cameroon economic update - world bank economic update iii table of contents abbreviations and...

TRANSCRIPT

January 2014 | Issue No 7

CAMEROON ECONOMIC UPDATEREVISITING THE SOURCES OF GROWTH

THE QUALITY OF BASIC EDUCATION

CAMEROON ECONOMIC UPDATE

Revisiting the Sources of GrowthThe Quality of Basic Education

January 2014

CAMEROON ECONOMIC UPDATE iii

TABLE OF CONTENTS

ABBREVIATIONS AND ACRONYMS ......................................................................................... V

ACKNOWLEDGEMENT ............................................................................................................ VII

EXECUTIVE SUMMARY .............................................................................................................. 1

RECENT ECONOMIC DEVELOPMENTS ....................................................................................32013 has seen some encouraging economic developments… ............................................................. 3…although the fiscal and external balances have deteriorated. ........................................................... 5Medium term prospects are positive… .................................................................................................. 6…but substantial risks remain ................................................................................................................ 7Looking forward, the sources of growth need to be revisited ............................................................... 9

BASIC EDUCATION IN CAMEROON .........................................................................................11Cameroon has made significant progress in access to basic education… ......................................... 11…but important disparities persist… .................................................................................................... 13…because of resource allocation and governance problems ............................................................. 15Looking forward, tackling these issues would strengthen the basic education system. ..................20

REFERENCES ............................................................................................................................23

CAMEROON ECONOMIC UPDATE v

ABBREVIATIONS AND ACRONYMS

CFAF CFAFranc

CONFEMEN Conférence des ministres de l’Éducation des États et gouvernements de la Francophonie

(ConferenceoftheMinistersofEducationofFrenchspeakingcountries)

CPI ConsumerPriceIndex

CTP ContractTeachersProgram

DENOs Dépenses engagées mais non-ordonnancées(expenditurecommittedbutforwhichnopayment

orderhasbeenissued)

DSCE Document de Stratégie pour la Croissance et l’Emploi (GrowthandEmploymentStrategyPaper)

ECAM Enquête Camerounaise auprès des Ménages(CameroonianHouseholdSurvey)

EESI Enquête sur l’Emploi et le Secteur Informel(EmploymentandInformalSectorSurvey)

EGMA EarlyGradeMathematicsAssessment

EGRA EarlyGradeReadingAssessment

EMIS EducationManagementInformationSystem

GDP GrossDomesticProduct

IMF InternationalMonetaryFund

INS Institut National de Statistique (NationalInstituteofStatistics)

MINEDUB Ministère d’Éducation de Base(MinistryofBasicEducation)

PASEC Programme d’Analyse des Systèmes Éducatifs de la CONFEMEN(ProgramfortheAnalysisof

EducationSystems)

PTR Pupil-TeacherRatio

PTA ParentTeachersAssociation

SNH Société Nationale des Hydrocarbures(NationalHydrocarbonsCorporation)

SONARA Société Nationale de Raffinage(NationalRefinery)

UNESCO UnitedNationsEducational,ScientificandCulturalOrganization

UNICEF UnitedNationsChildrenFund

WB WorldBank

ZEP Zones d’Éducation Prioritaires (EducationPriorityZones)

CAMEROON ECONOMIC UPDATE vii

ACKNOWLEDGEMENT

The Cameroon Economic Updates are produced

byaTeamledinitiallybyRajuJanSinghandnowby

SouleymaneCoulibaly.ShobhanaSosalepreparedthe

chapteroneducation.Forthispurpose,theTeamhas

builtupontherecently-completedEducationCountry

StatusReportforCameroon(Lesystèmed’éducation

etdeformationduCameroundanslaperspectivede

l’émergence).OtherTeammembersincludeFaustin

Koyassé,SimonDietrichandSylvieNdze.TheWorld

BankGSDTIunitensuredtheFrenchtranslationofthe

CEU.Thephotosinthisreport(includingonthecover)

aretothecreditofStephanBachenheimer,Consultant

Sr.Videographer,ECRBM,WorldBank.

CommentsreceivedfromBirgitHansl,JohnLitwack,

Cia Sjetnan, Ousmane Kolie and Abel Bove are

gratefully acknowledged. Greg Binkert (Country

Director for Cameroon), Mark Thomas (Economic

Policy Sector Manager), Peter Maseru (Education

Sector Manager), and Olivier Godron (Country

Program Coordinator) provided guidance and

advice, and have been an invaluable source of

encouragement.

TheTeamhasalsogreatlybenefitedfromconsulta-

tions with Cameroon’s key policy makers and ana-

lysts, who provided important insights, in particu-

larthefollowinginstitutions:theBEAC,theTechnical

MonitoringCommittee(CTS),theMinistryofEconomy

andPlanning,theMinistryofFinance,andtheNational

InstituteofStatistics.TheTeamisalsogratefultotheir

colleaguesattheInternationalMonetaryFund.

CAMEROON ECONOMIC UPDATE 1

EXECUTIVE SUMMARY

WiththeseCameroonEconomicUpdates,theWorld

Bank is pursuing a program of short and frequent

reports which analyze the trends and constraints

inCameroon’seconomicdevelopment.Eachissue,

producedbi-annually,providesanupdateofrecent

economicdevelopments,aswellasaspecialfocus

onatopicalissue.

The Cameroon Economic Updates aim at sharing

knowledge and stimulating debate among those

interestedinimprovingtheeconomicmanagement

ofCameroonandunleashingitsenormouspotential.

Thenotestherebyofferanothervoiceoneconomic

issuesinCameroon,andanadditionalplatformfor

engagement, learning and exchange. This seventh

issue of the Cameroon Economic Updates is enti-

tled“RevisitingtheSourcesofGrowth—TheQuality

ofBasicEducation”.

The average observed economic growth rate from

2010 to 2013 is a mere four percent, one percent-

agepointbelowthe‘Vision2035’targets.Achieving

the official objectives set for 2020 would require

Cameroon to move to double digit annual growth

ratesoverthe2014–2020period,comparedtothe

4.8to5.4percentprojectedbytheWorldBank.This

callsforrenewedattentiontothesourcesofgrowthin

Cameroontoidentifypolicyareasthatcanhelp“mus-

terallourenergytochampionthiscauseandsum-

monallourstrengthtoensuregrowth”,asemphat-

icallyexpressedbyPresidentBiyainhisendofyear

2013address.ThisseventheditionoftheCameroon

EconomicUpdatelooksatthequalityofbasicedu-

cationtoensurethattherightinvestmentsaremade

inpeopletobuildhumancapital,akeyingredientfor

sustainableeconomicgrowth.

Educationiskeytobuildingskills,enhancingthepro-

ductivity of workers, and contributing positively to

longtermgrowth.Attheindividual level,education

increasesearningpotentialandreducestheriskof

fallingintopoverty.Thereisastronglinkbetweenthe

educationlevelofahouseholdheadandtheproba-

bilityofthishouseholdtofallunderthepovertyline.

Studieshavealsoshownimportantindirecteffectsof

education,especiallyonhealth.Takingintoaccount

differencesinfactorssuchasincomeandresidency

(rural/urban), an increase in the level of education

positively affects issues such as family planning,

reproductivehealthandchildhealth.

Cameroon has achieved significant progress over

thelastdecadeinexpandingaccesstobasicedu-

cation.Thenumberofstudentscompletingprimary

school,theprimarycompletionrate,rosefrom53

percentin2001toabout80percentin2011.School

life expectancy rose by four years over the same

period,agreatimprovementinrelationtointerna-

tionalcomparators.Theprimarygrossenrollment

raterosefrom102.8percent in2001to112.9per-

centin2011.

Theincreaseingrossenrollment,however,doesnot

seemtohavebeenaccompaniedbybettereduca-

tionoutcomes.Cameroon’sresultsonthestandard

testPASEC(ProgramfortheAnalysisofEducation

Systems),astudentachievementtestdirectedby

the Conference of the Ministers of Education of

Frenchspeakingcountries,declinedbetween1998

and2005(latestyearforwhichdataisavailableat

the time of printing this report), although it is still

higherthaninmanyotherFrancophonecountries

inAfrica.

CAMEROON ECONOMIC UPDATE2

Theimprovementsinaccesstoeducationalsomask

significant differences in education performance

across and within individual regions, as well as

betweengenderandincomegroups.Thethreenorth-

ern regions (Far North, North and Adamawa) and

theEast lagbehindineducationoutcomesdespite

an increased attention through the ZEP (“Zones

d’Education Prioritaire”) program aimed at raising

schoolingaccess,attendance,andachievement.

TheEconomicUpdatesuggestsimprovingdatacol-

lection in order to better monitor education ser-

viceprovision,assessmoresystematicallystudent

learning, increase in budget allocation to educa-

tion as a whole, reprioritize public spending to the

ZEPs,ensuretransparencyinbudgetallocation,and

revisit the textbook policy to ensure durability and

affordability.

CAMEROON ECONOMIC UPDATE 3

RECENT ECONOMIC DEVELOPMENTS

2013 has seen some encouraging economic developments…

Growth

Inspiteofasluggishglobaleconomy,preliminaryinfor-

mationsuggeststhateconomicgrowthinCameroon

couldreachabout4.6percentin2013(comparedto

4.6percentin20121).Theeconomygrewby2.9and

3.8percentinthefirsttwoquarters,respectively(over

thesamequarterinthepreviousyear,Figure1).

As in recent years, the tertiary sector is the main

driver of economic growth (Figure 2), telecommu-

nicationsandtransportbeingparticularlydynamic.

