cars, consumers, & credit cycles - manheim auctions pickup cuv / suv van source: manheim...

TRANSCRIPT

Cars, Consumers, & Credit Cycles“History never repeats itself, but it often rhymes”

Tom WebbCox Automotive

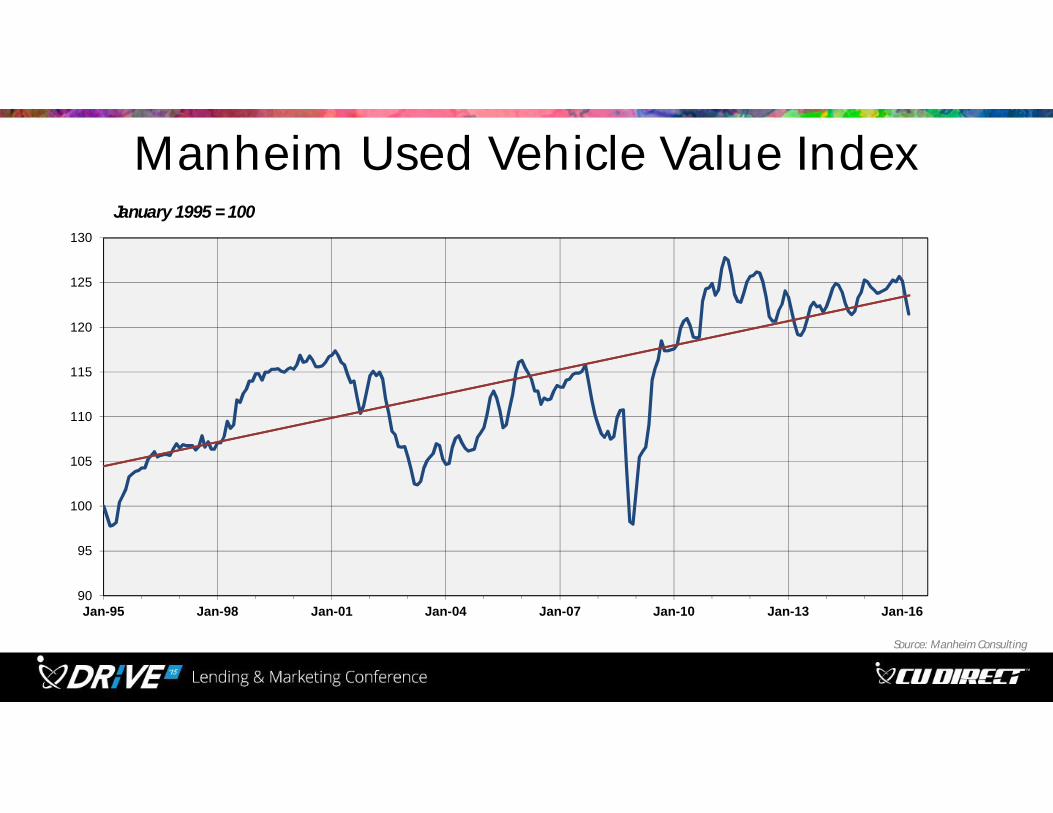

Manheim Used Vehicle Value Index

90

95

100

105

110

115

120

125

130

Jan-95 Jan-98 Jan-01 Jan-04 Jan-07 Jan-10 Jan-13 Jan-16

Source: Manheim Consulting

January 1995 = 100

30%

35%

40%

45%

50%

55%

60%

Source: Bureau of Labor Statistics & Manheim Consulting

Manheim Index vs. Mix & Quality Adjusted New Vehicle Price with 3 ½ year Lag

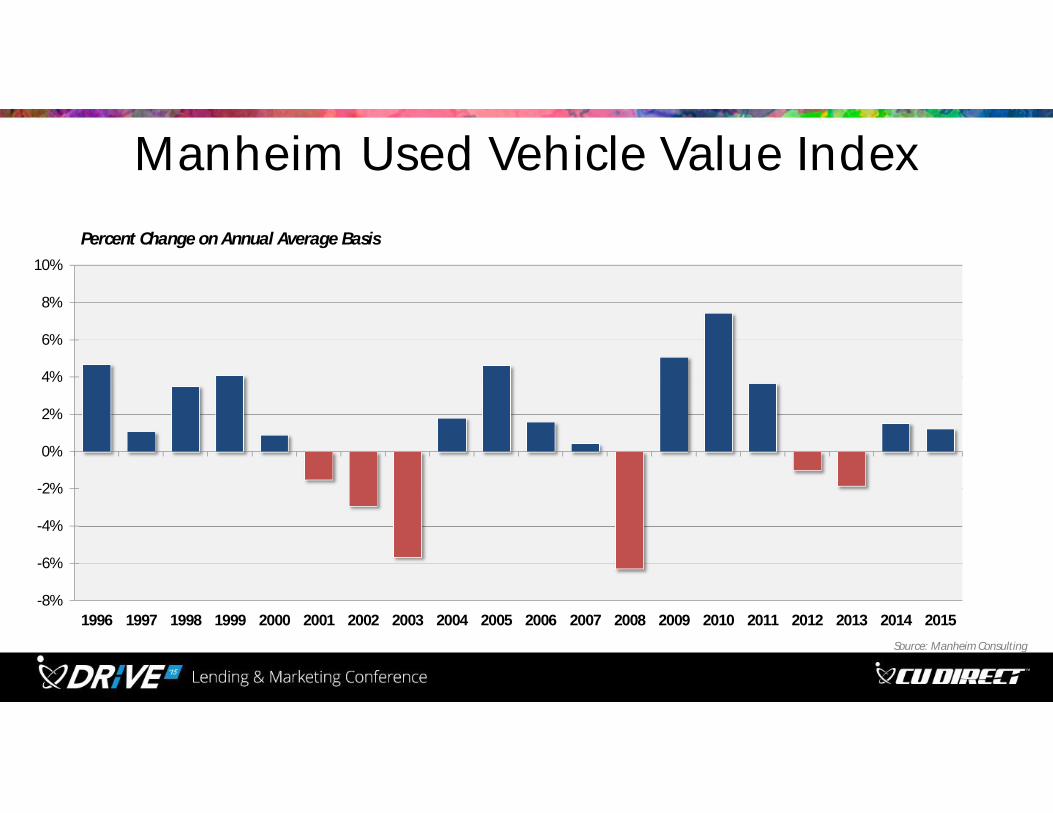

Manheim Used Vehicle Value Index

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percent Change on Annual Average Basis

Source: Manheim Consulting

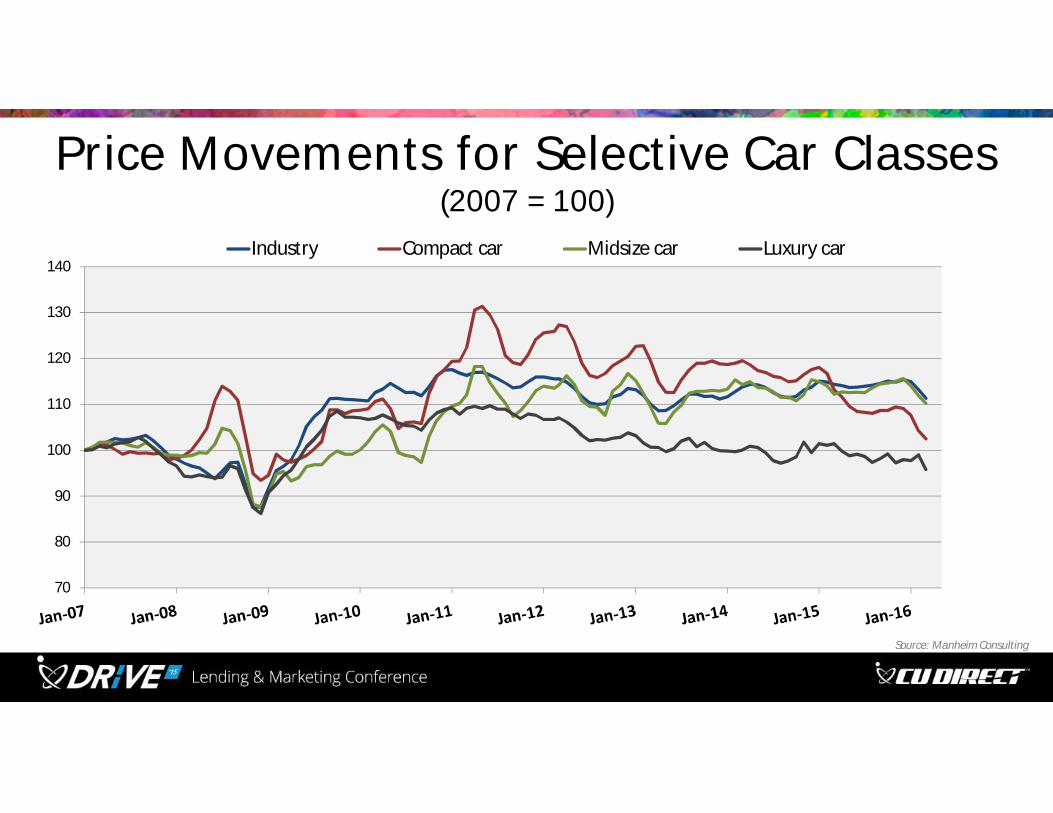

Price Movements for Selective Car Classes (2007 = 100)

