cash book bank reconciliation statement

TRANSCRIPT

Sub Division of JournalThough the principle of journalising all the transactions, known as Continental System of book-keeping is quite perfect in actual business but in a large business it is found inonvenient to journalise every transaction and sometime it becomes impossible to journalise numerous transactions of a business in one journal. Therefore, the journal is sub-divided into different journals known as subsidiary books.

The important Subsidiary Books used in modern business world are the following:

1)Cash Book2)Purchases Book3)Sales Book4)Purchases Returns Book5)Sales Returns Book6)Bills Receivable Book7)Bills Payable Book

Cash BookThe cash book is a book of original entry in which transactions relating only to cash receipts & payments are recorded in detail. When cash is received it is entered on the debit or left hand side. Similarly, when cash is paid out, the same is recorded on the credit or the right hand side of the cash book.

The cash book, though it serve the purpose of a book of original entry i.e Cash Journal as well as it represents Cash Account of Ledger. It is more a Ledger than a Journal. It is Journal as cash transactions are recorded chronologically recorded in it. It is a Ledger as it contains a classified record of all cash transactions.

The balance of cash book are included in the trial balance & balance sheet.

Kinds of Cash BookThe following are the three forms of cash books

met with in practice:

1)Single Column Cash Book or Simple Cash Book2)Double Column Cash Book3)Three Column Cash Book

Single Column Cash BookIt records only cash receipts & payments. It has only one amount column on each of the debit & credit sides of the book. All cash receipts are entered on debit side and cash payments on credit side.

