california broker february 2016

DESCRIPTION

ÂTRANSCRIPT

VOLUME 34, NUMBER 5 SERVING CALIFORNIA’S LIFE/HEALTH PROFESSIONALS & FINANCIAL PLANNERS FEBRUARY 2016

WellnessWorkout for

BrokersShaping upYour Sales

Also Inside:Large Group Health • Disability • Sales & Marketing • Wellness • 401(k)

GA View from the Top • Private Exchanges • Life Settlements • Life Insurance

© 2016 Landmark Healthplan Inc., All Rights Reserved www.LHP-CA.com

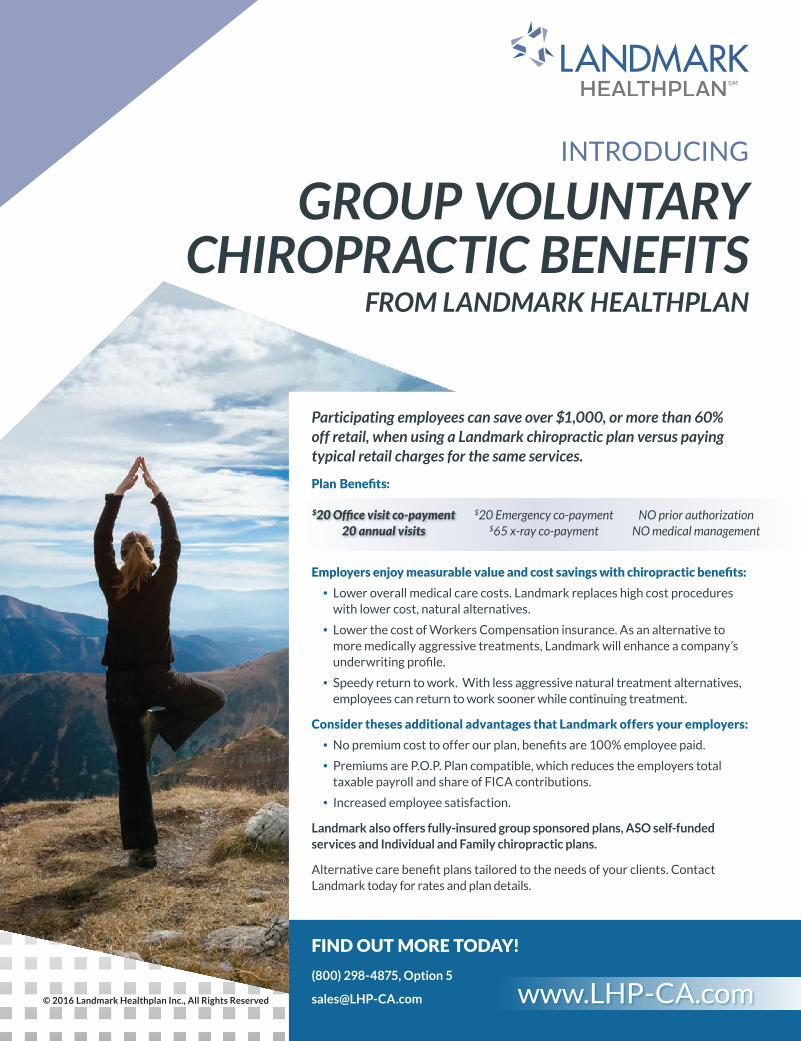

Group Voluntary ChiropraCtiC Benefits

from landmark healthplan

introduCing

Find out more today!

(800) 298-4875, Option 5

Employers enjoy measurable value and cost savings with chiropractic benefits:

Lower overall medical care costs. Landmark replaces high cost procedures with lower cost, natural alternatives.

Lower the cost of Workers Compensation insurance. As an alternative to more medically aggressive treatments, Landmark will enhance a company’s underwriting profile.

Speedy return to work. With less aggressive natural treatment alternatives, employees can return to work sooner while continuing treatment.

Consider theses additional advantages that Landmark offers your employers:

No premium cost to offer our plan, benefits are 100% employee paid.

Premiums are P.o.P. Plan compatible, which reduces the employers total taxable payroll and share of FiCA contributions.

increased employee satisfaction.

Landmark also offers fully-insured group sponsored plans, ASO self-funded services and Individual and Family chiropractic plans.

Alternative care benefit plans tailored to the needs of your clients. Contact Landmark today for rates and plan details.

$20 Office visit co-payment 20 annual visits

$20 Emergency co-payment $65 x-ray co-payment

NO prior authorization NO medical management

participating employees can save over $1,000, or more than 60% off retail, when using a landmark chiropractic plan versus paying typical retail charges for the same services.

Plan Benefits:

© 2016 Landmark Healthplan Inc., All Rights Reserved www.LHP-CA.com

Group Voluntary ChiropraCtiC Benefits

from landmark healthplan

introduCing

Find out more today!

(800) 298-4875, Option 5

Employers enjoy measurable value and cost savings with chiropractic benefits:

Lower overall medical care costs. Landmark replaces high cost procedures with lower cost, natural alternatives.

Lower the cost of Workers Compensation insurance. As an alternative to more medically aggressive treatments, Landmark will enhance a company’s underwriting profile.

Speedy return to work. With less aggressive natural treatment alternatives, employees can return to work sooner while continuing treatment.

Consider theses additional advantages that Landmark offers your employers:

No premium cost to offer our plan, benefits are 100% employee paid.

Premiums are P.o.P. Plan compatible, which reduces the employers total taxable payroll and share of FiCA contributions.

increased employee satisfaction.

Landmark also offers fully-insured group sponsored plans, ASO self-funded services and Individual and Family chiropractic plans.

Alternative care benefit plans tailored to the needs of your clients. Contact Landmark today for rates and plan details.

$20 Office visit co-payment 20 annual visits

$20 Emergency co-payment $65 x-ray co-payment

NO prior authorization NO medical management

participating employees can save over $1,000, or more than 60% off retail, when using a landmark chiropractic plan versus paying typical retail charges for the same services.

Plan Benefits:

800.542.4218 calchoice.com

A health care partner for California brokers and businesses for two decades.

Celebrating 20 years of Choice.

10

14

26

16

15

24

29

31

36

38

33

40

- CalBrokerMag.com -4 | CALIFORNIA BROKER FEBRUARY 2016

ALSO IN THIS ISSUE:

LARGE GROUP HEALTH

Navigating the 101 and Beyondby Michael Wolff

Brokers who are not selling in the large-group space may want to think again. Agents are finding many large groups with no prior coverage.

Opportunities Abound for Agents in the New Large Group Market

by Neil CrosbyThe year 2016 will truly

be a year of growth for agents and

brokers with limitless opportunity.

SALES & MARKETING

Win Today or Relevance Tomorrow How the Power of Consultative Sell-ing Can Help You Grow Your Business

by Jim McCabeHelpful tips for weaving consultative selling into your daily conversations to become more valued among clients.

GA VIEW FROM THE TOP

by Leila MorrisGeneral agen-cy executives give their take on challenges and opportuni-ties in today’s market.

DISABILITY

Why Millennials Make Attractive Disability Insurance Prospects

by Jim FardenDon’t miss out on the opportu-nity to target Millennials for income protection solutions.

WELLNESS

Finding a Work-place Wellness Program Fit for Every Client

by Heidi BowmanMore employers un-derstand the benefits of moving to a holistic wellness strategy.

Helping Employers Maximize the Return on Investment in Wellness

by Dinesh ShethHow employers can increase the ROI from their wellness investments.

PRIVATE EXCHANGES

An Option for the Futureby Dorothy Miraglia King

Is a private exchange part of your client’s benefit strategy? If not, you may want to consider it.

The Next Health ExchangesHave Already Been Built

by Joel WhiteCongress has an op-portunity to modify the exchange system to engage consumers.

LIFE SETTLEMENTS

A Primer for Healthy Insuredsby Robert Stark

Why a life settlement (traditional or no LE) can be a great option in certain circumstances.

LIFE INSURANCE

Trends That Are Shaping Today’s Wealth Transfer Policies

by Palmer WilliamsClients who’ve been hesitant to use life insur-ance for wealth transfer can now enjoy the benefits and maintain control of the policy.

401(K)

New Regulations for Employersby Ellen Bartholemy

Brokers need to understand the latest regu-lations and guidelines when selling 401(k)s and other qualified retirement plans.

Guest Editorial .........................6Annuity Sampler .....................8New Products ...................... 35

News ....................................... 42Classified Advertising ....... 46Ad Index ................................. 46

PUBLISHERRic Madden

email: [email protected]

EDITOR-IN-CHIEFKate Kinkade, CLU, ChFC

email: [email protected]

SENIOR EDITORLeila Morris

email: [email protected]

ART DIRECTOR/PRODUCTION MANAGERSteve Zdroik

ADVERTISINGScott Halversen, V.P. Mktg.

email: [email protected]

CIRCULATIONemail: [email protected]

BUSINESS MANAGERLexena Kool

email: [email protected]

LEGAL EDITORPaul Glad

EDITORIAL AND PRODUCTION:McGee Publishers

217 E. Alameda Ave. #207Burbank, CA 91502

Phone No.: 818-848-2957email: [email protected].

Subscriptions and advertising rates, U.S. one year: $42. Send change of address notification at least 20 days prior to effective date; include old/new address to: McGee Publishers, 217 E. Alameda Ave. #207, Burbank, CA 91502. To subscribe online: calbrokermag.com or call (800) 675-7563.

California Broker (ISSN #0883-6159) is published monthly. Periodicals Postage Rates Paid at Burbank, CA and additional entry offices (USPS #744-450). POSTMASTER: Send address changes to California Broker, 217 E. Alameda Ave. #207, Burbank, CA 91502.

