building guest relationships

DESCRIPTION

Building Lasting Relationships with guests all over as an Intercontinental Hotels Group specialist.TRANSCRIPT

Building lasting guest relationshipsJune 2010

1

Hotel Indigo Scottsdale, USA

IHG’s growth strategy to create sustainable value

2

Rooms RevPAR Royalty RateX X

“Where we play” “How we win”

Markets

Segments

Model

Powerful and distinct brands

Aligned and engaged organisation

Best demand delivery systems

Making best use of our scale to build and grow preferred hotel brands for guests and owners in high value markets

The top 5 things you may not know about the hotel market

3

1 Brands matter online Only 5% of our bookings are through online

travel agents

2 Vacations are a right Rooms sold for leisure increased in 2009

3 Searching isn’t booking 78% of hotel bookings begin with some

form of online search. Web bookings are

only 23% of our mix

5 Hotel guests are hard

to find

Only 50% of Americans stay in a hotel in

any given year

4 It’s a “drive to” business Less than 30% of midscale guests fly

4

Hotel Indigo London Paddington, UK

Building lasting guest relationships

Our journey to Great Hotels Guests Love

5

•Market segmentation and penetrating customer insight

•Thoughtful, innovative Brand evolution

•Consistent branded hotel experience

•Widely available, quality managed and up to the mark

•Great owners who buy into the strategy

•High visibility, multi-media marketing

•Effective, tailored reservation and loyalty systems

•Collaborative and engaged employees

Scale in…

….KNOWLEDGE

….EXPERTISE

…BEST PRACTICE

…PIPELINE

….RELATIONSHIPS

….MEDIA BUYING

….TECHNOLOGY

….NUMBERS

POWERFUL AND DISTINCT BRANDS THAT

PROVIDE A DIFFERENTIATED

GUEST EXPERIENCE

THE BEST DEMAND DELIVERY SYSTEM

ALIGNED AND ENGAGED ORGANISATION

System scale drives revenue delivery

• $16.8bn gross revenue* from all hotels in system

• c.$1bn system funds from hotel contributions

• Revenue delivered through the system up 19%pts since 2004 to 68%

• Delivery driven by

– Embedding lasting guest relationships

– Exploiting all booking channels

– Innovations

6

* Gross revenue is defined as total room revenue from franchised hotels and total hotel revenue from managed, owned and leased

hotels. It is not revenue attributable to IHG, as it is derived mainly from hotels owned by third parties.

