can feed in tariffs close the investment gap for renewable ... · university of exeter damian...

TRANSCRIPT

University of Exeter

DAMIAN WAGNER

RENEWABLE ENERGY FINANCE

CAN FEED‐IN TARIFFS CLOSE THE INVESTMENT GAP FOR RENEWABLE ENERGY IN DEVELOPING

COUNTRIES?

MSc THESIS

P a g e | 2

EXETER UNIVERSITY

SCHOOL OF GEOGRAPHY

MSc THESIS ACADEMIC YEAR 2009/2010

DAMIAN WAGNER

RENEWABLE ENERGY FINANCE

CAN FEED‐IN TARIFFS CLOSE THE INVESTMENT GAP FOR RENEWABLE ENERGY IN DEVELOPING

COUNTRIES?

Supervisor: Catherine Mitchell

September 2010

SUBMITTED BY DAMIAN WAGNER TO THE UNIVERSITY OF EXETER AS A

DISSERTATION TOWARDS THE DEGREE OF MASTER OF SCIENCE BY ADVANCED STUDY IN ENERGY POLICY AND SUSTAINABILITY

I certify that all material in this dissertation which is not my own work has been identified with appropriate acknowledgement and referencing and I also certify that no material is included for which a degree has been previously conferred upon me...........................

P a g e | 3

ABSTRACT

Over the last two years new global financial investment in sustainability energy has been at its

highest ever, surpassing even investment in new fossil fuel capacity. However, the world’s poorest

regions, Africa and most of Latin America have attracted little investment. This study aims to

complement the discussion about feed‐in tariffs in developing countries and the funding of those

schemes.

Data triangulation was utilized in order to gain a combination of research perspectives on the topic.

Semi‐ structured interviews were conducted in order to compile the perceptions and opinions of

major senior stakeholders with a strong link to Renewable Energy (RE) projects. Information on the

current role of feed‐in tariffs and whether those schemes can address the investment gap in

developing countries was collected from qualitative data analysis.

To date the right condition for investment in feed‐in tariff schemes are absent in developing

countries. As a result, such schemes are not yet fully operational. An approach to address this

problem and encourage the funding of feed‐in tariffs on the basis of avoided costs will be briefly

introduced in the final section of this study. Such measures will be essential to get projects ‘on the

ground’ and create track records and bankable projects in order to promote investment in

renewable energy.

P a g e | 4

ACKNOWLEDGEMENTS

I would like to express thanks to my tutor and supervisor Catherine Mitchell for her advice and support and Catherine and Bridget for making this a very inspiring and enjoyable energy policy‐ year

in Cornwall.

I very much like to thank all interviewees for the great interviews, excellent discussions and additional advice and support that many of them have provided along the way.

I am extremely grateful for the (moral) support I had in particular from Claudia and Hilli;

Special thanks to Glory and Valerie

P a g e | 5

TABLE OF CONTENT

ABSTRACT……………………………………………………………………………………………………………………………………..3

ACKNOWLEDGEMENTS………………………………………………………………………………………………………………….4

TABLE OF CONTENT……………………………………….……………………………………………………………………………..5

TABLE OF FIGURES………………………………………………………………………………………………………………………..7

ABBREVIATIONS AND TERMS OF REFERENCE ……………………………………………………..………………………..8

1 INTRODUCTION ..................................................................................................................... 10

1.1 Context .................................................................................................................................. 10

1.1.1 Global driver for Renewable Energy: Increasing Energy Demand ................................ 10

1.1.2 Beyond climate change: domestic drivers .................................................................... 10

1.1.3 Costs .............................................................................................................................. 11

1.2 Aims and objectives .............................................................................................................. 12

1.3 Structure of the study ........................................................................................................... 12

2 LITERATURE REVIEW ............................................................................................................. 14

2.1 Global financial investment in renewable energy ................................................................ 14

2.2 Renewable Energy Finance in Developing Countries ............................................................ 16

2.2.1 Sources of private capital .............................................................................................. 16

2.2.2 Constraints and challenges for Investment in Renewable Energy ................................ 18

2.2.3 The role of public Finance ............................................................................................. 21

2.3 Carbon Finance ‐ the icing on the cake ................................................................................. 23

2.4 Renewable Energy Policy – a finance perspective .............................................................. 25

2.4.1 NAMAs – Supporting RE in developing countries in post‐2012 .................................... 26

2.5 Feed‐in tariff schemes for developing countries .................................................................. 27

2.5.1 Core principles .............................................................................................................. 27

2.5.2 Remuneration models ................................................................................................... 28

2.5.3 Financing Mechanism ................................................................................................... 29

2.5.4 Feed‐in tariffs schemes in developing countries .......................................................... 30

2.5.5 CDM vs. Feed‐in tariffs .................................................................................................. 34

2.6 Research ................................................................................................................................ 35

2.7 Research Questions............................................................................................................... 36

P a g e | 6

3 METHODOLOGY .................................................................................................................... 37

3.1 Research approach ................................................................................................................ 37

3.2 Literature review ................................................................................................................... 39

3.3 Conferences and Preliminary Discussions ............................................................................ 39

3.4 Interviews .............................................................................................................................. 40

3.4.1 Selection of interviewees .............................................................................................. 40

3.4.2 Question design ............................................................................................................ 42

3.4.3 Interview Analysis ......................................................................................................... 43

4 IN PERSPECTIVE‐ RE FINANCE AND FEED‐ IN TARIFFS IN DEVELOPING COUNTRIES ................. 44

4.1 The start‐up finance gap ....................................................................................................... 44

4.2 Challenging RE Policy – a developer’s perspective ............................................................... 45

4.2.1 Domestic needs ............................................................................................................. 45

4.2.2 National leadership and coordination .......................................................................... 46

4.3 The current role of feed‐in tariffs in developing countries................................................... 48

4.3.1 Asia ................................................................................................................................ 48

4.3.2 Latin America ................................................................................................................ 49

4.3.3 Country Risk – The Example of Ecuador ....................................................................... 50

4.3.4 Africa ............................................................................................................................. 51

4.3.5 ESKOM ‐ Referee and Player: The Case of South Africa ............................................... 51

4.4 FIT for a renewable energy future in developing countries? ................................................ 53

4.4.1 Mini‐grids and off‐ grid solutions .................................................................................. 54

4.4.2 Funding feed‐in tariffs schemes .................................................................................... 54

4.5 NAMAs and FITs in a post‐Kyoto framework ........................................................................ 55

4.6 CRYSTAL BALL: Predictions about the direction of RE finance ............................................. 57

5 KEY FINDINGS ........................................................................................................................ 58

6 DISCUSSION .......................................................................................................................... 61

7 CONCLUSION ......................................................................................................................... 65

APPENDICES .................................................................................................................................. 67

REFERENCES.……………………………………………………………………………………………………………………………….69

P a g e | 7

LIST OF FIGURES

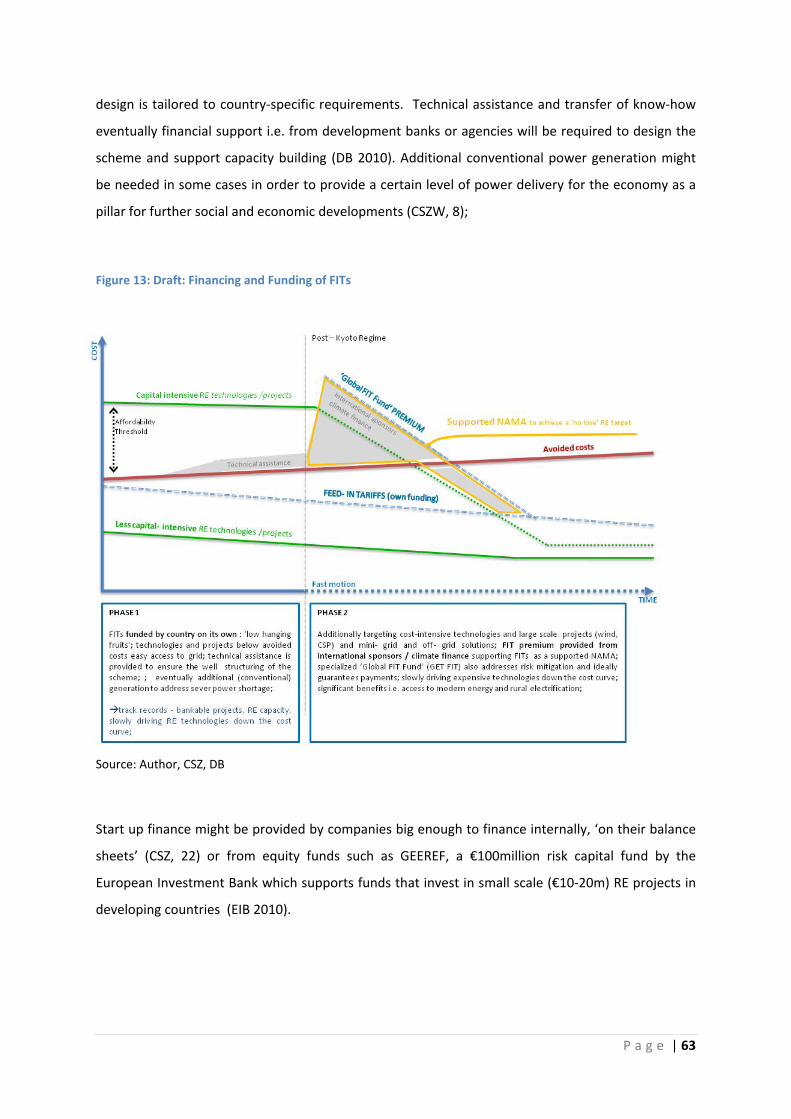

Figure 1: Share of people without access to electricity, 2008 .............................................................. 11 Figure 2: Global New Investment in sustainable energy, 2004‐2009 $BN ........................................... 14 Figure 3: Financial New Investment by Region ..................................................................................... 15 Figure 4: Types of finance …………………………………………………………………………………………………. ............ 18 Figure 5: Risks for private investors in renewable energy projects ...................................................... 18 Figure 6: The role of public finance ...................................................................................................... 21 Figure 7: FIT remuneration models ....................................................................................................... 28 Figure 8: FIT Basic Financing Mechanism ............................................................................................. 29 Figure 9: Developing Countries with FIT Policies .................................................................................. 30 Figure 11: Barriers to RE and 'GET FIT' solutions .................................................................................. 32 Figure 10: GET FIT Program ................................................................................................................... 32 Figure 12: Research Phases ................................................................................................................... 38 Figure 13: Financing and Funding of FITs .............................................................................................. 68

P a g e | 8

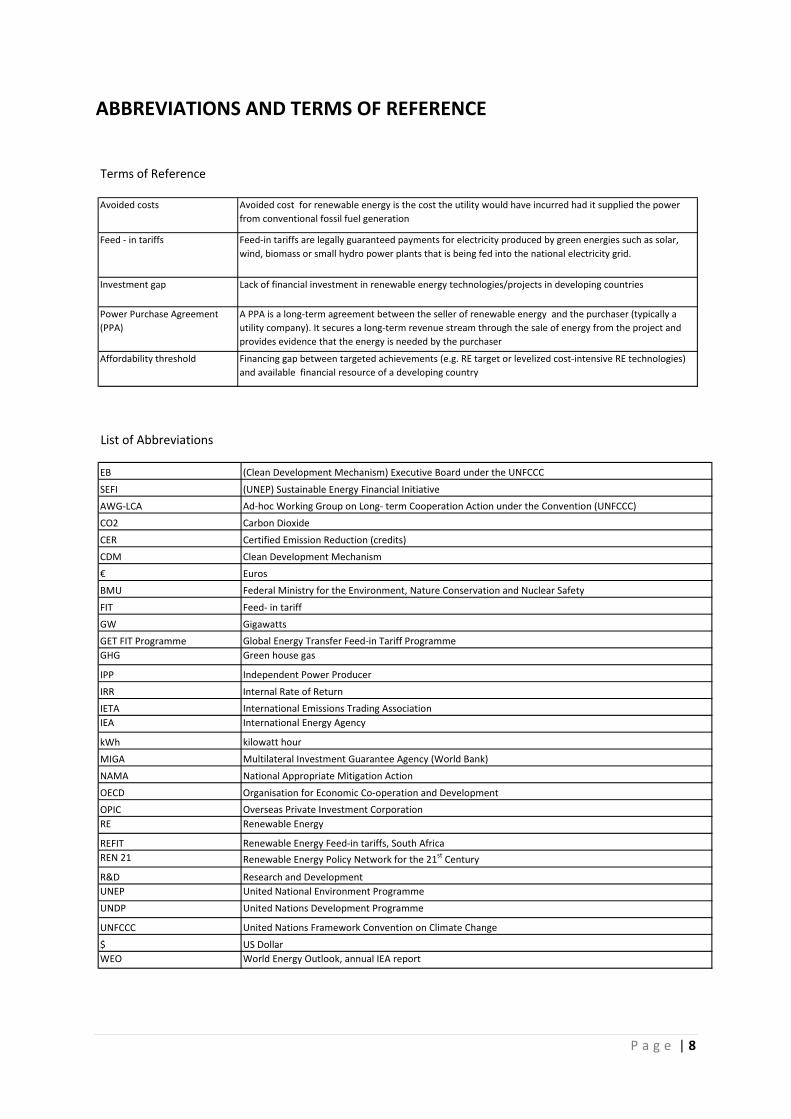

ABBREVIATIONS AND TERMS OF REFERENCE

Terms of Reference

Avoided costs Avoided cost for renewable energy is the cost the utility would have incurred had it supplied the power from conventional fossil fuel generation

Feed ‐ in tariffs Feed‐in tariffs are legally guaranteed payments for electricity produced by green energies such as solar, wind, biomass or small hydro power plants that is being fed into the national electricity grid.

