budgeting: keeping track of your money - g-w.com you keep track of your money and spend wisely. in...

TRANSCRIPT

60

TermsBudget

Expenses

Fixed expenses

Variable expenses

Income

Discretionary income

3Objectives

When you complete Chapter 3, you will be able to:

● Explain the purpose of a budget.

● Identify and calculate fixed and variable expenses.

● Calculate average monthly income and discretionary

income.

● Create a monthly budget.

Budgeting: Keeping Track of Your Money

Chapter 3 Budgeting: Keeping Track of Your Money 61

Your Financial IQ

Before you read this chapter, answer the following questions to see how much you already know about budgeting.

1. What is a budget?

2. How do you think using a budget could help you manage your money?

3. What does it mean to “pay yourself fi rst” when managing your money?

4. How do you keep track of how much money you spend in a typical day?

5. What is a fi xed expense?

6. What is a variable expense?

7. What is discretionary income?

8. Is a budget necessary if you have a high income?

9. What does it mean to have a surplus?

10. What does it mean to have a defi cit?

B f

This sample chapter is for review purposes only. Copyright © The Goodheart-Willcox Co., Inc. All rights reserved.

62 Becoming Money $mart

BudgetsIn Chapter 1, you learned some of the basics of fi nancial planning. The

next step you will take toward your fi nancial plan is to create a budget. What is a budget? A budget is an estimate (usually by category) of expected income and expenses for a given period of time. A budget may be prepared for a week, a month, or a longer period, such as a year. A budget is a useful tool that can help you keep track of your money and spend wisely.

In Chapter 1, you set short-term and long-term goals. These goals were based fi rst on your values, then on your needs and wants. These goals will help you as you create your budget. Go back to Chapter 1 and take a look at the goals you set. Review these goals before you move forward with the next section. Make sure these goals are appropriate for you so that you can use them to create your budget.

Being Financially Responsible

BudgetingA Checklist

Do you ever wonder where your money goes? Do you get to the end of the week and fi nd that you no longer have any money to spend? It is important to keep track of money you have and what you spend to be fi nancially responsible.

Yes No

_____ _____ 1. Did I spend my weekly budget on needs?

_____ _____ 2. Did I spend my weekly budget on wants?

_____ _____ 3. Did I have money left over this week to put in savings?

_____ _____ 4. Did I write down everything that I spent money on?

_____ _____ 5. Did I resist buying something that I really didn’t need?

_____ _____ 6. Did I run out of money this week?

_____ _____ 7. Did I have to borrow money to make it through the week?

_____ _____ 8. Did I learn anything this week about my spending and savings habits?

_____ _____ 9. Did I buy something this week that I regret?

______ ______ 10. Was there something I really wanted to buy this week that I did not have enough money to buy?

Chapter 3 Budgeting: Keeping Track of Your Money 63

Check Your

Understanding

What is the purpose of a budget?

ExpensesExpenses are amounts paid for goods or services. Do you pay for your

school lunches? Your clothes? Your cell phone? Entertainment? These are examples of expenses.

Expenses are categorized as either fi xed or variable. Fixed expenses are those that stay the same each month, such as amounts paid for school lunches or bus passes. Variable expenses are those that change from month to month, such as amounts paid for cell phones bills or spending for personal care items.

As a teen, you probably do not have many expenses beyond those for your personal needs. However, as you graduate and go to college or your fi rst full-time job, you will fi nd there are a lot more expenses to consider. Items such as rent, utilities, groceries, and many other expenses will need to be tracked. Getting in the habit of tracking your spending now will help make it easier when your expenses are greater.

Examples of

fixed expenses for

adults would be

mortgage or rent

payments and car

payments.

Having a cell phone is a variable expense that should be included in your budget each month.