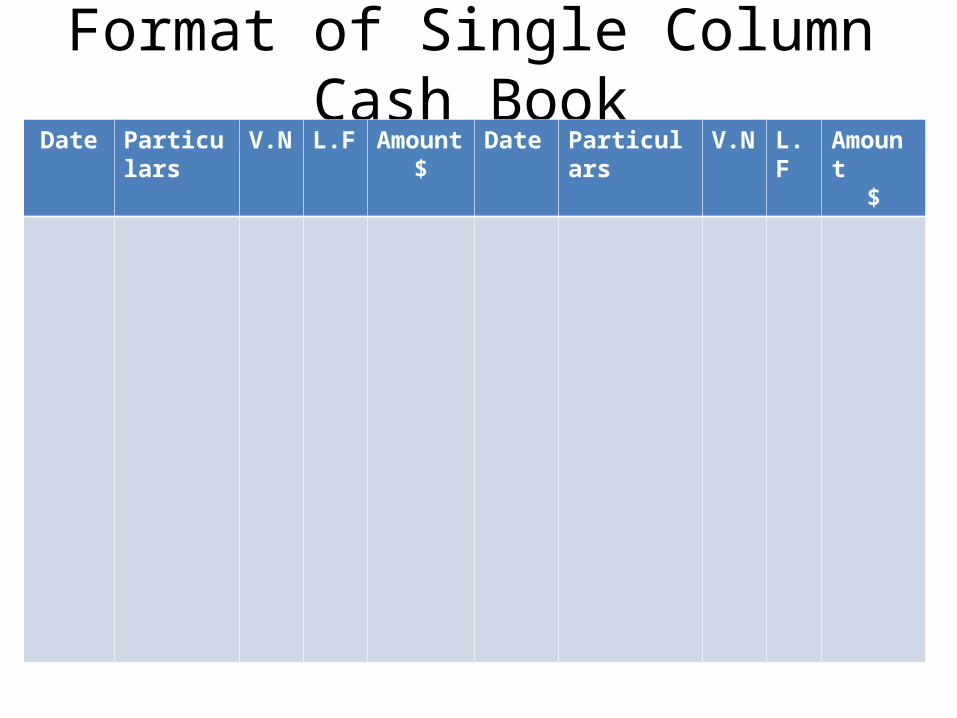

Format of Single Column Cash BookDate Particulars V.N L.F Amount

$Date Particulars V.N L.F Amount

$

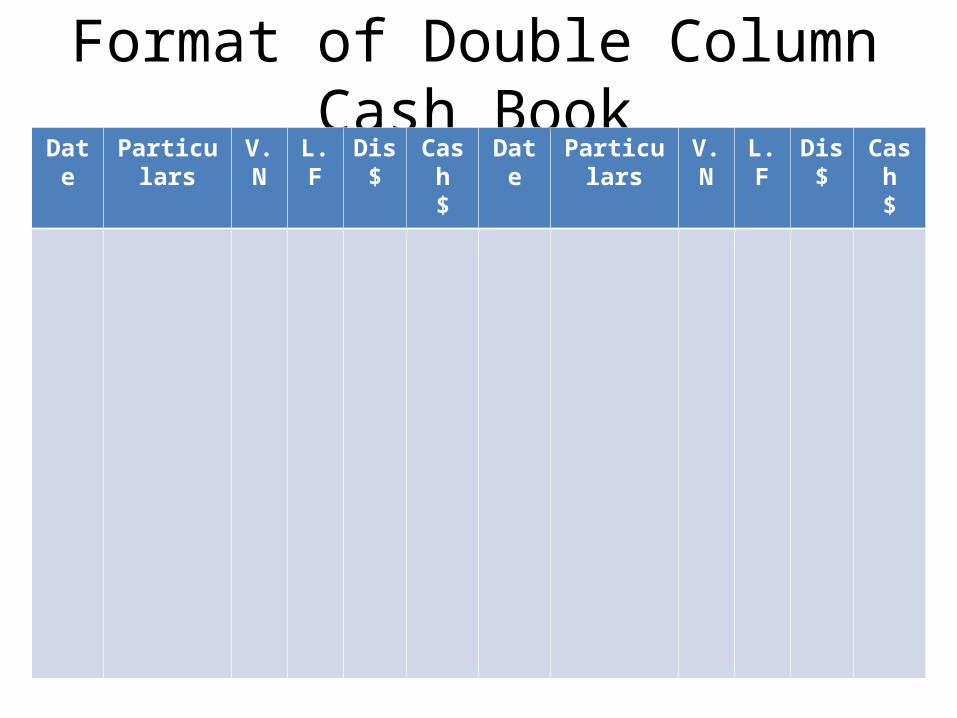

Double Column Cash BookA double column cash book is one which consists of two separate columns on debit & credit side of cash book for recording cash and discounts received or allowed. The discount column on the debit side of the cash book will record discounts allowed and that on the credit side discounts received.

Format of Double Column Cash BookDate Particulars V.N L.F Dis

$Cash

$Date Particulars V.N L.F Dis

$Cash

$

Three Column Cash BookA three column cash book is one which consists of three separate columns on debit & credit side of cash book for recording cash, discounts received or allowed & Bank. When a trader keeps a Bank Account it becomes necessary to record the amounts deposited into the bank and withdrawals from it. For this purpose one additional column is added on each side of Cash Book. Such a Cash Book is helpful to businessmen, since it reveals the Cash & Bank Balances at a glance.

