casualty actuarial society improving and protecting the balance sheet 2002 spring meeting san diego,...

TRANSCRIPT

Casualty Actuarial Society

Improving and Protecting the Balance Sheet

2002 Spring MeetingSan Diego, California

Improving and Protecting the Balance Sheet

• Moderator:Sean R. Devlin, Vice PresidentAmerican Re-Insurance Company

• Panelists:Michael J. Belfatti, Senior Vice President and Chief Actuary, ACE Financial Solutions

Peter J. Doyle, Vice President, American Re-Insurance Company

Agenda

• Environment• Capital Issues• Background of Finite Reinsurance• Accounting Issues• Case Study: Quota Share• Case Study: Adverse Loss Development Cover /

Loss Portfolio Transfer• Questions

Environment

Environment - Recent History

• Several Years of Competitive Pricing

• Under-reserved in recent accident years

• Asbestos refuses to go away

• Poor investment returns

• September 11

Environment – Result of Recent History

• A large percentage of balance sheets are strained

• Many companies are in danger of rating downgrades

Environment – Current Situation

• At long last, the hard market has recently returned

• But, companies may not be strong enough financially to take advantage of it

• Are there reinsurance solutions?

Capital Issues

Capital Issues

• Insurance companies need capital– Buffer against uncertainty– Provides comfort level for prospective

counterparties (e.g., lenders, policyholders)– Required to run the operation and build new

strategic efforts– Assures regulators and rating agencies that

“promise to pay” will be fulfilled.– Avoids “run on bank” mentality.

Capital Issues

• Various Standards for Capital Need Exist– NAIC RBC– AM Best (BCAR/ERM)– S&P– Economic Modeling

Capital Issues

• NAIC RBC– Implemented in mid-90s– Based on statutory financials– Charges to reserves and premium by line– Adjusts for company experience relative to

industry

Capital Issues

• AM Best– Design similar to NAIC RBC– Separate analysis of reserve inadequacy– Based on EPD calibration– Adjustment to “undo” effect of LPT

Capital Issues

• S&P– Traditional reserve and premium charges– Also based on EPD approach (AAA)– Adjust reserves to adequate level– No explicit covariance adjustment

Capital Issues

• Modeled Capital Need– Firms are developing their own view on capital

need• Centralized firmwide risk modeling

• Focus on common risk drivers

• Require assets to meet designated safety standard

– For these models in particular, finite products can reduce variability and capital need

Background of Finite Reinsurance

• History– Pre 1992– limited risk transfer

• Restricted payment timing

– 1992 and Subsequent• FAS 113, SAP 62 require risk transfer

• More delicate balance between risk transfer and risk finance.

– Late 1990s to today• Development of new structures

• Integration of new exposures

• Market has reached some maturity

Background of Finite Reinsurance

• Recent Demand– Response to increased traditional prices

• Covers that spread net lines of multiple years

– Response to reserve deterioration• LPTs

– Need to contain impact of “black hole” exposures• Asbestos

– Continued interest in blending traditional insurance risk with “uninsurable” exposures

• Integrated finite covers

– Companies with need for surplus to support growth• Quota Share

Accounting Issues

Accounting Issues

• Risk transfer

• Retroactive transactions

• Discounting loss reserves

• Offshore carriers

Risk Transfer – FASB 113

• The reinsurer assumes significant insurance risk under the reinsured portions of the underlying insurance contracts.

• It is REASONABLY possible that the reinsurer may realize a SIGNIFICANT loss from the transaction.

Risk Transfer – Deposit Accounting

• If transaction does not pass risk transfer test, it is booked under deposit accounting guidelines

• No initial impact on income statement or reserves

• No income or surplus recognition until loss payments exceed deposit

FASB 113 – Paragraph 11 Exception

… if substantially all of the insurance risk relating to the reinsured portions of the underlying insurance contracts has been assumed by the reinsurer.

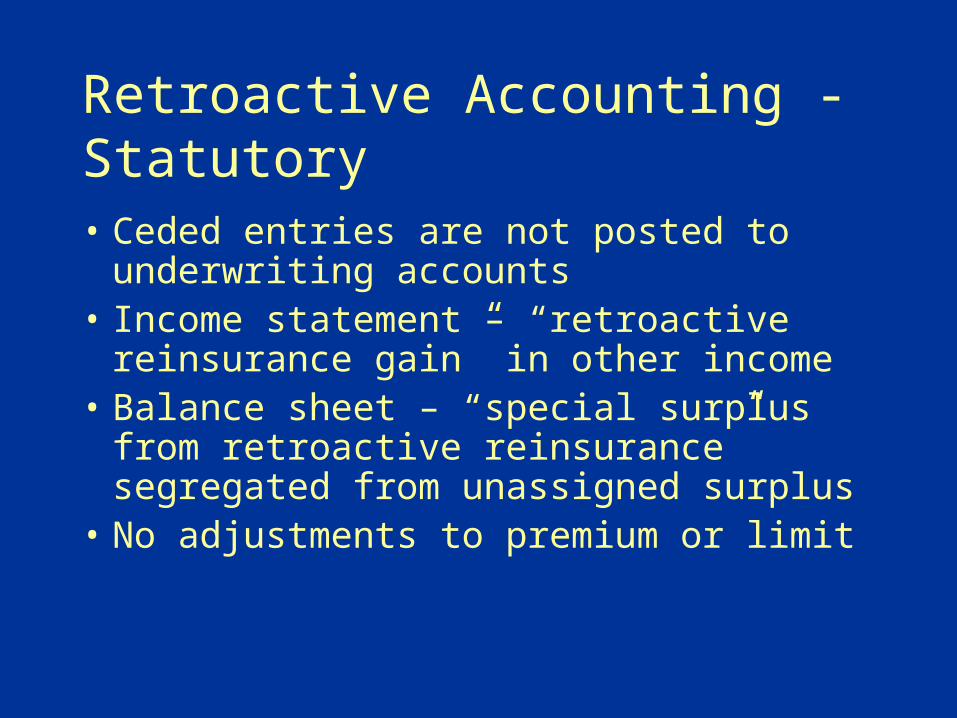

Retroactive Accounting - Statutory

• Ceded entries are not posted to underwriting accounts

• Income statement – “retroactive reinsurance gain” in other income

• Balance sheet – “special surplus from retroactive reinsurance” segregated from unassigned surplus

