brazillian mining, inc

DESCRIPTION

Beacon equity report on Brazillian Mining, IncTRANSCRIPT

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 1

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Company Introduction

Brazilian Mining, Corp.1528 Hwy 395 Suite 130 BGardnerville, NV 89410

Phone Number: (775) 782-9157 Fax Number: (775) 782-4984www.brazilianmining.net

MARKET DATA

SymbolExchangeCurrent PricePrice TargetRatingOutstanding SharesMarket Cap.Average 3M Volume

Source: Yahoo Finance, Analyst Estimates

BRZMOTC PK

$0.15$2.00

Speculative Buy60.45 Mn$9.1 Mn

NA

Brazilian Mining Inc. (formerly Sao Luis Mining Inc.) is a Nevada-based mineral exploration company engaged in diamond mining and precious metal exploration in Brazil. The Company’s strategy is to acquire interests in producing mines or properties with proven reserves, and to develop prospective assets. In 2006, the Company acquired a 51% interest in a joint-venture (JV) partnership with SL Mineradora Ltda, a top diamond producer in the prolific Mato Grosso region of western Brazil. The joint venture involved mining concessions on two properties (Property 231 and Property 117), as well as an existing processing plant in the Sao Luis River Basin. These properties cover an area of about 2,778.51 hectares (6,863 acres) and are part of a 30,000-hectare (74,100 acre) diamond-mining portfolio. The geological surface report on Property 231 filed with Brazil’s National Department of Mineral Production estimates defined surface resources associated with this property at 12.7 million carats, with an estimated value of approximately $300 million at current diamond prices. Bulk samplings taken from alluvial gravels of Property 117 indicate this property may be as rich as or even richer in diamonds than adjacent Property 231.

The Company is implementing a comprehensive plan to develop its mining properties in western Brazil. BRZM seeks to acquire properties that are already in production and/or have proven production-ready resources. In 2009, BRZM plans to expand production from an existing mine, which has been constrained by equipment limitations. BRZM plans to increase this mine’s production three-fold within six months by acquiring two additional diamond sorters and a heavy media plant, and making other mine improvements. With the addition of four DMS plants,

5/01/09

volume

1,400

1,200

1,000

800

600

400

200

0

1.5

1

0.5

0

© BigCharts.com

BRZM daily

Mar Apr

Mill

ions

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 2

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 2

each capable of processing a minimum of 250,000 carats annually, the Company expects to increase production to 100,000 carats per month by 2012. The second phase of the business plan, which will occur simultaneously with increasing production, is a detailed drilling program to delineate and define diamond reserves in the lower depths of its two properties. Current reserve estimates of 12.7 million carats for Property 231 fail to take into account additional resources below the surface or secondary alluvial gravel, which could significantly increase total diamond resource. BRZM offers investors the advantages of ownership interests in well-known, proven producing diamond properties along with additional mineral concessions with potential multi-million dollar resources. Management has assembled a team with deep experience in exploration, diamond mining, diamond polishing, jewelry manufacturing and wholesale marketing. While the Company will likely require significant additional financing to implement its production growth plan, BRZM anticipates a high return on investment resulting from exponential production and revenue growth.

Mining concessions in prolific region of Brazil

The Company’s two mining concessions are located in the state of Mato Grosso, the most productive area for diamond mining in Brazil. According to government data, Mato Grosso accounted for 96.4% of Brazil’s total diamond production in 2006. Several important development-stage mining projects are located in Mato Grosso, which will likely boost this region’s proven diamond reserves.

The Company’s concessions are thought to contain significant diamond reserves. Geological surface reports estimate potential reserves of approximately 12.7 million carats for Property 231. At current market prices, the value of these reserves exceeds $300 million, and this estimate excludes secondary alluvial gravels and/or diamonds below the primary surface. This concession began production in 2000 and the National Department of Mineral Production (DNPM) has documented 119,334 carats of diamond produced from Property 231 in 2004 and 2005. Samples extracted from a second concession, Property 117, indicate that this property may be as rich as or even richer in diamonds than adjacent Property 231.

