bqoe iii fundamentals of accounting and...

TRANSCRIPT

BQOE III FUNDAMENTALS OF ACCOUNTING AND FINANCE Noor Asma Jamaludin Nor Asma Lode Junaidah Hanim Ahmad Azlan Zainol Abidin Amin Ali Norazita Marina Abd. Aziz

First Printing, January 2009 Copyright @ Open University Malaysia (OUM), BQOE III All rights reserved. No part of this work may be reproduced in any form or by any means without the written permission of the President, Open University Malaysia (OUM). Version January 2009

Project Directors: Prof. Dr. Mansor Fadzil Prof. Dr. Shaari Abd. Hamid Open University Malaysia Module Writers: Noor Asma Jamaludin Nor Asma Lode Junaidah Hanim Ahmad Azlan Zainol Abidin Amin Ali Norazita Marina Abd. Aziz Universiti Utara Malaysia Moderators: Assoc Prof. Dr. Arfah Salleh Assoc. Prof. Hashanah Ismail Universiti Putra Malaysia Azlina Abdul Aziz Loo Sze Wei Rosila Abu Zarin Open University Malaysia Translated & Edited: Pearson (M) Sdn. Bhd. Compiled by: Lilian Kek Siew Yick Open University Malaysia Desktop Publishing: Centre for Instructional Design and Technology Open University Malaysia Printed by: Meteor Doc. Sdn. Bhd. Lot 47-48, Jalan SR 1/9, Seksyen 9, Jalan Serdang Raya, Taman Serdang Raya, 43300 Seri Kembangan, Selangor Darul Ehsan

Table of Contents Course Guide ix-xi Topic 1 Accounting Environment 1 1.1 Introduction to Accounting 2 1.1.1 Definition of Accounting 2 1.1.2 Users of Accounting Information 2 1.1.3 Branches of Accounting 3 1.1.4 Professional Accounting Bodies in Malaysia 4 1.2 Fundamental Accounting Concepts 6 1.2.1 Qualitative Characteristics of

Accounting Information 6 1.2.2 Accounting Assumptions 10 1.2.3 Basic Principles of Accounting 13 1.2.4 Accounting Constraints 16 1.3 Accounting Equation 17 1.3.1 Analysis of Transaction 17 1.3.2 Summary of Analysis 22 1.4 Types and Objectives of Financial Statements 24 1.4.1 Income Statement 25 1.4.2 Statement of Changes in Owner's Equity 25 1.4.3 Balance Sheet 26 1.4.4 Cash Flow Statement 27 Summary 33 Topic 2 Recording Process 34 2.1 Chart of Accounts 35 2.2 Format of Account 37 2.3 Rules of Debit and Credit 38 2.3.1 Normal Balance 39 2.4 Steps in Recording Process 41 2.4.1 Journal 41 2.4.2 Journalising and Posting of Entry 42 2.4.3 Example of Analysis and Summary Transactions 49 2.4.4 Trial Balance 73 Summary 77 Tutorial Question 78

TABLE OF CONTENTS

iv

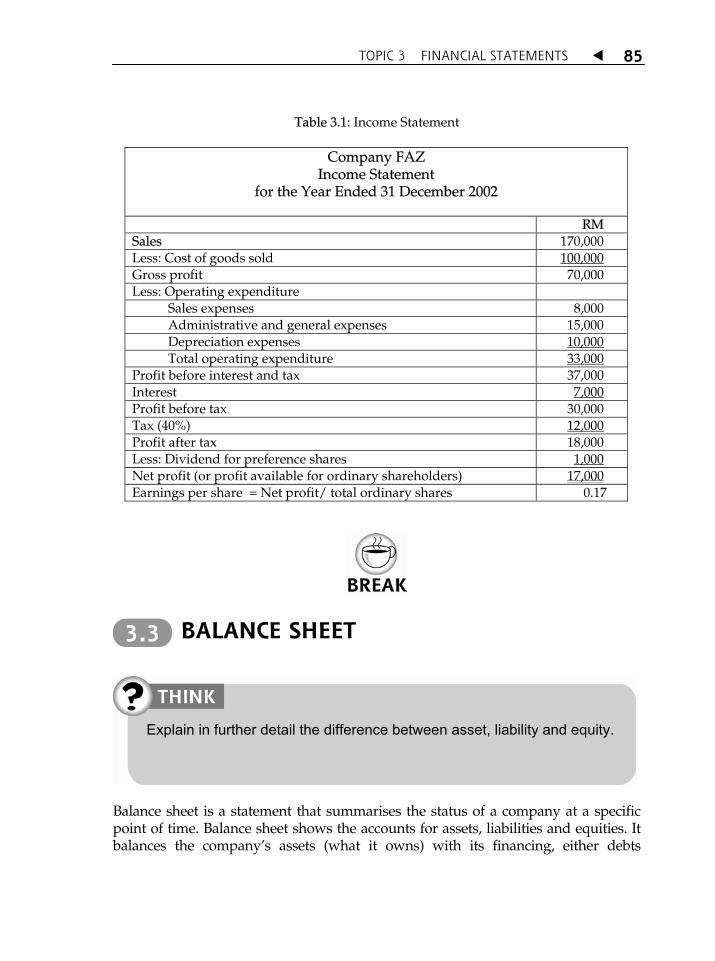

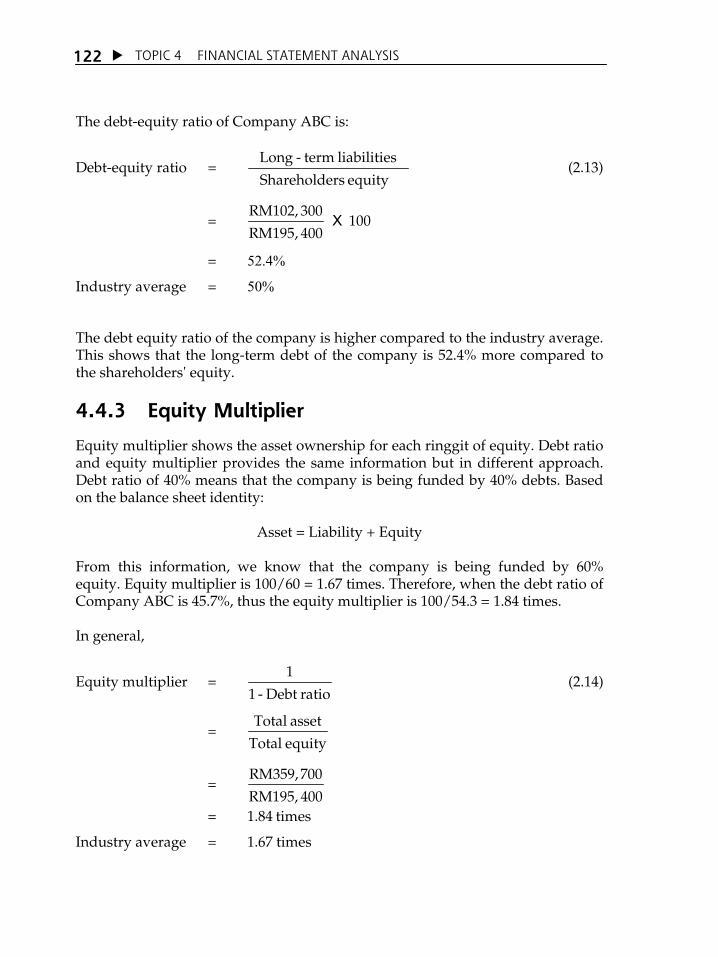

Topic 3 Financial Statements 79 3.1 Annual Report and Users of Financial Statements 80 3.2 Income Statement 82 3.3 Balance Sheet 85 3.3.1 Assets 87 3.3.2 Liabilities 88 3.3.3 OwnersÊ Equity or ShareholderÊs Equity 89 3.3.4 Summary of Basic Accounting 90 3.4 Statement of Retained Earnings 94 3.5 Cash Flow Statement 94 3.5.1 Preparing Cash Flow Statement 95 3.5.2 Differentiating Cash Resources and Usage 98 Summary 104 Topic 4 Financial Statement Analysis 105 4.1 Financial Ratio Analysis 106 4.1.1 Income Statement 108 4.1.2 Balance Sheet 108 4.2 Liquidity Ratio 110 4.2.1 Net Working Capital 110 4.2.2 Current Ratio 111 4.2.3 Quick Ratio 112 4.3 Asset Management Ratio 113 4.3.1 Account Receivable Turnover 114 4.3.2 Average Collection Period 115 4.3.3 Inventory Turnover 116 4.3.4 Average Inventory Sales Period 117 4.3.5 Fixed Asset Turnover 118 4.3.6 Total Asset Turnover 118 4.4 Leverage Ratio 120 4.4.1 Debt Ratio 121 4.4.2 Debt-Equity Ratio 121 4.4.3 Equity Multiplier 122 4.4.4 Interest Coverage Ratio 123 4.5 Profitability Ratio 124 4.5.1 Gross Profit Margin 125 4.5.2 Net Profit Margin 126 4.5.3 Operating Profit Margin 126 4.5.4 Return on Asset 127 4.5.5 Return on Equity 127 4.5.6 Earnings Per Share 128

TABLE OF CONTENTS

v

4.6 Market Value Ratio 128 4.6.1 Price Earnings Ratio 129 4.6.2 Dividend Yield Ratio 130 4.7 Conducting A Complete Ratio Analysis 132 4.7.1 DuPont Analysis 132 4.7.2 Summarising All Financial Ratios 134 4.8 Weakness in Financial Ratio 136 Summary 141 Tutorial Question 142 Topic 5 Time Value of Money 144 5.1 Concept of Compounding and Future Value 145 5.1.1 Time Line 145 5.1.2 Compounding Interest 146 5.1.3 Calculation of Future Value Using Schedule 148 5.1.4 Graphical Illustration of Future Value 149 5.2 Concept of Discounting and Present Value 151 5.2.1 Calculation of Present Value 152 5.2.2 Calculation of Present Value (Principal) Using Schedule 154 5.2.3 Graphical Illustration of Present Value 156 5.3 Single Cash Flow Money Value 157 5.4 Series Cash Flow Money Value 158 5.4.1 Annuity 158 5.4.2 Derivation Cash Flow 166 5.4.3 Perpetuity 170 5.5 Compounding and Discounting More Than Once a Year 172 5.6 Continuous Compounding and Discounting 173 Summary 176 Tutorial Question 176 Answers 178

COURSE GUIDE

INTRODUCTION

Fundamentals of Accounting and Finance is a preparatory course for open entry learners who intend to pursue postgraduate programmes in Masters in Management (MM) and Masters of Business Administration (MBA). This course provides learners with fundamental knowledge in the area of accounting and finance.

COURSE OBJECTIVES

This course integrates the fundamental concepts of Financial Accounting and Financial Management. The first section of this course handles the introduction to the fundamental accounting concepts. This section will also elaborate on the process of preparing accounting information starting from the journal entries to the preparation of financial statement or report. Students will then be taught on how to evaluate, use and apply the financial information provided. At the end of this course, you should be able to:

1. understand the fundamental concepts of accounting;

2. describe the meaning of accounting information, its role as well as its importance;

3. elaborate the process of preparing accounting information from beginning until the completion of the accounting cycle;

4. discuss the functions and information contained in financial statements;

5. analyse the financial performance of a company using financial ratio analysis; and

6. apply the concept of the time value of money in computing cash flows.

COURSE SYNOPSIS

Topic 1 discusses the Accounting Environment. It introduces you to accounting fundamentals, involving the definition of accounting, users of accounting information, branches of accounting, professional accounting bodies in Malaysia as well as the fundamental concepts found in accounting. Also discussed are the accounting assumptions and the four main types of financial statements in financial reporting, namely Income Statement, Statement of Changes in Equity, Balance Sheet and Cash Flow Statement.

COURSE GUIDE

x

Topic 2 discusses the Recording Process. It revolves around the usage of accounts as well as the rules of debit and credit for each type of accounts (asset, liability and owner equity accounts). The rule of debit and credit will also include the normal balance for each type of accounts. This topic also tracks the steps taken in the recording process, which include the journal entry, transfer of entries to ledger and consequently the preparation of balance sheet. A complete example of the whole process is included to provide better understanding. Topic 3 discusses on the different types of financial statements used in business such as the income statement, balance sheet, statement of retained earnings and cash flow statement. You will get to understand the functions well as the information contained in the financial statements. Topic 4 discusses the usage of financial ratio analysis such as the liquidity ratio, asset management, leverage, profitability, and market value ratio. Besides that, this topic also discuss on the DuPont analysis and the overall financial analysis. Topic 5 exposes students to the basic concept for time value of money, which is the concept of present value and future value. You will learn the application and formula for the time value of money for single cash flow and net cash flow, annuity, perpetuity and derivation cash flow. The discussion will also include compounding and discounting methods that occurs more than once a year and compounding and discounting that occurs continuously.

REFERENCES

Emery, D.R., et. al. (1997). Principles of Financial Management. (1st ed.). Prentice Hall.

Gitman, L.J. (2005). Principles of Managerial Finance, (11th ed.). Addison Wesley. Horngren C. T., Harrison W. T. Jr. and Bamber L. S. (2002), Accounting (5th ed.),

Prentice Hall, New Jersey. Larson Kermit D., Wild John J., Chiappetta Barbara, (2004) Fundamentals

Accounting Principles, (17th ed.), McGraw Hill.

Lasher, W.R. (2005). Practical Financial Management, (4th ed.). South-Western Thomson Learning.

