bursa malaysia berhad - bursa-cn.listedcompany.com · 34th annual general meeting . dato’...

TRANSCRIPT

34th Annual General Meeting

Dato’ Tajuddin Atan, CEO

14 April 2011

BURSA MALAYSIA BERHAD Destination of choice for listings and investments in the region

Presentation to Shareholders

MARKET PERFORMANCE IN 2010

KEY DEVELOPMENT & GLOBAL RECOGNITION IN 2010

FINANCIAL REVIEW

KEY FOCUS & PROSPECT

AGENDA

2

3

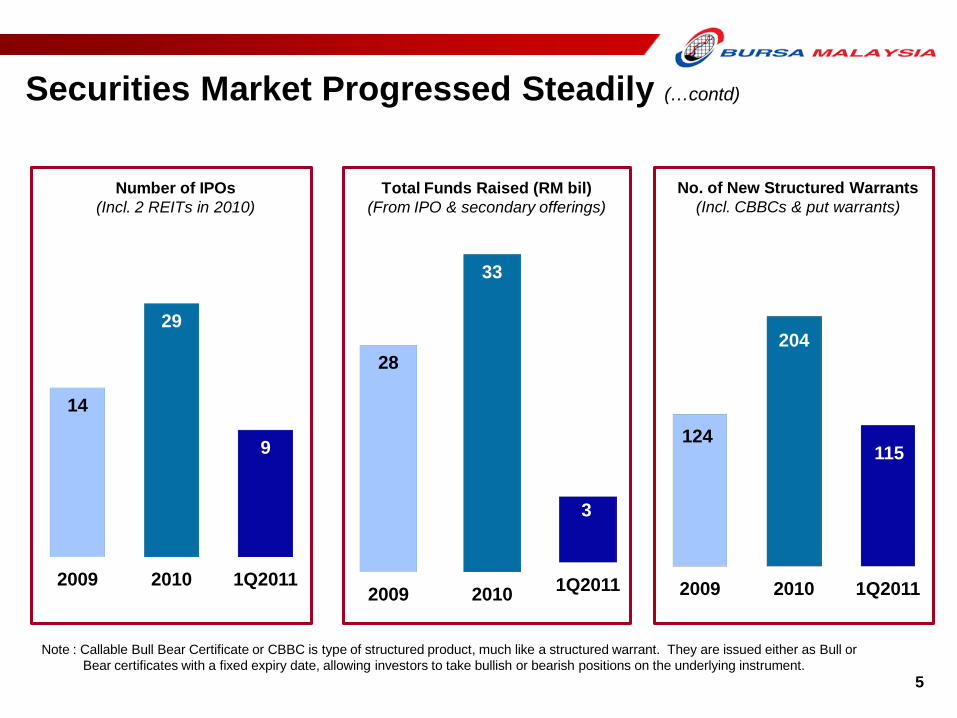

Securities Market Progressed Steadily 4 – 5

Securities Market Trading Activity 6

Securities Market Trading Participation 7

Increasing Interest in the Derivatives Market 8

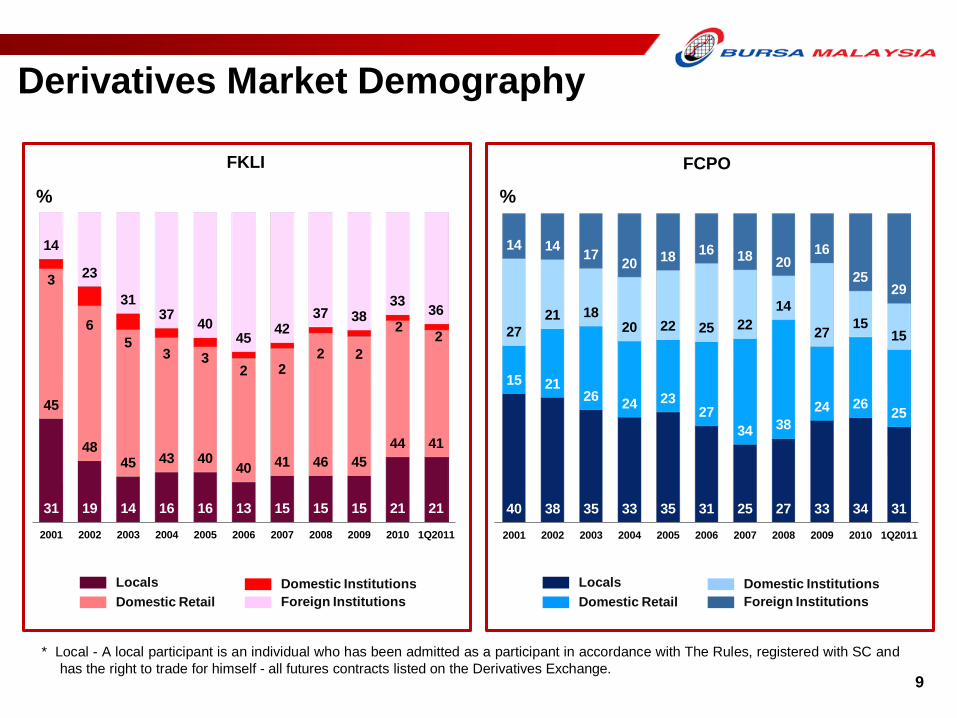

Derivatives Market Demography 9

Peer Comparison In 2010 10

Market Performance in 2010

4

2009 2010 1Q2011

28%

Securities Market Progressed Steadily

1,518.91

3%

Daily Average Trading Value -

OMT + DBT* (RM mil)

Turnover Velocity

Market Capitalisation (RM bil)

FBM KLCI Index 1,272.78 19%

1,221

1,574

29%

FBMKLCI Hits All Time High at 1574.49 on 17 Jan 2011

* OMT - On Market Transaction DBT - Direct Business Transaction

2,234

42%

1,288

1,545.13

1%

27%

42%

34%

999

33%

1,275

2%

31.12.2009 31.12.2010 31.3.2011

28

2009

33

2010 1Q2011

5

Securities Market Progressed Steadily (…contd)

124

204

115

2009 2010 1Q2011

14

29

9

2009 2010 1Q2011

No. of New Structured Warrants (Incl. CBBCs & put warrants)