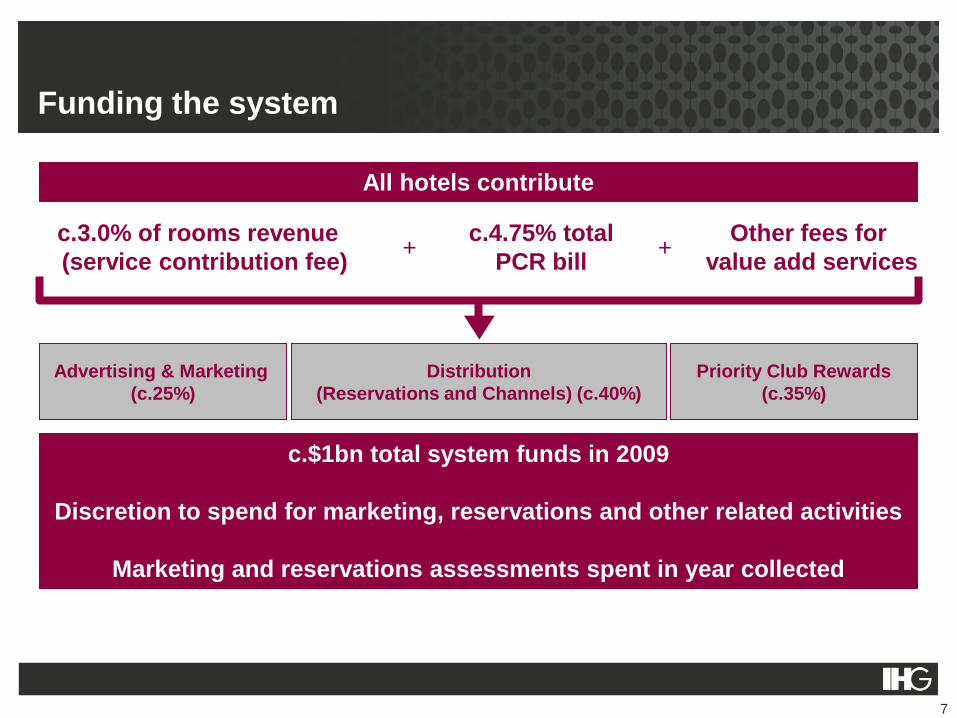

Funding the system

7

All hotels contribute

c.3.0% of rooms revenue

(service contribution fee)

c.4.75% total

PCR bill+ +

Other fees for

value add services

Distribution

(Reservations and Channels) (c.40%)

Priority Club Rewards

(c.35%)

Advertising & Marketing

(c.25%)

