cdmelb2015: gilbert + tobin

TRANSCRIPT

What will disrupt the disruption?A journey in Australian legal self awareness

CommsDay MelbourneOctober 2015

Cameron Whittfield and Simon MuysPowered by

2 | What will disrupt the disruption | October 2015

Structure of today’s presentation

A. Setting the scene (a scene like no other we have seen): Our distillation of the most fundamental disruptive forces at play.

B. An assessment of whether we can get out of our own way: Do our regulatory structures (and mindset) give us the ability to adapt? Some self reflection looking at:

•our past performance…

•our current attitudes…

•our potential if we can get out of our own way…

C. Three digital issues that are now well in play: The net neutrality debate, cyber / data vulnerability and new “agile” contracting.

B C

A

2 | What will disrupt the disruption | October 2015

The Australia of the future has to be a nation that is agile, that is innovative, that is creative. We can't be defensive, we can't futureproof ourselves. We have to recognise that the disruption that we see driven by technology, the volatility in change is our friend if we are agile and smart enough to take advantage of it.” M Turnbull – 15 Sept 2015

A. Setting the scene

3 | What will disrupt the disruption | October 2015

4 | What will disrupt the disruption | October 2015

A scene like no other we have seen

Competitors can rise in almost complete stealth

and burst upon the scene...vast new markets are conjured seemingly

from nothing…long term trend lines, once reliably

smooth, now more closely resemble

sawtooth mountain ridges…”

No Ordinary Disruption – Mckinsey, 2015

•Advances in technology and ability for technology to totally disrupt traditional business models

•Cheap debt and the borderless world of online commerce

•The projected imbalance between the overall population at its work force

•The rise and rise of the middle class in China, India…with more to come

Emerging markets

Aging population

Digital disruption

Free flowing

trade

5 | What will disrupt the disruption | October 2015

What is digital disruption…?

+ Technology (as a business and enabler)

+ New business models

+ New entrants

+ New engagement models

+ …but often evolving within an “old world” regulatory environment that simply doesn’t understand what it is…

Suggestion: Stop trying to define digital. It’s not a thing, it’s a way of doing things.

•Advances in technology and ability for technology to totally disrupt traditional business models

Digital disruption

6 | What will disrupt the disruption | October 2015

…but more importantly, what is disruptive innovation?

+ “Disruptive innovation” occurs when existing patterns of work, organisation and hierarchy are radically transformed in a relatively short space of time.

+ Four key steps (with unique legal issues at each step):

• new competitors arrive

• incumbents ignore them or head to higher ground

• disruptors establish a foundation in the middle of the market

• Causes a flip in the market, in which established players must compete on new grounds or risk market share or worse

B. Can we get out of our own way

Three industries show significant upward trends: Technology (+177%), Consumer Services (+163%) and Healthcare(+159%), which are the leading sectors to have grown market cap in the Top 100, driven by innovation and recovery from the financial crisis.

Technology has 2 very impressive risers with Apple and Google. 17 years ago Apple was valued at a few billion USD and Google was just founded. The technology sector predominantly consists of US domiciled companies.PWC, Global Top 100 Companies by Market Cap, March 2015

7 | What will disrupt the disruption | October 2015

8 | What will disrupt the disruption | October 2015

Global Top 100 - Technology

Source: PWC

9 | What will disrupt the disruption | October 2015

A self evident but inconvenient cycle

Disruption is uncomfortable and hard to predictRegulation is comfortable and easy to predictRegulation is usually bad for disruption

Disruption is usually good for consumers

10 | What will disrupt the disruption | October 2015

Australia will struggle to become a leading, disruptive digital economy unless we disrupt our own regulatory mindset

Australian competition law and telecoms/media regulation is rooted in the 20th century

+ ACCC refers to ‘dynamic efficiency’ but seldom relies on it

+ Telecoms regulation remains wedded to ‘structural’ arguments – not debates about incentives and innovation

+ The NBN story – including MTM – is one of government picking winners and trying to guide the invisible hand

… and this old world view continues to seep into current contractual structures and regulatory debates, including NBN and mobiles

11 | What will disrupt the disruption | October 2015

…but why are we like this?

11 | What will disrupt the disruption | October 2015

12 | What will disrupt the disruption | October 2015

First: we have been (understandably) cynical about convergence arriving

+ Waiting for Godot?

• We’ve been talking about “convergence” since 1997

• convergence was seen as a game of infrastructure and scale

+ It has arrived, but now we talk about “disruption” instead because it looks different to what we anticipated

• infrastructure ownership and scale are less important (OTT is the battleground)