70

80

90

100

110

120

130

140Industry Compact car Midsize car Luxury car

Source: Manheim Consulting

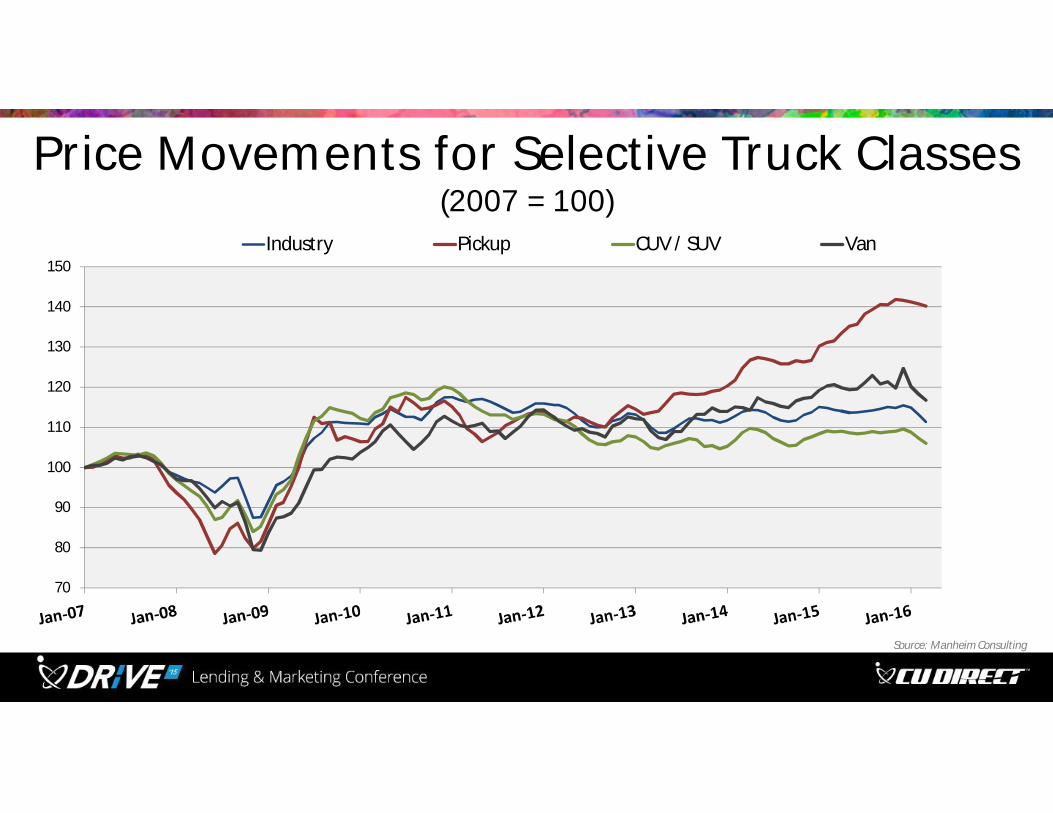

Price Movements for Selective Truck Classes (2007 = 100)

70

80

90

100

110

120

130

140

150Industry Pickup CUV / SUV Van

Source: Manheim Consulting

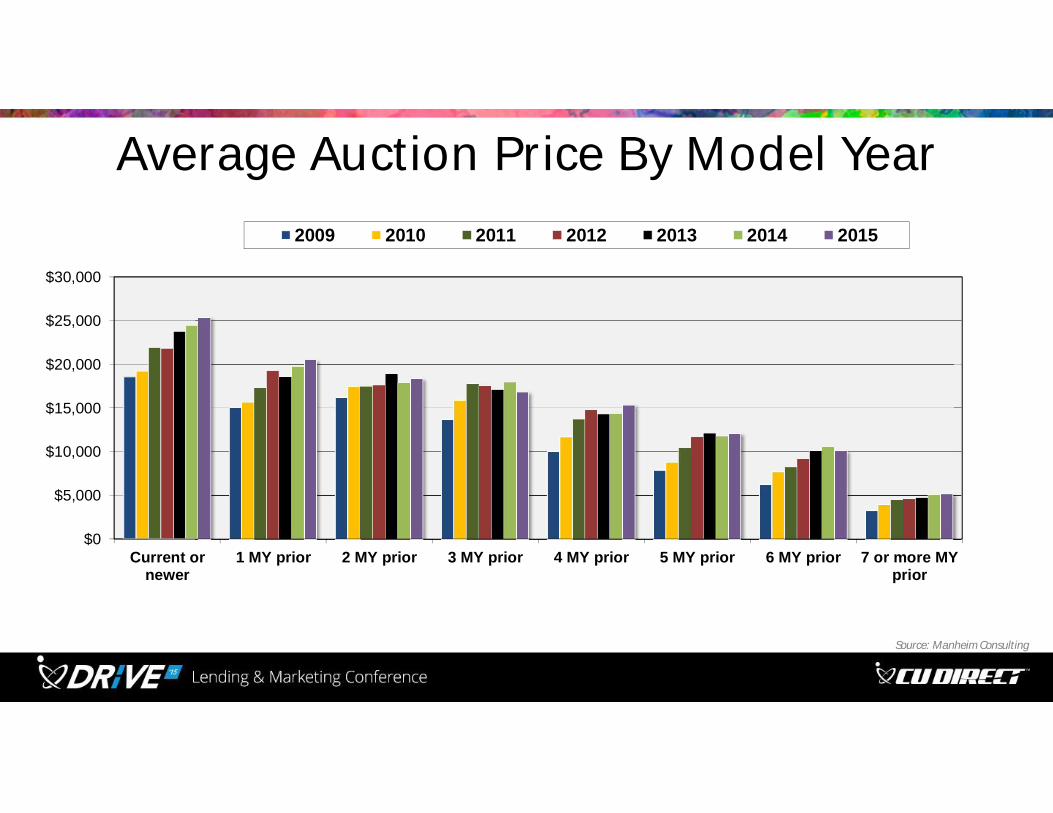

Average Auction Price By Model Year

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Current ornewer

1 MY prior 2 MY prior 3 MY prior 4 MY prior 5 MY prior 6 MY prior 7 or more MYprior

2009 2010 2011 2012 2013 2014 2015

Source: Manheim Consulting

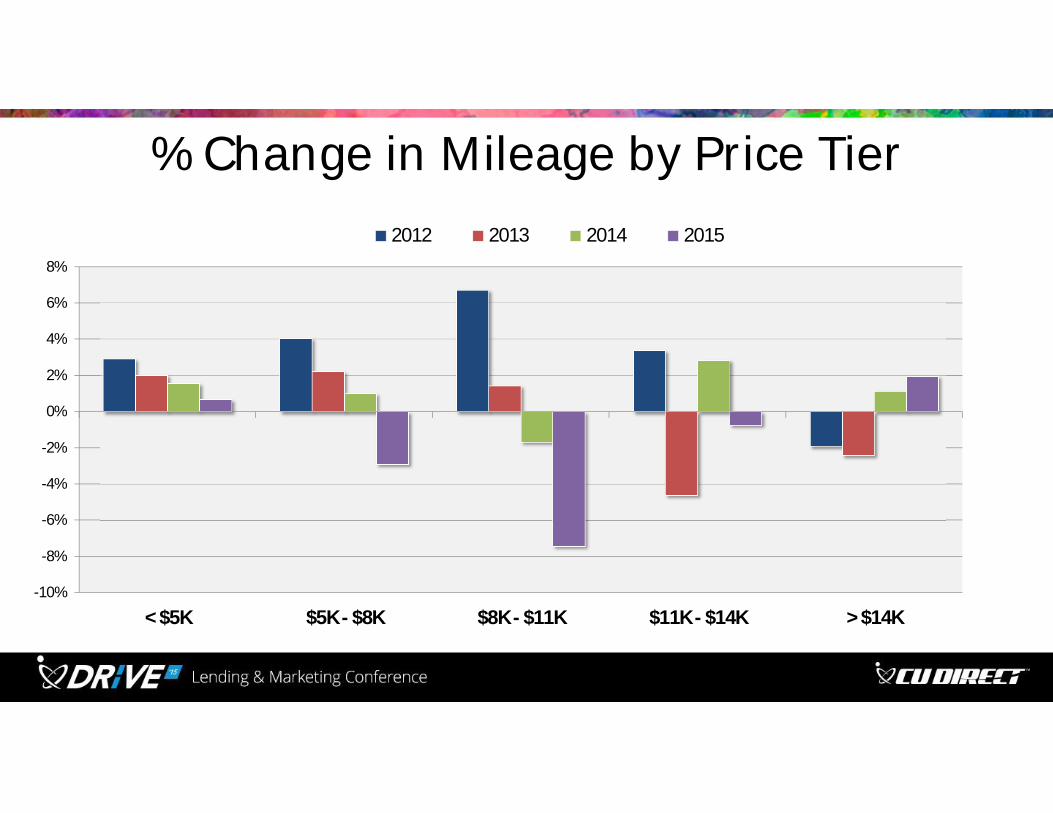

% Change in Mileage by Price Tier

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

< $5K $5K - $8K $8K - $11K $11K - $14K > $14K

2012 2013 2014 2015

Growing Wholesale Supplies

New Vehicle Lease Originations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Mill