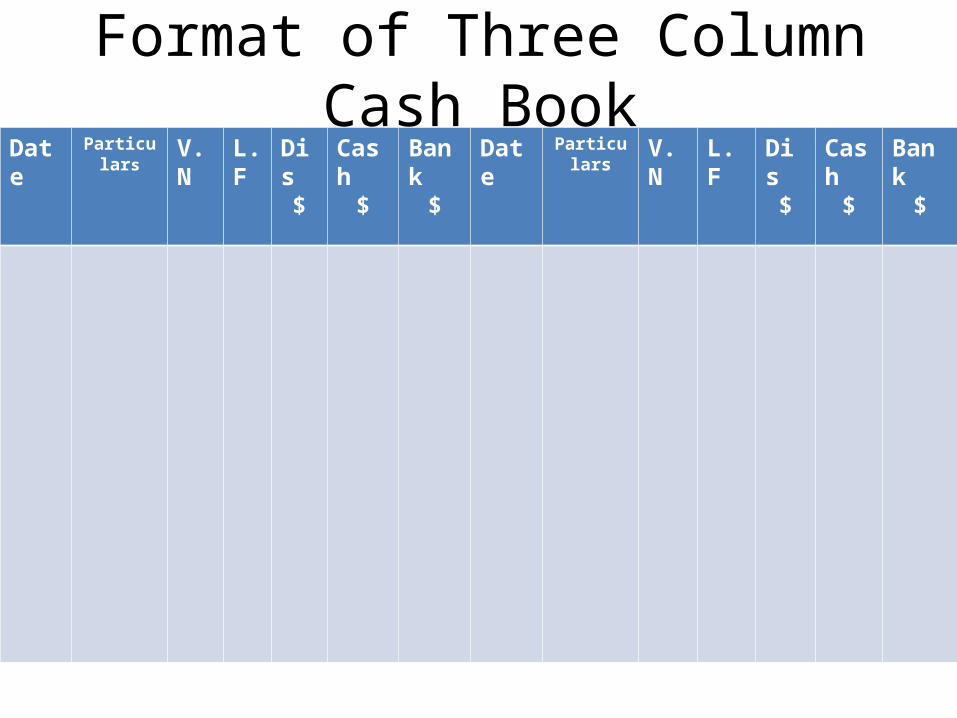

Format of Three Column Cash BookDate Particulars V.N L.F Dis

$Cash

$Bank

$Date Particulars V.N L.F Dis

$Cash

$Bank

$

Practice Questions For Cash Book

Bank StatementBank Statement:

Every month, banks provide each depositor with a bank statement (Pass Book) summarizing the activity in the depositor’s account. The bank statement shows all the deposits/receipts made into account and all the withdrawals/payments which bank has paid from the account. And it also indicating the nature & amount of any other changes in the account balance.

Bank Reconciliation StatementA bank reconciliation is a statement explaining any difference between the balance shown in the bank statement and the balance shown in the depositor’s accounting records. Remember that both the bank and the depositor are mainitaining independent records of the deposits & withdrawals. Each month, the depositor should prepare a bank reconciliation to verify that these independent sets of records are in agreement.

Bank Reconciliation Statement

A statement is prepared called Bank Reconciliation Statement to find out the reasons for disagreemnet between the Bank Statement balance and the Cash Book balance of the Bank, and to test whether the apparently conflicting balance do really agree.