Roger, H.H et al. (1997), Accounting: A Business Perspective, (7th ed.), Irwin US.

COURSE GUIDE xi

Scott, D.F. Jr., et. al. (1998). Basic Financial Management (8th ed.). Prentice Hall. Warren C.S., Reeve J. M. and Fess P. E. (2004), Accounting (21st ed.),

International Thompson Publishing, Ohio, USA. Warren et. Al (2001), Accounting: Customized by School Of Accountancy UUM

for Business Accounting Students, Thompson Learning. Weygandt Jerry J., Keiso Donald E., Kimmel Paul D., (2004) Accounting

Principles, (7th ed.), John Wiley & Sons, Inc.

EVALUATION

Refer to the CAPL website at http://capl.oum.edu.my for the evaluation method for this course.

INTRODUCTION

Accounting plays an important role in our daily lives without us realising it. Accounting is a financial information system that helps us make better economic decisions. We might assume that accounting is only important to businessmen or accountants. In fact, we also need accounting in our daily lives. We need financial information to make economic decisions. For example, when making a decision on buying a new car, we need to know the total net revenue in a month (gross revenues minus all expenses) to know whether we can afford to buy the car. We also need to estimate other costs that might be involved in having a car.

TTooppiicc 11 Accounting Environment

LEARNING OUTCOMES At the end of this topic, you should be able to: 1. explain the meaning, role and importance of accounting; 2. state the users and branches of accounting; 3. describe the main functions of professional accounting bodies in

Malaysia; 4. describe the qualitative characteristics of financial information,

assumptions, principles and constraints in accounting; 5. explain the accounting equation; 6. analyse transactions based on the accounting equation; and 7. list 4 main financial statements in financial reporting.

TOPIC 1 ACCOUNTING ENVIRONMENT

2

The above example is only a decision at an individual level. For a business entity, it might need to make a decision on whether to buy a new building or just rent it for operational purposes. Even though it is a higher level decision, the decision- maker still requires the necessary financial information. In this topic, you will be introduced to the basics of accounting. Among them are the definition and branches of accounting, users of accounting information, professional accounting bodies in Malaysia as well as the fundamental concepts in accounting.

INTRODUCTION TO ACCOUNTING

1.1.1 Definition of Accounting

Accounting is an information system that prepares reports on the economic activities of an entity for users to help them make better decisions. More accurately, accounting is:

Economic information are information related to economic activities; whereas an entity refers to a business unit.

1.1.2 Users of Accounting Information

Users of accounting information are parties that use the accounting information for specific purposes. The information required by the users might differ between one group and another. Users of accounting information can be divided into two groups - internal users and external users. Internal users are parties that have direct access to the resources of an entity and usually involved in the management of the entity, for example the management

1.1

You often heard the word ‘accounts’ in your daily lives. However, have you ever thought about the meaning of accounts or accounting? What do you understand about accounting?

A process to identify, measure, record and present the economic information of an entity to the users in order to help them make evaluations or economic decisions.

TOPIC 1 ACCOUNTING ENVIRONMENT 3

of the company. Meanwhile, external users would be the parties who do not have direct access to the resources of the company and do not involved in the management of the company. The other differences between these two groups are summarised in Table 1.1.

Table 1.1: Differences between Internal Users and External Users

Internal Users External Users

Types of information required

Information that can help them make planning and exercise control over the entity.

Information required are different depending on the type of decisions made.

Example: Investor: Require information on the profitability of the company before making decision to invest. Loan providers: Require information on the stability and liquidity of the company before making decision on giving out credit.

How does the information been obtained

Using the status or position in the company.

Limited to what is made available by the company. Example Annual report published by the company.

1.1.3 Branches of Accounting

Accounting is divided into several different branches or other specialised fields. Among them are:

(i) Financial Accounting;

(ii) Management Accounting;

(iii) Taxation; and

(iv) Auditing. These branches are not static as they evolving in time and requirement. This financial accounting course will combine two of the most basic and important accounting branches; that are financial accounting and management accounting.

TOPIC 1 ACCOUNTING ENVIRONMENT

4

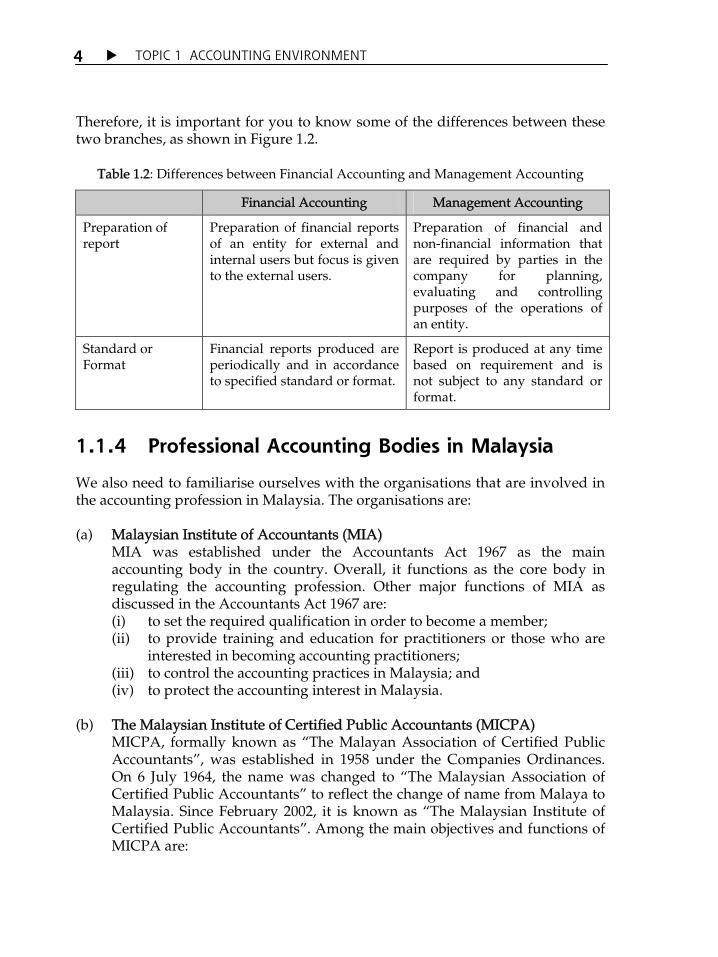

Therefore, it is important for you to know some of the differences between these two branches, as shown in Figure 1.2.

Table 1.2: Differences between Financial Accounting and Management Accounting

1.1.4 Professional Accounting Bodies in Malaysia

We also need to familiarise ourselves with the organisations that are involved in the accounting profession in Malaysia. The organisations are: (a) Malaysian Institute of Accountants (MIA) MIA was established under the Accountants Act 1967 as the main

accounting body in the country. Overall, it functions as the core body in regulating the accounting profession. Other major functions of MIA as discussed in the Accountants Act 1967 are: (i) to set the required qualification in order to become a member; (ii) to provide training and education for practitioners or those who are

interested in becoming accounting practitioners; (iii) to control the accounting practices in Malaysia; and (iv) to protect the accounting interest in Malaysia.

(b) The Malaysian Institute of Certified Public Accountants (MICPA) MICPA, formally known as „The Malayan Association of Certified Public

Accountants‰, was established in 1958 under the Companies Ordinances. On 6 July 1964, the name was changed to „The Malaysian Association of Certified Public Accountants‰ to reflect the change of name from Malaya to Malaysia. Since February 2002, it is known as „The Malaysian Institute of Certified Public Accountants‰. Among the main objectives and functions of MICPA are:

Financial Accounting Management Accounting

Preparation of report

Preparation of financial reports of an entity for external and internal users but focus is given to the external users.

Preparation of financial and non-financial information that are required by parties in the company for planning, evaluating and controlling purposes of the operations of an entity.

Standard or Format

Financial reports produced are periodically and in accordance to specified standard or format.

Report is produced at any time based on requirement and is not subject to any standard or format.

TOPIC 1 ACCOUNTING ENVIRONMENT 5

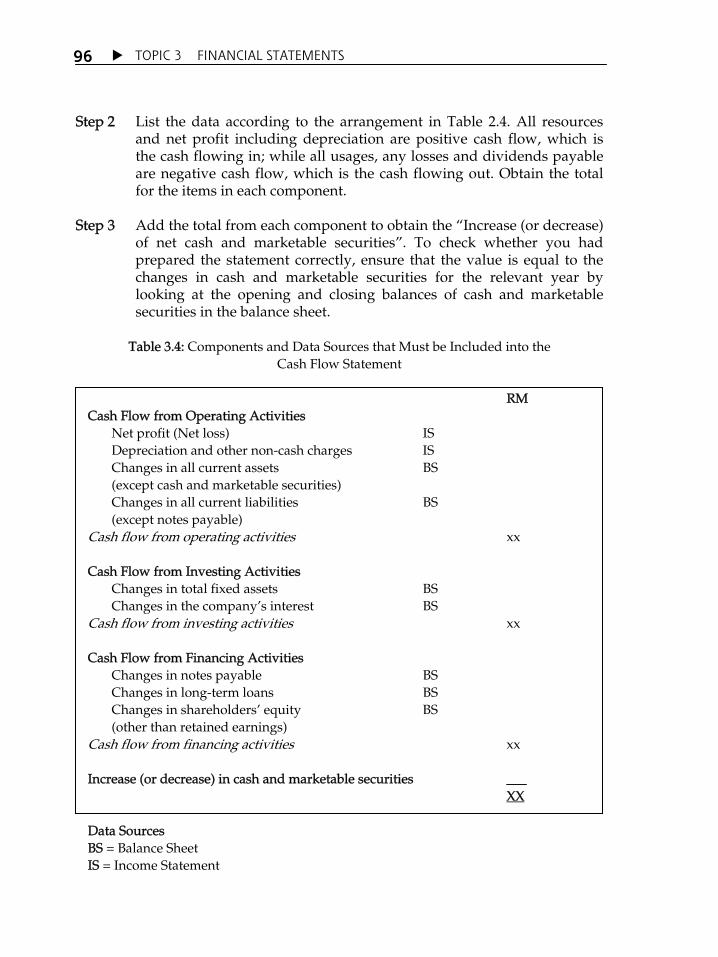

(i) to advance the accounting theories and practices in all aspects; (ii) to train and evaluate the competent members; (iii) to ensure the independence of professional accountants; and (iv) to oversee the practices and professional conducts of its members.

(c) Malaysian Accounting Standards Board (MASB) MASB was established under the Financial Reporting Act 1997. Among the

main functions of MASB are: (i) to set and approve new accounting standards; (ii) to revise or accept the usage of existing standards as approved

accounting standards; and (iii) to develop the conceptual accounting framework.

(d) Financial Reporting Foundation (FRF) FRF was established under the Financial Reporting Act 1997 together with

MASB. Among the main functions of FRF are: (i) to provide opinion to MASB on matters to be implemented; (ii) to evaluate the performance of MASB; and (iii) to be responsible for the overall funding of the operation of MASB,

including to approve its budget.

EXERCISE 1.1 1. Provide examples of common decisions made by both internal and

external users. 2. How does Financial Accounting and Management Accounting assist

users in making decision?

TOPIC 1 ACCOUNTING ENVIRONMENT

6

FUNDAMENTAL ACCOUNTING CONCEPTS

1.2.1 Qualitative Characteristics of Accounting Information

In this section, you will be exposed to the qualitative characteristics of accounting information. Qualitative characteristics of accounting information refer to the characteristics that must be present in the accounting information to make it useful. These characteristics are divided into two categories; primary and secondary qualities. The primary qualities of accounting information are relevant and reliability, while the secondary qualities are comparability and consistency. In summary, accounting information is only useful if it has relevant, reliability, comparability and consistency qualities. Figure 1.1 shows the summary for qualitative characteristics of accounting information.

Figure 1.1: Qualitative characteristics of accounting information

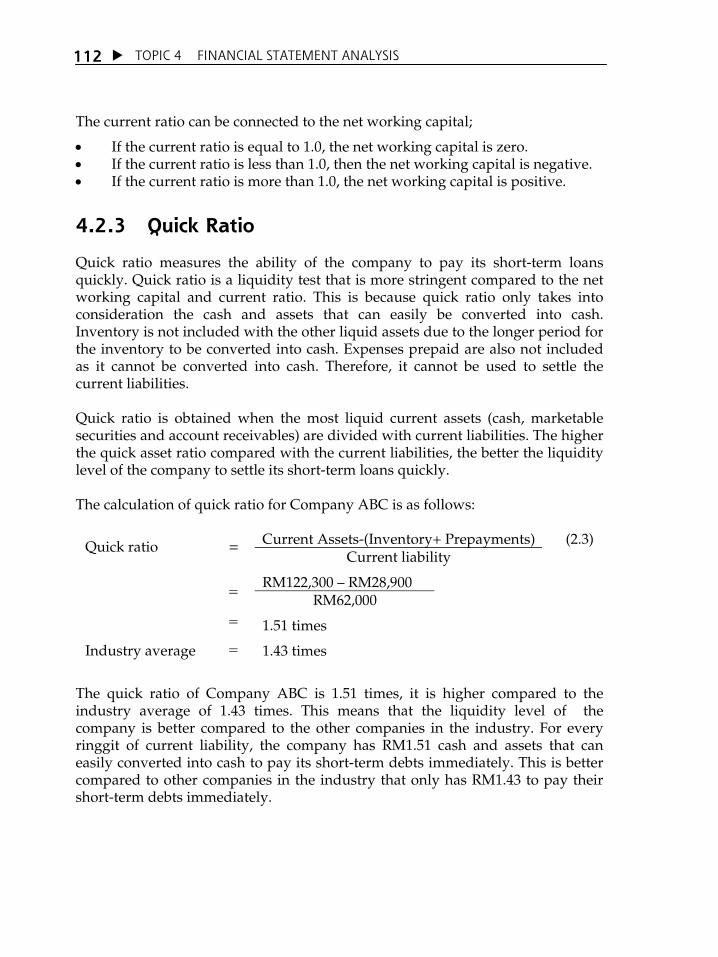

(a) Relevant In everyday terms, we might describe relevant as important or being

related. In accounting, relevant is described as something that makes a

1.2

What are the important qualitative characteristics of accounting information?

