-Link insurance is concerned, there is no specific tax laws regarding this and the Investment-Linked plans enjoy the same tax treatment as the traditional plans. (Chapter 10 will deal with the tax issues in detail).

2.8 PERFORMANCE OF THE INVESTMENT

The performance of an investment depends on the following factors:

These are some of the considerations that must be taken into account when we make an investment decision.

a) Country’s economic factors.

b) Regional and Global economic factors.

c) The competencies and capabilities of the management team.

e) Performance also depends on the past experience.f) History of the invested company..

g) Life cycle of the investment.

d) The invested company’s level of costs.

2.9 DIVERSIFICATION

Diversification in investment is the process of investing across different asset classes andacross different market segments. Diversification is a strategy used by professional fund managers that has proven effective, in reducing risk without sacrificing returns. Investors should also try to invest in a range of investment vehicles when they decide on their investment portfolio.

Diversification can substantially reduce risk with small reductions in return. It involves the spreading of risks by putting the money under management into several categories of investments such as shares, bonds, money market instruments and real estate investment trust(REITs). Diversification can also be achieved by buying shares in different countries and by choosing different types of shares.

Chapter 3 will discuss these areas in detail and illustrate the various options available in investments for the clients.

12 CEILLI

2KEY CONSIDERATIONSIN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

SELF-ASSESSMENT QUESTIONS

Why do you think, client’s nowadays are averse to investments?1.

The adverse economic conditions, in the last 15 years, have made them be wary of investments.The fall of many established financial institutions in the last few years.The stock market cannot be approached by ordinary people.Many investors have seen their fortunes dwindling, due to the financial crisis.

i.

ii.iii.iv.

i,ii,iii only.i,ii,iv only.ii,iii,iv only.i,ii,iii,iv.

a.b.c.d.

CHAPTER 2

An agent owes the client a moral obligation to...2.

educate a client to be an expert investor.to recommend specific funds to invest in.educate clients’ with some basic and sound investment principles.make decisions on behalf of the client.

a.b.c.d.

What considerations must be taken before making an investment decision?3.

Investment objectives, Availability of Funds, Diversification.Risk or Security, Promised Money, Tax issues.Investment Horizon, Performance of Investment, Accessibility of Funds.Economic Reports, Insurance Companies Asset base, Government Regulations.

i.ii.iii.iv.

i.iii only.i,ii only.i,iv only.iii,iv only.

a.b.c.d.

Clients want to invest;4.

to lead a comfortable lifestyle.to be comfortable during retirement.to amass great wealth.to provide adequate funding for their children’s needs.

i.ii.iii.iv.

i,iii.iv only.i,ii,iii only.i,ii,iv only.ii,iii,iv only.

a.b.c.d.

13CEILLI

2KEY CONSIDERATIONS IN INVESTMENT

K E Y C O N S I C E R A T I O N S I N I N V E S T M E N T

What must an agent do to ensure the client is given proper advice on investment?5.

Ensure that there is a right combination of objectives and make sure proper risk analysis is done.Show the wide selection of investment for the client to choose from.Motivate the client to borrow money to invest in guaranteed investment vehicles.Ensure that the advice is advantageous to the agent and the insurance company.

a.

b.c.d.

Why is diversification in investment recommended?6.

So as not to be exposed in one particular class of investments.To even out market fluctuations and not suffer too much losses.To ensure the investments will always do well.To ensure that they can realise their financial objectives faster.

i.ii.iii.iv.

i, iii only.i,ii only.ii,iv only.iii,iv only.

a.b.c.d.

YOU WILL FIND THE ANSWERS AT THE BACK OF THE BOOK.

14 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.1 INTRODUCTION

It is now possible for Malaysians to invest in a wide range of investment vehicles. Over the last 15 years the choices made available has been steadily improved and it is heartening to know that the Government is very pro-active in promoting the growth of these areas. It is also a sign of success when we see F inancia l Ins t i tu t ions and the man on the street responding positively to the new investment choices. In this chapter, we will look at the range of investment choices available to individual investors.

3.2 INVESTMENT CHOICES

3.3 CASH & DEPOSITS

The term cash and deposits refers to all liquid instruments that carry little or no risk. The possi-bility of losing the principal amount invested is very low.

Strictly speaking however, cash cannot be considered as an investment. Cash is, ultimately, used as a means only to finance investments. The capital value of cash will not increase and will not generate any additional income. It has no value in itself. It is of value only as a medium of exchange.

For the purpose of this course however, the definition of cash will include short-term debt instruments. These cover:-

a) Treasury Bills.

b) Bank accounts.

