c h a p t e r 4 capital investment decisions capital investment decisions

TRANSCRIPT

C H A P T E R 4

Capital InvestmentDecisionsCapital InvestmentDecisions

Learning Objective 1

Understand the importance of capital budgeting and the concepts underlying strategic and capital investment decisions.

Define Capital Budgeting and Capital

Capital Budgeting

Systematic planning for long-term investments in operating assets.

Capital

The total amount of money or other resources owned or used to acquire future income or benefits.

Capital Investment Decisions

What three aspects of capital investment decisions are critical to long-run profitability?What three aspects of capital investment decisions are critical to long-run profitability?

Large capital outlays are required.

There is a long-term impact on earnings.

There is a lack of liquidity (they cannot be readily disposed of).

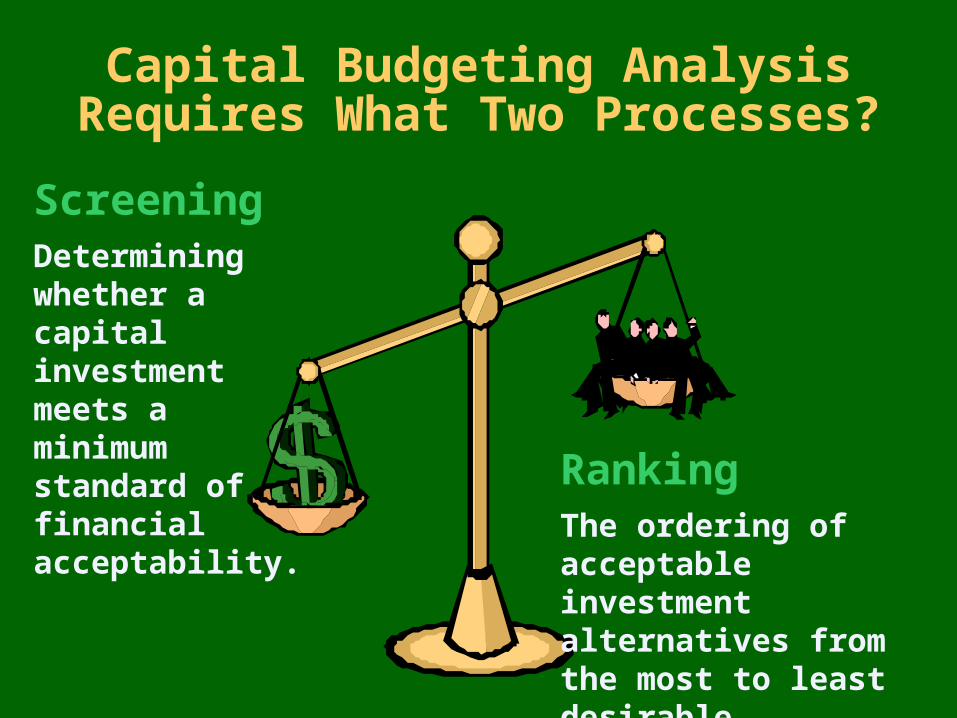

Capital Budgeting Analysis Requires What Two Processes?

ScreeningDetermining whether a capital investment meets a minimum standard of financial acceptability. Ranking

The ordering of acceptable investment alternatives from the most to least desirable.

What is the Time Value of Money?

- The concept that a dollar to be received now is worth more than a dollar to be received far in the future.

- Interest is the payment (cost) for the use of the money.

Because of the time value of money, a difference in the timing of cash flows can make one investment more attractive than another.

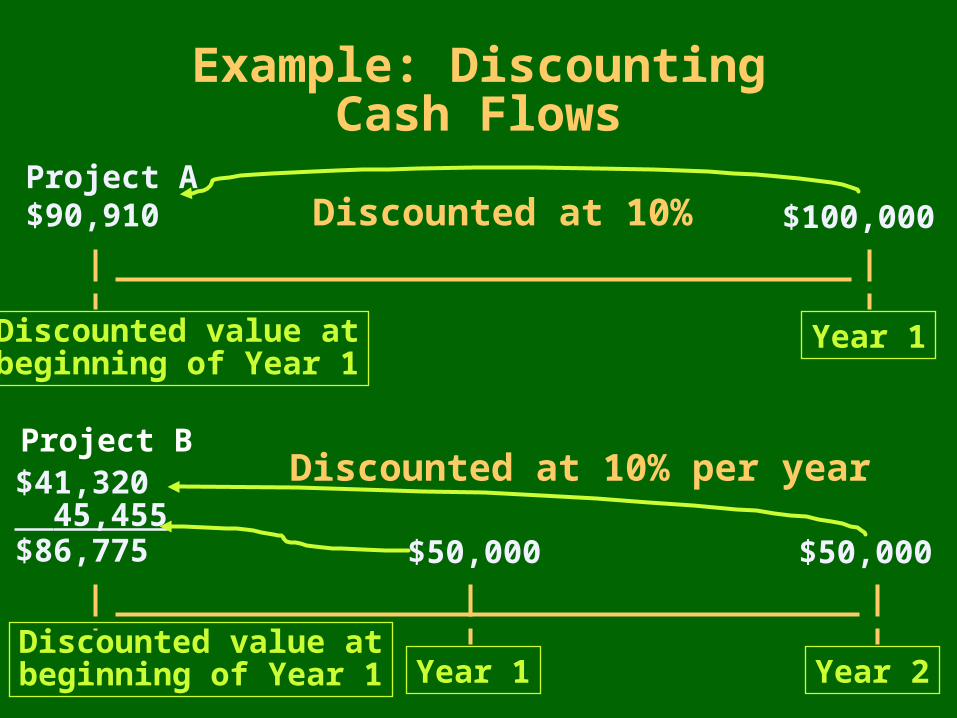

Example: DiscountingCash Flows

Project A$90,910 $100,000

Year 1

Discounted at 10%

Year 1 Year 2

$50,000 $50,000

$41,320 45,455$86,775

Discounted at 10% per year

Discounted value atbeginning of Year 1

Project B

Discounted value atbeginning of Year 1

What are Cash Outflows?

All investment opportunities have an initial cost plus other expected outlays or cash outflows associated with an investment.