Mining permits approved by the Brazil government

The Company has already secured the necessary regulatory approvals from Brazilian authorities for mining its two concessions. BRZM has obtained mining approval from SEMA (Secretiatiat Estadual do Meio Ambiente), the environmental agency for the state of Mato Grosso. Its sites have also been inspected by Brazil’s Department of National Mineral Production (DNPM), which has issued licenses allowing mining (Guia de Utilizacao) to commence. There are presently three different sources of diamonds on Property 231 alone, and geomagnetic surveys have identified another seven sources.

Three-fold production increase fuels revenue growth At present, the Company’s diamond mine has one diamond

Investment Highlights

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 3

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 3

sorter operating at full capacity. Capacity constraints limit the quantity of diamonds produced. BRZM plans to add new equipment and make improvements to its mining operations that will increase production three-fold within six months. Over the longer-term, as a new state-of-the-art processing plant is added and mining operations on Property 117 come on line, the Company anticipates increasing monthly production from 25,000 carats currently to 100,000 carats by 2012 and 125,000 carats by 2014. At a conservative price of $23 per carat and 1.2 million carats of production, annualized revenues could exceed $37.5 million by 2012.

Supply/demand imbalances may drive diamond prices higher

BRZM has picked an opportune time to commence diamond production. Many of the world’s diamond-producing mines are close to depleting their reserves, and demand for diamonds is likely to exceed available supply in the near future. According to Rio Tinto, demand for diamond jewelry will rise 3.0% annually while mine production will increase only about 1% annually in carat terms between 2006 and 2020. Supply/demand imbalances will likely drive diamond prices higher. Although the global recession caused demand to drop last year, De Beers, the world’s largest diamond producer, reported sales growth. De Beers and two other major players, Rio Tinto and Alrosa, recently announced production cuts to avert inventory build-up and support higher diamond prices.

BRZM may emerge as an attractive acquisition candidate

The credit crisis and subsequent economic downturn have affected small and medium-sized diamond-mining companies, which are finding it difficult to finance new exploration projects. This creates a favorable atmosphere for consolidation. Small mining companies may become attractive acquisition targets for larger participants who have the financial resources and expertise to develop complex projects. In addition, because of continued political turmoil in Africa, many international mining companies are establishing operations in new markets such as Brazil, and are acquiring producing properties and concessions in those countries.

Exhibit: Supply / demand outlook

Source: Rio Tinto Annual Report

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 4

BRZM is a precious metal mining, exploration and marketing company with mining operations in the São Luis River Basin of Brazil. The Company’s strategy is to seek out and acquire producing mineral assets in North and South America. BRZM owns a 51% interest in a mining joint venture, Comercio e Mineração São Luis Ltda. The Company’s partner, SL Mineradora, was Brazil’s top diamond producer in 2005. The joint venture encompasses two mining concessions, together covering 2,778.51 hectares (6,863 acres) in the Sao Luis River Basin. There concessions are a part of a larger 30,000-hectare (74,100 acres) diamond-mining portfolio located in Mato Grosso, the explorations rights of which are controlled by SL Mineradora. BRZM markets uncut and “conflict-free” diamonds under the Kimberley Process Accord, of which Brazil is a participating member. This accord guarantees these diamonds are produced under transparent and ethical conditions, and will not be sold to fund insurgent activities or war. The Company has already completed one round of private equity financing, and is currently seeking additional funding of $4.5 million for its Brazilian joint venture operations.

BRZM’s two mining concessions (Property 231 and Property 117) are located in the Mato Grosso area of Brazil, approximately 30 kilometers from the town of Juina. The two properties together cover a total area of 2,778.51 hectares.