• No adjustments to premium or limit

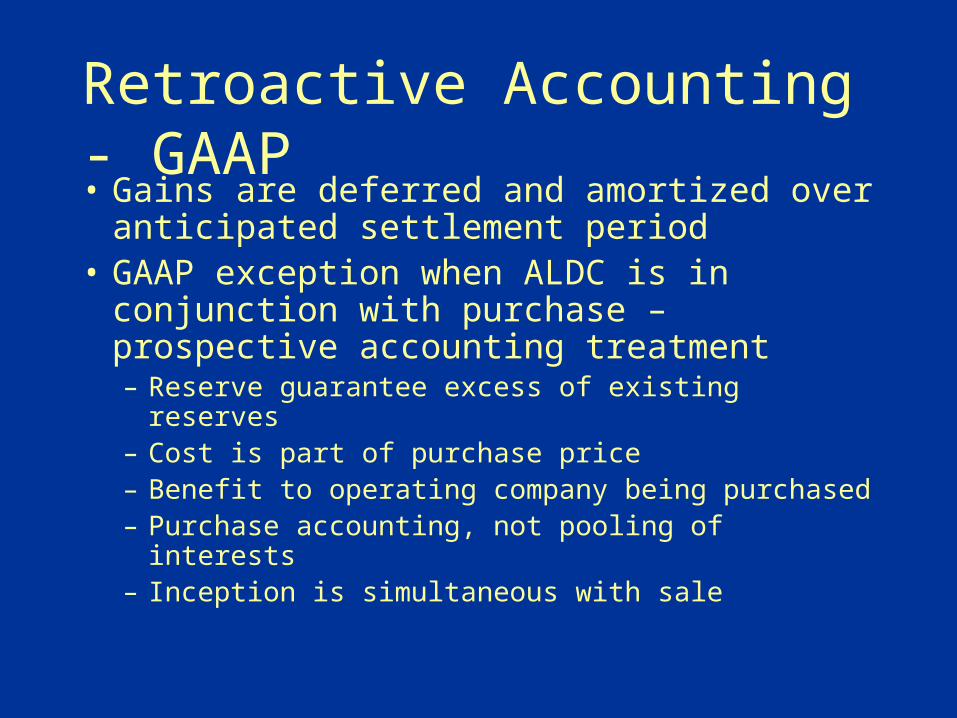

Retroactive Accounting - GAAP• Gains are deferred and amortized over

anticipated settlement period• GAAP exception when ALDC is in

conjunction with purchase – prospective accounting treatment– Reserve guarantee excess of existing reserves– Cost is part of purchase price– Benefit to operating company being purchased– Purchase accounting, not pooling of interests– Inception is simultaneous with sale

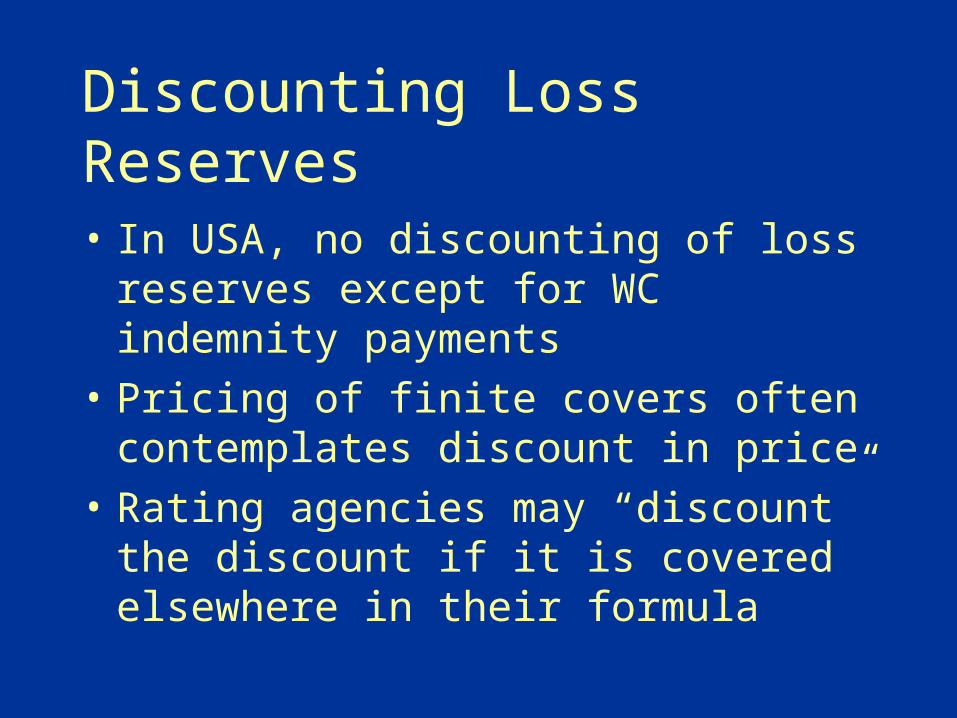

Discounting Loss Reserves

• In USA, no discounting of loss reserves except for WC indemnity payments

• Pricing of finite covers often contemplates discount in price

• Rating agencies may “discount” the discount if it is covered elsewhere in their formula