ions

Source: Manheim Consulting

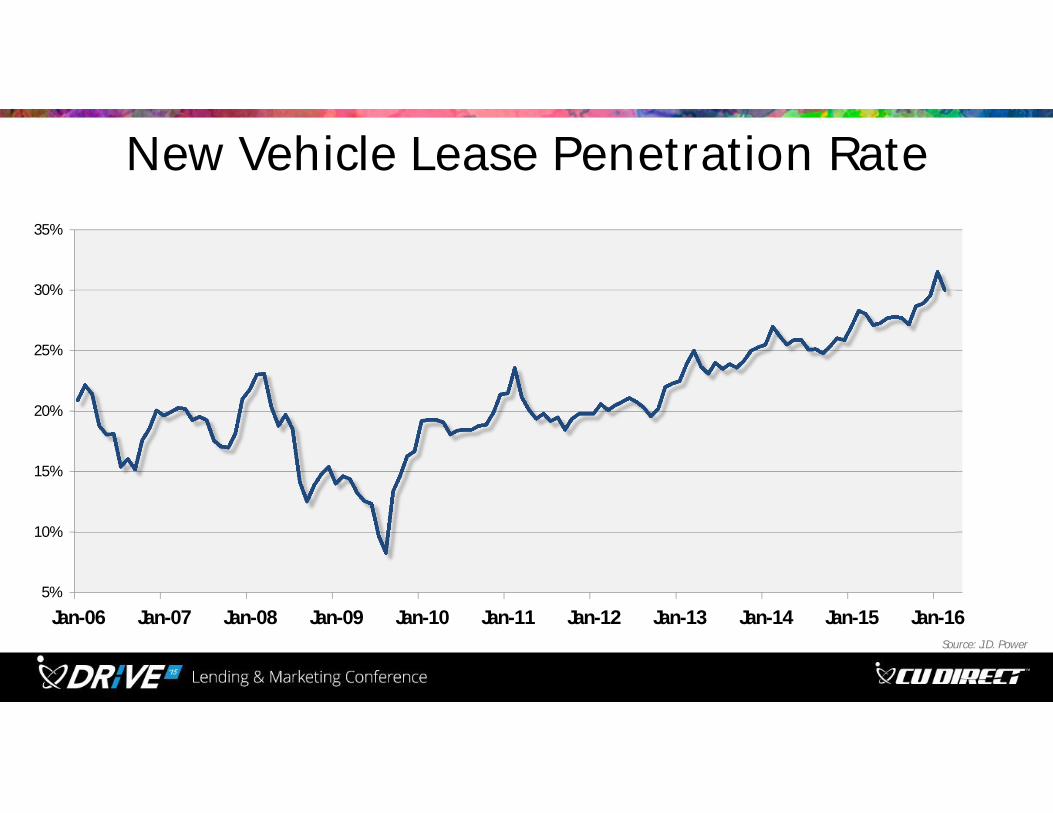

New Vehicle Lease Penetration Rate

5%

10%

15%

20%

25%

30%

35%

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16Source: J.D. Power

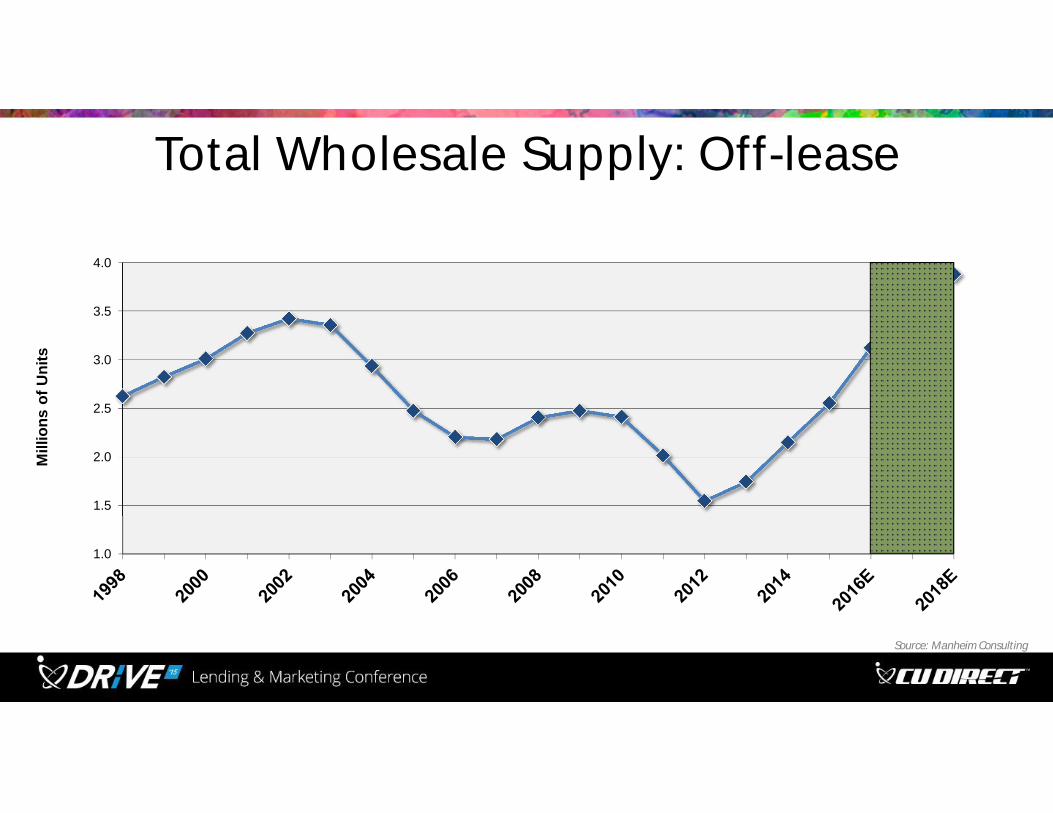

Total Wholesale Supply: Off-lease

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Mill

ions

of U

nits

Source: Manheim Consulting

Off-lease “Return Rate”(not bought by grounding dealer or lessee)

35%

40%

45%

50%

55%

60%

0.0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015 2016 2017 2018 2019 2020