Intheprimarysector,industrialandexport-oriented

agriculture has driven growth. Rubber and cotton

exportshavecontinuedtorisewhilecocoaexports

have reversed their downward trend due to better

prices(Figure3).Coffeeexportshoweverhavefallen

byabout50percent,duetoacombinationoffactors:

theslowdowninproductionduetoagingplantsand

agradualretreatfromthesector,wascompounded

withexportersbuildingupcoffeestocksbecauseof

lowinternationalprices.

The secondary sector has not been as dynamic as

in2012.Afteraslump in thefirstquarter, industrial

productionexpandedbythreepercentinthesecond

quarter (year-on-year). The performance is partly

explainedbyshortfallsinelectricityproductioncaused

FIGURE 3: Export Performance, Q1–Q3 2013 (y-o-y change in volume)

–60

40

–40

20

–20

0

60

Logs andwood

products

Coffee Cotton Aluminium Cocoa Rubber

Sources: CustomsandWBstaffcalculations.

FIGURE 2: Sectoral Contributions to GDP Growth, 2007–13 (in percent)

2007 2008 2009 2010 2011 2012 2013 Proj.–2

4

2

0

6

Primary sector Oil Secondary sector (excl. otil)GDP GrowthTertiary sector

Sources: INSandWBstaffcalculations.

FIGURE 1: GDP Growth by Quarter, 2011–2013 (percentage change over same quarter, previous year)

Q2 Q32011 2012 2013

Q4 Q1 Q2 Q3 Q4 Q1 Q20

4

5

6

3

2

1

7

Source: INSNationalAccountsandWBstaffcalculations.

1The4.4percentestimatementionedinthe2013JulyissueoftheCameroonEconomicUpdateswasrevisedto4.6percent.

CAMEROON ECONOMIC UPDATE4

bylimitedhydropowercapacityduringthedryseason

(December–June) as well as delays in the commis-

sioningofthenewgasfiredpowerplantinKribi.The

plant,216MWofinstalledcapacity,beganoperatingin

February2013(availablecapacityaround30MW)to

progressivelyreachitstotalinstalledcapacityinMay

2013.Theplantwasbuilttocomplementtheseasonal

productionpatternofCameroon’shydropowerplants.

Accordingly,itgeneratedbetween75and100MWdur-

ingtherainyseason(July–December),whenhydro-

powerwasabundantandcheap,andhasbeenrun-

ningalmostatfullcapacitysinceDecember(between

170and180MW).Itisplannedtoexpandtheplant’s

capacitybyanadditional114MWandthetransmission

linesconnectingKribi toEdéaarealreadyequipped

accordingly.However,whilethegasplantisusefulto

complementCameroon’senergymix,thegridtrans-

portingpowerfromEdéatoDoualaandYaoundé,the

country’smaincentersofelectricityconsumption,is

overloadedandoutworn.Iturgentlyneedsinvestment

tokeepupwithrisingdemandandensurethepower

supplyofCameroon’smainurbancenters.

Intheoilsector,theupwardtrendinproductionhas

continued,expandingto17.4millionbarrelsinthefirst

threequartersof2013,comparedto17millionbarrels

overthesameperiodlastyear(Figure5).However,this

expansionisslowerthanthatprojectedearlierthisyear

becauseofdelayedactivitiesinnewoilfields.Totaloil

productionfor2013isestimatedat24.3millionbar-

rels,comparedtothe27millionbarrelsprojectedin

April.Overall,itisimportanttonotethatCameroonis

notasdependentonoilasotherneighboringoilpro-

ducing countries (Figure 6). Oil GDP represented 8

percentoftotalGDPinCameroonin2011,compared

to38to48percentinAngola,NigeriaandChad.While

oilaccounts foronefourthofgovernmentrevenues

andhalfoftheexportsinCameroon,intheotherthree

countriesmorethanthreefourthoftherevenuesand

almostalloftheexportsstemfromoil.

Inflation

In2013,pricesrosemoderatelyandtheinflationrate

endedtheyearwellbelowtheregionalconvergence

criterionofthreepercent(Figure7).Theoverallprice

levelincreasedby1.6percentin2013(year-on-year),

comparedto2.5percentoverthesameperiodthe

yearbefore.Foodprices,whichhavebeenthemain

driverofinflationinrecentyears,roseonlyby2.2per-

cent,mainlybecauseofgoodharvests(comparedto

4.2percentoverthesameperiodlastyear).Thecon-

tinuedfreezeonretailfuelpriceshasalsocontributed

tocontaininginflationarypressures.

FIGURE 4: Industrial Production Index, 2010–2013 (y-o-y change in percent)

2013

–8

10

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q3 Q4Q1 Q2 Q1 Q22010 2011 2012

–6–4–2

02468

Sources: INSandWBstaffcalculations.

FIGURE 5: Quarterly Oil Production 2010–13 (in mio barrels)

2012

4.0Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q3 Q4Q1 Q2 Q1 Q2 Q3

2009 2010 2011

7.0

4.5

5.0

5.5

6.0

6.5

Sources: SNH.

FIGURE 6: Share of oil in GDP, revenues and exports, 2011 (in percent)

0

100

20

40

60

80

Oil GDP/total GDP Oil revenues/total gvtrevenues

Oil exports/totalexports

Angola Nigeria Chad Cameroon

Source: IMFandWBstaffcalculations.

RECENT ECONOMIC DEVELOPMENTS 5

…although the fiscal and external balances have deteriorated

Fiscal

Projections on the basis of the fiscal performance

observedoverthefirstthreequartersoftheyearindi-

cateanunderperformanceinfiscalrevenues.Total

revenues(includinggrants)areprojectedtoamount

to 18.4 percent of GDP (after cross-cancellation of

subsidiestothenationalrefinerySONARAandtaxes

owedbythelatter),whichis0.4percentagepoints

belowJulyprojectionsaswellasestimatedperfor-

mancein2012(Table1).Despitehighoilpricesand

anincreaseinproduction,oilrevenuesaredowndue

torisingoperatingcosts.

At the same time, current spending is expected to

exceedthebudgetbyaboutonepercentofGDP.The

mainreasonforthisistheunder-budgetingofthefuel

subsidies, which are projected at 450 billion CFAF

(3.3 percent of GDP) compared to only 220 billion

scheduledinthebudget.Investmentspending,mean-

while,isprojectedtoreach6.5percentofGDP,com-

paredto6.9percentbudgeted.Thisperformancecan

partlybeexplainedbytherecentreformsinpublicpro-

curementandtheintroductionoftheprogrambudget.

Overall, lower than budgeted revenues and under

budgetedexpensesforfuelsubsidiesleadtoawid-

eningbudgetdeficit,expectedtoreach3.7percent

ofGDP.Thenon-oilprimarybalanceisprojectedto

increaseto8.9percentofnon-oilGDP,comparedto

7.2percentin2012.

FIGURE 7: Selected Prices, 2007–13(y-o-y change in percent)

–6

14

–4–2

02468

1012

Jan-

07

Jun-

07

Nov-

07

Apr-

08

Sep-

08

Feb-

09

Jul-0

9

Dec-

09

May

-10

Oct-

10

Mar

-11

Aug-

11

Jan-

12

Jun-

12

Nov-

12

Apr-

13

Sep-

13

Total (headline) CPI Food price index Fuel price index

Sources: INSandWBstaffcalculations.

TABLE 1: Fiscal Performance, 2012–13y (in percent of GDP)

2012 2013 2013 2013

Est. Budget July Proj. Proj.

Revenue and Grants 18.8 19.2 18.8 18.4

OilRevenue 5.4 5.1 5.2 5.0

Non-oilRevenue 13.0 13.6 13.2 13.1

Directtaxes 3.6 3.6 — 3.5

Specialtaxonpetroleumproducts 0.8 0.8 — 0.8

Othertaxesongoodsandservices 5.6 6.3 — 6.6

Taxesoninternationaltrade 2.3 2.2 — 2.4

Non-taxrevenue 0.7 0.8 — 0.8

Grants 0.4 0.5 0.4 0.4

Total Spending 20.4 21.5 22.4 22.1

CurrentSpending 14.0 14.6 16.0 15.6

CapitalSpending 6.5 6.9 6.3 6.5

Overall Balance* –1.7 –2.3 –3.6 –3.7

Non-oilprimarybalance** –7.2 –7.7 — –8.9

Source: Dashboardofpublicfinances(MinistryofFinance)andWBstaffcalculations.*doesnotincludepaymentofarrears.**inpercentofnon-oilGDP.

CAMEROON ECONOMIC UPDATE6

External

Thetradedeficitisexpectedtohavegrownin2013to

1.6percentofGDP,comparedto1.1percentin2012

(Table2).Thisismainlyduetorisingimportsofinter-

mediarygoodsfortherealizationoflargeinfrastruc-

tureprojectsandlowpricesforsomeofCameroon’s

major export products, especially coffee. Non-oil

exportsareexpectedtohavedroppedfrom11.1per-

centofGDPin2012to10.5percentin2013.Atthe

sametime,thecurrentaccountdeficitisprojectedto

amountto4.9percentofGDPin2013,whichisabout

thesameastheyearbefore,butmorethanoneper-

centabove2011figures.Foreignreservesdropped

byabout63millionUSD(30billionFCFA)to3.3bil-

lionUSD.

Medium term prospects are positive…

Oil and Gas production are expected to increase

significantlyoverthecomingyears. In2014,theoil

sectorisestimatedtocontinueitsexpansionwitha

projected24percentincreaseinproduction.Inthe

mediumterm,oilproductioncouldmorethandouble

thankstotheexploitationofnewoilfields.According

to projections by the National Hydrocarbons

Association (SNH), oil production could reach

57.0 million barrels in 2016, compared to 24.4 mil-

lionbarrelsin2013.TheSNHexpectsoilproduction

todecreasethereafter,butnaturalgascouldfillthe

gapinthelongrun.