Investment gap Lack of financial investment in renewable energy technologies/projects in developing countries

Power Purchase Agreement (PPA)

A PPA is a long‐term agreement between the seller of renewable energy and the purchaser (typically a utility company). It secures a long‐term revenue stream through the sale of energy from the project and provides evidence that the energy is needed by the purchaser

Affordability threshold Financing gap between targeted achievements (e.g. RE target or levelized cost‐intensive RE technologies) and available financial resource of a developing country

List of Abbreviations

EB (Clean Development Mechanism) Executive Board under the UNFCCC

SEFI (UNEP) Sustainable Energy Financial Initiative

AWG‐LCA Ad‐hoc Working Group on Long‐ term Cooperation Action under the Convention (UNFCCC)

CO2 Carbon Dioxide

CER Certified Emission Reduction (credits)

CDM Clean Development Mechanism

€ Euros

BMU Federal Ministry for the Environment, Nature Conservation and Nuclear Safety

FIT Feed‐ in tariff

GW Gigawatts

GET FIT Programme Global Energy Transfer Feed‐in Tariff ProgrammeGHG Green house gas

IPP Independent Power Producer

IRR Internal Rate of Return

IETA International Emissions Trading AssociationIEA International Energy Agency

kWh kilowatt hour

MIGA Multilateral Investment Guarantee Agency (World Bank)

NAMA National Appropriate Mitigation Action

OECD Organisation for Economic Co‐operation and Development

OPIC Overseas Private Investment CorporationRE Renewable Energy

REFIT Renewable Energy Feed‐in tariffs, South AfricaREN 21 Renewable Energy Policy Network for the 21st Century

R&D Research and DevelopmentUNEP United National Environment Programme

UNDP United Nations Development Programme

UNFCCC United Nations Framework Convention on Climate Change

$ US DollarWEO World Energy Outlook, annual IEA report

P a g e | 9

"Paths are made by walking"

‐ Franz Kafka –

P a g e | 10

1 INTRODUCTION

This chapter introduces the current research project by setting the context, providing rationale and

identifying the research objectives.

1.1 Context

1.1.1 Global driver for Renewable Energy: Increasing Energy Demand

Renewable energy plays a key role in curbing man‐made greenhouse gas emissions (GHG). In 2007

energy use accounted for 65% of the world’s GHG emissions (IEA 2009). Only one year earlier, China

overtook the United States as the biggest absolute emitter of CO2 (PBL 2007).

Looking forward, global electricity demand will rise by 76% from 2007‐2030 requiring additional

power‐generation capacity of 4,800 Gigawatts (GW). By 2030 over 80% of the world’s electricity

demand will be originated in Non‐OECD countries. The lion’s share, about 53%, of incremental

demand will come from China and India (IEA 2009).

Africa’s population of currently more than 1 billion will rise to almost 2 billion in 2050 (UNDP 2008)

However, at present it only contributes to 1.5% of global annual energy‐related CO2 emissions rising

to 2‐3% by 2050 (WB 2009).

1.1.2 Beyond climate change: domestic drivers

One fifth of the world’s population, 1.5 billion people lack access to electricity in their homes (IEA

2009), of which 834 million live in a least developed country (WHO and UNDP 2009). About 2.4

billion people lack access to modern energy and use traditional biomass fuels such as waste or

fuelwood in their homes (IEA 2008). This practice causes the death of 1.94 million people, mostly

women and children, from indoor air pollution every year. (WHO and UNDP 2009).

P a g e | 11

At about 26%, Africa has the lowest global electrification rate, which means that 547 million people

have no access to electricity. A demand‐ supply balance would require investment of about $40

billion or 6.4% of the region’s GDP. About $11 billion are currently spent on the region’s electricity

infrastructure leaving an investment gap of $30 billion per year (WB 2009).

Constant power deficits in developing countries have led to large numbers of ‘emergency

generation’ from containerized mobile diesel units. Fuel based lightening costs households and

business in Africa about $17 billion every year (WB 2009). A UN and World Bank study found that oil

prices of about $20 per barrel could reduce poorer countries’ GDP by up to 3% (2008: oil price at

$148/barrel). Out of the world’s poorest 47 countries, 38 are net importers of oil and 25 import all

their oil (UNDP 2005).

Renewable energy can provide access to modern energy, ease dependency on fossil fuels and

increase resilience to volatile fuel prices while addressing both economic and social developments

and security of energy supply (ARE 2007; UNDP 2005).

1.1.3 Costs

In order to limit global warming to 2°C (450 part per million) by 2020, the International Energy

Agency (IEA) estimates that an additional investment in low‐ carbon technologies and energy

efficiency close to $430 billion will be needed. Over the period 2010‐2030energy‐related investment

Figure 1: Share of people without access to electricity, 2008

Source: UNDP, 2008

P a g e | 12

will sum up to $10.5 trillion. About $197 billion of additional investment in clean energy will be

required in non‐OECD countries (IEA 2009).

The ‘Energy [R]evolution Scenario‘ conducted by Greenpeace and the European Renewable Energy

Council (EREC) projects that overall investment of $14.7 trillion will be required for restructuring the

global energy sector up to 2030. (Greenpeace / EREC 2009) .

Calculations by the United Nations estimate that investment of $432 billion will be needed in the

power sector in 2030 of which $148 billion must be shifted into low carbon technologies such as

renewables, Carbon Capture and Storage CCS, nuclear and hydro. (UNFCCC 2009).

Of these amounts, by far the largest share, about 86% of overall global investment and financial

flows will come from the private sector (UNFCCC 2007).

1.2 Aims and objectives

This study aims to complement the discussion about feed‐in tariffs in developing countries and the

funding of those schemes by employing qualitative, evidence‐ based data from interviews with

major senior stakeholders linked to renewable energy projects in developing countries. The primary

objectives of the study are:

1. To undertake a critical review of recent literature and gain in‐ depth knowledge about

renewable energy finance and feed‐ in tariff schemes in developing countries;

2. To collect evidence‐ based data gained by compiling and analyzing the perceptions and

opinions of major senior stakeholders such as developers and financiers with a strong link

to RE projects;

3. To provide a practice‐ oriented perspective on issues related to present feed‐in tariff

schemes in developing countries and their potential future role and funding;

1.3 Structure of the study

This study begins by putting renewable energy in the context of climate change and the specific

needs of developing countries. Chapter two reviews present relevant background and literature on

renewable energy finance and feed‐in tariffs in developing countries. Chapter three defines the

P a g e | 13

research approach and describes the collection and analysis of data. Key statements and information

extracted from the interviews is described in Chapter four. Main findings from the interviews are

summarized in Chapter five. Finally, findings and a potential approach to funding feed‐in tariffs in

developing countries will be discussed in Chapter six and concluded in Chapter seven.

P a g e | 14

2 LITERATURE REVIEW

This chapter reviews present literature on renewable energy finance and feed‐in tariffs in the

context of developing countries, examining the investment gap and issues relevant to renewable

energy finance further providing relevant background knowledge on the topic.

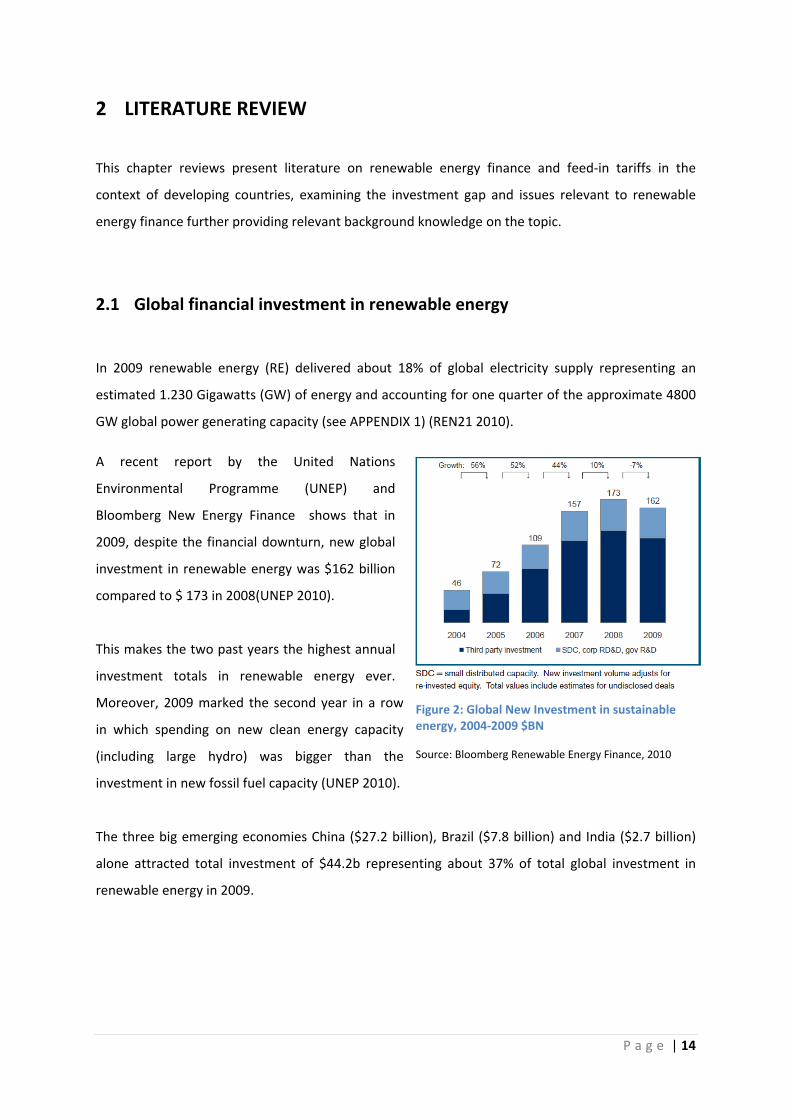

2.1 Global financial investment in renewable energy

In 2009 renewable energy (RE) delivered about 18% of global electricity supply representing an

estimated 1.230 Gigawatts (GW) of energy and accounting for one quarter of the approximate 4800

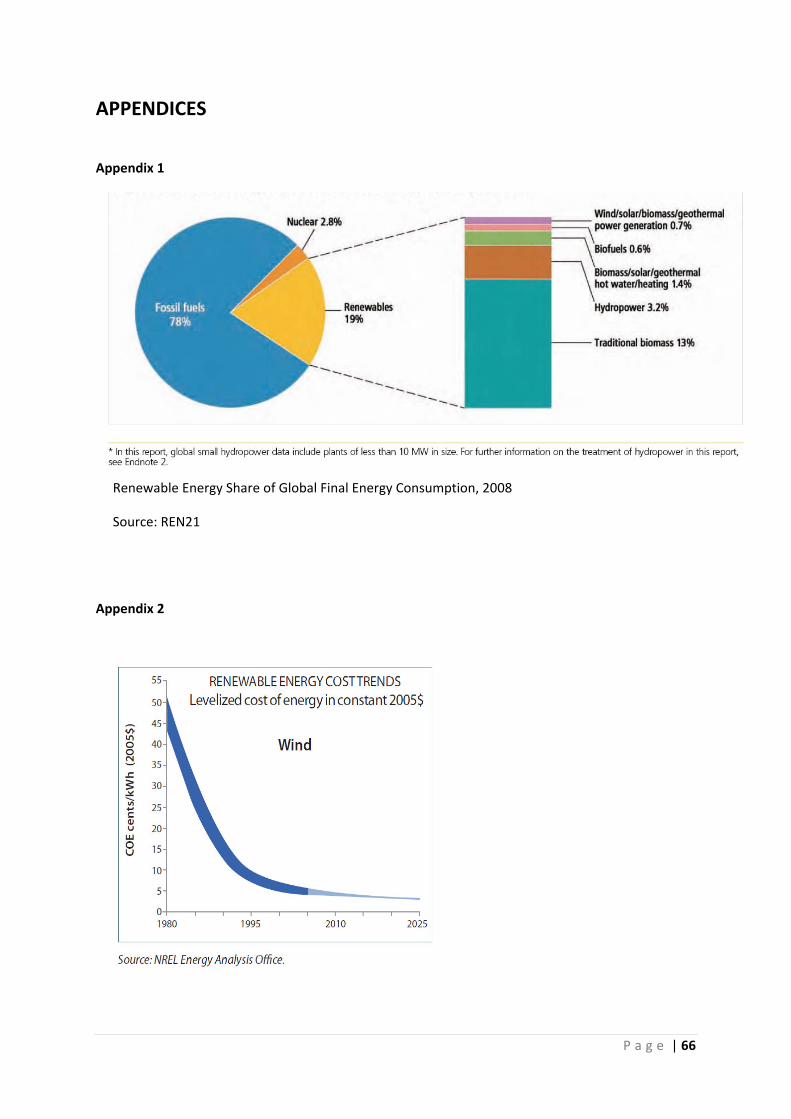

GW global power generating capacity (see APPENDIX 1) (REN21 2010).