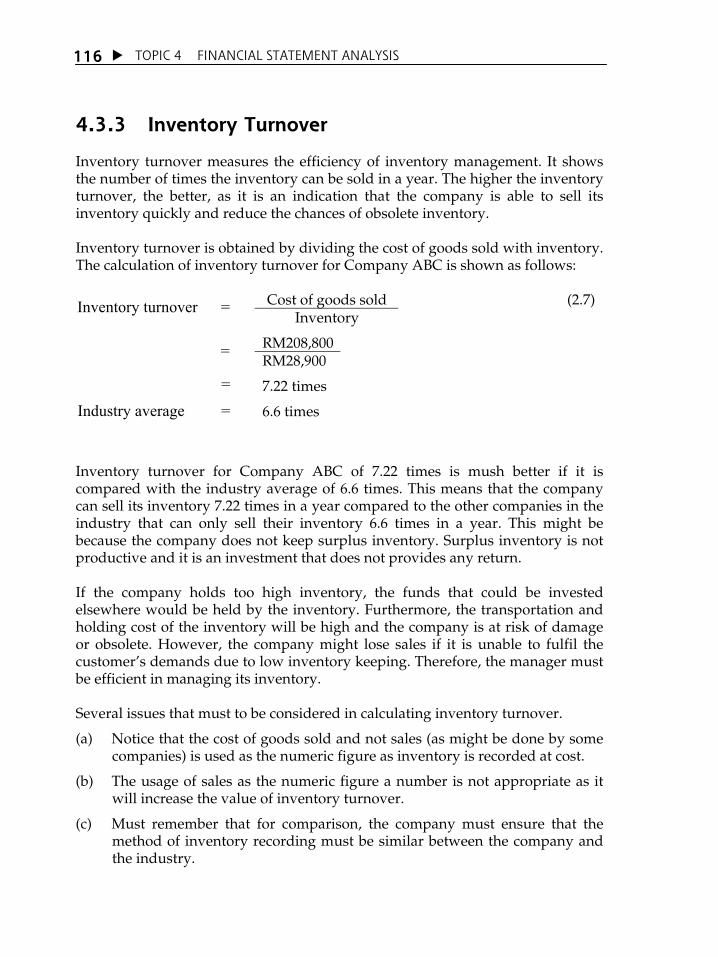

TOPIC 1 ACCOUNTING ENVIRONMENT 7

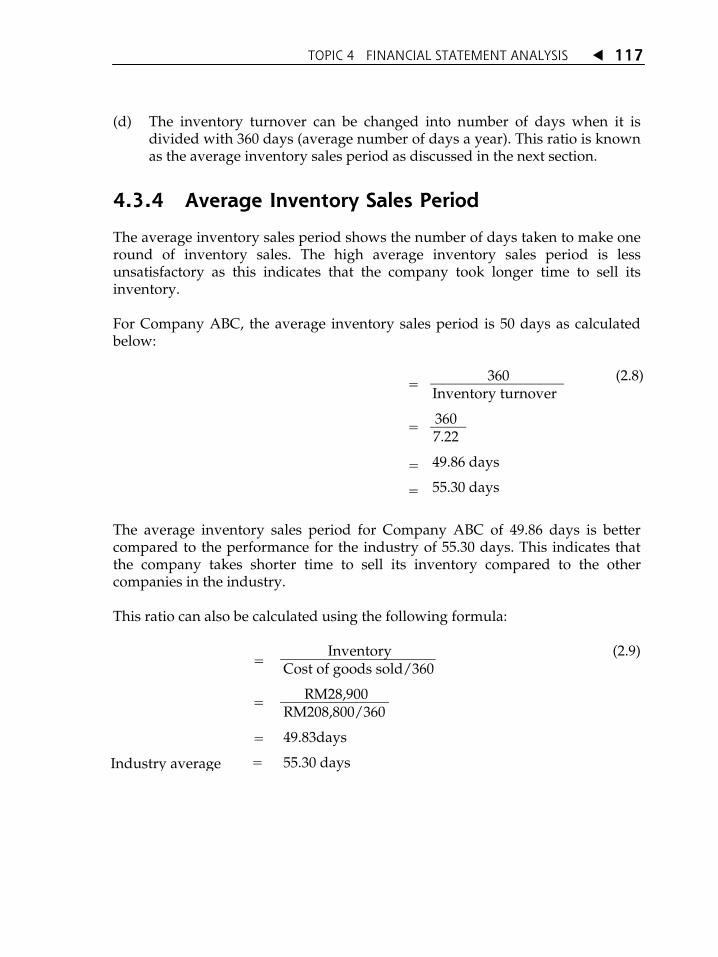

difference in arriving at a decision. In other words, something is said to be relevant if it influences or affects the decision being made.

The extent to which information is considered relevant depends on its

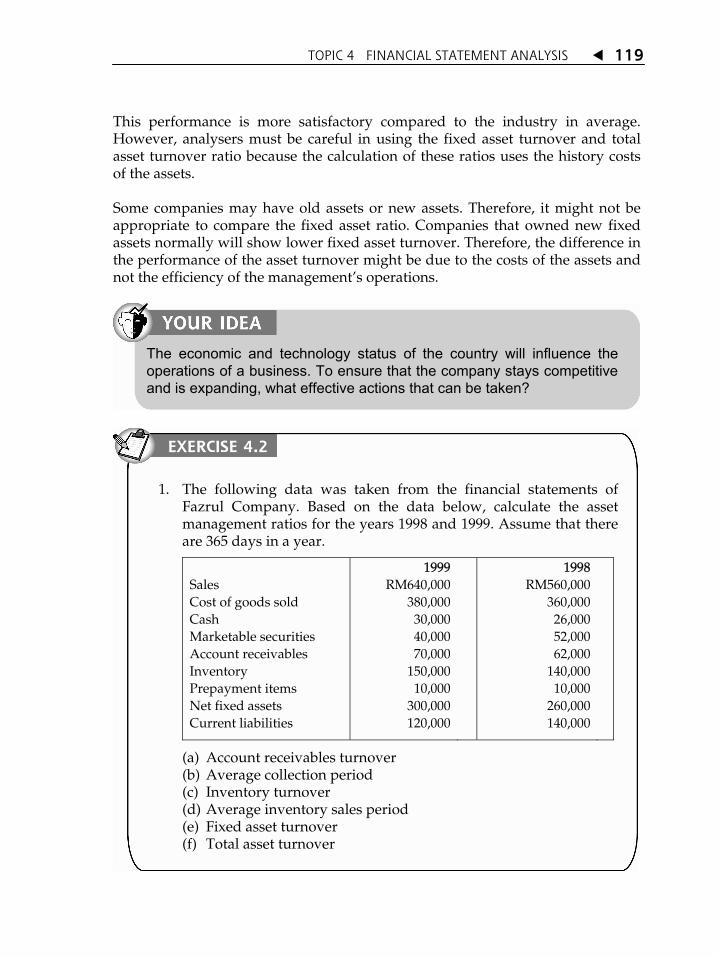

importance in decision making and may differ between one decision maker to another. Information that is relevant to you might not be relevant to another person and vice versa.

For example, suppose you are an investor and you intend to buy shares of a

public listed company. What kind of information might be relevant to your needs? You might want to know the profitability and performance of the said company for the past five years, including new projects or products for the company that will be profitable in the future. This information is relevant as it will influence your decision. Suppose the information that you obtained showed that the company is experiencing continuous losses for the past five years and it does not have any new projects. Will you still proceed with the proposal to invest in the company? Probably not.

Figure 1.2 shows an example of performance information of a company in

order to assist investors in decision making.

Figure 1.2: Performance information of a company to assist investor in decision making.

After knowing the meaning of relevant, you must also know how certain

information are said to be relevant. To become relevant, the information must have three characteristics, namely feedback value, forecast value and timeliness.

TOPIC 1 ACCOUNTING ENVIRONMENT

8

(i) Feedback Value Relevant information must be able to assist users in substantiating or

correcting early expectations matters at hand. (ii) Forecast Value Relevant information must be able to assist users in forecasting. (iii) Timeliness Relevant information must be obtained before it becomes obsolete or

unusable. (b) Reliability Reliability means that users can rely or depend on the said information to

make good decisions. This characteristic is important because users might not have the time or expertise to evaluate some information. Generally, users simply depend on the information presented by the related entity and assume it to be true. This information is then used in decision making.

Reliability does not mean that the said information must be precise. This is

because in accounting there are a lot of information that involves estimation and approximation that might not be precise. What is important is that the estimation and approximation made must be reliable.

Reliable information must have the following characteristics:

(i) Verifiable This means that the accounting information could be verified

objectively by another person using the same method. (ii) Objective Objective in this case means that the information is not biased.

Information contained in the financial statements must be able to fulfil the requirements of various users and not concentrating on certain groups only.

(iii) Trustworthy Information presented is based on the actual result of economic

activities using specified methods. (c) Comparability Comparability means that the information can be compared whether among

companies, industries or different periods. This will enable users to identify the similarities or differences that might exist in the said information. This characteristic is important because information that can be compared is more useful.

This example might help you to understand comparability. Let us assume

that you were told that the net profit of a business in the year 2000 was RM5 million. Is this information useful? This information would only be

TOPIC 1 ACCOUNTING ENVIRONMENT 9

meaningful if you can compare it with the net profit of the business in the year 1999 or the net profit of other businesses in the same industry as shown in Figure 1.3. Thus, financial statements contained in the Annual Report also include information on the previous year in addition to the current year for comparison purposes.

Figure 1.3: Profitability comparison

(d) Consistency Consistency means that an entity must use the same accounting procedures

in every period. It is for the purpose of enabling comparison to be made more effectively. In other words, a company cannot change their accounting procedure every year. This does not mean that the company cannot change the accounting procedure at all. Changes can still be made, but the company must make complete disclosure in the financial statement to explain to the users why they are making the changes and the effect of the changes towards the financial statements.

In your opinion, what will happen to a business entity if it only presents the qualitative characteristics of main accounting information in its annual report?

EXERCISE 1.2

1. State the qualitative characteristics of accounting information. 2. Explain the meaning of comparability provide an example to show

its role in making accounting information useful.

TOPIC 1 ACCOUNTING ENVIRONMENT

10

1.2.2 Accounting Assumptions

In this section you will be exposed to accounting assumptions. There are four accounting assumptions, created to aid the reporting entity and the users, which are generally accepted. They are: (a) Assumption of Separate Entity For the purpose of accounting, an entity is assumed to be separate from its

owner and also other entities. An accounting entity is an economic entity in its own right which controls resources involving economic activities. All activities relating to the accounting entity must be separated from the ownerÊs activities or other accounting entitiesÊ activities. The examples below should explain this concept clearly.

Example 1: Assume that you own a business, your personal economic activities must be

kept separate from the businessÊ economic activities. If you wish to buy products for personal use, you cannot take the businessÊ money and assume that as part of the business activities. Instead, you must record it as drawings. The Drawings Account shows the money or products from the business taken by the owner for personal use.

Example 2: Supposing you have just set up a business which offers computer repair

services. As it is a small business and you are the sole proprietor, the businessÊ cash is deposited into your private account. Assume that on 31 December 2003, the bank balance of your account is RM5,000. Based on your record, RM1,000 is the money from your business and the balance of RM4,000 is funds for your studies.

If you did not comply with the assumption of separate entity and assume

RM5,000 is the money from your business, you might make an inaccurate business decision. You might feel that your business has adequate funds while in fact only RM1,000 is the businessÊ cash. Although all the money belongs to you, from the accounting perspective, RM1,000 is for the business funds and the balance of RM4,000 is the money for your education purposes.

Segregation would enable you to evaluate the financial status of the

business much better and to make accurate decisions to enhance the performance of the business. If an owner has more than one business entity, each entity must be assumed as separate entity from the others. Please refer to the example below.

TOPIC 1 ACCOUNTING ENVIRONMENT 11

Assuming that Mr. Ali owns three different businesses, all three are considered to be separate from accounting perspective. Accounting records must be maintained separately; assets and liabilities for each business cannot be mixed together. Segregation would enable the owner to know the performance for each business.

As a simple example, suppose that Mr. AliÊs businesses show the following

result on 31 December 2003:

Business Transaction (RM)

Business 1 Profit 6,000

Business 2 Loss 8,000

Business 3 Profit 12,000

If the assumption of separate entity is not complied with and all the entities

are assumed as one, Mr. Ali will have an overall business profit of RM10,000 [RM6,000 + (-8,000) + RM12,000]. Based on this result, Mr. Ali might be satisfied and might not take any measures for improvement.

However, by preparing separate accounts, Mr. Ali will know that Business 2

is facing problems as it is suffering a loss of RM8,000, while Business 3 is performing very well with a profit of RM12,000.