The common instruments available include;

Cash and Deposits. Fixed Income Securities. Shares. Unit Trusts. Investment Trusts. Properties. Derivatives. Commodities. Life Insurance. Annuities. Exchange Traded Funds. Sukuk Bonds. Real Estate Investment Trusts. Capital Guaranteed Funds.

15CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.3.1 TREASURY BILLSThe Government plays a very important part in the life of its citizens. It has to make sure that the country has adequate amenit ies and ut i l i t ies that will serve the people well. Roads, schools, hospitals, security inside and outside the country have to be taken care off. This list is not exhaustive. To a large extend, the Malaysian Government finances these amenities funded by the taxes collected by the Government. However, total governmentexpenditure cannot be fully funded by taxes alone, thus the government has to come up with some borrowing on a short-term basis.

One of the methods used by the Government to borrow money from its citizens is via the issuance of Treasury Bills. These are short-term government funding vehicles issued on a regular basis with repayment normally within a year. The Treasury Bills are issued by Bank Negara Malaysia to the discount market. They are the safest type of investments and are considered to be of no risk except if the country is politically unstable.

3.3.2 BANK ACCOUNTS

These are time or fixed deposits placed with banks for fixed periods with fixed interest rates for that period. Generally, the longer the deposit period, the higher will be the interest rate. Some of the accounts available are Savings Accounts, Current Accounts, Fixed Deposits, Investment Accounts, Time Deposits and Offshore Accounts.

The factors that may influence the choice of deposits are as follows;

Funds available for investment. The duration the funds can remain in the account. Will there be emergency withdrawals. Prevailing market conditions.

As all banks in Malaysia are licensed and regulated by Bank Negara Malaysia, there is very little risk of loss of principal and interest. The Malaysian government has at all times assured depositors that their money is safe with the banks. A good initiative to further strengthen the confidence level of depositors, was the setting up of PERBADANAN INSURANS DEPOSIT MALAYSIA (PIDM).

PERBADANAN INSURANS DEPOSIT MALAYSIA (PIDM).

PIDM is a Government agency established under the Akta Perbadanan Insurans DepositMalaysia 2005 to protect you against, the loss of your deposits in the unlikely event of a bank failure, and promote financial system stability.

PIDM was set up to protect Islamic and c o n v e n t i o n a l d e p o s i t s , provide incentives for promoting sound risk management and promote and contribute to the stability of the financial system in Malaysia.

16 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

What Is Deposit Insurance?

Deposit insurance is a system that protects depositors against the loss of their insured deposits,placed with banks in the unlikely event of a bank failure. It is established by the Government to enhance the consumer protection framework and promote financial system stability. It is notrelated to or managed by general or life insurance companies. Generally, it is a Government sponsored scheme, although in certain countries it is sponsored by the banks.

The deposit insurance system in Malaysia was launched in September 2005 and is managed by Perbadanan Insurans Deposit Malaysia (PIDM). PIDM is a Government agency establishedunder the Akta Perbadanan Insurans Deposit Malaysia 2005.

The benefits to depositors are :-

Deposit insurance protection is automatic. PIDM protects depositors holding deposits with banks. There is no charge to depositors for deposit insurance protection. Should a bank fail, PIDM will promptly reimburse depositors their deposits.

The benefits to the financial system are :-

PIDM promotes public confidence in the Malaysian financial system by protecting depositors against the loss of their deposits.

PIDM reinforces and complements the existing regulatory and supervisory framework by providing incentives for sound risk management in the financial system. PIDM minimises costs to the financial system by finding least cost solutions to resolve troubled banks. PIDM contributes to the stability of the financial system by dealing with bank failures expeditiously and reimbursing depositors promptly.

With the introduction of a deposit insurance system in Malaysia, depositors receive protectionfor their deposits under the law. Depositors will know how and when reimbursement of their deposits will be made in the event of a bank failure.

As set in the Akta Perbadanan Insurans Deposit Malaysia 2005 PIDM’s objectives are as follows :-

Administer a deposit insurance system. Provide insurance against the loss of part or all of deposits of a financial institution. Provide incentives for sound risk management in the financial system. Promote and contribute to the stability of the Malaysian financial system.

Besides the above mentioned objectives, PIDM's main functions are to :-

Assess and collect premiums or fees from banks. Manage the Deposit Insurance Funds. Undertake resolution of non-viable banks. Reimburse depositors should a bank become insolvent. Comply with Shariah principles in respect of Islamic deposits and funds. Conduct ongoing public awareness and education initiatives.

17CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.4 FIXED INCOME SECURITIES

A group of investment vehicles that offer a fixed periodic return is known as Fixed Income Securities. It is a security or certificate showing that the investor has lent money to the issuer, usually a company or a government, in return for fixed interest income and repayment of principal at maturity. Fixed income securities can be regarded as IOUs issued by companies or government to raise funds.

Fixed income securities generally stress current income and offer little or no opportunity for appreciation in value. If there is an active secondary market, they can be bought and sold at anytime before maturity. This marketability gives the investor the opportunity to realise capital gains since fixed income securities prices may rise if interest rates fall. However, if the secondary market is inactive, the investors’ money is locked up for the full life span of the security.

The types of Fixed Income Securities include :- a) Money Market Instruments (as discussed under 3.3 on Cash and Deposits). b) Government Bonds. c) Corporate Bonds. d) Preference Shares (discussed under 3.5 on Shares later in this chapter).

3.4.1 GOVERNMENT BONDS

Government bonds are effectively financial instruments used by the government to borrow money from the public. Government bonds are the safest types of investments, carrying almost no default or credit risk, since the government guarantees interest payments and repayment of the principal. The term and interest rate of government bonds are fixed and usually issued in multiples of RM 1,000. The investor gets the interest and his capital back on maturity.

Government bonds can be classified according to the maturity period as follows:- Short term bonds, usually less than five years to maturity. Medium term bonds, usually five to ten years to maturity. Long term bonds, usually more than fifteen years to maturity.Government bonds are issued from time to time by the government when it wants to raise money to finance government projects aimed to serve the people of the country.

3.4.1.1 ADVANTAGES AND DISADVANTAGES

Government bonds are backed by the government. They are considered to be very safe. The marketability and income for the future is guaranteed. The only disadvantage is in times of high inflation, capital can be eroded when money is invested in these types of investments.

Deposit insurance is recognised internationally as an important component of a country’s financial safety net and has been implemented in some 100 countries around the world.

18 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.4.2 CORPORATE BONDS

3.4.2.1 DEBENTURE STOCKS

Companies can also issue bonds or loan stocks to raise capital. Just as the governmentraises capital to fund its development programmes, these companies also raise these instruments to fund the growth of their companies operations. Corporate bonds can be classified under three categories. They are as follows :-

Debenture stocks. Loan stocks. Convertible stocks.

Debenture stocks are effectively secured loans to a company. The security is either a fixed charge on the company’s property or some of its assets such as trading stock. If the companydefaults on the loan, the investor can take over the said assets and sell them to get his money back.

Trustees are appointed on the issue of stocks, to supervise the way the company performs its obligations concerning the payment of interest and capital. In the event of a default, the trustees act for the investors.

Like government bonds, debenture stocks pay fixed interest rates for a fixed term at the end of which the capital is repaid.

The company also has an option to repay the debenture stocks earlier, if it wishes to do so. Corporate stocks are not as secure as government bonds as the government does not guarantee them. A company can become insolvent and be unable to pay the interest due. Hopefully, the charge on property would mean that this could be sold to repay the capital, b u t a forced sale might not r a i s e e n o u g h m o n e y to cover the capital.

Interest rates for corporate bonds tend to be higher than government bonds as the security is lower.

3.4.2.2 LOAN STOCKS

These are unsecured loans to a company. Both the interest rate and term are fixed.

If the company defaults, the investor has no security and thus is in the same position as all the other unsecured creditors of the company. The investor may or may not get back his capital depending on the company’s performance. Compared to debentures, loan stocks are much less secure and therefore they carry a higher interest rate.

19CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.4.2.3 CONVERTIBLE STOCKS

3.4.2.4 ADVANTAGES AND DISADVANTAGES

3.5 SHARES

The difference between convertible stocks and the above two (i.e. debenture and loan stocks) are that, it can be converted to ordinary shares of a company on a fixed date.

On that date therefore, the investor can convert his investment from a fixed interest loan, to being a part owner and is entitled to a share of its profits through dividends declared. The decision to convert depends on whether dividend income and capital appreciation in share price are better than the fixed interest given.

In general, corporate bonds tend to give a higher return than government bonds. For some investors, they are also m o r e m a r k e t a b l e a n d can be sold for capital gains. However, they are more risky than government bonds.

Shares are different from stocks, in that, a shareholder is a part owner of the company. A company is a separate legal entity, which is to say, that it is owned by all of its shareholders. The shareholders control the company through the fact, that basically each share carries one vote at company meetings. The shareholders can then decide on major issues and vote in new directors to run the company if they wish. Shareholders are not liable for the debts of the company.