The first generation of large infrastructure projects

isscheduledtobecompletedoverthecomingyears.

Theseincludethenewdeep-seaportinKribi,expected

tostartoperationsmid-2014,theMemvéléandLom

Pangarhydropowerdams,aswellasthesecondWouri

bridge.Theseprojectscouldalleviatekeyinfrastruc-

turebottlenecksandcontributepositivelytoeconomic

growth. A second generation of large infrastructure

projectsisalreadybeingplannedbyGovernmentand

includesroadandrailtransportcorridors.

Withregardstoeconomicdevelopmentsinadvanced

economies,therearereasonstobecautiouslyopti-

misticfor2014.AccordingtotheEconomicSentiment

Indicator,economicconfidence,whilestillbelowthe

long-term average, is slowly rising in the euro zone

(Figure8).Atthesametime,theIMF,initsOctober

edition of the World Economic Outlook, projects a

growthrateofonepercentintheEurozoneaftertwo

yearsofcontraction.

TABLE 2: Balance of Payments, 2011–2013 (in percent of GDP)

2011 2012 2013 (proj.)

Trade balance –2.3 –1.1 –1.6

Imports 24.4 23.8 23.4

Non-oilexports 10.6 11.1 10.5

Current account balance

Excludinggrants –3.8 –4.8 –4.9

Includinggrants –2.9 –4.0 –4.0

Financial account balance 1.5 4.3 3.7

Officialcapital 1.0 1.6 1.7

Long-termborrowing 1.5 2.1 2.4

Amortization –0.5 –0.6 –0.7

Non-officialcapital(net) 1.0 2.2 1.9

Oilsector 0.4 0.6 0.7

Non-oilsector 0.6 1.6 1.2

Overall balance –1.3 0.3 –0.2

Source: IMF.

RECENT ECONOMIC DEVELOPMENTS 7

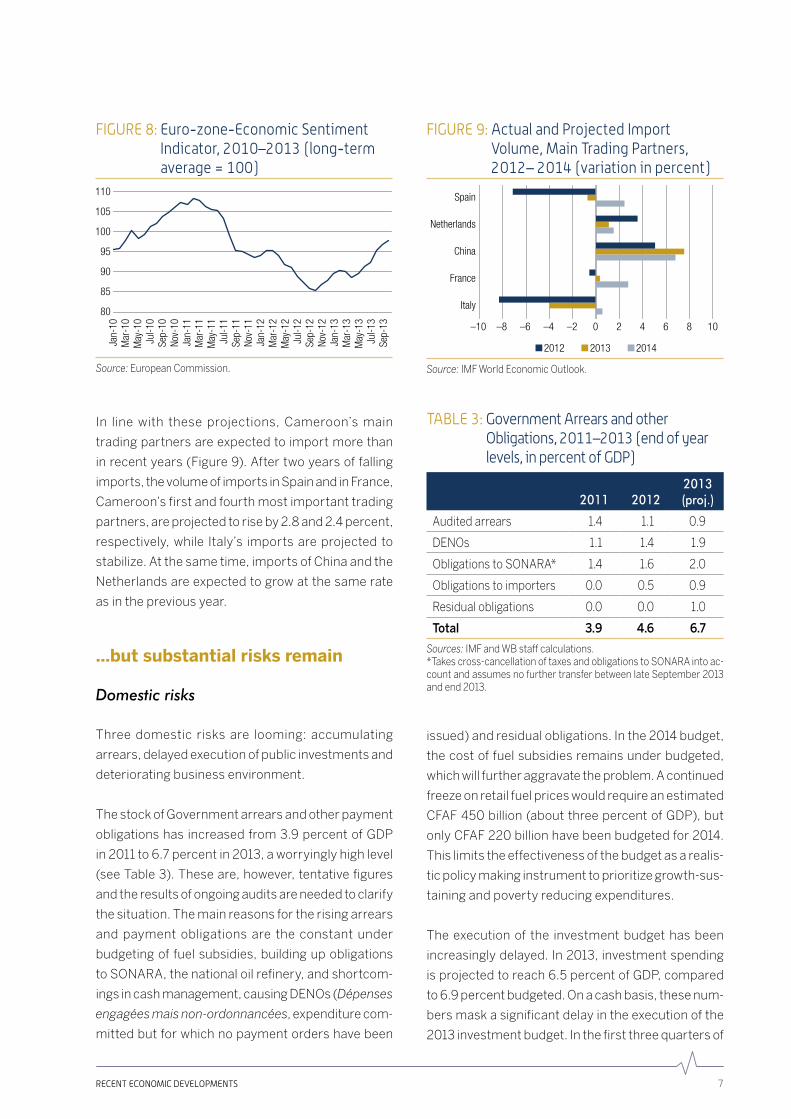

In line with these projections, Cameroon’s main

tradingpartnersareexpectedtoimportmorethan

inrecentyears(Figure9).Aftertwoyearsoffalling

imports,thevolumeofimportsinSpainandinFrance,

Cameroon’sfirstandfourthmostimportanttrading

partners,areprojectedtoriseby2.8and2.4percent,

respectively, while Italy’s imports are projected to

stabilize.Atthesametime,importsofChinaandthe

Netherlandsareexpectedtogrowatthesamerate

asinthepreviousyear.

…but substantial risks remain

Domestic risks

Three domestic risks are looming: accumulating

arrears,delayedexecutionofpublicinvestmentsand

deterioratingbusinessenvironment.

ThestockofGovernmentarrearsandotherpayment

obligationshas increasedfrom3.9percentofGDP

in2011to6.7percentin2013,aworryinglyhighlevel

(seeTable3).Theseare,however,tentativefigures

andtheresultsofongoingauditsareneededtoclarify

thesituation.Themainreasonsfortherisingarrears

and payment obligations are the constant under

budgetingof fuelsubsidies,buildingupobligations

toSONARA,thenationaloilrefinery,andshortcom-

ingsincashmanagement,causingDENOs(Dépenses

engagées mais non-ordonnancées,expenditurecom-

mittedbutforwhichnopaymentordershavebeen

issued)andresidualobligations.Inthe2014budget,

thecostoffuelsubsidiesremainsunderbudgeted,

whichwillfurtheraggravatetheproblem.Acontinued

freezeonretailfuelpriceswouldrequireanestimated

CFAF450billion(aboutthreepercentofGDP),but

onlyCFAF220billionhavebeenbudgetedfor2014.

Thislimitstheeffectivenessofthebudgetasarealis-

ticpolicymakinginstrumenttoprioritizegrowth-sus-

tainingandpovertyreducingexpenditures.

The execution of the investment budget has been

increasinglydelayed.In2013,investmentspending

isprojectedtoreach6.5percentofGDP,compared

to6.9percentbudgeted.Onacashbasis,thesenum-

bersmaskasignificantdelayintheexecutionofthe

2013investmentbudget.Inthefirstthreequartersof

FIGURE 8: Euro-zone-Economic Sentiment Indicator, 2010–2013 (long-term average = 100)

80

110

Jan-

10

Nov-

10Se

p-10

Jul-1

0M

ay-1

0M

ar-1

0

Jan-

11

Nov-

11Se

p-11

Jul-1

1M

ay-1

1M

ar-1

1

Jan-

12

Nov-

12Se

p-12

Jul-1

2M

ay-1

2M

ar-1

2

Jan-

13

Jul-1

3M

ay-1

3M

ar-1

3

Sep-

13

85

90

95

100

105

Source: EuropeanCommission.

FIGURE 9: Actual and Projected Import Volume, Main Trading Partners, 2012– 2014 (variation in percent)

–10 –4 0 42–2–6–8 6 8 10

Italy

France

China

Netherlands

Spain

2012 2013 2014

Source: IMFWorldEconomicOutlook.

TABLE 3: Government Arrears and other Obligations, 2011–2013 (end of year levels, in percent of GDP)

2011 20122013 (proj.)

Auditedarrears 1.4 1.1 0.9

DENOs 1.1 1.4 1.9

ObligationstoSONARA* 1.4 1.6 2.0

Obligationstoimporters 0.0 0.5 0.9

Residualobligations 0.0 0.0 1.0

Total 3.9 4.6 6.7

Sources: IMFandWBstaffcalculations.*Takescross-cancellationoftaxesandobligationstoSONARAintoac-countandassumesnofurthertransferbetweenlateSeptember2013andend2013.

CAMEROON ECONOMIC UPDATE8

theyear,only35percentofthebudgetedinvestments

financedthroughinternalresourceswereexecuted

(Table4).Thisperformancecanpartlybeexplained

bythereformofpublicprocurementwiththecreation

ofaMinistryofpublicprocurementandtheintroduc-

tionandimplementationoftheprogrambudget.Asa

consequence,theGovernmentextendedthecomple-

mentarybudgetperiodbytwomonths,untilMarch

2014.Ifthesedelaysbecomepersistent,thegrowth

dividendoftheseinvestmentsmightbediluted.

The business climate in Cameroon remains dis-

couraging to new investment. In the 2014 edition

ofWorldBank’sDoingBusinessReport,Cameroon

lost six positions compared to the 2013 ranking2,

and now ranks 168th out of 189 countries. In order

to make Cameroon more attractive to investors,

the Government adopted a new investment law in

April 2013. The law offers exemptions and reduc-

tionsonthemajorityoftaxestonewbusinessesas

well as to existing ones under certain conditions.