A recent report by the United Nations

Environmental Programme (UNEP) and

Bloomberg New Energy Finance shows that in

2009, despite the financial downturn, new global

investment in renewable energy was $162 billion

compared to $ 173 in 2008(UNEP 2010).

This makes the two past years the highest annual

investment totals in renewable energy ever.

Moreover, 2009 marked the second year in a row

in which spending on new clean energy capacity

(including large hydro) was bigger than the

investment in new fossil fuel capacity (UNEP 2010).

The three big emerging economies China ($27.2 billion), Brazil ($7.8 billion) and India ($2.7 billion)

alone attracted total investment of $44.2b representing about 37% of total global investment in

renewable energy in 2009.

Figure 2: Global New Investment in sustainable energy, 2004‐2009 $BN

Source: Bloomberg Renewable Energy Finance, 2010

P a g e | 15

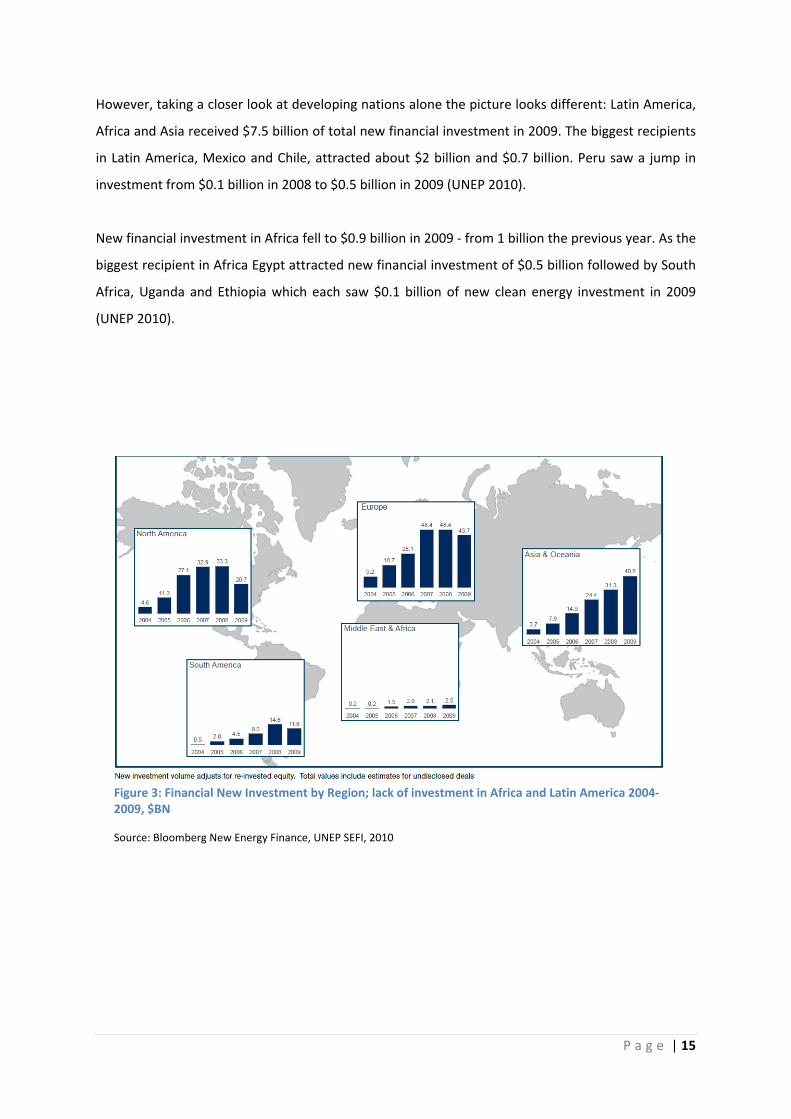

However, taking a closer look at developing nations alone the picture looks different: Latin America,

Africa and Asia received $7.5 billion of total new financial investment in 2009. The biggest recipients

in Latin America, Mexico and Chile, attracted about $2 billion and $0.7 billion. Peru saw a jump in

investment from $0.1 billion in 2008 to $0.5 billion in 2009 (UNEP 2010).

New financial investment in Africa fell to $0.9 billion in 2009 ‐ from 1 billion the previous year. As the

biggest recipient in Africa Egypt attracted new financial investment of $0.5 billion followed by South

Africa, Uganda and Ethiopia which each saw $0.1 billion of new clean energy investment in 2009

(UNEP 2010).

Figure 3: Financial New Investment by Region; lack of investment in Africa and Latin America 2004‐2009, $BN

Source: Bloomberg New Energy Finance, UNEP SEFI, 2010

P a g e | 16

2.2 Renewable Energy Finance in Developing Countries

The chapter outlines basic issues and challenges related to financing renewable energy (RE) in

developing countries.

2.2.1 Sources of private capital

Renewable energy companies have two basic ways to source capital: they can either borrow it from

a bank (debt financing), i.e. as a loan, or they can sell a stake in their business raising equity capital

(equity finance). Equity finance, such as Venture Capital, is used to finance the riskier earlier stages

of a RE project or company. Debt finance usually takes place at a later phase of the project. Bigger

investors and companies, e.g. utilities, might finance RE projects internally ‘on the balance sheet’

(Chatham House 2009; KfW 2005).

Financial institutions that provide debt finance and in particular equity finance will briefly be

outlined below:

Banks (debt finance) provide corporate lending, project finance (limited source finance), refinancing

and mezzanine finance which sits between the top level of senior bank debt (first to be paid in case

of insolvency) and equity ownership of a project or company.

Funds (Equity finance): The level of risk for capital is reflected in the expected ‘Internal Rate of

Return’ (IRR) e.g. high risk for early stage RE technologies. The IRR is a key tool to reach an

investment decision(Chatham House 2009). A listing of the various funds that provides equity

finance plus their defining characteristics and targets follows below:

Venture Capital (VE) funds:

o New technologies and markets, early stage companies

o High risk of failure

o Investment horizon 4‐7 years

o IRR: 50 – 500%

P a g e | 17

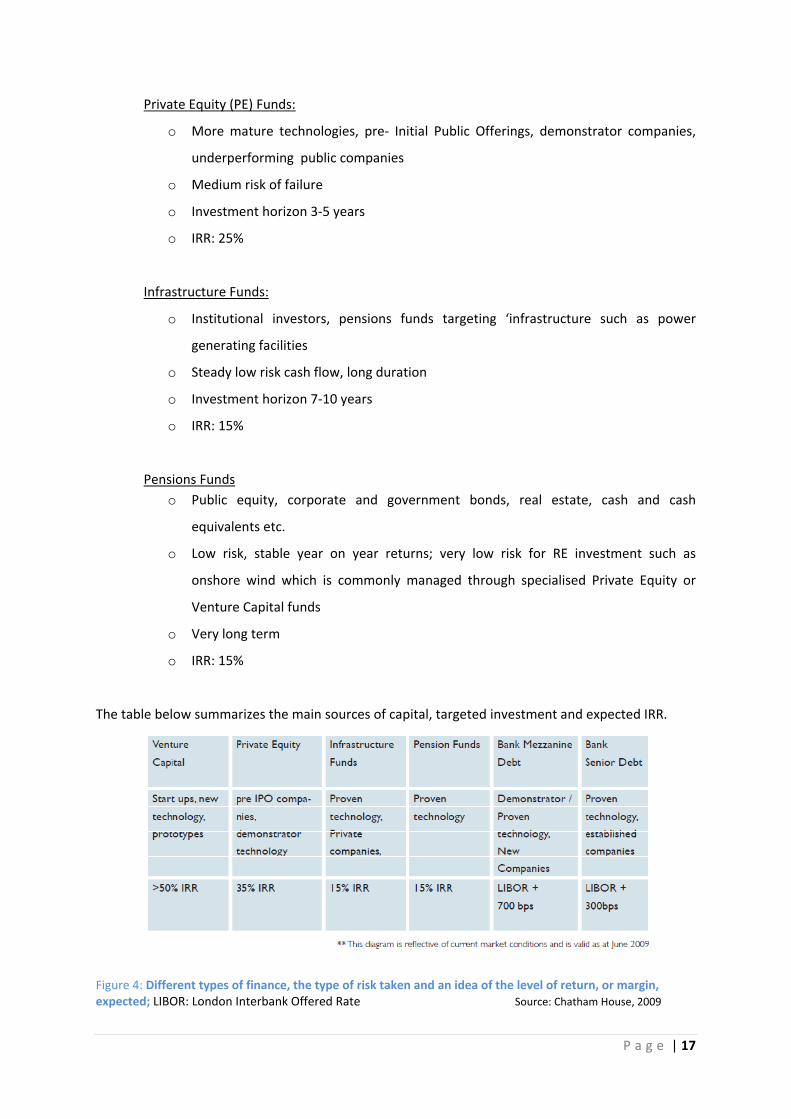

Private Equity (PE) Funds:

o More mature technologies, pre‐ Initial Public Offerings, demonstrator companies,

underperforming public companies

o Medium risk of failure

o Investment horizon 3‐5 years

o IRR: 25%

Infrastructure Funds:

o Institutional investors, pensions funds targeting ‘infrastructure such as power

generating facilities

o Steady low risk cash flow, long duration

o Investment horizon 7‐10 years

o IRR: 15%

Pensions Funds o Public equity, corporate and government bonds, real estate, cash and cash

equivalents etc.

o Low risk, stable year on year returns; very low risk for RE investment such as

onshore wind which is commonly managed through specialised Private Equity or

Venture Capital funds

o Very long term

o IRR: 15%

The table below summarizes the main sources of capital, targeted investment and expected IRR.

Figure 4: Different types of finance, the type of risk taken and an idea of the level of return, or margin, expected; LIBOR: London Interbank Offered Rate Source: Chatham House, 2009

P a g e | 18

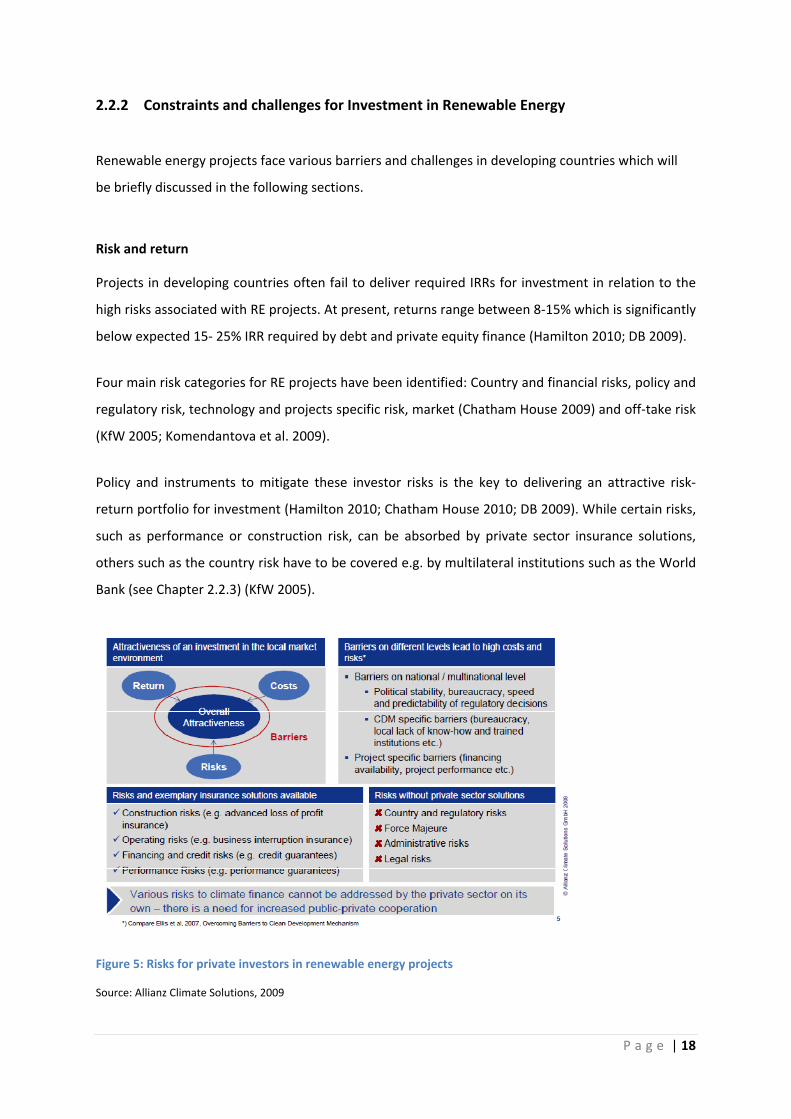

2.2.2 Constraints and challenges for Investment in Renewable Energy

Renewable energy projects face various barriers and challenges in developing countries which will

be briefly discussed in the following sections.