Investmentopportunity

Cash outflows

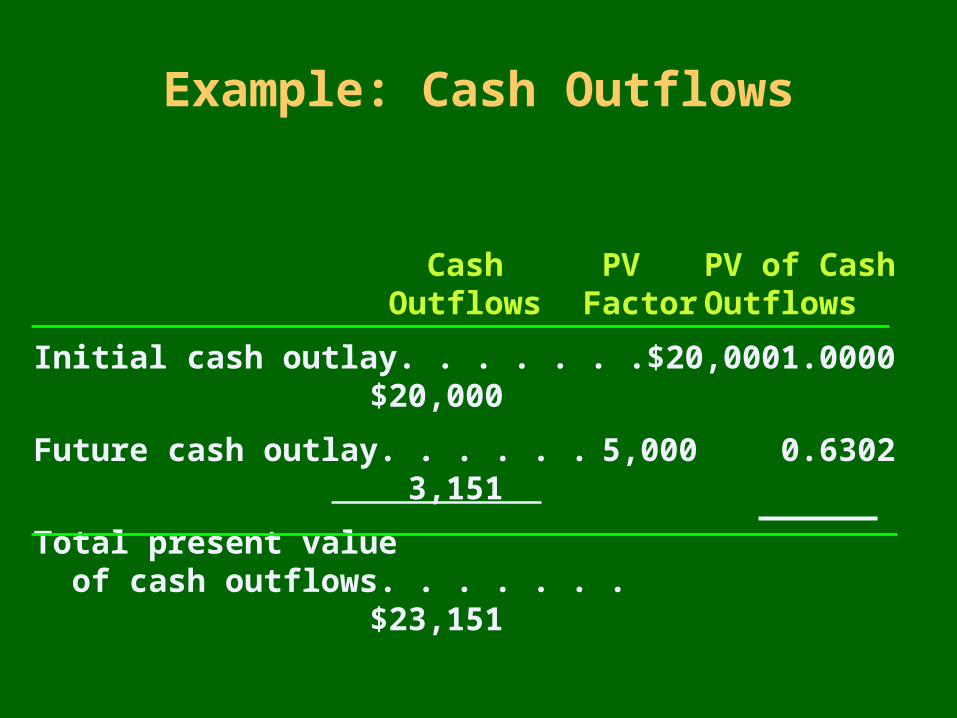

Example: Cash Outflows

Cash PV PV of CashOutflows Factor Outflows

Initial cash outlay. . . . . . . $20,000 1.0000 $20,000

Future cash outlay. . . . . . 5,000 0.6302 3,151

Total present value of cash outflows. . . . . . . $23,151

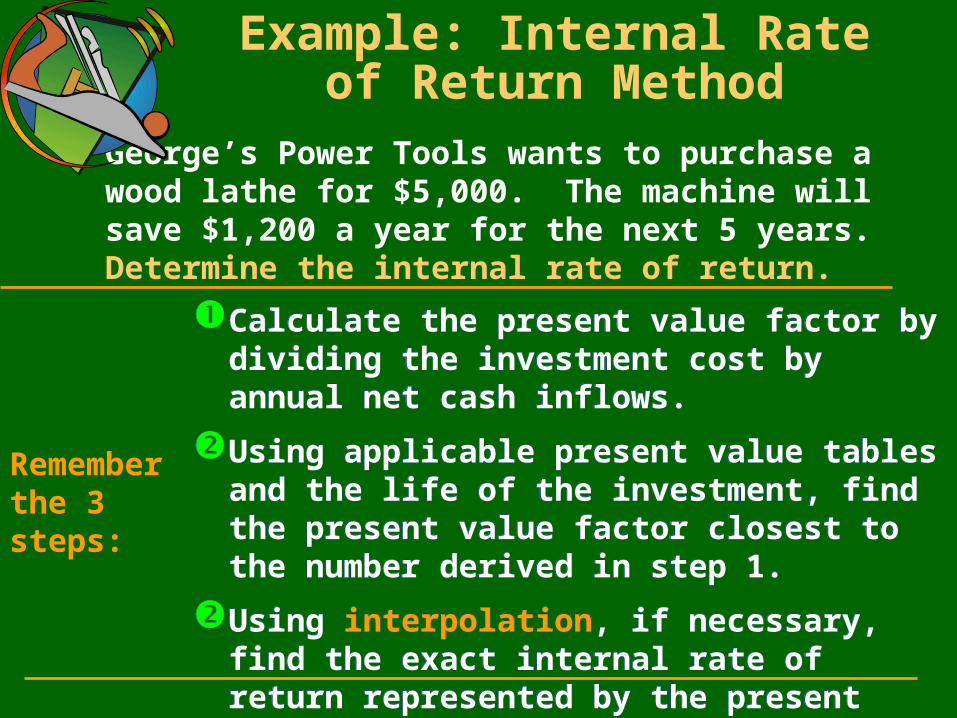

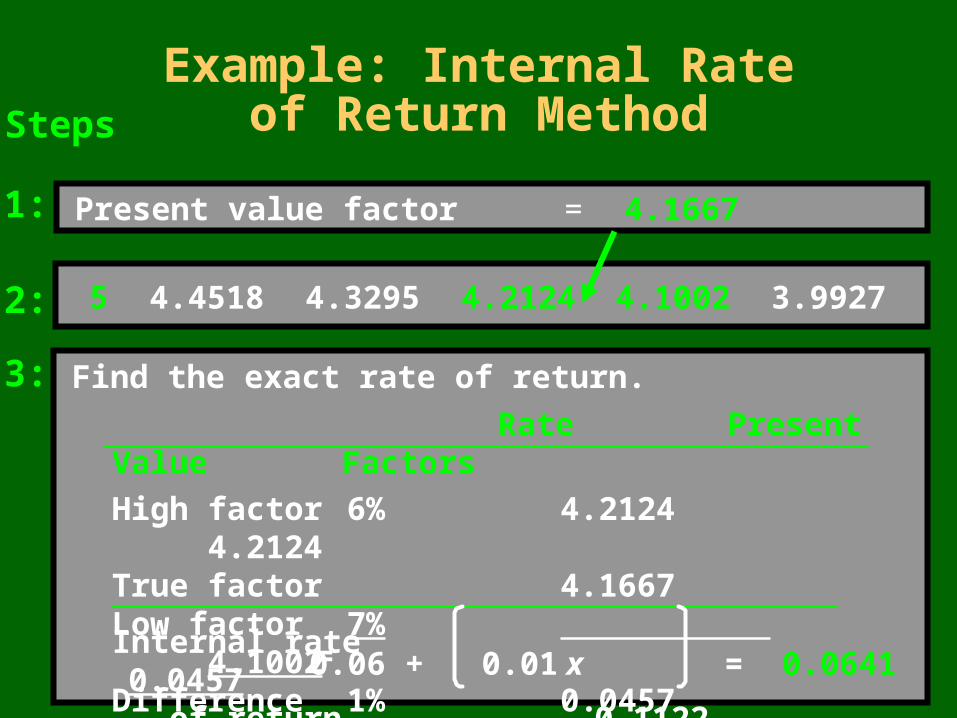

Example: Internal Rateof Return Method

George’s Power Tools wants to purchase a wood lathe for $5,000. The machine will save $1,200 a year for the next 5 years. Determine the internal rate of return.

Remember the 3 steps:

Calculate the present value factor by dividing the investment cost by annual net cash inflows.

Using applicable present value tables and the life of the investment, find the present value factor closest to the number derived in step 1.

Using interpolation, if necessary, find the exact internal rate of return represented by the present value factor in step 1.

Calculate the present value factor by dividing the investment cost by annual net cash inflows.

Using applicable present value tables and the life of the investment, find the present value factor closest to the number derived in step 1.

Using interpolation, if necessary, find the exact internal rate of return represented by the present value factor in step 1.

Example: Internal Rateof Return Method

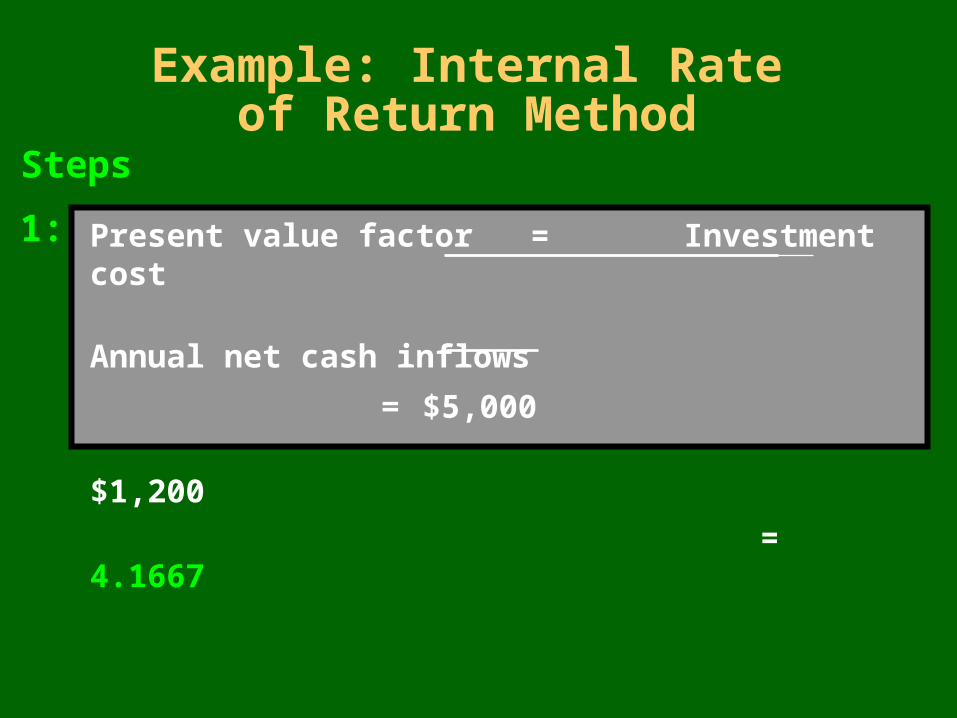

Present value factor = Investment cost Annual net cash inflows

= $5,000

$1,200

= 4.1667

1:

Steps

Example: Internal Rateof Return Method

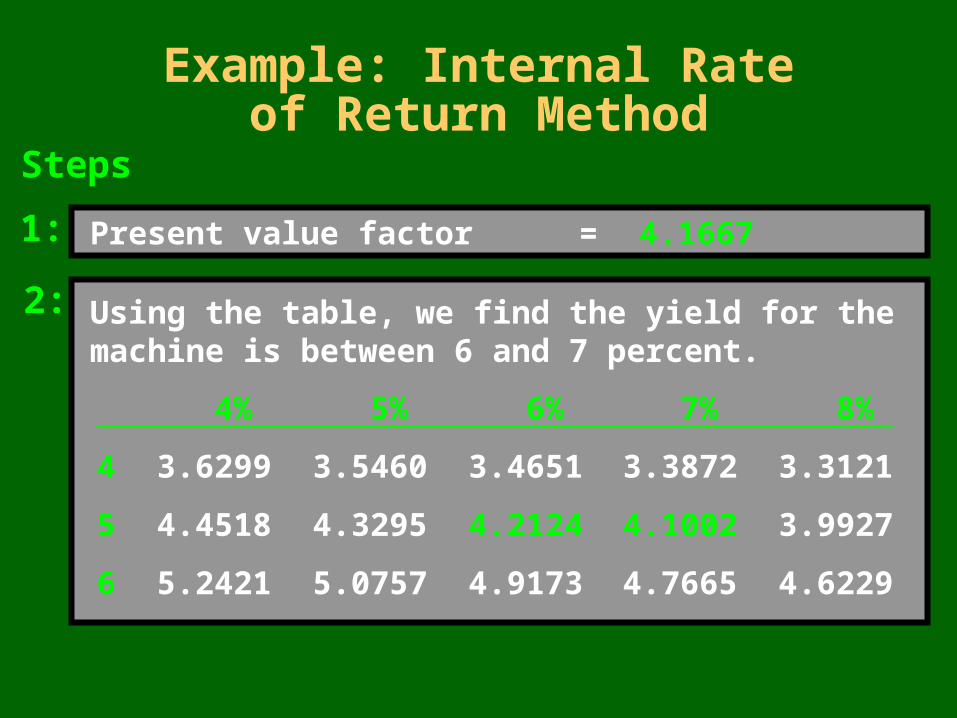

Present value factor = 4.1667

Steps

1:

Using the table, we find the yield for the machine is between 6 and 7 percent.