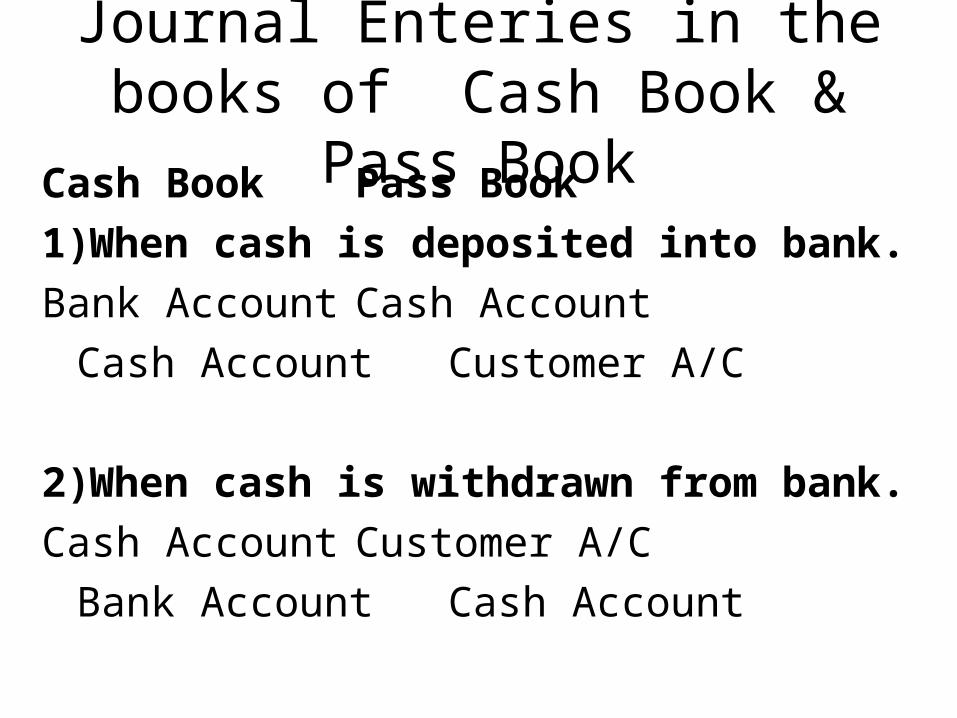

Journal Enteries in the books of Cash Book & Pass Book

Cash Book Pass Book1)When cash is deposited into bank.Bank Account Cash Account

Cash Account Customer A/C

2)When cash is withdrawn from bank.Cash Account Customer A/C

Bank Account Cash Account

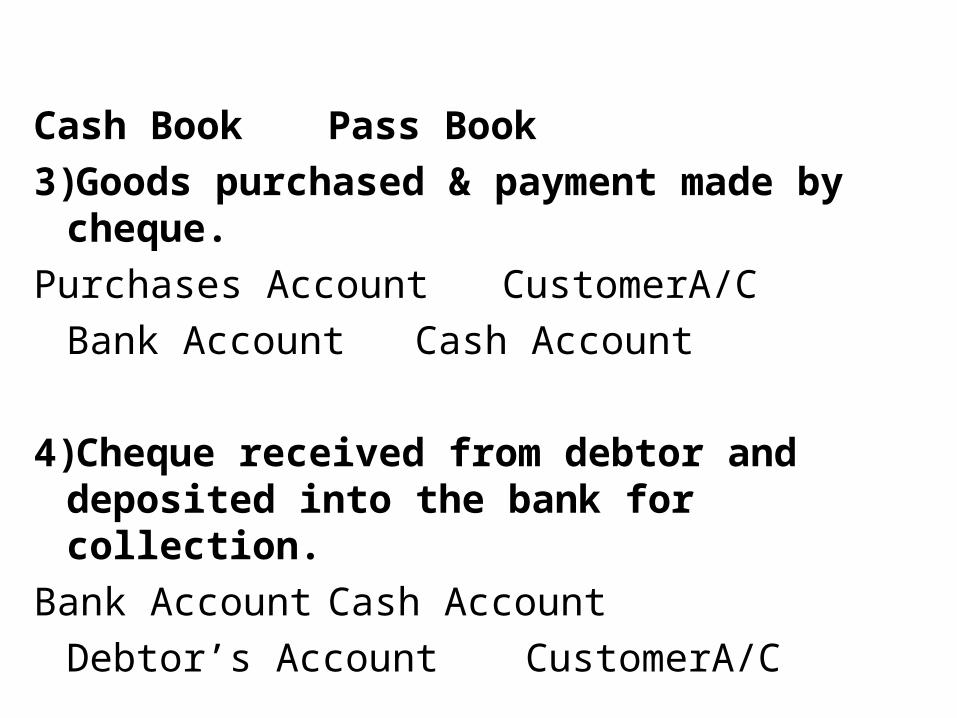

Cash Book Pass Book3)Goods purchased & payment made by cheque.Purchases Account CustomerA/C

Bank Account Cash Account

4)Cheque received from debtor and deposited into the bank for collection.