Each company maintains a register of each shareholder and each shareholder gets a share certificate as evidence of ownership.

Companies can be public or private. Generally, private company shares are not listed in the Stock Exchange and are not available to ordinary investors. Public limited company shares can be quoted in the Stock Exchange if they meet the Exchange’s requirements.

Shares of listed companies are easy to buy and sell through stockbrokers. In theory, the shares can be bought and sold on any working day, although on a new issue of shares in a popular company, there may be more would be buyers than shares available. Equally, if a company is in trouble, there may be no buyers at all.

The value of a share fluctuates according to the market’s view of the worth of the company. If a company is doing well, its share prices will tend to rise and if it is doing badly it will tend to fall.

20 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.5.1 ORDINARY SHARES

Share prices are also influenced by other factors, such as how the country’s economy is doing in the overall sense, the general level of interest rates, inflation rate, company’s earnings and currency performance. Since we are living in a more connected globalised era, sometimes adverse events in other countries and adverse performance of other major stock exchanges wi l l also affect the performance of the local stock exchange.

A share can thus, be a volatile investment. A shareholder must therefore realise that he could lose all his money in the invested share. In theory, the chances of this happening should be reduced by investing in shares of large, well established, well managed and reputable companies, but events like the Asian Financial Crisis in 1998 and the Global Financial Crisis in 2008 has shown, that this rule of thumb can sometimes be wrong in real life.

The cost of buying and sell ing shares include stockbroker’s commission as well as the difference between buying price and selling price.

In this section we will dissect the following :-

a) Ordinary Shares.

b) Preference Shares.

The holder of an ordinary share in a company is a part owner of the company and is entitled to share in its profits in the form of divide n d s . D ividends are paid out of the company’s profits as decided by the directors.

There is no certainty that a company will make profits and thus there is no certainty that there will be a dividend. However, a company’s track record can be inspected to judge whether profits are likely to be made and dividends paid.

Dividends are usually paid bi-annually, and provide income from the investment to the shareholders.

An investor will also hope to make a capital gain from the shares by an increase in the share price, although this is in no way guaranteed. The price of a listed share will fluctuate from day to day according to the company’s progress and general economic conditions. Announcements of high profits and dividends will tend to increase the price. Low profits have the opposite effect.

A shareholder can always realise his investment by selling the shares. This may be easy for a successful, listed company. Shares are thus a risky investment. An investor could lose all his money, particularly if he only invests in one company’s shares. A portfolio of shares in different companies is thus more advisable than having al l one’s eggs in one basket. Dividends on shares are paid net of basic tax rate. Profits that are made via capital gains are not liable to tax.

21CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.5.2 PREFERENCE SHARES

3.5.3 ADVANTAGES AND DISADVANTAGES

3.6 UNIT TRUSTS

By investing in shares, the investors participate directly in the future of the company. Shares also provide good dividends and capital appreciation. They are also very liquid, as shares can be traded in the open market. However, as mentioned before, shares can be very risky as the value can go below the price the shares were originally bought for.

These are shares which gives the holder a right to a fixed dividend provided enough profit has been made. This right takes precedence over the right of ordinary shareholders to dividends. Preference shares differ from stocks, in that although the income is fixed, it is not interest payment and they may not be paid if profits are not made.

Preference shares differ from ordinary shares in that the dividend will never be more than the fixed rate, even if profits are more than enough to cover it. They are therefore, slightly more secure than ordinary shares but less profitable.

Unit trusts are useful vehicles for small private investors. This is true when investors, who do not have sufficient funds and/or time, to receive the benefit of professional investment management, access to a diversified range and spread of investments which is not readily available to them individually. The investment in unit trusts could generate income in the form of dividends, interest and capital gains.

In Malaysia, unit trusts are author ised and supervised by the Securities Commission.

A unit trust is a pool of funds contributed by many investors kept in trust by a trustee(usually a bank) and managed by a professional fund manager.

A unit trust is established by a trust deed. This deed enables a trustee to hold the pool of money and assets in trust on behalf of the investors. Another party, the investmentmanager (also called fund manager), manages the pool. The fund manager manages the portfolio of investments and operates the market for the investments (i.e. administers the buying and selling of shares in the unit trust itself). The unit trust is essentially a three-way arrangement among investors, the trustee and the fund manager.