c.$1bn total system funds in 2009

Discretion to spend for marketing, reservations and other related activities

Marketing and reservations assessments spent in year collected

Exploiting all booking channels

8

InterContinental Hong Kong

Booking channels

51%

32%

10%

18%

14%

20%

13%14%

10%11%

2% 5%

2004 2009

9

Note: 2009 constant USD rates

$10.9bn $13.7bn

Global Distribution System

Call centres

IHG Websites

PCR Hotel Direct

Hotel Direct

Online Travel Agency

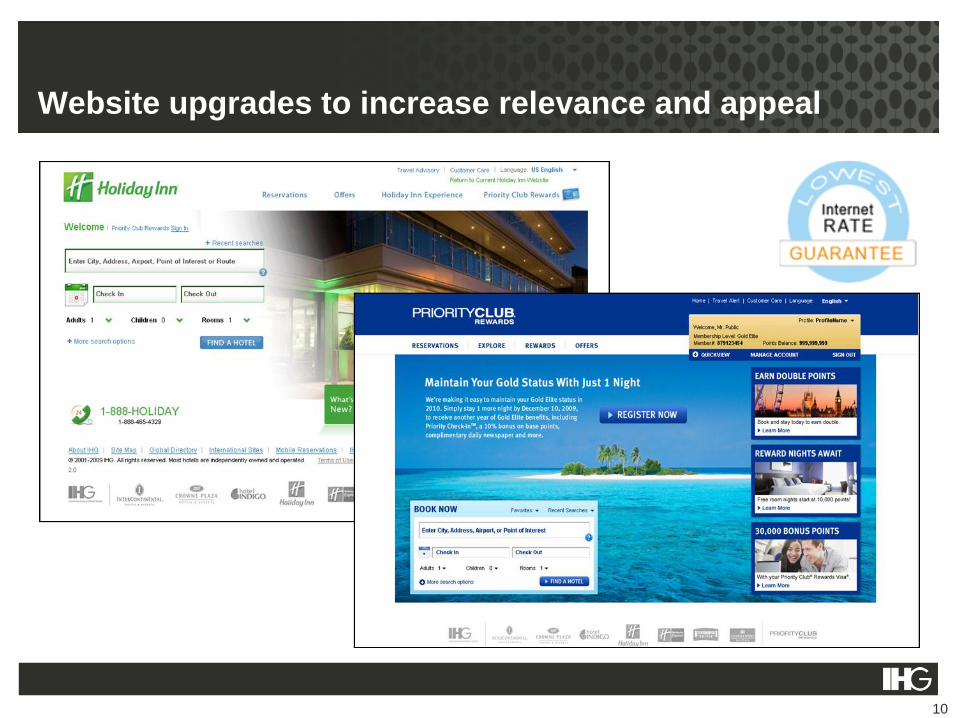

Website upgrades to increase relevance and appeal

10

Central Reservations – global scale and accessibility

11

Approximately 25 million calls handled per year with c.1,700 agents

Note: 2009 full-year call volumes and year-end agent counts

Charleston

324 agents

c.4.6m calls pa

Salt Lake City

368 agents

c.6.1m calls pa

Mexico City

48 agents

c.0.7m calls paSao Paulo

10 agents

c.0.1m calls pa

Birmingham

236 agents

c.2.6m calls pa

Bucharest

39 agents

c.0.4m calls pa

Tokyo

13 agents

c.0.1m calls pa

Guangzhou

31 agents

c.0.5m calls pa

Baguio

368 agents

c.6.4m calls pa

Manila

225 agents

c.3.3m calls pa

Embedding lasting guest relationships

12

Crowne Plaza Lijiang Ancient Town, China

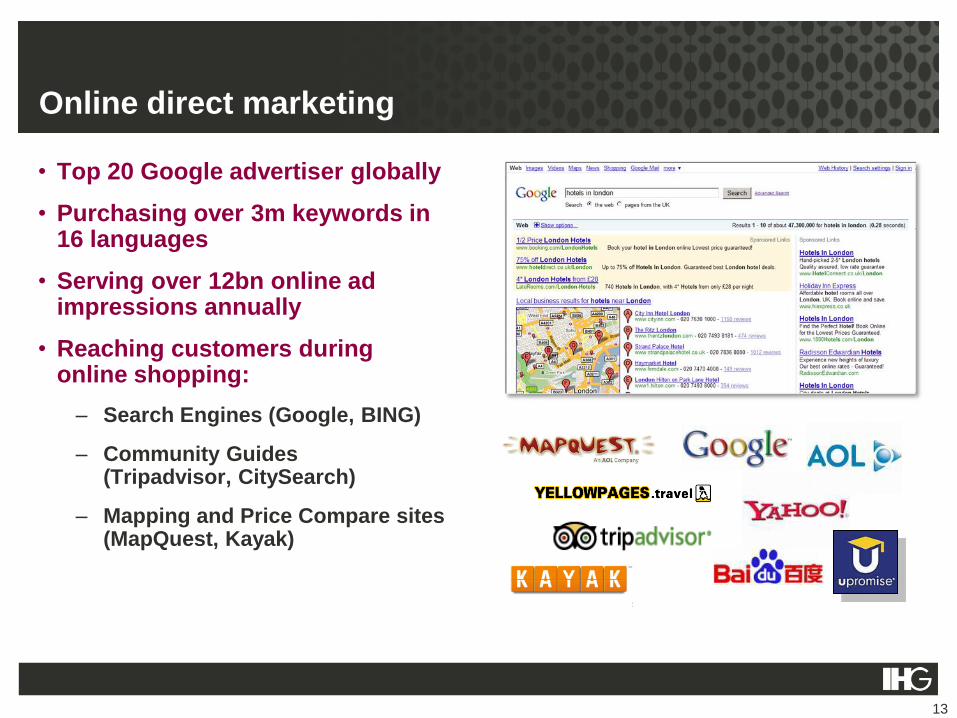

Online direct marketing

• Top 20 Google advertiser globally

• Purchasing over 3m keywords in16 languages

• Serving over 12bn online ad impressions annually

• Reaching customers duringonline shopping:

– Search Engines (Google, BING)

– Community Guides(Tripadvisor, CitySearch)

– Mapping and Price Compare sites (MapQuest, Kayak)

