bpn 2013 retail trends

TRANSCRIPT

2013 retailtrends

TECTONIC SHIFT: Forget consumers. Forget customers. Today it’s about the shopper.

C2C: Consumers aren’t just talking to each other, they are selling, trading, advising one another

INCONSPICUOUS CONSUMPTION: Increasingly retailers and shoppers are finding ways to lighten the load

MAN-SUMERISM: The rise of male shopping behavior

Tec-tonic Shift

two states: using & deciding

What drives shoppers to say “yes”?

DECIDING:USING:

rise of shopper marketing

$50BAND GROWING

ANNUAL SHOPPER MARKETING

source: GMA/Booz

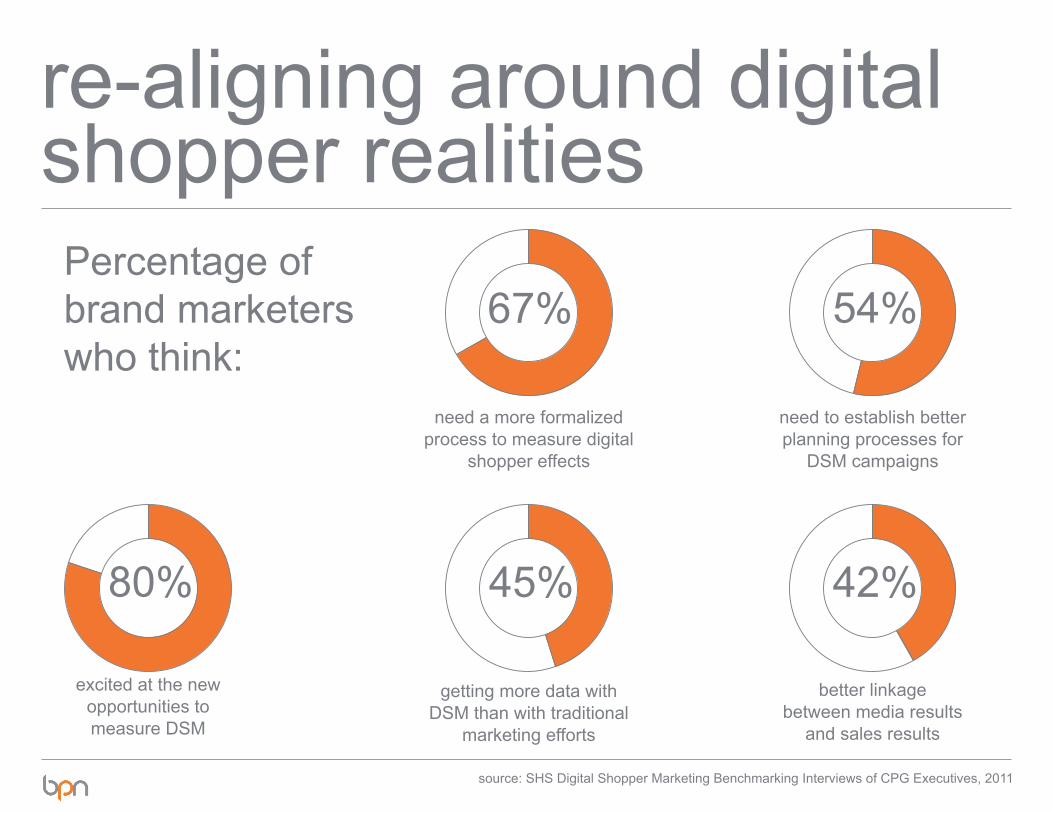

re-aligning around digital shopper realities

Percentage of brand marketers who think:

need a more formalized process to measure digital

shopper effects

getting more data with DSM than with traditional

marketing efforts

need to establish better planning processes for

DSM campaigns

better linkage between media results

and sales results

excited at the new opportunities to measure DSM

45%80%

67% 54%

42%

source: SHS Digital Shopper Marketing Benchmarking Interviews of CPG Executives, 2011