Number Percent

Unit growth from 2015 to 2020: 972,000 units or 82%

Source: Manheim Consulting

Millions of units

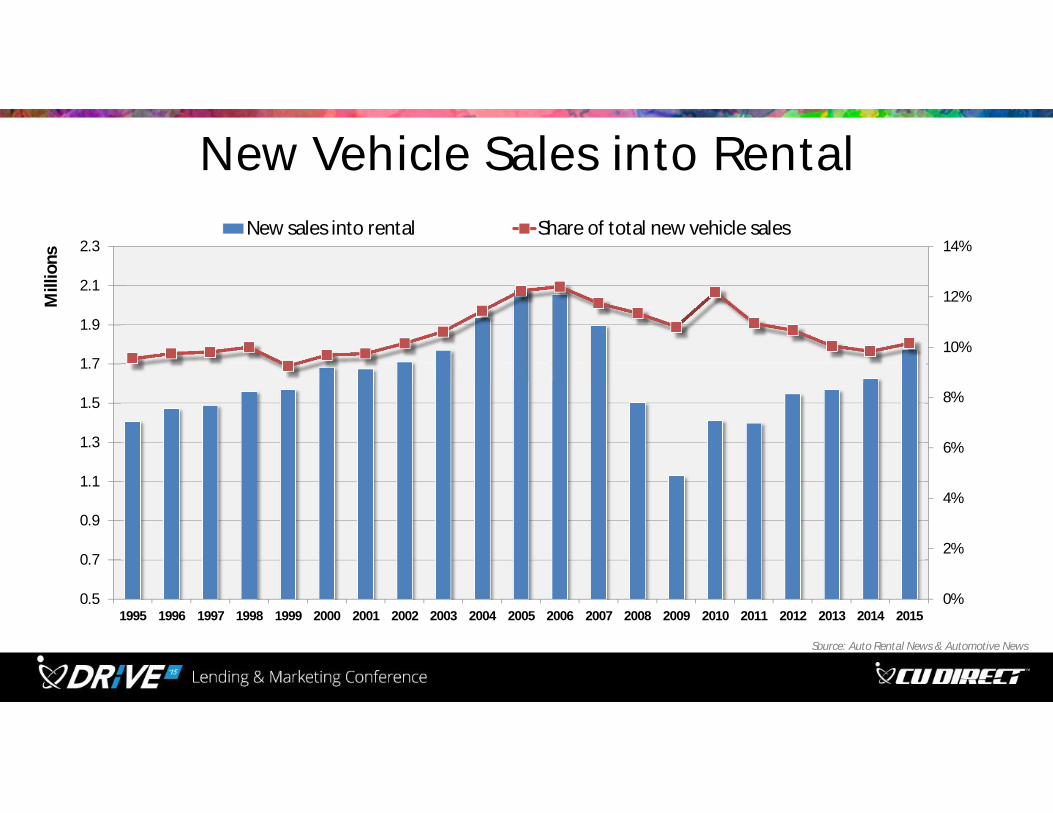

New Vehicle Sales into Rental

0%

2%

4%

6%

8%

10%

12%

14%

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mill

ions

New sales into rental Share of total new vehicle sales

Source: Auto Rental News & Automotive News

Total Wholesale Supply: Off-rental

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

Mill

ions

Source: Manheim Consulting

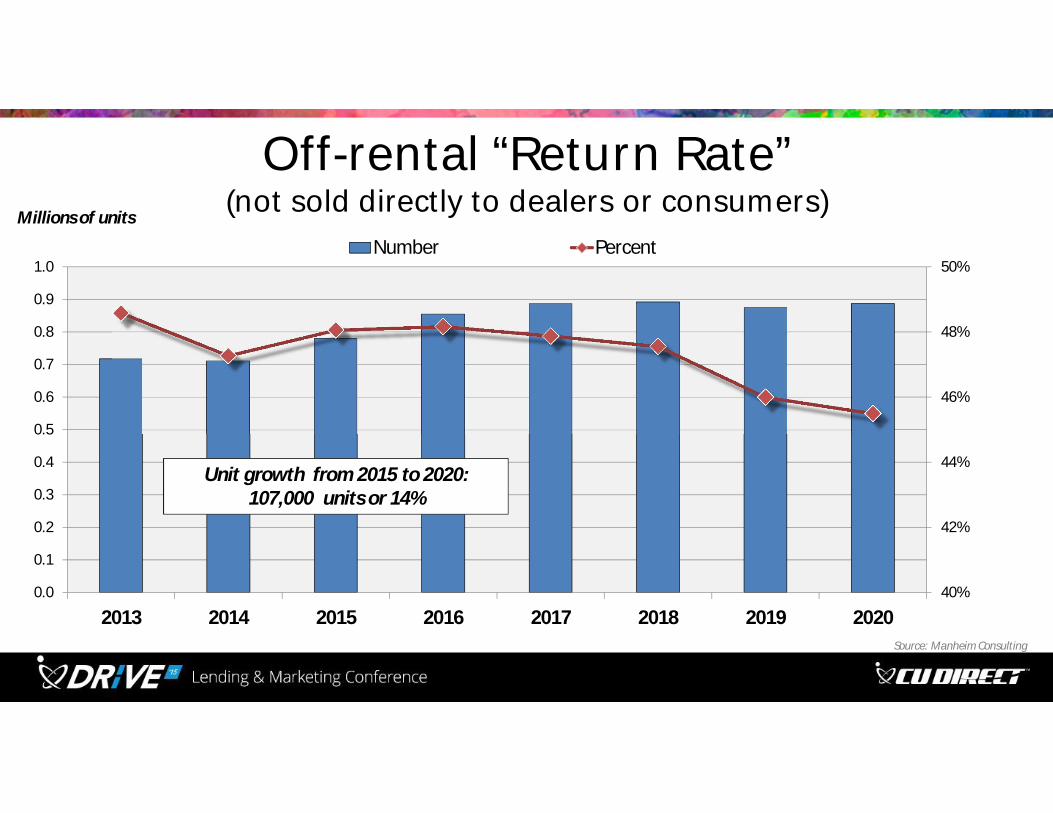

Off-rental “Return Rate”(not sold directly to dealers or consumers)

40%

42%

44%

46%

48%

50%

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

2013 2014 2015 2016 2017 2018 2019 2020

Number Percent

Unit growth from 2015 to 2020: 107,000 units or 14%

Source: Manheim Consulting

Millions of units

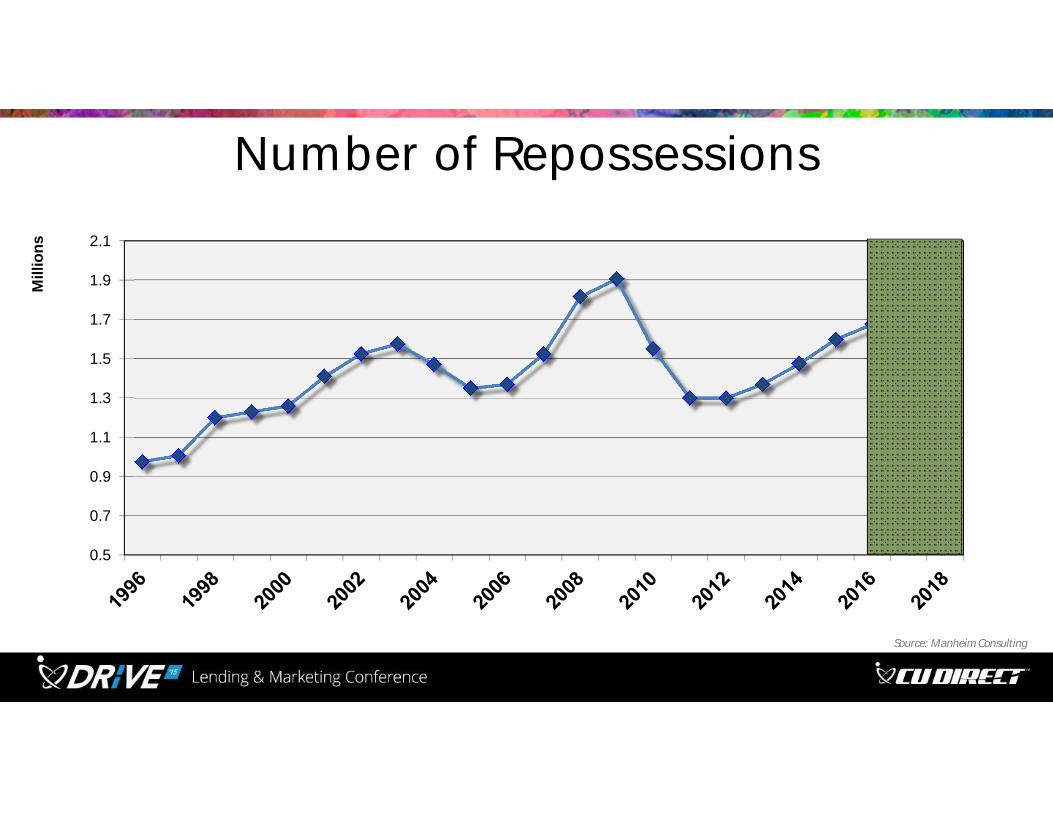

Number of Repossessions

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

Mill

ions

Source: Manheim Consulting

Total Wholesale Supply: Off-rental, Off-lease, & Repos

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Mill

ions

Source: Manheim Consulting

But the total wholesale market is more than 20 million transactions per year

Dominant ForcesShaping the Automotive Industry

19

ExchangeRates

EnergyMarkets

Credit ConditionsLonger-term loans

Availability

Lease subvention

Interest rates

Severity of loss

LTVs

Labor Market

Age & education differences

Participation rate

Hours and earnings

Involuntary part-time

Under-employed

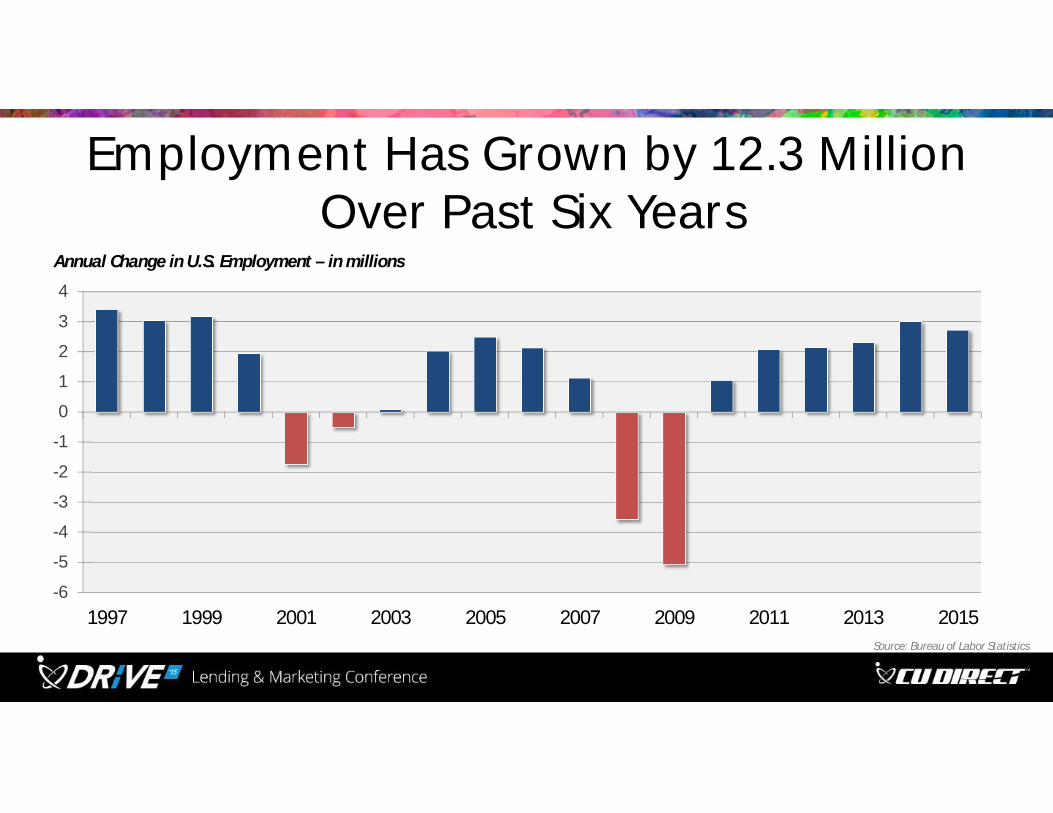

Employment Has Grown by 12.3 MillionOver Past Six Years

-6

-5

-4

-3

-2

-1

0

1

2

3

4

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015Source: Bureau of Labor Statistics

Annual Change in U.S. Employment – in millions

Percent Change From Previous Peak

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Full-time employment Total employment

Source: BLS

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Source: Bureau of Labor Statistics