The investments of the unit trusts, though selected and managed by the fund managers, are legally owned and held by the trustee for the benefit of the investors (who are the unit-holders). The trustee must ensure that the fund managers adhere to the provisions of the trust deeds and act accordingly to protect the unit-holders.

22 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.6.1 ADVANTAGES AND DISADVANTAGES

Investors buy units in the unit trust at the offer price calculated as per the trust deed. Units can be sold back at any time at the bid price.

It is not necessary to use a stockbroker and sales can be made without the need to find a purchaser, as would be in the case of shares. The fund manager can create as many new units as investors require and can cancel units, if new purchases are exceeded by encashment, i.e. the amount of cash that the units can be converted into.

Unit trusts however have no fixed redemption date. The trusts are open-ended funds and, if too many investors cash their units, the trust will have to sell the fund’s assets.

The unit trust investments fluctuate in line with the stock market prices and it also involves up-front charges. Unit trusts should not be seen as a very short-term investments option.

When investing in Unit Trusts, an investor can choose from an array of unit trusts funds with different investment objectives. These unit trusts can also be invested in a wide range of market instruments to provide the diverse appetite of the investor. A unit trust may aim for high income or a high capital growth, or a combination of both. Some unit trusts also invest in specific countries or regions.

It is important that the types of unit trusts chosen, match the investment objectives of the particular investor. All unit trusts are required to clearly state their investment objectives in their prospectus. Every investor should have this prospectus and read and understand it before buying into the trust. The types of assets that may be bought by the fund manager are also specif ied in the object ives of the trust c o ntained in the trust deed.

Examples of unit trusts include those marketed by Amanah Saham Nasional, Public Mutual Fund, Hwang DBS and a whole lot more.

The advantage in unit trusts is the spread of investments open to unit-holders. In addition, unit trusts have lower risks when compared to shares. Furthermore, professional investment services are provided by the fund managers and this minimises paper work to the investing unit-holders. Income from dividend can also be reinvested. Nowadays, the investor can utilise a portion of his contribution to the Employees’ Provident Fund (EPF) from account A to purchase EPF approved unit trusts from the Unit Trusts companies in Malaysia. This withdrawal can also be done on a regular basis provided all EPF terms and conditions are met.

The trust deed sets out :- The fund manager’s investment powers; The price structure; The registration of unit-holders; The remuneration to the fund managers; The accounting and auditing rules.

23CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.7 INVESTMENT TRUSTS

3.7.1 ADVANTAGES AND DISADVANTAGES

The function of the investment trust is similar to that of unit trusts, i.e. to make investment much simpler, more accessible and more cost effective for small investors.

It is important, however, to recognise that an Investment Trust Company, is a company registered under the Companies Act. An investor is therefore purchasing shares in that company. The company itself will invest in a wide range of equities and other investments.

Investment trusts, like unit trusts, both pool contributions from their investors, and the total fund is then managed by specialist fund managers, whose function is to buy and sell shares of the trust to make investment profits.

Those profits increase the value of the fund and the value of each investor’s share, if the fund increases. If the trusts suffer losses then the investor’s share will be reduced in value and the price of his units will fall.

The unit prices are recalculated every day and quoted daily in at least one national Bahasa Malaysia newspaper and one national English newspaper. The price reflects the value of the underlying investments.

If the Investment Trust has 10 million units and the investments could be sold for RM 20 million, then the bid price will be RM 2 per unit. There is a spread, generally around 5% between the bid and offer price, which is effectively a form of charge. There is also an annual management fee deducted by the fund managers from the income of the trust.

Investment trusts should also not be seen as very short term investments of less than, preferably,three years. Investment trust generally has a higher risk/reward profile than unit trusts.

Examples of an Investment trust is the listed Seacorp Schroders, ICapital.biz

These are similar to unit trusts mentioned above, except that investment trusts are more flexible as investors can borrow to finance their purchases of the investment trusts. This can be very beneficial to the investment trust holders. However, with the flexibility to borrow funds to purchase the investment trusts also means that investors are open to greater risk exposures if the price of investments suddenly goes down.

The disadvantage in unit trusts includes the bewildering array of funds, the extra costs or charges which must be paid when purchasing the units and also when switching from one fund to another.

24 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.8 PROPERTIES

3.8.1 REAL ESTATE INVESTMENT TRUST. (REITs)

Real Estates have always been part of the investment scene. There are basically three types of real estate investments. These are agricultural property, domestic property and commercial/industrial property both locally and overseas.

The price of an agricultural property depends on the following factors;

Quality of land as reflected on the quality and profitability of crops it grows. The location of the land. The value of the buildings on the land.