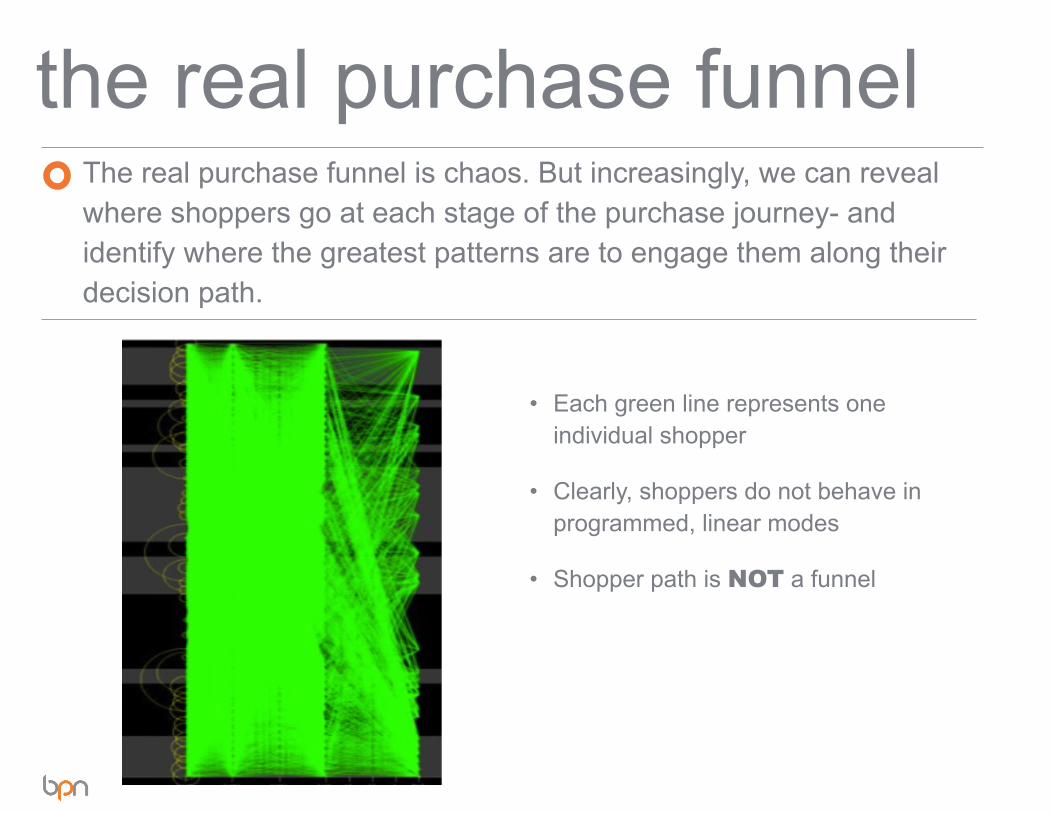

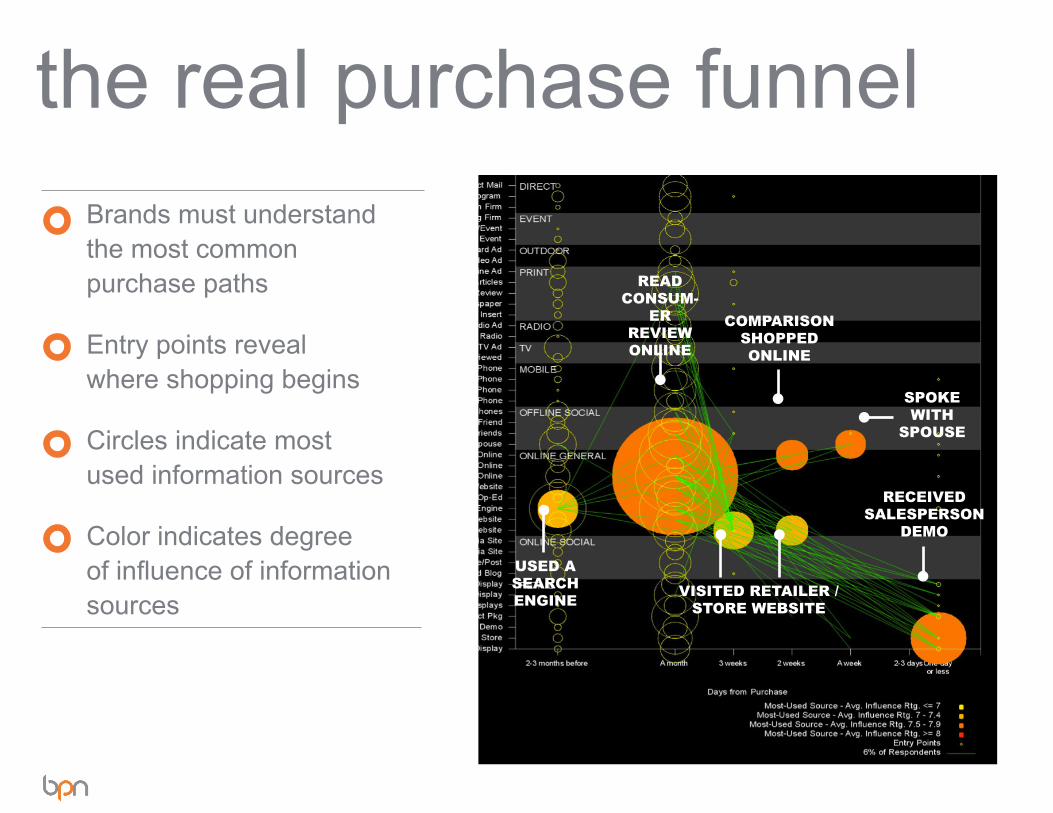

the real purchase funnelThe real purchase funnel is chaos. But increasingly, we can reveal where shoppers go at each stage of the purchase journey- and identify where the greatest patterns are to engage them along their decision path.

• Each green line represents one individual shopper

• Clearly, shoppers do not behave in programmed, linear modes

• Shopper path is NOT a funnel

the real purchase funnelBrands must understand the most common purchase paths

Entry points reveal where shopping begins

Circles indicate most used information sources

Color indicates degree of influence of information sources

USED A SEARCH ENGINE VISITED RETAILER /

STORE WEBSITE

COMPARISON SHOPPED ONLINE

SPOKE WITH

SPOUSE

RECEIVED SALESPERSON

DEMO

READ CONSUM-

ER REVIEW ONLINE

C2C

the ecology of shopper dialogueSocial media has re-written the rules of trade, opening up a world where shoppers can buy, sell, and trade... to each other.

B2B & B2C,meet C2CB2B & B2C,meet C2C

smart shopper platforms Access to information is making shoppers smart – really smart. Knowldege sharing sites are increasing in sophistication and number. Forget Google or Wikipedia- these sites are the future of decision making, accessible by shoppers at every step of the purchase journey.

Here, Decide.com tells shoppers if they should

purchase or wait for prices to drop.

Fooducate rates food products based on nutritioinal and expert information.

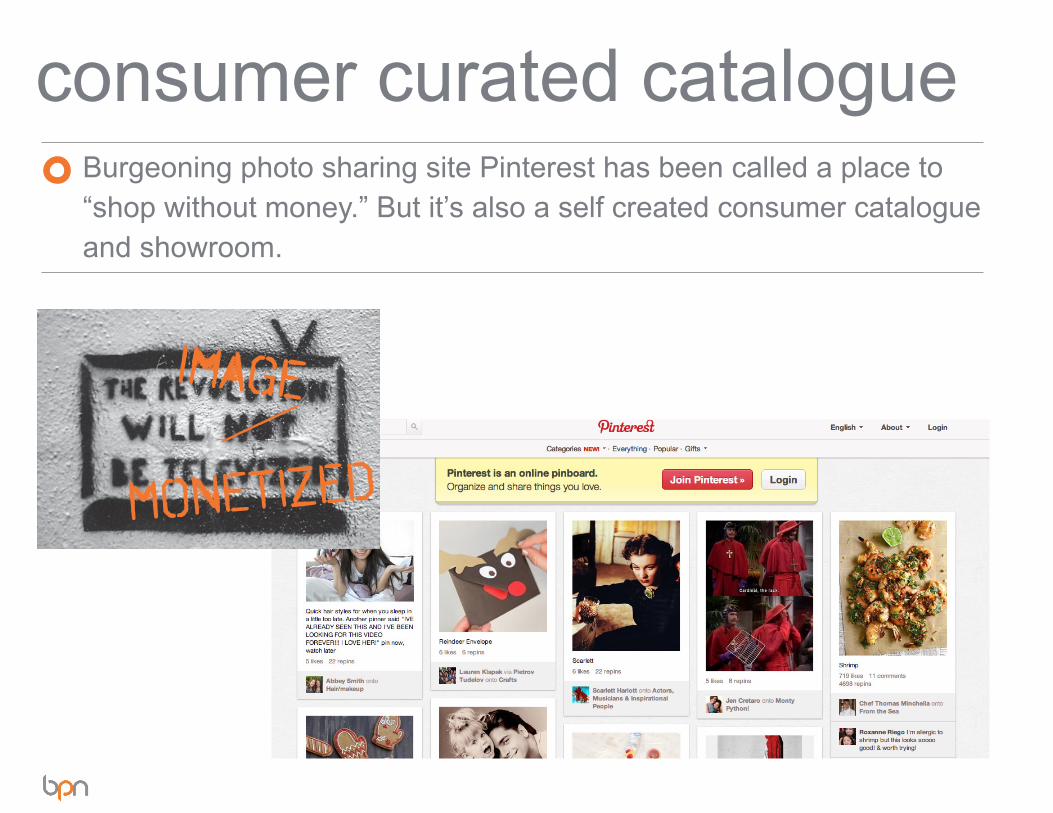

consumer curated catalogueBurgeoning photo sharing site Pinterest has been called a place to “shop without money.” But it’s also a self created consumer catalogue and showroom.

next gen marketplaceOnline craft site, Etsy has provided artists and craftmakers with a thriving marketplace to sell their goods. Smart retailers like WestElm are inking deals to bring online shoppers to their stores by featuring and selling Etsy artist goods.