©2016 by McGee Publishers, Inc. All rights reserved. No part of this publication should be reproduced without consent of the publisher.

No responsibility will be assumed for unsolicited editorial contributions. Manuscripts or other material to be returned should be accompanied by a self-addressed stamped envelope adequate to return the material.

The publishers of this magazine do not assume responsibility for statements made by their advertisers or contributors. Printed and mailed by Southwest Offset Printing, Gardena, CA.

FEBRUARY 2016

TABLE OF CONTENTS

• Electronic Enrollment and Benefits Administration• ACA Tracking • Optional 1094/1095 Reporting for a Nominal PEPM Fee• Employer/Employee Interface• Renewal Marketing and Commission Tracking

Call Today for More Information

(800) [email protected]

Protect and Grow Your Book at No Cost to You or Your Clients

Powerful Solutions for Power Brokers

If you knew how much time you could save with electronic enrollment...

you would go through anything to get it.

License #0F69768

www.thebrokersga.com

- CalBrokerMag.com -6 | CALIFORNIA BROKER FEBRUARY 2016

GUEST EDITORIAL

SIGN NEW BUSINESSGET FREE MARKETING

Covered California for Small Business helps you sell health insurance plans to small businesses in California. And we’re not just talking ideas. It’s materials and resources.

For every group you sign with 10 employees or more, you get a mailing of 1000 FREE POSTCARDS — including customization, printing, postage and a prospect list. You choose one of our professionally designed postcards and we take care of the rest!

Call today to learn how to order your free [email protected](844) 332-8384

SPECIAL OFFER!

Looking for more choices for your health plan?

SHOP.postcards.2015.newlogo.indd 9

4/30/15 11:09 AM

Health care has emerged as one of the flash points in the Democratic presidential race.

Vermont Sen. Bernie Sanders has been a longtime supporter of a concept he calls “Medicare for All,” a health system that falls under the heading of “single-payer.”

Sanders released more details about his proposal shortly be fore the Democratic debate in South Carolina. “What a Medicare-for-All program does is finally provide in this country health care for every man, woman and child as a right,” he said in Charleston.

Sanders’ main rival for the nomination, former Secretary of State Hillary Clinton, has criticized the plan for raising taxes on the middle class and said it is politically unattainable. “I don’t want to see us start over again with a contentious debate” about health care, she said.

Some of the details of Sanders’ plan are still to be released. But his proposal has renewed questions about what a single-payer health care system is and how it works. Here are some quick answers.

WHAT IS SINGLE-PAYER?Single-payer is not the same thing as socialized medicine. In a truly socialized medicine system, the government not only pays the bills, but also owns the health care facilities and em-ploys the professionals who work there.

The Veterans Health Administration (VA) is an example of a socialized health system run by the government. It owns the hospitals and clinics and pays the doctors, nurses and other health providers.

Medicare, on the other hand, is a single-payer system in which the federal government pays the bills for those who qualify, but hospitals and other providers remain private.

WHICH COUNTRIES HAVESINGLE-PAYER HEALTH SYSTEMS?Fewer than many people think. Most European countries never had or no longer have single-payer systems. “Most are basically what we call social insurance systems,” said Gerard Anderson, a professor at Johns Hopkins Bloomberg School of Public Health, who has studied international health systems. Social insurance programs ensure that almost everyone is covered. They are tax-payer-funded but are not necessarily run by the government.

Germany, for example, has 135 “sickness funds,” which are essentially private, nonprofit insurance plans that negoti-ate prices with health care providers. “So you have 135 funds to choose from,” Anderson said.

Nearby, Switzerland and the Netherlands require their resi-dents to have private insurance (just like the Affordable Care Act does), with subsidies to help those who cannot other-wise afford coverage.

And while conservatives in the United States often use Great Britain’s National Health Service as the poster child for a socialized system, there are many private insurance options available to residents there, too.

Among the countries that have true single-payer systems, Anderson lists only two — Canada and Taiwan.

ARE SINGLE-PAYER PLANS LESS EXPENSIVE THAN OTHER HEALTH COVERAGE SYSTEMS?Not necessarily. True, eliminating the profits and duplicative administrative costs associated with hundreds of different private insurance plans would reduce spending, perhaps as much as 10% of the nation’s $3 trillion annual health care bill, Anderson said. But, he noted, once that savings is achieved, there won’t be further reductions in following years.

More important, as many analysts have noted, is how much health services cost and how those prices are determined. In most other developed countries, even those with private insur-ance, writes Princeton Health Economist Uwe Reinhardt, prices “either are set by government or negotiated between associa-tions of insurers and providers of care on a regional, state or na-tional basis.” By contrast, in the U.S., “The payment side of the health care market in the private sector is fragmented, weaken-ing the bargaining power of individual insurers.”

WOULD MEDICARE FOR ALL BE JUST LIKE THE EXIST-ING MEDICARE PROGRAM?No, at least not as Sanders envisions it. Medicare is not nearly as generous as many people think. Between premiums (for doctor and drug coverage), cost-sharing (deductibles and coinsurance) and items Medicare does not cover at all (most dental, hearing and eye care), the average Medicare beneficiary still devotes an estimated 14% of all household spending to health care.

Sanders’ plan would be far more generous, including dental, vision, hearing, mental health and long-term care, all without copays or deductibles (which has given rise to a lively debate about how to pay for it and whether middle-class families will save money or pay more).

WOULD PRIVATE INSURANCE COMPANIES REALLY DISAPPEAR UNDER SANDERS’ PLAN?Probably not. Private insurers are fully integrated into Medicare, handling most of the claims processing and providing supple-mental coverage through “Medigap” plans. In addition, nearly a third of Medicare beneficiaries are enrolled in private managed care plans as part of the Medicare Advantage program.

Creating an entirely new federal claims processing structure would in all likelihood be more expensive than continuing to contract with private insurance companies. However, Sanders makes it clear insurers in the future would no longer be the risk-bearing entities they are today, but more like regulated utilities. H

Julie Rovner, the Robin Toner Distinguished Fellow, joined Kaiser Health Network after 16 years as health policy correspondent for NPR, where she helped lead the network’s coverage of the passage and implementation of the Affordable Care Act. A noted expert on health policy issues, Rovner is the author of a critically-praised reference book Health Care Politics and Policy A-Z, now in its third edition.

DEMOCRATIC CANDIDATES DEBATE “SINGLE-PAYER,” BUT WHAT DOES THAT MEAN? By JULIE ROVNER for KHN.ORG

SIGN NEW BUSINESSGET FREE MARKETING

Covered California for Small Business helps you sell health insurance plans to small businesses in California. And we’re not just talking ideas. It’s materials and resources.

For every group you sign with 10 employees or more, you get a mailing of 1000 FREE POSTCARDS — including customization, printing, postage and a prospect list. You choose one of our professionally designed postcards and we take care of the rest!

Call today to learn how to order your free [email protected](844) 332-8384

SPECIAL OFFER!

Looking for more choices for your health plan?

SHOP.postcards.2015.newlogo.indd 9

4/30/15 11:09 AM

- CalBrokerMag.com -8 | CALIFORNIA BROKER FEBRUARY 2016

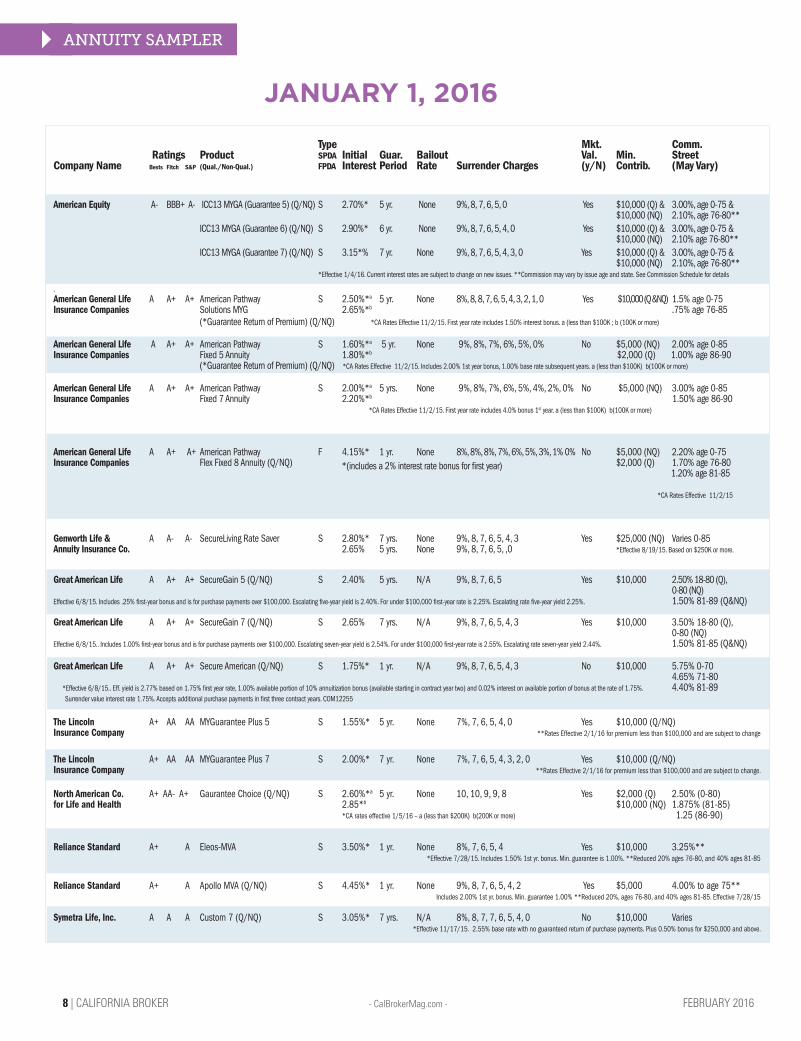

ANNUITY SAMPLER

Type Mkt. Comm. Ratings Product SPDA Initial Guar. Bailout Val. Min. StreetCompany Name Bests Fitch S&P (Qual./Non-Qual.) FPDA Interest Period Rate Surrender Charges (y/N) Contrib. (May Vary)