The first concession (Property 231) covers an area of 1,889.13 hectares (4,666 acres). Diamond production commenced on this site in 2000 and a total of 175,000 carats have been mined. Brazilian authorities documented 119,334 carats of diamonds produced from this property in 2004 and 2005. A geological surface report on file with the National Department of Mineral Production estimates total surface reserves at approximately 12.7 million carats. At current prices, the value of estimated reserves exceeds $300 million. These estimates do not attach a value to additional resources lying below the surface in three primary sources at lower depths or even secondary alluvial gravels deposited below the surface. This site was originally a De Beers concession and has been the subject of extensive geological surveys, the most recent being in 2005.

The second concession (Property 117) covers a total area of 889.38 hectares or 2,197 acres and lies adjacent to

Company Overview

Exhibit: Brazilian Mining Inc – Joint Venture

Source: Company Documents

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 5

the first property. Preliminary bulk samplings of alluvial gravel deposits taken from Property 117 indicate this property could be as mineral rich as or even richer than Property 231. Sampling done in 2007 produced 673 carats of diamonds, including three gem-quality diamonds exceeding two carats. About 50% of the diamonds from this sample averaged more than half a carat per stone, with a grade reaching 0.648 carats per cubic meter in one test area.

The Company’s goal is to become a major diamond producer in Brazil through exploration, acquisition, resource development and joint ventures. BRZM seeks to acquire properties that are already in production or have proven resources of diamonds, gold and silver. The Company holds a 51% interest in two concessions believed to contain significant diamond reserves, and is raising capital to increase production from an existing mine, commence a detailed drilling program to delineate and define reserves at lower depths, and acquire additional resources. In 2006, the Company acquired a 51% interest in the Comercio e Mineração São Luis joint venture. The joint venture has two properties in one of Brazil’s most productive diamond districts. BRZM estimates funding of $4.5 million will be required to develop these two properties. Of the total amount, the Company has earmarked $2 million for Property 231, which will be used to upgrade the existing facility, as well as for the purchase of two additional diamond sorters for the processing plant. The remaining $2.5 million is allocated for exploration and development of Property 117.At present, the Company is operating one diamond sorter at full capacity on Property 231. BRZM believes adding two new sorters and a heavy media plant, along with other planned improvements, will significantly increase diamond production. Three-fold production growth is targeted over the next six months. The Company has

Business Strategy

Exhibit: Map of BRZM.properties in Mato Grosso State, Brazil.

Source: Company web site

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 6

ordered and will soon take delivery of a Dense Media Separation (DMS) plant from ProMet Engineers of South Africa. Each DMS plant is capable of processing a minimum of 250,000 carats per year. The Company anticipates operating two DMS plants by year-end 2009, adding a third machine in 2010 and a fourth machine in 2011. As a result, the Company anticipates increasing production to 100,000 carats per month by 2012 125,000 carats per month by 2014.

The Company has already established a distribution network for marketing its diamonds, consisting of buyers in Israel, Belgium, India and the Republic of South Africa.

Since ancient times, diamonds have been perceived as symbols of luxury. Diamond jewelry is strongly associated with cherished events such as engagements and marriages. In the U.S., wedding and engagement rings account for approximately 50% of diamond sales.

Demand for diamond jewelry is increasing in emerging countries such as India and China as disposable income rises. China, India and the Middle East are expected to contribute significantly to future diamond demand, fueled by their burgeoning middle class, increasing disposable incomes levels and relatively untapped markets.

While the global recession has adversely affected demand for diamonds currently, the long-term trend suggests rising demand and dwindling supply. According to Rio Tinto estimates, demand for real diamond jewellery will increase 3.0% annually over the next decade, while mine production will climb only 1.0% annually in carat terms between 2006 and 2020.

Industry Outlook

Exhibit: Events driving diamond jewelry demand (% Sales generated from each event)

Source: Company Documents Source: IDEX

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 7

Because of the difficulties of securing funding in the current economic environment, many smaller producers have been forced to curtail investment in exploration and new mining projects. The end-result over time will be declining inventories and supply/demand imbalances as demand and the world economy gradually recovers.