Etsy is the 58th most popular website in the USA

source: appapeal.com

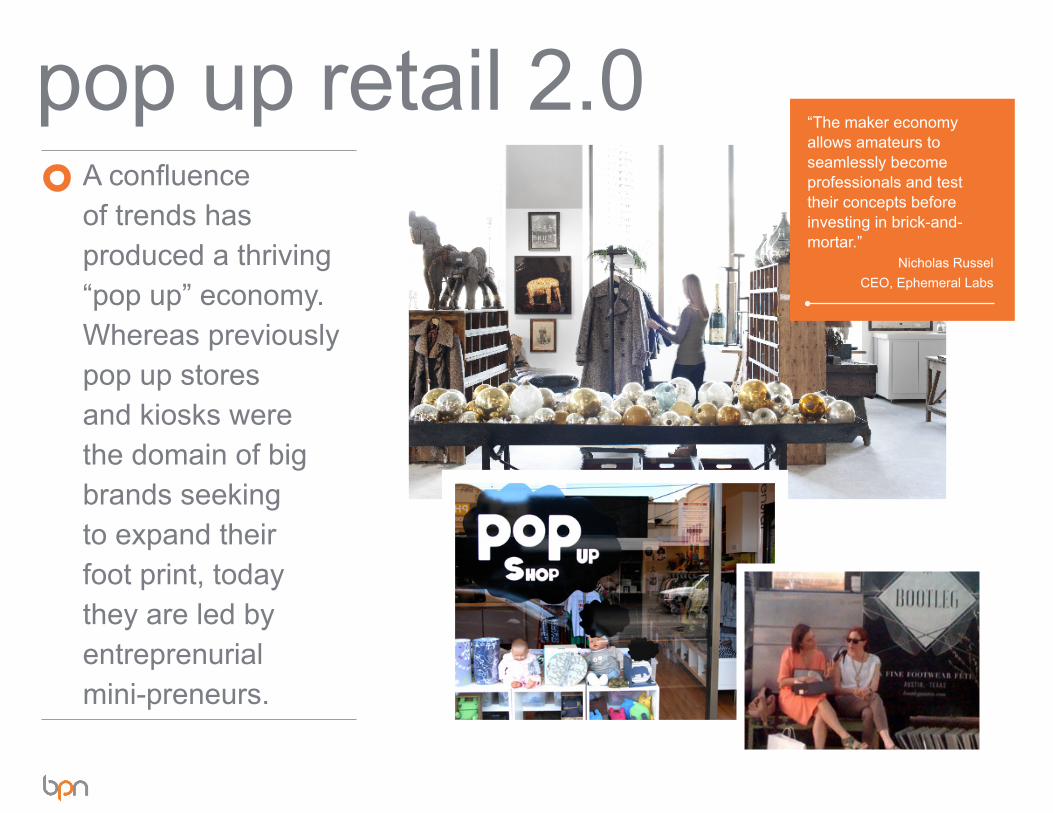

pop up retail 2.0A confluence of trends has produced a thriving “pop up” economy. Whereas previously pop up stores and kiosks were the domain of big brands seeking to expand their foot print, today they are led by entreprenurial mini-preneurs.

“The maker economy allows amateurs to seamlessly become professionals and test their concepts before investing in brick-and-mortar.”

Nicholas Russel CEO, Ephemeral Labs

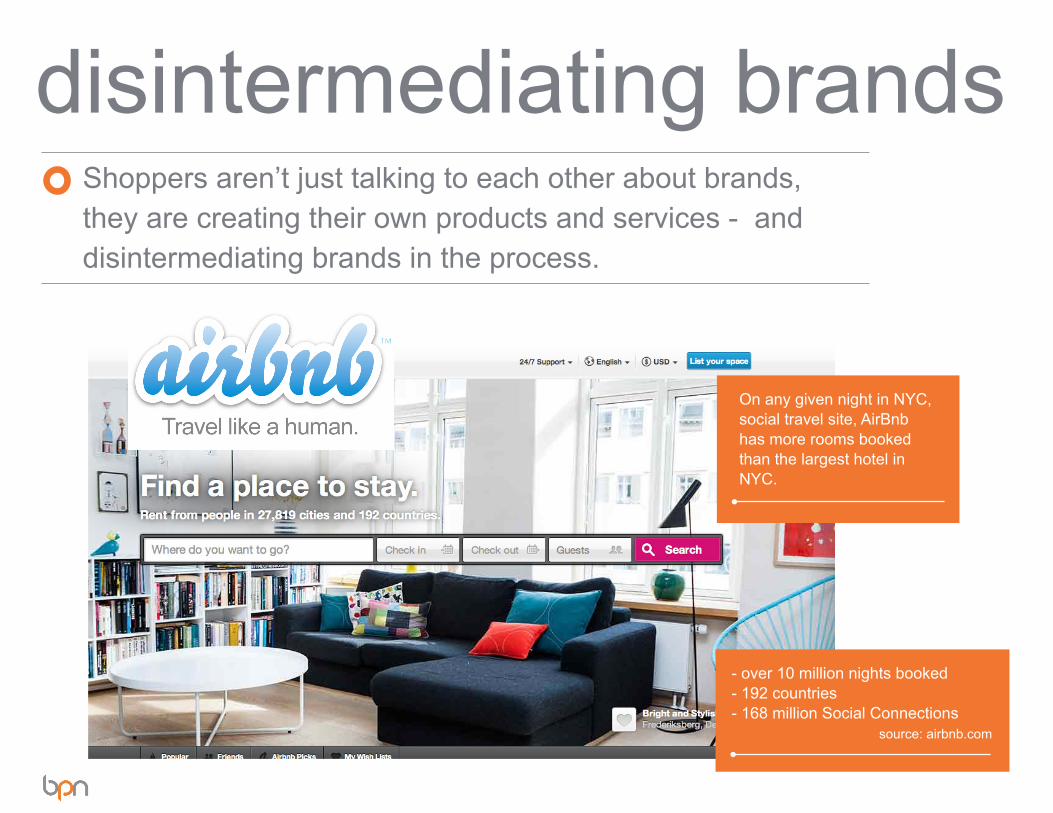

disintermediating brands Shoppers aren’t just talking to each other about brands, they are creating their own products and services - and disintermediating brands in the process.

On any given night in NYC, social travel site, AirBnb has more rooms booked than the largest hotel in NYC.

