bwi int l (2339 hk) - oriental patron intl (2339 hk...bwi int’l (2339 hk) a chinese-owned, global...

TRANSCRIPT

``

BWI Int’l (2339 HK)

A Chinese-owned, Global Auto Parts Leader with a strong product

A premier chassis supplier Beijing West Industries (BWI Group), the parent of

BWI Int’l (2339 HK) is a premier chassis supplier that designs and manufactures

brake and suspension systems for the global transportation market. BWI Intl

plans to acquire the profitable European auto suspension business from the

parent company for a consideration of HK$997mn to be settled by the issuance of

HK$697mn worth of new shares priced at HK$0.39 plus HK$300mn in cash to be

settled via funds raised from the capital markets. On 13 Nov 2004, the company

successfully raised the first tranche of HK$96mn out of the required HK$300m by

way of a private placement of 300mn new shares at HK$0.33/ share. We expect a

further share issuance to follow to bring the acquisition to completion by the end

of the year.

Investment Highlights 1) BWI Group owns a technologically advanced

suspension system (MagneRide Control Suspension System) that has been used

by the leading luxury automakers such Jaguar Land Rover, Audi, BMW and

Mercedes Benz given its superior performance characteristics compared to the

conventional electro-mechanical valve-based suspension system. This means

that it has the potential of enjoying increasing adoption over time. 2) BWI Group,

although Chinese owned, is essentially a high quality global MNC rather than a

conventional domestic Chinese manufacturer given that it originates from a

leading Western auto parts unit within Delphi Group which was acquired by BWI

in 2009. 3) Chinese ownership will have beneficial impact on the operations as

the gradual shift of production to the mainland will help to reduce production costs,

improve profitability and open a very big and yet untapped market in China. 4)

The company is primarily focused the strongest part of the auto market which is

luxury segment. 5) Within the European luxury vehicle segment, BWI Group is a

leading premium suspension system supplier with a strong market share 6) BWI

Group is also in the after sales market, a steady and recurring business where it

sells shock absorbers under the de Carbon brand. 7) BWI Group is injecting the

profitable European business first into the listco; to be followed North American

and China businesses respectively once they have met a certain threshold. We

expect BWI North America to be injected in 2016 and BWI China in 2018.

Valuation Based on our preliminary estimates which assume the listco has no

major liabilities or continued losses from the legacy, BWI Intl’s is likely to achieve

RMB137mn/RMB150mn net profits or HK$0.034/HK$0.037 fully diluted EPS in

FY14/15E. The fair value of HK$0.56 per share at 15x FY15E PE or 25%

premium to peers, in our view, is justified by (1) potential further asset injections

from parent group to double its revenue scale, (2) leading market position in

global brake and suspension system market, and (3) strong shareholder

background.

Risks 1) Client concentration 2) Pricing pressure from OEMs 3) Slower than

expected new car sales 4) M&A execution risk

Wed, 26 Nov 2014

Equity Research

Automobile/ China

Vivien Chan

+852 2135 0248

OP Express

Not Rated

Close price: HK$0.35

Key Data

HKEx code 2339

12 Months High (HK$) 3.65

12 Month Low (HK$) 0.35

3M Avg Dail Vol. (mn) 10.99

Issue Share (mn) 2,518.92

Market Cap (HK$mn) 881.62

Fiscal Year 03/2012

Major shareholder (s) BWI Group (51.9%)

Source: Company data, Bloomberg, OP Research

Closing price are as of 25/11/2014

Price Chart

1mth 3mth 6mth

Absolute % -7.9 -10.3 -16.7

Rel. MSCI CHINA % -11.8 -7.4 -23.9

Company Profi le

Beijing West Industries (BWI Group) is

a premier chassis supplier that designs

and manufactures brake and

suspension systems for the global

transportation market.

Beijing West Industries Co., Ltd. is a

joint venture of Shougang Corporation,

and Beijing Fangshan State-Owned

Asset Management Co. Ltd.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jan/14 Apr/14 Jul/14 Oct/14

HK$2339 HK MSCI CHINA

Wed, 26 Nov 2014

BWI (2339 HK)

Page 2 of 19

Europe; Part One of a Three-year plan

On 5 August 2014, parent co BWI announced that it would inject BWI Group's

European assets (BWI Europe) into BWI International (2339HK) listco for a

combination of shares and cash/convertible bonds. The transaction is valued at

HK$997mn to be satisfied by the issuance of 1.79bn news shares at 39cents per

share to the parent co and the remaining balance of HK$300mn to be paid for by

a combination of cash and convertible bonds, the ratio of which has yet to be

decided. Post the share issuance BWI parent co would end up with 75.47% of the

enlarged share capital of 2339 HK listco (before CB dilution). Upon conversion

of the CB, BWI’s stake will further increase to 79.18% and because BWI has

undertaken to ensure that the minimum public free float requirement is met, that it

would want to place out shares as an alternative to the issuance of the CBs.

On 13 Nov 2014, BWI International successfully raised net proceeds of HK$96mn

by a private placement of 300mn new shares at HK33 cents per share to

institutional investors. Post this round of fundraising BWI Group and associates

owned 51.88% of the listco, before the injection of BWI Europe.