Initial Jobless Claims

The Retail Financing Market

Longer loans with

Lower downs to

Lower FICOS

Record Lease Penetration

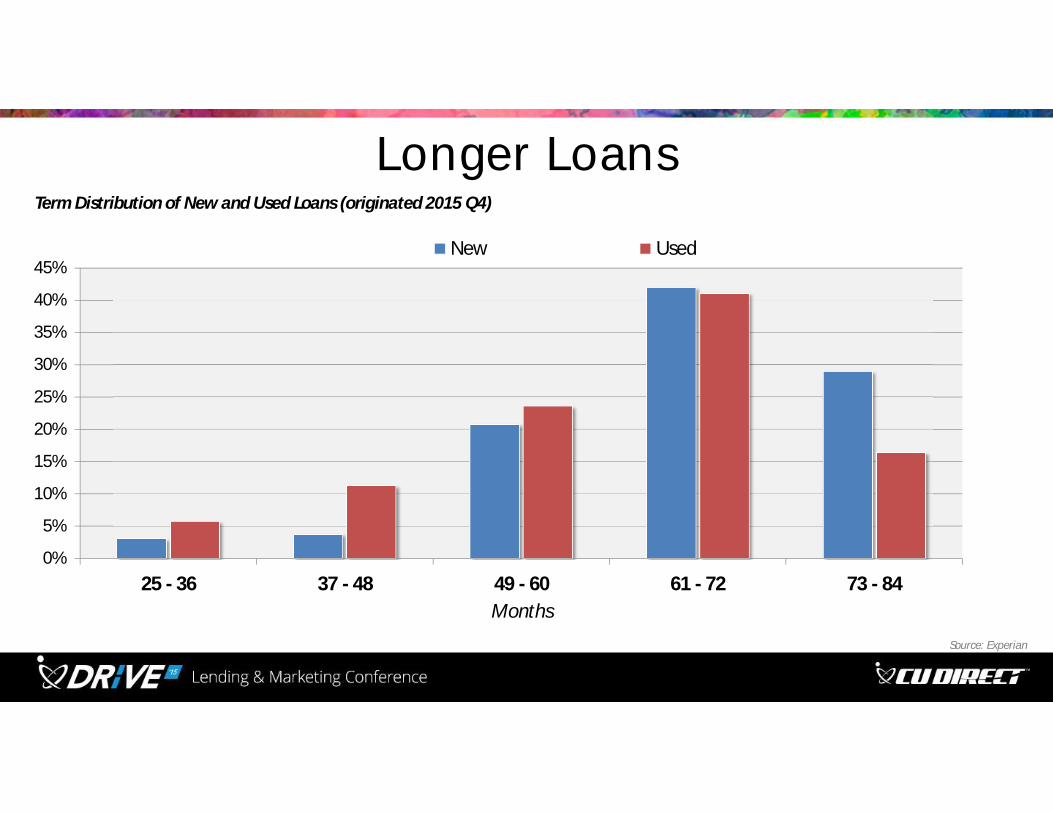

Longer Loans

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

25 - 36 37 - 48 49 - 60 61 - 72 73 - 84Months

New Used

Source: Experian

Term Distribution of New and Used Loans (originated 2015 Q4)