(b) Assumption of Going Concern According to this assumption, an entity is assumed to continue to exist and

in operation in the future. This assumption is important because it enables the principle of historical cost to be applied. According to the historical cost principle, all assets and liabilities must be recorded at the purchase price (original cost). For most assets, this cost would be depreciated throughout the life span of the assets to depict its usage. However, asset of property would not be depreciated as its value would always appreciate.

As an example, a machine with a life span of 25 years will be depreciated

for 25 years based on the assumption of going concern. With this assumption, the entity would continue to exist for a period of more than 25 years. If we assume that the entity would exist only for another 10 years in absence of this assumption, we obviously cannot use 25 years as the basis for calculating the depreciation.

The assumption also enables users to make decisions without any doubt or

worries. Suppose you are interested to invest in a company that has consistently achieved high profits in the past few years. However, you were

TOPIC 1 ACCOUNTING ENVIRONMENT

12

informed that the company would exist only for another five years. Would you still continue with your plan to invest in the said company? Generally, we will only invest when we believe the company will continue to exist in the future.

(c) Assumption of Monetary Unit According to this assumption, all economic activities are measured and

valued in currency unit. In Malaysia, the currency unit used is Malaysian Ringgit (RM). Only transactions that can be stated in currency unit will be recorded for accounting purposes. Currency unit enables the transactions to be summarised, reported and compared. Before the existence of currency, transactions were conducted by way of exchanging goods (barter system). The non-existence of currency unit had created difficulties in ascertaining the value of transactions. With a countryÊs standard currency unit, we would be able to value every product.

However, this assumption has two weaknesses, that are:

(i) It restricts the scope of accounting. Only transactions that can be measured in monetary terms will be taken into account, neglecting other factors that have impact on the business.

(ii) It assumes that the value of currency is constantly stable, whereas we know that the currency value is always changing.

(d) Assumption of Accounting Period In the assumption of going concern, we assumed that the entity will

continue to operate for an unlimited period. However, users (whether manager, shareholders, loan providers or other parties) require periodical measurements to help them making decisions. With this assumption, the lifetime of the entity is divided into a certain period for the purpose of reporting its economic activities. Normally the period selected is one year. Financial reports must be produced every accounting year.

The selected accounting period can start from 1 January and ends on 31

December, or starts from 1 July and ends on 30 June the following year, and so on depending on the operation of the company. For example, if an entity is established on 1 March, it might choose an accounting period that starts from 1 March and ends on 28 February of the following year. This accounting period can be changed if the entity feels that there is a need to do so.

TOPIC 1 ACCOUNTING ENVIRONMENT 13

Figure 1.4 shows examples of accounting period.

Starting Date Ending Date

1 January 2001 30 December 2001

1 July 2002 30 June 2003

1 March 2002 28 February 2003

Figure 1.4: Examples of accounting period There are also companies which produce reports within a period of less than a year, for example monthly, quarterly or half yearly. These reports are known as interim reports. Interim report is normally produced to fulfil the requirement of users that might need a more up-to-date report.

1.2.3 Basic Principles of Accounting

After understanding the qualitative characteristics of information and accounting assumptions, you will be exposed to the basic principles of accounting, which are the principles used in the process to identify, measure, evaluate and report financial information. There are four basic principles that you must know: (a) Principle of Historical Cost According to this principle, all business resources will be recorded based on

historical cost, which is the original cost at time of purchase. Although the value of the resources might change in the future, no adjustment will be made to recognise the changes in the value.

There is a company that has obtained high profits consistently for the past 5 years and would exist for a period of another 10 years. Would you invest in the company? Explain your decision.

The word income is used daily especially in relation to business. However, do you know what is meant by income?

TOPIC 1 ACCOUNTING ENVIRONMENT

14

For example, you want to buy a piece of land for your business site. The seller set the price at RM80,000. You do not agree with the price and ask the seller to sell it RM70,000. After negotiation, the seller agreed with the price of RM72,000. In this case, the land would be recorded at the value of RM72,000 in your financial statement. Five years later, you wish to revalue the land. The assessor informed you that the value of the land had appreciated to RM120,000. Although there is a high appreciation in value, you must still record it at the value of RM72,000, which is the original cost of the land during the purchase.

The principle of historical cost is justified by its high reliability. The value

recorded in the financial statement is based on the original cost at the time of purchase supported by documentation. This advantage is also a weakness for certain parties. These parties criticised the failure of the principle to recognise any possible changes in asset value. Regardless, this principle is still adopted.

(b) Principle of Income Recognition Principle of income recognition provides guidance regarding when and

how to recognise income. The three conditions that must be complied with before income is recognised are:

The seller had performed the necessary actions to obtain the income (for example, providing the goods for trade or rendering services);

The amount of income can be measured objectively; and The income can be collected.

Normally, income is recognised at the point of sale. The point of sale refers

to a situation whereby ownership has been transferred from the seller to the buyer, notwithstanding whether the cash has been received or not. For an entity that offers services, the point of sale is when the service has been provided to the customer.

However, in certain cases, the point of sale method is inappropriate. There

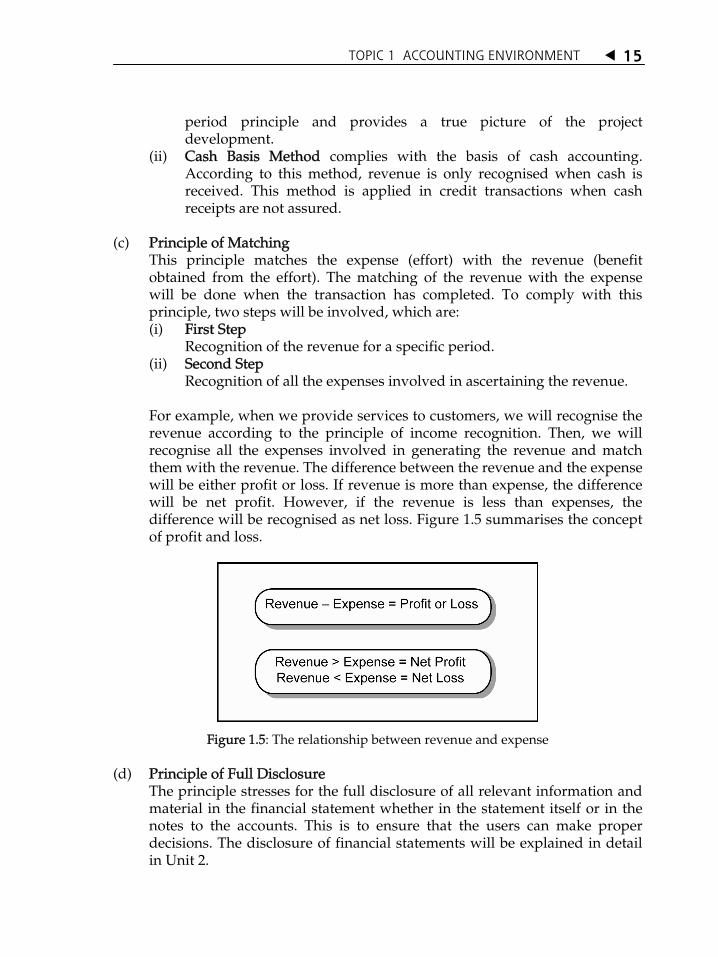

are several different methods that can be used, for instance the percentage of completion and cash basis methods. (i) Percentage of Completion Method is normally used by companies

involved in the construction industry which takes a long time to complete. For example, a housing project might take three years to complete. It would be inappropriate to recognise the revenue only after the project is completed. This is because revenue and expenses accrued throughout the duration of the project that could be determined periodically based on the degree of completion. This method is more appropriate because it complies with the accounting

TOPIC 1 ACCOUNTING ENVIRONMENT 15

period principle and provides a true picture of the project development.

(ii) Cash Basis Method complies with the basis of cash accounting. According to this method, revenue is only recognised when cash is received. This method is applied in credit transactions when cash receipts are not assured.

(c) Principle of Matching

This principle matches the expense (effort) with the revenue (benefit obtained from the effort). The matching of the revenue with the expense will be done when the transaction has completed. To comply with this principle, two steps will be involved, which are: (i) First Step Recognition of the revenue for a specific period. (ii) Second Step Recognition of all the expenses involved in ascertaining the revenue. For example, when we provide services to customers, we will recognise the revenue according to the principle of income recognition. Then, we will recognise all the expenses involved in generating the revenue and match them with the revenue. The difference between the revenue and the expense will be either profit or loss. If revenue is more than expense, the difference will be net profit. However, if the revenue is less than expenses, the difference will be recognised as net loss. Figure 1.5 summarises the concept of profit and loss.

Figure 1.5: The relationship between revenue and expense

(d) Principle of Full Disclosure The principle stresses for the full disclosure of all relevant information and

material in the financial statement whether in the statement itself or in the notes to the accounts. This is to ensure that the users can make proper decisions. The disclosure of financial statements will be explained in detail in Unit 2.

TOPIC 1 ACCOUNTING ENVIRONMENT

16

1.2.4 Accounting Constraints

We have seen the principles that must be complied with in accounting. However, there are constraints or obstructions that might result in these principles not being complied with. The main constraints in accounting are: (a) Cost-Benefit Relationship Before deciding on obtaining specific information, a company would

normally analyse the cost involved and the benefit that may be gained from the information. If the cost of obtaining the information is very high but the benefit generated is not so much, the company might not reveal the information even though all information must be completely disclosed in accordance with the principle of full disclosure.

(b) Materiality Materiality refers to the effect of an item towards the overall operation of

the entity. An item is considered immaterial if it does not affect the decision that will be made. Materiality is often measured based on size. A transaction that involves a huge amount is normally treated as material. A material transaction must be disclosed in detail, while immaterial transactions are sometimes combined or not disclosed in detail.

For example, a small amount of expense like a purchase of stamps and fares

are combined into one account known as sundry expenses. Another example will be the practice of approximation. You can see examples in the annual report published by companies. Generally, companies would not record the cents value, but instead will round the figures up to the nearest ringgit (example: RM471.20 is recorded as RM471). For larger companies, it might make the approximation to the nearest hundred ringgit (example: RM525,795 is recorded as 525,800).

ACTIVITY 1.3

1. Explain the weaknesses exist in the assumption of monetary unit. 2. Describe THREE conditions that must be fulfilled before revenue can

be recognised.

TOPIC 1 ACCOUNTING ENVIRONMENT 17

ACCOUNTING EQUATION

Accounting equation is the basis of accounting that will always be used each time we record a transaction. It consists of three components or basic elements, which are asset, liability and ownerÊs equity. What is meant by asset? Asset is the resources that can bring economic benefit, owned by the entity. For example, cash, building and fittings. For each resource, there must be a claim or rights on it. A simple example, if you own some money, the money belongs to you. If you buy a vehicle with bank loan, the ownership of the vehicle is claimed by the bank until you have settled your loan. In other words, the vehicle is not owned by you (but is owned by the bank) until you have settled your entire loan. It is the same in business. Every asset owned by the business can be claimed either by the owner itself, or loan providers. Rights or claims made by the loan providers are known as liabilities, whereas the rights or claims made by the owner itself are known as equities. Loan providers have priority over the rights to the business assets. If the entity is facing problems, it must first settle its loans. The owner can only claim his rights if there are assets left. Therefore, liability is put ahead of ownerÊs equity in the accounting equation as shown below:

1.3.1 Analysis of Transaction

You must always remember that the accounting equation is always equal regardless of the transaction that has transpired. All transactions can be stated by changes in the three components of the accounting equation. Now we will look at a few common transactions and analyse the results on the accounting equation.

1.3

Accounting Equation:

ASSET = LIABILITY + OWNERÊS EQUITY

A business has assets valued at RM120,000. RM50,000 is the owner’s capital and the balance is bank loan. What is the accounting equation?

TOPIC 1 ACCOUNTING ENVIRONMENT

18

We will use the example of a sole proprietor business owned by Reen. Reen, who is skilled in the computer field, has established her own company on 1 November 2000. For a start, the business (Reen Cyber Service) offers services in computer consultancy. If successful, Reen intends to expand her business to selling computers. The following is a list of transactions incurred by Reen Cyber Service throughout the month of November 2000:

Table 1.3: List of Transactions for Reen Cyber Service, November 2000

No. Date (Nov) Transactions

1 1 Reen invested cash of RM30,000 into Reen Cyber Service.

2 2 Purchased a piece of land valued at RM20,000. The business paid cash RM5,000 and the balance is financed by bank loan.

3 4 Purchased office supplies valued at RM2,700 on credit.

4 15 Received revenue from consultancy services provided to customer. The customer paid RM15,000 cash.

5 30 Paid staff salary expense RM4,250; rental expense RM1,600; utility expense RM900 and other expenses RM550.

6 30 Made payment for account payable of RM1,900.

7 30 Unused office supplies valued at RM1,100.

8 30 Reen withdrew money from the business amounting to RM4,000 for her personal use.

All the transactions above are pertaining to Reen Cyber Service. The personal transactions of the owner (Reen) will not be taken into account if it does not involve the business. Now we have to analyse each transaction to see their effects on the accounting equation. Transaction 1: Reen invested cash of RM30,000 into Reen Cyber Service. Again, it needs to be emphasised that we are only interested in transactions involving Reen Cyber Service, and not ReenÊs personal transactions. Therefore, even though the cash owned by Reen was reduced by RM30,000, the cash owned by Reen Cyber Service has increased by RM30,000. This capital was contributed by Reen. Therefore, ownerÊs equity will increase by RM30,000.