BWI Europe is one of the leading automobile controlled and passive suspension

products manufacturers in Europe and according to an Ipsos Report, in 2013,

was the fifth largest automobile controlled and passive suspension products

manufacturer in Europe by revenue and accounted for approximately 3.4% of the

total revenue in the automobile controlled and passive suspension products

industry in Europe. BWI Europe principally engages in design, research and

development and manufacturing of automobile controlled and passive

suspension products for premium passenger vehicle manufacturers and the

provision of technical services for suspension products.

BWI Europe has three main facilities in Europe. The production centre in the

United Kingdom focuses on automobile controlled suspension products, the

production centre in Poland on both controlled and passive suspension products,

and a technical centre in France focuses on testing and research and

development of both automobile controlled and passive suspension products and

a technical centre in Poland which focuses on technical services. BWI Europe

also has four sales offices located in Poland, the United Kingdom, France and

Germany, each of which serves the respective customers allocated to them.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 3 of 19

The transaction background

Parent co BWI Group acquired Delphi Group’s automobile suspension business

for US$81mn in 2009. At the time, Delphi had filed for Chapter 11 citing high labor

costs as the main reason for its technology being deemed to be a non-core asset

and requiring significant investment in R&D and capex. Under BWI Group’s

leadership, the business turned around to positive profit, and the parent now

plans to inject the European part of the suspension business into the listco.

The European suspension business generated a net profit of HK$142mn in FY13

on a net asset value for HK$508mn. The consideration of the injection was

HK$997mn, which translates to 7x FY13 PE and 1.9x FY13 PB.

The transaction structure

According to the announcement on 5 Aug. the total consideration of HK$997mn

will be settled by (1) HK$697mn (70% of total consideration) consideration share

or 1.79bn new shares at HK$0.39 to the parent, plus (2) HK$300mn cash or 5

years zero coupon with exercise price of HK$0.39 or issue new shares, or

combination of all possibilities.

Part 1 completed: HK$96mn raised

On 13 Nov. 2014, BWI Int’l announced that it successfully raised HK$96mn via a

new share issuance of 300mn new shares to investors at HK$0.33 per share.

After the placement, parent company BWI Group’s stake was been diluted from

58.06% to 51.88%.

Exhibit 1: The details of new shares placement on 11 Nov.

Shareholders shareholdings before the placement Shareholdings after the placement

Number of shares (mn) Approximate % Number of shares (mn) Approximate %

BWI 1,462.5 58.06 1,462.5 51.88

Placees - - 300.0 10.64

Public shareholders 1,056.4 41.94 1,056.4 37.48

Total 2,518.9 100.00 2,818.9 100.00

Wed, 26 Nov 2014

BWI (2339 HK)

Page 4 of 19

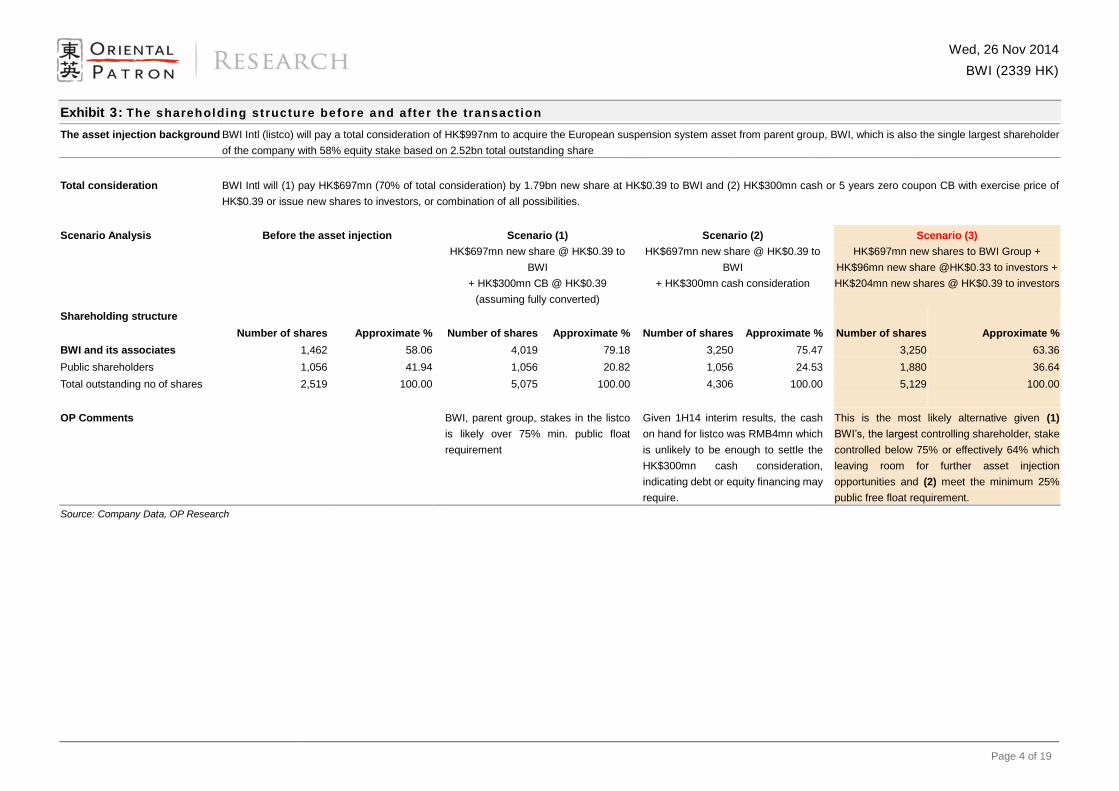

Exhibit 3: The shareholding structure before and after the transaction

The asset injection background BWI Intl (listco) will pay a total consideration of HK$997nm to acquire the European suspension system asset from parent group, BWI, which is also the single largest shareholder

of the company with 58% equity stake based on 2.52bn total outstanding share

Total consideration BWI Intl will (1) pay HK$697mn (70% of total consideration) by 1.79bn new share at HK$0.39 to BWI and (2) HK$300mn cash or 5 years zero coupon CB with exercise price of

HK$0.39 or issue new shares to investors, or combination of all possibilities.