4% 5% 6% 7% 8%

4 3.6299 3.5460 3.4651 3.3872 3.3121

5 4.4518 4.3295 4.2124 4.1002 3.9927

6 5.2421 5.0757 4.9173 4.7665 4.6229

2:

Example: Internal Rateof Return MethodSteps

Present value factor = 4.16671:

5 4.4518 4.3295 4.2124 4.1002 3.99272:

3: Find the exact rate of return.

Rate Present Value Factors

High factor 6% 4.2124 4.2124True factor 4.1667Low factor 7% 4.1002Difference 1% 0.0457 0.1122

Internal rate 0.0457 of return 0.1122 0.06 + 0.01 x = 0.0641=

What are Cash Inflows?

Investmentopportunity

Cash outflows

Cash inflows

Cash inflows are any current or expected revenues or savings directly associated with an investment.

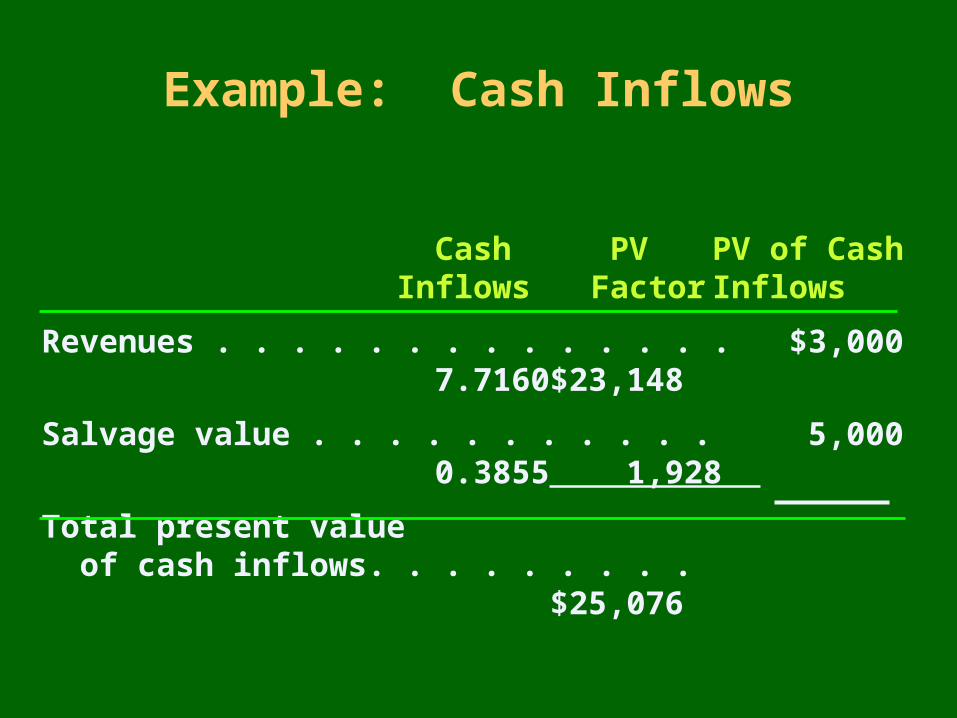

Example: Cash Inflows

Cash PV PV of Cash Inflows Factor Inflows

Revenues . . . . . . . . . . . . . . $3,000 7.7160 $23,148

Salvage value . . . . . . . . . . . 5,000 0.3855 1,928

Total present value of cash inflows. . . . . . . . . $25,076

Learning Objective 2

Describe and use two nondiscounted capital budgeting techniques: the payback method and the unadjusted rate of return method.

Capital Budgeting Techniques

Payback Method

Unadjusted Rate of Return Method

Non-discounted capital budgeting techniques do not take into account the time value of money. What are two common techniques?

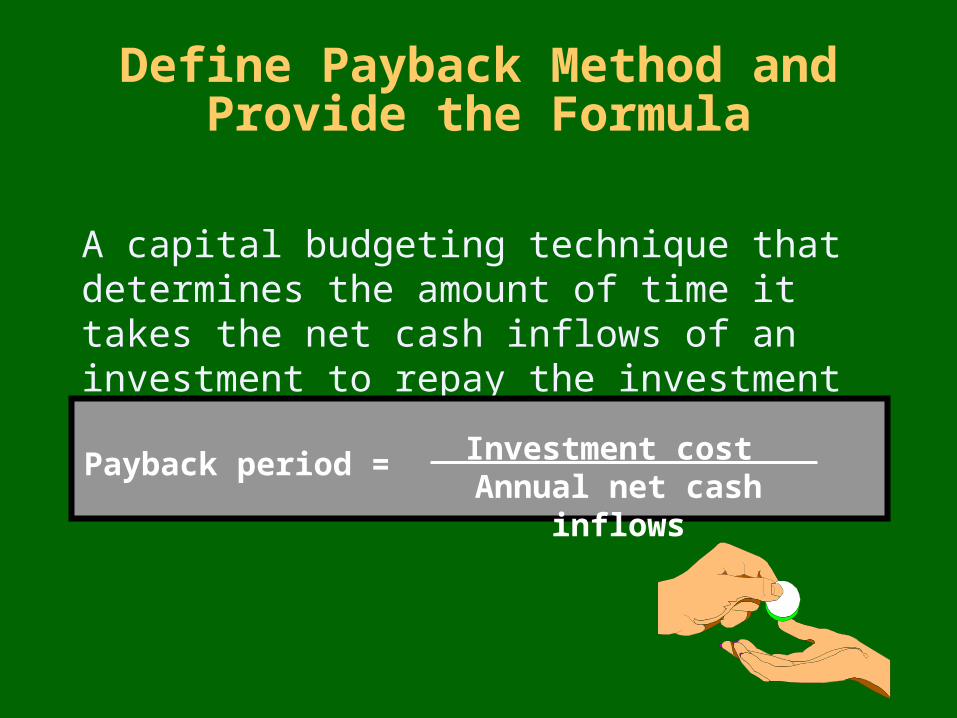

Define Payback Method and Provide the Formula

A capital budgeting technique that determines the amount of time it takes the net cash inflows of an investment to repay the investment costs.

Payback period = Investment cost Annual net cash inflows

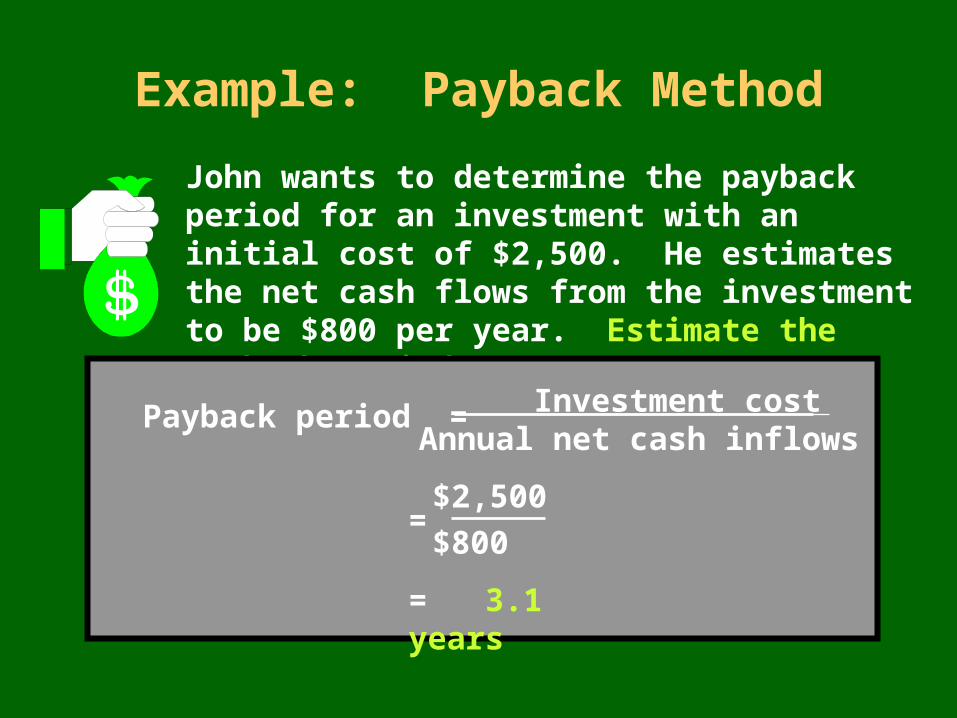

Example: Payback Method

John wants to determine the payback period for an investment with an initial cost of $2,500. He estimates the net cash flows from the investment to be $800 per year. Estimate the payback period.