The slowdown in exploration and new mine discoveries has led to a steady decline in the world’s proven diamond reserves. This trend is likely to continue and support higher diamond prices over the long-term.

Although the diamond market is experiencing considerable price volatility at present because of weak demand, supply/demand imbalances will translate into sustainable growth in diamond prices over the next decade. According to RBC Capital Markets, diamond prices will remain firm for up to five years and are forecast to increase 2% – 5% annually.

Exhibit: Polished diamond pipeline Exhibit: Polished diamond pipeline

Source: De Beers UK Ltd estimates.Note: Supply figure excludes existing polished stock in pipeline

PWP: Polished wholesale price

Source: Diamonds Annual Review 2008, Rio Tinto

Exhibit: Diamond prices by size October 2006 - January 2009

Source: IDEX

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 8

Consolidation among diamond mining companies

The global diamond market is consolidating, with capacity concentrated among a few key players. The top four industry participants (De Beers, Alrosa, BHP Billiton and Rio Tinto) together account for about 70% of world diamond production. Diamond prices remain relatively stable irrespective of demand because the large players form cartel to arrest any significant price declines in a down cycle by curtailing production.

BRZM competes for concessions, financing, workers and other resources with other diamond and precious metals mining companies operating in North and South America. The next section describes BRZM’s listed competitors. Although De Beers and Alrosa are major diamond producers, neither company is publicly traded.

Harry Winston Diamond Corp. (NYSE: HWD)

Harry Winston Diamond Corp., formerly Aber Diamond Corp., is a specialist diamond enterprise with assets in mining and retailing. HWD has a 40% ownership interest in the Diavik Diamond Mine, which is located in Canada’s Northwest Territories and supplies rough diamonds to the global market. Its retail division, Harry Winston Inc., is a premier diamond jeweler and luxury timepiece retailer, with salons at New York, Paris, London, Beijing, Tokyo and Beverly Hills. HWD’s revenues fell 10% in FY 2009 to $609.2 million because of reduced sales from its mining segment. Net income declined 34% year-over-year to $70.1 million. HWD has proven and probable reserves totaling 21.9 million tons, with 3.5 carats per ton.

Rio Tinto Plc (NYSE: RTP)Rio Tinto plc is one of the largest global mining and exploration companies. The company has major assets in Australia and North America, and business interests in South America, Asia, Europe and southern Africa. Rio Tinto mines for aluminum, copper, iron ore and diamonds. Revenues grew 82.7% in FY 2008 to $54.3 billion; net income climbed to $3.3 billion, led by higher sales of iron ore, aluminum, diamonds and other minerals. In 2007, Rio Tinto produced about 16% of the world’s rough diamonds by volume and 8% by value through its 100% controlled Argyle mine, 60% owned Diavik mine and a 78% interest in the Murowa Diamond Project.

Exhibit: 2007 world production by volume Exhibit: 2007 world production by value

Source: Diamonds Annual Review 2008, Rio Tinto

Competitive Analysis

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 9

Vaaldiam Resources Ltd. (TSE: VAA)

Vaaldiam Resources Ltd. is engaged in diamond production, mine development and exploration in Brazil and Canada. In Brazil, the company has alluvial diamond deposits at its Duas Barras and Chapada mines as well as advanced-stage diamond bearing kimberlite projects. Last year the company acquired Great Western Diamonds Corp. More recently, it suspended mining operations at its Duas Barras mine in Brazil. VAA’s revenues increased four-fold in FY 2008 to $6.3 million from $1.2 million in 2007. Diamond production averages 30,000 carats annually from its Duas Barras and Chapada mines. Inferred resources for the Duas Barras and Chapada mines are 432,000 carats and 270,000 carats, respectively, and the company owns several advanced exploration projects.

Diamond Fields International Ltd. (TSE: DFI)

DFI mines for diamonds and gold in Liberia, nickel in Madagascar, and zinc and copper in Zambia. The company produced more than 41,000 carats from its two diamond mines last year. Revenues rose 33.2% in FY 2008 to $3.3 million, but a net loss of $4.1 million was recorded. At its marine diamond mining operations, the company has estimated resource of 63,000 carats.