Scenario Analysis Before the asset injection Scenario (1)

HK$697mn new share @ HK$0.39 to

BWI

+ HK$300mn CB @ HK$0.39

(assuming fully converted)

Scenario (2)

HK$697mn new share @ HK$0.39 to

BWI

+ HK$300mn cash consideration

Scenario (3)

HK$697mn new shares to BWI Group +

HK$96mn new share @HK$0.33 to investors +

HK$204mn new shares @ HK$0.39 to investors

Shareholding structure

Number of shares Approximate % Number of shares Approximate % Number of shares Approximate % Number of shares Approximate %

BWI and its associates 1,462 58.06 4,019 79.18 3,250 75.47 3,250 63.36

Public shareholders 1,056 41.94 1,056 20.82 1,056 24.53 1,880 36.64

Total outstanding no of shares 2,519 100.00 5,075 100.00 4,306 100.00 5,129 100.00

OP Comments BWI, parent group, stakes in the listco

is likely over 75% min. public float

requirement

Given 1H14 interim results, the cash

on hand for listco was RMB4mn which

is unlikely to be enough to settle the

HK$300mn cash consideration,

indicating debt or equity financing may

require.

This is the most likely alternative given (1)

BWI’s, the largest controlling shareholder, stake

controlled below 75% or effectively 64% which

leaving room for further asset injection

opportunities and (2) meet the minimum 25%

public free float requirement.

Source: Company Data, OP Research

Wed, 26 Nov 2014

BWI (2339 HK)

Page 5 of 19

Exhibit 2: Shareholding structure before and af ter the t ransaction based on Scenario (3)

Source: Company Data, OP Research

Scenario (1) – HK$697mn new shares plus HK$300mn CB to BWI, BWI

Group’s (the current largest controlling shareholder) stake in the listco will

increase from 58% to 79% based a total share base of 5.1bn which would

contravene the 25% minimum public float requirement.

Therefore, we believe the transaction is more likely to be settled by Scenario (2)

HK$697mn new share plus HK$300mn cash to BWI, which leaves BWI Group

with a 75.5% equity stake in the listco based on a total share base of 4.3bn, and

allows room for the listco to undertake further asset injection opportunities in the

future.

However, given the listco only had RMB4.3mn cash balance as at the end of June

2014, we believe the listco is likely to raise debt from bank or equity financing

from the capital markets to pay for the HK$300mn cash consideration. We believe

that Scenario (3) HK$697mn new share to BWI + HK$96mn new share

@HK$0.33 to investors + HK$204 settled by fund raising in the capital

market will be the company’s preferred option given that (1) BWI Group’s

controlling stake will be well below 75% at 64% which leaves room for further

asset injection opportunities and (2) meets the minimum 25% public float

requirement.

Shougang

Corporation

Before the transaction

Fangshan District of

Beijing Municipality

BWI Group

BWI Int’l (2339 HK)

Public

55.45% 44.55%

58.06% 41.94%

Shougang

Corporation

After the transaction

Fangshan District of

Beijing Municipality

BWI Group

BWI Int’l (2339 HK)

Public

55.45% 44.55%

63.36% 36.64%

Wed, 26 Nov 2014

BWI (2339 HK)

Page 6 of 19

Parent Company Background – A premier chassis supplier

Beijing West Industries (BWI Group), the parent of BWI Int’l (2339 HK) is a

premier chassis supplier that designs and manufactures brake and suspension

systems for the global transportation market. The company started as Dayton

Engineering Laboratory Company (Delco), in Day- ton, Ohio. In 1927, Delco

Products was created as part of General Motors (GM) and focused on automotive

suspension products.

In 2009, BWI Group acquired Delphi Corporation’s (formerly Delco) suspension

and brake businesses (formerly known as Delphi Chassis Systems). Today, BWI

Group’s Controlled Suspensions business supplies to many global automotive

and motorcycle OEMs including General Motors, Jaguar-Land Rover, Audi, BMW

and Ferrari amongst others.

BWI Group is a company established in PRC with a registered capital of

RMB1.32bn. It is 55.45% is owned by Shougang corporation, a state-owned

enterprise under the State-Owned Asset Supervision and Administration

Commission of the People’s Government of the Beijing Municipality of the PRC

(北京市人民政府政府國有資產監督管理委員會). BWI Group’s remaining 44.55%

stake is held by Fangshan SOA Management, a company under the State-owned

Assets Supervision and Administration Commission of the People’s Government

of the Fangshan District of Beijing Municipality (北京市房山區人民政府國有資產

監督管理委員會 ). Shougang Corporation is one of China’s largest steel

corporations which intends to grow its auto parts footprint globally with BWI Intl

(2339 HK) as its flagship list co.