13

Targeted marketing

• $28m investment over 3 years in modernising of infrastructure and processes

• Enable the identification and marketing to an additional c.34m customers

• Improve time to market and accuracy of campaigns

• >$150m incremental revenue from these types of campaigns in 2009

14

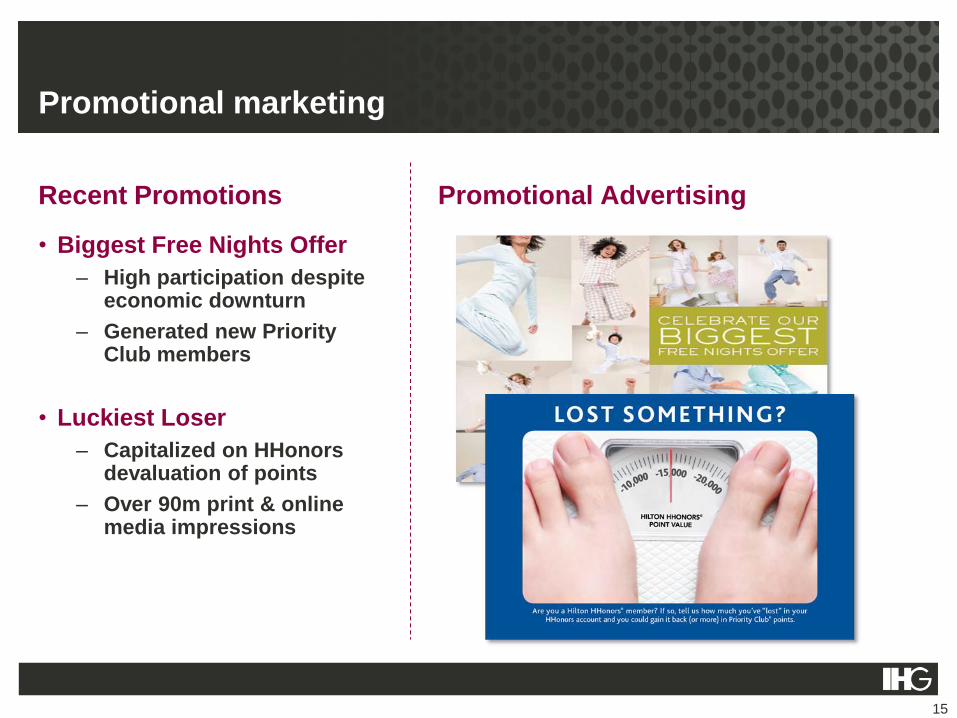

Promotional marketing

Recent Promotions

• Biggest Free Nights Offer

– High participation despite economic downturn

– Generated new PriorityClub members

• Luckiest Loser

– Capitalized on HHonorsdevaluation of points

– Over 90m print & onlinemedia impressions

Promotional Advertising

15

Social marketing

16

Mass marketing

17

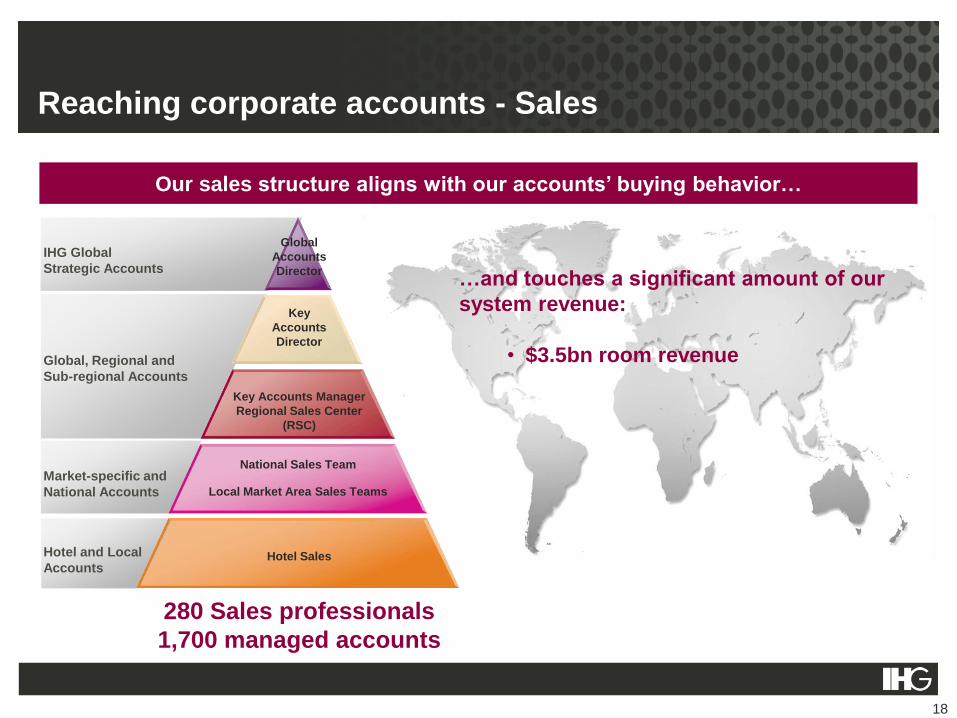

Reaching corporate accounts - Sales

18

Our sales structure aligns with our accounts’ buying behavior…

…and touches a significant amount of our

system revenue:

• $3.5bn room revenue

IHG Global

Strategic Accounts

Global, Regional and

Sub-regional Accounts

Market-specific and

National Accounts

Hotel and Local

Accounts

Key Accounts Manager

Regional Sales Center

(RSC)

National Sales Team

Local Market Area Sales Teams

Hotel Sales

Global

Accounts

Director

Key

Accounts

Director

280 Sales professionals

1,700 managed accounts

Recent sales initiatives

19

• Strategic Pricing - volume-based dynamic discount model

• PCR Engagement - drive PCR penetration in all managed accounts

• Easy Groups/Easy Meetings – driving share of small meetings.

• Meeting Broker - improving lead management and processes

Business

Travel

Optimisation

Meetings

Optimisation

Priority Club Rewards (PCR)

• Priority Club contribution +4% pts vs. 2008

• Over 51m PCR members worldwide

– Largest programme in hotel industry

– Record hotel enrolments in 2009 (+28% YOY)

• Increase value proposition of Priority Club points

– “Points & Cash” - combine points with cash to redeem free nights faster