Risk and return

Projects in developing countries often fail to deliver required IRRs for investment in relation to the

high risks associated with RE projects. At present, returns range between 8‐15% which is significantly

below expected 15‐ 25% IRR required by debt and private equity finance (Hamilton 2010; DB 2009).

Four main risk categories for RE projects have been identified: Country and financial risks, policy and

regulatory risk, technology and projects specific risk, market (Chatham House 2009) and off‐take risk

(KfW 2005; Komendantova et al. 2009).

Policy and instruments to mitigate these investor risks is the key to delivering an attractive risk‐

return portfolio for investment (Hamilton 2010; Chatham House 2010; DB 2009). While certain risks,

such as performance or construction risk, can be absorbed by private sector insurance solutions,

others such as the country risk have to be covered e.g. by multilateral institutions such as the World

Bank (see Chapter 2.2.3) (KfW 2005).

Figure 5: Risks for private investors in renewable energy projects

Source: Allianz Climate Solutions, 2009

P a g e | 19

Barriers and Challenges

Roundtables with RE investors and financiers organized by Kirsty Hamilton from Chatham House

highlight the need to bring RE technologies down the cost curve, in order to compete directly with

conventional fuels, which are still subsidized and often favoured by energy policy (Chatham House

2009; UNEP 2008). RE projects are still characterized by high up‐front capital costs, they have little

track record and high perceived risks. Again, the central challenge for private investors is how to

“deliver an attractive return for risks taken” (Hamilton 2010).

The CEO of an African investment firm speaking at the Carbon Expo 2010 in Cologne brought the

challenge for projects in Africa down to three main issues:

1) lack of knowledge;

2) lack of access to finance and;

3) High transition costs for (Clean Development Mechanism) projects.

He emphasized that in order to achieve progress; finance will have to be unlocked on a local level.

Efforts for capacity building will have to be intensified creating track records and implementing well

designed and reliable regulating frameworks (Chingambo 2010).

A Deutsche Bank (DB) study, based on the input of RE stakeholders has identified four main

categories concerning RE investment (DB 2010; DB 2009):

1) Cost competiveness for RE technology: Renewable energy technologies directly compete with

traditional and conventional power generation, which is still highly subsidized by about $170 billion

per year (IEA 2007).Capital competes on a global level and if better returns will be achieved, for

instance in a mature policy‐ backed market in Europe, investment decisions in favour of developing

countries will be hard to justify (Hamilton 2010; DB 2010).

2) Technical and engineering issues: Main issues are the lack of grid infrastructure, access to a

stable grid with the capacity to absorb additional renewable energy and a lack of grid operators that

are able and willing to integrate. Further issues are insufficient knowledge on part of managers and

service providers in order to operate, maintain and monitor the installation (DB 2010). Technology

risk is connected to the lack of track record for new RE technologies (Hamilton 2010).

3) Project development concerns: Mainly related to missing capacity and experience within utilities

and local developers in working with RE policies. Power purchase agreements (PPAs) and standard

P a g e | 20

offer agreements need to be in place. Projects require clear rules and mechanisms and a utility

regulatory structure that cuts down barriers for projects (DB 2010);

A participant at the Chatham House roundtable described the chance to gain access to finance for

‘small‐ scale’ projects at about $10 million and less as very difficult. In spite of the great potential

market for modern electricity and the proven viability and profitability of micro finance, small

institutions, companies and projects are fairly underrepresented. However, a financier at the

roundtable emphasized that ‘smaller deal sizes will be the ‘stepping stone’ for getting to larger deal’

in the future.’(Hamilton 2010).

4) Financial concerns and the access to finance: A good risk‐ return profile is crucial to address

financial concerns (DB 2010). Banks, private equity investors and institutional investors will expect

different rates of return while developers have to manage high up‐front costs and need access to

both equity and debt financing. Another crucial aspect with regards to the development and finance

of a project is to which extent corruption might play a role in a country (DB 2010).

Experience from project RE stakeholders further shows that a lack of familiarity in understanding

and managing technology risks and missing sector know‐how deflates willingness to invest in RE

available in developing countries (Hamilton 2010; KfW 2005). In many cases there is no track record

of well‐ developed RE projects and capacities to lend locally, especially to decentralize energy

systems, are not yet in place (DB 2010).

P a g e | 21

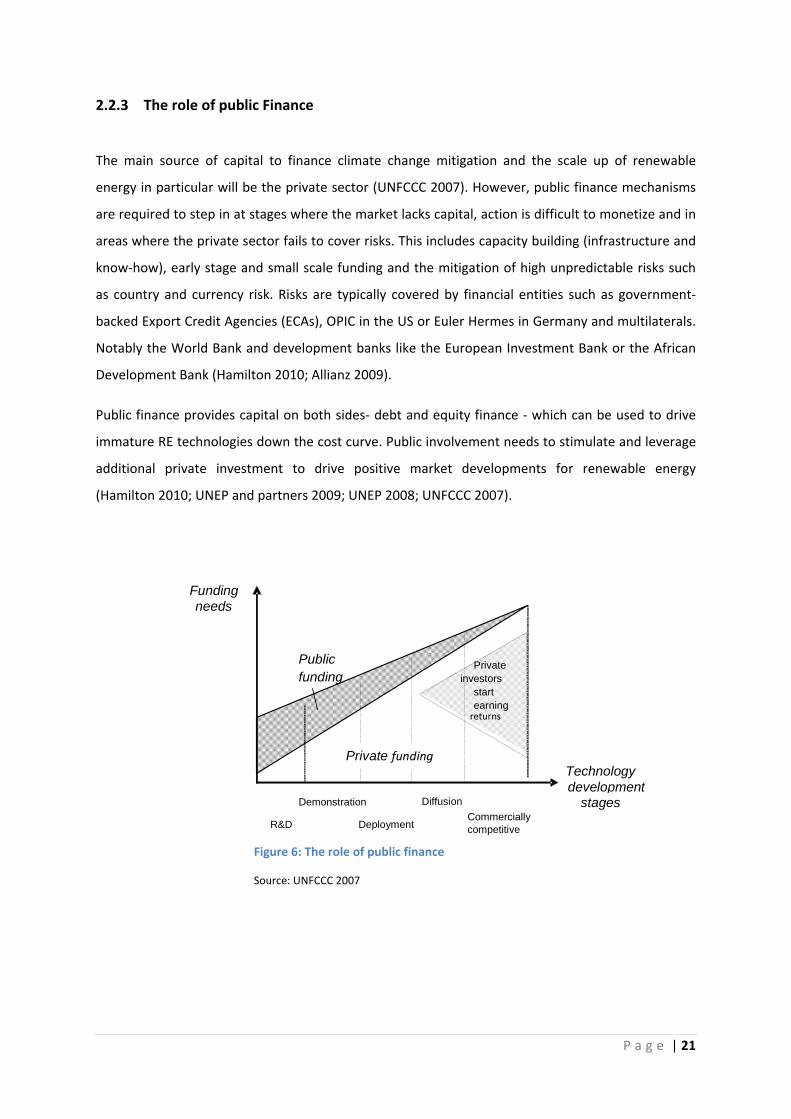

2.2.3 The role of public Finance

The main source of capital to finance climate change mitigation and the scale up of renewable

energy in particular will be the private sector (UNFCCC 2007). However, public finance mechanisms

are required to step in at stages where the market lacks capital, action is difficult to monetize and in

areas where the private sector fails to cover risks. This includes capacity building (infrastructure and

know‐how), early stage and small scale funding and the mitigation of high unpredictable risks such

as country and currency risk. Risks are typically covered by financial entities such as government‐

backed Export Credit Agencies (ECAs), OPIC in the US or Euler Hermes in Germany and multilaterals.

Notably the World Bank and development banks like the European Investment Bank or the African

Development Bank (Hamilton 2010; Allianz 2009).

Public finance provides capital on both sides‐ debt and equity finance ‐ which can be used to drive

immature RE technologies down the cost curve. Public involvement needs to stimulate and leverage

additional private investment to drive positive market developments for renewable energy

(Hamilton 2010; UNEP and partners 2009; UNEP 2008; UNFCCC 2007).

R&D Demonstration

Deployment

DiffusionCommercially competitive

Technology development

stages

Funding needs

Private investors

start

returnsearning

Public funding

Private funding

Figure 6: The role of public finance

Source: UNFCCC 2007

P a g e | 22

Public finance mechanisms

Four basic mechanisms are available to provide capital at different phases of a RE project. The so‐

called ‘valley of death’ will briefly be outlined in the next section (KfW 2009; UNEP 2008).

1. Debt: credit lines, concessional or ‘soft’ loans and guarantees;

2. Equity: Private equity and venture capital funds

3. Carbon: carbon finance e.g. carbon taxes, EU‐ETS auctioning revenues and the CDM;

4. Grants: official development assistance (ODA), climate finance and multilateral funds e.g.

provided by the Global Environmental Facility (GEF) or the World Bank;

The ‘Valley of death’

Well known to RE investors and developers is the so called ‘valley of death’ which is clearly one of

the project phases to be addressed by public finance mechanism (see figure above). Meant are

projects or technologies that get caught between venture capital (R&D) and project finance

(commercialization). Those projects happen to be too capital intensive for venture capital and too

risky for private equity. Both forms of financing are unwilling to take the high technology and scale

up risk. New small projects that lack any sort of track record face especially great difficulties

receiving start up finance to get their project of the ground ( BNEF 2010; Hamilton 2010).

Climate Finance

One of the few outcomes from last year’s climate negotiations in Copenhagen was the non‐binding

commitment by the EU and other industrialized countries to jointly mobilise $30 billion in‘ fast start

finance’ for the period 2010‐ 2012 and $100 billion a year by 2020 for adaptation and mitigation

action for the ‘most vulnerable developing countries’(UNFCCC 2009). In August 2010 pledges from

industrialized countries accounted to $27.8 billion (WRI 2010).

P a g e | 23

2.3 Carbon Finance ‐ the icing on the cake

The Clean Development Mechanism (CDM) promotes

emission reduction projects in developing countries by

generating certified emissions reduction credits (CERs)

which can be sold and traded in industrialized countries.

About 6281CDM projects have been registered, or are in

the project pipeline by 2012, of which about 60% are

renewables (UNFCCC 2010; UNEP Risoe Centre 2010).

The value of project‐based transactions totalled $2.7

billion in 2009– 59% less than in 2008 (UNEP 2010).

By far the biggest host country for CDM projects is China representing nearly a 40% share (910

projects) of total registered projects. Out of 2314 registered projects only 45 took place in Africa

(UNFCCC 2010).

The International Emissions Trading Association (IETA) summarized some of main issues that led to

the underrepresentation of CDM projects in less developed countries (IETA 2010):

• High operating and capital costs for projects in less developed countries and a lack of

expertise on the part of financial institutions and administrational entities; most materials

need to be imported (IETA 2010);

• High transaction costs especially for small‐scale projects in less developed countries; low

per capita emissions drive up the marginal costs of GHG abatement and the large share of

biomass and hydropower result in low grid emission factors leading to low baselines against

which the amount of CER for a project is measured. As a consequence especially small‐scale

RE projects in poorer countries are less attractive compared to China and India which have

high baselines due to their large share of fossil fuel generation(IETA 2010);

• Due to capacity bottlenecks and inefficiencies in the regulatory chain, e.g. at national

authorities (DNA’s) or the UNFCCC secretary itself, the CDM process is very time consuming,

expensive and makes it impossible to predict future revenues from the sale of credits(IETA

2010). Today it takes an average of 3 years until CERs are issued (WB 2009);

The Clean Development Mechanism (CDM)

The CDM allows emission‐reduction (or emission removal) projects in developing countries to earn certified emission reduction (CER) credits, each equivalent to one tonne of CO2. These CERs can be traded and sold, and used by industrialized countries (ANNEX‐ 1) to a meet a part of their emission reduction targets under the Kyoto Protocol.