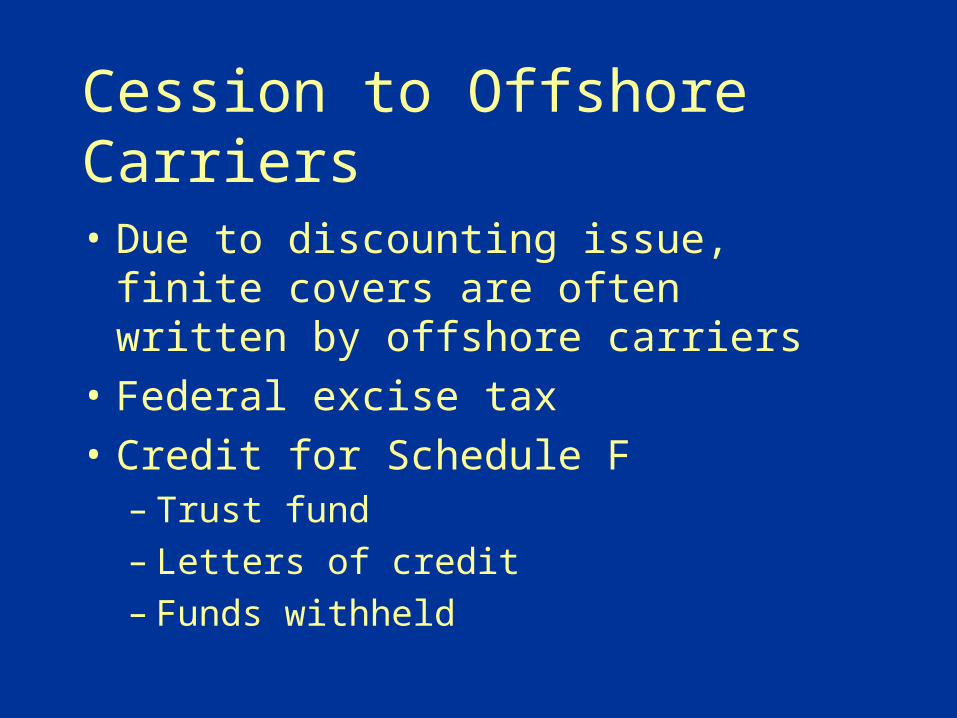

Cession to Offshore Carriers

• Due to discounting issue, finite covers are often written by offshore carriers

• Federal excise tax

• Credit for Schedule F– Trust fund– Letters of credit– Funds withheld

Case Study: Quota Share

Case Study: Quota Share

• Company is currently rated A minus• It is writing close to 3:1 WP-to-PHS• If they take advantage of hard market, ratio