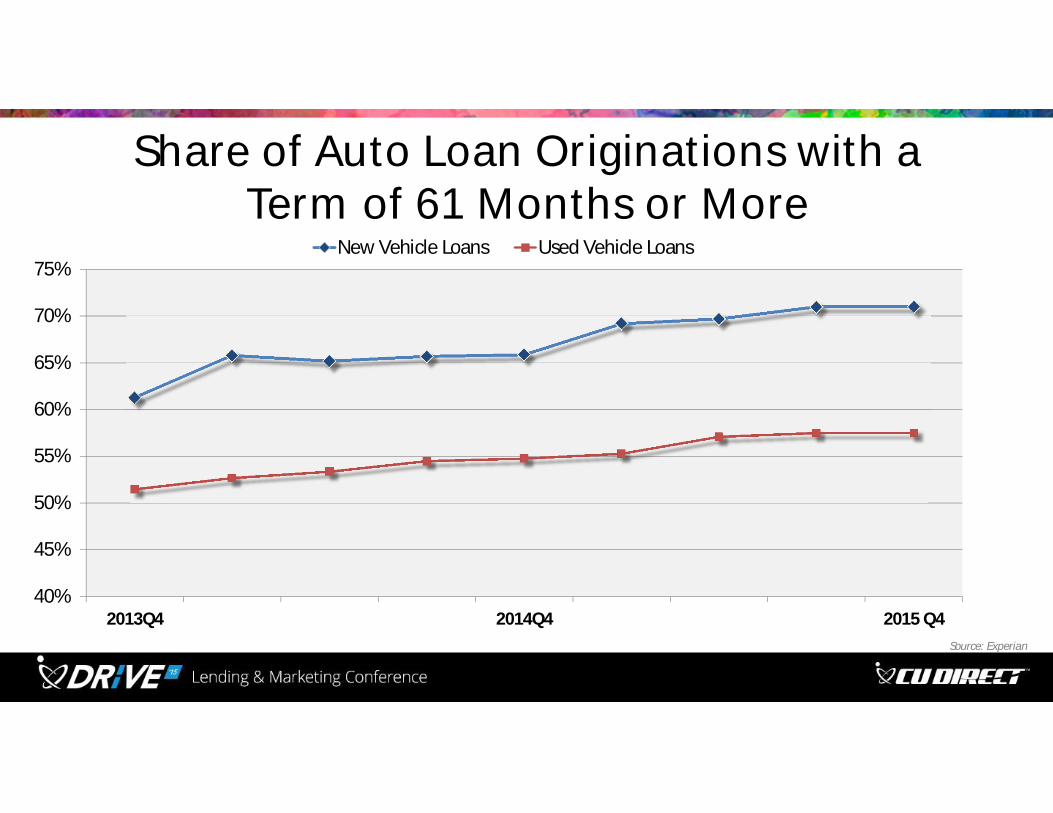

Share of Auto Loan Originations with a Term of 61 Months or More

40%

45%

50%

55%

60%

65%

70%

75%

2013Q4 2014Q4 2015 Q4

New Vehicle Loans Used Vehicle Loans

Source: Experian

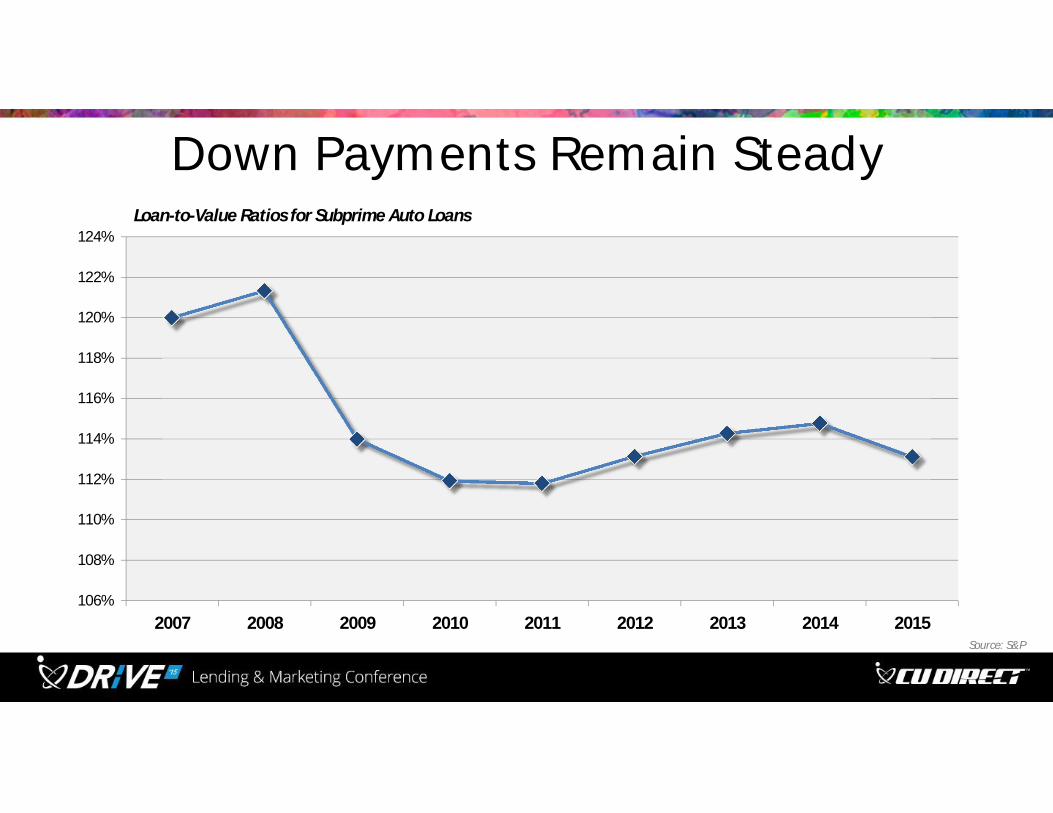

Down Payments Remain Steady

106%

108%

110%

112%

114%

116%

118%

120%

122%

124%

2007 2008 2009 2010 2011 2012 2013 2014 2015Source: S&P

Loan-to-Value Ratios for Subprime Auto Loans

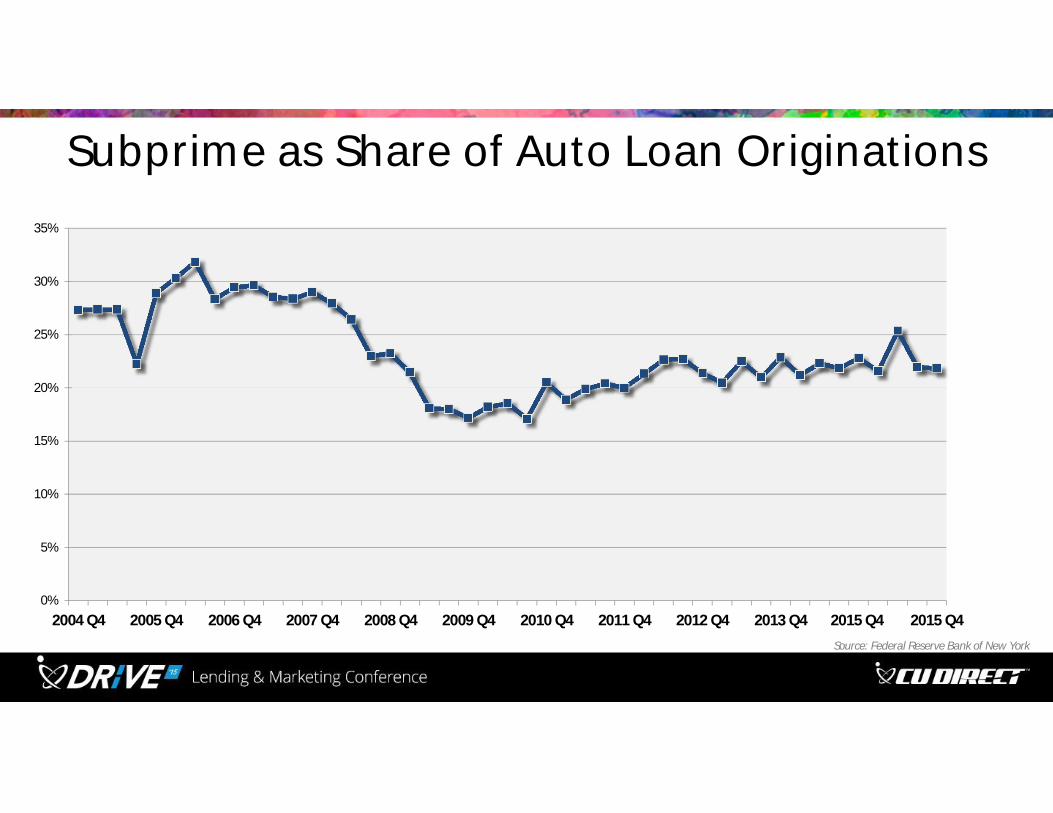

Subprime as Share of Auto Loan Originations

0%

5%

10%

15%

20%

25%

30%

35%

2004 Q4 2005 Q4 2006 Q4 2007 Q4 2008 Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q4 2013 Q4 2015 Q4 2015 Q4

Source: Federal Reserve Bank of New York

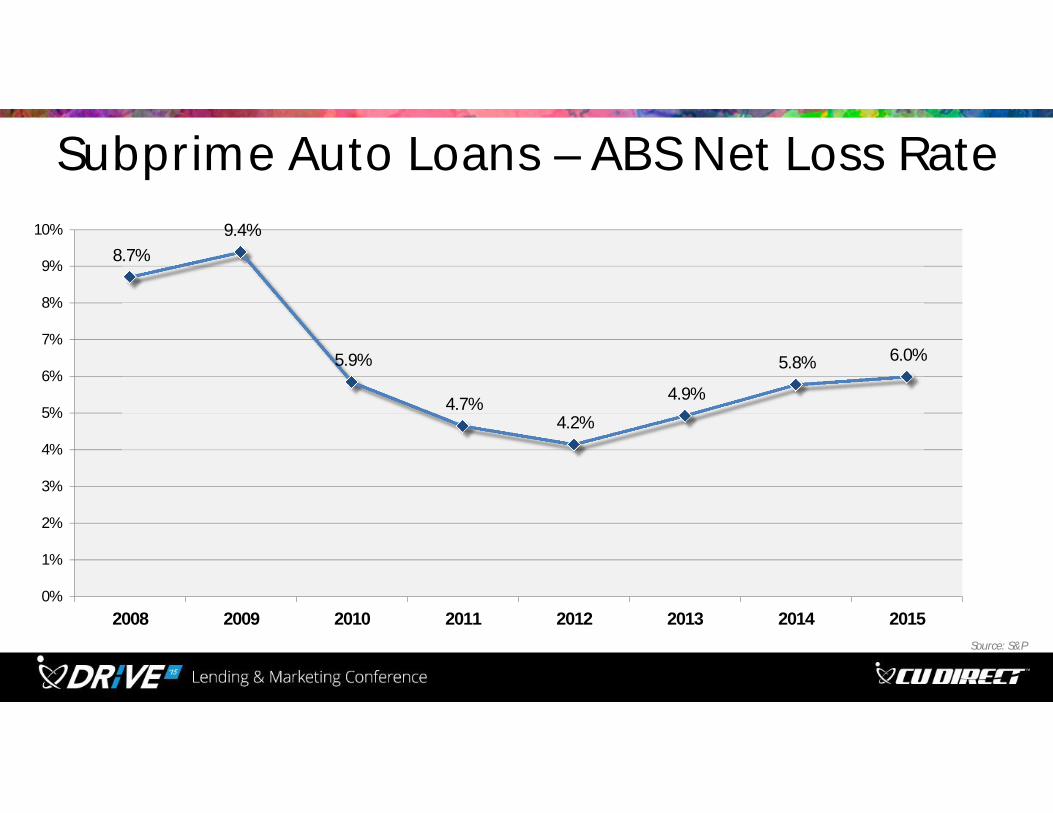

Subprime Auto Loans – ABS Net Loss Rate

8.7%9.4%

5.9%

4.7%4.2%

4.9%

5.8% 6.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2008 2009 2010 2011 2012 2013 2014 2015Source: S&P

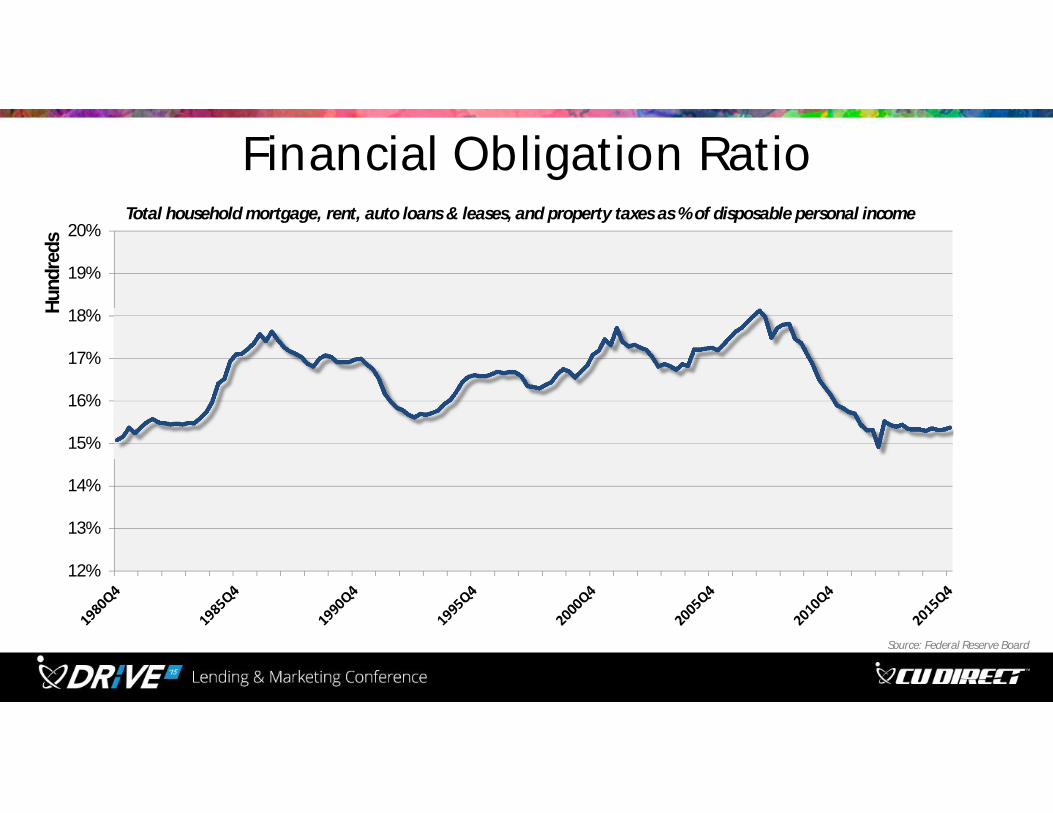

Financial Obligation Ratio

12%

13%

14%

15%

16%

17%

18%

19%

20%

Hund

reds

Total household mortgage, rent, auto loans & leases, and property taxes as % of disposable personal income