Shore Gold Inc. (TSE: SGF)Shore Gold Inc. is mainly engaged in diamond exploration. This company owns a 100% interest in two diamond properties located northwest of the Fort a la Corne kimberlite field area, around 60 kilometers east of Prince Albert, Saskatchewan. Revenues fell 59% in FY 2008 to $1.3 million, and net losses of $378.6 million were recorded.

BRZM is a development-stage company and expects to incur operating losses for the next several quarters as it ramps up investment in its diamond mining operations. In FY 2008, the Company reported revenues of $279,000 and a $1.43 million net loss.

Financial Analysis

RevenueGeneral and administrative expensesOperating Income/ (Loss)Net Income / (Loss)Basic and diluted loss per share

$279,000$1,685,910

$(1,406,910)$(1,437,915)

$(0.025)

_$1,122,556

$(1,122,556)$(1,571,838)

$(0.035)

June 30, 2008 June 30, 2007

Exhibit: Select income statement data

Source: Pink sheets

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 10

As of June 30, 2008, the Company had assets of $4.92 million, including cash of $37,379. Cash consumed by operating activities totaled around $1.34 million in FY 2008. Cash of $32,644 was consumed by investing activities. Financing activities raised cash of approximately $1.4 million, which consisted of the proceeds from loans and sales of common stock. To implement its business plan, BRZM estimates it must raise an additional amount of $4.5 million, most likely through equity sales.