Number of IPOs (Incl. 2 REITs in 2010)

Total Funds Raised (RM bil) (From IPO & secondary offerings)

3

Note : Callable Bull Bear Certificate or CBBC is type of structured product, much like a structured warrant. They are issued either as Bull or Bear certificates with a fixed expiry date, allowing investors to take bullish or bearish positions on the underlying instrument.

57%

31% 40% 39%

20% 23%

34% 32% 25%

34%

53%

34% 34% 33% 42%

1,924

497 805 911

350 472 748

874 718

1,019

2,179

1,181 1,129 1,454

2,161

-

400

800

1,200

1,600

2,000

2,400

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q2011

RM mil

Annual DATV & Velocity

68%

54% 50%

41% 46%

31% 25%

32% 23%

48%

36% 28%

35% 28% 31%

37% 42%

6

2,610 2,303

2,069 1,751 1,907

1,187 823 854

615

1,490 1,266 1,099 1,435 1,209 1,387

1,793 2,161

- 400 800

1,200 1,600 2,000 2,400 2,800

1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11

RM mil

Securities Market Trading Activity Quarterly DATV & Velocity

Daily Average Trading Value (RM mil) Turnover Velocity

Daily Average Trading Value (RM mil) Turnover Velocity

346

806

283 373 378

583

34 37 24

33 26 27

66 63 76 67 74 73

2006 2007 2008 2009 2010 1Q2011

7

Securities Market Trading Participation

From 2006 to 2009, the statistics were based on Brokers’ submission. From 2010 onwards statistics were based on Bursa’s internal system.