- over 10 million nights booked- 192 countries- 168 million Social Connections

source: airbnb.com

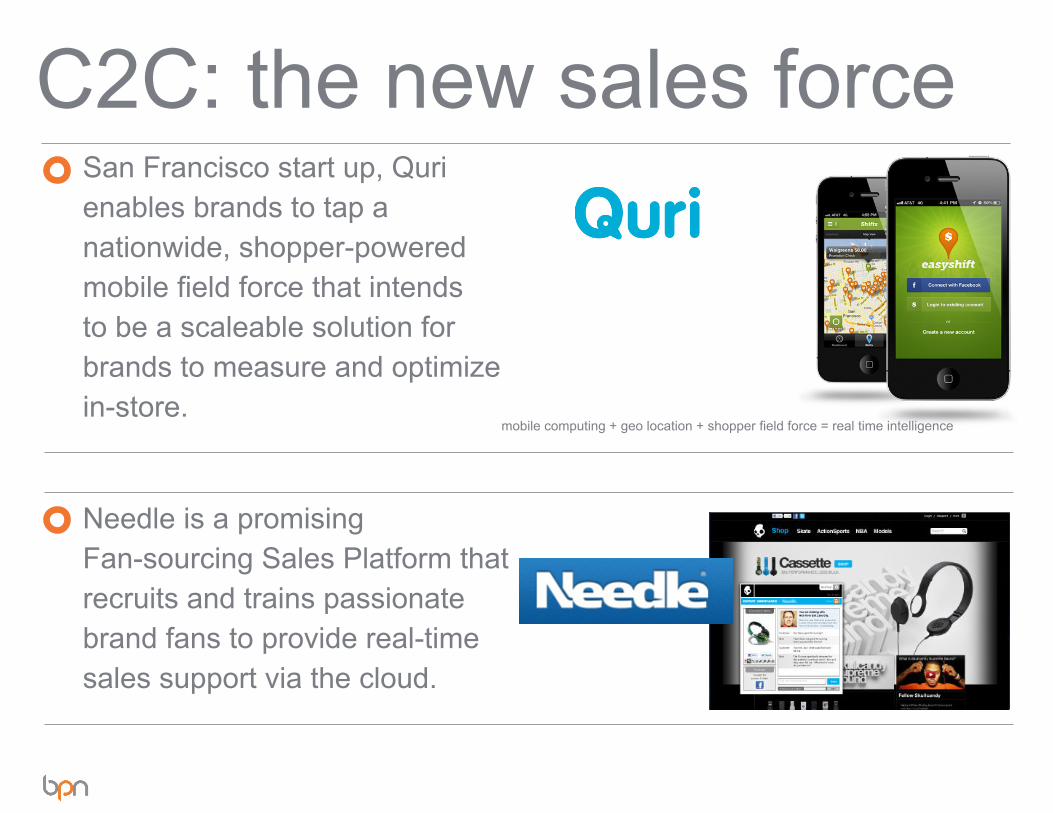

C2C: the new sales forceSan Francisco start up, Quri enables brands to tap a nationwide, shopper-powered mobile field force that intends to be a scaleable solution for brands to measure and optimize in-store.

Needle is a promising Fan-sourcing Sales Platform that recruits and trains passionate brand fans to provide real-time sales support via the cloud.

mobile computing + geo location + shopper field force = real time intelligence

Inconspicuous Consumption

loyalty, brand equity, “keeping up with the joneses”...

What do they all have in common? They are all casualties of the recession and the need for people to re-evaluate what matters most. Inconspicuous consumption, where maximizing resources is a primary driver of purchase decisions, is the reality.

average monthly spend on

groceries up $27 from 2007 to

2011.

two in five shoppers

purchasing more store brand or generic items

three in 10 respondents cut back on bakery items, candy, desserts and

magazines/books/DVDs

one in four have cut back on

prime cuts of meat/seafood

$27source: MaxPoint Interactive, conducted by 3IGInsight

eco packaging Reinforce differentiators. In unexpected places. Ketchup is ketchup… and a way to conserve resources.

Puma’s sustainable shoe box and reusable bag looks cool and saves: - 8,500 tons less paper - 20 million Megajoules of electricity - 1 million litres less of fuel oil used and 1 million litres of water - 275 tons of plastic

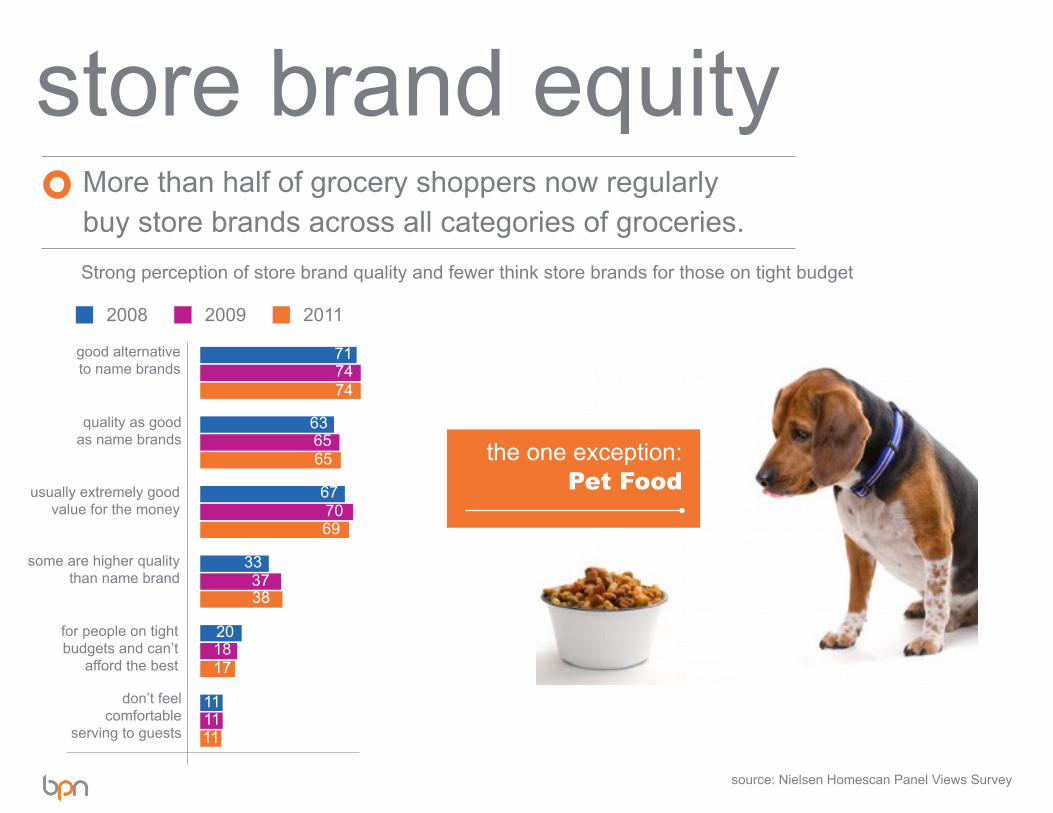

store brand equityMore than half of grocery shoppers now regularly buy store brands across all categories of groceries.

the one exception:Pet Food

Strong perception of store brand quality and fewer think store brands for those on tight budget