Source: UNFCCC

P a g e | 24

• CERs are issued ex‐post therefore being insufficient to cover the often significant upfront

capital costs which adds to the generally high registration risk, issuance and (carbon) price

risk; as a result the CDM often fails to deliver bankable mainstream project finance (IETA

2010; Sterk 2007);

A reformed mechanism under a post‐Kyoto regime will need to focus on areas where it has attracted

little activity yet: geographical (i.e. Africa), sectoral (i.e. energy efficiency), and in particular in terms

of scale (i.e. smaller projects) (Robins et al. 2009).

P a g e | 25

2.4 Renewable Energy Policy – a finance perspective

In early 2010 more than 83 countries, 42 of them developing, had some type of policy to promote

renewable power generation (REN21 2010). However, the high number of new climate policies was

mostly due to submissions of non‐binding emissions reduction targets, action plans or letters of

commitment submitted under the Copenhagen Accord‐ the concluding non‐legal document of the

UN climate negotiations last December (DB 2010; REN21 2010).

A report conducted for the European Commission in 2006 concluded that besides characteristics

such as effectiveness and efficiency of policy a long‐term and stable policy environment has been

shown to be actually the key criterion for the success of developing renewable electricity markets’

(Held et al., Haas and Ragwitz 2006). UNEP puts it into a nutshell: policy has to be ‘loud (improve

bankability), long (duration reflecting investment horizons) and legal’ (clear, stable framework)

(UNEP SEFI 2004).

Chatham House finance roundtables with RE stakeholders also strongly highlighted the key role of

policy in reaching investment decisions. Countries providing clear policy frameworks and incentives

will draw attention from investors. In many cases the availability of capital has been less of a

problem than the absence of good conditions to ‘unlock’ capital for financiers on the ground

(Hamilton 2010). Today, however, renewable energy policy is predominantly located within the

framework of climate policy (‘climate driver’) and energy security concerns.

Renewable energy investors further highlight the timing for policy has to be right considering that

investment horizons range from 15 to 20 years (Hamilton 2010). In particular banks see stability and

longevity as priority for markets, to secure both repayment of debts and their returns. Policy makers

will have to satisfy investor needs offering, as the Deutsche Bank summarizes, Transparency,

Longevity, and Certainty (TLC) (DB 2009).

Transparency – How easy is it to navigate through the policy structure and understand and execute?

Longevity – Does the policy match the investment horizon and create a stable environment for public policy support?

Certainty – Does the policy deliver measurable revenues to support a reasonable rate of return?

P a g e | 26

2.4.1 NAMAs – Supporting RE in developing countries in post‐2012

National Appropriate Mitigation Actions (NAMAs) seek to accelerate developing country

participation in emissions reductions efforts from a voluntary, non‐market based‐ bottom‐ up

regime (Chung 2009).

Under a NAMA, a developing country

commits to voluntary non‐legally binding

emissions or RE targets (‘no‐loose’ targets)

which they then seek to achieve through

domestic actions. Those actions can either be

policy based (i.e. feed‐in tariffs) or sector

based (i.e. transport or energy)(UNEP Risoe 2009). They might be supported by multilateral climate

finance or in the long‐term be linked to the carbon market.

Even though NAMAs are used to address many open challenges in developing countries there is no

official definition for the concept. Issues such as activities covered, institutional structures, the

funding and crucial points such as the measuring, reporting and verification (MRV) of NAMA actions

remain unsolved (Ecofys 2010).

According to Ecofys, a consultancy, the types of actions proposed to the UNFCCC vary significantly.

They include data collection, strategy development, (pilot) ‐ projects, regulation, capacity and

institutional building, financial incentives and awareness raising campaigns (Ecofys 2010).

Of these larger groups Ecofys has categorized NAMAs into three groups (Ecofys 2010):

1. Unilateral NAMAs: mitigation actions undertaken by developing countries on their own;

2. Supported NAMAs: mitigation actions in developing countries, supported by direct climate finance from industrialised countries (Annex ‐1);

3. Credited NAMAs: mitigation actions in developing countries, which generate credits to be sold on the carbon market (e.g. from sectoral crediting) (Ecofys 2010); credits could be issued for emissions reductions below a no‐loose (sector) baseline (MLCE 2010);

Ecofys proposes that taking the potential financing available from a NAMA mechanism, national

support/incentive schemes such as feed‐in tariffs could be implemented to deploy and scale up

electricity in developing countries (Ecofys 2010).

The Bali Action Plan calls for “Nationally appropriate mitigation actions’ by developing country Parties in the context of sustainable development, supported and enabled by technology, financing and capacity building, in a measurable, reportable and verifiable manner.“

Source: UNFCCC, Bali Action Plan Paragraph 1 (b) (ii), 2007

P a g e | 27

2.5 Feed‐in tariff schemes for developing countries

Generally two support schemes are used to encourage new renewable energy generation and

capacity installation (I) quantity market‐based mechanisms such as tendering, green certificates and

quota obligations and (ii) price based instruments such as fiscal incentives and feed‐in tariffs

(premiums) (EC 2008). The Stern review summarizes recent global observations:

Feed‐ in tariff (FIT) schemes offers a fixed price for purchase of renewable power. Renewable energy

(RE) producers usually receive a premium rate over the retail price per kilowatt‐hour (kWh) fed into

the grid. The costs are equally distributed among electricity consumers. In early 2010 at least 50

countries and 25 states and provinces had adopted feed‐in tariff schemes worldwide. The majority

of the schemes have been implemented within the last five years (REN21 2010).

Today feed‐in tariff (FIT) schemes are considered to be most effective in stimulating the rapid

deployment of renewable energy and providing long‐term financial stability for investors in

renewable energy (Mendonca et al. 2010; EC 2008; Klessmann et al. 2008; IEA 2008; Mitchell et al.

2006).

2.5.1 Core principles

Well‐designed FIT polices include five core principles which will be key to their success (Mendonca et

al. 2010, WFC 2010, DB 2009, Klessmann et al. 2008):

• Eligible technologies: the types of RE technologies and size of plants must be suitable for a

given region;

• Specified tariff by technology: Technology specific rates lead to precise tariff pricing for the

wide range of renewable energy technologies;

• Guaranteed Payments: FITs provide guaranteed payment rates that need to be based on the

cost of generation plus a reasonable profit;

A comparison between deployment support through tradable quotas and feed‐in tariff price support

suggest that feed‐in mechanisms achieve larger deployment at lower costs

Source: Stern Review 2007 (Stern 2007, 266)

P a g e | 28

• Interconnection: Policies should provide a mandate for grid operators to grant RE priority

grid access;

• Payment term: Long term contracts should provide a revenue stream to match the project

life (usually 15‐20 years) with pre‐determined prices increase investor certainty;

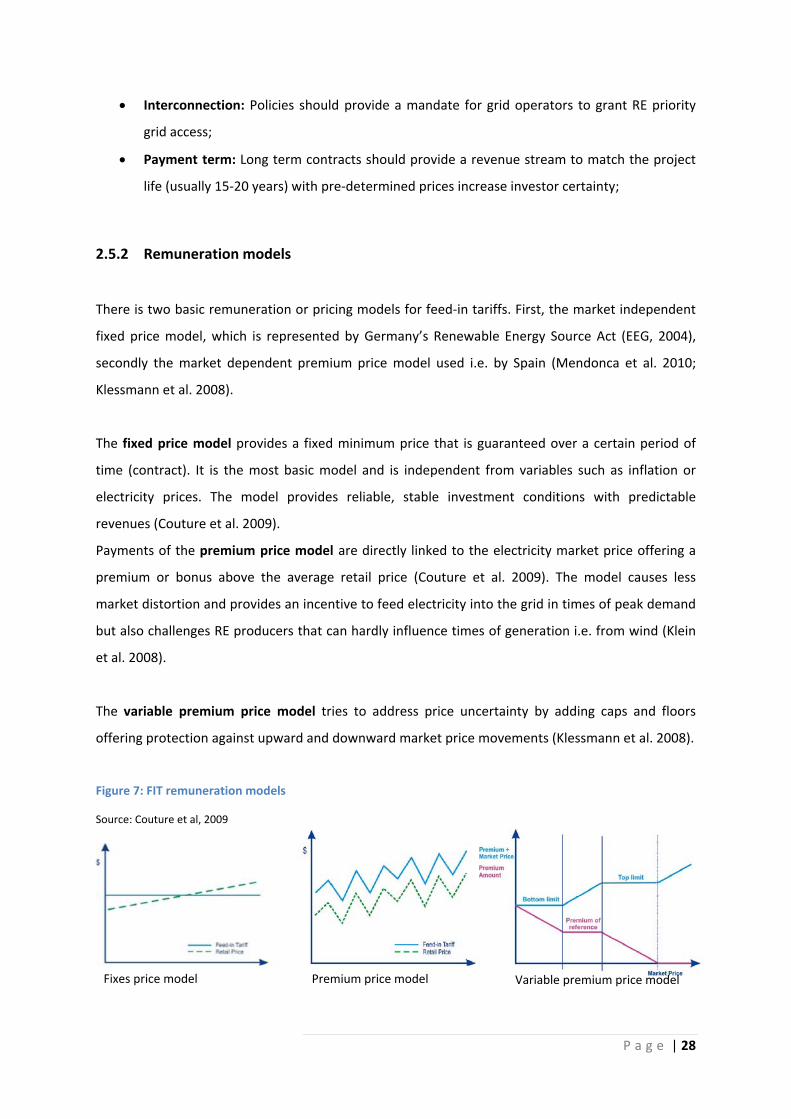

2.5.2 Remuneration models

There is two basic remuneration or pricing models for feed‐in tariffs. First, the market independent

fixed price model, which is represented by Germany’s Renewable Energy Source Act (EEG, 2004),

secondly the market dependent premium price model used i.e. by Spain (Mendonca et al. 2010;

Klessmann et al. 2008).

The fixed price model provides a fixed minimum price that is guaranteed over a certain period of

time (contract). It is the most basic model and is independent from variables such as inflation or

electricity prices. The model provides reliable, stable investment conditions with predictable

revenues (Couture et al. 2009).

Payments of the premium price model are directly linked to the electricity market price offering a

premium or bonus above the average retail price (Couture et al. 2009). The model causes less

market distortion and provides an incentive to feed electricity into the grid in times of peak demand

but also challenges RE producers that can hardly influence times of generation i.e. from wind (Klein

et al. 2008).

The variable premium price model tries to address price uncertainty by adding caps and floors

offering protection against upward and downward market price movements (Klessmann et al. 2008).

Figure 7: FIT remuneration models

Source: Couture et al, 2009

Fixes price model

Premium price model

Variable premium price model

P a g e | 29

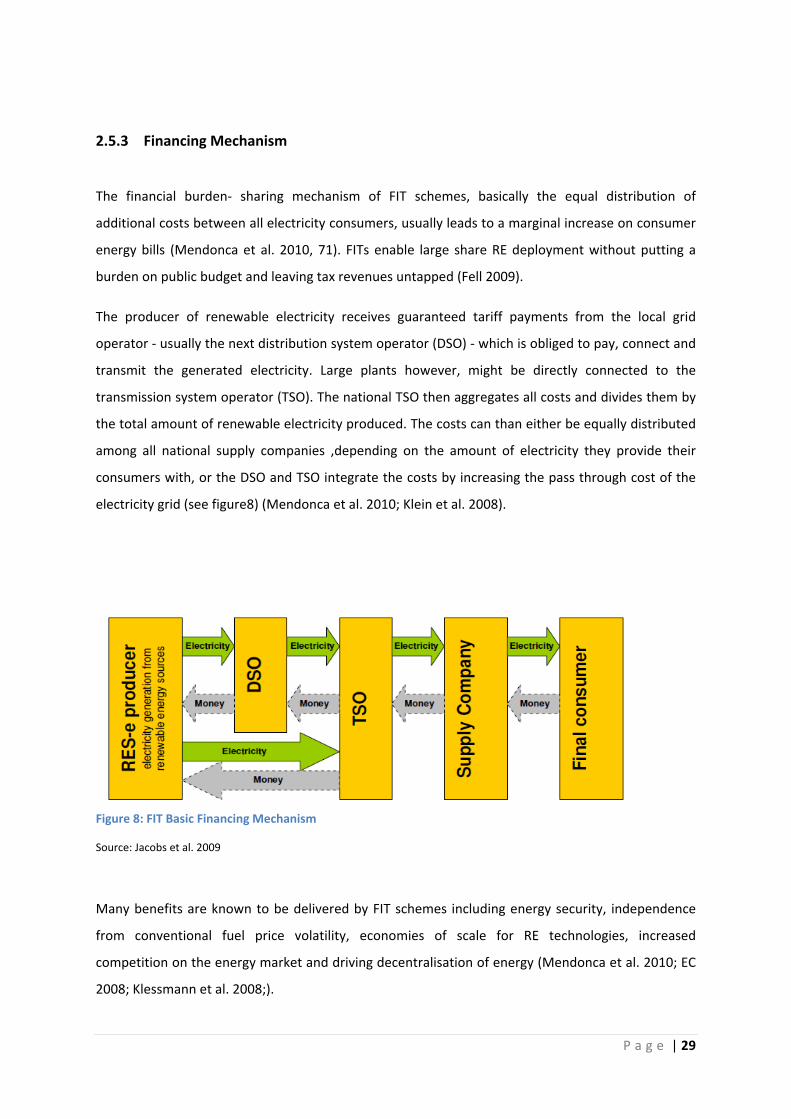

2.5.3 Financing Mechanism

The financial burden‐ sharing mechanism of FIT schemes, basically the equal distribution of

additional costs between all electricity consumers, usually leads to a marginal increase on consumer

energy bills (Mendonca et al. 2010, 71). FITs enable large share RE deployment without putting a

burden on public budget and leaving tax revenues untapped (Fell 2009).