Shutterstock

64 Becoming Money $mart

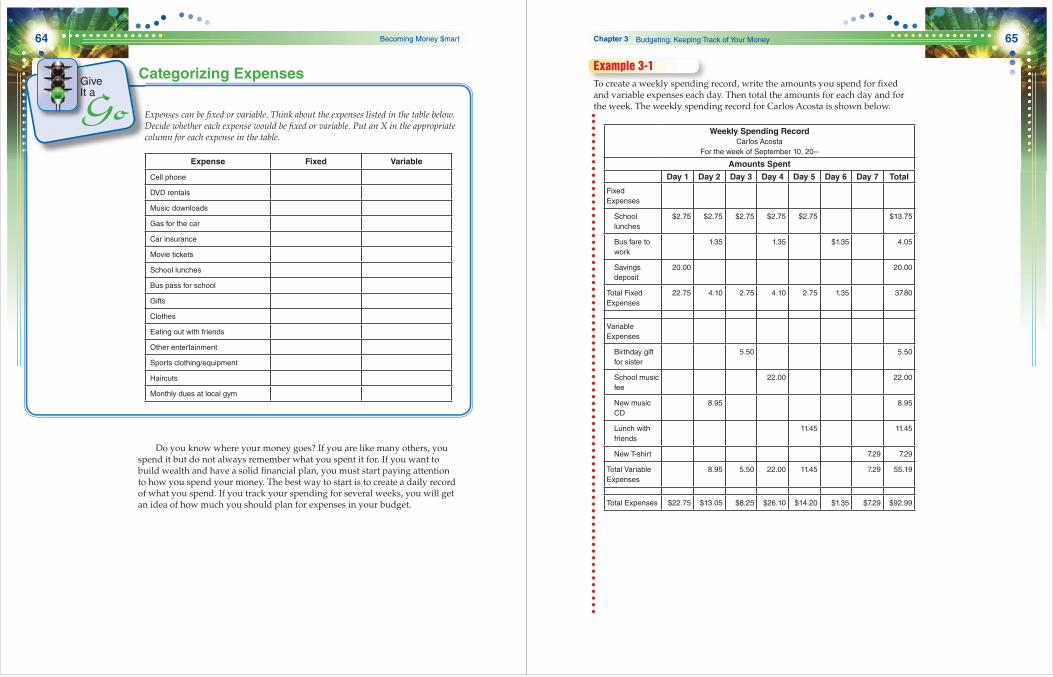

Do you know where your money goes? If you are like many others, you spend it but do not always remember what you spent it for. If you want to build wealth and have a solid fi nancial plan, you must start paying attention to how you spend your money. The best way to start is to create a daily record of what you spend. If you track your spending for several weeks, you will get an idea of how much you should plan for expenses in your budget.

Expenses can be fi xed or variable. Think about the expenses listed in the table below. Decide whether each expense would be fi xed or variable. Put an X in the appropriate column for each expense in the table.

Expense Fixed Variable

Cell phone

DVD rentals

Music downloads

Gas for the car

Car insurance

Movie tickets

School lunches

Bus pass for school

Gifts

Clothes

Eating out with friends

Other entertainment

Sports clothing/equipment

Haircuts

Monthly dues at local gym

Give It a

GoCategorizing Expenses

Chapter 3 Budgeting: Keeping Track of Your Money 65

Example 3-1To create a weekly spending record, write the amounts you spend for fi xed and variable expenses each day. Then total the amounts for each day and for the week. The weekly spending record for Carlos Acosta is shown below.

Weekly Spending RecordCarlos Acosta

For the week of September 10, 20--

Amounts Spent

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7 Total

Fixed

Expenses

School

lunches

$2.75 $2.75 $2.75 $2.75 $2.75 $13.75

Bus fare to

work

1.35 1.35 $1.35 4.05

Savings

deposit

20.00 20.00

Total Fixed

Expenses

22.75 4.10 2.75 4.10 2.75 1.35 37.80

Variable

Expenses

Birthday gift

for sister

5.50 5.50

School music

fee

22.00 22.00

New music

CD

8.95 8.95

Lunch with

friends

11.45 11.45

New T-shirt 7.29 7.29

Total Variable

Expenses

8.95 5.50 22.00 11.45 7.29 55.19

Total Expenses $22.75 $13.05 $8.25 $26.10 $14.20 $1.35 $7.29 $92.99

66 Becoming Money $mart

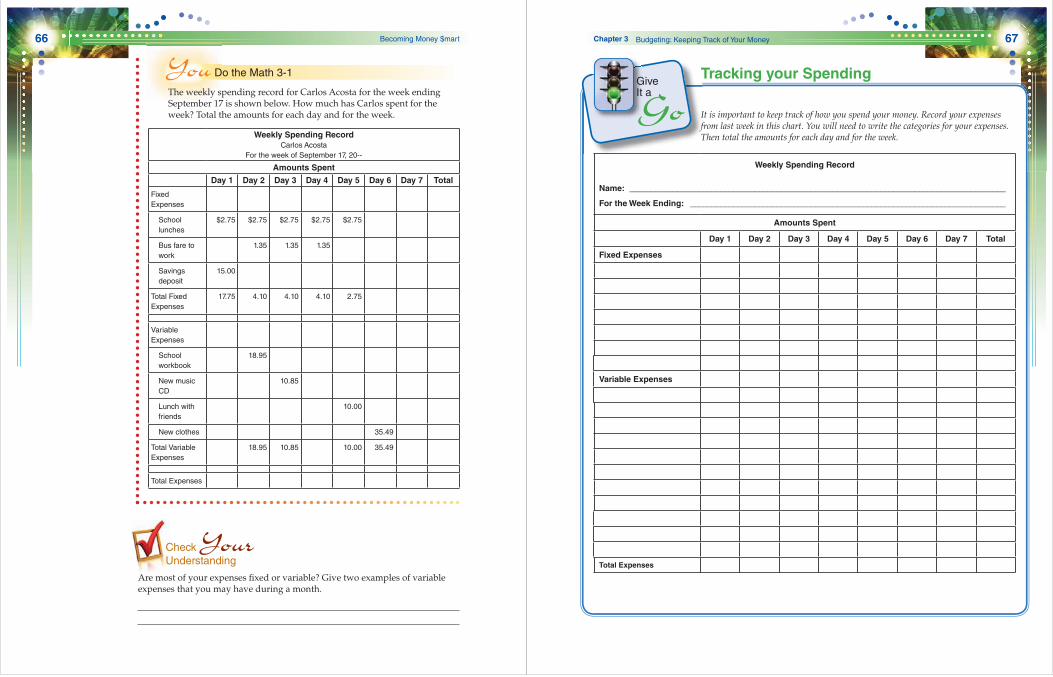

You Do the Math 3-1

The weekly spending record for Carlos Acosta for the week ending September 17 is shown below. How much has Carlos spent for the week? Total the amounts for each day and for the week.