Thelaw’simpactonGovernmentrevenueisuncer-

tain but might be substantial and should therefore

be closely monitored. The text remains vague on

the administrative procedures necessary to bene-

fitfromthetaxexemptions,whichmightraisetrans-

parencyconcerns.

External risks

Ontheexternalside,oilpricevolatilityandincreasing

financingcostsoninternalmarketsshouldbecare-

fullywatched.

Cameroonisvulnerabletovolatilecommodityprices.

Adropininternationaloilpriceswouldputpressure

onpublicfinances,asaboutafourthofGovernment

revenuesstemsfromtheoilsector.ThelatestWorld

BankCommodityPriceForecastprojectsoilpricesto

berelativelystableinnominalUSDollars,butsteadily

decreasinginrealterms(Figure10)duetogrowing

suppliesofunconventionaloil,efficiencygains,and

(lessso)substitutionawayfromoil.Coffee,another

sectorthatcontributestotheCameroonianeconomy,

is also dependent on international prices. In 2013,

coffee exports halved, due among other things, to

exportersbuildingupcoffeestocksbecauseoflow

international prices. A fall in prices of other impor-

tant agricultural export commodities, such as cot-

ton, rubber, wood or cocoa, would severely affect

theprimarysector.

Thecostoffinancingrepresentsanindirectsource

of external risk. Financial conditions in developing

countriesoverthepastsixmonthshavebeenroiled

byaportfolioadjustmentthatwassetinmotionby

speculationsoverthetimingofaUSFederalReserve

2The Doing Business (DB) 2014 ranking is not comparedtothepublishedrankingforDB2013,buttoacomparablerankingforDB2013thatcapturestheeffectsofsuchfactorsasdatacorrectionsandtheadditionof4economies(Libya,Myanmar,SanMarinoandSouthSudan)tothesample in2014.

TABLE 4: Execution of Investment Budget Q1–Q3, 2013 (in CFAF billion)

Budget Execution%

Executed

InternalResources 676 239 35.4

ExternalResources 281 232 82.6

Total 957 471 49.2

Sources: MINFI,MINEPAT,CAA.

FIGURE 10: Oil Price Forecasts, 2013–2025 (in USD per barrel)

60

80

70

110

90

100

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Nominal USD Real 2010 USD

Source: WBCommodityPriceForecastJanuary2014.

RECENT ECONOMIC DEVELOPMENTS 9

withdrawalofsomeofthemeasuresputinplaceto

supportgrowth,despitenoactualchangeinthelong-

termassetpurchases.Theyieldon10-yearUnited

StatesTreasurybillsroseby100basispoints,spark-

ingasignificantportfolioreadjustmentasinvestors

increasedtheshareofnowhigher-yieldingUSbonds

intheiroverallportfolios.Thisportfolioadjustment

caused a temporary—but significant—reversal in

capitalflowsfromdevelopingcountriestotheUnited

States.Onacumulativebasis,investorswithdrewa

net total of US$64 billion from developing country

mutualfundsbetweenJuneandAugust.Grosscap-

italflowstodevelopingcountriesfellbyhalfandthe

currenciesandstockmarketsofseveralmajordevel-

opingeconomiesdeclinedbyasmuchas15percent.

Suchmovementscanhaveanindirectimpactonthe

Cameroonianeconomythroughitsincreasingtrade

flowswithemergingmarkets.NowthattheFederal

Reservehasannouncedaslowdownofitsquantita-

tiveeasingprogramfor2014,theimpactoffinancing

costsof theemergingeconomiesthat increasingly

tradewithCameroonshouldbecloselyexamined.

Looking forward, the sources of growth need to be revisited

The developments laid out above could negatively

affect capital accumulation or preclude the reallo-

cationofproductionfactorstotheirmosteffective

usesandhencemaintaingrowthbelowthetargets

formulatedinthe2009Document de Stratégie pour

la Croissance et l’Emploi (DSCE), absent a timely

policy response. Cameroon needs an acceleration

tomeetthe2020referencescenarioobjectiveslaid

outintheDSCE.Theaverageobservedgrowthrate

from 2010 to 2013 is 4.1 percent3, one percentage

pointbelowthe ‘Vision2035’ targets(and0.8per-

centagepointsbelowtheDSCEreferencescenario;

Figure11).Achievingtheobjectivessetfor2020would

require an annual growth rate of 9.5 percent dur-

ingthe2014–2020period,comparedto the4.8to

5.4percentprojectedbytheWorldBank(Figure12).

Thissituationcallsforrenewedattentiontothe

sourcesofgrowthinCameroon—toidentifypolicy

areasthatcanhelpCameroonreachtheeconomic

growthlevelsthatareneededtosustainablydevel-

opthecountryandreducepoverty.Giventheim-

portantimpactofeducationonlongtermgrowth,

arevisionofthesourcesofgrowthshouldstartby

lookingatthequalityofhumancapital.

Endogenousgrowththeorieshavebeentestedover

decadesinawiderangeofcountriesandconfirmed

thathumancapitalplaysacriticalroleinachieving

economicgrowth.Inthisregard,education,to-

FIGURE 11: Actual and Projected GDP Growth Rates compared to Government Objectives, 2010–2020 (in percent)

0

12

8

6

4

2

10

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Vision 2035 Scenario Reference Scenario Actual/Projected

Sources: DCSEandWBstaffcalculations.

FIGURE 12: GDP Growth Rate necessary to reach Government Objectives (in percent)

0

12

8

6

4

2

10

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Catch up Vision 2035 Actual/Projected

Sources: DCSEandWBstaffcalculations.

3Actualgrowthratefor2010–2012,projectedgrowthratefor2013.

CAMEROON ECONOMIC UPDATE10

getherwithhealth(coveredinthepreviousissueof

the“CameroonEconomicUpdate”),contributein

animportantmannertoCameroon’saspirationto

becominganemergingeconomyby2035.Thenext

chapterlooksatthequalityofbasiceducationto

ensurethattherightinvestmentismadeinpeople

tobuildhumancapitalatanearlyage,akeyingredi-

entforsustainablegrowthanddevelopment.

CAMEROON ECONOMIC UPDATE 11

BASIC EDUCATION IN CAMEROON

Educationiskeytobuildingskillsandenhancinglabor

productivityandtocontributepositivelytolong-term

economicgrowth.Educationiskeytobuildingskills

andenhancinglaborproductivityandtocontribute

positivelytolong-termeconomicgrowth.

Atthe individual level,education increasesearning

potentialandreducestheriskoffallingintopoverty.

Thereisastronglinkbetweentheeducationlevelof

ahouseholdheadandtheprobabilityofthishouse-

holdtofallunderthepovertyline.A2013Education

Country Status Report shows important indirect

effects of education, especially regarding health.

Taking into account differences in factors such as

income and residency (rural/urban), a higher level

ofeducationpositivelyaffectsissuessuchasfamily

planning,reproductivehealthandchildhealth.

Againstthisbackdrop,thelackofimprovementinedu-

cationoutcomesinCameroon,despitebetteraccess

to education, is a cause for concern. Furthermore,

importantdisparitiesexistineducationperformance

acrossandwithinregions,aswellasbetweengender

and income groups. The poorest benefit less from

publicspendingineducationastheyprimarilylivein

disadvantagedareas,sufferfromthechronicunder-

fundingoftheprimarysector,andarehitespecially

hardbyhighout-of-pocketspendingforeducation.

This chapter draws on the recently-completed

EducationCountryStatusReportforCameroon(Le

système d’éducation et de formation du Cameroun

dans la perspective de l’émergence). It describes

Cameroon’s education profile, discusses resource

allocationtoeducationandgovernanceissuesinthe

educationsector,andsuggestssomeoptionsgoing

forward.

Cameroon has made significant progress when it comes to access to basic education…