– “Flights Anywhere” - redeem points for airline travel

– “Hotels Anywhere” – redeem points online for non IHG hotel rooms

• Best Hotel Loyalty Programme

– Business Traveller Magazine – 2007, 2008, 2009

– Global Traveller Magazine – 2005, 2006, 2007, 2008, 2009

– SmarterTravel Editors’ Choice Awards - 2009

20

The most valuable customers

• They PAY more

– 10% premium on ADR versus other guests

– Less price sensitive - choosing our brands for reasons other than strictly price

• They STAY more

– Studies show that PCR members stay >30% more with IHG post enrollment

– PCR members 10 times more likely to stay at more than one hotel than non-members

• They COST less

– PCR members 3 times more likely to use lower cost on-line booking than non members

– They use online travel agencies less

21

PCR members deliver more than double the profit of non-PCR members

Innovations

22

Staybridge Suites Cairo City Stars, Egypt

Mobile

• Mobile bookings increased 600% (March 2010 vs. 2009)

• Future enhancements to mobile in progress

• Mobile Awareness Campaign launched March 2010

• New IHG iPhone app launched April 2010

23

Retargeted online marketing

• Retargeting those who leave IHG’s website

• YTD global campaigns generated

– 386m+ impressions for IHG brands

– >$40m in revenue for the system

• Creative messaging being used for all brands in multiple languages

• Media partners

– Google, AOL, Yahoo! and Netmining

24

Note: Gross data all channels from 1 Jan 2010 to 7 April 2010

Customer Clusters

IHG

Websites

IHG’s growth strategy to create sustainable value

25

Rooms RevPAR Royalty RateX X

“Where we play” “How we win”

Markets

Segments

Model

Powerful and distinct brands

Aligned and engaged organisation

Best demand delivery systems

Making best use of our scale to build and grow preferred hotel brands for guests and owners in high value markets

26

WHY?