American Equity A- BBB+ A- ICC13 MYGA (Guarantee 5) (Q/NQ) S 2.70%* 5 yr. None 9%, 8, 7, 6, 5, 0 Yes $10,000 (Q) & 3.00%, age 0-75 & $10,000 (NQ) 2.10%, age 76-80** ICC13 MYGA (Guarantee 6) (Q/NQ) S 2.90%* 6 yr. None 9%, 8, 7, 6, 5, 4, 0 Yes $10,000 (Q) & 3.00%, age 0-75 & $10,000 (NQ) 2.10% age 76-80** ICC13 MYGA (Guarantee 7) (Q/NQ) S 3.15*% 7 yr. None 9%, 8, 7, 6, 5, 4, 3, 0 Yes $10,000 (Q) & 3.00%, age 0-75 & $10,000 (NQ) 2.10%, age 76-80** *Effective 1/4/16. Current interest rates are subject to change on new issues. **Commission may vary by issue age and state. See Commission Schedule for details

.American General Life A A+ A+ American Pathway S 2.50%*a 5 yr. None 8%, 8, 8, 7, 6, 5, 4, 3, 2, 1, 0 Yes $10,000 (Q &NQ) 1.5% age 0-75Insurance Companies Solutions MYG 2.65%*b .75% age 76-85 *CA Rates Effective 11/2/15. First year rate includes 1.50% interest bonus. a (less than $100K ; b (100K or more)

American General Life A A+ A+ American Pathway S 1.60%*a 5 yr. None 9%, 8%, 7%, 6%, 5%, 0% No $5,000 (NQ) 2.00% age 0-85Insurance Companies Fixed 5 Annuity 1.80%*b $2,000 (Q) 1.00% age 86-90 *CA Rates Effective 11/2/15. Includes 2.00% 1st year bonus, 1.00% base rate subsequent years. a (less than $100K) b(100K or more)

American General Life A A+ A+ American Pathway S 2.00%*a 5 yrs. None 9%, 8%, 7%, 6%, 5%, 4%, 2%, 0% No $5,000 (NQ) 3.00% age 0-85Insurance Companies Fixed 7 Annuity 2.20%*b 1.50% age 86-90 *CA Rates Effective 11/2/15. First year rate includes 4.0% bonus 1st year. a (less than $100K) b(100K or more)

American General Life A A+ A+ American Pathway F 4.15%* 1 yr. None 8%, 8%, 8%, 7%, 6%, 5%, 3%, 1% 0% No $5,000 (NQ) 2.20% age 0-75 Insurance Companies Flex Fixed 8 Annuity (Q/NQ) $2,000 (Q) 1.70% age 76-80 1.20% age 81-85 *CA Rates Effective 11/2/15

Genworth Life & A A- A- SecureLiving Rate Saver S 2.80%* 7 yrs. None 9%, 8, 7, 6, 5, 4, 3 Yes $25,000 (NQ) Varies 0-85Annuity Insurance Co. 2.65% 5 yrs. None 9%, 8, 7, 6, 5, ,0 *Effective 8/19/15. Based on $250K or more.

Great American Life A A+ A+ SecureGain 5 (Q/NQ) S 2.40% 5 yrs. N/A 9%, 8, 7, 6, 5 Yes $10,000 2.50% 18-80 (Q), 0-80 (NQ) Effective 6/8/15. Includes .25% first-year bonus and is for purchase payments over $100,000. Escalating five-year yield is 2.40%. For under $100,000 first-year rate is 2.25%. Escalating rate five-year yield 2.25%. 1.50% 81-89 (Q&NQ)

Great American Life A A+ A+ SecureGain 7 (Q/NQ) S 2.65% 7 yrs. N/A 9%, 8, 7, 6, 5, 4, 3 Yes $10,000 3.50% 18-80 (Q), 0-80 (NQ) Effective 6/8/15.. Includes 1.00% first-year bonus and is for purchase payments over $100,000. Escalating seven-year yield is 2.54%. For under $100,000 first-year rate is 2.55%. Escalating rate seven-year yield 2.44%. 1.50% 81-85 (Q&NQ) Great American Life A A+ A+ Secure American (Q/NQ) S 1.75%* 1 yr. N/A 9%, 8, 7, 6, 5, 4, 3 No $10,000 5.75% 0-70 4.65% 71-80 *Effective 6/8/15.. Eff. yield is 2.77% based on 1.75% first year rate, 1.00% available portion of 10% annuitization bonus (available starting in contract year two) and 0.02% interest on available portion of bonus at the rate of 1.75%. 4.40% 81-89 Surrender value interest rate 1.75%. Accepts additional purchase payments in first three contract years. COM12255

The Lincoln A+ AA AA MYGuarantee Plus 5 S 1.55%* 5 yr. None 7%, 7, 6, 5, 4, 0 Yes $10,000 (Q/NQ)Insurance Company **Rates Effective 2/1/16 for premium less than $100,000 and are subject to change

The Lincoln A+ AA AA MYGuarantee Plus 7 S 2.00%* 7 yr. None 7%, 7, 6, 5, 4, 3, 2, 0 Yes $10,000 (Q/NQ)Insurance Company **Rates Effective 2/1/16 for premium less than $100,000 and are subject to change.

North American Co. A+ AA- A+ Gaurantee Choice (Q/NQ) S 2.60%*a 5 yr. None 10, 10, 9, 9, 8 Yes $2,000 (Q) 2.50% (0-80)for Life and Health 2.85*b $10,000 (NQ) 1.875% (81-85) *CA rates effective 1/5/16 – a (less than $200K) b(200K or more) 1.25 (86-90)

Reliance Standard A+ A Eleos-MVA S 3.50%* 1 yr. None 8%, 7, 6, 5, 4 Yes $10,000 3.25%***Effective 7/28/15. Includes 1.50% 1st yr. bonus. Min. guarantee is 1.00%. **Reduced 20% ages 76-80, and 40% ages 81-85

Reliance Standard A+ A Apollo MVA (Q/NQ) S 4.45%* 1 yr. None 9%, 8, 7, 6, 5, 4, 2 Yes $5,000 4.00% to age 75**Includes 2.00% 1st yr. bonus. Min. guarantee 1.00% **Reduced 20%, ages 76-80, and 40% ages 81-85. Effective 7/28/15

Symetra Life, Inc. A A A Custom 7 (Q/NQ) S 3.05%* 7 yrs. N/A 8%, 8, 7, 7, 6, 5, 4, 0 No $10,000 Varies*Effective 11/17/15. 2.55% base rate with no guaranteed return of purchase payments. Plus 0.50% bonus for $250,000 and above.

JANUARY 1, 2016

(*Guarantee Return of Premium) (Q/NQ)

*(includes a 2% interest rate bonus for first year)

(*Guarantee Return of Premium) (Q/NQ)

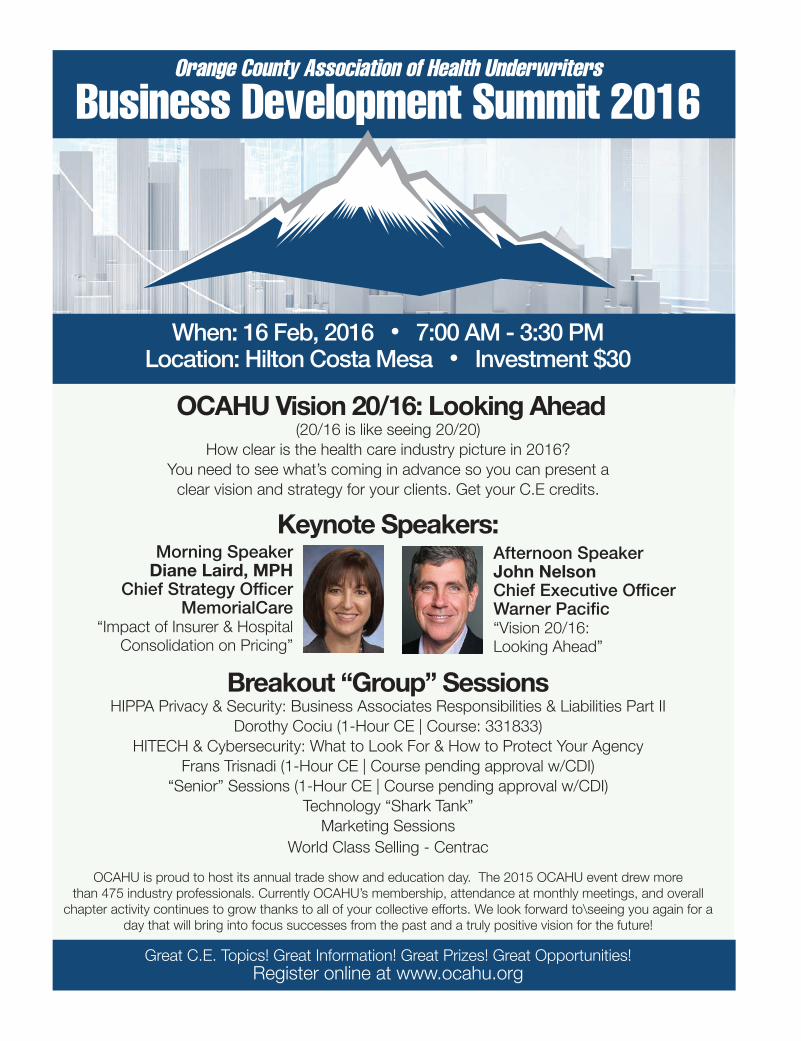

Orange County Association of Health Underwriters

Business Development Summit 2016

When: 16 Feb, 2016 • 7:00 AM - 3:30 PMLocation: Hilton Costa Mesa • Investment $30

OCAHU Vision 20/16: Looking Ahead(20/16 is like seeing 20/20)

How clear is the health care industry picture in 2016?You need to see what’s coming in advance so you can present a

clear vision and strategy for your clients. Get your C.E credits.