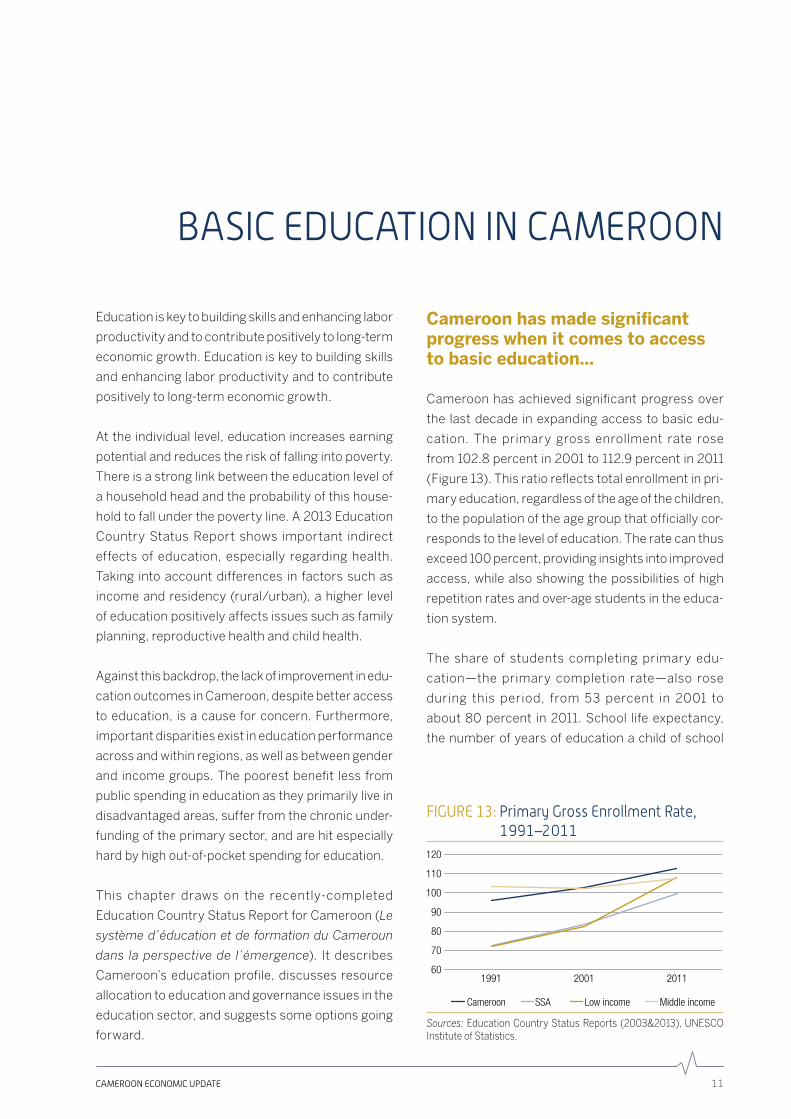

Cameroon has achieved significant progress over

the last decade in expanding access to basic edu-

cation. The primary gross enrollment rate rose

from102.8percentin2001to112.9percentin2011

(Figure13).Thisratioreflectstotalenrollmentinpri-

maryeducation,regardlessoftheageofthechildren,

tothepopulationoftheagegroupthatofficiallycor-

respondstothelevelofeducation.Theratecanthus

exceed100percent,providinginsightsintoimproved

access, while also showing the possibilities of high

repetitionratesandover-agestudentsintheeduca-

tionsystem.

The share of students completing primary edu-

cation—the primary completion rate—also rose

during this period, from 53 percent in 2001 to

about 80 percent in 2011. School life expectancy,

thenumberofyearsofeducationachildofschool

FIGURE 13: Primary Gross Enrollment Rate, 1991–2011

60

70

80

100

120

90

110

1991 2001 2011

Cameroon SSA Low income Middle income

Sources: Education Country Status Reports (2003&2013), UNESCOInstituteofStatistics.

CAMEROON ECONOMIC UPDATE12

enteringagecanexpecttoreceiveduringhisorher

life-time, increased by four years over the same

period,agreat improvementwhenlookingat inter-

nationalcomparators(Figures14and15).Theexpla-

nation isdue inpart to theabolitionofschool fees

inprimaryeducation in2000whichspurredsome

increaseintotalenrolmentandtoimprovedservice

deliverythroughthecontractteachersprogramdur-

ingtheperiod2007–2011.Totalsecondaryenrolment

morethandoubledinthepasttwodecades,reach-

ingnearly1.3milliontotalstudentsin2009.Overall,

children spend 2.5 more years in school than two

decadesago,totalinganaverage10yearsofeduca-

tion,wellintosecondaryschool.

Butsomecontradictionsexist.Theseimprovements

do not seem to have been accompanied by bet-

tereducationoutcomes.Cameroonparticipatesin

theProgramfortheAnalysisofEducationSystems

(PASEC),astudentachievementtestdirectedbythe

ConferenceoftheMinistersofEducationofFrench

speaking countries (CONFEMEN). Although still

higher than in many other Francophone countries

inAfrica,Cameroon’sresultsonthisstandardtest

declined between 1998 and 2005 (Figures 16 and

17).Onthe5thgradePASECstudentassessment,

only Gabon achieved a higher average score over

CamerooninFrench,andonlyMadagascardidbetter

thanCamerooninmathematics.Datafromthe2010

PASECresultsarenotyetavailable.Cameroonwill

participateinthenextPASECstudentassessment

in2014.Resultsfromthesewouldhelptoconstruct

comparative time series data on student learning

outcomes.Therecurrentlyexistnoothercompara-

tivelearningassessments.Itisimportanttonotethat

Cameroon’s performance over time has declined

slightly, although from a comparative perspective

the results are higher than in comparable African

countries.In2010,theMinistryofBasicEducation

(MINEDUB) conducted a national Early Grade

ReadingAssessment(EGRA).Theresultsshowthat

49percentof3rdgradestudentshadgreatdifficulty

inreading,and27percentcouldnotreadatall.

Furthermore, important disparities persist: The

improvements in access to education mask signif-

icantdifferences ineducationperformanceacross

andwithinindividualregions,aswellasbetweengen-

derandincomegroups.

FIGURE 16: Evolution of PASEC Results in Cameroon, 1996–2005 (scale 0–100)

0

20

10

30

40

50

60

70

1996 2005

Average score French 5th grade Average score Maths 5th grade

Source: PASEC.

FIGURE 15: School Life Expectancy, 2001–2011 (in Years)

5

6

7

8

10

12

9

11

2001 2011

Cameroon* SSA Low income Middle income

Sources: Education Country Status Reports (2003&2013), UNESCOInstituteofStatistics.*RESENdoesnotcontainyearofCameroondata.

FIGURE 14: Primary Completion Rates, 1981–2011 (in percent)

40

50

60

80

100

70

90

1991 2001 2011

Cameroon SSA Low income Middle income

Sources: Education Country Status Reports (2003&2013), UNESCOInstituteofStatistics.

BASIC EDUCATION IN CAMEROON 13

… but important disparities persist…

Regions

The Government has identified the three north-

ern regions (Far North, North and Adamawa)

togetherwiththeEastandpocketsofunderserved

areas around urban centers and close to borders,

as “education priority zones” (“Zones d’Éducation

Prioritaires”, ZEP). These ZEP are subject to tar-

getedGovernmentsupporttoraiseschoolingaccess,

attainment, and achievement. In recent years, as

a result of this focalization, the northern regions

haveshownsomeprogressineducationindicators

(Figures18and19).

Despitetheincreasedattentionandprogressshown,

theseregionsstilllagbehindineducationoutcomes.

Comparison between regions shows that in 2011,

primarycompletionratesintheZEPregionsranged

between46percent(intheFarNorth)and81percent

(intheEast),comparedtomorethan94percentin

eachoftheotherregions(Figure20).Thedisparities

inadultilliteracyareevenmorepronounced,where

theFarNorth, theNorth,andAdamawafiguresig-

nificantlyabovethenationalaverageof35percent

(Figure21).Between55and76percentofthepop-

ulationare illiterate inAdamawaandtheFarNorthrespectively,comparedtoonly10and13percentin

theLittoralandCenterregions,respectively.

FIGURE 17: PASEC results in all African Countries tested since 2005 (scale 0–100)

0

20

40

80

60

Gabo

n

Cam

eroo

n

Mad

agas

car

DRC

Buru

ndi

Sene

gal

Togo

Burk

ina

Faso

Cong

o

Chad

Com

ores

Côte

d'Iv

oire

Beni

nAverage score French 5th grade Average score Maths 5th grade

Source: PASEC.

FIGURE 18: Change in Primary Education Attendance, 2001–2007 (in percentage points)

–10

–5

5

0

20

15

10

North

Far N

orth

Wes

t

Litto

ral

Cent

er

Adam

aoua

Sout

h W

est

Sout

h

Yaou

ndé

Doua

la

North

Wes

t

East

Sources: ECAM2&3,WBstaffcalculations.

FIGURE 20: Primary Completion Rates by Region, 2011 (in percent)

0

40

20

100

60

80

Far N

orth

North

Wes

t

Litto

ral

Cent

re

Adam

aoua

Sout

h W

est

Cam

eroo

n

Sout

h

Urba

n

North

Wes

t

East

Rura

l

Source: EducationCountryStatusReport(2013).

FIGURE 19: Change in Adult Literacy, 2001–2007 (in percentage points)

–10

–5

5

0

30

25

10

15

20

North

Far N

orth

Wes

t

Litto

ral

Cent

er

Adam

aoua

Sout

h W

est

Sout

h

Yaou

ndé

Doua

la

North

Wes

t

East

Sources: ECAM2&3,WBstaffcalculations.

CAMEROON ECONOMIC UPDATE14

As the above figures show, there is also a strong

rural-urbandivideinbasiceducationperformance.

Inurbanareas,91percentofthestudentscomplete

primaryschool,comparedtoonly68percentinrural

areas.Theadultilliteracyrateinruralareasis57per-

cent, more than three times higher than in urban

areas(about17percent).Thesefiguresmirrorgeneral

povertyrates,wherethesameregionsaresubjectto

higherlevelsofpovertyaswellaschronicpoverty.

Gender

GenderparityinbasiceducationinCameroonhasnot

improvedsincethe1990s.Onceenrolled,fewergirls

complete primary education than boys. The gender

parityindexforprimarycompletionrateistheratioof

thefemaleprimarycompletionratetothemaleprimary

completionrate,avalueof1 indicatesgenderparity.

InCameroon,theindexvaluewasat0.86in2011,the

samelevelastwentyyearsearlier(Figure22).Overthe

sameperiod,manyothercountrieshavemadesignif-

icantprogresstowardsgenderequalityineducation,

whileCameroonhasmadelittleprogressandhasas

suchfallenbehindinternationalcomparators.

While the overall gender gap remains significant, its

magnitudediffersaccordingtolocation.Forexample,

thenetprimaryschoolattendancerateforgirls,which

istheratioofprimaryschoolagegirlsenrolledinpri-

maryeducationtothetotalnumberofprimaryschool

agegirls,revealsimportantdifferencesbetweenrural

andurbanareas.Inruralareas,primarynetattendance

forgirlsisonlyabout65percent,comparedto79per-

centforboys.Inurbanareas,whereschoolattendance

ishighforallchildren,thegendergapisnarrower.