On the other hand, the price of domestic and commercial/industrial properties generally depends on the location and types of buildings on the land.

Besides investing in the original form of Real Estate properties i.e. land, building, houses etc, there is now a new form of real estate investment available to the Malaysian public. It is known as Real Estate Investment Trust ( REITs).

A new asset class investment option has emerged with potential fair return of investment in Malaysia. REIT - also known as Real Estate Investment Trust has a similiar concept like unit trust.It operates in a similiar fashion like unit trust whereby money that goes into this investment is gathered from all size of investors. REITs based companies will invest, manage and distribute rental as dividend back to the investors. It is also being trade in Bursa Kuala Lumpur with ease of buying and selling back like a normal equity.

REITs is not new to the world, in many other developed countries, REITs has been developed for decades - with steady fixed income as opposed to fixed deposit as an alternative.It targets long term investor with moderate risk such as insurance companies, pension funds, unit trust funds and even individual investor. As many investors may not be able to invest in a huge property portfolio, REITs gain strength from pool of funds gathered from the investors and is invested into high profile and high value properties for better return.

REIT returns averagely in develop market is around 3-5% depending on its individual performance.However, REITs in Malaysia are very attractive because, as we are in a so-called last phase of becoming a developed nation, our nation’s property’s values are still behind many developed countries in Asia. This emerges as an opportunity with average attractive yields between 6-8% which is higher than other major developed countries.

As our nation property’s value is undervalued for decades, there will be a high potential of asset revaluation that will bring capital growth to the investor. Typical a potential return will be between 20-30% around a five year period.

25CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.8.2 ADVANTAGES AND DISADVANTAGES

STAREIT, launched in 2006 has, to date, performed at a 7% dividend yield return based on the Net Tangible Asset (NTA) of 97 sen. If compared to fixed deposit of 3-4% and even with goverment based senior citizen bond that offer 5.5%, STAREIT becomes much more attractive to investors in general.

A high perfomance reit is like your property fund manager. They will develop new opportunities, acquire more properties into their portfolios locally and some countries and jointly develop property projects. This will provide even a higher potential return compared to those low to moderate risk investment instruments.

Thus, if you are trying to find a good investment tool for your long term retirement plan, do consider REITs in Malaysia within the next few years. REITs will be attractive with a fair risk to be tolerated compared to Fixed Deposit. As equities are high risk to some extent, bonds have relatively moderate returns, investing in property directly will require high capital investment and also you have to manage all these investment portfolios yourself. REITs will be a good choice as an alternative asset class for investment.

Properties can provide good capital appreciation and a steady flow of income. They are therefore, considered low risk investment especially if you have good tenants and good repayment methods are obtained. By mortgaging the property, capital can also be freed. However, during economic recession, property could be difficult to be disposed off.

3.9 DERIVATIVES

Instead of buying a security outright, an investor can buy a derivative of the security instead. Derivatives are financial instruments whose values are linked to the price of underlyinginstruments in the cash markets. For example, a stock index future is linked to the performance of a specified stock market. Stock options and financial futures are two popular derivative instruments for investors.

3.9.1 OPTIONS

Rather than trading directly in a security, investors can buy a right, not an obligation, to purchase or sell the security at a future date. This is called an option. Option need not be exercised, and often will not be worth exercising.

26 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

A share option is a financial instrument that gives the investor the right to buy or sell a given number of shares of the underlying stock at a fixed price within a specified time period.

The life of an option may vary but the common duration adopted is three, six and nine months. Over-the-counter options can also be bought by institutions for longer periods, from one to five years.

A call option gives the holder of the option the right to buy(or ‘call away’), say, 100 shares of a particular stock at a specified price, premium, any time, prior to the specified expiration date.

A put option gives the holder of this option the right to sell (or ‘put away’), say, 100 shares of a particular stock at a specified price prior to a specified expiration date.

Investors purchasing call options will be hoping that the share price will rise so that when the option is exercised, the premium plus the fixed price will be less than the value of the shares. Call options, therefore permit investors to speculate on a rise in the price of the underlying shares without buying the shares itself.

Investors purchase put options if they expect the share price to fall, because the value of the put options will rise as the share price declines. Put options allow investors to speculate on a decline in the share price without selling the shares short.

Sellers of either of these options will want the reverse to happen so the options will not be exercised and they will profit by the amount of the premium.

3.9.1.1 ADVANTAGES AND DISADVANTAGES

By investing in options the investor has the potential to boost profits from share price movements. However, investing in options is also risky as an investor must be prepared to lose all his money.