65 63 58

73 73 76

35 37 42 27 27 24

2006 2007 2008 2009 2010 1Q2011

Retail (%)

Institutions (%)

Local (%)

Foreign (%)

Retail DATV (RM mil)

Foreign DATV (RM mil)

357

806

496

305 393

519

Retail vs Institutions Foreign vs Local

2010

24,818

2010 1Q2011

24,749

2009

Increasing Interest in the Derivatives Market

8

FCPO & Total Volume Reach All Time Monthly Highs of 619,326 & 856,791 contracts in March 2011

FCPO

Daily Average Contracts

(Units)

Open Positions

0.3%

123,141 132,151 36,785

136,202

48%

1Q2011 2010 2009

FKLI

1Q2011 2009

25,606

16,389 16,165 8,056 8,044

10,274

9

Derivatives Market Demography

* Local - A local participant is an individual who has been admitted as a participant in accordance with The Rules, registered with SC and has the right to trade for himself - all futures contracts listed on the Derivatives Exchange.

31 19 14 16 16 13 15 15 15 21 21

45

48 45 43 40

40 41 46 45 44 41

3

6 5

3 3 2 2

2 2

2 2

14

23

31 37 40

45 42 37 38

33 36

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q2011

%

FKLI

Locals Domestic Retail

Domestic Institutions Foreign Institutions

40 38 35 33 35 31 25 27 33 34 31

15 21 26 24 23

27 34 38

24 26 25

27 21 18

20 22 25 22 14

27 15 15

14 14 17 20 18 16 18 20 16

25 29

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 1Q2011

%

FCPO

Locals Domestic Retail

Domestic Institutions Foreign Institutions

-20% 0%

20% 40% 60% 80%

100% 120%

Col

ombo

Phili

ppin

es

Osa

ka

Indo

nesi

a

Shen

zhen

Thai

land

Kore

a

Nat

iona

l SE

Indi

a

Sing

apor

e

Bom

bay

Hon

g Ko

ng

Taiw

an

Aust

ralia

Toky

o

Shan

ghai

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Col

ombo

Thai

land

Indo

nesi

a

Kore

a

Nat

iona

l SE

Indi

a

Bom

bay

SE

Sing

apor

e

Taiw

an

Hon

g Ko

ng

Osa

ka

Shen

zhen

SE

Aust

ralia

Toky

o SE

Shan

ghai

SE

Mal

aysi

a

10

0

200

400

600

800

1,000

1,200

Hon

g Ko

ng

Shan

ghai

Shen

zhen

Aust

ralia

n

Toky

o

Nat

iona

l SE

Indi

a

Kore

a

Indo

nesi

a

Sing

apor

e

Taiw

an

Thai

land

Phili

ppin

es

Col

ombo

Osa

ka

USD

bil

Funds Raised

Peer Comparison in 2010 Asian Benchmark Index Growth % Asian Market Capitalisation Growth %

Mal

aysi

a

100

80

60

40

20

0

-20

-40

120 100 80 60 40 20 0

-20

Source: World Federation Exchanges (WFE)