Source: Federal Reserve Board

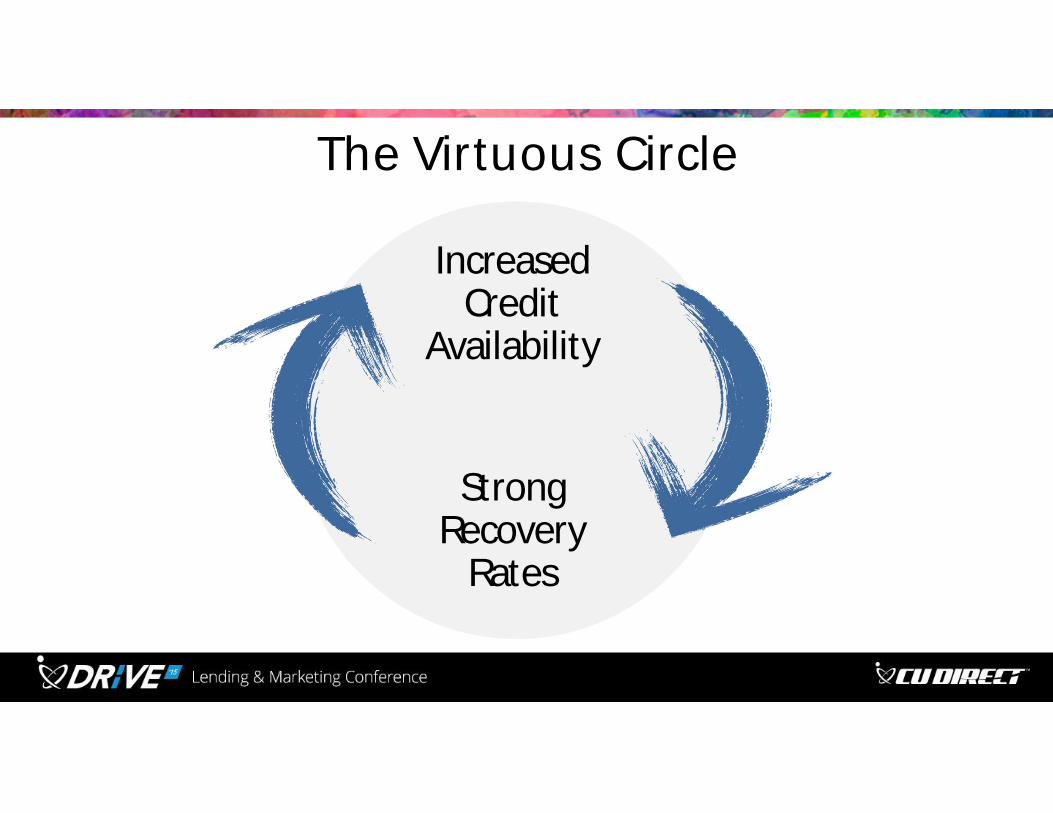

The Virtuous Circle

IncreasedCredit

Availability

StrongRecovery

Rates

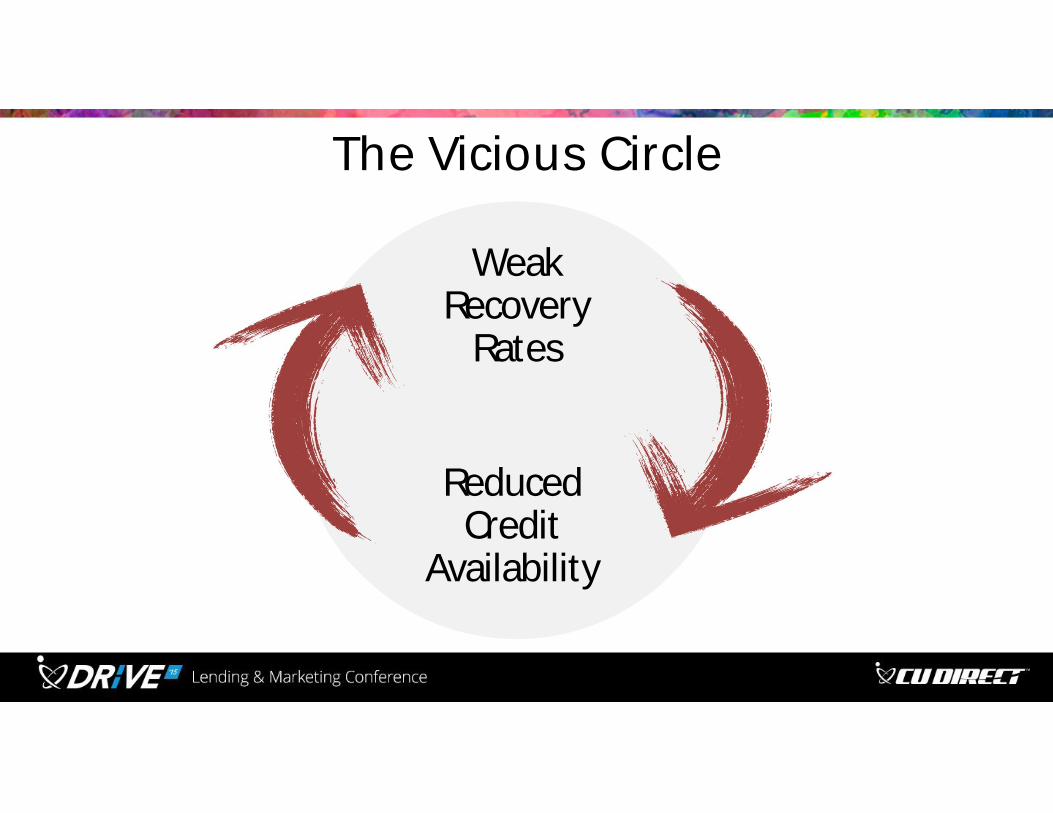

The Vicious Circle

WeakRecovery

Rates

ReducedCredit

Availability

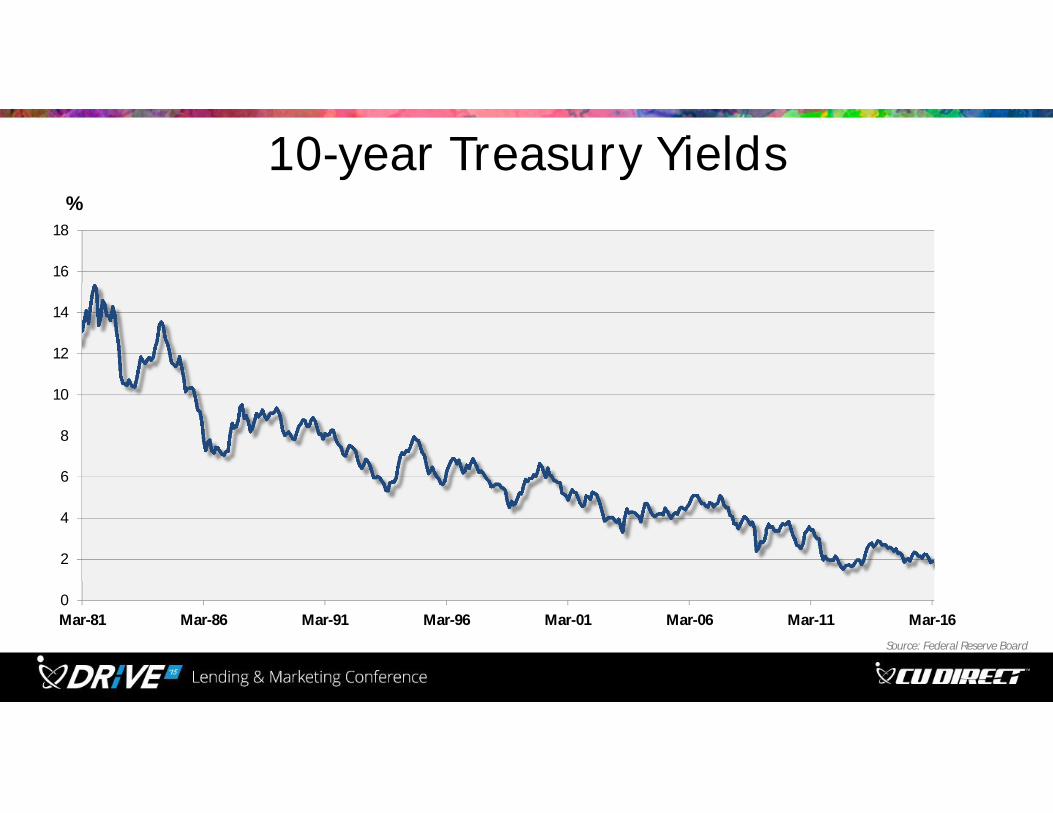

10-year Treasury Yields

0

2

4

6

8

10

12

14

16

18

Mar-81 Mar-86 Mar-91 Mar-96 Mar-01 Mar-06 Mar-11 Mar-16

Source: Federal Reserve Board

%

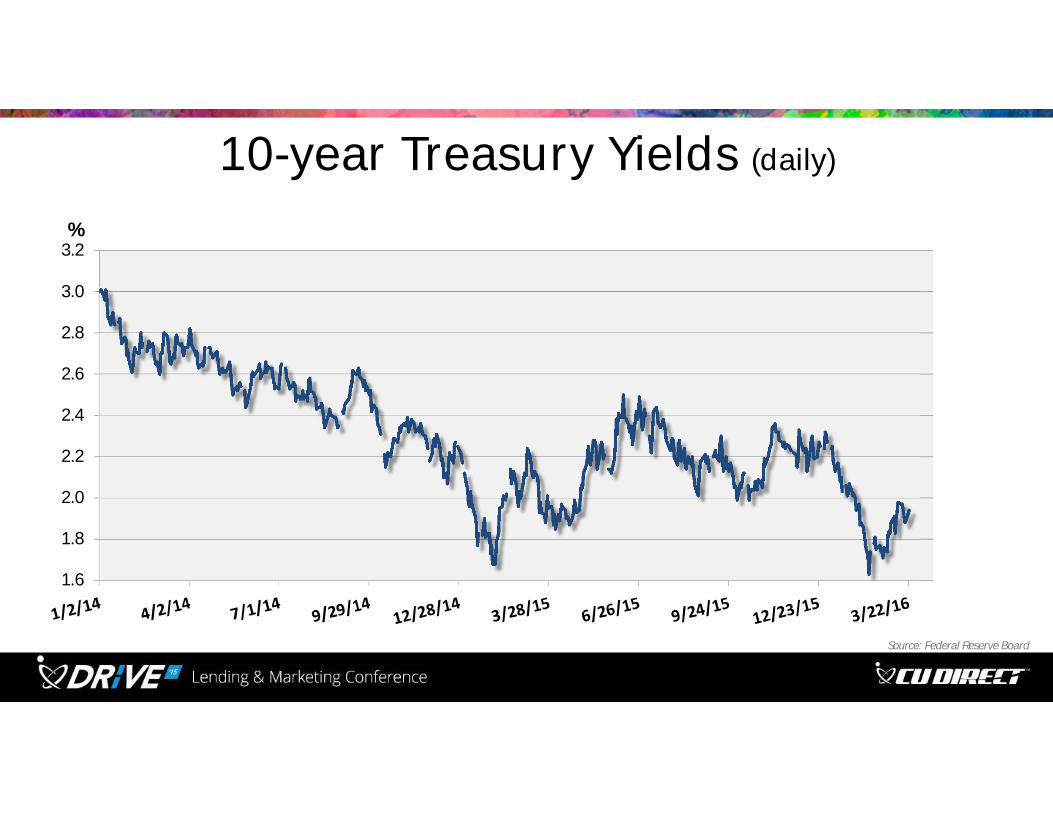

10-year Treasury Yields (daily)

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2%

Source: Federal Reserve Board

“A shift in auto lending will not be the proximate cause for any near-term downturn in the auto industry or the economy at large.

Reporters, financial analysts, and regulators who are focusing their concern on auto lending are looking at the tree. Meanwhile, the forest – global financial markets – is encircled in flames and infested with parasites.”