Weekly Spending RecordCarlos Acosta

For the week of September 17, 20--

Amounts Spent

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7 Total

Fixed

Expenses

School

lunches

$2.75 $2.75 $2.75 $2.75 $2.75

Bus fare to

work

1.35 1.35 1.35

Savings

deposit

15.00

Total Fixed

Expenses

17.75 4.10 4.10 4.10 2.75

Variable

Expenses

School

workbook

18.95

New music

CD

10.85

Lunch with

friends

10.00

New clothes 35.49

Total Variable

Expenses

18.95 10.85 10.00 35.49

Total Expenses

Check Your

Understanding

Are most of your expenses fi xed or variable? Give two examples of variable expenses that you may have during a month.

Chapter 3 Budgeting: Keeping Track of Your Money 67

It is important to keep track of how you spend your money. Record your expenses from last week in this chart. You will need to write the categories for your expenses. Then total the amounts for each day and for the week.

Weekly Spending Record

Name: _______________________________________________________________________________________

For the Week Ending: _________________________________________________________________________

Amounts Spent

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7 Total

Fixed Expenses

Variable Expenses

Total Expenses

Give It a

GoTracking your Spending

68 Becoming Money $mart

IncomeIn planning a budget, an important step is to estimate what your income

will be. Income is money you receive. Pay from a job, a birthday gift, and an allowance are examples of income. In the following examples, you will work with a monthly budget and monthly income amounts.

Average Monthly IncomePay from a job is a major source of income for many people. Your net pay

may not be the same every week or every month. If you have a part-time job, you may work a different number of days or hours each week. If you have a full-time job, you might sometimes be sick and not work a full week. To create a monthly budget, you will need to calculate your average monthly net pay. To fi nd average monthly net pay, divide the total net pay by the number of months.

Total Net Pay ÷ Number of Months = Average Monthly Net Pay

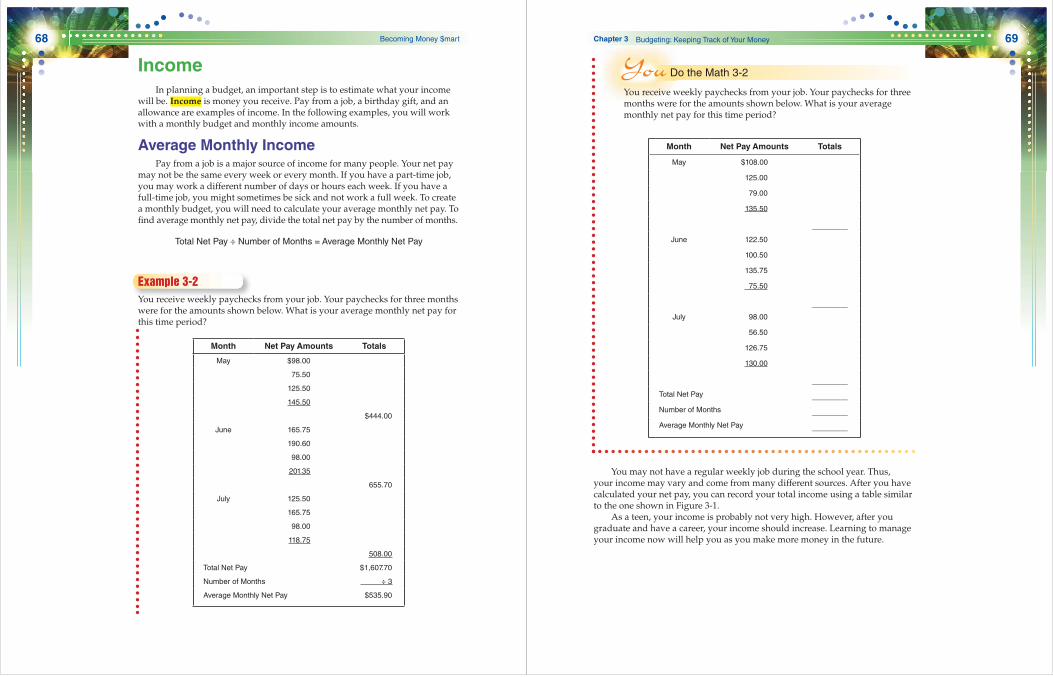

Example 3-2You receive weekly paychecks from your job. Your paychecks for three months were for the amounts shown below. What is your average monthly net pay for this time period?

Month Net Pay Amounts Totals

May $98.00

75.50

125.50

145.50

$444.00

June 165.75

190.60

98.00

201.35

655.70

July 125.50

165.75

98.00

118.75

508.00

Total Net Pay $1,607.70

Number of Months ÷ 3

Average Monthly Net Pay $535.90

Chapter 3 Budgeting: Keeping Track of Your Money 69

You Do the Math 3-2

You receive weekly paychecks from your job. Your paychecks for three months were for the amounts shown below. What is your average monthly net pay for this time period?