Transaction ASSET = LIABILITY + OWNERÊS EQUITY Cash Capital, Reen 1 30,000 = 30,000

TOPIC 1 ACCOUNTING ENVIRONMENT 19

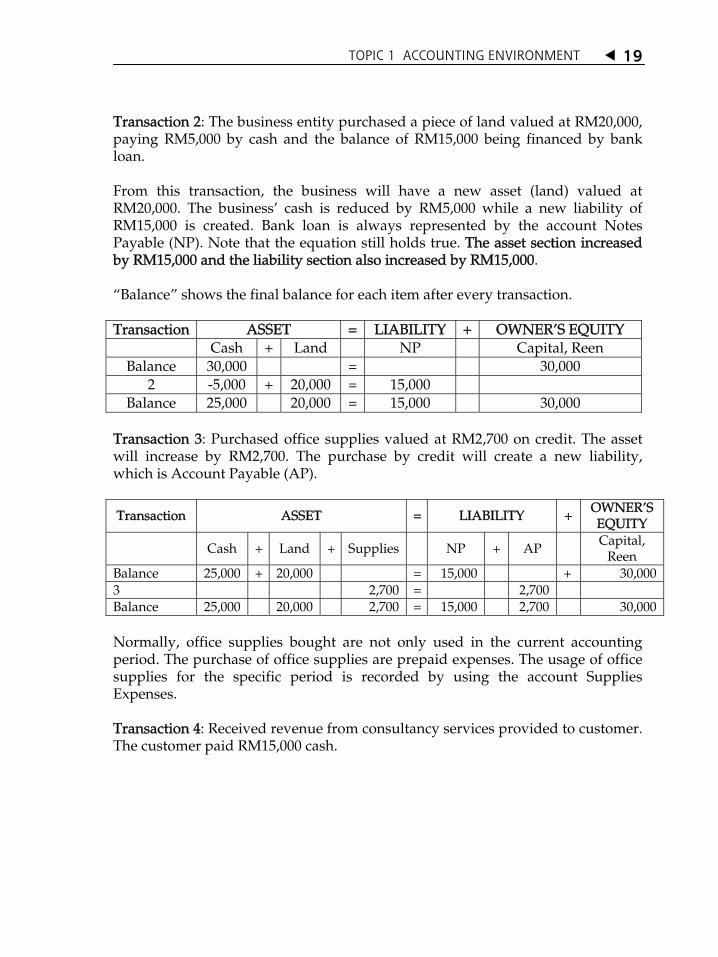

Transaction 2: The business entity purchased a piece of land valued at RM20,000, paying RM5,000 by cash and the balance of RM15,000 being financed by bank loan. From this transaction, the business will have a new asset (land) valued at RM20,000. The businessÊ cash is reduced by RM5,000 while a new liability of RM15,000 is created. Bank loan is always represented by the account Notes Payable (NP). Note that the equation still holds true. The asset section increased by RM15,000 and the liability section also increased by RM15,000. „Balance‰ shows the final balance for each item after every transaction. Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land NP Capital, Reen Balance 30,000 = 30,000

2 -5,000 + 20,000 = 15,000 Balance 25,000 20,000 = 15,000 30,000

Transaction 3: Purchased office supplies valued at RM2,700 on credit. The asset will increase by RM2,700. The purchase by credit will create a new liability, which is Account Payable (AP).

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 25,000 + 20,000 = 15,000 + 30,000 3 2,700 = 2,700 Balance 25,000 20,000 2,700 = 15,000 2,700 30,000 Normally, office supplies bought are not only used in the current accounting period. The purchase of office supplies are prepaid expenses. The usage of office supplies for the specific period is recorded by using the account Supplies Expenses. Transaction 4: Received revenue from consultancy services provided to customer. The customer paid RM15,000 cash.

TOPIC 1 ACCOUNTING ENVIRONMENT

20

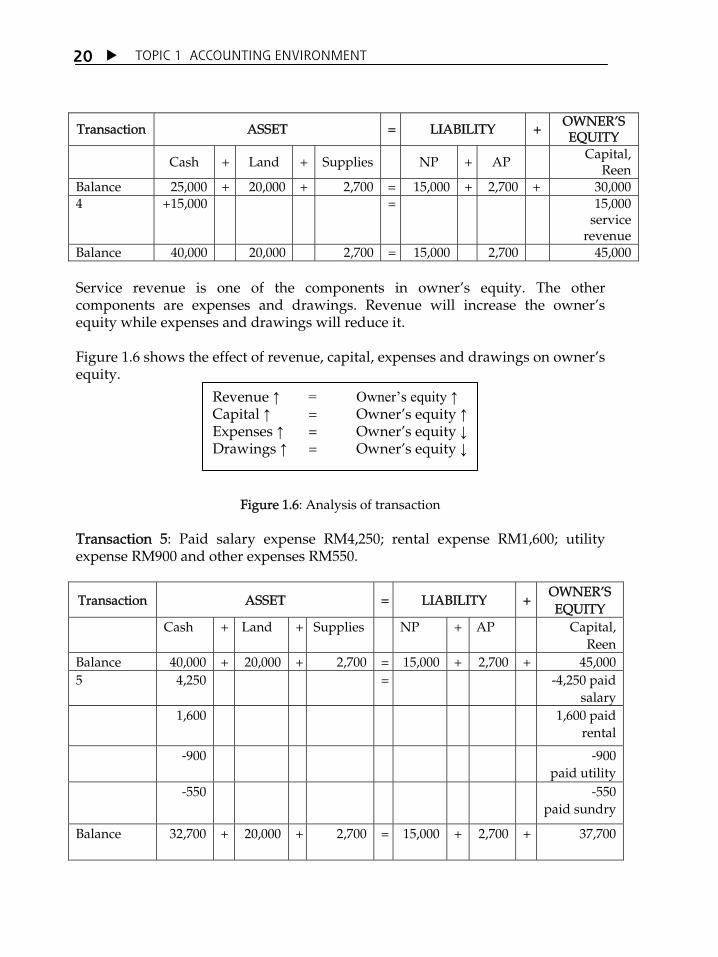

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 25,000 + 20,000 + 2,700 = 15,000 + 2,700 + 30,000 4 +15,000

=

15,000

service revenue

Balance 40,000 20,000 2,700 = 15,000 2,700 45,000 Service revenue is one of the components in ownerÊs equity. The other components are expenses and drawings. Revenue will increase the ownerÊs equity while expenses and drawings will reduce it. Figure 1.6 shows the effect of revenue, capital, expenses and drawings on ownerÊs equity.

Figure 1.6: Analysis of transaction Transaction 5: Paid salary expense RM4,250; rental expense RM1,600; utility expense RM900 and other expenses RM550.

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 40,000 + 20,000 + 2,700 = 15,000 + 2,700 + 45,000 5 4,250 = -4,250 paid

salary 1,600

1,600 paid

rental

-900 -900 paid utility

-550 -550 paid sundry

Balance 32,700 + 20,000 + 2,700 = 15,000 + 2,700 + 37,700

Revenue ↑ = Owner’s equity ↑ Capital ↑ = OwnerÊs equity ↑Expenses ↑ = OwnerÊs equity ↓Drawings ↑ = OwnerÊs equity ↓

TOPIC 1 ACCOUNTING ENVIRONMENT 21

In this transaction, all the expenses were paid by cash. Therefore, cash will decrease according to the amount involved. Each expense item has to be recorded separately and cannot be combined. As explained in transaction 4, expenses will reduce ownerÊs equity. Transaction 6: Made payment for account payable of RM1,900. When the business paid RM1,900, cash will decrease by RM1,900 and liability will also decrease by RM1,900.

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 32,700 + 20,000 + 2,700 = 15,000 + 2,700 + 37,700 6 1,900 = -1,900 Balance 30,800 + 20,000 + 2,700 = 15,000 + 800 + 37,700 Transaction 7: At the end of the month, the unused office supplies were valued at RM1,100. The office supplies was originally bought for RM2,700. The value of office supplies used up during the period is RM1,600 (RM2,700 RM1,100)

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 30,800 + 20,000 + 2,700 = 15,000 + 800 + 37,700 7 -1,600 -1,600 = -1,600

Supplies expenses

Balance 30,800 + 20,000 + 1,100 = 15,000 + 800 + 36,100 Transaction 8: Reen took RM4,000 of the businessÊ cash for personal use.

Transaction ASSET = LIABILITY + OWNERÊS EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

Balance 30,800 + 20,000 + 1,100 = 15,000 + 800 + 36,100 8 4,000 = -4,000 cash

drawings Balance 26,800 + 20,000 + 1,100 = 15,000 + 800 + 32,100

TOPIC 1 ACCOUNTING ENVIRONMENT

22

Drawings is the reverse of capital investment. Capital investment will increase the capital (example in the form of cash) of the business. Drawings will reduce the capital. At the end of the accounting period, the drawings account will be closed and the balance will be transferred to the capital account. Therefore, drawings will be recorded as a reduction in capital account. Although both drawings and expenses reduced capital, there is a clear difference between these two types of accounts. Drawings are not for the purpose of generating revenue, but for the ownerÊs personal use.

1.3.2 Summary of Analysis

Some important items that we must be aware of during the analysis of transaction:

(a) Each transaction will affect, either as an increase or decrease, one or more components in the accounting equation. However, each transaction will definitely involve more than one item in the financial statements;

(b) The accounting equation explained at the earlier stage will always be equal. You can examine this yourself by looking into the „Balance‰ section after every transaction analysis; and

(c) OwnerÊs equity will increase with investment from the owner and revenue, while drawings by the owner and expenses will reduce ownerÊs equity.

Table 1.4 is a summary of analysis for all the transactions of Reen Cyber Service. After all the transactions have been recorded, we will discover that the accounting equation will still be equal.

TOPIC 1 ACCOUNTING ENVIRONMENT 23

Table 1.4: Analysis of Transaction for R.C.S, November 2000

Transaction ASSET = LIABILITY + OWNER EQUITY

Cash + Land + Supplies NP + AP Capital, Reen

1 30,000 = 30,000 investment

by Reen Balance 30,000 = 30,000

2 -5,000 20,000 = 15,000 Balance 25,000 20,000 = 15,000 + 30,000

3 + 2,700 = 2,700 Balance 25,000 + 20,000 + 2,700 = 15,000 + 2,700 + 30,000

4 15,000 = 15,000 service

revenue Balance 40,000 + 20,000 + 2,700 = 15,000 + 2,700 + 45,000

5 4,250 = -4,250 paid

salary -1,600 -1,600

paid rental

-900 -900 paid

utility -550 -550

paid sundry

Balance 32,700 + 20,000 + 2,700 = 15,000 + 2,700 + 37,700 6 1,900 = -1,900

Balance 30,800 + 20,000 + 2,700 = 15,000 + 800 + 37,700 7 1,600 = -1,600

bought supplies

Balance 30,800 + 20,000 + 1,100 = 15,000 + 800 + 36,100 8 4,000 = -4,000

cash drawings

Balance 26,800 + 20,000 + 1,100 = 15,000 + 800 + 32,100

ASSET = LIABILITY + OWNERÊS EQUITY 47,900 = 15,800 + 32,100 47,900 = 47,900

TOPIC 1 ACCOUNTING ENVIRONMENT

24

TYPES AND OBJECTIVES OF FINANCIAL STATEMENT

After the transactions have been identified, analysed and recorded, we need to prepare a report for the users. This report is the final product of the accounting process and is known as financial statement. There are four types of financial statement that you need to know:

(a) Income Statement;

(b) Statement of Changes in OwnerÊs Equity;

(c) Balance Sheet; and

(d) Cash Flow Statement. These statements are interconnected with one another. The title for each statement must contain the reporting entityÊs name, type of statement and the reporting period covered. In this section, we will see in summary, the format for each of the four statements based on the transactions for Reen Cyber Service. We will learn about the preparation of each statement in detail in Unit 2.

Figure 1.7: Types of business

Let us take a look at Figure 1.7. Generally, businesses are divided into three types, which are sole proprietorship, partnership and company. Sole proprietorship is owned by a single owner while partnership is owned by 2 to 20 owners. Financial statements for these two types of business are not subject to the standards released by MASB. Therefore, there might be several formats used by these two types of business. Companies are divided into private limited and public listed companies. Private limited companies can be owned by 2 to 50 owners. However, there are unlimited number of owners for public listed companies. The preparation of financial

1.4

TOPIC 1 ACCOUNTING ENVIRONMENT 25

statements for companies is subject to the standards released by MASB, whether in the form of accounting method, disclosure and reporting format.

1.4.1 Income Statement

This statement is also known as Profit and Loss statement which lists all the revenues and expenses incurred by the entity for a specific period. The difference between the revenue and expense will result in either net profit or net loss. Excess of revenue over expense will give us net profit, while expense in excess of revenue will give us net loss. Figure 1.8 shows the income statement for Reen Cyber Service for the month ended 30 November 2000.

Reen Cyber Service Income Statement

for the month ended 30 November 2000 RM RM

Service revenue Expenses: Salary expenses Rental expenses Utility expenses Supplies expenses Sundry expenses

4,250 1,600

900 1,600

550

15,000

(8,900)

Net profit 6,100

Figure 1.8: Income statement/Profit and loss statement

1.4.2 Statement of Changes in Owner’s Equity

This statement shows the changes in ownerÊs equity for a specific accounting period. OwnerÊs equity will increase when the owner makes a capital investment or when the entity gains net profit. OwnerÊs equity will decrease when the owner makes drawings or when the entity incurs net loss. Figure 1.9 shows the statement of changes in ownerÊs equity for Reen Cyber Services.