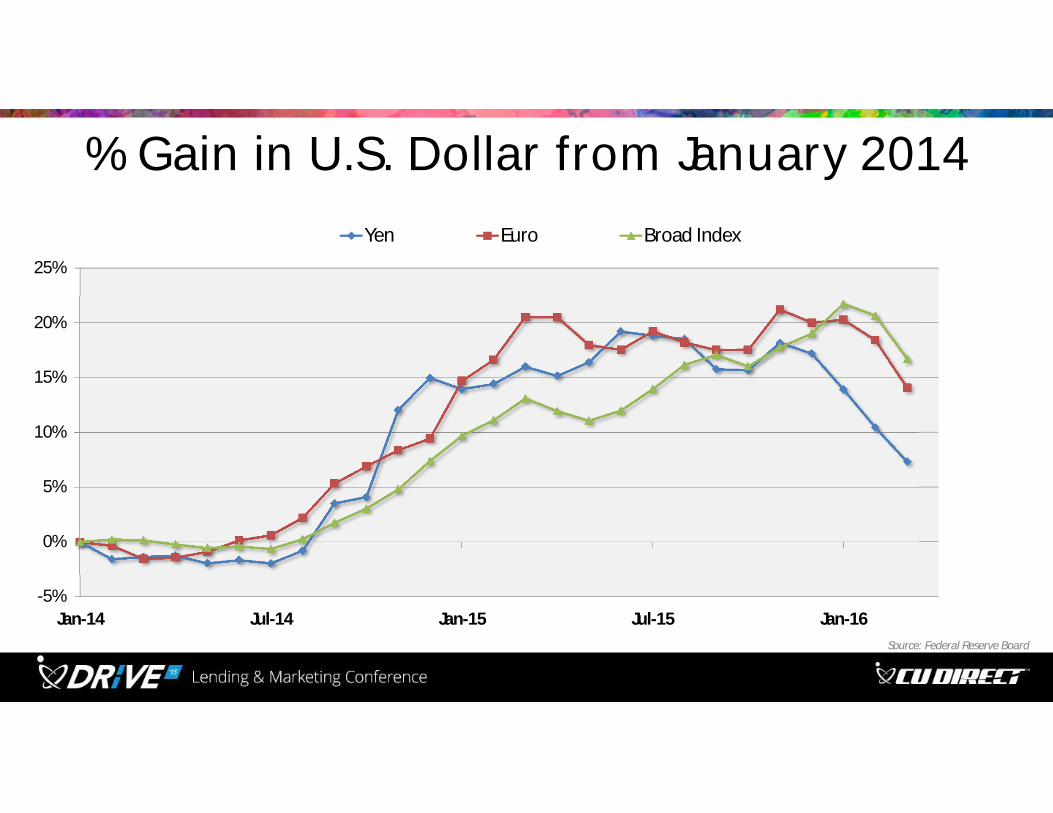

% Gain in U.S. Dollar from January 2014

-5%

0%

5%

10%

15%

20%

25%

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Yen Euro Broad Index

Source: Federal Reserve Board

New Car & Light-Duty Truck Sales

4

6

8

10

12

14

16

18

20

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

millions of units

Source: Automotive News

Used Vehicle Production

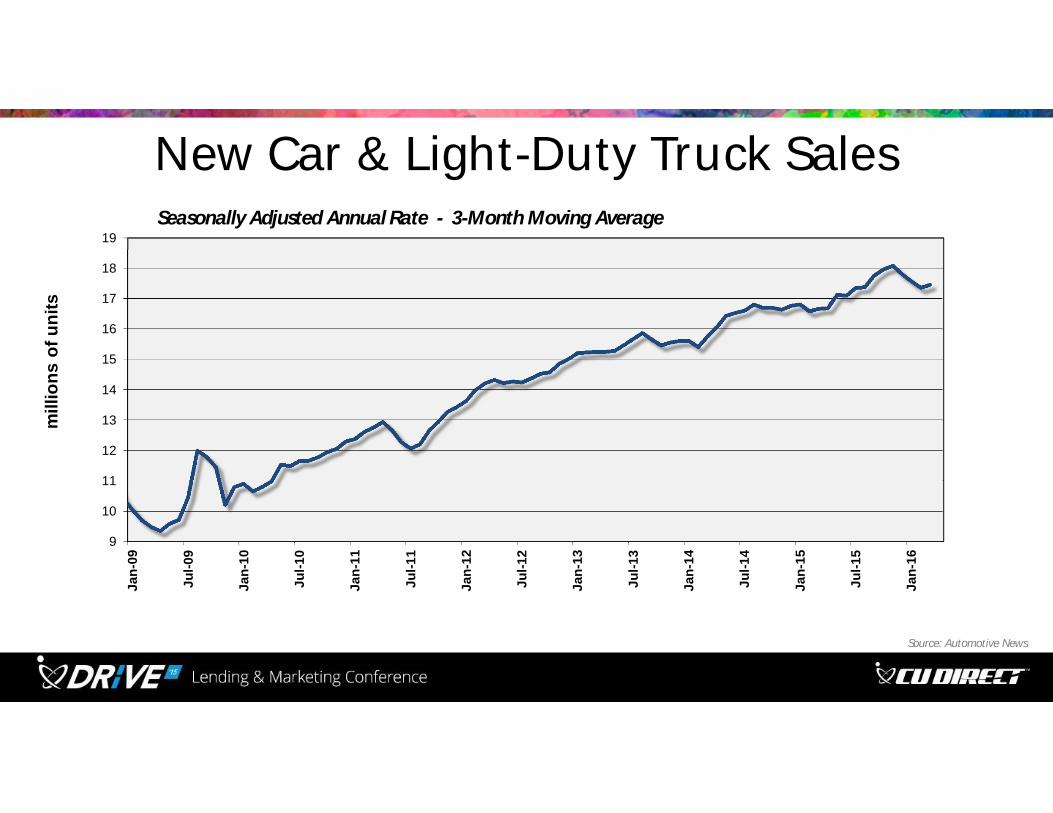

New Car & Light-Duty Truck Sales

9

10

11

12

13

14

15

16

17

18

19

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

mill

ions

of u

nits

Source: Automotive News

Seasonally Adjusted Annual Rate - 3-Month Moving Average

% Change Used Units Retailed – Same Store Basis(Publicly-traded Dealership Groups)

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Company filings

Weighted average for KMX *, AN, PAG, SAH, GPI, ABG, and LAD

*KMX shifted forward one month to correspond with calendar quarter

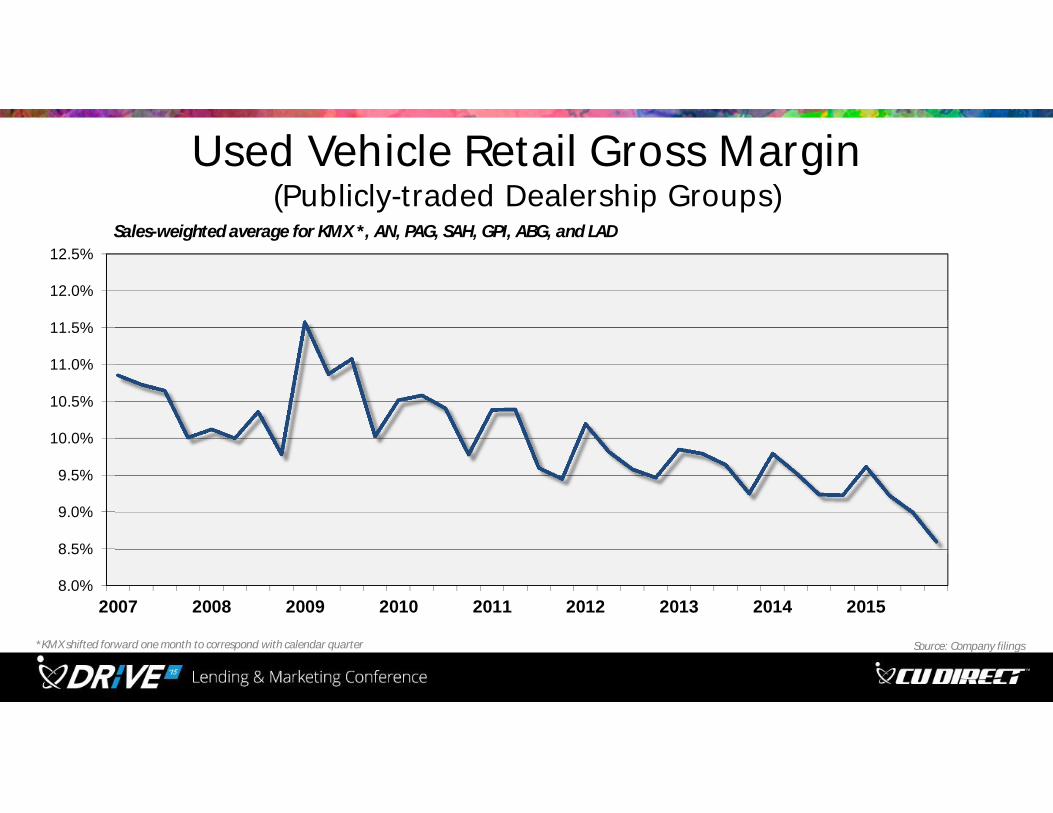

Used Vehicle Retail Gross Margin (Publicly-traded Dealership Groups)

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

12.0%

12.5%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Sales-weighted average for KMX *, AN, PAG, SAH, GPI, ABG, and LAD

Source: Company filings *KMX shifted forward one month to correspond with calendar quarter

SummarySlow economic growth with rising recession risks.

New vehicle sales pace levels off.

Growing wholesale supplies force higher used vehicle sales.

Favorable financing environment runs awhile longer.