BWI Europe

BWI Europe is one of the leading automobile controlled and passive suspension

products manufacturers in Europe and according to an Ipsos Report, in 2013,

was the fifth largest automobile controlled and passive suspension products

manufacturer in Europe by revenue and accounted for approximately 3.4% of the

total revenue in the automobile controlled and passive suspension products

industry in Europe. BWI Europe principally engages in design, research and

development and manufacturing of automobile controlled and passive

suspension products for premium passenger vehicle manufacturers and the

provision of technical services for suspension products.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 7 of 19

Exhibit 3: Major products of BWI Europe

Source: Company

Wed, 26 Nov 2014

BWI (2339 HK)

Page 8 of 19

Investment Highlights

Asset injection opportunities

BWI Group acquired Delphi’s global controlled and passive suspension assets in

2009 and believes that the time is right to inject the European business into the

listco. BWI Intl (2339 HK) is the only listed vehicle related to automobile parts

business for BWI Group and management has indicated that the parent company

will at the appropriate time inject the company’s North American and Chinese

suspension businesses into the listco.

BWI North America

With the exception of BWI Group’s production facility in Chihuahua, Mexico, the

Group’s headquarters, R&D and management centers are all located in the US.

The Mexican production plant manufactures passive suspension systems and

mainly supplies its products to GM, Chrysler and Ford, etc. According to

management, the North American business recorded an unaudited revenue of

roughly USD150mn and incurred a net loss of ~USD22mn in 2013.

Conservatively, management expects to be able to generate revenues of

USD175mn but still incur a net loss of between USD28mn-USD30mn in FY14,

which will mainly be attributable to high costs, and in particular, given that the

North American region bears R&D and management costs for China.

Going forward, BWI Group’s various divisions including production/sales and

R&D/management will be split by region. Management expects that will result in

higher profitability for BWI N. America by 2016 by which time the North American

suspension assets will be ready to be injected into the listco. Thereafter,

management expects the North American business to generate ~20% profit

growth per annum.

BWI China

BWI China is home to two facilities; a braking system production plant in

Shanghai and a newer suspension system production plant in Fangshan District,

Beijing. BWI China is a key supplier to domestic automobile OEMs such as Buick,

GM for their high-end vehicles. BWI China is currently loss making given low

utilization at the Shanghai facility, and as Beijing production has just begun

ramping up. Management expects to be able to turn this business around by 2017

on more rigorous cost controls and aggressive sales strategies. Management

plans to set up another production facility in Southern China to cater to local

demand once the production at the two existing facilities reaches an acceptable

threshold.

1) R&D localization Suspension system providers are involved in the initial

stages of R&D and design processes with the auto brand owners. BWI Group

plans to meaningfully reduce R&D costs going forward by localizing the

suspension system R&D process in China. The parent company will transfer

key R&D personnel from the US to China, who will be responsible for training

the local R&D employees. Management estimates that this initiative alone will

be able to save USD6mn – USD8mn in annual R&D expenses.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 9 of 19

2) Relocation from Shanghai Free Trade Zone BWI China’s Shanghai plant

which is currently located in the Shanghai Waigaoqiao Free Trade Zone will

be relocated to a more suburban area which will be able to result in annual

rental savings of USD5mn.

3) Untapped potential of domestic mid-end passenger vehicle brands BWI

Group is the only SOE in China which owns the intellectual property rights of

a high-end suspension manufacturing system in China. BWI Group is

therefore eligible to benefit from supportive domestic auto component

policies and has recently begun to raise their profile amongst the domestic

mid-end vehicle OEMs. BWI China currently supplies suspension systems to

30-40 domestic/JV auto OEMs, including Buick, Shanghai GM, Shanghai GM

Wuling, Dongfeng Yulon Motor, Beijing Auto Group and Changan Auto

amongst others and expects to further penetrate this market in the future.

4) Domestic M&A opportunities BWI Europe is also on the lookout for

domestic braking system M&A targets with reputable technology and market

share.

5) Expansion into after-market sales The NDRC’s recent initiatives to put a

stop to monopolistic behavior in spare parts by the major OEMs and open up

the market to other non-authorized spare parts makers will be a major

positive for the suspension systems division.

BWI China is expected to post revenues of USD240mn and a net loss of between

USD3-USD4mn in 2014. BWI Group conservatively has earmarked the next 3

years for major restructuring efforts and expects the business to turnaround by

2017, ahead of the injection of the China’s suspension business into the listco by

2018.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 10 of 19

Earnings growth supported by strong luxury vehicle sales

BWI Europe’s largest customer Jaguar/Land-Rover reported a 11%yoy growth in

global sales in 10M14 over 33,512 units, while 35% growth in China and 4%

sales up in North America and in Europe. Expecting strong growth in China, JLR

recently established a JV with local brand Chery Auto to manufacture Jaguar and

Land Rover vehicles in China. According to reports, the construction of the JV’s

first production facility in Changshu is now underway.

BMW which a/c for 11% of BWI Europe’s revenues, achieved global sales growth

of 7% yoy in 10M14 to 1.7mn units, and expects global sales of over 2mn units in

2014. BMW and MINI European sales rose 11% to 78,483 units in October. It also

saw double-digit growth in several European markets, such as France were up

25%; Italy also delivered a monthly rise of 20% compare to Oct. 2013. BMW’s

deliveries increased 4.1% in Europe for 10M14.

Separately, Mercedes-Benz recorded a sales growth of 11.5%yoy in 10M14

globally, and European sales growth of 7.8% yoy in 10M14.