Income/Wealth

There are significant differences in educational

achievementsbetweenincomegroupsinCameroon.

Whilealmostall(97percent)studentsbelongingtothe

richest20percentfinishprimaryschool,only40per-

centofthepoorestquintiledoso.Figure23showsthe

compositionofthestudentbodyineachoftheeduca-

tionsubsectorsbywealthquintile.Whileenrollmentin

theprimarysectorismoreorlessequallydistributed,

thedistributionbecomesincreasinglyunequalaswe

moveuptheeducationladder.Inthefirstcycleofthe

FIGURE 21: Adult Illiteracy Rate by Region, 2011

0

50

40

30

20

10

80

60

70

Far N

orth

North

Wes

t

Litto

ral

Cent

er

Adam

aoua

Sout

h W

est

Cam

eroo

n

Sout

h

Urba

n

North

Wes

t

East

Rura

l

Source: EducationCountryStatusReport(2013).

FIGURE 22: Gender Parity Index for Primary Completion Rate, 1981–2011

0.6

0.7

0.8

1.0

0.9

1981 1991 2001 2011

Cameroon* SSA Low income Middle income

Source: UNESCOInstituteofStatistics.*nodatafor2001,so2000dataisused.

FIGURE 23: Share of Enrollment in Education Subsectors by Wealth Quintile, 2011 (in percent)

0

40

20

60

100

80

Primary Secondary 1 Secondary 2 Tertiary

Q1 (poorest) Q5 (richest)Q2 Q3 Q4

Source: EducationCountryStatusReport(2013).

BASIC EDUCATION IN CAMEROON 15

secondary,58percentofstudentsarefromthetwo

richestquintiles,comparedto21percentfromthetwo

poorestquintiles.Inthesecondcycleofthesecond-

ary,aswellasinthetertiary,thetworichestquintiles

representalargemajorityofstudents(81and97per-

cent,respectively),whiletherearealmostnostudents

fromthepoorestquintiles.

From a policy point, basic education is “free” in

Cameroon. In spite of this, basic education repre-

sentsrelativelyimportantcoststofamilies—interms

ofactivityandexaminationfees,feesforadditional

(non-governmentpaid)teachers,textbooks,school

uniformsetc.Thecurrentpricingstructureofprimary

enrollmentintroducesintra-regionalinequitiesinthe

system.Parentsarebearingadisproportionatecost

ofprimaryeducationandtheirpreferencefunction

hasresultedinsendingsomechildrentoschooland

notothers(especiallygirls).Poorerhouseholdsare

unabletobearthecost.Theanalysisofallocativeinef-

ficienciesacrosssub-sectorsofeducationisbeyond

thescopeofthisreport.Overallbudgetforeducation

needstobeincreasedandallocativeefficiencyneeds

tobereviewedbasedonquintileanalysis.

… because of inadequate and inefficient resource allocation, utilization and governance problems.

Public and Private Spending

Whyaretheresuchgreatvariationsineducationout-

comes across geographic locations and socioeco-

nomicstatus?Partoftheanswercanbefoundinthe

allocationofresources.AlthoughGovernmentspend-

ing in education has increased from 1.9 percent of

GDPin2000to3.3in2003,ithassincestagnated,

remainingbelowtheregionalaverageof4.3percent

ofGDP(Figure24).

Furthermore, thedistributionof these limitedpub-

lic resources is unequal. In 2011, secondary edu-

cation received a significantly large allocation than

whatwasallocatedtoprimaryorhighereducation.

Incontrast,governmentsinSub-SaharanAfricaput,

onaverage,mostoftheirresourcesinprimaryedu-

cation(Figure25).

CAMEROON ECONOMIC UPDATE16

Disparitiesinpublicspendingarealsosignificantwhen

lookingateducationspendingperstudentinthediffer-

entsub-sectors.Perstudentspending inthesecond

cycleofsecondaryandinthetertiaryaremorethanfive

timeshigherthaninprimaryeducation(Figure26).This

ispartlyaresultofsecondaryandtertiaryeducation

being more expensive per student than for primary

education.Yet,giventhatstudentsfrompoorfamilyare

lesslikelytoreachthesehigherlevelsofeducation(the

secondcycleofthesecondaryortertiary),thispattern

somehowcontributestoanunequaldistributionofedu-

cationspendingbetweenincomegroups.

ThelowGovernmentcontributiontoprimaryeduca-

tionresultsinhighout-of-pocketexpensesforparents

(Figure 27). Also, parents of children enrolled in pri-

maryschoolneedtopayfortextbooks,uniforms,exam

fees,transportationandsometimesextrafeesforextra

homeclasses.Privatefinancingisalsousedtopayfor

teachersthroughParents-TeachersAssociation(PTA)

feecollectionatbothprimaryandsecondaryeduca-

tionlevels(about18percentofprimaryschoolteach-

ersarepaidbyparents).Hence,althoughprimaryedu-

cationisofficiallyfree,inpracticeitisnot.

Theresultinghighcostofprimaryeducationmeans

manyfamiliescannotaffordtosendtheirchildrento

school.Accordingtothelatestsurveyonemployment

andtheinformalsector,lackoffinancingrankedas

themainreasonforchildrendroppingoutofschool

(Figure28).

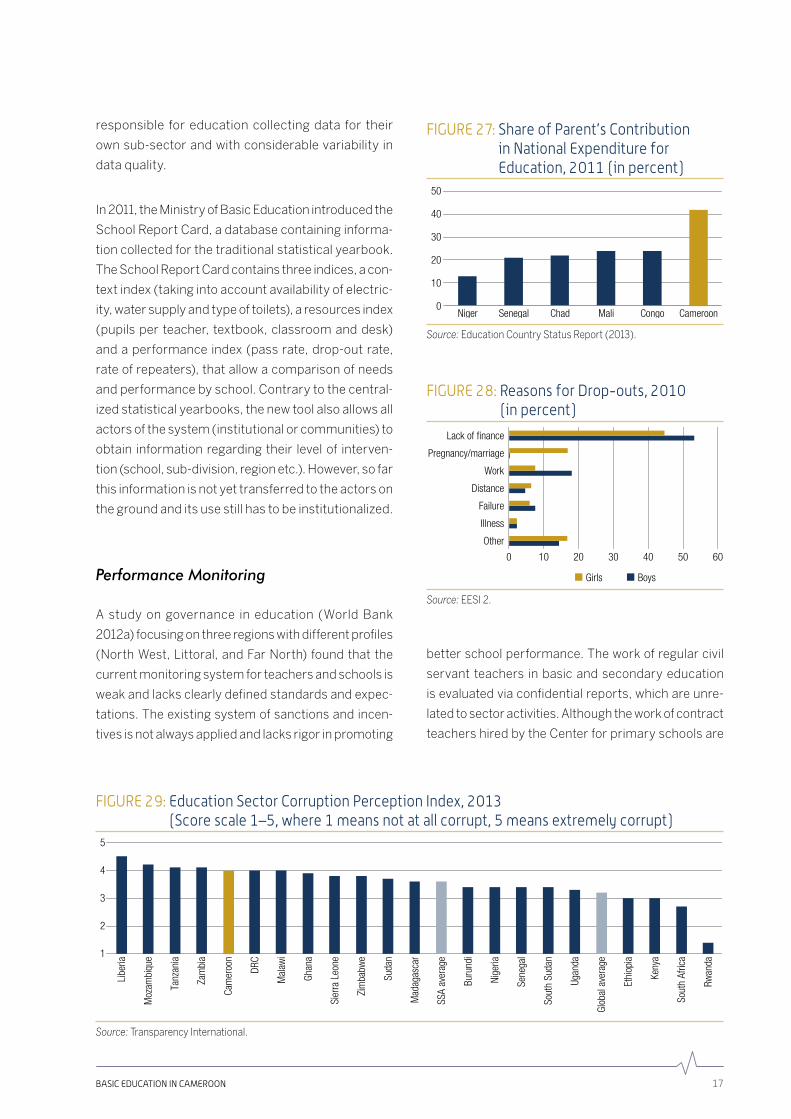

Weak governance and accountability further under-

minestheefficiencyoftheseslimitedpublicresources

invested in education. In 2013, Transparency

InternationalrankedtheCameroonianeducationsys-

temasbeingperceivedasthefifthmostcorruptinSub-

SaharanAfrica(Figure29).Thesamestudyrevealed

that 72 percent of the population think the educa-

tion sector is “corrupt” or “extremely corrupt” (Sub-

SaharanAfricaaveragewas57percent,whiletheglobal

averagestoodat41percent)andthat36percentofthe

peopleincontactwiththeeducationsystempaidabribe

inthelast12months(Sub-SaharanAfricaaveragewas

31percent,whiletheglobalaveragestoodat16percent).

Data availability

Accesstoreliableandtimelydataonsectorperfor-

mance hampers accountability. The current edu-

cation management information system (EMIS)

in Cameroon is fragmented, with five ministries

FIGURE 24: Public Expenditure on Education, 2010 (in percent of GDP)

0.0

2.0

1.0

3.0

5.0

4.0

Sub-SaharanAfrica

Cameroon Low incomecountries

Middle incomecountries

Sources: EducationCountryStatusReport(2013)andWBEducationStatistics.

FIGURE 25: Current Education Spending by Sub-sector, 2011 (in percent of total education spending)

0

20

10

30

50

40

Primary Secondary Tertiary

Sub-Saharan Africa Cameroon

Source: EducationCountryStatusReport(2013).