Bank Account Cash AccountDebtor’s Account CustomerA/C

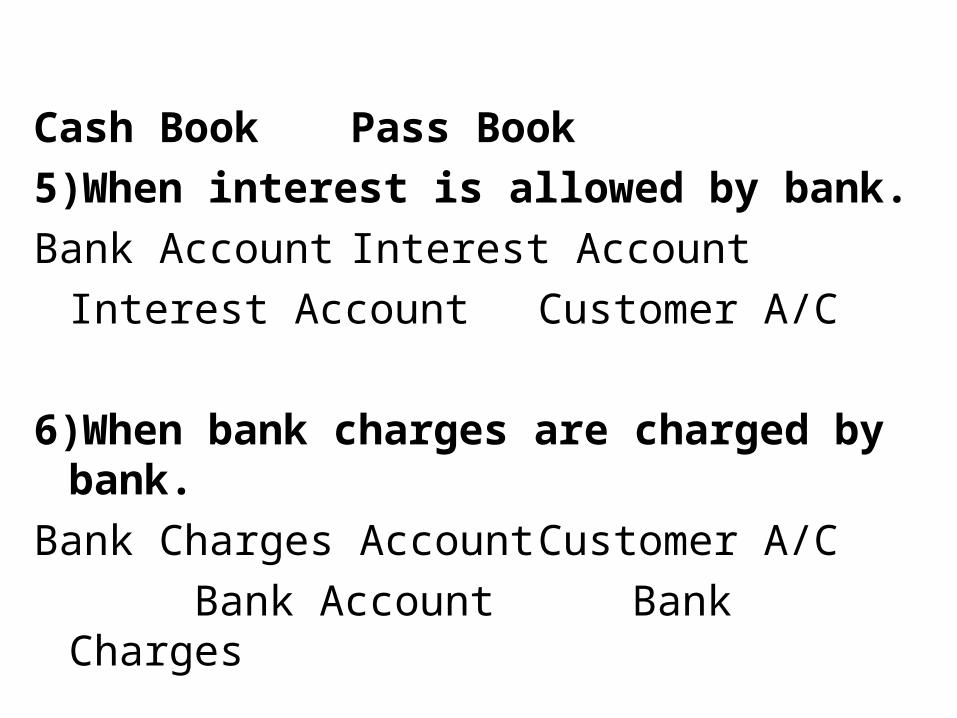

Cash Book Pass Book5)When interest is allowed by bank.Bank Account Interest Account

Interest Account Customer A/C

6)When bank charges are charged by bank.Bank Charges Account Customer A/C

Bank Account Bank Charges

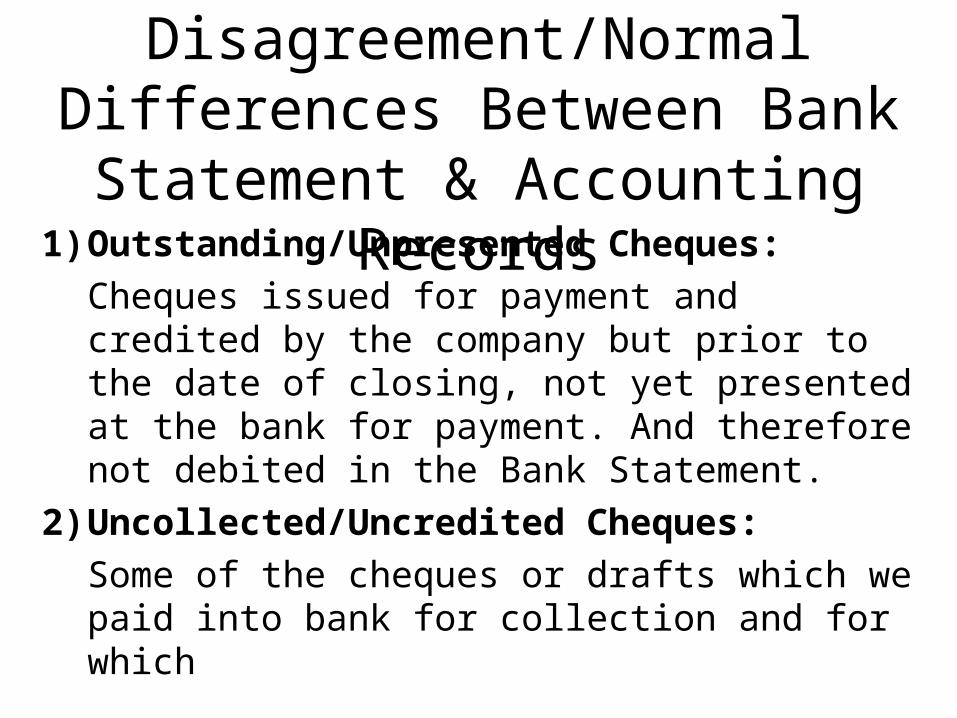

Causes of Disagreement/Normal Differences Between Bank Statement

& Accounting Records1) Outstanding/Unpresented Cheques:

Cheques issued for payment and credited by the company but prior to the date of closing, not yet presented at the bank for payment. And therefore not debited in the Bank Statement.