Payback period =

=

= 3.1 years

Investment cost Annual net cash inflows

$2,500

$800

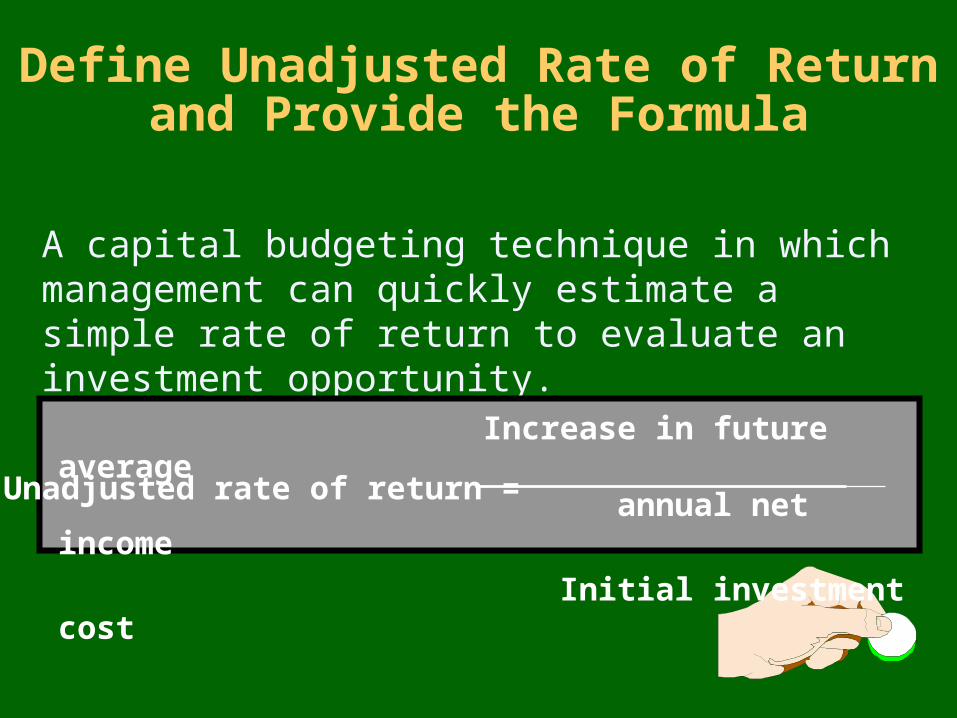

Define Unadjusted Rate of Return and Provide the Formula

A capital budgeting technique in which management can quickly estimate a simple rate of return to evaluate an investment opportunity.

Increase in future average annual net income

Initial investment costUnadjusted rate of return =

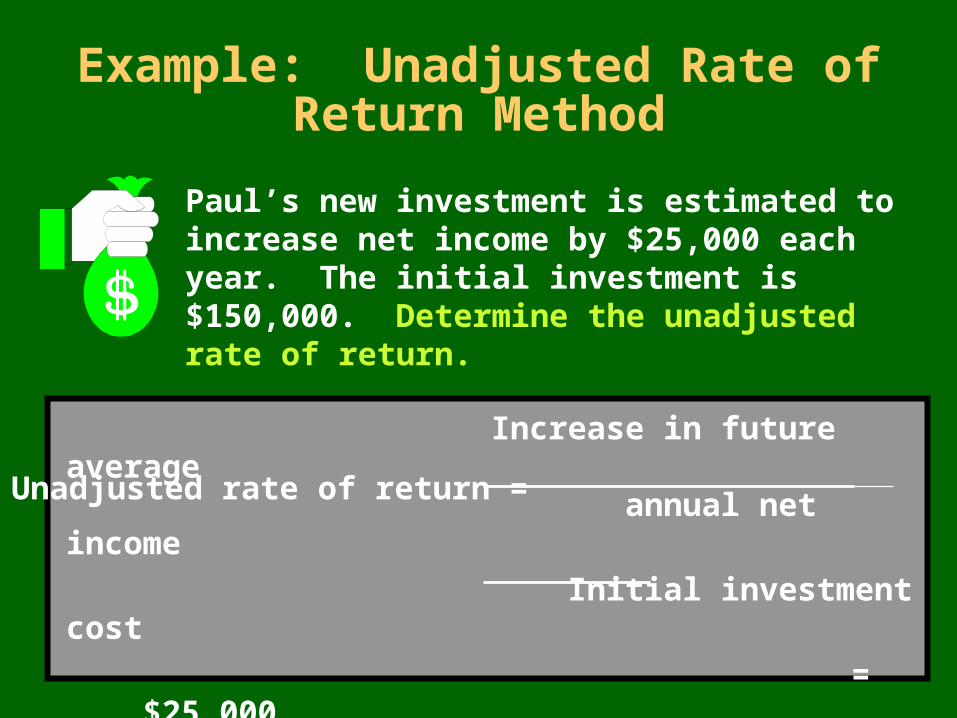

Example: Unadjusted Rate of Return Method

Paul’s new investment is estimated to increase net income by $25,000 each year. The initial investment is $150,000. Determine the unadjusted rate of return.

Increase in future average annual net income

Initial investment cost

= $25,000

$150,000

= 16.67%

Unadjusted rate of return =

Learning Objective 3

Describe and use two discounted capital budgeting techniques: the net present value method and the internal rate of return method.

Define Capital Budgeting Techniques

Discounted capital budgeting techniques take into account the time value of money by comparing discounted cash flows. What are two common techniques?

Internal Rate of Return Method

Net Present Value Method

Selecting a Discount Rate

Define Cost of Capital

The average cost of a firm’s debt and its equity; equals the rate of return that a company must earn in order to satisfy the demands of its owners and creditors.

Define Cost of Capital

The average cost of a firm’s debt and its equity; equals the rate of return that a company must earn in order to satisfy the demands of its owners and creditors.

In order to evaluate investments using discounted cash flows, a firm must first establish a cost of capital, or acceptable rate of return.

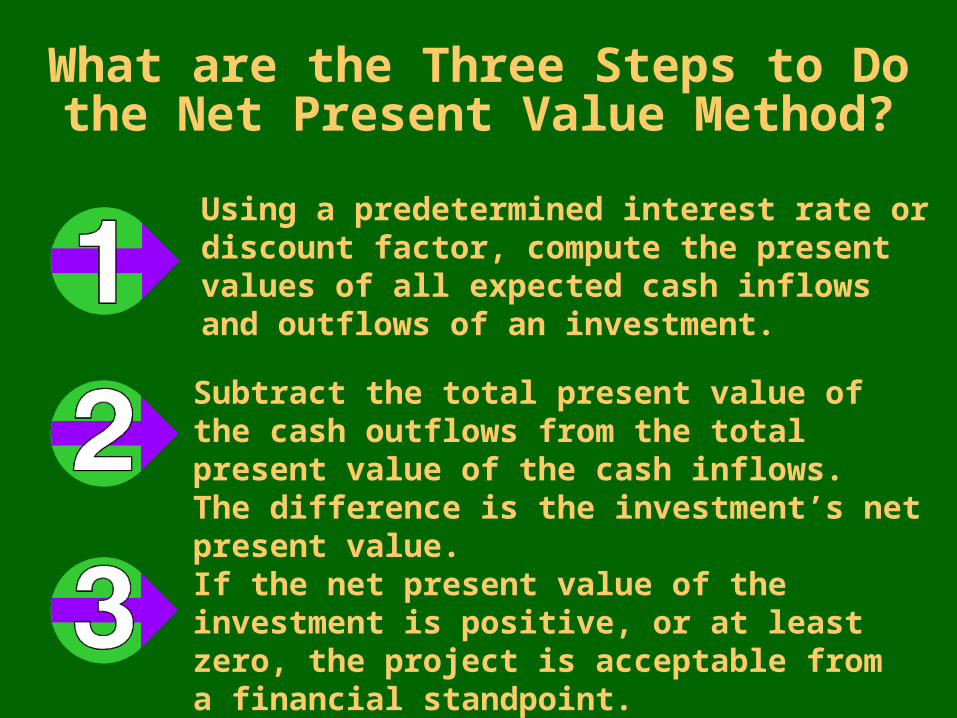

What are the Three Steps to Do the Net Present Value Method?

If the net present value of the investment is positive, or at least zero, the project is acceptable from a financial standpoint.

Subtract the total present value of the cash outflows from the total present value of the cash inflows. The difference is the investment’s net present value.

Using a predetermined interest rate or discount factor, compute the present values of all expected cash inflows and outflows of an investment.

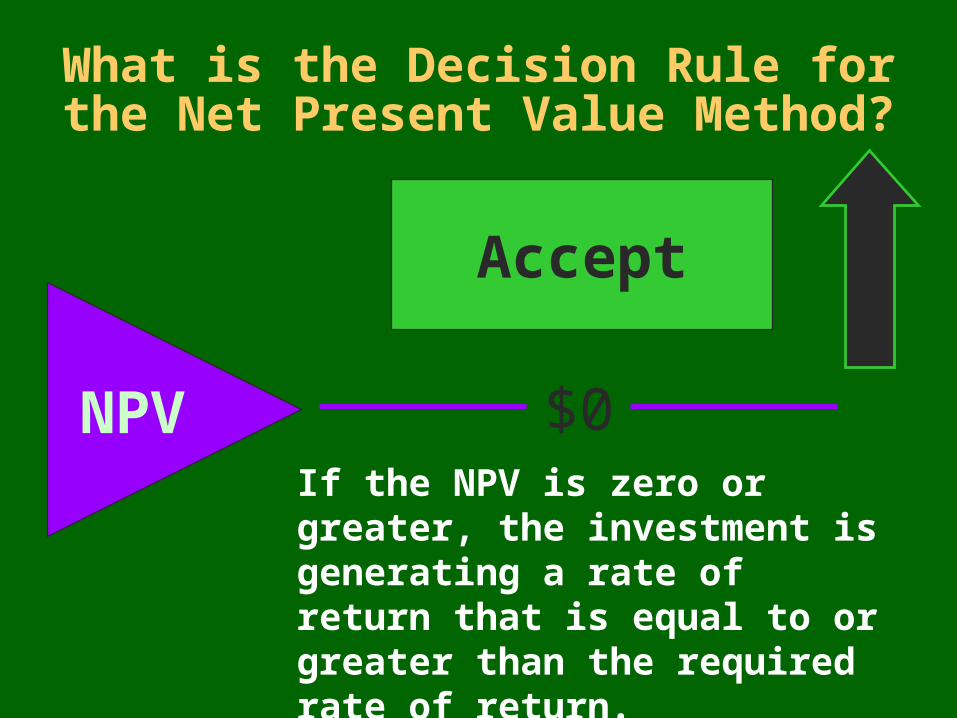

What is the Decision Rule for the Net Present Value Method?