Month Net Pay Amounts Totals

May $108.00

125.00

79.00

135.50

_________

June 122.50

100.50

135.75

75.50

_________

July 98.00

56.50

126.75

130.00

_________

Total Net Pay _________

Number of Months _________

Average Monthly Net Pay _________

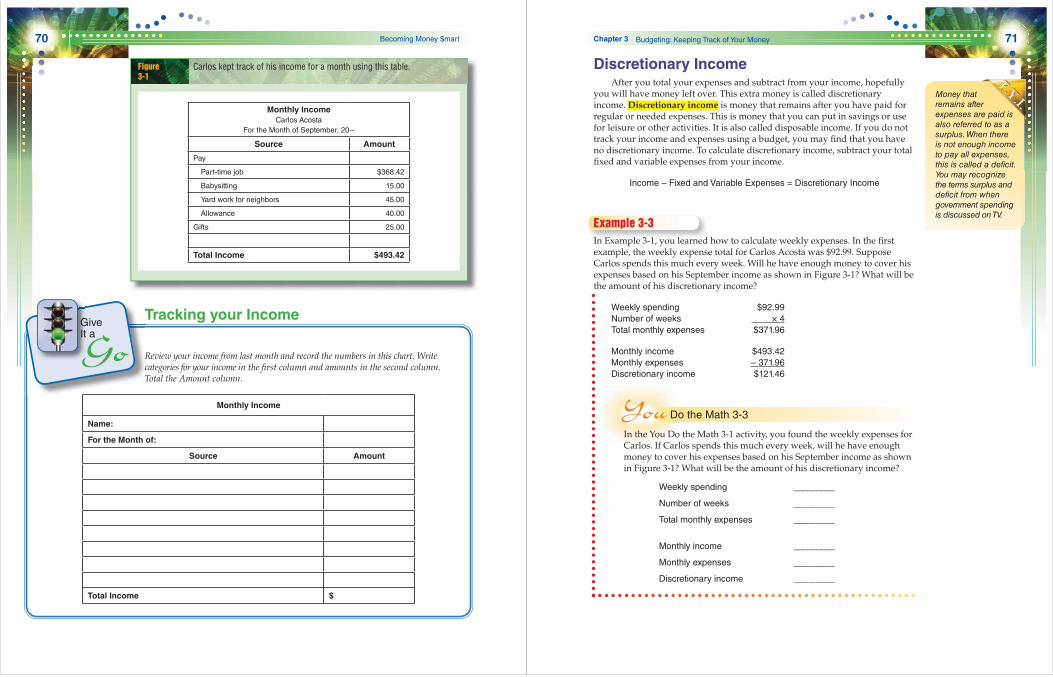

You may not have a regular weekly job during the school year. Thus, your income may vary and come from many different sources. After you have calculated your net pay, you can record your total income using a table similar to the one shown in Figure 3-1.

As a teen, your income is probably not very high. However, after you graduate and have a career, your income should increase. Learning to manage your income now will help you as you make more money in the future.

70 Becoming Money $mart

Carlos kept track of his income for a month using this table.Figure 3-1

Monthly IncomeCarlos Acosta

For the Month of September, 20--

Source Amount

Pay

Part-time job $368.42

Babysitting 15.00

Yard work for neighbors 45.00

Allowance 40.00

Gifts 25.00

Total Income $493.42

Review your income from last month and record the numbers in this chart. Write categories for your income in the fi rst column and amounts in the second column. Total the Amount column.

Monthly Income

Name:

For the Month of:

Source Amount

Total Income $

Give It a

GoTracking your Income

Chapter 3 Budgeting: Keeping Track of Your Money 71

Discretionary IncomeAfter you total your expenses and subtract from your income, hopefully

you will have money left over. This extra money is called discretionary income. Discretionary income is money that remains after you have paid for regular or needed expenses. This is money that you can put in savings or use for leisure or other activities. It is also called disposable income. If you do not track your income and expenses using a budget, you may fi nd that you have no discretionary income. To calculate discretionary income, subtract your total fi xed and variable expenses from your income.

Income – Fixed and Variable Expenses = Discretionary Income

Example 3-3In Example 3-1, you learned how to calculate weekly expenses. In the fi rst example, the weekly expense total for Carlos Acosta was $92.99. Suppose Carlos spends this much every week. Will he have enough money to cover his expenses based on his September income as shown in Figure 3-1? What will be the amount of his discretionary income?

Weekly spending $92.99

Number of weeks × 4

Total monthly expenses $371.96

Monthly income $493.42

Monthly expenses – 371.96

Discretionary income $121.46

You Do the Math 3-3

In the You Do the Math 3-1 activity, you found the weekly expenses for Carlos. If Carlos spends this much every week, will he have enough money to cover his expenses based on his September income as shown in Figure 3-1? What will be the amount of his discretionary income?