Keynote Speakers:

Breakout “Group” SessionsHIPPA Privacy & Security: Business Associates Responsibilities & Liabilities Part II

Dorothy Cociu (1-Hour CE | Course: 331833)HITECH & Cybersecurity: What to Look For & How to Protect Your Agency

Frans Trisnadi (1-Hour CE | Course pending approval w/CDI)“Senior” Sessions (1-Hour CE | Course pending approval w/CDI)

Technology “Shark Tank”Marketing Sessions

World Class Selling - Centrac

OCAHU is proud to host its annual trade show and education day. The 2015 OCAHU event drew morethan 475 industry professionals. Currently OCAHU’s membership, attendance at monthly meetings, and overall

chapter activity continues to grow thanks to all of your collective efforts. We look forward to\seeing you again for aday that will bring into focus successes from the past and a truly positive vision for the future!

Great C.E. Topics! Great Information! Great Prizes! Great Opportunities!Register online at www.ocahu.org

Morning SpeakerDiane Laird, MPH

Chief Strategy OfficerMemorialCare

“Impact of Insurer & HospitalConsolidation on Pricing”

Afternoon SpeakerJohn NelsonChief Executive OfficerWarner Pacific“Vision 20/16:Looking Ahead”

- CalBrokerMag.com -10 | CALIFORNIA BROKER FEBRUARY 2016

HEALTHCARE

No, this is not a travel log recant-ing my last vacation along the beautiful California coast. In-

stead, it’s a basic guide to selling in the large group (101 and over) market along with some reflections on recent trends.

Brokers who are not selling in this space may want to think again. Agents are finding that there are more large groups with no prior coverage than they may have thought. The Employer Shared Responsibility rules within the ACA have brought these groups out of hiding as they face penalties for not of-fering coverage that is affordable and of minimum value.

Although the small group market continues to experience many chang-

es that require a broker’s guidance, there is more opportunity than ever to help large employers make sound decisions for their companies and em-ployees. There are several differences between marketing a small and a large group. Brokers should keep these in mind as they equip themselves to bring the right solutions to the table.

DO YOUR HOMEWORKA broker who is developing a large group request for proposal (RFP) for a prospect is a bit like an attorney who is preparing for a trial. The research, attention to detail, and time spent de-veloping your case have a direct effect on the outcome. So, not only do your homework, but also you need to start

early – not days or weeks, but months ahead of the requested effective date. Depending on the size of the group, 90 to 100 days is a good benchmark.

The process of formulating a large-group quote is quite different from that in the small-group market. Most nota-bly, the underwriting of a large group is done up front before a quote is re-leased by a carrier. This means that the time spent gathering an accurate census and the required information/documentation happens before you even see a rate. (Yes, health condi-tions play a large part in determining rates as do current and anticipated par-ticipation, age, gender, home zip code, and industry). In general, the more information that is gathered, includ-ing claims and rate history, the greater the chance there is of getting the best possible rates.

Successful brokers know that the key to a large-group strategy that meets budgetary and coverage needs is asking the right questions of their prospects and listening carefully to the answers before they develop a proposal. The ACA has created a whole new set of questions that need to be answered to determine who is eligible for coverage and whether an employer is part of a larger population by virtue of common ownership and/or tax law. Many times, the composi-tion of a group may not be what you or even the owner thinks. At this stage, a large group qualifying questionnaire or checklist can be your greatest asset.

CHECK YOUR FACTSOnce you have a complete census for your prospect and have gathered information about current coverage

Navigating the101 and Beyond

BY MICHAEL WOLFF

A BASIC GUIDE TO SELLING IN THE LARGE GROUP (101 & OVER) MARKET

2016–25th ANNUAL IEAHU SALES SYMPOSIUMMarch 10, 2016–Ontario Convention CenterFantastic Speaker Line-up!!!!

The Highway Has Changed, What Road Are You On?

Date: Thursday, March 10, 2016Time: 7:00am to 3:30pm

Where: Ontario Convention Center 2000 Convention Center Way, Ontario, CA

Cost: If Purchased by 03/03/16:Member–$45, Non-Member–$75Purchased day of Symposium:Member–$75, Non-Member–$100

PriceIncludes:

Continental Breakfast& Lunch and earn

CE Credits for attending

Register On-Line Today: http://guestli.st/400125

Phone: 866-922-8387 Email: [email protected]

- CalBrokerMag.com -12 | CALIFORNIA BROKER FEBRUARY 2016

HEALTHCARE

for groups who have a plan in place (renewal, benefit summaries, etc.), put on your underwriter hat and look for details that don’t add up or simply don’t make sense. These include dis-crepancies between the renewal and the census, invalid dates of birth and/or home zip codes, and the absence of any large claims data. It is best that you find them before you submit your RFP to the carrier rather than waiting until later in the game when they are requested of you. This also may help your chances of getting a quote when more than one broker presents the group to the carrier – a.k.a. “duplicate activity.” Carriers will be more willing to release a quote when the facts are clear and complete.

PREPARE YOUR STRATEGY A very successful large group agent in the Inland Empire once told me that an RFP without a sound strategy is tan-tamount to throwing spaghetti against the wall to see whether it will stick. And any of the best large group car-rier reps will always ask for the story of why the group is shopping (better ben-efits, lower rates, ACA compliance) and what you believe to be the best combination of products to meet their needs. Be prepared to answer these all-important questions by using what you learned during your initial pros-pect meetings, including any special circumstances surrounding the group (e.g. controlled group status, large vari-ances in employee wages).

There are a lot of good options out there for large groups. Your prospect may want to consider a fully insured program, partial or full self-insurance and/or a minimum essential coverage (MEC) plan combined with critical ill-ness and hospital indemnity plans.

Self-insurance is on the rise, as Employer Shared Responsibility rules leave companies in search of an afford-able option to increase participation in the plan. With this option, remember to always do your due diligence before you select a claims payer or third-party administrator (TPA).

Groups looking for a bundling of em-ployee benefits and additional servic-es such as HR, compliance, workers’ compensation or payroll alongside em-ployee benefits may want to consider

PEOs or private exchanges. Many of these services can also be added to core medical offerings through a bun-dled technology solution.

The service and account manage-ment strategy is of equal importance when marketing large groups. Who is the point person? Who is the service person? Where does the buck stop? These important staffing decisions cannot be overlooked when managing the expectations of a large employer.

Finally, be prepared with a plan of how you are going to generate revenue. Will you adopt a fee-based model or ask that commissions be built into the rates?

You are ready to submit your RFP to the carriers of your choosing when you have examined all of the angles and anticipated most of the questions you may be asked during the underwriting process.

BE READY WITH PLAN BWhat if, despite your best efforts as outlined above, the quote comes back and you find that your prospect is not a good fit for your proposed strategy? If your prospect has not had prior cov-erage and, like many, is striving for ACA compliance, perhaps a two-year strategy is in order. Employers that have never paid a portion of their em-ployees’ benefit premium are suffering from sticker shock even when present-ed with very competitive rates. Simi-larly, employees who are contemplat-ing the purchase of medical insurance for the first time have a very different understanding of affordability than that which is derived from the calculators.

As agents try to balance all of the moving pieces to keep their prospects away from penalties, provide employ-ees with meaningful benefits and not break the budget, many find them-selves putting one solution in place for year one, with an end goal of achieving a different solution in year two.

Remember, too, that in addition to having a second strategy, coverage op-tion, or funding mechanism in mind, there may be room for negotiation with carriers when it comes to holding rates for the next effective date, reducing commission in order to lower rates, or writing a short or long contract to achieve the group’s ideal effective date during year two.

EXPLAIN THE OPTIONSTHOROUGHLYBusiness owners and their staffs know their industries, for certain, but often they neither speak the language of employee benefits nor have a realis-tic idea of what benefits cost. Because carriers can and do re-rate groups if as-sumptions regarding the census, par-ticipation or the health of the group are different than the actual enrollment, your thorough review with the pros-pect must include the what-ifs.

You know your prospect better than anyone does. If you know that the decision-maker may take a while mull-ing over the options, don’t expect to be able to close the deal in a couple of weeks. Avoid putting the group through a rushed enrollment only to find out that you cannot meet partici-pation or have missed the cutoff date to submit your case.

READY, SET, GONew to selling in the large group mar-ket? General agencies employ spe-cialists who are skilled at guiding you through each of the steps above in order to help you complete the sale and provide your clients with the best products and services for their particu-lar needs and budgets.

When you have done an outstanding job for your prospects, remember to be actively involved throughout the year with any and all that turn into clients and revisit next year those you were not able to convert. Remember, too, that business owners know other busi-ness owners and decision-makers, so don’t forget to ask for referrals to keep your large group pipeline full. H

Michael Wolff is president of Dickerson Employee Benefits, a general agency serving brokers and their clients for the past 50 years. A graduate of Germany’s Albert Ludwig University of Freiburg, Wolff holds a law degree with qualification as a superior court judge in Stuttgart. Before joining Dickerson in 2005, he was recruited into the German Diplomatic Service where he headed the legal, press and cultural divisions in several countries, ending with a post that brought him to California with the Los Angeles German Consulate. Dickerson Employee Benefits is headquartered near Dodger Stadium in Los Angeles and offers employee benefits and worker’s compensation products, con-cierge service and technology tools. Wolff can be reached at [email protected].