NPV $0

Accept

If the NPV is zero or greater, the investment is generating a rate of return that is equal to or greater than the required rate of return.

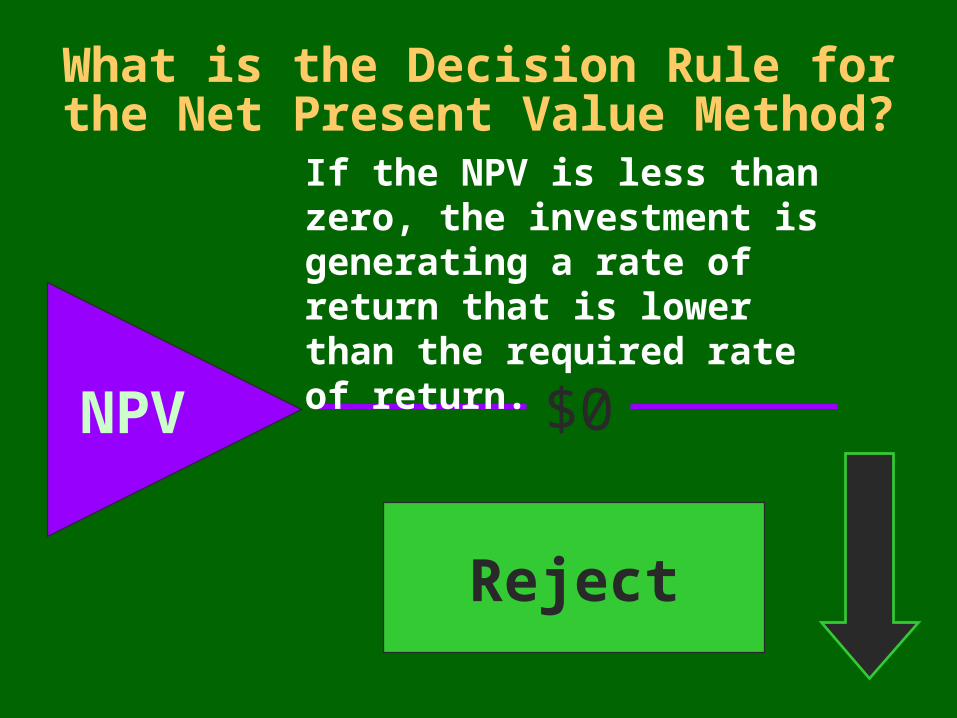

NPV $0

Reject

If the NPV is less than zero, the investment is generating a rate of return that is lower than the required rate of return.

What is the Decision Rule for the Net Present Value Method?

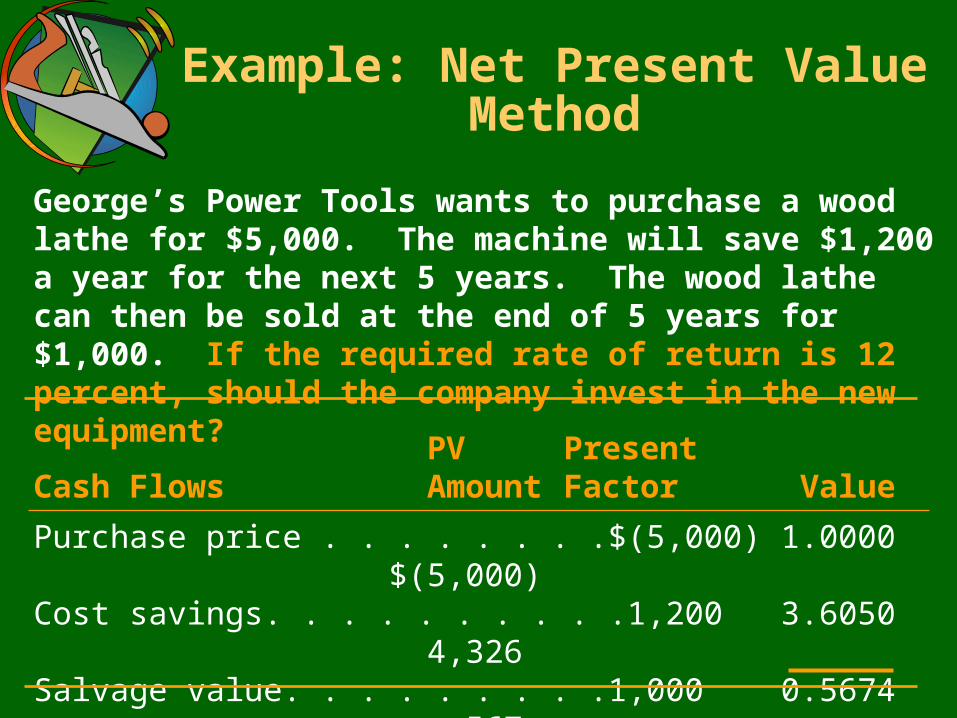

George’s Power Tools wants to purchase a wood lathe for $5,000. The machine will save $1,200 a year for the next 5 years. The wood lathe can then be sold at the end of 5 years for $1,000. If the required rate of return is 12 percent, should the company invest in the new equipment?

Example: Net Present Value Method

PV PresentCash Flows Amount Factor Value

Purchase price . . . . . . . . $(5,000) 1.0000 $(5,000)Cost savings. . . . . . . . . . 1,200 3.6050 4,326 Salvage value. . . . . . . . . 1,000 0.5674 567 Net present value. . . . $ (107)

What is a Least-Cost Decision?

Least-cost decision:

A decision to undertake the project with the smallest negative net present value.

Such a decision satisfies certain requirements at the lowest possible cost to the firm.

Least-cost decision:

A decision to undertake the project with the smallest negative net present value.

Such a decision satisfies certain requirements at the lowest possible cost to the firm.

In cases where investments must be made, managers should use a least-cost decision.

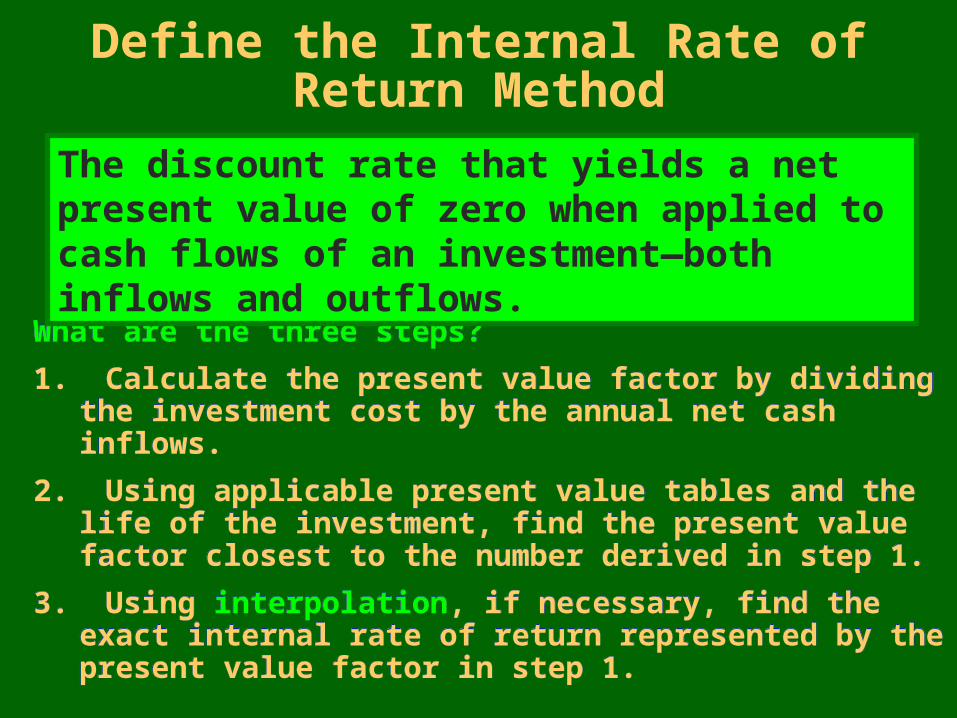

What are the three steps?

1. Calculate the present value factor by dividing the investment cost by the annual net cash inflows.

2. Using applicable present value tables and the life of the investment, find the present value factor closest to the number derived in step 1.

3. Using interpolation, if necessary, find the exact internal rate of return represented by the present value factor in step 1.

What are the three steps?

1. Calculate the present value factor by dividing the investment cost by the annual net cash inflows.

2. Using applicable present value tables and the life of the investment, find the present value factor closest to the number derived in step 1.

3. Using interpolation, if necessary, find the exact internal rate of return represented by the present value factor in step 1.

The discount rate that yields a net present value of zero when applied to cash flows of an investment—both inflows and outflows.

Define the Internal Rate of Return Method

Internal Rate of Return The “true” discount rate that will produce a net

present value of zero when applied to the cash flows of investment inventory goods held for resale.

What is Interpolation? A method of determining the internal rate of return

when the factor for that rate lies between the factors given in the present value table.

Its purpose is to determine the “true” rate of interest indicated by the present value factor.