19% 28%

USD10.8 bil

Mal

aysi

a

11

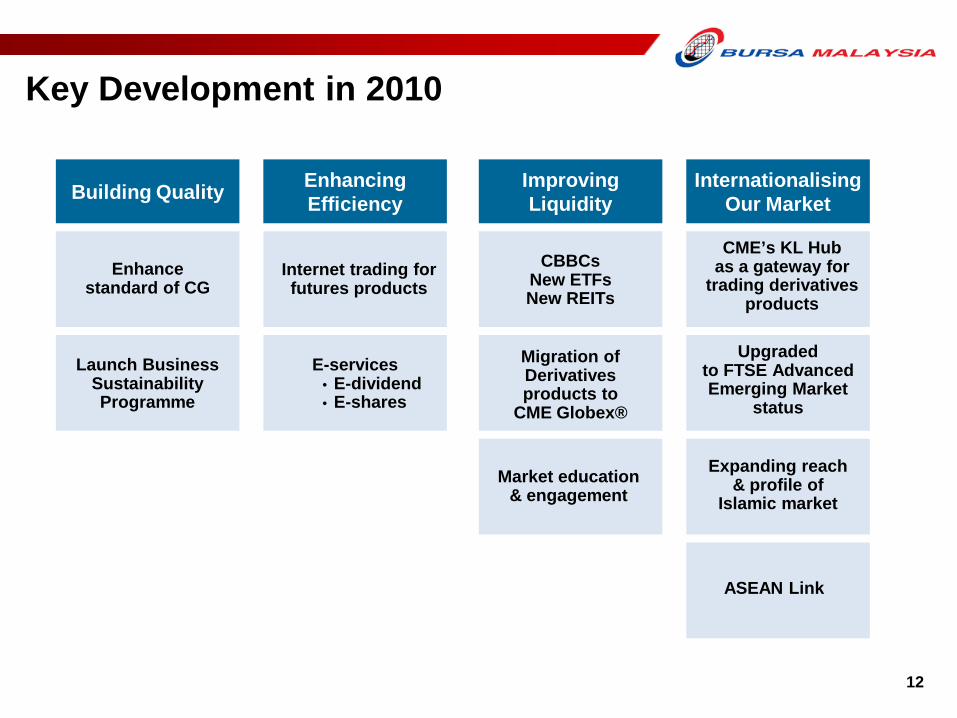

Key Development in 2010 12

Global Recognition 13

Awards and Accolades in 2010 14

Key Development & Global Recognition in 2010

12

Enhance standard of CG

Market education & engagement

CME’s KL Hub as a gateway for

trading derivatives products

Expanding reach & profile of

Islamic market

Upgraded to FTSE Advanced Emerging Market

status

Key Development in 2010

CBBCs New ETFs New REITs

E-services • E-dividend • E-shares

ASEAN Link

Migration of Derivatives products to

CME Globex®

Internet trading for futures products

Internationalising Our Market

Improving Liquidity Building Quality Enhancing

Efficiency

Launch Business Sustainability Programme

Global Recognition

Approval from US Commodity Futures Trading Commission (CFTC) to enable Malaysian Futures brokers to deal with US customers

Migration of Malaysian derivatives products to CME Globex®

QDII – Malaysia Investment destination for China investors

13

CBRC Recognition

FTSE Upgrade

CFTC Approval

U.S. SEC Approval

“Designated Offshore Securities Market” recognition to ease trading in Malaysian listed securities & shelf listed bonds by U.S. investors

CME Partnership

Malaysia promoted to Advanced Emerging Market status in FTSE Global Equity Index Series

Bursa Suq Al-Sila’s Innovation Awards

14

Awards and Accolades in 2010

Malaysian CG Index Awards by MSWG

• Top 3 (overall) Award for excellent in CG • Distinction Award • Special Transparency Award

• Market innovation award for The Asset Triple Awards for Islamic Finance

• Islamic innovation award by Ministry of Science, Technology and Innovation (MOSTI)

Investor Relations Awards by Investor Relations Global Ranking

• Best Corporate Governance practices • Best Online Annual Report in Asia Pacific