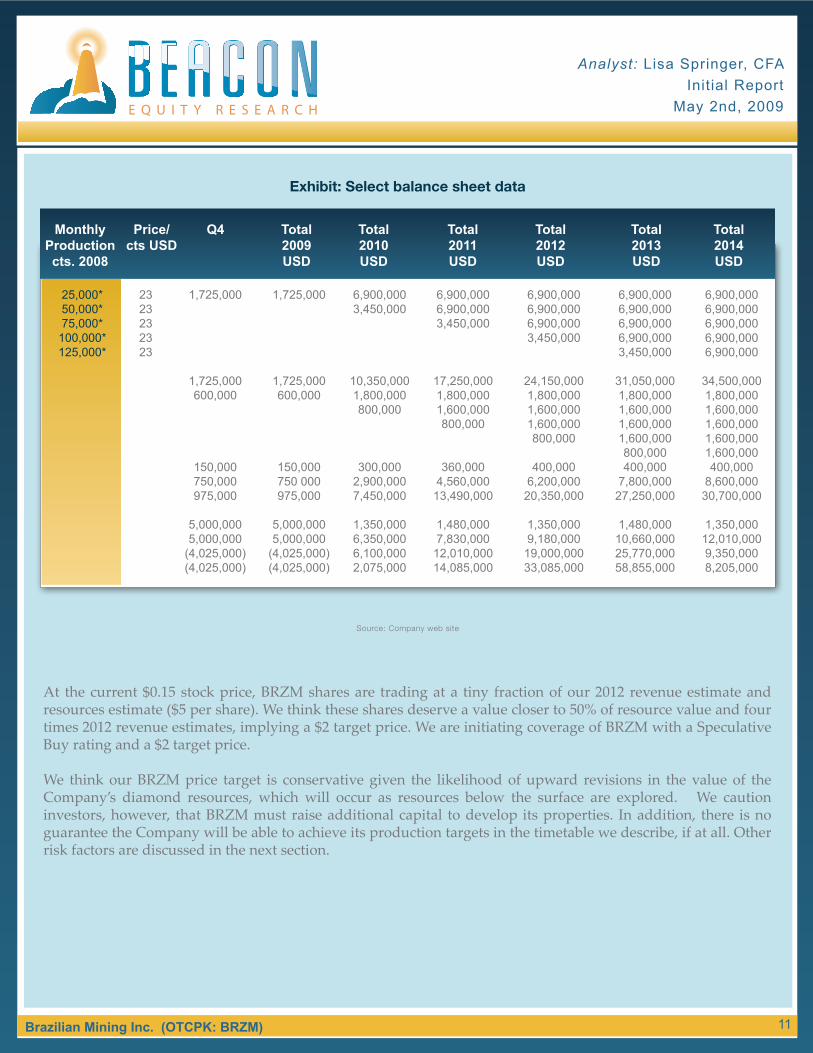

BRZM holds a majority interest in Property 231, which is estimated to contain surface diamond resources of approximately 12.7 million carats (worth $300 million at today’s prices) and Property 117, which may be as rich in diamonds as adjacent Property 231. Currently producing at one mine, BRZM anticipates boosting production three-fold over the next six months. The installation of a DMS plant, which is ready to ship from South Africa, could boost production to 25,000 carats per month. At $23 per carat, this would fuel growth in monthly revenues to $575,000. BRZM targets growth in monthly production to 100,000 carats by 2012 and 125,000 carats by 2014. Assuming 1.2 million carats of production and pricing at $23 per carat, BRZM’s annualized revenues could exceed $27.5 million by 2012. At 1.5 million carats of annual production and $23 prices, the Company’s annualized revenues could rise to $34.5 million in 2014.

Current Assets Property and equipment, netIntangible AssetsTotal assets Total long term liabilities Total current liabilitiesStock holders’ Equity ( deficit )Total liabilities

$467,927$1,711,116$2,744,029$4,923,071$4,505,975$1,021,642$(604,546)$4,923,071

$136,982$1,681,331$2,744,029$4,562,342$4,457,307$1,190,557

$(1,085,522)$4,562,342

June 30, June 30,

Exhibit: Select balance sheet data

Source: Pink Sheets

Financial Outlook and Valuation

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 11

At the current $0.15 stock price, BRZM shares are trading at a tiny fraction of our 2012 revenue estimate and resources estimate ($5 per share). We think these shares deserve a value closer to 50% of resource value and four times 2012 revenue estimates, implying a $2 target price. We are initiating coverage of BRZM with a Speculative Buy rating and a $2 target price.

We think our BRZM price target is conservative given the likelihood of upward revisions in the value of the Company’s diamond resources, which will occur as resources below the surface are explored. We caution investors, however, that BRZM must raise additional capital to develop its properties. In addition, there is no guarantee the Company will be able to achieve its production targets in the timetable we describe, if at all. Other risk factors are discussed in the next section.

25,000*50,000*75,000*

100,000*125,000*

2323232323

1,725,000

1,725,000600,000

150,000750,000975,000

5,000,0005,000,000

(4,025,000)(4,025,000)

1,725,000

1,725,000600,000

150,000750 000975,000

5,000,0005,000,000

(4,025,000)(4,025,000)

6,900,0003,450,000

10,350,0001,800,000800,000

300,0002,900,0007,450,000

1,350,0006,350,0006,100,0002,075,000

6,900,0006,900,0003,450,000

17,250,0001,800,0001,600,000800,000

360,0004,560,000

13,490,000

1,480,0007,830,000

12,010,00014,085,000

6,900,0006,900,0006,900,0003,450,000

24,150,0001,800,0001,600,0001,600,000800,000

400,0006,200,000

20,350,000

1,350,0009,180,000

19,000,00033,085,000

6,900,0006,900,0006,900,0006,900,0003,450,000

31,050,0001,800,0001,600,0001,600,0001,600,000800,000400,000

7,800,00027,250,000

1,480,00010,660,00025,770,00058,855,000

6,900,0006,900,0006,900,0006,900,0006,900,000

34,500,0001,800,0001,600,0001,600,0001,600,0001,600,000400,000

8,600,00030,700,000

1,350,00012,010,0009,350,0008,205,000

Monthly Production cts. 2008

Price/cts USD

Q4 Total 2009 USD

Total 2010 USD

Total 2011 USD

Total 2012 USD

Total 2013 USD

Total 2014 USD

Exhibit: Select balance sheet data

Source: Company web site

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 12

Limited operating history

The Company is still in an early development stage and has a limited production and sales history. It is only re-cently that BRZM has begun generating revenues. Although the Company expects to produce substantial quanti-ties of diamonds from its two concessions, there is no guarantee that the Company’s production estimates will be realized or that its operations will become profitable.