good alternative to name brands

2008 2009

quality as good as name brands

usually extremely good value for the money

some are higher quality than name brand

for people on tight budgets and can’t

afford the best

don’t feel comfortable

serving to guests

333738

201817

111111

2011

717474

636565

677069

source: Nielsen Homescan Panel Views Survey

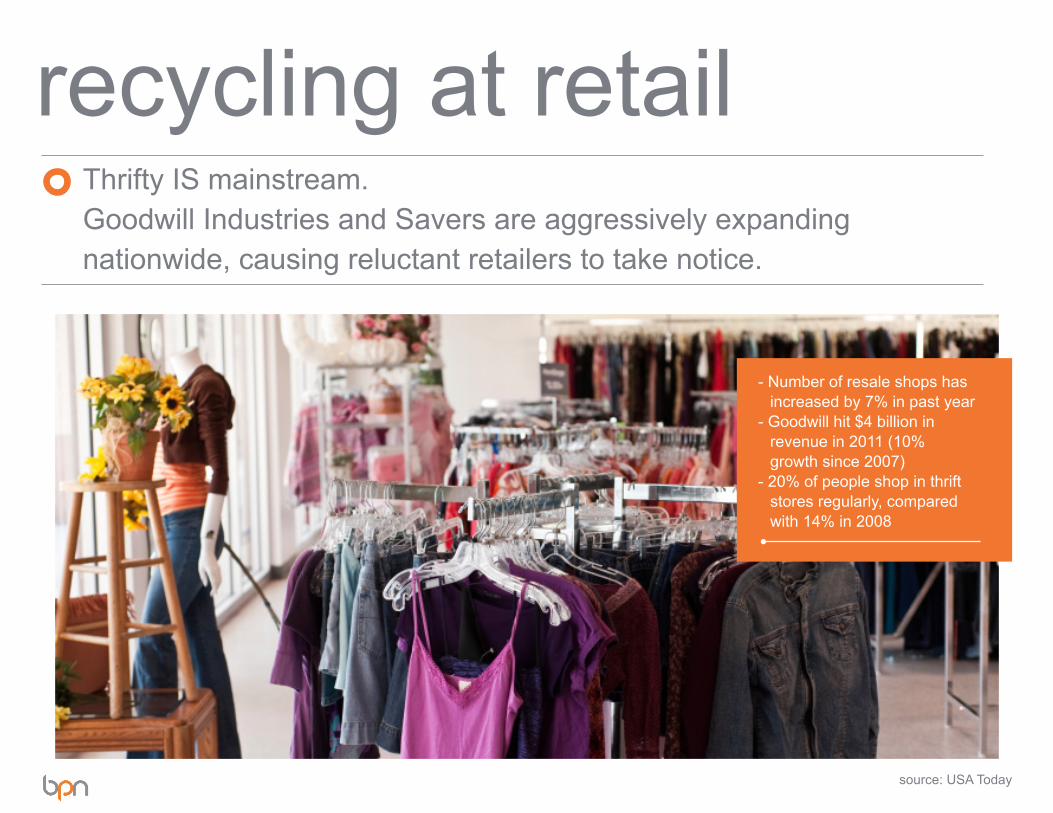

recycling at retailThrifty IS mainstream. Goodwill Industries and Savers are aggressively expanding nationwide, causing reluctant retailers to take notice.

- Number of resale shops has increased by 7% in past year

- Goodwill hit $4 billion in revenue in 2011 (10% growth since 2007)

- 20% of people shop in thrift stores regularly, compared with 14% in 2008

source: USA Today

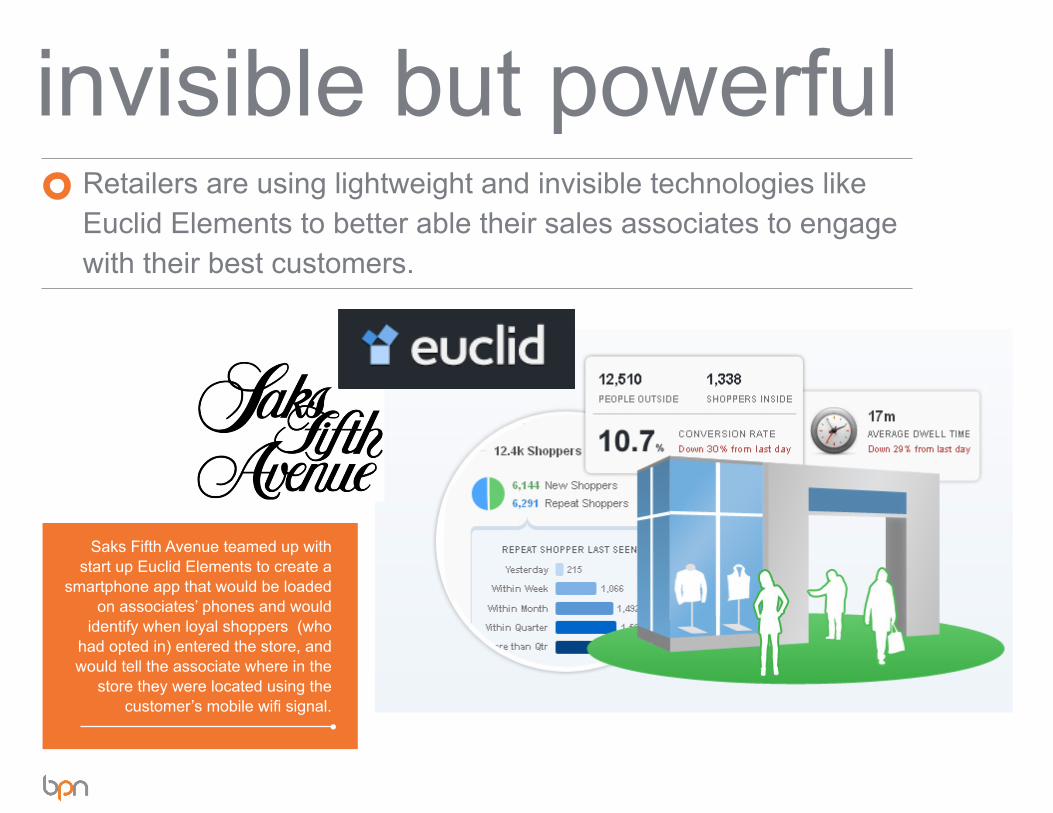

invisible but powerfulRetailers are using lightweight and invisible technologies like Euclid Elements to better able their sales associates to engage with their best customers.

Saks Fifth Avenue teamed up with start up Euclid Elements to create a

smartphone app that would be loaded on associates’ phones and would

identify when loyal shoppers (who had opted in) entered the store, and would tell the associate where in the

store they were located using the customer’s mobile wifi signal.

loyalty is not a free t-shirtShoppers want more than just free ‘stuff.’ Savvy retailers and brands are shifting from extrinsic to intrinsic rewards - rewarding all shopper interaction, instead of just purchase.

Most loyalty members are unsatisfied with the value of loyalty programs (grocery/drug most satisfied at only 42%).

18average number of loyalty programs per US household: less than half are active:

source: Colloquy: The Art and Science of Building Customer Value, April 2011

PROGRAM OPT-IN

RECOGNITION/FAME

SOCIAL CURRENCY

A VOICE IN BRAND DECISIONS

VIRTUAL GOODS

EXCLUSIVE ACCESS

THE NEW LOYALTY:

8

Man- sumerism

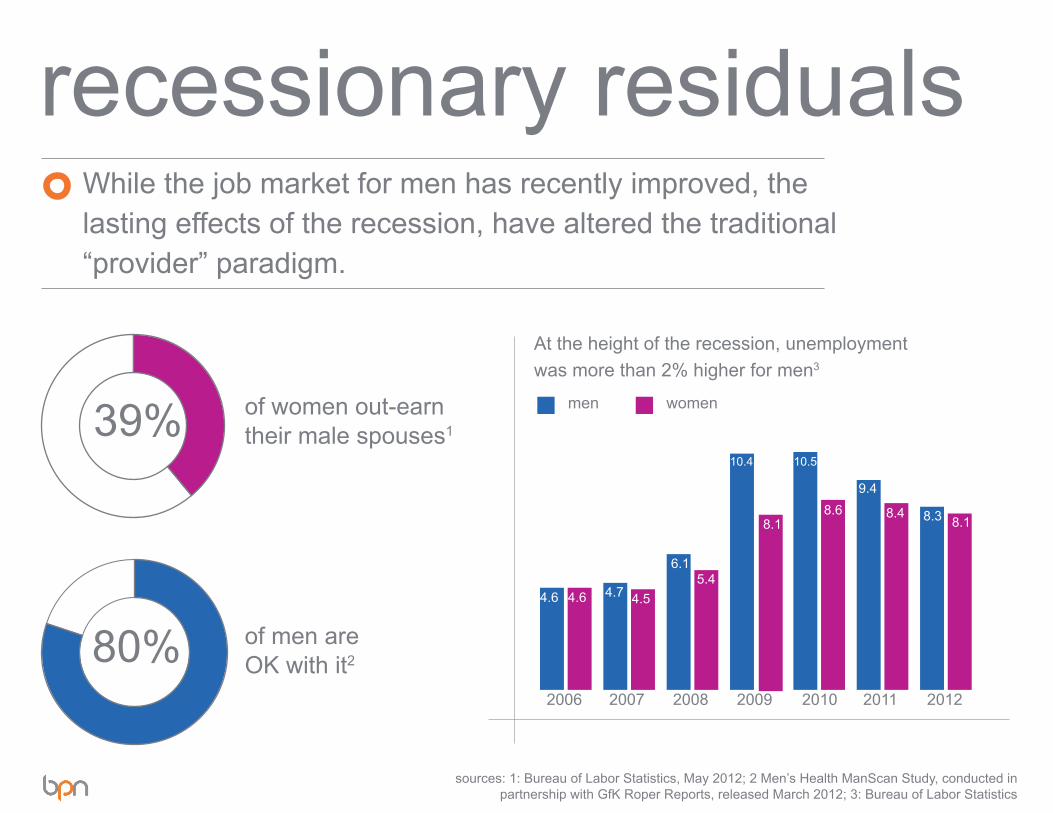

of women out-earn their male spouses1

of men are OK with it280%

At the height of the recession, unemployment was more than 2% higher for men3

men

recessionary residuals

39%

While the job market for men has recently improved, the lasting effects of the recession, have altered the traditional “provider” paradigm.

2006

4.6

2007 2008 2009 2010 2011 2012

4.6 4.7 4.5

6.15.4

10.4 10.5

8.69.4

8.4 8.3 8.18.1

women

sources: 1: Bureau of Labor Statistics, May 2012; 2 Men’s Health ManScan Study, conducted in partnership with GfK Roper Reports, released March 2012; 3: Bureau of Labor Statistics

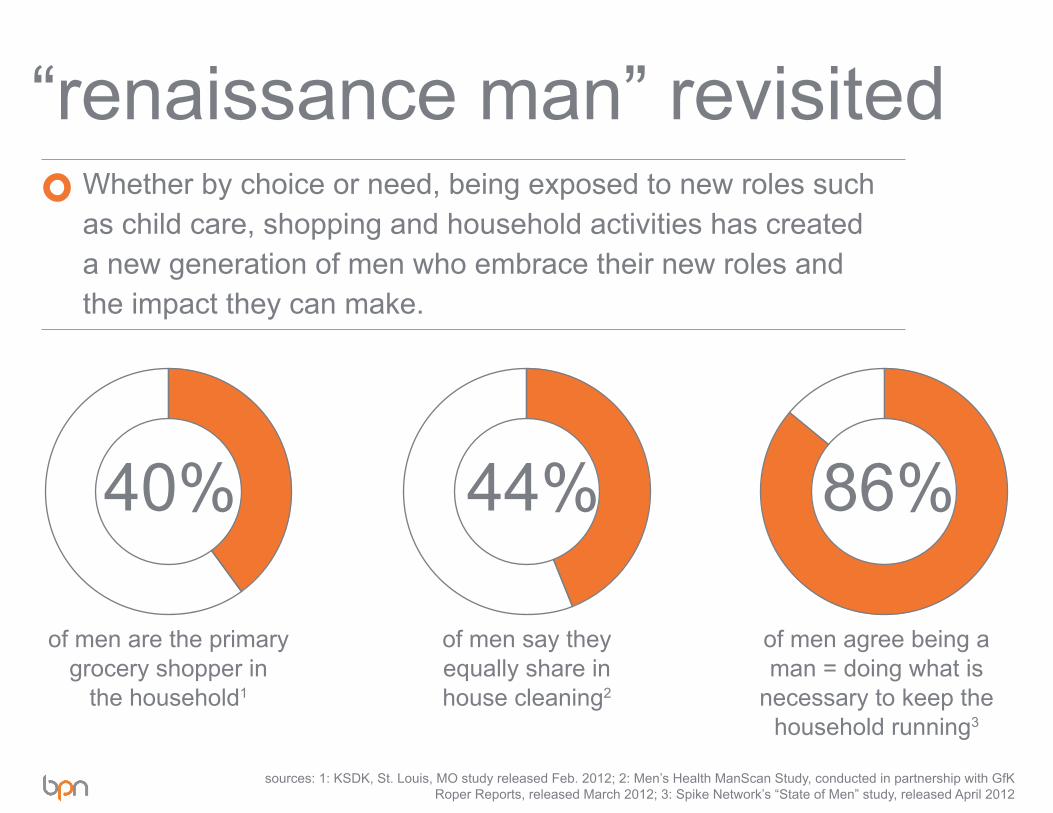

of men are the primary grocery shopper in

the household1

of men say they equally share in house cleaning2

of men agree being a man = doing what is

necessary to keep the household running3

“renaissance man” revisitedWhether by choice or need, being exposed to new roles such as child care, shopping and household activities has created a new generation of men who embrace their new roles and the impact they can make.

40% 44% 86%

sources: 1: KSDK, St. Louis, MO study released Feb. 2012; 2: Men’s Health ManScan Study, conducted in partnership with GfK Roper Reports, released March 2012; 3: Spike Network’s “State of Men” study, released April 2012

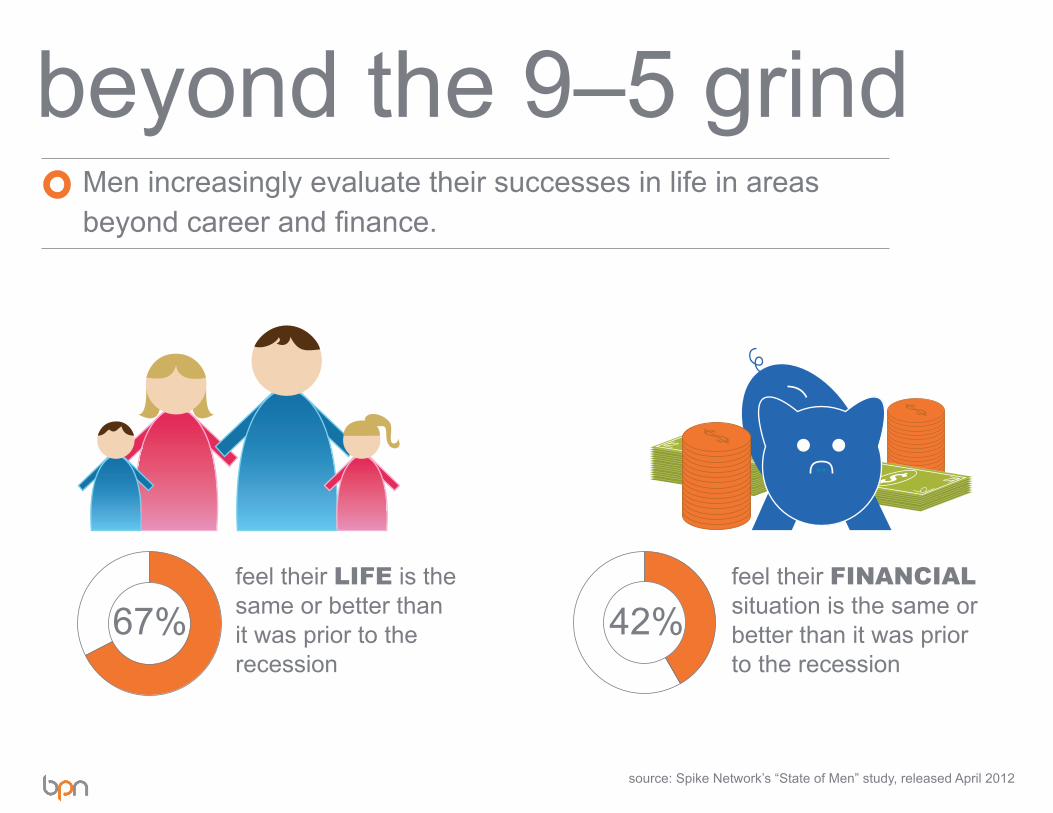

feel their LIFE is the same or better than it was prior to the recession

feel their FINANCIAL situation is the same or better than it was prior to the recession

beyond the 9–5 grindMen increasingly evaluate their successes in life in areas beyond career and finance.