Weekly spending _________

Number of weeks _________

Total monthly expenses _________

Monthly income _________

Monthly expenses _________

Discretionary income _________

Money that

remains after

expenses are paid is

also referred to as a

surplus. When there

is not enough income

to pay all expenses,

this is called a deficit.

You may recognize

the terms surplus and

deficit from when

government spending

is discussed on TV.

72 Becoming Money $mart

Creating a BudgetAfter you have tracked your spending for a few weeks, you will see a pattern.

This pattern of spending will help you decide how much you need for movies, lunch, and other items that you purchase during the week. Once you have an idea of how much you need for specifi c items, you are ready to create your budget. A budget will remind you how much you want to spend each week.

To create a budget:

• Select a time period for the budget, such as one month.

• List the amounts of income for the period and total them.

• List the fi xed and variable expenses for the time period and total them.

• Subtract the total expenses from the total income to fi nd discretionary income.

• If the discretionary income amount is a negative number, reduce expenses.

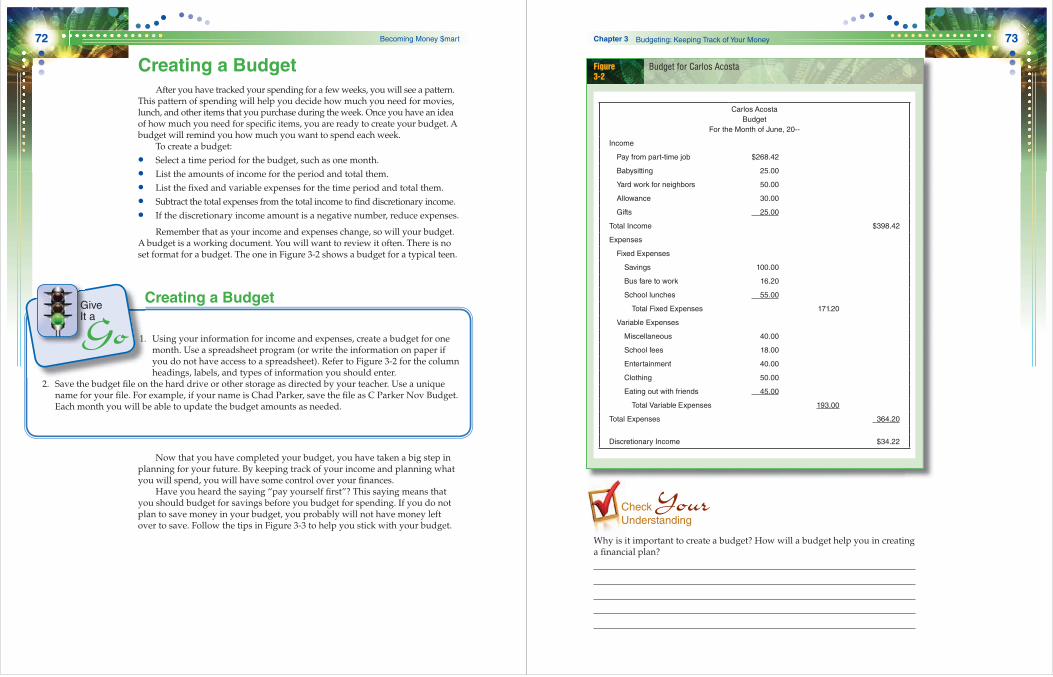

Remember that as your income and expenses change, so will your budget. A budget is a working document. You will want to review it often. There is no set format for a budget. The one in Figure 3-2 shows a budget for a typical teen.

1. Using your information for income and expenses, create a budget for one month. Use a spreadsheet program (or write the information on paper if you do not have access to a spreadsheet). Refer to Figure 3-2 for the column headings, labels, and types of information you should enter.

2. Save the budget fi le on the hard drive or other storage as directed by your teacher. Use a unique name for your fi le. For example, if your name is Chad Parker, save the fi le as C Parker Nov Budget. Each month you will be able to update the budget amounts as needed.

Give It a

GoCreating a Budget

Now that you have completed your budget, you have taken a big step in planning for your future. By keeping track of your income and planning what you will spend, you will have some control over your fi nances.

Have you heard the saying “pay yourself fi rst”? This saying means that you should budget for savings before you budget for spending. If you do not plan to save money in your budget, you probably will not have money left over to save. Follow the tips in Figure 3-3 to help you stick with your budget.

Chapter 3 Budgeting: Keeping Track of Your Money 73

Budget for Carlos AcostaFigure 3-2

Carlos Acosta

Budget

For the Month of June, 20--

Income

Pay from part-time job $268.42

Babysitting 25.00

Yard work for neighbors 50.00

Allowance 30.00

Gifts 25.00

Total Income $398.42

Expenses

Fixed Expenses

Savings 100.00

Bus fare to work 16.20

School lunches 55.00

Total Fixed Expenses 171.20

Variable Expenses

Miscellaneous 40.00

School fees 18.00

Entertainment 40.00

Clothing 50.00

Eating out with friends 45.00

Total Variable Expenses 193.00

Total Expenses 364.20

Discretionary Income $34.22

Check Yo ur

Understanding

Why is it important to create a budget? How will a budget help you in creating a fi nancial plan?