Financing requirements

Management estimates that BRZM must raise at least $4.5 million in additional capital to develop its concessions. Given the Company’s limited production and sales history, there is no guarantee that it will be able to raise the necessary funding on acceptable terms, if at all. In addition, capital raised through equity sales may dilute the ownership interests of existing shareholders.

Growth of counterfeit diamond market

Although there is growing demand for genuine diamonds, there is also a parallel market for less costly substi-tute synthetic stones such as Moissanite. These synthetic stones cost less than one-tenth of genuine diamonds and serve as affordable alternatives for precious stones. Going forward, counterfeit diamonds may cannibalize a larger portion of the genuine diamond market, eroding sales and profits for BRZM and other producers.

Commodity price fluctuations

The prices for rough and polished diamonds are impacted by various supply/demand factors outside the Com-pany’s control, such as demand for jewelry in the international market and disposable income growth. Declining demand could cause diamond prices to fall and adversely affect the Company’s revenues and profits and the value of its mineral reserves.

Risk Factors

Analyst: Lisa Springer, CFA Initial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 13

Mr. Pearl has served as BRZM’s secretary and treasurer since February 2007 and held similar positions with its predecessor, Sao Luis Mining, Inc. He has 30 years of experience in the diamond industry, encompassing the areas of buying, selling and sourcing diamonds and is especially skilled at working with manufactur-ers, wholesalers and major retail chains. Mr. Pearl has served as president of Lad Diamond LLC, a Los Angeles-based international wholesale diamond distribution company, since 2005. He graduated in 1975 as a gemologist from the Gemological Institute of America and received a certificate in jewelry design from the same institute in 1978.

Louis PearlTreasurer and Director

Mr. Müller has been self-employed since 1997 as a financial and business consultant. He has more than 20 years experience in senior executive positions such as CEO, CFO and COO, and has worked for sev-eral international companies. Mr. Müller has held important positions with Eurocellular, Apple Computer Europe, Reuters Ltd., and Zurich (ETH Zürich). He graduated from the Federal Institute of Technology, Zürich (ETH Zürich) with a degree in construction engineering in 1973, and received an MBA from the University of Zürich, Switzerland in 1978.

Stephan P. Müller Director

Management Team

Mr. Dillon became chairman and president of Brazilian Mining Inc. in February 2007 and held similar posi-tions with its predecessor, Sao Luis Mining, Inc. He brings to the Company substantial experience in the mining and energy sectors, as well as expertise in the areas of investor relations, research and development and intellectual property rights. Over the past two decades, he has been involved with a number of suc-cessful several start-up companies, serving in various executive roles such as president, vice president and director of operations. Since January 2007, Mr. Dillon has been the president and director of AC Energy, an alternative energy company. He also served as a consultant and member of the Advisory Board for Juina Mining from 1998 until 2003. Mr. Dillon holds a Bachelor of Arts in business from California State Univer-sity, Sacramento.

Michael J. DillonPresident, Chairman, CEO and Secretary

Analyst: Lisa Springer, CFAInitial Report

May 2nd, 2009

Brazilian Mining Inc. (OTCPK: BRZM) 14

Disclaimer

DO NOT BASE ANY INVESTMENT DECISION UPON ANY MATERIALS FOUND ON THIS REPORT. We are not registered as a securities broker-dealer or an investment adviser either with the U.S. Securities and Exchange Commission (the “SEC”) or with any state securities regulatory authority. We are neither licensed nor qualified to provide investment advice.