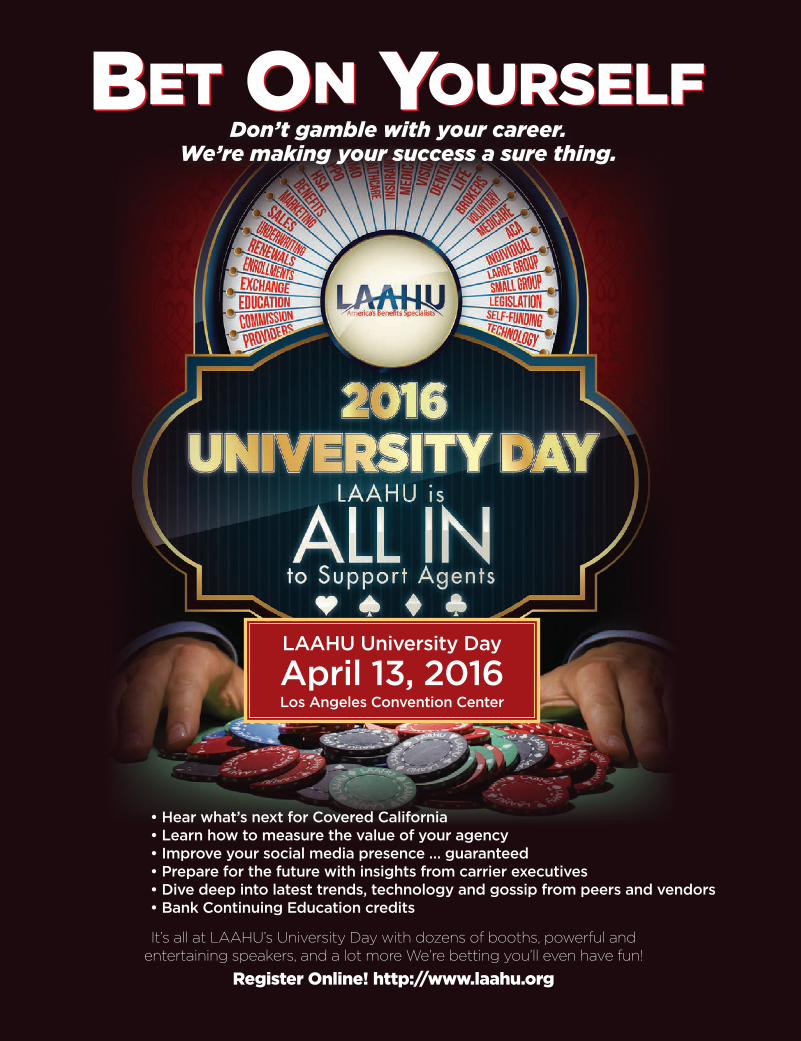

• Hear what’s next for Covered California• Learn how to measure the value of your agency• Improve your social media presence … guaranteed• Prepare for the future with insights from carrier executives• Dive deep into latest trends, technology and gossip from peers and vendors• Bank Continuing Education credits

Bet On YOurselfBet On YOurselfDon’t gamble with your career.

We’re making your success a sure thing.

LAAHU University Day

April 13, 2016Los Angeles Convention Center

It’s all at LAAHU’s University Day with dozens of booths, powerful andentertaining speakers, and a lot more We’re betting you’ll even have fun!

Register Online! http://www.laahu.org

- CalBrokerMag.com -14 | CALIFORNIA BROKER FEBRUARY 2016

HEALTHCARE

and publications, and providing links to valuable resources. Agents and bro-kers also offer professional relation-ships that come from their experience and connections.

All of the ACA provisions suggest that agents and brokers have new opportunities to retain and grow their large-group business, including the IRS requirements as well as the new size guidelines for large employers.

The fact that large groups can no longer be declined for pre-existing health conditions is a huge plus, which opens many doors. Another opportu-nity is that carriers are allowing lower participation, so employers who have not been able to meet normal partici-pation requirements may now be able

to qualify for a large-group plan.As you are aware, the ACA’s Cadil-

lac Tax has been delayed another two years, which will push it away another four years from now. There is a good chance that it will be repealed com-pletely. Employers who were worried about having more expensive plan designs needn’t worry about that for the time being. That’s great news for

agents and brokers. They no longer have to help clients select reduced benefit plans for employees and their dependents in order to stay under the allowed premium maximums and avoid the 40% excise tax on premium amounts over the allowed thresholds.

There is another provision that af-fects large-group verses small-group premiums. Large group claims ex-perience is subject to an 85% MLR, verses the 80% MLR for small group and individual. Of course, all of this is borne by the carriers, not the employ-ers, but it leaves carriers a lower mar-gin for error with many large-group employers. It will give carriers more flexibility with rates in the expanding small-group market.

Overall, it’s increasingly clear to all employers, whether small group or large group, that they need help. They

need their professional agent/bro-ker. They are keenly aware that

they need assistance from a professional – someone who deals with the ACA on a daily

basis, can guide them without crossing the line of providing legal

advice, and help them go back to running their busi-ness when they have the confidence that their benefit needs are in order. Many employers have told

me that their confidence rises tremendously if their advi-

sor is a member of a professional association, such as the Califor-nia Association of Health Under-writers (CAHU) or the National Association of Insurance and

Financial Advisors (NAIFA). Em-ployers have found that agents and

brokers who are members of these great organizations are more prepared, receive more information, and can of-fer more pertinent advice than can most of those who are not members.

The year 2016 will truly be a year of growth for agents and brokers with lim-itless opportunity. Keep reading, learn-ing, and investing in yourself for your future; it will pay off big time for you in this ever-changing marketplace. H

Neil Crosby is director of Sales for Warner Pacific General Agency.

The year 2016 is a year of change for California’s smaller large-group employers. As you know,

the ACA has changed every-thing in the minds of many employers that fall into the 51+ size margins. Employ-ers with 51 to 100 employ-ees had been in the mid-market, large-group segment. But they are preparing for the fact that they are now small-group employers. Or they kicked the can down the road one last time and will have to deal with the new provisions at the end of 2016.

Meanwhile, large-group employers are still trying to determine what the ACA provisions mean to them. They are looking at having to comply with the pay-or-play employer mandate that requires them to provide minimum-essential coverage to employees, comply with new IRS tax reporting documents, and comply with many other ACA provisions. What is certain is that large employers, throughout California, are searching for meaning-ful, relevant information to determine what they need to do moving forward.

They need their agent/broker to pro-vide information and direct them down the path of health care reform, such as giving verbal advice, providing articles

OPPORTUNITIES ABOUND FOR

AGENTS IN THE NEW LARGE

GROUP MARKETBY NEIL CROSBY

- CalBrokerMag.com -FEBRUARY 2016 CALIFORNIA BROKER | 15

SALES & MARKETING

Win Today or Relevance TomorrowHOW THE POWER OF CONSULTATIVE SELLING CAN HELP YOU GROW YOUR BUSINESS

Many brokers and agents in California are meeting with their sales managers to kick

off a whole new year of big, intimidat-ing goals. We all have different goals, whether it’s achieving a giant sales number, learning a new product, or adding a new territory. This article will give you tips for weaving consul-tative selling into your daily conversa-tions to become more valued among clients and prospects to meet your 2016 goals.

WHAT CLIENTS WANTIt’s pretty simple why our clients chose us as their agent or broker. They want our expert help. They are too busy to do the research, compare pricing, and stay on top of legislation; they expect their agent or broker to do it for them.

Our clients also expect us to un-derstand their business. We need to know their operations, their competi-tors, their pain points, and their suc-cesses. As their agent or broker, it’s up to us to know their financial and busi-ness structure, their challenges, their competitors, and their goals.

Consider helping your clients from a holistic business perspective. For ex-ample, are they trying to fill a specific position? Help them network. Are they running into a contractual challenge? Recommend legal counsel. A little ef-fort will create trust, and enhance the business relationship, which will pay off for everyone in the long run.

ASK QUESTIONS How do you become more consulta-tive? Ask questions beyond what you need to get your job done. Find out what problems your client is trying to solve today and in the next three to five years. What pain points are the cli-ent’s problems creating? Do the prob-lems span multiple departments or lo-cations? Are the problems increasing? Are there competing issues?

HOW DOES YOUR CLIENT OR PROSPECT MAKE DECISIONSWho is the decision-maker? Your con-tact may be in human resources or fi-nance, but are there other stakeholders in the mix? Since every company is dif-ferent, make sure that your sales pre-sentations speak to the full audience ahead of time. It is 100% acceptable to ask who will be reviewing your propos-als. It is 100% acceptable to ask if there are questions or areas you should cover in order to satisfy all parties, even those who won’t be present at your meeting.

Know your client or prospect’s cul-ture. When you present a solution, il-lustrate how it ties into their culture. Doing so will strengthen your offering, and show that you not only understand their culture, but also that you care about why it is critical to their success. That’s the sign of a true business part-ner, not just a transactional vendor.

COST VERSUS VALUEIn any industry, most buyers fall into two categories: those who value cost and those who value quality and ser-vice. The problem with buyers who val-ue cost is that there is always a lower cost option. Always. Clients who only value cost will leave you at renewal if a cheaper option comes along.

Be respectful of your own time, and seek clients who are looking for a long-term business partner. How? When you present your solution, show that you’ve done your research. Show them the math, not only for the sale, but also to show how it could save money in the long run or for employ-ees. Show the additional benefits of your solution. Maybe it’s a tax benefit, increased employee communication and engagement, or something that could help human resources improve morale. If possible, offer evidence in favor of your solution. If you are of-fering something that will save em-ployees money, demonstrate it with a graph or calculator.