The European auto market is expected to pick up this year after six years of

decline. And car makers expect European Union sales to growth 3% this year.

BWI Europe expects a 6.7% earnings CAGR growth from 2015 to 2019, which

will be facilitated by a new Czech production plant which is expected to be online

by 2017. According to current plans, Production capacity in Poland will grow from

current 9.5mn suspension component units to over 10mn units by 2016, China

capacity from 1.2mn units to 2mn in near term. The UK and US facilities will

continue to produce 2mn sets suspension and 8mn suspension component units

respectively.

Exhibit 4: Revenue breakdown by segment

Source: Company data, OP Research

968 998 1,217

472 603

1,038 1,099

1,168

551 559

119 88

92

32 40

0

500

1,000

1,500

2,000

2,500

3,000

2011 2012 2013 5M13 5M14

(RMB mn)

Controlled suspension Passive suspension Technical services income

Wed, 26 Nov 2014

BWI (2339 HK)

Page 11 of 19

Exhibit 5: Forecast order growth

Source: Company data, OP Research

Cost savings from increased China production

BWI China has a current annual capacity of 1.2mn units, whilst the group’s

production plants in Poland and UK each have a current production capacity of

9.5mn units and 2mn sets respectively. The Group plans to further ramp up

capacity in China to meet the demands of their key customers all of which are

growing their presence on the Mainland, and over time will make China a key

manufacturing centre, which management expects will reduce production costs

and enhance overall profitability.

Strong order backlog from blue chip customers

Automobile controlled and passive suspension products are tailored according to

the specifications provided by automobile OEMs which mean that suspension

suppliers and vehicle ODMs work very closely from a very early stage in the

suspension design stage. Typically, OEMs invite several suspension system

providers to propose their respective solutions, the best or most appropriate of

which will be chosen to be the preferred vendor. BWI has worked closely with all

the leading luxury automobile brands, including Jaguar/Land-Rover, BMW/MINI,

Volvo, Mercedes-Benz, Audi, Porsche, Ferrari and Lamborghini since the Delphi

era.

According to management, OEMs usually sign a 3-year contract term with

suspension suppliers which may be for the life of a particular model which is why

BWI Group enjoys clear order backlog visibility. In addition, given that the

suspension system is a critical automobile component, especially for luxury

brands, OEMs infrequently switch between suppliers. BWI Group’s longstanding,

well-established relationships with the major luxury auto OEMs and the high

technological and safety requirements set by these marques represent high

barriers to entry.

10,500 10,900 11,000 11,000 11,000

250 1,050

2,600

0

4,000

8,000

12,000

16,000

2015 2016 2017 2018 2018

(units '000)

Poland Czech

Wed, 26 Nov 2014

BWI (2339 HK)

Page 12 of 19

Exhibit 6: Client Mix

Source: Company data, OP Research

Strong Aftermarket Potential

BWI Europe also sells its products to aftermarket under the brand “de Carbon” via

distributors throughout Europe. Aftermarket sales generated RMB64mn of

revenue in FY13, or ~2.6% of total sales. According to Ipsos Report, in 2012, the

size of the global suspension aftermarket was around US$12bn, with the EU the

largest market, accounting for 29% of total. Western Europe UK, Germany,

France, Italy and Spain) represented 57% of EU. BWI Group aims to further

penetrate the suspension system aftermarket segment which will be another

meaningful profit driver given that the aftermarket segment gross margin is 50%

compared with 23% - 25% in the primary market. BWI Group estimates

aftermarket sales to expand from HK$80mn in 2014 to HK$170mn by 2017.

Exhibit 7: Aftermarket sa les forecast

Source: Company data, OP Research

Jaguar/Land Rover49%

BMW/MINI11%

GM5%

Citroen/Peugeot4%

Volvo3%

Others28%

40 40 40 40

4570

95

130

0

40

80

120

160

200

2014 2015 2016 2017

(HK$ mn)

UK Poland

Wed, 26 Nov 2014

BWI (2339 HK)

Page 13 of 19

Valuation

The target company reported a net profit of RMB114mn in FY13, and a net profit

of RMB75mn in 5M14, up 25% yoy compared with 5M13. Management believes

BWI Europe to deliver net profit growth of 20% in 2014, and a sustainable

10%-15% profit growth beyond 2015.

Based on our preliminary estimates which assume the listco has no major

liabilities or continued losses from the legacy, BWI Intl’s is likely to achieve

RMB137mn/RMB150mn net profits or HK$0.034/HK$0.037 fully diluted EPS in

FY14/15E based on 5.129bn outstanding shares.

The fair value of HK$0.56 per share at 15x FY15E PE or 25% premium to peers

average 12x FY15E PE, in our view, is justified by (1) potential further asset

injections from parent group, the North American in 2016 and China business in

2017, which with similar sales scale (USD150mn sales for North American

business and USD240mn sales for China business as compared to ~USD380mn

sales for European business in FY14E), (2) a leading market position in global

brake and suspension system market, and (3) strong shareholder backgrounds.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 14 of 19

Investment risks

Client concentration

In 2013, Jaguar/Land Rover was BWI Europe’s single largest customer

accounting for 49% of BWI Europe’s revenue followed by BMW 11%, GM 5%,

Peugeot/Citroen 4% Volvo 3% respectively.