15

Financial Review

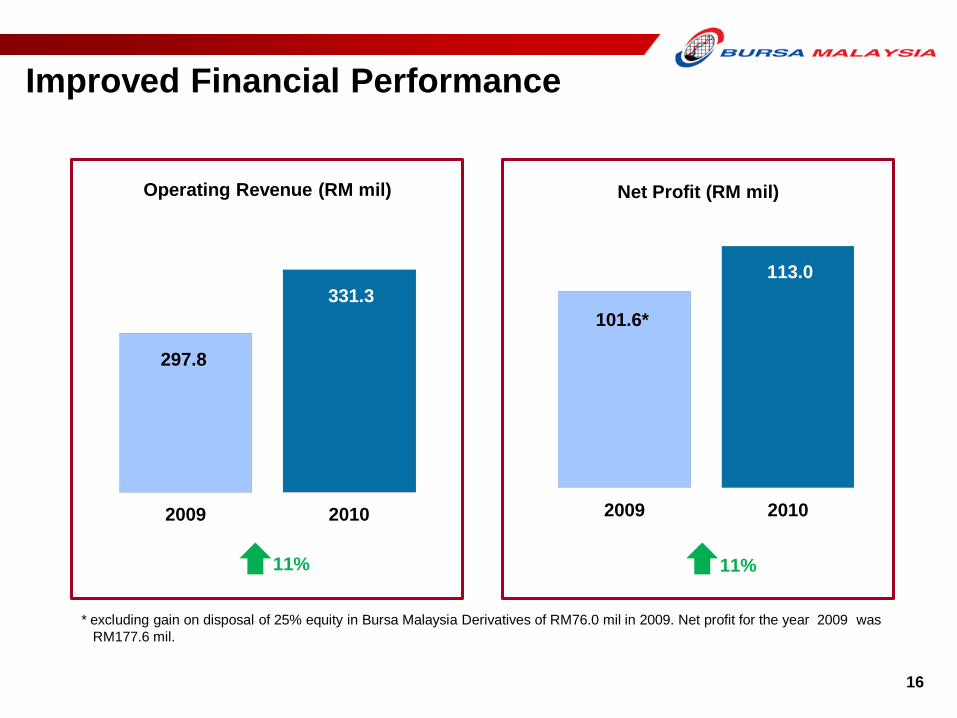

Improved Financial Performance 16

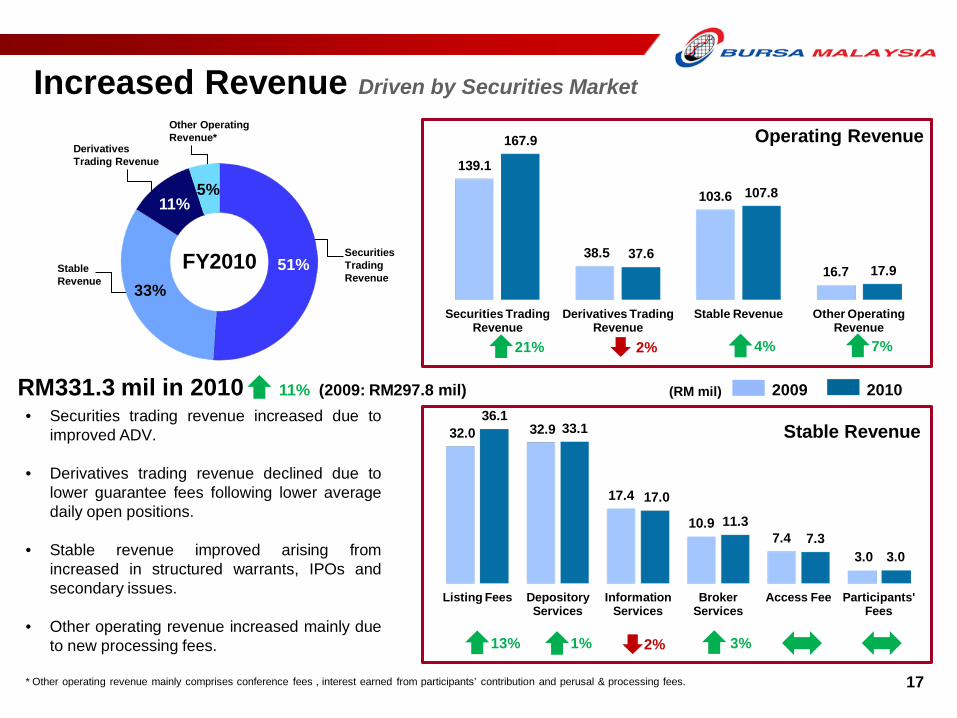

Increased Revenue 17

Higher Operating Expenses 18

Sustainable Performance Ratios 19

Strong Reserves 20

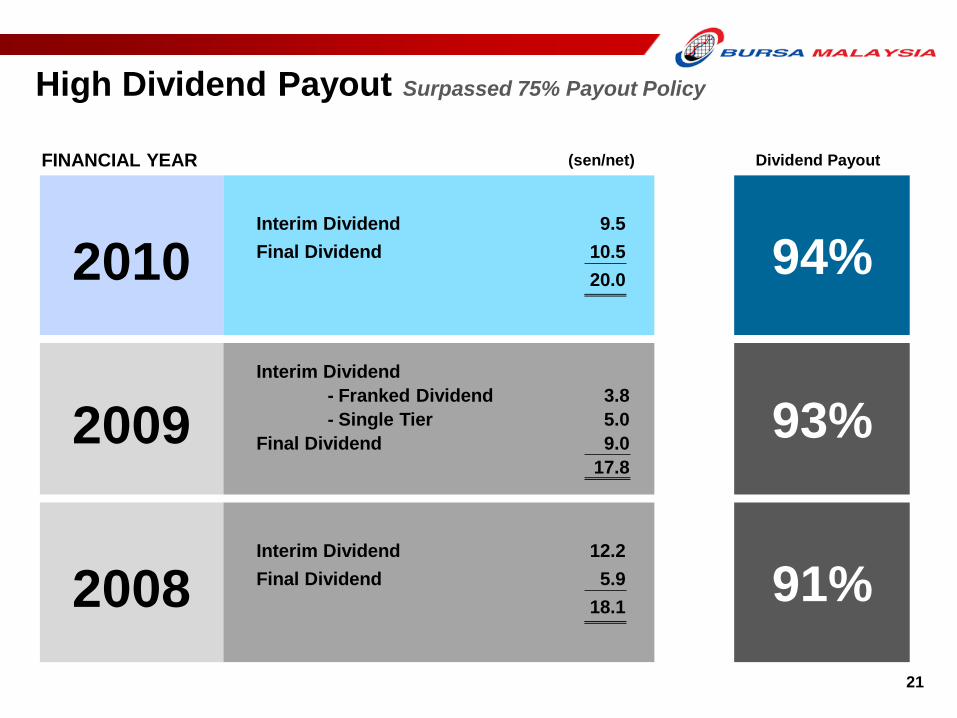

High Dividend Payout 21

2009 2010

16

Improved Financial Performance

2009 2010

Operating Revenue (RM mil)

297.8

331.3

Net Profit (RM mil)

11%

* excluding gain on disposal of 25% equity in Bursa Malaysia Derivatives of RM76.0 mil in 2009. Net profit for the year 2009 was RM177.6 mil.

11%

101.6*

113.0

17

139.1

38.5

103.6

16.7

167.9

37.6

107.8

17.9

Securities Trading Revenue

Derivatives Trading Revenue

Stable Revenue Other Operating Revenue

32.0 32.9

17.4

10.9 7.4

3.0

36.1 33.1

17.0

11.3 7.3

3.0

Listing Fees Depository Services

Information Services

Broker Services

Access Fee Participants' Fees

Operating Revenue

Increased Revenue Driven by Securities Market

17 * Other operating revenue mainly comprises conference fees , interest earned from participants’ contribution and perusal & processing fees.

FY2010

21% 4% 7% 2%

RM331.3 mil in 2010 11% (2009: RM297.8 mil) • Securities trading revenue increased due to

improved ADV.

• Derivatives trading revenue declined due to lower guarantee fees following lower average daily open positions.

• Stable revenue improved arising from increased in structured warrants, IPOs and secondary issues.

• Other operating revenue increased mainly due to new processing fees.

Stable Revenue

(RM mil) 2009 2010

13% 3% 2% 1%

Other Operating Revenue*

Securities Trading Revenue

Stable Revenue

Derivatives Trading Revenue

51% 33%

11% 5%

47%

22%

6%

9% 5%

2% 9%

18 18

83.3

38.9

15.4 14.2 10.1 3.2

17.5

92.4

43.2

12.3 17.7

10.2 2.7

18.2

• Other OPEX comprises administrative expenses, CDS consumables & other miscellaneous expenses..