Internal Rate of Return Method

What is a Hurdle Rate?

Hurdle rate:

To determine the value of an investment, management must compare the project’s internal rate of return with the company’s usual discount or hurdle rate.

Hurdle rate:

To determine the value of an investment, management must compare the project’s internal rate of return with the company’s usual discount or hurdle rate.

The minimum rate of return that an investment must provide in order to be acceptable.

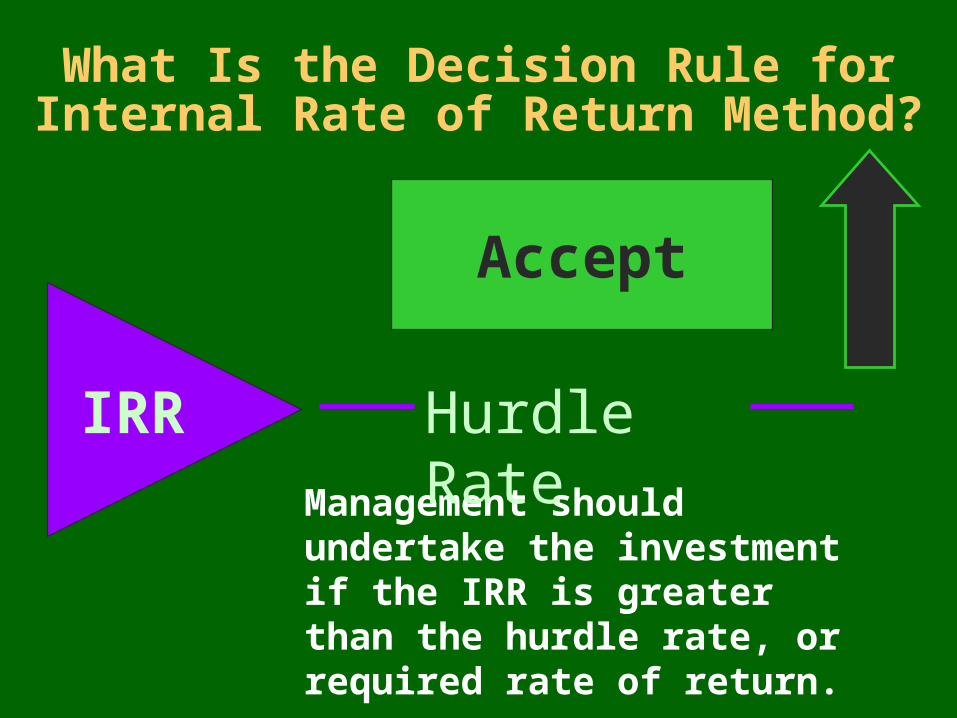

What Is the Decision Rule forInternal Rate of Return Method?

Accept

Management should undertake the investment if the IRR is greater than the hurdle rate, or required rate of return.

IRR Hurdle Rate

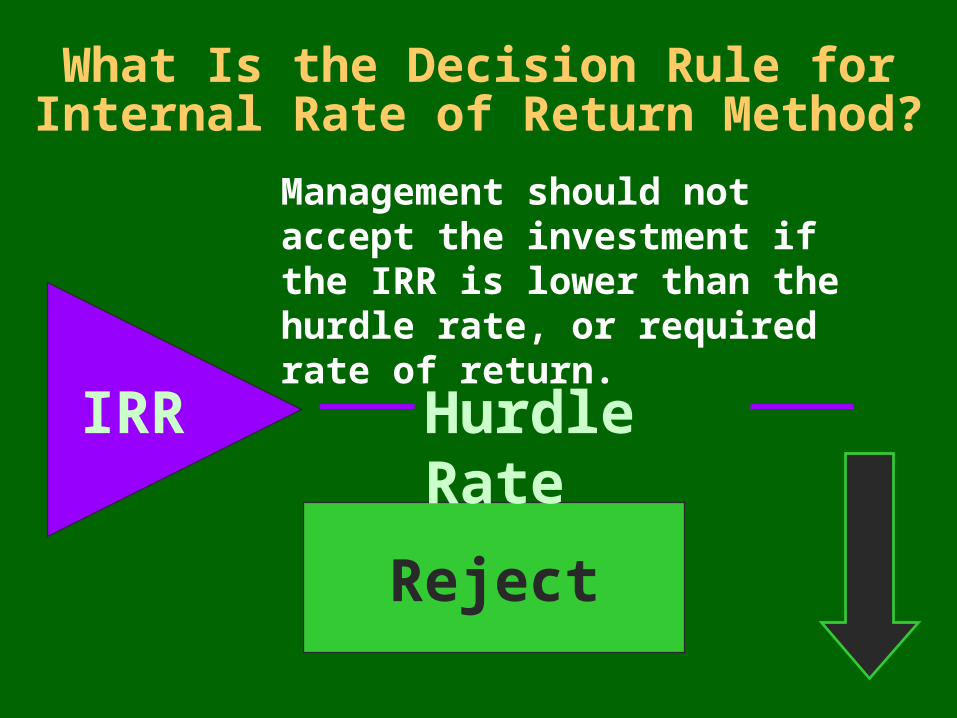

Reject

Management should not accept the investment if the IRR is lower than the hurdle rate, or required rate of return.

What Is the Decision Rule forInternal Rate of Return Method?

IRR Hurdle Rate

Learning Objective 4

Understand the need for evaluating qualitative factors in strategic and capital investment decisions.

$$

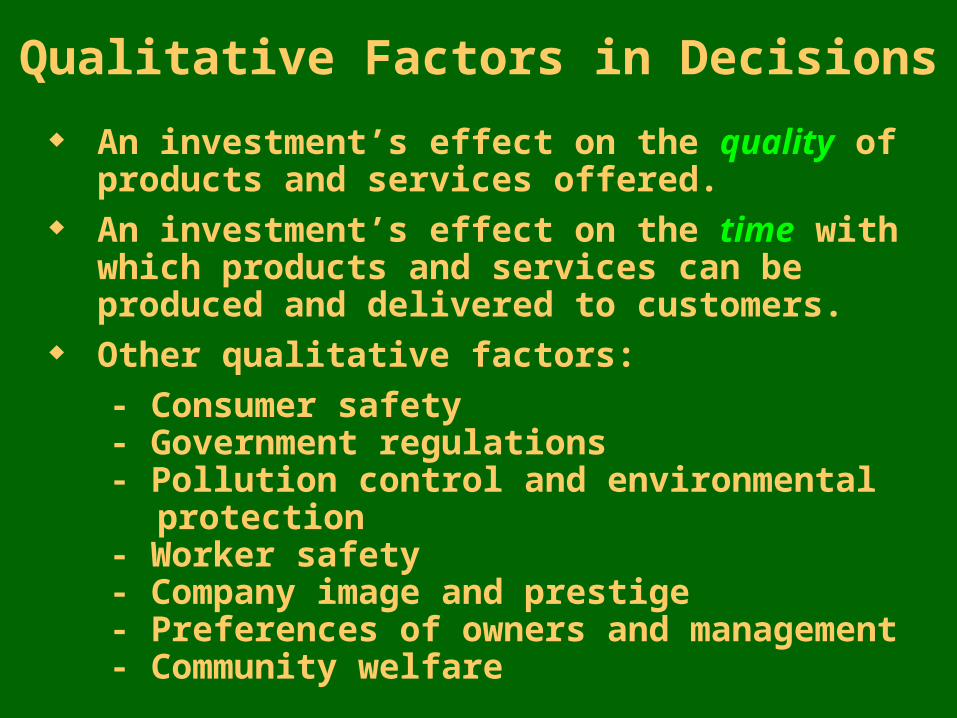

Qualitative Factors in Decisions

An investment’s effect on the quality of products and services offered.

An investment’s effect on the time with which products and services can be produced and delivered to customers.

Other qualitative factors:

- Consumer safety- Government regulations- Pollution control and environmental protection- Worker safety- Company image and prestige- Preferences of owners and management- Community welfare

Expanded MaterialLearning Objective 5

Use sensitivity analysis to assess the potential effects of uncertainty in capital budgeting. ??

Define Sensitivity Analysis

Sensitivity Analysis

A method of assessing the reasonableness of a decision that was based upon estimates; involves calculating how far reality can differ from an estimate without invalidating the decision.

Used to determine whether the conclusions still seem reasonable under modified circumstances.

Sensitivity Analysis

A method of assessing the reasonableness of a decision that was based upon estimates; involves calculating how far reality can differ from an estimate without invalidating the decision.

Used to determine whether the conclusions still seem reasonable under modified circumstances.