74 Becoming Money $mart

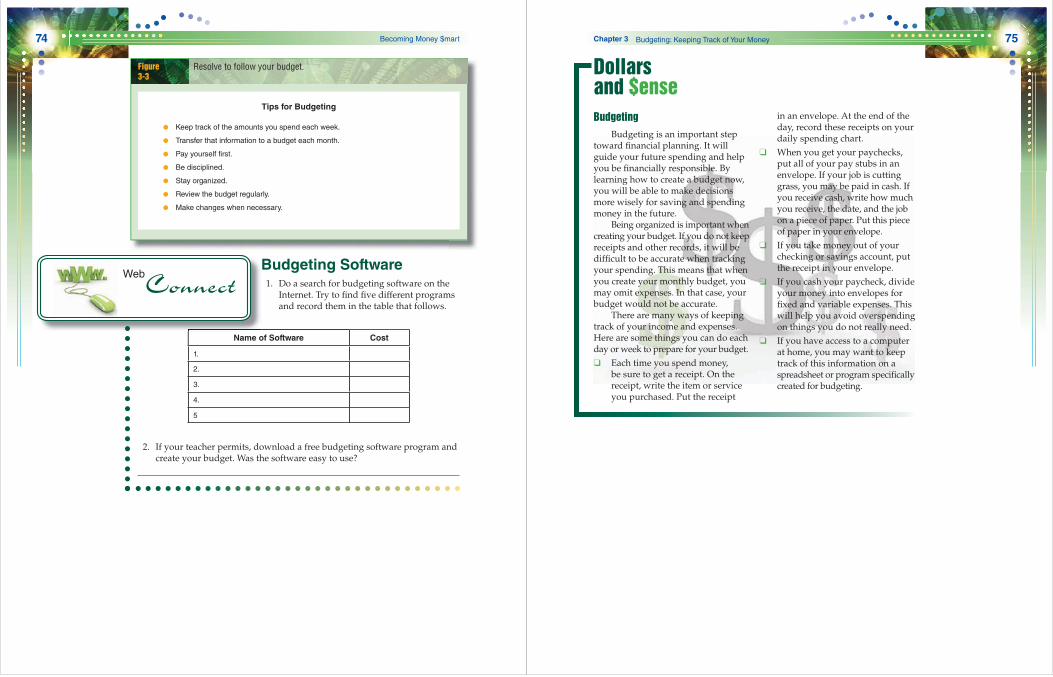

Resolve to follow your budget.Figure 3-3

Tips for Budgeting

● Keep track of the amounts you spend each week.

● Transfer that information to a budget each month.

● Pay yourself first.

● Be disciplined.

● Stay organized.

● Review the budget regularly.

● Make changes when necessary.

1. Do a search for budgeting software on the Internet. Try to fi nd fi ve different programs and record them in the table that follows.

Name of Software Cost

1.

2.

3.

4.

5

2. If your teacher permits, download a free budgeting software program and create your budget. Was the software easy to use?

Web

ConnectBudgeting Software

Chapter 3 Budgeting: Keeping Track of Your Money 75

Dollars and $enseBudgeting

Budgeting is an important step toward fi nancial planning. It will guide your future spending and help you be fi nancially responsible. By learning how to create a budget now, you will be able to make decisions more wisely for saving and spending money in the future.

Being organized is important when creating your budget. If you do not keep receipts and other records, it will be diffi cult to be accurate when tracking your spending. This means that when you create your monthly budget, you may omit expenses. In that case, your budget would not be accurate.

There are many ways of keeping track of your income and expenses. Here are some things you can do each day or week to prepare for your budget.

❑ Each time you spend money, be sure to get a receipt. On the receipt, write the item or service you purchased. Put the receipt

in an envelope. At the end of the day, record these receipts on your daily spending chart.

❑ When you get your paychecks, put all of your pay stubs in an envelope. If your job is cutting grass, you may be paid in cash. If you receive cash, write how much you receive, the date, and the job on a piece of paper. Put this piece of paper in your envelope.

❑ If you take money out of your checking or savings account, put the receipt in your envelope.

❑ If you cash your paycheck, divide your money into envelopes for fi xed and variable expenses. This will help you avoid overspending on things you do not really need.

❑ If you have access to a computer at home, you may want to keep track of this information on a spreadsheet or program specifi cally created for budgeting.