will be greater than 3:1 and rating will be jeopardized

• Quota share is a solution

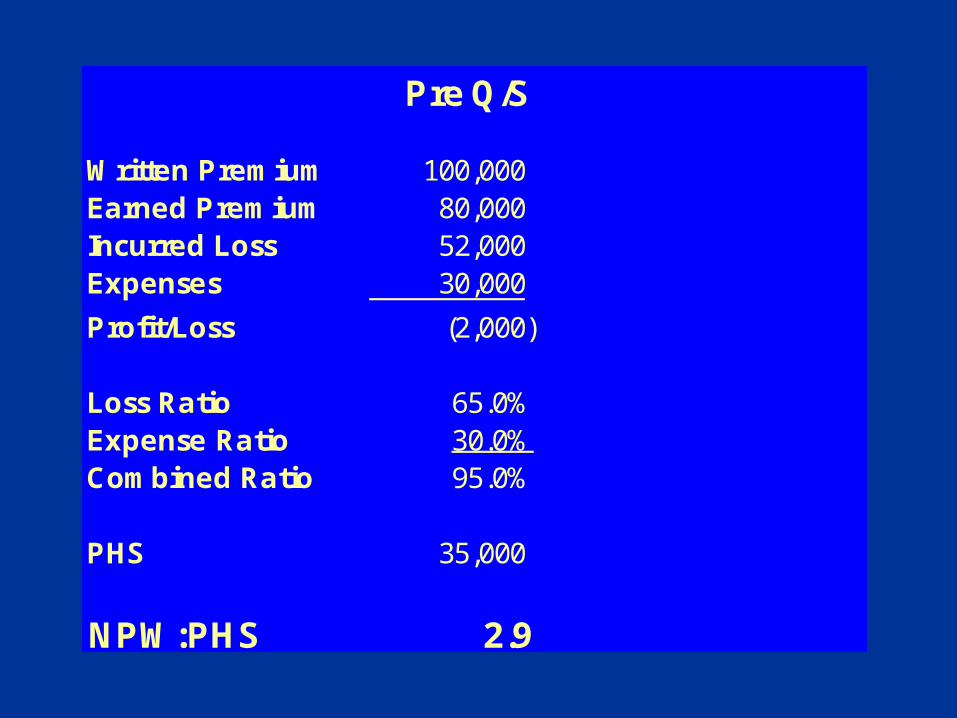

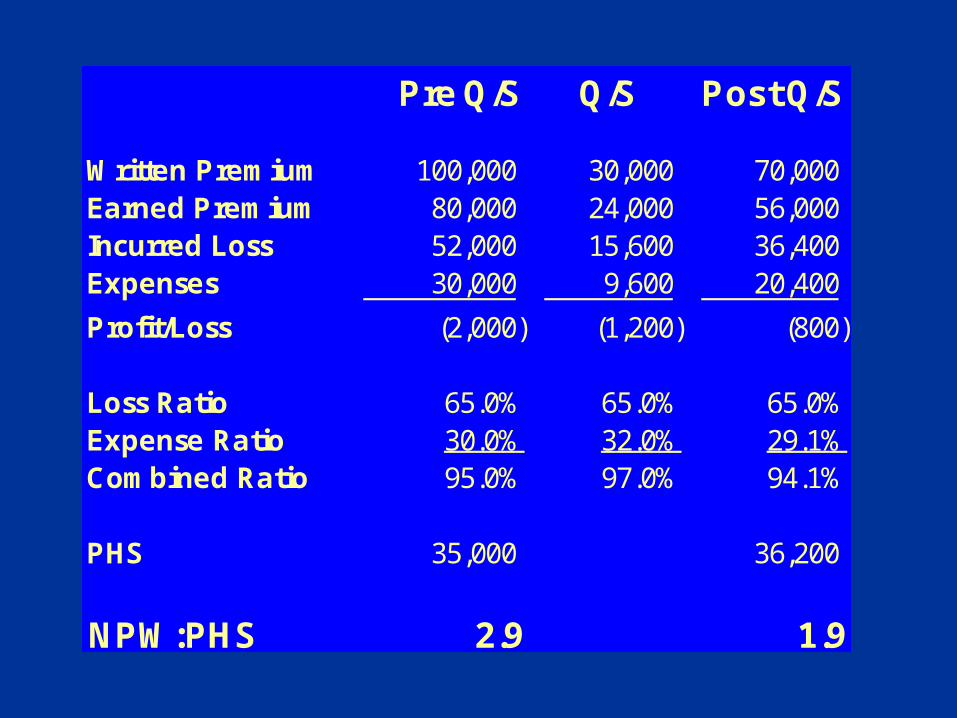

Pre Q/S

Written Premium 100,000 Earned Premium 80,000 Incurred Loss 52,000 Expenses 30,000

Profit/Loss (2,000)

Loss Ratio 65.0%Expense Ratio 30.0%Combined Ratio 95.0%

PHS 35,000

NPW:PHS 2.9

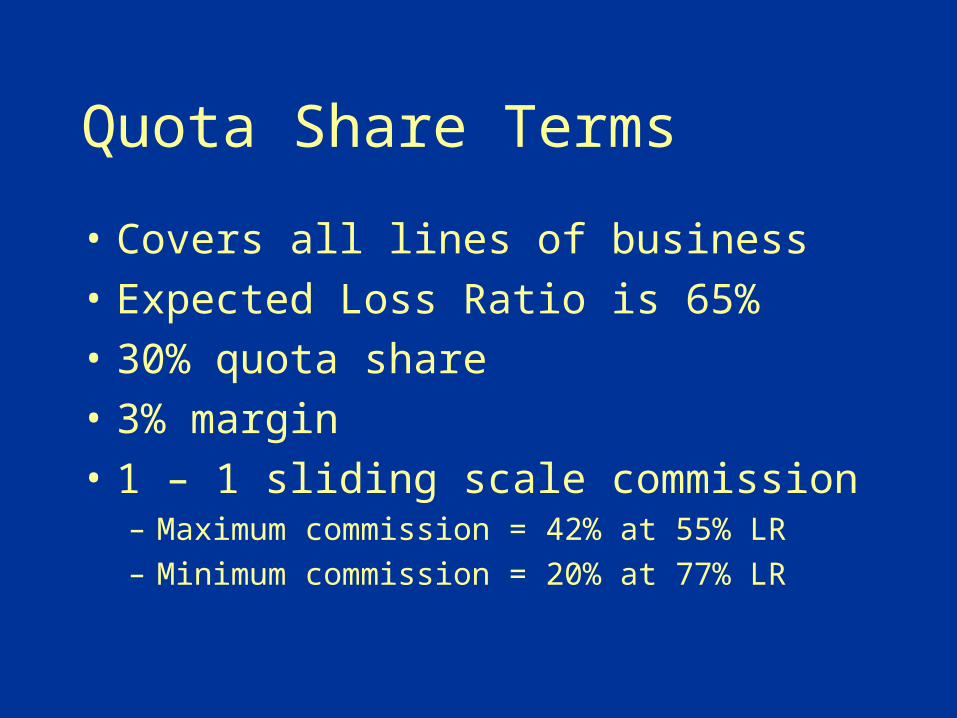

Quota Share Terms

• Covers all lines of business

• Expected Loss Ratio is 65%

• 30% quota share

• 3% margin

• 1 – 1 sliding scale commission– Maximum commission = 42% at 55% LR

– Minimum commission = 20% at 77% LR

Pre Q/S Q/S Post Q/S

Written Premium 100,000 30,000 70,000 Earned Premium 80,000 24,000 56,000 Incurred Loss 52,000 15,600 36,400 Expenses 30,000 9,600 20,400

Profit/Loss (2,000) (1,200) (800)

Loss Ratio 65.0% 65.0% 65.0%Expense Ratio 30.0% 32.0% 29.1%Combined Ratio 95.0% 97.0% 94.1%