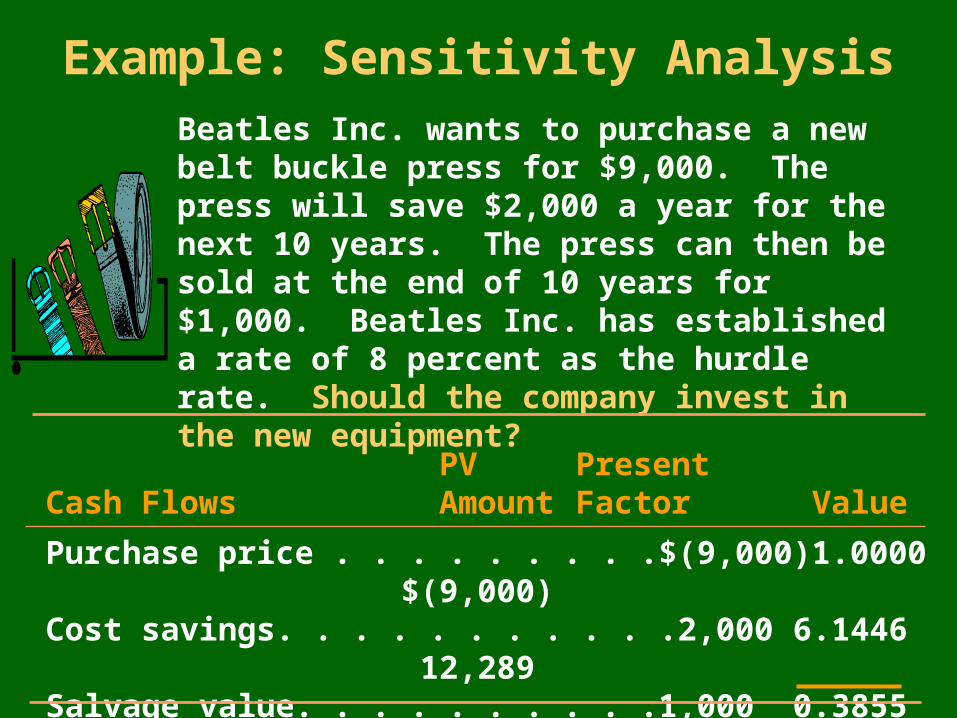

Beatles Inc. wants to purchase a new belt buckle press for $9,000. The press will save $2,000 a year for the next 10 years. The press can then be sold at the end of 10 years for $1,000. Beatles Inc. has established a rate of 8 percent as the hurdle rate. Should the company invest in the new equipment?

Example: Sensitivity Analysis

PV PresentCash Flows Amount Factor Value

Purchase price . . . . . . . . .$(9,000) 1.0000 $(9,000)Cost savings. . . . . . . . . . . 2,000 6.1446 12,289 Salvage value. . . . . . . . . . 1,000 0.3855 386 Net present value. . . . . $ 3,675

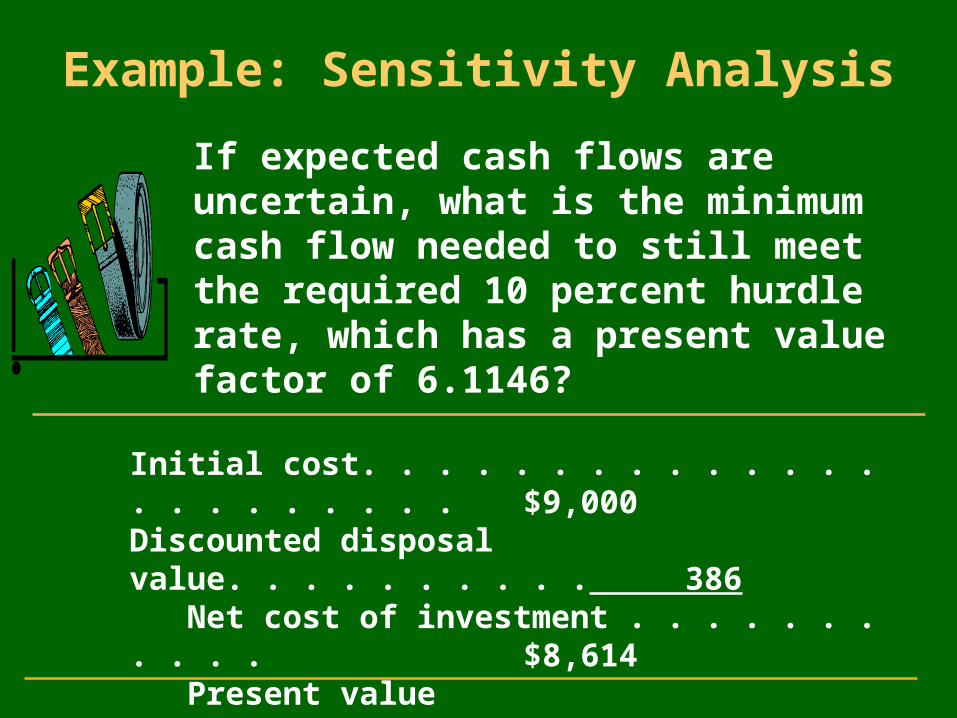

Example: Sensitivity Analysis

If expected cash flows are uncertain, what is the minimum cash flow needed to still meet the required 10 percent hurdle rate, which has a present value factor of 6.1146?

Initial cost. . . . . . . . . . . . . . . . . . . . . . . $9,000Discounted disposal value. . . . . . . . . . 386 Net cost of investment . . . . . . . . . . .$8,614 Present value factor . . . . . . .. . . . . 6.1146Minimum cash flows needed. . . . . . . $1,409

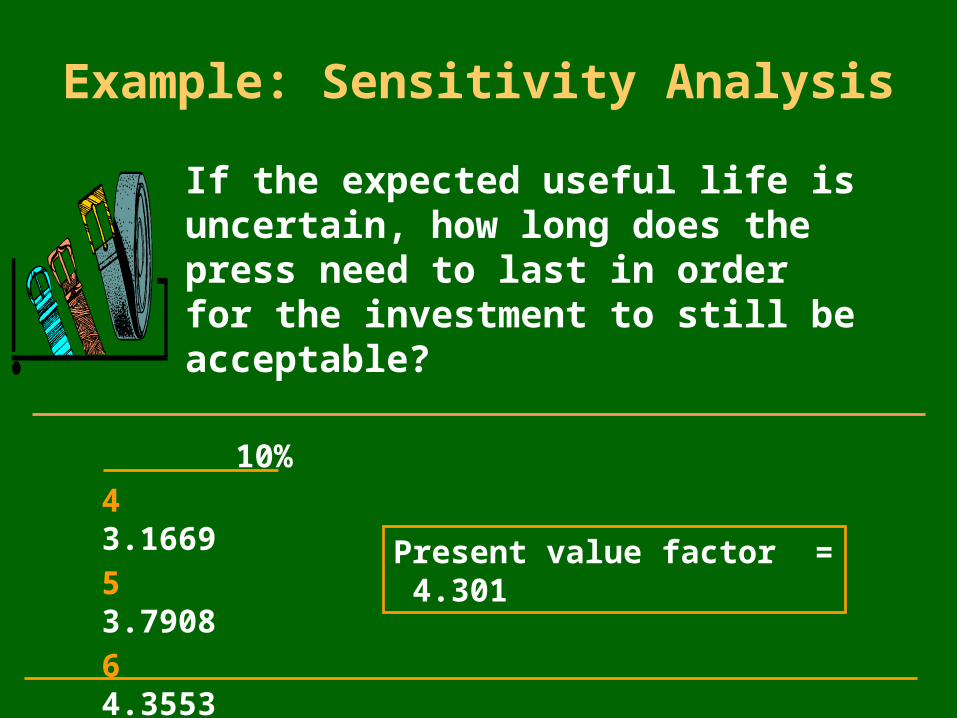

Example: Sensitivity Analysis

If the expected useful life is uncertain, how long does the press need to last in order for the investment to still be acceptable?

10%4 3.16695 3.79086 4.35537 4.8684

Present value factor = 4.301

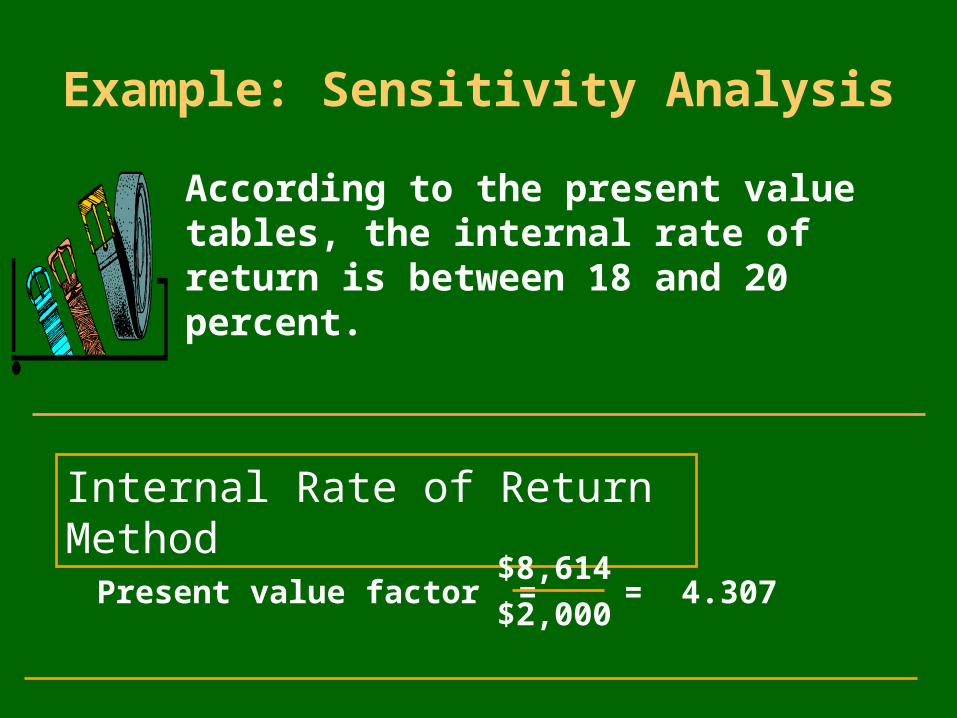

Example: Sensitivity Analysis

According to the present value tables, the internal rate of return is between 18 and 20 percent.