Cost pressure from OEM

According to management, OEMs typically ask for discounts on auto parts which

BWI Europe will need to mitigate by streamlining costs.

Slower than expected luxury vehicle sales

Given BWI Europe’s exposure to the luxury passenger vehicle market, slower

than expected sales will hurt the company’s revenue and profitability.

Currency risk

BWI Europe’s reporting currency is in RMB, whilst sales and expenses are

denominated in a mixture of foreign currencies including USD, Pound Sterling,

Polish Zloty and Euro. For example, in the first five months of this year, BWI

Europe recorded an exchange loss of RMB10.3mn mainly on RMB appreciation.

M&A execution risk

BWI’s solid earnings growth in future and stock re-rate catalysts are highly related

to the successfully of injection and further M&A events. BWI needs to overcome

the obstacle of culture, politics and managements of different regions. Any

shortfall may cause failure, and that will adversely hurt investment sentiment, as

well as earnings forecasts and valuations.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 15 of 19

Management profile

Mr. Jiang Yunan (蔣運安), Executive Director and Managing Director, aged 53,

responsible for the overall business development and day-to-day management of

the group. Prior joined BWI, he served in various positions in the groups of

Shougang Corporation. Since June 2014, Mr. Jiang started serving as the deputy

part secretary, a director and the president of BWI, where is responsible for the

implementation of strategy, business development and day-to-day management

of BWI Group.

Mr. Li Shaofeng (李少峰 ), Executive Director, aged 47, responsible for

overseeing the operations of the group. Mr. Li also holds various positions in

other listed companies, such as Shougang Concord Int’l Enterprises Company

Ltd; Shougang Fushan Resourses Group Ltd; and Global digital Creations

Holding Ltd.

Mr. Xu Ning (徐凝), Non-executive Director and the Chairman, aged 60,

responsible for providing leadership of the Board and ensuring the Board’s

working efficiently and performing its responsibilities. Mr. Xu is the member of the

standing committee of the communist party since 1996. He also has been the

director and deputy chairman of Beijing Shougang Company Ltd.

Mr. Zhang Yaochun (張耀春), Non-executive Director, aged 56, responsible for

scrutinizing the performance of the group. He was the chairman and GM of

Beijing City Fangshan District General Company in 2002. He has been the

chairman of the labour union of BWI in 2012.

Mr. Craig Allen Diem, Non-executive Director, aged 53, responsible for

scrutinizing the performance of the group. Mr. Diem is currently the director of

programme management and strategic development of BWI. He had served in

different positions in GM since 1983 with the last position as the country manager

of Korea. He was also transferred to Delphi Automotive Systems Limited. In 2001,

Mr. Diem became the product team leader of the brake corner team in Delphi

Automotive Systems.

Wed, 26 Nov 2014

BWI (2339 HK)

Page 16 of 19

Exhibit 8: Financial summary of BWI Europe

Year to Mar (RMB mn) FY11 FY12 FY13 5M13 5M14

Income Statement

Turnover 2,125 2,185 2,477 1,055 1,202

COGS (1,602) (1,673) (1,916) (816) (926)

Gross profit 523 513 561 239 276

Other revenue 15 11 21 3 15

Selling costs (36) (14) (14) (6) (13)

Administrative costs (425) (350) (411) (155) (170)

Other expenses (32) (11) (5) 0 (10)

Operating profit 46 149 151 80 97

Finance income (7) (6) (6) (2) (2)

Profit before tax 39 143 146 78 96

Taxation (10) (29) (32) (18) (20)

Net income 29 115 114 60 75

Balance Sheet (RMB mn)

Non-current assets 165 219 256 261

Current assets 668 781 831 991

Current liabilities 495 496 520 578

Non-current liabilities 116 171 161 163

Source: Company data, OP Research

Exhibit 9: Key financial ratios of BWI Europe

FY11 FY12 FY13 5M14

Inventory turnover days 25 29 29 25

A/C receivable turnover days 49 52 51 51

A/C payable turnover days 54 61 61 59

Current ratio 134.9% 157.6% 159.8% 166.2%

Quick ratio 111.9% 126.9% 130.8% 138.7%

Gearing ratio 62.4% 36.5% 25.4% 20.5%

Net debt / equity 4.5% Net cash Net cash Net Cash

Interest coverage (X) 6.2 24.9 26.8 49.7

ROE 12.9% 41.2% 30.8% N/A

ROA 3.5% 12.5% 10.9% N/A

Operating cash flow 69,360 136,708 169,490 42,659

Source: Company data, OP Research

Exhibit 10: Key financial summary of listco

(RMB mn) Year ended 31 March 2013 Six months end 30 June 2014

Revenue 133 39

Growth (%) -34%

Net profit 3 218

Growth (%) -52%

Diluted EPS (RMB) 0.003 0.102

Consensus EPS (RMB)

EPS growth (%) -53%

ROE (%) 1.7% 136.6%

P/E (x) 121.6 3.0

P/B (x) N/A 21.2

Yield (%) 0 0

DPS (HK$) 0 0

Source: Company data, OP Research

Wed, 26 Nov 2014

BWI (2339 HK)

Page 17 of 19

Exhibit 11: Peer Group Comparison

Company Ticker Price

Mkt cap

(US$m)

3-mth

avg t/o

(US$m)

PER

Hist (x)

PER

FY1 (x)

PER

FY2 (x)

EPS

FY1

YoY%

EPS FY2

YoY%

3-Yr EPS

Cagr (%) PEG (x)