PHS 35,000 36,200

NPW:PHS 2.9 1.9

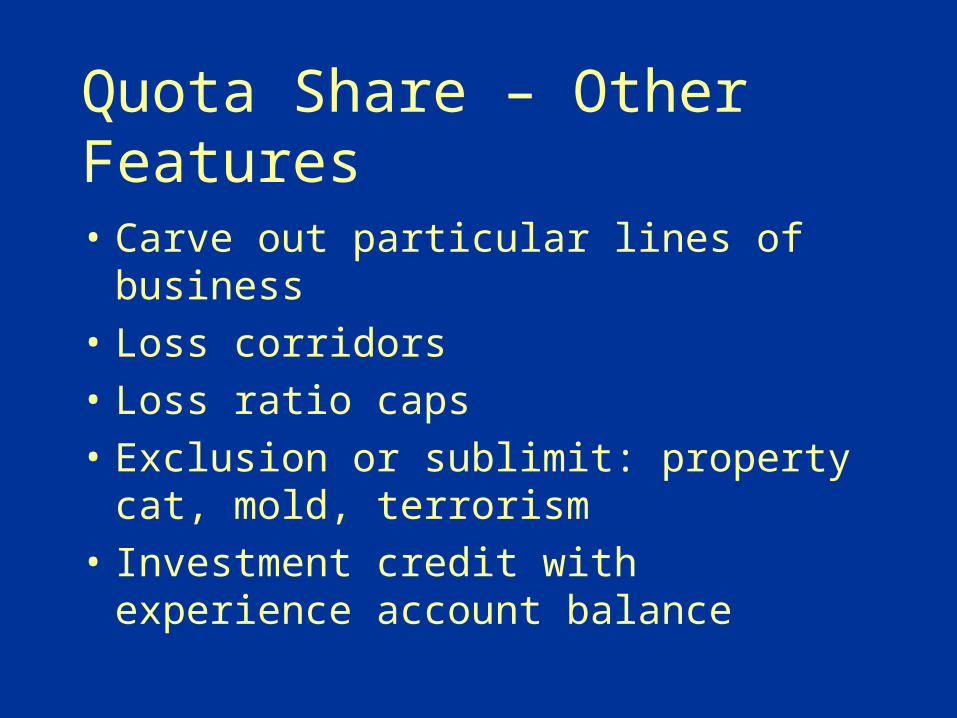

Quota Share – Other Features

• Carve out particular lines of business

• Loss corridors

• Loss ratio caps

• Exclusion or sublimit: property cat, mold, terrorism

• Investment credit with experience account balance

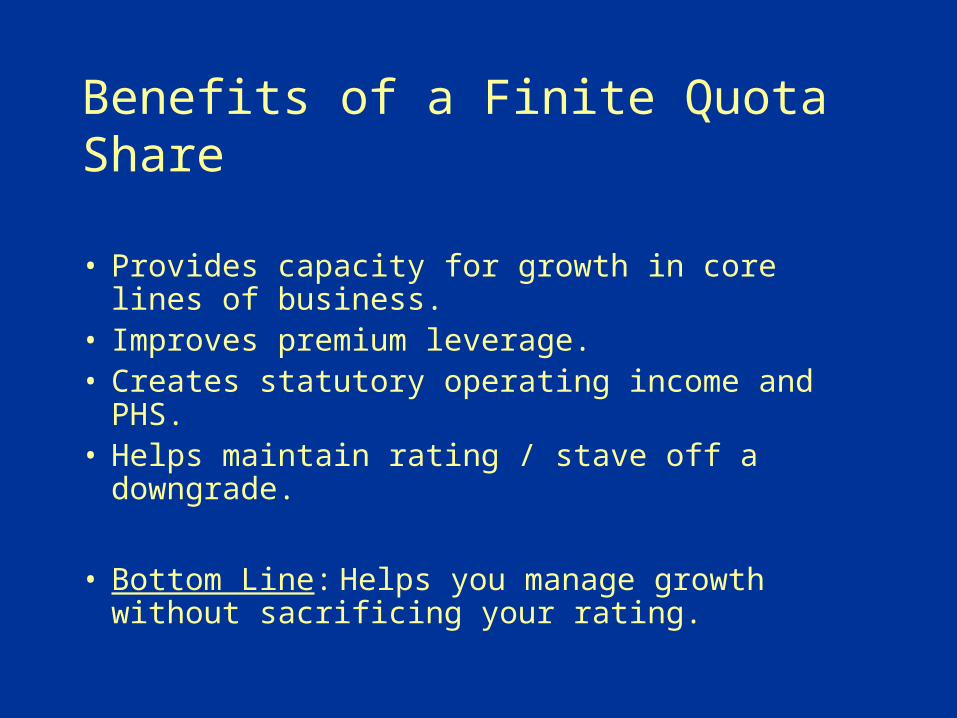

Benefits of a Finite Quota Share

• Provides capacity for growth in core lines of business.

• Improves premium leverage.• Creates statutory operating income and PHS.• Helps maintain rating / stave off a downgrade.

• Bottom Line: Helps you manage growth without sacrificing your rating.

Case Study: ALDC / LPT

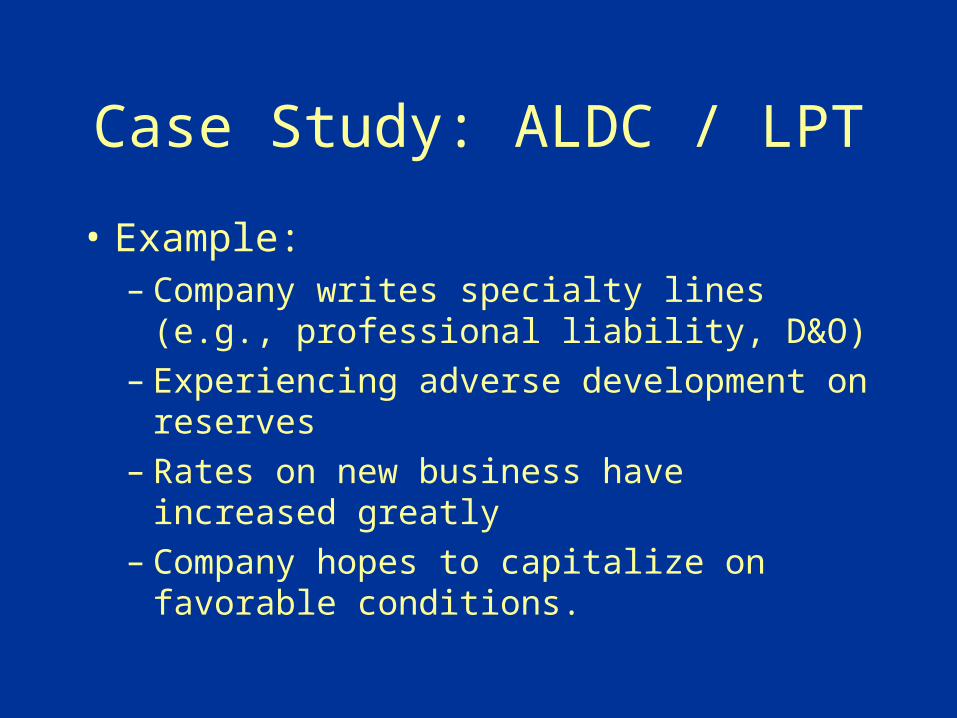

Case Study: ALDC / LPT

• Example:– Company writes specialty lines (e.g.,

professional liability, D&O)– Experiencing adverse development on reserves– Rates on new business have increased greatly– Company hopes to capitalize on favorable

conditions.