FIGURE 26: Current Education Spending per Student by Sub-Sector, 2011 (in CFAF thousands per student)

0

100

200

300

Primary Secondary 1 Secondary 2 Tertiary

Source: EducationCountryStatusReport(2013)andWBstaffcalcula-tions.

BASIC EDUCATION IN CAMEROON 17

responsible for education collecting data for their

ownsub-sectorandwithconsiderablevariability in

dataquality.

In2011,theMinistryofBasicEducationintroducedthe

SchoolReportCard,adatabasecontaininginforma-

tioncollectedforthetraditionalstatisticalyearbook.

TheSchoolReportCardcontainsthreeindices,acon-

textindex(takingintoaccountavailabilityofelectric-

ity,watersupplyandtypeoftoilets),aresourcesindex

(pupils per teacher, textbook, classroom and desk)

andaperformance index(passrate,drop-outrate,

rateofrepeaters),thatallowacomparisonofneeds

andperformancebyschool.Contrarytothecentral-

izedstatisticalyearbooks,thenewtoolalsoallowsall

actorsofthesystem(institutionalorcommunities)to

obtain information regarding their level of interven-

tion(school,sub-division,regionetc.).However,sofar

thisinformationisnotyettransferredtotheactorson

thegroundanditsusestillhastobeinstitutionalized.

Performance Monitoring

A study on governance in education (World Bank

2012a)focusingonthreeregionswithdifferentprofiles

(NorthWest,Littoral,andFarNorth) foundthat the

currentmonitoringsystemforteachersandschoolsis

weakandlacksclearlydefinedstandardsandexpec-

tations.Theexistingsystemofsanctionsandincen-

tivesisnotalwaysappliedandlacksrigorinpromoting

betterschoolperformance.Theworkofregularcivil

servant teachers in basic and secondary education

isevaluatedviaconfidentialreports,whichareunre-

latedtosectoractivities.Althoughtheworkofcontract

teachershiredbytheCenterforprimaryschoolsare

FIGURE 27: Share of Parent’s Contribution in National Expenditure for Education, 2011 (in percent)

0

20

10

30

50

40

Niger Senegal Chad Mali Congo Cameroon

Source: EducationCountryStatusReport(2013).

FIGURE 28: Reasons for Drop-outs, 2010 (in percent)

Other

Distance

Failure

Work

Lack of finance

Pregnancy/marriage

Illness

0 10 20 30

Girls

40 50 60

Boys

Source: EESI2.

FIGURE 29: Education Sector Corruption Perception Index, 2013 (Score scale 1–5, where 1 means not at all corrupt, 5 means extremely corrupt)

1

2

3

4

5

Ghan

a

Sier

ra L

eone

Zim

babw

e

Suda

n

Mad

agas

car

SSA

aver

age

Buru

ndi

Nige

ria

Sene

gal

Sout

h Su

dan

Ugan

da

Glob

al a

vera

ge

Ethi

opia

Keny

a

Sout

h Af

rica

Rwan

da

Libe

ria

Moz

ambi

que

Tanz

ania

Zam

bia

Cam

eroo

n

DRC

Mal

awi

Source: TransparencyInternational.

CAMEROON ECONOMIC UPDATE18

morecloselymonitored,thishaslittleimpactontheir

performance.Themonitoringofschoolandteacher

performanceisparticularlyweakinbasiceducation,

whilethereseemstobemoreaccountabilityinsecond-

aryeducation—likelyaresultofthenation-wideexam-

inationsthatarerequiredtobepassedbyanystudent

beforehecanmovetothenextlevelofeducation.

Sinceaccountabilityforperformanceinbasiceduca-

tion,especiallywithregardstoimprovingquality,is

imperfectattheschoollevel,thenextlevel,thesub-

division inspectorate, needs to play a critical role

in monitoring school performance. Inspectors are

expectedtovisiteachschoolseveraltimesduringthe

yearandsurprisevisitsareencouraged.However,in

practice,inspectorsfacesevereconstraintsintrav-

ellingtoschools.Theyoftendonothavetransport

and,iftheydo,theroadsareoftenbad.Mostimpor-

tant, this administrative level is seriously under-

staffed, making effective performance monitoring

adifficulttask.

Teachers

ThereisasevereshortageofteachersinCameroon,

which affects the quality of services rendered in

schools. On average, the pupil-teacher ratio is

about53,whichishighininternationalcomparison

(Figure30).Geographicaldisparitiesarepronounced

with the northern and eastern regions above the

nationalaverage(Figure31).

To address the teacher shortage, the Government

introducedtheContractTeachersProgram(CTP)in

thecontextofafreezeincivilservantrecruitmentin

Camerooninthe1990s.Initiallytheprogramwasnot

well defined and suffered from inequitable deploy-

ment, high attrition and uneven performance. In

2000, the system was revamped. The new policy

outlined salary scales, benefits, and a career path

forcontractteachers.4ThroughaWorldBanksuper-

visedGlobalPartnershipforEducationfundedproj-

ect with Agence Française de Développement co-

financingatotalof37,200qualifiedcontractteachers

were hired between 2007 and 2011, 60 percent of

them female. This resulted in improving teacher

availabilityintheZEP.Initsneweducationstrategy

theGovernmentaimsatreducingthepupil-teacher

ratio to 51 by 2016. A follow-on World Bank super-

visedGlobalPartnershipforEducationfundedproj-

ectwouldsupporttheconversionofapproximately

7,253PTAteacherstocontractteacherstatusand

FIGURE 30: Pupil-Teacher Ratio, 2011

30

20

10

0

60

40

50

Low incomecountries

Sub-SaharanAfrica

Middle incomecountries

Cameroon*

Sources: MINEDUBStatisticalYearbookandWBEducationStatistics.*2012dataforCameroon.

FIGURE 31: Pupil-Teacher Ratio by Region, 2012

0

50

40

30

20

10

80

60

70Fa

r Nor

th

North

Wes

t

Cent

er

Adam

aoua

Sout

h W

est

Cam

eroo

n

Sout

h

Litto

ral

North

Wes

t

East

2016 national target

Source: MINEDUBStatisticalYearbook.

4Thesalaryofcontractteacherswassetatapproximatelythree times the average GDP per capita and two-thirds ofregularcivilservantssalary.TheGovernmentofCameroonalsoestablishedacareerdevelopmentstrategyforcontractteachers,includingseverallevelsofpromotion.TheGovern-mentprovidesanadditionalpaymenttocontractteachersinlieuofaguaranteeofapension.Contractteachersarealsogiven similar benefits as regular civil servants, such as 18daysofleaveduringtheschoolyear.Teacherswithchildrenareentitledtotwoadditionaldaysofleaveperchild.Ifleaveisnottakenduringtheschoolyear,contractteachersareal-lowedtocumulatetheleave(civilserviceteachers,however,arenotallowedtocumulateleave).

BASIC EDUCATION IN CAMEROON 19

about1,747newrecruitsascontractteachersover

thenextfouryears.

Nevertheless, the level of teacher attrition among

CTPteachersremainshigh.Attritionhasbeenpar-

ticularlyhigh(about18percent)amongfemalecon-

tractteachersfromthesouthwhoweredeployedin

thenorthernpartofthecountry,particularlywhen

deployedtotheZEPandruralareas,wherelifecon-

ditionsforyoungandeducatedteachersaredifficult.

Attritionhasalsooccurredascontractteachershave

migrated to other ministries after being registered

ascivilservantsintheMinistryofBasicEducation.

Inadditiontowideregionaldisparities,therearewide

differenceswithinregions,withapronouncedurban/

ruraldivide.Highoverallpupil-teacherratios in the

northernregionsmaskthefactthatcertain,mainly

urbanareas,exhibitrelativelymoderatePTRswhile

insomeremoteruralareasthereisonlyoneteacher

for 150 students or more, making effective learn-

ingvirtuallyimpossible.Atthesametime,inregions

with lowoverallPTRs,pocketswithsevereteacher

shortagescontinuetoexist.Figure32illustratesthe

sub-divisionswiththehighestandthelowestpupil-

teacherratiosineachregion.Allregions,exceptthe

South, contain sub-divisions with PTRs above and

belowthenationalaverageof53andinsixregions

therearesub-divisionswithPTRsof150andabove.

Teaching materials

Primary education is also affected by a shortage

of teaching materials. Cameroon has the lowest

pupil-textbook ratio of all the countries surveyed

by UNESCO in Sub-Saharan Africa: on average

onlyoneoutoftwelvestudentshadaccesstotext-

booksin2011(Figure33).Hereagain,thenational

average masks significant regional differences. In

manydisadvantagedareas,therearenotextbooks

inclassrooms.

Thelackoftextbooksinschoolsinlinedtothesup-

ply of textbooks—a process that is controversial.

Thecurrentpracticeofdesigningtextbookssothat

students can write in them requires new books to

be purchased every year. Such a design prevents

acheapertextbookprovisionsystem,whichwould

meantheGovernmentcouldmoreeasilydeliveron

thepromiseoffreeprovision.Furthermore,pressure

frompublishershasbeenreportedforcingMinistries

to make marginal changes to the curriculum each

year,requiringinturntheprintingofneweditionsof

books.Asaresult,thechildrenwhohavebooksare

those whose parents can afford to buy them. The

FIGURE 32: Intraregional Differences in Pupil-Teacher Ratios: Sub-divisions with Highest and Lowest PTR by Region*, 2013

0

150

100

50

300

200

250

Far N

orth

North

Wes

t

Cent

er

Adam

aoua

Sout

h W

est

Sout

h

Litto

ral

North

Wes

t

East

Sub-division with lowest PTR Sub-division with highest PTR

Sources: MINEDUBSchoolReportCardandWBstaffcalculations.*Publicschoolsonly,doesnotconsiderteacherspaidbyPTAs.