RESEARCH IS CRITICALTO UNDERSTANDINGAdjust your message to your client’s needs. Ask what is possible before engaging. For example, if they say the budget is $30,000, don’t present something that is $60,000. If your cli-ent needs bilingual service, deliver that option. Show that you are listening.

Secondly, use language that’s con-sistent with your client’s style. If they refer to employees at teammates, you should too. If they refer to locations as storefronts, you should too. Make it easy for them to translate your propos-al into their terminology to share within their organization.

VALIDATE BEFORE OFFERING YOUR SOLUTIONDo your fact-checking. Ten minutes of your time could make a huge differ-ence in your presentation. Also, inves-tigate any internal politics. Is the issue the same in everyone’s eyes? Since your proposal may be shared across departments, make sure that you are sensitive to the whole organization.

KNOW YOUR STRENGTHSDon’t try to be all things to all people. When you need help, find partners who provide that expertise. Don’t try to fake it; it will just backfire. Maybe that partner will remember you next time and give you an opportunity.

GROW WITH YOUR CLIENTSKeep up on industry trends and forward meaningful information to your clients, whether it’s a news article about them or a competitor or about legislation. Join LinkedIn groups to get relevant news that helps you and your clients. Once you create value, you will be valued, and your clients will be more likely to stay with you and refer you to their peers. H

Jim McCabe is a vice president of Sales Strategy for Sterling Administration. For more information, visit [email protected].

BY JIM MCCABE

- CalBrokerMag.com -16 | CALIFORNIA BROKER FEBRUARY 2016

GENERAL AGENCY

General Agency View From the Top

HOW HAVE GAs CHANGED OVER THE PAST FEW YEARS? David L. Fear, Sr., president and CEO of Shepler & Fear General Agency: The GA market in California is different. In California, GAs have had a strong role in delivering competing health care products for many years. However, like other industries, there have been acquisitions and mergers, which will continue as you see fewer GAs in the California marketplace. Some larger GAs have expanded with a multi-state presence while others remain as strictly regional. The big-gest changes I see are that GAs are not just product wholesalers anymore, but have taken on more of a consulta-tive role with their clients being agents and brokers who no longer get the support from the carriers that was pro-vided in the past. GAs have expanded their services into areas where carriers have retreated due to cost constraints. California is fortunate to have multiple, competing GAs in this market, which bodes well for their agent clients.

Dennis Fallon, senior vice president, Insurance Field Sales and Services for BenefitMall: To meet the changing needs of their brokers, general agen-cies have broadened their capabilities

through diversified product and ser-vice offerings. These additional offer-ings are designed to increase agent revenue streams, compete in the marketplace, and address employee and employer benefit needs to pro-tect health benefit books of business. Many general agencies are building proprietary tools and services for their brokers and employer groups while others are partnering to create best-in-class offerings to meet the needs of brokers and employers. As today’s business environment continues to evolve, general agencies are expand-ing their geographic footprint. The ability to provide not only a diversified product and service offering, but also multi-state support, is now a base re-quirement to provide the support that brokers and their clients expect.

Jessica Word, president of the Word & Brown General Agency: The Af-fordable Care Act (ACA) has undeniably shaped our service model, putting an in-creased emphasis on ACA compliance. The transition of 51- to 100-employee groups to the small-group market has increased demands for products and services that have been tradition-ally reserved for the mid-sized market: composite (tier) rating, rich coverage options, customized benefit solutions, integrated billing, and list enrollments. That has led to these becoming require-ments across our customer base and, like our brokers, GAs have become part insurance sales and support and part technology developer.

Jim McCabe, vice president of Sales Strategy for Sterling Administra-tion (McCabe is providing answers as they relate to a TPA, not a GA): Over the past few years, consumers across all types of businesses are doing busi-ness via mobile. We’ve seen a big in-crease in our mobile customers. We’ve seen an uptick in our Spanish-speaking

customers. We are also increasingly being asked to provide more back-shop support in compliance, technol-ogy, and client communication to the brokerage community.

Ken Doyle, executive director Sales for LISI: Despite minor idiosyncrasies here and there, the value proposition of a GA basically remains the same. The bigger question is how will they be changing in the upcoming years, and what will they choose to implement?

Colleen M. Gimbel, vice president of Marketing/Recruitment/Compli-ance for Berwick Insurance Group: One of the biggest changes, over the past few years, is the amount of com-pliance information that agents are re-quired to understand. Agents want to know what they can and cannot do, which increases the need for compli-ance staff and training programs.

Jennifer Lisanti, director of Sales with beere&purves: While general agents continue to be actively involved in marketing and sales of employee benefits, their role in providing ongo-ing, day-to-day service for existing business has increased considerably. Compliance has become more com-plex and burdensome for employers as a result of the ACA, along with the constant introduction of state and fed-eral regulations. General agents are providing agents and agencies with the resources and contacts to ensure that they are informed on these mat-ters. Employers are also looking for ways to simplify benefits and HR ad-ministration through technology. With the proliferation of online HRIS op-tions, general agents have respond-ed by researching these systems so agents can recommend viable solu-tions to their clients. General agents have introduced their own technology solutions on behalf of agents for on-

In this article, executives from California’s leading general agencies givetheir take on critical trends in the health and employee benefit marketplace.

GENERAL AGENCY

By LEILA MORRIS

ben•e•fit bro•ker \ ben- -fit bro-k r\nounA person who advises businesses on employee benefit solutions.

Including, but not limited to: medical, ancillary, benefits administration, payroll, HR, tax/ACA compliance.

The definition has changed. How will you respond?

Concord (800) 354-6926 | Orange (800) 966-3791 | Woodland Hills (800) 877-0101 | www.benefitmall.com

- CalBrokerMag.com -18 | CALIFORNIA BROKER FEBRUARY 2016

GENERAL AGENCY

line enrollment, census collection, and more, which improves data quality and expedites group enrollments.

Michael Wolff, president of Dicker-son Employee Ben-efits: During the past few years, and particularly since the signing into law of the ACA, GAs have become centers of education for agents who pass the infor-

mation along to their clients. This is particularly true with compliance and legislation. GAs, like their agent cus-tomers, are taking a more consultative approach to working with employers and individual clients. This often takes the form of a total-solution proposal that includes traditional and expanded product and service offerings.

Jeff Papenfus, senior vice presi-dent, Sales of Warner Pacific Insur-ance Services: Over the past several years, GAs have been doing more ad-ministrative tasks for carrier partners. With the implementation of healthcare reform, broker education has become critical. Vetting and partnering with outside vendors for online enrollment, HRIS, ACA, and ERISA compliance, COBRA, travel insurance, and so on, has taken that burden off the brokers and their clients.

WHAT ARE THE MOST IMPORTANT MARKET TRENDS THAT AGENTS NEED TO BE AWARE OF THIS YEAR? Dennis Fallon of BenefitMall: We see three primary trends that are af-fecting agents most heavily in 2016. The benefit arena now reaches well beyond the traditional broker market with employee workforce services and technology companies vying for a piece of market. These competitors are luring clients away through the promise of free technology and other value-added services. ACA compli-ance is confusing consumers who are often not savvy enough to be aware when a broker-of-record is occurring. Many employers will seek various on-line workforce solutions and end up with a new broker-of-record without even being fully aware it. When this

happens, employers lose the valuable expertise of their local broker. The con-solidation of health benefit carriers has expanded and can be seen in banking, payroll services, and human-resource management. With these consolida-tions, we see diversification in product portfolios, larger marketing spending, and more growth in retail sales, which often competes directly with the bro-ker channel. Finally, for group agents, there is a change in the small-group definition in California to two to 100. The continued creativity around multi-carrier and multi-product offerings will be a battle on the small-group front as brokers strive to provide a compre-hensive solution at an affordable price with the service that clients are accus-tomed to receiving.

Jennifer Lisanti of beere&purves: Transitioning 51 to 100 groups into small group products will be an important focus in 2016. The small-group market presents en-tirely new rates, rules, and product offerings to agents who have

not focused in the under-50 market. Working with a knowledgeable gen-eral agent will provide a considerable advantage in getting up to speed quickly. Employers want to minimize their management systems and points of contact through an online HR system. To remain competitive, agents are offer-ing their own value-added services or at least, they are becoming knowledge-able enough to direct clients to the most viable options. Employers are turning to their insurance agents for help with HR-related issues that are outside their tradi-tional scope of business. General agents provide much needed help with these client demands, but agents also need to stay up to date on their clients’ issues and challenges, including vendors and secondary resources to provide further guidance.

David L. Fear, Sr., of Shepler & Fear: The number one issue, this year, is the full implementation of the ACA’s Employer Shared Responsibility man-date. The government has not done a very good job of communicating

things to employers, which will show up as large employers struggle to file their 1094/1095-C reports this spring. They’ll soon face the IRS and have to provide proof that they have been offer-ing affordable coverage to their eligible employees that meets a minimum-val-ue standard. Agents need to be at the front of this new and confusing process. The second issue is how agents will provide solutions to reduce the cost of their clients’ health insurance benefits. Obviously, the cost of insurance cov-erage has not come down. Many em-ployers are getting closer to throwing in the towel and dropping their group health plan. It’s become unaffordable. Employees are not happy about their high out-of-pocket costs under the new ACA pricing and benefit requirements. Agents need to provide solutions now.

Jeff Papenfus of Warner Pacific: Since we just got through moving the one to 50 groups into ACA-compliant plans, the next focus should be on the 51 to 100 groups. Many of these groups took renewals in December to delay moving to ACA-compliant plans. Does that sound familiar? The biggest chal-lenge is that most of these groups will have to go to an age-rated plan from a composite-rated plan. However, a fair percentage will actually save premium dollars by moving into the new plan de-signs and rating structure. While premi-ums may be significantly higher or low-er under the new ACA rating, there will be employees in each group who are winners and losers in regards to their personal premiums. The other trend we are likely to see, this year, is that car-riers and brokers are working together to move groups from the 12/1 renewal date. I think all of us would agree that renewing 80% of all business in a two-month period is not good for GAs, carri-ers, brokers, or their clients.