67% 42%

source: Spike Network’s “State of Men” study, released April 2012

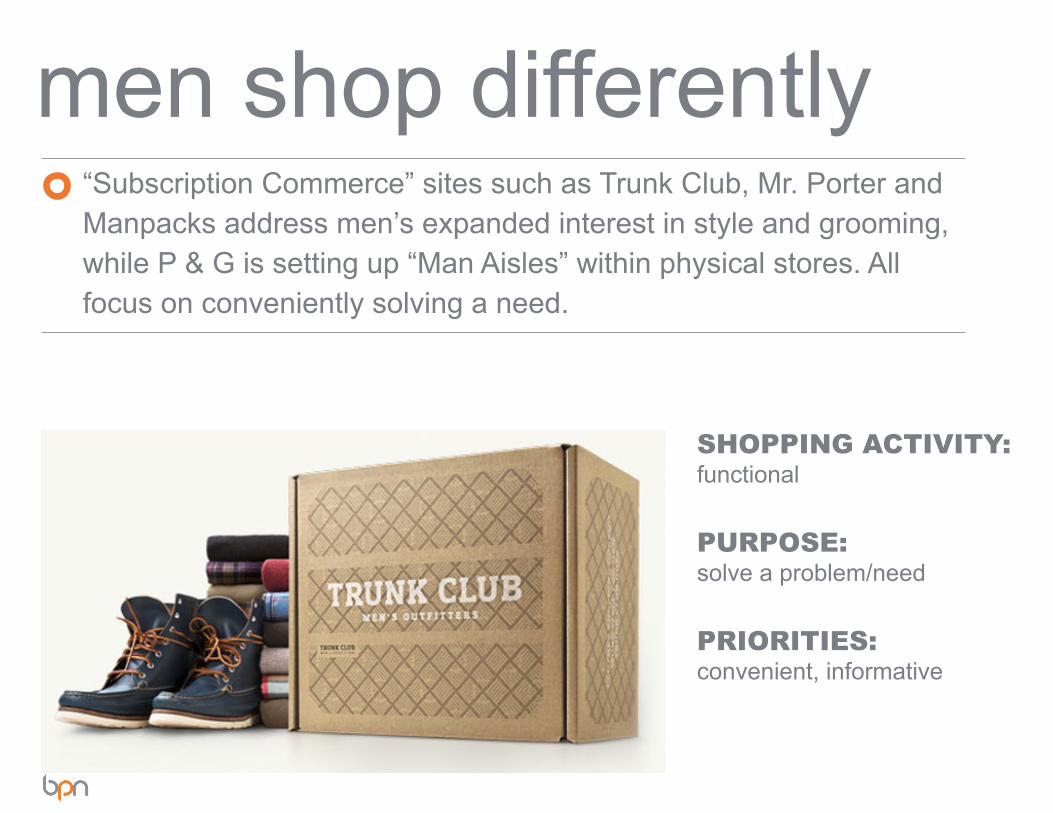

men shop differently “Subscription Commerce” sites such as Trunk Club, Mr. Porter and Manpacks address men’s expanded interest in style and grooming, while P & G is setting up “Man Aisles” within physical stores. All focus on conveniently solving a need.

SHOPPING ACTIVITY: functional

PURPOSE: solve a problem/need

PRIORITIES: convenient, informative

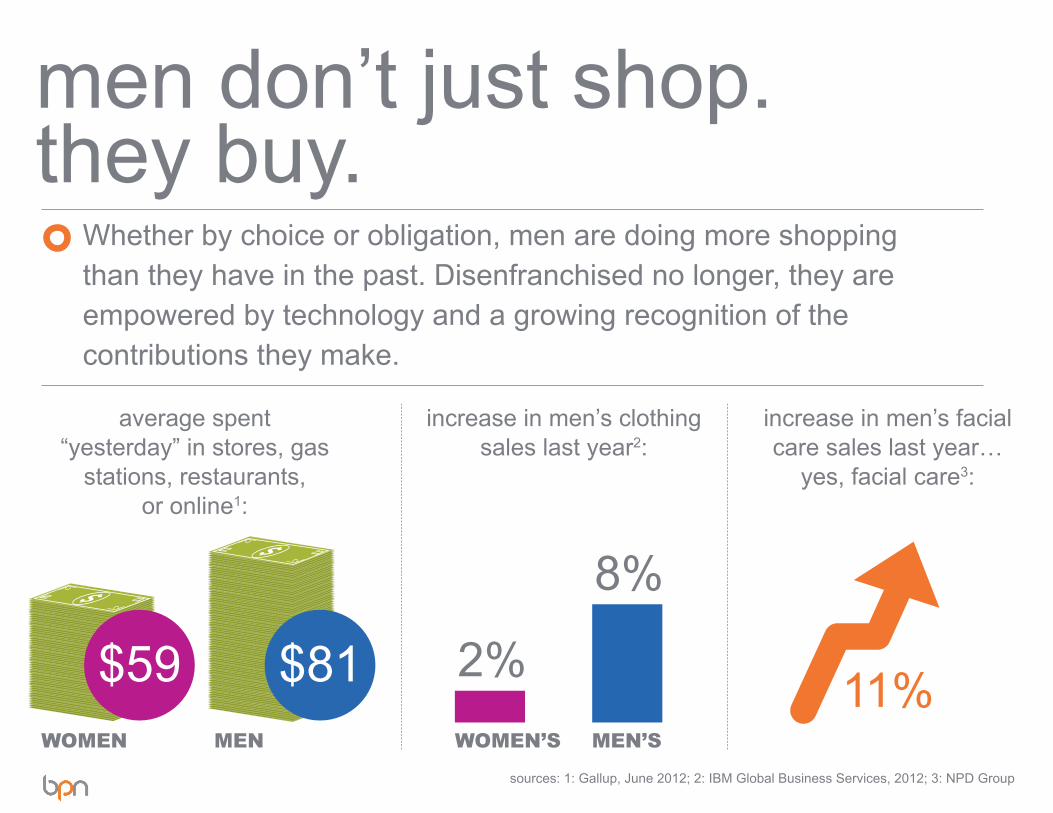

men don’t just shop. they buy.