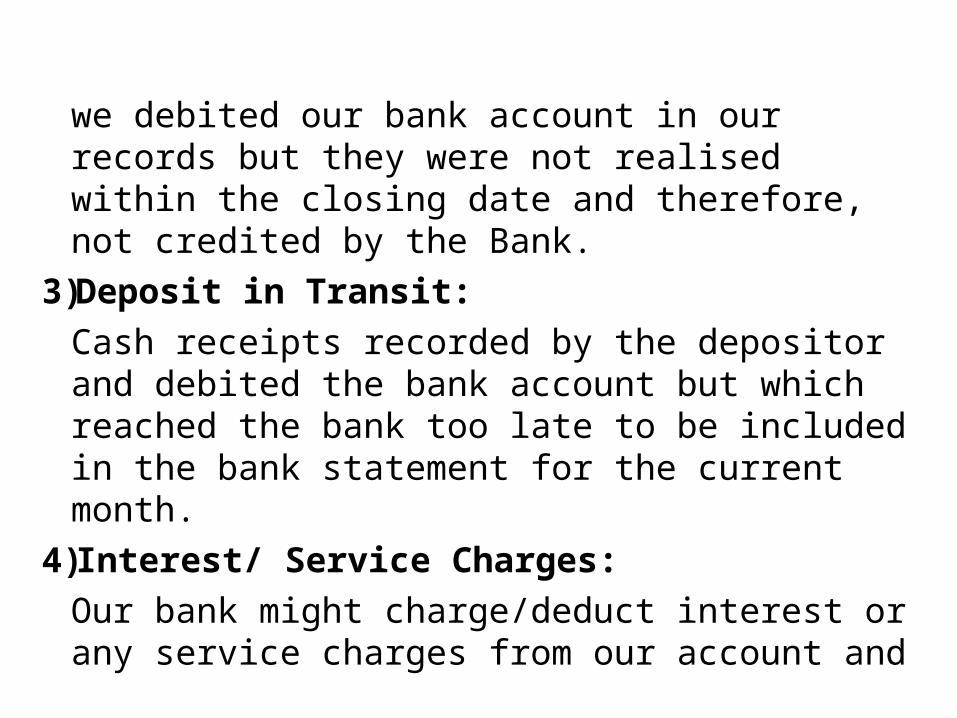

2) Uncollected/Uncredited Cheques:Some of the cheques or drafts which

we paid into bank for collection and for which

we debited our bank account in our records but they were not realised within the closing date and therefore, not credited by the Bank.

3)Deposit in Transit:Cash receipts recorded by the

depositor and debited the bank account but which reached the bank too late to be included in the bank statement for the current month.