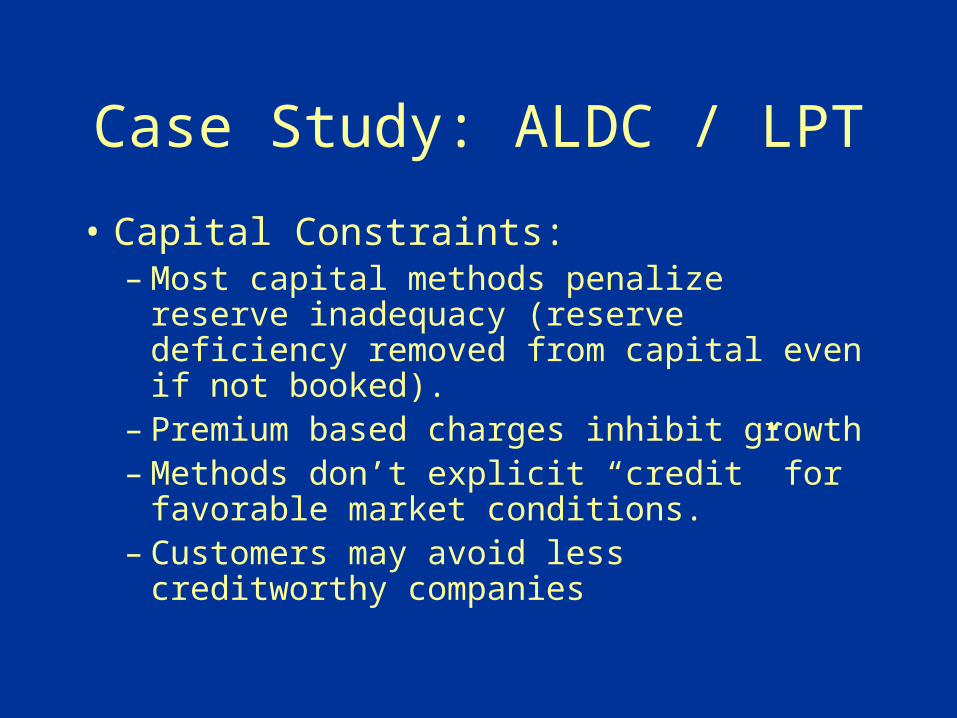

Case Study: ALDC / LPT

• Capital Constraints:– Most capital methods penalize reserve

inadequacy (reserve deficiency removed from capital even if not booked).

– Premium based charges inhibit growth– Methods don’t explicit “credit” for favorable

market conditions.– Customers may avoid less creditworthy

companies

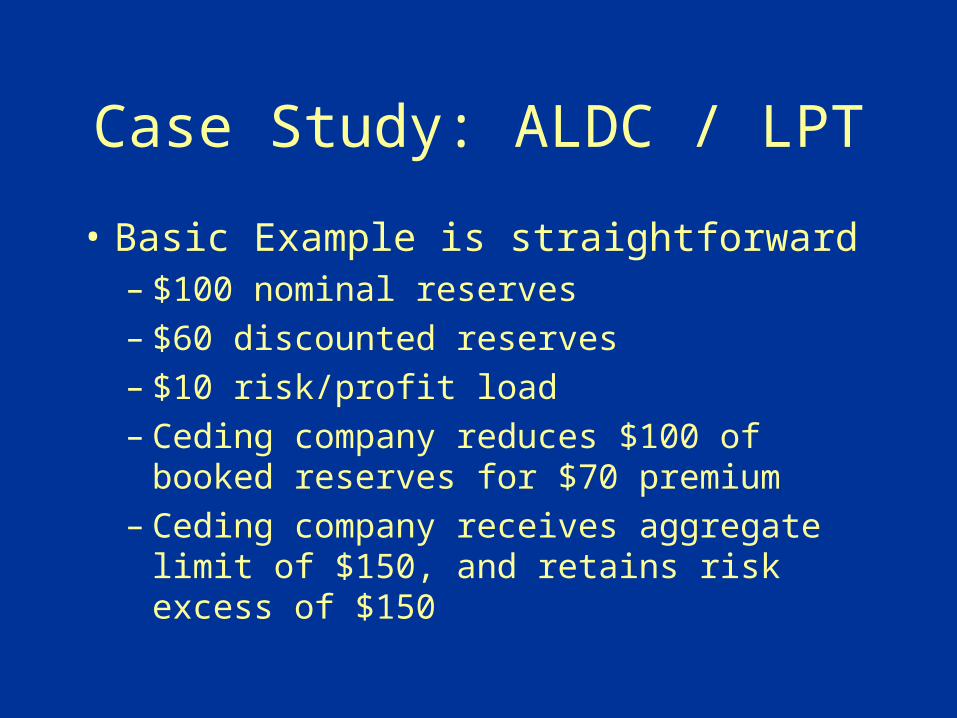

Case Study: ALDC / LPT

• Basic Example is straightforward– $100 nominal reserves– $60 discounted reserves– $10 risk/profit load– Ceding company reduces $100 of booked