TOPIC 1 ACCOUNTING ENVIRONMENT

26

Reen Cyber Service Statement of Changes in OwnerÊs Equity for the month ended 30 November 2000

Opening Capital 1 November (+) Net profit

(-) Drawings

Closing Capital 30 November

RM 30,000 6,100

36,100 (4,000)

32,100

Figure 1.9: Statement of changes in ownerÊs equity

1.4.3 Balance Sheet

This statement is also known as the financial position statement, listing all the assets, liabilities and ownerÊs equity of the entity on a specific date. The purpose of this statement is to show the financial status of the entity on a specific date. There are two formats normally used, which are the statement format and accounts format. The accounts format places the asset on the left side with liability and ownerÊs equity on the right side (refer to Figure 1.10 and Figure 1.11)

Reen Cyber Service Balance Sheet

as at 30 November 2000

ASSETS RM LIABILITIES AND OWNERÊS EQUITY RM

Current Assets: Liabilities:

Cash 26,800 Current Liabilities:

Supplies 1,100 Account payable 800

27,900 Long-term liabilities:

Fixed Assets: Notes payable 15,000

Land 20,000 Total liabilities 15,800

Owner Equity:

Capital 32,100

TOTAL LIABILITIES AND

TOTAL ASSETS 47,900 OWNERÊS EQUITY 47,900

Figure 1.10: Balance Sheet in accounts format

TOPIC 1 ACCOUNTING ENVIRONMENT 27

In the statement format, the asset, liability and ownerÊs equity are listed vertically.

Reen Cyber Service Balance Sheet

as at 30 November 2000

RM RM

Fixed Assets:

Land 20,000

Current Assets:

Cash 26,800

Supplies 1,100

27,900

( ) Current liabilities:

Account payable (800)

27,100

Net current assets 47,100

Financed by:

OwnerÊs equity:

Capital, Reen 32,100

Long term liabilities:

Notes payable 15,000

47,100

Figure 1.11: Balance Sheet in statement format

1.4.4 Cash Flow Statement

This statement reports all the cash receipts and payments of the entity in a specific period. Through this statement, the users will know the sources of cash received and why cash is paid. The difference between cash inflows and outflows will provide the final cash account balance of the entity. This balance will be the same as the cash amount shown in the Balance Sheet. In the cash flow statement, cash transactions are divided according to the type of activities, which are operating, investing and financing activities. Figure 1.12 shows the cash flow statement for Reen Cyber Services.

TOPIC 1 ACCOUNTING ENVIRONMENT

28

Reen Cyber Services Cash Flow Statement

for the month ended 30 November 2000

RM RM RM Cash from operating activities:

Cash received from customers 15,000 ( ) Expenditure paid 7,300 Payment to supplier 1,900 (9,200) Net cash flow from operating activities 5,800

Cash from investing activities: Payment for purchase of land (5,000) Net cash flow from investing activities (5,000)

Cash flow from financing activities: Investment by owner 30,000 ( ) Drawings by owner (4,000) Net cash flow from financing activities 26,000 Net cash flow for entity and cash account balance as at 30 November 26,800

Figure 1.12: Cash flow statement

Discuss the issues that might arise if a business entity did not disclose the relevant information in its financial statement.

TOPIC 1 ACCOUNTING ENVIRONMENT 29

Further information regarding the professional accounting bodies in Malaysia can be obtained from the following websites: Malaysian Institute of Accountants (MIA) www.mia.org.my

The Malaysian Institute of Certified Public Accountants (MICPA)

www.micpa.com.my

Malaysian Accounting Standards Board (MASB) www.masb.org.my

Financial Reporting Foundation (FRF) www.masb.org.my

EXERCISE 1.4

1. Fill the blanks with the most accurate answer: (a) Financial statement prepared on a yearly basis complies with the

assumption of ______________. (b) The principle that requires the economic resources of the entity

to be recorded at the original cost at time of purchase is the principle of ___________.

(c) _____________ information must have feedback value, forecast value and is presented on a timely basis.

(d) The professional body responsible for setting the accounting standards in Malaysia is _______________________________.

(e) The qualitative characteristic that enables users to depend or rely on the information presented is _____________.

(f) The principle that matches the revenue with the expenses in the specific accounting period is ___________________.

(g) Not all accounting information can be disclosed in detail due to constraints of ___________________ and __________________.

(h) The branch of accounting that prepares specialised information for internal users and not subject to specified standard or format is ______________.

(i) According to the assumption of _____________, the entity is assumed to continue to exist and in operation in the future.

(j) Revenue is normally recognised when ________________. (k) The statement that shows the cash flow of an entity for a specific

period is _______________. (l) ____________________ lists all the assets, liabilities and ownerÊs

equity of an entity in a specific period.

TOPIC 1 ACCOUNTING ENVIRONMENT

30

2. If revenue = RM12,000; expense = RM8,400 and drawings by owner =

RM2,000; how much is the net profit or net loss for that period? A. Net profit RM5,600 B. Net loss RM3,600 C. Net profit RM1,600 D. Net profit RM3,600

3. Which of these is NOT a qualitative characteristic of accounting

information? A. Materiality B. Reliability C. Relevant D. Comparability

4. One example of internal user is:

A. Inland Revenue Board B. Investor C. Creditors D. Management

5. If the total assets increased by RM15,000 and the total liabilities decreased

by RM10,000; ownerÊs equity had: A. increased by RM5,000 B. decreased by RM5,000 C. increased by RM25,000 D. decreased by RM25,000

6. For the purpose of simplifying accounting, the business owner and

business entity are assumed as the same.

True False 7. The accounting period for all businesses must start from 1 January and

ends at 31 December each year.

True False

8. Income statement shows the net profit or loss of a business entity at a specific date.

True False

TOPIC 1 ACCOUNTING ENVIRONMENT 31

9. Determine the appropriate amount in the spaces marked „?‰

ASSET = LIABILITY + OWNERÊS EQUITY

(a) 84,000 = ? + 38,000

(b) ? = 72,000 + 28,000

(c) 125,000 = 50,000 + ?

10. State the effects of the following transactions on the asset, liability and ownerÊs equity. An example is shown in transaction (a):

Transaction Effect

(a) Paid debts to supplier. Asset decreased, Liability decreased.

(b) Purchased office equipment by cash.

(c) Owner took cash from the business for personal use.

(d) Paid staff salary for the current period.

(e) Received cash from customer to settle his account receivable.

(f) Owner contributed office equipment for business use.

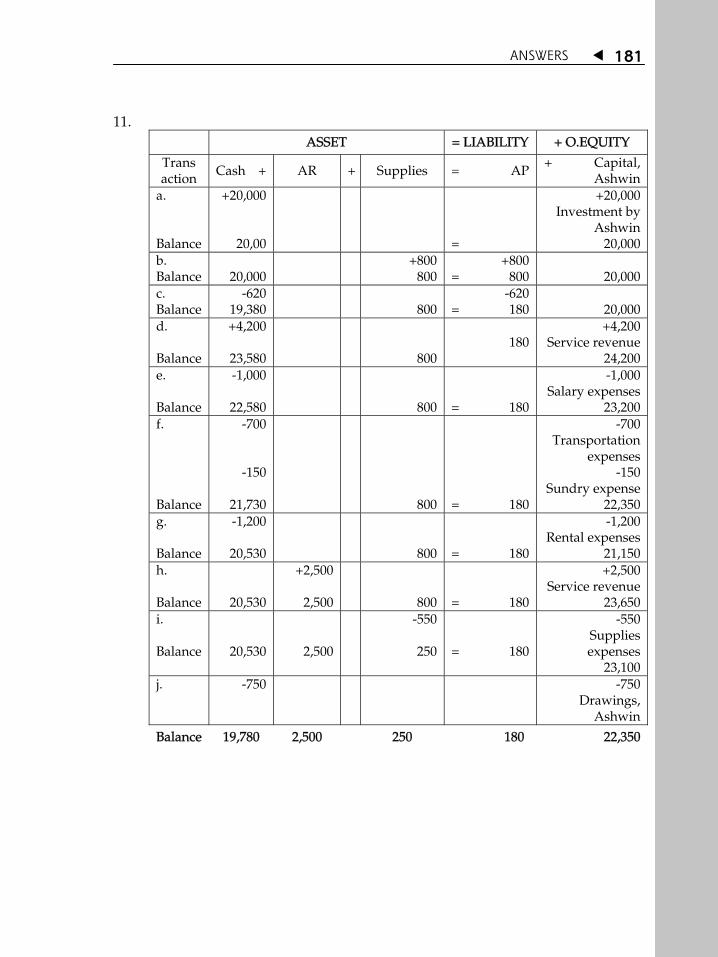

11. Mr. Ashwin established a tour agency on 1 June 2001. The transactions

for the month are as follows: (a) Deposited cash into the business account totalling RM20,000. (b) Purchased supplies on credit for RM800. (c) Made payment to supplier for RM620. (d) Received cash on the services provided for RM4,200. (e) Paid staff salary of RM1,000. (f) Paid transportation of RM700 and sundry expenses of RM150. (g) Paid office rental of RM1,200. (h) Charged customer RM2,500 for services provided. (i) Supplies unused at the end of the period is valued at RM250. (j) Mr. Ashwin took cash from the business totalling RM750 for his

personal use.

TOPIC 1 ACCOUNTING ENVIRONMENT

32

Required: (a) State the effect of each transaction and the balance after each

transaction using the accounting equation format that you have learned.

(b) Create the accounting equation for Mr. Ashwin business after the last transaction for that month.

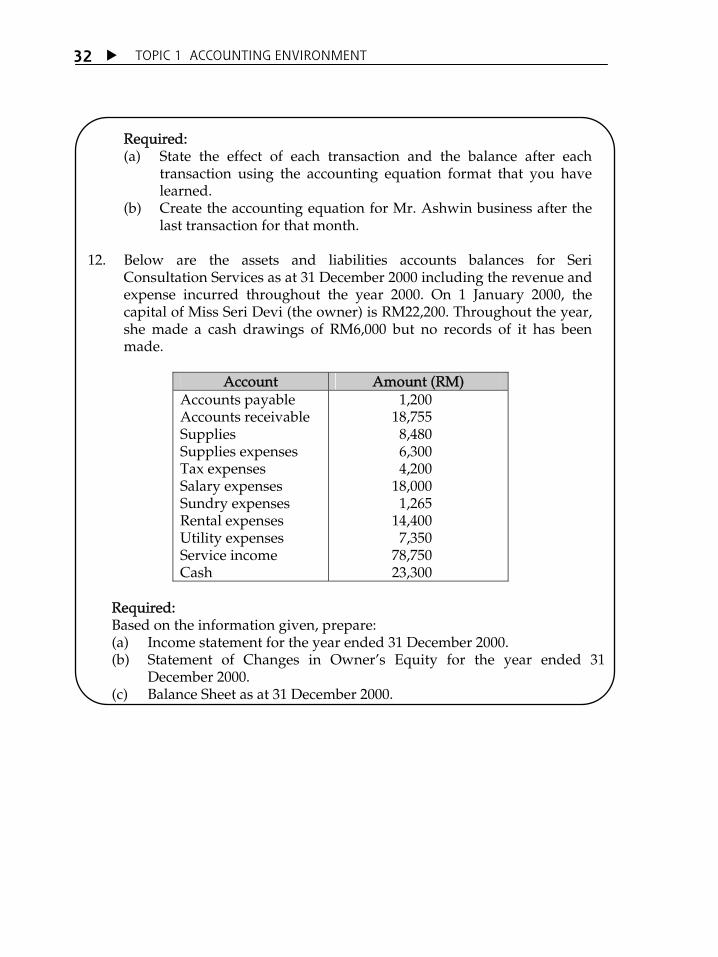

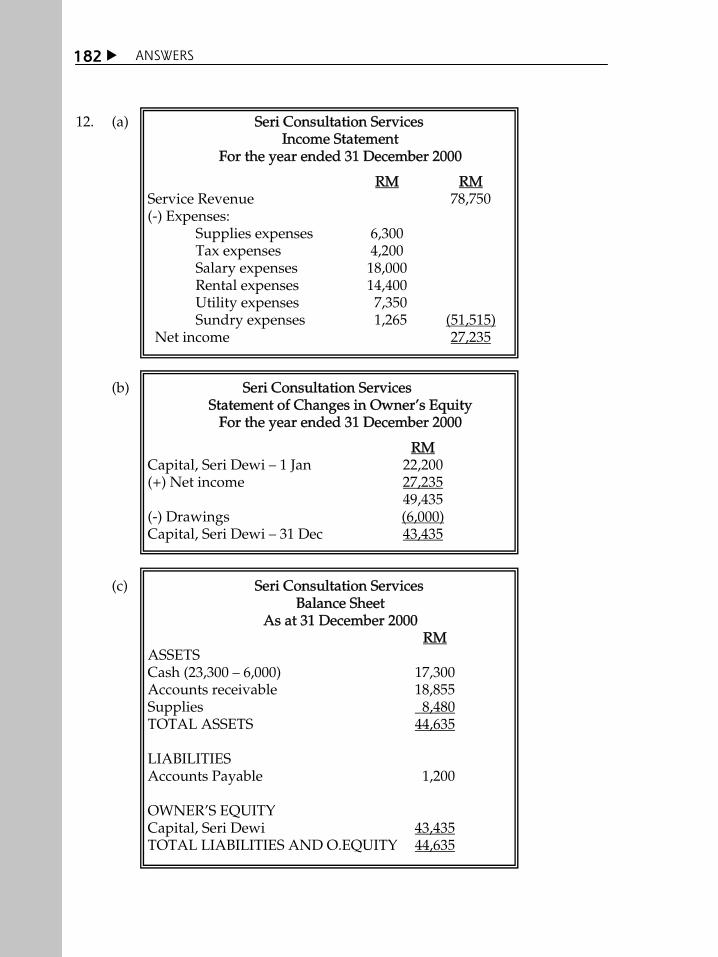

12. Below are the assets and liabilities accounts balances for Seri

Consultation Services as at 31 December 2000 including the revenue and expense incurred throughout the year 2000. On 1 January 2000, the capital of Miss Seri Devi (the owner) is RM22,200. Throughout the year, she made a cash drawings of RM6,000 but no records of it has been made.