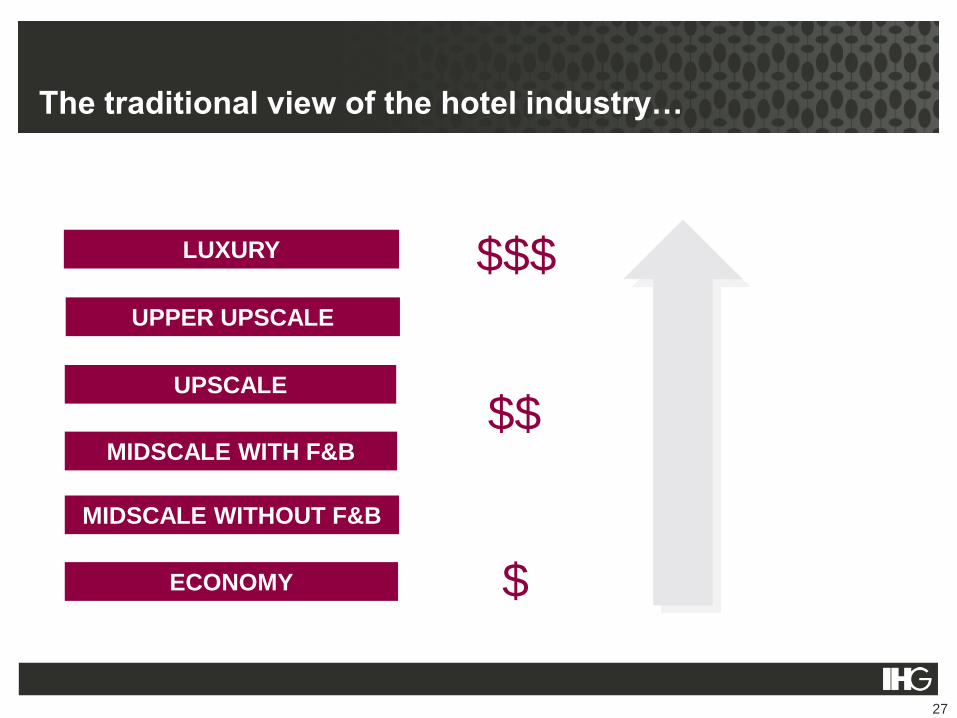

The traditional view of the hotel industry…

27

ECONOMY

MIDSCALE WITHOUT F&B

MIDSCALE WITH F&B

UPSCALE

UPPER UPSCALE

LUXURY

$

$$

$$$

Then we thought we got sophisticated….