reserves for $70 premium– Ceding company receives aggregate limit of

$150, and retains risk excess of $150

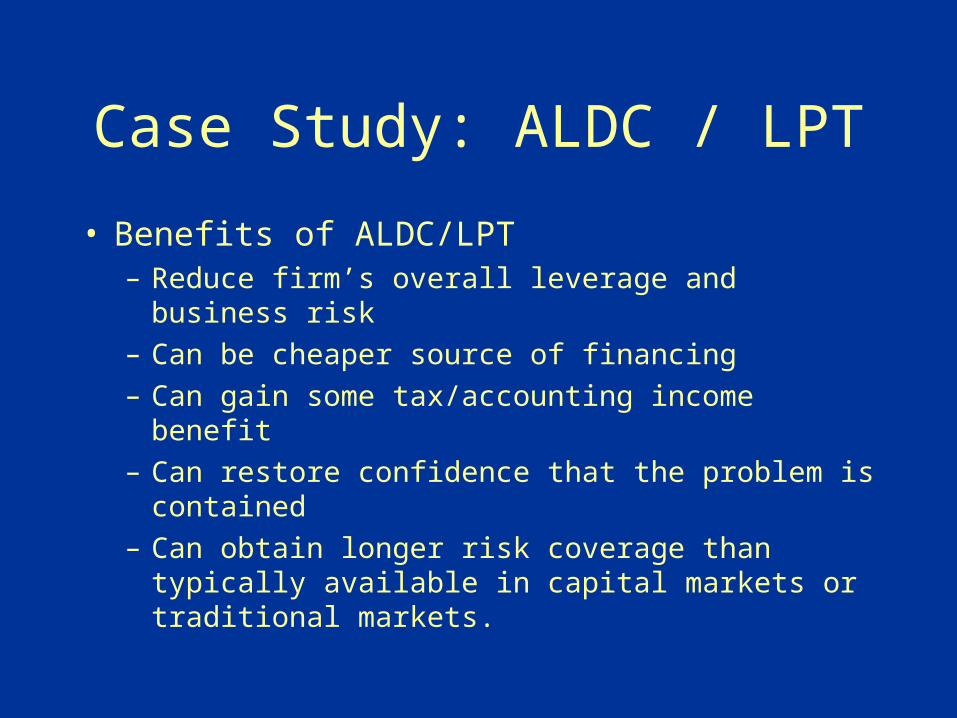

Case Study: ALDC / LPT

• Benefits of ALDC/LPT– Reduce firm’s overall leverage and business risk

– Can be cheaper source of financing

– Can gain some tax/accounting income benefit

– Can restore confidence that the problem is contained

– Can obtain longer risk coverage than typically available in capital markets or traditional markets.

Case Study: ALDC / LPT

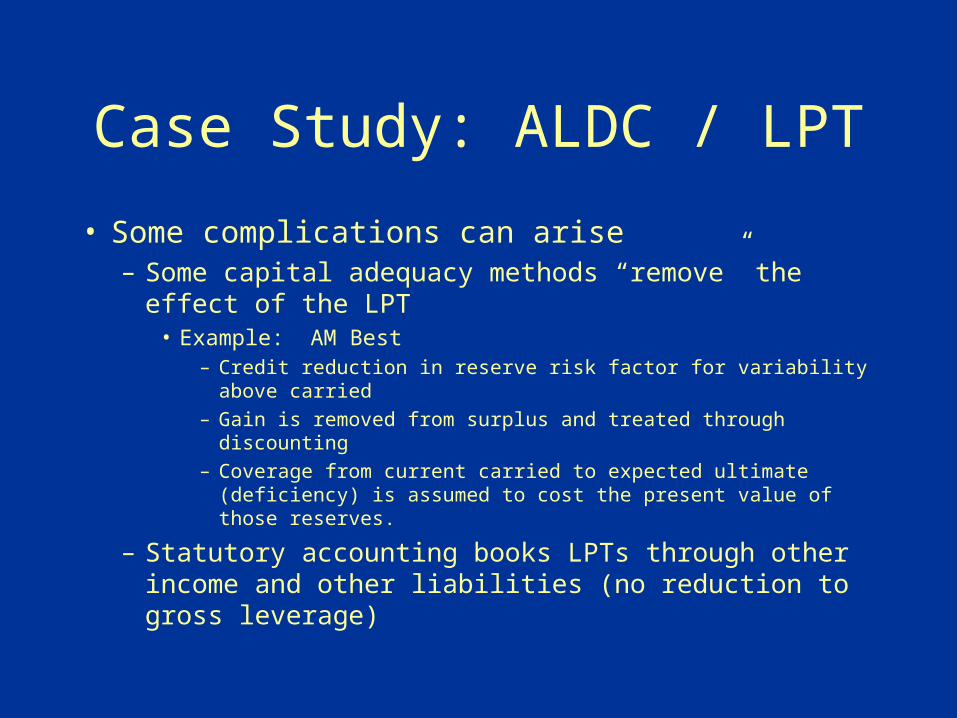

• Some complications can arise– Some capital adequacy methods “remove” the effect of

the LPT• Example: AM Best

– Credit reduction in reserve risk factor for variability above carried

– Gain is removed from surplus and treated through discounting

– Coverage from current carried to expected ultimate (deficiency) is assumed to cost the present value of those reserves.

– Statutory accounting books LPTs through other income and other liabilities (no reduction to gross leverage)

Case Study: ALDC / LPT

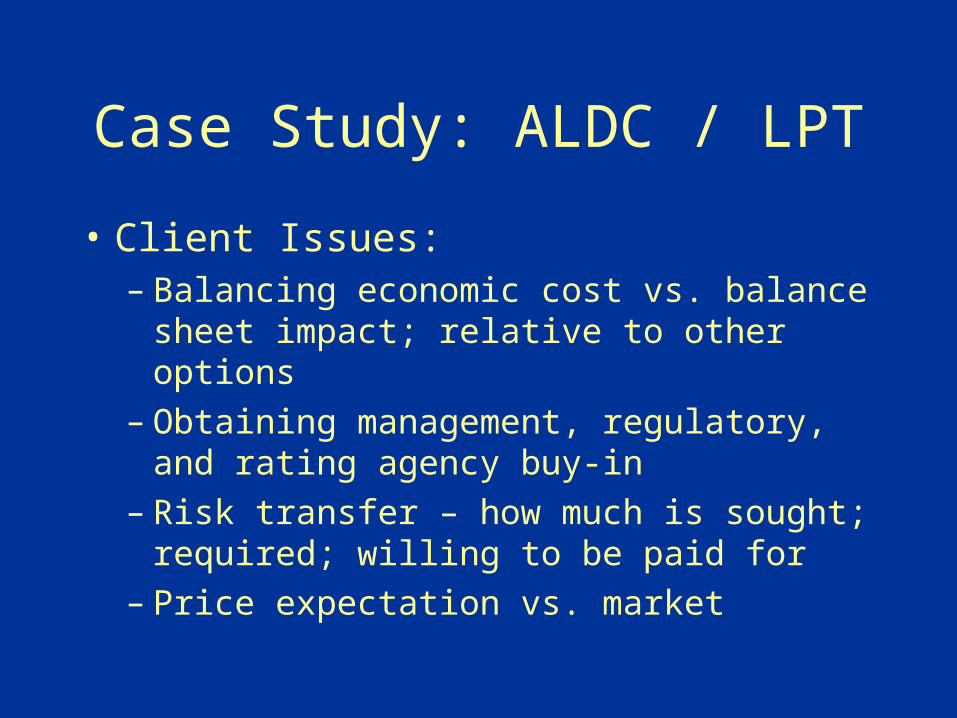

• Client Issues:– Balancing economic cost vs. balance sheet

impact; relative to other options– Obtaining management, regulatory, and rating

agency buy-in– Risk transfer – how much is sought; required;