76

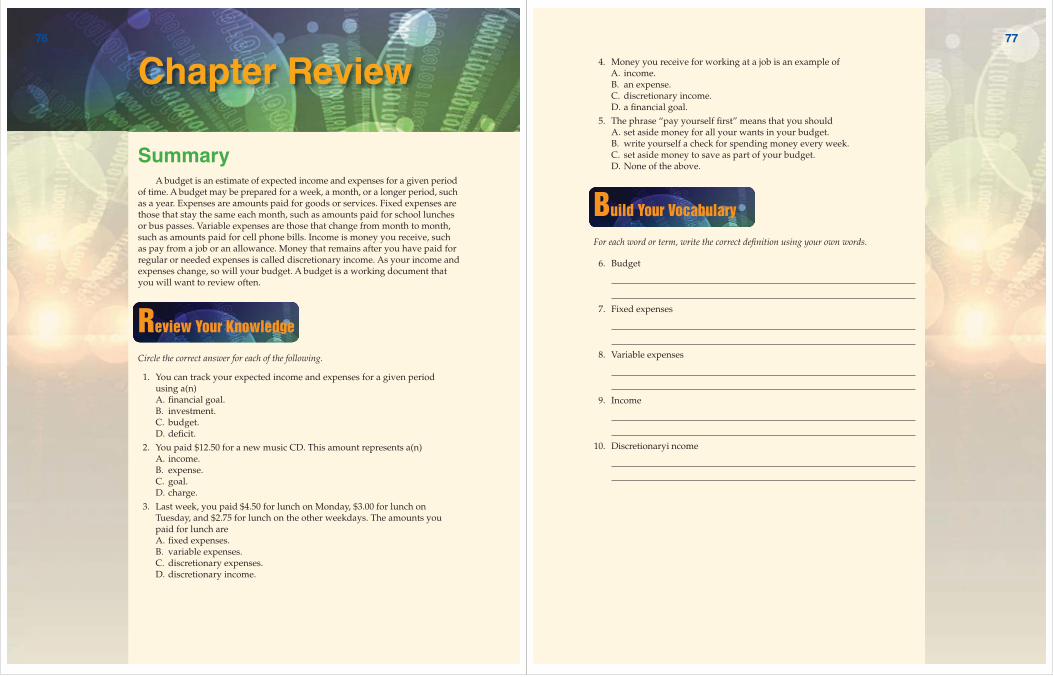

Chapter Review

SummaryA budget is an estimate of expected income and expenses for a given period

of time. A budget may be prepared for a week, a month, or a longer period, such as a year. Expenses are amounts paid for goods or services. Fixed expenses are those that stay the same each month, such as amounts paid for school lunches or bus passes. Variable expenses are those that change from month to month, such as amounts paid for cell phone bills. Income is money you receive, such as pay from a job or an allowance. Money that remains after you have paid for regular or needed expenses is called discretionary income. As your income and expenses change, so will your budget. A budget is a working document that you will want to review often.

Review Your Knowledge

Circle the correct answer for each of the following.

1. You can track your expected income and expenses for a given period using a(n)A. fi nancial goal.B. investment.C. budget.D. defi cit.

2. You paid $12.50 for a new music CD. This amount represents a(n)A. income.B. expense.C. goal.D. charge.

3. Last week, you paid $4.50 for lunch on Monday, $3.00 for lunch on Tuesday, and $2.75 for lunch on the other weekdays. The amounts you paid for lunch areA. fi xed expenses.B. variable expenses.C. discretionary expenses.D. discretionary income.

77

4. Money you receive for working at a job is an example ofA. income.B. an expense.C. discretionary income.D. a fi nancial goal.

5. The phrase “pay yourself fi rst” means that you shouldA. set aside money for all your wants in your budget.B. write yourself a check for spending money every week.C. set aside money to save as part of your budget.D. None of the above.

Build Your Vocabulary

For each word or term, write the correct defi nition using your own words.

6. Budget

7. Fixed expenses

8. Variable expenses

9. Income

10. Discretionary i ncome

78

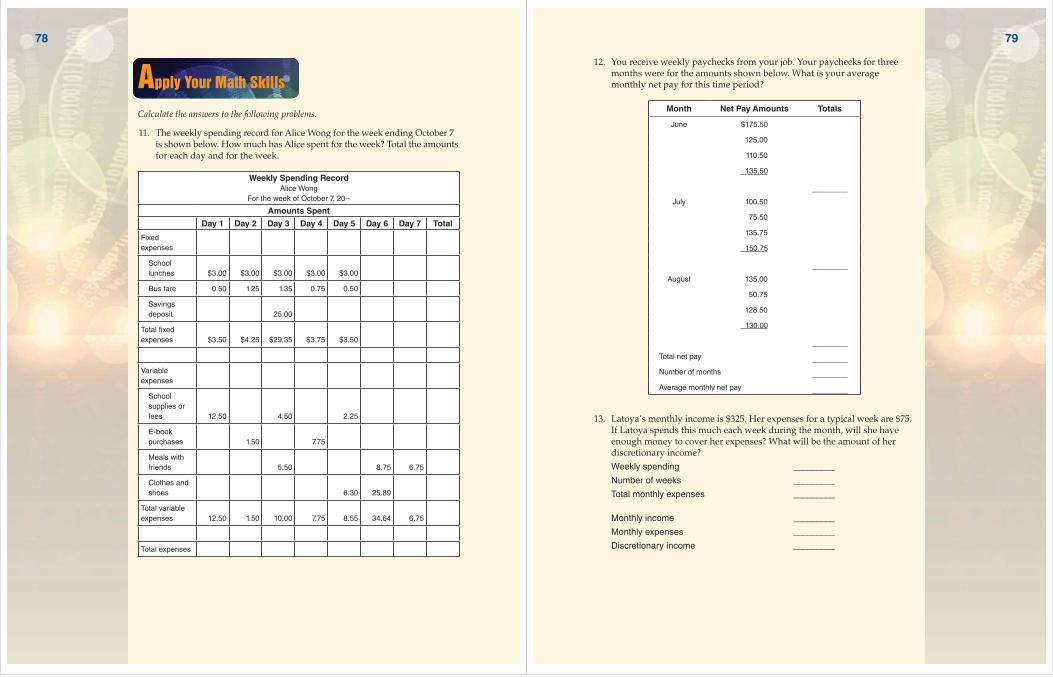

Apply Your Math Skills

Calculate the answers to the following problems.