Account Amount (RM)

Accounts payable Accounts receivable Supplies Supplies expenses Tax expenses Salary expenses Sundry expenses Rental expenses Utility expenses Service income Cash

1,200 18,755

8,480 6,300 4,200

18,000 1,265

14,400 7,350

78,750 23,300

Required: Based on the information given, prepare:

(a) Income statement for the year ended 31 December 2000. (b) Statement of Changes in OwnerÊs Equity for the year ended 31

December 2000. (c) Balance Sheet as at 31 December 2000.

TOPIC 1 ACCOUNTING ENVIRONMENT 33

In this topic, you have learned and discovered: 1. The users of accounting information consist of internal users and external

users. 2. The difference between financial accounting and management accounting

are: Financial accounting prepares the financial report for external users

while management accounting prepares the monetary and non-financial information for internal users.

The financial reports in financial accounting is produced periodically and subject to specified format while the report for management accounting is produced according to specific needs and not subject to specified standards.

3. The professional bodies involved in the accounting profession are

Malaysian Institute of Accountants (MIA), The Malaysian Institute of Certified Public Accountants (MICPA), Malaysian Accounting Standards Board (MASB) and Financial Reporting Foundation (FRF).

4. The assumptions and fundamental principles of accounting consist of:

assumption of separate entity; assumption of going concern; assumption of monetary unit; assumption of accounting period; principle of historical cost; principle of income recognition; principle of matching; and principle of full disclosure.

5. The accounting equation is fundamental in accounting and it consists of

three components, namely asset, liability and ownerÊs equity. 6. Financial statement is the final product of the accounting process and it

consists of Income Statement, Statement of Changes in OwnerÊs Equity, Balance Sheet and Cash Flow Statement.

INTRODUCTION

After studying how to analyse transactions, we will now learn about recording. Recording is the most important step in accounting for a business entity. However, before recording, we must identify the event that had occurred. Only events that occur to the business entity will be recorded in the entityÊs book. Not all events are transactions, for example, recruitment of staff. Although it will affect the entity economically, this event is not considered a transaction.

TTooppiicc 22 Recording Process

LEARNING OUTCOMES At the end of this topic, you should be able to: 1. describe the chart of accounts for recording and summarise the effect

of transactions on financial statement; 2. explain the format of accounts used; 3. list the rule of debit and credit for each type of accounts; 4. prepare journal entries; 5. transfer entries to ledger; and 6. prepare trial balance.

TOPIC 2 RECORDING PROCESS 35

CHART OF ACCOUNTS

When we analysed the transactions in the example of Reen Cyber Service, we have recorded and summarised the transactions that occurred using the accounting equation format. Although this format is easy to understand, it will become difficult to use when there are a lot of transactions to be recorded daily. In the example, we have analysed 8 transactions in a period of one month. In an actual situation, a medium-sized service firm may have several transactions in a day. If we use that accounting equation format, we will need a huge amount of space. Whenever there is a new item, we must add it into the limited columns available. We need to reshuffle the whole original format to accommodate this change. This also applies if errors are detected. It would be difficult for us to make any alteration without re-arranging the whole original format. As a result, the accounting system was created to show the increase or decrease of each item in the financial statement separately. The separate recording of each item is known as account. As an example, cash account is a separate recording especially to show the increase or decrease in the cash item. This also applies to other items like account payable, service revenue and salary expense. The group of accounts in a business entity is known as ledger. The list of accounts in the ledger is known as a chart of accounts. Chart of accounts was created particularly to enable the users of financial statements to refer to specific accounts. Each account is given a special number as reference. These accounts are normally listed systematically in the financial statement. Normally in the chart of accounts, balance sheet items (asset, liability and ownerÊs equity) are put in front, followed by income statement items (revenue and expense). Figure 2.1 summarises the concept of ledger and chart of accounts.

2.1

Why must transactions be recorded in accounts and not some other format?

TOPIC 2 RECORDING PROCESS

36

Figure 2.1: Ledger and chart of accounts

Figure 2.1 explains the chart of accounts clearly. This chart will be used as an example in this topic. New accounts will be introduced in the following units when the entity increases its business scope. The chart is created by the entity itself. Therefore, the chart of accounts between one entity and another entity might be different. For Reen Cyber Service, its chart of accounts consists of only two digits. The first digit will show the type of account (example: 1 for asset account, 2 for liability account, 3 for ownerÊs equity account, 4 for revenue account and 5 for expense account). The second digit will show the account itself. For larger businesses, the chart might consist of three to four digits. If the entity has a branch at different location, the first digit might be used to show the branch location.

TOPIC 2 RECORDING PROCESS 37

Table 2.1: Chart of Accounts for Reen Cyber Service

Accounts in Balance Sheet Accounts in Income Statement

1 ASSETS 11 Cash 12 Account receivable 14 Supplies 15 Insurance prepayment 17 Land 18 Office equipment

4 REVENUE 41 Service revenue

2 LIABILITIES 21 Account payable 22 Notes Payable 23 Deferred Rental

3 OWNERÊS EQUITY 31 Capital, Reen 32 Drawings, Reen

5 EXPENSES 51 Salary expenses 52 Rental expenses 53 Utility expenses 54 Supplies expenses 55 Sundry expenses

FORMAT OF ACCOUNT

Each account has three sections: (a) Title or name of the account, which is the name of the items recorded in that

particular account. (b) Debit section on the left side. (c) Credit section on the right side. The debit and credit section are used to record either the increase or decrease in the specific account. However, do remember that, debit does not necessarily show an increase and that credit does not necessarily show a reduction. It depends on the type of account. This subject will be explained in detail later under the rule of debit and credit.

2.2

EXERCISE 2.1

Which of these events can be considered as a transaction and must be recorded? Please discuss. (a) The death of a branch manager. (b) The capital contribution of the owner into the business.

TOPIC 2 RECORDING PROCESS

38

Accounts are also known as T-accounts due to their shapes that look like the letter T.

Account Title

Debit (left)

Credit (right)

Figure 2.2: T-Account (simple format ) Each section of the T-account should have four columns in the debit section and four columns in the credit section. Debit Account Title Credit

Date Description Reference Amount Date Description Reference Amount

Figure 2.3: T-Account (detailed format ) There is another format of account known as the three column account. Although in fact there are actually six columns in this accountÊs format, the three columns refer to the debit, credit and balance columns. An advantage of this format is that it can show the latest account balance at any particular time.

Date Description Reference Debit Credit Balance

Figure 2.4: Three column account format

RULES OF DEBIT AND CREDIT

2.3

What will happen if the rule of debit and credit are not complied with while recording the business transaction?

TOPIC 2 RECORDING PROCESS 39

We have previously stated that asset, liability and ownerÊs equity are the three main components in the accounting equation. Other items that are involved include drawings, revenue and expense. Every transaction that occurs will involve debit and credit and every transaction will affect at least two accounts. For every transaction, the total debit must be equal to the total credit. This is the basis of the double entry system. This rule of debit and credit is important to ensure that we make accurate recording. Table 2.2 shows the rules of debit and credit for each type of accounts.

Table 2.2: Rules of Debit and Credit

Type of Account Increase Decrease Asset Debit Credit

Liability Credit Debit Capital Credit Debit

Drawings Debit Credit Revenue Credit Debit Expense Debit Credit

Do you understand the rules listed in Table 2.2? Table 2.2 shows that when the asset account increases, we will debit the said account. For example, when the entity receives cash, we will debit cash account. When the asset account decreases, we will credit the said account. For example, when the entity made cash payment, we will credit the entityÊs cash account. Referring to Table 2.2, we will discover that the nature of the asset account is opposite to that of the liability and ownerÊs equity accounts. To observe this more clearly, please refer back to the accounting equation we had learned:

The asset item is on the left side while the liability and ownerÊs equity are on the right side. Asset is the economic resources owned by the entity while liability and owner equity are parties claiming ownership on the asset. Therefore, asset is the opposite of liability and ownerÊs equity.

2.3.1 Normal Balance

Normal balance is included in the rule of debit and credit. This refers to the balance ordinarily shown in the account.

ASSET = LIABILITY + OWNERÊS EQUITY

TOPIC 2 RECORDING PROCESS

40

Let us take the asset account as an example. When asset increases, the account is debited. When asset decreases, the account is credited. Therefore, the normal balance for asset account is debit. This is because the reduction in asset normally would not exceed the increase that had occurred. As a simple example, if we have cash of RM1,000 in the bank, normally we cannot withdraw more than the said value. Table 2.3 shows the rules of debit and credit including the normal balances for each type of accounts.

Table 2.3: The Rules of Debit and Credit Including Normal Balances

Type of Account Increase Decrease Normal Balance Asset Debit Credit Debit

Liability Credit Debit Credit Capital Credit Debit Credit

Drawings Debit Credit Debit Revenue Credit Debit Credit Expense Debit Credit Debit

Note that the normal balance for each account is the same as the increase in the said account. The rule of normal balance is important as it may help you to identify errors. For example, if the land account has a credit balance, you might have made a mistake in recording. However, you must also remember that normal balance is the balance that is ordinarily shown. The cash account that normally has a debit balance can also have a credit balance. This occurs when a company has withdrawn more cash than what is available. This might occur if the company has an overdraft agreement with the bank. When an entity has an overdraft agreement with the bank, it will be allowed to withdraw more money than what it is available in its account. The amount that can be withdrawn is subject to agreement.

Identify the characteristics that allow an event to be viewed as a transaction and therefore must be recorded?

TOPIC 2 RECORDING PROCESS 41

STEPS IN RECORDING PROCESS

Once the entityÊs transactions are identified, they must be recorded according to the accounting procedure specified. Recording begins with journal entry, then post to ledger and finally preparation of trial balance. This process can be illustrated in Figure 2.5.

Figure 2.5: Steps in recording process

2.4.1 Journal

Journal is the first book to be used in the recording process. Recording in journals (journalising) is the first process of recording. Transactions are recorded chronologically in the journal before been transferred to ledger. There are two main types of journal, the general journal and special journal. (a) General Journal General journal is the journal normally owned by all entities. This journal

can be used to record all kinds of transaction like sales, purchases, cash receipts and cash payments.

(b) Special Journal Large businesses normally have many transactions. Special journals are

created to avoid confusion due to many entries made in the general journal. The type of special journal created depends on the needs of the entity.

For example, an entity that have numerous cash transactions might want to

create Cash Receipts Journal and Cash Payment Journal that will be specially used for cash transactions. All the other transactions can still be recorded in the General Journal. This segregation will simplify recording and control. Among the special journals that are commonly used are:

2.4

TOPIC 2 RECORDING PROCESS

42

(i) Purchase Journal: particularly for recording purchases of goods on credit.

(ii) Sales Journal: particularly for recording sales of goods on credit. (iii) Cash Receipt Journal: particularly for recording all cash received. (iv) Cash Payment Journal: particularly for recording all cash payment.

However, this course will only emphasise to the general journal. The format of general journal is shown in Figure 2.6.

Figure 2.6: Format of general journal

It is important to ensure that journalising is done correctly. This is because these information will be transferred to ledger for the purpose of preparing the financial statement. Errors made in the journal will result in errors in the financial statement. The name of accounts used must be specified in the beginning and used consistently in order to avoid confusion.