3.9.2 WARRANTS (TRANSFERABLE SUBSCRIPTION RIGHTS [TSR])

Warrants are similar to that of the call options. A warrant is a corporate-created option to purchase, within a specified time period, a stated number of shares of the underlying stock at a specified price.

Warrants, also known as Transferable Subscription Rights (TSR), give the holder of the option to subscribe the shares in the company

At a pre-determined ratio ( conversion ratio); At a pre-determined subscription price ( exercise price); and

Within a specified time period. The life span of a warrant is fixed at the beginning and cannot be varied.

27CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.9.2.1 ADVANTAGES AND DISADVANTAGES

Warrants typically have maturities of at least several years, and their terms are notstandardised. Each warrant is unique.

Warrants are seldom issued on their own, but are often issued free and attached to rights or loan stocks as an added attraction or sweetener allowing the corporate issuer to obtain a lower interest rate (i.e. financing cost). Warrants can be detached from the loan stock and sold separately in the securities market. The options attached to the warrants can be exercised by subscribing for ordinary shares in cash, by exchanging the loan stock or by a combination of both.

Purchasing warrants is one benefit to investors without a large initial outlay to establish an exposure to shares. The investor will buy the warrant, pay the exercise price at a later date and convert the warrant to the underlying share.

By selling the warrants given to him in the first instance, an investor can benefit from the capital gain. When the price of the underlying shares goes up, the investor may profit by selling the warrant or exercise it to get the stock.

The disadvantage of the warrants is that on expiry, warrants which are not exercised lose their value completely. Unlike ordinary shares, there is no chance for price recovery. Once the warrant has expired, it is worthless. In addition, holders of warrants do not receive any income in the form of interest or dividends. They also carry no voting privileges.

3.9.3 FUTURES

Physical commodities and financial instruments typically are traded in cash markets. A cash contract calls for immediate delivery and is used by those who need a commodity now. Cash contracts cannot be cancelled unless both parties agree. The current cashprices of commodities and financial instruments can be found daily in such sources as the business pages of the national newspapers.

There are two types of cash markets:- spot markets and forward markets. Spot markets are markets for immediate delivery. The spot price refers to the current market price of an item available for immediate delivery. Forward markets are markets for deferred delivery. The forward price of an item is the price of an item for deferred delivery.

Forward contracts are centuries old, traceable to at least the ancient Romans and Greeks. Organised future markets, on the other hand, only go back to the 1860s, with financial futures being relatively new, dating from the introduction of foreign currency futures in 1972.

28 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

Futures markets are, in effect, organised and standard i sed forward markets. An organised futures exchange standardised the non-standard forward contracts, establishing such features as contract s ize, delivery dates and condition of the items that can be delivered. Only the price and the number of the contracts are left for the future traders to negotiate. Individuals can trade without personal contact with each other because of the centralised market place. Performance is guaranteed by a clearinghouse, relieving one party to the transaction from worry, that the other party will fail to honour its commitments.

A future contract between two parties (the buyer and the seller) thus set a price today for an instrument that will be delivered on a specified future date. Stock index futures are futures contracts, based on a particular share price index, constructed to measure the overall price movement of a stock market.

The trading of the index futures involves standardised contracts to buy or sell a hypothetical portfolio of all stocks included in the index at some specified future date, at a price agreed at the time of the deal.

The buyers agree to take delivery and to make cash payment at expiry date, and the sellers agree to make delivery at the same time. The settlement of the contracts is made in cash without the actual delivery of the securities covered by the index. The profit derived from trading stock index futures is determined by comparing the original contract value with the contract value at the time of settlement.

3.9.3.1 ADVANTAGES AND DISADVANTAGES

The futures market serves a valuable economic purpose by enabling investors to protect their investments (or hedging) by taking positions, in the futures market to protect the gains they have made in the cash market. The risk of price fluctuations is shifted from participants unwilling to assume such risk, to those who are.

Another economic function performed by futures market is price discovery. Because the price of the futures contract reflects current expectations about the values at some future date, transactions can establish current prices against later transactions.

An investor may also wish to engage in speculative trading and takes on price fluctuation risks in order to have a chance at making large gains. However, a clear understanding of the concept of hedging (which can be briefly described as, assuming of futures positions opposite to cash positions, in an attempt to minimise the risk of financial loss from adverse price changes) and the amount of gain or loss that could result from any change in the price of the index futures contracts is necessary before an investor ventures intoinvesting some of the money in futures contracts.

29CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

3.10 EXCHANGE TRADED FUNDS (ETF)

An exchange-traded fund (ETF), also known as an exchange-traded product (ETP), is an investment fund traded on stock exchanges, much like stocks. An ETF holds assets such as stocks or bonds and trades, at approximately the same price as the net asset value of its underlying assets, over the course of the trading day. Most ETFs track an index, such as the S&P 500 or MSCI EAFE. ETFs may be attractive as investments because of their low costs, tax efficiency, and stock-like features.

Only so-called authorized participants (typically, large institutional investors) actually buy or sell shares of an ETF directly f rom/to the fund manager, and then only in creationunits, large blocks of tens of thousands of ETF shares, which are usually exchanged in-kind with baskets of the underlying securities. Authorized participants may wish to invest in the ETF shares long-term, but usually act as market makers on the open market, using their ability to exchange creation units with their underlying securities to provide liquidity of the ETF shares and help ensure that their intraday market price approximates to the net asset value of the underlying assets. Other investors, such as individuals using a retail broker, trade ETF shares on this secondary market.

An ETF combines the valuation feature of a mutual fund or unit investment trust, which can be bought or sold at the end of each trading day for its net asset value, with the tradability feature of a closed-end fund, which trades throughout the trading day at prices that may be more or less than its net asset value. Closed-end funds are not considered to be "ETFs", even though they are funds and are traded on an exchange. ETFs have been available in the US since 1993 and in Europe since 1999. ETFs traditionally have been index funds, but in 2008 the U.S. Securities and Exchange Commission began to authorize the creation of actively managed ETFs.

Types of ETFs a) Index ETFs b) Commodity ETFs or ETCs c) Bond ETFs d) Currency ETF or ETCs e) Actively managed ETFs f) Exchange-traded grantor trusts g) Leveraged ETF

3.11 SUKUK BONDS

Sukuk is the Arabic name for financial certificates, commonly referring to the Islamic equivalent of bonds. Since fixed income, interest bearing bonds are not permissible in Islam, Sukuk securities are structured to comply with the Islamic law and its investment principles, which prohibits the charging, or paying of interest. Financial assets that complywith the Islamic law can be classif ied in accordance with their tradabil ity andnon-tradability in the secondary markets.

30 CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

Conservative estimates by the Ten-Year Framework and Strategies suggest that over $1.2 trillion of assets are being managed according to Islamic investment principles. Such principles form part of Shari'ah, which is often understood to be ‘Islamic Law’, but it is actually broader than this, in that it also encompasses the general body of spiritual and moral obligations and duties in Islam. In the Persian Gulf and Asia, Standard & Poorestimates that 20 per cent of banking customers would now spontaneously choose an Islamic financial product over a conventional one with a similar risk-return profile.

The Sukuk is similar to an obligation backed by an asset but is not in anyway a bond because it is not based on debt. It can be regarded as a commercial paper which gives the investor a share of ownership in the underlying asset.

The issuer must identify the assets to be sold to investors by transferring it on an ad hoc basis.

Investors enjoy the division of the assets in proportion to their investment and bear thecredit risk of the issuer.

The Sukuk are therefore equity securities which have the following characteristics:

They are issued by pooled funds (Mutual funds) ;They are based on hard assets that generate steady income and expectations;They may be guaranteed or not by their originators;Investors receive a fee equal to the income of the underlying assets;These securities are issued by Special Purpose Vehicles (SPVs), often subsidiaries of banks or trusts called SPV;Most Sukuk are issued in dollars;The Sukuk differ from conventional bonds because they are based on tangible assetsinstead of being based on the debt;There are about fourteen kinds of Sukuk but the most used today are Sukuk Al Ijara and Sukuk Al Mucharaka.

1.2.3.4.5.

6.7.

8.

3.12 CAPITAL GUARANTEED FUND

Capital Guaranteed Fund is an investment vehicle offered by certain institutions that guarantees the investor's initial capital investment from any losses. Even though these products prevent investors from losing their invested capital, they also limit the amount of return that investors can obtain if the investments appreciate. This is how the offeringinstitutions can afford to guarantee the principal investment.

Definition of Capital Guaranteed Fund (CGF)

CGF is an investment vehicle offered by certain institutions that guarantees the investor’s initial capital investment from any losses. When you invest in a CGF, it is guaranteed that you will not lose any money provided that you don’t redeem your investment before the maturity date.

31CEILLI

3TYPES OF INVESTMENTASSETS

T Y P E S O F I N V E S T M E N T A S S E T S

Features of Capital Guaranteed Fund