4)Interest/ Service Charges:Our bank might charge/deduct interest

or any service charges from our account and

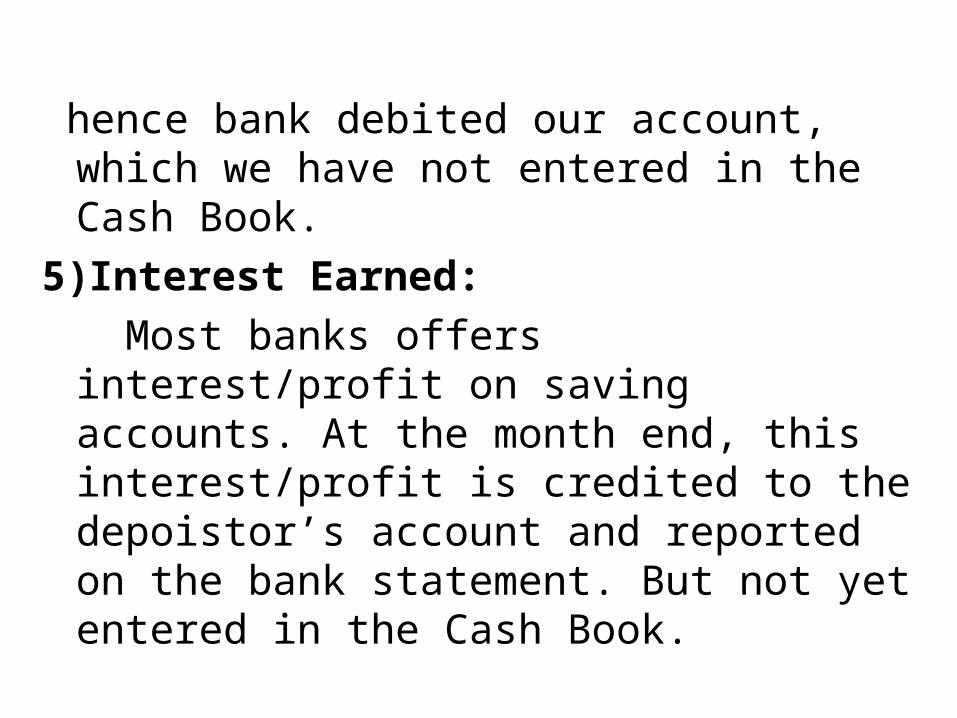

hence bank debited our account, which we have not entered in the Cash Book.

5)Interest Earned: Most banks offers interest/profit on

saving accounts. At the month end, this interest/profit is credited to the depoistor’s account and reported on the bank statement. But not yet entered in the Cash Book.

Balances for Cash Book & Bank Statement

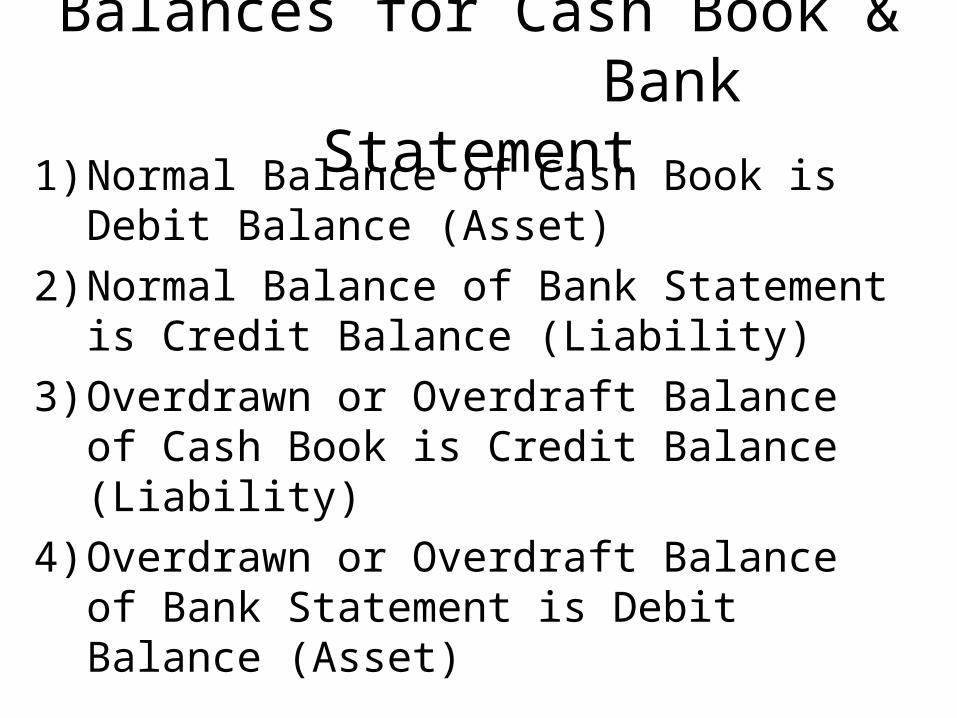

1) Normal Balance of Cash Book is Debit Balance (Asset)

2) Normal Balance of Bank Statement is Credit Balance (Liability)

3) Overdrawn or Overdraft Balance of Cash Book is Credit Balance (Liability)

4) Overdrawn or Overdraft Balance of Bank Statement is Debit Balance (Asset)

Practice Questions For Bank Reconciliation Statement