Jessica Word of Word & Brown: Brokers would do well to get very cre-ative this year. The old standard of sell-ing an out-of-the-box solution is gone, or will be soon. Multi-carrier packages with unique funding options are win-ning the marketplace as they offer the most diverse coverage, providers, and prescription benefits for a large organization to meet the needs of its

- CalBrokerMag.com -FEBRUARY 2016 CALIFORNIA BROKER | 19

GENERAL AGENCY

many constituents. Offering combined solutions will keep insurance rates low for customers while quality and satisfaction remain high. Brokers can deliver customized solutions to meet each employee’s medical and finan-cial needs by allowing them to choose their own options within a set of car-riers, plans, and coverage. The de-mand for technology is growing, too. If brokers don’t have a solution and are speaking to clients about it, they need to find one (or more) to meet their cli-ents’ needs. Or, they can partner with a GA that is offering support in imple-menting and running cases through an online solution.

Jim McCabe, Sterling: The changing legislative landscape is one of the most im portant things to watch this year. The Cadillac tax was de-layed, and more changes are on the way. A majority of employees may have

less disposable income to handle larger deductibles and out-of-pocket costs with narrow networks and less choice, and high deductible plans.

Ken Doyle of LISI: It will be another interesting year with the second half of the small-group market (51 to 100) hav-ing to move. Being a highly politicized year, more legislation will be introduced in hopes of easing some of the ACA pain. I also think that we will see a move-ment to get viable software technolo-gies in place before the fourth quarter. With this shift in technology, it would be-hoove you to assess whether you have the aptitude, the resources, and the agil-ity to keep up with all the trends. If you can’t respond with a vehement “yes” to these concerns, consider hiring some-one or partnering with a resource to help you take it to the next level. Re-evaluate your workforce. Agents need a service team that can keep up with today’s pace with tomorrow’s forward thinking men-tality. Agents should be looking at the concept of all-in-one-place platforms, such as concierge services.

Michael Wolff of Dickerson: Agents continue to look for ways to differenti-

ate themselves. In 2016, it will be key to access integrated technology and compliance tools while keeping an eye on products and services beyond the traditional. For example, don’t overlook including voluntary benefits for small and large employers. Agents don’t have to know all the answers. They just need to know where to go for information and creative alternatives.

DO YOU SEE ANY SPECIFIC TRENDS RELATED TO THE SMALL GROUP VERSUS THE BIG GROUP MARKET?Michael Wolff of Dickerson: It will be important to be sensitive to the chang-es affecting mid-size groups that are becoming small groups. These chang-es include the move to small group rating and underwriting guidelines, as well as the employer shared respon-sibility requirements that are new to groups of 50 to 99. These groups will look to agents to educate them on the differences between large and small group plan designs. They will seek the account management-level service to which they have become accustomed.

Jessica Word of Word & Brown: With mid-sized employers (with 51 to 100 employees) moving into the small-group marketplace, we are wit-nessing a blending of requirements in our small group product portfolio. Benefit-administration systems have typically been reserved for larger cli-ents who could afford higher-priced, integrated functionality involving pay-roll, benefits, and billing. But cost-effective solutions are emerging to simplify the administrative burden of tiny groups. We saw significant diver-sification of our broker-customers in 2015 into new products and additional marketplaces to make up for the re-cent cuts in carrier commissions. Brokers who have been the servicing agent on a single in-force policy are looking to increase their reach into a client’s coverage portfolio to enhance and further bind the relationship. We’ve seen brokers exit the market-place – some leaving the industry and some selling their books of business to rivals and larger agencies. That consolidation has reduced our active broker population by roughly 5%, a trend we anticipate will continue.

Jim McCabe, Sterling: The need for education in all things benefit-related has to be more focused. All of the voluntary products, retirement, and tax efficient savings accounts require more information about individual risk tolerance as well as short- and long-term goals. Companies have to pro-vide more insight, and address em-ployees’ financial goals based on their life events.

David L. Fear, Sr. of Shepler & Fear: Smaller employers are looking into alterna-tive funding, such as HRAs, HSAs, and FSAs to help curb the cost of health care and health insurance. Many large employers have done it success-

fully. Now it’s time for small employ-ers to implement some of these ideas. Even though small employers are not subject to the ACA employer mandate, they still have to deal with other things out of their control. Small employers are struggling to deal with health insur-ance, which is one of the most regu-lated products in the United State. They are going to look to their trusted advisor for solutions on how to comply with the law and how to reduce costs while still attracting and retaining good workers. If the employer-based system remains, it’s up to agents to help clients work through these challenges.

Jennifer Lisanti of beere&purves: The biggest trend we see is the move-ment to private exchanges in the small-group market. The private ex-change model allows small groups to implement cost controls through de-fined contribution and offer multiple carriers, which provides access to a significantly larger pool of providers. This simply does not exist in the mid-market segment (100+). Another trend is the onslaught of fourth-quarter re-newals. This year, it will affect an even larger number of renewals due to the 51 to 100 groups taking advantage of early renewal opportunities in 2015. This trend will continue to create quot-ing, enrollment, and approval challeng-es for agents and agencies servicing these groups.

- CalBrokerMag.com -20 | CALIFORNIA BROKER FEBRUARY 2016

GENERAL AGENCY

Dennis Fallon of BenefitMall: Small groups are weighing the value of con-tinuing to offer benefits versus the cost and compliance burden. Large groups face the heavy costs of having to offer benefits to everyone when they may have only covered a portion of their population. The compliance burden may be heavier on the small group sector since they don’t often have HR departments to take on the burden. It falls on owners and managers who can become overwhelmed by the task.

WHAT THINGS HAVE YOU NOTICED THAT SET APART SUCCESSFUL AGENTS?Jeff Papenfus of Warner Pacific: Our

broker partners have a passion for what they do. They are adapting to a new marketplace and be-coming more knowl-edgeable. They are evaluating what they offer and looking to

technology tools with personalized service to grow their business.

Michael Wolff of Dickerson: Agents who have truly embraced consulta-tive selling and the latest technolo-gies are standing out among their contemporaries. These agents are educators as much as they are bril-liant salespeople. They use all avail-able communications vehicles to stay in front of their clients – face-to-face, telephone, webcasts, social media, print and email – to deliver meaning-ful information to their multi-genera-tional client bases.

Dennis Fallon of BenefitMall: Agents who are evolving with the trends are the most successful. To com-pete in our chang-ing industry, agents must be confident, committed, and passionate about

providing the best benefit cover-age possible, and stay relevant to employers and the management of health benefits. Agents also need to provide a complete human capital

management offering that ensures that competitors do not compromise their health benefit book of business. No matter how valuable the benefit consultation may be, an employer group can be easily stolen in 80% of scenarios when another provider offers a comprehensive workforce solution. Successful agents are con-stantly bringing new solutions to their clients, educating themselves on market trends and new products, embracing technology solutions, and maintaining a level of service to be responsive to the needs of new and existing clients.

Jennifer Lisanti of beere&purves: Agents who are open to change in our increasingly complex industry will have an advantage over those who do business as usual. Agents who avoid technology trends and compliance is-sues expose themselves to competi-tion and their clients to unnecessary risk. Successful agents stay informed of carrier product offerings and rules, as well as state and federal legislative issues. They are prepared to inform their clients of any positive or negative issues. Successful agents continu-ally prospect for sales opportunities, add new lines of coverage to existing clients, introduce product lines, and demonstrate the value they bring to the agent-client relationship to ensure client retention.

Jessica Word, Word & Brown: The best brokers – like the best and most suc-cessful businesses in any maturing indus-try – are adaptable and flexible. They meet new strains on their resources, client requirements,

and government regulation without resistance, always looking for and vet-ting solutions that deliver meaningful results. They are innovative, looking for gaps in the solutions their competi-tors provide, and delivering meaning-ful ways that attract customers and generate referrals. Finally, successful brokers form deep partnerships with organizations that fulfill these needs, adapt to changes, and are responsive

to requests for support. They pass the labor onto service partnerships while maintaining their focus on their own business and on the growth of their sales opportunities.

Ken Doyle of LISI: How do you become scalable? Utilize partners through this transformation and build your sales/service model to meet the new consumers’ needs through tech-nology, and create an experience that provides value. Cutting-edge agencies understand analytics and how the in-formation can help provide financial solutions. These agencies are moving from descriptive (what happened) to diagnostic analysis (why it happened), to predictive (what is likely to happen), and to prescriptive (determining the right outcome). This is where you will see movement in the types of prod-ucts offered in the market. A sharper customer targeting approach and a variety of wellness strategies will shift the discussion for the agent in becom-ing a preventative risk advisor.

Jim McCabe, Sterling: Successful agents have a personal touch and at-tention to detail. They also understand where our client brokers are in their life-cycle. Not every firm wants the same things.

Colleen M. Gimbel of Berwick In-surance Group: It’s knowledge, train-ing and confidence. An agent who is confident with the material they rep-resent will be much more successful. It goes without saying that an agent needs to know the material in order to sell a plan. Many agents have the knowledge, but they don’t feel confi-dent with the information. Every agent needs a different amount or type of training to feel comfortable enough to sell a Medicare plan.