Div yld

Hist (%)

Div yld

FY1 (%)

P/B Hist

(x)

P/B FY1

(x)

EV/

Ebitda

Hist

EV/

Ebitda

Cur Yr

Net

gearing

Hist (%)

Gross

margin

Hist (%)

Net

margin

Hist (%)

ROE

Hist

(%)

ROE

FY1

(%)

Sh px

1-mth %

Sh px

3-mth %

Beijingwest Indu 2339 HK 0.35 114 0.6 10.5 N/A N/A N/A N/A N/A N/A N/A N/A 19.35 N/A 73.3 N/A N/A 10.5 3.3 N/A N/A (7.9) (11.4)

HSI 23,843.91 10.3 11.1 10.3 (6.9) 7.4 3.2 3.48 3.8 3.6 1.34 1.32 13.0 11.9 2.3 (5.3)

HSCEI 10,782.91 7.5 7.3 6.8 1.6 7.5 6.3 1.16 4.1 4.4 1.13 1.09 15.2 14.9 3.8 (3.0)

CSI300 2,685.56 11.6 10.9 9.5 6.8 15.2 12.1 0.90 2.2 2.7 1.67 1.57 14.4 14.4 12.3 14.6

Adjusted sector avg* 16.0 13.3 10.6 35.4 18.4 25.2 0.54 1.8 1.7 3.34 3.63 10.4 8.6 21.6 16.9 5.6 16.1 21.5 5.7 1.4

Nexteer Automoti 1316 HK 6.40 2,061 2.1 13.8 13.5 10.7 1.7 26.2 17.8 0.76 1.1 1.5 3.63 2.72 9.9 7.3 46.4 14.2 4.6 29.6 22.6 (6.2) 9.8

Minth Group Ltd 425 HK 15.62 2,209 1.4 13.8 11.7 10.1 17.7 16.1 16.3 0.72 2.9 3.1 1.76 1.61 10.4 8.2 0.0 33.0 17.6 14.2 14.5 1.3 (3.5)

Xinchen China Po 1148 HK 3.71 616 1.1 13.2 12.9 10.0 2.3 29.1 40.8 0.32 N/A N/A 1.73 1.51 10.5 9.1 0.0 19.7 10.5 15.5 12.0 (8.4) (15.1)

Amer Axle & Mfg AXL US 20.94 1,586 22.7 17.0 9.4 8.3 82.0 12.7 27.5 0.34 N/A 0.0 9.37 7.65 7.0 5.7 4,181.8 14.9 2.9 N/A 131.7 18.2 16.3

Autoliv Inc ALV US 99.55 9,012 66.4 19.6 17.3 15.0 13.3 15.0 14.8 1.17 2.1 2.1 2.46 2.44 8.5 8.2 0.0 19.4 5.5 10.9 13.1 10.2 (3.7)

Delphi Automotiv DLPH US 72.81 21,558 146.2 18.7 14.4 12.8 30.1 12.4 19.3 0.74 1.4 1.4 7.46 6.88 10.6 9.0 29.8 17.6 7.4 46.3 48.1 9.0 2.9

Johnson Controls JCI US 50.52 33,656 162.9 28.1 14.0 12.0 100.8 16.9 39.8 0.35 1.7 1.9 2.97 2.61 12.3 9.7 53.3 15.5 2.8 10.3 18.8 16.0 3.3

* Outliners and "N/A" entries are in red and excl. from the calculation of averages

Source: Bloomberg, OP Research

Wed, 26 Nov 2014

BWI (2339 HK)

Page 18 of 19

Our recent reports

Date Company / Sector Stock Code Title Rating Analyst

24/11/2014 Tiangong 826 Solid order growth remains BUY Vivien Chan

19/11/2014 Sinotrans 598 A shift to risk aversion HOLD Bruce Yeung

17/11/2014 CMGC 8081 Mobile game coming to the stage NR Lindsay Hu/ Yuji Fung

13/11/2014 HC International 2280 3Q14 results miss BUY Yuji Fung

13/11/2014 CHINA FIBER OPTIC

NETWORK

3777 In line 3Q14 operation results BUY Yuji Fung

12/11/2014 Shenzhen International 152 A visionary logistics development plan with solid

executions

BUY Bruce Yeung

11/11/2014 UKF 8168 Interim results meet expectation NR Lily Man

11/11/2014 Geely Auto 175 Xindihao sales is ramping up BUY Vivien Chan

05/11/2014 UKF 8168 Got Fur NR Lily Man

04/11/2014 SCUD Group 1399 NDR Takeaway BUY Vivien Chan/ Yuji Fung

30/10/2014 SCUD Group 1399 Working capital further enhanced to fuel robust

earnings growth

BUY Vivien Chan/ Yuji Fung

29/10/2014 Sinotrans 598 Good results are well expected HOLD Bruce Yeung

27/10/2014 SCUD Group 1399 Upgrade on tablet battery shipment ramp BUY Vivien Chan/ Yuji Fung

24/10/2014 Great Wall Motor 2333 3Q results miss consensus HOLD Vivien Chan

24/10/2014 TCL COMM 2618 Upgrade on undemanding valuation BUY Yuji Fung

20/10/2014 Technovator 1206 Spin-off unlock value from Distech Controls BUY Lily Man/ Yuji Fung