28

ECONOMY

MIDSCALE WITHOUT F&B

MIDSCALE WITH F&B

UPSCALE

UPPER UPSCALE

LUXURY

$

$$

$$$BOUTIQUES

EXTENDED STAY

Approaching branding

29

Rifle-shot brands

System

BRAND BRAND BRAND

House brand

BRAND

By xx

System

BRAND

By xxBRAND

By xx

HOUSE

BRAND

Single brand

BRAND

System

Our brands

30

Rifle-shot brands

System

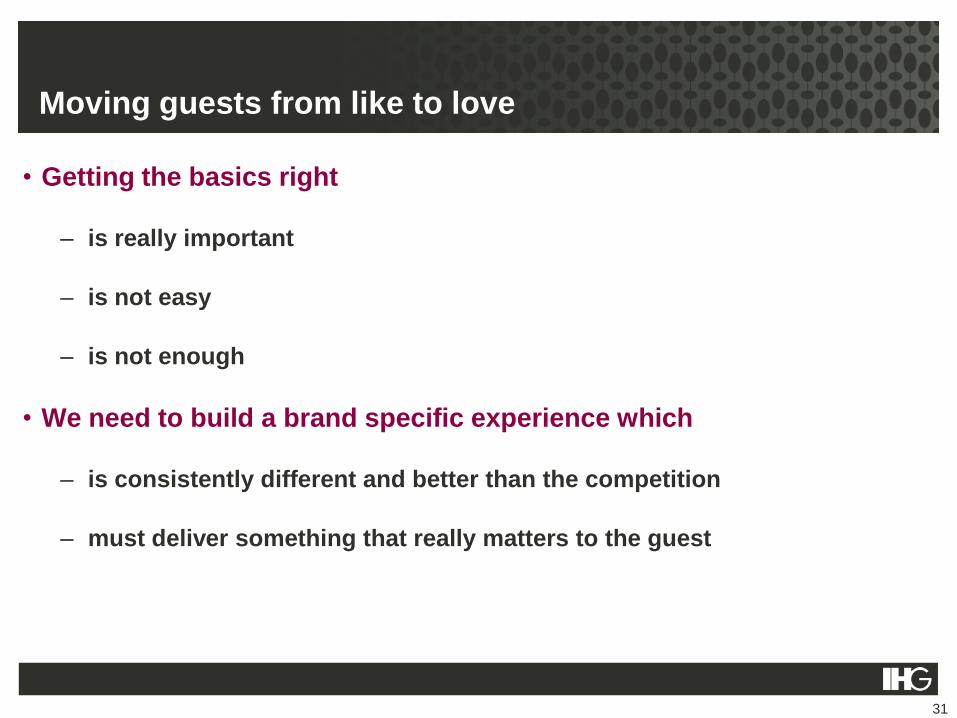

Moving guests from like to love

• Getting the basics right

– is really important

– is not easy

– is not enough

• We need to build a brand specific experience which

– is consistently different and better than the competition

– must deliver something that really matters to the guest

31

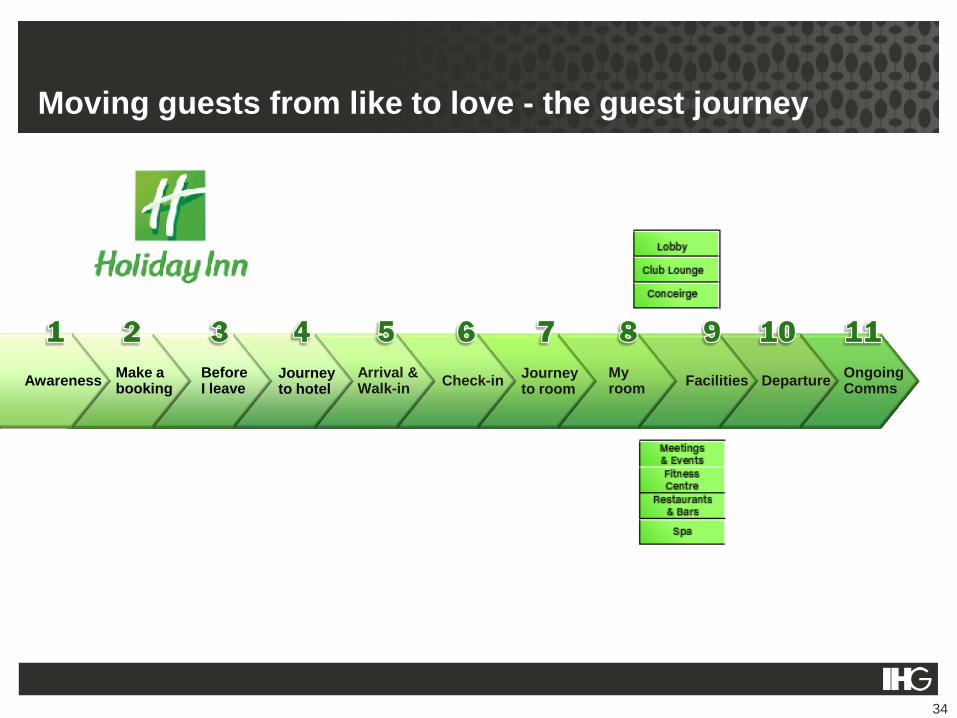

Moving guests from like to love - the guest journey

OngoingComms

DepartureFacilitiesMyroom

Journeyto room

Check-inArrival &Walk-in

Journey to hotel

BeforeI leave

Make abooking

Awareness

32

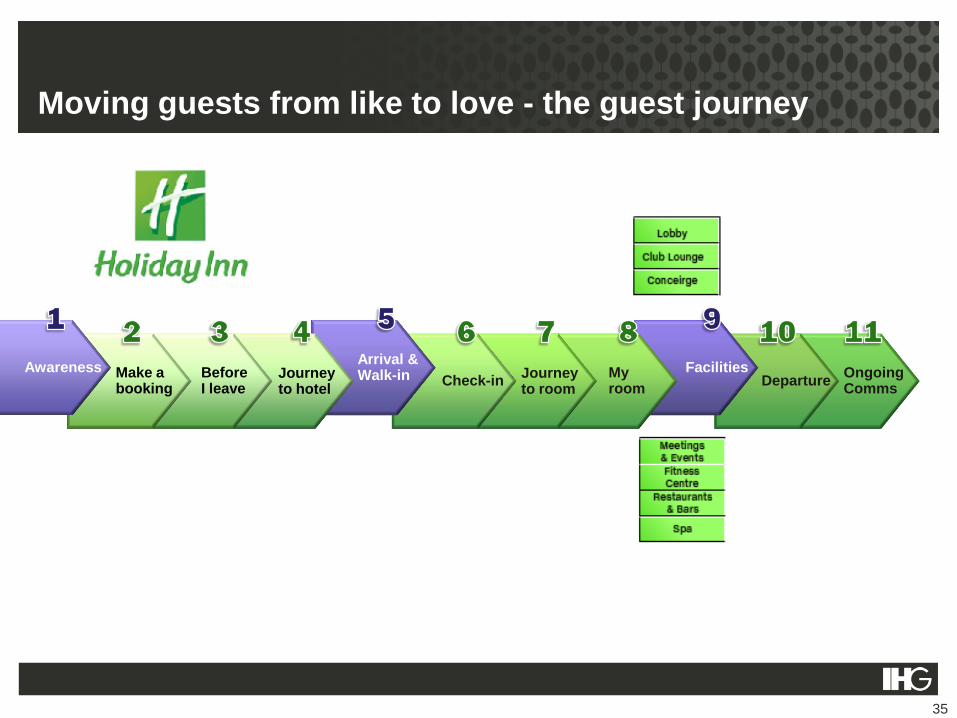

Moving guests from like to love - the guest journey

OngoingComms

DepartureFacilitiesMyroom

Journeyto room

Check-inArrival &Walk-in

Journey to hotel

BeforeI leave

Make abooking

Awareness

33

Moving guests from like to love - the guest journey

OngoingComms

DepartureFacilitiesMyroom