11. The weekly spending record for Alice Wong for the week ending October 7 is shown below. How much has Alice spent for the week? Total the amounts for each day and for the week.

Weekly Spending RecordAlice Wong

For the week of October 7, 20--

Amounts Spent

Day 1 Day 2 Day 3 Day 4 Day 5 Day 6 Day 7 Total

Fixed

expenses

School

lunches $3.00 $3.00 $3.00 $3.00 $3.00

Bus fare 0.50 1.25 1.35 0.75 0.50

Savings

deposit 25.00

Total fixed

expenses $3.50 $4.25 $29.35 $3.75 $3.50

Variable

expenses

School

supplies or

fees 12.50 4.50 2.25

E-book

purchases 1.50 7.75

Meals with

friends 5.50 8.75 6.75

Clothes and

shoes 6.30 25.89

Total variable

expenses 12.50 1.50 10.00 7.75 8.55 34.64 6.75

Total expenses

79

12. You receive weekly paychecks from your job. Your paychecks for three months were for the amounts shown below. What is your average monthly net pay for this time period?

Month Net Pay Amounts Totals

June $175.50

125.00

110.50

135.50

_________

July 100.50

75.50

135.75

150.75

_________

August 135.00

50.75

128.50

130.00

_________

Total net pay _________

Number of months _________

Average monthly net pay _________

13. Latoya’s monthly income is $325. Her expenses for a typical week are $75. If Latoya spends this much each week during the month, will she have enough money to cover her expenses? What will be the amount of her discretionary income?

Weekly spending _________

Number of weeks _________

Total monthly expenses _________

Monthly income _________

Monthly expenses _________

Discretionary income _________

80

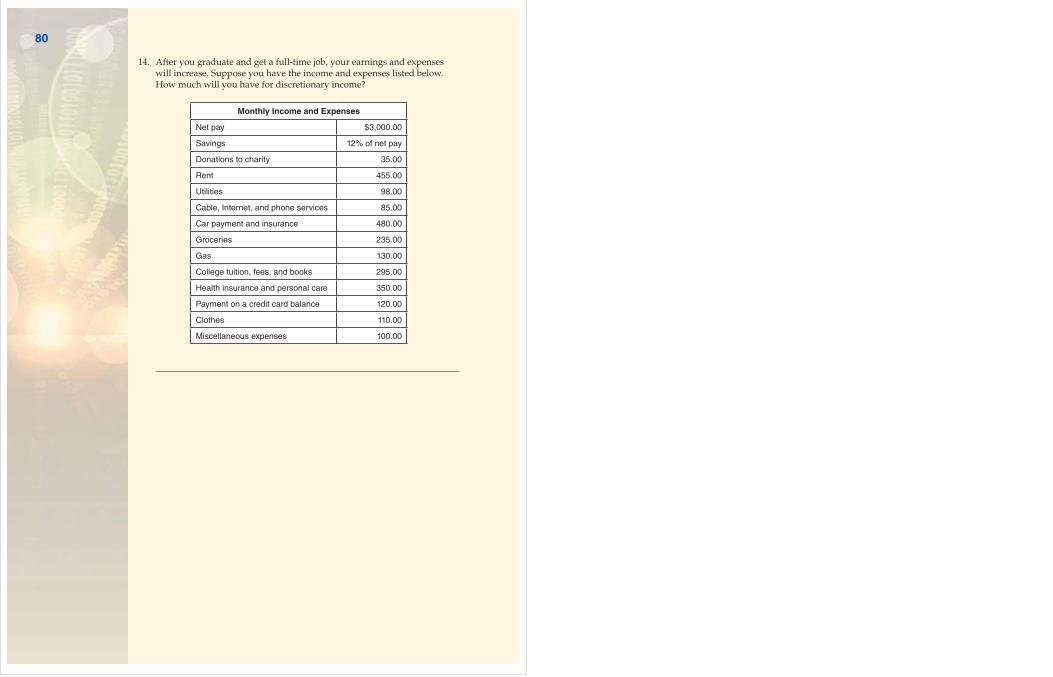

14. After you graduate and get a full-time job, your earnings and expenses will increase. Suppose you have the income and expenses listed below. How much will you have for discretionary income?

Monthly Income and Expenses

Net pay $3,000.00

Savings 12% of net pay

Donations to charity 35.00

Rent 455.00

Utilities 98.00

Cable, Internet, and phone services 85.00

Car payment and insurance 480.00

Groceries 235.00

Gas 130.00

College tuition, fees, and books 295.00

Health insurance and personal care 350.00

Payment on a credit card balance 120.00

Clothes 110.00

Miscellaneous expenses 100.00