13/10/2014 Geely Auto 175 September sales up 41% mom BUY Vivien Chan

09/10/2014 ASR Holdings 1803 Potential change in control HOLD Bruce Yeung

24/09/2014 SCUD Group 1399 Key customers support fast growth BUY Vivien Chan

16/09/2014 Smart Grid in China 3393 Next station - distribution automation BUY Lily Man

16/09/2014 China All Access 633 Awaiting the pickup of core earnings growth HOLD Yuji Fung

16/09/2014 Geely Auto 175 A recovery in August BUY Vivien Chan

12/09/2014 Beijing Properties 925 NDR takeaway – Acquisitions on the way BUY Bruce Yeung

11/09/2014 Great Wall Motor 2333 August sales down 20% yoy HOLD Vivien Chan

02/09/2014 Chinasoft Int’l 354 Upgrade on solid ramp of OSG and ESG BUY Yuji Fung

01/09/2014 Wasion Group 3393 Well begun is half done BUY Lily Man

29/08/2014 Sinomedia 623 Weak 1H14 results are likely to recover in 2H14 BUY Yuji Fung

TERMS FOR PROVISION OF REPORT, DISCLAIMERS AND DISCLOSURES

By accepting this report, you represent and warrant that you are entitled to receive such report in accordance with the restrictions set forth below and agree to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of law or termination of such services provided to you.

Disclaimer

Research distributed in Hong Kong is intended only for institutional investors whose ordinary business activities involve investing in shares, bonds and associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not an institutional investor must not rely on this communication.

The information and material presented herein are not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject Oriental Patron Securities Limited (“OPSL”) and/or its associated companies and/or its affiliates (collectively “Oriental Patron”) to any registration or licensing requirement within such jurisdiction.

The information and material presented herein are provided for information purposes only and are not to be used or considered as an offer or a solicitation to sell or an offer or solicitation to buy or subscribe for securities, investment products or other financial instruments, nor to constitute any advice or recommendation with respect to such securities, investment products or other financial instruments.

This research report is prepared for general circulation. It does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. This report is not to be relied upon in substitution for the exercise of independent judgment. Oriental Patron may have issued other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them. You should independently evaluate particular investments and you should consult an independent financial adviser before making any investments or entering into any transaction in relation to any securities mentioned in this report.

Information and opinions presented in this report have been obtained or derived from sources believed by Oriental Patron to be reliable, but Oriental Patron makes no representation as to their accuracy or completeness and Oriental Patron accepts no liability for loss arising from the use of the material presented in this report where permitted by law and/or regulation. Further, opinions expressed in this report are subject to change without notice. Oriental Patron does not accept any liability whatsoever whether direct or indirect that may arise from the use of information contained in this report.

The research analyst(s) primarily responsible for the preparation of this report confirm(s) that (a) all of the views expressed in this report accurately reflects his or their personal views about any and all of the subject securities or issuers; and (b) that no part of his or their compensation was, is or will be, directly or indirectly, related to the specific recommendations or views he or they expressed in this report.

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance.

Oriental Patron, its directors, officers and employees may have investments in securities or derivatives of any companies mentioned in this report, and may make investment decisions that are inconsistent with the views expressed in this report.

General Disclosure

Oriental Patron, its directors, officers and employees, including persons involved in the preparation or issuance of this report, may, to the extent permitted by law, from time to time participate or invest in financing transactions with the issuer(s) of the securities mentioned in this report, perform services for or solicit business from such issuers, and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto. In addition, it may make markets in the securities mentioned in the material presented in this report. Oriental Patron may, to the extent permitted by law, act upon or use the information presented herein, or the research or analysis on which they are based, before the material is published. One or more directors, officers and/or employees of Oriental Patron may be a director of the issuers of the securities mentioned in this report. Oriental Patron may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the previous 12 months, significant advice or investment services in relation to the investment concerned or a related investment or investment banking service to the issuers of the securities mentioned in this report.

Regulatory Disclosures as required by the Hong Kong Securities and Futures Commission

Particular matters which may give rise to potential conflict of interests between Oriental Patron (inclusive of OPSL) which is carrying on a business in Hong Kong in investment banking, proprietary trading or market making or agency broking and the investors or the potential investors are now disclosed as follows:

As at the date of the report, Oriental Patron has an investment banking relationship with the subject company(ies) and received compensation or mandate for investment banking services from the subject company(ies) within the preceding 12 months and may be currently seeking an investment banking mandate from the subject company(ies).

Analyst Certification:

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research analyst’s compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in the report.

Rating and Related Definitions

Buy (B) We expect this stock outperform the relevant benchmark greater than 15% over the next 12 months. Hold (H) We expect this stock to perform in line with the relevant benchmark over the next 12 months. Sell (S) We expect this stock to underperform the relevant benchmark greater than 15% over the next 12 month. Relevant Benchmark Represents the stock closing price as at the date quoted in this report.

Copyright © 2014 Oriental Patron Financial Group. All Rights Reserved

This report is being supplied to you strictly on the basis that it will remain confidential. Except as specifically permitted, no part of this presentation may be reproduced or distributed in any manner without the prior written permission of Oriental Patron. Oriental Patron accepts no liability whatsoever for the actions of third parties in this respect.

CONTACT

27/F, Two Exchange Square, www.oriental-patron.com.hk Tel: (852) 2135 0248

8 Connaught Place, Central, Hong Kong [email protected] Fax: (852) 2135 0295