Journeyto room

Check-inArrival &Walk-in

Journey to hotel

BeforeI leave

Make abooking

Awareness

34

Moving guests from like to love - the guest journey

OngoingComms

DepartureFacilitiesMy

roomJourneyto room

Check-in

Arrival &Walk-inJourney

to hotelBeforeI leave

Make abooking

Awareness

35

Summary

• System scale key to building the best demand delivery system

– Leading investment in marketing and expertise

– System delivery up 19%pts since 2004 to 68%

• Creating powerful and distinct brands

– Psychology and emotion, not just price and function

– Brought to life everywhere we touch the guest

36

Building lasting guest relationships –longstanding Priority Club Reward members

37

Michael Jorgeson

26yrs

2009: 114 nights

Robert Bonnem

20yrs

2009: 31 nights

Stephen Sohns

19yrs

2009: 21 nights

Martyn Cornell

12yrs

2009: 15 nights

Ruth Farrell

9yrs

2009: 23 nights

Valerie Manso

24yrs

2009: 77 nights

Andrew Watson

12 yrs

2009: 26 nights

Jerry Harwood

12 yrs

2009: 70 nights

Peter Duke

14 yrs

2009: 52 nights

Peter Kesterton

13 yrs

2009: 17 nights

Mark Gilley

11yrs

2009: 35 nights

Q & A

38

Holiday Inn Pataya, Thailand

Building lasting guest relationshipsJune 2010

39

Hotel Indigo Scottsdale, USA