The information contained in our report should be viewed as commercial advertisement and is not intended to be investment advice. The report is not provided to any particular individual with a view toward their individual circumstances. The information contained in our report is not an offer to buy or sell securities. We distribute opinions, comments and information free of charge exclusively to individuals who wish to receive them.

Our newsletter and website have been prepared for informational purposes only and are not intended to be used as a complete source of information on any particular company. An individual should never invest in the securities of any of the companies profiled based solely on information contained in our report. Individuals should assume that all information contained in the report about profiled companies is not trustworthy unless verified by their own independent research.

Any individual who chooses to invest in any securities should do so with caution. Investing in securities is speculative and carries a high degree of risk; you may lose some or all of the money that is invested. Always research your own investments and consult with a registered investment advisor or licensed stock broker before investing.

The report is a service of BlueWave Advisors, LLC, a financial public relations firm that has been compensated by the companies profiled. All direct and third party compensation received has been disclosed within each individual profile in accordance with section 17(b) of the Securities Act of 1933. This compensation constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BlueWave Advisors, LLC, and/or its affiliated will hold, buy, and sell securities in the companies profiled. When compensated in shares, all readers should be aware that is our policy to liquidate all shares immediately. We reserve the right to buy or sell the shares of any the com-panies mentioned in any materials we produce at any time. This compensation constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BeaconEquity.com is a Web site wholly-owned by Bluewave Advisors, LLC has been compensated $6,500 from Bismark Consulting. We currently do not hold any position in BRZM. as a marketing budget to manage a comprehensive investor awareness program including the creation and distribution of this report as well as other investor relations efforts.

Information contained in our report will contain “forward looking statements” as defined under Section 27A of the Securities Act of 1933 and Section 21B of the Securities Exchange Act of 1934. Subscribers are cautioned not to place undue reliance upon these forward looking statements. These forward looking statements are subject to a number of known and unknown risks and uncertainties outside of our control that could cause actual operations or results to differ materially from those anticipated. Factors that could affect performance include, but are not limited to, those factors that are discussed in each profiled company’s most recent reports or registration statements filed with the SEC. You should consider these factors in evaluating the forward looking statements included in the report and not place undue reliance upon such statements.

We are committed to providing factual information on the companies that are profiled. However, we do not provide any assurance as to the accuracy or completeness of the informa-tion provided, including information regarding a profiled company’s plans or ability to effect any planned or proposed actions. We have no first-hand knowledge of any profiled company’s operations and therefore cannot comment on their capabilities, intent, resources, nor experience and we make no attempt to do so. Statistical information, dollar amounts, and market size data was provided by the subject company and related sources which we believe to be reliable.

To the fullest extent of the law, we will not be liable to any person or entity for the quality, accuracy, completeness, reliability, or timeliness of the information provided in the report, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information we provide to any person or entity (including, but not limited to, lost profits, loss of opportunities, trading losses, and damages that may result from any inaccuracy or incompleteness of this information).

We encourage you to invest carefully and read investment information available at the websites of the SEC at http://www.sec.gov and FINRA at http://www.finra.org.

All decisions are made solely by the analyst and independent of outside parties or influence.

I, Lisa Springer, CFA, the author of this report, certify that the material and views presented herein represent my personal opinion regarding the content and securities included in this report. In no way has my opinion been influenced by outside parties, nor has my compensation been either directly or indirectly tied to the performance of any security listed. I certify that I do not currently own, nor will own and shares or securities in any of the companies featured in this report.

Lisa Springer, MBA, CFA - Senior Analyst Lisa serves Beacon Research Partners as a research analyst. She brings to the company over 15 years experience in equity research and investment marketing. Prior to joining Beacon, Lisa worked as an equity analyst for an independent research provider. She has also held positions as investor relations officer for a NYSE-listed company and director of financial analysis for a large consulting firm. Lisa earned an MBA from the University of Chicago and is a Chartered Financial Analyst (CFA).