CAMEROON ECONOMIC UPDATE20

rest of the children—the vast majority, especially

in the northern regions—are deprived of access to

textbooks.

Looking forward, tackling these issues would strengthen the basic education system

Improving data collection

Improved accountability will require a solid and

reliable education management information sys-

tem(EMIS).ThecurrentstatusoftheEMISisrela-

tivelyweakandofpoorquality. In thiscontext, the

Governmentanditspartnersaretakingthefollow-

ing actions to strengthen production of education

statistics:

i. UNESCO is supporting Government efforts to

createandlinkregionallycomparabledata.

ii. MINEDUBisplanningtomainstreamtheuseof

itsSchoolReportCarddatabaseaspartofthe

efforts to decentralize the education system.

Additionally, it is envisaging the geo-referenc-

ingofschoolsandlinkingthisdatatotheSchool

ReportCards.

iii. UNICEF is undertaking a pilot data collection

andschoolmappingexerciseintheZEPtocap-

ture information on various equity indicators

fromschools.Thepilotwouldresultinnewdata

being collected on refugees, disabled children,

andminoritypopulations(e.g.Baka, Mbororo).

Thedatawouldincludedistrictandschoollevel

information by gender thus allowing deeper

analysis on gender disparities, and serve as a

tool for improved planning and tracking of the

most vulnerable children (girls, ethnic minori-

ties,refugees).

PoliticalwillisessentialtoimprovetheEMIS,partic-

ularlyatsecondaryeducationlevel,andthefinancial

andtechnicalmeanstomaintainanadequateEMIS.

Thelackofcomprehensive,reliableandrecentdata

on education cannot be resolved by external inter-

ventionsalone.

Rationalizing resource allocation and improving systemic efficiency

Theongoingimprovementineducationdataprovides

theGovernmentwithanopportunitytoincreasethe

budgetforeducation,introduceefficienciesinresource

allocationanduse,andalignpublicspendingmoreeas-

ilytoneeds.Withrespecttorationalizingthedistribu-

tion of resources budget analysis shows that there

is continuous bias towards the Center and Littoral

regionsprimarilyexplainedbypoliticalconsiderations.

Targetinginvestmentsindisadvantagedareas(rural

areas,thethreenorthernregionsandtheEast,pock-

etsofunder-servedareasaroundurbancentersand

closetoborders)wouldcontributetogreaterequity

FIGURE 33: Pupil-Textbook Ratio, 2011

0

2

8

6

4

10

14

12

Seyc

helle

s

Mau

ritiu

s

Guin

ea

Beni

n

Gam

bia

Mal

i

Cape

Ver

de

Eritr

ea

Swaz

iland

Burk

ina

Faso

Nige

r

STP

Rwan

da

CAR

Moz

ambi

que

Mal

awi

Cong

o

Zam

bia

Togo

Ugan

da

Libe

ria

Buru

ndi

Chad

Cam

eroo

n

Source: UNESCOInstituteofStatistics.

BASIC EDUCATION IN CAMEROON 21

and equality of opportunity to education. The data

wouldalsoallowtheadministrationtoidentifyschools

in difficulty and take action to help these schools

improve.

TheEducationCountryStatusReportshowsthatpri-

maryeducationhasthebiggestdevelopmentimpact.It

iskeytofightilliteracyandaccountsforthebiggestshare

of education’s positive effects on income and health.

Primaryeducationisessentialtoaccessinghigherlev-

elsofeducation.Cameroonisaspiringtoconsolidateits

statusasamiddle-incomecountry.Therefore,continued

emphasisonprimaryeducationisessentialtoensure

educationforall.Atthesametime,theprimarysector

inCameroonischronicallyunderfunded.

Greater numbers of students are graduating from

primarytosecondaryeducation.Thisisthereason

forrelativelyhigherallocationtosecondaryeduca-

tion.Furthermore,secondaryeducationcurriculum

isrelativelylarge.Thishasrequiredmorenumbersof

specializedandlesspolyvalentteachers.Thismakes

secondary education quite expensive. At present

Governmentdependsonexternalgrantsforprimary

education.However,Governmenthascommittedto

increasingthebudgetforeducationandforprimary

educationspecificallyoverthecourseofthenextfew

years.Aportionofadditionalresourcesforprimary

educationcouldalsobegeneratedbyimprovingeffi-

cienciesinpublicspending.Thepolicyactionsrequire

politicalwillingnessandasupportingpoliticalecon-

omyenvironment.Finally,anyadditionalresourcesto

primaryeducationshouldbetargetedtoinputsthat

improvelearningachievements.

Assessing more systematically student learning

Thereisnonationalassessmentsframework withfor-

mativestudentlearningevaluations.Studentlearn-

ing achievement is mainly tested at the end of the

primary and secondary education cycles through

high-stakes exams. Cameroon has participated in

atleastthreeroundsoftheProgramfortheAnalysis

ofEducationSystems(PASEC)andhascarriedout

anationalEarlyGradeReadingAssessment(EGRA).

TheGovernmentiskeentoadministertheECRAonce

againandanEarlyGradeMathematicsAssessment

(EGMA). It will be important to place such assess-

ments within a more systematic national assess-

mentframeworkthatemphasizesthedevelopment

ofnationaltechnicalcapacityforassessment,wider

sharing of assessment results, and improving the

feedback loop from assessment results to those

responsibleforcurriculumandteachertraining.

Increasing budget transparency

The2012WorldBankstudyongovernanceinedu-

cationrevealedthatpublicschoolresourcesarenot

transparentlyallocatedandthatthereareinstances

of inefficient resource management. Against this

backdrop, the role of stakeholders at the regional

level will be crucial to engage in collective actions

that will promote good governance and increased

accountability.Localcommunitieswillneedtoplay

an important role in demanding schools to pub-

lishandpubliclyannouncethelevelofstatefunding

received,thetimeofreceiptoffunding,andthepro-

posedusesofthefunds.Inaddition,parents-teach-

ers’association(PTA)contributionsanduseshould

bemadepublic.

Revising textbook policy

Thenationaltextbookpolicyiscurrentlyunderrevi-

sionbyGovernmentandpublishers.Theadministra-

tionplanstograduallymovefromaprivatelyfinanced

systemtoastate-fundedsysteminwhichtheadmin-

istrationsuppliestextbooks.Thisreformwouldsig-

nificantlyimprovetheavailabilityoftextbooks,which

is considered one the most cost-effective way of

improvingthequalityoflearning.

Withinthisframework,theissueofdurabilityoftext-

bookswouldneedtobeaddressed.Inordertomake

aGovernment-financedsystemfeasible, textbooks

willhave tobereused forat least three, preferably

four years. This means that (i) the books cannot

CAMEROON ECONOMIC UPDATE22

bedesignedsothatthestudentswriteinthem;and

(ii)thattheschoolmustpreservethebookssothey

canbeissuedtothenextyearintake,andreusedin

asimilarmannerforaminimumofthreeyears.They

mustthereforebephysicallydurableenoughtolast

threetofouryears.

CAMEROON ECONOMIC UPDATE 23

REFERENCES

Institut National de la Statistique (2008), ECAM

3. Enquête Camerounaise auprès des ménages.

Tendances, profils et déterminants de la pauvreté au

Cameroun entre 2001–2007,Yaoundé.

InstitutNationaldelaStatistique,(2011),Deuxième

Enquête sur l’Emploi et le Secteur Informel (EESI 2).

Phase 1: Enquête sur l’Emploi. Rapport Principal,

Yaoundé.

InstitutNationaldelaStatistique,(2011),Deuxième

Enquête sur l’Emploi et le Secteur Informel (EESI 2).

Phase 2: Enquête sur le Secteur Informel. Rapport

Principal,Yaoundé.

République du Cameroun (2009). Document de

Stratégie pour la Croissance et l’Emploi (DSCE),

Yaoundé.

RépubliqueduCameroun(2011),Rapport provisoire

sur l’évaluation des acquis scolaires en CM1/Class

5 au Cameroun, Ministère de l’Éducation de Base,

Yaoundé.

République du Cameroun (2013a), Document

de Stratégie de l’Éducation et de la Formation,

Ministère de l’Économie, de la Plannification et de

l’AménagementduTerritoire,Yaoundé.

République du Cameroun (2013b), Le Système

d’Education et de Formation du Cameroun dans la

Perspective de l’Emergence,Yaoundé.

République du Cameroun (2013c), Maquette annu-

aire statistiques 2012. Document de travail.Ministère

d’ÉducationdeBase.Yaoundé.

République du Cameroun (2013d), Tableau de

Bord Ecole 2012/13. Document de travail.Ministère

d’ÉducationdeBase.Yaoundé

World Bank (2012a), Cameroon: Governance and

Management in the Education Sector, Washington,

D:C:

World Bank (2012b), Implementation Completion

and Results Report on a Catalytic Fund Grant for an

Education For All-Fast Track Initiative: Support to the

Education Sector,Washington,D.C.

World Bank (2013), Implementation Completion

and Results Report on a Credit to the Government of

Cameroon for an Education Development Capacity

Building Project,Washington,D.C.

Databases

Programmed’AnalysedesSystèmesÉducatifsdela

CONFEMEN (PASEC), http://www.confemen.org/

le-pasec/acces-aux-donnees-du-pasec

Transparency International Corruption Perception

Index,cpi.transparency.org

UNESCOInstituteofStatistics,www.uis.unesco.org

World Bank Education Statistics, databank.world-

bank.org

World Bank World Development Indicators, data-

bank.worldbank.org