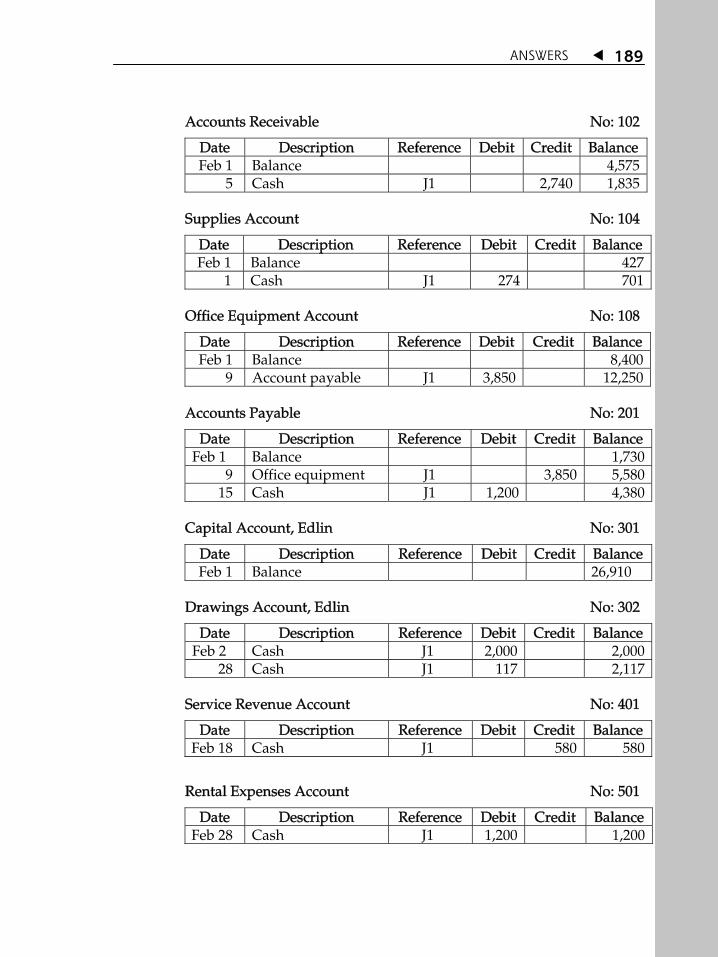

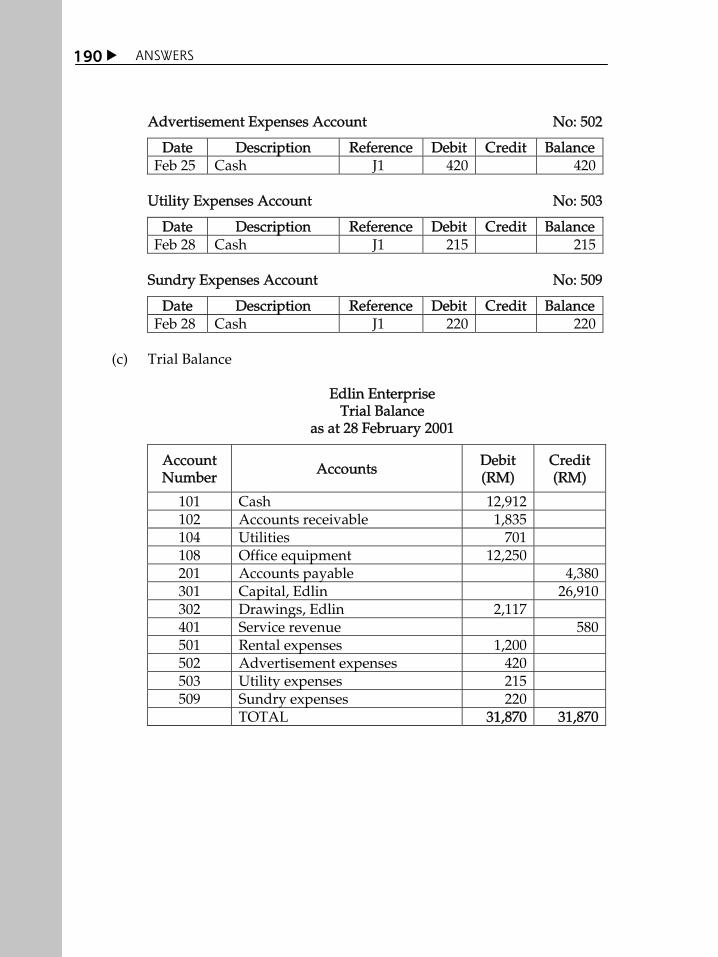

2.4.2 Journalising and Posting of Entry

After the transactions have been recorded in the journal, it will be posted to the ledger. This process is known as transfer of entry or posting. We will now record the transactions of Reen Cyber Service in the General Journal and then post them to the ledger using the T-account format.

In your opinion, what are the appropriate journals for a book shop in a school? Please discuss.

TOPIC 2 RECORDING PROCESS 43

Transaction 1: On I November, Reen invested RM30,000 as capital for Reen Cyber Service business. From our analysis in Topic 1, we know that this transaction will increase the cash and ownerÊs equity by RM30,000. According to the rules of debit and credit, the increase in asset account (cash) will be debited and increase in ownerÊs equity account (capital) will be credited. When recording, note that the name of the account to be debited is listed first, followed by the name of account to be credited. The name of the credited account will be aligned slightly to the right to differentiate it from the account to be debited. Journal entry: General Journal pg 1

Date Description Reference Debit Credit

Nov 1 Cash 30,000

Capital, Reen 30,000

(Cash invested by Reen)

Journal 1: General Journal for Transaction 1 Post to ledger:

Cash

Nov 1 Capital, Reen 30,000

Capital, Reen

Nov 1 Cash 30,000

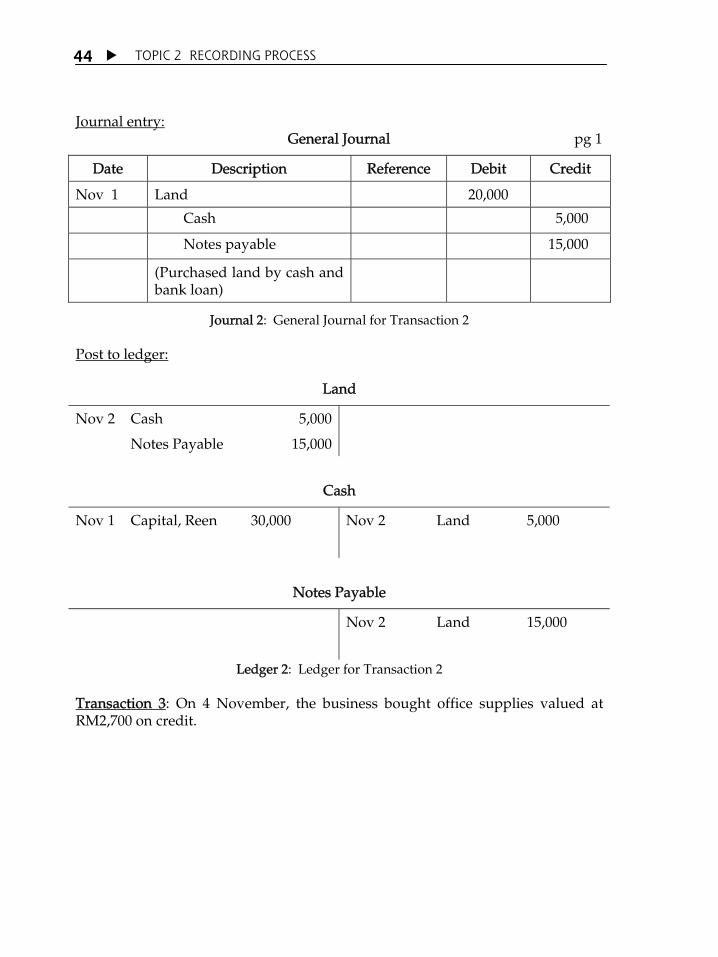

Ledger 1: Ledger for Transaction 1 Transaction 2: On 2 November, the business purchased a piece of land valued at RM20,000. A total of RM5,000 cash had been paid while the balance is financed by bank loan (notes payable). Note that even though this transaction involves more than two accounts, the total amount of debit is still equal to the total amount of credit.

TOPIC 2 RECORDING PROCESS

44

Journal entry: General Journal pg 1

Date Description Reference Debit Credit

Nov 1 Land 20,000

Cash 5,000

Notes payable 15,000

(Purchased land by cash and bank loan)

Journal 2: General Journal for Transaction 2 Post to ledger:

Land

Nov 2 Cash 5,000

Notes Payable 15,000

Cash

Nov 1 Capital, Reen 30,000 Nov 2 Land 5,000

Notes Payable

Nov 2 Land 15,000

Ledger 2: Ledger for Transaction 2

Transaction 3: On 4 November, the business bought office supplies valued at RM2,700 on credit.

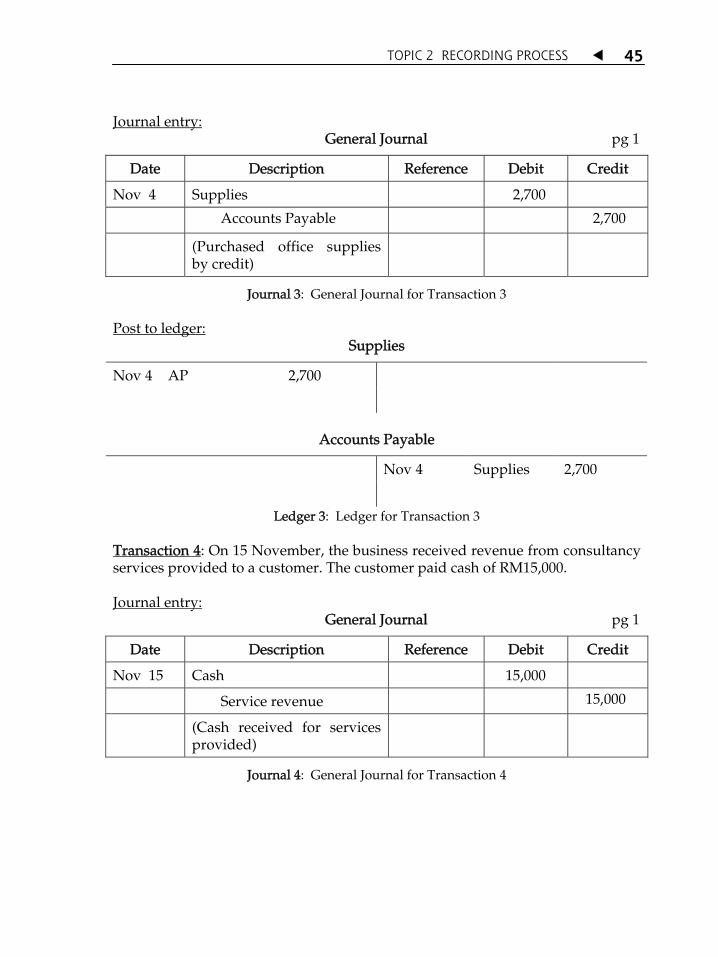

TOPIC 2 RECORDING PROCESS 45

Journal entry: General Journal pg 1

Date Description Reference Debit Credit

Nov 4 Supplies 2,700

Accounts Payable 2,700

(Purchased office supplies by credit)

Journal 3: General Journal for Transaction 3 Post to ledger:

Supplies

Nov 4 AP 2,700

Accounts Payable

Nov 4 Supplies 2,700

Ledger 3: Ledger for Transaction 3

Transaction 4: On 15 November, the business received revenue from consultancy services provided to a customer. The customer paid cash of RM15,000. Journal entry: General Journal pg 1

Date Description Reference Debit Credit

Nov 15 Cash 15,000

Service revenue 15,000

(Cash received for services provided)

Journal 4: General Journal for Transaction 4

TOPIC 2 RECORDING PROCESS

46

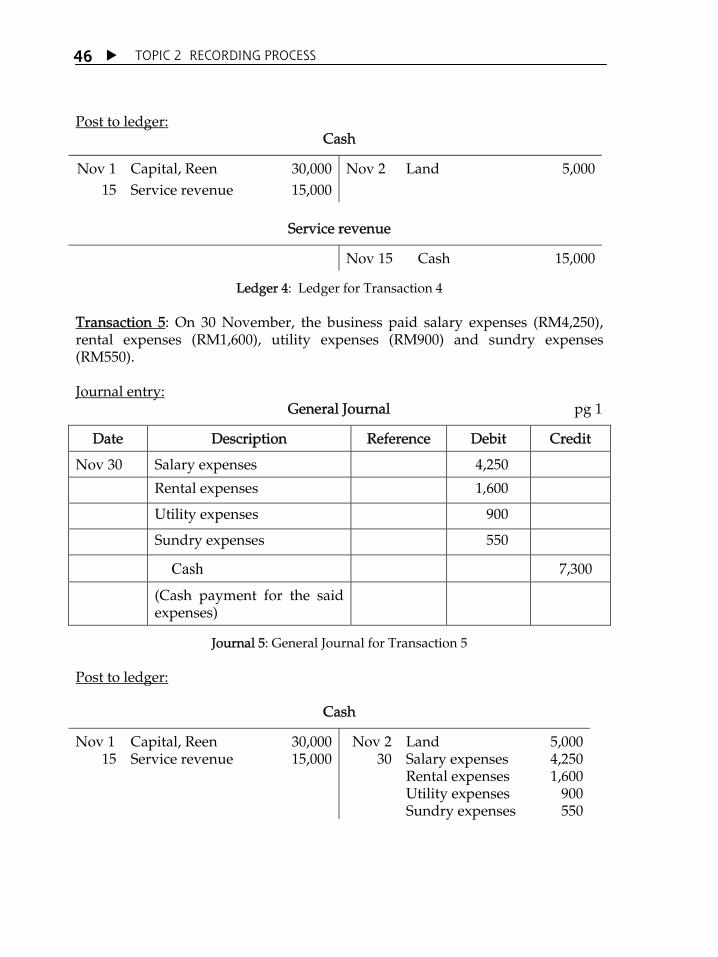

Post to ledger: Cash

Nov 1 15

Capital, Reen Service revenue

30,00015,000

Nov 2 Land 5,000

Service revenue

Nov 15 Cash 15,000

Ledger 4: Ledger for Transaction 4 Transaction 5: On 30 November, the business paid salary expenses (RM4,250), rental expenses (RM1,600), utility expenses (RM900) and sundry expenses (RM550). Journal entry: General Journal pg 1

Date Description Reference Debit Credit

Nov 30 Salary expenses 4,250

Rental expenses 1,600

Utility expenses 900