The producer of renewable electricity receives guaranteed tariff payments from the local grid

operator ‐ usually the next distribution system operator (DSO) ‐ which is obliged to pay, connect and

transmit the generated electricity. Large plants however, might be directly connected to the

transmission system operator (TSO). The national TSO then aggregates all costs and divides them by

the total amount of renewable electricity produced. The costs can than either be equally distributed

among all national supply companies ,depending on the amount of electricity they provide their

consumers with, or the DSO and TSO integrate the costs by increasing the pass through cost of the

electricity grid (see figure8) (Mendonca et al. 2010; Klein et al. 2008).

Many benefits are known to be delivered by FIT schemes including energy security, independence

from conventional fuel price volatility, economies of scale for RE technologies, increased

competition on the energy market and driving decentralisation of energy (Mendonca et al. 2010; EC

2008; Klessmann et al. 2008;).

Figure 8: FIT Basic Financing Mechanism

Source: Jacobs et al. 2009

P a g e | 30

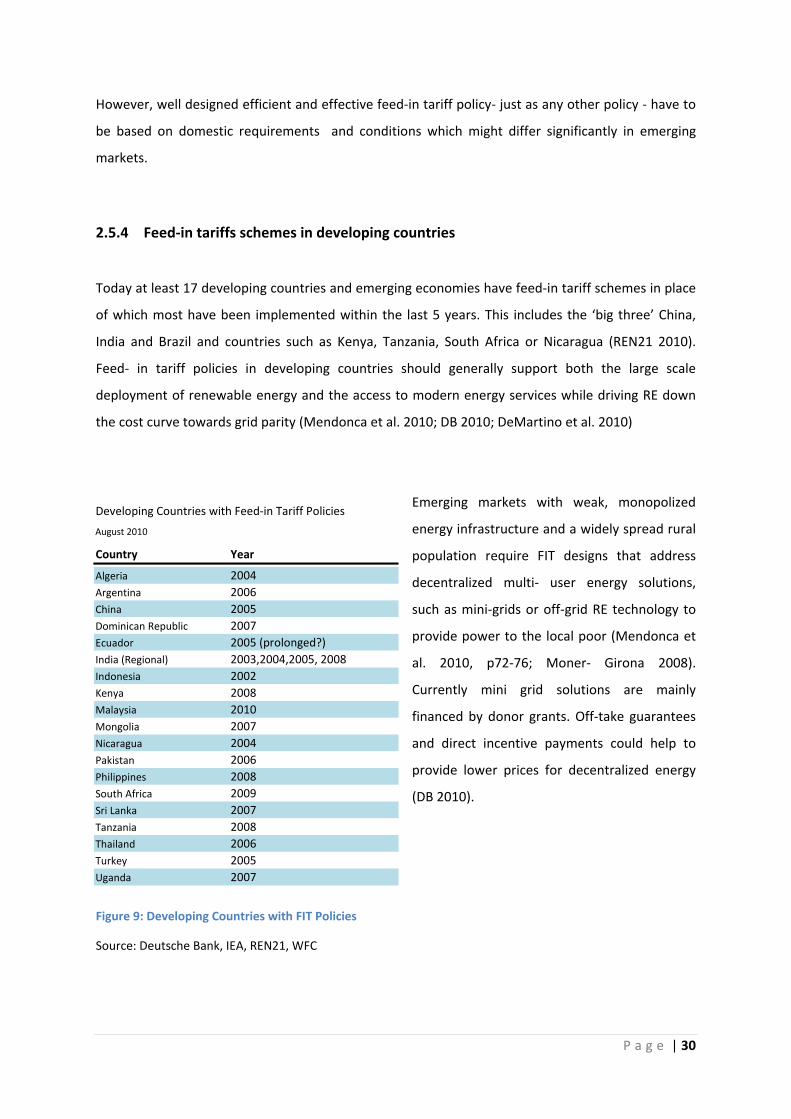

Developing Countries with Feed‐in Tariff Policies

August 2010

Country Year

Algeria 2004Argentina 2006China 2005Dominican Republic 2007Ecuador 2005 (prolonged?)India (Regional) 2003,2004,2005, 2008Indonesia 2002Kenya 2008Malaysia 2010Mongolia 2007Nicaragua 2004Pakistan 2006Philippines 2008South Africa 2009Sri Lanka 2007Tanzania 2008Thailand 2006Turkey 2005Uganda 2007

However, well designed efficient and effective feed‐in tariff policy‐ just as any other policy ‐ have to

be based on domestic requirements and conditions which might differ significantly in emerging

markets.

2.5.4 Feed‐in tariffs schemes in developing countries

Today at least 17 developing countries and emerging economies have feed‐in tariff schemes in place

of which most have been implemented within the last 5 years. This includes the ‘big three’ China,

India and Brazil and countries such as Kenya, Tanzania, South Africa or Nicaragua (REN21 2010).

Feed‐ in tariff policies in developing countries should generally support both the large scale

deployment of renewable energy and the access to modern energy services while driving RE down

the cost curve towards grid parity (Mendonca et al. 2010; DB 2010; DeMartino et al. 2010)

Emerging markets with weak, monopolized

energy infrastructure and a widely spread rural

population require FIT designs that address

decentralized multi‐ user energy solutions,

such as mini‐grids or off‐grid RE technology to

provide power to the local poor (Mendonca et

al. 2010, p72‐76; Moner‐ Girona 2008).

Currently mini grid solutions are mainly

financed by donor grants. Off‐take guarantees

and direct incentive payments could help to

provide lower prices for decentralized energy

(DB 2010).

Figure 9: Developing Countries with FIT Policies

Source: Deutsche Bank, IEA, REN21, WFC

P a g e | 31

Reliable, stable and long‐ term frameworks that provide RE investors returns matching the project

life will determine the success of FIT schemes. However, consumers and countries in poorer regions

often lack financial strength and capacity to provide long‐ term funding for FIT payments (DB 2010).

A feed‐in tariff fund

Within the last 12 months the concept of financing feed‐in tariffs in developing countries through a

national or global fund have been widely discussed and proposed. A ‘FIT Fund’ combined with risk

mitigation instruments and capacity building efforts, to be financed from sources such as

international sponsors, a CDM tax, emissions auctioning or climate finance could help to overcome

barriers such as the lack of financial and infrastructural capacity (DeMartino et al. 2010;

Greenpeace/EREC 2009; WFC 2009; WWEA 2009).

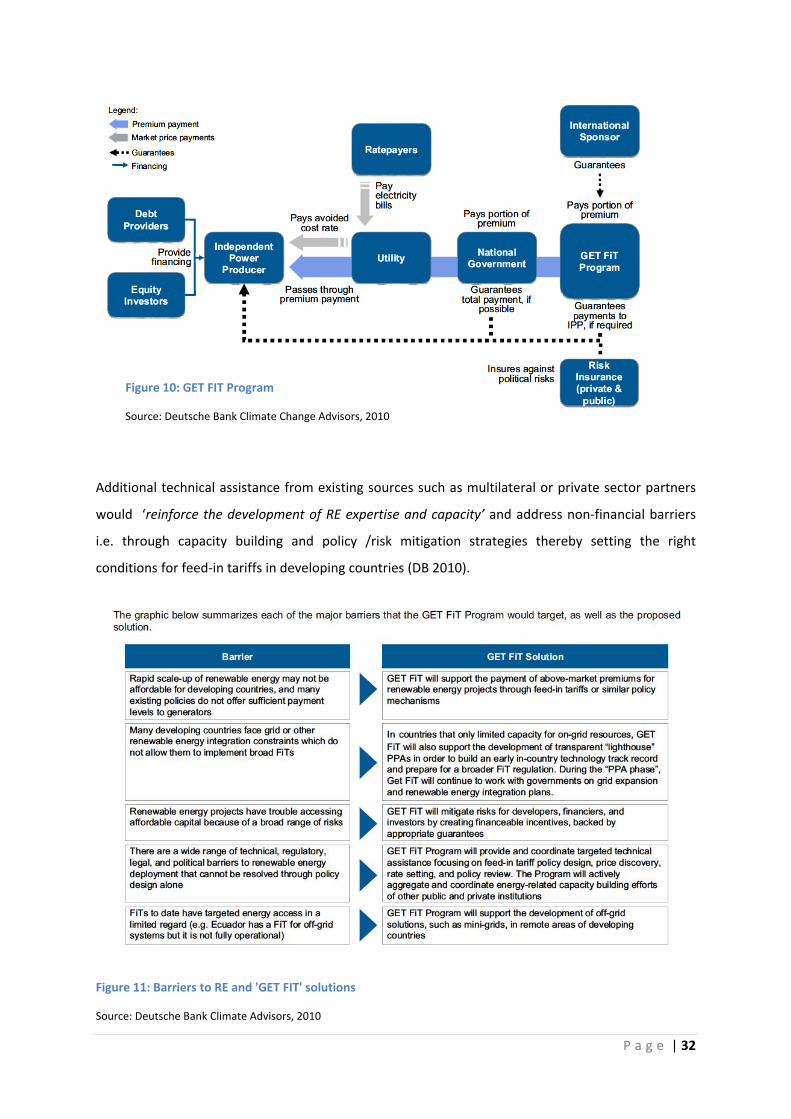

The GET FIT Programme (Global Energy Transfer Feed‐in Tariff for Developing Countries) by

Deutsche Bank Climate Change Advisors combines the existing proposals and provides an example

for a FIT programme possibly as National Appropriate Mitigation Action (NAMA). Utilities will at least

pay the market rate of electricity (or avoided cost rate) to independent power producers (IPPs). A FIT

premium for IPPs will ideally be paid by both the national government and the GET FIT fund.

International (AAA‐rated) sponsors such as (ideally) national governments, development banks, and

climate finance funds will provide funding and guarantees for the long‐ term premium payments of

the GET FIT Fund. Risk mitigation entities (e.g. MIGA, OPIC, private sector providers) will cover

political and sovereign risks. Currency risk will be avoided by premium payments in a hard currency

(DB 2010).

P a g e | 32

Additional technical assistance from existing sources such as multilateral or private sector partners

would ‘reinforce the development of RE expertise and capacity’ and address non‐financial barriers

i.e. through capacity building and policy /risk mitigation strategies thereby setting the right

conditions for feed‐in tariffs in developing countries (DB 2010).

Figure 11: Barriers to RE and 'GET FIT' solutions

Source: Deutsche Bank Climate Advisors, 2010

Figure 10: GET FIT Program

Source: Deutsche Bank Climate Change Advisors, 2010

P a g e | 33

Deutsche Bank estimates that a $3 billion commitment under the GET FIT fund could facilitate over

1GW of new on‐grid and off‐grid RE capacity attracting project finance capital of around $4 billion

(DB 2010).

However, though the proposal does not address capitalization strategies and governance structure it

provides very interesting overall approach which includes all main issues for FITs in developing

countries

The concept of a global fund to support feed‐in tariff programmes has already found its way into the

footnotes of the climate negotiations in the context of NAMAs (UNFCCC 2009):

An example of how important the reliable and sustainable long term financing for FIT schemes is,

shows a current case from Europe: Facing massive deficits from the financial downturn, Spain needs

to keep a lid on electric costs. The response by the Spanish government shocked RE investors and

developers: Over the next years tariffs for new PV installations might be cut by up to 45%. Even

greater concerns, however, caused the announcement to cut down premium tariff payments up to

15% for operating installations by (Bloomberg 2010).