FY2010

Staff Cost Depreciation & Amortisation (D & A) Market Development Technology Charges Building Management Costs Professional Fees Other OPEX

Higher Operating Expenses Talent Investment for Future Growth

` (RM mil) 2009 2010

• Higher staff cost due to talent attraction and retention efforts.

• Higher D&A due to accelerated depreciation following the migration from Bursa Trade

Derivatives to Globex.

• Market development cost was higher in 2009 as compared to 2010 mainly due to advisory fees incurred for the Globex implementation project.

• Higher technology charges due to Globex license fee.

RM196.7 mil in 2010 8% (2009: RM182.6 mil)

Staff Cost D&A Market Development

Technology Charges

Building Management

Costs

Professional Fees

Other OPEX

11% 11% 20% 16% 4% 25%

31.2*

51.7

12.1

12.9*

32.0

53.7

13.4

13.4

Net Profit Margin (%) Operating EBITDA Margin (%)

Return on Equity (%) EPS (sen)

19 19

Sustainable Performance Ratios

4%

2009 2010 ̀

* excluding gain on disposal of 25% equity in Bursa Malaysia Derivatives of RM76.0 mil in 2009.

4% 11%

840 852

2009 2010

(RM mil)

453

512

2009 2010

20 20

Strong Reserves

Shareholders’ Fund

Financial Resources Available for Use

(RM mil)

1%

13%

`

The Company has sufficient financial resources to cover its Clearing Guarantee Fund commitment, CAPEX and working capital requirements.

`

21 21

High Dividend Payout Surpassed 75% Payout Policy

(sen/net) Dividend Payout

2010

94%

FINANCIAL YEAR

2009

Interim Dividend 9.5 Final Dividend 10.5

20.0

Interim Dividend - Franked Dividend 3.8 - Single Tier 5.0

Final Dividend 9.0 17.8

2008

91% Interim Dividend 12.2 Final Dividend 5.9

18.1

93%

22 22

Key Focus & Prospect

Key Focus for 2011 23

Positive Prospect & Outlook 24

23 23

Strengthen Equity Market

Expand Derivatives

Market Widen &

Internationalise Islamic Market

TO REMAIN COMPETITIVE IN THE REGION

Key Focus for 2011

24 24

Positive Prospect & Outlook

Barring any adverse developments, we expect an improved performance in our markets and results in 2011.

Potential Market Catalysts

Acceleration in the implementation of various economic transformation programmes.

Greater M&A activities & government transformation programmes. Prospects for further divestments by government-linked companies.

Bursa remains committed in ensuring markets continues to be sustainable and vibrant despite increasing volatility from external factors.

Malaysia’s strong economic fundamentals. Liberalisation efforts by the government. Sustained domestic corporate earnings growth attracting portfolio inflows.

Strong and Solid System

Progressive Developmental

Efforts

We continue to invest in the development of the capital market and the

regulatory environment. And at the same time, putting a close watch on our expenditure.

Thank you

KOAY LEAN LEE [email protected]

603-2034 7306

Disclaimer :

Bursa Malaysia and its Group of Companies (the Company) reserve all proprietary rights to the contents of this Presentation.

Whilst the Company endeavours to ensure that the contents in the presentation booklet are accurate, complete or have been obtained from sources believed by the Company to be accurate and reliable, neither the Company nor the Presenter make any warranty, express or implied, nor assume any legal liability or responsibility for the accuracy, completeness or currency of the contents of this Presentation.

In no event shall the Company be liable for any claim, howsoever arising, out of or in relation to this presentation booklet to the recipient of this presentation booklet and/or to any other third party.