David L. Fear, Sr., of Shepler & Fear: We see a group of younger agents who approach this business in a very smart way – using tools that make them more efficient with their time. We see a lot of younger agents going out and sharing ideas that employers have not heard before. They are demanding that our industry respond better to the needs of their clients through online

There Is Only One Healthcare Reform Certification®

USE PROMO CODE: CALBROKER16EXPIRES MARCH. 30, 2016

$995$2000 VALUE

GETCERTIFIED

TODAY

EXCLUSIVE TO CALI BROKER MAGAZINE + WEST COAST BROKERSGET CERTIFIED

TODAY ONLINE OR AT THE CONGRESS

RECEIVE A COMPLIMENTARY PASS TO THE 2016 EMPLOYER

HEALTHCARE & BENEFITS CONGRESS, SEPT. 25-28 IN WASHINGTON D.C.

WITH ONLINE CERTIFICATION

Info at 561.790.1176 or www.HealthcareReformCertification.com

Maintain existing business to advise clients on IRS audit and litigation avoidance

Increase revenue and drive new business with client trust

Earn a seat at the table with HR Executives and C-Suite decision makers

Build client credibility with direct access to the nation’s top legal experts

TOP BROKERS AND AGENTS EARNING THEIR DESIGNATION AS CERTIFIED HEALTHCARE REFORM SPECIALIST CAN RETAIN CLIENTS BY LEARNING TO ADVISE ON THE ACA MANDATE.

LARGE IRS FINES CAN PUT YOUR CLIENTS OUT OF BUSINESS.

- CalBrokerMag.com -22 | CALIFORNIA BROKER FEBRUARY 2016

GENERAL AGENCY

capability, simplification of processes, and ease of communication. Success-ful agents think out-of-the-box and communicate more effectively with their clients. Many GAs can assist in providing these value-added services.

WHAT KINDS OF GA SERVICES ARE MOST VITAL TO TODAY’S AGENTS?Jessica Word, Word & Brown: Two key areas affect our brokers today: compliance and technology. ACA compliance is a maze. Each scenario creates a different compliance require-ment. Mandates are repeatedly re-vised, shuffled, and updated. Brokers have to align themselves, very quickly, with emerging technology, find the so-lutions that meet their clients’ diverse needs, and learn to operate and imple-ment these solutions for their groups.

Ken Doyle of LISI: To understand what is vital to the agent, you need to look at the end-user (con-sumer). What are they demanding in the way of customer experience and me-dium of information? You are now hearing

that we are experiencing disruption in our industry. This is true, but most peo-ple think that disruption is in the soft-ware being introduced that provides benefit administration or HRIS linked to payroll, time and attendance, and/or compliance, etc. Well, it’s much more than that. Think about customer experi-ence. How do they interact with tech-nology and the information they can get at their fingertips? You will see the adoption of the “Internet of things” and other new technologies. But this follow-the-leader paradigm of the industry will mean that any edge that a GA has will disappear quickly. Sure these technolo-gies are impressive, even evolutionary, and long over-due in our industry. Still, they are not disruptive, nor are they rev-olutionary. Revolution comes from prod-ucts and services that do something with technology to create a better expe-rience through personalization. We have a whole new generation of consumers moving into the workforce who will not accept how we have always done things. This generation was immersed

in technology, and embraced it — seem-ingly before they were even wheeled out of the maternity ward. So it will be vital to help the agent comprehend and deliver to this new and rising population of consumers while keeping in touch and relevant to existing clientele.

Jim McCabe, Sterling: Agents want personal customer service for their clients, as well as easy online access to check balances and plan renewals. Knowledge-based support, original con-tent to share, sales education, and chan-nel support are among the top requests.

Colleen M. Gimbel, Berwick Insur-ance Group: Agents want compliance information that is digestible and imple-mentable in their day-to-day activities. They also need ac-cess to sales support staff. It is vital for an

agent to be able to contact the FMO whenever they have questions.

Jeff Papenfus, Warner Pacific: The most common need is probably quick access to information. Because of fre-quent changes to carriers’ products, plan designs, networks, and compliance requirements, agents need to find the most up-to-date information quickly and preferably in one place to be efficient. With new technology-centered brokers, agencies and brokers are asking us how they can compete. When it comes to online enrollment and HR systems, one size definitely does not fit all.

Michael Wolff of Dickerson: Next to product and price consultation, ACA-related education and resourc-es top the list of GA services most often requested by our agents. And in a blending of areas, agents are looking for the most cost-effective employee benefit solutions to help ensure ACA compliance for their cli-ents. In addition to core medical and ancillary plans, products that were once considered to be voluntary are increasingly offered as employer-sponsored coverages. Technology tools are critical to the extent that they can integrate enrollment, pay-

roll, benefit, and HR data. A GA that can provide these tools and the tech-nical support to use them will help the agent enhance retention as well as create employer efficiencies and mandated reporting capabilities.

Dennis Fallon of BenefitMall: Bro-kers need solid general agency, back-office support more than ever. The basics of being accessible, providing a timely response, providing insight and guidance are still important. But offer-ing access to tools being requested by employer groups is probably the most significant area of GA services. Gen-eral agencies should provide a wide ar-ray of services beyond health and an-cillary including benefit administration tools, ACA compliance, payroll servic-es, tax compliance, and supplemental products, such as workers’ comp and 401K. A combined product offering is where the marketplace has moved. A strong GA partner will provide safe access to these tools and services through a channel that will not com-pete with or steal your business. If a general agency is not helping agents compete with product and technology companies that are calling on their em-ployer groups, the agent should move to a general agency that is committed to their success.

Jennifer Lisanti of beere&purves: One would not necessarily consider knowledge a service, but ensuring that your general agent trains and ed-ucates their staff so they know their products and resources inside and out is critical to an agent’s success. General agents offer a wide variety of services and technology tools, but they are only as good as the expertise of the people filling the service roles. As employers face extensive com-pliance requirements, they are ask-ing their agent to help simplify these daunting obligations with the aid of educational resources, access to on-line HR and compliance systems, and/or vendor relationships with preferred pricing. Working with a general agent that understands an employer’s com-pliance and technology needs not only provides tremendous relief to an em-ployer, but it also helps to strengthen the agent/client relationship.

- CalBrokerMag.com -FEBRUARY 2016 CALIFORNIA BROKER | 23

GENERAL AGENCY

WHAT IS THE MOST IMPORTANT THING TO KEEP IN MIND WHEN CHOOSING A GA?Jessica Word, Word & Brown: It is definitely the people; I encourage bro-kers to vet a general agency by engag-ing its people because service depends a great deal on those who deliver it.

Each GA offers what appears to be the same or similar services, at least on paper. They all have products for their marketplaces. They all have a solution for quoting, whether it’s pro-prietary or purchased. They all have a sales team. Longevity of service is im-portant. Is the general agency staffed by experts who have worked in our industry for a long time? That can be a differentiator. And offering guaran-teed accuracy of quotes is critical for brokers and clients. Being adaptive to what’s happened in our industry in the past five years is also important.

Jim McCabe of Sterling: When you are choosing GA or administrator, know what is most important to your employer population. Do they need bilingual access, mobile access, or educational materials? Can the general agency or administrator enhance your client relationships? Can this relation-ship assist in growing and retaining profitable revenue? Can the GA re-duce your cost of business by supply-ing support so that you don’t have to invest in it on your own?

David L. Fear, Sr., of Shepler & Fear: Who owns and operates the GA? Are they aligned with agents and their role in delivering insurance benefits? Does the GA have a track record of support-ing agents and brokers? Are they fo-cused on meeting the needs of agents or are they focused on profits? What do they do differently than their com-petitors and why are they different? Are they a supporter of the industry? Will the GA provide personal service and attention to the agent and their cli-ents? Will they go out with the agent and meet with their clients personally and act in a consultative role or are they just trying to push products?

Colleen M. Gimbel of Berwick Insur-ance Group: Work with people you like and who are easily accessible. Many

times we hear about agents who are contracted with an FMO/GA that never returns their calls. That’s a huge prob-lem because the whole purpose of the FMO/GA is to support its down line. Too many times agents just look for an FMO/GA who will give them leads; they don’t think about any of the other services they might need. In my experi-ence, agents who choose an FMO/GA based solely on the amount of leads the FMO/GA said they would provide is often disappointed and disgruntled. This is a crazy industry, and no com-pany is perfect. But if you have a good working relationship with your FMO/GA it makes everything go much more smoothly, and it’s more enjoyable.

Ken Doyle of LISI: Work with a thought leader who understands in-surance 2020. The central message or strategy needs to be looking at how they will keep pace with social media, technology, economic, and political de-velopments. Digitization will be key for the GA, carrier, agent, and group cli-ent. Previously everyone talked about big data. Well, we have more data in our industry than we know what to do with, and therein lies the issue. As we move toward digitization of informa-tion, it will depend on algorithms and analytical techniques that will reshape customer targeting, financial advice, and individual customization. With that said, choose a GA whose approach to the new market will complement you, your agency, and your business phi-losophies through transformation. Not everyone is created equal, so it cannot be a one-size-fits-all approach.

Jennifer Lisanti of beere&purves: Agents should consider the total value the general agent will deliver through the entire sales cycle. General agents provide value beyond quoting and en-rollment form collection. Don’t just fall for the sales pitch. Make sure that you work with a general agent who actu-ally services your business so you have more time to focus on sales. Ask to see samples of their agent commu-nications. Find out if they provide de-ductible credit services or if they get in-volved in claim and billing issues. Find out if they offer online enrollment and who does the setup. Ask to see their

average group approval turnaround times. Ask enough questions to make sure they will deliver value to your agency and your clients. Also make sure the general agent is knowledge-able and exhibits expertise about the products they sell and the rules that must be followed in order to sell those products. When a general agent has educated and informed employees, miscommunications and oversights are minimized, allowing everyone to work more effectively and efficiently.

Jeff Papenfus of Warner Pacific: When evaluating a GA relationship, brokers and agencies should ask what are the most important aspects of that relationship, the technology, the ac-cessibility, the responsiveness, and the personal touch. The answers will point them to the right GA for their needs.