‘A global fund shall be established to support a global feed‐in tariff program, providing guaranteed purchase prices, over and above the retail energy price in developing countries, of energy from renewable

sources […]’ Source: UNFCCC: 3. Report of the AWG‐LCA on its Seventh Session, Annex VI, Barcelona 2009

P a g e | 34

2.5.5 CDM vs. Feed‐in tariffs An ongoing, unsolved and complex controversy, which is often referred to as E+/E‐ issue, was

triggered in December 2009 when the UNFCCC’s CDM Executive Board (EB 51 meeting) shocked the

carbon market by rejecting 10 Chinese wind projects failing to prove ‘additionality’ in combination

with power tariffs for wind which, as the EB claims, had been lowered to be eligible with the CDM

(WB 2009).

Ensuring that carbon offset payments result in ‘real’ emissions reductions that would ‘not have

happened anyway’ without CDM revenues (Business as usual ‐ BAU) projects have to prove their

(financial) ‘additionality’ to the CDM EB (He et al. 2010).

However, the EB 51 decision is contrary to a ruling in 2001: Seeking to avoid potential perverse

incentives to meet CDM criteria in host countries (IETA 2009) to implement policies that ‘give

positive comparative advantages to less emissions‐intensive technologies (E‐) over more emissions‐

intensive technologies (E+)’ the EB (16th meeting) clarified that ‘E‐‘ policies are not to be considered

either the baseline scenario or the additionality of projects after November 2001 (UNFCCC 2001).

Lex de Jonge, former chair of the CDM EB warned that ‘this very important issue could have quite an

impact on the credibility of the whole CDM” (Carbon, Point 2009). The controversy further adds

significant uncertainty to the world’s largest CDM market. China, once considered to be the safest

CDM bet ‐ might have become the riskiest’ (He et al. 2010). There are implications for other host

countries as a World Bank analyst concludes, saying that renewable energy CDM projects in

developing countries with existing or new renewable feed‐in tariff schemes will run a higher

regulatory risk than countries without incentive schemes (WB 2009). During the UN climate

negotiations in Bonn in August 2010 the EB had refused to clarify this issue (Carnahan 2010).

P a g e | 35

2.6 Research

Financial Investment in renewable energy and the Clean Development Mechanism have bypassed

poorer countries in regions such as Latin America and Africa (IETA 2010; UNEP 2010).

Feed‐in tariffs (FITs) are known as an efficient and effective tool to scale up renewable energy

generation and have been implemented in numerous developing countries in the last five years

(REN21 2010; Mendonca et al. 2010). However, due to their recent implementation, little

information is available as to how FITs are perceived by stakeholders of renewable energy projects,

and what their actual impact on renewable energy investment is.

One of the biggest challenges facing FIT schemes in developing countries is securing long term

funding to support the program. The concept of a feed‐in tariff fund co‐ financed by donor money is

briefly outlined in various papers published within the last year and has been discussed in detail in

the GET FIT paper by Deutsche Bank (DB 2010; DeMartino et al. 2010; Greenpeace/EREC 2009; WFC

2009; WWEA 2009) The capitalization and governance of the GET FIT program is only covered

briefly.

National Appropriate Mitigation Actions (NAMAs) might be a way to address the funding issue of

FITs in developing countries channelling existing and new multilateral donor money into FIT schemes

in general and a potential GET FIT or Global FIT Fund in particular (DB 2010; UNFCCC 2010b). Even

though the concept of NAMAs in the context of a post 2012‐ climate change regime has been under

discussion for several years (Ecofys 2010; UNEP Risoe 2009), the option to finance FITs or through

NAMAs has not yet been further considered by policy experts.

This study seeks to complement the discussion about FITs schemes in developing countries and the

funding of those schemes. This will be achieved by compiling the perceptions and opinions of major

senior stakeholders such as developers and financiers with a strong link to RE projects. Information

gained through this study on perceptions and issues with current FIT schemes in developing

countries and the potential role of NAMAs to fund them will provide a solid basis for structuring

further research.

P a g e | 36

1. What is the present role of FIT schemes in developing countries?

2. What is the potential future role of FIT schemes in developing countries?

3. Are NAMAs the best way to support FITs in developing counties in a post‐Kyoto framework?

4. How do renewable energy stakeholders perceive developments for renewable energy projects within the next 2‐5 years?

2.7 Research Questions

The research questions posed to major stakeholders are listed below.

P a g e | 37

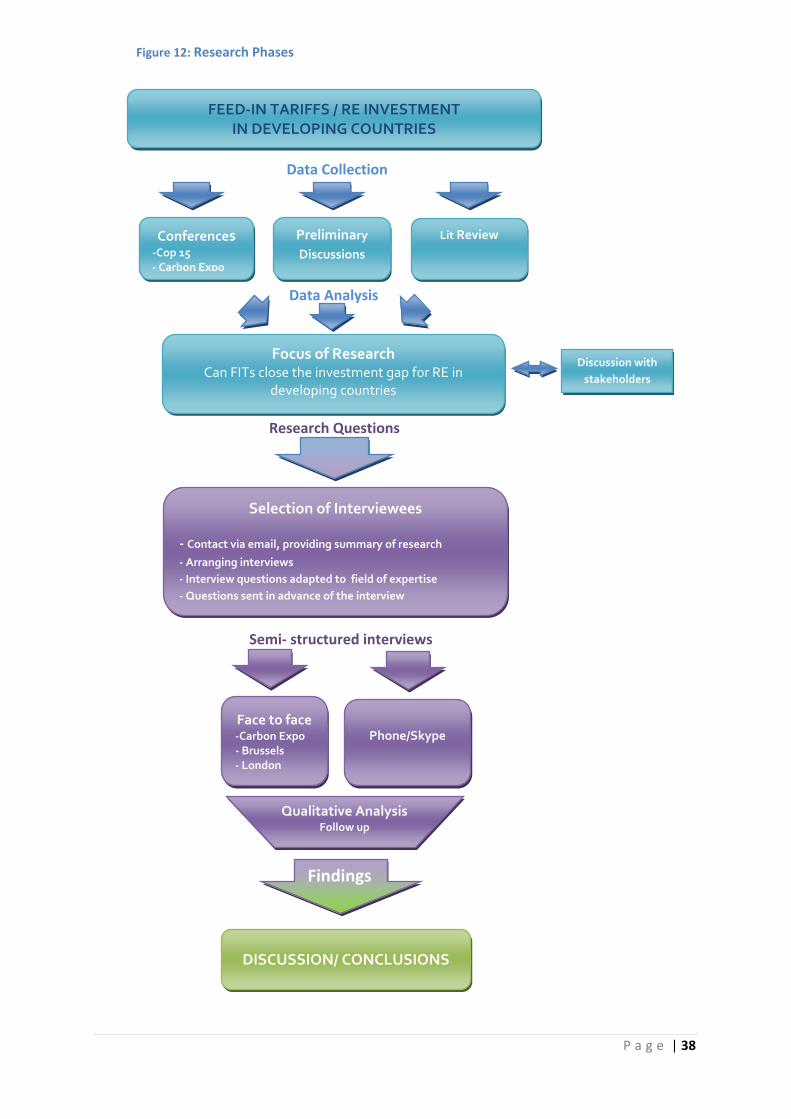

3 METHODOLOGY

The study utilizes data triangulation in order to gain a combination of research perspectives on the

topic (Flick 1992; Denzin 1989). Information was employed from multiple data sources such as pre‐

elementary discussions, reports, interviews and conferences namely the UN climate negotiations in

Copenhagen in 2009, Falmouth Energy Week and the Carbon Expo in May 2010. A qualitative

approach enabled the collection of evidence‐based information. Semi‐structured interviews

addressing open ended questions encouraged in–depth discussions from which additional issues and

perspectives on the topic evolved (Blaxter et al.; Flick 1998).

3.1 Research approach

The objective of the study is to gain first hand information from senior RE finance stakeholders in

order to draw an evidence‐based picture of experiences and perceptions in terms of current and

potential developments for renewable energy finance in developing countries. A special focus is on

feed‐in tariff schemes as one of the most promising mechanisms to scale up renewable energy in

developing countries (Mendonca et al. 2010; DB 2010). However, most FIT schemes in developing

countries have been implemented recently or are in the process of being implemented (REN21

2010).

High country risk, poor institutional and network infrastructure (Hamilton 2010) as well as the lack of

a post‐Kyoto agreement (including a reformed Clean Development Mechanism) make fairly difficult

ground for investment in developing countries (IETA, 2010). Geographically, this research takes a

rather breadth than country specific approach focusing on the world’s poorest regions Latin America

and Africa that are most concerned by a lack in RE investment.

P a g e | 38

FEED‐IN TARIFFS / RE INVESTMENT IN DEVELOPING COUNTRIES

Conferences ‐Cop 15 ‐ Carbon Expo

Preliminary Discussions

Lit Review

Focus of Research Can FITs close the investment gap for RE in

developing countries

Discussion with stakeholders

Selection of Interviewees

‐ Contact via email, providing summary of research

‐ Arranging interviews ‐ Interview questions adapted to field of expertise ‐ Questions sent in advance of the interview

Research Questions

Semi‐ structured interviews

Face to face ‐Carbon Expo ‐ Brussels ‐ London

Phone/Skype

Data Collection

Data Analysis

DISCUSSION/ CONCLUSIONS

Qualitative Analysis Follow up

Findings

Figure 12: Research Phases

P a g e | 39

3.2 Literature review

Secondary data has been employed for the literature review providing basic background knowledge

about issues relevant to renewable energy finance and feed‐in tariffs in developing countries. Due to

the rapid developments and continuously changing policy frameworks for RE in developing

countries, as well as uncertainty caused by the absence of a post‐Kyoto framework, the study

focused on evidence based and practice‐ oriented literature. Secondary data sources were studies,

publications and presentations obtained from renowned organisations and institutions such as

Chatham House, the UN and Deutsche Bank Climate Change Advisors. Information about RE finance

and FITs in developing countries was mainly employed from two studies:

• ‘Scaling up Renewable Energy in Developing Countries: Finance and investment perspectives’,

a report from finance roundtables with RE financiers by Kirsty Hamilton, published by

Chatham House in April 2010 (Hamilton 2010) and

• The GET FIT Programme, a whitepaper by Deutsche Bank Climate Change Advisors, covering

issues around FIT schemes in developing countries and ‐ based on earlier proposals ‐

outlining a potential architecture of a ‘FIT – Fund’ programme for developing countries; The

paper, which includes input from various RE finance and FIT experts was published in April

2010;

3.3 Conferences and Preliminary Discussions

Various discussion and information collected from conferences contributed to developing the

research project and led to further contacts with stakeholders. Discussions were carried out at the

UN Climate Negotiations (COP15) and IETA side events in Copenhagen in December 2009 (WFC,

WWEA), at the Falmouth Energy Week (Chatham House) and finally at the Carbon Expo in Cologne in

May 2010. Additional discussions e.g. with Miguel Mendonca, a renowned expert for feed‐in tariffs,

took place over the phone.

P a g e | 40

3.4 Interviews

The following chapter will provide information about the selection of interviewees, how interviews

were carried out, the design of questions and finally the analysis of interviews.

3.4.1 Selection of interviewees

In order to gain best possible insights and perspectives on the topic senior staff from the following

relevant professional backgrounds was selected: policy making, project development, ‐ finance and

consultancy, RE market and finance analysis and associations. Interviewees hold positions in the

private sector, international organisations such as the European Commission and United Nations, in

Non‐Governmental Organisations and associations such as the International Hydropower

Association (IHA) and the International Emissions Trading Association (IETA). Most participants have

a strong link to the carbon market particularly to CDM projects therefore having gained long‐ term

experience and expertise in terms of RE project development and finance in developing countries.

About 25 potential interviewees have been contacted by email which had detailed information

about the research project in attachment. Some contacts appeared to be specialised in fields not

relevant to the study, others were simply not available for interviews due to work commitments or

holidays. After all 19 interviews have been carried out, including 25 participants (see table below).

3.4.1.1 Interviews

Out of 19 semi‐structured interviews carried out in English and German, eight were conducted face‐

to‐face taking place at the Carbon Expo in Cologne, the European Commission in Brussels and in

London. The remaining interviews were carried out over the phone but mainly over Skype, a free

Voice over IP software, which provided a good solution since Interviewees were based around the

globe. In order to leave the interviewee enough time for preparation and to eventually invite further

colleagues to the session, questions were provided by email prior to the session. This resulted in

more in‐depth discussions. The duration of the interviews and discussions ranged from 25 to 120

minutes. Most interviews were recorded and additional notes were taken throughout the sessions.