• it is not limited to existing telecom/media players

• no/low barriers to entry

• massive disruption from below

13 | What will disrupt the disruption | October 2015

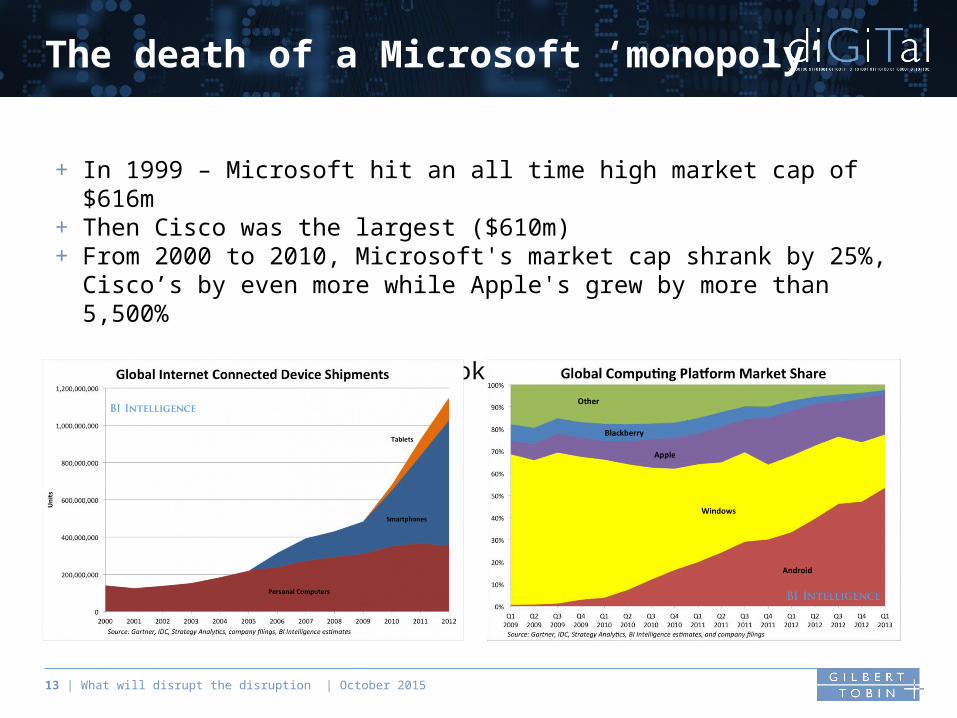

The death of a Microsoft ‘monopoly’

+ In 1999 – Microsoft hit an all time high market cap of $616m+ Then Cisco was the largest ($610m)+ From 2000 to 2010, Microsoft's market cap shrank by 25%, Cisco’s by even

more while Apple's grew by more than 5,500%

… and then Google and Facebook …

14 | What will disrupt the disruption | October 2015

Australian energy comparator websites

15 | What will disrupt the disruption | October 2015

Second: we don’t enjoy change

Government and regulators often try to “manage” innovation and prevent the discomfort of real market disruption

+ The ACCC (and other antitrust authorities) seldom trust dynamic efficiency enough to rely on it, even in digital markets • narrow markets – yet disruption seldom comes from direct competitors• still typically use 20th century structural approaches (“4 to 3”, “cosy duopoly”)• price/value test vs innovation/dynamism• fear (do not embrace) tipping points and network effects• competition for the market (platform) may be more important than competition in the

market – and that is ok!• transient market power

+ We ask governments to make technology bets and funding calls; crowding out private investment (sometimes explicitly)

16 | What will disrupt the disruption | October 2015

ACCC opposes Trading Post / carsales.com EU issues a statement of

objections about Google ShoppingCommences an inquiry into Android terms ACCC issues a

statement of issues about Foxtel taking 15% stake in Ten

ACCC requires undertakings in Video Ezy / Blockbuster

2007

20122015

2015

17 | What will disrupt the disruption | October 2015

… and the telecoms regulatory framework is similar

+ A nationalised, monopoly network with highly complex and rigid regulatory and contractual models• Explicit constraints (commercial and regulatory) on competitive investment• Government technology policy mandates that layer complexity on the

rollout and products

+ ACCC is fretting about the ‘last customer’ problem in regulated pricing of legacy fixed telecoms, postal services and energy networks

+ The constant threat of regulation (or re-regulation) in dynamic markets – e.g. mobiles, content, on-line business models

18 | What will disrupt the disruption | October 2015

What is a ‘disruptive’ mindset?

+ Optimistic about change and uncertainty

+ Not afraid to fail

+ Size doesn’t matter – you are only as successful as your next idea and always vulnerable to someone else’s

+ Global – not parochial

19 | What will disrupt the disruption | October 2015

Is it time to disrupt the regulatory mindset?

+ Red tape reviews and tax breaks for start ups are helpful, but can amount to moving deck chairs

+ A disrupted mindset for a competition or telco regulator:• values innovation as the most important element of competition• accepts the reality of broader market definition (disruption and competition

come from unexpected places) • accepts that tipping points happen and that competition for the market

(platform) can be preferable • no empirical link between size and innovation• takes a dynamic view focused on capability, entry and market dynamics,

rather than market shares • errs on the side of caution and simplicity in digital markets

C. Three digital issues that are well in play

…lovers of print are simply confusing the plate for the food...”Douglas Adams

20 | What will disrupt the disruption | October 2015

21 | What will disrupt the disruption | October 2015

Don’t shoot the gatekeeper…

…it is abundantly clear, the net neutrality debate is far from over…

FCC 2015 Net Neutrality Rules

…and managing / sharing the burden on internet infrastructure is essential…

22 | What will disrupt the disruption | October 2015

Every director is thinking about data crisis management…

In this digital age, there is no place to hide behind public relations people. This digital age requires leaders …to engage in the debate: Gail Kelly

23 | What will disrupt the disruption | October 2015

Agile contracting in the digital economy

+ Cloud, mobility and the Internet of Everything are driving the emergence of a new As-A-Service economy.

+ These changes are driving agility and flexibility into business operations - leading to the development of entirely new commercial models.

+ The emergence of the As-A-Service economy enables businesses to avoid up-front investment in the facilities and resources Instead, they can acquire a bunch of specialised services to run their business operations with:

24 | What will disrupt the disruption | October 2015

MELBOURNE

Level 22101 Collins StreetMelbourne VIC 3000T +61 3 8656 3300F +61 3 8656 3400

PERTH

1202 Hay StreetWest Perth WA 6005T +61 8 9413 8400F +61 8 9413 8444

SYDNEY

Level 372 Park StreetSydney NSW 2000T +61 2 9263 4000F +61 2 9263 4111

+

www.gtlaw.com.au