Internal Rate of Return Method

Present value factor =$8,614

$2,000= 4.307

Expanded MaterialLearning Objective 6

Explain how to use capital budgeting techniques in ranking capital investment projects.

What Is Capital Rationing?

Allocating limited resources among ranked acceptable investments.

Enables management to select the most profitable investments first.

Helps a company use limited resources to the best advantage by investing only in the projects that offer the highest return.

Either the internal rate of return method or the net present value method may be used in ranking investments.

Allocating limited resources among ranked acceptable investments.

Enables management to select the most profitable investments first.

Helps a company use limited resources to the best advantage by investing only in the projects that offer the highest return.

Either the internal rate of return method or the net present value method may be used in ranking investments.

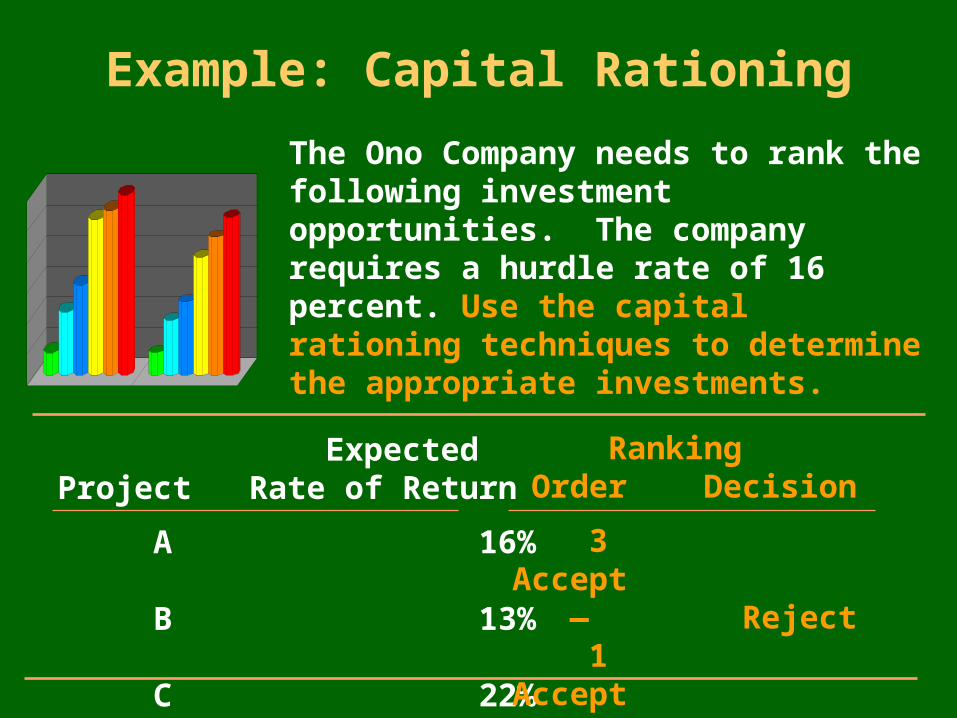

Example: Capital Rationing

The Ono Company needs to rank the following investment opportunities. The company requires a hurdle rate of 16 percent. Use the capital rationing techniques to determine the appropriate investments.

ExpectedProject Rate of Return

A 16% B 13% C 22% D 18%

Ranking Order Decision

3 Accept — Reject 1 Accept 2 Accept

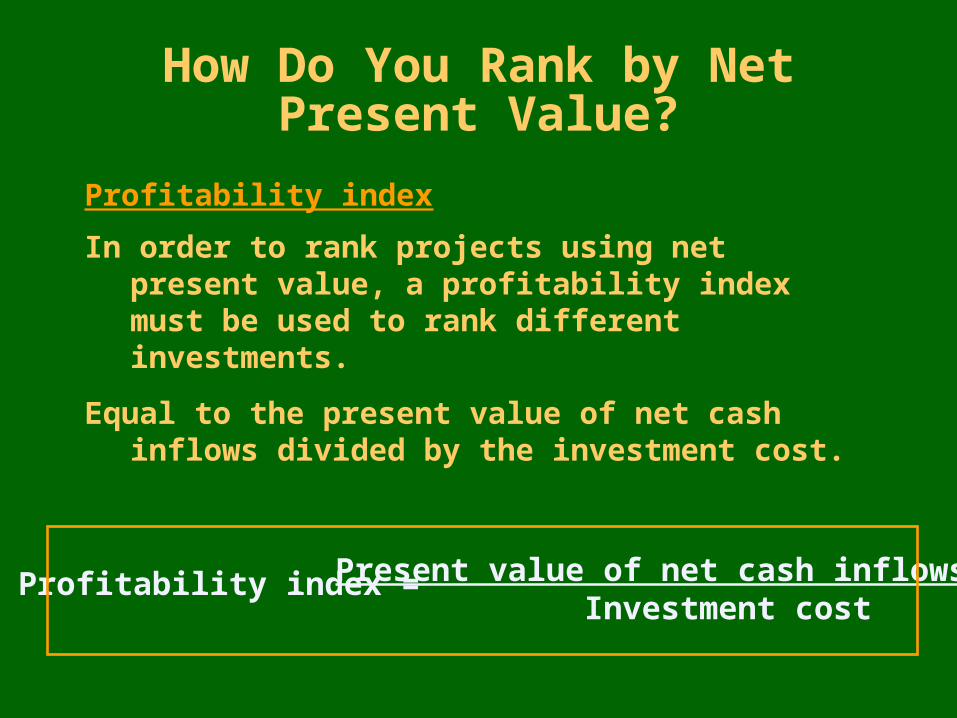

How Do You Rank by NetPresent Value?

Profitability index

In order to rank projects using net present value, a profitability index must be used to rank different investments.

Equal to the present value of net cash inflows divided by the investment cost.

Profitability index = Present value of net cash inflows Investment cost

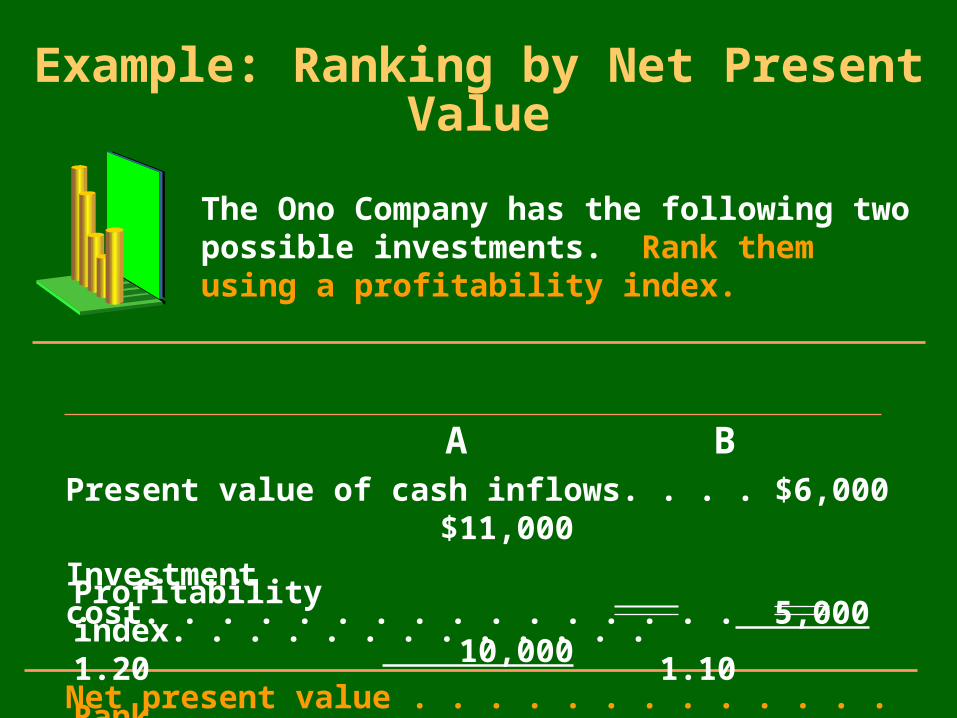

Example: Ranking by Net Present Value

The Ono Company has the following two possible investments. Rank them using a profitability index.

A B Present value of cash inflows. . . . $6,000 $11,000

Investment cost. . . . . . . . . . . . . . . . 5,000 10,000

Net present value . . . . . . . . . . . . . .$1,000 $ 1,000

Profitability index. . . . . . . . . . . . . 1.20 1.10

Rank . . . . . . . . . . . . . . . . . . . . . . . . 1 2

Expanded MaterialLearning Objective 7

Explain how income taxes affect capital budgeting decisions.

Income Tax Considerations

Examples of income tax effects: A capital investment may allow a company to

take an expense deduction for the cost of the asset and expense deductions for repairs and depreciation.

The resulting income from operations and any gain on the eventual sale of an asset are affected by taxes.

Such tax effects can be so significant that the net present value of the cash flows changes from positive to negative, or vice versa.

Income Tax Considerations

Cash inflows and outflows of capital budgeting decisions must be converted to after-tax amounts before the present values are computed.

They are converted to after-tax amounts by including such amounts as: Expense deduction for the cost of the asset. Expense deduction for repairs to the asset. Expense deduction for depreciation (MACRS). Income from operations. Gain on sale of disposal of asset.