Follow up emails –to exchange information and contacts – have been sent subsequently to the

session. Further consultation about topic specific issues took place alongside the writing process.

P a g e | 41

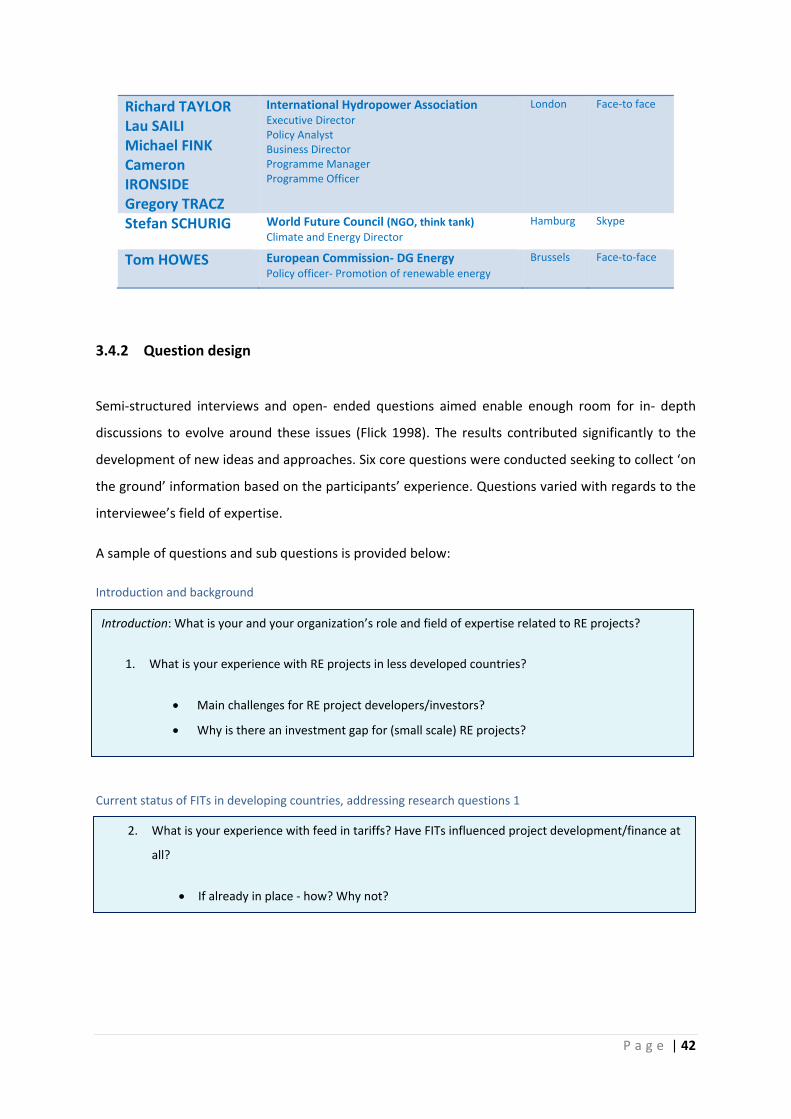

The table below provides a brief overview of the interviews and discussions that have been carried out:

Interviewee Organization and function Based Interview

Andrew PRAG CAMCO GLOBAL (project developer)Principal Consultant, Climate Change Policy and Strategy, chair Project Developers Forum

London Face‐to‐face

Astrid, LADEFOGED

European Commission‐ DG ClimatePolicy Officer ‐ International relations, GEEREF

Brussels Phone

David JACOBS Environmental Policy Research CentreFeed‐in tariff expert, PhD feed‐ in tariffs, book author (Powering the Green Economy)

Berlin Skype

Dr Jörg Henninger Private Hydropower Project Developer, Ecuador Nurnberg Skype

Edwin AALDERS IDEA Carbon (Consultancy, rating)Partner Business Development & Operations former director IETA

London Face‐to‐face

Guy TURNER Marisa BECK

Bloomberg New Energy FinanceDirector Carbon Markets Carbon Market Analyst

London Face‐to‐face

John FAY African Carbon Credit ExchangeTechnical Adviser, PhD feed‐in tariffs

South Africa

Skype

Jonathan CURREN CAMCO GLOBAL Managing Director South Africa

South Africa

Skype

Jorge O BARRIGH SenGen S.A. (Env. Finance Advisory)Senior Managing Partner Former Manager, Latin America NATSOURCE LLC

Panama Skype

Jorund BUEN Point CarbonSenior Adviser/Co‐Founder

Oslo Skype

Kai Remco FISCHER

UNEP Financial InitiativeProgramme Manager Climate change

Geneva Skype

Kim CARNAHAN International Emissions Trading Association (IETA) Policy Leader, Flexible Mechanisms, CDM

Washington D.C.

Skype

Martin BERGER Merrill Lynch Commodities EuropeVice President ‐ Carbon Markets Origination

London Face‐to‐face

Martina JUNG Ecofys International (consultancy)Senior Consultant Energy & Climate Strategies

Cologne Face‐to‐face

Micha CLASSEN Sudhir BHAT

First Climate (project investor/developer)Senior Project Manager Director Project Finance

Zurich Face‐to‐face Carbon Expo

Reiner HAKALA European Commission‐ DG Development

Energy Policy Adviser, RECP

Brussels Phone

P a g e | 42

Introduction: What is your and your organization’s role and field of expertise related to RE projects?

1. What is your experience with RE projects in less developed countries?

• Main challenges for RE project developers/investors?

• Why is there an investment gap for (small scale) RE projects?

2. What is your experience with feed in tariffs? Have FITs influenced project development/finance at

all?

• If already in place ‐ how? Why not?

Richard TAYLOR Lau SAILI Michael FINK Cameron IRONSIDE Gregory TRACZ

International Hydropower AssociationExecutive Director Policy Analyst Business Director Programme Manager Programme Officer

London Face‐to face

Stefan SCHURIG World Future Council (NGO, think tank)Climate and Energy Director

Hamburg Skype

Tom HOWES European Commission‐ DG EnergyPolicy officer‐ Promotion of renewable energy

Brussels Face‐to‐face

3.4.2 Question design

Semi‐structured interviews and open‐ ended questions aimed enable enough room for in‐ depth

discussions to evolve around these issues (Flick 1998). The results contributed significantly to the

development of new ideas and approaches. Six core questions were conducted seeking to collect ‘on

the ground’ information based on the participants’ experience. Questions varied with regards to the

interviewee’s field of expertise.

A sample of questions and sub questions is provided below:

Introduction and background

Current status of FITs in developing countries, addressing research questions 1

P a g e | 43

3. What is the potential future role of feed‐ in tariffs and national policy to scale up investment in

renewable energy?

• What will be the main challenges?

4. Will NAMAs be able to provide a link between FITs/national policy and finance from the private

sector/carbon finance?

• Where do you see the main challenges for a NAMA?

• What alternatives are there to mobilize private sector money for national?

5. Your ‘crystal ball’: Which developments regarding the deployment of RE do you expect to happen

over the next 2‐ 5 years?

• What will be the future role of carbon finance and climate finance?

The future role of FITs, addressing research questions 2

Funding FITs, linking national policy and private sector money (in post‐2012), addressing research question 3

Outlook on developments of RE investment from the interviewee’s personal stand point (rather than how it

should be), addressing research question 4

3.4.3 Interview Analysis

Primary data gained from interview recordings was entered into an Excel table. Names of

interviewees were coded for confidentiality (transcriptions are therefore not attached). The content

of the interviews was analysed and clustered according to responses that:

a) directly addressed the research questions; and

b) provided additional commentary on ‘sub‐issues’ and information that was of value to the

discussion;

Key statements and information was then extracted and sorted according to relevance and topic.

Finally, experiences from stakeholders and key findings were linked to available literature. Trends

were identified, and potential opportunities for renewable energy finance and feed‐in tariffs in

developing countries were compared and analysed.

P a g e | 44

4 IN PERSPECTIVE: Renewable Energy Finance and Feed‐ in Tariffs in developing countries

The following Chapter summarizes the information collected from interviews with senior renewable

energy finance experts and project developers.

4.1 The start‐up finance gap

The interest in renewable energy (RE) projects in Africa is, as a developer notes, ‘ridiculous’ and

firms such as Standard Bank, the African Development Bank and many more are ‘standing in line’

looking for investment opportunities in renewable energy projects in the South Africa’ (CSZ, 18). An

interviewee from Latin America draws a similar picture (CSZW, 15) referring to funds that have

investment volumes of at least $100 million often targeting small scale RE projects in the range of $

1‐ 20 million (CSZW, 14) .

However, project finance in both regions generally faces the same problem: the lack of start‐ up

investment for early stage projects. Investors look for advanced projects ‘further down the line’

which have done their feasibility study, calculation of IRR (internal return of investment),

environmental assessment (EIA) and most important ‐ that have their power purchase agreement

(PPA) in place. These projects have reached a stage at which they can be presented to potential

investors (CSZ, 18; CSZW, 15). A financier emphasises the great interest in the regions, with the

investment community even willing to get involved at medium level returns but at this point it

comes down to high risk equity investment and chances to lose investment at once, i.e. in countries

like Kenya or Uganda, are just too high (CSR, 7; CSZ, 18).

At present countries such as South Africa seek therefore to attract the ‘big guys’, companies and

firms that have the capacity to finance projects internally, ‘on their balance sheets’ (CSZ, 22).

P a g e | 45

4.2 Challenging RE Policy – a developer’s perspective

Participants of projects brought up two basic concerns typically linked to projects which are briefly

be outlined below.

4.2.1 Domestic needs

The success of projects is directly linked to national, regional or local needs which have to be well

understood. First of all, explains a developer, forget ‘about the environmental perspective’! Most less

developed countries aim for – health, education, poverty reduction and economic development and

RE projects can only work if they can support that – if not they will take the second place’ (CSZ, 2).

Another interviewee adds that RE in developing countries has been mostly driven by the lack of

security of supply and high fuel prices, which makes RE generation as an alternative more attractive

(CSA, 11).

Three main requirements in terms of energy are described by a consultant (CSZ, 2):

• Quality of resource supply (large high tech plants need good supply)

• Constancy and consistency of supply and services

• Upgrading of transmission and distribution infrastructure (basis for good power quality)

A hydropower expert further highlights the importance to actually deliver quality of supply

emphasizing that storage of water and civil services have to be incentivized e.g. within a feed‐in

tariff framework (CSA, 1b). Especially benefits from hydropower plants including storage could fill

supply gaps; this is important to be understood by policy makers, adds a colleague (CSA, 3). Water

storage in connection with hydroelectric generation might in fact be able to address current issues

like those in Uganda, which overwhelmingly depends on hydropower: Five years ago rain and

therefore power supply used to be very predictable. Today, in contrast, rain patterns have changed

severely and hydropower has become very intermittent and unreliable – a problem that has

occurred in many developing countries with high shares of hydropower generation (CSZ, 3).

P a g e | 46

‘People in Latin America are among the most optimistic people on the planet. They love happy

endings and believe things will always be better tomorrow. Therefore you will find the

willingness to plan ahead boldly but following through is the problem’

Interview CSWZ, 24

4.2.2 National leadership and coordination

Issues occurring from lack of institutional capacity and knowledge, missing willingness to follow up

policy and to coordinate activity on part of regulatory bodies and of law makers are omni‐present

and have been mentioned by project stakeholders in Africa, Asia and Latin America (CSE, 5).

A senior analyst believes the weak institutional framework to be one of the major problems in less

developed countries, which will always have to be faced by projects. ‘Why would a developer trust in

local institutions and long‐ term policy such as feed‐in tariffs’, he asks (CSZE, 4). Generally very short‐

term horizons of governments make academic solutions difficult and after all they might never be

implemented (CSWZ, 3).

Governments, especially in Latin America, tend to be very centralized and typically hold a lot of

power. Thus the success of a project might be directly linked to the interest of a ruling entity. A

project needs to be well in line with its own objectives and with those from the ‘guys holding the

power’ such as the environmental agencies or ministries, explains a consultant. Current examples

are Ecuador, where ‐ in spite of massive power shortages ‐ the socialistic president has created

hostile conditions for private RE investors (see example 4.3.3 below) or a country in Central America

where 250MW of RE where successfully auctioned but the types of concessions strongly reflected

personalities of people in power at that point (CSN, 2; CSWZ, 1)

In terms of developing a project in these conditions one finds that there tends to be more than

one gate available at any time, but usually only a restricted number of gate keepers or key holders

Interview CSWZ, 11

P a g e | 47

However, all stakeholders underline the importance of effective and efficient national policy. In