Whether by choice or obligation, men are doing more shopping than they have in the past. Disenfranchised no longer, they are empowered by technology and a growing recognition of the contributions they make.

average spent “yesterday” in stores, gas

stations, restaurants, or online1:

increase in men’s clothing sales last year2:

increase in men’s facial care sales last year…

yes, facial care3:

$81$59

8%

2% 11%MENWOMEN MEN’SWOMEN’S

sources: 1: Gallup, June 2012; 2: IBM Global Business Services, 2012; 3: NPD Group

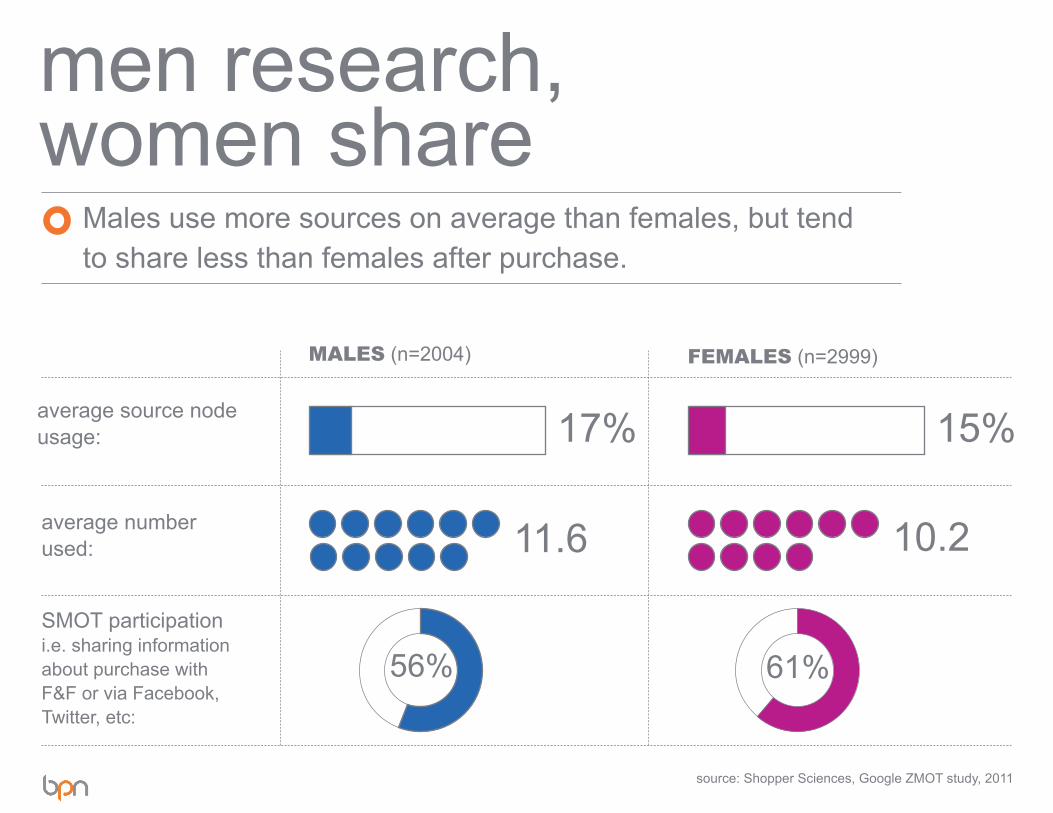

men research, women share

Males use more sources on average than females, but tend to share less than females after purchase.

average source node usage:

MALES (n=2004) FEMALES (n=2999)

average number used:

SMOT participation i.e. sharing information about purchase with F&F or via Facebook, Twitter, etc:

source: Shopper Sciences, Google ZMOT study, 2011

17%

11.6

56% 61%

10.2

15%

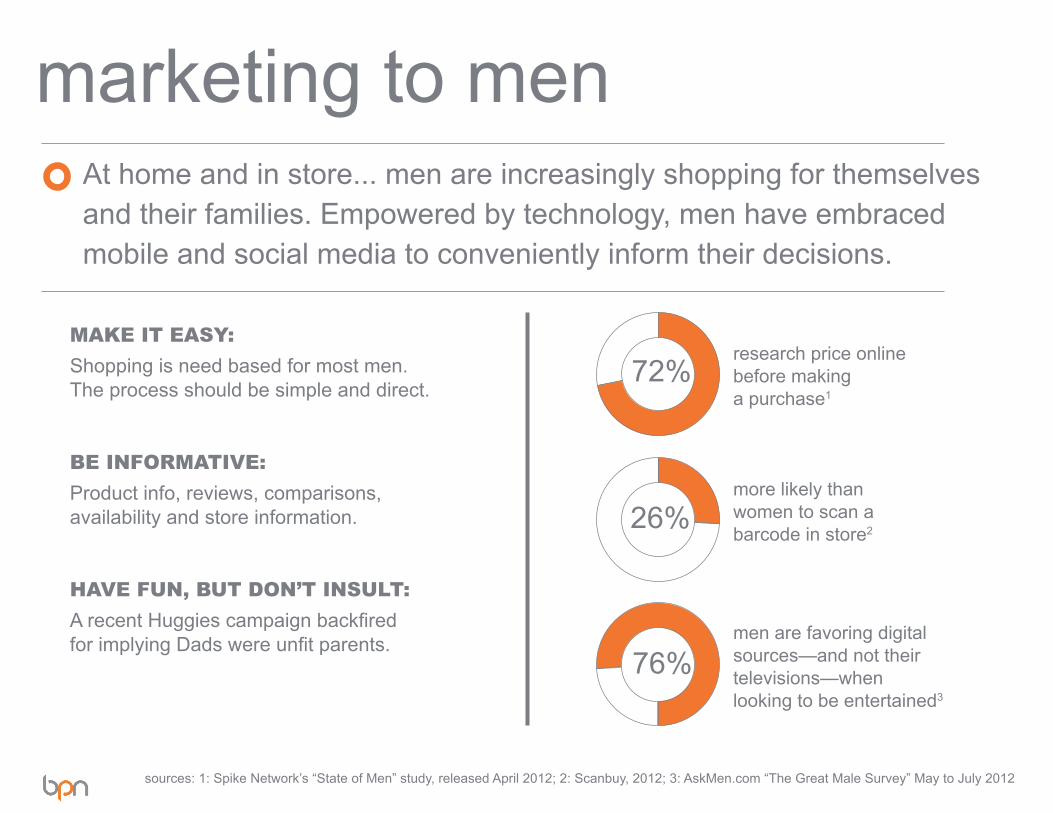

marketing to menAt home and in store... men are increasingly shopping for themselves and their families. Empowered by technology, men have embraced mobile and social media to conveniently inform their decisions.

MAKE IT EASY: Shopping is need based for most men. The process should be simple and direct.

BE INFORMATIVE: Product info, reviews, comparisons, availability and store information.

HAVE FUN, BUT DON’T INSULT: A recent Huggies campaign backfired for implying Dads were unfit parents.

26%

72%research price online before making a purchase1

more likely than women to scan a barcode in store2

men are favoring digital sources—and not their televisions—whenlooking to be entertained3

sources: 1: Spike Network’s “State of Men” study, released April 2012; 2: Scanbuy, 2012; 3: AskMen.com “The Great Male Survey” May to July 2012

76%

LIZ ROSS President, North America BPN101 E. Erie, 10th FloorChicago, IL 60611 312-799-4101 [email protected]

DOUG JOHNSON SVP, Customer Experience & Shopping Insights BPN101 E. Erie, 10th FloorChicago, IL 60611 312-799-4104 [email protected]

conclusion