willing to be paid for– Price expectation vs. market

Case Study: ALDC / LPT

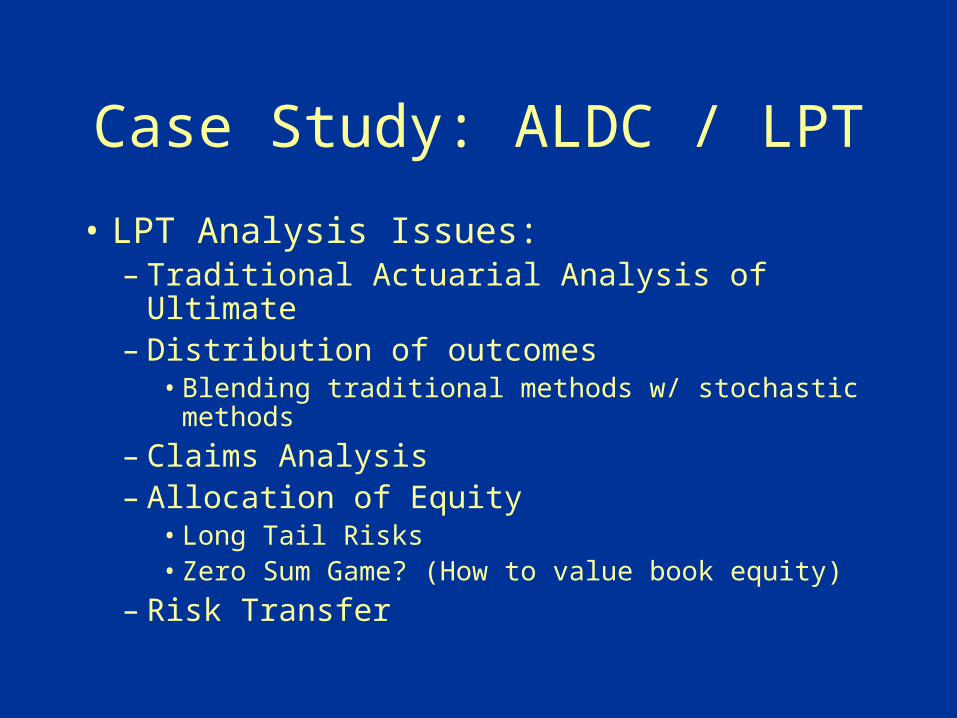

• LPT Analysis Issues:– Traditional Actuarial Analysis of Ultimate– Distribution of outcomes

• Blending traditional methods w/ stochastic methods

– Claims Analysis– Allocation of Equity

• Long Tail Risks• Zero Sum Game? (How to value book equity)

– Risk Transfer

Case Study: ALDC / LPT

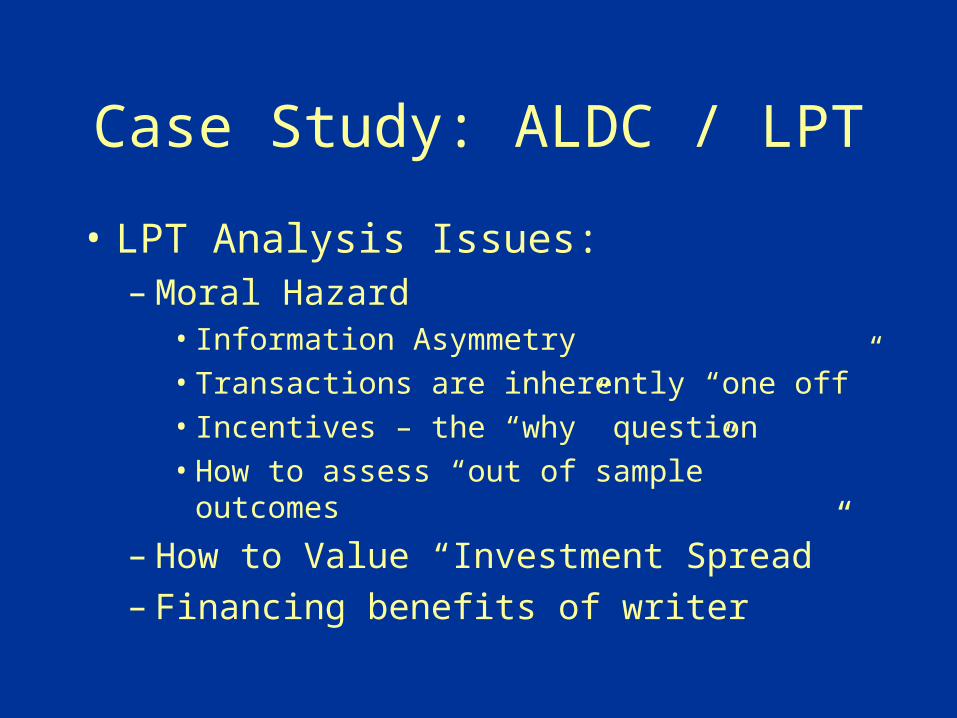

• LPT Analysis Issues:– Moral Hazard

• Information Asymmetry

• Transactions are inherently “one off”

• Incentives – the “why” question

• How to assess “out of sample” outcomes

– How to Value “Investment Spread”– Financing benefits of writer

Questions

???????