© Bursa Malaysia 2011

INTAN DIYANA TAJUDIN [email protected]

603-2034 7049

INVESTOR RELATIONS CONTACT INFORMATION

E-mail : [email protected] Fax : 603-2026 3684

MUHAMMAD ALI [email protected]

603-2034 7673

26 26

Additional Information

Board of Directors & Shareholdings Structure 27

Securities Market Foreign Ownership 28

Derivatives Market Activity 29

27 27

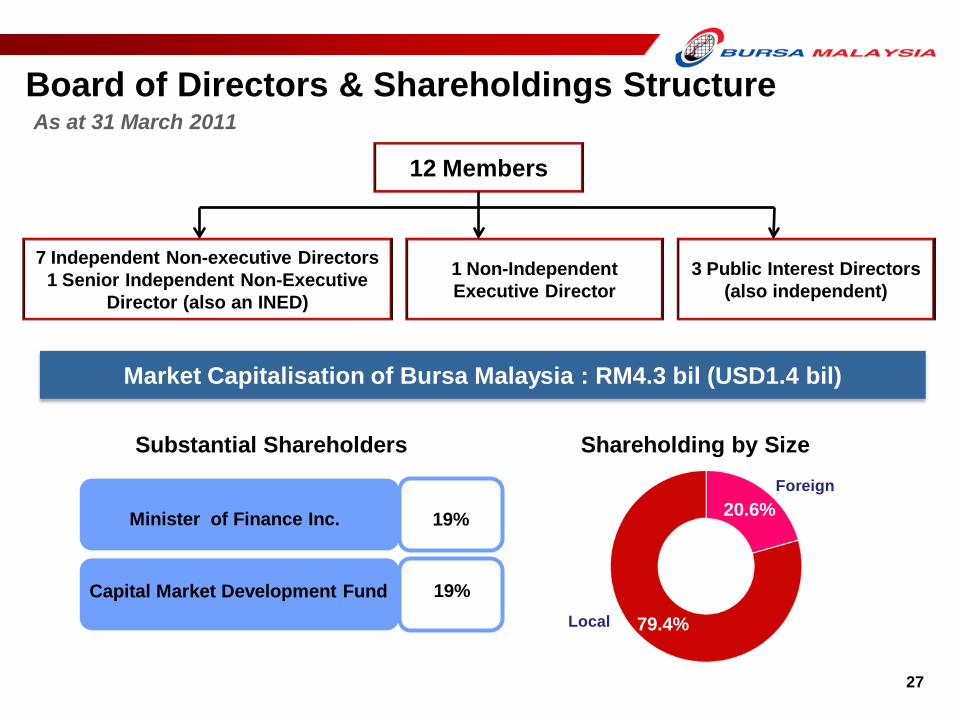

Board of Directors & Shareholdings Structure As at 31 March 2011

12 Members

7 Independent Non-executive Directors 1 Senior Independent Non-Executive

Director (also an INED)

1 Non-Independent Executive Director

3 Public Interest Directors (also independent)

20.6%

79.4%

Foreign

Local

Substantial Shareholders Shareholding by Size

Minister of Finance Inc.

Capital Market Development Fund

19%

19%

Market Capitalisation of Bursa Malaysia : RM4.3 bil (USD1.4 bil)

28 28

7.8%

1.9%

0.9%

0.4%

0.1%

13.2%

Singapore

Hong Kong

UK

USA

Mid-East

Others

25.8%

74.2%

Foreign Ownership by Nationality

Foreign Nominees

Based on Market Capitalisation (as at month end)

26.5

25.7

24.1

21.7

20.9

20.7

20.7

20.9

20.4

20.4

20.6

20.8

21.8

21.9

22.0

21.4

Mar 2011

%

Securities Market Foreign Ownership

1.6% China / Taiwan

2003 2004 2005 2006 2007 2008 2009 2010

49K

66K

85K

159K

125K

156K

123K

29 29

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10

Derivatives Market Activity

2.0

2.6

2.5 4.

2

6.2

6.1

6.1

Annually (Total, million units)

KLCI Futures

Crude Palm Oil Futures Open Position

Others

29%

24K

29K

24K

70%

Quarterly (Daily Average Contracts 000’)

KLCI Futures

Crude Palm Oil Futures Open Position

Others

22K

132K

6.2

24K

32%

6

6%

25K

23K

28K

139K

122K

136K

156K 148K

117K 142K

124K